10-Year yield hits 2.31%, 30-year fixed mortgage rate hits 4.66%. And why the funny kangaroo-shaped yield curve says nothing about the economy.

By Wolf Richter for WOLF STREET.

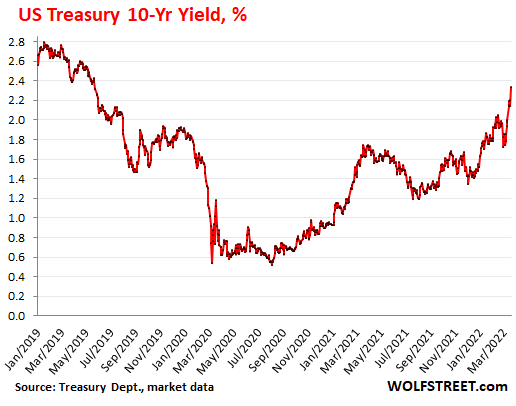

Another day, another rout in the bond market. Bond yields are an inverse reflection of bond prices: rising yields means bond prices fell. The 10-year Treasury yield at the moment spiked by 16 basis points to hit 2.31% in afternoon trading, the highest since May 2019.

One of the trigger points was possibly – though you can never really tell with these crazy markets – that Fed Chair Pro Tempore Jerome Powell spoke, confirming the Fed’s new-found religion in using its monetary tools to tamp down on inflation, at least a little bit, while trying to achieve a “soft landing” or at least a “soft-ish landing.”

His speech included a line that stated that the Fed may impose bigger rate hikes, such as 50-basis-point rate hikes, (possibly plural) if needed to get there:

“In particular, if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so,” he said.

So here we go. The two-year Treasury yield spiked by 18 basis points to 2.13% at the moment, the highest since May 2019:

All Treasury yields are still ridiculously below the rate of CPI inflation, which spiked to 7.9% in February, and they have a lot of catching-up to do, and they remain deeply negative in real terms.

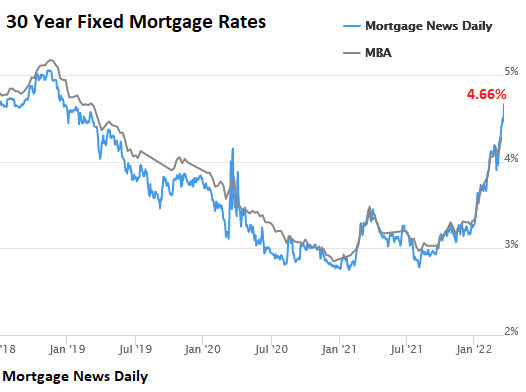

The average 30-year fixed mortgage rate jumped to 4.66% today, the highest since December 2018, according to the daily data by Mortgage New Daily. And all mortgage rates, though they spiked, remain negative in real terms, even for subprime mortgages:

And nearly all corporate bond yields, though they too have risen sharply, remain negative in real terms, including most junk bond yields down through the category of single-B, which is considered “highly speculative” – here’s my cheat sheet on corporate bond credit ratings by ratings agency.

You have to go down all the way into deep-junk, to CCC-rated bonds and below to beat inflation, where you’re facing anything from “substantial risk” of default to actual default, which is what it now takes to beat inflation while losing all or part of your capital trying, thanks to the most reckless Fed ever.

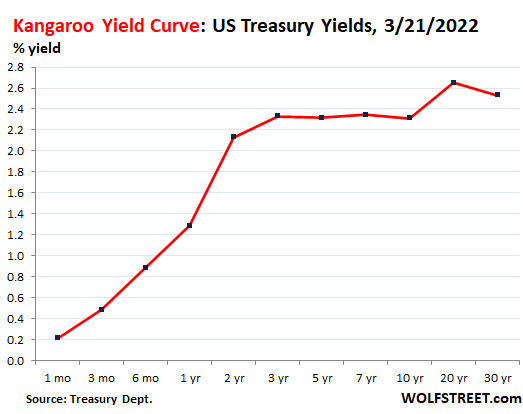

The yield curve groans under the Fed’s gigantic balance sheet.

The weight of the Fed’s gargantuan balance sheet is pushing down on long-term yields that the Fed spent years repressing with trillions of dollars of QE since 2008, and most radically since March 2020. QE has ended, but the weight is still there, the $5.76 trillion in Treasury securities and the $2.73 trillion in MBS, for a combined $8.5 trillion in securities. The Fed has taken $8.5 trillion in supply of bonds off the market, and the yield curve reflects that.

The Fed is talking about lowering its weight. Quantitative Tightening “could come as soon as” in May, Powell confirmed today, adding that no decision has been made. But when it starts, it won’t move nearly fast enough.

At the same time, while long-term yields are repressed by the Fed’s balance sheet, the shortest-term yields of one month to three months are firmly controlled by the Fed’s policy rates.

In the one-year through three-year range, it’s a three-way tug of war (why has no one invented that sport yet?) between the Fed’s policy rates at the short end, rate-hike expectations shooting up for the next couple of years, and the Fed’s gargantuan balance sheet sitting on top of the longer-term yields and long-term yields and weighing them down.

This is producing a funny kangaroo-shaped yield curve, which is steep in the front up through the three-year yield, but then essentially flat through the 10-year yield, a bump at 20 years, followed by an inversion between the 20-year and the 30-year yields:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

And he dragged the stock market down today with his comments. But we all know that’s the game plan.

The mainstream media is to tell ya to Buy high and sell low! Be careful of the mainstream media. They told Americans to buy Dogcoin when it was at its peak at 70 cents. It has crashed to 15 cents for quite a while.

Who exactly “told Americans to buy Dogcoin”?

Just curious, and I am sure it was not J. Powell.

Other Americans who already held Dogecoin.

The “mainstream media” reported on it, but as a curiosity. The hype was 100% social media based.

Pretty sure the culprit was Elon

Ciena, thanks for reminding me. It skipped my mind.

What really stops fed Presidents from owning Dog Coin?

Its good to see that Senators have fed trapped. They are waiting for shit to blow so that they can blame it on current guys and then “cancel” them. That way the new feds can start with a clean shirt (the current fed has lost people trust).

Senators won’t confirm fed nominees before that because its easier to cancel than to fire. Also they know the high probability of shit blowing up in the “greatest economy ever”.

Except that Dogecoin should be worth nothing, since it is actually nothing.

WR has already told you everything you need to know about cryptocurrencies, and it’s not good:

https://wolfstreet.com/2021/02/28/the-big-buy-hype-bitcoin-casino/

Sue Webber refers to CCs as ‘prosecution futures’, and for good reason.

S&P down a grand total of … 2 pts today.

4,463 to 4,461.

Another Jawboning attempt. Last week when he had to walk his talk about reigning in inflation, he backtracked. The data did not change in last 1 week. He knows media will raise enough concerns

in next 5 weeks that he can backtrack again.

Well, while some American companies may have future prospects that justify their stock prices, a majority now are grossly over valued, so anything that pushes those values down will reduce any future crash. At least we are not in the economically apocalyptic situation that the CCP created in China. Watch Stoic Finance, which is a yt commenter, who just explained how China’s real estate market and stocks are essentially tulip mania writ large. Ha, schadenfreude feels so good. LOL

Apocalyptic situation in any major economies will unfortunately find its way back to our US economy. Just like the COVID. The world either wins or loses together! It’s already happening with the hyper-inflation.

Not true. We are their consumers. They are not our consumers, except in small amounts. Thus, if they go under, it does not affect us, except if the quasi-slave factories that produce the cheap TVs, etc., that they sell us were to go under. They will not.

Powell’s usual attempt to sound forceful and yet to back off, to equivocate, to finesse it, is on display. But the question of our times is, when assets and employment really drop, at new levels, will he blink?

As usual, I think he tries the trial balloon, the jawboning, the feint, up front, to see if that works. The test is yet to come.

It is all priced in they say. Well exactly what is priced in? He said back on 3/21/22 the FED is aggressively looking to take into consideration the possible increase of rates. Check back and see how the market digests it and then when the next meeting comes they will talk about the talking and meetings they have been having. Expect it will be in direct response to the people they know impacted and need support right now

What

Well said Phleep. I thought 50 basis point hike was on table before also. So what really changed? Is Wolf Jawboning for fed now :). I believe Wolf is smart enough to know that Fed is no longer defendable or even dependable.

Yes, go ahead and fight the Fed on this one.

Dont we own the Fed. From wiki: Democracy (Greek: δημοκρατία, dēmokratiā, from dēmos ‘people’ and kratos ‘rule'[1]) is a form of government in which the people have the authority to deliberate and decide legislation (“direct democracy”), or to choose governing officials to do so (“representative democracy”).

Re :Raj

No we don’t own the Fed. The fed is controlled by the banks and it’s shareholders.

The US is a corporation, not a democracy.

@Raj – no, it’s communism where the state owns the Fed and the elites run it. We just sit on committees and jawbone.

I don’t think that’s communism.

In the U.S. private investors make bets (capitalism!) but the well-connected investors never lose. They privatize the profits but socialize the losses.

The lay name for that is “lemon socialism”. The wealthy get ever richer while the rest get angrier and angrier.

China is supporting there economy,we’re destroying ours

China? Sure, if you mean the CCP nationalizing choice developer assets (letting the bondholders eat the worst assets), clamping down on tech companies until they pop, then turning around with some plunge protection to prop up equities?

Greg,

China has been targeting one key industry after another to subsidize, protect, and corner. They haven’t climbed the ladder to the top of the knowledge economy quite yet but they dominate many lower and middle tiers of manufacturing.

Maybe you are suggesting this won’t work for the knowledge economy or that they’ll eventually ruin what they’ve built because central planning has such obvious downsides. It’s certainly possible. On the other hand, many people think mercantilism can work for a good long while if the other side doesn’t fight back.

Best regards,

Ed

C’mon folks,,, everyone knows USA is a REPUBLIC,,, and most folks know WHY that is so, as opposed to a democracy.

It starts with SPQR (Senatus Populus Quod Romanus) and we all know how that turned out,,,

And proceeds from there to ”demos” or the MOB, yes, the MOB who has, would and does vote for any of the UNIPARTY people who will give them MORE OPM!!!

The answer my friends IS blowing in the Wind,,, in this case the wind of change.

And until we actually DO have some semblance of democracy IMO we will continue to progress as has been the case for eva, with the rich getting richer and WE the PEONs getting the shaft(s).

What do you think Powell would do if the S&P 500 entered a bear market but inflation is still high and there isn’t visible deterioration in the economic data (like a 2018 year end situation?)

Would he delay tightening to save the market, or proceed anyway?

I don’t believe in bull / bear markets, only euphoria & panics, but when the S&P ‘does’ see 4000 to 3850 this year, Powell will start taking rate hikes off the table and even that will be enough to spark a massive rally in time for mid-terms.

Couple that with a $2K stimmie check (er the American Relief Stimulus ̶B̶i̶l̶l̶ Executive Order) with the promise of moar if the Dems get elected, and that’s how you kick the can down the road to a ‘win’. Rinse wash and repeat for 2023 and you get the idea…at least until CPI > 10% with DXY < 82. That's when the 3% unannounced rate hike happens and markets don't open for a week. Oops spoilers.

If inflation expectations really set in (i.e. wage inflation picks up as well) then he will have to hike. There is no point trying to protect asset prices if confidence in the dollar has collapsed. Asset pricing is all about confidence in the future (even in the current ponzi-esk form) and if we cross the rubicon of out-of-control dollar inflation, then that confidence will erode very quickly.

I don’t think anyone is questioning his desire to tamp down inflation (yet). But what plenty of people are questioning is whether he’s being way too timid and will let the situation escalate to the point where something drastic has to be done. In the end you either value monetary stability above all else – including potentially inflicting huge amounts of pain on the economy and your buddies at the country club – or you don’t and you keep trying to hope the problem just goes away by itself. Experience tends to suggest it doesn’t just go away, but maybe it’s going to be different this time (TM).

i want to go a bit further than you. nobody is questioning his desire to tamp down inflation in a purely theoretical sense. that is, if he had the option to push two buttons, one would magically stop inflation, and the other would keep inflation going as it has, he would pick the former, all else equal.

what people are questioning is his desire to tamp down inflation *despite* the fact that it will have negative consequences to the asset markets.

that’s what remains to be seen.

The S&P entered a bear market when it topped out on January 3. (No I don’t buy the financial-media-lite formulation that a bear market gets “entered” after it’s already 20% down … waaay tooo late to do any good!)

Powell: stop talking, start doing.

he reminds me of the smoker who is always “trying to quit.”

either do it or stfu about it.

He said he didn’t want negative rates. Inflation is 8%. Does ANYONE think this clown is gonna raise short rates to 9%?

We’ve had 30 years of Greenspan and all the others looting this nation. It won’t end until the dollar is literally swirling down the drain.

Harold –

Paul Volker didn’t act emphatically until inflation was “double digit.” (See quote below). Eventually he raised rates much higher than 9%.

Because it reports to congress, the central bank is not constructed to react until things are so bad that it’s actually POLITICALLY acceptable to act with conviction. Like it or not, CB policy shifts take time….

___________________________

“The Federal Reserve increased short-term interest rates last Wednesday 3/16/2022, raising the federal funds rate to a target range of 0.25% to 0.50%. From 8/15/1979 to 3/18/1980, the Fed under Paul Volcker’s leadership raised the fed funds rate from 11% to 20% to eradicate the double-digit inflation the US w as experiencing at that time (source: Federal Reserve).”

From By The Numbers, 3/21/22

“Because it reports to congress,”

Did you watch the hearings?

They report to a bunch of idiots reading inane questions written by their recently graduated staff….much which have nothing to do with monetary policy, but more to do with gender, social justice, green energy, etc.

“Paul Volker didn’t act emphatically until inflation was ‘double digit.'”

If the CPI were still calculated as it was back then it would already be double digits. I cringe when I see graphs of CPI over time. It’s like comparing apples and oranges.

” … corporate bond yields, though they too have risen sharply, remain negative in real terms ….”

Maybe since the Powell put embraced junk in spring 2020, bond punters still think he is bluffing?

So .. The Ruddy Bloody Roo Leap of $hock .. e.i. the death-throws of overly leveraged corporates, thieves, rakes, and scoundrels?

Outstanding!

Wolf,

Just off the top of your head, it would be good to hear your observations about how Powell’s tone, demeanor and words have shifted over the last year or too. He has transitioned from being almost casual to concerned and now maybe very concerned. Now the guidance is somewhat more clear and the timeline no longer vague. I don’t know if his statements are becoming more frequent. The tone and frequency of announcements would indicate a lot. Even without current unfolding developments, it will be too little and too late.

i get the impression that he’s concerned, not because he actually cares about the common man (he doesn’t), but because he’s concerned about his legacy.

he doesn’t want to be seen as the guy who destroyed the u.s. dollar.

Jake…

I am just guessing, but when the Saudi and China were talking about Oil pricing not in dollars….I think Powell saw his legacy flash before his eyes.

We all know savers have be slaughtered by the Fed, but imagine these foreign countries that hold Trillions in US debt with an inflation delivered negative rate?

America is the world’s debtor nation. The dollar is the world’s reserve currency at about 60% of all assets at Central Banks. The right policy domestically is to tax the oligarchs who run the government and own or manage 80% of all assets. . That would reign in inflation. But the ‘free market’ libertarians simply won’t pay taxes! They are defunding government at all levels. What they cannot defund they privatize. Up to and including public education. The Republican Party is anti-democracy and autocratic.

and that’s ultimately the problem with money printing. you can believe all you want that it’s fine as long as the new money goes to assets, or even better, is held overseas. but the reality is that once the money is printed, you can’t control what happens with it. if foreign countries decide that these trillions will be inflated away, they’ll come back to the u.s. with them and buy whatever assets they can.

the fed saw their insane scheme appear to “work” from 2009-2021, so it emboldened them. but money printing didn’t work. it never does. it’s just that the u.s. dollar’s relative strength and our position in the world meant that the consequences were delayed. but the consequences always come eventually, and now they’re staring us in the face.

So did India. By the way, the Reserve Bank of India – the country’s central bank – has just announced “the diversification of its dollar reserves”, that is, it stops storing dollars almost exclusively and will also do so “in other currencies and in gold. India has $622 billion in reserves. Although percentages or amounts are not specified, the fact is notorious because there are already many who are seeing how the West uses the economic weapon to bend countries. “India does not expect the US to impose similar sanctions [as those of Russia], but this is a wake-up call for the world. It cannot be predicted and I think that all countries will start thinking about it in the future”, is what said the governor of the BRI when announcing the measure.

Powell is probably afraid of Americans starting a revolt against the inflation. I’m amazed to see how arms are like a home tool in America. It’s like every American is armed to the teeth, including in the Blue states.

The 22 members of my extended family are all progressives and include several military veterans. We are armed to the teeth and prepared for civil war.

Escierto

And exactly what will that accomplish? What would your extended family do with central banking if it takes over the government

and yet nothing ever happens, except psychos periodically shooting up schools or grocery stores. We’ll continue to destroy ourselves while the elites loot the country.

My take is that he and the other talking heads are preparing the markets for more and bigger rate hikes and higher interest rates. But they’re still so woefully behind the curve, and they’re still hoping that interest rates of somewhere between 2% and 4%, depending on talking head, will bring 7.9% CPI inflation back down.

CPI inflation will go over 8% in the coming months. And they know it too. Powell said as much today. This is pretty scary inflation.

They also want to rely on QT more than rate hikes, and we’ll see how they will do that, but in principle, that makes sense to me. The fastest way to bring inflation down is to sell outright lots of assets to get long-term Treasury yields to spike 2-3 percentage points above CPI. This would be chaotic, but it would bring inflation down quickly.

Short-term rates don’t matter all that much. So the rate hikes, which raise short-term interest rates directly, might matter less than QT if it’s big enough.

There is no doubt in my mind that they’re now taking inflation very seriously. But they’re still trying to get that “soft-ish landing.” And that will cause them to dilly-dally around too long, and to let inflation get worse, before they really crack down, and that might then cause some real damage.

According to CNN.com, Powell said their policies will help bring inflation near 2 percent within 3 years. That’s so comforting.

Anyone still watching CNN? SMH

“The fastest way to bring inflation down is to sell outright lots of assets to get long-term Treasury yields to spike 2-3 percentage points above CPI. This would be chaotic, but it would bring inflation down quickly. ”

Is that right?

Interest rates increases via increasing the supply of long term bonds in going to decrease inflation?

It might decrease “inflation” in monetary assets and maybe decrease “inflation” in real estate prices in three or four months, but it isn’t going to decrease inflation in items that are basically immune to interest rate changes.

A 4 or 5% fed funds rate isn’t going increase the supply of wheat, oil, fertilizer and it certainly isn’t going to decrease the price of those items.

The scenario I outlined will crash stocks and bonds and much of everything else, and zombie companies will sort out their debts in bankruptcy courts at the expense of investors, and state and local governments will suddenly find out that their tax revenues are shrinking, and they’ll suddenly have to cut back on their spending, and consumer will suddenly have trouble borrowing to spend, and they can’t do cash-out refis because interest rates are too high, and so they’re stuck with spending the money they actually earn, etc. etc. and this crazy demand for everything will cool off by a lot, overcapacity will set in again, as will price competition amid shrinking demand, which spells the end of this bout of inflation.

Powell knows this too but doesn’t have the appetite to do it.

“Powell knows this too but doesn’t have the appetite to do it.”

Yeah, yet he talks about being a student of Volker. This guy is a fraudster through and through. He desperately wants these inflated asset prices to stick. He has zero tolerance for falling asset prices, the young, the poor and the working class be damned.

I think it is likely that Powell has gotten some forward indications of what this next CPI and PPI numbers are going to be with the Ukraine situation fully accounted for. And it won’t be a 40 year high in inflation, it just might be an all-time high.

All time by the old CPI calculations? I could buy that…heh

Wolf thanks for your insights. Does JPow have to wait until the next Fed meeting to raise rates? Or can they do it earlier?

The Fed does rate changes occasionally on an emergency basis between regular meetings. They normally want to project a calm and orderly process though, not panic. Especially with hikes. Rate drops come as a sort of relief but hikes are like quitting the booze during the party.

Powell is smart I think to signal a .5 hike in advance, for whenever it is done. We may have inflation spikes fast with things like the war, and the cry of “do something!” may emerge quickly.

Well Wolf, “They” … the movers n shakers (both .gov … AND corpserates .. need to realize that ‘they’ ARE • PLAYING • WITH • FIRE – with regard to the lowlymokian plebes – who’ll will EAT Them Alive .. or shoot them dead, or hang them from the nearest light standard .. when they realize just how screwed they became, due to the chichanery & swindling brought upon them .. by our vaunted CONgreasers, State Dept., I T ‘ community .. at the behest of GIANTMONEY .. who care not one wit – for ANYTHING! but their own • grifting • EGO$.

I rest my case.

No they won’t. They might attempt to do that for some bs reason like CRT but the populace has been conditioned to accept that their financial condition is a personal failing rather than a structural issue

Re: phoenix

This is America, who takes responsibility for their own actions? lol

The idiots flooded the world with money, or the thieves flooded the world with money, take your pick. Probably the latter. Inflation is no surprise, and it’s not going to be undone. Your saved dollars are worth less. Your reduced standard of living is baked in the cake.

I think both: thieves initially, but idiots in that the extent of inflation was grossly underestimated. It’s been so long since high inflation that the ‘experts’ grew complacent.

“CPI inflation will go over 8% in the coming months”

The next numbers have the Ukraine impact.

The “40 year high” just might change to ALL TIME HIGH.

This will bring the surprise, and warranted 1/2pt.

Wow, all the way to .8 %….less than one tenth of the reported inflation. So, so far behind the curve….as you note.

Peeling the assets off the balance sheet is likely more important than rate hikes. The “sopping” up of the $4 Trillion of new money injected the past two years must be as prompt as was the dispensing of that money.

“But when it starts, it won’t move nearly fast enough.”

Totally agree. I’ll be stunned if the initial pace is greater than $75 / mo.

Inflation will easily top 10% if the food shortages that are being predicted come to roost later this year.

Nowadays, the economic conditions seem to be much worse than the late 70’s / early 80’s. Maybe I need to brush up on my history.

Wolf said: “The fastest way to bring inflation down is to sell outright lots of assets to get long-term Treasury yields to spike 2-3 percentage points above CPI. This would be chaotic, but it would bring inflation down quickly”

==============================

Does this remove any purchasing power from the system. or just shift it around? Dollars exchanged for FED Treasuries are out of circulation, assuming the FED holds them out, but have only been replaced by Treasuries introduced into the system. These Treasuries can be used as collateral for bank loans; these bank loans can be via newly created dollars. Meanwhile the FED had to sell the Treasuries at a discount, leaving many of the dollars still in the system.

cb,

Lower asset values remove “purchasing power” of asset holders — usually they’ll buy fewer assets and pay off leverage. The reverse is also true: rising asset values add purchasing power to asset holders, which is the “Wealth Effect.”

Quantitative Tightening removes liquidity from the system, which causes asset prices to decline over time, which removes purchasing power of asset holders. It generally doesn’t touch labor.

Inflation removes purchasing power from the system across the board, and hits labor particularly hard.

@ Wolf –

Thanks for the answer, which included:

“Quantitative Tightening removes liquidity from the system, which causes asset prices to decline over time, which removes purchasing power of asset holders”

————————————————

I will put forth that quanitative tightening, to the extent that the FED sells it’s treasuries for dollars, does not remove liquidity but merely thickens the viscosity of the liquidity.

A. The treasuries are sold at a discount, leaving profit and dollars in the system.

B. The treasuries are great collateral, and can be easily used for bank loans, which can create new dollars. Now the Treasuries and new dollars are in the system.

Side benefit: The purchaser of the Treasuries not only received them at a discount, but now receives interest and holds an asset quickly convertible to cash.

Your fundamental claim is QE/QT are inert swaps of reserves for treasuries that have no effect on asset prices. This is not true and we have unambigous empirical evidence for this.

If the FED actually does what it is alluding to (dilly dallying it may still be) it would still cut its BS by 3T over 3 years. This along with new Treasury issuance (see great steepening by Joseph Wang) would create a supply of 2T of new treasuries to be absorbed by private sector, foreign guvs etc in the next year. Take any equilibrium and throw a trillion dollars worth of supply in that, prices tend to down.

QE monetizes fiscal deficits and suppresses interest rates. QT by definition does the reverse, i.e., long term rates will have to go higher. That is toxic for asset values in the fundamental sense of higher discount rate or lower relative yields vis a vis recently cheaper Treasuries (high Risk free rate). Cheaper treasuries also force asset allocations to readjust in favor of Treasuries over Risk. TINA dies with Treasury yield going higher than Equity yield.

Housing at the very least slows as coming up 1% from super low mortgages (say 3.5% to 4.5%) craters demand much faster than going from (6.5% to 7.5%).

Inflation is already causing sharp drops in EPS estimates, making the relative forward yield of Equities even worse as T yields continue to race up. There is just scenario that one can visualize in which forcing addnl 2T in treasuries down the throat of pvt sector does not cause yields to rise ..except an asset meltdown. The die is cast, time to pay the piper.

@ Wolf –

Treasuries, once monetized, don’t get unmonetized by way of selling those Treasuries.

Nonsense.

@ Wolf-

Effectively Monetizing Treasuries is not he same as conducting textbook open market operations.

@ Tweedledum, who said:

“Your fundamental claim is QE/QT are inert swaps of reserves for treasuries that have no effect on asset prices.”

—————————————————-

Who made this claim? Where?

Not Wolf. Not me.

maybe Jeff Snider, but not on this site …………..

Wolf-

I would like to help make a market in Wolf Richter “Nothing Goes to Heck in a Straight Line” beer mugs. My current bid is $200 for an existing mug. Do you mind if I request asking prices from humans who legitimately own an authentic one on your website?

Perhaps you have an idea on how to provide100% price disclosure on the ask and bid. You have the best information for authenticity.

Please consider adding serial numbers to all future mugs after this production lull. Please consider assigning serial numbers to all previously distributed mugs, if possible.

You never had a friend like me.

We appreciate your laser focus on the truth, dispelling misconceptions and analyzing data releases in perspective.

Wolfstreet: PWDD : Pure Wisdom Dispensed Daily

Harry,

Thank you for your very kind words. Music to my ears.

In terms of the mugs, I’m not sure I totally understood your proposal. So I’ll address some points that I think you made.

If you want to buy a mug from an existing owner, you can make a clear offer to do so in the comments, and then if you get someone willing to sell you a mug for the price, I can put the two of you together via email, and I can verify that the other party actually got a mug and confirm that with you, and you can exchange info and close the deal via email.

I don’t think I (the mug printer) can put an indelible serial number on the mugs. They’re not equipped to do that. These are production runs where each mug is the same. And if I just stick a serial number on it, anyone can do it, and it would be meaningless.

BTW, I’m still strongly hoping to get a new shipment of the mugs. It has just been incredibly frustrating. There are rumors that the blank glass mugs will go into production next month. But no one can confirm anything. Drives me nuts.

We can discuss further details by email if you wish.

I called my bank today, because I was tired of them charging me 50 cents a check to deposit them through their mobile app. When I deposit checks into my personal checking using the app it is free. This is just a charge for business customers.

In addition, my personal checking receives 0.10% interest (wow, right?). My business checking receives 0.00%. So I called up the banker and he said it cost the banks to verify the checks, etc. and that is why they charge for business deposits through the app and why they don’t give any interest on my money sitting in the bank. I asked, “What would a small business pay for a business loan?” His answer was between 3 to 10%. So basically, the bank can use my deposits and pay me 0.00% and then turn around and charge another business up to 10%, but they can’t absorb the costs associated with mobile deposits? I would think it would cost less for a bank when I make a mobile deposit than for me to physically walk into the bank and take up a teller’s time.

Back to the interest rates…even if I got 0.10% like my personal account, they could charge 100 times more (10%) to another business customer!

Frustrated with Banks,

Seems like you need to shop for a better business bank account. Maybe your current bank offers something better. If not, another bank will. Sometimes there are minimum balance requirements (such as $5,000 or $20,000) to get the free deposits. And if you generally have enough cash in your account for that kind of minimum balance, you need to go fishing for a better bank, or for a better account at your current bank.

Banks are in a competitive business, and you need to shop around. I have never paid for deposits at my business bank.

Thanks Wolf…I have been looking…

The bank down the street offers a business account with free mobile deposits and 0.10% interest with balances over $1500. I usually have $20,000+ in the account, so I should be getting something. When I complained they credited me back all my mobile deposit fees for the last few months. When I shared with them that the other local bank offers free mobile deposits and 0.10% interest they said “we will see what we can do.”

I looked into online banks, such as BlueVine which offers 1.20%, but with conditions. BlueVine requires a customer to spend $500 per month with their debit card or have $2500 per month in direct deposits to get the 1.2%. I hate having conditions like that and I prefer having a local bank.

It is a hassle to change banks. I have many customers that use ACH, so I would have to update all of those. Hopefully my bank will make some changes and keep me there. I have been banking there for 12 years.

I think in the 1980s I would get about 8-10% interest at my local credit union.

I opened an account with a local bank in May 1969, it is stated on my checks along side my name and address. That bank was known at the time to bounce anyone who bounced checks. This was a known feature by local businesses so I liked how it worked. I have never been refused by any business.

This all went out when the banks began consolidating. Even though all the numbers on my account have remained the same I have been shuffled through several mergers. Even today I use this account for everyday business. In the time I’ve has the account I can count the times I’ve been inside the bank. Everything was handled by mail in the old days, today electronic banking has become a life saver. Not to mention time and fuel to going back and forth.

99% percent of all my purchases are made with other bank’s credit cards, along with all utilities. These cards all return a small percentage of rewards for my use and prompt payment. A large portion of all bills are handled online and electronically.

Never in the course of doing business have I paid a fee for anything. Needless to say I don’t have an ATM card.

This got a major reaction from another banker as I’m not paying my way according to him. He by the way is no longer in business.

This is a bit long winded and off topic but put it out there to show what can be done in the Midwest. It probably explains my grey hair!

Frustrated:

Volcker jacked up rates to 20% in the 1980s. Cratered the economy, but savers made out like banditos.

Savers didn’t make out like bandits. The purchasing power of their principal got wiped out by inflation, and they got some interest income to compensate them in part for the wipe-out of purchasing power of their principal.

The people who made out like bandits were the buyers of 30-year bonds at the peak of inflation in the early 1980s, when they yielded something like 15%, and these people collected 15% interest for 30 years, as inflation dropped into the low single digits. That was one of the best deals ever.

Those paper US Savings Bonds grandma gave to the kids in the 1990’s did very well. Not 15% but 6%-9%.

This will be an interesting show for the latter part of this year. I am just trying to bet on when Weimar Powell will reverse course once the market really tank back to 2018 level and inflation is slowing (not decrease) and employment market is slowing down…My guess is by 2 FOMC out, this tone will change.

If true price discovery were to be allowed, I think the market would tank back to pre-Trump tax cuts that was signed in December 2017. That’s when everything became so…fake.

It’s been fake quite a bit longer than since 2017. It’s been fake since at least the beginning of QE after the GFC and more likely it’s been fake since Greenspan dropped interest rates after the dot com bust, and wittingly or unwittingly (you decide) inflated the housing bubble.

Phoenix ikki…….Exactly…..this guy is nothing but a political schill……….his idea of patriotism is akin to Joe Stalin being a friend of the US.

JP says he will take “necessary actions” to control inflation……….HAHAHAHAHA!……..somebody save me……I’am going to laugh to death.

This is better than Saturday night live.

Does JP know that his credibility is less than zero. He has destroyed any credibility the fed has…….now he wants half point increases.

Jay…….you should have started with a full point a year ago…..asset sales last fall………but of course I’am not a crooked, political, egotistical moron that has no morals.

Fred you forgot EVIL!!

Are you related to Depth Charge by any chance?

We are all depth charge.

Fight Club!

“This is better than Saturday night live.”

a low bar

The US dollar is real bla-bla-bla show. Enjoy it.

Meantime real inflation is at high velocity against mid term elections.

And Powell have lost the war.

So democrats will reappoint him???

Don´t think so

Easy way out for JP he might have planned it ,ride off into the sunset

“You have to go down all the way into deep-junk, to CCC-rated bonds and below to beat inflation…”

Man-o-man, that’s tough. What to do, I don’t know.

Precious metals?? I’ve been going the silver route.

In a deflating economy everything goes down including PM check carts in depression

As the interest rate increases, tomorrows CPI will decrease. Inflation and Assets will come down very quickly, as interest rates approach ‘tomorrows’ inflation rate. I see 4.5% totally doing a ream job on either the stock/assets side, or the increasing debt to be paid back by the government.

I think this real estate market reflects a loss of confidence in the dollar. Lots of all cash deals. But you just know the fed will raise rates until it hurts. They can’t let the dollar lose reserve currency status so up we go!

After the dot-com crash many people took what they could recover from the market and put it into real estate (because everyone knows you can’t lose money in real estate). The fact that so many home purchases are being made with cash only leads me to believe this is happening again.

Yes, except that real estate is also in its own bubble and in some locations a mania.

Owning property 100% free and clear (except for taxes) is better than some maniacally priced financial asset that should be worth a huge discount to current value but is still destined to result in losing wealth.

Real estate is good. They won’t be printing up any more of it.

As Lex Luthor’s father told him (before he said “get out”):

“Son, stocks may rise and fall, utilities and transportation systems may collapse. People are no damn good, but they will always need land and they will pay through the nose to get it.”

And so they do.

Land values can, and have, dropped dramatically, even in prime locations. And while it’s hard to make more land (but possible with land fill, e.g. Foster City), yes, they can “make” a lot more housing – higher density, convert land from other uses (farm land, office parks, airports, race tracks, etc).

What’s wrong with a 30 yr fixed at 3%?

That’s what I have and pretty happy about it.

Not planning on selling or moving.

Even if land values drop, as long as you are sound in your financing for the land, it means the cash you can get for the land will itself be gaining relative value in hard times. At least then you are on a property ladder with an asset with some agreed value. And one you can live on, meanwhile. By sticking with this rationale, with discipline, my house payment is now $372 and almost paid off.

Whereas NFTs of bored apes will be selling for negative prices, IMO. You would already have to pay me a lot to take one of those things.

It’s nice to have a positive cash flow from a renter or two when house values start to depreciate to help stay above water on a mortgage. It helps when there is still some cash flow during bad times with deflation or inflation.

But during bad times, governments now have a precedent of allowing renters free room at others’ properties, and most won’t hesitate to do so. Good return (with current rents high), but I don’t like the risk.

“I think this real estate market reflects a loss of confidence in the dollar.”

Much of this inflation is NOT what the item is worth, it is an uncertainty as to what a DOLLAR IS WORTH.

Never has having a dollar been so punished. An intentionally so by the Fed. Criminal and the greatest theft in history, IMO.

“When central planners decide, they intentionally harm one group as they assist another.” F A Hayek

And we know what “they” decided in 2009, who was to get harmed, who was to be aided by a new disregard for Federal Reserve duties and mandates.

“The Fed is talking about lowering its weight. Quantitative Tightening “could come as soon as” in May, Powell confirmed today, adding that no decision has been made. But when it starts, it won’t move nearly fast enough.”

You have to laugh at the “could”…WTF are they waiting for? Serendipity’s blessing and for all planets to align in one straight line?

This FED…the market must feel like being a in narcissistic relationship most of the time, constantly gas lighted and plenty of promises to dangle in front to market gyrating up and down…

Damned if they do. Damned if they don’t. Heads or Tails. Pretty rare if coin lands on the edge.

Waiting for midterms. I’m convinced the Fed phools actually believe in their Magic Money Tree. And it sure has been a nice tree for them and their clients in Congress.

Agree. Mid-terms would have to loom large in their calculations.

Reverse course to keep asset bubbles from popping? If Powell thought he could keep printing and inflating assets without killing the dollar he would not have blinked or attempted a pause. The Stock market and any other market will be thrown under the bus because the US is an Empire of War and King Dollar Fiat Debt makes the War Machine possible. He is a bitch of the Empire. He will service the machine. War has never been abandoned by an Empire. Empires fall because they go broke from War. There is only one political party in America that really counts. The Party of Constant War.

Totally correct

The public, economy, and markets will be thrown under the bus to preserve the Empire which needs the USD as reserve currency to survive.

No vote can changer this either. It’s been the same policy for at least 30 years which as evidenced by current events, has no prospect for change.

The good news (if it is good) is that there are about 30 points on the DXY before the “printing” will need to stop but this still doesn’t mean the financial markets won’t crash first anyway.

We shall wee if the tides change if China enters the fray by supporting Russia. That might be the make or break moment for us to put up or shut up. The markets will likely see that as the black swan -mid 2022 version. Since we get new ones years now. I wonder if there is a subscription for Black Swan events

China is going to have to make a decision and maybe soon because US foreign policy has gone completely off the deep end just as fiscal and monetary policy have since 2008.

China isn’t going to let the Russian economy collapse. If the US (and Europe) is idiotic enough to impose similar or identical sanctions on them, it means an economic trade war worse than the 1930’s.

Blinked announced sanctions on China today, Tuesday 3/22. Blinken said sanctions were for human rights reasons and not Russian support retaliation. Chinese (Gov’t ) press say ” bull shit” . It is about Russia and the (Gov’t) press has hardened its support of Russia. US sanctions will be escalated on China because that is what The War Machine Party (Dems + Repubs) always agree on. Russia is firmly tied to China . Russia and China’s engagement is final and Blinken announced the marriage today 3/22/2022. Neo-Con’s must believe the Reserve King Dollar was given to them from God like God gave the 10 Commandments to Moses.

Things may be out of the Empire’s hands soon about the world’s reserve currency status. We know China and Russia have deals going on. Now with whoever is calling the shots for POTUS trying to get this Iran Nuke deal revived, the Saudi’s aren’t happy about that. So as oil starts to get traded in currencies out of USD, and other countries watching what we are doing as financial weapons, stay tuned. Not saying it will happen overnight, just saying, like others, reserve currency status days are numbered. And oh our military is only a fraction of what it once was. No fault of the men and women who serve….

‘And oh our military is only a fraction of what it once was.’

What? The budget is greater and greater for the military, every time congress convenes…

The process to lose the global reserve currency is not one or many deals. It is a progression that starts. This might be the start of that on a global level. Lots of politics and where we appear to fall short is a cohesive 5, 10, 50 year plan that I see other countries major outline and then execute upon. Our plan is all based on the four year presidential cycle

> And oh our military is only a fraction of what it once was.

Oh really? If Putin thought so, he would already be using bigger weapons and expanding the theater of conflict. He is being a poker player instead.

The USA may have exported much of its manufacturing base and hollowed the middle class, but we have the best weapons out there. We can do any amount of damage. And as needed, much more surgically than anybody else (a relative term). Add to that whatever remains of our financial network prowess, not yet fully deployed.

Hilariously wrong on the military point

August

“It’s been the same policy for at least 30 years ”

I’ll give you 13 years….

But in 2007, the Dow made its all time high of 14K….

Fed Funds were 4%. Imagine that. That was the “old Fed”.

And just recently Dow 35K and FF .05%. That is the “New Fed”…..in effect since 2009. IMO

I think Powell, over the weekend, studied the CPI vs. FFR chart from a few articles back and concluded that the FFR needs to be leading the CPI instead of lagging, as it is now.

Posh…

I think his secretary was out and he answered the phone himself …

It was historicus calling… :)

We can only hope and pray that’s true.

That’s the chart that should have been at the hearings.

The Fed uses the CPI, which is pure deception. The Fedsters claim CPI is 8%, and in reality, CPI is north of 15%.

Why is this dangerous? Imagine driving down a desert highway in a car whose fuel gauge says the tank is half full, but your tank is empty in reality. You start to make decisions about your future based on that fuel gauge. You decide to pass the gas station because you believe you have enough gas to get to the next gas station.

Millions of Americans are making future decisions based on what the Fed tells them about inflation. Remember when the Fedsters said inflation was transient? Remember when Nixon said taking the dollar off the gold standard was temporary 50 years ago? Remember when Bernanke said, QE was a one-off and was not monetizing debt? What are we on now QE7?

Now, these clowns are pretending to be hawkish with tweedle dee increments of .25 basis points, and Mr. Powell and his carnival barker Bostic today are saying they may have to raise rates .50 basis points multiple times. Guess what? That’s still far too low to address this inflation problem. They need to raise rates quickly and hit a number like Vulker (16-20%). But use your imagination to visualize what happens to the united states when rates go to 20% with $30 trillion in debt and a balance sheet that is almost $9 trillion. Imagine what the stock market will do. Imagine what pension funds will do as the Bond market crashes.

The bottom line is the Fed can’t squash inflation without popping the everything bubble, and the only thing they can do is pray for a miracle and shout while not carrying a stick (instead of speaking softly and carrying a big stick). They won’t fight inflation; they will surrender to it. They will try to take the easy way out and inflate their way out of debt, and these morons will invite the US to have a collision with hyperinflation. Think that’s crazy? Think again.

Remember when Nikola aired that commercial with that cool-looking truck blazing down the highway in a commercial? And then we found out that the truck didn’t even have an engine, and it was operating not even on fumes but strictly on gravity. It was a hoax, just like the US economy is a hoax.

Our leaders have misled us for years, and we believed them. As the system crumbles, it’s time to run for safety. The dollar is doomed, and when planning for the future, I suggest not trusting Jay Powell—not trusting Washington DC. Don’t trust your fuel gauge. Trust your common sense.

Start planning to hedge for inflation. Inflation will be your companion until the end of this decade. We’ll be introduced to a new term that our grandchildren will read about – Inflationary Depression – the perfect title for the current state of affairs. It’s an oxymoron, and our leaders are just morons.

Phil

Bingo!

“You decide to pass the gas station because you believe you have enough gas to get to the next gas station.”

Inflation is a race to the bottom. A leak in the gas tank.

I am still aghast that the Fed decided to promote inflation at what appears to be a meager rate of 2%, when their mandate is clearly STABLE PRICES. And not a word of objection.

2% rips 22% off the dollar in ten years, and to promote such and still pretend to be for “stable prices” is cognitive dissonance.

Now we have 8% inflation….and that STICKS. It does not go backwards. So if Powell gets his dream scenario of back to 2% annual, the subsequent years of 2% increase are tacked onto the recent 8% surge.

So in ten years where are we? 8+ (9×2)+= 26% …and, with compounding, that’s well over 30%. That’s the current goal of the Fed? (and that’s the dream scenario of a return to 2%, which is highly unlikely)

The “stable prices” Fed? Oh for a Congressman to make that point in a hearing….

Phil Hendrie

Agree inflation is north of 10% probably more like 13 to 15% and going higher. David Stockman who I used to follow a few years back pegged inflation at 13.8% before the Ukraine Crisis. I was in the grocery store today and noticed some items, juices, spices, imported items up 20%. This was probably due to the supply chain issues and rising gas prices for shipping. We are already in Stagflation and both ends are going in the wrong direction. The Fed will back off tightening as soon as the economy collapses. This may happen soon than you think.

My quick inspection of interest rates since the onset of the GFC — after mid 2011, mortgage rates only hit 4.66% of above twice. Briefly at the end of 2013 and for a sustained 8 months during the last 2/3 of 2018. I think the stagnation in real estate during 2018 and 2019 is considerably underreported nationally, the national median dropped 5% nominally and 10% adjusted for inflation during that period of time. Then consider that 2016 and 2017 were years of price increases still somewhat in the normal range, around 5% a year nominally, around 5% total adjusted for inflation.

Compare that to the runup that we’ve seen since around Q3 2020, 27% nominally in around 20 months vs 10% nominally over two years.

There are markets that have vastly exceeded that 27% figure. My house literally appreciated over 60% from February 2020 through August 2021. I couldn’t resist selling last summer and sit things out for a year, the madness couldn’t be sustained. At this point in time as far I can tell from comparable listings, I couldn’t sell my house for more now than I could have in August 2021.

If someone lives in place where the price increases have been less than 20% over the past couple years and you’re able to buy, I would just buy. However, if you live in place where mania took hold (numerous markets out West and in the South), I would sit this one out.

I may be jaded to the bearish side because I was a mediator during 2011-2012 in Nevada involved with state-mandated mediations (at the homeowners’ option). Basically, Nevada passed a law requiring lenders to give a mediation option to homeowners whenever a notice of default was filed. The goal of the mediation was a loan modification. I literally saw people who owed over $500k get appraisals from the lender showing a value of less than $200k. People use the general absence of crazy lending this time around as a crutch to why prices won’t decrease this time.

The real underlying problem, however, still exists — investors/speculators buying too much of the inventory. Last time it was the Option ARMs that enabled it, this time the money was too cheap in 2020 and 2021. Now, the money isn’t nearly as cheap and when the prices show their peak, investors will flood the market with inventory. When the buying of real estate becomes more similar to buying shares of stock, then the selling of real estate also becomes more similar to the stock market on the downside. We saw that in abundance in 2008-2012.

Trich, appreciate the insight, but why would investors flood the market when they can rent out to cover mortgage payments. Rents are up 20%+ so I’m sure that covers a mortgage taken with a 25% downpayment, as is required for investment properties

Good points, for if you’re lucky enough to be in that situation.

However, rent prices usually go down when house values go down, and your typical home owner isn’t prepared to rent out part of their house.

When the shtf everything goes down yeah!

You’re assuming there are enough renters who can afford to pay the higher rents for the additional supply.

Where are these people supposed to come up with the money?

A low proportion have gains from the asset mania but most people do not. It’s not like income increased enough since March 2020 to pay these higher rents and all other price increases.

The economy was mediocre in March 2020 (when the economy was also fake) and it’s been experiencing a crack-up boom of fake prosperity ever since the government and FRB turned on the monetary spigot.

You don’t partially shut down an economy like the US did and then magically come out on the other side better off than you were before.

If that really happened, let’s do it again, over and over forever and then we can all be really rich.

that’s what i get for not refreshing before posting. looks like you beat me to it, augustus!

Augustus ( and Jake),

As Augustus repeats often, living standards are going to go down…

And it’s going to start with a very painful reset of behavior and expectations, especially with the bottom 60% of income…

The people are going to have to decide what’s more important… a roof over your head or $25 for two people at the drive thru…

That’s where the money to pay higher rents will come from… the excessive consumption by people who, in a “normal” world, wouldn’t have access to that amount of discretionary consumption. They are going to be really, really pissed off when inflation and higher rates dry up the largess they have enjoyed and now feel entitled to…

The numbers don’t lie…

If you want to rent a place for $2000 a month, and your income is $50000 a year, fully 50% of your income is rent… you are going to have to reduce consumption ( lower your standard of living) or find a cheaper place ( also reducing your standard of living) to survive…

Either choice will result in a behavioral change or a necessary change of expectations…

because there isn’t the money in the wage economy to support those rents. remember, prices are set at the margins. from my anecdotal experience, asking rents went up, but average rents actually paid did not. meaning that the higher rents were generally for new leases, not for renewals on existing leases. most landlords were not eager to lose good paying tenants, especially after seeing how moratoriums and other shenanigans could have screwed them really badly.

given that the average american doesn’t have a pot to pee in, where is the average person going to get the money to pay 20-25% higher rents?

“People use the general absence of crazy lending this time around as a crutch to why prices won’t decrease this time.”

Pure rationalization

The idea that lending standards are strict is a farce. LTV of 80% to 95% on a bubble or mania priced asset is not strict.

The GFC also exposed the lie that someone with a high credit score is a “prime” credit risk. Many of these people are broke or near it. No actual prime credit risk is at risk of default or defaults at the first hint of economic duress, as in when they lose their employment.

The bigger consideration is that real estate is part of a larger mania where illiquidity or “risk off” in a supposedly totally unrelated segment can set off contagion risk noticeably tightening credit conditions and plunging asset prices.

That’s what happened during the GFC, as it wasn’t a mechanical result due to subprime lending. The bond mania was at risk of imploding during GFC and that’s what triggered the real estate meltdown. The bond mania is even bigger today, with more debt, lower interest rates, and the loosest credit conditions in the history of human civilization.

AF: how man is “many”? “The GFC also exposed the lie that someone with a high credit score is a “prime” credit risk. Many of these people are broke or near it.” Any facts to back this up? Ranting is one thing, making up “facts” is another.

Hi Unamused! Glad to be reading your comments, but I’m still wondering, with the chaos all around us, how can you still be un-amused?

Correction: “…how many is “many”?

Do you cite sources for every single claim you make?

Supposedly “prime” credit consumers are substantially if not mostly based upon the fake economy. That’s the point.

Without the fake economy, millions lose their jobs. Without the asset mania, the net worth of millions collapses.

If one or both happen, millions or tens of millions default on their debts.

That’s why they are not actually prime credits.

“how can you still be un-amused?”

Credit my tenacious resistance to despair.

“When the buying of real estate becomes more similar to buying shares of stock, ”

Real estate is perhaps the most illiquid of all markets….at times.

Nothing but buyers……then suddenly keys in the mailbox.

Imagine all those who bought bonds at 0.5% during the height of the pandemic. I wonder what the losses in bond portfolios will do going forward.

I bought Vanguard’s intermediate-term ETF (VFIUX) at around 11.54 (Aug 2021), and it’s now down to 10.77. My investment is down 6.4%, and it feels like it’s going to only get worse. The standard advice is that treasuries are considered a safe investment. Hmmm.

One article stated that, over time, the investment will pay off because new bonds are purchased with higher yields. I wonder if the higher yields compensate for the plummeting value of the investment. It’s quite nerve-racking!

Sorry to hear about your losses.

I am also wondering about the repo market–the bond losses should affect the repo market and possibly cause another repo crisis, no?

RoseN,

If you want to own bonds long term, NEVER buy bond funds (bond funds may be ok as short-term trading vehicles though). Buy the bonds outright, collect the coupon interest, and hold them to maturity, when you will get paid face value. You can buy Treasuries at Treasurydirect.gov

I HATE bond funds — for the reason you point out, and more so because they also add a huge risk that bonds themselves don’t have: run on the fund. If that happens, you’re cooked. You can lose 40% to 60%, even though most of the underlying bonds are just fine.

You probably don’t give recommendations, Wolf, but I wondered if anyone wanted to weigh in as to whether I should cut my losses and sell. (Maybe I should have listened to my sister and hired a financial advisor.)

RoseN,

I would never tell you what to do. And I’m sorry the investment didn’t work out for you. You can kind of figure where I stand, in terms of what I would do, from my comment above.

The problem is that you thought you bought a conservative instrument, when in fact they sold you something that is far riskier than the Treasuries themselves.

I like bonds (though not at these yields) and I own some Treasuries too, and we’ve been buying I-bonds every year directly.

But I hate bond funds for long-term invest-and-forget investments. I would never buy Treasuries in a bond fund if I want to keep them long term. Buy them direct. I-Bonds are great. You cannot move a lot of money into I-Bonds, but if you and your family members each buy them every year up to the $10k per-entity limit, it starts to pile up after a while. They pay a variable yield that is indexed to CPI and they have some real tax advantages. They currently pay over 7%. You can read more about I-bonds on Treasurydirect.gov

In my view, bond funds are short-term trading instruments to make money off movements in yield.

RoseN, if you do pick a financial advisor, be sure they’re a fiduciary. They’re mandated to work for YOUR best interests, rather than the interests of sellers of financial products.

Remember that your best investment is always in yourself. If Fun With Finance is what you want to do, you have to learn. And there is a lot to learn. It’s good for you.

RoseN,

First off, you’re not in an ETF, you’re in a bond fund. If the paper loss is “nerve-racking,” sell. I guarantee you that if the loss becomes larger, it’ll be even harder for you to pull the trigger. You asked for advice, there it is. You do not know what tomorrow may bring, but you do know, as of today, that you’re sitting on a 6.4% unrealized loss. And stay away from those damn inverse ETFs, they’re a rip off, unless you short them.

Agreed, Wolf. I do not understand why many bond funds even exist. I get it for lower grade corps, diversification purposes, to get access to munis, etc. The yield lag alone is reason for most to never own them.

RoseN,

What the good advice above that beats around the bush means…

You bought a piece of a FUND ( ETF, mutual, etc)…

The fund (of which you own a piece) owns the bond, not you…

You are at the mercy of the fund managers who decide in the interest of the fund, and not you individually…

The risk you have is the decisions of the fund managers AND other FUND owners who may or may not have your best interest at heart…

Other fund owners may chose to liquidate their positions in the fund for numerous reasons leaving your investment in the fund insolvent…

If you give your money to many financial advisors, they will do the lazy way and put you right back into funds or etfs… remember, your money is their income…

Not to tell you what to do…

The advice of treasury direct investment is a good place to start…

Commenting here is also a good way to learn…

Stodgy old VWLUX Vanguard Long Term Muni Bond Fund shows a YTD return of -5.3% and is down -8% over the last 9 months. Ouch….it tosses off only a 2.5%/year tax free return. Wait till bonds really start to puke….this fund could easily be down 20% or even 30%. Lots of owners will be trapped as many fail to open their quarterly statements. A better investment would be a +9.1% vehicle like a 24 ounce Hurricaine….the outside of the can accurately describes the contents as category 5.

Thanks for the input, everyone, and thank you, Wolf, for the suggestion to invest in I bonds. I’ve actually spent a fair amount of time studying financial issues, but you must admit, there’s a lot of conflicting information out there! Some so-called conservative books recommend purchasing bond funds. But I get it – if your fund can lose 20% or more in a short period, how can we call these funds a stabilizing presence. It seems like the brokerage houses should have some warning about these so-called “safe investments”.

RoseN wrote:

It seems like the brokerage houses should have some warning about these so-called “safe investments”.

To which I reply:

“Safe” for who, you or them?

RoseN, brokerages are also dealers, and they are not in business to benefit the retail investor. Keep that in mind.

RoseN

Also through TreasuryDirect you can acquire Series EE savings bonds. These are guaranteed to double @ 20 years regardless of their interest rate. If you’re looking for an instrument to hold over a 20 year period, this equates to a ~3.5% interest rate.

Similarly to the I-Bonds (formally “Series I Savings Bonds”) that Wolf mentioned, the EE’s mature at 30 years (although 20 years is the optimal time to hold them at current nominal offered rates), you do not pay any tax on interest until they are redeemed, are exempt from state income tax, and may be redeemed early (there’s some very short mandatory holding time) if need be.

In short both the I and EE savings bonds offered directly through the treasury portal are some of the safest, most secure, straightforward savings/investment products that you can own.

Max purchase of $10k/year per person though, so it takes a while to move your funds into them. There are some loopholes around this though. Although may of these are too complex to be worth your while, an easy one is that you may purchase an additional $5k in paper I-bonds by redirecting your tax return to this purpose by filling out IRS 8888 (the tax form) when you file your taxes.

A note on I-Bonds. Interest rates reset on May 1st, and Nov 1st. In a rising-rate environment, these reset dates may be important.

Best of luck & I agree that Bond funds (and most ETFs generally) are terrible.

It was a pain in the ass to cash out my treasury, they required a stamp from my bank. Had to spend the time to go into the bank and talk to a rep.

Zark Muckerberg,

Mine is set up with a two-way ACH to my bank. When a bond matures, a couple of days later, the cash shows up in my bank account. If I want to buy another bond, I just buy it, and the Treasury draws money from my bank account via ACH to fund the purchase. It’s all done automatically. I have no idea what problems you ran into. Seems you didn’t set up the ACH.

In My Humble Opinion, if you believe there is a better place to obtain financial or investment advice, you are wrong.

Yeah it was set up w/ ACH, one year maturity. It was over a decade ago so maybe they improve their process or I was just unlucky but giving me a hard time over a measly $100 was enough for me to not trust them

I own a short term muni bond fund DMBAX. Its where I park money for safekeeping. So far so good. They do the research for me and buy only the short term stuff. Matures in less than 2 to 3 years. No interest rate risk, no credit default risk, and no taxes.

Swamp Creature,

Funds loaded up mostly with short-term liquid securities should be relatively stable. But they don’t yield much.

But with 2-year yields at 2%, maybe it’s get better over the next few months as those securities start to show up in your fund.

I think you’re able to see their top 10 positions. Make sure there are no maturities over 2-3 years among them. If you see a bunch of stuff that matures in 10 years, it’s a problem.

And you’re still not protected from a run on the fund. That’s a risk that is always there. It’s inherent in bond funds.

With bond funds, I’ve owned them over the years and have done very well except for junk bond funds. After the GFC and the meltdown of funds across the board I was out of them at the time, fortunately. Now I have become more cautious. With the one bond fund that I own, DMBAX (Short term muni bond fund), I check the 3 month statements carefully. The red flags to look for are falling total assets (increased redemptions), huge turnover in their portfolio, falling share price, negative yield, increased ave maturity, poor performance relative to competing funds. Of all of these my fund has a couple of red flags but it hasn’t gotten over the deep end yet. One more red flag though and I’m out of dodge.

There’s one other risk enhancer on bond funds: when rates are dropping and bond prices are rising, money pours into bond funds. They don’t generally turn it away (some actually do close to new money, but relatively unusual). The manager is forced to establish new positions as prices rise.

Conversely, when yields rise and bond prices drop, funds leave the manager — just as you are considering, RoseN. The fund is forced to liquidate at the wrong time, as prices decline.

From a strategic standpoint, the fund manager is forced to “buy high” and “sell low.”

Not the road to investment success….

Rose,

I wouldn’t worry about the Vanguard bond fund you bought. It’s big and they hold treasuries so risk of it getting shuttered is as close to zero as you can get.

If you had bought a single 5 year Treasury it would have been down about the same amount and you would have to pay a broker to sell it if you needed money.

Don’t do a panic sell. Do research about the fund and what your purpose is. If it is for savings in the 5 – 10 year range with the option to take out some of the money from time to time it might be a good choice.

Old School,

During the Financial Crisis, lots of bond funds got wiped out and shuttered, including the biggest bond-fund family at Schwab, where people who didn’t get out in time lost something like 60% of their principal. You can Google the class-action lawsuits that ensued.

If you buy Treasuries at issuance from the US Treasury and hold it to maturity, you get paid face value, and in between, you collect the interest. And there are no fees involved. That’s “invest and forget.” You will never lose money. But you might not make a lot either, depending on the yields at the time you bought.

Bond funds make up subject to speculation. And if the fund contains bonds with longer maturities, there is a superb chance you will lose money when rates go up, as they’re doing now, even if there is no run on the fund. That’s how bond mutual funds are structured. Bond ETFs trade in the stock market, and they’re dependent on trading activity. But if they contain bonds with longer maturities, you will also lose money when rates go up, as they’re doing now.

OOOps. I was in the Schwab bond funds during the period just before the GFC. Got out just in time. The finds were used to pay my kids college tuition. I didn’t lose a dime, in fact made out pretty well. One of the funds had some issues with the SEC for illegal trading and the fund manager went to prison. It was a short term bond fund. Schwab sucks. It took almost an act of Congree to close out my accounts with them.

John

The carnage in the bond market maybe the straw….the cinder block that breaks the camel’s back.

Who or what and to what extent will be much speculation.

That yield curve really does look like a hopping kangaroo.

It must be an omen of some sort. I googled “dream jumping kangaroo money” and the first site that popped up (“Guide to Dreams”) said a jumping kangaroo “indicates that you will pay your debts in the short term.”

There you have it.

HQ

The Fed skews all they touch……and the yield curve is exhibit A

It wasnt but months ago that the talking heads on cable pointed to the yield curve and said “See, people are not worried about inflation.”

and Powell was saying the same thing.

using the fed manipulated yield curve as proof that people are not worried about inflation is like the kid who kills his parents and begs for mercy because he’s an orphan.

I’m inspired.

There’s a term called Kangaroo Court that implies a farce of a judicial proceeding, where the verdict is already in, and everything is being done for show. Excellent song by Capital Cities on the subject.

We’re in a Kangaroo Economy.

Apparently you’ve never been in moderation jail…:)

““In particular, if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so,” he said.”

This guy is the living version of “The Boy Who Cried Wolf.” Nobody believes his tired old BS anymore.

“If we conclude that it is appropriate.”

You mean it’s not appropriate yet when the rigged to be low CPI numbers are running 8% over the Fed Funds Rate? What do we need, 10%? What’s the magic number, you fraudster? Anybody ask him that? This guy speaks in tongues and nobody calls him out on hit. He is the consummate bullsh!tter. Don’t listen to what they say, watch what they do. He’s stalling. WHY ARE YOU STALLING, YOU CORRUPT B@STARD?

The bond market is starting to believe him, no?

It will be a classic battle again between who is right: the bond market or the stock market. Right now the stock market is betting on only one more hike and then QE to the moon. They apparently think we will deal with Russia like Desert Storm.

John…

I think the stock market resilience to the events of the day has much to do with scared money from overseas coming into these markets.

In your own words, maestro Wolf:

“The Fed is talking about lowering its weight. Quantitative Tightening “could come as soon as” in May, Powell confirmed today, adding that no decision has been made. But when it starts, it won’t move nearly fast enough.”

“But they’re still trying to get that “soft-ish landing.” And that will cause them to dilly-dally around too long, and to let inflation get worse, before they really crack down, and that might then cause some real damage.”

It seems you agree with me, he’s STALLING.

The economy is overheated, and inflation is payback for all that gasoline thrown on it. The gasoline is burning out, and the cooling is beginning…

Hopefully we can cool off slowly.

“Hopefully we can cool off slowly.”

Good luck with that. There is no “soft landing” from the greatest asset, credit and debt mania in the history of human civilization.

Believing it is the equivalent of believing in something for nothing. The country has gorged on credit for decades living beyond its means and for this to be true, supposedly American living standards can and will increase in perpetuity.

Look at the last three recessions: post dot.com bust, GFC, and the brief one in 2020. The dot.com bust was the last stop on the train for the country to take its medicine to restore stability. Without fiscal and monetary stimulus, the recession would have been much worse because it was still the aftermath of a mania.

But now, we’re talking about a 5X and 14X increase in the national debt and FRB’s balance sheet since 2000.

The result has been a fake economy since 2008 and over two decades of the most overpriced manic asset markets in history.

Income and wealth inequality has been identified as a root cause which it really isn’t, not the way most probably believe.

If distribution of both had more closely resembled the 80’s and 90’s, there would have been noticeably higher inflation long before 2021 because much of this income and “wealth” would have been spent instead of used to buy financial assets with no incremental production to absorb it.

Take all the people in the United States who bought their house 5 or more years ago and refinanced during Covid interest rates at under 3% and are now paying 50% or less the monthly payment as what the same house would cost today. They’re now stuck in their house forever because it’s either same price for half the house or they’re priced out altogether – there is no downsizing option.

Then add anyone who made Covid lifestyle adjustments (one parent stopping work, starting their own business, moving to a more rural area, early retirement) who bought during the height of the pandemic. They now have a sub 3% interest too, likely less income, less savings from a huge down payment and leaving means buying back into the old market at 50% higher interest rates and higher prices than when they left a year or two ago.

Then squeeze these two groups of people whose ships are burned and have no easy options to downsize by double digit inflation of goods – with huge increases in the most inelastic items like gas and groceries.

…should end well.

There are a lot of people who won’t sell, but others will sell. I analyzed sales in some markets that I follow, and about the half of sales over the last few months were people who bought their homes than 5 years ago. Many of them bought in the last two years and want to capture a quick 30%-50% gain on the coasts. These are the flippers and other opportunistic types of people that will bring the market down 20% or so very quickly, as all other sellers stand by and watch.

I don’t just want massive rate hikes and the FED to empty its balance sheet, I want the country’s money back from Powell. I don’t want he and his buddies to keep that stolen loot. It’s time for clawbacks. I want all of those central bank fraudsters in prison. Using a health crisis and public emergency to steal from the people, especially the future of the young, is unacceptable. We don’t just want and need answers, we want consequences.