Powell should pay attention here so he’s better prepared at the next press conference when asked about the impact of inflation on regular Americans.

By Wolf Richter for WOLF STREET.

Fed chair Jerome Powell’s reaction today after he saw the consequences of his reckless monetary policies. Imagined by cartoonist Marco Ricolli for WOLF STREET.

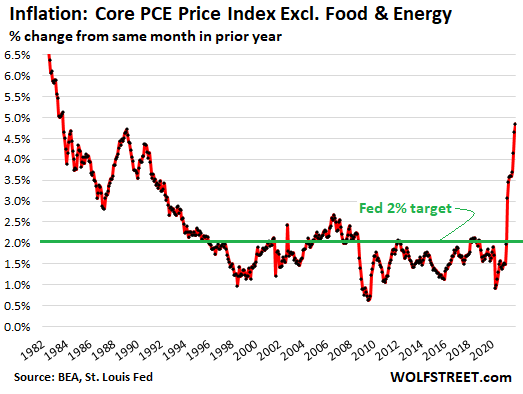

The “core PCE” price index, which excludes food and energy and which understates inflation by the most of all of the government’s inflation measures and which is therefore wisely used by the Fed for its inflation target, spiked by 0.50% in December from November, and by 4.9% year-over-year, the worst inflation reading since 1983, according to the Bureau of Economic Analysis today. As measured by this lowest lowball inflation measure, inflation, is well over double the Fed’s inflation target:

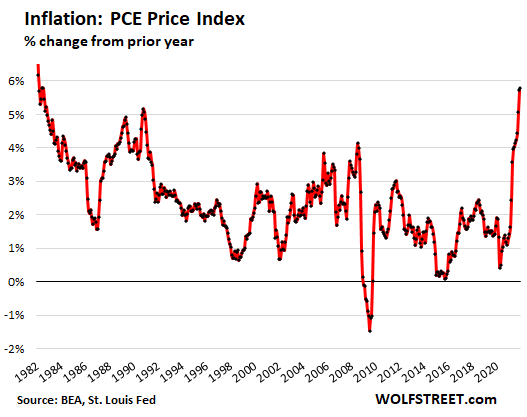

The overall PCE inflation index, which includes food and energy, spiked by 0.45% in December from November, and by 5.8% year-over-year, the worst reading since 1982.

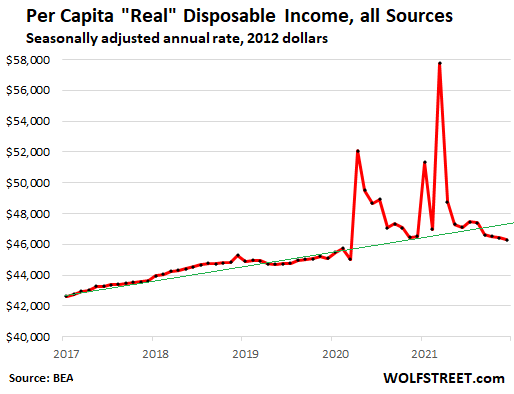

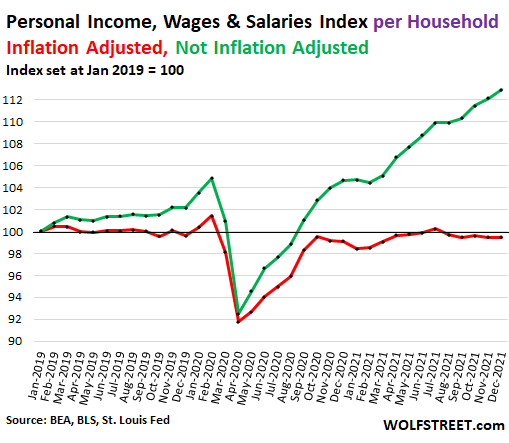

So how did this inflation – the worst in 40 years – impact wages and salaries? Powell should pay attention here so that he is better prepared for the next post-meeting press conference when some wayward reporter asks him about the impact of inflation on regular Americans.

Adjusted for inflation, per-capita disposable income (income from all sources minus income-related taxes, on a per person basis) fell by 0.3% for the month and fell by 0.5% year-over-year, continuing the relentless decline that started last summer when inflation took off at a velocity not seen in decades. Note the pre-pandemic, pre-massive-inflation trend line (green):

Compensation from wages and salaries, not adjusted for inflation, and not including government transfer payments, rose by 0.7% in December, by 9.2% year-over-year. And those kinds of wage and salary gains would be something to celebrate. But they were eaten up entirely by inflation. On a per-household basis, after inflation, those wage and salary gains disappeared entirely, opening up an ever-wider gap between the money people earn with their labor, and what’s left over after inflation.

As inflation whittled down the purchasing power of labor, the rising number of households reduced the slice each household gets of the aggregate inflation-diminished income figures to where inflation-adjusted income from wages and salaries is now below where it was two years ago and below where it was three years ago:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As always, excellent information with great graphs.

Thank you, Wolf!

Wolf: what is the fixed inflow of money to the stock market from standard retirement vehicles like 401k, Roth’s, etc etc?

Resjudicata,

What is the fixed outflow of money from the stock market as boomers are retiring in large numbers and are now drawing on their retirement funds? We just had this huge wage of retirements in 2020 and 2021. Everyone talked about it.

The only figure that would make sense is some kind of net flow (inflow minus outflow). And I’m not sure it would make sense either because investors also shift money between their investment vehicles.

There is a documentary called “Demographic drought” that discusses demographic effects on items like this, which summarised well what many, many articles say. The US is much better off than China or Japan or other countries, even though immigration fell with the pandemic and the birthrate also fell sharply reportedly due to the pandemic but not immune in the long term.

This pandemic will not go away, so people may wait even longer to have kids. Only smallpox was eradicated by vaccination of all persons possible. 100% vaccination rates are not achievable here, since too many believe vaccines will be used to control their minds via chips, etc. New variants will develop and come.

RH,

“The US is better off” — no, it’s not. Corporate America is better off if there are more consumers and more workers (cheap labor). INDIVIDUALS are not better off because they have to divide that pie into smaller pieces. The LAST thing any of these countries you mentioned needs is more population. They’re immensely overpopulated already.

The Japanese and the Chinese individually and as households are FAR BETTER OFF today than they were 30 years ago, in part because their populations have stopped growing, and they don’t have to cut the pie constantly into smaller slices.

You’re unapologetically rooting for the billionaires that need more consumers to sell their crap to, and that need more cheap labor.

“INDIVIDUALS are not better off because they have to divide that pie into smaller pieces.”

Wow!

The fixed pie fallacy is back.

Thank you, Thanos.

You are right that reduced populations (as after the Black Death) are better for ordinary Europeans and Americans as individuals by giving them increased bargaining power but there is a reason why I fear the contraction of the populations of the US and EU: the CCP and its genocides. A weakened West might allow them in the future to dominate Japan and South Korea if they can invade Taiwan. Russia is also a big threat militarily despite its other weaknesses.

The skill/quality of workers, meaning their education, is also critical: that is why Asian countries with better K TO 12 educational systems are so competitive.

I didn’t say anything about Black Death. We’re talking about Japan and China where birth rates are low enough — as they are in many other countries, such as Germany, Ireland, Russia, Italy, the US etc. — to cause the population to no longer grow or to cause the population do decline in tiny increments. Anyone who compares the effects of these low birthrates with the Black Death has a screw loose.

Zero. Unless the new funds are used to buy new issues of stock. Otherwise one person’s purchase is another person’s sale = net no change.

If stocks are sold off, there can be outflows as the price of assets fall and people withdraw from stock accounts.

Mr Wolff

If I buy a stock today for $10 a share from someone else who gets my $10 a share, how is there any net increase of money “going into the stock market?”

There isn’t and that wasn’t the question. The question was about buying-pressure and selling-pressure from specific groups (taking money out or putting money into their portfolios), not from the market overall. Boomers that retired start taking their money out individually, thereby creating selling pressure, and if there isn’t an equal amount of buying pressure at these prices, then prices will have to drop until lower prices draw enough buyers in to create an equal amount of buying-pressure. When selling pressure is higher than buying pressure, prices will have to drop for sellers to find buyers.

Individuals, groups like “boomers,” and specific funds can and do take their money out of the market by selling stocks. That’s what we were talking about. But if there aren’t enough buyers at these prices, then prices drop until there are enough buyers. It’s that simple.

The market overall cannot take money out of the market, but individuals and funds can take money out of the market, and do all the time, and price is the mechanism that make sure that transactions happen.

“And those kinds of wage and salary gains would be something to celebrate. But they were eaten up entirely by inflation.”

A few years ago I joined the ranks of the ‘fixed-income’ set. And inflation has impacted us so much that we have almost stopped eating at restaurants. Consequently, we eat most meals at home, which is fine of course. But I think that, if others are in the same boat, this will negatively impact restaurants. Or reduce eating out to food trucks visits and not sit-down restaurants.

Interesting interview with David Hunter on wealtheon predicting how this is going to play out. He has gotten a lot correct this year. He is predicting sp500 going on a fast blowoff top to 6000 as Fed misplays it’s hand and then having to over react taking sp500 down to 1200.

Is he correct? Who knows, but have a plan so you don’t make a big mistake.

David Hunter has been surprisingly accurate and criticized roundly for his predictions. We also subscribe to Jim Rickards newsletters & pay attention when Jeremy Grantham posts his newsletter.

I guess that makes us old school, too.

Rickards predicted deflation then inflation. Schiff predicted the opposite with a gold boom for miners and metal. There is an old you tube debate between them the about this. Rickards missed the mark on inflation and Schiff missed the mark on gold and miners but got inflation right. They both agree on a crash of some kind at the end. Rickards wanders off topic like a beagle in an interview.Peter Schiff says the same thing 5 different ways. I find them all entertaining. If Hunter is correct then jump in the S&P now to ride it to 6000 in the melt-up. They are all peddling something, and that is fine. I wish them success. Here is some advice that works every time but it ain’t very exciting. If you don’t know what to do, do nothing. Yogi Berra expanded that to include thinking. Wise man. I do not know what to do. I am in cash which is doing nothing. I do gamble with 2% of my cash trading SQQQ inverse shorts. It is not investing. A safe 5% return on my money is great for me. I do not need to out run inflation. Death will catch me way before inflation does.

David Hunter has been wrong 99% of the time. People don’t realize he has been calling for a melt ups for years. He expected SPX to be 4000 in 2017, then 2018, then 2019, look at his seeking alpha if it’s still up. I can make a prediction every year and sooner or later I will be right.

Retired couple here (in our 70’s) and we have cut back on eating out to maybe once every two weeks with the daughter and her husband. We get to see them and we spit the bill. Otherwise, we are cooking at home and that is getting pricier because of higher grocery cost. Fortunately, we are not big beef eaters and usually cook chicken or make a big pot of Texas chili or soup with lasts for a week.

Consumer spending stats seen today suggest a lot of people are pulling back. That would, I guess, be disinflationary: high prices curing high prices.

I haven’t eaten out for years. Meanwhile I’ve built my portfolio all around, home(s) equity, cash stash, net worth. One can eat well or sleep well, to me, and I like my sleep. And healthy foods aren’t too terribly expensive. I last ate beef/pork/lamb in 2003, drink only water, and in my mid 60s I can run up the side of this valley at 3 am in winter. Simple exercise gear bought once lasts decades.

Oh, and I just got my first (2.5%) wage raise since 2008. A tiny bonus is thrown on that is a joke. When the road gets narrower, I say, get better: evolve.

“I last ate beef/pork/lamb in 2003, drink only water, and in my mid 60s I can run up the side of this valley at 3 am in winter. Simple exercise gear bought once lasts decades.”

Impressive!!

If everybody lived the way you do, there would be no “Healthcare Crisis” in America. However, I’m guessing about 5% of the population could live the way you are.

“I last ate beef/pork/lamb in 2003, drink only water, and in my mid 60’s..”

Ph,

You ain’t gonna live longer, it will just feel like it….

elysianfield: I might not live longer, but I sure feel good moment-to-moment. I presume that denotes good health, and a mutually reinforcing foundation for the other pillars of health and fitness: mental and financial.

Out here in flyover, I’m surrounded by small operations doing layers.

That flock gets changed out at 14 months.

Last year I could get them for free to butcher. Processors & trucking

was leaving them in a tough spot.

Can and/or make soup. Great bone broth as well.

1 day butchering, and the freezer is full & the canning starts.

Today we’re taking out 4 young roosters that are so full of desire to make the hens hide hours at a time. We have about 60 birds and let 3 or 4 hatch a new set every spring, to replenish the flock.

Selling at the farmstand by the endbof the driveway best eggs possible for $7/doz

I am wired to not enjoying being around a lot of action and people. I think it was because I wasn’t around a lot of people as a child.

Always enjoy solitary or maybe up to four people at one time. No sacrifice not hanging out in eating joints, bars and ballparks.

Give me something to read or a trail to hike or yard work to do and I am in my happy place.

My preferences are very similar. For example, I never understood why, for me, bars were so unenjoybable. I’m on the tall side, and it seemed like short guys always wanted to fight me (slim, easy target).

But probably it was more that the social games people play, and the status competition, were uncomfortable and seemed stupid.

Research on elderly people indicates they are less willing to deal with social contacts which have some type of negative issue. Younger relatives can mistakenly think their elderly relative is too lonely, when actually the person has just decided “effit” to relationships s/he may have tolerated at a younger age for practical reasons.

Pure enjoyment of life is the name of the game in retirement. And for some, that is achieved by having only essential social contacts.

Ditto.

A role model for being happy. Whatever blows up ur skirt…go for it. Chasing the crowd usually leads to a lemming moment.

Amen, relationships to me feel like entanglements. The fewer the better.

We used to eat dinner at restaurants for many decades when we were workers. After retirement in 2004, about three lunches a week. After Covid hit in March 2020, not at all. i don’t know how they stay in business … But I lose weight when not eating at restaurants — that’s a good thing.

I just found a local grocery clearing out what must be the remains of Christmas hams. Nice smoked spiral cut hams at 99 cents a pound. I filled the freezer to last a while. I love chicken thighs also found at .99 lb. You can eat reasonably cheap at home.

Beef is ridiculous, it’s an absolute price gouge at retail. My cousin said he just sold a load of cows for a little less than $2 at market, not much more than from years before.

We almost never eat out because quality at home is so much better. We’re eating beef for $5.25/lb by purchasing a half cow once a year right off the farm; lamb for $7.50/lb buying a whole lamb each year; chicken at $5.00/lb for 8-10 at a time twice a year; and pork for $4.50/lb half or whole once a year. All organic, grass raised. Feeds the two of us all year, plus visiting family in midwinter and for an extended summer season. We produce our own eggs and a lot of our vegetables – to be expanded this spring via a large new polycarbonate greenhouse (waiting in boxes for the snow to melt). 5 freezers in the basement – 2 are cast offs from neighbors and friends, 2 inherited, 1 purchased for $30 used. This summer we start raising grains and cereals, too: hulled barley, wheat, sweet canning corn, flour corn, and upland (dryland) rice. We store winter veggies and can summer produce.

In addition, we’ve put all of our savings and investment money into bitcoin. Crazy, right? Well, we’ve seen over 175% average annualized gains since 2014 despite interim volatility. And life gets cheaper in bitcoin terms. Example: I drive Subaru Foresters. The MSRP of a base model 2014 was $21,995 and I bought my first bitcoins that year for $485/ea, so a base model Subaru Forester price was equivalent to 45.35 bitcoin. For 2022 the MSRP of a base model Subaru Forester is $25,195, a 14.5% nominal price increase. Right now, bitcoin is priced around $38,000, making the Subaru price equivalent to about 0.66 bitcoin, a 75x price decrease. That’s why we converted it all in 2018-2020. BTC holds and increases our purchasing power over the years; nothing else does that. Our retirement is comfortable, and we’ll leave a healthy legacy to our children and grandchildren.

OK Boomer,

Your last paragraph makes me feel sorry for you, unless you’re able to sell your BTC and get some fiat for it. How can you have your entire retirement nest egg in one gambling token that has already plunged by 50%, hoping that it will go back to somewhere? You should be using your play-money for that, not your entire retirement nest egg.

Which makes me think you’re a BTC troll, and so in that case, I don’t feel sorry for you.

Given that you have posted only two comments here, both hyping bitcoin in this idiotic manner, you’re surely a bitcoin troll who is now getting desperate.

“Given that you have posted only two comments here, both hyping bitcoin in this idiotic manner, you’re surely a bitcoin troll who is now getting desperate.”

Hahahahaha. I love Wolf.

We’re cooking more at home because our favorite places have all closed up. Not much choice. Still have a local Thai place that serves good dishes for a reasonable price. Mostly vegetarian.

I can serve up virtually anything of good restaurant quality .. at HOME!

If one has a decent spice cabinet/dry pantry/larder, and taking the time to master a few cooking skills, then one owns a pot of golden possibilities..

Miturn

Inflation stops expenditures as you note…..and raises the cost of business doing business.

This is why the Federal Reserve has a “stable prices” mandate. INFLATION is a bad bad thing. And once started, difficult to stop.

The Fed had NO BUSINESS promoting ANY inflation, then their policies were so reckless their course could only lead to this just beginning rampant inflation.

Wait till all the unions go on strike…..and they will.

I spend only on necessities … and have been for a while. I expect when stocks roll over, this will become very common.

“I spend only on necessities … and have been for a while.”

Historicus,

If inflation continues to rage, this sort of thrift will be self-imposed by necessity. And if fuel prices get high enough, people will, through necessity, cut back on driving and traveling. They might even get a chance to really know their neighbors!

Like Powell said…

inflation effects all Americans…

except some have very tough decisions to make.

What a stupid self contradicting statement.

Right Jay, some people have to decide fill up the car or fill up the grocery cart. Others must decide if 3 country clubs are just too many,

Eating out is probably the worst budget killer in the average American household. Almost 20 years ago I did the math and realized I was spending close to $300 per month just on coffees and snacks at local espresso shacks. I bought an espresso machine and started making my own every morning. Not only do I enjoy a home made coffee drink more, I don’t miss drive-thru lines and I love the financial savings. At this point in time, I have saved over $50,000 just by eliminating that habit.

Eating out is much, much more expensive than my own personal coffee example. Most people can’t actually afford it, but they do it anyway. I treat eating out as a luxury to be enjoyed on rare occasions, or in certain instances where I am so hungry and not home that I just have to get something. It is not uncommon for me to go 2 months without eating out a single time. I enjoy home-cooked food much more than what restaurants serve these days anyhow.

Most people are either economic illiterates or lack the discipline you describe.

I think the same way you do, I don’t waste my money on trivial expenditures.

I don’t care that others do, except that I know (yes know) many are concurrently wasting their own money and feeding at the public trough at taxpayer expense.

Something that I didn’t even mention but which is just as important as the budget implications is the poor quality of restaurant food and its deleterious effects on peoples’ health. It is laden with sodium and all sorts of nasty chemicals and things. There’s so much processed stuff in everything. The people who eat out most are generally the most unhealthy.

When buying uncooked food at the grocery store you can mainly buy basic ingredients, bakery items, staples, pre packaged mixes, or ready to eat meals like most things microwavable or eatable direct from package (like junk food and TV dinners).

For most meals ready to eat, I would say that inflation has gone up on this category more than restaurants and is in fact less healthy and more expensive than cheaper restaurants. Most of the reduction in restaurant eating has gone here, unfortunately.

Right at the start of the lockdowns in America, alot of grocery chains cancelled all their usual sales that they didn’t already advertise, effectively a large price hike. While they did bring back the sales, the lack of competition and ability to to get away with price gouging, is the main culprit of the rise in food prices. Gas prices were higher 12 years ago and food was less than half as much.

The average family and person is going to have to use mixes, basic ingredients and staples to bypass most of the price gouging and to obtain healthy food. Unfortunately, little can be done for most people to bypass the meat gouging. You can always see if there is a local butcher in your area, it just might be cheaper and almost definitely healthier.

Grocery shopping has become nothing more than a game. The stores no longer feature the best “sales” in their flyers, but only a few loss leader items to get you to act (and often available Friday and Saturday only).

However, get their app, use their website, and you can find a bunch of sale items you might not otherwise find – even $10 off a grocery purchase of $50 or more…. Of course, you become a “product” and they track your every purchase and frequency of your visits to their stores, if you always go to the same store, and behavior (if you’re a hoarder or not).

There’s also “geezer day” for those over 55. Safeway and Fry’s (Kroger) have geezer day on the first Wednesday of the month. They offer a 10% discount on most items (not booze). Playing their coupon games, I’ve sometimes “saved” more than 50% of the bill vs. if I just walked in off the street and purchased the same items. Then there’s the gasoline discounts ($.10-.$20 a gallon) which is a nice side perk (gasbuddy plus rewards even comes with a bigger savings). Puts Shell in the same price category as Costco (at least in our market).

Sadly, this is our “normal” behavior. Inflation, recession, good times – doesn’t matter. We’ve done it for years. Sure, it takes planning but we only shop twice a month (big one on geezer day and a “fill in” of fresh) so it’s not a burden.

Thomas Robert:

“Right at the start of the lockdowns in America, alot of grocery chains cancelled all their usual sales that they didn’t already advertise, effectively a large price hike.”

Because we all know grocers are colluding…

Grocers did what they did to survive. Do you expect them to eat the price hikes, plus the additional costs caused by the lock downs?

“the lack of competition and ability to to get away with price gouging, is the main culprit of the rise in food prices.”

Blame it on the retailers, never the government and central planners. We need price controls! Right?

One of the last places you’ll find price gouging is grocery retail. It’s a hyper competitive industry. They are as much a victim as everyone else.

“You can always see if there is a local butcher in your area, it just might be cheaper”

In most cases it won’t. They’re up against excessive rules & regs and industrial farming. And it’s only getting worse.

Totally agree DC:

My better half is a ”semi-retired” gourmet chef who loves to cook,,, and has taught me SO much that we eat a ton better at home than at any but the very best restaurants.

SO, we go out to enjoy the very best foods and service, with table cloths and cloth napkins, and to hell with the cost…

If we wanted to ”save” money, we would stay home, but WE want to enjoy a great meal, and do so two or three ++ times per year, birthdays and our anniversary, etc.,,,

And are very thankful, usually in the form of great ”tips” for the wait staff and cook staff,,, WE having been in those roles in our past lives…

Surely, WE have not been in any junk food palace in the last couple decades, and have no wish to go there ,,, ever…

My husband refuses to dine out….averse to being indoors with others, weather still too cold to sit outside….and he thinks I cook better than anything on offer at restaurants we’d likely visit …I also enjoy it….my kitchen time is my zen time…saves a fortune, too!

Good comments from all the commenters.

Just wanted to add that I’m one of the ones that wastes his money, but try to combine socializing when I can. A meal eaten over a table with good company is 10x better/more worth having than a bite snatched alone.

Yeah, it’s a shame most people are too lazy to come over to each others places anymore.

Potlucks should be way more common. Homemade, store bought, or even fast food mixed together is almost always good.

One thing I could never understand, starting in my teen years, was American packaged breakfast cereal thing. Not only is the price for the grains or other components super-gouged, the sugar added has probably contributed to the obesity / diabetes etc. problems.

One of my top rules of being thrifty (pretty much a cheapskate) has always been make my own breakfast. And in the last decade or so, my pour-over “Clever Coffee Dripper.”

Since virtually all restaurants use cheap unhealthy oils, eating at home can be much healthier, as well.

Over the past year, my family has cut restaurant bills in half. This was largely to reduce risk COVID. And we don’t order takeout, so the restaurant industry lost 50% of our restaurant attendance last year.

The few times I did go out during the last few months, I thought the bills were outrageous. The tab for breakfast at IHOP, two people with coffee, was over $40 before tip last week, and one of us ate off the reduced price senior menu. The average price of a breakfast was $15, before drink.

On the bright side, when you order coffee, you do get unlimited refills.

I feel sorry for restaurant owners, but the COVID, along with associated lack of ambience and hassles (masks) and cost increases, makes dining out much less enticing.

The cost of restaurant food is getting downright criminal. But then, all of this points at least partly back to the wreckless Fed monetary policies and J-Rome.

Our family does not eat out. Instead, we will order take out once in a while. We are not on a fixed income yet but it’s just ridiculously expensive to dine out. And I also don’t know why so many people are so willing to spend so much for food.

I feel bad for the restaurants as some of those that have been in business for a long time have had to close. But I can’t see spending 15.00 on eggs, toast and hash browns when it costs 1.00 to make myself.

In the city I live in and is in flyover country, you better have a reservation or be prepared for an hour wait on Friday night and Saturday. It was this way before covid and it is that way now. Hardly any restaurants have closed near me. Maybe 1 out of 30 closed because of COVID but writing was on the wall for that one leading up to COVID. It was never busy.

Crazy!

Out here in fly over, we couldn’t even tolerate the march 2020 shutdown.

We had the speakeasy set up

And grills fired up.

Odds on that EBT bennies will beat inflation and keep the grocery stores and restaurants going. It’s the middle class that will continue to be ground between the millstones of taxation and inflation.

“Odds on that EBT bennies will beat inflation and keep the grocery stores and restaurants going.”

This is correct. That’s how it was done in the 70’s.

“It’s the middle class that will continue to be ground between the millstones of taxation and inflation.”

At the cost of the middle class, correct again. Right from the 1970’s hyper inflation playbook.

Can’t hide the sun forever with your thumb, the cat is out of the bag.

Fed is going to have to take the political blame for the social unrest and social upheaval that is no doubt coming as regular people begin to understand they are screwed for the most part under the current system.

Glib comebacks/political distractions are not working, look at the Biden poll numbers, someone is going to take the fall and it may be the Fed if they are not careful.

These banker scum just couldn’t help themselves after they were given free reign following the first meltdown they caused with the housing bubble/bust. When you hire the arsonist as the Fire Captain, this is what you get.

The FED and all of these rich pukes and ivory tower hacks are blinded by rapacious greed and unrelenting hubris. Alarms have been ringing for years, yet they did not even so much as pay them a glance because they just couldn’t get enough. They’ve even started taking heat from some of the billionaires who benefited the most (though I think that’s more a case of the billionaires getting a bit nervous when they look at their pile while the world is starting to burn around them). Such dereliction of duty has never before been seen in this country. The far-reaching implications and effects of these horrific policies are too vast to list.

For years we have listened to these filthy central bankers, ad nauseam, blow smoke up our aszes while they were basically stealing the futures of everybody but the wealthy. Those paying attention saw exactly what was happening, and have been criticizing them the whole time, myself included. I have been calling that crackpot Bernanke out since the beginning. And now the chickens have come home to roost, and Weimar Boy Powell is stammering his way through more bullshit and lies.

This is not going to end well at all. The lack of affordable shelter has created a powder keg of anger, hopelessness and frustration. I see and hear it everywhere. And now you can add cars, food and everything else to the mix. This is an unmitigated disaster. What kind of disgusting society does this to their youth? And these pigs just keep on pigging out. Did the FED members really need another 50 million dollars each, or whatever?

I can’t even type here what I really hope would happen to these filthy, vile sociopaths. I refrain out of respect for Wolf and his rules which I have tried my best to adhere to. But they are an evil cabal, and to exorcise evil, you have to sometimes resort to unpleasant measures which are necessary to restore the balance and health of a society. The future of our youth depends upon it.

Great rant! I honestly appreciate your passion. Its so lacking in our oversensitive pc world. Im a prehistoric ole guy.

I know and remember hatd times. Its my opinion that few under 60 know difficult times. Go back 40 yrs to the Volker times…1980 14% inflation. Same as now but the formula

Has been massaged. 40 yrs ago anyone under sixty was probably still living home.. a bir sheltered from reality! Remember back to back recessions in 1979 to 82? Ugly!

What do you think the coping skills of todays average adult will be?

DC – I couldn’t have said what you said any better, — hope you are still reading this post.

I have been outraged for so long over all this, but when you mention that Fed policy has been doing for many over 10 years to other people their eyes glaze over and they say it’s whatever the current Pres in office is doings fault, and turn away, and see how many “likes” they got on a stupid FB post.

This is one of the reasons why I started this website many years ago. My wife’s eyes were glazing over, and my friends thought I was nuts.

Same with my wife, and just about all my friends, they all say it’s the Pres responsibility, and I try to explain it’s Fed policy changes that don’t take affect for a long time, of course, the same glazed look.

Your effort and website is excellent and sure has opened up my eyes as to what the “H” is going on.

Along with all the fine commentators who are aware too.

So many times what is talked about by you and others becomes headlines days, weeks, or months later!

“This is not going to end well at all.”

Since the beginning of (un)civilization, it never does end well.

“The lack of affordable shelter has created a powder keg of anger, hopelessness and frustration.”

All by design.

“I see and hear it everywhere.”

It’s hard not to see it, but ignoring it is the path of least resistance for the average citizen.

“And now you can add cars, food and everything else to the mix.”

Your flesh and blood too.

“This is an unmitigated disaster.”

To which a white knight will come to the rescue. Take a wild guess who that will be?

“What kind of disgusting society does this to their youth?”

A society with an apathetic majority that values comfort over freedom, not to mention bread and circuses.

“And these pigs just keep on pigging out. Did the FED members really need another 50 million dollars each, or whatever?”

No. But that’s not any of your business. It’s a big club, and you’re not in it.

“I can’t even type here what I really hope would happen to these filthy, vile sociopaths.”

Little by little, they will wear you out, until you’re left hollow, numb, and without a soul.

“they are an evil cabal, and to exorcise evil, you have to sometimes resort to unpleasant measures which are necessary to restore the balance and health of a society.”

True. The unpleasant measure, however, is not a revolution, it’s choosing freedom over comfort. Do you really believe the average world citizen will do this?

“The future of our youth depends upon it.”

The future is a human face being stomped on forever. No one cares about the future or the youth. That is the real frustration.

Well that settles it. Peter Schiff was right, the Fed was wrong.

If the world was that simple, we could all get rich on a few trades. If I had that level of confidence, I would be all-in on a few simple trades, within minutes, and ready for delivery of my Maserati. In today’s brokerage environment, investors have almost zero-cost access to securities that would cash in.

In Schiff’s case it’s gold, right? Or was the last time I looked, about a decade ago when he was preaching the same chorus. That’s a long time to wait for a broken clock to be right, a huge opportunity cost paid.

As for whether any thesis remains right or settled, I note that time does actually keep moving into a fundamentally uncertain future (and us stumbling into its fog). Wars thought to be won, great victories of history, like anything, decay in their meaning and impact. (Exhibit A, B: New Deal, USA WW2 victory and aftermath.) But maybe you just got that Maserati?

Gold and silver should be the two best performers starting in 2023. They’ll lie about the inflation rate coming into the midterm elections then inflation will turn to hyperinflation starting in 2023. It could be too early to buy gold but its what to buy towards the end of 2022. There’s only 3 possibilities in 2023 recession, depression or hyperinflation. Hyperinflation seems to be the heavy favourite.

Fed has us addicted to debt. Rates go down houses for up. That cycle causes more debt and ever lower rates must be maintained.

Once you hit zero, then you have to start handing out subsidies for having children so you can afford a roof over their heads.

The 40 year trend in rates is down. It could go to 50 with 10 year sub 1%. Not a prediction, but it is one scenario. It’s a 40 year trend for a reason. Has that reason changed?

There won’t be anything close to hyperinflation in the US with the 10YR @ less than 2%. It will have to be a lot higher than that first. Unless of course, your definition of hyperinflation is different than mine.

What is crazy is the commodity index are shooting higher this past year. But the odd thing is that Gold and Silver have not budged. They are still not getting any love and have been going straight sideways for a year while inflation is over 6%. . Not sure why. Those are two commodities that have zero inflation? I guess it still costs less than $20 to get silver out of the ground? Ther e must not be any wage increases, equipment cost increase, or fuel costs increases for the miners?

That’s hilarious. Gold and silver are getting annihilated and the prospects for both are dim.

Escierto,

Are you into platinum? Or have you achieved ascension and are buying up gen 1 Pokémon cards?

Real Tony,

What makes you lean toward hyperinflation? Personally, I don’t think that is likely and it doesn’t appear that the Fed/gov will allow a depression. The biggest question I have is whether or not the Fed has learned its lesson with QE or if we could see it again in a few years.

Most people that never actually listen to Schiff believe he is just hoarding gold and waiting for the crash. People only hear what they want to hear. For one thing, he is also in foreign stocks, which nobody ever mentions. All anybody mentions is the tired broken clock routine.

Foreign stocks have significant drawdowns too, ironically (in terms of your stated holdings of Schiff) in tightening cycles by US Fed. There is a list of these events (among tons of other good data and views) in a really good book, The End of The Risk Free Rate (2nd ed. is now out and updated) by Ben Emons.

And I believe the broken clock metaphor is spot on. One needs not only to be right in a prediction, but have a time frame on it that actually works, that is profitably actionale, or why have it? (Trick question: the answer is to occupy a place in the commentariat and sell books). Look where a person’s cash flows from. If he had such hot inbestments, why would he keep selling books with the same theses?

Goober

The Fed was very wrong for most of the country.

https://wolfstreet.com/wp-content/uploads/2021/10/US-wealth-effect-monitor-2021-10-02_category-per-household.png

I love that graph. Wolf, can you explain something to me? When I read the headlines and listen to all the talking points, I hear how 60% of Americans don’t have $1k of savings. They say the median income is $34k. When I hear this I like to thump my chest with pride as I figure with net assets of $200k I must be in the ‘upper half of the bottom 90%’. But looking at your graph and I think you mentioned that to be in that ‘upper’ class I would have to have over $400 in net assets. What gives?

Gooberville Smack,

Yes, “Americans have no savings” is a conundrum. For many decades, they have been asking the same question. But today, many people don’t have savings. They have credit. If they need to pay for something, they use their credit card, even if they pay if off every month when they get paid. They don’t need to have $400 in savings. But they might have $50,000 in credit lines that have not been used. A millionaire today might not have $400 in “savings,” but when an emergency comes along, they pay by credit card, as most Americans do. Once I figured out that the payment reality of today obviated the survey about “savings,” I stopped paying attention to those surveys.

Gooberville

Most of the people on this web site were right….and the Fed was wrong.

and what are the consequences for bad decision making at the Fed?

Time for the Taylor Rule……and solid connections between Fed Funds and inflation…..money supply growth and GDP growh.

David Hunter said Fed’s big problem is they are a deliberative body looking at old data. Always has them looking in the rear view mirror.

Powell paying attention to anything other than his investments.

Good luck on that

The End of the Risk-Free Rate by Ben Emons, page 164, pinpoints the moment (late 2018) when Trump openly jawboned and attacked Powell, policy (at the time of rolling off the balance sheet, i.e., a very graduated tightening). The two met, and Powell about-faced (compared by the author to Nixon’s arm-twisting Burns in ’71-’72, and Schumer arm-twisting Bernanke in the election cycle of 2012). Quotes are provided. At these key moments the then-Fed chair (different person each time) , it is readily arguable, caved to political pressure and loosened before an election.

The 2018 event, not foreseeing COVID, juiced the economy into an inflationary overshoot mode. When the pandemic happened, the Fed had already spent its ammo and could only loosen more, resulting in this overshoot of inflation. The track record (including Powell’s) has been caving in crucial election years.

But we did have the lame duck moment of Carter-new Chair Volcker when everybody commenced to do the right thing. Everybody waits for that moment like the Second Coming, but business as usual (gradualism, equivocating) is still happening. Is the current medicine strong enough? We have front row seats.

“”Numbers released today by the Bureau of Economic Analysis, which is part of the U.S. Federal Statistical System producing data and official statistics, show that the U.S. economy grew by an astonishing 6.9 percent annual rate from October to December 2021. That puts the growth of the U.S. economy for 2021 at 5.7 percent in 2021. Despite the ongoing pandemic, this is the fastest full-year growth since 1984.

At the same time, the U.S. added 6 million jobs in 2021, pegging the unemployment rate below 4%….” Different point of view, I suppose.

The US economy added 6 million jobs after losing 11 millions jobs. It’s still millions of jobs below where it had been. Go look at my charts.

All this would work a heck of a lot better without all this idiotic inflation that is now eating up the wage gains and that was brought about largely by the Fed’s reckless monetary policies.

Never forget the corrupt government handing out all of that free PPP money – almost a trillion dollars! – and paying people to stay home. That had a massive hand in it as well.

Estimates for the government …$100 billion of fraud…

they have recovered about $2 billion.

A lot of the money went OUT OF THE COUNTRY!!!

The government can just go borrow some more at near zero….

and that is the problem.

Look at a labor force participation rate chart.

Not good news.

Try to hire and keep employees if you own a small business. Our wealthy friends are having nervous breakdowns over labor shortages and quits at their small business.

The US economy declined -3.4% in 2020 and rose +5.7% in 2021. That adds up to +2% growth in two years WITH a HUGE expansion of deficit spending and a similar HUGE growth of Fed assets. And the 2% imay over state growth — many people believe it is based on an inflation rate that understates actual inflation.

In 4Q 2021, the Real GDP rose at a 6.9% annual rate.

But 4.9 points of the 6.9% growth rate was inventory growth that did not seem to be needed for rising sales in early 2022. Meaning that Real Final Sales rose at a 2% annual rate in 4Q 2021.

I don’t see both 2% numbers as something to brag about. Plus Junpin’ Joe Biden will find some way to make the economy worse.

And Powell at the Fed talks about “tightening” but so far Fed Assets rose $82 billion in the past two weeks — that not a serious signal about fighting inflation. So far just Blah blah blah. Wolf does not agree with me on this but Fed members will have strong pressure on them to not hurt the economy in the next nine months before an election where it currently looks like Democrats will lose Control of Congress. Fed members who arer Democrats won’t want to see that happen. Those who are Republicans will be pressured to ‘take it easy’ in an election year. Everything is political these days. Even Covid vaccines are political.

The most overvalued stock market in history (capitalization as a % of GDP) will not ignore the amount of Fed tightening needed to cut inflation in half. Investors are already nervous just from talk about “tapering” — if their confidence has peaked, stock prices will go down. Stock prices climb a “ladder” of increasing confidence that peaks when stock prices peak.

The new numbers are in for this week:

Federal Reserve Credit this week

expanded $12.9bn to a record $8.839 TN.

Over the past 124 weeks,

Fed Credit expanded $5.112 TN, or 137%.

Federal Reserve Credit last week

surged $88.6bn to a record $8.826TN.

Over the past 123 weeks,

Fed Credit expanded $5.099 TN, or 137%.

Summary:

The Fed keeps “printing money”, with $88.6 billion last week, and $12.9 billion this week.

An optimist would say the “money printing” slowed down a lot this week.

A pessimist would say the “money printing” in the past two weeks does not add up to a Federal Reserve Bank very serious about “fighting inflation” in 2022.

The banksters’ privately owned “Federal” Reserve only pretends to care about inflation or most Americans’ interests. Coincidentally, no doubt, they continually funnel billions in QE commissions, “Federal” Reserve dividends, ultra slow interest rate loans, etc., to their banksters and their group.

Read about the history of organized crime, the non-Italian part, and you will discover who has been running this brilliant scam on gullible Americans for decades and so controlling our money and thereby our politicians and government. Where do you think the billions generated from gambling, drugs, high-level prostitution, Las Vegas casinos, etc., wound up?

Fed STILL not worried … near zero Interest Rates , QE still flowing , no QT for months

Do you think they’re really not worried? Or do you think they’ve painted themselves into a corner? I mean, it really is a ‘damned if you do, damned if you don’t” situation.

They’re not worried. They became fantastically wealthy. And the longer they put off the tightening and the raising of rates, the more money it means for them. They are going to slow-mo this thing as much as possible. They are never going to get ahead of inflation.

Have to agree.

Not a bug but a feature …

True, there many things happening in the US that appear to be accepted by blind people, but are instead well planned and orchestrated.

, “it really is a ‘damned if you do, damned if you don’t” situation.”

It’s DAMNED because you DID stupid over the top policy moves.

Continuing is not an option. Hard measures now must be implemented by the responsible parties.

Biden must send FBI to storm Fed headquarters, arrest all their members for insider trading, perp walk them on live TV, blame inflation squarely on the Fed, bring on Volcker II and tell the nation the hard truth about our economy.

That will deliver a big win for him in November.

Fed is a crime syndicate.

Unless, presumably, Biden is complicit…I know, surely not likely…

I’d watch that on TV all day long.

And who is going to storm congress?

^ This!

Congress could repeal the federal reserve any time it likes.

And after another month and a half of this, the Fed might raise rates to 4-5% under inflation. That’s what I call “nimble”!

I’m looking for a chintzy quarter point hike, and then the FED acting like “look at us, we’re so aggressive.”

a quarter point is what the media calls “stunning and brave” and “a serious threat to the economy”

Inflation just went up about 24 1/4pts…….

and the hand wringing is about 2,3,or 4 1/4pt rate hikes?

It is beyond absurd.

the Taylor Rule would have Fed Funds about 6% right now…

and that would have shaken the boots of the cavalier Fed Governors.

That is what is needed. IMO

The real question is what is the political impact in the hallowed halls of Congress . The Fed’s bitch master has a problem they are ignoring, for now. Powell is their man. He’s got this. The next Whooooosh they hear might be the voters chucking them out on their grifter ass. We need a new set of grifter’s. Spread the wealth around by bringing in a new batch of grifter’s in a form of Congressional Grifter Equity. It’s the American way.

Little nuggets like this are the reason I drop-by here often. Simple, straight-forward but speaks to a systemic cluster of bad behavior… Samuel Clemens had it nailed many years ago… “There is no criminal Class in the United States other than the US Congress”

The effective duopoly in Congress ensures that nothing will ever fundamentally change.

It wouldn’t matter if there are more than two parties. The voters are equally at fault. Voters overwhelmingly want the government to do more of what’s failed spectacularly, believing it will be “different next time”. It’s called long term social decay.

It would matter a lot if there was a sane party. Voters would chose it if they could. Some places are >50% on a dole, but most are not – those people have no representation, not in media, not in academia, not by a party even outside of power. Those people would chose better if there was such a choice.

Great points! I think it is both decadent voters and institutional decay. Everybody drifts into their own grifts, by small increments, with excuses plastered on. I think it is a mistake to pick one corner of this many-sided problem and should “there’s the (exclusive) bad guy!”

Tom,

Your argument is for political devolution with which I agree. At the state or local level, your preference might work. With most policy centralized, never.

their ages along should be a disqualifier. these geriatrics have had the reins of power long enough.

DR

” the political impact in the hallowed halls of Congress ”

The questioning at the last hearing from Sherrod Brown, the chairman of the Senate Banking Committee that allegedly oversees the Fed….weak, off topic, orchestrated.

Congress loves the low cost of the Trillion dollar spending bills….and that is a caution.

Unfortunately, parties vote as bundled package. There is not too much thinking about it. To tell the truth, a lot of our decisions deal with the good and the bad bundled together. Heck, that’s how CONgress works!

WR: I’m putting this here so u can kill after reading:

‘These two vile wastes of human flesh have presided over the death of this country. All of the bad stuff has happened right under their noses. You know why? Because they WANTED it. They should be facing the death penalty for treason.’

This would never have appeared on yr site 2 years ago. The tone is going downhill and I see you getting testy. You kill my digressions/ rants all the time. No prob. But the above is over the top. I suggest you do one of 2 things: either limit comments to biz. finance, money OR start a second site ( hire some kid) called maybe Wolf Hunters, where culture wars can flourish. Hey, with all respect. if that’s where the eyeballs are..

These fools and their .25 rate increases will do nothing to stem this tide. Powell should be incarcerated for such blatant malfeasance.

Of course the rate of inflation will magically move lower as the midterms approach. In 2023 the U.S. dollar will fall off a cliff as hyperinflation ravages America.

The best election poster is to post supermarket ads with prices from five, ten or twenty years ago.

Plenty available on historical newspaper sites, which you can often use your library’s subscription to so as to view for free.

Breach of fiduciary responsibility

Failure to follow the three mandates as laid out in the Federal Reserve Act Reformation of 1977

Max employment (success)

Stable Prices (fail)

Moderate Long Term interest rates (fail) All time lows are immoderately extreme.

“The Federal Reserve Act 1977 states that the Board of Governors and the FOMC should conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.””

Their “Dual mandate” game intentionally carves out the third mandate, the one that would have prevented what they did to get us in this mess.

Moderate long term interest rates keeps a balance between lender and borrower, it prohibits irresponsible long term debt creation by keeping a moderate cost to do so, thus it prevents current decisions making to pull wealth forward from the future to fluff the present.

The Fed intentionally flattened the yield curve, then they pointed to their work and said “see, people arent worried about inflation”.

Powell said the other day, “The government has no problem borrowing at these current low levels.” Missing was someone pointing out all the Treasuries and MBSs the Fed has and is purchasing to keep their foot on the interest rate scale.

The solution to your problem is to end interest rate targeting (price fixing). There is no “correct” price anything.

The way to prevent irresponsible borrowing is end government sponsored moral hazard. Let creditors who make foolish lending decisions suffer the consequences of their bad judgment. No bailouts and no lending guarantees.

Augustus Frost

‘Let creditors who make foolish lending decisions suffer the consequences of their bad judgment.’

Agree 100%

If students could discharge their LOANS with personal bankruptcy but that choice is available to other types of loan including Business loans and Home mortgage but NOT for student loans!

How did it happen? That Bankruptcy ‘protrction’ was removed at the behest and campaign from Banks. Mind you All banks and majority of US Corporations are registered in Delaware with PO Box addresses!

Mr Biden who was VP at that was key instrumental in removing that protection! Public has a short memory! No wonder Educational cost went sky high! MSM has been very silent of this fact. Apparently NOT good for the establishment! It is/was tragedy which could have been prevented, corrupt politicians in power!

Every Fed Head .. from Greasedspan on up!

There is velocity, there is acceleration, or the rate of increase in velocity and there is an increase in acceleration. Depending on where the data places the change in inflation, maybe a .5% bump in March is appropriate.

To quote Bernanke: the Fed can always re-inflate even if it has to ‘drop money from helicopters’.

In practice this would mean just ‘dropping’, depositing, money in every personal bank account.

So what if the stock market drops 30%? If everyone, including the majority who aren’t glued to market screens, wakes up with an extra 1 or 2 thousand in their account, wouldn’t that be net inflationary?

Although you can do the reverse, drain personal liquidity via taxes, you can’t just suck it out of accounts overnight.

In which direction is there more risk of policy error, raising too fast or not fast enough?

“So what if the stock market drops 30%?”

Dow 26,000?

It was 20,000 in 2016

It was 22,000 in 2018

maybe it was too high at 36,000

If you punch into a dividend discount calculator the SP500 doesn’t even keep up with inflation rate at nominal 4% trend growth rate. Everyone thinks bonds stink, but stocks stink too

With dollar strong, it’s probably good to rotate some funds outside of over priced USA.

The USD is weak versus currencies that count.

DXY is about 95 now. It was 120 in 2000 and 2002. It was equivalent to 185 back in 1985. Don’t know what it was in the 1960’s but presumably higher, when the FX rate versus D-Mark and CHF were about 4:1.

The above does not incorporate interest rate or tax differentials.

‘The USD is weak versus currencies that count.’

Which currencies are those? Or is this a flashback to days of the D-mark?

Returning to the present: the dollar is strong against other dirty shirts and getting stronger but weakening against oil.

Holy Sh%t: just read this over at Zoo hedge

“We might need to bring back Paul Volcker,” Waldron said. “And have somebody that would be willing to kind of stay the course without regard to exactly what’s going on in the markets.”

But who is this guy? He’s number two at Goldman.

It’s from a piece posted yesterday with title: ‘Fed lacks will…’

It looks the pressure on Powell is coming from unusual directions. One other thing: if he was to bump .5, no one would take his jawboning lightly for the rest of his term.

I am just guessing Waldron probably has a big short on bonds and is getting impatient waiting on a rate increase. He probably makes so much money inflation is not effecting him.

Just time for a new “Fed’s Favorite Inflation Index”.

If you believe Steve Hanke core is going to be in this range for all of 2022. The money is already out sloshing around in the economy.

The professor Steve Hanke is armed with Milton Friedman’s Exchange Equation. He is a dangerous hombre. He has also got that wry mid-western dry biting humor he uses to educate even the dim witted among us. The lesson is simple, “its the money supply stupid”.

Late last year, my mother got her annual update on what Social Security would be paying her each month in 2022. She was very happy because she had heard about the adjustment upwards being the highest in decades. However, when she got the update, it showed that less money would be deposited into her checking account each month than in 2021. The Medicare plan deductions had eaten up the entire increase and then some.

She was not happy.

Very common situation.

Medicare Advantage: almost free.

Medicare Advantage (C) costs at least the same as conventional Medicare (A), (B) and (D) combined. And Medicare standard premiums went up +14% in 2022.

Many Medicare Advantage plans are FREE. Under Medicare Advantage, the government pays your HMO/insurer about $1,000 a month to keep you healthy, and when you get sick, your Advantage insurer has to pay the bill. This payment of about $1,000 per month assumes that you’re healthy. If your insurer shows that you have some chronic issues, the monthly payments can be far larger — I have read up to $4,000 per month. There was some good reporting in the NY Times (?) on the incentives for the insurer to cheat the government by claiming that you have bigger health problems than you actually have.

Advantage plans change the equation for the patient. And there are pros and cons with it.

Advantage plans also often include caps, which Medicare does not, they include prescription drug plans, and they often include basic dental care (free teeth-cleaning, etc.), health club memberships, etc.

The thing to remember is that the government pays the insurer to keep you healthy. Under Medicare, the government pays the health care provider to do as much surgery and tests and other stuff as possible, often unneeded. So the incentives are very different.

Most Medicare Advantage plans are NOT free. except for low income people also on Medicaid — they are called “dual eligible”.

Our Medicare Advantage plan, which we have had for several years are partially financed with the same amount of OUR money that would have gone to buy standard Medicare B and D coverage combined. It is NOT free for us. There are also deductibles and co-pays. Also some extra benefits, such as two teeth cleanings and one dental exam a year. The most important extra benefit may be the limit on our annual out of pocket payments which does not exist with standard Medicare. Our annual out of pocket limit is about $5,000.

If you’re a low-income person eligible for Medicare, you also may be eligible for Medicaid. Being eligible for both Medicare and Medicaid is called being “dual eligible.” Unlike other types of Medicare coverage, you may not have premiums, deductibles, or co-payments/coinsurance if you are covered by Medicaid. Medicaid may also offer additional benefits that Medicare doesn’t, such as routine dental and routine vision services and hearing aids.

Medicare Advantage is funded from two main sources. The plans receive some funding through monthly plan premiums, but most of the money comes from Medicare. The private insurance companies that offer the plans receive a payment each month from Medicare which averages about $1,000 a month.

My upcoming Medicare Advantage is (one of several) offered in my area FREE. As in $0 out of pocket per month. Oh yeah, $12/month for dental. Includes all Medicare wrapped in. No medicaid involved. I think it depends on what networks are near you. Living in a well-populated city with several providers has definite advantages (no pun intended). Also living remotely adds other costs to your health picture anyway. Also for me several major provider complexes within the network within a few miles. I might also ask what state one is in — not sure if this affects it — mine is a blue state.

That’s what you call “no lube.”

We had friends who thought their Humana Medicare Advantage plan was “free”. They did not realize their Social Security checks had been reduced by the standard basic payment for Medicare B and Medicare D.

They did not pay extra for Medicare Advantage (although some MA policies do have higher premiums than standard base Medicare) so it appeared to be free.

If they were low income, and had qualified for Medicaid in their state, they could have had a Medicare Advantage policy for free.

But if you are not low income, you don’t get Medicare A coverage for free.

You must pay for Medicare B and Medicare D … whose price increases with income Payments, and are often are deducted from your monthly Social Security checks.

well, yes, Medicare Part B is always there and has to be paid. It’s a requirement for the Advantage plan. The Advantage plan itself is often free and INCLUDES Part D coverage, often better (lower deductibles and no donut hole). It includes a bunch of other stuff, depending on the plan.

Real income almost flat to 2019, after this huge global shock, doesn’t look so bad to me. Yes, there was a big dip. There was a big shock. The Fed didn’t create that (though it was irresponsibly loose in years preceding the shock, in my view).

when you consider that we had to print $5 trillion to get that, it does look pretty bad to me.

It looks bad to you because it’s another piece of evidence the economy is falling apart, a fake economy held together by government spending and “printing”.

“Ponzi Economy” or “Ponziconomy” for short.

Wolf, yours is the only site I read that reports honest data and not sugar coated BS. Fed is enriching rich and enslaving poor. It will be nice to see these curves for rich (top 10% and 1%) and the rest and it will look even more disturbing.

Fed should be abolished and its members should serve jail time for blatant robbery from ordinary Americans. 10+% real inflation and they won’t raise rates to even 0.25%. But ordinary Americans deserve to be scr ewed because they are typical sheep and still listen to and believe in Fed.

Funny how, over time, the old 2% ceiling has now been accepted as the Fed’s target and is kneaded into being accepted as an average. Next steps are getting it accepted as a bottom and then raise that up.

Sounds crazy. Just crazy enough to work. Headline reads…

“We need CPI > 2% or we are failing as a nation! What are you doing to help your country?”

Giving raises to my employees on the first of February. Also, giving notices to our tenants that rents will going up on the first of April. Just been informed by vendors that most materials will see increases on Feb 10 or so. Some vendors posting 38 week lead times for higher end windows. I sent out notices to customers three weeks ago announcing increases in my rates to them.

Even the dems I know are calling this Venezuela.

Somebody tell me how this ends well. It won’t.

When I ordered my home audio sub-woofers ten months ago (engineered & made in Florida) they were $2,000 per unit.

Recently, that has been changed to $2,500 per.

I really enjoy them and am glad I did not wait longer to pull the trigger and buy ’em.

The Bob who quote is perfect: “… most materials will see increases.”

Welcome to the world of full range frequency response.

Cheapskates can save a lot of money by building their own subwoofer(s). You can buy a finished box if you’re not handy. Or buying one instead of two.

I’ve been building subs since the 1990s. My lowest cost 15″ driver sub cost only $300 to build including a used amplifier and low pass filter. It will outperform any commercial product for $2,000 or less. Adding a parametric equalizer for about $150, with at least 3 bands to tame bass resonances in your room, and your sub will outperform $5,000 subs.

The test tone called a slow sine wave sweep, from 20 Hz. to 100Hz., will reveal how uneven the bass frequencies are at your listening position (that is a problem in every room of every home).

Richard,

Right there with you on building subwoofers.

My living room has a slight resonance in the low 40 Hz area, but I definitely prefer a “less is more” approach and run all my audio systems as flat as possible. Not into tone controls or equalizers.

These subs take a line-level input from the preamp & run through a 4th order Linkwitz-Riley active crossover, which I set @ 80 Hz, to feed a high-pass line-level signal to the main amp directly. From 22 to 118 Hz, they run within plus or minus 1.5 dB output in an anechoic test set up!

I do have a pair of actively crossed 15″ Rockford Fosgate subs in airtight cabinets (2.5 cubic feet volume) I made with 3/4″ marine grade plywood & no internal parallel surfaces, for my second audio system, but doubt I would be able to match the new subs’ accuracy with anything I could make myself.

Dan, as an audiophile since 1965, I hate to disappoint you … but no subwoofer in any location is likely to do better than +/- 6db in an ordinary home listening room, when using the correct test tones and a sound meter for measurements.

Anechoic response is irrelevant in a home listening room.

But the bottom line is if you enjoy the music, the audio system has done it’s job.

Haven’t done a set of test tones & a microphone check analysis, but my ears are indeed very happy with the balance of my system.

The frequency vs dB sound output response is definitely dependent on room acoustics from the time it leaves the subs until it arrives to my ears (or a microphone). But it is the “Holy Grail” to have a dead-flat response in an anechoic test. Plus, this can be replicated and can be used to compare with other speakers.

Kind of like having zero to 100 kph stats. It’s never going to be identical between different drivers and all the other variables that come into play to make the stats published in the car magazines. But I want the shortest time to go fast, and I want the flattest response from my speakers.

My goal is to have the most accurate set up; without going off the deep end spending money to do it. From that perspective Richard, I think we speak the same language, eh?

Wolf could you do an article if you believe the price of oil will handicap anything the FED does moving forward?

Thank you as always.

If oil goes much higher, inflation will go higher, and the Fed will tighten faster, sooner, further….

Oil is still cheap at $87 for WTI. Between 2011 and 2014, it was running between $80 and $110. In 2008, it hit $150. There has been a lot of inflation in that decade, but oil got cheaper.

Wolf,

Another theory. If oil goes higher, prices at the pump will go higher, but inflation overall may not go higher as the price of gas is somewhat inelastic. People who just shelled out 50K for a new car are not going to let it sit on the driveway just because gas is 1$ or $2 more a gallon. They are going to pay. That means they have less money to buy other things. Less money chasing the same amount of goods. That’s deflationary. Add in the Fed tightening and you have all the ingrediants for a major recession.

Saudi has announced price increase coming.

By now I think this is all done on purpose. These people playing monetary Lords, are either complete idiots or crooks. In my view the later is more likely to be the truth.

I was thinking how did we get to the place that a Fed chairman can blow up the world by one bad sentence. But it is what you get when you play God and leverage up the world. But maybe that’s what you have to do when you are in fourth quarter of reserve currency game.

Old School

“blow up the world by one bad sentence.”

Ask a friend in the brokerage business if he heard what the Fed just said………then be sure you can watch his face.

It will prove that Powell is the most powerful man in the world without an army

Read somewhere that under the old way of how FED measured inflation, we are well at 11% or higher YoY. Wolf, would you happen to have those numbers?

If looking at real estate, especially in SoCal, one can only dream about inflation at 5% YoY, definitely in the double digits.

The real inflation on the ground is at least 20% plus. Manipulated govt metric is 7% plus I guess.

Jon

Real unemployment is close to 18%. Add that to the inflation rate and you have a misery index of close to 40%. Carter’s topped out at 20%. We own Jimmy boy an apoligy.

Phoenix_Ikki.

The purchase of a home is considered the purchase of an asset, such as stocks, and is not included in the CPI. What is included is the cost of “shelter,” which is a service, and this figure is based on two rent factors that I discuss every time when CPI is released. “Shelter” counts for about 32% of CPI. It’s huge.

I’m OK with this theory of using rent to approximate the cost of shelter as a service. But the problem is that the two rent factors, though they’re now spiking (chart below), are way behind reality. Rents are spiking by the double digits (article coming this weekend), and this is very slow in getting picked up by the two rent factors.

Below are the two relevant charts. To find out more, click on the link:

https://wolfstreet.com/2022/01/12/purchasing-power-of-dollar-inflation-whoosh/

If house prices had been included in the CPI, it would have generated massively negative overall CPI readings (deflation) during the housing bust. Instead, CPI remained positive (inflation). That’s why I think that it is valid to exclude home prices from CPI, and use the cost of shelter instead. But the cost of shelter needs to be calculated properly.

David Stockman has inflation at 13.8%. I go with his figures, not government bull s$it.

His number is bullshit. Basic math proves it. And I have had to explain these here a bunch of times. If inflation is 13.8% every year for six years, and you got by with an income of $40,000 in the first year, in year six you will need an income of $86,900. Which is of course bullshit. That is not happening. It’s the math of compounding that blows this nonsense from Shadowstats and all the others out of the water. Just do the math!!!

CPI-W is nearly 8% as a national average. And that may be getting close. Every town and city has different inflation dynamics. So local inflation rates differ.

Good news, growth is strong, the Fed won’t be raising rates. The markets get it. Those comps are going to disappear, inflation is a moving target, pretty soon it stops moving or it falls.

is this for real?

Yes.

“The Cause can not be the Solution. In fact, and nearly always, the solution is 180 degrees from the Cause.”

Johnson’s Razor

This is dumb. Of course the FED will be raising rates, but it will be woefully late and insignificant. But to say they won’t be raising at all if foolish. Will you be back here to eat your words in March?

We have a slowing economy

Ambrose Bierce,

Are you basing your investment decisions on this?

‘Are you basing your investment decisions on this?’

This is the dominant, prevailing ‘hopium’ talk from the financial media!

A Lot of wishful thinking out there.

NOT many there with very few exceptions (in bloggers’ world) are NOT dissecting & systematically analyzing the data. like you do! Thank you for that!

Haven’t made an investment decision in years. I feel better now about growth prospects than I did twenty years ago. That was a lost decade by the way. The big issue to me is the end of consumer focused solutions. The real problems are corporate. How do you stop a pandemic, or a cyber attack? The solutions aren’t more government either.

Would you be interested in buying my 25% share of the Brooklyn Bridge?

Na, He wants to buy a bridge in Penn. OOOps, it just collapsed

Just allowing rates to normalize (positive real rates) will crush stocks, bonds and housing. Inflation will collapse with it! If the Fed simply gets out of the way, as they claim they are going to do in March.

Just got my SoCal electric bill and even though we used virtually the same number of kilowatts it was 12.75% higher than last month. Must be the benefit of solar and wind?

Did you check the price of natural gas recently? Wind didn’t get any more expensive. Actually, it’s still free. But the price of natural gas at the NYMEX more than tripled since 2020, NOT including the 46% spike and plunge the other day.

Natural gas used to be cheaper than coal. Global coal consumption is increasing. One day in West Texas it is windy and electricity is cheap. Another day less wind and the price of electricity spikes.

Wind is always free. The price of natural gas ranges from cheap to expensive, but it’s never free. You need expensive equipment for both to generate electricity. But for one, the fuel is free.

Th word “free” is very deceptive.

Wind itself may be “free” but the cost of generating electric power with the wind is considerably more expensive than coal, natural gas and nuclear power.

The power generated by wind is highly variable and unpredictable, so requires 100% natural gas backup for when the wind is too slow to generate electricity.

The claimed Levelized Cost of Energy numbers leave out many large expenses, including fossil furl backup, long transmission lines and the much shorter lifespans for windmills and solar panels versus other sources of electric power power.

LCOE really means Liars Cost Of Energy.

It’s transitory.

…..

Next time it will be even higher!!! I promise

– Pow Team

Why should Powell care? Like James Cagney’s Cody Jarrett character, he’s “made it ma, top of the world”. It’s nothing but rainbow for Jerome from here out. When he retires the money will flow into his pockets. Powell is taking care of the only people who count.

By the way, He’s tearing his hair out in that cartoon because one of the maids showed him the price of caviar.

Just wait until the IRS makes their tax adjustments. Every Gov’t bureau will increase “fees” too, but they are not technically taxes.

Still it all comes out of the pocket doesn’t it.

“Regular Americans”

Please define, as I am unfamiliar with this term.

Use your head and try to figure it out. You can do it!

Regular Americans are those who don’t have to shop for clothing at a Big and Tall Shop.

@Richard Sure it’s not the other way around?

But the Fed says it did all this ZIRP and QE

to *support* the economy. Is it possible things don’t work the way the Fed claims?

They’re “supporting” their bank accounts. They were frontrunning Wall St., day trading on their own future policies. They were using the US Treasury – the money of the people – to amass fantastic personal fortunes. There has never been a greater level of corruption. This is treason, and should be treated as such. Powell should be removed from office IMMEDIATELY. Instead, this corrupt-to-the-core Cadaver In Chief, has nominated him for reelection. He likes what he sees.

Wolf, FYI you were quoted in this article.

https://dailyreckoning.com/the-truth-about-todays-blowout-gdp-number/

Thanks for letting me know.

These people quoted me as if I had said this about the Q4 2022 GDP report, which is BS. I wrote this in April 2019 discussing the Q1 2019 GDP report. And I’m not an “affiliate” of them either. They just publish some of my articles. I need to tell them to stop it. This is garbage what they’re doing.

Your statement made sense even out of context. A large quarterly increase in inventories is good news if economic growth is accelerating. But I don’t see that happening in 1Q 2022.

That Reckoning website is strange:

They wrote:

“Assume the government pays a fellow to shovel out a hole. Assume further it pays him to shovel it back in. In the official telling, you have just witnessed an increase to the gross domestic product. Have you? Or have you merely witnessed a derangement, the fruitless birth and death of a hole?”

That’s very colorful language, although I have no idea how it explains volatility of inventories from quarter to quarter.

Sounds pretty FN stupid to me….and…..”colorful”?

Assume a CORP designs and advertises a car/fridge/washer, or whatever, that people can talk to…..

The DOW is up for the week, erasing the entirety of the losses. Weimar Boy Powell is a gutless, yellow-bellied coward. He is one of the weakest human beings we have ever seen in power. I bet his handshake is like a cold, wet noodle.

Day isn’t over bud. Markets have been moving to the opposite of the open every afternoon.

B of A called for 7 rate hikes this morning. Don’t give up on the Fed as an inflation fighter just yet. Employment is going to remain near a maximum for quite a while as far as I can tell, gives them a lot of room to act.

Day’s over now. Finished green

Not just green, 565 points green – a parabolic moonshot at the end.

Multiple Wall St banks recently lifted their predictions for fed funds rates this year and next. Looks like 1.5-2% this year and 2.5-3% next would not be a big shock to investors now.

Maybe the FOMC’s forward guidance dot plot will reflect this at the next meeting or they may take another couple of meetings to catch up. As long as inflation and jobs reports stay hot, this tightening of forward guidance could continue for many months.

Next up is the Jan jobs report next week.