But long-term Treasury yields have surged, to the great consternation of our Wall Street Crybabies.

By Wolf Richter for WOLF STREET.

The Fed has shut down or put on ice nearly the entire alphabet soup of bailout programs designed to prop up the markets during their tantrum a year ago, including the Special Purpose Vehicles (SPVs) that bought corporate bonds, corporate bond ETFs, commercial mortgage-backed securities, asset-backed securities, municipal bonds, etc. Its repos faded into nothing last summer. And foreign central bank dollar swaps have nearly zeroed out.

What the Fed is still buying are large amounts of Treasury securities and residential MBS, though no one can figure out why the Fed is still buying them, given the crazy Everything Mania in the markets.

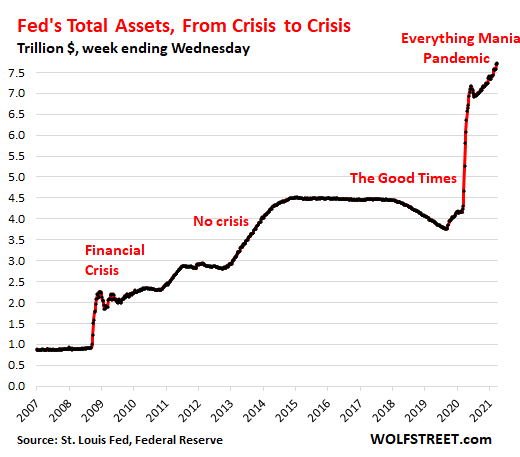

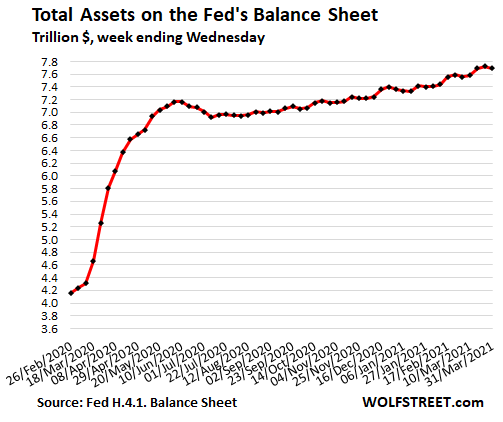

But for the week, total assets on the Fed’s weekly balance sheet through Wednesday, March 31, fell by $31 billion from the record level in the prior week, to $7.69 trillion. Over the past 13 months of this miracle money-printing show, the Fed has added $3.5 trillion in assets to its balance sheet:

One of the purposes of QE is to force down long-term interest rates and long-term mortgage rates. But long-term Treasury yields started rising last summer. The 10-year Treasury has more than tripled since then and closed today at 1.72%. Mortgage rates started rising in early January. Bond prices fall as yields rise, and the crybabies on Wall Street want the Fed to do something about those rising long-term yields and the bloodbath they have created in the prices of long-term Treasury securities and high-grade corporate bonds.

But instead, the Fed has said in monotonous uniformity that rising long-term yields despite $120 billion of QE a month are a welcome sign of rising inflation expectations and a growing economy:

To put that $30 billion dip this week into perspective, here is the detailed view of the Fed’s total assets since early 2020:

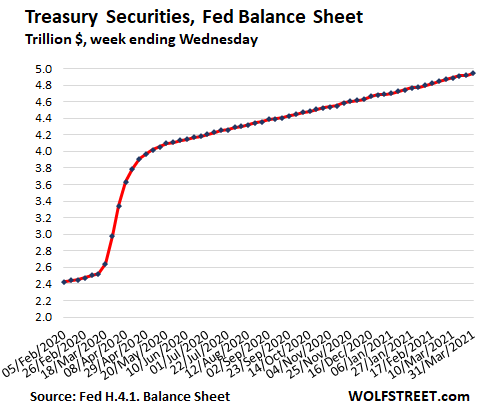

Purchases of Treasury securities purr along, $4.94 trillion.

After the initial blast a year ago, the Fed has continued to add around $80 billion a month in Treasury securities to its balance sheet, bringing the 13-month total addition to $2.47 trillion, which more than doubled its Treasury holdings over the period to $4.94 trillion:

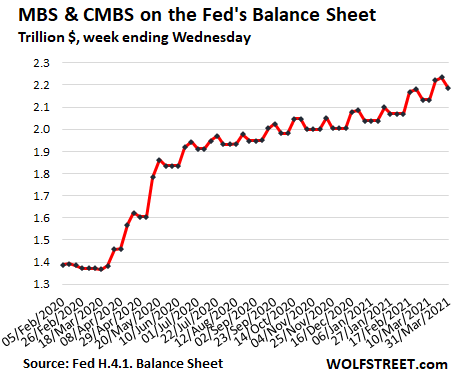

MBS zigzag higher, but for the week drop by $50 billion to $2.18 trillion.

Holders of mortgage-backed securities receive pass-through principal payments as the underlying mortgages are paid down or are paid off. The Fed buys MBS in the “To Be Announced” (TBA) market to replace the pass-through principal payments and to increase its balance. But trades in the TBA market take months to settle, and timing differences create the zig-zags.

The pace of the increase of the balance has steepened a little this year as pass-through principal payments slowed down due to the slowdown in mortgage refis caused by rising mortgage rates.

CMBS bailout program is shut down.

This $2.18 trillion of MBS include the Fed’s purchases of commercial mortgage-backed securities, a program it announced during the crisis. It was going to be a huge program, according to media hoopla. But in effect, it purchased only $10 billion of CMBS, mostly during April and May last year. This program is now shut down, and the Fed has ceased buying CMBS as of last week. Principal payments that the Fed receives will reduce the balance going forward.

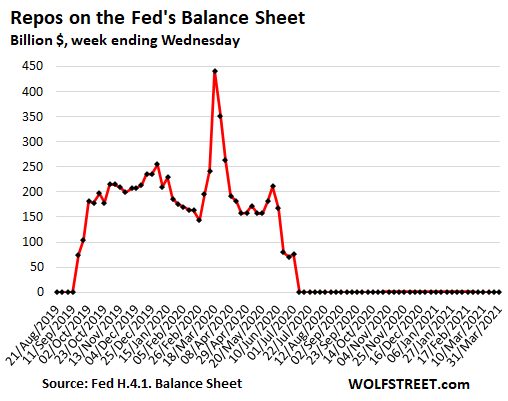

Repos (Repurchase Agreements) remain at zero:

The Fed continues to offer repos, but after it had raised the bid rate last June, making its repos unattractive, there have been no takers. The remaining repos matured and were unwound last summer:

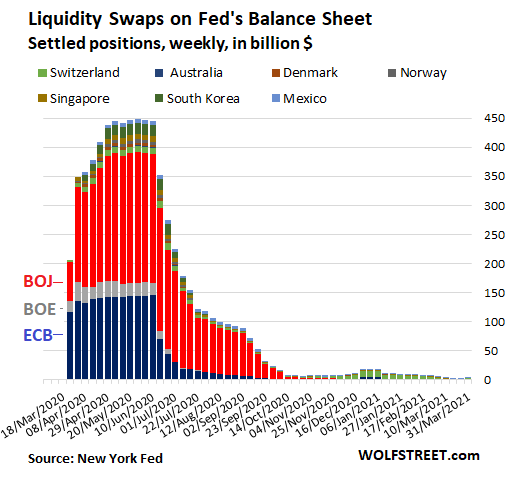

Central-bank liquidity-swaps are phased out.

The Fed offered dollars to 14 other central banks in exchange for their currency. Nearly all these “central bank liquidity swaps” matured and were unwound. Just $2.5 billion remain, split between the ECB, the Swiss National Bank, and the Bank of Mexico – down from $450 billion during the peak:

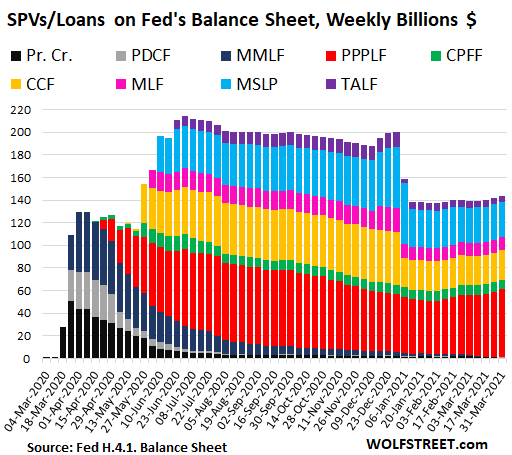

All SPVs except PPP facility on ice, at $144 billion

The Fed created these Special Purpose Vehicles (SPVs) as legal entities that can buy assets that the Fed is not allowed to buy otherwise, such as corporate bonds, junk bonds, bond ETFs including junk bond ETFs, auto-loan backed securities, municipal bonds, corporate paper, etc. The Fed lent to the SPVs, and the Treasury Department provided equity funding that would take the first loss.

These SPVs are now on ice and have expired with exception of the PPP liquidity facility (red), which the Fed extended for another three months through June. It buys PPP loans from banks and is the only SPV that is growing. All others are either frozen or declining:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

With a $1.9 trillion COVID package just passed by Congress last month… and a $3 trillion infrastructure package being pushed for later this year… it doesn’t look like it will be up to the FED to stimulate the economy any more.

So that means they can start Qualitative Tightening pretty soon. The last time they did it they shed 20% of their assets over the course of two years. So $1.5 trillion this time if they do the same.

It will be interesting to see what they choose to cut back on first. My guess is the MBS’s will go first… certainly the purchases. As Wolf said, it is hard to understand why they are buying them in the first place.

The FED is putting people out onto the streets, literally. The homelessness epidemic lies directly on their doorstep. Turning shelter into a speculative mania is despicable, and should be criminal.

When the fed purchases Treasurys, don’t they pay interest to themself?

Fluxite,

The US Treasury pays the interest to all holders of Treasury securities, including the Fed. The Fed then remits the largest portion of that interest back to the US Treasury. For 2020, it remitted $88 billion to the US Treasury (click on the image to enlarge):

Is that the ultimate negative interest rate? To not only borrow from yourself but to pay interest to yourself and end up with even more money in the end.

“The US Treasury pays the interest to all holders of Treasury securities”

The US Treasury or taxpayers?

Wolf,

A post dedicated to the Treasury-Fed-Treasury circularity would be very helpful I think.

The Fed-Treasury relationship is at the beating heart of Federal Debt monetarization but DC goes out of its way to obfuscate the issue.

By going step by step through the process,

1) Executive branch proposes/starts execution of large scale spending it lacks tax revenues to pay for…

2) Treasury issues debt to finance shortfall,

3) If domestic or international buyers of Treasury debt fail to show up or require “too high” interest on Treasury debt, the Fed steps into breach, buying enough of the Treasury debt to keep interest rates below target,

4) Since the Fed has no source of revenue, it prints unbacked money to make such purchases of Treasury debt…

5) And so forth explaining Fed giveback of Treasury paid interest, implications of system for private sector economy, etc.

The system is usually muddied through obscure lingo, opaque relationships, half true descriptions, ignored implications, etc.

I think a plain language post, laid out systematically, with some simple charts laying out the scale of the operation, would be well received.

“We’re all kinnesians now!”

The result ~ “We’re all millionaires now!”

There is nothing normal in in forcibly keeping interest rates at close to zero in order to run limitless money printing to finance limitless government deficits that will eventually destroy this country’s currency and very existence.

They could accomplish this by only buying treasuries though. The fact they are buying mbs and cmbs shows they are also out to keep the rich from losing anything. They don’t even need to keep interest rates at 0 to buy more treasuries and keep the govt from going bankrupt. Low interest rates are purely about trying to goose investment and disincentivize people from saving.

DC

Yes indeed.

Houses/flats should be only used as homes.

Well said!

The Fed tightening?

NOT in our lifetime.

+1. No chance of tightening at least in the foreseeable future.

One thing I don’t get is what gives when they keep increasing the balance sheet with magic money and then at some point simply decide to “write-off” the treasury debt? i.e. The treasury doesn’t need to pay the fed for those Treasury securities the fed is holding, and the fed will wipe out their magic money ledger entry (liability).

Because I don’t see the balance sheet normalizing for decades – so the logical conclusion may be a jubilee?

My guess is the Fed plans to print money and grow its balance indefinitely, which is necessary to avoid a collapse of the financial system. The balance sheet and its growth is now a permanent fixture, necessary to create inflation. Interest will continue to be paid by the Treasury, but this interest will be remitted back to Treasury (round-tripped) in order to maintain the illusion of fiscal prudence.

When the Treasury allocates newly printed money to people who are in debt, it IS a debt jubilee. There is no difference between forgiving debt and giving people free money to pay down debt.

People don’t seem to understand that the Fed has been doing helicopter drops for quite some time. So far, $7.5 T has been dropped indiscriminately, with most of it winding up in the pockets of speculators who have too much debt.

Bobber,

“People don’t seem to understand”

I think the fundamental problem is that the “DC way” of government finance has become (especially in the last 20 to 50 years) so inconceivably corrupt, that the general public has had a hard time…conceiving of it.

Most Americans have historically thought of DC as ultimately, fundamentally honest/benign and this messiah illusion has been extensively and carefully cultivated by DC.

This fatally mistaken impression has allowed a lot of terminally toxic practices to grow beneath its canopy.

…Fed doesn’t control the long end of the curve…10-yr and further out…

just FYI

Not willfully.

But the Fed is NOT BIGGER THAN THE MARKET.

The more they subsidize debt creation the more the amount of debt, then the more they have to purchase to keep rates below real levels, which begets more debt, round and round we go.

For all the governmental debt created, imagine the amount of off the books private debt created.

In the 70s, the Fed was forced to FOLLOW the market higher….and I think we are starting to see the Fed lose control and FIGHT the market.

I agree. The Fed will disappear before it tightens.

MonkeyBusiness,

That’s what they said last time before the Fed tightened. Then the Fed tightened, raising interest rates to 2.5% and trimming its balance sheet by about 20% until markets blew up again in 2018, followed by the repo market blowup in 2019. It’s funny how fast people forget. That was just a few of years ago.

“…it doesn’t look like it will be up to the FED to stimulate the economy any more.”

More?

Since when was the Fed about stimulating the economy?

By and large, that can only be done via vigorous government fiscal spending.

The Fed is only interested in increasing the value of the assets owned by Fed members and their friends.

the fed has often said monetary policy can only do so much and have been pushing for fiscal spending for years. here it comes. enjoy.

“By and large, that can only be done via vigorous government fiscal spending.”

But if that “vigorous government spending” habitually fails to grow the real economy (because it ultimately concerns itself more with political payoffs than objective accomplishments), then the Fed *must* intervene precisely because the “fiscal engine” habitually fails to grow tax revenue (because the real GDP hasn’t grown…because fiscal spending in practice is more about payoffs than accomplishments).

Fed monetary manipulation (money printing) does cause investment pricing derangements (by badly distorting the interest rates at the heart of discounted cash flow models) but that is the byproduct/accomplice, not the initiator, of the fundamental DC sickness.

Not sure who this “Fed” guy is (Fred?) but he is rich!

Pretty amazing when you compare it to the 2019 Federal Budget of $4.4 trllion.

Literally doubled government debt and spending…and most people didn’t even get a T shirt.

“Over the past 13 months of this miracle money-printing show, the Fed has added $3.5 trillion in assets to its balance sheet”

No.

You are confusing government deficits (see Team Red, previous King of Deficits – the previous Admin) to the Fed’s balance sheet. They are not the same.

Team Blue is the party of austerity and balanced budgets. That’s why they are pretending to support tax increases on the rich and gigantic corporations. Pretending because the propose it, only because they know it won’t pass.

Go Sounders!

What confusion?

2019 US budget was 4.4T.

Why not do a simple search before loudly advertising your ignorance to the world?

“Team Blue is the party of austerity and balanced budgets.” As much as Oregon is an island nation.

And the Federal spending makes up about a third of GDP….so as they borrow and spend, they will applaud themselves with the improved GDP numbers.

US GDP in 2020 = $21.5 trillion

US GDP in 2010 = $15.2 trillion

US GDP In 2000 = $10.4 trillion

St. Louis Fed, Gross Domestic Product Chart

Part of this GDP growth is real economic growth through increased productivity. The other part is inflation.

Ah but how much of each?

Answer that and you’ve cracked it!

Velocity of money

“V has declined from a high of about 2.2 in the 1990s to a bit below 1.5 before COVID-19, and to 1.1 during the pandemic. So why is V so low and why has it been declining since the 1980s?

One reason is that the Federal Reserve Bank (Fed) has been pumping money into the economy, but to little avail because money is not changing hands. Another is that a lot of the money is concentrated among the richest Americans who are not spending most of their wealth. Look at the difference between mean and median family net worth. The larger the difference implies greater wealth inequality, which you can see has been increasing since the 1990s.

A lot of the country’s wealth is increasingly concentrated in the hands of the rich and the super-rich who do not spend most of their money — its V being zero — because they already own all they want to own. The richest 10 percent own about 70 percent of the country’s wealth. This is why long-term inflation is expected to remain low. The economy is awash in cash, but most of it is concentrated in the hands of a few who will not spend it. In contrast lower-and-middle income workers spend most of the money that they earn.” Opinion

|

Guest Column

Murad Antia Tampa Bay Times

It’s almost as if the Fed’s monetary policy has failed.

But that’s inconceivable.

Implicit

Plausible theory which, if taken with demand going abroad through trade deficit, could contribute to understanding why no amount of money demand(stimulus) since 2008 has caused a, to be expected, massive general inflation.

Accelerating money velocity was put up by politicians as an excuse for accelerating inflation in the UK in the 1970’s

DH

So the MKT Cap to GDP ratio is almost 200% if not very close!

Mkt Cap – 42T+

GDP – – – 22 T

The missing 20T ? in the overvalued (+ buy-back shares) stock shares?

The GDP has to DOUBLE to catch up with current valuation of Mkts!

WOW!

By 2030 the real economy will have doubled. You won’t need stocks because we’ll all be rich and social security will pay you enough to live on. Everyone will also live in large affordable houses and drive Tesla model S’s. But, if you did buy stocks anyway, you’ll be a trillionaire, retire asap, and float away on a shimmering golden cloud.

Why didn’t qe 1-4 cause more inflation?

The current Fed Chairman is not qualified to do what he is doing by any stretch of the imagination. Yellen must know she is wrong. Her advisor was Tobin. I do not get it. I know, we are living in an alternative universe. That must be it. We have somehow failed to teach a least a couple of generations about economics. I think I will go hide under my bed again. That is the solution. Where are all of the grown ups? How can all of this be true. What happened to the Ivy league?

But, but but Powell worth maybe $55 million, a product of the Carlyle Group! How could he not know about money?

What happened to the Ivy league?

You mean like Krugman and Bernanke and Summers?

Where is the Paul Volker of this era?

“What happened to the Ivy league?” the well spring of what is wrong with this country?

This is certainly about economics, but there is something greater going on.

The violations of the Constitution (minting and taxing powers the Fed has assumed) and violations of the THREE mandates of the Fed (max employment, stable prices, moderate long term interest rates)….all these violations are ENJOYED by those who are allegedly supposed to be the guardians. Congress loves the free money…to wit, Trillions and Trillions in misnamed bills passed by Congress…(vote buying). Congress loves the Fed is off the rails. Wall St loves the Fed is off the rails.

Only a catastrophic inflation will create a People’s rebellion to shock the “guardians” into action.

What happened to the Ivy league?

They realized that they could sell out to Wall Street.

We have been sending our best and brightest to Wall Street for about two generations now – ever since the 1980s. All of that brainpower wasn’t designing better widgets or developing better manufacturing technology. It was redistributing existing wealth into a small number of pockets, rather than creating new wealth to be shared with everyone.

Now we need to beg Taiwan and South Korea to build semiconductor chip factories in Texas and Arizona because we no longer have the capability of manufacturing the latest and greatest technology. Intel practically invented the commercially viable semiconductor chip, now they are about two generations behind the Asian companies in actually building them. Our auto plants are shutting down because we don’t have enough chips to build cars.

Yet the stock market goes up and up and up, at the same time that the real economy is sputtering and blowing smoke and slowing down to a crawl. The smart kids all want to become hedge fund managers. Engineers are seen as the dumb grunts whom you fire and then outsource their work to Asia, right after you do a leveraged buyout of the company.

I have serious concerns about the chips that will be manufactured here in the future. Some of the big fabricators got out of the business because they were pushed out by big brother in DC. Apparently, the final chip design approval will come from the swamp. I hope the squad is up to it.

As someone who graduated from an Ivy League college, this is spot on. I had a lot of engineer friends in school. Only ONE is still working as an engineer. The others went to medical school, work on Wall Street, work for PE funds, work in management consulting, etc.

RnY

Russia and China are awash with top class engineers who love what they are doing making modern day equivalents of aka your dc-3 or Golden Gate bridge. How far down the pecking order are engineers now in your corporations? Boeing for example. The financial engineers are in charge and not us materials methods guys

“They realized that they could sell out to Wall Street.”

Indeed they did. But why study calculus and differential equations when money and fortunes can be created with the tap of a keystroke?

I graduated with an M.E. degree in 1973 and took all the calculus and Diff E courses (hard stuff) and worked as an engineer for decades. If I had to do the repeat today, I would get a degree in some easy liberal arts crap and then get a government job.

Story of my life. While, I did stick with engineering field, if could turn back the clock, I would “sell out to Wall Street” in a heartbeat…

Thank you for your analysis Wolf. I try to stay up with all your writing about the Fed. Congress has relied on the Fed far to long to bail them out with monetary policy when the hard decisions implementing progressive fiscal policy would be the appropriate medicine. Hopefully, fiscal policy be the driver of investments in our infrastructure, education, and healthcare to help our marketplace be more productive for this next economic cycle.

Yes…and tax the rich and the corps to pay for it. Productive investment for a change, and reverse some of this absurd wealth inequality caused by monetary stimulus. It’s so simple, and yet so frustratingly hard to do.

Was it Churchill who said the Americans always do the right thing, after they have tried everything else.

Exceptionalism is that US can print tonne of monies. If the sub-saharan nations can print unlimited $ like US, guess what? They also an “exceptional” continent. Print more $ when recession hit!

Growth without productivity is destined to failure.

Easy $ to speculate whatsoever assets classes, be it stock market, bond, crypto, SPAC, real estates and NFT are flourishing during “lockdown period”. Who want to work if $ is so easy to get? Import whatever we need because we have the $. At the end, who want these $ without any intrinsic value?

The the FED owns the majority of mortgages, are we now a communist country for housing?

Blackstone is/was managing some of their money with the stimulus I heard. If so, who do you think is going to buy them at a discount?

Another violation…

The Fed is coupled with a private entity….

no room for games there, huh?

No. Mortgage debt is 10 trillion the Fed has 2 Trillion.

I love the coincidences in all this.

Your 3t$ infrastructure package is to be funded by “future” corporation tax increases (rates quoted). Funnily enough a couple of weeks back our (UK) govt announced a major spending package to be funded by “future” corporation tax increases. Just making sure relocation doesn’t become an issue folks. Were all the usual suspects on the Zoom call I wonder?

On a spending point, it must be great being a US taxpayer. I read today on local news that MS won a 22b$ contract for 120 thousand augmented reality headsets for US army over 10yrs. I make that $183k per set. The Taliban will want these for resale on the games market.

Helps us foreigners understand how your trillions run up.

Somebody needs to drop a Daisy Cutter on the Davos crowd. The world would be better off.

When is the CRYPTO Davos get together, with all the double speak and sea food towers and private jets?

Not gonna happen. And that is why there are CRYPTOS.

People are sick and tired of the central banking gangster game.

So bad it has gotten, a new form of tender has been created…

Do Lagarde and Powell even recognize the rejection of their antics by the rest of the world? OR are they just in a “cocktail party” bubble with their friends.. “You’re doing great!” echo chamber

Cryptos aren’t any better. There’s a lot of money laundering and capital flight in those. Just as corrupt and possibly even less beneficial in the long run to average people. It’s just another angle.

These future corporate tax increases crack me up. They will be made up to the corps by increased subsidies and future stimulus. Paid for, of course, by generalized price inflation.

Be afraid, be very afraid. We went through 7 xboxes in 5 years. Check out the “ring of doom” in regard to MS quality.

Wow! Grandson has one and the last one worked well for a long time, but he wanted the new upgraded one this Xmas. His seem to last and work well.

Are you a “gamer”?

No I don’t play. My son played, but he got fed up with the hardware quality of MS and moved to other systems. It saved us a lot of money.

Built my first computer this year. Got one of the current best line of AMD processors. The software on it is cheating to go faster and had to be under volted to work right. Otherwise it probably wouldn’t last 5 years- would just burn itself out and IDK, maybe take the motherboard with it. The only hardware in the thing that is solid in it are the fans. Everything else had quality control issues. I lucked out- it works. I think it will last 12 years now.

You’re understanding ofhow the American Military Industrial complex works is incomplete.

In 3 years, those augmented reality headsets will be obsolete. That will require additional re-engineering the software and hardware to keep them compatible with new weapons systems. Much more money.

Don’t forget the administrative overhead on the industrial AND the military side of the equation. THAT alone will eat up at least 50% of the cost.

You can see that the actual cost of fully updated and current headsets MINUS the obsolete headsets already out there means that each headset that actually works in year 10 will be on the order of $10 million each.

Actually, the way the govt works is those headsets will be obsolete on delivery. It will take years before the first sets go out and users are trained to use them. Usually, the tech the govt buys is already obsolete by the time the contracts are awarded, because the selling cycle are long, and it takes years to get bids and make awards.

The worst part is years later when the contractor wants to sell them the better stuff, the govt won’t take it, because it’s too new and they can’t evaluate it anyway.

Wow… sounds like we’re in perfect shape to take on the Russkies and China’s combined might!!!

…I mean, what could go wrong.???

Wow… sounds like we’re in perfect shape to take on the Russkies and China’s combined might!!!

…I mean, what could go wrong.???

(lol)

I’m learning JW

We’ve got our own problems ie 2 aircraft carriers built to win an election in Brown’s constituency and now giving China & Russia the biggest laugh they’ve had in years.

These augmented reality gogs would be great for looking at US tech stock prices don’t you think?

Forgot to mention Microsoft was up 3% on the same day.

Scvmbag Bernanke said that QE would be temporary and that they would unwind in a year. We’re on like year 13 and they are doing it on steroids now. These creeps are as bad as the narcos south of the border.

Depth..

Indeed. I cut the article out of the WSJ, July of 2009. He laid out how the QE would roll off and all would be well when things returned to normal. Later he said it would all begin when unemployment dropped below 6.5%.

Well, as we know, it went to 3.5%. And the Dow went from 10K when the article was posted to three times that….

Being lied to just rubs me the wrong way. So is being stolen from …for those who promote inflation when they are directed by what authorizes them…their mandates…to guard prices and keep them stable.

To also promote moderate long term interest rates which prohibit the raping of future generations with current debt creation at immoderately LOW interest rates. Moderate long rates prevent this…and keep a fair balance between lenders and borrowers.

You’re beginning to see the equation. Our government is corrupt. We’re the hapless pawns.

Wonder how many houses daddy Jerome owns..maybe that’s why FED is still buying MBS…gotta keep that market as frothy as possible

That sort of thing really should be transparent.

Tesla just reported another strong quarter (for them)

S&P 500 at 5000 by year end?

“…,the Fed has said in monotonous uniformity that rising long-term yields despite $120 billion of QE a month are a welcome sign of rising inflation expectations and a growing economy”!!!

This statement from the FED is really troubling.

The pure deceptive conduct by a “structure created primarily to control inflation and promote Employment “!

This basic statement from the Fed can be answered thus;

Firstly, injecting copious amounts of liquidity into any economy ( creates and contribute to rising inflation). So , the inflation here is not a NATURAL FUNCTION of a growing economy but rather an artificial consequence of the policy of the EMU aka the FED.

Secondly, the Economy is NOT growing at all. The measures brought by various levels of governments in the outset of the crisis have rendered the Economies of the US, as well as the majority of world’s Economic powers stagnant.

The restart of the economic activity WILL TAKE a good 12-18 months to bring it to the semblance of what existed before the crisis this includes the RE establishment of the broken supply chains ( exacerbated by the quabble over trade war, Suez blunder, and the likelihood of huge backlash against CHINA’s new assertiveness in implementing its Nine Dash lines opaque policy)!

Accordingly, the arrival at the levels of March 2020, is Nothing to be celebrated ( if reached).

We are NOWHERE NEAR a growing economy at all. We’re merely going at a sluggish pace toward the levels of economic fluidity required to a FUNCTIONING GLOBAL ECONOMY.

I cannot begin to imagine how the reaction to the rising yields will pan out once we reach the 2.5% mark?!

The FED can talk its ASS off all it wants, but the market will have to contend with one reality, when the BOND MARKET COLLIDE WITH THE SHARE MARKET, the later tend to kind of ummm dive.

Thank you .

I don’t think the virus is bogus. I know it exists. What’s bogus is the way it’s been used as a tool for politicians to achieve goals which have nothing to do with the safety and welfare of the people or their best interests, instead serving the special interests and politicians themselves. Worse, scientists have proven to be paid liars on many fronts, leading to a loss of credibility.

the worst is the media though. they have an overwhelming bias and influence over society. they are clumsy with their brainwashing, but it’s still effective on a lot of the population. it’s really scary right now if you think cooties19 is an excuse for vaccine mandates and political power grabbing (which obviously it is). the witch hunt is about to heat up. throw in some hyperinflations, some welfare state, a little paranoid hypochondria in a country full of snitches and you’ve got yourself a dose of interesting times. (sorry, i spent today working in the tenderloin. pretty sure the apocalypse is upon us)

+1000 Depth Charge

Right you are Jack.

The upside down world…created by the Fed.

They want rates low, and want people to buy 5yrs at .5 and 10yrs at 1.65….but also push for an inflation rate of 2-2.5%. This doesnt make sense.

For the 20th Century and until 2009, Fed Funds were kept around inflation rates….equal to or in excess.

When the Dow made its all time high at the time, 14k in July of 2007, Fed Funds were 4%.

Now, a Fed Funds rate of 1% would tank the market.

2% in Dec of 2018 took 5K off the Dow pronto.

Now Fed Funds are .06. Last Month over Month CPI was up .4.

Month over Month CPI increase six times the Fed Funds rate!

This is theft…from holders of dollars to holders of equities and real estate (housing).

Remember when the Hedge Funds started buying residential properties?

Suddenly, the Fed started buy MBS. Remarkable timing.

Monkey……the S&P might be at 6000 by year end. If inflation starts to roll……nominal earnings will really shoot up the next few years and with high multiples due to the fiscal put provided by the drunken congress. Anything is possible. Those that refuse to play will be left hopelessly behind……..until the day a few central banks signal that the party will end. The politicians like the spoiled brats they are will complain and threaten but we will be faced by the entire world telling us we have pooped in the pool and nobody wants to play with us any longer. At that point the standard of living for most Americans will drop 10-20 percent overnight.

Good article as always. I run a trading forum on Discord and everyone in there loves your stuff. Thank you

“Everything mania”

It’s like a rich person’s financial orgy going on, with the poor picking up a few crumbs here and there.

Who picks up and eats crumbs at an orgy? Ew!

That which we do not wish we cannot perceive.

My guess would be Wolf is sitting mainly on a pile of cash.

It’s hard not to read in Wolfs commentary a desire for higher rates.

Wolf was calling for higher rates precovid too until Powell went berserk in 2018 when markets started to crack, then again with the repo disaster.

How can higher rates come about?

Fed already owns more than 20% of the residential market. What is to stop owning 100%?

Same with the treasury market, Fed can own it all and set the rates were they please. Look at Japan, there are days not a single government bond is traded.

It’s a terrible idea to keep currency when the issuer is a debtor.

Technically I don’t see how the market can win against the Fed, look at central banks of ex communist countries, the market was powerless . We are headed that way.

I see more trouble coming from social unrest.

Our society rests on trust and rule of law.

Those crisis are making it plain to average joe that the rich and connected aren’t allowed to fail and the rules aren’t the same for everyone.

There is one small step for the masses to jump to the conclusion that the rich didn’t get their wealth from ingenuity and hard work but Fed printing and government lobbying, and that will give to the poor the moral high ground to dispossess the wealthy through taxes or revolution, remains to be seen.

Everybody knows the system is rigged. The reason the FED is getting a pass is because most Americans are so stupid they don’t even know what the FED is. If you asked them, they’d just look at you slack-jawed. If the majority of Americans understood the FED and what they were doing, they’d probably be facing assassination attempts long ago.

Couldn’t agree with you more. American’s ignorance and willful blindness to things that truly matter is like a true gift for the elites. Combine that with their effectiveness in distracting the public to go after culture war craps instead of protest and fight back on things that truly matter, you have the absurdity that we see today and worse yet to come

I bet they have really good security..

Even moreso now. These people are scared. They know what they’ve done and continue to do. They’re looting the country.

“They’re looting the country.”

Depth Charge, you’re right on. A bunch of sociopaths who are rationalizing their actions, e.g. “hey, everybodies doing it…” sort of thing.

Gonna be hard to break their headlock.

DC, there actually HAVE been at least 2 protests outside of Fed offices. I was curious a while back and did a search. Only found 3 news articles which covered them. I imagine there is a real damper on any coverage and on on any protests.

One thing that is different this time is that the Fed has all the mortgages. When and if there are a ton of foreclosures, if they then sell those mortgages to Blackstone etc, then they’ll be more visible.

People do understand what the Fed is if it’s put in simple terms. “The Fed is the head of the banks, it’s the group of highest bankers, like a banker’s union” is easily understood.

.

I am puzzled by the bashing here of the Federal Reserve.

They are doing what is necessary to keep the economy from seizing up.

If they can monetize a trillion a year as they are currently doing, that means we have benefited from a trillion in fiscal stimulus that we do not have to pay for.

There are free lunches – especially in economics.

.

Avraam Jack Dectis,

there is a lot of fed bashing here as most of the commenters are american. i think the reason is that people believe the world is a place to be thankfully enjoyed rather than suffered. or at least that it should be. this is an error which leads them to blame, since money dominates many of our affairs, the federal reserve as the source of pain while simultaneously acknowledging its power to relieve suffering (if they would just raise rates! oh then we’d be free and happy! just like king volker once did). maybe they fear the poorhouse more than death. idk.

money is of course a deeply spiritual subject and the fed represents an unfathomable control mechanism that appears as some kind of dark injustice. an institution that can brew the magic substance but only gives it to their friends and not to us. talking down to us and mansplaining away all of our concerns. if only they would do what we say… give us a risk-free yield! puhleeeeeese…

but the suffering IS real. and the banks DO have lots of power. so it’s only natural. but the angry plebs don’t want to think about how difficult raising rates would truly be. look at the guy from turkey. he’s lucky to be alive (for now)

no one is asking for risk free yield, Fed has no business in keeping interest rates below inflation rates, Fed is operating outside their mandates.

i believe the excuse right now is that its, ‘symmetrical’

What the Fed has created is “Return Free Risk”, as we rocket towards an indeterminate “Peak Liquidity” euphoria. The Fed started with his own $50 million long only US index fund ETFs when he became Fed chair, and since much of that was in the small cap funds, it looks like he will have almost $80-$100 million to cash out when his chair postition expires. Conflict of interest, as what casino in Vegas would hire a pit boss who was allowed to bet while he managed the casino floor? Yet J-Pow can be $50 million LONG ONLY in US index ETFs…how is this not a massive MSM story and an epic conflict of interest???

The Fed also removed is the time value of money. Any number divided by infinity is ZERO. Printing near infinite amount of currency ends in ZERO…if time is allowed to proceed naturally. Extend, pretend, time inevitably wins the temporal war the Fed has foolishly waged against “Time”…

Perhaps “Time” wins in a week, a year, a century…TBD Yet the Minsky moment will finally happen given enough “Time”, as forcing stability breeds instability, so they are only making the situation more unstable when a mean reversion ulitmately occurs.

“All stable economies sow the seeds of their own destruction.” – Hyman Minsky, Professor of Economics, Washington University

Yet I suspect the Fed gets out before the markets crash “someday”…pure luck, of course…

Good comment, bungee.

I actually have cash waiting for better returns, but pleased enough to have what we do have, let alone the health and lifestyle our family is lucky enough to enjoy.

As I read today’s drum pounding all I could think about is comparing the lot of workers of even 100 years ago, let alone back 150 years. And yes, people may invest, have portfolios, and work in tech,….but that is just the definition of a worker in the tech economy. Same role, different collar.

I remember once being a Teamster. Our pilot cadre joined a Teamster construction local. Reasons aplenty. Oh, the outrage, the how could you, and do you know what this union is? My reply was the words of a Detroit truck driver at the time of Hoffa. “Yes to all that, but my wages are better, I have a health plan, and my Dad has a pension from the Teamsters. Before that, we had nothing. We are better off than before, pure and simple”.

Respect. Consideration. Decent pay for a good days work.

The US is already teetering on the edge of dysfunction as it slides ever further into decline. More labels and name calling, and an above commenter suggested dropping bombs on those he disagreed with. Meanwhile, things are still limping along without open warfare in the streets for the most part.

The people at the bottom are still quiet with having enough to eat and an ability to buy basic clothing. Or as my long deceased mom used to say when people railed about communism in the Reagan years, “These shouters just forget 100 years ago people were bought and sold with the land, what did they think would happen”? And Margaret Thatcher shut down the mines and declared war on the coal unions with the blessing of Ronald Reagan.

And now people on WS want to stop QE, Pandemic relief, and infrastucture investment. What do you think will happen? What do think will really happen beyond Red State talking points.? You know what else my well read mom used to say when people used to say there was no money for this and that. “Oh, if you believe that….there’s always money. There’s money for what other people want. There’s money for ships, planes and guns. War. There’s always money. They just don’t want you to have any of what they think is theirs”.

Henry Ford had a quote about that premise [Bankster focus] very early in the 20th century.

Henry’s antisemitic stance did not endear him to the money lenders.

“The US is already teetering on the edge of dysfunction as it slides ever further into decline. More labels and name calling,”

Teetering? It’s there. And this sort of thing could/might/will bring down the country. And with all due respect, Canada, et. al., are going to suffer collateral damage and might collapse as well.

It’s scary, but history is a tale of foolish people in power often doing very foolish things.

The problem with this is that humans are pack animals. When one gorilla hoards all the food, the other gorillas go insane with rage. Same thing here: low interest rates allow elites to use speculative leverage to simply take away things from working people — like affordable housing. See January 6 for an example of where the ends.

Krugman and crowd simply refuse to acknowledge that low interest rates have a downside (inequality) that can become dangerous.

They stormed the wrong building. It should have been the Eccles building.

Krugman etc are complicit in the scam. These are smart guys so they know exactly what they are doing.

The general public needs to be educated, because most people don’t understand how the scam exactly works, but do feel instinctively that they are being screwed. Wolf and some others are doing a great job at educating the public on this, but of course they will never be allowed widespread mass media exposure.

Avraam Jack Dectis,

Yes, there are lots of free lunches for the wealthy. Read this and make sure to study the charts, with data from the Federal Reserve:

https://wolfstreet.com/2021/03/19/i-truly-believe-that-we-the-rich-will-emerge-from-this-crisis-stronger-and-better-as-we-the-rich-have-done-so-often-before-jerome-powell-in-wsj-op-ed/

If you want to rip a country apart, keep going like this. You’re on the right track.

Well, to your point, our glorious leader is thinking about ways to forgive $50K of student debt. Isn’t it odd that those people who would be on the receiving end are likely the ones who don’t need it.

In the interim, Mayor Pete is thinking about a mileage tax. I wonder who will suffer more from that one, the guys who owns Teslas or the poor schmuck who makes monthly payments on his used car. Way to go, Mayor Pete, leverage that mighty brain of yours and change the world.

You know though, Wolf, your chart is perhaps a sign for you, after everything mania, there should be a period labeled “THE BEST OF TIMES” soon to be followed by the period “THE WORST OF TIMES.” It’s a sign for you to release your inner Dickens and come up a timeless tome, A Tale of Two Economies: the American Conundrum. Has a nice ring to it, right?

Forgiving Student debt is a terrible inequity.

What of all the people who…

decided not to go to college because the debt was too high

the families that did without to pay for college

the people who worked two jobs to pay for college

the people who actually paid off their debt

and…

those who could pay but don’t.

Who have parents with two homes, a boat, swanky vacations, etc….and choose to indebt their children with debt they hope will be forgiven some day…

Colleges with a certain size endowment must …..

cosign the student loan, or….

be lender themselves for the entire tuition or a lion’s share

and why not?

We have an arrangement now where the federal govt provides the credit for the purchase of a service from a “business”. (schools are big business, don’t kid yourself)

This in itself pushes tuition costs up.

If a person wants to buy a Ford, he deals with Ford credit. Not the federal car loan dept. What would the price of Fords be if federal credit was involved?

If you want to go ABC University, deal with ABC University Credit Dept.

If these steps, in some form, were implemented, two things would happen…

Tuition costs would cease their dramatic rise

Worthless degrees would disappear

Both, because the school would suddenly have an interest in repayment of loan.

True ♨️

Howdy Wolf!

If the instead Fed sat idly by while the country instead was smeared into a full blown depression, who would we be blaming?

The FED!

The FED just keeps the boat floating, their tools are very crude.

Imputing other motivations are just a way of revealing the innate psychology of the imputer.

The fine tools come from the fiscal folks. Bottom half not doing better? That is the fiscal failures.

The chart is a great success for half the population.

The fiscal folks need to work on the other half. It sounds like maybe they understand that now.

Cheers!

Avraam

Avraam Jack Dectis,

This depression story is a red herring put out there by the beneficiaries of the Fed’s bailouts (asset holders).

The government’s unemployment insurance and emergency loans kept the economy going.

The Fed just bailed out the asset holders — not the economy.

I’m working on this article now, and so I haven’t yet published the chart below and the data, which comes from the Federal Reserve itself.

At the end of Q4, the per-capita wealth (assets minus debts) of:

— the 1% = $11.7 million in wealth per person (green);

— the next 9% = $1.6 million in wealth per person (blue);

— the bottom 90% = $42,083 in wealth per person (red).

— the bottom 50% = $3,800 in wealth per person, most of it tied up in durable goods (cars, appliances, etc.).

The bottom 50% own essentially zero stocks. In other words, they have to spend every dime they make just to get by. They spent the government money. But they didn’t get the Fed’s money. The Fed’s money went to the rich.

Note that the line for the bottom 50% per capita doesn’t even show up on this scale of the wealth of the 1%.

And note whose wealth increased in 2020 — the people who already had enough money to spend money.

Wolf – I assume your wealth chart is average wealth, not median. Is there any way to break out the top 1%, as it will be skewed by billionaires if it is “average wealth”. Perhaps break top 1% into top 0.01%, top 0.1%, top 1%. Even with the top 90-99%, I’m betting if you broke out the top 5%, the top 90-95% “average” would be much, much lower.

I really think it is important for people to not believe that top 1% are all packing bank accounts holding $12 milllion. Top 1% by wealth,not income, the age is a huge factor as you need milllions less to be top 1% at age 30 vs age 60, etc. The definition of “Top 1%” matters also…

Median, average, age…all part of the equation of truth. It works out nicely for the top 0.10% to 0.01% if they can focus society anger at the top 10%, as the top 0.10% to 0.01% will always be able to evade taxes and re-distribution of wealth if they can blame those below them, which are much easier targets due to not having billions to throw at lobby and lawyer schemes. Think Waltons versus the guy who owns three Mcdonalds…$100billion vs $12million…you know which one society will punish first..

It really gets messy when the govt wants to punish those with wealth. Who gets hit first and worst, the person who won the billion dollar lotto, the person who bought bitcoin at $1, the person who spend 50 years, 70 hours per week starting a company from scratch which now employees 800 people? I think the charts can do some good, but they can do some massive damage too as most people make decisions on emotions and not logic, and thus thinking the top 10% are the “rich” via an chart is going to end in the top 0.01% having everything in the future, as most people do not even begin to comprehend the difference between median, mean, standard deviation, sample size, age variations, etc.

Personally, I think the school system is set up to make sure 90% are not able to figure out the mathematical truths of base reality. Ignorance is both complacent and bliss, until pushed too far…

Yort,

To clarify:

The 1% = 3.3 million people of all ages at the end of 2020. This is total wealth of the top 1% divided by 3.3 million people (in 2020). In prior years, the US population was of course smaller, and the number of 1%-ers was smaller too because it’s always 1% of that year’s population.

The per-capita numbers are: wealth in that year in that group divided by the number of people in that year in that group (% of total US population).

Yes, within each group, there are big differences. We always read the numbers of how the richest 25 billionaires or whatever are wealthier than the 95% or the 99% or whatever combined.

In the bottom 50%, there are also huge differences, ranging from the homeless, and the bottom 20% who likely have negative wealth, and cannot even afford to buy a decent used car, to the top of the bottom 50%, that may have a small-ish 401k and some equity in a house.

No one has to “punish” the wealthy. But the Fed has to stop inflating asset prices and bring interest rates above the rate of inflation, reduce its balance sheet, and let asset prices go where they may. The Fed’s measures are exclusively designed to make asset holders wealthier and rip off the bottom 50%. The Fed has a word for it: the “Wealth Effect.”

AJD, keep an eye on inflation and the U.S. Dollar. No such thing as a free lunch in economics, monetary policy, or fiscal policy. Monetizing Debt has a cost, and we peons are starting to see it as we pay the monthly bills. The Federal Reserve is a rogue government agency that has caused more pain and suffering to Americans than the seasonal flu. History will not be kind to these retired bankers and Wall Streeters.

“History will not be kind to these retired bankers and Wall Streeters.”

You can’t eat history! And it’s the ordinary folk who will suffer, not the retired louts! They’ve made their millions!!

Howdy David!

In a low inflation environment resistant to inflation, some monetization is free.

It requires capacity utilization rates to be below maximum, and that is another big argument.

But yes, there are free lunches.

.

Free lunch as in “Free Lunch Tomorrow!”

“History” is always written by the winners.

“There are free lunches – especially in economics.”

Patently and absurdly false. There is no free lunch. What may appear free for some comes at a heavy cost to others. Try to read a little bit around here to educate yourself before uttering such embarrassing falsehoods.

A J D

Fed thinks the equity mkts represents the real Economy, that’s knee jerk reaction to prop the mkts up, ever since ’09. Check the chart of S&P with various puming actions of Fed!

BOND mkt is the foundation upon which Equity Mkts is built. If the Bond Mkt revolts, What will Fed do? YCC or more QEs besides 120B/month!?

So enlightening to get down to just the facts.

So much for the “the whole world wants Dollars” myth.

In fact, seems nobody has any appetite for them any more other than the inmates in the U.S. asylum, probably to unwind their insane hedge fund bets gone wrong.

LOL. I actually knew Beckenbauer personally Gunter Netzer too…my father was a professional soccer coach for 45 years. Coached both of them at Real Madrid in the 1970’s.

I think where we are heading towards a full reserve system where the central banks simply print money and hand it over to the government to spend. Note that this is already being implemented by all major central banks in the form of Central Bank Digital Currencies, which unlike the current $ £ € etc do not require purchasing of Treasuries to create them. They are genuinely created out of thin air.

IF we allow 2% inflation and real economic growth is 2%, central banks can then on average print 4% of GDP annually and just hand this over to the government as spending money. As long as the government deficit is <4%, no money needs to be borrowed and inflation should still average 2%.

This can work, PROVIDED THAT you take away the power of commercial banks to create money. In other words, a full reserve system.

Central Bank Digital Currency would be interest free. If you need capital, you would have to issue bonds or borrow from a commercial bank. But this commercial bank has to actually attract savings (so needs to pay interest). These deposits won't be insured, so a savings account is more like buying bonds. But it also means there is no too big to fail anymore.

When the central bank wants to move to a full reserve system, it can simply convert all money on checking accounts into the new currency and cancel the same amount of government debt that it has on its balance sheet, reducing government debt. (if $1T in checking accounts, it eliminates $1T worth of Treasuries at the same time). This is probably most interesting in Europa, as there is more money in bank accounts there.

Another wildcard in some situations is revaluing gold. Assuming that the gold is actually there, the US gold supply is worth about $450 billion at current prices. But when confidence in the system erodes and it rises to, say, 10 times the price, suddenly half your M0 is then backed by gold.

For some countries this could become a life saver. Suppose Italy drops out of the euro and defaults on its debts. They actually have 2451 tonnes of gold, which at current prices is worth $157 billion. Suppose the gold price rises by a factor of 10, they will be golden (pun intended).

Right now, central banks probably don't want to see the price of gold rise. But when eventually the wheels come off, they have a massive horse in the gold game because they have such big holdings themselves. This is the reason why they are still holding on to the "barbarous relic". On the other hand, should BTC threaten to take over, that would never be allowed to happen as they have no horse in that game.

Central Bankers are the great enablers of “progressive” and “socialist” programs. Real interest rates and real costs of borrowing would not allow, through market disciplines, such reckless borrowing.

They are stealing from future generations, and Jerome Powell is driving the getaway car.

But now the Fed is fighting the market. And the massive debt, private and public is unbridled. So is the creation of more stock.

Deeper into the abyss they go….

YuShan, it is the comments from you and so many other long-timers on this board that make this the absolute best site on the internet. Thank you!

What you described could be the underbelly of what people will call the Great Reset. Most of the attention will of course be focused on the social uproar that will accompany such moves, but you stick to the practical machinery of money.

Strangest thing, but whenever I read your comments I find myself wanting to go search if Michael Pettis has posted anything new.

“I think where we are heading towards a full reserve system where the central banks simply print money and hand it over to the government to spend.”

In practical terms, we are already there. The Fed buys the debt but remits most of the interest payment back to the government (treasury). Yes, the debt is there but the government is not ultimately out for much of the interest-payment being made (on the portion of the debt being bought by the Fed).

Of course, this something-for-nothing scheme is what it always has been; a currency-depreciation game that is being used to inflate asset prices.

I can only guess that the Fed and govt are allowing private crypto to exist only to act like a giant monetary sponge to soak up some of the speculative liquidity from trillions recently printed. Crypto is a clear and present danger to fiat currency, CBDC (Central bank digital currency), full reserve system, etc. It can not be, and thus will not be allowed, yet they allow it for now for reasons I can only speculate. Perhaps better that a few trillion gets stuck in crypto versus those few trillion going into housing and the stock markets? The previous Treasury started to stomp on Cryptos, but someone paused that effort…and that pause is most likely purposeful and time delayed at best…

At some point, all the Treasury has to do is state “crypto is used mostly for illegal activity”, and “Crypto needs to be Fed regulated and approved”, just like the current wire transfer Fed regulated and approved system. Social security numbers required, access to the encrypted blockchain data for name, address, SS number verification…for buyer, seller, etc. Simple “flick of the executive pen” could make all crypto impossibly difficult to manage via new regulations, by forcing it through the current banking system cartel, with time and money consuming regulations the banks will fee crypto into oblivion. Plus we know crypto is a huge energy drain on the entire world via the necessary computations and the multi-trillion (G)reen (M)agic (M)oney (T)rain is gaining full speed.

Crypto will survive until the Fed, Treasury, and world CBs decide it needs to be replaced with CBDCs. And the new CBDC will allow the govt to place time stamps to force people to pay “full reserve” crypto at the time of their choosing, force either positive or negative interest rates depending on your “social score”, etc…know exactly what everyone purchases, from who they purchase, when it was purchased. Fed into a Watson God level A.I. algorithm (think WestWorld Season 3), people will be buying what they “think” they want or need, yet it will be what the A.I. tricks them into thinking they want or need…controlled by whoever is first to create the technology to control such a dystopia pinnacle existence. What shall we call such a beast….”Full Reserve Dystopia Matrix”???

Dystopia Definition – “societies in cataclysmic decline, with characters who battle environmental ruin, technological control, and government oppression.”

There are a few things being blatantly violated by the Federal Reserve.

1. Forcing long rates to historical record lows is in conflict with their third unmentioned (dual mandate game) “promote moderate long term rates”.

Moderate means “not extreme”, and near record lows are extreme by any metric.

2. Promoting inflation. Violation of stable prices mandate. 2-2.5% rips 22-28% off the dollar in ten years. Stable?

3. Digital Minting. Unilaterally raising M2 by 27% in under a year. The Constitution leaves the power to mint with Congress. The Fed is in place to provide “short term” liquidities.

4. Inflation is a tax. The Constitution leaves the power to tax with Congress, not an unelected body on which the People have no representation. Taxation without Representation….Ring a Bell?

That’s FOUR fundamental violations of the Constitution and/or the mandates under which the Fed is allegedly obligated to operate.

The Fed has gone ROGUE and Wall St and Congress cheer, for they are the great beneficiaries.

Who do we call?

FED Busters!

“Where life had no value, death, sometimes, had its price. That is why the bounty killers appeared.”

-Sergio

What we are living through is what happens is when a country has no real fiscal policy for decades, or should I say has a fiscal policy that is massively distorted towards the rich and corporations. Monetary and policy can only do so much and becomes what we are seeing now, BECAUSE there is no effective monetary policy coming from Congress. Taxes must go up big time for wealthy and corporations. We must temper inequality and at the same time the market lunacy. The FED is realistically pushing on a string. Without real monetary policy and tax increases, as mentioned, we are hurtling towards guillotines being rolled out…

Fed: we keep filling the pockets of billionaires with trillions of dollars. Why are the tent cities still growing?

I doubt that anyone living in a tent shows up on any GAO charts – having long lost their jobs and run dry of any unemployment benefits.

DHS & FEMA way ahead of this curve.

The revolution will not be allowed to (social media conduit) bloom as the leaders will ‘disappear’ [and replaced by well groomed gov’t insiders].

Occupy Wall St. leaders received that ‘message’

last go-around and have been quiet ever since.

The culling (algo driven) will be quiet, quick, and very effective.

Federal troops (no name tags green machines] implementation just a tell of what will unfold.

China’s response(s) to “problems” is the playbook.

“Freedom’s just another word for nothing left to lose”. (Janis sang it, guess who wrote it?)

@Sam, (Janis sang it, guess who wrote it?)

Kris Kristofferson…..

Mobs aren’t much safer, and definitely more random.

The US GDP between 1994 and 2020 increased by 13.5 Trillion dollars but its debt increased by 23.5 Trillion dollars! This is Insane!

And unsustainable.

I wonder what kind of losses our illustrious FED (up?) is sitting on with its illegal bond ETF holdings via backdoor SPV’s. Transparency does not exist in U.S. Government. They can hold MBS to maturity to avoid losses and certainly Treasuries as well, but do they ever have to Mark to Market like the bonus paying Banksters are forced to do in some fashion? Me thinks not.

I think Wolf has already reported on the softening in a Mars level housing market with rising mortgage rates, and just wait until the forbearance BS is ended as this ocean of non-performing loans puts a definite strain on the banking system. The Free Lunch has not been invented yet, Mr. Powell. Now if we could just earn 1% on our cash balances, even though that is still probably a negative 3% to 4% inflation adjusted return.

Am still amazed that anyone with any bond buying experience would buy any debt instrument yielding below 2% and expect to come out with their pants and shirt intact. No margin for error at such a microscopic yield. And with corporate debt at record levels, after stock buybacks out the whaazu and not reinvestment in productive capacity or R&D, the stinkers are going to start rising out of the swamp as the year progresses.

Will be interesting to see if Washington has much more Free Money Ammunition in the months and quarters ahead. I think even the Blue side of the aisles is getting nervous. Everyone should be very nervous in this Mars-style environment. Still haven’t found any consumer money trees in the gardening sections at Home Depot or Lowe’s?!

If college is free the government owes me 220 K pathetic of course all the cronies (rich) will be first to jump off a sinking ship like rats they are of course they have many bug out places need to realize they can run but not hide global economies will be the ending

My Long Term Care insurance premium just went up 134%. Take it or leave after paying in for 17 years. It was sold to me and the suggestion was the premium would never go up. In the 17 years the premium has gone up a total of 370%. All approved by state insurance regulators. Inability of insurance companies to get any interest on their safe investments cited as primary cause of rate increases. Screwing the middle class…

RM

This is truly shocking … but I fear not uncommon … (?)

One of the many elephants in the room still to be dealt with by society

I think at this point, unless you’re wealthy, the smartest move is to take all cash out of the bank, appear poor, and go on Medicaid.

DC, hard to do that and hide the cash if you want to keep it available. Medicaid wants to know where it went and there is a 5 year look back period. Now if you have only say $200K, you can buy yourself a car (Ferrari) and use that as your daily drive and then go on Medicaid.

We have two extended family members (not my favorites) who did similar and are “living the good life” with no bank assets or “real” jobs, but with a nice car, a place to live (with “friend”), and free medical for life. (dental too!)

Only in ‘merica can you do this!

Then there’s the gold/silver that was lost when the canoe overturned.

Smart? The dumbest move without question. Not only unethical but Medicaid is substandard health insurance. If you’re going to scam the health insurance support system find some other way to do it.

Your comment reminded me of something I read, “The Mandibles, A Family” it contains a fictional account of what happens to an older couple who planned well in a collapsing society. The short version is, it didn’t matter when the shtf.

RM

I never believed in buying insurance for long time care (assisted living+)

b/c, actuaries always under estimate the true cost and make premium ‘attractive’ at that moment. Many Insurance Cos (Equitable Life?) have gone under in spite their promises and gurantees by their agent.

I was aware of this ‘pitfall’ almost 35 yrs ago! So I decided to ear mark saving ( periodically add, when I could afford) for that purpose and invested in Vang Variable Annuity which has mkt risk but managed actively and ‘directly’ by me. It is nearly 300% of the original cost. Under a step -up basis at Vanguard, the cost basis even has gone up, favoring me. I told many at that time but got laughed at!

(been in the mkt since ’82)

Fed buys a bond with an IOU, the bond doesn’t exist, only the money that was applied to government spending, and the benefit of interest rate repression on economic growth. Cancel the IOU, you still have money, and the economic benefits. Rogoff at Guardian thinks China will float their exchange rate and the dollar will lose half it’s value. He maybe 180 off. The value of a currency depends on that nations economic policy, are they running huge deficits. But if the US Fed is ready to plug any global dollar gaps, why wouldn’t you print debt in dollars, like Turkey? Is Turkey going to switch their debt to Renimbi? Without a carry trade how is an aging, isolated, financialized economy like Japan going to get by? Taiwan is also an island, a small distance away from a bulging superpower. The Fed is making policy for the planet. So dollar index up, American prestige, love it or leave it. Fed will retire (some of) that debt early. Those dollars are going to good homes, part of a foreign policy tete'(-tete’). The expression of national power, symbolic or otherwise, makes people nervous. It makes Xi Jiping nervous.

A B

‘But if the US Fed is ready to plug any global dollar gaps, why wouldn’t you print debt in dollars, like Turkey?’

That’s why DOLLAR SWAPS exist for foreign Countries/Banks at Fed’s window. But it’s only for short time period but don’t forget US $ is part of US foreign policy tool!

The FED has increased its balance sheet 1/3 of a trillion since the current puppet was installed on January 20th. That’s still massive QE. That’s an annual rate of over 1.5 trillion.

D C

Of Course, but, is there a public out rage ( want more stimmy checka) or from the Congress ( who love deficit spending)?

NONE!

More printing and business as usual!

1) In 2008 when USD reached nadir, EUR/USD made dbl tops pattern

@1.60. WTI was @32.

2) In Dec 2016 EUR/USD completed dbl bottoms pattern @1.05.

3) If Europe entered recession, this low will be breached, perhaps

reach 0.85.

4) UK in troubles.

5) In Nov 2007 GBP/USD was 2.12. Today @1.3.

6) If UK enter recession GBP/USD will reach parity, or perhaps drop to 0.7.

7) If our unsinkable allies in Asia will be in troubles, because of China,

USD/JPY will rise.

8) JP will become the king and Janet will be a queen.

9) As long as USD is strong, US gov can print as much as they want.

Micheal Engel

I agree with you but you should add that the dollar is strong because it is the most requested reserve currency in the world due to its military strength based all over the world, the strength of a currency goes hand in hand with its strength. military. China appears to want to compete with its military strength to support its Reminbi but as long as China is run by a dictatorship I doubt that other countries will do it the courtesy of keeping reminbi as a reserve currency.

Only when the US no longer has the money for the continuous renewal to remain in command of its world armed force will the decline of the US come, for now and for the next 10/20 years its decline is not foreseeable.

Inflation is just the simplest way to make the population pay for the cost of a country’s waste of resources by incompetent or corrupt administrators, the only reason why you need to have 2 or 4% inflation.

As long as YUAN is pegged to US$, it is a paper tiger!

10) Us 10Y @1.69%. DET 10Y @ minus 0.32%.

11) US10Y minus the German 10Y = 2%.

12) If Germany entered recession, DET 10Y NR will sink further.

13) US Treasury build a wall against Europe NR, buy printing $.

14) Arsenal of printed $ to sell Germany.

There was 66.837% inflation between 1990 and 2010. Holding cash for twenty years created a 2/3 loss on investment.

If you hold bitcoin, it is not a currency. When you convert it to currency to buy something, that may create a taxable capital gain or a capital loss.

“Bitcoin”

LMFAO, How short memories are. This PONZI COIN was a little over $3,000 a year ago. It’s going to melt down in spectacular fashion.

David Hall,

Holding “cash” — meaning bank savings products or short-term Treasury securities or money market funds (corporate paper) — generated interest income during that time, to compensate you for inflation. The 1-year Treasury yield during that time was mostly between 2.5% and 6%. 5-year CDs could be gotten with over 5% a year.

You’re talking about cash under the mattress, which makes for a very lumpy mattress and is not recommended by sleep experts :-]

“You’re talking about cash under the mattress, which makes for a very lumpy mattress”

Silver coins are smooth and flat and not lumpy at all.

Holding Cash (to invest at the trough) was a winner when the mkts tanked almost 35% last March (’20).

i periodically prune my portfolio, to increase cah holdings. As per me Cash is NOT trash but saved ‘capitasl’ for the next mini dip. Also my cash levels meet my needs for livelihood for the next 3-5 or some times 5-7 yrs period, like now. Close to my ‘sleeping’ point.

Wolf, I think we will have some sort of Bank Holiday within the next 3 years as the financial system hits a giant air pocket and totally freezes up. It could be as simple as a Chinese system hack, they seem to have no problem getting past our computer security systems. But it will more likely be a systemic failure of interlocking counterparties to the sea of junk securities floating about the system. A daisy chain of defaults/failures of Biblical proportions.

Lumpy mattress, but pays me almost as much as any bank and I definitely don’t have to worry about getting to it. Have plenty of lead also. Semi-precious metal these days. Hidden in pvc in a national park with GPS location.

I pay a lot for insurance, after which, if I don’t use it, I have zilch. Some cash fills in the low spots in my mattress, afterwards I have exactly what I started with. I carefully distribute the cash so as to be un-lumpy. Such is the nature of insurance and cash.

Wolf, thanks for all your great posts.

I find it funny all of the comments on here coupling the fed printing with a political party affiliation.

Prior to the pandemic we had a different party in charge, putting massive amounts of pressure on the fed for more print/less unwinding, which they did, prior to covid.

I think that, we would be in a great depression if the fed hadn’t done what they have done.

I also think, that there are now permanent structural changes that have taken place because we have avoided a great depression.

Inflation debate is not the relevant one, but it is the fact that we are now a fully nationally managed economy, with much less foundation on any capitalistic principles.

We cannot unwind anything because everything is now so tightly bound.

There are multiple reasons for this, but it is a systematic change. This will need to be followed by political change.

Why? Because how can we as a nation defend not supporting individual citizens to the utmost when we have supported corporations to the utmost?

Has even a cruise line declared bankruptcy yet?

Give me a break.

We are supposed to fend for ourselves when our patrons take on zero risks and all the rewards.

I don’t think so. But, any unwinding will break whatever pile we have now.

The UNWIND begins ( along with regression to the mean) when the folly of NOT discounting the future cash flow. will surface slowly and at some point, irrespective of sea of liquidity provided by Fed/CBers.

The expected growth rate/future cash flow will be/has already determined by what you pay ( over or under) for that stock!

porque,

that’s always been bernanke’s stance, that this was the only way to stave off another GD. but the irony is that a hyperinflationary collapse looks very similar to the GD. only difference is there’s a bunch of paper money. but some of the problems are almost identical because the fundamental issue is the same; no one can afford to buy stuff.

as for us having to ‘fend for ourselves’ remember PPP, 600$ extra a week, stimmie checks, rent and loan payment deferrals, eviction bans…

another irony is that in socialism, there is no social mobility. it’s about keeping everybody right where they are. the feds attitude is ‘cruise ships gonna keep on cruisin and losers gonna keep on losin’

I don’t see any comments from anyone alleging that the Fed behaves differently depending on the political party in power. They are independent and unelected and do what they please. That’s the problem!

What’s a Stock bubble? Does providing more & more liquidity by CBers, change the ultimate outcome?

“What defines a bubble is that investors drive valuations higher without simultaneously adjusting expectations for returns lower. That is, investors extrapolate past returns based on price behavior, even though those expectations are inconsistent with the returns that would equate price with discounted cash flows. The defining feature of a bubble is inconsistency between expected returns based on price behavior and expected returns based on valuations

The defining feature of a bubble is inconsistency between expected returns based on price behavior and expected returns based on valuations. If investors pay $150 today for a security that will deliver a single $100 payment a decade from now, but they also fully understand that they’ll lose 4% annually on the deal, without extrapolating past gains into the future, then we might say the security is overvalued, and we might question why investors would accept that trade, but we can’t call it a bubble.

-John Hussman

So you are implying that the economy will generically have negative 4% growth going forward, already priced in, so we can stay inline with this definition of a bubble?

All, perhaps, due to the markets hyper, rationality features.

Or, maybe, our “markets” are just a distorted, unregulated, miss-informed, steaming pile of too big to fail.

Yes, either way, you are correct, it is the same God.

The bubble in asset prices is a result of added money in the system. Hussman names speculators as cause, however the money which comes under investment, has to be put to work, causing a fierce competition for available shares. Does it matter whether you own shares directly or on margin, or through leverage? When Archegos collapsed the investment banks holding the underlying made block trades with one another. They go around the market, in order to sell at the market price, and not lose money. There is usually a quid pro quo in block trades, in this case it was in the mutual interest of banks holding these hot potatoes to make a deal. They get on the phone, I have a bunch of X, you have a bunch of Y, let’s swap positions at the market price and nobody loses. Fed is the agent of institutional corruption, building stop gap measures to bridge the economy over these slow periods, recessions, ie the business cycle, which they have abolished through globalization, If there was never going to be another recession, why would you sell your stock, or worry about valuations? When Fed said they want to let inflation run hot they mean let the printing presses run hot. The laws of financial physics still apply, adding shares or dollars, dilutes their value.

All the future demand (growth/cash earnings stream) has been brought forward.

By NOT discounting flow, the premium paid to own that stock is NOT justfied. But in the current mania and momo trading, this falls on deaf ears!

I am still invested in specific div paying ETFs with large cash level on the side. This is the most surreal mkt, since I have been in the mkt since ’82! Higher they go, harder they fall. Reversion to the mean can be delayed, but cannot be banned!

Does LOW interest rate, justify HIGH valuation?