The Fed smiles upon rising long-term Treasury yields as sign of economic growth and rising inflation expectations.

By Wolf Richter for WOLF STREET.

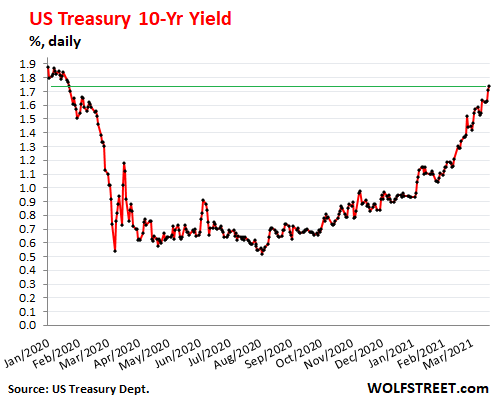

Long-term US Treasury yields have continued to march higher despite the Fed’s purchases of about $120 billion a month in Treasury securities and MBS, whose purpose it is to push down long-term rates. And the Fed governors continue to voice unanimous support for those higher yields as a sign of a growing economy and rising inflation expectations. Just about every day, they come out shrugging and expressing their support for those higher yields. On Friday, it was Richmond Fed President Thomas Barkin’s job to spread the gospel.

“There’s a lot of momentum in the economy right now,” he told CNBC. “I think we are going to have a very strong summer, a very strong fall, as pent-up demand comes back in the economy, as vaccines roll out, and I think the economy is going to be strong enough to take somewhat higher rates.”

This comes on top of Jerome Powell’s insistence earlier in the week that the Fed will consider the rise in inflation as temporary, and that the Fed won’t do anything about it, and that the resulting rise in long-term yields, as long as it doesn’t create “disorderly conditions” in markets, are a welcome sign of economic growth and rising inflation expectations. This Fed is looking forward to a surge in inflation, and is promoting it, and so on Friday, the 10-year yield closed at 1.74%, the highest since January 2020:

The 30-year yield closed at 2.45% on Friday, the highest since July 2019. When yields rise, bond prices fall. The price of the iShares 20 Plus Year Treasury Bond ETF [TLT], which tracks Treasury securities with maturities of 20 years or more, has dropped 21.5% since August 4.

Mortgage rates have belatedly started to follow, and with a vengeance, after hitting their low point late last year. On Friday, according to the Daily Rate Survey by Mortgage News Daily, the average 30-year fixed-rate mortgage rate reached 3.45%, up 70 basis points from the low at the end of December (2.75%).

Mortgage rates are moving so relentlessly that measures of weekly mortgage rates are woefully behind. On Wednesday, the Mortgage Bankers Association reported that its measure of the average weekly conforming 30-year mortgage rate had risen to 3.28%, up 43 basis points from the low at the end of December (2.85%). Freddie Mac said on Thursday that its measure of the average weekly mortgage had risen to 3.09%, up 44 basis points from the low at the beginning of January (2.65%).

These mortgage rates are still very low by historical standards, but they’re a lot higher than they were three months ago.

First signs that these higher mortgage rates impact the housing market.

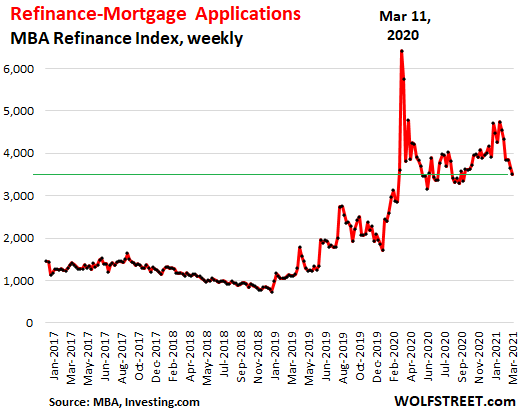

Mortgage refis have dropped since January, driven by a sharp drop in no-cash-out refis; cash-out refis have also dropped, but less so, for a reason we’ll get to in a moment. This chart shows the Mortgage Bankers Association’s mortgage refi index:

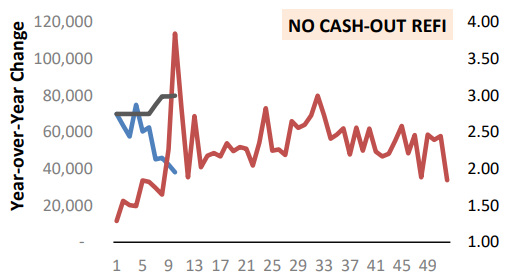

No-cash out refis “are already seeing large volume declines,” according to a report by the AEI Housing Center, which pointed out that due to the higher rates, fewer loans are “in the money.”

Cash-out refis are also down but only modestly, “as these borrowers are driven more by cash needs than rates,” the AEI report said.

The chart by the AEI Housing Center shows the weekly no-cash-out refis in 2021 (light-blue line, left scale) heading south, and in 2020 (brown line); it also shows the median mortgage rate in 2021 (dark blue line). The time line indicates the weeks of the year:

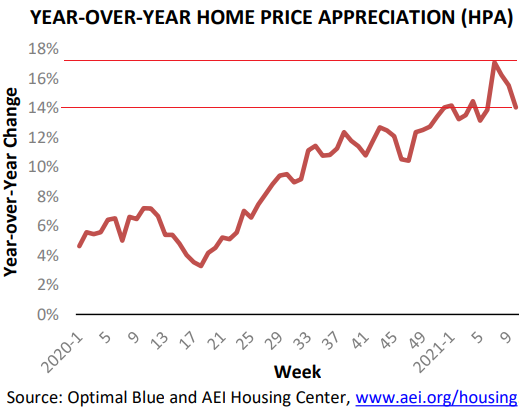

The AEI’s weekly Home Price Appreciation index, while still up a massive 14% year-over-year, has started to back off tad: at one point in early February, it was up over 17% year-over-year.

The “decreased buying power” due to the rising interest rates is “already having a limited effect in slowing HPA,” The AEI said. “The somewhat lower HPA in week 10 of 2021 looks to be the first sign of this trend.”

But the AEI added that “a loan rate of 4% might, due to severe supply constraints, still result in an unsustainable HPA rate of 8%-11%.”

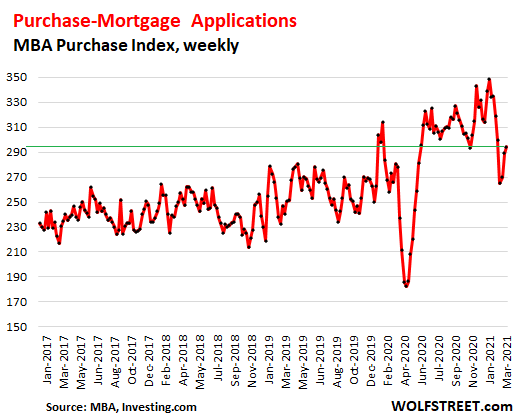

Mortgage applications for the purchase of a home have also declined from the peak in mid-January:

So it seems from this weekly data that the housing market remains red-hot, but the higher mortgage rates, which remain ultra-low by historical measures, have already started dialing down the heat.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The ad I am seeing viewing Wolfe Street says I need to take out a second mortgage! I guess I am just not pulling my weight in the economy these days!

My ad says, “buy an asus zen10 laptop”, so I might have less pulling weight than you got or I’m considered a better mug, as in fool, and not one of Wolf’s mugs which I can’t get sent to UK.

Wolf Street not Wolfe Street

There are many homes in traditionally nice blue collar neighborhoods that are going for over $1 million outside of Boston The math for getting this many million dollar mortgages applications doesn’t work even with low interest rates. Using the old 28/36 rule for the ability to qualify it’s not even close for 2 people making 75 grand /yr for 150grand.

,8 x1,000,000 = 280,000

.28 not 8

Most of them are in large neighborhoods without even a 1/2 acre

20 miles north of Boston here and been renting a smallish 1 bedroom condo (that could use a remodel and updated appliances) for the last 4 years. Even so, that’s $1500 a month (heat and Gas included). People tell me that’s a relative deal. In light of all the million dollar homes I pass on the way to work, I’d probably have to agree.

There’s a tremendous amount of renovation going on with GC’s buying up homes and flipping them. Some of the ones I’ve contacted to renovate our home are looking for $ 300,000 for the entire home and $ 100,000 and above to just remodel the kitchen. The neighborhood’s recent sales show a lot of work went into opening up the floor plan, adding support beams, and additions. Homes that don’t update or upgrade sell for about $150,000 less.

Are those Dyson or Hoover vacuums that are ‘sucking’ people into these cosmetic ‘renovations’ at such a ridiculously expensive point in time?

No working person or family or poor person or small business is though…

What kind of warped bubble does the Fed live in?

“This Fed is looking forward to a surge in inflation, and is promoting it…”

Historically, The Fed controlled inflation with higher interest rates… Could this be one of those times?

If the Fed was really looking for higher mortgage rates, it would stop buying mortgages and let the private mortgage buyers decide on what rates it could live with.

“What kind of warped bubble does the Fed live in?”

The obscene bubble of servicing your oligarchic vulture capitalist buddies, at the expense of everybody else ?

This is a repeat of an earlier post I made but it applies here.

I believe the 30 year bond interest rate is the key metric to watch. I don’t think the Fed has much control over those rates. The inflation premium on these bonds and supply & demand factors could spike these rates without warning. If these rates keep going up the Fed will likely not buy all of them, and will lose credibility (Not that they have much now anyway) if they purchase a large portion of the existing bonds or new issues coming on the market just to keep rates down. So 30 year bond rates could keep going up, with a spillover to the 15 year and 10 year bond rates as investors seek safety in shorter maturities. That will kill the Mortgage financing market and the real estate bubble in short order. Maybe it has started happening already as we are seeing a drop in mortgage originations and cash out refinances.

There are also a lot of variable rate equity loans/mortgages that use the 10 yr. The 10yr at 2.5% would result in the climb above 4% on the variable rate at many banks on equity lines.

Can guesstimate by adding a 1.5% to the 2.5%.

Trouble would be a’brewen in Gotham City. Probably before it even got that high.

I agree, 2.5% on the 10yr would cause a home price drop and similar starting conditions for a GFC event. The Fed would have to step in above 2% add the data would force him to. That would then leaf to a weaker dollar. It is possible to have inflation and low rates. It’s the currency that’s inflating relative to other currencies not itself.

Perhaps the Federal Reserve Bank isn’t wanting to buy the bonds but are doing so in part of their two card switch a roo swindle?

Could it be hard assets like other central bank holdings, real properties, world supply chains, big stuff that these crime families are after?

Me thinks it’s getting very apparent.

30 year bond. Thirty years ago I bought my first computer, a 486….look where we are now. Anything could happen, and change could entail every possibility as far as economic conditions and opportunity goes.

I realise that isn’t how the purchasing works, but still…..

My mindset is no debt, have some cash, real assets, and make a plan. My plan includes the possibility of rampant inflation. It does not factor in 0 interest rates for much longer, or these debt levels climbing forever. I’ve lived through 18% mortgage rates and it was a very hard time. I lost my job in the slowdown and worked away from home to pay the bills. There were no bailouts. If you bounced a cheque your NSF cheque and name went up on the wall behind the till; the wall of shame. I never bounced a cheque in my life because of that stigma, let alone whine for forgiveness and forbearance. People paid their debts.

We’re in a fools paradise as far as spending and debt goes, imho.

What’s that old saying? Plan for the worst and hope for the best?

The best time to take new debt is the period immediately preceeding an inflationary cycle. If you anticipate rampant inflation in the near to mid term, the best thing you can do is lock in long term loans at low rates and use the funds to purchase cash flowing hard assets that will appreciate with the inflation. Your cost of money is fixed, but the value of the money you must repay decreases over time, and the asset into which you converted the cash is appreciated in nominal terms.

Borrow a dollar, repay $0.75 in real terms.

Inflation is a debtors best friend.

If the income they rely on does to pay that mortgage does not disappear, sure, they’re golden.

“Sounds great in theory, but good luck finding “cash flowing hard assets that will appreciate with the inflation.”

Rates go up, house prices go down. If you buy a house now, you’re paying peak pricing and locking in the principle. You can’t refi that like you can the rate. I’ll go ahead and watch housing get crucified as rates go up, then I’ll buy. I’d rather buy a cheaper house at a higher rate than an expensive house at a low rate. My down payment goes much further.

I choose to decline playing in either scenario….high inflation rates and huge debt. Neither has much appeal for me. Everything about the Fed Reserve is ridiculous. That’s exactly what they want you to do is accrue more debt.

@Paulo

I bought my first PC 30 years ago as well, also a 486… love your story cause I seem to be in almost exactly the same boat- paid off house, some land, a little gold, some cash- enough to put up a house on the 10ac parcel my wife and I just acquired from my parents who still farm in their 80’s. We will start construction in about 45 days if we can find the materials… (ICF on a slab, so minimal lumber required) That’s my plan- but it still feels like I’m not positioned just right. I have some short ETF’s I keep feeding in wait of a correction that never seems to arrive. I keep buying tools, new Ford Expedition, some guns, tangible stuff, and sure enough prices are going up. What’s left to plan? I still feel unprepared. This feels like the twilight zone.

Same here. Bought mine 30 years ago also, a 486 DX 33 MHz.

I know exactly what you mean about the unsettled feeling and this twilight zone.

As for unforeseen circumstances and events, one need look no further than Covid, a scant year old. Like many we had a tough year, but have nothing to complain about compared to others. As it nears the conclusion on Vancouver Island, low infection rate and my wife and I get vaccinated tomorrow, (due to our small and isolated community), we are going to use this experience to spring forward. We’ll never miss an opportunity to hug the kids. Never miss the monthly community potlucks at the ‘Hall’. We’ll dust off the hospitality skills and renew dinners and evening fire pits with a brew or glass of wine.

Preps and a plan is nice….but I think family and community is key for us. It will light the twilight. :-)

All the best to you folks.

Boy are people going to be surprised when they find out this “fools paradise” isn’t actually the “new normal”.

With many homeowners still in forebearance, it will not end well. FNMA and other government entities have extended their eviction moratoriums as well, so many properties that are already foreclosed on are just sitting because the former owner is still there.

Eviction moratoriums are pretty much over in most places except the bluest areas. The renters have zero hope of ever catching up, the landlord has zero hope of ever recovering the back rent.

And moratoriums can just be instituted again, and the cycle continues until private property is a thing of the past.

Who would want to own rental properties when you have no idea if you’ll ever be able to consistently collect rent or get non-paying tenants out?

Rising mortgage rates are only the tip of the iceberg.

In the past they called this extend, and pretend….

How about switching from Renting Out, to being an Air-BnB? If no payment from occupier, then out you go!

Oh wait! I forgot, the government is making all the distressed landlords whole!

Housing inflation does not necessarily equate to over all inflation. It is an important component, but still a component. So, why would the Fed necessarily pay attention to the 30 year mortgage rate? I would think other interest rates might be more important. For example borrowing for productive investment, not just some more rentier income which is what mortgage rates are–rentier income. Investment rates for utilities, for one example, may be more economically important than higher rentier rates on homes. From the Fed’s standpoint. Anyway, I’m in favor of higher mortgage rates, because they will deflate the inflated purchase prices. That’s just one part of the over all asset bubble, which needs deflating.

The 30yr rate is important because it represents the profit spread for mortgage lenders. But there are other reasons why the long term bonds are important as well.

Big players, like other CBs and large multinationals that transact in USDs, use long term bonds to guarantee they will always have access to USDs when they need them. Those players don’t care too much about the rate or spread, they rely on access to USD liquidity.

The 30yr is coin of the realm in reserve currency exchange. China is selling plenty of their own sovereign paper. Does the US need to keep rates competitive? Rising 30yr yields would lock the bid under not so transitory 10yr rates. I imagine a global competition to sell bonds, and attract investment.

The Fed clearly wanted to alleviate Socal Jim’s anxiety!!!

Given the old prevailing mortgage rates, he was probably churning through neighbors every 3 days or so!!! In the past, when you welcome a new neighbor, you can at least rely on the neighbor still living in the property when the treat you brought over goes bad. Nowadays?

In my neighborhood it’s not the mortgage rates that have for of the six families on our cul de sac planning on a move this summer; it’s the crazy appreciation in property values. the retiree’s have decided they can follow the grandkids to Texas when the son moves the family for work, the disabled vet figures with his steady check and what he’ll pull out of the house he can live in Arkansas and never have to worry about working, the guy with three kids is looking at the cost of raising them here vs. Ohio where they have family, and another couple have decided to retire early to Belize.

I’m going to miss them because they are good neighbors, we all watch out for each other and they put effort into keeping up their homes. I’m expecting either the places become rentals or a developer moving in and putting 2-3 houses on each of the lots (which are big enough).

The middle class is leaving the coast. They can’t justify staying.

That mythical developer better have cash buyers lined up because with all the forbearance, few will have the credit to qualify for the loan, or the job for that matter.

At this point, rising interest rates are the least significant thing in the housing market.

The cash buyers arranged their financing elsewhere. What do rising mortgage rates do to a HELOC or PLOC? A few years ago a CITI analyst predicted that investors would one day being borrowing money and putting the proceeds in a savings account. QE brought that about. Now the trade unwinds? Call it the inverse margin call. Fed could retire those bonds. Monetary base shrinks and money velocity rises. Just unwinding all the second homes would be a major shock to the RE market. I would sell out now, but not for paper assets. Problem with cash buyers, is who wants it?

Same story as 2006. All the newcomers overpay then lose the house to foreclosure once the worm turns. My mom watched all of her neighbors on the cul-de-sac sell into that vicious bubble, then one by one the houses went back to the bank as none of the new “owners” could afford the houses to begin with, and once prices went into reverse they hurried to try to sell but there were no buyers and they were underwater.

And there were the stories as it all played out…. “We got ripped off by that REALTOR.” “We decided we don’t like this town.” “We’re going to move back to be closer with our parents.” “The school system isn’t what we thought it was.” A lot of anger and blame. Then there were the ones who left under the cover of darkness and never said a word.

Nobody likes to admit they bought at or near the peak. I refinanced at the peak, same thing. I went down in flames in a perfect Financial Trifecta of debt. Foreclosure, bankruptcy, and divorce. This was almost 30 years ago. Nobody listens to me when I warn them now. The noise you hear in the background is me printing “I told you so” form letters.

Sadly 2006 might as well be 1806 for the majority of house humping lemmings out there, all happened in the distant past and will never happen again. If only I get a dollar for everytime now I hear from friends and family, why don’t you buy now or be priced out, real estate can only go up.

In fact, the way the market has acted since 2012 and especially last 6 months, make me starting to question my own sanity and perhaps these lemmings are right. So far they have only been proven right with their housing is a no risk sure bet, tough to sell my case when I am the one with eggs on my face. Furthur more, try explaining why FED’s action matter and how things can potentially unfold through data, most of the time, you will see most of my friends and family eyes starting to glaze over as if I am explaining quantum physics. Did I mention how much I hate this “New Normal?”

I dont even know what to do anymore. I moved to Idaho in 2016 for my job and looked at buying a house and thought they were overpriced for what you got back then. Well these same house are selling for 2X – 3X as much now. I dont understand it. There aren’t that many high paying jobs here. I make decent money but cant even afford a $350K starter home anymore. And rent just keeps going up. Might have to move back to the midwest if this doesnt turn around soon

Young Buck,

Complain to your Representative in Congress and to your Senators about it so that they crack down on the Fed.

Come on Wolf. You know it’s not going to work. This country needs a rework from top to bottom.

Remember when Obomba drank that bottle of water when he visited Flint? “Hei guys, I know you are drinking poison everyday, but I don’t give a crap, let me take a sip from this bottle of water that I brought over from Washington DC to prove that yes the water in Flint is safe to drink”

“Come on Wolf. You know it’s not going to work. This country needs a rework from top to bottom.”

I agree. Nothing is going to change until we have a complete collapse. The FED and the politicians have shown us they will, IN NO WAY, do the right thing. EVER. Every response lines the pockets of the wealthy more and more. EVERY SINGLE TIME.

Great article and graphics Wolf. These movement metrics are miniscule (nice alliteration – eh?).

Increasing interest rates will not likely put much more housing inventory into the market. Prices will stay high. If rates get above 5% we might see some minor price decreases, but housing moves slowly and inventory (lack of) remains the driver of the pricing, not interest rates.

I was in FL in 2008. You are mistaken that house prices move slowly all the time. I saw them crash in a couple of months in early 2008. It wasn’t the interest rates, it was employment and credit that dried up in a matter of a few weeks. You better rethink your premise.

The FED has completely back themselves into the corner with no way out. They can’t even start to talk about thinking about raising the interest rate. The second they do all hell will break out. While there is low inventory now, people are just speculating and not listing their homes to see prices go higher. We see this in 2006. The second prices drop it will be game over. That shortage can turn can turn into a glut real quick as we see in the office space. Right now, if I was a realtor, start saving those commission checks.

I see both sides to what you and Petunia are saying. I believe the reason housing moves slowly is when you look at it from the seller’s side. Buyers make the market and without them, there IS no housing market. Sellers are always the last to know when the market tanks. So yes, they take their sweet time to reduce their prices, but buyers get the memo quick and get out of dodge. I worked for a homebuilder during the last crash. Our phones just stopped ringing, like, in a day. And the harder we peddled to incentivize buyers, the faster they ran.

MT

I have great respect for Petunia. My opinion is based upon the fact that this covid-19 non-recession, which is simply an extension of years of QE reflects that the Fed and to some extent our congress control the market now.

In 2008, the market functioned and housing prices dropped quickly. Even if interest rates doubled quickly from where they are now, Sellers will intuitively continue to control the inventory and price drops will be minimal.

If you think debt bailouts and massive daily intervention are the basis of good fundementals and positive outlook for good future cashflows for RE… 13.9 bps spread between 10y UST and IG bonds after fee/tax and subtraction of rfr on a hedged basis EOD friday… if you think negative return on a risk adj basis (despite massive daily support) wont do anything for RE… id love to perpetually buy some long dated OTM puts on REIT’s from you for $0.01 a pop ;-)

“Even if interest rates doubled quickly from where they are now, Sellers will intuitively continue to control the inventory and price drops will be minimal.”

These are the words of a total real estate novice, or somebody blinded by greed – or both.

Sellers are going to control the inventory?

It only takes one desperate individual to start a cascade. They sell at a heavy discount to get out and save what equity they have (if any) and get out of dodge.

Buyers (if any) see the drop, compare properties, and hold out longer than the seller can.

Not long ago, we bought an over improved house in SFO East Bay. I couldn’t remodel the house for what we paid for the whole enchilada. The previous family sent jingle mail to the bank as dad lost his job and had to move where employment was.

Sometimes circumstances control the seller….

Michigan will be a good test of housing price resilience. Auto industry going into short term pullback due to supply chain shutdowns. Add to that the EV dream with all the auto component loss from ICE production no place in the USA will have a greater challenge in the near future.

The boom and bust in housing is a direct result of the Politburo (the Fed) killing free market interest rates.

Rather than building value in a home through enterprise, the entire housing market is some kind of speculation on what the Dictatorship at the Fed is going to do.

And this is Free Enterprise Capitalism? I think not.

Builders are the last to know. They are still pouring foundations when the whole world is talking about how badly the market has collapsed. My theory is that they have access to the best cocaine.

Haha, you’re not kidding! Builders and contractors are notorious for going belly up, with no cushion. When I was young and strong in my early 20s, running equipment for a contractor, he asked me if I would mind leaving the job for a few days and helping his old dad who was pouring a foundation for an addition on a house. Of course I said I’d do it.

When I got there I found an older, broken man who was working himself to the bone, and in above his head with the project. He just did not have the strength to wheelbarrow heavy wet concrete to the forms, and pour it. I suppose he didn’t want to pay a truck for such a small job.

I spent two days listening to him caution me about the pitfalls of contracting, and warning me to go into another field if at all possible. He had gone belly up twice, and that latest one ruined him for good. He had no money, no retirement, and was working odd jobs to make ends meet.

His youngest son, who I worked for, was helping him out financially as well. It was a sad tale of terrible money mismanagement and an inability to read the tea leaves. To listen to him would be to think that the economy fell off a cliff in an hour, with no warning, twice.

It takes me back, though, to 2007 when I was building houses with two other guys. I was cautioning them that things looked really ugly, but they didn’t take it seriously. We went from having work lined up for months to canceled projects and nothing. One of them ended up losing everything and got divorced, though they had three young boys. The small town I lived in at the time went into something I’d imagine people saw during the Great Depression. Small businesses were shuttered by the score. Kinda like now, when I think about it.

My experience is that housing prices can fall precipitously fast. It’s the recovery that takes time, because the leverage needs to be worked out.

In terms of supply… Wait till the people that bought new homes before selling their old homes put their old and now vacant homes on the market.

The reason why there is little inventory is because the shadow inventory remains in the shadows and is not being put on the market (low interest rates and price gains make this profitable). It isn’t because the number of households just increased by millions in a few months.

WOLF

I agree the “2nd home” factor may eventually bring some of that shadow inventory into the market. However, with rentability high enough to cover that shadow home’s mortgage plus tax benefits of rental home ownership, a good percentage of those homes will not make it into the market, thus continuing the upward housing price trend.

I don’t have a crystal ball by any means, but after surviving the Great Recession as a real estate investor, a huge number of homes are being bought for cash already in this escalating environment. This is not a developing credit crisis (for housing), just supply / demand IMHO.

Depth Charge

Neither novice nor greed actually. Owned rentals for 18 years but don’t own real estate anymore (not a novice). Live OTG and near poverty line by govt standards (not greedy).

As stated, no crystal ball, but with so much Fed / Govt intervention in plain sight, Sellers are more prepared this time around.

Accountant here. Your assessment is wrong.

Sounds like a good reason to increase property taxes to me. The point was originally to ensure that property was actually being used as opposed to held solely as an asset. I’d personally prefer to see these people flushed out of the market. The notorious renters who continually trash properties can go live in the slums and responsible middle class types can finally have their peace.

Wolf, what are your thoughts on forbearance holding down inventory? Those folks can’t sell… yet.

Yes, that is an issue. Still over 5% of all mortgages are in forbearance. If just half of them end up having to be sold to exit forbearance, that’s a lot of homes to come on the market.

Biden has already extended the program for people in the program an additional 90 days… Is there anything stopping them from perpetually doing that? At some point will Fannie & Freddie be ordered to forgive the missed payments? Like mortgage write downs were forgiven in the last housing bust. This could be the next great ‘cash for clunkers’ give away.

Right you are.

US housing units per capita are well within 0.5% of their all time highs.

Basically, there are as many housing units available per person as ever.

And household size hasn’t really been dropping significantly over the last 20 years.

There’s a lot of that crap going on here in Swampland. That explains the large number of empty homes that are being refinanced. Everyone now thinks they are some kind of big real estate investor. That is until the bottom falls out like it did in 2007. I don’t feel sorry for any of these people. If you want to gamble go to the racetrack or play the options trading market. A home should be a place to live and shelter.

You know what I see in the next couple years Wolf? When the single income family w young kids who recently bought a house at a way too high price, experiences a major economic downturn, job loss and a house worth $125k less than they bought it for. AI will take a lot f 6 figure jobs away and combined w severe recession…

Why higher interest rates? There’s no risk!?! You have to love how the real reason for gauging ‘interest rates’ has been lost in the wind!

This puts the production home builders in a bind. My son is looking at buying a new home in a Lennar subdivision. The lot costs, SDC’s, utilities are already baked in the cake. The type of house to be put on each available lot is already set with building officials. This is a a subdivision for modestly salaried tech workers and each level of home pushed up against affordability for each prospective buyer group. So with interest rates driving up payments and building materials still high, you can hear the stress at the sales office. People who were planning on a 4 bedroom model on being pushed down to a 3 and the top end models have hit a brick wall.

“People who were planning on a 4 bedroom model on being pushed down to a 3 and the top end models have hit a brick wall.”

It always works this way and whenever the market tops, the central planners intervene with lower interest rates or some gimmick to bring in buyers again.

“It always works this way and whenever the market tops, the central planners intervene with lower interest rates or some gimmick to bring in buyers again.”

Except when you’re already at zero and inflation is roaring and the 10 year treasury yield has caught fire and you realize you are completely out of options and it’s time to take your medicine. Kick the can just turned into kick the Abrams tank.

The Fed has lost control, sure I get it. Just view any historical stock market chart or housing chart and tell me they don’t have control. On the Internet, we all seem to know “it’s going to end badly”. Read it on zerohedge.

https://www.macrotrends.net/2324/sp-500-historical-chart-data

https://fred.stlouisfed.org/series/MSPUS

“Kick the can just turned into kick the Abrams tank.”

Well put.

The only problem is that the US has had pretty awful people (the corrupt and the incompetent) running things for a pretty long time (decades).

And pretty much every time the public has thought that DC could not be so destructively short sighted and insanely insular in their perspective as to undertake a particular action…they have always exceeded their prior awfulness.

(In the 90’s, who ever thought that ZIRP/money printing could become a thing…let alone a 20 yr, heroin drip necessity?)

Your point about reality ultimately being immovable is well taken.

But it is *already* pretty clear that DC is at least willing to risk/court things like race/civil war in order to hold on to its own “vision”/power.

At this late date, no one should assume DC is incapable of horrific, final steps in order to perpetuate its diseased grasp on power.

Reality will reintroduce itself to America, but DC is fully capable of getting many people killed denying it.

The pandemic was (perhaps) just an unintentional foretaste of this fact.

There’s a new 15 house development near us. They put up the standard sign, “Homes from the low 700’s” about six months ago. There were some permit delays and so far only two houses have been built. A few weeks ago the sign changed to “Homes from the low 800’s”. Prices are climbing before they can even finish building them!

Come on Wolf, you should know better, If the Fed was really concerned about housing prices overheating they will stop buying 40billion of MBS every month. I dont think Fed will tolerate higher interest rates, this should be obvious by now.

JAYPOW’s leitmotif on this officially is “slowly” — he said this many times. They’re going to tighten very slowly. The Fed has already stopped a lot of marginal parts of QE. I will include the marginal things the Fed has stopped doing in my next Fed balance sheet article. There is a growing list. Treasuries and MBS will be last.

Is that “slowly” as in heating that poor frog’s bath?

Redfin says my house value went up 7.7% last year (just got the email). That means it’s worth $265,000. That’s about $134.00 sq.ft. since it’s 1,974 sq feet in size. Not bad for a very desirable brick ranch about 20 years old in The Woodlands, Texas, a great place to live. No mortgage on it.

I just pulled up my old house in Thousand Oaks, Ca that we left years ago. Redfin says it’s worth $1.25 million and it’s about 2,200 sq, ft. in size. Guess I should have stayed as my original 10% mortgage would have been refinanced by now.

If Zillow or Redfin showed up at my door at 2 a.m. to buy my house at 80% of what they say it’s worth I’d leave in my underwear and bare feet, that’s how much I think they’ve overshot.

Zillow is flipping houses and losing big on every one. They are financially incentivized to lie as big as possible about house values. Maybe they can lose less than $40,000 per flip, or whatever it was. They should cease to exist as a company. They’re the epitome of a useless endeavor built entirely upon a housing bubble.

I think Zillow was great in terms of putting downward pressure on the Realtor monopoly (I always thought the 6% fee was too high for the value the agents added to the transaction), so if Zillow was purely a system of paying a small amount to list a house with photos, avoiding MLS, I’d like it. The business lines they’ve tried to get into in later years are useless, as you put it.

I see zillow has stopped posting the sale price of properties on their website. I guess they are hiding the bad news, because high prices are good news, right?

GREAT analogy S1! LOL

But Zillow seems to be pretty accurate around our hood in the saintly part of the tpa bay area,,, and sometimes a bit low with their speculative evaluations. Same at friend’s home/hood in Tahoe area.

Old houses here going for approx. $150-175, with the ”tearer downer” on the low end, though might still be fairly livable.

New houses are usually sold before any work other than the demo of the old house commences, probably due to bottle neck in the permit process of one sort or another, etc. They going about $200-250/AC area.

Some houses sitting awhile, but I suspect they are over priced, overbuilt, over re-habbed, or any of the above done poorly.

$265K for just about anything in Woodland Hills was a good deal even five years ago. God bless Texas.

It’s the same for us per square foot in a ‘burb just outside one of the other major metros. Newer area, new schools within walking distance, lake 5 minutes away, Whole Foods (and all else) 12 minutes, downtown 18 minutes on a beautifully landscaped toll road. Sure, prices may have doubled from 10 years ago but they doubled from virtually nothing.

People hear about Austin or Frisco and think all of Texas has bubbled up irrationally. Nope, that’s only if you’re expecting something burdensomely large next to your newly relocated corporate headquarters. Green Lamborghinis are your clue.

I saw a development of homes in Austin, starting at $500K, that are really town homes with space between them, with outstretched arms you could touch them both. Some exotic cars, but Teslas all over the place.

That’s not going on in other desirable parts of Texas. Austin is where the wealthy Californians are settling and those people just love high prices!

Not many Tesla’s here, just BMW’s and MB’s.

500K in Texas means some serious property tax bills. I wonder how many people ever calculate the cost of property taxes over the course of their whole life….

Jdog, everyone jumps on TX property taxes. I pay 2% of assessed value and that’s high around here. Plus, our houses don’t cost as much as most of the nation’s similar areas.

But please remember, we have no state income tax. And sales tax is at 6.25% with a max of 8.25% when special district tax is added in, where appropriate.

I lived in Ca for 12 years and paid the 1.25 % and then they added bond repayments where another 1.25% was added to my tax bill (but not called a TAX) – BUT I STILL HAD TO PAY IT!

“everyone jumps on TX property taxes”

I know, the reality is that for those of us who left California for Texas, we don’t pay a penny more in property tax. Yes, the rate is multiple times higher but the house is multiple times less.

So, we pay roughly the same total amount for property tax, way less for the house and zero for income tax. I save thousands of dollars every month even though my property tax is “high”.

There’s a reason for every one Texan that moves to California, two Californians move into Texas. It really does cost a lot less for a comparable lifestyle (weather aside).

…. is the FED watching Turkey right now…?

May be they should (well, all ‘developed countries’ central banks really).

LoL, I guess you missed the last wilfully ignorant Dotard that was president who ignored the Fed & the executive; who was only interested in making himself richer, feeding his ego, and jerking off racists.

Amen for that comment!

“The Fed smiles upon rising long-term Treasury yields as sign of economic growth and rising inflation expectations.”

The Fed smile will turn up-side-down into a frown the moment Mr. Market throws a hissy fit.

How much more QE will the Fed deploy to make Mr. Market happy again with it’s new heroin fix?

That’s really the only question…having seen this movie before.

Not to be too catty, but the Fed should stay focused on short term, overnight interest rates and forget about manipulating longer term debt. Manipulating interest rates is a very blunt instrument, and when it is used the only winners are the already rich. Higher rates? Fine more interest income for me. Lower stock prices? Fine, I’ve got money to burn so I’ll buy the stuff up cheap. Win, Win baby. That’s what the Fed’s all about.

“Jerome Powell’s insistence…that the Fed won’t do anything…as long as it doesn’t create “disorderly conditions” in markets…”

Like GameStop?

Jerome did nothing when GameStop happened, so he told us by his actions that’s totally not disorderly market conditions.

So that means it’s totally OK for Mr. Market to go down 95% or 100%, because that’s just like GameStop which Jerome has told us – by his actions – is totally orderly.

Gamestop != Market

Gamestop != Market

I think you underestimate.

Granted GameStop had it’s 15 minutes of fame. But did you know or work with anyone involved with it’s stock at that time?

It wasn’t The Market it them: It was their ENTIRE LIFE.

Not to mention it did impact the rest of the market.

Gamestop is not important. It is the same as a penny stock pumped by a thousand boiler rooms of Jordan Belforts.

The fed crime family headed by Don Jay is failing to adhere to one of its primary duties…..monetary stability. In fact it is encouraging destabilizing policies.

The greatest issue which Don Jay is advancing is a total lack of credibility. Americans have no faith in the fed regarding the value of their dollar. If he would allow rates to climb the DC congressional crime family would be forced to tow the line regarding their fiscal drunken sailor policies. The cost of the debts would be forcing them to balance the budget.

Yes…..a severe recession would result…..better a recession than a collapse of the US dollar which may result in a depression or worse. See 1917 in Russia.

Where I live stuff that is below a million seems to move pretty quick. Townhouse near me sold for $625K (bought two years ago for $540?) basically before it went on market. For sale sign went up with a Sold on it. So many of my friends have bought recently, I don’t know who is left to rent? I would like to find something but I’m an oddball and not seeing much that checks the boxes I care about. I really want an unfinished basement and many of them are already finished. Also, the contract I support might be up at the end of the year and I don’t know what is next. Maybe with all the new cash floating around other tech jobs are offering a lot more money now.

I wish the market would weaken. But at this rate the forbearance will never end.

Wolf:

> the housing market remains red-hot

Seattle landlords -would- sell their homes, if they could.

I manage a 32 unit rooming house — 32 housemates.

I have to navigate an angry landlord & a mob of squatters/junkies.

Here, Seattle, “imminent danger” is the only excuse to evict someone.

Not even selling the house is reason enough to evict; judges ignore leases.

“Just Cause Eviction” is wrong for the same reason “no-fault divorce” is right.

As to stopping squatters from trashing the place willy-nilly…

Lectures don’t help. Making an example of someone doesn’t help because,

then, they’ll make an example of “me” ( the well-hated messenger ).

Higher bond yields aren’t a sign or a result of a healthy economy. Higher yields are a necessary CAUSE and INGREDIENT of a healthy economy. Now that the Fed is starting to encourage the regrowth of interest, money will start to migrate away from crazy frauds and infinite debt, and toward sane storage and real investment.

Higher bond yields are a sign of demand for money. Whether or not it is healthy depends on the reasons the money is needed. If the money is needed to finance new business based on a growing economy, it is good.

If the demand is predicated on the need to replace income, or being used to speculate in rising markets, despite little or no organic growth that is a danger area.

The so called recovery after 2008 to 2020 was the weakest recovery in US history despite massive borrowing. That borrowing increased substantially in 2020, and is growing now even faster.

The problem with debt, is that as it increases, it provides diminishing returns in growth.

I would think that the Fed will do its old trick, of keeping interest rates low until all the suckers have been sucked in and then increase them, therefore, turning worthless printed numbers into real assets for the banks to forclose on…..

“Cash-out refis are also down but only modestly, “as these borrowers are driven more by cash needs than rates,” the AEI report said.”

We are used to this now but it is actually extremely worrying

The Fed has said it won’t raise interest rates any time soon, but if the market continues to push rates up, then that is not the Fed’s doing. They never said they would stop the market from pushing up rates. At a deep level, the market wants higher rates because we are all beginning to suffer from market psychosis exhaustion syndrome.

There is a lot of money just drifting and not finding a home because everything is just too damn risky or worthless. Some sanity and a reasonable amount of predictability is what the economy needs. In the cleanup after Covid, it will be seen that real investment is required to repair the damage. Actual cash that needs to be outlaid for actual productive investment. To continue this twilight zone during such an important recovery is madness.

“Sure”, you say, “that’s why they are handing out trillions of dollars.” Yes, but that is not the only thing needed. The secret sauce is confidence. We are not just talking buying discretionary items to pull the economy out of a rut, we are talking about a real return to spending your hard earned money on something that may never show a return. Hopefully it will, but only time will tell. The ol’ entrepreneurial spirit happens to be the best option, post covid. I’m sure many people in the Hospitality sector know what I am saying. There is a lot of good prospects with a restaurant in the post covid era.

Once we are all inoculated against Covid ?, the government will most likely create incentive schemes for people to start a business that they hope may fill gaps in supply chains. In fact, I’m sure that some of those stimulus dollars have been earmarked just for that purpose. That’s where the confidence comes in. People will need the confidence of knowing that this is not just a confidence trick.

That is to say that it IS a confidence trick, but it is more than that. It is serious and may take more than five minutes of tapping away at a phone to make it happen. You may have to do some work. You will probably have to come down from that Robinhood high you’ve been on. You may also have to drive to and from your place of business every day, heaven forbid.

The first mover advantage is a proven method of success. Get started now, because once you have had your shot, you are free and clear to re-immerse yourself back into the real world.

Yes, I am well aware that all you contrarians out there think that I’m a shill for the man, but honestly, I am just over this schitt and want life to go back to normal. So I’m going to play along with it.

End of rant.

You are not ranting at all. You are really rather discreetly referring to real fundamental individual concerns based on many real unknowns that the generalized expectation from many narrative sources and writers based on an expected behavior of “following” and “doing” by mass population behavior criterion.

You are quite right about “The first mover advantage is the proven method of success”.

Ultimately the only thing that you possess is your own body. Take the best care of your self that you can do, anything else that you can do is part of the game, especially where you are the only game in town in some places. It remains to be seen how many games survive and what the moves are, and where, and when.

“Once we are all inoculated against Covid”

Anyone who is counting on this pandemic suddenly ending, or is counting on vaccines being successful, may want to do some research on the new strains and mutations of the virus, and whether the vaccines are effective against them.

While we all hope that this virus will be suppressed and we will be able to return to a more normal life, the reality is that at this point the outcome is not written in stone.

It would be prudent to plan your finances to be prepared for all possible outcomes.

I just purchased a home for $540k in an extremely hot market. While I know that these are peak prices, I have been saying that since 2014 and really missed out by waiting for the bubble to burst. Not only did I pay more money, but I lost out on 7 years of payments going towards overpriced rent instead of a mortgage. I locked in back in January at 2.25% on a 30 year fixed, so my mortgage payments are now less than my rent on a 2br/2ba apartment is. Even with rates going up, how much could demand crater? Millennials are tired of renting, immigration keeps adding more bodies, and there is no land close to the metropolitan areas to build. So, that leaves you fighting for either a lousy townhome or cluster home close in or an ungodly commute that makes you want to gargle draino.

Yeah I can certainly relate. I am at the same boat myself, although maybe because I am stubborn or stupid, still holding out for prices to adjust back down to earth a little, especially given the rise in the last couple of months are especially problematic from a buyer’s and bubble trend perspective.

Perhaps this is the new normal and all the lemmings are right, housing can only go up forever. However, the way I look at it, if that’s the case then I guess am the missed out of the FOMO fundamentals. Already too late but for sure I am not paying way above for a POS crapbox just so I can own a home. Rather, I will continue to rent and invest my money elsewhere. If everything is hype to the moon with no end in sight, then tell me which investment has generated a better return so far? Amazon bought in 2014 vs a house bought in 2014? I think we all know the answer to that. After all, if the logic is this market, both stock and housing’s new normal is to defy gravity..I would rather take my chances with something more liquid. It’s sad that people looking for a place to live and raise a family have to resort to casino timing sensibility to get a decent place for a decent price, what an American Dream. As long as I get rich, F everyone else.

All of the things you cite were red flag warnings to you that something was terribly wrong, but you ignored all of them and bought a house at the peak at the worst time in history. I’m sorry. Maybe post here in a few years about this decision which will most certainly be a valuable lesson in life about asset price bubbles, debt and illiquid assets.

He has an interest rate of 2.25%. Even if he paid more for the house he won’t know until later on down the road if it was worth it. No one will know now.

And if the house price drops to $200K

or if property taxes go up to $3K/month…

“Oh, but that will never happen”

I think having hard assets during times of inflation is key. I don’t trust that politicians and the fed (one and the same) will not continue to devalue the dollar. So, even if they do, I will be paying this house off with Zimbabwean-tier dollary-doos in the next few years. And even if I did pay more, I still don’t think this anywhere near the top of the market. Plus, I look forward to having more space to do my various hobbies and interests that simply aren’t feasible in a cramped apartment.

Also, if rates do go down it should, under normal market conditions, cause house prices to go up. Win for me. If rates continue to climb and house prices do dip, I’m still paying 2.25% on a house I can either live in or rent out. It’s fine by me at this point. No one knows, no one is an expert, and my magic 8 ball does a better job at predicting the future than all know-it-all analysts and financial doomers posting nonsense about how we’ll be bartering in animal pelts and ammunition “any day now”, just like they were when the Dow was “too high” at 13k.

No one can time the market. You made a choice. It sounds like you’re happy with it.

I got out of debt and stayed out of debt. Housing inventory is low in my area. Rentals are seasonal. Builders have seen their backlog of unbuilt homes rising. They started buying up lots. I bought one with road frontage, water and cable. Sandy soil percolates well. I think people will need shelter no matter what interest rates are. There are rural areas with cheaper land. SpaceX is building satellite Internet for rural people.

It’s gonna get interesting in CA over the next few years for the RE market, especially if the State or Bureau of Reclamation starts very nicely and sweetly, and probably quietly, buying out multi-million dollar homes to “RENT OUT”, as the ocean reclaims the beach and of course the structures that were built way too close to the at-that-time shoreline begin with. Especially if all political favorites continue to play their standard game plays, just guess who gets to walk away with more “loot”. Guess what happens with all taxes, and all access from non-benevolent real “GATEKEEPERS”.

Really, you think the ocean is going to start swallowing up coastal California real estate in just a few years? It seems to me the bulk of those houses are at least 10 feet above sea level, even up on cliffs and Tsunami safe. And of those at sand’s level, the beaches are quite wide. I’m mostly familiar with SoCal, though. And of course, “the big one” could change the landscape. ;)

Rates will be negative until everyone’s favorite self-less and caring generation passes away.

This real estate rally has legs. It will take more than 50bps to kill it off. And, even if the rate increases does cool off the housing market, rates will hit new lows shortly.

My common sense says you’re wrong but Uncle Sam has been killin’ it with ways to work around reality lately. I mean, really All Star level stuff coming out of DC. We’ll have Universal Basic Income by the end of April.

Still, I’m rooting for reality. This madness has to end.

Here’s the real future:

UBI isn’t coming, we are too broke. We have seen the last of the stimulus checks and probably extended unemployment as well. Student loan forgiveness is turning into a return to allowing discharge in bankruptcy. And they are even going after the credit bureaus by proposing to give the function to the CFPB. They need to control your social credit score and need a starting point.

UBI will come in one way or the other. Billionares don’t want uprise from their debt slavs among the bottom 90%. They want to protect their wealth at any cost and the Fed is willing to do their bidding!

UBI: It’s my money and I want it NOW! LOL

You sound just like a REALTOR shill. Do you have a real estate license?

Nah, SoCal Jim is another cat you can’t take down here as he also turns out to be right just about all the time. Like Petunia, Mr Engel, and Unamused.

Ever looked at real estate prices in first tier Europe?

Rates go up a bit, then crash down to ever lower mortgage payments.

An prices, as a result, are stratospheric despite depressed economies.

Guess that’s what’s coming to the US too.

How long has that been their normal?

20 years

Here in Ne andIa farmers hurting taxes way to high losing100$ a acre on corn better start to worry about eating instead of 1 million$ houses history always repeats

1) The current average home price is $313.

2) The RE statistic : Y/Y price rose : 14% from $270K to $313K, or $40K/Y.

3) That’s fantastic.

4) But in SF & NYC they collapsed in the hundreds of thousands $ and

in the millions. NYC became a slave ship.

5) Every bubble collapse is led by the upper echelon, thanks to WFH.

6) Y/Y Home Price Appreciation chart : a jump from week 21.

7) Shortening the thrust from week 33.

8) An uptrend channel coming from week 37 to week 50.

9) This channel was breached.

10) The flyover boom is over. Home for sale signs take longer. NYC + SF will cont to lead.

There are lots of fat cats on the West Coast that did nothing to earn a nice retirement. All they did was buy a property 20-30 years ago with a big mortgage attached to it. That little bit of starting equity probably returned them 25x their money. In other words, $60k down on a $300k house (now worth $2 million), turned into $1.94 million gain without lifting a finger.

Why did the Federal Reserve and legislators think it was a good idea to provide some people with such windfall gains, to the detriment of later generations who want to live in these areas?

These gains were not prompted by market forces. They exist because the Federal Reserve and government have been subsidizing home ownership through continual interest rate reductions.

Can anybody explain why such generational wealth transfers are desirable or necessary, from the standpoint of the Federal Reserve Board. How does the policy to enrich some at the expense of others benefit the economy overall? When economic activity is accelerated, or shifted from future generations to the present time, how does that benefit the economy in the long-term?

1. Have you looked at the composition of Fed Board Members? You see anyone who’s 35 years old or below?

2. Have you read Shakespear’s King Lear?

Do you have any concept of what it took to have a $60K down payment 30 yrs ago? Did nothing? Really? It always amuses me how some people delude themselves into thinking there are rainbows and pots of gold just to be stumbled upon….

There is something in life called the pinsetter theory. It dictates that sooner or later we all end up where we deserve to be, based on the things we have done to better or worsen our position over the long haul….

The other side of that coin is that the described windfalls will either be passed down to the next generation, or taxed away for the commons. Or both.

Perhaps the solution for these generational and geographical blips is simply tax reform? But nobody wants that, either.

CA has 55 electoral votes and the Speaker of the House.

Dear Bobber,

I hate to destroy such innocence. Consider the possibility that the (not government owned and deceptively named) “Federal” Reserve might not have your or most American’s best interests in mind when it does that. As to politicians, those that are not bribed and corrupt just want to get re-elected.

Their worry is the next election like many corporate leaders who are not crooks just worry about their year’s earnings. They live for today and do not plan much for the future, which might become the epitaph of our brilliant republic if things continue the same.

I really wish all of the smarter-than-thou people here talking down to anyone looking to buy a house would explain what they expect non-homeowners to do. Keep renting? Seems like a guaranteed, gigantic waste of money to me. Have you seen what rent costs in an area people aren’t referencing in their newest rap song? It’s easily more than a rent payment. Since every new build is a “luxury apartment”, l one bedroom apartments in this area are $1400+ dollars unless you want to “keep it real” and live sandwiched between the sex predator on one side and the gang-banger on the next. No thanks.

And, further, how do you propose housing costs will catastrophically plummet? I’ve been following this topic for years now, and each and every quarter since 2014 or so we’ve seen warnings about the real estate bubble and have been shown fancy charts showing how much higher we are above 2008 crisis. Where was this impending crash? Let me guess, it’s coming any day now. Trust the plan, right? Please. Between increasing migration, destruction of the dollar, God taking a hiatus from making more land, how do you propose we are going to return back to 1970s housing prices outside of a Mad Max dystopian environment?

The fact is that there are cycles to any market. Always. If you think going back to 2014 gives you some kind of comprehensive outlook on the market, you are very short sighted.

I have seen many housing bubbles and corrections in my life, and every bubble causes people to panic feeling prices will never again come down, and they must buy now or be priced out forever.

In 2007, no one believed housing prices would ever drop again, yet in 2012 I purchased a home by short sale in a San Diego suburb for about 60% of its 2007 valuation.

While the trajectory of prices is always higher, it does not get there in a straight line.

I’ll concede that you are more right than any of us who still believe in market forces. The markets, especially real estate, have been manipulated by the fed to keep their best customers whole. Since the fed is owned by the banks, they will not bite the hand that feeds them. The banks, equities, insurance, real estate, and now healthcare are the darlings of the fed and the swamp.

Expect the wealth transfer to continue until it doesn’t. Back in the 1990’s, I expected Bear Stearns would fail within 5 years. Had I stated that back then, I would have been relegated to loony status, but I could see it coming. It took a lot longer than I expected, but eventually the rot was too great to hide. So too with the current state of affairs. Lots of people can see the rot, but it may take awhile for it to cause a failure. It’s up to you where you want to be when that happens. That’s the point of the conversation.

Not so much smarter than thou MH as older and more experienced with the RE market,,, and many of us have been burned to some extent over the last 50 or even 70 years as a result of the cycles that seem to have occurred fairly regularly over that time.

Dad had no work for six months in 1956 and we had to sell the farm and one of the houses for a lot less to be able to keep the house/home we lived in, and even though both sales produced a profit over their cost basis, that too was a lot less than it would have been six months prior.

IF you can ride out the likely coming crash, a crash that is almost a question of when, not IF, your home/house will or can eventually help you find a debt free life.

IF you did your ”due diligence”, and are happy with it, pay no attention to anyone’s negativity, but start now to improve or at least thinking and planning about improving your new home with as much leveraging of your labor as possible.

Sweat Equity is a great way to accumulate capital; actually the best way if you can do, or learn to do the maintenance and repairs and any needed rehabilitations and improvements.

There are SO many U-T videos available these days that are helpful on every subject if you are just beginning.

I encourage you to study as many different ones you can and then make your own careful lists of materials and even lists of procedures in the order they are done best.

Good Luck.

Another 3 trillion dollars coming down the pipeline. Interest rate heading down again.