How can a SoftBank-backed real-estate broker in a red-hot housing market lose $212 million in Q1? Compass Shows how.

By Wolf Richter for WOLF STREET.

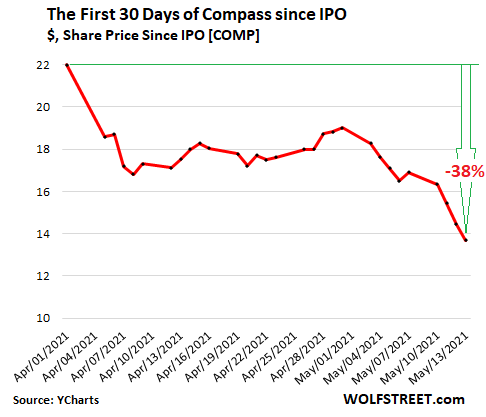

Shares of SoftBank-backed Compass, a real estate broker that calls itself “a tech company reinventing the space,” meaning the real estate broker space, dropped 5.5% today and closed at $13.66, having fallen 38% in 30 trading days from its intraday high on April 1, the day it started trading. It has now dropped 24% below its IPO price of $18. Despite the drop, its market cap is still $5.3 billion (data via YCharts):

Compass spent the past few years going around the US, buying up real estate brokerages and hiring brokers away from other brokerages, with the oodles of money it had raised as unicorn in various rounds of funding, including from SoftBank – $1.5 billion in total.

But today’s stock move was a reaction to Compass’ first earnings report as a public company on Wednesday after hours. “Earnings report” is a misnomer because it reported a net loss of $212 million, on $1.1 billion in revenues. About 82% of its revenues are paid in commissions to its brokers. That was the case in 2020, and it was the case in Q1 this year.

How can a real estate broker in the reddest-hottest no-questions-asked housing market the US has seen in something like 14 years lose $212 million? But OK, it’s not a real estate broker. It’s “a tech company reinventing the space.” And SoftBank was backing it. And losing oodles of money was part of the plan.

The loss of $212 million in Q1 comes on top of a series of annual losses: $224 million in 2018, $388 million in 2019, and $270 million in 2020. Those three years plus Q1 generated a net loss of $1.09 billion. That’s a lot of money to blow through for a real estate brokerage in a hot housing market.

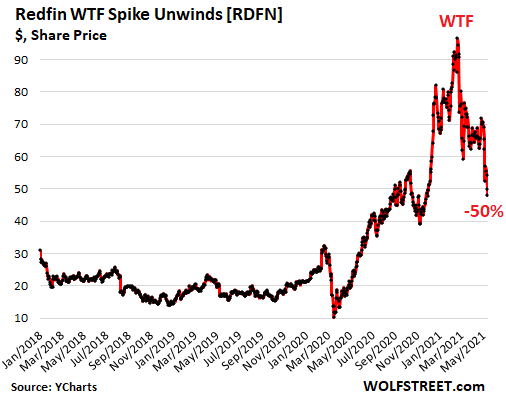

And the meme-stock chasers got a hold of Redfin, a real estate broker that has been around for years, had its IPO in 2017, and also tries to come off as a “tech” company. It lost money in every one of the past five years. What is it with these money-losing brokers with “tech” ambitions during hot housing markets?

For the first three years of being publicly traded, the shares hobbled along in the $15 to $30 range, and March last year hit a low of $10. But then, the meme-stock chasers homed in on it, and the shares exploded by a factor of 10, to $98 a share by mid-February, a true WTF moment, and then gave up their ghost and plunged by half, including 2.6% today during the rally, to $48.68 a share. It’s still valued at $5 billion, about 5.6 times its annual revenues (data via YCharts):

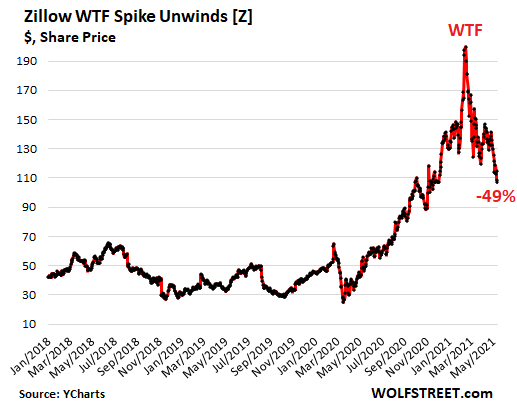

Zillow too has lost money every one of the past five years, despite the real estate boom. But it has gotten into house flipping. Its shares suddenly became miracle real estate meme in March last year and shot up from $28 to $200 in the same 11 months, in near lockstep with Redfin, and after that beautiful WTF moment, gave up their ghost.

The shares have now plunged by 49% from its raging-mania peak in February, including the 1.5% drop today during the rally. At $107.10 at the close today, the company still has an astonishing market capitalization of $27 billion, about 8 times revenues (data via YCharts):

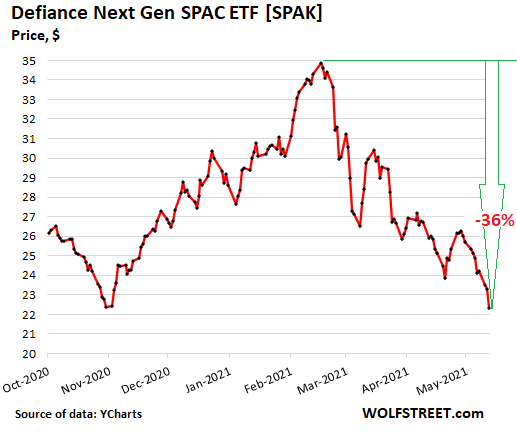

Another SoftBank-backed unicorn, mortgage lender Better – which calls itself “digital homeownership platform” – announced on May 10 it would go public via a merger with a SPAC, namely Aurora Acquisition Corp. [AURC], at an “implied” valuation of $7.7 billion.

That was a quick paper buck for SoftBank. Now it just needs to be able to unload its stake. And it makes you wonder: On April 9, SoftBank invested $500 million in Better at a valuation of $6 billion. In just five weeks, the already mega-massive valuation, negotiated behind closed doors, has jumped by another 28%.

But wait… that $6 billion valuation in April was up by 50% from the $4 billion valuation in November 2020, established during its Series D round of funding. In other words, in about six months, the valuation has nearly doubled.

And now the public is being asked to step up to the plate to support and keep going the wonders of the craziest WTF financial doings the world has ever seen – the “raging mania,” as Stanley Druckenmiller called it so aptly.

But SPACs have had a rough time in the stock market recently, and so good luck with this Better one. It’ll need it. The Defiance Next Gen SPAC ETF [SPAK], which was launched last October to track SPACs, sagged 1.9% today, despite the rally in the overall market, to $22.35, down 36% from its peak in mid-February, and now at its lowest close ever (data via YCharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Where does one sign up to get behind these closed doors?

There’s a house in Malibu I can’t live without.

1) Just pick a company, borrow stock from your broker saying you are going to short it but don’t, buy one share at 10 times the asking price to set a new price at the margin, wait for the new 10 times price and then sell your borrowed shares, wait for everyone to figure out what you did and dump the stock as fast as they can, rebuy the shares and pay back your broker.

2) Pay tax on obscene profits.

3) Buy house in Malibu next to the homeless tents.

ALRIGHT, WTF charts are back.

I was afraid you’ll start to taper back on those, and making them only a transitory feature.

Heh heh.

I’m very curious what happens if the market actually crashes ahead of time even before actual interest hikes start taking effect. The Feds are caught in one of the most ridiculous positions ever. Raise the rates, and drive the deficit out of control, let inflation run out of control, and destroy the economy.

One has to wonder how it ever got to this stage.

But getting back onto stocks, one has to wonder how many of these companies will survive the next decade as we go through some kind of a great unwinding. How much trillions in value do you think will get destroyed in this process?

Companies like Zillow shouldn’t even exist. They have been losing like $60,000 per house on their flips – IN GOOD TIMES. This company can’t make money if their life depended upon it, but their stock rocketed almost 10X? This is an embarrassment. The FED should be ashamed of themselves.

You mean like Al should’ve been ashamed of himself when he inflated the housing bubble.

The J team is saying hold my beer. And besides, as the old saying goes in sales, don’t worry, we’ll lose money on individual units, but we’ll make up for it in volume.

I never understood the Zillow model to be honest, they are essentially a big data service that keeps track of house and I suppose rental values. (the same goes for Redfin, etc) To survive, they went into the another line of work, and stop me if you’ve heard this, “using their technology to affect better outcomes.”

This is like a stripper buying five houses all on no income and sucking down ARMs, except the stripper is a nerd that probably got wedgies throughout college.

When there is an ocean of cheap money (thank you Fed), it’s easy for any hustler to borrow money.

So many ‘tech’ companies were founded, so many billions burnt. Did the humanity benefit? Has the quality of life improved due to these ‘tech’ companies? I highly doubt it.

The Fed has caused massive malinvestments and has set back human progress by at least a decade.

That’s reminiscent of the scene in the movie “The Big Short” where Steve Carell’s character goes to a strip club and talks to one of the strippers to find out how she was able to get a multi-hundred thousand dollar mortgage despite having not so steady income. She said she was given an adjustable rate mortgage on a NINJA loan that she could pay with her income. When he explains how the ARM could adjust ridiculously upward if and when interest rates go up, she sort of freaks out and reveals that she had five properties mortgaged out this way.

I agree, and I hope they go out of business, no offense to the employees.

Per Google:

2019 Q4

“Zillow sold 1,902 homes and purchased 1,787 homes, ending the quarter with 2,707 homes in inventory. The average sale price of those homes was $317,155. But between buying the home, fixing it up, the cost of holding onto it and selling costs, Zillow spent an average $318,667 on each transaction. Add in interest expenses, and Zillow posted an average loss of about $6,400 per home sold in the fourth quarter.”

2020 Q3

“Zillow bought 808 homes and sold 583 during the third quarter. It paid an average of $290,369 per home and sold each for an average $318,875, according to a shareholder letter. It lost an average of $2,868 per home.”

Zillow will make it up in volume!

It’s an old game. Capture market share of a product or service by bleeding your competition.

Burning cash to do this, is funded by the Fed, while the rest of the American economy is killed off.

I agree with Wolf’s general sentiment about the ridiculous valuations of these RE stocks. I think it was egged on by ARK investments.

But to be fair, Zillow is projected to earn $1.00/share this year and you can’t draw a lot of inferences from the low volume of homes they have sold thus far. What they’re betting on, and remains to be seen, is that it will become the norm to by and sell homes from Ibuyers.

I also think they don’t care so much about losing a little money on house sales as they are hoping to make money on mortgage originations, insurance, etc.

DepthCharge, I highly approve of Zillow losing $60K per flip.

It’s stupidity based wealth redistribution going in an unusual direction, think of it as an eddy in the insanity..

Wolf….you forgot EXPI. They have been adding realtors like crazy as it is a MLM kind of model. They might have the 2nd most agents now?

They more agents you hire underneath you the more you can earn. Part of your compensation is also stock.

They called themselves a virtual real estate company because they were creating a second life type of environment for agents to take training online.

Stock has gone from 90 to 23 in the past few months.

It might be a good company I did some calculations and it looked like they were paying out 92% of their revenue to agents. So after expense their profit margin was 1.7% and they had a PE of 400 or 500 at the peak.

To justify the stock price and a normal PE, they would have had to pretty much controlled 80% of all real estate transactions going forward.

The Great Bear Market of 2021 (May 9-May 13) will be over tomorrow.

Why are they so scared to let the markets correct? A crash at this point just seems so incredibly necessary.

Every stock in every sector is extremely overvalued, far more so than in the dot-com bubble.

They should have already let it happen back in March last year, but instead decided to blow air into the bubble. They’ve been blowing air in since then.

I’m just wondering why this crash is going to be such a Big F… Deal that they’re literally inflating the HELL out of the USD to avoid it?!

Why? Because the rich people who matter own most of the stocks, and that’s who the FED works for.

Ultra-rich are scarce,most stocks are owned by the retirement funds like CalPERS.

Old joke about the books-never-written comes to mind:

1.Italian War Heroes

2.Polish Who is Who

3.”The Mistakes I’ve Made” by Jerome Powell

Yeah but fronting these pension funds are companies like Vanguard and BlackRock. They have the ears of J Powell.

‘Ultra-rich are scarce,most stocks are owned by the retirement funds like CalPERS.”

This is simply FALSE. The wealthiest 10% own 85% of all stocks.

The retirement funds were never even supposed to own big percentage in stocks.

4. “My journey from arsonists to firefighter” by Dr.Ben Bernanke

The “Most Americans have exposure to stocks through pension plans and 401Ks” is just the lie that is used to justify blowing bubbles.

The fact is, most people have a very small 401K, if at all. So if you print $4 trillion to inflate assets, the puny $45,000 401K is now worth $66,000, while the richest who have $100 million portfolios now have $150 million.

The idea that the printed money is equitably distributed is a complete farce.

Trying to avoid Extreme Nationalism, Revolutions, and China taking over the former US sphere of influence.

What happens in US gets magnified all over the world. US in recession, the world is in recession.

In the end, like in 2008, somebody needs to get the blame. What happened, why did it happened, who to blame? in this case is kinda easy; Blame all on corona virus.

Dudu, if it weren’t such an outrageous idea, I’d think they CAUSED the virus just so they’d have something to blame the coming crash on other than THE FED, which deserves all the blame. It also deserves

to be abolished. Are we CRAZY for allowing a tiny group of cronies to control our economic destiny?

All this started AFTER I retired when it was too late to “jump back in the market on the bottom floor”. Am I the only one in this position?

No one is saying a word. I figure that’s because they’ve got only debt and no money so what difference does it make, as a politician famously said.

You’re right, last two days already made up quite a bit of the drop…remember the gospel is buy the dips…gravity for the market is so 1920s…

That’s how it’s been the past year. Every drop has led to a swarm of “buy the dippers.” It’ll take a prolonged drop to flush them out.

Because in their minds we can not withstand a severe recession. They created the monster by pumping up asset values with ZIRP. Now asset values dominate the economy. Stock market getting cut in half is going to feed on itself and spill over into the real economy.

By the way I took my 94 to mother to doctor in Greensboro, NC. Someone at nearly every intersection with cardboard sign asking for money. Must be profitable as it looked like they were competing for prime intersections. My parents grew up in great depression and begging is a no-no.

Sadly, I think it is pride and integrity that is now a no-no.

Smoke, meet mirror.

You know how I feel about this. I too was watching Compasa stock nose dive today.

Sent it to a friend who went to work there and he said “they will be buying your company stock next” which was a joke because my brokerage isn’t public.

But it IS owned by Berkshire Hathaway…

When and how does this real estate bubble end? It’s so far beyond rationality or viability that I am starting to believe that the laws of economics and nature simply no longer apply.

Do the rising Treasury yield set off a chain reaction that culminates in a big market selloff, producing even more liquidity and worsening inflation, leading to a rate hike that further tanks the equity markets and forces liquidation of other assets to cover margin calls?

It ends with inflation..

Housing prices wont really go down much (nominally), and stocks may fall a bit, while earnings will also “improve” (nominally) as inflation sets in.

This will allow CAPE ratios to fall back to something more sensible as inflation affected earnings catch up to currently bubbly stock prices.

Inflation will also reduce the size of the national debt (as a percentage of the economy which nominally gets bigger).

It’s all intentional and a beautiful scheme..wish I had thought of it myself. :-)

..but a hamburger will also cost $50 and gas will be $15 per gallon once this is all done..

And therefore by that reasoning Gold should be 10k minimum

How much should Bitcoin be?

Fed is going to fund the treasury forever if they have to. Ten year rates will not blow out more than 2.5% before Fed has to buy all if required to cap interest.

Just call it the Potemkin economy.

Sea,

But with the internet it becomes (much) harder to deceive the public about where the inflation comes from.

And if DC hates anything, it hates a crime that can’t be pinned on a patsy. That’s how elections get lost and phoney baloney DC jobs among the Eloi get lost.

Although…inflation does help with DC’s beloved 2 sided scam (heads we win, tails we win).

Soaring prices automatically hike taxes that don’t adjust for inflation and create bracket creep.

And, *if* DC can push through private patsies for inflation, they can vilify them (again) and *increase* tax rates on their inflation-fictional increased incomes.

If anybody ever wonders why people are hesitant to start new businesses in the US…see above.

You become both tax prey and tax collector for a rotted state.

“If anybody ever wonders why people are hesitant to start new businesses in the US…see above.”

My understanding is that new business creation has increased annually over the past decade including a spike in new businesses in 2020. It’ll be interesting to see how 2021 plays out based upon your points above.

I became self employed 8 years ago and it was one of the best gambles of my life that paid off. I choose my customers carefully…all decent people…and set my own schedule and my own rate.

No one can honestly answer this question. Housing “experts” thought that housing was going to hit bottom when the pandemic hit and the opposite happened. So, “predictions” on what might happen is as good as anyone else’s. Unless you’re a psychic with 100% accuracy then its just an opinion

I’m starting, after months of reading Wolf WTFing, to think the same as MM.

Too many people calling for a crash: when someone expects a lie you don’t don’t lie to them…

I’m thinking that all this money injection WILL have the intended effect.

To me it feels more like modern medicine: you can, using drugs, maintain someone alive beyond what they naturally be alive… What we have now for economy is still officially alive, but it’s starting to look a lot like some zombie or Frankenstein… Nothing graceful about it. But alive? Yes.

What the Fed sees its role to be is to maintain the creature alive whatever happens… Until it’s holding by threads

Government has really let us down by running the country on ponzi economics. It’s been building a long time. Who can make a rational long term decision when value is determined by a committee?

I look with much attention at the performance and evolution of the companies in the new age of uncertainty and fluctuation.

I suspect their top management designed the business models with little resilience under assumption of perfect stability of finance and economy.

Yes, and how computer algorithms can sort out issues like tradespeople juicing their costs. Computers are extremely inflexible devices and are easily fooled with a bit of social engineering. Do you remember the old blue boxes? They played DTMF tones through the telephone line which were commands for the whole telephone system. Free calls was just the start of it. Legend has it that they found the list of tones in the dumpsters behind the local exchange.

“One phreaker, who was an exception (to making poorly constructed blue boxes), was Steve Wozniak. He built robust blue boxes which Steve Jobs sold.”

Nah, we found the DTMF tones listed in a Bell Labs technical journal article in the public domain. The phone company has always thought that people are stupid.

A representative democracy can not discipline itself regarding money. That’s the Fed chairman’s role. J. Powell has 8 months left to go down in history as another enabler or as a Paul Volker tough guy. If you believe Druckenmiller it’s now or never.

1) The market might not crash. They poison the well for the next

president, a republican. That’s their block diagram.

2) They always do it. That’s their history.

3) Enjoy the ride as long as it last.

I’m old enough to remember when Joey B called J Pow an enemy of the American people last year to bully him into dropping rates to zero.

Or, in December 2018, when we had most tremendousest bigly economy that’s ever existed but Joey B called J Pow an enemy of the American people cuz he started to raise rates and the stonk market went down….

Democrat Joey B poisoning the well for Joey B. SAD!

Seconded. And Michael Engel is a crackpot with no credibility.

Oops sounds like a boy genius for Compass must have had a spreadsheet error in the projections used.

The DOW crashed because AAPL and Salesforce (CRM) crashed.

The Defiance Spac aptly named! HaHa! Good one! Yea I’m woke now

Wolf, you’re missing a bet on a bet on a bet! Package your precious WTF charts into NFTs, then set up an ETF based on the NFTs. You’d then be the proud owner of the WTF NFT ETF.

Your graphs have far more real value than other “works of art”, so the WTF NFT ETF would be somewhat more “real” than others of its ilk.

? Working on it ?

Lol! Wolf, I would absolutely buy a booklet of your amazing WTF charts for comedic relief/comedic perspective on the last several years.

For a cut of the sales, I would also joyfully edit/compile said comedic booklet for you :)

“WTF NFT ETF”

LOL.

As pointed out here in the comments some time ago: WTF = Wealth Transfer Fund

Surely it does!!

And STFU = Start Trying For Utility…

Really and truly folks,,, now ya got me doing similar to commenter on here ”spraying his coffee” due to the mirth!!

Except mine is my margarita, since it IS past noon local time, when all us old, frail, hardly able to move retired guys take the ”nooner” we all deserve SO much after years and years and years of ”service”…

Yo, Vintage! I have always taken the view that it is after 17:00 somewhere. Будем здоровы.

Brilliant.

Polista,

What’s a better hedge against inflation, WTF NFT ETF or wolfecoin?

I’m asking for a millenial friend with ample liquidity.

Don’t you think the Deep State or Fed is trying to get the public to sell their gold and silver and invest in stocks so they can then crash stocks and send gold and silver to the moon??

Cmoore, I say this with all sincerity. For your own financial well-being, try to stay out of the weeds of grand conspiracy theories. That will only cost you dearly in terms of opportunity cost. Be diversified because no one truly knows what is going to happen or when.

Thanks Tim

Just a thought I had as stocks continued their dizzing climb and PM seems range bound…

That’s exactly what’s happening. Fortunately, Q has announced, via a top secret drop, that there is a way for patriots to stop this catastrophe from happening: they must send all of their money to me for safekeeping.

Reply immediately if you want my Venmo.

Lord what a jumble. Raise the rates, lower the stocks. The uber wealthy do not care. They will always have the ability to pick up the marbles. Now do you understand why the top income tax rate was 90%? Probably not. Using debt, not dollars, is a form of masochism. Does it hurt enough now, honey?

The dual mandate is not voluntary.

When will the first citizen file suit against the federal reserve for violating their mandate. Inflation requires the fed to attack it….particularly when it is aware that the congress has injected huge fiscal stimulus with more coming.

Powell should be in jail.

People wanted Social Justice Warriorship to be part of Fed’s mandate and now it is. The idea that they can impact that with monetary policy is insulting to begin with. But that’s where we are at

“When will the first citizen file suit against the federal reserve for violating their mandate.”

I think citizens are usually better off looking to the Constitution rather than Statutes to protect themselves against the G (it is easier for Courts to intentionally misinterpret/misrepresent Statutes and it is easier to change Statutes).

That said, I don’t know how the Fed’s systemic dilution of private savings (on a rather huge scale) doesn’t violate the Takings Clause (there might be a case buried somewhere but I haven’t seen it).

The reality, though, is that most (not all) judges are wholly creatures of the State (see FISA farce) and those who don’t eagerly do the G’s bidding are often scared not to (they get calls from DC saying, “If we can’t print money freely, you will destroy the country within a week. Millions will die.”)

Cleveland Fed Chair Miser says “policy is in a good place, this is not the time to be adjusting anything, we should remain watchful.” So she will watch as wealth disparity crushes the middle and lower class into submission thanks to meddling know it all behavior by these Fed pseudo-scientists. An embarrassing new low for the supposed protectors of employment and price stability. Jpow talking about seeing homeless on his way to work makes him sad :(. It’s the taxpayer money to invest through the power invested in congress by the constitution to spend from the Treasury. Not any foolish bankers and Wall Street types fueling speculative hype trains that hardly create any jobs. The working man loses again.

Tinkering with American consumerism by pegging interest rates is where this really gets risky. Why would anyone ever pay interest again? People will learn to wait for the next crises to buy that new house or new car.

Realtor.com is owned by a publishing company not breaking even.

Florida property and casualty insurers have been doing double digit rate increases due to storm damage and excess litigation fees.

In 2020 U.S. property owners saw a 5.4% increase in property taxes.

Hoarding empty homes may be expensive.

Pre-pandemic, I thought people were trying to VRBO them, or AirBnB them?

@David Hall,

Excellent point to raise, David.

Here’s a downstream implication…

a) The commercial tax base of many cities & towns has been hit hard by the pandemic

b) This increases the reliance on residential property taxes

c) Valuation of residential real estate is soaring – which means taxes are, too.

How long will it be before we read headlines about homeowners taking out HELOCs just to pay their property taxes?

Not long, I expect.

Bit off topic, but very pertinent on many levels.

Very good 90 min interview with Michael Hudson over at Moderate Rebels regarding the early signs of an entirely new global financial system work-a-round to the USD.

Quick summary please.

Never mind…that web site is pretty far to the Left (or actual Russian collusionists – anti Ukraine, anti-Russian dissident).

More MMT garbage being promoted??

MMT is like saying that a credit card that’s not maxed out should be used until transactions get denied.

Everyone knows it’s a bad idea, but it sounds like fun to try.

We’re already seeing the devastating effects of MMT. The people who think it will work are mentally ill, or mentally handicapped – or both.

A friend of mine bought new a bathroom on his credit card. Then he moved to another country and forgot about it.

A couple of years later, a collection agency tracks him down and threatens him with bringing righteous fury and brimstone upon his head unless he pays the outstanding GBP 8000 right now.

He says they can get 1500 or they can go fuck themselves, They immediately say “Deal”!

Friends only regret is that he didn’t say 500!

The More Money Theory.

More Money for everyone!

@timbers,

This is based on the “De-dollarizing the American Empire” article that he published last summer, IIRC.

Seems plausible to me.

RealPolitik is a b*tch when one is on the wrong side of it. And it seems about to flip…

The Roman coins were used long after the empire collapsed because that’s what everybody had in their pocket, figuratively speaking.

In just word… hilarious!

I can’t wait until Pacaso try to go public by finding a way through SPAC. Talk about wrapping a time share turd in shiny fancy wrapping. Saw one of their commercial the other day, fancy ad, now you can also be 1/8 of a homeowner for seaside property, only for couple of hundred Ks…what a deal!

It appears there is a slow motion price deflation of the hyped-up stocks as people come to their senses, which implies maximum pain for retail investors who are buying all the way down.

A valuable lesson will be learned. When something drops 50%, it’s not necessarily a good time to buy. All momentum has been lost at that point. Lacking fundamentals, momentum is all that matters for these stocks.

No surprises here. These aren’t he only stocks overvalued, I’m certain more are to follow.

I walked through a well-to-do neighborhood earlier this week.

“Well-to-do” equates to an average house price of about ~$1.9 million per Zillow

Two houses up for sale – both for in excess of $2 million.

Both were “for-sale-by-owner”. That marked the *first time* I’d over observed a house for sale in that neighborhood without a realtor being attached.

So the lesson here is that the housing market has become *so hot*, in fact, that price discovery, realtors, etc are all being cast to the cub. Buy, baby, buy. None of this helps the Zillows/Compass’s of the world

Just a matter of time before “home inspections” go by the wayside, too. They aren’t needed unless you’re applying for a mortgage and it seems everybody is dealing in cash now.

Can confirm. Seeing lots of people waiving the home inspection. Not smart…

Geoff,

That would be true…

…but in the Boston-area most of the buying is being done by large institutions or the extremely-wealthy who are purchasing for “rent-to-own” purposes. Most of the concerns are out-of-state…and, therefore, rather difficult to litigate against if the future tenants complain.

Besides – at this point in time – good luck in getting any GC to inspect your property; they are all busy elsewhere by the look of things

I am very pleased to hear this news. They have taken my sarcastic advice from a couple of months ago. These actions mark peak stupid and now it is clear for all to see how much of a scam the housing bubble is. The Fed can’t deal with this. Only when people see for themselves the stupidity of an overblown housing market that can be easily manipulated with a sarcastic post to a blog will they come to their senses and stay out of the shitshow, thus deflating said bubble.

No point in holding ones breath for that. The UK has had a chousing bubble since the mid 1990’s. It is still going. Property defines the UK.

In Denmark, since the naughties, every time it looks like property is settling down to just tracking inflation, political measures will be taken to get “The Market” increasing in price again. 2008 did catch people off guard and made some impression, but this has all been buffed right out!

The lesson is that: Once something becomes a big enough part of the economy, it’s growth will be nurtured, supported and protected! There is no point in fretting about it, it is what it is.

There were internet grocery delivery companies in the 2000s, but they went away in the GFC. These businesses have their reason, whether or not they make money, or survive the next market crash. A mobile workforce, is now, or was then, the secret of success for the US economy. The problem with a Nomadland solution is the carbon footprint, fruitpickers in their jalopies. Nevermind the social fallout of wandering poor rootless parasites. It’s bad for the planet. So commoditize housing. All market trends are social trends. We love you Joh Biedun.

Softbank buy Bitcoin! For a good explanation see Dan Held you utube.

What does this even mean? What a joke.

Crash can’t some soon enough, working class people are going to be utterly slaughtered, I’m being hit hard now. Landlord says rent is jumping from 1200/month for a 1br1ba apartment to 1600 and now utilities have to be paid in addition to that price jump come July. No matter how far I look out from town, nothing is available. Everything is rented out and on a waiting list up to 18 months long. Housing simply doesn’t exit unless you have 400k+ in cash and can bid 10-20% over asking. Don’t even bother with trying to get a mortgage, you get laughed at for even asking.

I make 23 dollars an hour and I’m legitimately considering buying a camper and living out of it. Except for the fact that you can’t even buy a crappy 6*12 enclosed trailer for less than 8k locally. Let alone a real camper. I just downgraded from a Toyota Tacoma to a 1978 Chevrolet rust bucket pickup. Sold a Toyota Tacoma from 2005 with 230k on the odometer for 9500 dollars when I bought it 5 years ago for 4 grand.

Something’s gotta give, at least I hope. It’s pretty absurd that a full time working class guy in a skilled trade has to think about buying a truck canopy to live out of because housing has gone ballistic, apartments are all booked out for months and months and soak up 60-70% of your income at a minimum. Meanwhile everyone I see around me, even the same people at my job are somehow buying these houses, have new vehicles, toys, etc. I have no idea where all this free money is coming from but I want in on it. I’m getting bitter about the whole ordeal.

Check into limo bus type things. I see some parked near work. I can’t imagine there is much demand for them right now, and they seem like they could make a sweet camper conversion. Not sure what you call them, camper busses or party bus?

Also check Craigslist for rentals. It’s a pain due to spam but might find better deals through there versus institutional landlords.

Or maybe you can take the $1600 then immediately go into rent forbearance. Do research on that first.

Realistically they is the route I’m going to be forced to take. I’ll have to find some craigslist roommate deal and hope they don’t steal my belongings or kidnap me. God I don’t want to go back to living with a room mates again. Working nights and sleeping during the day is bad enough in an apartment. Came so close to being able to buy a house a couple years ago with a good down payment, somewhat reasonable prices, and near zero interest. Missed the bus and I’m still standing at the bus stop only with it now cold and raining and my wallet no longer to afford bus fair even if it came back for me. I’m hoping for a tornado at this point to blow the bus over and tear down the bus barn as well.

Even on craigslist folks are wanting 800+ a month without utilities for a single bedroom and shared bathroom.

I left home ownership and never looked back. Been very fortunate finding cheap places for a single guy. Sometimes people need cash and they have real estate that they need someone in.

My best deal was a small farm with three residences. Two were marginal, but both were acceptable after clean and paint. I have lived in all 3 at various times depending on what the property owner wants.

Another deal I got was house sitting for 6 months while someone was in rehab.

Don’t get discouraged. Keep asking around and try not to pay a market rate.

Mobile homes are much more liveable than campers although I had a friend that bought a nice older camper for $3000 that I believe I could have lived in. I see people living in campers on a permanent hookup, but it’s pretty rare where I am at.

What market are you in?

Hey, but that $3,200 per person SURE was worth it, right? The FED and politicians have destroyed the country, and you’re living it.

Covid year-end PR for a UK closed-end fund.

Sorry we had to part-sell out of Tesla because a 500% rise took us above our 20% single stock mandate.

Perhaps with hindsight we should have weighted more to the Chinese equivalent Nio which was up 1000% and is now a 6.8% position. Looking forward we see further prospects for these types of tech holdings.

So there you have it, get in now, everything is perfectly normal and we are all worrying for nothing.

This is nervous breakdown territory for me.

Pass the Scotch or something, I’m out of here!

It’s with noting that Jared Kushners family venture capital fund (Thrive Capital) was the lead investor in Compass for its seed round as well as its series A through D funding. Interestingly, the Saudi backed Softbank Vision Fund followed up with an enormous $400 Million funding round in 2017, and the Qatar Investment Authority led similar size funding rounds in 2018 and 2019. Pumping the valuation of Compass back then possibly had more to do with who owned it than what its prospects were.