Forbearance Effect: Serious delinquencies of mortgages & student loans plunge to record lows as delinquent loans in forbearance don’t count as delinquent.

By Wolf Richter for WOLF STREET.

Our always amazing American debt slaves are still borrowing, mind you, but to the great consternation of the Fed, they’re reducing their debt where banks and shadow banks make a big pile of their money: credit cards and other high-interest-rate debt such as personal lines of credit.

Total household debt – mortgages, HELOCs, credit cards, auto loans, student loans, and other debt – rose by $85 billion in Q1, to $14.6 trillion, according to the New York Fed’s Household Debt and Credit report Wednesday afternoon, based on data from Equifax.

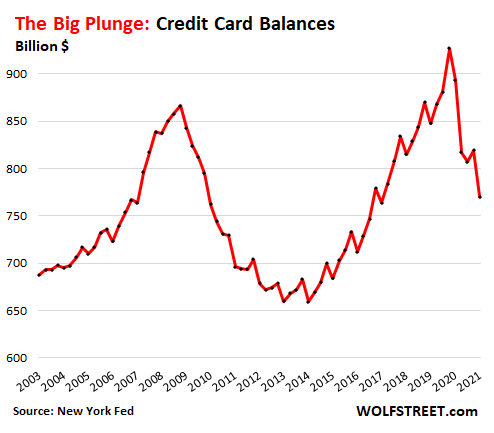

But the thing is, Americans paid down their credit cards in Q1 by the second largest amount ever, by $49 billion, behind only the $76 billion they paid down in Q2 2020. “One of the most confounding changes in debt balances,” the New York Fed called it in a blog post. In the five quarters since Q4 2019, the last full quarter of the Good Times, Americans have paid down their credit cards by $157 billion.

In the wake of the Financial Crisis, credit card balances also plunged, but they took a lot more time – four years, from Q4 2008 to Q4 2012 – and it wasn’t because consumers paid them down, but because consumers defaulted on them, and those balances were written off.

This time around, there are waves of stimulus money, and PPP loans, and extra unemployment benefits, and eviction bans, and foreclosure moratoriums, and rent aid, and whatnot. The government has taken a fire hose and has sprayed the land with cash, and it has put collection of some debts on hold.

Many consumers received the series of stimmies, starting in April 2020. For many of them, it was extra money that suddenly showed up, and instead of putting it into a checking account where it serves no purpose, some people used it to pay down their usurious-interest rate debt – smart thing to do.

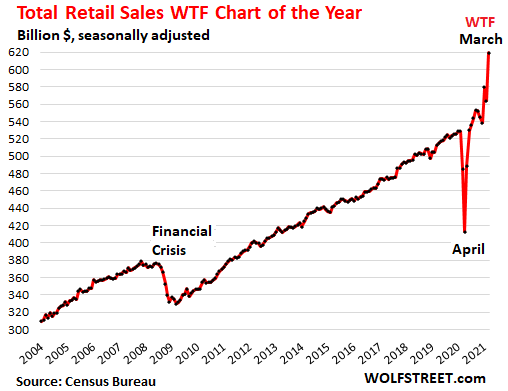

Some of the stimmies were also spent on goods, as retail sales have experienced a glorious previously unheard-of WTF spike despite the drop in credit card balances:

Those people who used their stimmies to pay down their credit cards and those that used their stimmies to contribute to the WTF spike in retail sales may have been two separate groups of people with only partial overlap.

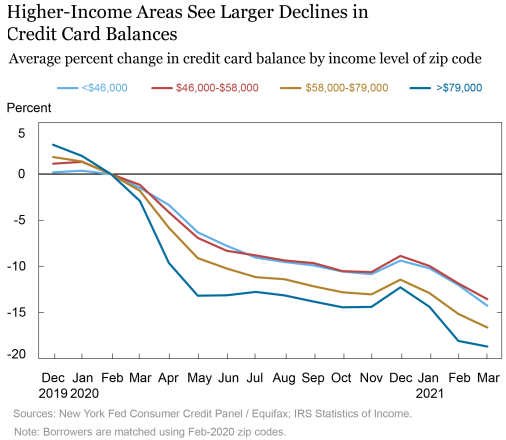

People living in higher-income zip codes paid down their credit cards more than people living in lower income zip codes, the New York Fed found, based on data from the IRS on income levels by zip codes, and Equifax data on credit card balances for those zip codes.

In high-income zip codes (over $79,000), average credit card balances have fallen by 19% over the year; in the lowest-income zip codes (below $46,000), average credit card balances have fallen by 15%:

The fact that the Fed is trying to sort out this phenomenon of Americans actually paying down their usurious-interest debts and depriving the banks of some serious moolah shows how serious this situation is.

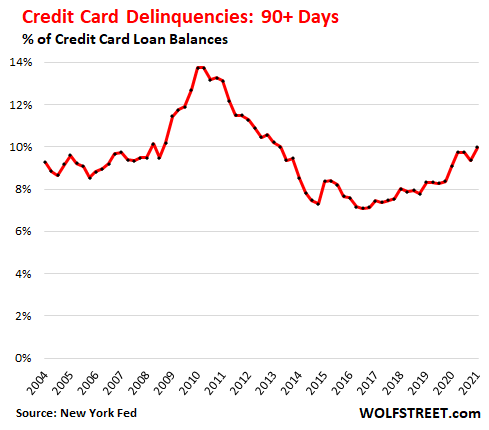

Despite the stimmies and the other government moneys washing over consumers, the serious delinquency rate (90+ days past due) has been high and in Q1 hit 10% of total credit card balances, the highest rate since 2013, according to New York Fed data. But it remains far below the Financial Crisis peak of nearly 14%:

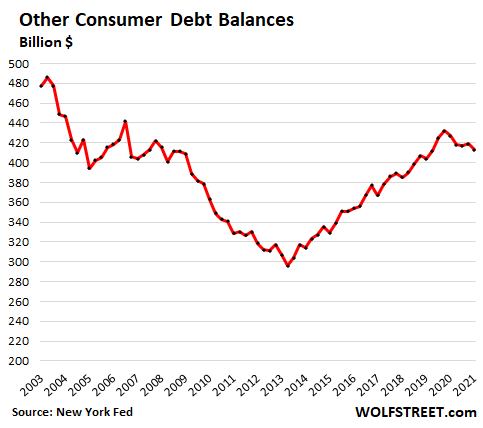

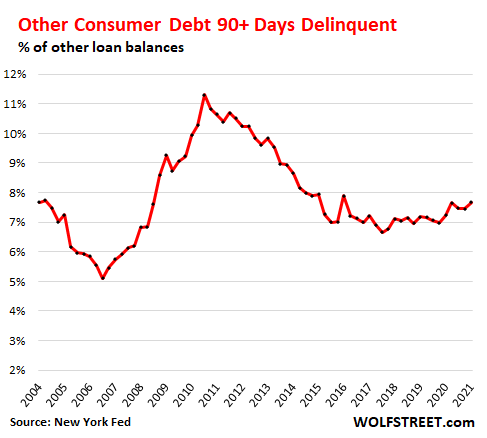

“Other” consumer debt balances also declined.

The balances of personal loans, lines of credit, and other loans from banks, shadow banks, peer-to-peer lenders, and payday lenders have declined during the Pandemic, after rising for years. This too was an effect of the stimmies and other measures. In Q1, balances dropped by $6 billion from the prior quarter and by $19 billion since Q4 2019, to $413 billion:

Serious delinquencies of 90+ days past due ticked up to 7.7% of total balances, having risen steadily since the recent low of 2017, but remain below the peak during the Financial Crisis:

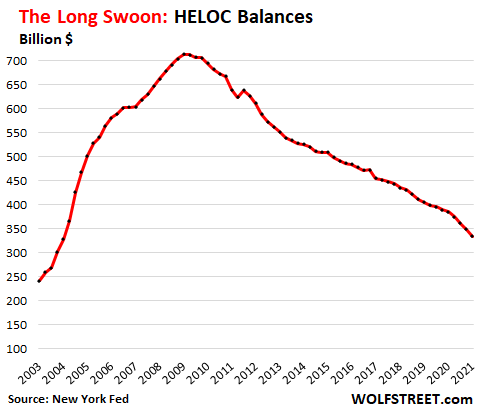

HELOC balances decline on decade-long trend.

This is a long-term phenomenon that started in 2009, when people massively defaulted on their HELOCs during the mortgage bust, and it has continued unabated as people have switched to cash-out refis to leverage up their home, rather than relying on HELOCs.

Balances declined by $14 billion in Q1 from the prior quarter and have plunged by more than half since the peak in 2009, to $335 billion, the lowest since Q1 2004:

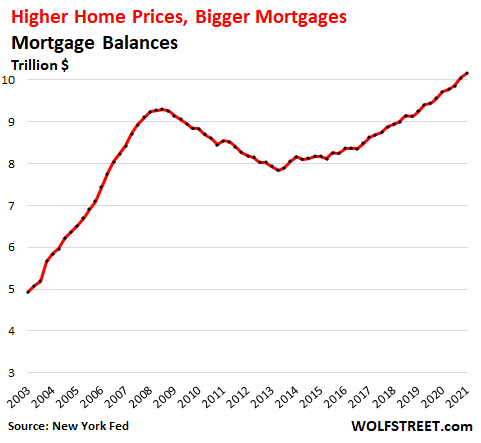

Mortgage debts balloon with home prices.

Mortgage debt jumped by $120 billion in Q1, after jumping by $182 billion in Q4, powered by record-high levels of mortgage originations and ballooning home prices that require ballooning mortgages:

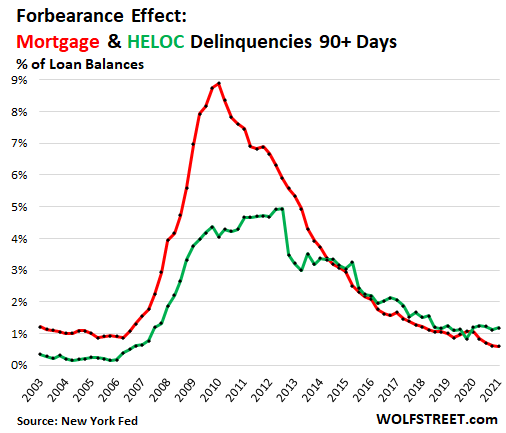

Mortgage forbearance at work: serious delinquencies drop to record low.

The balance of mortgages that are 90+ days delinquent declined to 0.59% of total mortgage balances, a new record low in the data.

This comes as 2.2 million mortgages are still in forbearance, according to the Mortgage Bankers Association, and those that are delinquent don’t count as delinquent in this data here, which is from Equifax. Forbearance programs have been extended.

Forbearance is also the reason credit scores have risen during the Pandemic: credit bureaus don’t count delinquent debt that is in forbearance as delinquent.

Also shown: The HELOC delinquency rate (green line) ticked up to 1.18%, but remains at the low end of the range of the 12 years:

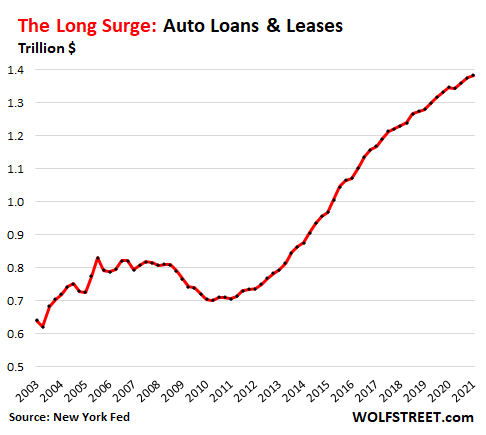

Auto loans and leases.

Soaring new and used vehicle prices lead to surging loan balances. The balance of auto loans and leases rose by $8 billion in Q1 after having surged by $14 billion in Q4 and by $17 billion in Q3, from record to record, except in Q2 when loan balances dipped as auto sales briefly collapsed:

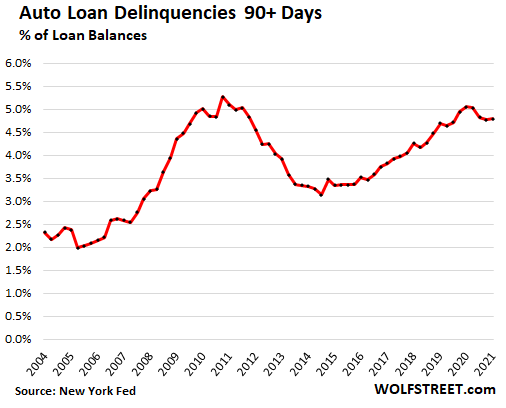

Seriously delinquent auto loan balances have dipped during the Pandemic as stimmies were used to catch up with car payments, but after growing for years, they remain high at 4.8% of total balances. During the peak of the Financial Crisis, seriously delinquent balances peaked at 5.3%:

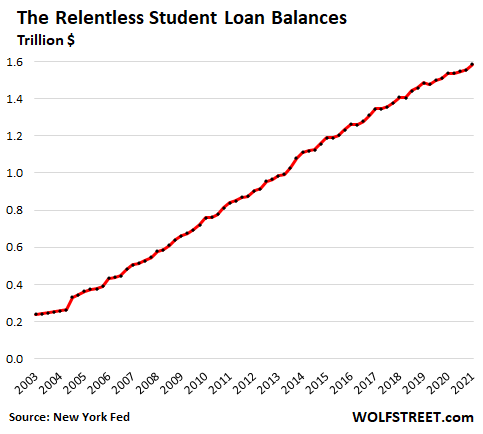

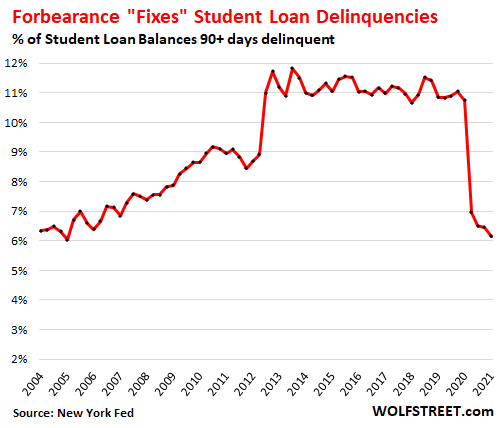

The Student Loan Quagmire.

Last year, all government-backed student loans were automatically enrolled in forbearance programs that have now been extended. And everyone is hoping for loan forgiveness. As a consequence, few borrowers are making payments on their student loans.

And even as new student borrowing was down last year as many colleges could not charge for room and board, and some had to refund the amounts already paid for room and board, student loan balances continued to rise, but at a slower rate. Then in Q1, student loan balances jumped by $29 billion, in line with Q1 2019.

Repayments had already been minimal and declining for years. These low repayment rates in the past, based on numerous programs available to borrowers to slow or stall repayments, were a large contributor to the ballooning balance of student loans even as college enrollment has declined every year since 2011.

Student loans that are in automatic forbearance don’t count as delinquent in the Equifax data here, and so the rate of seriously delinquent student loans plunged in Q2 last year, when the forbearance went into effect, and continued to decline, and in Q1 hit a record low of 6.2%, even as loan repayments have ground to a halt:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Debt Slave Revolt!

A growing percentage of Americans in living lives in states of precarity and peonage.

Yeah, “precarity”.

If job, medical, house/car repair, etc, issues hit, being able to use that precious credit card right then, may be the last thing between the “luckier” folks and the payday loan bunch. I already see tons of ads on TV for cash advances/loans using smart phone.

The next level is homeless?

Nobody had very much in the lower middle class when I was growing up, BUT, few worried about losing what little they had. That IS a BIG DEAL….It is NOT so today.

The Lender has been the slave to the borrower since 2009

historicus,

Fed is slave to the Lender, though….

The Lender has been the slave to the borrower since 2009 BC

Corrected that for you.

Actually the the reverse is true. The banks get money for almost nothing and then lend it back to you for 2.5 percent and more..much more. Credit card companies lend money at rates of 8-29%.

PROVERBS 22:7 “the rich one rules the poor, and the borrower is a slave to the lender” True since money was invented!

You can only get next to nothing interest wise saving money, but you can garner up to nearly 30% on the wrong side of a credit card balance so easily.

Seems like a no brainer paying off a credit card…

Yeah, but it seems it took decades for Americans to get that.

Us boomer hippies tried to point what “THAT” really IS out, as did Carter, but he was canned immediately for heresy. But he just wandered off and built small houses, knowing he tried, anyway.

Us hippies just wandered off to the communes, Vietnam, or Canada….or eventually sold out/were bought off by “THAT”.

I don’t think many ever got what “THAT” is……all were total advertising victims…..why it’s a business tax deduction still pisses me off, with all due respect for Wolf’s situation.

But how to pay off credit cards? Take a HELOC or REFI with 30 year and wrap that up with super low rate but over 30 years? Added bonus of tax credit for the interest

The amount of money we threw at people had to be historic. It was enough to drive inflation to insane levels and at the same time allow people to pay down their credit card balances.

I’ve said this before, why not have a new pandemic every month?

Don’t give DC any ideas…

That aside, your pt is very well taken, that looking at these specific delinquency/default charts in isolation is very misleading…since the stimmies simply created enormous federal debt (read money printing/inflation) in order to keep individuals’ delinq/default levels lower than otherwise.

Damaging the currency/creating inflation in order to improve some other metric isn’t a “win”…it is exactly what it has been for the 20 yrs of ZIRP…a wholly unvoted/unacknowledged redistribution.

Got to thinking…. Call me dumb but I think the whole game plan is to have massive inflation without ack it. This keeps people in a panic of spend spend spend since CASH is DEAD or at least going to lose so much value that you better spend it before it is whittled away by the scary Inflation monster. So fake creation of panic buying to induce people to FOMO

This is what the authorities did during Weimer Germany in 1021 and 1922 to cover up the pact that they could not pay the reparations. They tried to inflate away their debt. It worked for awhile and then it didn’t.

Most credit cards are a better way to earn “interest” via cash back then a savings account. But its not a plan, it’s not done on purpose. Are we fighting a plague or are we fighting deflation?

I don’t disagree with you, just don’t want to be censored ;)

Now debt, that may be a plague. But nobody forces the population to be responsible with their money………..

Is this an acid trip, or what?

It all depends it you place a purple microdot in front of a round number or behind it…

I don’t see any fractals in the above charts, also, contemplating and experiencing the universe in a more interactive way feels a lot more satisfying than contemplating what the hell’s wrong with our economy.

I guess maybe on an emotional level the Fed and U.S. govt are the substance of a perpetually mild nightmare trip, but then again, maybe it only matters if you think it does. We’re here today and gone tomorrow. Luckily (or unluckily depending on if you believe in higher reality) for billionaires, they can pay a lot of money to be cryogenically frozen until resurrection day. That is, unless the Chinese halt supply lines or Americans go nuts buying electronics and suddenly they can’t get the parts to repair the freezers. Good times, good times.

Still, it’s kinda nice to see people running a BS racket (cryogenics) on people who accumulated wealth by running bigger rackets on all the rest of us.

Where I used to work we had literally tons of LN2. We first threw a cricket in and he just crunched up. We tried a slow method holding him way over the vapor (took an hr) and he looked ok. Put a lamp near him and another hour or so unfreezing. Like all simple animals (even dead humans) he moved his legs a bit. We tried this several times, but never had one crawl off afterward.

Besides, who is to say the place doesn’t go BK, or corporate raided, and all the equipment sold for scrap….and the heads and bodies go into one stinky dumpster.

Probably why I still like watching Columbo….we need many more higher level cops like him.

Feeling more like shrooms, the grodiness is more pronounced than a Berlin microdot. Or so they say. And less to grin stupidly about

Ha-Ha!!! Nowhere near one Mr Turtle, nowhere near…….trust me.

Wolf:

I think “The comes as 2.2 million mortgages are still in forbearance, … ” wants to be This comes as 2.2 million…

Oh, and please delete this comment.

Lisa_Hooker,

Thanks! I always appreciate the important work of my line editors… I’m guilty as charged, using and appreciating unpaid labor :-]

At least she’s over 12.

Except for the end of the article about student loans and rising mortgages, what a good news article. People seem to have learned about paying down debt.

Kind of a ‘debt jubilee’ with a middleman, the consumer, handing the Govt money over. So I guess it is another kind of bailout for the CC companies in the long run. Still better than defaults.

Now, back to work and no computer. :-)

“Kind of a ‘debt jubilee’ with a middleman, the consumer, handing the Govt money over.”

I really liked this comment. We got so many middlemen now.

As a public service announcement: “Govt has no money. All the money it has is taken from taxpayers or by means of inflation tax”.

Banks are not making 20% interest on that credit card debt, they are sure not happy with everyone who has put their stimulus money to paying off CC debt.

I bet the pawn stores and payday loan places are also extremely unhappy about this.

I think it’s time for the banks to start flooding everyone’s mailboxes with new credit cards with special offers like 80,000 miles free on United if you charge up $5,000 in three months.

That should get the ball rolling for the banks again.

Anthony,

To qualify for that United card, you probably already have to have excellent credit. Spending $5000 over a period of three months is not a big deal to many people. You just switch your spending from your other cards to this one. As someone who takes advantage of these deals, I’m never going into debt on one of these promotions. I pay off my entire balance every month.

Oh Harrold, now I won’t get a wink of sleep worrying about banks and pawnbrokers and payday loansharks not profiting from the misfortune of others.

If the Fed had wanted to help Main Street vs Wall Street with rate manipulation, they would have figured out how to reduce the charge on credit card balances. But that is the golden goose for the banks, so they didnt.

Then they splash money around and the people take it and pay down their balances. The Fed didnt see that coming. The banksters must be upset.

For every action, there is an equal and opposite reaction…in Physics and Economics

Sorry, but I find applying Newtonian Physics to today’s Economics patently absurd.

A Biloxi pawn shop I buy coins from has no unredeemed merch to sell, no loan demand, pistol and rifle ammunition@$100/box, if they have it. Gas 2.65 available

Here comes the debt deflation. Hope y’all have some of that pitiful asset called cash.

Forbearance is just another term for “kicking the can”. It’s been kicked like crazy for years. Some day this is going to go south, but not before the banks and their Fed puppets try to save their asses by any means possible .

Like the Romans calling back Cincinnatus fromhis farm we need William Black.

There’s nothing that says that kicking the can cannot be extended. We still have years to go. Heck we might already be dead when the whole thing implodes.

I think the only way it implodes is if we learn the art of local feudalism. This might happen when enough people discover there’s more value and quality of life in supporting local small organic businesses, boycotting multinationals and resisting federal interference. I expect the luxuries we take for granted are soon going to cost us 2-3 times more than the money were able to earn. As demand is reduced, prices will rise and the benefit of hard work, and innovation will have no reward or incentive left. Time will be better spent and directed towards self-sufficiency rather than participating in city life.

Stoneweapon:

A rebirth of the “commons” in the middle of America’s streets!

Monkey,

” Heck we might already be dead when the whole thing implodes.”

—

Quite possible. With all the Covid mutants flying around.

Just heard 10th death in the extended family –

yep. you guessed it. was in India

Michael Gorback,

Debt deflation means debt gets defaulted on and gets written off, and holders of this debt (lenders, bond holders, stockholders of lenders, etc.) eat the losses. Those huge losses on debt triggered the Financial Crisis.

If the Fed hadn’t bailed out those creditors, “cash” (Treasury bills, etc.) would have been a great investment to make it through the period and have liquidity to buy stuff at fire-sale prices when no one else has liquidity left.

For now, given the historically loose financial conditions (thank you Fed) and government support, almost no company has to default… they can nearly always get fresh money. And business bankruptcies are way down. Similar for consumers. It won’t be a problem until asset prices (collateral) skid, and then all that debt (other people’s assets) will become a real threat.

That’s the whole game, Wolf, to protect “all that debt (other people’s assets).” This entire charade is so that pigmen don’t have to take losses on their bad bets.

1st step in “game” is having PEOPLE who OWN a large % of said “democracy” at federal level (which is much more costly), and who also OWN enough of (much cheaper) state “democracies” and are able to crush them like bugs.

Get the masses arguing mostly vague non-issues (red/blue and misc conspiracy crapp) and …well…here we are!

As one of my Canadian friends put it, “How can a corporation be a “person” if it can’t face capital punishment?

Some years ago when the euro zone first started with negative interest rates, somebody started an ETF that invested in physical cash (i.e. euro banknotes in a vault).

That sounds stupid at first, but makes perfect sense when you face the threat of negative interest rates, bank defaults and potential bail-ins of your savings (as happened in Cyprus with acccounts above €100,000), and a bond- and stockmarket meltdown.

I don’t think it caught on and I haven’t heard about it since, but I wouldn’t be surprised to see this reappear at some point.

Other physical-storage ETFs (e.g. for gold or silver) have expense ratios in the 0.2%-0.4% range. So that’s a limit for how deeply negative rates can go before people will start Cash-storage alternatives.

@Wisdom Seeker, in the eurozone, banks are already routinely charging -0.5% on bank accounts above a certain limit, on top of the bail-in risk that you have!

Kinesis Money (100% allocated gold and silver in your own name) actually pays a positive yield on gold/ silver holdings (from shared transaction fees). I expect a lot of savers are going to find their way to them if the current central bank clown shows keeps going on.

But of course then you have the risk of the gold/ silver price relative to fiat money and that can go both ways (at least in the short run), so it is not a 100% alternative for cash.

So I would actually still be interested to put some cash in an allocated physical cash ETF that is redeemable even if it charges -0.5% because at least you avoid the bail-in risk of the banking system while avoiding the gold/€ exchange risk.

Wolf, what can’t go on forever won’t go on forever. Eventually that debt has to be discharged by either inflation, paying it off, or default.

It would take a ton of inflation to eradicate this much debt. However, long term debtors would love it. Can you think of a huge long-term debtor? How about a huge long-term debtor that can control money supply?

To quote Jim Reid, “When you have full control over how much money you can print and spend . . . you can always create inflation if the inclination is there regardless of demographics, digitalisation, globalisation or weak growth.”

Good luck with that infrastructure plan. Nope, not inflationary at all. Nothing to see here.

I don’t see people paying off their debt. I see a tidal wave coming when forbearance ends – unless the government is stupid enough to try run the GFC solution again. Business bankruptcies down? What businesses are left to go bankrupt?

That leaves door #3, default. There’s a difference between immediate and inevitable. I’m talking about inevitable.

I have no idea about the timing but there’s really no escaping debt deflation. And debt deflation is not a cause, it’s a result.

Well, there is a fourth option. Remove the debt from the books, less checks and balances. Remember it is all FIAT money and money is only entrants in a database.

Find a way to it without to many recognize and to quiet all concerns and there we go. Debt gone without the banks losing anything more than future interest. And, the amount of money deflates.

Sams,

One person’s debt (loan, bond, mortgage, etc.) is another person’s asset. If you wipe out the debt, you wipe out the asset. That’s what happens in bankruptcy court on a small scale — see Lehman bankruptcy. But now imagine if this happened on a large general scale, as you propose.

We only get bankruptcies from gross negligence, ineptitude, and malfeasance. This corruption of basic economics is da fault of the FRB.

It’s easy to get discouraged if you are conservative with finances and investments instead of short term leveraged momentum trader. I member Charlie Munger’s words which is to invert the situation to look for opportunities. Things are so divorced from fundamentals and if history at least rhymes there are going to half price sales on a lot of assets in the next few months or years.

Agree with your comment part about going to bee a lot of half price ‘stuff’ for sale OS,,,

Only question is when, not IF!

Been in the RE related construction mkt, mostly, for the last 60 years or so, and have seen the cycle, clearly at times, since 1956.

Stopped with the SM in the 80s due to perceived manipulations, and clear records of NOT making serious profits except with what is now known as insider trading now forbidden except for what DC calls, appropriately IMO, ”pigmen” of all genders, but especially allowed for our current crop of pig people in guff mints.

Time and enough to make ALL Laws and the rules and regulations following those laws THE EXACT SAME FOR EVERYONE!!!

My main hopium these days is that we can really make this happen before the situation deteriorates to the point of revolution, at which point nobody wins.

Gold and gold stocks are filthy cheap, some sporting 3 or 4% dividends and a PE of 15. Plus it’s a hedge against more monetary insanity, which is practically guaranteed at this point.

Lest we forget – some animals are created more equal than others as George told us long ago.

I still wouldn’t buy the overall stock market at half the price. It would still be historically expensive.

Also, stuff is leveraged at so many levels. Not only people buying stocks with margin debt, but also corporates have record amounts of debt and profits are artificially high because of all the stimulus. So the record high P/E ratios are actually artificially low because the “E” is artificially high. And then there is the Fed put that everybody still believes in, propping things up.

If this goes into reverse, all these layers of leverage are going to work into reverse. It will be really ugly.

So borrowing money to buy stocks of companies that are also borrowed up the wazoo is a bad idea?

When the cost of money is manipulated you can’t analyze fundamentals.

The CB’s have been undermining the profits of the commercial banks. My business qualified for a $60K interest free loan for 30 months, $20K forgiveness if $40K is paid by Dec 2022. The funds were deposited in my business operating line, therefore my bank just lost approx $10K (7%) in income. It’s a domino affect, because I now have an extra $10K to make sure the full balance of my credit card is paid monthly, and I still have the operating line I can use to stock inflationary/volatile raw materials for my order book.

Regarding the HELOC’s, my bank offered to roll it into a fixed mortgage 4yr term at 1.79%, so I took it because the 10yr treasury was on fire just before the offer expired. I keep enough reserve on the side just in case the system unravels so I can pay out my loans if the bank calls them in or I decide to shut the factory down.

There you have it….

I forgot to add, the executive management of the commercial banks is exceptionally compensated via stock valuations.

The govt student loan forbearance was a good thing for those who still made payments. The entire payment went towards paying down the principle and the interest owed was forgiven. If your interest was $100 a month, it all went to the principle, and you saved $1200 in interest for the year. The bigger the loan, the bigger the benefit.

When forbearance ends, for students who have been paying all along, their monthly payments should reset to a lower amount.

I think the student loan forbearance is pretty big deal. My son still has about $30 student loan debt. He has a good job, but you know paying off any kind of debt is not fun.

Since he has been in forbearance he basically has been blowing the money that would have went to student loans. Forbearance is an opportunity. What have most people done with the opportunity?

Thing are worse for the banks than Wolf’s article might imply.

From the May 13, 2021 Wall Street Journal.

“JPMorgan, Others Plan to Issue Credit Cards to People With No Credit Scores”

It is aimed at individuals who don’t have credit scores but who are financially responsible”

I assume the banks will be trying to get every 14 year old with a paper route a credit card. Get em in debt young then they can later use student loans to pay off their credit card balances!

Robert,

I saw this differently. I saw this as a sign that credit scores are becoming useless because of forbearance and other programs that hide debt problems. Credit scores have surged during the pandemic because of all the ways delinquent debt is getting swept under the rug, which makes credit scores increasingly useless as a predictor of credit worthiness.

Banks have been saying for months that they’re trying to find alternatives to credit scores — newer smarter ways of doing it. And banks have the bank account info on their customers and banks can share that with other banks, and that tells them a lot about the credit worthiness of their potential client. To me that was a no-brainer. My question was: “What took you so long?”

Another element is that banks pay the credit bureaus a lot of money. So if they can figure out how to find a better way without having to pay the credit bureaus, they will do it.

I’m one of those idiots who doesn’t owe a dollar to anybody. I have not had any debt for 15 years. And I don’t even own a credit card. I used to have a few with BofA but closed them when I decided they were a filthy organization during the financial crisis, and also closed my checking account to open a new one with a credit union. I never applied for a credit card with the new credit union.

Then, a few years ago I was thinking about renting a car and found that many rental agencies were starting to require a credit card instead of the debit card I used to use. So, I decided to apply with my bank (no longer the credit union from years ago) for a credit card. I had 6 figures in my savings account with them. They declined me for a credit card! Haha. I was absolutely floored. I do not have bad credit whatsoever, the problem is I use very little credit, the last time being over 15 years ago for a small auto loan. So, I still have no credit card but it really hasn’t mattered.

You can likely get a secured credit card. Ask the bank.

I’m sure I could, but my interest in that sort of “product” is LESS THAN ZERO. The idea that I would loan a bank my money so that they could turn around and charge me interest on it is preposterous. OVER MY DEAD BODY. But I’m not the kind of guy who pays interest. In fact, my goal is to never pay another dime of it so long as I live.

DC, you are missing out on free 2% cashback.

I am one of their ‘bad’ customers who pays off every month and bags the 2% cashback. I find it easier to track my spending this way too.

Whenever possible I pay cash in small shops to save them the credit card transaction fee.

Since you already have your savings at the credit union, why not use some of that for a secured credit card? It won’t cost you anything extra.

I would have told them they either approve that card or I cancel my account and move all six figures of that savings out.

If ya can’t beat ’em, join ’em.

The aberration of negative interest rates got ya down? It’s not just for bloated European bureaucracies. Join the party and play along.

Get a card with 2% cash back, use it for everything, pay it off on time each time every time. Bada bing, you just got yourself a negative 2% interest rate on your “debt” for the month.

Where does this money come from? Dunno… I guess from people who forgot to set up auto-pay.

I am in the exact same boat for 15 years as well. I still think it’s the way to go especially if you are older. It teaches you discipline and every decade or two when there is a bust you can buy financial assets or car or real estate in a panic for cash.

Ha, that’s the way to go. No credit score because zero debt for a long time? Very Dave Ramsey. We’re debt free “fools” too, but haven’t been able to give up our 5% Amazon card. We buy 90% of our things and food from Amazon and get $1,000+ back in a year. The card gets paid off every month.

The world is designed on people being debt slaves. I never had any debt in my life, so when I wanted a credit card I had problems getting it because I had no credit record! A bank balance in high 6 digits and a well paying job (at the time) didn’t matter. I was baffled. I did get a card finally, but with very low limit.

Anyway, I almost never use a CC and always pay off the balance. They have never earned a single $ in interest from me.

” I still have no credit card”

This underscores my view that credit scores aren’t to find out who is creditworthy – they are for finding out who is profitable. People who pay on time are not profitable. Too much debt sends the payments to zero, so the key is to keep people solvent, but just barely.

Banks also like these programs because they can replace loan officers with computers that never take a day off or complain about being coerced to sign people up for stuff they don’t need or even know about.

I have a bit less than a dozen credit cards. I have paid every one when due for over twenty years. I don’t pay interest or late fees. I get cash back that the merchant or folks that carry a balance pay. I have over $150k in credit lines should a true emergency arise. For decades I kept a daily journal of expenditures, now I just archive the statements and downloaded monthly xls files. I do keep a journal of card expenditure dates and am careful to spend something on each card at least twice a year ($5 hamburger ;-). The convenience is wonderful. I pay cash whenever I don’t want the transaction published.

That doesn’t sound convenient at all! That sounds like a huge amount of effort for what exactly?

I am often confused about credit scores.

I refi’d last year and being responsible, went to a few lenders for quotes. After the 3rd credit check, I noticed my credit score dropped 40 points. So much for being responsible. Even if you close the loan, the credit check ding isn’t removed until after a year.

Last month, I purchased a high priced item at Lowes and put it on the card. My credit score dropped 60 points due to “A large increase in balances”. I paid off the charges completely and am waiting to see how long it takes to recover those 60 points.

I always pay off my card but even then, using it too much negatively affects my score.

Unless I’m buying a house or car, I really don’t care. Should I?

This is kind of like a game with multiple articles online on how you can improve your credit score. Most don’t involve paying off your card.

Yes. In fact, paying off your debts will LOWER you FICO score. Applying for new credit also lowers your FICO score (briefly).

There have got to be better ways to evaluate credit worthiness than that silly FICO score.

The purpose of the FICO score seems to have changed over time.

In the past it was perhaps a measure of creditworthiness. Now it’s like the Pied Piper’s flute, an instrument of social influence that makes people dance to a particular financial tune.

There probably is an opportunity for another kind of score. Call it the financial intelligence score. Any borrowing for consumption would reduce your score.

Been following the credit ratings agencies, as they are to the consumer economy what mastercard was several decades ago. Someday we won’t spend money we will use points from our credit score. Equifax had a serious data breach, then the Biden admin hinted they would like to nationalize the agencies. Then the shareprice hockeysticked, vexxing my plan to bottomfish the stock. Credit scores may have to take a Chinese turn, with social metrics. Are you a good citizen or an insurrectionist? We shall see.

One step away from China’s social credit system.

Amazing thing is when it is introduced, many people will praise how amazing it is.

re: “Banks have been saying for months that they’re trying to find alternatives to credit scores — newer smarter ways of doing it.”

I certainly hope so; FICO holds WAY too much power over consumers with, AFAIK, no regulation or oversight. I interviewed with them once; I felt like I was in a CIA command center.

The UK model of credit is/was very similar to how it seems the US version works; the more debt you have historically taken on, and made your regular payments on, the more debt they’ll give you.

My wife, who came to the UK as a student from Switzerland around 2001, was astounded to learn that she couldn’t sign up for a phone contract despite having money in her newly opened bank account that would more than cover the annual costs.

I had precious little money in my bank account at the time, with a pitance coming in each month, but had a few mostly unused credit cards with quite high credit limits (each one roughly equivalent to my annual income at the time), and plenty more offers of cheap credit had I wished to accept them.

Never having missed a payment, I was apparently a low credit risk, despite having virtually no money.

Here in Switzerland, it works the other way; the banks or lenders look at your yearly tax return and any current debts such as mortgages or car loans, and if your outstanding commitments are more than a certain % of your income, they won’t lend to you, despite the fact that your own calculations may show that you can make the payments.

FICO is garbage. When I got divorced I changed bank accounts and credit cards.

I have no debt.

Without a wife, I went from 11 credit cards in my name to only 4. Of those, only one has an outstanding balance – a Visa card with awesome benefits.

The others are there because I could use store cards like Best Buy and Cabela’s for discounts on large one-time purchases. Those are paid off. The 4th card goes back to 2005 and I don’t even know how I have it.

My FICO score still hasn’t fully recovered. When I reviewed the criteria everything was “excellent” except my credit history average is only 6 years and therefore only rated “good” and my credit use was just “looks good” because I have so few cards and no debt.

So I’m 68 years old and despite my age I have a 6 year credit history. If you don’t use enough credit it hurts your credit score.

FICO punishes you for being financially responsible.

Yes, FICO is a ridiculously twisted measure.

Thats hardly new. When I was in college you could get a free t-shirt for signing up for a credit card.

However, I am puzzled as to how its possible that 10% of adults in the US have no credit history.

How are these people able to stay invisible to Equifax, Experian and TransUnion?

It’s not hard. Just be poor. I mean really poor. Credit is the working man’s albatross. Or at least one of them. When I was in my early to mid 20s I cashed my paychecks at Walmart and paid cash for everything and used prepaid phones etc. No banks, no credit, no debt, nothing. Couch surf and pay cash to room mates.

I never stopped living that way. I do have a few bank accounts, a monthly cell phone bill and the usual insurance and other recurring bills, but I pay cash and don’t use credit or buy anything I can’t pay for that day.

Before covid I got nearly invisible. I paid cash for everything. All of my utilities were included in my cash rent. I had to pay car insurance with a bank transaction, but that was about it. It became a fun game really. Didn’t even have a mailbox.

Folks, what some of you don’t understand is that no one is “invisible.” Regardless of what you think you are doing a dossier is being kept on you. That’s their business and a profitable one. You can play the game correctly and feed them what YOU want them to see, or you can try hiding and allow them to publish whatever they can scrape up. It is the credit agencies well-paid JOB to sell information about you. They will find some and they’re not about to quit.

THIS IS OUTRAGEOUS!!!! I CAN’T BELIEVE YOU PEOPLE ARE PAYING OFF YOUR DEBTS!!!! NO MORE STIMULUS FOR YOU!!!!! I WILL NEVER RAISE RATES!!! GO BUY YOIR $10 FAST FOOD HAMBURGERS!!!! YOU’RE WELCOME!!!!!

Some of the “lower credit card balances” could be high-flyers simply spending less on credit cards, due to everything being closed, no travel, no business lunches etc.

Is there a way to break out the data between “balances earning interest” vs. “balances paid off on time”? That would be informative as to whether debt is actually being reduced, vs. lifestyles constrained…

Exactly this. I always balk at the “what is the balance on your credit card” question. It might be x dollars but that will be paid off when due.

Yes!

My credit score is based on instantaneous balances for my credit cards. Even though they are all paid off monthly and don’t accrue interest, the score seems to go down rapidly if I have a high balance one month. It seems to go back up slowly when the balances decrease. It seems to be measuring instantaneous debt that is covered monthly rather than longer term debt.

Since I don’t travel now, the balances are lower.

A chart with the total of all debt that is paying interest on credit cards would be interesting. ie cards that are not paid off on time.

1) it would show all of the CC debt paying 25%-30% interest on the cards long term.

2) It could also show short term spikes in CC debt when people are getting into trouble and can’t pay the current CC bill.

I use the credit card as a convenience rather than carrying a suitcase full of cash or writing a check. It is also easier to contest any returns for a refund when buying online. As a bonus, the 1%-4% points paid is better than having the cash in the bank.

The problem with cards is that I have to remember to pay the bill on time or there are late fees along with 25%-30% interest.

It is just like any utility bill, if you forget to pay, then you pay more.

After I got vaccinated, I did more retail shopping than normal. I got items without paying the $5.99 shipping fee. Specialty items are purchased online. I hate getting bad fitting shoes delivered from online. The mall shoe store went out of business before the virus hit.

I rented the streaming movie “Nomad,” for about $6.00. It was nominated for two academy awards. I checked movie theater ticket prices are $12.00. No buttered popcorn needed.

My debts were already paid down. How good it felt to pay off my student loan decades ago. People with no college do better financially in their careers than people with only some college, but no degree. It is good to learn a trade.

Said it in another post but will say it again but that mortgage debt chart pretty much backs up the thesis and research done by Fernando Ferreira, Joe Gyourko and Antoinette Schoar on the prime reason for the last housing bust. The debt level outside of subprime was much larger, combine these prime debt with derivatives and that was the powder keg needed to have everything coming crash down. Interesting to see we’re back and exceeded 08 and beyond.

Couple of interesting points from their studies

Your second surprising insight was that the housing crash was mostly caused by middle-class homebuyers — not by less-wealthy buyers with subprime mortgages, who are often blamed.

Right. Many economists studying the crisis looked at it through the lens that had been touted in the press: this idea that the subprime segment caused everything. We thought that seemed too narrow an understanding of what had been going on. Maybe because we were living in Boston, a city where similar effects were going on in middle-class or upper-middle-class neighborhoods.

If you actually look at the size of the subprime market in the US, it is very small. These are mortgages of people who are poorer, have much lower income and can only take very small mortgages. The typical middle-class person in the US has a mortgage of around $230,000. The typical subprime loan is below $70,000.

Most mortgage dollars lent in the US economy go to the middle class and the upper middle class. When those segments have problems, that’s when the banking system and the rest of the financial system is impacted.

What are you studying now?

We just finished a project where we looked at how people assess risks in the housing market, using a housing survey Fannie Mae conducts.

We found that despite having just lived through this crisis, American homeowners see housing as a non-risky asset. Renters, on the other hand, think housing is very risky.

We think this explains why these boom-and-bust cycles are sometimes so prolonged. Part of the population — renters — only convinces itself that housing is safe after it has seen steep house price increases. Renters jump into the market at the very end of the housing cycle. That’s obviously the wrong time.

That is probably one of the top five investing mistakes for any type of asset. Investing especially using leverage is always risky because future is always unknown, but good times give us a false sense that life will continue at current trajectory.

Read Minsky’s financial instability-hypothesis. See also Greenspan on “irrational exuberance” before he became a total sycophant.

I know several people who paid down CC balances, not because of increased income, rather because of the shutdown, their expenses drastically declined.

The executive order on April 27 to change the Fed contractor pay rate minimum from $10.95 to $15 could be helping pay off debt for Fed contracted workers.

A 37% raise in one year is a lot of extra money instantly. It would have been wiser to tier up such a raise over 2-3 years, years. Of course it would have been wiser to allow the economy to tier up naturally instead of artificially with trillions in printed money. That would have solved the “bottlenecks”, 200%-400% price increases on certain necessary commodities, etc. The money was injected too fast…and we are going to have to deal with a bunch of unintended consequences for a few years…

I agree. That same logic could have been applied to the recent 1.5 trillion dollar tax cut for the extremely wealthy members of our society but since that cash was stashed as apposed to being used to pay off debt, making the elite wait for their tax break may not have made a difference in the long run.

Ridiculous. I’m not a big supporter of the tax cut because it didn’t come with spending cuts, but that was $1.5 trillion over ten years. Much of the $6 trillion we borrowed in the past year has already been deployed. It’s not even close to a reasonable comparison.

In some ways the tax cut paid for itself as it extended the business cycle and brought new people in the labor market. I don’t think government revenues went down.

Then covid came and blew things to smithereens.

I’m not sure it paid for itself, simply because the extra money was used for buybacks.

But the fact is, our corporate rate should be competitive with other developed countries. It doesn’t benefit anyone for Apple to be leaving huge amounts of money in Ireland to avoid U.S. taxes.

The pay raise would only be 1 or 2 paydays so far. Not really enough time to pay off much debt.

Min wage for many States is above the $10.95 Fed min. Az, which is a pretty low wage State is $12.50 hr.

Doesn’t it seem likely as states start denying the Federal unemployment supplement, and money comes out of circulation, and more people return to the subsistence level, that this trend will reverse?

Although fact that higher income areas are seeing larger declines in credit card debt may contradict that. If that is indeed the driver of the credit card debt reduction, then it sounds like a cultural paradigm shift.

Incomes are up 9% from March 2020 to April 2021, according to Bloomberg today. If that continues, and humans start “thinking” inflation is real and long term, then we will have folks asking for raises, refusing to work and live on stimmy if they do not get paid more, partly because they question if the risk is worth the reward at $10-$20 buck an hour. Keep an eye on incomes, as that will be key to if this is “transitory” few months inflation or long term multi-year inflation spikes. The fed is playing a very dangerous game in which we do not have the tools to deal with, given the debt levels currently. This is not the 1970s…they can not raise rates from zero to 20%, they can not even raise rates from zero to 5% without the entire house of cards debt construct collapsing. Higher interest rates will initiate the debt resonance frequency and the Fed knows he is trapped below the resonance frequency limits. When the bottom 99% figure out the Fed is trapped, then that is when we see the real society issues happen. So far the majority are clueless when it comes to inflation and Fed idiocracy. I know I’m clued in almost daily because I just orded a product for my company that has doubled in the last three months, and cost me and extra that would have bought a new truck. The say don’t fight the fed? I say Fck the Fed…he is destroying small biz and true capitalism and “IF” inflation gets out of hand, the bottom 99% will finally catch on and perhaps start saying “Fck the Fed” too…as he is making all our lives way more complex and uncertain than it would be otherwise…

Per Bloomberg today (My exact concerns written more eloquently than I could write):

Inflation skeptics seem to think that explaining the quirks dismisses the problem. It doesn’t. The relevant issue isn’t whether one-off factors explain any one month’s data. Instead, the question is whether the accumulated effect of several months of price spikes — each driven by unique factors — leads consumers, workers and businesses to change their expectations about the pace of future price increases.

I have been a freelance contracted employee since the great financial crisis. The two largest companies that hired me in the past have lowered their wages post-pandemic. One has cut the hourly rate from $75 per hour to $45 for the same job. The other hasn’t cut per se, however they have asked about hiring me full time, but it would be at a lower rate than they pay me as a contracted employee and I would still be at home using my own utilities and equipment. Thankfully, I have many other smaller companies that care a bit more about their product and who they hire. True inflation will only happen with rising wages.

The experience of my company is different. We have been doing contract SW engineering for 32 years. (Founded in 1990. I joined in 1994.) Last year we did an across the board 20% bump in our hourly rate and there was no push back at all. None.) For our geographic area we are typically billing 2x to 3x the “customary” rate for contract SW engineers.

We are fully booked right now and everyone is working as much as they care to work. This is coming off of the Covid shutdown in Q3/Q4 of last year, when things slowed down for us.

This could turn around and end just as quickly as it ramped up. I have no idea how this is going to play out at the end of this year and into next.

YORT…

1000 +s

LOL… They’ll just push real rates even more negative to push debt levels backup.

God forbid we ever shrink our debt. Must protect all those “well-intentioned” people and businesses that took out loans. Clearly all those loans were for productive investment… none of those loans were used for speculative betting on markets, or self-LBOs to enrich equity holders…

Nope, must save the debtors, they are the worthy ones!! Screw the savers!!

… honestly… it’s deeply, profoundly insulting.

Overall debt is still climbing. Only a recession will reduce private debt through write offs. Government debt is still climbing faster than ever! The banks are still in heaven.

Have Fed Funds ever been 4% under the inflation rate?

Have 30 yr mortgages ever been under the inflation rate?

The Fed that knows better than the free market (just ask them) is trapped.

The citizenry will revolt at the arrangement , to meet the emergency of 2008 and COVID…that savings equal no return, and inflation is running at a rate that takes 45% off the dollar in ten years.

How is it that a Fed Chairman can boast of promoting inflation when he is INSTRUCTED to fight inflation with a “stable prices” mandate?

The Fed regulates itself because it knows more about the subject than Congress.

It gets to define “stable” as constantly changing (+3ish % now?).

I wonder what it gets to define “transitory” as…

Didnt Orwell say the first casualty of devious activity is the altering of the language?

Stable = Fixed according to the dictionary

Moderate (3rd mandate, “promote moderate long term interest rates”) = not extreme, up or down

Record lows are extreme by any metric.

The Fed alters the definitions of key words.

As for the Fed understanding better than Congress…

Simple understanding of the language doesnt require any great knowledge. And for observers of the Fed to witness things never before seen……ie the Fed PROMOTING INFLATION, that Fed Funds under the inflation rate is historically abnormal, that balance sheet expansion is historically abnormal, that Fed Funds 4% under the inflation rate has never happened before….

All beg serious questioning, and there actually are people other than the Fed that knows the game

Listened to an interview with Chris Whalen. Used to work at the Fed. He basically said the Federal Reserve is a sick monoculture who wants no one on the board with alternative views. T tried to get two independent thinkers on the board and they were DOA.

Here’s another Orwellian word:

Deadbeat – somebody who pays their credit card balance every month.

It is going to be interesting to see how this works out in Europe, because unlike the Fed, the ECB really has only one mandate: “price stability”. But they have announced that they not raise rates until 2024 or so….

The Fed’s stable inflation is akin to when Congress cuts the budget. Congress doesn’t cut absolute spending, they just cut the rate of growth.

Got to thinking…. Call me dumb but I think the whole game plan is to have massive inflation without ack it. This keeps people in a panic of spend spend spend since CASH is DEAD or at least going to lose so much value that you better spend it before it is whittled away by the scary Inflation monster. So fake creation of panic buying to induce people to FOMO

Economy is double messed up from debt and covid. It’s being sprayed with money and forbearance right now, but it’s still too foggy to see what things are going to be more than a few months out.

Normally an economy is self healing as people make adjustments. Fed says they didn’t want scarring so we are still stealing from our future to cushion the blow. At some point it’s got to go back to reality and then we will see what we have left of a functioning economy.

Being the world’s reserve currency has made us the world go to for consumption. It’s making for a sick country with perverse incentives. We probably getting toward the end of the road with current imbalances in world economy.

1) The big plunge : c/c balances.

2) Why Discovery big plunge since March.

3) Why JPM biggie said : everything is fine besides some problems in c/c.

Discovery used to send pre-approveds weekly, as my score went up they quit, perhaps such credit profiles presage poor profits for them. If a card prospect already has three cards without balances, they’re unlikely to run up a fourth. I wouldn’t, anyway.

During the time period listed below when there was no worldwide “Everything Bubble” where US markets reached record highs during a world pandemic thanks to Fed manipulation, the prime rate was raised to fight inflation. The rates were as follows using 10% as the start and end points:

October 13, 1978 10.00%

December 19, 1980 21.50%

May 20, 1985 10.00%

Cumulative Average of The U.S. Prime Interest Rate: 6.902%

The Median U.S. Prime Interest Rate: 6.00%

What would happen today if rates were raised to fight inflation? Besides crashing all equities, lowering property valuations and loss of demand for same due to many no longer being able to afford the monthly payments, etc., would it have an effect on the interest payments on the national debt?

Apparently, no one has any idea…

rates cannot be raised.

seasonal adjustments and hedonics seem to be the go to strategy to try to obfuscate what should be obvious to any consumer paying a modicum of interest to the prices they pay for most of the things they purchase.

the people i work with, who i will optimistically describe as not very booksmart about financial matters, are wise to the fact that they are getting ripped off.

once they find out how, and by whom, they are getting ripped off, we will see whether a new law encouraging 84oz Big Gulps and free netflix and robot delivered domino’s is needed to once again placate the precariat.

my money is on the 84oz Big Gulp.

Regarding 2% cash back:

I hate to appear to be anti-capitalist but I got an even better deal for ya. In order to capture the 2% cash back you have to first spend the 100%. Imagine the result if you managed to cut your spending by 25% :-)

The cash back is basically the bank splitting the fee they charge the merchant with you. The merchant is raising prices to account for the merchant fee as overhead.

You are really not getting anything back because you pay the entire cost of the merchant fee when you purchase an item. The bank is keeping some and rebating you some of the fee. But everything would be cheaper if people weren’t playing this game.

Some retailers charge a different price for cash vs CC. I haven’t seen this much in my area but there are some places around the country where it’s common.

You might see gas station signs that have both a cash price and a credit card price.

If you’re using a retailer that doesn’t discount for cash then you’re subsidizing the people with cash-back credit cards if you pay with cash. If I’m making a purchase where there’s no cash discount I’ll happily use my card, which often pays 2-3x cash back.

Reminds me of the time I bought a used car. After negotiating price I tried to pay with a cash-back credit card. The dealer and I had a good laugh and I wrote him a check.

Great article as usual…..

Judging from all the comments so far no-one really has a “clear” idea of where this economy is going.

All the old rules of doing business, borrowing, spending seem to be “out the window”!

Talked to one of my middle aged children in Silicon V. last night who works in commercial construction. Lives in SV all his life. Was mortgage broker for many years until the ’08 crash and changed careers. He has no clue where this economy is going. No clue whatsoever but does agree that we are heading for some kind of “greater adjustment” in our economic lives.

The FED has painted itself into a corner. Even a fraction of a percentage of interest rate rise has indicated that this economy will not tolerate.

Our economic “tree” is overgrown and needs severe pruning. Otherwise it will become weak-rooted and topple.

This is not “capitalism”; this is economic robbery of the Commons by the “false capitalists”!

Consumers using big low interest loans to pay down small high interest loans. This is the Great Depression, with money. Remember my mother telling the story about finding a penny and giving it to her mother. Got a mailer from my CU for Jumbo Mortgage REFIs, picture of a minority couple frolicking in the pool. I think Wall St loves it, this is a consumer class buried in penury. Now you too can get the same interest rates that the big banks use to make their clients rich, borrow money and buy stocks. I think borrow money and buy gold might be the trick this time around. Hide the gold in the bottom of the pool.

I fully expect the credit card companies to refuse payment as per credit card agreement in the next year or two.

Mr. Richter,

I would be interested in your opinion on how this may or may not affect inflation?

If the money is being soaked up in paying off debt, it would seem to perhaps dampen some of the impending inflation. But it also frees up credit later on to purchase more stuff and stimulate inflation later.

What do you think?

Yes, some of the stimulus money has been used to pay down CC debt. But some of it (a big part) has been used to buy goods with it, including as down-payment for loans to buy vehicles.