The Magic Number in 2018 was around 4.8%. In 2006, it was around 6%. But with today’s super-inflated home prices? Here are the signs.

By Wolf Richter for WOLF STREET.

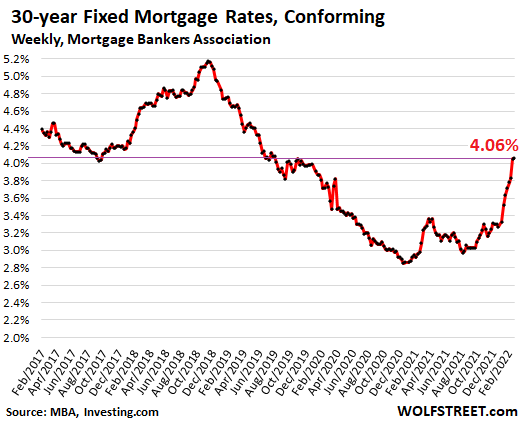

The average weekly contract interest rate for 30-year fixed-rate mortgages with conforming loan balances rose to 4.06 percent for the week ended February 18, the second week in a row above 4%, and the highest since July 2019, according to the Mortgage Bankers Association today. The average rate for FHA-backed 30-year fixed-rate mortgages increased to 4.09%.

So where is the magic number beyond which this super-inflated housing market starts to feel the pressure of higher mortgage rates?

But mortgage rates remain ridiculously low, in face of CPI inflation that has shot to 7.5% and is still being fueled by the Fed’s ongoing interest rate repression and QE – which makes this the most reckless Fed ever.

The “Magic Number” in 2018.

In the fall of 2018, as mortgage rates headed toward 5%, the housing market was beginning to wheeze, and stocks were spiraling down. The magic number at the time appears to have been about 4.8%, and when mortgage rates moved above it in September, all heck started breaking loose.

After the S&P 500 had dropped about 20% by December 24, 2018, and with the housing market weakening, Fed Chair Powell caved under Trump’s daily hammering and did the now infamous U-Turn.

However, back then in early 2019, inflation was below the Fed’s target, as measured by its yard stick “core PCE,” at 1.6%, and that provided Powell a fig leaf.

Now inflation is the worst in 40 years and spiraling higher, and “core PCE” inflation is 2.5 times the Fed’s target. It’s now inflation that is hammering Powell on a daily basis – him who’d made a fool of himself calling this monster he’d unleashed “temporary” when everyone already knew that it would spiral higher.

So where is the magic number this time beyond which the housing market starts to feel the pressure?

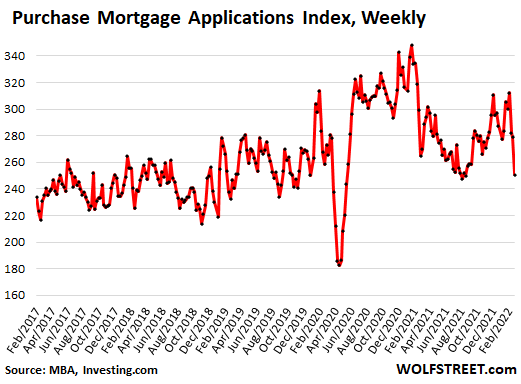

Mortgage applications to purchase a home have dropped sharply for three weeks in a row, coinciding with the surge in mortgage rates, and in the week ended February 18 reached lows briefly kissed in August 2021, and then during the lockdown, to enter the lower part of the range in 2019. The MBA’s index for purchase mortgage applications has now dropped by 28% from the January 2021 pandemic highs (data via Investing.com):

The “Magic Number” in 2006.

Not shown in the chart: Back during the peak of Housing Bubble 1, in January 2005, the MBA’s Purchase Mortgage Index had maxed out at 500 – twice today’s level – before it collapsed.

At that time, the Fed was in the middle of its rate-hike cycle, taking the federal funds rate from 1.0% in June 2004 to ultimately 5.25% by July 2006, which pushed the average 30-year fixed mortgage rate to 6.4%, at which time the housing market ever so slowly began to collapse.

The Nasdaq started heading lower in the summer of 2007, and little by little all heck broke loose in a global manner, punctuated by the collapse of Lehman in September 2008.

Higher mortgage rates, when home prices are already sky-high, are very tough on housing markets. And higher interest rates in general are tough on stocks.

So where was the magic number back then? Obviously 6.4% for the 30-year fixed mortgage rate, at those Housing Bubble 1 prices, was beyond the magic number.

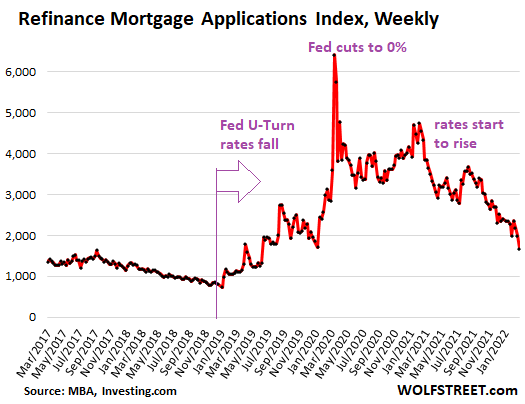

Refi mortgage applications plunge.

Rising mortgage rates means that households are putting refinancing their mortgages on the back burner. This happens despite the historic explosion of home prices that brings with it a lot of home equity that could be drawn out via cash-out refis.

The MBA’s Refinance Mortgage Applications Index has now plunged to the lowest level since June 2019 and is down by 74% from the pandemic highs – and mortgage rates have just started rising and are still ridiculously low, given that CPI inflation has surged to 7.5% (data via Investing.com):

The Magic Number now.

First-time home buyers, facing these higher mortgage rates and sky-high prices, have already pulled back from this ridiculous Fed-inflated market, as investors and cash buyers have piled into the market.

In January, first-time buyers dropped to just 27% of total home purchases, down from 30% in December, and down from 34% in all of 2021, according the National Association of Realtors.

Going forward, “some moderate-income buyers who barely qualified for a mortgage when interest rates were lower will now be unable to afford a mortgage,” the NAR said.

With each increase in home prices, and with each increase in mortgage rates, more layers of potential buyers get wiped off the table. At first no one notices, but then the layers are starting to accumulate, and at some point, the regular buyers – such as first-time buyers – are starting to thin out. And that’s what we’re now seeing.

At first, cash buyers and investors may be able to make up the difference. And that’s what happened during Housing Bubble 1, which was in part driven by investors, who then become the core of the mortgage crisis when they walked away from multiple properties at once.

Individual investors or second-home buyers piled into the market, accounting for 22% of home purchases in January, up from 17% in December and up from 15% in January last year, according to the NAR.

All-cash purchases jumped to 27% of home purchases in January, up from 23% in December and up from 19% in January 2021, according to the NAR.

But in January, mortgage rates were still in the 3.5% to 3.7% range, well below the 4% line. And already, visible layers of first-time buyers started to get pushed out of the market that has been artificially inflated by the Fed’s reckless monetary policies, and that now faces rising but still artificially low mortgage rates.

So it looks like the Magic Number now for the average 30-year fixed mortgage rate is a little north of 4%, a level when the layers of potential buyers, such as first time buyers, are disappearing from the market. This is already happening.

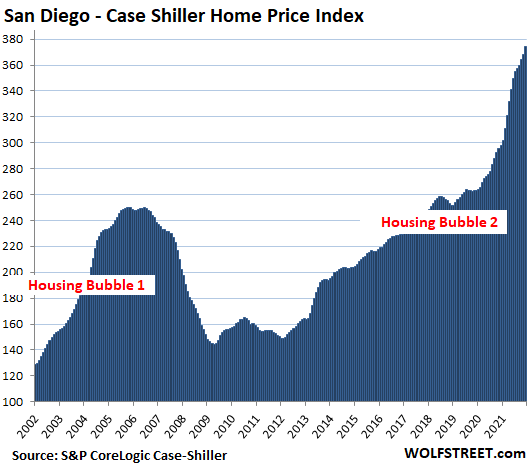

For now, as last time, over-enthusiastic investors are making up the difference, but if we’ve learned anything from the debacle 15 years ago, it’s that this investor enthusiasm too will fade in these ridiculously over-inflated markets when interest rates rise in face of spiking home prices as in the Most Splendid Housing Bubbles In America:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So if we assume that a 1% increase results in 10% decrease in collateral value, isn’t the magic number at the threshold where collateral values decrease by more than 20%? In other words, whenever mortgage rates increase by 2% or more from any collateral value peak?

Isn’t that when banks start to freak out since the collateral no longer covers the remaining debt obligation?

Peanut Gallery,

Assuming that this holds, it will affect only a relatively small number of homes — those purchased in the last year or two and financed with mortgages, not the overall pool of mortgages, many of which have been paid down by a lot.

About one-third of homes are free and clear. Another third have mortgages that have been paid down by a lot, and have large amounts of equity in them. They’re not at all at risk.

At risk are the most recent purchases at the most recent price spikes; and of course cash-out refis if they pushed the limits.

Good point.

Is there any good data out there on equity levels of homes now and past?

Looks like CoreLogic has some decent aggregate data on homeowner equity. Google search CoreLogic Homeowner Equity Insights written Dec 9, 2021.

The data was for Q3 2021, but it reads that only 2.1% of mortgaged homes had negative equity, down from 3% the previous year.

So what will then bring down collateral values in a meaningful way? It has to be that people lose their jobs and sell because they need the cash?

An increase in for sale inventory to change the balance between supply and demand, whether it’s from job losses or otherwise.

A crash or noticeable decline in other markets could also do it, though any decline in the bond market is going to be highly correlated to RE.

We don’t know where hidden leverage is out there ready to detonate like a neutron bomb.

People that took out equity lines with variable rate mortgages for extra cash will start getting pinched first.

These variable rate mortgages by homeowners with low fixed rates on their first mortgages could cause problems for many homeowners.

Apart from job losses, a change in mindset of people can raise the inventory level.

Anyway, home prices are set in the margins.

Of the 1/3 without mortgages what pct. are outright owned by “investors” and/or 2nd and 3rd homes?

Wolf,

A few “known” unknowns:

1) Use of collateralized asset lines (through brokers) to make “all-cash” purchases; assets that may have already declined 20+%. If the LTV is 50% – 60%, Mr. Margin may be placing a call in the near future. And there’s no 90 day workout – make the margin call or we sell you out. No idea how much this is used, but I think it can impact at the margin (no pun intended).

2) Carrying ability – lots of “investors” who plan to rent. Unfortunately, tough to cover carrying costs on many rentals. Now there are tax advantages that offset the losses (to a limited degree), but they’re not as advantageous on a single property as most people think. Again, I think a lot of naive investors figure they can rent for close to carrying costs.

3) Taxes, insurance, etc. increase as the value of the property increases. One commenter below mentioned a $1.2mm house in Austin – that runs about $25k in taxes alone. Those costs increase even though there’s no change in cash flow.

Interest rate increases just lower the pool of potential buyers if the prices don’t change. For most people, it’s all “how much a month”.

There have already been a select few on Reddit seeking help and suggestions because they’re getting margin calls in line with your item 1 above.

When you use the term “collateralized asset line” through brokers, are you referring to institutional investors who pay (borrowed) cash for a home?

I can’t imagine that this would be a very big portion of the population? Is there any data on this?

FastEddie,

Yes. In fact, I’ll go a step beyond that.

Institutional buyers that were buying homes with finance they obtained at preposteriously-low rates are now pivoting to simply paying cash for the properties (i.e. no financing). This is most-likely to be motivated by a desire to hold less cash, anyhow, in a high-inflation environment.

Good points, Wolf.

But there is another dimension of housing affordability to consider – property taxes.

As a result of the pandemic, lots of cities and towns have lost significant portions of their tax base due to the loss of commercial tax revenue from small businesses and sales tax revenue.

These losses have not had a major impact on municipal cash flow – yet – because these cities and towns have benefitted from significant pandemic aid packages delivered by the states. These are now ending…which, to me at least, strongly suggests that property tax rates are going to rise. Add in the likelihood that many cities and towns “froze” assessment values at the start of the pandemic to give some form of relief in the absence of outright abatements – and the increase in property tax rates next year could be breath-taking.

This is an affordability crisis of a different nature. And I don’t think very many people have mentioned it yet.

Surely the most at risk are multi-mortgage holders.

If a 1% rate increase leads to a 10% decrease in prices, if they have 10 mortgages they are getting hit across each one and have nowhere else to go for margin as most of these landlords are all in.

Banks aren’t going to be worried on most loans because it’s the taxpayer at risk.

Besides, a bank isn’t a human being and the management responsible for credit policy doesn’t necessarily worry until the cycle has turned, loan quality deteriorates noticeably, their bonuses get cut, and lastly their job is at risk.

It’s still someone else’s money.

Moral hazard on steroids.

The banks have been neutered since the GFC. JPM has a loan to deposit ratio of 45% today vs. 85% in 2006. All the banks have way too much liquidity. In addition, it is not easy to qualify for a loan. You have to have skin in the game and have proven recurring cash flow.

I don’t doubt we will see some markets take a 10% to 25% haircut, but the banks will not be asking Janet Yellen for capital injections.

Thanks to insured mortgages, required down payments for conforming mortgages are low, lower than selling costs.

There is no “strict lending”. 80/20 loans issued against current bubble valued collateral is not “strict”.

Loan standards are a joke and it’s mostly because of government created moral hazard. It’s strict to most because they have only lived in an environment of lax lending standards their entire life.

As for your data on JPM, this bank and others now large portfolios of garbage quality securities: sovereign, corporate and consumer debt.

There is plenty of commentary on this site about overpriced stocks and real estate.

The bond (debt) mania is the biggest one of all.

Perhaps the housing industry will have Uncle Sam foot the bill for the workforce that might have to be furloughed during this temporary slowdown to the industry. Maybe like the airlines we can pay the people to stay employed while not doing the job. I mean it isn’t their fault the housing market is getting pricked.

Sarcasm ON

Taxpayers are tapped out

3% is my call. They will never let it get to 4%.

Danno,

They’re ALREADY over 4%.

Please RTGDFA :-]

See Wolf how easy that was????

RTGDFA lol

I get moderated for that kind of stuff ….

Hahahahahhahaha

decode that

Read the dadgum flippin’ article?

RTGDFA. Dang. I just spit my Mountain Dew.

Was this abbreviation in the article? I didn’t read it… :)

I believe it is “read the blank blank full article”.

C,

Close. It’s: read the blank blank blank article

Thanks Wolf. Got it on the first guess. A bit of levity that brightened my day.

A friend of mine keeps using WABOFBS, from the recent Dana Carvey podcast:

“What a bunch of …”

Also useful!

Acronyms are a slippery slope that leads to over use of emojis which eventually become kanji then we all turn Japanese.

You state average rates which means that some are more and some are less. My local Credit Union just dropped 30yr fixed from 3.625 to 3.500 after it had gone up the same amount 2 weeks ago.

Still pretty cheap money. Even 4.00 sounds good compared to my 1984 rate of 13.6%, which was refinanced to 7.5%. Of course, I only paid 130K for the house.

Yeah. I remember a couple buddies across the street from each other with Cal-Vet loans really pissed when theirs hit 6%…early 80’s..I guess they were adjustable loans? I was getting close to my homeless days and renting a room from one of them and more financially ignorant than I am now…..which was pre-school level or below.

That 80’s recession was bad….many never came out of it….I was just plain LUCKY.

I did and it gave me a little hope! Waiting is sometimes the hardest thing to do! Thanks for the laugh!

hahahaha!

or $4 [gas]

I sure hope/wish/pray your headline will become a reality but I am also a realist. In SoCal, maybe it will never happen, nothing is going to prick this housing religion short of a Volcker style rate hike (which we will NEVER get).

I am sure I will see countless comments on here reinstating how strong the SoCal market still is and people are still tripping themselves over to pay over asking. If I have one genie wish though, I do wish house price would collapse by 30-40% just so I can see prices reflect somewhat of a reality baseline.

Maybe we will see this kind of price adjustment if we have a “Don’t Look up” moment in the makings or maybe it will just spike home prices even more…it’s exhausting trying to time and understand this insane market.

The entire USA population does not reside in SoCal.

RE prices in SoCal are a local problem.

Although RE prices are local but this time the prices went up all of usa. Not only in all usa but all over the world.

The reason was simple: Yield chasing and availability of cheap money which happened everywhere.

The CBs all over the world have really distorted the market.

True.

Also, hype, fomo, pricing at the margin, complete financial ignorance of normal risk/return, ignoring carrying costs, ignoring income to price ratios… all while waiting for the next dreaming genius to buy a house made of wood, wires, and pipes.

Been said a lot here about the epic day of reckoning coming. There will be a lot of young ones who haven’t seen it all before and are going to get their faces slammed into their own stucco and particle board walls. I feel sorry for this group. They were so misled.

I am in SoCal and have some homes.

I thought the same last time in 2008 ” home prices in socal” would never go down.

Not sure what would happen but people in general socal are struggling although housing market is hot.

Utilities are getting expensive day by day in SoCal and aa lot of homes need fire insurance in san diego where I reside. My friend is paying $7K/year just for home insurance.

It’s gonna be interesting to say the least.

I want to leave socal for other part but need to wait for few more years till my kid graduate from high school.

jon-stay or move, you’ll be seeking water…(left san diego, where my family had been since 1910, primarily for that reason. Thought i’d adequately addressed securing a life necessity, but have seen the annual rainfall rates in what had been the second-wettest area in the state in steady decline since the late ’90’s. Our spring’s still good, but many open ones in the area that used to run dry in July are now gone by March/April due to declining recharge/increased ag&population demand). Good fortune to you…

may we all find a better day.

may we all find a better day.

People oughta consider water and food security more in their house purchases. I mean, Phoenix, what are these people thinking? And have you seen all the jorts there?

The nifty mapping tools on the house trafficking websites have a function to see the aerial photos with pins on the dirt that is for sale showing the topography and green areas. Asking prices have exploded in places like the Cascades where there is always water and a good climate.

The green and temperate west coast area listings usually have historical selling vs current asking prices on rural houses and land attached to the listing. I’ve seen doubles and even triples vs two years ago apparently from country folk trying to sell out to the work from underwear crowd.

Lots of these work from anywhere people will be disappointed with rural life. Both the social ones and the anitsocial ones. Social ones have limited options close in and antisocial ones will be feared in a small town and need to move very far out where internet is difficult and there is no delivery.

i seen the future and it looks like regret.

Agriculture still accounts for 80% of water use in CA. If you think the large urban metros in CA are close to running out of water you don’t understand that water flows uphill to money in the west.

Lake Powell is running out of water. 10 more years of drought, and Arizona is done for.

Happy-have always understood that, but all of the money in the world won’t guarantee previous annual snowpacks in the Sierra, Cascades and Rockies. Will there be enough resources/will/money in the ag AND urban areas for workable amounts of desal (or, gawd forbid, more pipeline projects that assume other area’s water resources are just there for the taking?). That jury has yet to seriously convene, let alone be out…

may we all find a better day.

jon, are you children incapable of adapting to a new school? Have you ever thought that it might do them some good?

> “In SoCal, maybe it will never happen, nothing is going to prick this housing religion short of a Volcker style rate hike ….”

That reminds me of “real estate never goes down” old shop-worn memes.

Short time horizon/sample space there? I bought my San Diego townhouse for $90K starting in 1994. By around 2006 it was around $350K market value, and in 2008-2009 it almost halved to $160K. I was never underwater then. But I paid a big down and had paid steadily before the GFC, so I lost no sleep. Now I owe 2% of its supposed worth. The loan payment is so low, I could beg it standing at a traffic light in a couple days time (all in, tax and condo fees, less than half the expected rent for the same place). So being risk-averse and not trying to pull and foolish financial tricks worked out very well. It would take more than a Volcker-level event to get me sweating. That, with a 4.25% mortgage.

These are not new concepts, and it is not different this time.

We at 4% already DYRTFA?

Congrats anyways, nice job. You’ve been at it a while. Hopefully you can pass some of that on to your heirs.

LOL, I laughed at your new acronym.

I got it on the first try too

You bought before the huge, relentless rise. Please get a grip.

I lived in SoCal in the mid 70s to turn of the 80s. San Diego. RE was a religion then. But if you look at the San Diego chart above you’ll find proof that these markets tank.

Rising rates, rising gas prices (who walks or takes public transport in SoCal?), skyrocketing insurance costs, job related recession…It’s not that hard to envision. Hang in there.

I grew up in Floriduh in the 70s and 80s. RE was always a religion there too. Now this religion is a nationwide cult.

I heard a long time ago that RE is cyclical. Hard to imagine, I know.

Keeping the faith for me involves the understanding that nothing goes up in in a straight line forever. Tends to go to heck.

Your wish will be granted and then some. As reported in “The Great Retirement” more and more American baby boomers will retire. The variants will keep coming and some may be deadlier.

That will cause more elderly persons to retire to save themselves. There will be less demand for a lot of homes, which younger generations cannot afford. However, the price of low to mid-priced homes may not collapse as much. The same retirees will also get out of the inflated stock market, which sooner or later will cause margin calls that will collapse.

…collapse the stock market.

(A cute munchkin interrupted my thought.)

No one and I mean no one knows what the future holds for this virus. Really intelligent people have been dead wrong about the twist and turns of the pandemic in the last two years. But my strong hunch is that we are past the worst of it, and that most people looking to retire because of the pandemic have already done so.

Nope, the price declines have already started at the high end. In 2003 inventory build in rancho Santa Fe took place in the fall. In my area, Cardiff, the peak price was right as the first hike was done. I sold about 3 months after. Mind you, no one was noticing this and the part y was still going on in places like north park into summer 2005 as fools chased the cheaper areas out of desperation. SD was the first out of the gate with 20% appreciation every year after 9/11 when Greenspan cut rates and I believe it was the first to go down. I moved to another state in 2006 and it was still bubble mania there but people just laughed at my warnings. Many got wrecked.

Same question in my mind about South Florida. We are hemmed in here (ocean on the east, Everglades on the West) and the exodus from the NorthEast continues. No matter what people pay for housing here, its always at least 10% cheaper than up North, (no state income tax).

Wondering if interest rates will matter, or whether local dynamics will win out. Middle class being eaten alive down here.

how many of those people were people planning on living in south florida and working remote full time, and are going to be asked to go back to the office on a hybrid schedule?

miami rents are up 30-40%, which is destroying many people. i don’t see how that is sustainable.

The jobs are following the people. When hybrid is required, it will be in Miami, not NYC.

Not even “Volckerism” will work.

Institutional investors are *awash* in cash – which they no longer wish to hold due to high inflation. What I mean is – they don’t need to finance anything at all.

They are buying to rent – mostly with tenant-at-will arrangements , if the Greater Boston Area is any guide – so they can replenish their cash at the prevailing rate of rental inflation.

So, yes, it really *is* different this time. Housing prices will *not* fall. You may see inflation in the housing sector lag inflation in other sectors but, nope, the prices aren’t going to go down.

Regardless of whether it’s 4 or 4.3, judging from the slope of that graph it looks like interest rates are poised to blow through it. Fast. The Fed is always behind the curve so I expect we’ll see >5% rates before the official stats that the Fed follows will even start to show real stress. By then the bubble will be pricked.

1) Didier Sornette : most bubbles decay, they don’t end up in mighty collapse. JP might not need an extreme Paul Volcker act.

2) BCOM 2008/ 2020 prolong calamity.

3) BCOM : NDX might fix JP problems. Inflation might chew up RE & NDX real value.

4) Real stuff vs paper money & Buybacks.

5) NDX weekly is sinking inside the cloud. If the bottom of the cloud don’t hold, it might reach Aug 31 fz.

6) Germany pulled out in the last act, frustrating NG. By year end

NG might erect.

7) BCOM : NDX might rise towards the top of a channel, coming from 2008 top.

8) Thereafter the rising dollar will take care of both.

No, financial Market bubbles do not “decay”. They implode, and quickly.

Well they decay after they implode

False. 2001 dot com bubble decayed over years. Nikkei decayed over decades.

1. The consumer brainwashing from the media, schools, government, etc. Is nauseating. Normalizing $300,000+ for a house, $100,000+/yr salaries for little work , and needing the most expensive gadgets and toys is just wrong and unhealthy.

2. Government entities, non profits, private corporations, and banks are so entrenched in real estate I doubt we will see mortgage rates over 5% again.

Michael Engel,

A scenario you are missing….

There’s a very significant chance that the Ukranian conflict spills over into Poland (e.g. Russian fighter incursion into Polish airspace resulting in it being show down). This could well result in an escalation of the hostilities to a NATO country – leading to suspension of all Russian energy exports to NATO countries. Remember that China will happily backstop any Russian economic losses – and is rather happy to get all the gas via Power of Siberia 2 in the future, anyhow.

Scholz’s Nordstream2 certification delay will age like an already-ripe banana!

‘This could well result in an escalation of the hostilities to a NATO country – leading to suspension of all Russian energy exports to NATO countries.’

In the event of an escalation of hostilities to NATO, exports will not be concern number one. If Russia gets seriously involved with Nato Putin is going to need to keep a very close eye on his own military. There are protests across Russia over the invasion. The retired General who heads the retired officers association has called on Putin to resign. Russia can kick around a small country: Nato would be very different.

Rule by KGB hasn’t turned out well for the average Russian. I expect the assets frozen will soon include all the oligarchs RE in Londongrad. How odd that a country with a lower GDP per cap than Romania has so many buyers in this very expensive area.

US gov constricted oil. ESG & NG destroyed nuke and coal…selling at half prices.

Thanks to their success, coal & nuke will dominate. Their junk, their dumps, pack more energy than NG.

New innovative co will extract energy from today junk.

Follow up.

The housing bubble will likely get pricked but it may not make houses more affordable for most. A significant housing down-turn implies a a meaningful recession. Many people will find the reduced home prices just as unaffordable because their ability to purchase will also have gone down. Partly due to increased interest rates, lack of employment, out of control inflation, etc.

Consider it an universal law: Housing is always expensive/barely affordable. People have to stretch. Looking back 30, 40 years, housing back then now looks insanely cheap. Trust me, it was not. Just an inflationary mirage.

And many of the homes built in last few years are in suburban usa with long commutes.

Combo of fuel vehicle housing utilities and rent all up crushing the consumer driven economy as well.

I thought i read something today about iphone sales are expected to be down in 2022? If true that’s a real surprise.

Ben Sargent,

I concur, especially if there are high new car payments thrown into the mix. And fuel prices look like they’re inevitably going to rise…

iPhone sales down? Apple pushed out one of their “updates” and fried the batteries in my 6S, my wife’s 7S, and several of our friends’ phones. I’m sure it was a coincidence that all these phone batteries took a dump simultaneously – literally within days of each other.

Translates into instant sales as most of us without landlines cannot be without our pocket nanny.

Consider a $20 per month text and talk only plan. Your pocket computer will work exactly the same as it does with a cellular connection. If you need a map download it from googly maps. GPS still works.

Don’t stream, that’s for serfs. Easy for me to say, though. I have about 6 months of consecutive music on the fingernail sized drive on my phone. Slaves rent their music.

Still kind of in awe that I can fit my whole digital life, which for me was from the start of digital, on a few stamp sized cards that can fit in my wallet.

implying that you have a wifi connection at home and either don’t go too far or have access to something like Xfinity hotspots

You should reconsider buying anything else from that evil company.

Jovi,

there is no escaping “those evil companies” anymore. i used to work at the most evil of “those evil companies” and honestly how many people can really escape the clutches of their claws?

google search “the onion google opt out village”

I don’t understand the attraction of the iPhone. I can buy 5 perfectly serviceable android handsets for the price of one iPhone.

” … suburban usa with long commutes.

Combo of fuel vehicle housing utilities and rent all up …”

Replay of 2005-2008. Credit card minimum payments went up, gas prices surged, exurban McMansions were occupied by housing construction workers with new double-cab trucks and pricey granite kitchen work. It all spiraled away. Some of these are the people so twisted with rage now. The euphoria had been high then, savings rate was worse, consumer credit was everywhere and casually handed out and used. Nowadays there are more household capital buffers for the aspiring middle class but that can be eaten up pretty quickly with high liabilities. Like a butterfly causing a storm, faraway financial events can be transmitted to one’s location instantly. That’s thanks to the genuises who connected everything to everything instantly.

Oh yeah, and there were those resets on the mortgages. I don’t know how many adjustable rate mortgages are out there now. Mine started adjustable but was modded courtesy of JPM to a fixed in 2009. I took it expecting inflation, which has finally arrived.

This comment would be underrated if it was rated by our great grandchildren.

These poor frickin kids buying particle board, wires, pipes, and stucco, expecting vast riches and youtube famous wealth from the Potomkin living room they bought in their unwitting facsimile of a Hollywood western ghost town in the sky. .

Cannot know precisely when the housing bubble will be pricked but we certainly know the identity of the p**cks who created it.

Does his last name rhyme with “owell”?

I suppose I could also type out every congressman but that would take too much time.

GSH wrote:

“Consider it an universal law: Housing is always expensive/barely affordable. People have to stretch. Looking back 30, 40 years, housing back then now looks insanely cheap. Trust me, it was not. Just an inflationary mirage.”

I was skeptical about your assertion so I ran some numbers.

Since 2000:

Median household income is up 77%.

Median house sales price is up 147% so deposit required to buy one is up 147%.

PITI for median house is up 72% (mortage rates fell from 8% to 4% since 2000).

I had to double check this since it seemed unbelievable given the 25+% run up in house prices nationwide since the pandemic began.

But surprisingly the figures seem to confirm your assertion about monthly payments being about as (un)affordable as ever (tax breaks are less generous now) but it’s clearly now much harder to save up for a deposit than it was in 2000.

Someone who cannot come up with the measly down payment for the median priced home (my assumption in both posts) has no business buying a home.

If they cannot come up with 3% or somewhat more, they are broke and cannot afford it.

In law relative (cousin) had to borrow $8k from his mom to use as down payment for a house in Porterville, CA.

Pure wisdom there, if you can’t come up with $8K cash, you really have no business buying a home. Then again in the age of house prices will go up forever and ever…borrow money to take advantage of future gains seems to be a win win bet, similar to borrowing money to place it all in one hand in blackjack when you think you will hit 21 no matter what.

Intredasting.

“Looking back 30, 40 years, housing back then now looks insanely cheap. Trust me, it was not. Just an inflationary mirage.”

It felt hard to buy a house then, 30-40 years ago, same as it probably does now, but the current rewards of being there THEN were unimaginable to me at the time.

The rewards of buying property on the old metrics were obvious then but they were based on history and historical returns and math that showed when and how your purchase of wood, wires, stucco and 2x4s would eventually pan out.

Any reckoning of those old metrics has bean massively distorted by now by the helicopter urinators. Now they are based on hype, centrally programmed jawboning and self reinforcing circles of central banks monetizing central government debt.

Living in a nice place is desired by nearly everyone, but we are all limited by income. Saw a nice plot one time that housing plus transportation averages about 50% of people’s income.

It makes sense. It can’t be 90% and why would you live in a slum on 20% of your income if you can afford more.

In a low interest rate environment like now it becomes more about the payment, than the sale price, but high leverage means high risk.

When rates are lower the monthly payment is the same on a more expensive house, but as wages have been stagnant the debt is eroded slower and it’s harder to make a dent on repaying the principal as it is several multiples of your income.

So lower rates do make it far harder.

Housing was “cheap” in much of the country around 2008-2012, depending upon the market.

Prior to that, it would have been affordable by current standards when prices and interest rates were both much lower.

The difference then was lending standards which were actually somewhat prudent. This as opposed to the basement level ones in place for most of my adult life. The ones which many posts have claimed or inferred are “strict”.

I omitted 1960’s. That’s when price-median income and interest rates were both low prior to post GFC.

Augustus Frost wrote:

“Housing was “cheap” in much of the country around 2008-2012, depending upon the market.”

I redid the analysis from 2010- now since that was right in the middle of your “cheap” period:

Since 2010:

Median household income is up 48%.

Median house sales price is up 83% so deposit required to buy one is up 83%.

PITI for median house is up 67% (mortage rates fell from 5% to 4% since 2010).

So that confirms that 2010 was indeed significantly more affordable than it is now.

Of course, that was in a bad recession with widespread job insecurity ….

for GSH:

As a full time student/ part time semi skilled any work I could get at Cal in late sixties, my very nice studio apt with two bridge view was $50 per month and I was getting $5 per hour, so 10 hours a month to pay the rent. Also rented many places in CA and OR for that same ratio then…

Last I heard, my apt was $2500 per month, and ”handy people” were getting $20-40.

QUITE a bit more affordable ”back in those days”,,, eh

Also, very entertaining area to live in. Life was a lot more enjoyable back then.

Great comment. Need to add in the inability to get credit when that cycle runs it’s course – in conjunction with the housing downturn.

When the 30 yr is over the inflation rate…then the “hot” money might stop.

Like in 2006

Yep, 4.0% should put a pin in the “I need an 80%+ mortgage” buyer crowd.

Ok, sorry, I was thinking of domestic real estate.

Chernobyl was not on my short list of places to move. I like the good old USA for lots of reasons.

But that 4.0% matters not a whit for the Institutional Buyers who are doing most of the buying in most of the markets…

And many of the homes built in last few years are in suburban usa with long commutes.

Combo of fuel vehicle housing utilities and rent all up crushing the consumer driven economy as well.

I thought i read something today about iphone sales are expected to be down in 2022? If true that’s a real surprise.

Ben Sargent,

You should add “soon-to-soar property taxes” to that list…

Lots of cities & towns froze assessments in 2020 and were able to avoid raising property tax rates due to generous state-distributed pandemic relief packages. That relief is drying up. Many of those cities and towns have permanently lost large potions of their commercial tax base during the pandemic due to the loss of small businesses. So they will simply have to raise the lost revenue either through municipal debt offerings (which no investor will touch in a high-inflation environment) or through increased property tax rates.

The beginning of the realization that things will not grow to the sky is taking a chunk out of certain markets. Only an across the board slowdown in consumer spending with rates at 0% and inflation at 7% could cause a complete collapse.

Is it a coincidence that the number 4 is nearly homophonous to the word “death” in Chinese numerology? No…. But its an interesting factoid right? Anyone…? No? … Guess I’ll just go back and RTGDFA lol

4 does suck. Associated with death.

But 9 rules and 7 is divine.

I challenge all common core mathematicians to a duel.

Wolf, great article.

I think the idea of leverage comes more into play here. The situation here with the rising proportion of RE purchases by investors now maintaining support for even valuation of the market can spiral more easily if valuations start to dip. Investors in real estate (who also invest in stock market and perhaps corporate bonds) start to feel the heat of a general market decline not just real estate itself. They are leveraged in their own loans and need to make capital to cover other losses (due to the broader market declines) and manage debt interest payments they have. They may also feel the need to cash in on the bubble in RE before valuations drops more quickly. I think the more valuation is supported by investors in real estate, the greater the momentum in unwinding the market and the farther and faster it will fall ultimately. The trigger in this case can be other markets coming apart and the FOMO as prices start to fall to any significant degree (I think many recognize the bubble for what it is).

My 2 cents. Also loved the RTGDFA.

Stop being logical. You will be labelled as a disrupter.

Sorry to break it to you Wolf, nothing is going to prick this housing bubble.

It’s not that the benefits/gains of owning a home have gotten so much better, it’s that the costs and risks of being homeless have gotten so much higher.

HOAs, REITs, and environmental groups have made new construction nearly impossible for anything with fewer bedrooms than bathrooms or a wetbar and walk-in pantry.

Cheap credit has priced anyone without direct access to it out of the market.

The powers-that-be buying up the houses now don’t need to see y.o.y returns on appraisals because they will simply see returns on rental payments.

Unless there’s radically less demand for living indoors, nothing will stop this train.

The only thing that would change this would be state intervention to increase supply and housing programs like we saw in the frontier days or after any war period, but that’s unlikely to happen in a country that’s lost faith in government.

Congratulations.

“…..nothing will stop this train.”

Hahaha, yes, that’s what they said last time.

Ah, but This Time It’s Different.

Permanently high plateau!

Ah, but the Market will Regulate Itself.

Yep, “…..nothing will stop this train.” when all the lemmings find out that they can’t afford houses because of the higher interest rates, in comes Larry Fink and his 10 trillion of investment capital from Blackrock to pick up the pieces. “This train will keep rollin on ….”

Maybe my lexicon is a bit off, but this business of using leverage and borrowing dollars cheaply to invest in higher-returning assets, seems in ways like a carry trade. If it is, it is regarded as “picking up nickels in front of a steamroller,” or akin to selling insurance. One collects the premiums steadily until an adverse event forces the conditions to reverse, and then the losses can be fast and ugly.

There is a glaring error in this reasoning. Many baby boomers have sadly remortgaged their homes to cover the inflation on a fixed income. Many houses not paid off and suspect to higher taxes. Social Media accounts are littered with parents moving in with kids and losing their “legacy” over misunderstandings on “reverse mortgages”. I doubt investors will buy all of these houses. Only time will tell.

“Larry Fink and his 10 trillion of investment capital from Blackrock”

Swamper, come on, man. That $10T is client-driven money, mostly in index or lightly actively managed funds, etc., like iShares and giant ERISA pension funds. It’s not like BLK can decide to take a half trillion or whatever and buy up a ton of homes. I’d bet the most they could get on board for a residential RE fund would be in the low billions, and it would take a lot of work to set up and manage that fund.

However, there are entire PE outfits that specialize in running SFH funds. They’re pretty small, too, because it’s hard to manage scale when renting out houses.

100% correct.

Institutional Investors like Blackrock are dumping their dollars like they are going out of style (which is true) and buying homes to rent them.

They don’t NEED to finance anything. Mortgages are a convenience, not a necessity.

Inflation in the housing market may well be outstripped by inflation in other sectors – but, yes, it really is different this time. And not in a good way.

Wanna bet?

Last time, as I laid out, the conditions were different.

If your theories don’t adapt for new information, they’re hardly theories. More like dogma.

Chris,

In all your trolling on my inflation articles last year (under different screen names), you were so ridiculously wrong it was just funny, and you have been proven wrong and wronger with every CPI release along the way until you finally gave up. So now we will see about your current claim…

“Last time, as I laid out, the conditions were different” = This time it’s different: the most expensive words ever spoken.

I’d advise to read up on the 18 year real estate cycle. This will illustrate the boom and bust nature of land prices since 1800 in the USA. The ups and downs correlate with the credit cycle. When this current cycle shuts down there will be a lot of scrambling.

It can’t be a bubble because:

1929 stock market: It’s stocks not tulip bulbs

2000 dotcom: It’s IT stocks not industrial stocks

2005 housing market: It’s hard assets not stocks

2020s housing market: It’s fixed interest not variable

Pure wisdom dispensed daily. Real estate prices are going down.

For those of you who are profiting from the crash by using SRTY and SQQQ, Putin’s invasion of Ukraine (it appears to me to be the end of his political career based upon the reaction on the street in Moscow) is a black swan event and it is time to take some chips off the table.

Just buy back a larger position on the rally.

In this sort of inflationary environment there is little-to-no chance that housing prices will go down.

The rate of increase in housing prices may be slower than the rate of price increases in other sectors of the economy – but they are most certainly not going to go down.

As for Putin – he’s playing a much lower-risk game than many seem to think given China’s willingness to backstop Russia’s capital accounts and the sheer-impossibility of replacing his countries energy exports.

I wouldn’t mess around with SRTY and SQQQ – but the brave among us should certainly take a look at LETRX given that Western sanctions will likely fly as well as a concrete airplane over the long haul…

It is regional. Some area will drop and some will not.

I was talking to a friend who lives in Austin, TX. I live in a state in flyover. He bought his house in 1999 for $300k. I bought mine for $184k.

Same size house. Built in the mid 90s. His house is worth 1.21million. Mine is worth $360k.

My house is up 100%. His is up 300%. My house has appreciated at 3.09% YOY while his appreciated at 6.06%. No bubble in my city. Now his house might drop some but his house rose so much because of all the tech money that is moving into Austin and they are still moving in.

“It is regional. Some area will drop and some will not.”

That’s precisely what most everybody thought and said, before the GFC in ’08. That was precisely the surprise that blindsided most people: for the first time, the newly cross-linked credit and real estate markets correlated and fell everywhere, from Spain to California to Texas. What happened was a liquidity and credit crisis that swept across all locations, real estate markets and the financial world, corporate and personal. There were a few exceptions but they were outliers. A strong enough swirl will take almost everyone down the drain.

I agree. But some areas have appreciated much more than others. My house dropped about 5% in GFC and by 2013 the price was right back to where is was before the GFC.

Sure, a couple of houses in my neighborhood were foreclosed on and if you were lucky to get one of those, ( I tried by offering 15% below market value but that was too low), you could get it for a 10% discount. It seemed like relators where the ones scoring the foreclosed deals in my area. They never hit the MLS.

Worst case scenario in my area, I think I will see a 5% drop. Other areas…just like GFC….could see 30%.

Just remember, the charts wolf posts (which are great!) look bubblicious. But they are not adjusted for inflation. So in reality, it is not as bad as it appears.

Doug Short (Advisors Perspectives web site) has a lot of charts in real and nominal values. Since 1990, housing is up 267%. Guess what, CPI inflation is up 95% Housing adjusted for inflation is up…..89%. Interstestingly…this means current housing is priced about right.

He has another chart that compares zillow housing index to inflation. When adjusted for inflation, the price of a house today is at the exact price as 2006 dollars. $325k

Was 2006 a bubble…yes. Is this bubble bigger….probably not?

Exactly! Also, would the % drop during GFC be the right measure?

1. This bubble is bigger

2. Rates are yet to rise

3. Inflation

4. QE was started in 2009 whereas it is now QT time

A bigger drop may still keep it in bubble territory.

ru82, isn’t “adjusting housing for inflation” double counting?

ru82 you are going to get your fingers slapped by Wolf when you say that the Case Shiller HPI charts are “not adjusted for inflation”.

Those charts ARE a measure of inflation.

Wow, now even I HAVE TO SAY THIS ON BEHALF OF WOLF

RTGDFA!

Peanut Gallery,

Hahahaha, thanks!!

Eventually even the dumbest Cal refugees will wake up and realize that Austin (unlike SF) exists in the middle of an ocean of buildable land (well, not to the west, were some CA-flavored highly suspect baloney pertains).

Still, drive 20 minutes N, S, or E and there is a *huge* supply of raw land.

It is hard to build a forever bubble in the absence of restricted supply, in the dawning era of work from home.

Right now the cash engorged Cal refugees are in the “drunken sailor” phase that comes from halving housing costs…it won’t last forever.

Paying half for something that is 4x overpriced is still a mug’s game…but it doesn’t seem so at first.

Austin got Portlandiated.

I can’t imagine that any city (even Austin) in Texas would get Portlandiated…

Is there open drug use and violent crime rampant in the streets? Do you step in human feces and urine wherever you go?

I doubt it

Peanut Gallery,

There was when I lived in Austin (1980s). I could see the homeless encampment from my apartment, along with drug dealing, etc. It just wasn’t downtown.

In November, I went to Tulsa (where I also used to live) and stayed at a hotel downtown: homeless people everywhere.

All cities struggle with it. But some cities push the homeless into areas where you cannot see them when you drive by on your way to work and so you think they’re not there.

Port St. Lucie, FL is considering mandating circular driveways for all their houses. Sure looks like they support affordable housing going forward.

That’s nothing.

Parking a pickup truck in your driveway in Cape Coral, FL (aka cape coma) in the late 90s and early 2000s would earn you a parking ticket. It was illegal to park a truck outside.

No joke, seriously, I’m not kidding. At the time it seemed so absurd but it went on for years.

What if there had been an insurrection of pick-up owners in that time that left their tucks in their driveways in protest?

Intredasting.

Carbert 8hr,

Here’s another one for you.

As recently as the early 00s….parking *ANY* out-of-state commerical vehicle in *ANY* legal, public parking space in Providence, RI would earn you a parking ticket. I’m not joking.

The other side is that few people want to see a half dozen crappy cars + tons of junk in their neighbor’s driveway (in a 3-br house occupied by 8-12 people).

Agree that the circular driveway mandate is draconian. There is a middle ground; the trick is in finding it.

Chris,

I have been seeing good innovation as entrepreneurs realize there is a need for low cost one bedroom housing. I hope it continues.

Biggest obstacles are rigid housing codes, but as the need gets more severe some state and local governments are becoming more flexible with the codes. It’s better to have someone living in inexpensive housing than being homeless.

I’m anxiously waiting for SoCalJim to add his take here.

AA-he was so upset with the comment tenor last time he was here, i think he might be contemplating my advice that he start a blog of his very own…

may we all find a better day.

It must be lonely being SoCalJim

In the first 1/2 of the 90’s, SoCal RE lost approximately 15% of value. This was primarily due to a recession. There was no exotic lending and no significant inflation in that era. A recession, alone, can and likely would produce a sizable dip in sales prices. If you couple a recession with a stock bear market, that sizable dip probably gets even bigger.

In the end, someone with a pen in hand must sign on the line which is dotted to close a deal. Once consumer sentiment flips and is benign to negative toward housing, look out. It’s happened twice in about a 15 year span in SoCal. It will happen again.

“A recession, alone, can and likely would produce a sizable dip in sales prices.”

Yes, exactly.

The longest expansion in history was followed by the shortest recession.

Lots of homebuyers (consumers generally in fact) seem to be behaving like they have total job security and there’ll never be another normal length recession ever again ….

Ok, sorry, I was thinking of domestic real estate.

Chernobyl was not on my short list of places to move. I like the good old USA for lots of reasons.

I think of RE as a long term investment. So it goes up a lot and then goes down a little. You still make money.

Where has real estate lost value relative to 20-30 years ago?

Plus you have to live somewhere.

“Where has real estate lost value relative to 20-30 years ago?”

There used to be answers to that trivia question a few years ago e.g. Japan, Detroit etc. After the pandemic craziness I’m not sure if there is an answer any more.

How about Chernobyl?

RE there might be worth less now than it was 35 years ago.

“How about Chernobyl?”

San Diego could be that if one of the Kims or their ilk gets big ideas. We are one strike away from being a glass lake. Lots of Navy here. Cornerstone of the Pacific fleet.

Tokyo condos have surpassed their previous peak valuations.

Real estate outside of the big cities in Japan, unless it is something special, have not regained or even come close to the previous top. Most people never sold or engaged in real estate speculation in the country areas either.

Rents vary by a huge amount even in the big cities in Japan and overall I would say for the average person they are much cheaper than rent in the USA.

Young people in Japan have a much better chance to get ahead than in the USA as there are many jobs and the cost of living can be much cheaper. University education is much cheaper too.

It’s an investment if you can afford to hold onto it and generate rent. It’s not if you have to sell during a downturn and lost money on the house

Lisa,

Yes, that’s good reasoning And you are right to provide that particular qualification.

We are going to see a huge surge in property taxes in the USA very soon. Truly seismic stuff. I honestly articles about homeowners having to take out HELOCs to pay their property taxes will be front-page news in the next year.

“We are going to see a huge surge in property taxes in the USA very soon. Truly seismic stuff. I honestly [think?] articles about homeowners having to take out HELOCs to pay their property taxes will be front-page news in the next year.”

ah! yes yes yes, Big Al… this stood out in red flashing lights like a true prophecy. interesting… no: FASCINATING.

x

That is a good observation. RE is a long term investment.

It seems like before 2000, housing rose steadily growing slightly faster than inflation.

After 2000, housing went into massive boom/bust swings.

It is true today that Real Estate has gained value relative to 20-30 years ago before 2000.

Given the sharp increase up to 2006 and then the steep plunge until 2012, I don’t know with today’s market whether that will always be true. However, on average, the price of houses steadily increase.

If the market does crash again, it will likely be below the 2006 peak if history repeats itself.

We’ll see in 2026 if the price of housing is higher or lower than the 2006 peak 20 years before.

The peaks are higher and the valleys are now lower.

Where I live we don’t tend to have the big swings in the housing market. Last 18 months has been an exception.

Was thinking about my parents home, built with mostly local materials in 1954 for about $11/ sq.ft. I would guess average labor cost in the house was about $1 per hour.

It’s in this way that housing can be an inflation hedge over the long term as it can’t be rebuilt with the low labor rate for materials or assembly labor.

Old School,

Yes, this is how home valuation grew before 2000. CPI inflation.

The boom/busts used to be local and now they have become US wide.

As an interesting experiment, I took the CPI inflation adjusted dollars and applied it to Wolf’s excellent chart above for San Diego. I used the 2002 value since the data does not go before 2000.

San Diego Median House value

From Wolf’s Chart:

2002 – 125

2006 – 250

2012 – 150 – Note this number

2022 – 375

Projected value of the home based on an online Inflation Calculator from the 2002 value

2002 – 125

2006 – 140.08 – Huge deviation from at the peak.

2012 – 159.53 – Close to inflation growth. Compared to 150

2022 – 195.35 – Huge deviation from inflation today.

In summary the home values in 2012 had returned to the normal or mean inflation growth. 2012 wasn’t the bottom of a crash, it was a return to the times before massive speculation drove house values into a bubble.

If I look at my house value, it follows the same pattern.

I also looked at the US housing data and it also follows the same pattern.

All of these fairly accurately predicted the bottom in 2012.

The bottom is the return to the mean.

The inflation adjusted house value from a value before 2000 should give you an accurate estimation of a house price bottom.

If we have another crash, I would use this to predict a bottom.

The data now shows that housing prices would have to fall 50% today to achieve the inflation mean in San Diego.

However:

If the Fed drives inflation at 10% per year for 5 years and housing prices remain flat, then there would not be a large drop in price. Maybe this is part of the Fed plan.

This for OS:

Not sure where you were seeing $11/SF in ’54, but that sounds high for the parts of FL I was working in from then to mid sixties.

Best houses in Port Royal subdivision of Naples area were costing $12.50/SF in early sixties.

I was getting $1.25 as helper/apprentice, journey level was getting $2.50, and lead guys $3.50.

That was construction cost only, not including land, utility hook ups, etc.

I knew a fellow that was a newly minted realtor in the SFV in the early 90’s, and remember him telling me how completely dead it was, and as you stated that was under rigorous loaning practices.

That said, back then you only had regional bubbles, not the whole shooting works of every developed country playing along!

15%??? Pffffffffffffffffffffffft. It was much more than 15% value decreases during the RTC/S&L Crisis. That was the worst period I have seen in my life. Buyers under-contract were coming to closing tables with banks and demanding further price concession. No concession; no close! The bank’s broker would re-introduce the property to market and almost inevitably they ended up unloading the property at a lower price. Closing table haircuts became the norm.

I dont disagree with your conclusion though. The offset between r.e. prices and lack of real wage gains has to be realized at some point and my guess its not huge wage gains.

BTW, my son is again negotiating with a new employer and the salaries, benefits, etc., are UNREAL as in totally mind-boggling.

“It’s now inflation that is hammering Powell on a daily basis – him who’d made a fool of himself calling this monster he’d unleashed “temporary” when everyone already knew that it would spiral higher.”

And this was after he’d already foolishly promised literally years of ZIRP back in the spring of 2020. As if he could know what interest rate was going to be appropriate years into the future. The most reckless use of “forward guidance” by the “most reckless Fed ever”.

the man is a complete clown. i’ve never seen such a poor public speaker put into such a high position of power before.

It is idiotic to put important decision making in the hands of those who incurr no consequence for being wrong.

In a system that boasts “checks and balances” who “checks” the Fed?

And if it is Patriotic to pay your taxes, what exactly is the intentional debasing of the nation’s currency by the Fed? A patriotic race to the bottom?

There are checks and balances.

The Fed has to report to Congress on a regular basis.

The POTUS nominates Fed Governors and Chairs and the Senate confirms or rejects them.

The problem is that Congress and the POTUS do not appear to be holding the Fed Chair and his co-conspirators accountable for their failings and misdeeds.

Ultimately Congress and POTUS will be held accountable by the electorate for their negligent Fed supervision.

“The Fed has to report to Congress on a regular basis.”

Green energy, climate change, gender makeup of the Fed…did they mention women’s soccer?

If the Senate Banking Committee is indeed the overseer…..

Where was the “are you holding to your mandates?” question from ANY of the Congressmen?

The Fed admittedly promotes a 2-2.5% inflation tax on the PEOPLE of this nation….and the Committee doesnt say, “Hey, wait a second.”

Would a 2-2.5% inflation tax on the holders of dollars pass a Congressional vote?

Yes – of course you’re right – that Committee is a disgrace.

But we the people should hold them accountable and throw the bums out.

“But we the people should hold them accountable and throw the bums out.”

That’s not gonna happen because the vast majority of voters will not vote for anyone other than the bums in their own party. Even most “independents” lean heavily to one of the two major parties. So there are only a small fraction of voters that would actually throw the bums out if they got the chance (which the major parties prevent being given to them).

Maybe it would be better to just let the corporations directly run national/state/local governments, instead of them wasting all that money buying politicians and promoting wedge issues that control cultural values. Then people could just vote with their feet — move and affiliate to the corporate jurisdiction they preferred.

Like on crook making sure other crooks are accountable hahahahaha

The everything bubble will eventually act in unison and descend with the stock market. The stock market has just barely started its descent. By the end of the year there will be shear panic with holders of bonds, stocks and real estate trying to unload their holdings wishing they had never been so greedy.

I haven’t heard a central banker say “we’ll do whatever it takes” for a long time.

It’s what they don’t say that matters. It’s the gibberish they say out loud.

I say 6.5% 15yr (no points – haha).

Sounds reasonable. That would certainly wake some people up. Markets can fall and people still survive with some bruising

A lot depends on inventory. If it stays super tight as it has been then there may not be much price relief for the housing market.

Max Power,

Yes. Nobody is going to unload their highest-value hard asset in these inflationary times unless they need to or are certain they can move to a different part of the world where inflation is not a consideration.

The number of buyers and number of sellers is declining – but the rate of price increases has barely cooled if at all.

As the saying goes it’s a recession if you have a job ,with no job it’s a depression,history

It’s a recession when your neighbor loses his job. It’s a depression when you lose yours.

Mud

Whan your neighbor loses his job it’s a recession.

When you lose your job it’s a depression.

Yeah, despite all the technological innovation, we should use hunter-gatherers as your measuring stick and be happy with any increase whatsoever! You know, because “the elites” are the ones that invented electricity, modern medicine, and all the things that we are grateful for. Wtf?

typo: *our* measuring stick

“hunter-gatherers” is an exaggeration. How about circa The 1800’s?

The U.S. is the 12th highest in the world with an obesity rate of 36.2%. Canada is 29.4% per World Population Review.

I think your number of 2/3 is highly suspect.

I live in the midwest. I am really not worried about the price of my house dropping anymore than 10% at the most.

I bought my house in 1999 for 184k. It probably can sell for $360k now. This come to 3.09 YOY appreciation. Typically housing appreciates on average 1 to 2% more than the inflation rate. Even though the price has risen $100k in just 4 years from $260k to $360k, which is an 8% a year gain the past 4 years, the price is about right where it should be versus inflation. In 2009 it only dropped from $220k to $210k or about 5%.

Prior to this big run-up the past 4 years I had calculated my house as appreciating less than 2% a year. It was undervalued. It was actually frustrating to see other areas shoot up in price.

My wife says we should sell and then buy when the bubble pops. I say what bubble. It is regional. Sure, houses in my area are selling 10% over asking with no inspection, etc. But I think houses in our neighborhood are not in a bubble. Housing is selling barely over $125 sq ft. No way can you come close to build a house at $125.

The city is always listed in the top 100 cities to live in an was listed as a top 20 safest city.

So no worries here. Maybe that is why a company from India is buying up a lot of properties?

> “My wife says we should sell and then buy when the bubble pops.”

I like to trade securities. I do not cash in my shelter for chips and expecting to hop back to the table. But circumstances do differ. What I cashed out was my now ex-wife. Just before my house value (I held onto) zoomed into the stratosphere. The foregoing is to be construed as professional legal, financial, or lonely hearts advice.

ru82, where in the midwest?

Lively crowd here and a great site owner. Just tossing out a bone to chew on.

I took your bone and buried it :-]

It was an off-the-charts-unrelated comments-thread hijacker.

Mortgage rates already over 4% and the 10 year is around 2. Does the FED even need to raise rates. Jawboning seems to be working. Just like in 2018.

Maybe they do one token rate increase so it looks like they not lying?

RE bubble wich popped in 2008 was much more fun.Remember “Lost another one to Ditech” ads circa 2004 where fat guy throws paper airplanes ?

Its the only reason I keep my old VCR-to watch those BS RE ads which I lovingly recorded.

My favorite RE ad plays the slightly modified song of DD Sound “1-2-3-4 Gimme Some More !!!”

4 bikini-clad girls dancing in the background & goofy idiot signing papers w/o reading (which cute RE agent pushes under his nose).

“I met you here it was a closing night

You looked so pretty and I felt alright

You′ve got me signin’ to a disco beat

But really baby it′s a love that I need”

And what do we have now ?

Army-on-the-march of cash buyers buying $1M shacks w/o even bothering to look at them.

Art is dead my friends.

We still have Jim Cramer.

In 2010-12 my company reimbursed me first $40 of motel bills so I usually stayed at Motel 6.Nothing fancy, new furniture etc.Abject luxury compared to Army barracks 😀

Then all of a sudden eviction wave hit and there were numerous motel rooms occupied with families with kids.Because only major cities have shelter system where one may check in & get 3 hots and a cot.

So I switched from Motel 6 to Super 8,paid $20 extra of my money but did not have to look at all those failed “homeowners” or step over the kids sleeping in front of my room.

Once I overheard one family complaining about non-working A/C.Hotel clerk told them “Beggars are non choosers.Be grateful for having roof over your head – paid by the State of…”

Brent

Oh interesting. Those motel nights for those families were state funded?

@Peanut Gallery

Back then I read in local newspaper that a large chunk of State highway funds was diverted to house evicted families.That State was in the South East.I will say no more.

Also,according to my observations:

IF there are 5 Motel 6 in the area charging respectively $45,$42,$39,$37 and $35 per room and

IF you choose $35 room trying to save a couple of bucks

THEN you’ll meet a couple of former jail birds housed there.In no time they will be your best friends trying to borrow $5 😁

8 or 10% inflation is a real possibility. That said 5% interest on a .4 or .5 million starter home should not be a problem if the proud owners eat marinated cardboard and share ride in a wheelbarrow. After all we are heroic consumers. The heroic, patriotic consumer will not be deterred.

I think I may know why foreigners may like to invest in U.S. real estate. I was reading that in some of the European countries, you have to pay tax when you buy a house.

In Belgium, I read the cost of purchasing a house is a follows. The seller will have to pay the relator 5% , then the buyer will have to pay a tax of 10% to 20% depending if it is an old or new home.

i.e. So in the U.S. if you buy a 400k house, you will have to pay about 2.5k closing costs. The seller pays the 6% relator fee.

In Belgium, the seller pays a 5% relator fee. The buyer has to pay a Registration or a VAT tax depending if it is a new or old house. Anyway, an old house will set they buyer back 13% to 16% and new house 22%.

From my understanding, if one is buying a $400k house in Belgium it would set the buyer back 84k just in taxes. You need 20% price inflation just to break ever. I think this is the case for other Euro countries.

So if you are a speculator, I am guessing American and Canada are good places to buy real estate.

It easy to leverage with only a 10% down payment and if thing go bad, you are only out the 10% plus the closing costs. It is easy to walk away. If you ar a foreign buyer you do not have to worry about your credit score getting hit. LOL

If the house goes up 10%, you could actually be up 50% to 100% on you down payment investment.

Why not buy houses in the U.S.

“I think this is the case for other Euro countries. ”

what I know for sure: in Finland you only pay 4% tax for SFH and 2% for condo. And first-time buyers under 40 are exempt.

Let free markets be free. Why bother intervening and selectively tax people?

One thing many are unaware of is that property taxes are significantly less in Europe. (All of this, of course, varies by country.) For example in Ireland, one might pay .18% which is considerably less than the 1.38% paid in my California neighbor hood.

Judging by the FRED Case-Shiller graph for San Diego, the prior peak took about 2 years to peak from when appreciation began to slow (i.e. from the point of greatest price slope). If history repeats, we’ve still got some appreciation and time left, albeit slower, before we see declines. And assuming the Fed doesn’t U-turn.

For entertainment only.

1) By Fri close SPX and NDX will be officially in a bear market.

We don’t need Claudia Sahn Fed best bear indicator.

2) We will stay there, in a bear market as long as it take, until proven otherwise.

3) Next week magic #9.

That didn’t happened for SPX & NDX during the Feb/ Mar 2020 plunge.

4) From volatility to tranquility. SPX might start a bear market rally

that will last several months in a low slog up.

That will slow Case Shiller thrust.

5) The CPI will cont to accumulate. The demure Fed will raise rates.

The 5Y/ 10Y might invert.

6) Putin will cont to aggravate the Golan Heights.

In 2007, I finally went into a Countrywide out of curiosity and was told I could put anything I wanted down as income. That convinced me once and for all that the bubble was about to pop. When interest rates were rising then, people could fake more income on a NINJA loan. The same is not true this time.

People know what they are qualified for, and at the bottom end where first-time moderate-income homebuyers compete, a rise from 3% to 4% now means at least 10% less base mortgage purchasing power before the taxes and insurance. No garbage lending makes up for that this time. That alone should slow things down because housing inflation has that group bidding at their maximum already. Only high-income/asset buyers have the luxury of deciding what price range they feel comfortable with. They can also afford insane rents better and wait it out.

Renting in desirable locations is now incredibly hard and expensive, thanks in part to remote work. Even if housing sales decline or rates go higher, I don’t know how that will get much better.

Which areas are you finding rents to be difficult?

Saw a funny quote: “If your portfolio is down 10%, please stay calm and remember that it’s actually down 17.5% after inflation.” :)

Gold and silver jumped on the invasion bees and cryptos tanked hard. I don’t think that was supposed to happen to cryptos as they are a store of value.

Well, maybe they will go tomorrow?

Interactive Brokers didn’t let my trades go through for Gazprom. Had a limit in for 135 that should have hit and now apparently it’s back up to 190? UGHHHHH

Trading was below 135 for several minutes and not executed while the market was not halted. Does anyone have any experience with that sort of thing … is it possible to be reimbursed / make them eat the loss (loss of profit)?

PS there was a trading halt and the order was cancelled right before trading resumed. Does anyone know whether “Good till Cancelled” vs “Day” makes any difference for that?

Maybe you can file a claim with FINRA, although I am guessing there is some small print in a contract that allows them to not execute an order.

The World just changed. ( morning of 2/24/2022)

Recalculate EVERYTHING

There should be a flight to safety so treasury yields should drop significantly taking mortgage rates down with them.

OTOH, energy prices will spike pushing inflation close to double digits.

Unclear what that might do to Fed rate hike and QT plans.

Brent and WTI up 8+% already

With Russia driving up oil, and Joe working hard to shut down oil in the US, the Fed will have a small window for rate increases as we dive into recession.

Talking heads on cable….Fed cant raise…they say

SO, inflation runs hot….unaddressed…..

Savers lose and now investors double losing…(inflation and market losses)

The Fed has set this table, and Putin exacerbated the meal.

And Powell continues to deny Quantitative Monetary Theory…not connecting the bulge in money supply with inflation. Willful ignorance.

If paying taxes is Patriotic, what exactly is destroying the buying power of the nation’s currency?

SPY -1.5% QQQ -1.2% … markets rebounding / shrugging it off pretty well

I was pretty lucky and had a 100K in a gold miner. It popped about 25% above my buy price in one day last week. I sold 60% of my position thinking Russia was bluffing. It’s going to pop again today and I will probably sell out more or maybe all of my position today. You can never play these events just right though.

Old school,

Don’t feel too bad….

Gold miners are tricky….you need to keep a close eye on where there mines are located. While they are often a useful inflation hedge…there is real geopolitical risk there, too.

If the USA/West is perceived as losing influence on the world stage…lots of precious metals mines could be appropriated by unfriendly governments. Or they could become the target of sanctions.

I really don’t think the Western games of sanctions will work – and I am building a position in LETRX.

1) Crude oil futures reached $100, NG futures near $5.

2) SPX monthly : Feb 2022 low is a lower low, under Jan 2020 low. Feb is a setup bar.

3) SPX might dip lower < Feb low, to form a trigger.

4) SPX monthly flipped in Feb 2022. We have never seen two big red supply bars like that before. It might start Jeremy Grantham road map to hell.

5) But, SPX monthly might rise to magic #13 in mid year, instead. It will cancel Grantham major depression countdown. After all, he is an old British gentleman !

6) SPX monthly is still bullish, yes. SPX weekly and daily are in a bear market.

nah, not yet. the dip buyers swarmed in this morning. nasdaq went from 3% down to only 1% down.

Bitcoin at $35,500 paints a confused picture… can anyone add color?

Inflation and interest rates that are near zero are the best friends of Cryptos.

If we are leaving that condition, Cryptos suffer…

BUT….

Now the mantra is that the Fed can NOT raise rates…even the paltry 1/4pt.

Those are my “colorings”.

Are Cryptos a “fear” play? Gold seems to have broken out here.

Cryptocurrency – apart from being a last-resort in desperate places like Afghanistan – remain gloriously-disconnected from the real economy. For the present they are nothing more than Anarchocapitalist fan fiction!

…except for the enormous burden that crypto mining and blockchain transactions place on the electricity grid. So, actually, the are accretive to inflation.

John H.,