The most reckless Fed ever is still just watching – and fueling – the consequences of 23 months of policy errors as the Inflation Monster gets bigger and bigger.

By Wolf Richter for WOLF STREET.

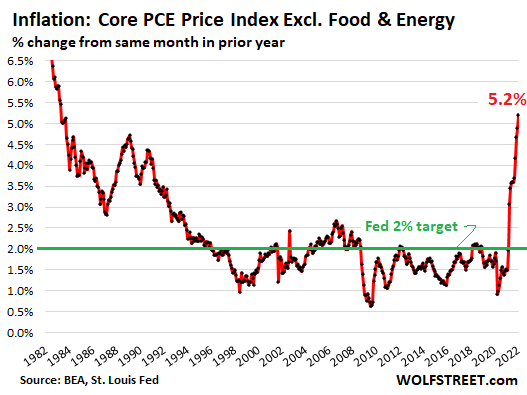

The Fed’s official yardstick for inflation, the “core PCE” price index, which excludes food and energy and is the lowest lowball inflation measure the US government produces and which understates actual inflation more than any other inflation measure, spiked by another 0.5% in January from December, and by 5.2% year-over-year, the worst inflation spike since April 1983, according to the Bureau of Economic Analysis today.

The Fed’s official and inexplicable inflation target is 2%, as measured by this lowest lowball inflation measure. And now even this lowball measure is 2.6 times the Fed’s target:

But back in 1982 and 1983, inflation was on the way down; now inflation is spiking to high heaven. Back in 1982 and 1983, the Fed’s policy rates were over 10%; now they’re near 0%.

Several Fed governors have put a 50-basis-point rate hike on the table for the March meeting. Yesterday it was Federal Reserve Board Governor Christopher Waller who said that “a strong case can be made for a 50-basis-point hike in March” if we get hot readings for today’s core PCE index, and the jobs report and CPI in early March. The first of the three conditions has now been met with panache.

“In this state of the world, front-loading a 50-point hike would help convey the Committee’s determination to address high inflation, about which there should be no question,” he said in his speech.

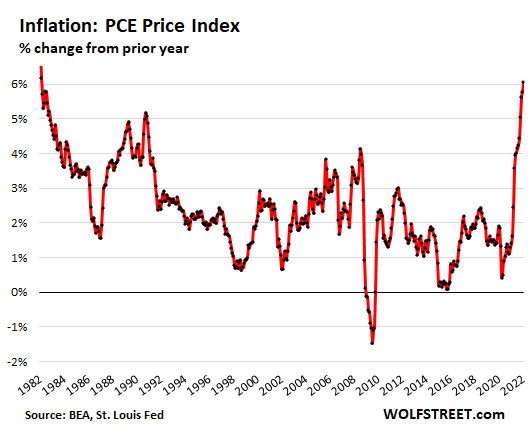

The overall PCE price index, which includes food and energy, spiked by 0.6% in January from December, and by 6.1% year-over-year, the worst reading since February 1982.

Here is Fed chair Jerome Powell’s reaction after he saw today’s data, documenting the consequences of his reckless monetary policies, as imagined by cartoonist Marco Ricolli for WOLF STREET:

This not-so-mind-boggling inflation monster was created by $4.8 trillion in money-printing in 23 months — I mean, duh! — which continues though at a slower pace and is slated to end in early March, and by the most insane interest-rate repression ever in face of spiking inflation, which is slated to be softened somewhat – too little, too late – on March 16 with the liftoff rate hike.

The Fed, the most reckless Fed ever, has brushed off this surging inflation for over a year, and has continued to print money and repress short-term interest rates to zero for over a year despite this surging inflation, with the goal to pump up asset prices further to make the already wealthy that hold these assets even wealthier. And now people who are working for a living are paying the price as the purchasing power of their labor plunges.

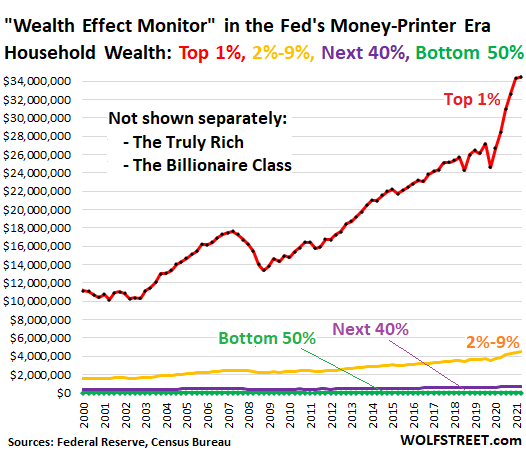

In the process, the Fed has created the biggest wealth disparity ever in the shortest amount of time ever, based on the Fed’s own wealth distribution data that I’m now tracking with my “Wealth Effect Monitor” & “Wealth Disparity Monitor” for the Fed’s Money-Printer Economy:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

SHOULD the FED raise rates a 1/2 point in March?…yes. SHOULD the FED have already raised rates a long time ago?…yes. WILL the FED raise rates by a 1/2 point in March?…No. Ukraine has given them the convenient black swan excuse they needed to delay/reduce any and all rate hikes, QT, etc. If it wasn’t Ukraine, it would have been something else. Sadly, there will be no meaningful or serious fight against inflation by the FED. Pathetic.

Increasingly, nothing the FED can do (or fail to do) is going to propel paper asset appreciation higher than real asset appreciation. That gig is up.

The FED may well choose to drag its feet on interest rate increases so as to avoid giving the game away that interest rate increases aren’t going to solve the supply chain mess – and that nothing can.

Look, there simply are not enough Indians, or new immigrants, or minorities of color left anymore to absorb all the austerity that is now needed, so one hell of a lot of you WASPs are just going to have to take up all the slack. Deal with it.

Unregulated unilateral class warfare is a bitch, ain’t it?

Gilded Age 2.

NB

Woohoo !

Somebody gets it.

The FED will drag its feet to keep the real estate market from cratering. Rates have risen 1% in three months with only 2/3 of the MBS purchases removed from QE. With the removal of the final 1/3 and a 50 basis point hike, 30Y mortgage rates could be approaching 4.5% by early April. At 4.5% the REFI market will nearly dry up. At 5%, the housing market will start at least a 5-10% correction.

What I would really want a full accounting of is the PPP money spent. With a reported 75% staying in the small business owner’s hands, that was an ENORMOUS amount of money that went right into the hands of people who, oftentimes, didn’t need it and turned around and paid “whatever” for used & new cars.

My point is that Congress needs to get to the bottom of this. In the future, they need to spend more time making sure their emergency funding measures work properly and without so much waste and fraud. Probably not going to happen though.

I agree with you that the Fed now has the justification they need to slow down tightening or not hike at all. But doesn’t the Ukraine situation cut the other way as well — i.e., won’t this tension put additional upward pressure on inflation?

Yep… gives an excuse, but raises inflation even more

My sentiments exactly 80s_Guy.

The funny question at hand, though, is we know we have a politically inclined Federal Reserve. Whose interest will they serve?

If we assume Dems want inflation down, then the Fed would have already hiked some time ago. They didn’t have to wait until March 16; they could have held an emergency meeting and immediately started hiking as soon as they wanted.

But why wait? There is a reason….

Not sure I agree. Even if they are politically motivated to fight inflation for real (and I’m far from certain on this), they still need to slow walk it to avoid market panic.

I fully agree peanut.

Nobody can tell me they got it completely wrong with transitory inflation!!!

They waited till it was to late deliberately

The stock market is NOT the economy. The economy can and should be able to handle at least 2% fed funds, just as it did in 2018.

The REVERSING of bad policies must take place to REVERSE to ill effects of those bad policies.

To continue with FAKE rates at RECORD LOWS below the inflation rate is MADDNESS. The harm to the citizens and businesses of this nation are immeasureable….which is perhaps why there is little mention in the headlines.

The CAUSE can not logically also be the SOLUTION. In fact, the SOLUTION is nearly always 180 degrees from the CAUSE.

Rates MUST GO UP. NOW.

The economy may be able to handle 2% FFR but it can’t handle higher rates, any noticeable QT, and removal of the additional fiscal support (in response to COVID) without a (noticeable) recession at minimum.

The economy is fake, smoke and mirrors. The “greatest economy ever” before COVID was already fake and weak, also dependent upon more deficit spending.

Closing the economy down, losing millions of jobs and then offsetting it with “printing” and mountains of more debt didn’t miraculously make it more robust than it was in February 2020.

The CAUSE can not logically also be the SOLUTION. In fact, the SOLUTION is nearly always 180 degrees from the CAUSE.

Rates MUST GO UP. NOW.

Historicus the hysterical!! Calm down fella.

The crisis in Ukraine gives the Fed a very good reason to pause it’s rate hiking cycle and assess the impact of the war on the economy – and that includes the many sanctions that are flying about.

Correct

What? And get the same result they got in 2000 the last time they did a 50 basis point hike? I really doubt that no one at the Fed remembers what happened after that titanic mistake.

They got burned by that once. I really hope they aren’t stupid enough to fall for that again.

What was the mistake in purging all that Dot.com stuff. It belongs in the trashcan.

Bigger and bigger government with more and more spending leads to just that logical conclusion.

Those in the front of the cheap and easy money line get uber wealthy.

Those is in the back get $750,000 crack shacks, $40,000 Hondas and $70,000 per year communications degrees.

“And now people who are working for a living are paying the price as the purchasing power of their labor plunges.

In the process, the Fed has created the biggest wealth disparity ever in the shortest amount of time ever…”

After combining info from Wolf with that from George Gammon, here is the biggest possibility:

1. Fed will carry out minute rate hikes very slowly (when compared to inflation rate) to delay the inevitable : High / Hyper Inflation with slow onset of poverty as Dollar loses value to real goods and services and US productivity decreases as many jobs will no longer provide sufficient earnings for a decent lifestyle.

2. After a few months, when markets throw tantrum, Fed will reverse course: The super-rich will get richer. The 1% will “think” that they are getting richer in dollars but will merely retain state in net and the other 99% will get poorer.

There will be nothing approaching hyperinflation as long as the 10YR UST is anywhere near 2%.

There isn’t a single instance where any economy which could borrow at anywhere near current US sovereign rates ever experienced hyperinflation.

That’s only because US is borrowing in its own currency that it can print, otherwise interest rates would exceed 20% already. As US runs a big deficits and exports become in-competitive, it will experience high to hyper inflation for goods it now longer produces but does consume. Even today inflation when accounted for house prices crosses 15%.

Mission accomplished: stealth negative real interest rates for ever! Thanks, Jpow!

It wasn’t by accident. The FED, after all, are all bankers. They won’t stop until you are penniless, homeless, and ready to fight.

I wish there are not more and more people mad and desperate enough that they start fighting. And robbing. And giving up being productive. The “forth turning” keeps getting closer and loser to reality.

Visit the anti-work reddit :)

We need a modern day Robin Hood!

That’s Bernie Sanders!

>Anthony A.: Re Robin Hood

We have a modern day Robin Hood but he is the reverse of the original. Now he is the government, robbing the poor and giving to the rich.

Fourth Turning is yet another unproven theory. Nowhere near enough cycles to substantiate it.

It intuitively makes sense. I can also come up with scenarios which are presumably a lot different from what any of these people expect.

Anthony A.,

Where I grew up it was Hood-a-Robbing’ :)

“ Those is in the back get $750,000 crack shacks, $40,000 Hondas and $70,000 per year communications degrees.”

2b,

Do you feel sorry for them?

I don’t… eff em…

You don’t have to buy… won’t be long and these same people will be screaming for taxpayer bailouts because they don’t want to pay for their mistakes…

When you get your clock cleaned, you will learn how to make better decisions… or not…

Success rides a turtle, failure rides a rocket…

Those items 2bannana brought up would typically represent the BARE minimum. And those costs are pretty spot on for these days.

You need shelter, transportation in most areas, and a degree (or technical cert which ain’t free either)

I mean I’d love to hear what short sighted solution you have beyond “eff em.”

Cem,

I saw that!

The only thing I can say about short sighted solutions… is not get in one…

They usually don’t end well..

First, individually, you have to realize the world doesn’t really care about you or how you feel…everybody can’t be and won’t be a winner… buying a lottery ticket, for example… a lot of people without skills, an aptitude and/or an intelligence to handle more responsibility will always be at the bottom…

If you do get to the point where you may have won a little, you never put the basic four, food clothing, transportation and shelter, at risk… period…

College is a waste of time and money for most people… part time job related, directed college can be beneficial for some… the trades are there if you aren’t lazy…

Understand, everybody, literally, everybody wants your money… it’s their income… only you can decide to give it to them…

Check out the ads on the bus stop bench and what do you see… you don’t see 3/4 million houses for sale… you see pay day loans, injury lawyers, pawn shops, etc… what do these people know that you don’t…

Everything also has a relative cost structure… if you can afford to play the game, more power to you go for it… but if you lose your ass, stand up and take it like a man in bankruptcy court…

By the same token, if you bought that $75000 pickup and want to trade it in on a fuel efficient Camry, that’s going to cost $55000 because the world changed and you’re $30000 upside down… oh wait, I know… you’re going to blame the Fed….

Sorry, didn’t mean to go so long, but hopefully you get the gist…

So yeah, eff em…

$750K for housing and $40K for a car is the bare minimum?

They can move if living in California.

In my limited sample, I have personally never met a person experiencing financial difficulty who didn’t substantially (if not entirely) arrive in their current condition through their own bad choices. Yes, they were of limited means or “middle class” but substantially wasted whatever resources they had.

I also know that in the public sphere, no one except the taxpayer is accountable for anything: not the voters, the recipients of social programs, government bureaucrats administering the programs, and certainly not the politicians.

Add it all up and it’s a society designed for guaranteed eventual failure.

Historically most people couldn’t afford their own single-family home, nor brand-new cars. It’d be nice to move the goalposts on what is “bare minimum”, but until people in this country produce more, they are not entitled to consume more.

Perhaps the greatest injustice in this country isn’t that some people don’t have their own housing, it’s that those who produce get so little in return for their labor.

Compensation for labor, as a share of the total economy, is near all-time lows while corporate profits as a share of GDP are near all-time highs.

Within labor, government employment is too high and production is too low.

As a result, between taxes (to pay the government workers) and the bloated corporate “profit margins” (to pay rich owners), wages for the actual productive workers don’t go very far!

Yeah, they can just live on the street. And then morons like you will start complaining about all of the homeless and increased crime Ordinary people don’t get bailed out. That’s Wall Street. What world are you living in?

The “homeless” (what were called “Bums” in my youth) are not innocent.

It is not a “home” they lack.

phoenix,

Where I come from, if you got the mouth, put your money behind…

Please post a video of you giving $10000 cash to any group of homeless… then I’ll listen better to what you have to say…

And don’t try to take it back when you turn the camera off :)

You won’t and I don’t blame you…

It’s ok to be naive, Don Quixote, but moron? I read your posts and generally agree so I know you’re better than that…

I will never give cash to homeless. That is even worse than fiscal stimulus of 2020.

There are other (far more effective) ways to help others in need.

Quite the army of strawmen you’ve built up in your reply btw.

I agree with you COWG … only I spent the decade after 2008 telling myself that and what I really underestimated was the government’s willingness to do the wrong thing.

They will all get bailed out. All we do is bail out people for doing what they shouldn’t have. It seems like we are constantly just trying to manage things so there are no consequences anymore. We need to get back the capitalist spirit which inextricably has a part in it that says if you make the wrong bet or do the wrong thing … you lose.

If we keep saving everyone from their stupidity and recklessness eventually the whole thing will come down … and it does seem like we have gotten there in a way now with interest rates and inflation but don’t underestimate how long the government can step in and do absurd things to stop those people from feeling the pain of their actions.

I wish there was but I don’t think there will ever be a “see, I made the right decisions and now have all the money” moment for all of us responsible types. We will continue to lose until we all finally lose.

You are describing moral hazard.

Many are aware of it in the financial realm and a minority apply it to the wealthy but virtually no one thinks of it in the context of the general population.

The majority of US society has concluded that everyone has an effective birthright to minimum living standards at someone else’s or no one’s expense. The majority posting on this site possibly believe it too.

That’s where the country is collectively at now, no one is accountable for virtually anything.

Add it all up and it equals one outcome, the majority of Americans are destined to become poorer or a lot poorer.

And it’s not decades and decades in the future either, as this country has been living beyond its collective means at an accelerating pace for two decades already as the social decay also accelerates.

You betcha…

I wonder if the social media real estate guru in Ukraine still feels the same as he did a month ago…

After Crimea in 2014, part of my planning for the future would have been a way to get the hell off Russia’s front porch…

For AF:

Don’t think it is anywhere near a ”majority” on Wolf’s Wonder, OR USA population in general, as in your sentence: ”The majority of US society has concluded that everyone has an effective birthright to minimum living standards at someone else’s or no one’s expense.”

YET!

That USA society is moving in that direction NOW is certainly my opinion too,,, and it also certainly seems to me that that movement is directly correlated with the intentional ”dumbing down” of the USA population through massive propaganda AKA advertising, as well as the substitution of ”social promotion” for earned advancement through merit as was the case when it was actually necessary to achieve at least minimum standards in the public education system.

ViintageNet,

Ask the population specifics and I suspect it’s exactly what they believe.

Like “free” or affordable health care, a dignified retirement (whatever that means), and minimum quality housing.

I attribute this belief to the fallacy that voting for “free” benefits at someone else’s expense is “helping” and “compassionate”. I call it what it actually theft.

If most people aren’t in favor of it, they certainly do not vote against it.

I don’t have factual proof of this opinion, but it sure seems like it.

If someone actually wants to help, make the sacrifice or experience the inconvenience yourself.

Have you seen the movie, Dr. Zhivago?

JeffD,

Not in a while…

If you’ll give me your thoughts on the relevance or the meaning you got from it , l’ll be happy to watch it again and gain a different perspective…

Others might as well…

People are most likely to overthrow the current regime when they are unhappy, whether they are the contributing factor to the decline or not. Those with the attitude “it’s their own fault” are the first in line to have their lives dismantled.

2banana

As a matter of clarity, please explain how the multi-millionaire and billionaire class gets the QE $$ vs the restofus. It is an honest question because I don’t really understand it that well. Though it is low interest debt, it is still debt, and debt does not increase your net worth.

because qe basically means that the fed will print money and give it to you in exchange for your treasury bills. it’s large institutional investors and banks that have those treasury bills, so they get the cash. since prices of assets haven’t yet adjusted to the fact that there is a lot more cash now in the economy, they get to use that printed cash to buy assets at the lower prices. in other words, they buy assets today for yesterday’s prices.

Jake W

Thanks for that. Still puzzled though. Are you saying Fidelity, Schwab, Wells Fargo etc have massive amounts of intetest-bearing T-bills and trade those for cash ?

Why trade an interest-bearing asset for non-interest bearing asset (cash) ?

you’re welcome.

and yes, those banks have huge amounts of t-bills. they trade them for cash because they are effectively selling them for way above what they could sell them on the free market.

Guess who was going to get all those high paying “Green Jobs” that Build Back Better was supposed to generate? You know that the politicians would have their asshole kids inserted as administrators.

I think that we’ve already passed the Rubicon of too many people deriving their incomes both directly and indirectly from government.

Do you have any doubts that they would target each and every person to confiscation of some kind to ensure that their own pensions and health insurance has no interruptions?

I believe the simple fact that the rich should take care of the rich why should they raise the rate when they’re getting rich working people will become working

Mohammad El Erian, former PIMCO CEO, thinks there’s as much as a 30% chance the Federal Reserve will eventually give up on getting inflation back down to 2% PCE. He predicts they’ll either end up moving the goalpost, such as raising the inflation target, or they’ll just make excuses about supply chain disruptions not being solvable through rate increases, or when GDP growth & employment inevitably begin to slow after some amount of tightening, they’ll go back to touting the importance of their “full employment” mandate.

I’m inclined to agree with him. Right now, with “40-YEAR RECORD HIGH INFLATION” dominating the headlines – not to mention FOMC governor nominations/hearings in Congress – it’s politically impossible for them not to act. But I can well imagine a scenario in which inflation decelerates to a still-elevated but no longer boiling 4% CPI / 3.5% PCE, and they decide it’s politically easier (not to mention better for their personal portfolios & post-FOMC careers) to simply raise the target & make excuses instead of crashing the markets and/or causing a recession.

That is a very risky strategy.

The thing with inflation is that it feeds on itself once it becomes unanchored. And to have it anchored, people need to BELIEVE that government/ central banks will do whatever it takes to curtail it. This is basically what Volcker did in the 1980’s.

Right now, inflation is the top worry of many people. It has already gone way to far. So now people need to see inflation coming down very quickly. If they just see the Fed doing some half ass attempt instead of whatever it takes, it could further run out of control. Eventually you’ll then end up having to do a Volcker style rate rise (and crash markets anyway).

Exactly. The FED is not serious at all about fighting inflation with any real meaningful rate hikes or QT. I would love to be proven wrong, but the FED always caves to politics, wall street, and the real estate industry. I’ll believe they’re serious when I actually seem them DO something, not just TALK about doing something.

If market wise up and stop buying the dip and let it tank another 10%, I would raise that 30% to 60% they reverse course or change the goal posts.

From FED’s pov, general population might be hurt by inflation but so far they have been conditioned to suck it up and deal with it without massive social unrest. Side benefit as well, a lot of people with stake in the game seeing their taco tuesday crapshack now worth double or triple what they paid, wealth effect is keeping things going, so no need to create any real urgency to tame inflation other than getting heat from current administration but even at that, the pressure they are getting is probably tame by comparison to the previous administration.

Not to mention, they officially retired the word “transitory” but probably still very much alive in their mindset, I guess anything is transitory if you stretch out the period long enough. Inflation rage on for a year or two, it would be transitory in the grand scheme of 10 or 20 years.

The Fed says they…they…may have to live with high inflation. Such a sacrifice.

A cushy government job, insane pensions and insider trading

What about working Americans who can’t afford food or an apartment now…let alone 10% inflation for a few years?

Yeah…that’s not gonna work for long.

Don’t forget all the gov jobs and pensions indexed to inflation.

10%? Who cares?

Jackson Y,

El Erian has said a lot of goofball things over time. He’s always in the media and constantly talks, no matter what.

That said, this inflation isn’t going away on its own. It will go higher then go lower then higher again, remaining at high levels overall, and the Fed will raise interest rates too gradually to bring inflation down, so we’ll have higher inflation and higher interest rates and QT for longer.

The exception will be a huge and long-lasting drop in asset prices across the board which will bring consumer price inflation down more effectively than rate hikes. The Fed can do that with sufficient amounts of QT. And it might be going that route.

Wolf,

The cooling of inflation via interest rate increases is based on the belief that if you can reduce available financing – you can achieve the required level of demand destruction required to bring inflation down.

Unforutnately, I think we’ve moved from a backdrop in which EIP and increased UI benefits – coupled with a shift in consumption away from services to finished goods driven by the pandemic – to one in which supply chain disruptions are meeting the early statges of commodity price inflation with a wage-price prial mixed in for good measure.

I really do doubt the efficacy of interest rate increases in that environment.

I still do support interest rates increases and if it were up to me, I would have begun tapering last February and would have begun raising interest rates by August.

Hey Wolf, how’s that article on how prudent investors over the past decade being made whole cumming?

So you are presuming that money printing will be going at high levels for some time? At the level of debt we’re experiencing, aren’t you worried about a currency collapse?

El Erian…. in the Ivory Tower of Academia, Nuff said.

Wasn’t he at one point was in the running to replace Yellen? Nuff said

Ray Dalio take from Changing World Order Ch. 11 on the three policies being used.

#1 – Interest rate driven (First used)

#2 – Printing money and buying financial assets like bonds (QE)

#3 – Coordination between fiscal policy and monetary policy. Central govt does a lot of debt financed spending and CB buy debt (last to use when first two fails)

If you can’t hit the target, move it!

b

Even if the Fed acts to raise rates by .25%, it doesn’t mean squat in terms of bringing down inflation. It’s more of the same. Especially with gas prices now approaching $5/gallon across the country, and heading for $6 and $7/gallon in some places.

We are still at low $3/gal here in the Great State of Texas. California is over $6 in some areas.

Oil is used in so many products that the higher cost of gasoline is the least of your worries.

To say nothing of fertilizer, wheat, aluminum, nickel, etc. – all the goodies that Putin can take off the market

I know that as I spent 35+ years in oil & gas. Gasoline is the most visible expense for the masses. Increases in stuff made out of plastics and synthetics are not as obvious.

For instance, auto/truck tires are going up in price as they are made from synthetic rubber (essentially a base latex colored with carbon black). The belts are steel wire coated with brass. You only see that price increases once in a great while when your car needs tires.

The 2015 Fed held rates too low too long, we got the fracking boom and oil prices collapsed. The fracking industry has indicated they won’t go back to debt induced profits. Never say never. Just too many reasons not to raise interest rates here. Rates are currently high enough to attract foreign investment. America needs to grow its business to take care of domestic needs. $100 oil is going to push us into recession.

When consumers are forced to hunker down as they now are in increasing numbers, and spreading upward in the economic classes, the recession drivers are in place now. How many have abandoned vacation plans, or a new car purchase, a home renovation because the costs have cut their budget priorities down to food, fuel and shelter.

Our household has done just that, reeling in spending and replacing more costly goods/services with cheaper option. Or eliminating them when possible.

And we’re fairly well off, can’t imagine the effect this raging inflation is having on lower earning households.

In the supermarket where I usually get my groceries, there is a specific corner where every day around 15:00, they put all stuff that will go past the “use before” date on that day, for a significantly reduced price. Before, there was never much interest for it. But in the past months, there are always loads of people checking what is there. That includes myself.

Have 3 major grocery chains ,got all three apps .shop all there sales oin ads and digital, doing well got canned Vegas for 29 cents,but limit was 12 be prudent

Back when I was a kid in the 1960’s, I remember going to the “day old bread” store with Mom to buy bread.

Walmart has the same now and it is well shopped, and by me ever time I go to the store.

We used to have 3 dogs, now we have only 1.

You ate them!?!

I wish your statement would appear as a headline on the front page of NYT. Perhaps it would finally convinced them that inflation is the real thing. There are way too many articles on the “establishment” media that argue that inflation is no big deal, or even a good thing. They apparently can’t relate to the predicament that inflation puts the working folks, but hopefully they will be able to understand this via animal’s predicament.

AK,

“…argue that inflation is no big deal, or even a good thing.”

The NYT is absolutely the worst about that.

WE have done the exact same thing.

No more restaurants. None

No new clothes until you wear out everything else.

No vacations.

Watch the A/C like hawks.

No junk food. No chips, cookies, sauces, condiments, “snacks”. None.

No junk drinks. Water and Coffee, only.

No “perms”, nails,

No designer named stuff except from Goodwill.

It is actually fun.

MA

Of course, your wife and kids share your enthusiasm.

It IS fun MA,,, especially when your spouse has been trying to get you to do all that you mention for many years; and now you can have fun competing to see who can find the bigger bargains at Salvation Army and other thrift stores…

Only problem is that now two are checking out all the ”kitsch” instead of just one.

But brand new top of the line brand clothing for less than 10 cents on the dollar are hard to beat.

Could not believe getting $100 shirts for a buck when I was first enticed to go along…WOWZA

Why are “perms” in air quotes lol

IStever,

It is not your problem to worry about what the “other people” do or don’t do…

I guarantee you nobody cares about how you “feel”… except to use it against you…

It is your job to be cold, calculating and responsible to provide the best for you and yours…

And to protect it with sound decisions and an emotionless, jaundiced eye toward everybody…

When it comes to money, you have no friends…

This is what happens to people who watch too many “survivor” reality shows.

Try WWE for a while before you go over the edge.

“ How many have abandoned vacation plans, or a new car purchase, a home renovation because the costs have cut their budget priorities down to food, fuel and shelter.”

I dunno…

Maybe three…

some are hurrying to spend their money before it becomes worthless.

cb,

Exactly.

Then spend it on Mercury Dimes and Ben Franklin half dollars as fast as you can.

They are in limited quantities. When they are gone, they are gone.

Methinks you underestimate.

In looking at the market this morning I’m up 2.3% and it does allow me to feel better.

In regards to inflation I watch the traffic into a local bar and grill. It has remained steady since the beginning of the pandemic. I’m thinking some of this has to do with supporting local business. It also may be due to we are a small town and travel costs have increased for all.

My guess is that when QT actually dries up excess government largess we will see a downturn in our local business.

Just my two cents,

Anyone who has to cut their budget to pay for food, fuel and shelter cannot actually afford a new car or home renovation. They might not be able to afford a vacation either.

AF,

The problem is everything they see tells them not only can they afford it, but they “deserve” it…

My kids finally understand the most important phrase they could ever learn… “ I can’t afford that”….

Marriott and Hilton said the consumers are going on vacation and are spending big. They expect a very busy summer.

yeah, times are great! all we need to do is lockdown our economies every year, print $5 trillion and hand it out, and we can “boom” in perpetuity. too bad no one thought of this in the past!

There lying. The very first thing to go during inflation is vacation!

This is me because of paid airplane tickets to Cabo fronm 2019, now using them ,otherwise would stay home half of this is fake

It’s almost like there are different classes. One has lots of cash to burn – houses, cars, vacations, meals out. And the other does not.

CreditGB,

Honestly, if you see the demand for Cruise Ship Bookings and Airline Bookings – 3, 4, 5, and 6 months out – there really isn’t any evidence of widespread demand destruction yet.

One of the more pernicious attributes of inflation is that it exerts a “demand pull” effect. Essentially “I better buy this while I can still afford to buy it” – which, of course, supports demand and makes inflation worse.

BigAl, my daughter and her husband are scheduled to go on a cruise this April. It’s the one they paid for in late 2019 that was cancelled due to the Pandemic. I’ll bet there are a lot of folks who are catching up on previously paid for trips.

She tried to get her money back once the cancellations started, but the cruise line refused and just gave her a trip credit extension.

Southwest Airlines did same to me going to Cabo in 2019 now going next month

That wealth effect is soooo ingrain in their dogma that perhaps these jackass will end up moving the goal posts or change how they calculate inflation again just to fit their narrative and create that perception they are doing something..oh yeah that’s what Mary Daly meant when she said transparency to the market.

The literal metaphor comes to mind when I read stuff like this and seeing FED slow motion action or rather inaction is me picturing a bunch of firefighters standing right in front of a house burning under raging fire and debating if they should turn on the hose and by how much sometime next week..

If the Fed fumbles this one, it could all come unraveled. The 1970s had some social turmoil, but now every street kid has a gun and Internet phone coordination. Some geniuses have thought up flash mobs to block freeways with trucks. Maybe that’s why some .1 percenters are putting all that excessive gain into buying land in the remote west and building little forts. The Fed is playing for keeps on our dime, and I pray it somewhat works out.

We have recently seen what a few thousand guys with trucks can achieve. This must be really scary stuff for the 0.01%.

Fortunately for them, most people of rioting age are still more concerned with gender neutral toilets and taking down statues. I’m sure this is by design, paying both sides to fight each other so they don’t get any ideas.

>most people of rioting age are still more concerned with gender neutral toilets and taking down statues.

Who is telling you this narrative? I can tell you as a person of rioting age, that many people are concerned about rent/house prices and cost of living. I’m sure Fox News likes to talk about culture war items, but most people of rioting age worry more about the economy.

Almost all the public toilets I frequent in California are gender neutral, and nobody seems to care, although I must say that the formerly female ones tend to be a bit spiffier.

Fox says those modern cultural concerns are not what we should be focused on, we have real problems to deal with.

CNN insists that those are exactly and only what we should be focused on.

Which one is right?

But I haven’t seen any mass demonstrations yet protesting inflation/ high house prices/ etc, while I do see many culture war demonstrations (and not just on TV, but also in the city where I live).

So I guess you are right that people worry, but for some reason they don’t take to the streets for this.

Perhaps it has to do with the fact that most people don’t understand what inflation is, and the mass media presents it as something that is either good (The BBC calls rising house prices “house price GROWTH”!), or that it is something external that just happens and has nothing to do with money printing and overspending by the government.

Exactly.

Most people of rioting age are concerned if they will be able to exist in our oligarchic kleptocracy, or if NYC will be drowning in 30 years.

There is no rioting age if things get bad enough it all comes unraveled back to 1883

Fox News makes sure that the rabble are always foaming at the mouth about some nonsense. God forbid they actually figure out that the oligarchy wants it that way.

My youngest son just got out of his teens.

He and his friends are more conservative than I. In fact, when I hear them talking, it scares even me.

They all know. They all talk. They tell me about things I never knew since they share everything they find from the internet within minutes.

I am stunned how aware this bunch is, and they assure me “all our friends know”.

Escierto:

I don’t think that tactic is limited to Fox News.

Fromks,

Is this a recent phenomenon?

Were you worried 5 years ago?

What were you doing 5 years ago?

Not being sarcastic, just curious as to where you were then and your ascension to today?

Be honest about your journey please…

Trying to learn the mindset…

Us top 20%ers and elites won’t tolerate a working class revolt. Trudeau made that clear. Our Amazon packages will be delivered on time or else.

The vast amount of coverage was on the blockaders. A tiny amount was about the people living and working with their streets blocked for 22 days. One item: an eighty year old lady living by herself near downtown took the bus twice a week to shop, get out of the apt. The little bit of life left to her.

Then a few weeks ago, on the return trip the bus driver told her the route was blocked. She was dropped off 8 blocks from home in sub- zero weather.

The emergency powers should not have been necessary because it should be a crime

to prevent anyone from their legal access. This would also apply to the natives who blocked a rail road in Ontario to ‘protest’ the Trans-Mountain pipeline in BC! (PS: does everyone know there is already a pipeline there. The project is twinning it.)

Should be no more emergency power needed if someone steals your access than if they steal your goods. Jail. And if the weapon used to prevent access is a truck it should have its MV reg cancelled, subject to return with fine and conditions.

nick, were you as adamant when blm protesters shut down interstate highways?

Sure: But I’m Canadian living in Canada and this issue was brought up. A ‘protest’ is communication. Holding placards etc. or in the case of a legal strike, picketing the specific target. The average citizens living in Ottawa and your folks on the highway were innocent victims. 22 days is a long time for a blockade.

So this whole thread from YuShan on down is a…a…. “discussion”?

A “meeting of the minds”……so to speak…..?

Sounds like Theatre of the Absurd to me……

Godot is coming, trust me…..anytime now….

Make that down to COWG….It looked like it ended there when I posted this. I’m not going to read any further…maybe I’ll go watch Columbo…..easier to understand.

I believe the saying goes something like:

“When people who have nothing lose everything…that’s when they lose it!”

One per enters have no idea how to survive ,most never did any honest work.that being said hope they know how to cook ,clean dish’s,wash clothes or raise a garden ,they will perish faster than a kid in ghetto who knows animal instinct survival,because they’ve lived it there whole life

Complete bullshit. Many are like me, worked hard, lived cheap, and invested in the future. We became 1%ers in our 60’s. We lived thru the 50’s, 60’s, 70’s and 80’s.

Believe me, we know how to survive. It’s my kids and grandkids I am worried about.

obviously he was generalizing, but in many cases, he’s not far off. a lot of the people who are now in their late 50s and early 60s, who started off trading at new york investment banks in the early 80s don’t know how to change a tire, much less grow food or anything else.

Aren’t you the guy who went broke with dependents, somehow bought some real estate and watched it “shoot the moon” in just a decade or so to give you a 20 million worth? That sounds a lot more like good fortune than hard work. Nothing wrong with doing the right thing at the right time, especially if the FED is providing big tailwinds. I saw a lot of people heavy with leveraged real estate, about to go under, get bailed out by Government and FED actions. They went from being under water to being wealthy in a matter of 8 to 12 years, and now pinch their renters for every penny they can. Oh yea, they lean libertarian, but never saw a subsidized loan they didn’t like.

Let’s not confuse good fortune with “hard work.”

phleep.

The Fed HAS fumbled this one. This situation is of their doing.

Record low interest rates combined with 40% jump in M2 in two years…and they blame bottlenecks?

And now they are afraid to do what they should have done 5 months ago.

All traders know, going in is easy…it is the exit that requires deft, agility and forethought

As long as the FED maintains their stated goal of 2% inflation, and they maintain the power to print money and suppress interest rates, anything they do to “taper” current inflation will be little more than short term blips. Long term, they will continue to deny free markets and will favor owners over workers. They will favor financial engineering and insiders close to money printing, over savings and prudent practice.

To save dollars in the face of dollar digitizers who get to pick winners and losers, looks like a fools errand. Talk of the importance of financial markets and capital formation is just cover in the hope of establishing some merit to the Private Equity, stock market practitioners and other financial engineers. Capital formation – what a joke. The FED creates all the “capital” it wants with a keystroke, and that destroys the dollars you have saved.

Forget about free markets. The FED has done their part to place overwhelming advantage to favored players and to destroy any concept of free markets within the asset ownership markets.

The FED has fully realized with limited resources, an ageing demographic worldwide that growth as we know it is over in regard to actually producing GOODS.

As a result, the only game in town is exchanging digits thus where we are now.

It’s completely ridiculous that in the current situation with inflation at a 40 year high and still ZIRP(!) that we are even discussing whether they should raise rates with 0.25% or 0.5%.

Although imo it is fundamentally wrong to have the Fed mess with interest rates at all, at least in the past they had a policy framework that they followed, so it was at least rule based and not completely discretionary like it has been for more than a decade now. Before the GFC, this was mainly based on the Taylor Rule (which uses real GDP output gap and core PCE inflation).

At the moment, the Taylor Rule would put the Fed Funds at about 7.75%.

No wonder markets are completely broken and nothing makes sense anymore!

I partly attribute it to an implied awareness that society is falling apart.

Normalize monetary and fiscal policy and all the supposed (fake) prosperity evaporates.

Face it, the country is actually close to being broke.

Most supposed wealth is actually someone else’s debt and most of the rest is attributable to ridiculously overpriced stocks and real estate.

The country has outsourced much of its manufacturing capacity and doesn’t even produce sufficient and sometimes any essentials, as reported during COVID with pharmaceutical components.

The top 10% will eventually realize how much of their “wealth” was only on paper. And any of them who borrowed against it will get to experience the terror of a margin call.

There is a resdin why the Zuckerbergs, Gates and Bezos are selling stock and buying hard assets.

Especially productive land.

And beach front properties…because, yeah, you know why.

2banana,

If they were clever…they would be buying it outside of the USA unless they have an army of robot servants ready to work the land for them.

Good point.

Also, if the wealth inequality increases a lot then the rich are the ones having big problem and their freedom curtailed. Just look what is happening in South/Central America or other countries.

Wealth inequality is a pretty bad for rich people in USA especially with guns all around us.

Maybe they don’t intend to work the land.

Maybe the point is to take it off the market.

Control the Food, Control the People.

They DO or will have robots to do the vast majority of the work BA!

About 20 years ago, we began to see the first GPS directed bulldozers and graders start to do a better job than any but the most experienced operators in the ”civil” part of the construction industry.

Surely, there will always be some demand for the delicate work of digging new foundations under existing houses, but that will likely go back to being done by hmns with shovels as we used to do.

Beach front home owners may worry about beach erosion, storm surges and higher property insurance rates as wind velocities are higher close to the ocean. Those in designated flood zones may be asked to get separate flood insurance when applying for a mortgage.

Why not the entire 100%, if wealth is only on paper, er computer?

Aye, there’s the rub…

…it’s very difficult for company founders to dump their stock without triggering a collapse in the stock value.

One has to resort to “Bill and Melinda Gates Foundation”s and other such administrative difficulties for the proper diversionary air cover. So messy.

No they won’t they’ll hedge against market and make more money

Just got hacked again after buying a couple of books off of the Amazon.com website. Jeff Bozos wants everything. Even your soul.

Yes,only 1% of wealthy will do good.The rest will be surviving.Sellection of the flexible will take place,finally.

How are you people not seeing this…

If you take all the squigglies on the pce chart that are above two percent and then carry them down to the squigglies that are below two percent, then you have a nice straight line with the green one… duh, easy…

The man’s a fricking genius…

I believe our host is just a pot stirrer :)

I’m not old enough to remember the early 1980’s during high inflation of how many zombie companies/ banks/ hedgefunds etc , imploded, but i suspect the stock market will hit some major turbulence this spring

There were few hedge funds (none blew up), very few bank failures, and few zombie companies in the early 80’s.

Unemployment was high and the stock market was really cheap.

Times were tough for a lot of people, but it was acknowledged generally as bad times.

This is supposedly the good times

You forget the S&L crisis where taxpayers bailed out billions to people like Jeb Bush of the Bush dynasty.

If money was of worth such as it was in the early 1980’s, we’d see interest rates within hailing distance of inflation, but when you conjure up as much as you’d like to those that matter who don’t mind, the ones that mind, don’t matter.

Since 1913, we have not had money.

Money, as defined by our own Constitution was COIN made of Gold or Silver. Not Paper. There was a reason for this. Those who established America knew of the relationship between civilization, chaos, and “real” money.

Paper, Letters of Credit, Bonds, Notes, Promissory Notes, Certificates of Deposit (not backed by Gold-Silver on Deposit), etc., are not coin, not gold, not silver. They are not money.

Why should any bank pay you any interest for printed paper? They can print their own. If we used Gold Coin or Silver Coin (Historically used as money far more often than Gold) then banks, and lenders, would have to pay YOU interest to get you to deposit your Gold-Silver.

For those who think Gold and Silver are a joke, and really have no purpose, think again. Could all this mess occur IF we used them?

Look up photos and pictures of “Money” over the ages. Especially Paper. Read what it says. “Gold On Deposit”, etc. Why was this wording, slowly and quietly removed? Where is all that Gold?

The most incredible, audacious, and brilliant Theft in History.

Btw: I find the ECB even more scary. At least the Fed has signaled that they are starting a series of (tiny) rate hikes and perhaps even reduce their balance sheet.

But the ECB is still “perhaps we will do our first tiny rate hike in 2024”. Although their ONLY mandate is inflation (not even employment), their main worry now is to keep insolvent southern countries like Italy and Greece within the euro (which really is none of their business).

The ECB has deliberately (and illegally) stuffed their balance sheet full of Italian debt, so now when this thing falls apart the cost to paymasters Germany and The Netherlands will be so high that politics never dares to go there.

YuShan,

“But the ECB is still “perhaps we will do our first tiny rate hike in 2024”. ”

That is outdated. The new line is “rate hike later in 2022.”

Thanks for correcting me on that. I missed that somehow.

Jeez at this rate by the time interest rates get to where they should I’ll be dead, and I’m hoping to live another 30 years!

And inflation will match your “30”……..30%.

I really don’t see a return to a low inflationary environment…regardless of FED action or inaction.

It’s very interesting to contemplate a chart like this:

https://tradingeconomics.com/commodity/coal

This is the price of Chinese coal. As you can see it has remained stubbornly-high evern after the use of government price controls and an emergency program to raise both domestic coal output and increase coal imports (ex-Australia, of course).

Here’s the scary part:

This is all happening against a backdrop in which the Chinese *household* share of GDP is the lowest in many years. At some point – that household share *will* rise again and the output that uses this coal will be consumed domestically rather than internationally (e.g. exports to USA).

So, in the long-term, making stuff in China might be cheaper in the USA (disinflationary) – but not deflationary. Reshoring – if even possible – is not the work of a moment, or even a couple of decades.

So – regardless of what the FED does – we might as well all pitch our tents (assuming, of course, we can still afford one)

– I continue to think that the FED will raise rates 0.25% this or next month. That’s as far as I am willing venture right now. Only when the 3 month T-bill rate climbs above 0.40% or 0.45% I am willing to entertain the thought of the FED raising rates more.

– I am much more worried by rising long term rates. But I am NOT convinced that these rate will continue to “go ballistic” (yet ??).

– I continue to point to what happened in the 2000s. In that decade we saw oil go up from about $ 20 to over $ 140. But in spite of rising inflation long term rates actually went from about 6.5% in the year 2000 to about 4.5% in mid 2008. This is for me the best example that interest rates are NOT driven by inflation.

– ‘I continue to think that the FED will raise rates 0.25% this or next month.’

You think that? No one doubts there will be at least a .25 hike in March. The only question is whether it will be .50

Don’t expect the FOMC to burn their “Lords Of Easy Money” satin “tour jackets” anytime soon! I am currently reading the book “The Lords of Easy Money”, and learning about J-POW’s time at Carlyle Group. His hand in destroying companies like Rexnord makes me sick. (As does the empty Rexnord parking lot in West Milwaukee). Don’t expect much from this bunch in terms of what’s right or wrong. It’s all about them “making bank”.

Duane

I think Powell considers all those CLO’s that the venture capitalists float and roll when he considers raising rates. (if he does)

What stuck out in my mind while reading that book was the CONTRAST in backgrounds of Hoenig and Powell and how their value systems were molded by their life experiences. One worked his way up with Midwestern values….One was fast tracked through prep school, ivy league, venture capital gaming, and then plugged into high level government.

No wonder Hoenig considered and identified the dangers and ill effects of these rogue Fed policies, while Powell seemingly held more allegiance to those with whom he rubbed elbows with on the way up to his perch.

Joe sometimes wears a Members Only jacket to remind himself of the inflationary era in which said garments were popular.

you’ve got to remember that bankers duty is to screw you. Oh they’ll talk nice and try to convince you that they’re normal and have your best interests at heart. Don’t you believe it. Print money out of thin air and loan it to you at interest. What a racket!

I sure hope you are not including community bankers in that statement. I spent most of my life in community banking and we have nothing to do with the giant “bullion banks” that manipulate precious metal prices and the other giant banks that manipulate bond prices and currency values. Community banks make large financial contributions to their local communities and it is their best interest to support their local communities unlike the giant banks of the banking industry.

Exactly! Pay of all interest first! That will fix them! 😅

The worse the news, the better for the stock market

No, we just had two days of relief rallies, which is standard practice in the stock market on the way down. Bear market rallies are the biggest rallies.

The Cpi is inaccurate. 7.5%? The largest part of the CPI involves a phone call survey to determine rents. It says they are 3.5%. When real world data screams far higher. The US government has an incentive to understate inflation. Just look at COLA and what more the US would owe if it were higher.

So those that say the fed are hawkish raising rates 7 to 10 times this year are wrong. The fed is dovish. They are not even planning on normalizing rates. Even if we raise rates .50 10 times that would only be 5%. In order to squash inflation you need to raise raise rates to 16% or more.

The fed is pretending to attack inflation and they are lying to all of us. Inflation is a hidden tax on all of us. The fed printed trillions of dollars. That is why we are where we are today.

The fed should be audited. We should not be involved in wars in other countries. We need a president who is cognitive and answers questions after speeches.

“Inflation is a hidden tax on all of us”

I work all day in a futile attempt to replace what the FED steals while I’m sleeping.

So, no, that tax ain’t very well hidden from “all of us”.

Hal..

” The printing press allows the government to tap the property of its people without having obtained their consent, and in fact against their consent. What kind of government is it that arbitrarily takes the property of its citizens? Aristotle and many other political philosophers have called it tyranny. And monetary theorists from Oresme to Mises have pointed out that fiat inflation, considered as a tool of government finance, is the characteristic financial technique of tyranny.” mises.org

Get an “END THE FED” bumper sticker and display it proudly. I do.

John Q

The rent and housing input proves intellectual dishonesty by the compilers of the index.

Case Schiller has hard firm data that is cold stoned for anyone to analyze.

Who compiles the “rent” survey…and who would know if the results were being “massaged” before published?

Jerome is a tough TASS master who must realize he’s in too deep, thus the constant obfuscating.

The slowness of dealing with this crippling inflation can only mean

intent

or

ineptitude

About the only way out is to divorce yourself from dollar denominated assets, but how do you go about doing that?

Fed is not stupid or inept. It’s all happening by design.

John Q Public,

RTGDFA

This was NOT about CPI. It was about the measure that the Fed uses for its inflation target.

From the article

“This not-so-mind-boggling inflation monster was created by $4.8 trillion in money-printing in 23 months — ”

In 2007, the total M2 was circa $7.5 Trillion….

In 15 years the money supply nearly TRIPLED…….

So, for the first 217 years of this nation, money supply $7.5 Trillion

and the National Debt $9 Trillion.

Since 2007 money supply now circa $21 Trillion, National debt $30 Trillion

That is quite a 15 years of “NEW” Fed policy…..Bernanke, Yellen and Powell….oh my.

And the Fed blames bottlenecks, and Powell rejects the Quantitative Theory of Money..

“The Quantitative Theory of Money doesn’t apply according to the Chairman of the Federal Reserve……“the growth of M2 … doesn’t really have important implications for the economic outlook.” Since then, the U.S. annual inflation rate has climbed to 7.5% from 1.7%, but Mr. Powell hasn’t changed his mind…”

WSJ 2/23/2022″

Get the feeling they are making it up as they go along?

No, the know exactly what they are doing to continue living at the standards they created with no care whatsoever about anyone living below them.

As long as they placate the public, keeping them dumb, fat and happy they will continue to enjoy their status.

Once enough people actually wake up (if they ever do) watch out. It’s just a balancing act at the moment, keeping enough scraps on the table to prevent big problems to “them”.

See Truckers in Canada…not until they used the controls they had to hit the pocket books to survive did anything happen. Get enough hungry desperate people in the future…

Thus oil prices will come down, some asset prices through QT, stocks prices for the few that actually hold them then the game will start again.

That’s funny, because the Fed Monetary Policy Report released today reads, “business as usual”. Inflation is not really mentioned, and they expect Fed Funds rates to remain at or near the lower bound. I encourage you to read the report.

I don’t see FED would be hiking rates to tame inflation in a meaning ful way.

Inflation on ground is close to ~19%, govt manipulated metric says it is ~7%.

When I say meaningful way, it means that raising rate to match inflation rate. Going by so called Tyler’s rule, Fed’s rate should be 7%.

Even if Fed raises rates by 50 basis points in March, it does nothing to tame inflation.

“23 months of policy errors”?

How long ago was Greenspan?

Debt by definition is “pulling consumption from the future to the present.” We have built a tremendous bout of future consumption which needs to be paid for today. Raise rates, stop future consumption; we might have a chance.

Not if you plan, one day, to raise inflation to 18% yoy. Then it’s not really pulling demand forward, but rather sustaining demand. Of course, anyone not working (i.e. retirees) is screwed when this happens.

the working are screwed too, as the wage increases don’t come close to keeping up.

Hopefully, the Fed can print up some energy for Europe.

The idea that the fed is going to overdue the increase….or somehow be forced to tighten……is off base…….it is based on the idea that the fed is staffed by patriots who got the inflation call wrong

The fed is staffed by a crooked pack of greedy bastards who have no US blood in them…….they will continually find excuses why they must let grandma get her life savings stolen while they party at the country club. After government they will go to that overpaid position collecting their just reward for ripping off grandpa at a large bank.

The US is no longer a country…..its a global enterprise dedicated to enhancing the wealth of the royal few while providing military protection to their investments.

As long as the FED maintains their stated goal of 2% inflation, and they maintain the power to print money and suppress interest rates, anything they do to “taper” current inflation will be little more than short term blips.

You can’t have a goal of 2% inflation and not be at odds with “tame inflation” rhetoric.

It looks like more of the same: continued lip service, continued nothingness or de minimis action, continued inflation.

America only produces 2 things:

“Dollars” and “The Dow”.

MA: You forgot things to blow up stuff.

You forgot ‘trash’, that’s where all the Chinese crap is going.

[content deleted by Wolf Richter]

Noname,

I deleted the BS you posted. However, I want to direct your attention to my commenting guidelines: read the whole thing, then re-read the 4th paragraph from the top. It essentially tells you to stick political stuff somewhere else.

I spent four years deleting stuff posted by the Trump haters, and now I’m in my second year of deleting stuff posted by the Biden haters. It’s a dirty job, but someone’s gotta do it. This is a financial site, and it’s for people of all political persuasions, and I don’t need for people to shout at each other.

If Biden-hater stuff is the only thing you can post, then don’t post here. Go somewhere else.

https://wolfstreet.com/2017/10/07/finally-my-guidelines-for-commenting/

This is exactly the kind of monetary policy decision making I would expect given that a journalist and a few lawyers are key decision makers sitting on the FOMC board.

Jim Grant just said it would take 38 0.25% rate hikes today to get us where the Taylor rule says we should be for a stable monetary policy.

.5 point rise is tantamount to hunting an elephant with a BB gun.

It’s going to make inflation angrier.

Well , the Chairman does not recognize that the 4.8 trillion in 23 months did anything of the sort other than perhaps a wee smidgen of the inflation print. He made a blanket statement to that effect in Feb 2021. Mrs Magoo over at treasury said the same thing. You might have to put yourself in moderation telling whoppers like that.

Wolf; I looked at the markets’ 2.5℅+ rise today with the backdrop of Ukraine and wondered whether it was a smackdown of Powell, with the markets signalling that they don’t believe he has the balls to raise interest rates, or whether it was a sign of gratitude that he has stayed the course and continued to do nothing. Could it ,in fact, be both? I tend to lean more toward the former, but, of course, I am not J. Powell. People who think like me are generally an anomoly, except perhaps on this site.

Relief rally, yesterday and today.

This rally may be due to Europeans moving their money out of Europe into US based companies in a flight to safety.

Anyone else getting sick of the FED and its lowball inflation figures?

We need a positive force that is PRO the US, not one which seeks to take

it down, or at least does so in practice. WTF did these geniuses at the

FED come from anyway and why are they in charge of the country now?

Are we so pathetically weak that we can’t function with these cretins?

“This not-so-mind-boggling inflation monster was created by $4.8 trillion in money-printing in 23 months..”

This is wrong Wolf; not the money printing did it but to hand the money out to the consumer for free in an exorbitant amount.Money were printed already since the financial crisis.

But free money to the consumres will be spent freely by them. Hard earned money is much more valuable and people think twice to spent it.

“Thanks” to Corona the people in charge found a situation allows them to do it. What a coincidence.

What happened were unprecedented and happened as far as I know only in your country. In Europa businesses got some money but consumers not got any extra money. Inflation here comes from the energy prices.

You continuously block my reply button to your answers. Could it be that your ability for critical discourse is limited ?

Wakarimasen,

Hahahahaha… it’s OK if the Fed throws $4.8 trillion at the biggest asset holders – a small percentage of the US population – to make them richer and trigger the biggest big-ticket spending boom ever, but when you hand the unemployed a few hundred extra bucks a month, it suddenly triggers this monster inflation???

In reality, both play their role, as I pointed out. But the far bigger role is played by money printing and interest rate repression.

In terms of the “Reply” button: Don’t make up silly theories. Comments here can be nested up to four deep, and with the comment nested in fourth position, there is no more reply button. This counts for everyone, not just you. Just click the nearest reply button above it.

IMHO Federal Reserve is waiting to see if inflation will come down after pandemic disruptions are fully over, and if it does, to what level. I think this situation (inflation subsiding by itself) is the only case when Federal Reserve can actually fight [weakened] inflation with some hope of success. Otherwise (if inflation remains high) they have no chance of bringing inflation down without stock market and possibly housing market crash ,

so they wont even try.

the pandemic disruptions haven’t been an issue since maybe july of 2020. it’s all demand created inflation at this point.

It probably is not as complicated as that. I’m sure Powell and others are waiting for senate confirmation votes before making any changes.

Wolf, do you know what exactly is accounting for this increasingly massive gap between CPI (7.5%) & PCE (5.2%)? I know the baskets & weights are different. But in the past, however low PCE got, it was typically within 0.5 to 1% of CPI, and there have been rare occasions when PCE actually exceeded CPI.

I know it’s in the Fraud Reserve’s interest to pick the lowest of lowball inflation metrics to benchmark against, but given the heavy weightings of shelter & other necessities no matter which index, where else is the discrepancy coming from?

Jackson Y,

First, we need to stick to apples and apples.

overall CPI = 7.5%; overall PCE = 6.1%

core CPI = 6.0%; cover PCE = 5.2%

So on this apples-to-apples basis, the difference is smaller.

One of the other big differences is the weight of housing in PCE; it’s less than in CPI.

Another difference is that PCE is a chain-type price index, which means it’s more aggressive in taking into account changing consumer purchase patterns, such as when something gets too expensive, consumers are assumed to switch to something cheaper, and the index adjusts the weights. This lowers the weight of the biggest price movers.

What the Fed should do and will do are two different matters altogether. That the market has more than held up gives me hope that there will be at least a 25 bps hike. I for one am skeptic about 50 bps hike. If market tanks, the King Kongs could swing into action with their money guns claiming the higher inflation now is due to war and hence “transitory”. One cannot put this past them!!

Since 2008 the Fed’s stomach turns queasy when market starts dropping (me thinks having seen what can happen to the Financial system in 2008 has given them the heebie-jeebies permanently and they are unable to get over it. Add to it they think their actions have saved the system and has made them look like King Kongs). So they have been going along merrily. However, inflation has landed one on their jaw. A well-deserved one if I may say so.

The more interesting thing is at what S&P level will the Fed cave in. The figure bandied about is 3800s. Given that market has doubled from 2020 lows a drop to 3800s is still a 50% jump from 2020 lows. So the market is still happy!

Hopefully oil and commodities rise in the wake of the war should fuel inflation further and show up the Fed for the arsonists they are.

“What the Fed should do and will do are two different matters”

In a system that boasts of “checks and balances”, WHO CHECKS THE FED?

1/4pt …1/2pt….wait for the FOMC meeting? BS!

Inflation just jumped 5% in 7 months….that 5 x’s 1/2pt. And they hand wring over ONE 1/2pt?

$21 Trillion in new national debt….to prop the markets

Now, promoted and unaddressed inflation to prop the markets….

This is a race to the bottom……

IMO, the economy would welcome higher short rates and lesser inflation…the markets may not….the venture capital buddies of Powell might not like it, Larry Fink might not like it…..but if the markets cant handle a FF rate 5% below the inflation rate, how fragile is it?

should read TEN TIMES a 1/2 pt

Steve Hanke has a historical chart out showing the very high predictive power of money supply vs. inflation. His logic is sound also.

Without increasing money supply, there is not an increase in the total price of a basket of goods. Gas may go up relative to other goods, but if it does something must go down as consumers are forced to choose where available income goes.

Not sure if he is exactly right, but he has been able to predict inflation rates one year ahead very accurately. It might be because he is professor of APPLIED economics and not the Fed style of economics which has a lot of politics woven through it.

“• The Quantitative Theory of Money doesn’t apply according to the Chairman of the Federal Reserve……“the growth of M2 … doesn’t really have important implications for the economic outlook.” Since then, the U.S. annual inflation rate has climbed to 7.5% from 1.7%, but Mr. Powell hasn’t changed his mind…”

WSJ 2/23/2022

Willful ignorance …… or just ignorance?

“inflation is always a monetary phenomenon.”

Hyper stagflation?

Well for once we seem to be on the same page Wolf.

“An asylum for the sane would be empty in America.” ~ George Bernard Shaw

“We live in an age when unnecessary things are our only necessities.” ~ Oscar Wilde

“The most reckless Fed ever is still just watching – and fueling – the consequences of 23 months of policy errors as the Inflation Monster gets bigger and bigger.”

Excellent summation. I would take it one step further by saying that the policy error can be traced back as far as 2013 … when the 2008 crisis was clearly over but ZIRP persisted anyway. Had the Fed begun to allow rates to normalize at the time the economy would have entered 2020 in much better shape.

Going into the next crisis with dangerous levels of debt, an exploding wealth gap and asset markets already in bubble territory was an avoidable error. We could go back even further … the Fed underwriting the nineties stock market bubble, etcetera … it takes a lot of mistakes to wreck a once strong economy this badly.