But the deals were made when mortgage rates were still 3%, not 4% as today.

By Wolf Richter for WOLF STREET.

In some cities, house prices continued their crazy spikes, such as in Phoenix, where prices have exploded by over 30% year-over-year for the sixth month in a row. In other cities, prices only surged, so to speak. And in a few cities, that surge slowed. Condo prices in the San Francisco Bay Area started to dip last summer and haven’t gone anywhere since 2018. That’s the range for the most splendid housing bubbles in America, as depicted by the S&P CoreLogic Case-Shiller Home Price Index today.

The overall National Index ticked up 0.9% in December from November, same as in the prior month. Compared to a year ago, the index jumped by 18.8%, same as in the prior month. “Buyers may have been rushing in anticipation of higher rates,” S&P CoreLogic said.

But the home prices here don’t yet reflect the higher mortgage rates. Today’s “December” data are a three-month moving average of closed sales that were entered into public records in October, November, and December, reflecting deals made roughly in September, October, and November, when the average 30-year fixed mortgage rate hovered at around 3%. On Friday, the average 30-year fixed rate was 4.08%, according to Mortgage News Daily.

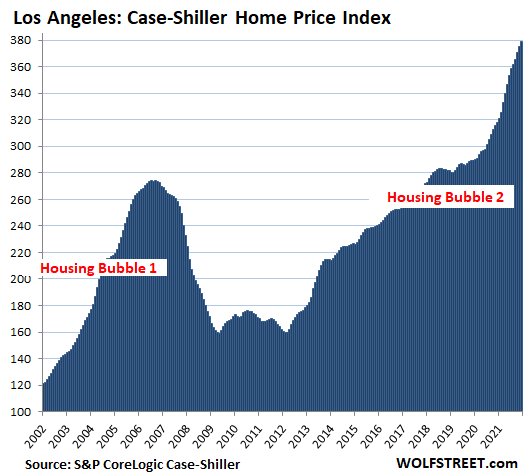

All Case-Shiller Home Price Indices were set at 100 for January 2000. The National Case-Shiller Home Price Index, with a value of 279 for “December,” indicates that national home price inflation is now 179% since 2000. Over the period, consumer price inflation, as tracked by the CPI, has risen 67%. In Los Angeles, house price inflation since 2000 has now hit 279%, over four times the rate of consumer price inflation.

Los Angeles metro: Prices of single-family houses rose 1.0% in December from November. Though steep, it was the slowest month-to-month increase since August. Year-over-year, the index jumped 19.3%. This 279% home price inflation since January 2000 makes Los Angeles the Number 1 most splendid housing bubble on this list.

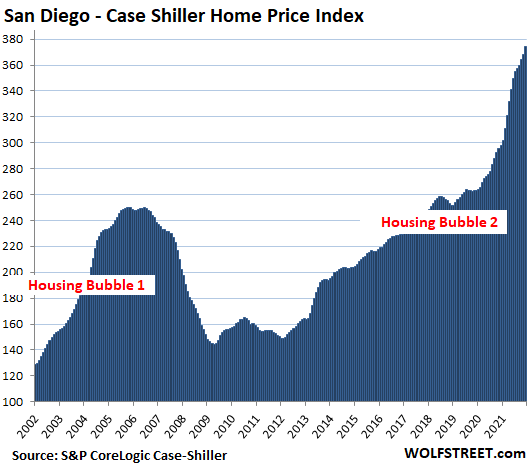

San Diego metro: The Case-Shiller Index spiked 1.8% for the month, and 29% year-over-year. Since 2000, house price inflation has ballooned by 276%:

House price inflation as measured by the Case-Shiller Index. The index’s “sales pairs method,” compares the sales price of a house when it sells in the current period to the price of the same house when it sold previously, often years earlier. The data includes adjustments for home improvements and the passage of time between sales. By measuring the price movements of the same house, the index tracks how many dollars it takes to buy the same house over time and thereby measures house price inflation.

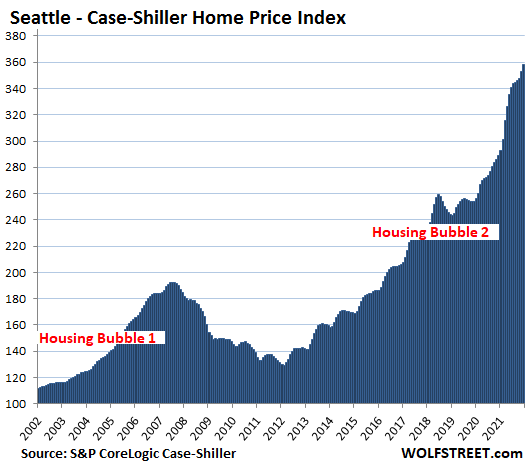

Seattle metro: House prices spiked 1.5% for the month, and 23.9% year-over-year. Since January 2000, house price inflation in the Seattle metro has ballooned to 258%:

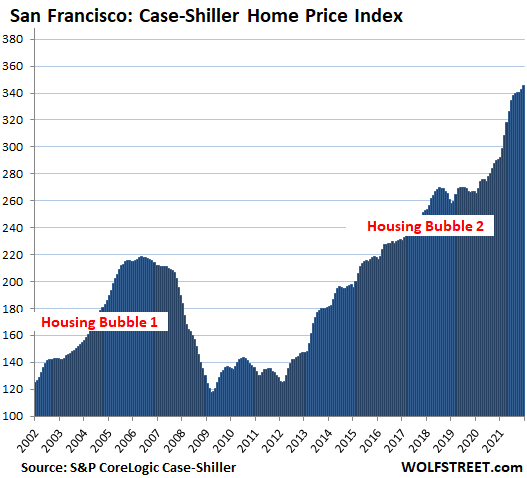

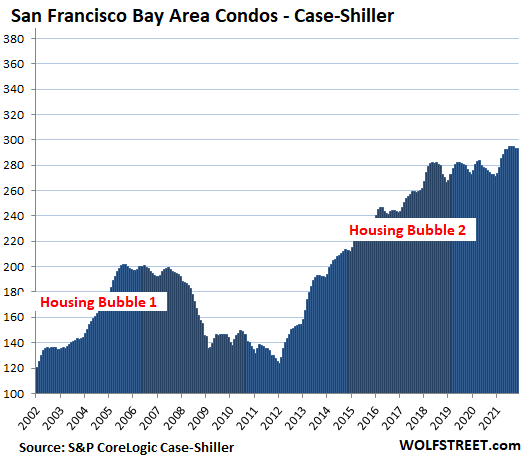

San Francisco Bay Area: House prices rose 0.8% for the month, after having nearly stalled in the fall. Year-over-year, prices jumped 18.8%:

San Francisco Bay Area: Condo prices for the month were unchanged, after having dropped three months in a row. For the past seven months, prices have gone essentially nowhere. This whittled down the year-over-year gain to 7.5%. Since June 2018, condo prices have risen just 3.9%:

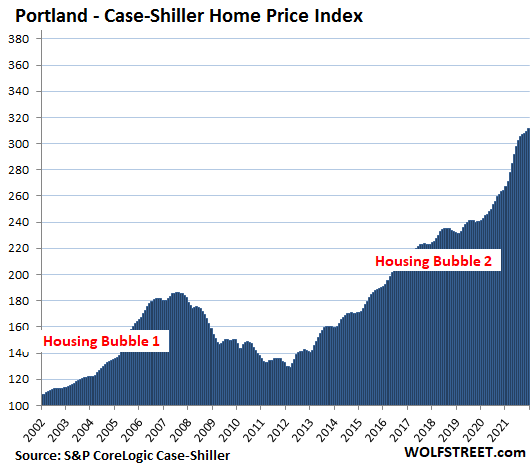

Portland metro: House prices rose by 0.8% for the month, and by 17.9% year-over-year:

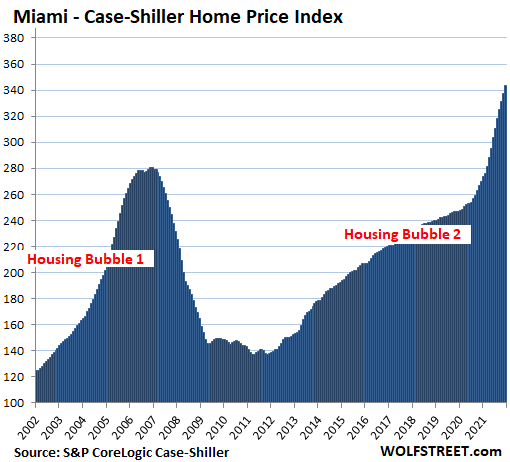

Miami metro: House prices jumped by 1.8% for the month, and by 27.3% year-over-year, the fastest since February 2006, when Miami was approaching its epic Housing Bust:

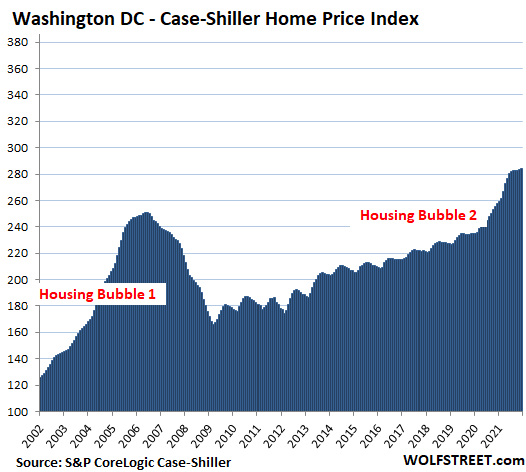

Washington D.C. metro: House prices ticked up 0.4% for the month, which whittled down the year-over-year gain to 10.5%, the slowest since January 2021:

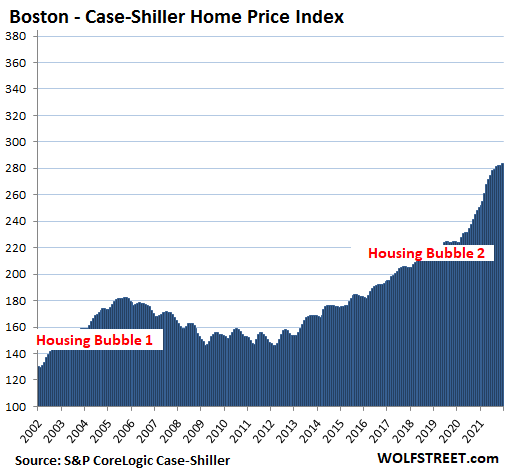

Boston metro: House prices rose 0.7% for the month, after having been flat for two months, which whittled down the year-over-year gain to 13.4%:

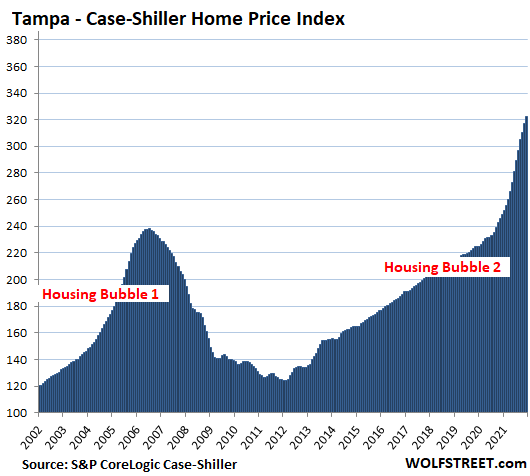

Tampa metro: +1.6% for the month, and halleluiah, +29.4% year-over-year, a new record spike for this metro, out-doing even the nutty spikes during Housing Bubble 1 before it all came apart:

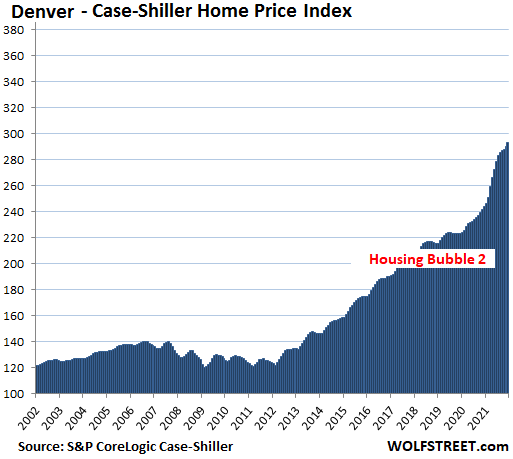

Denver metro: +1.1% for the month, and 20.3% year-over-year:

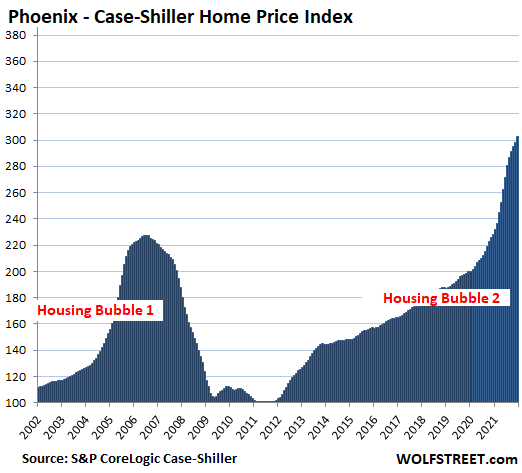

Phoenix metro: +1.3% for the month, bringing the year-over-year gain to 32.5%, a new record, out-spiking even the peak of crazy Housing Bubble 1. For months now, Phoenix has been the metro with the red-hottest year-over-year price spikes among our most splendid housing bubbles:

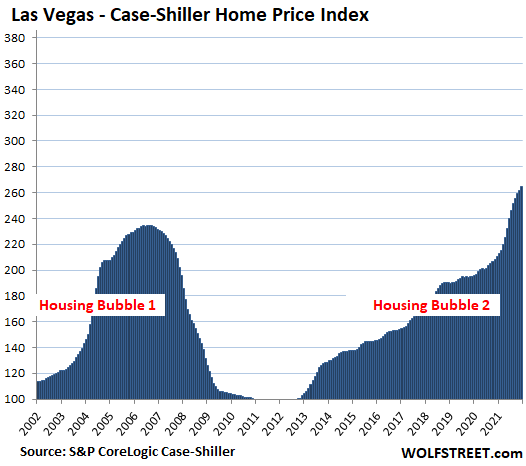

Las Vegas metro: +1.0% for the month, and +25.5% year-over-year:

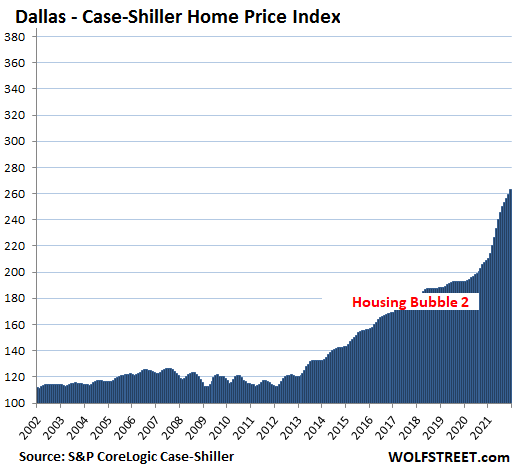

Dallas metro: +1.2% for the month, and a record +26.0% year-over-year:

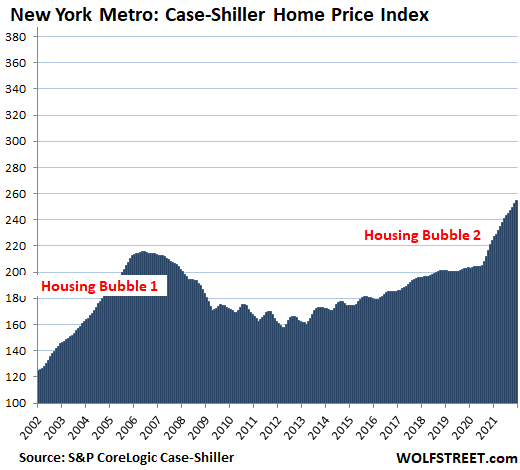

New York metro: House prices +1.1% for the month, and +13.6% year-over-year. At an index value of 255, the metro has experienced 155% house price inflation since 2000.

The remaining metros in the 20-metro Case-Shiller Index – Atlanta, Charlotte, Chicago, Cleveland, Detroit, and Minneapolis – have house price inflation since 2000 of less than 150% and thereby don’t qualify for this list of the most splendid housing bubbles.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Very splendid. I have been curious about quoted rates and actual rates when you apply for the mortgage. Do banks honor the quoted rate when applied on day 1? in other words, my application 90 days ago quoted X%. Does that X% rate change when the deal closes 60, 90, however many days afterward, or do banks honor the quoted rate?

wife and i are young and in good financial shape (by 2019 standards) but the recent mania had us saying no way to this and that price. We never closed or had an accepted offer, but curious about that 90 day rate window, and the lag it may have on pricing.

You need to ask them how long they will keep a lock for you. Most lenders give only 30 days lock. If you want more, you need to ask them. Usually you pay for this, and it ain’t cheap. If it is cheap or free, then the fee is most likely “baked-in” the rate they’re offering. So most likely the answer is no.

This is particularly painful for new construction. I’ve seen people stressed out and backing out when they signed a contract to build a house, and 6 months later the rate is higher. Sometimes (especially in the past few years), the rate would be lower, so that’s nice.

But now, you really have to make sure you can 1) afford a higher payment if the rate goes up or 2) negotiate a longer rate lock, or some other deal that would soften the blow if the rates go up.

Generally, you’d have a better luck with a direct lender. For instance, DR Horton is a direct lender and are able to give better terms most of the time. Smaller builders typically have “preferred” lenders, where such lenders will basically kick-back fees to the builder, and graciously give you a higher interest rates. Terms vary.

Currently renting a brand new Dr Horton home and it is junk!

Steve,

Is that house in a “build to rent” community?

Hi Wolf

No

The interest rate should be locked in for a set number of days. Typically 30 days. If the loan does not close within that time frame you be quoted a new rate.

This is where it helps to work with a local bank where you can actually work with a single mortgage broker. They can and will extend the rate lock if, for example, it takes longer than expected to obtain the appraisal.

My friend got his rate locked for 6 months in his local bank.

Realtor here. Pretty certain that nearly all banks will require an actual signed purchase contract to lock a loan rate. You will be quoted a rate with a pre-qual or pre-approval but it is not locked. At least that is how our local lenders work.

ace,

“Do banks honor the quoted rate when applied on day 1?”

If you get a rate lock from a bank, the bank will honor it for a set period of time (unless they find out you lied about your income, or whatever).

I wonder how many people lie.

Be sure to check your paperwork very carefully.

Sometimes the bank or broker will enter different numbers than the ones you gave them.

They have a stake in selling the mortgage and may jigger the numbers to ensure that

you qualify for a mortgage you cannot affordthey get paid.This was a huge issue with Housing Bubble 1.

OK got it. Thanks all for your information. Mostly curious how rate locks could delay economic reporting/prices, and it sounds as though it does.

In real estate, everything takes time. It’s not like stock sales; and even they take time to settle. Real estate deals can take weeks or longer to close, though that has been getting a lot faster. Then it takes more time before the closed sale actually shows up in the public records, from where it gets picked up by the Case-Shiller index, which then forms it into a 3-month moving average and reports it with one month delay.

Actually, When I bought years ago interest rates went up, and the mortgage rate went up when it came time to sign the final papers, despite the rate previously quoted when applying for the loan. When I, protested the bank said “take it or leave it. That’s the rate now.” That was B of A, in 1979.

No, not unless you have a property in the process already. They may tell you differently, but unless you’ve already paid points or something and have it in writing I would not count on it another month or two down the road. Learned that this past year while looking for something and was told this by a multi-bank mortgage agent for a smaller loan. Could be different for a larger loan, but I’d imagine it would have to be a very big loan.

Typically most lenders will give you a rate lock for a certain period of days after providing a purchase agreement.

You can typically purchase a rate lock in advance, or extend the number of days originally extended.

Each lender will have their own specific mix of rules and benefits they offer.

I close on a refi on Thursday. 60 day lock. Had to put up 1 percent of loan total which counts towards closing costs. Credit Union fyi.

That’s a great deal.

Most of the lenders I spoke with require a purchasing contract to lock in a rate.

Typically you can only lock a rate up to 60 days out, with some banks letting you pay a deposit to lock for a longer time period. The rate “floats” until then, i.e. the quoted rate could move.

Here in Arizona, even with 4% rates, prices still moving up, albeit slower.

Surprisingly, Northern Arizona, specifically Prescott Valley area is experiencing even stronger moves up. Perhaps that’s due to the fact that this area is known as a place where wealthy retirees are buying homes, and as a second home mecca for people all over. The area is relatively close to Phoenix (1h 45 mins), but has a fantastic weather with 4 mild seasons and stunning vistas at 5000ft of elevation and above. And unemployment rate (Jan 2022) is a mere 2.4%. You see thousands of new homes built (Granville etc), with more in the pipeline (PV540 etc). The town reported 20% sales tax increase and more to come. I predict Meyer-Dewey-Prescott Valley to be the next hot spot.

Here in the Valley, it’s clear to me that prices will not come down, despite my desire for them to do so, as I was pining to buy one more rental. If you drive up and down Ray Rd near the Mesa Gateway airport, you will see what’s dubbed ‘Warehouse District’. In a few short years, about two dozen huge warehouses were built here (each 500,000-1,000,000sqft), and all around the business is booming. The same for the West Valley, and pretty much everywhere else.

The reason why Phoenix is booming is unlike the previous boom (2007), when they said ‘construction workers are building houses for other construction workers’, this time, massive job influx is to blame. This is “Orange County-ification” of the Phoenix area. Many folks thought huge prices increases in the early 2000’s were to be reversed. Aside from a dip in 2009-ish, you would have been lucky to have bought back then.

The same is happening in Phoenix area all over again. Good paying jobs are arriving in staggering amounts. Business like low taxes, good weather, no natural disasters, massive younger work force, and relatively well balanced politics. We see license plates from all over the country; people are coming here for jobs.

This is not to say there won’t be a dip. There probably will be, but a mild one. And the Fed is likely to back off before year’s end on their tough rethoric, and go back to stealthy QE.

“Surprisingly, Northern Arizona, specifically Prescott Valley…”

Maybe that was the last affordable-ish place in Arizona that any reasonable person would want to live. Relatively cold winter but much nicer summer than the rest of AZ, pretty things to look at and all the amenities. Also possible to get to the SoCal beaches before noon just like Phoenix.

Maybe that’s why driving through Prescott this fall I couldn’t help observing how ugly it’s becoming and how it’s so no longer the magical place it was

The end of the fake economy and asset mania can easily reverse the price trends you described. No, it isn’t different this time.

I lived in Phoenix from late 2001-2011 with a gap during part of 2004-2005. The main thing I liked about it is that the traffic was much better than where I live now (metro ATL), presumably because of the road network.

On the other hand, summers absolutely suck.

As another post here states, you can actually fry an egg on the sidewalk. It’s absolutely brutal. So much of the Valley has been paved over, even at night for hours after sunset, feels like opening the door to your oven.

Also, much of the metro area isn’t very nice. I didn’t travel to all of it, but I’d describe most of what I saw as “sucking”. Housing was ridiculously overpriced for what you actually get, mostly tiny lots with unappealing architecture. The limited vegetation also makes much or most of the Valley look dirty. There is dirt everywhere.

I lived in North Scottsdale the last three years, near Scottsdale Rd and the 101. It’s one of the few areas in the Valley I actually liked.

I can understand why snowbirds like it seasonally, as November to March or April is quite nice. Concurrently, there are definitely better places to live year-round.

Agree. Live in PHX metro now for past two decades. The summers brutally suck. Most of the metro isn’t that nice.

Yes, the summers suck. No question. I like a scale I heard somewhere:

– hot

– very hot

– extremely hot

– stupid hot – hint: this is summer in Phoenix. The saving grace is that humidity is very low (3% in June), so you can breath just fine. I have never experienced super-low humidity before I came here and it really makes a difference, though it won’t be “nice”, just bearable. Monsoons bring humidity and I don’t like them at all, though they bring rain, so that helps.

The rest of the year is very nice though. Winters are nicer than anywhere in California.

I also lived in Scottsdale, on Scottsdale Rd, just north of the mall. It was nice.

The southeast Valley is the nicest. Gilbert, Chandler, parts of Mesa, Queen Creek. West Valley is nice for the most part. Phoenix so so, depends where, Ahwatukee is quite nice. Scottsdale is nice mostly.

When we came to the Valley many years ago, we felt the same about the summer. We don’t notice it much anymore. Generally we go to Prescott Valley or Flagstaff to cool off. We used to go to California, but with homeless everywhere, overcrowded and politics that start to look like Canada, we don’t feel like going anymore.

I used to live in MidWest and one thing I can say: extreme cold sucks more than extreme heat.

The traffic is generally better than other major cities. Phoenix downtown gets congested, we never go there. 202 loop is usually good, 101 depends where. Again, relative to other metro areas, traffic is beter. If you were ever stuck in LA or OC traffic, you’ll love the Valley system of highways and roads.

Yes, there’s lots of dust, especially if you live where it’s not all that much developed. We get about one Haboob a year (a sand storm). More of a spectactle to watch in disbelief if you’ve never seen it. It usually comes and it’s gone in a few hours.

The nice thing though is that it’s always green year round, the desert plants are out-of-this world beautiful and it never snows.

Housing is overpriced now. But compared to West Coast, still a great deal.

As with everything else, pros and cons. I like it here, but everyone has their own taste, I respect that.

You know it’s bad when its past 10 at night and over 100 degrees at night. Loved my whole life in the valley. The last few years are starting to remind me of southern Cal without the cooler weather. That’s not a good thing.

Yes, Phoenix is known as the concrete jungle.

4 mild seasons? At least one of them (summer) I would not consider mild. But to each his own.

I was talking about Prescott Valley. High-country Arizona is very different than Phoenix.

So yes, parts of Arizona have fantastic weather, 4 mild seasons, such as in Presctot Valley AZ for instance. At 5000 feet, it’s probably one of the nicest climates anywhere in the world.

Half your post was or sounded like it was about PHX.

I never understood how prices could be so high there, as it was never cheap even before housing bubble 1. It was overpriced even then.

And it’s not like the job market is loaded with high paying jobs either because it isn’t. There are a decent number of technology related positions locally and a few large employers (like my previous one) but it’s not a corporate center.

I’m aware that there are California transplants who have and presumably continue to inflate the price level but it’s not affordable for most local wage earners.

It’s not like the PHX area is loaded with a high proportion of affluent or wealthy people. Where I live in ATL now, I’m confident there are far more affluent people here than there, though both have a high proportion of lower income residents and ATL probably has more poverty.

Do businesses like water?

A common misconception is that Phoenix will run out of water. At present population, the underground aquifer is sufficent for another 400 years, without restocking. It came to be when the last glaciers north of Flagstaff melted and filled it up.

And everytime it rains, it gets restocked, due to sandy soils. Phoenix area gets around 11 inches a year, though last year just in the summer stomrs we got about 17 inches in 3 months. Rainfall varies. In addition, the mountains north of Phoenix get more water and a good amount of it flows down to the Valley.

The images of the desert always evoke apocaliptic visions. I get that. But the facts tell a different story.

Sure, if there’s 17 million people living here, like in LA, that may be a problem. As it is, it’s not.

If this is true why does the Central Arizona Project exist? I am not sure where you are getting your numbers here but implied in your statement is that groundwater draw down is acceptable. It is not and results in subsidence (see Mexico City). Thus, the rate of GW replenishment must be equal to withdraws. Without the CAP, the math doesn’t work. And the CAP pulls from the Colorado. and Lake Mead is in a bad place. and Arizona is in the absolute worst possible position in terms of negotiating power with Lake Mead/Colorado R rights. Good luck. I lived there for a while, generally liked it, and you’ll be fine for quite a while but your comments grossly misrepresent what’s actually going on.

I live in the Phoenix area too and I don’t share your enthusiasm about abundant water. You do know that the water levels of Lakes Mead and Powell are the lowest they’ve been since initially filling? This continuing drought shows little sign of abating. Aquifer reliance — really? Some municipalities that don’t get CAP water are in dire straits. I fully expect to have to ditch my backyard lawn soon to be a good doobie and lighten up on my own water use.

@DanW

Your stats are bad on water supply. Phoenix metro averages 7 in/yr and most years don’t even get that. Last year exceeded that average but that was an anomaly for the last 15 years. Trust me. I work in this industry.

If needed at some point, AZ will fund a desalination project that has a Yuma as its hub with a line leased from CA across its southern border to the Pacific.

No one in this country, certainly not the political or business leaders, thinks more than 5 years ahead. It doesn’t help that we live in a gerontocracy and they all plan on kicking the bucket before the shit hits the fan anyway so who cares. At least China pretends to care about future generations and the long-term. Prices up 20-30% in Phoenix, Miami, Tampa, etc. That’s a pretty big bet on the miniscule chance that climate change isn’t serious or it can be mitigated by a technological moonshot

You should have bought there 45 years ago when they couldn’t give the houses away and Sedona had one traffic light……………

DanW you appear to be greatly downplaying the prior Phoenix RE implosion. Why is that? Per Case-Shiller, prices peaked in ’06 and then cratered, not reaching the rocky bottom until approximately 2011. With an average of 56% evaporation of value. A massive, long and deep crater. Nominally, RE prices did not return to their ’06 peak until late 2020, over 14 years later.

Please see more posts below about what really happened last time in Phoenix. I did alot of business there and have alot of friends/acquaintances there. It was UGLY. And it is likely to be so again.

and what will happen when phoenix runs out of water?

Buffet will transport all the water you want, on his railway!

I was going to say build a water pipeline but that will never happen!

No you will not, just got offered Silicon Valley salary to work there in a local job remotely, will not buy SV housing prices, so Phoenix here I come! (Specially Chandler)

Even with the rising prices, housing is still very affordable in my new salary which is California level but in Phoenix. With TSMC moving to the north part of the town, the Cave Creek area is going to boom as well. I agree the price won’t come down for a while in the valley. Maybe the scotching hot weather will get some people to think twice.

Prediction for future:

As everyone flocks to Arizona and Florida, those same people will be looking to escape the increasingly brutal summers. Especially the affluent. They’ll be buying summer homes and cottages in the North. Especially waterfront. Vacation areas, such as Idaho lakefront, Northern Michigan, etc will boom

Yes reverse of what was traditional. Now summer house up north! I know people that do just that (winter house in Texas, summer cottage in northern Wisconsin).

Four months for any increases in mortgages rates to start to hit housing prices.

Four months for tech stocks imploding to start to hit housing in high tech areas of the country.

Looks like June is gonna be a heck of a month…

With a concurrent stock market crash, RE market crash, recession and inflation, the evaporation of household wealth is going to be huge.

The Case-Shiller charts are ominous. Stock market valuation metrics are ominous.

Like Mr. T in Rocky III, my prediction? Pain.

Ominous is a good word for those graphs. If there ever was a case of “this cannot go on forever,”, this is it. Those steep upward price slopes have a sinister 1929-ish appearance.

Yes, there is a big difference when financial assets exhibit this behavior as opposed to “investments” like housing and now even consumer durables like cars going parabolic.

A house is supposed to be a place to live but modern finance has incorporated it into the casino where the average American gets to “roll the dice” with their living standards.

Guess wrong and you get caught in an upward spiral of increasing housing costs or take a roller coaster ride in another housing crash.

I would love to agree with you guys on the pain, but the inventory levels are going nowhere. In my little piece of paradise in Naples, we have 535 SF homes listed. This figure is normally 3,500. Rents are up 38% YOY. It is a really tough time to be a buyer or a renter.

Feel for ya…

Tough choice…

Pay the laborers a lot more money so they can afford to live there…

Or sit back and watch the “special” people try to figure out how a lawnmower works… :)

Actually I would guess that Naples will ultimately get pounded by a steeper RE devaluation than many other places due to the lack of a diverse, vibrant economy. Doesn’t everyone pretty much have to pack their money into Naples because there is no money to be made there? Naples got blasted during the last downturn, what has changed that will cause it avoid mucho pain during the next one?

Falcon is correct,,,, that’s why we locals called it “Naples on the cuff” back in the ’50s and 60s,,,

And most of us got out of there asap after high school, of which there was one in Collier County…

Now, there is money to be made fixing all the concrete condos built in the ’80s and since that are certifiably falling apart, sometimes in large chunks!!!

Don’t count the mass populace out! I’m sure they are timing the housing market for increased mortgage rates, and maximum real estate prices! I would not be surprised.

Good joke

Now is a good time to buy. Things will get worse because of the low inventory. It’s just gonna get lower coz people are buying up everything. Real estate is predicted to appreciate 34% this year. Rates are near all time lows. Buy now or be priced out forever. Owning a home is the American dream. It will be double next year coZ we live in Zimbabwe. Phoenix is a great place if you like frying eggs on the sidewalk. Guess it’s better than Green Bay. At least they had Aaron Rodgers.

We used to fry eggs on the sidewalk in suburban Chicago.

This is the same sentiment all the realtors told everyone back in 2005-06…”Things will get worst .. BUY now, Buy now”, and we all see what happened in 2006-2007. It about to happen again. The reason we have so much low inventory now is because we have too much speculation in real-estate these days, along with many wall street funds buying up whole neighborhoods. The low inventory is also because of artificially low interest rates that have been kept so low, for so long. Inflation is now hitting hard..these rates will have to be raised to normal levels (or higher)soon.. which may end all the speculation, but at the homeowner’s expense( again).

Draw a radius of 2 hour drive from the”BayArea” or any big metropolis and you’ll see how much damage it does to affordable housing in rural areas such as the Central Valley.

Soon it will balance out and folks will sit tight..

But until then, blue collar folks are getting squeezed out.

Blue collar workers are moving out. Out of state or into their cars. Or the bushes.

They aren’t making anymore Fresno.

Xavier Caveat, you certainly do have a way with words.

Amen. Blue collar folks and the poor are getting what remains after the rich took the elevator. Prior “low income housing” programs were made into jokes to give tax breaks to rich developers. We need housing projects that build small, low-cost housing for first time owners and the poor.

LA has a tiny home program for the homeless that is a great idea, so long as it is policed adequately, because many of the poor have substance abuse problems and may be used by dealers. Ideally, treatment should be provided with maybe a sanctuary system to enable drug users to get over their addiction or at least become functional.

It is frustrating the endemic corruption within our system that resulted in more than 100,000 Americans dying from opioids per the CDC in 2021 and thousands more dying from drugs or the effects of drugs, e.g., suicide or related health problems. Think about how much money the ultrarich parasites in organized crime who sold them those drugs made, because for each dead opioid addict there are dozens of live ones.

Our concrete guy showed up in a beat up Tacoma a few months ago to do work. He did work on our property and then our neighbors all flagged him down to do work on theirs. This concrete guy pulls up yesterday to our neighbors… he’s now driving a 70k+ brand new truck. Blue collar guys are doing alright in this Valley but it reminds me of 2005, 2006 all over again. I know several construction related people who had to file for bankruptcy and give their fancy trucks back to the bank in the last bust… some of them weren’t around to remember or have forgotten about that time.

In fact, our former neighbor used to be the largest insulation distributor in the valley last boom round. He lost everything in the last bust, the trucks, the house… Know several general contractors, plumbers, roofers, dry wallers who went back to 15 year old work trucks, and nearly lost their homes. It’s interesting how some of them make large purchases thinking the demand for their services will stay strong long enough to pay their mortgages and ten year big truck notes.

Invert it, that’s real wages for young people, not the real wages you see on the graphs that use CPI.

Young and older people live in different countries.

The former pay for the latter.

Tastes Great! Less Filling!

This is absolutely true in generalities. And the folks who have a lot are generally blind to that fact or how it effects the overall real economy. . However, I’m seeing more and more elderly people on the streets. Living in the rough will kill some of them.

A friend of mine is in her 70’s and her health isn’t good. She’s just gotten a 60 day eviction notice even though her rent is paid up. I offered her to stay with me but she will probably try to move out of state. If she can find something she can afford. My place is extremely small. She may end up in a tent or couch on relatives land.

that’s a shame, but it’s an anecdote.

Younger people will mostly be like this. Renting, no savings, no pension, lower standard of living.

That flippancy is either disingenuous or completely out of touch. It’s also reeking of missionary-ism as I agreed with you for the most part and also agreed with your basic tenent.

Take a long walk in any city’s tent city area and tell me what you see. I see 60-80 YO people living in the bushes in my area. Many more in their late 40’s and 50’s. In addition to so many young people.

How is it flippant to write that it’s a shame?

I won’t be continuing further down this highly unproductive path, however my point was that your mention of someone you saw is, by definition, an anecdote.

Now, back to data. For the next generation home ownership has fallen, savings have fallen, unfunded defined benefit pension schemes have ended. There will be more poor old people from the next generation. Far more. And no anecdote can change that reality, nor any appeal to how sad I am about it compared to how sad you are about it.

Grow up man. This is class warfare; not generational warfare. Want to know what life was like for the so called boomer generation? If you came of age in the 60s your ass was targeted for Viet Nam (unless you came from a monied back round in which case you may get a college deferment). People didn’t eat out except maybe once a month. Credit cards were only for the well to do. You needed to put down 20% of the purchase price to buy a home.

Fast forward to the 70s. Stagflation. Low wages. I graduated from college at a time when I was lucky to get a $13 an hour job. Sure housing was much cheaper but if you brought a home by the end of the 70s the interest rate was as high as 18%.

And what has this generation of “leaders” given us? AirBnB which has taken a significant amount of housing off the market and promoted a world wide travel boom unimaginable in my day (so that housing in those locations can be taken off the market for even more “vacation rentals”). DoorDash and all the other ridiculous ventures that makes like “easier” for those uninvested in shopping and preparing meals. I literally could not afford to eat out during the 70s.

I just don’t see where this new generation has done anything to roll back the tide of the elite as they consume a greater share of the working man’s labor. What specifically are you doing?

All I see from the Millennial generation is an almost hero worship of people like Elon Musk or Steve Jobs or whomever is heading up some “new age” corporation. They all use services like the aforementioned DoorDash (or whatever) to fritter their earnings away just to make things easier.

Life is more difficult in many ways in today’s world but focusing your rage on a generation that endured a lot of problems you don’t even seem to be aware of is a waste of life.

“Living in the rough will kill some of them.”

That is a feature, not a bug.

Does anyone have any good stories from when Phoenix collapsed in the last bubble burst?

Curious whether if we are seeing any similar pre-indicators right now.

The house next to the one I currently rent sold for $120k in ‘12. The house on the other side just sold for $800k.

I work two jobs and make a decent living, I cannot afford a house anywhere in the valley. The upper end of what I could safely afford is $100k lower than the average price. Bottom of the dist. curve gets sold in days for cash to speculators and large landlords.

If that is happening in the Phoenix area we are doomed. It will either crash or the entire country is going down the drain. Or both.

If IRC the phoenix area was last or second to last to explode just before the GR. A year after it started to explode everything crashed.

I think it’s gone further than just before the GR though, even small towns in Ohio and Utah have blown up.

This housing bubble is worse than the last one. The prices are more insane and it’s a lot more distributed. The actual economic fundamentals “suck” too. The economy is fake.

Look at the charts for Dallas and Denver which weren’t in a bubble last time. I live in the metro ATL area and though it’s not nearly as bad as many other cities, I’d still call it a bubble. Prices used to be “reasonable”.

Augustus, I lurk on an investors’ forum. The reason Dallas went up is because there were new jobs there when there weren’t new jobs in many other areas of the country. It snowballed from there.

Denver has blown up because of the weed industry. The Weed industry is way overblown but it’s not seen as such. At first a ton of weed money came into Denver. Then it snowballed.

But I don’t see any reason small towns in Ohio or Utah have blown up. There is literally nothing there. People are moving out of Ohio towns and onto the streets in warmer climates. IDK what they are doing in Utah. Possibly just floating around in that deadly heat.

You couldn’t possibly engineer a better way to ruin countries and render it’s citizens unfunctional than this economic scenario. As effective as an actual war.

Lynn,

Utah has some huge data repositories for the govt. It’s a big tech area because of these data centers. These data centers are massive.

Thanks Petunia. Wow. It must have blown up the whole state on speculation. I saw it in a town so small and so very far away from anything.. Talked to a local who was worried where people were going to move to because they could no longer afford it there. If they couldn’t live there then yeah, where would they move to? Under a bridge in SLC?

Central Ohio is having a huge affordability problem and I think it will become a big business problem in the long run. If enough people become use to the multigenerational home, then corporations will lose scientist, inventors, and innovators to new startups that are family owned and operated. New businesses will start encroaching on the bottom line. That is when investors in RE will be banned from owning single family homes. I think that will bust this bubble. The job reports are telling.

Gabby Cat that was certainly thinking outside the box! I think you’re right, makes perfect sense, but I don’t know if many corporations are going to put 2 and 2 together.

During my business travels I buy local newspapers, cut out the most interesting articles and add them to my scrapbook.Almost all that stuff is online now but yellowed scrapbooks, like diamonds, are forever.

Phoenix,AZ in 2011:

“Stuck in Phoenix, the epicenter of housing crisis”

=In metropolitan Phoenix, two-thirds of all residential mortgages are underwater. Of these, some 200,000 are 50% larger than the current market value of the properties. Many homeowners have come to doubt whether they’ll ever retrieve their lost equity.=

=Adam Stankus, a hotel manager in Tempe, and his schoolteacher wife are in the enviable position of being prospective buyers in a buyers’ market. They hope to purchase the home they currently rent in the suburb of Buckeye for under $50,000. Lucky to have savings equal to a 20% down payment, Stankus believes their monthly mortgage payment will be well below their $800 monthly rent.=

Also I took many Polaroid pictures of new housing developments in the process of being bulldozed over for the lack of buyers.

Sic Transit Gloria Mundi.

Translated into English it means “Every Bubble will pop”

Brent, while all that was going on in 2011 in Phoenix, I bought a 2,000 SF, 3 year old brick ranch house in Spring, TX for $64/SF. They were everywhere, and I only had enough to buy one at the time. Daughter lives in it now. Best deal I ever made in anything I invested in.

TX is my favorite state.Unfortunately I am not qualified to live there.More than once I tried to drive 148 miles on I-40 across the handle of Texas Panhandle in less than one hour and never quite made it.Amarillo always slows me down,that f… speed bump.

Speaking of bubbles…

There is a song dedicated to popping Bubbles – “99 Luftballons” by Nena

I was stationed in Germany in the 80’s and we danced to this tune and grossly misbehaved any way we could.Because it were Ronnie Reagan gung-ho years.

Another Nena’s song describes the evicted family living in the cramped hotel room, begging the Fed to re-inflate RE Bubble:

HILFE ! RETTE MICH !!!

(HELP ! SAVE ME !!!)

Nichts auf dieser Welt ist schlimmer

Als ein leeres Hotelzimmer in der Nacht

Wenn die Einsamkeit erwacht

Nothing in the world is worse than empty hotel room during the night – when the lonliness wakes up.

Brent, LOL! I was in Germany 1965-66 during the “Johnson” years. I don’t quite remember those songs, but I do remember the partying.

The U.S. Census Bureau quarterly rental vacancy report showed rental vacancies north of 10% before the foreclosure crisis peaked. In Florida there were “For Sale” signs everywhere in 2012. The banks had offered NINJA loans – no income, no job, no assets – not a problem. Money was easily obtained, hard to pay back. Bad debt brought down the U.S. economy.

From what I understand, there are no accurate vacant housing unit statistics. If no one answers the door or the neighbors don’t chime in then the home is not counted by the census bureau as vacant. IDK what it is counted as or if it is even counted. AFAIK they are the only entity counting them.

Does anyone have any good stories from when Phoenix collapsed in the last bubble burst?

Looks like a repeat of the Market in Las Vegas

when I bought Homes for Next to nothing and made a lot of money. Thank You Wells Fargo Foreclosure Department!

I wish I never sold them! I Had no Idea What J Powell was going to do I could have more than Tripled my Huge profit rather than selling out in 2017

I bought in 2012 sold in 2017

It’s not 2012 Yet but it sure looks like it’s going to Head that way!

All the People who Buy Now or who have already Bought at these Huge Prices are going to have to walk /run away from those Loans I predict.

Who in their right mind? is going to keep a property

They Paid something Like $300,000 to 400,000 OVER: what it going to be worth when the Bubble Bursts?

Your far Better off to Walk away go Bankrupt and start over again because it far more affordable to do Just that.

Who wants to stay? in a $300,000 Property

They Paid 800,000 for? and still Owe 500,000 on?

Easy, the ‘gotta have it’ crowd. Didn’t you know, it’s everyone’s (anyone’s?) government given right to own a home (at any price).

Just for fun I will share the optimistic side of things. Optimistic from my perspective – there will be an opportunity to make money and hopefully regular people will be able to afford homes again.

I went to grad school at ASU, beginning in 2011. Another student who became a good friend of mine took a small inheritance and bought a small house when he arrived (also in 2011). He was absolutely broke trying to keep up with this mortgage on grad school stipend. After two years he sold it and moved into a crappy apartment like the rest of us, 100k richer, a staggering amount of money considering we were all earning sub 30k/yr.

Go Sun Devils!

I sold my house last August. When I saw what my neighbor got in April, I knew that 60% appreciation in 18 months spelled trouble. Take a good look at the Phoenix and Las Vegas charts from 2002-2010 and compare and contrast with the San Francisco Bay Area Condos.

If you live in a place that has had a big runup since Summer 2020, your best case is the Bay Area and that’s if your area does indeed limit building. If they don’t, then you’re Vegas/Phoenix. I live in a Vegas-Phoenix type market.

Marketwatch article about the ongoing ukraine-russia conflict indicates inflation may go to 10% and has a quote from Blackrock that the Fed may have to live with 10% inflation. Yea, because that favors all their investments in single family rentals.

Dark times ahead one way or the other.

Abomb,

“…has a quote from Blackrock that the Fed may have to live with 10% inflation.”

Hahahaha, Blackrock talking its own book, which is bonds and bond funds, which WILL get killed as the Fed raises rates and unwinds its balance sheet. These Blackrock gangsters should keep their mouth shut and start working on their communications to their bond-fund investors that are going to lose an arm and a leg.

Blackrock vs Blackstone.. Didn’t one spring out of the other? Aren’t they still affiliated or co-invested in some ways? Are some of Blackrock’s holdings in Blackstone?

I looked at it but it brought up more questions for me than answers.

The Fed and Blackstone have the same agenda. I consider Blackstone a mouthpiece for the Fed. And they certainly have a say in what the fed actions will be. Just look at who JP called on day 1 of the Covid crash. Anything Blackstone signals has to be considered as a very possible outcome now. Sad but true. Inflation at 10% would be brutal, however it will be mass communicated as something where nothing can be done unless we dare risk a depression… and the 63% home ownership in the US along with all the beneficiary’s of stock market gains will happily look the other way on those hardest hit by these unjust fed policies/decisions… just my opinion, Wolf.

Fresh wisdom dispensed daily. Get on the waiting list for a Wolfstreet mug.

Look out below.

“may have to live with 10% inflation”

Yep. and that’s 20% inflation in the honest 1982 CPI that Volker was facing.

Thanks, Fed. You ruined an entire nation to please the rich.

Instead of throwing all that money to investors we could have granted low interest loans to people who were going to build and LIVE in their newly constructed houses with a mandated stay of 4 years or to small time developers for apartment buildings.

But no, we had to feed the bloody sharks.

Most countries limit foreign investment in their housing stock in some way. They actually PROTECT their citizens. Try buying a residential property on the Mexican coast or Costa Rica or China if you are not a citizen. We need protection from both from foreign and domestic investors at this point. The whole thing has snowballed to the extreme. World wide.

Pervasive corruption. The country is rotting from the inside out. This is capitalism in it’s purest form despite what all the brainwashed masses will tell you (and the retired ones who lived through an anomalous period of prosperity in this country dependent on a decimated Europe and exploiting the labor of 3rd world countries will no doubt come running to say that we actually need more capitalism and less regulation, just give it another shot) . Monopolization, financialization, and regulatory capture. Demographically, the bottom has fallen out of the pyramid scheme, everybody is atomized, birth rates are plummeting, younger generations are all checked out, and we’re now seeing the parasites sucking the marrow out of what’s left of the middle class.

Any system is prone to corruption unless it’s societal values actually change.

I’m hoping it’s more comparable to a ‘colonic cleansing’.

It’s not all doom and gloom for young people. My friend’s daughter just graduated last year with four year degree and is a dental hygienist. Got at least three offers and is making very good money at 24 years old. Buying her first home at about 2.2 X her salary.

My daughter, her husband and my nephew are all engineers around 40 years old and are doing well. My nephew’s wife also around 40 got her MBA, works in HR and makes more than the engineers.

No, and good for them. But each generation that has come of age since somewhere around 1973 – 1976 has had less opportunities.

Our young neighbor just graduated from nursing school, and has an incredible first job, complete with substantial signing bonus.

So, yes, not all doom and gloom.

Nurses are in high demand because of Covid AND all us old people getting older.

Government “affordable” housing programs make housing less affordable. So does central bank monetary policy.

This is aside from any other distortions created by tax policy or local governments.

If you want affordable housing, get the government out of housing by eliminating mortgage guarantees and interest rate price fixing.

For the benefit of lower income Americans, properly enforce immigration policy which would both reduce demand in metro areas and increase their bargaining power to obtain higher wages. People need affordable shelter which doesn’t require home ownership.

I do agree with you that foreigners don’t have any right to buy real estate in another country, though it would be a lot less or no problem in the US if the government wasn’t distorting the housing market.

I think citizens buying N homes as and “investment” is N times more of a problem than a foreigner buying one.

“Government “affordable” housing programs make housing less affordable.”

Not necessarily. It depends on if they are sincerely trying to do what they say they are. Usually not. And how much corruption there is down the line. For instance “Affordable” housing built in Santa Cruz Ca in the 2000’s was aimed at an income of 90K for instance. Other places spend far more per sq ft and pr unit in construction than what is remotely reasonable.

How much housing could the US government have funded with $2T? I said funded, as in paying for and loans? not outright paying for all. The programs they have in place for such things “waste” or pocket so much. Just like our infrastructure funding.

Would be a good investment for the security of the country at this point to hire more forensic auditors. Would save more money than anything else I think.

Government programs inflate demand by either allowing someone who cannot afford to buy at all to buy. Or, buy a more expensive one.

It artificially inflates demand that otherwise would not exist.

This is the economic reality. It’s Economics 101. You are allowing sentiment to change your perception.

What I am describing to you is the same with higher “education” and health care.

Any area where the government comes in to make it “affordable” results in the opposite. If progressives get their way, child care will be next and it isn’t affordable even now.

” You are allowing sentiment to change your perception.”

“Government programs inflate demand by either allowing someone who cannot afford to buy at all to buy. Or, buy a more expensive one.”

Respectfully, I think you missing the point. Studies have shown the buyers who foreclosed in TGR were by far investors, not homeowners. Families who own one single home will do everything they can to keep it. Investors will walk away.

The system is rigged for investors, and large ones at that, not home buyers.

You know, it wouldn’t be that hard to initiate a compromise on immigration if either side was sincere. Properly enforced, decreasing illegal immigration and increasing legal immigration could work- most working immigrants in my state are illegal anyway.

The problem with that is too many industries rely on slave labor. What else do you have when people will work for less and have no rights?

It’s not right. OTOH, all my neighbors who have lived and worked their butts off here for well over 20 years deserve full citizenship.

nobody “deserves” full citizenship because they managed to get away with breaking the law for 20 years.

it should be done on a case by case basis, based on literacy tests, ability to support oneself, iq tests, and so forth.

Jake W – IQ tests, don’t even go there. It’s pointless, it’s over. But there is also good news: we are rapidly approaching a time when humans will be genetically engineered / upgraded via the germ line. Our global devolution will reverse soon, unless we blow ourselves up first.

You’re missing my entire point.

The point is contradictory government policy. The government allows millions of people who have no legal basis to be in the country which inflates housing demand. They have to live somewhere, even if it’s piling in somewhere like sardines.

This undeniably inflates housing costs, especially rentals since most of these people cannot buy yet. (Don’t worry, I’m sure the government is working on that to.)

Same thing for wages. The lower income groups of legal residents can afford less housing due to both inflated demand and lower wages.

Legalizing illegal immigrants is an idiotic solution. So is subsidizing housing to make it even less affordable.

What I describe here wouldn’t in and of itself resolve the affordability problem. It’s an example of how idiotic government policy always makes things worse and usually for those least able to respond to it.

@Jake W

The persons washing your cars and dishes and picking your vegetables and fighting in our military, “illegally” for twenty years are most likely not literate. What about the “illegal” companies that employ them, illegally. Should they be citizens?

Long term trend is US population growth is 0.5% and productivity is around 1% to give real GDP growth of 1.5%. It seems clear to me that with birth rates so low, that government ‘s long term position is to keep population growing by legal and illegal immigration.

I know an immigration lawyer. It’s very long and expensive road to go the legal route as court system is backed up.

Augustus Frost, No I’m not. I actually agree with you on most of it. I’m talking about a compromise that might work. Certainly better than the 2 sides fighting over it endlessly and not accomplishing anything.

By increasing legal immigration and making the steps to citizenship clearer – (NOT unlimited immigration by any means).. AND simultaneously stopping illegal immigration..

We would have less immigration total. PLUS those that immigrated would not have a semi-slave status in US. They would have rights.

I think the DACA and PACA programs are bullshit. Giving people limited amnesty that has to be renewed periodically with the threat of revocation is a hell of way to live. It’s a false promise.

A good compromise would be to give DACA and PACA people who have been here for a long time full citizenship if there are no felonies. Improve immigration processes and increase the allowable numbers somewhat. AND build the wall, so to speak. This would decrease ACTUAL – legal and illegal combined, immigration numbers.

I don’t particularly like Trump but I think he came up with a similar idea or suggestion and the Dems didn’t bite. Because they (and the Repubs) benefit from a semi-slave population. I mean hell, lets call it what it is. It’s wrong.

LoL, the market top is in. My brother in law said “This time it’s different.” His sister nearly choked on the beef round roast Sunday dinner. She later said she wanted to hit him.

Someday this war’s gonna end…

Predicting bubbles are a funny business. Have you ever observe a bubble floating close to destruction only to catch an air current and lift to amazing heights? Others do not pop even after landing on a sharp blade of grass. Then other bubbles pop from nothing at all. I hope this bubble mania calms down soon.

although mortgage rates are closer to 4%, I still don’t see any slowing down in the market yet.

4% is cheap money. I remember when I got an 8 1/2 % mortgage and I thought it was cheap. I also remember 18% mortgage money in 1981.

4% is cheap if home prices are reasonable.

A bunch of my friends were priced out of market because the mortgage rate jumped 33%, ie 30 yr rate from 3% to ~4%.

On top of this, inflation is taking a bite in to their affordability.

jon,

If your friends couldn’t afford 4%, then they truthfully couldn’t afford 3%…

Affordability is subjective…

I use an affordability matrix based on a 1 year, 3 year, and 5 year planning…

In that matrix, you have to plan forward on likely scenarios that can and will bite you… such as projected income, loss of an income, new roof, new appliances, auto replacement or repair,, tax and insurance increases, inflation increases, home values decreasing/increasing, etc…

This is your blueprint that governs what you do everyday…

My one year is pretty much spot on, my 3 year is about 50% correct (right now) and the 5 year is a crystal ball…

You have to pay attention… how I live today was projected a year ago and it’s actually way better than I planned for…

It’s not hard but you do have to be honest and use worst case scenarios…

Otherwise you’re just fooling yourself….

Sorry if it sounds like preaching, but it’s just how one guy does it…

He can afford 4% but the monthly mortgage along with price hike is hurting him like anyone.

Another friend in san diego looking to buy 1.4mill home is surprised to know that his insurance cost per year would be ~$7K because almost all of san diego come under fire hazard area.

The point is: Price hike is coming and hitting people from all directions. Something has to give in.. Let’s see

Anthony A.

4% is cheap money:

The Rate is Not the Issue.

Forget the rate It’s about the Value? the Investment How can anyone not see that?

Just Look at Wolf’s Charts he Put up they are real

he did not make them up.

Do you really think at today’s prices? Now is a good time to invest?

I suggest you read the articles & slow way slow and digest what’s Happening

The Market is set to fall, and the WAR has started. The dollar has become weakened by the crazy Fed trying to Trick USA and the Public is going to suffer and has already. There is a reason why all the prices shot way way up it’s because the people in control have set the stage.

A Low Loan rate is a sucker Draw and if that’s you be ready to take a Loss unless you’re a Day Trader and if so, you better look closely at the sucess Rate. What would have happened the “Last time” if no-one bailed out the Banks.

Who’s going to Bail them out next time? You Perhaps

My comment was not about value it was about the rate. I’m living in the 8th house I have bought over the years and I understand what you are saying. I never said today’s prices are a good time to invest. The last house I bought was in 2011 at $64/SF (3 year old brick ranch in foreclosure).

Actually, it’s a great time to sell your inflated house.

This stuff is insane.

A friend of mine in his early 30’s just bought new construction home in phoenix about a year ago. He said others in the subdivision are already going for $80k more than they paid. I think they paid around $450k.

There is no way this can continue for long.

Said everybody for the last 18 months. Somehow however they just keep making new highs. This is almost tracking like the stock market since Feb 2020 where all it seemed capable was ATH. Then it wasn’t. Perhaps the FED QT and rate increases in about a month will actually begin to constrain the money supply enough to slow inflation. There is no thinking we can contain in that quickly. Too much loose money policy to try to ward off the R

I predict the Mr Powell will do the opposite of Teddy Roosevelt. He will speak loudly and carry a small stick, at least for as long as possible. US long term real growth rate is 1.5% and with insanely high debt to GDP it’s going to be tough to Goldilocks it from here.

The $80K: How much of that is driven by cost of materials?

Lumber packages are up. Window units are up. Appliances are up. Concrete is up. While the $80K sounds like the market is nuts, consider the replacement cost if it needed to be rebuilt today.

You”d better hope that you don’t have a war with Russia.

You think people under 40 are going to fight for western countries where they rent, work all hours and have no savings?

How could the new guy be worse than this situation? They won’t lift a finger.

That’s quite the assumption. I’d like to see you back it up. Comrade.

Okay a few quick points:

1. yes it’s an assumption about the future, would you claim now is like 1930s for patriotism among the under 40s? That would be a bigger reach.

2. why is everything on american forums reduced to calling people a communist? What did I write that makes me a communist?

I agree with your point #1, as a guy in his 30’s. I still love my country, but I lost a lot of faith in our military and leadership with the middle east wars. My friends with military experience are all now neutral or negative on the whole thing.

For #2, it’s because American’s are taught from a young age that communism=bad. They never really seek to understand economic systems at a deep level. Capitalism good, communism bad. That’s all the average American feels they need to know.

random guy 62, i’m also in my 30s, and i agree with georgist. our generation is being financially raped by the boom generation. why should we fight for them?

You wrote nothing to that effect. Intelluctual laziness yields those comments. The fact is that America has been successfully Politically Balkanized by divisive and manipulative politicians. An impressive Russian historian wrote about this a long time ago. The name does not matter because he’s a commie also. The commie label is a fall back learned behavior. This behavior was demonstrated on MSM recently when the A.P. reporter Matt Lee was basically called a commie becaused he pressed a State Dept. spokesman on providing the de-classified Intel that backed up his claims during a Press Conference. It would be better to just issue Tass or Pravada Soviet Politoburo type dictums to the people and stop the charade. Our money was not de-based to the point of being nearly worthless by a foreign power. The Gov’t loves to hear the people call each other a commie. They started it.

Wolf wrote:

“But the home prices here don’t yet reflect the higher mortgage rates. Today’s “December” data are a three-month moving average of closed sales that were entered into public records in October, November, and December, reflecting deals made roughly in September, October, and November, when the average 30-year fixed mortgage rate hovered at around 3%. On Friday, the average 30-year fixed rate was 4.08%, according to Mortgage News Daily.”

It’s 4.12% today for conforming 30 year mortgages. But for Jumbo 30 year mortgages it’s just 3.62%. Does this mean that the more expensive end of the market will be less likely to crash?

Wolf wrote:

“national home price inflation is now 179% since 2000. Over the period, consumer price inflation, as tracked by the CPI, has risen 67%.”

CPI Rent of Primary Residence is up 97.5% since Jan 2000.

Strangely, CPI Owners Equivalent Rent is up only 79.5% since Jan 2000.

Yes, both of them are rent-based. The first based on actual rents paid by tenants; the second based on what homeowners estimate their home would rent for. But they’re starting to surge … catching up a little (only a little).

> the second based on what homeowners estimate their home would rent for.

This shouldn’t be used for anything, ever as it’s clearly totally invalid.

But the second (OER) has been the higher of the two for a year, picking up the rent inflation earlier and showing more rent inflation:

“Rent of primary residence” rose by 3.8% in January compared to a year ago (red in the chart below).

“Owner’s equivalent rent of residences” rose 4.1%. This measure, used to estimate the costs of homeownership as a service, is based on surveys that ask homeowners what their home might rent for (green line).

That’s interesting that OER was historically lower than actual rents paid. I would have automatically assumed that homeowners would have over-estimated potential rents?

Massive spread between the two compounded over the course of a decade.

For me the whole idea of OER is just absurd. Why is this even a thing, when they have the data on real rents.

Why not replace supermarket prices with the equivalent estimate if some guy on the street owned a supermarket?

the oer concept is absurd because most people have no clue what their house would rent out for, any more than they have a clue what their used car would sell for, without doing research.

Homes are a traditional hedge against inflation. Some of the rich went all in on real estate. Typically the stock market outperformed real estate, but not every year.

In 1974 Joe Biden bought the 10,000 sq ft Dupont mansion for $185,000 dollars.

He moved to a custom built home on four acres with a twenty car garage. Biden’s father managed dealerships. Biden collects cars including a 1967 Corvette Stingray.

Friend of mine is being offered to move to Northern California from Southern California to run two new branches of an expanding title/mortgage company. Gave her my thoughts. Pro: Great opportunity for job growth. Fresh start. Con: Market could go quickly south based on many factors. Leaving SoCal and uprooting family is challenging and complex.

Her sister a realtor voiced her support to sell and take maximum profits from SoCal housing.

Nathan – geographical arbitrage? If it makes sense, do it. Those kinds of decisions are personal. I’ve lived in northern california and don’t care what the losers say…

Seems like it is likely that party is coming to an end. 2 / 10 treasury spread is down to 0.4% while the bubble is still inflating. Things could change very quickly.

Treasury yields stopped predicting the economy when the Fed started buying Treasuries in 2008. The Fed needs to sell a big part of its holdings, and then maybe the yield (which will be much much higher) will mean something again.

The Fed is talking rate hikes, which pushes up the short end of the curve that are impacted by those rate hikes; and the Fed is STILL buying the long end of the curve, and owns a HUGE Part of the long end of the curve, both of which push down long-term yields. That’s why the yield curve is now meaningless.

Free free markets

That’s an interesting view. I would think that would be a minority view in the market. I would make the counter point:

1. Fed only owns about 25% of the bonds, so they don’t totally control the market.

2. It’s not a sure thing Fed is going to be able to run off very much of their balance sheet without economy stumbling.

3. It’s not a sure thing that rates will be higher in one year because of very high debt levels. Economy may stumble with two or three rate hikes. If economy goes into recession it will kill demand and most inflation

It’s going to be an interesting 2022.

I have been reading up on the Mississippi stock bubble and the French revolution that occurred about 60 years later. Calamity came when they tried to ease out of the financial asset bubble both times, but they were not able to prevent the panic either time. I see central banks in a very similar position. Maybe that’s why they went in so big during the Pandemic as a panic is a dangerous situation

“1. Fed only owns about 25% of the bonds”

Hahahaha, yes, but this “only” is a huge gigantic amount and huge in proportion, nothing and no one comes even close. And the Fed doesn’t sell one thing to buy bonds with; it creates money to buy bonds with, and it doesn’t trade, it only buys, and everyone knows that, and the whole thing has hugely pumped up the markets.

See what’s going on in the markets even at the mere suggestion that the Fed will reduce its holdings? Wait until the Fed actually reduces its holdings. The long end of the curve still cannot react to it because the Fed is still buying it, but the stock market is reacting to it.

Shiller prose, BCOM on Prozac since the 2008 bubble bust. BCOM is back to BC/AR area from Feb/ Mar 2003.

If Shiller prick, or rise moderately and BCOM fly, in real terms the housing market will (sharply) decline.

BCOM is Bloomberg commodity index.

Not much chatter here about institutions’ role in run-up of single family home prices in major markets.

1) What is magnitude of institutional buying?

2) What lending rates (or other variables) would cause institutions to stop buying or, god forbid, actually sell their holdings?

Are you talking about MBS?

Money managers, pensions, insurance companies, REITs and such, is what I was wondering about…

Just a rough guess at why inventory is low and demand for investors is high.

If a RE Investment company purchased a house for 800K cash + (16K taxes + 8K maintenance per year) and they can rent it for 4K/month, the approximate ROI is:

48K-16K-8K = 24K

24K/800K = 3%/year

With rent increases at 30% in some areas, the ROI continues to go higher.

These are likely put into REIT bonds and sold paying 2.5%/year.

This is better than a savings account or S&P 500 dividend fund.

When savings rates go above 3%, the demand for these REITs should plummet. Will this cause a flood of investment rental housing to hit the market as REITs try to recover the gains part of their investments?

This is just a rough guess on why housing demand is strong from investors.

In which part of the country are you buying at 800K, renting for 4K/mo?

That seems a little steep.

A friend of mine rents a 2.6M home for 5K/mo in the Seattle/Bellevue area.

This is happening in my hood aka San Diego. Home sold for $800K would fetch would $4k/month rent.

I used 4K-5K rent for an 800K-1M house since that is the rate a relative is seeing in Goleta CA. They confirmed with Realtors (and Zillow)

800K is a typical 1960’s tract house in coastal CA in that area.

I’m sure there are distortions at the high end for any area.

ie a 2.5M house is rarer in these older neighborhoods and would not rent for 3X, $12K.

The Blackrocks are probably not gobbling up high end homes either for rentals which causes more distortion.

Likely your friend is a great tenant and the landlord is not raising rents by 30% so he can keep him.

In some major metros, buying a habitable house for $800K is no longer even possible.

Southern California has some of the highest payment to income levels in the nation. So I guess if you are talking about that market, then yes I suppose 800K could fetch close to 4K, although I still think that ratio is pretty optimistic.

Many, many (most, if not all?) other markets would struggle to rent for 4K at 800K purchase price.

Bob,

You would also have to factor depreciation and tax deductions into the ROI…

Which would probably give a higher net ROI….

COWG, You are correct.

A rental is a business so the asset is depreciated and all maintenance and taxes are written off on Federal/State taxes as a business expense.

As a potential buyer, an 800K mortgage with the taxes and maintenance above would be:

4% 30 Year loan $800K (zero down for comparison)

Monthly PI = $3819

Monthly Maintenance+taxes = $2K

(Not tax deductible since a homeowner cannot deduct maintenance and are capped at 10K/year for taxes. It only makes sense to itemize if you are over the std deduction)

=$5819

You’d have to make at least $120K in income to qualify for this loan.

A homeowner cannot depreciate the house either for taxes.

It would be cheaper to rent from the REIT in the short term while they reap the profits and tax benefits of a business.

Is it irony that if you are trying to purchase a house and you have your 401K and down payment invested in a REIT, that you may be losing bids on a house to a company that is using your money to purchase your starter home from underneath you and driving up home prices?

The sad part or maybe the criminal part is that you could make the case that with sound money the price of a home would be basically flat for many decades.

Home building has gotten more efficient as more components are factory made (a door for example) and foundations are quickly dug with equipment (not with a shovel).

Agreed. But we don’t have sound money!!!

Hence the reason why housing jumps like the way it does, hence the real estate hoarding, etc.

Hence the “shortage”. If we took away the low interest rates / price controls, the markets would find its own equilibrium and consumers would consume housing in a more rational manner.

Your theory doesn’t consider the rising cost of buildable land, taxes, government fees, permits, government mandates (road improvements) etc..

More to it than brix and stix.

its investors and all cash deals that’s driving prices. they’ll buy your home and then rent it back to you. Schwabs “you’ll own nothing and be happy” plan.

b,

Somebody is SELLING to these people….

You may find truth when you ask the seller why…

“But the deals were made when mortgage rates were still 3%, not 4% as today.”

That’s a crucial caveat … the deals now being made will show a retreat in the pace of increase if not the level of prices. We see it in other asset markets; it’s only a matter of time before we see it here too.

Agreed. By the spring and summer I bet we will see HPI plateau or even dip in some regions

Two biggest threats to AZ real estate

1. Lack of Water

2. Illegal aliens permeating the communities

3. Out of control summer temps, if it hit 117 in Portland, why couldn’t it be 132 in Tempe?

Water would always be available but it’d be very expensive. I see it in southern California, all utility bills are increasing every year

Lotsa hate on here for Arizona. I live here and am amused by what people are willing to pay for these boxes…. Of course, some of them will drive a Cullinan or Huracan to the Safeway, so what do I know?

In our little corner of Arizona, the utility that runs our water/waste treatment plant claims to have a 100 year supply available from 8 deep wells within the boundaries of our community of about 3,500 homes/lots, and has, as recently as January 2022, made a presentation at a town meeting to that effect. The effluent is also processed locally and the water is then sold for turf irrigation that then filters through the sandy soil and back into the aquifer. Further, they cannot legally add customers to their service area unless those customers “bring their own water” (aka provide a productive well or other source to serve the additional load). That greatly reduces the urge to further develop this area because you can drill a lot of dry holes in the desert. One neophyte real estate genius, who purchased an adjacent parcel of land, just got stung by that little detail. Might make a nice dog park, but for the coyote, bobcats, mountain lions, and raptors.

The real “threat” to water in Arizona is that used for agriculture… which will effect food prices nationally as the “leadership” plans to cut their supply before it ever impacts the residents (that’s the main purpose of the canals – agriculture). Please note that agriculture uses @74 percent of the available water supply of the state per the most recent propaganda from azwater.gov.

Illegal aliens are a national issue that plagues the entire SW border, not just Arizona. Are you claiming the San Diego and LA prices are “threatened” as well? You do realize that there are airplane loads of illegals being moved around the county, possibly to a city near you?

However, I have only bought houses for use as shelter – not as an “investment”. If it goes up in value, fine. If it goes down, so what? I haven’t made nor lost a dime in the current “market” as I presently have no plans to sell. I’ve never taken an equity loan out of a home for precisely that reason. Those that do are stupid – especially in an unsustainable market and to spend on a pickup or luxury vacation that “you deserve”.

Truthfully, I can’t say with conviction that I know what someone would be willing to pay for this joint any more than I know (or care) what the buckets of bolts in the garage are “worth” as none of it’s for sale anyway. Up until you sell it, it only has it’s utility value.

Besides, the quiet here is deafening, the climate is predictable, there’s little chance of natural disaster (hurricane, tornado, earthquake, sinkhole, flood, landslide), don’t have to take my life in my hands riding public transportation, and the view from our great room is breathtaking. I can pick an orange off the tree in the yard for breakfast or a snack for several months out of the year.

Oh! Wait! Let’s rethink this.

Best to steer clear of Arizona. It’s awful and anyone who lives here is totally stupid. The heat is stifling 13 months of the year. We have bugs the size of turtles, poisonous snakes, predatory cats and raptors that will eat your “fur baby”, toads that emit a neurotoxin, airborne fungi that can cause Valley Fever, and we regularly fry eggs on our sidewalks. It’s dusty (which aids in the release of the fried egg from the concrete for consumption). Nothing but rocks and scrub for terrain. The local Starbucks is overrun with illegal aliens. Scary armed residents because there is no permit required to buy nor carry a concealed weapon. Don’t even come here to visit. Stay in your safe place. /s

Thanks, I enjoyed this lol.

Currently looking at property in greater PHX area…

Used to watch Marty Zweig on PBS’ Wall Street Week, and have ever since remembered his “three steps and a stumble” rule for connecting Fed actions to economic pullback.

No rule works 100% of course, but the simple sentiment seems apt for today’s economy, including RE…

The rules states that “whenever the Federal Reserve raises either the federal funds target rate, margin requirements, or reserve requirements three consecutive times without a decline, the stock market is likely to suffer a substantial, perhaps serious, setback”

(Schade, 2004). This simple rule is still relevant. Although it tends to lead a market top, it is something that should not be disregarded.

Source: Kirkpatrick, Charles and Dahlquist, Julie. Technical Analysis: The Complete resource for Financial Market Technicians; (c) 2007

That was a great show. It got me interested in investing at a very early age.

1) REALOGY RE dominate.

2) USD pump muscles. Both Shiller and BCOM will need Prozac.

3. Tardive Dyskinesia.

Blackrock, Blackstone, Manchurian Global….are they not all one and the same 🤣🤣

I think Blackwater changed their name to Academy because they were tired of being confused with mercenaries.

Lol, thay one went over everyone’s heads

Bubble related: ‘Elon Musk cheers govt investigation of short sellers’

The BIG Canadian experience of a short seller was in 2011 when Carson Block’s outfit Muddy Waters published that China- based but Toronto- listed Sino-Forest was a Ponzi scheme involving theft. Investor John Paulson sold his entire stake for a 720 million dollar loss. Which was less than he’d have lost if he’d listened to the blizzard of counter accusations and law suits from Sino and hung on.

As it turned out, Block was right. In 2017 (fast eh?) the legal authorities determined it was a fraud and named 3 Chinese as the perpetrators. The Sino auditors Ernest and Young paid 117 million towards investor law suits and a ‘who’s who’ of the Canadian financial sector ( e.g. RBC) kicked in over 30 million.

Unfortunately for Canadians and many others, there was no short seller to warn of the largest Toronto exchange fraud: Bre-Ex gold.

To be clear, Tesla is not a Sino. There is a genuine business. But by any standard metric the shares are very expensive. Some of the accounting looks odd. Apparently the lease fleet is not being depreciated because by the time the lease is up, they will receive full Self Driving and be resurrected as profitable robo-taxis.

Musk’s antagonism to doubters does not make the case for the share value any brighter.

The problem is TSLA is part of the SP500 and passive investing owns the market right now. So everyone is buying TSLA at any given price (myself included).

I checked Tesla price today. Stock is not that far away from getting cut in half from all time highs. It seems like manias in stocks like South Sea bubble, Mississippi bubble, Great Depression, Japanese stock bubble, the tech stock bubble all crash between 80% and 90% before they hit bottom.

I kind of expect that for the QQQ again this time.

Germany might lose it’s NG hedging.

Invasion : legally Nuto have the right to close the Bosphorus restaurant.