“The economy can handle higher interest rates, and they are needed.” The BoC is way behind the curve, but way ahead of the Fed.

By Wolf Richter for WOLF STREET.

The Bank of Canada, after telegraphing it for weeks, hiked its overnight rate by 50 basis points today, the first 50-basis-point hike since 2000, after having hiked by 25 basis points at its March meeting. This brought its overnight rate to 1.0%.

“Interest rates will need to rise further,” governor Tiff Macklem said in the opening statement. The economy is “moving into excess demand” and inflation is “persisting well above target,” he said.

“The economy can handle higher interest rates, and they are needed,” he said. Interest rates would continue to rise “to more normal settings,” which would be the “neutral” rate, which the BoC estimates to be somewhere in the 2% to 3% range. “We may need to take rates modestly above neutral for a period to bring demand and supply back to balance and inflation back to target,” he said.

Official QT now, unofficial QT since March 2021.

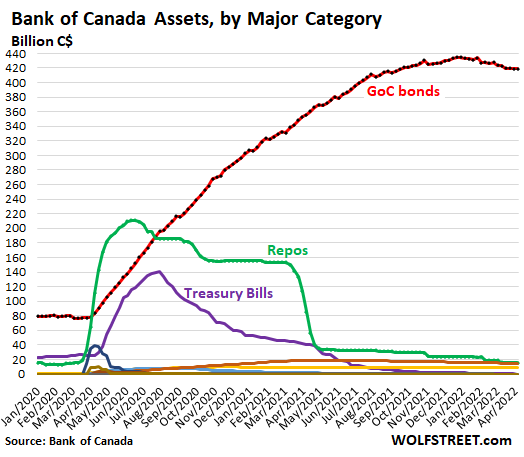

The official Quantitative Tightening will begin on April 25, the BoC said. it will no longer buy any Government of Canada (GoC) bonds at all, and it will let maturing bonds roll of the balance sheet without replacement, which will shrink the balance sheet.

The unofficial Quantitative Tightening began a year ago. The BoC already shrank its balance sheet by 15%, from C$575 billion in total assets at the peak in March 2021, to C$487 billion as of last week. In March 2021, when it announced this QT, it specifically denied that this was QT, just like when it denied in late 2020 that it was “tapering” when it started tapering its purchases of GoC bonds and ended entirely its purchases of MBS.

The BoC already shed or sharply reduced its other assets that had been part of the Covid money-printing binge, particularly its repos, now down to just C$15 billion (green), and its short-term Canada Treasury Bills, now down to zero (purple):

Assets to be “far lower than the current level.”

The biggie left on the balance sheet are the GoC bonds, and as they mature, they’re going to roll off, which is what the BoC announced today. But how low will they go?

“The longer-run level” of its bond holdings “is yet to be determined, but it is far lower than the current level,” the BoC said in a separate market notice.

How far behind the curve is the BoC?

Canada’s inflation rate jumped to 5.7%. And the BoC’s policy rate is now 1.0%.

But the BoC is way ahead of the Fed, whose policy rate target is 0.50% at the upper end, even as CPI inflation has exploded to 8.5%.

But markets have started chasing after inflation.

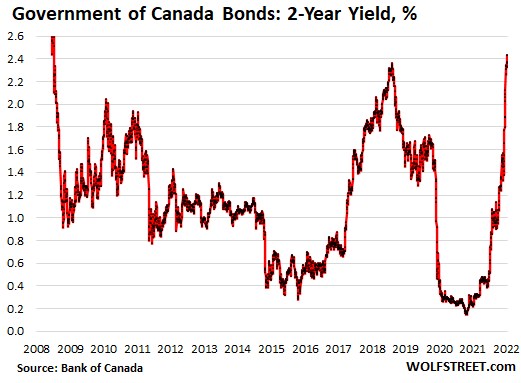

Interest rates started reacting to expected rate hikes in September 2021. The two-year Canada Treasury yield soared from 0.4% at the time to 2.33% today, after having hit 2.43% on Friday. Both of them the highest since 2008. This is a huge move in short-term yields.

For the Canadian housing market – where most mortgages are either variable-rate or “fixed rate” with relatively short terms, such a “two-year fixed” or a “five-year fixed” rate – the shorter-term yields are very impactful.

This was a massive series of jumps in the yield leading up to the 50-basis-point hike today and QT:

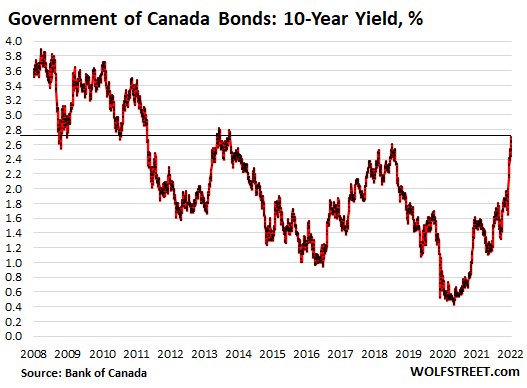

The Canada 10-year Government Bond yield closed today at 2.64%, after having hit 2.70% on Monday, the highest since January 2014.

“Inflation is too [damn] high.”

“Inflation is too high. It is higher than we expected, and it’s going to be elevated for longer than we previously thought,” Macklem said in the opening statement.

“The Bank’s primary focus is inflation. We are acutely aware that already-high inflation has risen further above our target,” he said.

More rate hikes to tamp down on “overall demand.”

“By making borrowing more expensive and increasing the return on saving, a higher policy interest rate dampens spending, reducing overall demand in the economy. And with demand starting to run ahead of the economy’s supply capacity, we need that to happen to bring the economy into balance and cool domestic inflation,” he said.

“The economy has entered this period of excess demand with considerable momentum and high inflation, and we are committed to getting inflation back to target,” he said.

The BoC also lowered its forecast for Canada’s growth in 2022 to a still red-hot 4.25% and a very strong 3.25% in 2023. It said that robust business investment, labor productivity growth, and higher immigration will add to productive capacity, while the rate hikes would moderate growth in domestic demand, which should help balance the economy. That’s the plan.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Not bad, Canada, not bad. Now I wish the Fed would feel the shame it should and put teeth to their words.

except BOC bot 5 bln a week or 20bln a mth during last 2 yrs of Qe,,,, that would roughly translate in 200 bln a month for US equivalent. you wonder our housing prices exploded,,,,,,,

I’m still surprised they banned foreign real estate investment. Or at least that’s what the headlines I saw said. I don’t know the specifics.

It makes a good headline, but it’s not enforceable, too easy to work around it. They are also going to create a tax free savings account for first time home buyers under 40. That’s in addition to the existing TFSA for general purposes. So the rich can easily max it out (40K contribution limit) early, grow it for twenty years on risky stocks, and bid even more over asking. The poors can go pound sand.

The foreign Chinese payoff the local Chinese so they can claim the tax free principal residence. The money usually goes to very poor local Chinese and the money comes from China and then the property is sold tax free. The Chinese also send countless students here from China doing basically the same thing claiming the tax free principal residence. The Canadian government did nothing about this and the Chinese are very crafty so they’ll get around the 2 year ban.

It’s a little like closing the gates after the horses have bolted. The Canadian housing market it vastly inflated and has locked out millions while producing no wealth.

Thank you Wolf for alerting us all to the Canadian situation… Pure wisdom dispensed daily.

With the PPI ensuring next month’s CPI will be higher (read all about it right here)

https://wolfstreet.com/2022/04/13/inflation-nightmare-keeps-getting-worse-producer-prices-break-out-inflationary-mindset-rules/,

Wolf’s shepherding of this website since July 5, 2014 (Read the Testosterone Pit – it explains Wolf’s incredible wisdom in the American car and truck market) is the result of a passion for the truth, tolerant of dissent and intolerant of misinformation.

Wolf provides us with framework to assess our current situation in the U.S.

Opportunity has rarely been better.

The banksters’ “Fed” (actually privately owned) bank cartel painted the US economy into a corner, particularly after the 2017 tax cuts, which really were to benefit the ultrarich and rich, who just lied and claimed that the tax cuts benefitted ordinary Americans: e.g., the child tax credit went down from $4050 to $3000 for kids older than 6 years of age. Thus, any increase in interest rates paid on rolled over US treasuries will either bankrupt or budget or cause more, MASSIVE money printing (which started in 2019 due to the tax cuts and bankters needs for repo market assistance/bailouts) and thus, even greater inflation.

Raising the taxes on the ultrarich, e.g., the top 1% richest Americans, who reportedly own more than 50% of US assets, is out of the question because we have many, utterly corrupt, US politicians.

Those recently proposed tax laws were desperately opposed by the ultrarich’s puppet politicians and blocked, because just their tax reporting requirements would have shocked the world, since filing the tax forms would have required the ultrarich to reveal themselves and their true wealth due to the wealth tax portion of the tax. Americans would have been totally shocked at the level of hidden wealth.

CORRECTION: … any substantial increase in interest rates paid on rolled over treasuries.

CORRECTION: Thus, any increase in interest rates paid on rolled over US treasuries will either bankrupt our US federal budget or cause more, MASSIVE money printing …

(Sorry, but try not to make any errors when kids keep interrupting you.)

The well known billionaires are just the tippy-tip of a GINORMOUS iceberg of ultrarich families who are living hedonistic lives, effectively, in hiding with trustees and money managers handling their funds, in the USA, EU, Thailand, etc. I devoutly hope that such a wealth tax will eventually be passed, since huge numbers of both parties’ members support it, and that the hidden wealth finally can become known. See “Britain’s Second Empire: The Spider’s Web” which hints at just the 55 TRILLION British pounds that were in just British tax shelter havens many years ago when that documentary was made.

Frank Vogl wrote a book called “The Enablers” about the corrupt oligarchs who now rule not just Russia, but much of the West too. Read also Simon Johnson’s “The Quiet Coup.” That is why the French are forced to choose between a female Mussolini and a boy sponsored by oligarchs.

Listened to Peter Schiff last night. If I heard correctly US budget deficit exceeded all forecasts for the last month. If you run a deficit you are running stimulus. No wonder inflation is sticky.

We’re going to run close to a $1.5T deficit this year. At least $500B of it will be from Medicare Part B, doctors. This year, we’ll spend close to $600B on interest on the debt. Combined, the FED and Congress have juiced the economy with $11T in the last two years, or more than 2 times what the federal government spends in one year. That’s a ton of inflation.

I guess the looking on the bright side, the deficit was $4 trillion the year before. At least they reduced it by 2.5 trillion. LOL

Old School,

The first mistake you made is listening to Schiff, who will say whatever in order to sell his stuff.

The second mistake you made is not checking the budget numbers yourself. So here they are:

In March, the deficit was $191 billion, down by 71% from March 2021.

In the fiscal year so far (6th month), the budget deficit = $667 billion, down 61% from the same period in 2021, and down 3% from 2019 ($691 billion).

You come across as very arrogant Wolf.

1. I listen to probably 50 people and listen more to Peter as free entertainment. I actually use him to fall asleep.

2. I am not stupid. I know the budget deficit is down year over year. All I said was nobody was forecasting a budget deficit so large. A $191 budget deficit contributes to the inflation number.

Well, then don’t try to spread Schiff’s stuff via the comments here. Listen to it, enjoy it, take out of it whatever you want, and end of story. It’s when you drag it into here that I have to deal with it.

A deficit is a deficit. Less bad is still bad. We need to change this mentality!

That is a small factor. Greater and greater inflation is with us, but it is not due to last month’s budget deficit. It is due to reckless money printing for decades and twenty years since 2000 when the US never, ever had a balanced budget, which reached a climax with the bank repo bailouts then with “Perfect Storm: 80% of All US Dollars in Existence Were Printed Over the Last 2 Years, while One-Third Of US Workers Make Less Than $15 An Hour” in the 2nd smartest guy in the room.

Of course, the Ukraine war and the sudden, unexpected removal of those two countries’ wheat and other exports will also cause much of the inflation, e.g., of food and energy. All the “Fed” president and members of its board, not just Powell or his board, for the last twenty years are to blame for this disaster. The only consolation is that the CCP is even more foolish and corrupt by an order of magnitude than the “Fed” and its bankster owners, so we are the sole superpower that will be left.

Canada has absolutely insane land prices (the main driver of property prices) compared to the USA. Canada has land coming out their ears.

The BoC have done a terrible job and are simply forced to respond to the Fed raises, albeit on a slightly staggered schedule due to central bank meeting calendars. If they do not CAD is toast.

Lots of land in Canada near Norman Wells. You should go there sometime. Land is not that expensive either. Nice place, if you like permafrost.

Exactly the kind of comment I am referring to.

There is land aplenty all over the place with perfectly acceptable weather.

“There is land aplenty all over the place with perfectly acceptable weather.”

When?

For a couple of months in late summer and early fall?

Canada weather is crap.

KWHPete,

Living in Minneapolis puts weather in Canada as a: “Yeah, it is winter, what do expect?”

But on Friday 17 June 2022, the Formula 1 tour hits Montreal. A beautiful city with beautiful women (IMO). And the most technically advanced speed machines that stick to the ground are there in one place to take in and enjoy (figuratively speaking on the women, eh).

I’m just sayin’ …

Winnipeg does get cold in January though.

The banks that rule the government here in Canada even more than the FED in the USA, had a boner yesterday.

I can’t imagine how fast they raised the prime rate to borrow, likely a milli second after the words came out of Tift’s mouth.

Inflation is so incredibly non-linear that these 2-3% estimates could be very far off.

Would be a disaster if that ended up being true. Imagine trying for a soft landing at 3% when the actual neutral rate was 7%? You have to be at ground level to land and these people would be at 10,000 feet and not even know it.

May be the Fed is so late because its really out of options and doesn’t want to say it. In 70s when inflation was this high, Debt to GDP ratio was 40% and not 120%, trade deficits were not huge, we were not dependent on China for essentials, bond markets were not in this crazy bubble.

Biden already announced that we will do everything in his power and then clearly implied that “He could do nothing!”.

I don’t think govt debt is the issue. Govt has almost the definition of an inflation protected revenue stream, so it’s real interest rates that matter. That debt is running at absurdly negative rates, and investors are still buying it up. Also most of the COVID debt is QE money and the interest payments on this are immaterial unless the govt wants to self-flagellate (which is may do to justify cutting expenditure, but that’s a political decision not a practical one).

IMHO, the big problem for the fed is that it has spent 20 years creating an everything bubble. The idea was that the young worker today would happily accept paying most of their income into, say, their mortgage, on the basis that they can flog it off to someone for even more in 40 years time and retire off the capital gains. The money they put into their mortgage would then flow into funding the pension promises made to previous generations. This is a huge ponzi scheme that relies on a multi-generational belief that future workers will be happy to pay even more for the same asset regardless of the asset’s actual ability to every return the capital paid in the form of cashflow.

If that bubble blows up, then the games is over, and the western world’s unfunded pension obligations are laid bare for all to see (especially the young who are supposed to fund it).

If Biden were really going to do everything in his power to avoid an economic catastrophe, he would have started by reversing his ban on the completion of the Keystone Pipeline. But it is business as usual in DC these days. The two political parties are as far apart as ever on most issues.

It is politically convenient to blame Putin for all of our economic troubles, but they have been at least 20 years in the making, starting with the Bush 43 tax cuts of 2001-03 and his Middle East wars. It took Germany less than 10 years to destroy its old currency after it left the gold standard at the outbreak of WWI. The US has been given a reprieve but it won’t last forever.

Excellent post – you hit most of the reasons why the US is financially crippled relative to even the “bad old days” 40 years ago.

Basically we have had generations of worthless, degenerate political “leadership” that always took the easiest way out – refusing to address worsening problems, deficit spending and money printing to paper over the economic rot.

All the while, promising ever more grandiose political fantasies.

I agree with you Leo… I have thought for a while that the Fed has held back because it can’t (easily) design a monetary shrinkage policy that makes sense while the Federal government is simultaneously expanding the fiscal stimulus by an unknown amount. Until Manchin pulled the plug on the Build Back Better stimulus in December we were talking about adding up to $2.3 trillion in additional spending… and that was down from $6 trillion being proposed just a few months earlier.

But now that we seem to have a fiscal plan for the next three years the Fed can get on with it. And they NEED to get on with it.

I learned a worrying news from my friend who owns 40+ acres of actively farmed land. He said, as the fertilizer prices have jumped more than 2X, diesel by more than 1.5X, farming will not be profitable this year. So he would reduce farming to bare minimum to retain water rights and property tax benefits.

If more US farmers do this, we may look at real food shortages and hunger later this year. Shouldn’t someone raising alarm on this?

Is an armed and hungry populace easier to control or scarier to police?

JWB-

Good question. Three progressively harsher views of societal change:

1) “We conclude that the concentration of wealth is natural and inevitable, and is periodically alleviated by violent or peaceable redistribution. In this view, all economic history is the slow heartbeat of the social organism, vast systole and diastole of concentrating wealth and compulsory recirculation.”

– Will and Ariel Durant, The Lessons of History

2) “Those who make peaceful evolution impossible make violent revolution inevitable.“

– John F. Kennedy, Remarks on the first anniversary of the Alliance for Progress, 13 March 1962

3) “[A] bunch of mindless jerks who’ll be the first against the wall when the revolution comes.”

– Douglas Adams, The Hitchhiker’s Guide to the Galaxy – Describing the marketing division of the Sirius Cybernetics Corporation

Police will be hungry also, which song said every cop is a criminal.

Survival is everything…full bellies reduce stress.

Putin’s war I believe is really about the resources and having oil at a price high enough to feed his population.

Anything else is noise.

I live in a very small state, but I have heard farmers say they wont have fertilizer this year in the past week. They gripe about the other costs also (deisel, feed etc.)

I have a friend in Arkansas who leases land for farming. His newest tenant has a big chicken operation and so he will be using the chicken manure as his fertilizer. Apparently the runoff laws allow him to put a lot more of it on the land than chemical fertilizer anyway.

We have to soil test and lime our land this fall. I have planned for a 40% increase from 4 years ago. That number is really just a shot in the dark. I will update late Oct/early Nov as to what the actual price will be.

Big agri-biz has more pricing power and geographic diversification, like big biz does generally. This conversation has been happening for centuries. Jefferson was fighting to intentionally keep things spread out and small. Hamilton said lack of centralization in business and finance will make us road-kill for competitor-nations. The Grange movement, 1800s was farmers banding together to protect their interests, as other forces were eating their lunch, railroads, etc. The latter period is where early federal agencies (Interstate Commerce Commission) appeared to put a lid on pricing power of railroads (and were immediately captured),

The challenge for your friend is the size problem. Small farm operations of that size are likely orchards or ranchers, and the expenses are small compared to the average farm, which in the US is 400+ acres and in Canada it’s 800+ acres. These price increases over the last 30 years have crushed small operations, this years spike is why every farm has gotten bigger over the years. In agriculture you have to build a large profit margin because every 5 to 10 years a new regulation, or new technology comes along and takes all the profit anyway.

Leo1992,

“The crop produced in 2022 will be the most expensive, as far as dollars spent producing it, in the history of farmers. Across the board, we’ll be looking at more dollars spent on a per-acre base for each farm than farmers have spent in prior years. With higher commodity prices and a normal production year, this year should pencil out.”

-Ron Dvergsten, Northland Community and Technical College, quoted in the 11 April Farm Net News from Grand Forks.

What’s the drought situation in the Red River Valley area and other prime ag areas in North Dakota and Minnesota?

All the other inputs mean squat if there is no moisture at the right time.

Australia looks like it will have a pretty good harvest this year.

These shortages relate to the economic embargoes placed on Russia by the US (the chief instigator) and by its allies. They have boomeranged back to hit the US and the rest of the world. During WWII, the US had food rationing complete with coupons, but it was lifted at the end of the war. Britain had food rationing until 1953 or 1954.

This is why I think it’s so stupid to use more ethanol to make gas cheaper – corn is pretty fertilizer intensive, and is used in a ton of stuff (‘regular’ corn, HFCS, and animal feed).

People can drive less, but you can’t really eat less.

(Well, maybe Americans can.)

That is weird… why wouldn’t he just charge more? Fuel and Fertilizer costs are up because of what is happening in Ukraine and Russia… but their production will be down as well.

Leo,

It seems to me that the smart farmer would go all in, but by and large they are a conservative lot. There is not going to be an abundant surplus of food next year. Supply and demand should dictate a profit, even with the increased input costs.

The losers here are the poorest 20% of the world.

We should all hope for favorable farming conditions in the northern hemisphere this year.

It is unconscionable that Biden extended ethanol season in gasoline. Using food to create fuel while millions worldwide are going to die of starvation, and all for the sake of gasoline prices.

I am guessing the government will give out farm subsidies to keep the farmers ago.

The big farming organization will lobby congress for some handouts if they have any losses

Housing is up 20% in Canada. So they are claiming 4% growth. 7% inflation, or whatever it was. But the real rate of inflation is higher, meaning real growth is zero at best.

You only have to go outside in Montreal to see it. Half the economy is driven by renovations in rich neighbourhoods. Assets go up, they HELOC, get their roof fixed and landscaping by the guy who lives in the suburbs, he goes out and buys a bigger TV. There’s *some* value creation (fixed roof) but at a huge input and future cost as nobody can afford a home, a pension and are demotivated.

Our tech employer has seen many quits recently. One moved to the USA, another to a USA firm. Wage inflation is rife.

There is no “correct” interest rate. That’s the supposed neutral rate.

Here in Thailand, the central bank is among the diminishing number of central banks who still view inflation as “transitory.”

In February, the Bank of Thailand monetary policy committee voted unanimously to hold its policy rate at a record low of 0.5 percent. This seems strange, since Thai economic growth has been fairly strong this year. Their rationale may be to continue recovery of the covid damaged tourist industry, which is about 7% of GDP.

The annual inflation rate in Thailand rose to 5.73% in March 2022, from 5.28% in February (expectations were 5.6%). This is the highest increase since September 2008. Thailand’s headline CPI for projected to rise between 4 to 5% in 2022, compared with 1.23% in 2021.

However, my wife has not noticed much inflation in the local open-air markets (traditional versions still exist in almost all districts). These markets are packed many small vendors, who sell fully cooked main meals as well as produce, nuts, sugar foods, meats, etc.

We can live much more cheaply than in the U.S. in almost all ways, but now I’m less optimistic about the converting USD to Thai baht. Like the U.S., Thai bank interest rates are rock bottom for savers. And now the two year U.S. Treasury Note is approaching what I can get in my wife’s credit union.

USD will have to jump up significantly, before I convert more dollars to Thai baht.

Wasn’t the 1994 US (Greenspan) rate hike linked to the SE Asian currencies including the baht crashing in the mid-later 1990s?

I’ve read about that, but forget the details.

It not hard to be ahead of the Fed. The whole bond market is. Look at the yield curve and the only part of it that is obviously out of whack with the rest is the extreme short end … where the Fed is sitting on it, holding rates down.

The FED is so outrageously derelict in its duties that I cannot even comprehend why the hell Jerome Powell still has a job. This guy needs to be fired YESTERDAY.

Powell’s job is temporary right now, that’s the problem. He doesn’t dare risk re-confirmation by rocking the boat right before an election. They are so ridiculously political. Once upon a time banker types were conservative, but now they’re democrat activists.

I am expecting lip service and maybe some more baby steps, but nothing meaningful before december.

Which would be hilarious because that will ensure that the Dems get wiped out. Inflation makes people purple-faced angry, much more than falling stocks of the rich.

I don’t think he needs the money.

He’s worried about his legacy and what will be said of the job he did ruining the economy.

Powell is an R. The central bankers aren’t playing a partisan game, they are aiding and abetting the banking industry.

An unholy alliance from FRS inception:

Bankers + Politicians

Most senators from both parties thought he was doing a great job.

of course they did. most senators are multi millionaires with huge stock portfolios.

All interest rate policy guidance decisions at the Federal Reserve are made by the 12 member FOMC (Federal Open Market Committee) and not by the Federal Reserve Chairman. Learn how the Federal Reserve works.

The FED chair is the top position, and is the face and the voice of the FED. Learn about accountability.

It is not demand that is the problem. It was and remains supply. The BoC as the FED has it backwards.

This is the most grotesquely overstimulated economy ever in Canada and the US, accomplished via money-printing, interest rate repression, and government deficit spending, and you’re saying demand is not the problem? That’s hilarious.

My assistant at work told me she spends $5000 for 4 days at Disney World. That is about 8% of her annual salary.

This is the result of WTF Fed overstimulation, IMHO, which will hopefully correct.

Most Florida Resident passes are sold out. Expect a peak in Disney’s theme park revenues, IMHO.

Wow! Didn’t realize how expensive that place was.

“My assistant at work told me she spends $5000 for 4 days at Disney World.”

That will soon be one night’s stay at Motel 6 with Weimar Boy Powell at the helm.

“… 4 days at Disney World …. [for] about 8% of her annual salary.”

This tells me everything I need to hear about the role (and guilt) of the masses in contributing to their own ruin. I’ll bet Disney+ takes a nice chunk of the rest, as she, like so many, have outsourced imagination and parenting to that global corporation. How do you spell d-e-c-a-d-e-n-c-e?

She could buy one seriously good book, read and discuss it with her kids, and improve their brains substantially. Fed or none.

Then Depth Charge, I imagine, could stop complaining about Powell as the root of all evil, who should be drawn and quartered.

“$5000 for 4 days at Disney World”

I get it that people have kids that “will only be kids once”, so I can somewhat understand spending money you don’t have to take them *once*.

But I know multiple people that take the kids *every* year, at great expense while they have no savings and are deeper in debt than Stanley Johnson.

Oh well. It’s their borrowed money.

My friend bought 5 annual passes to Dolly Wood for the same price as 2 one day passes to Disney World. And Dolly Wood hasn’t gone Woke. Woke costs more money.

Jay–

I went to Dollywood a few times as a kid in the 60s. Back then, it was called “Goldrush Junction”. I imagine it’s a lot bigger/better now (I’m sure Dolly spent quite a bit on it).

They had a train ride and all the kids could get a “rifle” (wooden) out of a ole big box before the ride — we got them to “shoot” indians if we ran into any (uhhh… yeah… we always did).

We came up on bank robbers to shoot (holed up in a cabin out there) and lots of indians to shoot.

Terribly politically incorrect by today’s standards, but my God, it was insanely fun for a kid.

Local Cherokees played the indians, so I guess they didn’t mind us shooting them (at least with the rifles we had).

The good thing is consumers have 2 trillion sitting in savings at commercial banks. The amount was 1 trillion pre-covid and at peak stimulus it hit 3.5 trillion.

So consumers have been on a spending spree as seen in many of Wolf’s charts the past year.

It appears they still have a nice cash cushion?

that’s a gross exaggeration. disney passes are about $110 a day for non-residents. even if you get fastpass, stay in expensive hotels on property, i don’t see how you spend that much.

Jake —

No, it ain’t. You *could* spend less, but the on-site packages can get astronomical. Fabulous hotels with all-access passes and food… It gets CRAZY.

Meh, it’s her money…

Is she married? Husband making a killing? How many went?

Probably just a couple of days at the mouse…. You’ve got EPCOT , Universal, Sea World, etc… Eating out for 5 days, souvenirs….

Yeah, I could see it…

Hal,

I went to Dollywood in the late 70s as a teenager when it was called “Silver Dollar City.” I didn’t enjoy it all that much but my parents were going through their Garnola-eating “back to earth” phase so we got to see how lye soap was made, tin plate photography, and other “Mountain People” processes.

If one wants to really piss money away, take your family on a Disney cruise. One of my friends did that for a week and went thru $18 K, including trip transportation.

And Hal, Dollywood was a lot of fun. Everyone had fun, even the Indians. That’s what’s wrong with this country now, they are taking the fun away from people.

My day at Disney World earlier this year consisted of eating lunch at the Polynesian and riding Disney transportation to other Disney resorts. Cost was $30 for lunch. Went back to the nondisney timeshare at the end of the day. Much more enjoyable than spending a fortune only to stand in lines all day.

I disagree. Most of the stimulus has ended up in the pockets of the rich. The poor and lower middle classes don’t have enough money to maintain a high level of demand in the current economy. Now there are also supply problems. We could end up with high demand/low supply for essentials and no demand for anything else.

Consumer credit and debit transactions increased by 15% in 2022 over 2021 and that is causing unprecedented demand in the US economy and is further proof that there is way too much money sloshing around in the US economy making demand the key critical problem in the US.

and the “rich” are spending tons of money, affecting supply chains on all products.

Supply chain definitely has issues but nothing high rates can’t tame.

Demand has gone through the roof because of easy money and this should be reigned in first.

Nothing like a deep recession, eh, to tame demand? That’ll fix energy/commodity driven components of the current economic dilemma; that’ll fix the geopolitical shifts in international finance that undercut the US ability to export dollar devaluation!

The whole point is that the Fed has few tools at this point. As long as Climate Change ideology drives Western economic policies it is only going to get worse.

You’ve been watching too much biased news. The converse is true. Rising inflation is causing the supply chain issues. Powell conveniently comes up with that line about the supply chain being the problem.

Yep.

Firstly, it’s both. There is no way that demand gets out of whack without supply responding in kind, or vice versa. Prices are the indicator of imbalance, strong nations maintain balance.

The problem to me is the labor market tightness. The Fed told you it was going to goose the labor market to prevent “scarring”, then they goosed it. If congress or the president wants to create jobs that’s great, it generally helps the overall economy. The fed ignored it’s mandate of price stability in favor of labor market tightness. Now here we are with an abnormally low unemployment rate, and massive price instability.

There way out of labor market tightness is higher unemployment, reduced demand, and lower prices. Everyone knows this, the debate is about how long it’s going to take.

Not going to end well for gold bugs again. Every central bank is going to be raising rates. The dollar will go verticle and break everything including gold. Gold bugs will cry manipulation the same way Charlie Brown is surprised when Lucy pulls the football for the millionth time.

Once that happens is when the real fun begins.

Totally. Gold bugs do not realize what’s coming. Many will go broke. Again.

Tell me – just how can this gold bug go broke, if it is paid for and purchased over many years?

You may be thinking of the newbies holding receipts for paper gold?

Yep, as always!

I don’t think “gold bugs” are ever going broke. Precious metals are a hedge against a Venezuela type meltdown, nothing more. The traditional “gold bug” isn’t buying gold to get rich.

Proportionately few “gold bugs” are “rich”, though they are in my experience financially conservative and aren’t loaded with debt.

My expectation is that, at some point, a terrible economy with high unemployment will turn enough of them into forced sellers.

Rising rates don’t hurt gold when real rates are negative. This is not Volcker raising rates by double digits. Rates high enough to hurt gold would make debts unrepayable.

There is no threshold. It’s psychological. Looking at historical precedent (in this context) is only of limited use because there really isn’t one to the conditions of today anyway.

Gold is primarily a form of insurance. You’re only going to get rich buying it if bought at a really depressed price, like in 2001. It isn’t relatively cheap today but expensive.

Okay, I’ll sit on my precious metal for two more years and you hide your greenbacks in the mattress for same, let’s see what happens with 10%+ inflation.

I don’t have any PMs, but who says it has to be one or the other exclusively? I do have counter-moving bets in various assets. That’s how I sleep at night.

“ Okay, I’ll sit on my precious metal for two more years and you hide your greenbacks in the mattress for same, let’s see what happens with 10%+ inflation.”

Ummmm…

I’ll take my greenbacks that lost 10% and buy all your gold that lost 30%….

I tried to find good studies on gold in a diversified portfolio if you are an asset allocator. Most were over a too short term period, but to me it looked like you would always improve your risk/return Sharpe ratio by adding some gold. Depending on what other stuff is in your portfolio you probably could make a case from 2% – 20%.

$550 in 1915. Almost $2000 now.

Pffft.

Wasn’t gold at $20 US per ounce in 1915?

Yes I’ve opened a USD account to move CAD across.

If the Fed keep raising rates the BoC will balk at some point, and CAD will tank. We have no gold reserves, although we do have miners who could be nationalized.

Do you mind explaining why do you think Bank of Canada will fail to keep pace with Federal Reserve ? Because housing bubble in Canada is more fragile that US stock markets ? Or some other reason ?

Also, Canada has wast commodities wealth, wouldn’t this fact be bullish for CAD ?

> Because housing bubble in Canada is more fragile

Yes that’s my guess

Mike,

I’m not sure what you understand gold to be. It’s basically a hedge against inflation. Since 1970, against the US dollar, it has gone up 107% a year…against the UK pound (who had even more inflation) it has gone up 198% a year…..

Since 2000 gold has gone up around 28% a year against the dollar and around 30% against the pound…..

Yep Anthony. If you live in a country like Russia or Venezuela or Argentina or Mexico. Gold has performed even better.

When the dollar is strong, that is when you buy some gold as it is on sale.

Gold was at $35/oz. in 1970, I think.

If gold doubled (your “107% a year”) would surpass $2000 in 6 years.

I’m too lazy to carry out 50 years of doubling…

John H

Gold is now…. $1974.00 dollars…. an ounce……. an increase of roughly 5,800% on your original purchase or 58 times in 50 years

and that is inflation

ps some USA stock markets have gone up much more….

$35 growing to $1974 over 50 years at 8.4% (based on annual compounding.

$35 growing at the 107% mentioned in your post, for 50 years, grows to $220 Trillion (rounded down to nearest T)

I am not sure how you get that. If EVERY central bank is starting QT then there should be a global run to gold. If they eventually get inflation under control (a BIG if) then gold will settle back down. But it is hard to see it going down too much.

How many billions have the banks been fined for manipulation of the precious metals markets recently?

The only question in Canada is how high the BOC can go before they have to reverse. We have have a crazy real estate bubble here. Mortgage rates go too high and there will be a real estate crash. In my view, the BOC won’t get to 2% before they have to throw in the towel. All this yap, yap, tough talk, “we can go higher stuff” is just done in the hope that they can talk inflation and house prices down without blowing everything up. Good luck with that….Oh yeah, like the US, nobody believes the governments inflation figures…5.7%…what a joke…

“In my view, the BOC won’t get to 2% before they have to throw in the towel.”

This is the new narrative of all the speculators. First it was “the FED will NEVER raise rates.” Now that their first hit of hopium turned out to be bunk, they’ve taken a hit of some new hopium, which will turn out to be bunk as well.

Actually there are two levels of hopium for the over-leveraged:

1. Central banks will reverse course

2. If central banks don’t reverse course Blackrock will buy it _all_ up (apparently)

Not quite sure what the logic is on the second one.

I think current government of Canada is hoping that drastic increase in immigration will prop up the housing market. In other words, they will bring fresh greater fools in ever bigger numbers.

Somehow the Canadian move in advance of a Fed increase reminds me of when Marlin Perkins (MUO Wild Kingdom) would send Jim in to see if the mother bear had birthed her cubs yet.

Not unlike a coal miner’s canary.

How much to Central Bankers coordinate their actions?

Oops: meant to say “How much do Central Bankers coordinate their actions?”

Search google for “Bank of canada calendar”. Their next interest rate decision is 1st June, Fed is the start of May. So yesterday’s meeting was the last time for the BoC to raise “in parallel” with the Fed, without falling behind.

Given the Fed has already telegraphed their decision, the BoC had to raise here, they are not “front-running”. They are being dragged by a rope behind the Fed’s car.

“dragged by a rope” — no, but maybe “pushed by a rope” LOL

So BoC aren’t aware of the Fed’s moves?

And CAD rates haven’t historically moved in lock-step with the Fed?

CAD is a tiny currency, it’s not like we can run our own monetary policy with our own rates.

That’s why the BOC front-runs the Fed.

Everyone who believes there is some form of logical practices behind the people that allowed trade deficits, destruction of industry, plagues, and inflation as well as underestimating the madness of the old KGB stooge elevated to P-Rex needs to stop and drink deep of a song that was timely before, and plays at so many levels:

“I said baby, baby, baby you’re out of time

Well baby, baby, baby you’re out of time

I said baby, baby, baby you’re out of time

Yes you are left out, outta there with-a-out a doubt

Cause baby, baby, baby you’re out of time.”

You can never go back, you can never go back.

The world (someone’s world) has been ending ever since it began. It has not ended cumulatively yet. It has weird ways of not ending, so far. It stumbles forward, through the fog of war, ALWAYS. The tea leaves always suggest this moment looks like this or that apocalypse.

You guys are way too negative and need to look at the bright side.

In 2008 the your Illustrious Lords of Finance very nearly blew up the Global Economy. This time around all they’ve done is create raging inflation.

Admit it, that’s a vast improvement. And better than we deserve, under the circumstances.

The life of a Central Banker is an arduous one. They have to be certain of the facts and must be extremely cautious because they don’t dare make any mistake. It takes immense fortitude and polished skills to come up with a quarter-point rate hike. Paul Volcker himself couldn’t do a better job, mostly because he’s dead.

I applaud the counter-position. Sometimes the comments chorus here gets too harmonious.

i think he was being sarcastic.

I misspelled ‘Illusionist’ and couldn’t find the ‘edit’ button. Sorry.

Since 2008 the economy has been stimulated by deficits and negative real short term rates in US averaging about -1.5%.

With more debt to carry around it seems to me the go to playbook is going to be larger deficits and larger negative rates for the next decade. I will guess we will average around negative 3% to keep it all going for a while.

Negative real rates might keep assets relatively high for another decade, but real per Capita income will not grow.

Doesn’t raging inflation help to diminish the national debt?

Let it run hot for few years and bingo, debt back below 100% GDP?

Not with spending always increasing. It’s not the 1940’s after WWII (the last time debt to GDP was this high). Back then, the budget was cut deeply by reducing defense spending. Now, eliminating the “defense” budget entirely would not balance the budget.

Rising rates don’t hurt gold when real rates are negative. This is not Volcker raising rates by double digits. Rates high enough to hurt gold would make debts unrepayable.

Gold price is tough to forecast. What we know is currently Fed has screwed up enough that gold mining is one of the most profitable businesses with gross margins at $800 per ounce. That’s even with people dumping money in alternatives to fiat like crypto.

Read an article that Nigerians are going into Bitcoin in a big way, with a lot of people keeping nearly all their savings in it due to currency debasement. If Bitcoin doesn’t survive they are broke.

Gold silver platinum are at top of bubble when buying margins are 20% ,people are fools

Is that so.

I can buy a lot Australia silver coins at a whopping 5% over silver content price.

And some NZ coins at less than silver value.

Just like any other asset it pays to have knowledge about what you are buying and selling.

You can also buy collector coins at little over silver content value that may go up in value as well.

The fools are people who don’t know what they are talking about.

Having been in Nigeria many times that is hardly a bad plan. Most people there prefer to hold onto dollars but the current Nigerian President has cracked down on that for the past seven years. Crypto strikes me as insane, but if I was in a 3rd World country with a dodgy currency then it might well appeal to me more than stuffing dollars and gold into my mattress where it can be stolen.

L Hunt-

Is there literature/research that examines long-term comparison of gold price to real interest rates that you know of?

Does steepness of curve matter?

Excellent post.

Gold is working just fine as a long term store of value. It is not a speculative play for me. I hold it as a liquid store of the value of my labor.

Bought my first 1/2 ounce of gold in 2004 for $200. 18 years later the annualized return is 9.23%. All just while sitting there doing nothing. My bet is the next ten years will be no different.

Very different story if you bought in 1989.

Happy, pointing out that there are bad times to buy any commodity or stock or market is simply to state the obvious. I am not price insensitive. But in a time when the M1 money supply has quadrupled in a couple of years, I am content to continue to use gold as a store of value.

Happy1-

Wasn’t gold about $500/oz in 1989. For a money asset, 500 to 1900 seems quite acceptable to me.

What am I missing?

@John H,

$500 to $1,900 over the last 30 years for gold is decent, a four-fold return on investment.

S& P 500 return for the same time span is 34 fold.

So the same $500 would be $17,000, almost 10 times the return on the same investment in gold, and this doesn’t even account for the dividend yield which probably makes the total return almost twice as much.

Gold is and even worse investment if you pick its peak in 1980 at around $800. You have had a return of about two fold over 40 years while the stock market total return would have been something like 50 fold.

Gold would have been a very excellent investment when the US left the gold standard from roughly 1972 to 1980, no question about that. Also pretty solid from its low point around 2000 until now.

Other than that a pretty lackluster investment. So in the last 50 years they were maybe 4 or 5 years where it would have been a really good investment and quite a few where it has been a really crappy one.

Happy1-

No major beef from me on your comparison, except that I don’t think of gold as an “investment.”

It’s more of an “alternative to bank money. In fact, it was such a good alternative to bank money back in the 1930’s that they outlawed it for a period, which I’m guessing you know. As an alternative to bank money over the last 100 years it compares quite favorably.

Aside: Using your argument, a person should not buy a car because it’s return pale next to stocks (or gold!).

Respectfully!

There is so much small-investor noise in gold. That’s why I don’t trust it. The theoretical justification makes some sense. But it lurches around strangely like some other meme-ish things, IMO.

Comparing gold and its price action to that of meme stocks is one of the most foolish things I have ever read. There are absolutely no similarities whatsoever.

Correct. Volcker raised rates above the inflation rate. Something that is not going to happen anytime soon. Until he did gold boomed.

Last inflation reading for the Netherlands was 11.9%. The Fed is way behind the curve, but way ahead of the ECB… What a clown show.

Yes, the ECB doesn’t even know there is a curve. The ECB has its head stuck in the sand.

Lagarde this morning…paraphrasing…”we know there’s terrible inflation that we intend to fight but you have to understand there’s a war going on that created this mess”. Not my fault if it goes bad, all the credit when things go well.

It’s been evident for years that the primary goal of the ECB is to preserve the Euro and the EU, regardless of the cost. Look at Greece.

Europe seems to have widely diverging inflation rates. Netherlands 11.9% based on your comment, Austria 6.8% (March estimate), Italy 4.8% (January). I’d have expected Italy to be over 10%.

The ECB has one interest rate policy (0%) for all these very different economies. It will be interesting to watch.

Kind of like shutting the barn door after the cows have gotten out. One could easily think this was the plan all along.

This is like shutting the barn door after the cows’ skeletons have been found out in the hinterlands, picked clean by vultures.

Ha ha yes!

The international perspective is much appreciated. One things is apparent, this is the western economies (again), not just a USA-Fed thing. Inflation is most everywhere on the planet, and central bankers are in similar plights. Russia and especially China are interesting wildcards though.

There are 160 central banks in world ,I believe that work in coordination. This is all planned to become a 1 world currency, who said control the currency, control the people.

On a side note who said they where out of Rothschild dollar , now in a war that I believe will become ww3 it’s spreading

Wolf,

Thank you for the superb, unique, and accurate insight you provide to us. Help me understand why reverse repos are remaining at a high amount of $1.815 trillion. Stupid me, with elementary understanding, expected a decrease after the first of the year. I guess it means that the big money market folks cannot get over 0.05% at a risk and duration acceptable to them? Aren’t a lot of counterparties NOT banks?

Clark

Clark Jernigan,

With reverse repos, the Fed pays counterparties, mostly money market funds as you said, interest (now 0.30%, not 0.05%) on cash they hand to the Fed, in exchange for collateral. It’s a sign that there is way too much cash (aka “liquidity”) in the financial system after $4.8 trillion in money printing, and no one knows what to do with it, and so they give it to the Fed to earn interest on it.

At its last meeting, the Fed hiked the interest it pays on these Overnight Reverse Repos by 25 basis points, to 0.30%, from 0.05%.

Enough QT will bring the reverse repos to zero. But QT hasn’t started yet. Likely to start after the May meeting.

I sell mortgages – and our business is down 70% from 5 months ago. Priced a 2nd home with 20% down perfect credit at almost 6% – FNMA Risk overlays up the wazoo. It is now cheaper now to just call it a Rental…better pricing. The bond market will do what the FED will not….cause Powell does not control long-term bond prices except he will dump more bonds to sell on an unhappy market with his taper. There is a strange silence in our broker chat group of 7000+ Mtg brokers on Facebook…… It has gone really quiet…..Too quiet….layoff notices now appearing.

Are you quietly looking for a new job?

Canadians are frankly insane and poorly informed.

Most think housing costs are a result of supply, and from this are somehow a function of construction materials. They very rarely have a concept of the price of land and location value. This leads them to conclude that housing in Ottawa should indeed be $1mm+ on the outskirts, despite an ocean of green moments from their door. Go look yourself on google maps and cross-reference with a realtor site.

No other Western nation has as much land to build on as Canada. Canadians will cite crazy information like the Canadian Shield, when they have an area the size of the UK sat nearly empty around Montreal, around Ottawa and around Toronto. The UK has 70mm people. Canada has half that.

Canadians price houses in houses. Your house sells for $1mm? Well my house has a second garage, it’s $1.2mm. What’s the median wage? Why are you asking that?!

One of the most common reasons given by Canadians for high house prices is that “people need them to stay high for their retirement”. That’s not a fundamental, that’s a wish. Wanting this to be true doesn’t factor into reality.

Reality: house price pumping is the last step for a government that has admitted it cannot fund its liabilities. And in pumping house prices growth is hurt and the state accelerates its descent.

One extra point: Canadians are also deeply mistaken about how attractive Canada is for immigrants. When you factor in housing costs and high taxes, and low wages, net wage is very low.

They tend to compare themselves to America a lot, but this leads to very low standards. Massive healthcare wait? At least it’s not America. Bad roads? At least you didn’t get shot, etc.

Immigrants will fall in earning power as only the most desperate will come. Those with greater earning power have several choices internationally .

In short: oh canada.

They aren’t making anymore muskeg!

“ One of the most common reasons given by Canadians for high house prices is that “people need them to stay high for their retirement”.

g,

Is that so they can retire somewhere else?

Canada does not include residential rents in the CPI. Rents doubled in the last 5 to 6 years in two thirds of Canada so the real inflation rate is much higher than 5.7 percent.

The Real Tony,

This is BS. Where do you people pick up this BS? Who is spreading it?

Rents are included and weigh 6.6% in overall CPI.

“Shelter” weighs 29.78% of the overall CPI. Shelter includes these categories, and their weights in overall CPI:

Rent: 6.59%

Mortgage interest cost: 3.68%

Homeowners’ replacement cost: 5.24%

Other owned accommodation expenses: 4.01%

https://www150.statcan.gc.ca/n1/pub/62f0014m/62f0014m2021011-eng.htm

If that was true why was inflation in Canada under 2 percent for all those years prior to 2021? They tell you one thing but the figures don’t bore that out.

It is true. Just click on the link and check it out. Note that “house prices” is not one of the items on the list because a house is considered an investment, not a consumption item. But “Rent” is on the list.

And also note that in a whole bunch of markets in Canada, real estate hasn’t been doing well for many years, including Calgary and Edmonton, and lots of others.

I just sold my house on Vancouver Island. We had 3 offers, 1 cash, 2 subject to finance. I knew the subject to’s would not go through, took less as cash. The rate rises will have large impacts on these high prices. In some areas in Canada prices are already dropping

I hope prices go down soon in the states. We are in the south and I’m still seeing ridiculous prices. Yesterday I got a call from our credit union encouraging us to take advantage of lower rates before they go up. We have used this bank for 7 years and they have never called us. That gives me hope that housing prices may turn in a few months. It’s sad, but I keep telling my husband we should RV full time. We could save so much money. Of course he thinks I’m crazy and my brother insists living in an RV full time is one step above being homeless, but a lot of people do that down here.

Don’t do it – that is, going RV full-time. Very different experience than vacationing in an RV. With the flood of RVs out there, there are very few reasonable long-term sites with services available. You’ll end up boon docking on public land to save money. No water, no power, no sewage disposal, etc.

All the recent deals outside of Alberta will fall apart and the sellers will sue the buyers. The courts will be backlogged for years and years to come.

If the Federal Reserve raised its interbank overnight Federal Funds lending advisory rate to 10% to 10.5% (it’s always set in a rate range) tonight, that would have no impact whatsoever on inflation which is consumer demand and government regulation driven in the US and globally.

SoCalBeachDude,

That’s clueless thoughtless BS. If the Fed raised the ff rate, as you say, by 10 percentage points tonight, the stock market would crash and the bond market would first freeze and then crash, with yields spiking, and mortgage rates would spike too, and so the housing market would freeze. And everyone would be shocked, and demand would on the spot vanish, and any company that wants to sell anything would have to put it on sale — and you can kiss price increases goodbye. This would be the end of inflation on the spot, driven by a plunge in demand. That’s how that works, and maybe the Fed should do it.

If you don’t understand that monetary policies are working through DEMAND (increasing or decreasing demand), you don’t understand anything about central banks and inflation.

There would be looting in the streets with a 10% FFR

I wonder how many times it has to be said that raising interest rates will not impact the demand for necessities such as food.

You can only do so much substitution for things like that.

Not everyone is so budget-constrained that every dollar is spoken for every month to buy necessities. Lots of people make lots of money and spend lots of money, and they spend some of it on expensive foods that are NOT necessities, including restaurant foods, and steaks, etc. and these people have assets, and rising interest rates cause asset prices to fall, and so these people are cutting back some and reduce demand.

Obviously, commodity cycles don’t run in parallel with interest rates, they go all over the place all the time. But when you crash the asset markets, often commodities come crashing down as well (we’ve seen that during the Financial Crisis).

Do you guys remember the Great Financial Crisis of 2008, when the Financial Industrial Complex very nearly detonated the Global Economy? The one The Fed had to rescue with trillions in debt, negative real interest rates, and much weeping and gnashing of teeth? The millions of unprosecuted cases of conveyance fraud? Lehman, Bear Stearns, Indymac, TARP? Yeah, that one.

That crisis was never actually resolved because that debt and those rates have had to remain in place ever since. It’s why The Fed has been so dilatory about raising rates and rolling off the toxic financial sludge. They can’t. The economy is dependent on keeping them where they are, and so as to preserve the wealthy campaign contributor class. Those distortions have been showing up as federal budget deficits, corporate debt, household debt, and crap jobs for years. It was only a matter of time before the distortions showed up as inflation as well.

They’ve been kicking the can down the road ever since.

Guess what?

They’ve run out of road.

No matter how bad things may be, they can always get worse. And they will. Next year the US goes full-on autocracy, Alternate Realities become dominant, and the widening cracks in domestic social order fall open. The crop failures become serious a couple of years after that. By 2030 the mass die-offs start ramping up. The Anthropocene Extinction accelerates year by year unabated. Projections that civilization would begin to collapse by 2040 have steadily held since 1972 and have been confirmed by decades of solid and extensive research.

This will all end in tears.

Post lux, tenebras.

The idea is to keep nominal values stable, or perhaps increasing slightly, like wages, below the rate of inflation. The sheeple won’t notice.

Soylant Green will be all left that is edible.

I have been wondering the scenario you were seeing play out. Thanks for posting your view.

You left out a hot war, but presented us with plenty to ponder.

I look forward to the light.

Also want to thank Wolf for calling inflation early and often when few else were discussing. He was right, the rest were not. There was a lot of push back that turned out to be incorrect.

And locally, I am seeing tons of houses coming on the market, and longer times on the market, with more aspirational pricing.

You forgot about the slow carbon asphyxiation.

With you completely until the last paragraph. People have predicted the end of times since Malthus and climate change ain’t it.

una:

seems like your last, or recent, comment was that WE, in this case we the commentariat on Wolf’s wonder were being too negative…

change your mind, eh?

Consistency is the hobgoblin of little minds.

– Emerson

Anyone else experiencing major shortages still? Just this week my alternator went and while covered under Honda warranty, my dealer said they are on backorder. They bumped me up to critical, but said it could take weeks to months. Tried to rent a car and was told they didn’t have any. Was able to get one the next day, but many people waiting. I rented a small car for $49/day. They had to give me a minivan for the same price because they had nothing else. Wait until we get to Memorial Day and summer vacations.

Janna,

The definition of damned if you do and damned if you don’t…

The dealer has to order the part from Honda new to protect the warranty, his work and charge Honda…

You can order a replacement and pay for it, install it yourself or have an independent shop do it for you… it’s not that difficult…

Most reputable people parts places have their own warranty on the parts they sell…

Or you can keep renting at $50 a day…

Personally, I’d ditch the dealer and move on…

We may go that route if it takes too long. We were already looking into rideshare so this just pushed us closer faster. Thankfully, I return the rental tomorrow.

Bank of Canada:

“By making borrowing more expensive and increasing the return on saving, a higher policy interest rate dampens spending, reducing overall demand in the economy”

Is this statement always true, even in the cases when interest rate is much lower than inflation rate ? Lets say I have X dollars in my bank account, they are not bearing any interest, and their purchasing power receds at the annual rate of 6%. I am looking to buy a nice item (car etc) for X dollars, not because I really need it, but because I wish to put my money into something of real value. Now bank raises interest on my money from 0 to 0.5%, still far below 6% inflation. So now my purchasing power inflates away at real interest rate of 5.5% (6% – 0.5% = 5.5%) rather than 6%. It still inflates away at right rate, but slightly slower than before. This is not going to change my decision to make a purchase. So it seems to me that there is a threshold on the interest rate such that any changes in interest rate that still leave this interest rate significantly below the inflation, are not affecting spending decisions (“inflation mindset” that Wolf talks about). Any thoughts ?

What is especially not true is that the interest rate banks pay on savings will somehow increase if the policy guidance interest rate from the Federal Reserve is increased. That all depends on LOAN DEMAND and if loan demand does not increase then the banks will not now raise the interest rate on savings as the last thing they want is more money from customers that they have no use for.

AK

Your argument seems logical to me, even for depreciable items (vehicles, appliances, maybe even furniture).

I use 10% depreciation (per year) as a rule of thumb. Might as well buy a $500 sofa today if it will be worth $500 in 10 years. Intuitively, it just feels right to buy buy buy.

That makes real estate a no brainer during inflation – appreciating asset, or at minimum, holds its value.

Real estate is historically very expensive. This isn’t the 1970’s. Interest rates have been very low for a long time (the entire 21st century) and while rents are very high.

Higher inflation isn’t going to lower interest rates and it won’t make rents more affordable either.

AF

True – but paying cash for real estate is a good play vs long term inflation. As Wolf has pointed out many times, rents are climbing but have not caught up with prices yet.

Low priced high margin rental real estate bought for cash used to to be a no brainer. I used to have some SFHs with 15%+ ROIs. With leverage, they would have been 22%+ but I have always been “no debt.” Those same properties are pretty much break even now – i.e. “bank on the equity appreciation.” However, when everything else is losing 10% annually, an appreciating asset with a break even cash flow looks pretty good.

Front Running the Fed…

At first glance I thought they caught some more Fed Governors….

But, I guess….So what if they did?

Michael Burry on Twitter:

“The Fed has no intention of fighting inflation. Serial half-point hikes are for getting elevation before stocks and the consumer tap out. Same with with rapid-fire QT. The Fed’s all about reloading the monetary bazooka. So it can ride to the rescue & finance the fiscal put.”

Got Dogecoin?

…still transitory

Humble nsa’s compound is located south of Victoria BC across the Salish Sea (formerly the Straight of Juan de Fuca). Canucks visit south for an authentic third world experience, just as San Diegans frequent Tijuana. Cloistored americanos realize not that canucks are considerably more affluent than americanos, though hobbled by their long border along the 49th parallel (thanks to James K. Polk) with the US. Studies show that the three countries with the greatest wealth potential based on per capita resources are the Russian Federation, Canada, then Australia in that order. Econoniic analogies between the affluent canucks and americanos descending into third world chaos are not accurate. Visit Victoria BC or Vancouver BC (known locally as Hongcouver) to confirm these observations.

nsa,

LOL. You’re confusing a resource economy, such as many poor African countries, with economies that produce high-value-added goods and services, such as Japan, the US, Germany, South Korea, etc. The US is a mix of both, because it has a lot of resources as well, in addition to being the second largest manufacturer in the world (behind China) and the largest services provider. Germany, Japan, and South Korea have very few resources and have to import resources from poor countries such as Russia and African countries, to make high-value added products.

you’re a moron

What studies?

If these studies had any merit whatsoever, Switzerland would be dirt poor. It isn’t because affluence doesn’t depend upon natural resources. It’s a factor but not the deciding factor, not even close.

Look at the poorest countries. Many of them (maybe most) have a lot of natural resources though often it’s concentrated in one or a few.

What these countries have in common is dysfunctional government from a culture which isn’t conductive to economic development.

Two different things entirely.

Equatorial Guinea, a country that hasn’t been involved in any geopolitical warfare, had a GDP per capita that quadrupled every five years, yet the citizens were dirt poor and lived on less than US$1 a day.

Sounds a lot like the USA: dysfunctional government……

On cue after any news and as predicted The Fed trotted out ( cautious ) Williams to declare a .5% increase in the rate in May is ” reasonable”. Williams is a “very cautious” Fed Man because a .5% increase could cut into his and the other Fed parasite’s rate repression fueled bubble wealth. Cautious Willie is a very careful man. So we need to be real cautious also , just like Cautious Willie. I would recommend a slow and stealthy stalk of the meat case at your grocery store and pounce on your $+7 a lb burger and run like hell to the checkout before the “swarm” takes you down and adds another $1 to your burger. Rest assure Cautious Willie has his cautious eyeball on inflation.

I am not sure if I a reading the BOJ balance sheet chart correctly but just when I thought they were under control, did they just increase their balance sheet in March 2022?

ru82,

I’m so tired of this nonsense.

Its weekly balance sheet totals:

Feb 23 (last point before March): $494 billion

Apr 6 (first point after March): $487 billion

Total fell by $7 billion or by -1.5%

The BOJ includes things such as gold, stocks, REITS, Trusts, and loans along with foreign currency assets on their books.

As such, those BOJ figures will jump about a lot depending on the valuation of those things.

Gold appears to be carried at a fixed valuation, but the others vary and would be often more than 1.5% over that time period.

If you are talking about only JGB’s then that is probably different.

KWHPete,

Below is my update on the BoJ’s balance sheet by asset category. Its equity holdings, despite all the hype about them, are minuscule compared to its huge holdings of government debt, and movements in the stock market don’t have a big impact on the overall balance sheet. What does have a big impact is when big issues if of long-term bonds mature in one month and come off the balance sheet, to be replaced in another month by another big purchase of long-term bonds. All this is spelled out here:

https://wolfstreet.com/2022/04/07/bank-of-japans-mind-game-despite-all-the-hype-about-massive-bond-buys-to-cap-the-10-year-yield-at-0-25-actual-bond-holdings-fell/

Well I went to the BOJ web site and actually looked at the figures. These amounts are as follows in thousands of yen:

Date JGB Balance Total Assets

Dec 31 521,119,559,775 723,765,934,627

Jan 10 520,576,959,613 725,052,847,621

Jan 20 521,122,074,006 723,850,169,736

Jan 31 523,227,928,907 725,144,402,640

Feb 10 525,152,519,983 727,093,261,373

Feb 20 526,590,194,092 728,810,176,769

Feb 28 527,547,270,501 730,555,391,482

Mar 10 529,768,131,981 737,252,062,040

Mar 20 532,147,793,178 737,616,067,360

Mar 31 526,173,698,752 735,820,259,585

Apr 10 526,830,982,898 736,595,048,486

So from Dec 31 the total JGB balance at the BOJ is up and the total assets on the books is also up.

As of April 10 2021:

Apr 10 533,520,407,566 715,303,333,908

The balance of JGB’s has fallen a little, but the total assets on the BOJ’s books is still way up from a year ago.

So I went back another year to April 2020:

Apr 10 488,796,113,912 609,891,039,359

Just looking at the JGB balance shows a slight reduction from April 10 2021, but overall the BOJ is still expanding its balance sheet.

The reduction in the JGB balance has been more than made up by other items.

Are you looking at the US dollar equivalent instead of the actual yen value?

KWHPete,

RTGDFA

If you don’t know what RTGDFA means, it means Read The G** D*** F**king Article

You refuse to click on the link I gave you. You refuse to read my articles. It gives you all the charts and data. LOANS. LOANS. LOANS. LOANS jumped. I explained that in my article and supplied a chart. Why should I let you post your crap here if you don’t RTGDFA. My article that I linked includes these charts (I think I’m done with your comments):

Anyone noticing on this last bounce that started in Mid march did not include the banks like JPM or BAC. Rising interest rates are supposed to be good for banks because they borrow short rates and lend long rates. But when short rates are almost as high as long rates it is hard to make a profit.

Anyway, you cannot have a true upswing or bull market unless the banks are participating.

JPM Chase may be in trouble again already. They’ve spent $84 Bil on stock buybacks the last five years and its stock is sinking.

Where have we seen this before?

Nomura, JPMorgan and Goldman Sachs received a cumulative $8 Trillion from the Fed’s emergency repo loans in 4q 2019, which isn’t legal but so what. They’ve had Fed bailouts in 2019 and 2020. Related Fed documents aren’t transparent so one Could reasonably assume the game’s afoot but probably Should not.

They may have found an innovative way to lose money, or the appearance thereof. Laundering off assets through central London isn’t innovative.

wonder if Powell and Co. will have an inter meeting hike? Like over this weekend? Can’t let the BOC steal their thunder.

1) TSX backbone Oct 26 high // 27 low 2021.

2) TSX Buying climax : Nov 16 high // AR : Dec 1 low.

3) There will be no honeymoon between Europe and Putin for many years.

4) Ukraine war might be equivalent to the closure of the Suez canal

in 1967 for a decade.

5) If u want to eat, Canada & US produce soybean and wheat.

6) If u want to drive, we produce oil and Natgas.

7) When TM pipeline is good to go ready, there will be a war between CA and Asia.

8) RRP is a negative feedback loop sucking liquidity when the inflation is too hot.

9) When the market plunge, RRP will provide liquidity.

10) If SPX plunge more than 1,000 points, JP will not cut rates as he did in 2018, he will flood the markets with liquidity, reducing RRP, producing stopping actions and a quickie.

1) Is the Fed behind the curve : no.

2) RRP is rising since Mar 2021sucking liquidity from the market.

3) In June 2021 RRP was $1T.

4) In Oct 2021 > $1.6T.

5) In Dec 2021 = $1.9T.

6) Window dressing : no.

7) Fed war chest, JP secret ammunition.

The BoC has to hike some more so that the Escalade driving soccer moms feel the pinch.

“By making borrowing more expensive and increasing the return on saving, a higher policy interest rate dampens spending…”

No, not really until the rate of return on savings is positive.

As long as inflation is higher than the interest rate on savings there is no incentive to save.