Unfinished supply is amassing in the pipeline.

By Wolf Richter for WOLF STREET.

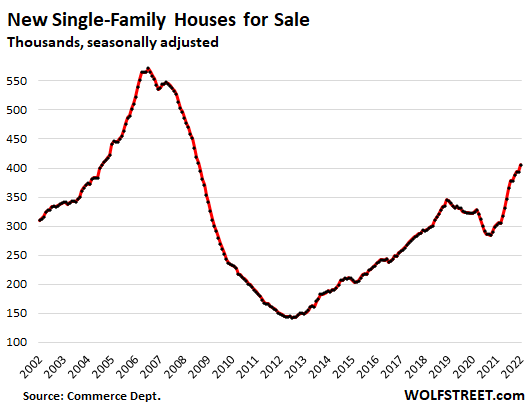

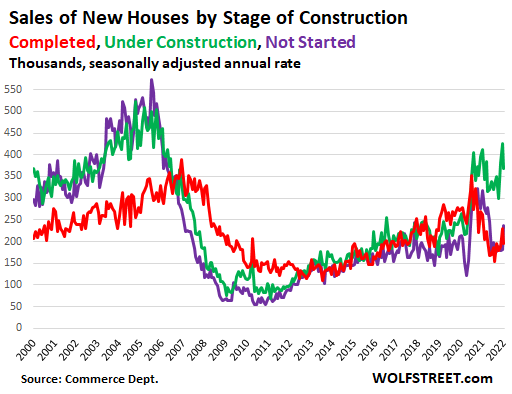

Amid shortages of materials, supplies, and labor that caused construction projects to get bogged down, and struggling with a historic spike in costs, homebuilders have amassed 406,000 single-family houses for sale (seasonally adjusted) at all stages of construction, according to date from the Census Bureau today. This is the biggest unsold inventory since August 2008, up by 69% from a year ago, representing 6.1 months of supply:

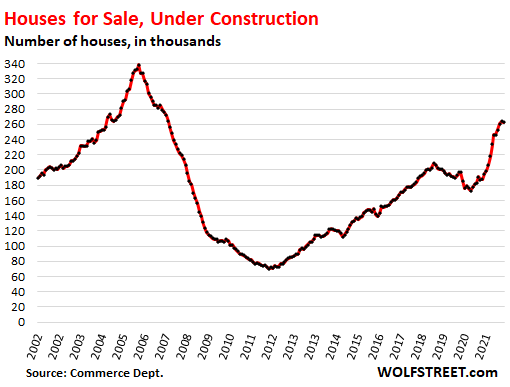

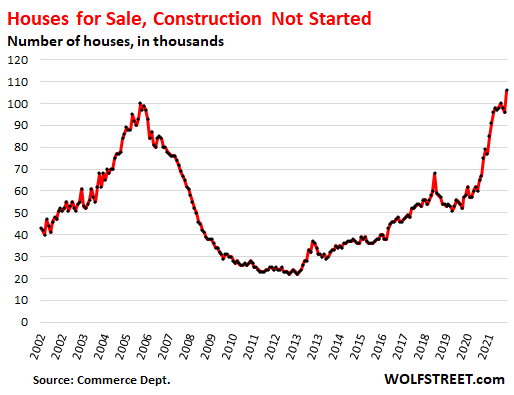

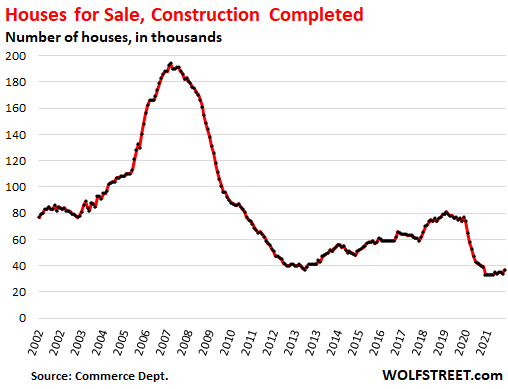

Massive supply in the pipeline, by stage of construction.

Under construction: The number of houses for sale in January that were still under construction was essentially unchanged from December, at 263,000, and both were the highest since August 2007. About 46% of the houses sold in January were in this category; more on that in a moment.

Construction not started: The number of houses for sale where construction hasn’t started yet jumped to 106,000 in January, the highest in the data going back to 1963, as homebuilders – seeing a red-hot market – are piling on new development projects. Nearly 30% of the houses sold in January were in this category.

Completed houses: The number of completed houses for sale ticked up to 37,000 houses, still bouncing along the lowest levels in the data going back to 1963, as homebuilders complain about shortages of all kinds that stall projects and prevent them from completing the houses. When unsold houses are finally completed, they sell quickly. Only about 24% of the homes sold were in this category:

Sales of New Houses, in Total and by Stage of Construction.

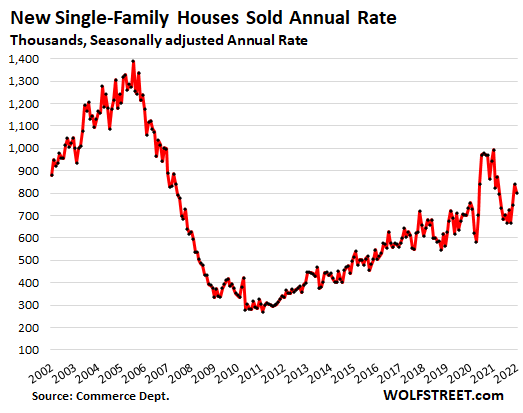

Total sales of new houses in January ticked down to a seasonally adjusted annual rate of 801,000 houses, down 19% from January 2021 but up 6% from January 2020. Sales are far below the boom years of 2002-2006.

Multi-family buildings and towers experienced a construction boom over the past decade, but they are not included here.

Sales of houses under construction fell to a seasonally adjusted annual rate of 368,000 houses in January, from December’s level, which had been the highest since April 2006 (green line in the chart below). As a percent of total sales, under-construction houses ticked down to 46%.

Sales of houses where construction hasn’t started yet – that the homebuilder will build for the customer – jumped to a seasonally adjusted annual rate of 237,000 houses (purple line). Their share of total sales rose to 30%, about the middle of the range of the past decade.

Sales of completed houses fell to a seasonally adjusted annual rate of 196,000 houses (red line), down 29% from two years ago, as inventories for sale remained near record lows, and there weren’t many completed homes to sell. The share of completed houses as a percent of total sales dropped to 24%.

Note how sales of homes that were still under construction are now dominating (green), as builders are facing eternal lead times to get what they need to finish their houses, ranging from windows and bricks to garage doors to appliances.

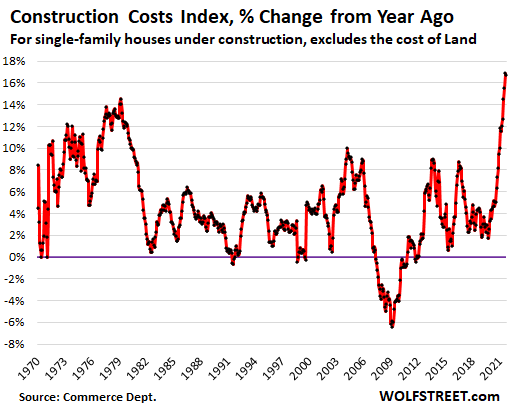

The construction-cost mega-spike.

Construction costs of single-family houses – excluding the cost of land and other non-construction costs – spiked by another 1.1% for the month and by 16.8% year-over-year, according to separate data from the Census Bureau today. These year-over-year cost spikes in January and December were the worst in the data going back to 1964.

Passing on the mega-spikes in construction costs, plus some…

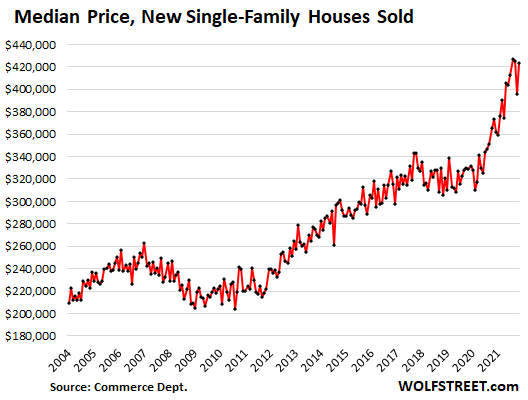

The median price of single-family houses sold in January undid most of the mix-based drop in December, and at $423,000 was up 13% year-over-year. And as big as that increase seems, it was down from the increases in the 20% to 23% range that prevailed last year through November.

Enabled by the willingness of homebuyers to pay whatever they can afford to pay, homebuilders are able to pass on the spike in construction costs, plus some, to book massive profits: The largest homebuilder, D.R. Horton, booked a massive record profit of $4.2 billion in 2021, up 162% from its 2019 net profit. The spike in median prices at elevated sales volumes shows how:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As someone still awaiting approval to build a house for ourselves (not spec)….ouch. And it’s already been 13 months in the approval process, probably 4-6 more to go. Bureaucracy has been expensive.

Gattopardo

Better hope the builder doesn’t go bankrupt before starting to work on the house.

My sister and her husband have been waiting a year and might still have another year’s wait to get their place up. The builders are overwhelmed. So now they’re ‘temporarily’ living in a 5th-wheel RV.

To sweeten the deal, maybe they could throw in an unfinished new car!

Chip shortage just got worse…

“Enabled by the willingness of homebuyers to pay whatever they can afford to pay, homebuilders are able to pass on the spike in construction costs, plus some, to book massive profits.”

I hope there’s some integrity in the free-enterprise process. That is to say, I hope the appliances they’re installing are top-notch, I hope the windows don’t crack with extreme temperature changes, and I hope ordinary people can build a life there.

Appliances and windows are now whatever the builders can get. Builders are furiously looking for alternatives when their chosen brand isn’t available.

Maybe they should band together and start appliance and window companies?

Those are not brain surgery rocket science to make.

Builders around here in normal times put the cheapest s$it they can get away with into the new homes. I’ve noticed a few new homes on my block with multiple trucks and contractors working on the houses after the owner has moved in, just to correct all the defects in the original construction. And now with the shortages the quality of materials and appliances has gone from bad to worse.

For example, I had a local windows contractor provide me with a live demo of how these cheap windows leak heat and said that most home owners would come out ahead by replacing all of their windows in their new home immediately upon moving in.

Methinks you met a shyster.

“I’m here from the government and I’m not going to interfere with anything having to do with building your house or what’s in it because my entire department is gutted”.

Enjoy your free market.

I feel confident saying two things:

a) Don’t call it a bubble when construction costs are rising as fast as they are.

b) Those homebuilders would be only too happy for the customer to cancel and request their deposit back due to the consturction delays. Because they’ll be able to fetch more for that home from whichever replacement customer they find. And – for new construction at least – there’s no shortage of those.

A housing bubble = asset price inflation (house price inflation).

The market establishes the price, and the market doesn’t care what the costs are. The market is driven by buyers willing and able to pay those prices. If buyers refuse to pay those prices, the gig is up. This happened last time.

And it then brings down the costs because when demand vanishes, builders build less, and then demand for construction materials etc. vanishes. Look at the chart of construction costs: you’ll see the big negative area during the housing bust, when construction costs plunged.

the bizarre actions in the asset markets (stocks, bonds, gold, and bitcoin) says to me that the gig isn’t up just yet.

Nicely summarized but some people just do not get it.

Your chart shows the number of completed new homes on the market is substantially lower than previous cycles, while pop base is larger. So they can’t get bits to build this small number, or workers to erect the bits… presumably the lack of new supply is at least one cause of existing home price increases. Is a shortage a bubble? And is this shortage gonna end because of more supply or higher rates?

Just saw a study showing long Covid keeping about 5 mil at home, plus many boomers suddenly deciding to hang it up and take ss. Imo the new home shortage persists no matter what happens to rates.

And… in 08 unemployment started the housing crash, doesn’t seem likely just now.

People don’t need stocks to live, but they do need shelter. Imo stocks in more danger than houses. Imo

But is it a bubble if it never pops?

If inflation keeps going and today’s buyers aren’t underwater, ever, are we in a bubble?

A bubble always pops. Underwater is a way of saying, “I lost my job and I have no equity in the home. I can’t afford the taxes, the payment, or the repairs. I can’t refinance due to it being worth less then what I owe. I should file for bankruptcy and walk away.” This is what happened in 2008. It does not matter if you have 20% or 50% down. It is what you can afford and if you want to keep the house. My newly 1/2 built subdivision died a slow death in 2008. Now, I see the same FOMO attitude this last year. There is an entire new generation that has thrown everything they have into these home bidding wars. A lost job or hard times will change everything. Heck, tax increases alone may break their bank accounts. We are most definitely seeing the same NINJA loans of 2008. It is just a matter of time. I just hope it’s not a blood bath to Main Street this time.

Gabby Cat

Yes, by definition. But can you call it a bubble before it pops?

This potential bubble is multi-causal.

1) inflation (may cause prices to go up but not come down?)

2) supply chain shortage/materials cost up (might come down if everyone decides to list for sale. )

3) Construction labor costs up (probably won’t come down)

4) Rush to buy second homes during covid (could reverse)

5) Interest rates low (could change cost of ownership for purchasers with mortgages, but not cash buyers)

6) Airbnb gold rush (limiting regulations and bans in process in many communities)

did I miss any?

There must be a notable percent of cash buyers who have parked cash in homes to make rental income and they won’t care if the asset/home price goes down as long as they keep collecting rent.

Anyway, we surely would have had a recession due to covid if monetary policy hadn’t juiced the economy.

Higher interest rates and a belief that prices will drop causing a rush to sell are the triggers to watch for, but will the countervailing forces prevent a massive crash?

idk

Wolf,

I agree with you…to a point.

When you say “The market establishes the price and the market doesn’t care what the costs are” – that is certainly true…to a point.

At some point somewhere when you are building something as significant as a home – there are contracts involved and when price uncertainty or good unavailability – prevents that contract from being honored – you have a problem.

So there is a distinction to be drawn between saying “home price increases simply cannot continue because the buyers will leave the market” and “it is pointless to talk about the prices of new homes because they cannot be built given the current level of economic dysfunction”.

I am saying that, increasingly, it is pertient to contemplate the latter and that is why buyers are in a rush.

I’m president of our condo board. The cost of skylights and patio doors have doubled in the last 2 years, labor and materials. Availability is 3-4 months out, maybe.

Bless your heart. Being on the board is rewarding in that you are giving something back. But no matter how you present it you are the face of the evil costs being taken via HOA dues. All costs have gone up and our HOA is increasing the annual rate by the maximum allowed in the bylaws. Costs are killing us on all fronts

I’ve heard stories of subcontractors using clauses that void their estimate if materials and labor prices rise more than 10%. In some cases this might be happening in the middle of a project.

Anyone who pays for crap knowingly, get what you deserve folks

Question for the day.

Historically,

What happens when increasing housing inventory smacks into rising interest rates?

Now coupled with insane inflation for the basics and no more mortgage/rent forbearance and a declining stock market!

Bubble meet pin.

NaNa

What happens when increasing housing inventory smacks into rising interest rates?

its kind of like a Hand Grenade when you pull the pin All Hell can brake loose.

The Inventory simply runs into the “Current Market” made by conditions at that time .

Sales /Price will be governed simply what they can get for the property same as always

I beg to differ…

When you pull the pin from the hand grenade nothing happens.Only after grenade is thrown and the lever is released the delay fuse starts burning.

You pull the pin and give hand grenade to the FNG so he will not fall asleep while doing guard duty.In the morning you pry it from his hands (which is the hardest part of this SOP), reinsert the pin and everything is tip top.

Times are a-changin’.All the FNGs now play with their smartphones, totally unaware of what goes on around them.

2banana,

We are not talking about an asset bubble bursting…

…we are simply talking about goods becoming unavailble at any price.

Might look into apartment construction, I hear that a lot of units are under construction, creating supply, that along with the eviction moratorium be lifted and the end of stimulus payments and high rent, may bring about a huge reset in the rental market. May put pressure on single family home investors if their rents drop. A substantial number of cash investor buyers driving up the market.

How many of these “cash” investors are really pulling loans from their brokerage accounts, e.g. a pledged asset line, to purchase these homes? There’s some limited anecdotal evidence on Reddit that some people were really that stupid, and are now receiving “margin calls” due to their tech heavy stock portfolios losing value.

A University of Florida research on housing bubbles found that during the pre-2008 housing bubble, folks who paid nearly $340,000 on average to purchase a home in Miami in 2006, many of them are only now able to sell their house without taking a loss.

Just like buying a stock at the peak then holding on for 16 years with nothing to show for, or losing to get out..

Funny you mentioned this point…every time I mention the fact that if you buy Dow or NASDAQ mirroring index over 20 yrs and then compare to RE even in hot market like SF, you’ll still come out ahead in stock..

Trying to convince my idiot european living in the US friend about this point always end up in ” I don’t care, RE only go up and all the rich people I know made their money in RE, stock is not the same and way more violatile” I simply roll my eyes at that point and smirk at the fact that in the age of search engine, just freaking search for a stock value calculator vs RE value calculator and see the difference in real time yourself.

that’s if you actually have a productive economy. we don’t anymore. i wouldn’t count on anyone who buys stonks at today’s valuations making money over 20 years.

Stock market only goes up. It hiccups but only goes up. What a country invading another country. WAR. Nasdaq up 3%

But the Nasdaq is down about 17% since November. Did you already forget?

This morning, it was down 20% from November.

nathan, that just says to me that the btfders haven’t yet lost their shirts. they will

The country believes itself to be rich, but the reality without the fake economy and an asset mania, most Americans are a lot closer to being poor, wretched, and naked.

Phoenix lkki

I am familiar with the Kool aid mantra of your friend. I have a good friend who will NEVER invest in direct RE, only a REITs, if at all.

We hike together and talk for hours. I 100% acknowledge in the QE era (past 12 years basically), 7% “net” index returns in the market are now 10% (minimum).

However, RE 3-10% net ROI is cash flow. Equity growth (I never count on it) is just a bonus.

For retirement minded people (like me),

the cashflow, tangibility + relative predictability of RE is attractive. The tax bennies are huge also.

With stocks / indexes, I am constantly hovering and paranoid the big boys are monitoring my limit orders to trigger me. I am horrible with ETF index investing. S&P does 20% for the year and I do 5%. I guess I just rotate at the wrong time….every time. 😕

RE peeps are weird ducks. I know, I is one. :-)

I was a Realtor (and homeowner) in CT in 1988. House prices started to drop. In many towns they sank 50%, and did not reach their 1988 level for ten years.

Wait for it….wait for it…here we go. Not in SoCal, remember around here it’s the land of invincible when it comes to RE, only up and up all the way.

I just drove by Irvine and surrounding cities and apparently this is now cheap in Mission Viejo so none of that supply is making it in prime SoCal location..

MISSION VIEJO, CA — Take a look at the most affordable home that has hit the market in Mission Viejo. Located at the end of a cul-de-sac, the asking price is $799,900.

Address: 27222 Rosario, Mission Viejo, CA

Price: $799900

Square feet: 976

Bedrooms: 2

Bathrooms: 1.5

Homes having work done right after buying. could be 1 of 2 things … poor quality …. or people have so much money that nothing is good enough and they can borrow any amount they want to upgrade ….

Wow! We decided to wait and build. Still exploring house builders. What we found have been 2 years in delivery, 35K jump in cost for supply issues every three months, and absolutely no guarantees that what you design will be delivered. Kind of like 2006 when we built our first home. It took us 16 years to get above water from that build. We learned our lesson and now we will wait for a buyers market. I just hope there are good business left when it’s time.

They will be begging for the work….

Building now in insanity

Jason,

They may be begging for work….but it won’t be work for building houses.

The supply chain interruptions are making houses impossible to build outright.

And we’re in the top of the 1st inning of the commodity price inflation ballgame…

“The number of houses for sale where construction hasn’t started…”

Has anyone else seen this? In my area there is a waiting list to get new houses built, there are lots for sale with planned construction for sale, yet current homes on the market are now being marked down. Oh, and rents are through the roof.

Doesn’t make any sense.

Welcome to the early stages of hyperinflation.

It’s not going to be pretty.

B

Wolf – Isn’t the main driver here a lack of supply? Not new construction home supply, but resale listings supply. The inventory of pre-owned homes for sale is lowest it has ever been. People just stopped selling their homes during 2020 / 2021. New construction has always been a small minority of the homes sold, but with 85% of the home supply (pre-owned homes) gone, the builders are left to ramp up construction and charge eager buyers whatever they want. Look at the resale inventory adjusted for population growth (listings per 1,000) and it is lowest in recorded history. If (when) people decide to sell their houses again, the supply of homes for sale will sky rocket and these builders may find themselves in for a hard landing.

What says you?

AnxiousRealEstateGuy,

“Supply” of existing homes = owners putting houses up for sale.

If I own 5 vacant homes and want to ride up the house price increases, that’s not supply. But it’s shadow supply. When house prices come down, suddenly I want to sell those homes to get out at the peak, and then these vacant homes turn into a flood of supply.

In San Francisco, the vacant home issue is such a problem that the City is now considering a vacant home tax. This is a particular issue with investor-owned condos that no one ever lives in. There is a condo building down the street from here, completed something like 3 years ago. All units sold long ago. Outside of a vacation renter every now and then, I don’t ever see anyone going in or out.

So that’s the first thing you need to know about “supply”: right now, many homeowners are not putting their vacant homes on the market for whatever reason — including riding up that 20% to 30% annual gain that with a lot of leverage (the mortgage) becomes a huge return on equity.

By contrast, homebuilders aren’t holding back their homes. They’re trying to sell them. And that’s what you see on the market.

You still pushing vacant home nonsense? Vacant homes are at their lowest level since 2003, and trending down.

I think Wolf is talking specifically about San Francisco.

Jon,

“Vacant homes are at their lowest level since 2003, and trending down.”

No one knows how many vacant homes there are. They’re essentially impossible to track. The Census is trying, and others are trying, but it’s really tough to establish how many vacant homes there are. In Canada — I think it was in Vancouver — they looked at usage of utilities (electric & water) and had some success with that… and found lots of homes where no one was using utilities.

What we do know is that during market down turns, this stuff suddenly comes on the market, and that’s where you see this huge burst of “supply.” It’s not like millions of people just vanished into thin air and disappeared from their homes. Those homes were vacant…. 2nd, 3rd homes, investment properties, etc. and suddenly they show up.

Another tidbit – article on the way: Opendoor, a home flipper like Zillow was, had 17,000 homes in inventory at the end of 2021. Only a smaller portion was for sale. They rest were backlogged in its processes. In 2021, they bought 15,000 more homes than they sold. NO ONE lives in those homes. They’re vacant. Zillow sold thousands of homes (vacant) to institutional investors to get rid of them when it got out of the flipping business. This shit is going on everywhere.

New housing in the Florida Villages are just being thrown together with cheapest quality and extremely poor workmanship, just awful.

Interesting the construction cost index is almost always above zero, so seems like no time like now to start building. It’s only going to be more expensive down the road, maybe 5% instead of 15% though.

TimIN,

“…construction cost index is almost always above zero,”

No. Check out the years of the housing bust: deeply negative.

In terms of the actual index and not YoY %-change: The index peaked in March 2007 and then fell until March 2010, and then stayed in that range for two more years before rising again. It didn’t hit that March 2007 level again until the beginning of 2014:

Reminds me of when I was a kid riding around on my dirt bike seeing all the subdivisions that had been cleared and graded during the last housing bubble. A dozen massive developments had been cleared and paved but no houses every got built. Years later they were still there only weeds were growing in the asphalt, new growth trees were up 10-15 foot tall and the back parts of the subdivisions we’re trash dumps.

Warmed up enough to take the motorcycle out in the new area I live and it reminds me of it. Huge subdivisions tracts cleared with no or maybe one or two houses in the whole thing. None of the houses finished.

Lot next door to me was bought over a year ago, 3/4 acre for 660k. They’ve cleared the lot, water meters and utilities in, cinder blocks stacked but progress is very slow. After the last bubble burst, the same developer bought the lot on the other side of me for 300k, and built and sold 6 townhomes for about 600 each. Took over 2 years. Right now one of them is for sale for 900. Crazy times, money is no object to fools. I rent next door for 1100/mo :)

You live surrounded by 600k – 900k homes and you pay $1100 rent? Doubt it. Love stories like this that make zero sense. Of course I’m sure you’re leaving out all the relevant details on purpose.

I t appears to me there is lot in development on one side. The expensive homes on the other just sold. They may well not be rented out. It is quite possible that the writer’s home is small compared with the others.

Great article Wolf! I see stalled homes and projects in my neighborhood on Long Island where both labor and raw materials are in short supply!

Home builders counting home orders as inventory is potentially deceptive. The inventory of completed homes for sale seems low.

New housing starts for homes in buildings with more than 20 units is above normal (FRED statistics).

While COVID supply chain disruptions should go away, sanction supply chain issues and labor shortages are not going away.

David Hall,

“Home builders counting home orders as inventory is potentially deceptive.”

BS.

RTGDFA.

They’re not counting “orders” as inventory. They’re counting properties as inventory, and sales (orders) as sales. And the vast majority of sales are properties where construction either hasn’t started yet or hasn’t been completed yet.

When unsold completed homes are piling up, the industry is in REAL trouble. This happened during the housing bust. Look at the chart.

Why is our current inflation going to accelerate inequality, possibly finishing off what was left of the American middle class? Here is a real world example

I have 2 friends who own competing construction businesses. One inherited a large biz from his daddy, and made it much larger. The other is firmly middle class.

The smaller one called me the other day on the verge of tears. Just can’t get labor or materials to finish his work. Can’t pay his foreman enough.

The guy with the much larger biz also called. Labor and materials have been challenges, but he’s just flexed his muscles and has gotten what he needs. Has stolen contracts from smaller competitors that couldn’t.

My small biz friend is a grizzled, heading into late middle aged guy who has only worked from himself. If his biz doesn’t make it, he is only very marginally employable.

The big guy may very well get much richer, and the small guy is about to get a lot poorer.

The dark magic of inflation at work!

“….non-construction costs – spiked by another 1.1% for the month and by 16.8% year-over-year”

Nah, can’t be,… the BLS says inflation is only 7.5%. there must be something wrong with these figures, just don’t agree with the always honest Government reporting.

Just look at the Gods and Goddesses at the FED, they know all is OK, they keep pumping monopoly money daily.

My daughters Sub contractor business of building new residential foundations is projected to quintuple this year. It will hold at that level until the building stops. Building normally doesn’t stop until 6 months after after a collapse in the market.

This housing bubble is the pent demand from the repressed housing market post GFC. Three generations is a home sounds folksy but its not what people want. The conversation is usually between husband and wife, but now fewer people get married and those who do don’t have children. The amount of living space per person is a direct expression of a nations economy.

I don’t know about Cali, but I’m building full throttle and selling and renting everything I put on the market. So long as you stay out of debt or don’t overleverge, the risk is minimal.

In the construction business you make hay while the sun shines and go on vacation when it starts raining. There’s plenty of sun right now in the right markets. That’s why they call it the sun belt.

“…. the risk is minimal.”

Maybe for the builder and seller. Not for the buyer.

Everyone looks like a genius when things are in a bubble.

Drop a pin in the center of downtown Houston, then draw a radius 100 miles around it, everything inside that radius is in a bubble.

I’m sure it extends beyond that, but I’m only speaking of the area of my personal knowledge.

Houses here are selling above asking price,sometimes within minutes of listing, I can assure you that this is an anomaly that has no precedent for this area.

I have asked realtors here about where these people are coming from?

The number one response I get is California.

My question I then ask is “ ok , but where are the people buying the houses in California to allow them to come here coming from?”

I have not received a straight answer, everything from Investors, to China.

Currently, land prices here are skyrocketing, as developers are snatching up everything they can get their hands on to get in on the “action”.

Commercial property is also going gang busters as well, everything from fast food chains, big box retail, light and heavy industrial/ warehouse and everything in between you could imagine.

This is happening north/south/east/west.

Of course property taxes, which are extremely high in Texas anyway, (we don’t have a state income tax) are skyrocketing.

Went to a Ford dealer to order a couple of work trucks last week, these are basic models without all the frills, the exact model that I purchased in 2018 for 38,500$ is now 54,000$ .

I said “thanks “ and walked out, they never even batted an eye.

Went across the street to a Chevrolet dealer to enquire about a medium duty cab and chassis to build a small vocational truck for small local deliveries. She did a national search, said nothing available. Once again, this is a regular cab , white in color, rubber seats and floor mats, air conditioner, Diesel engine, no spare tire and no bed , just very basic, priced it up at 65,000$ plus TTL . That in itself is absurd , but she then told me I was looking at approximately one year build time. This is also the case for boats , RVs, and especially used cars and trucks in this area.

I know of people that have sold vehicles they have owned for several years for more than they paid for them new.

I could tell the fleet manager at the Chevy dealer had been around the block a time or two, I asked him what was going to happen when this market shift hits, and everyone, including the banks are stuck with all of this mess that have been purchased at 20 /30 / 40 percent over Market?

He just laughed and said the repo man and auction houses are going to be the only business booming.