With actual house price inflation based on market data, overall CPI would have jumped by 3.7%. Lifting the cover on the deception to keep CPI low.

By Wolf Richter for WOLF STREET.

For most Americans, housing costs are the largest item in their budget, ranging from 30% to 60% of their total monthly spending. In its Consumer Price Index (CPI) for February, released yesterday, the Bureau of Labor Statistics reported that the costs of homeownership (which the BLS calls “Owner’s equivalent rent of residence”) have increased by just 2.0% from a year ago, and that rents (“rent of primary residence”) have increased by 2.0%. They’re the biggest items among the 211 items in the CPI basket and together account for about one-third of overall CPI. They play a huge role in CPI. So…

Rent inflation of 2.0% year-over-year on average across the US might be roughly on target, from what I can see in other rental data. But homeowner’s inflation of just 2.0%, given the skyrocketing home prices? Ludicrous. In its latest release, the Case-Shiller National Home Price index jumped by 10.4%.

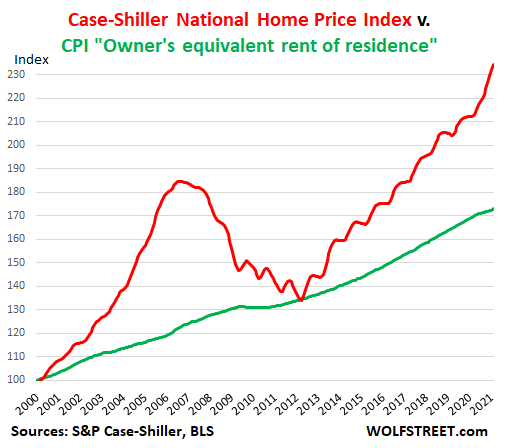

This discrepancy between home price increases and the CPI for homeowners – which has for years contributed to understating the overall CPI – is depicted in the chart of the Case-Shiller National Home Price Index (red line) and the CPI for “owner’s equivalent rent of residence” (green line). I set the homeowners CPI at 100 for January 2000 to match the Case-Shiller index, which is set by default at 100 for January 2000. This allows you to see the progression of both indices on the same axis.

The thus corrected CPI increases by 3.7%.

The “owner’s equivalent rent of residence” accounts for 24.2% of CPI. If it had increased by 10.4%, in line with the Case-Shiller index, instead of 2.0%, the overall CPI would have increased by 2.03 percentage points more. So add the 2.03 percentage points to the reported overall CPI increase of 1.7%. And the thus corrected overall CPI would have shot up by 3.7%!

During the Housing Bust, after five years of dropping, the Case-Shiller Index briefly joined the CPI for homeowners before taking off again – and there is a reason for that we’ll get into in a moment.

The S&P Case-Shiller Home Price index is a good measure of house price inflation because it is based on the “sales pairs” method, comparing the price of a house when it was sold in the current month, to the price of the same house in prior transactions years ago. It also accounts for improvements and removes outliers. In other words, it measures how many dollars it takes to buy the same house over time – and thereby it measures house-price inflation.

This discrepancy – in reality, a form of purposeful deception – between actual home price increases and the CPI for homeownership has been bemoaned before and is not a secret. But it’s not broadly discussed in the media so that everyone knows by just how much the homeownership component in the CPI understates the actual homeownership inflation that Americans confront.

To its credit, the BLS includes homeownership costs in the CPI basket. By contrast, the EU does not include homeownership costs at all in its basket underlying its Harmonised Index of Consumer Prices (HICP). It only includes rent. And thereby housing costs are woefully underrepresented in the EU’s inflation data.

The rationalization put forth by the BLS for this discrepancy is that it doesn’t actually consider house prices relevant for inflation. It considers houses an “investment,” and investments don’t enter into the CPI. What it does try to put a price on is the cost of “shelter,” which is a service. This makes sense with rent. A renter pays for a service. But the BLS extrapolates this rent-as-a-service to homeownership. And that’s where the logic croaks.

The BLS housing inflation data is based on the “Consumer Expenditure Survey” sent to consumers, rather than market data for prices and rents. It’s up to the homeowner to decide what their primary residence would rent for it they tried to rent it out.

This is the question in the survey: “If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?” So homeowners have to come up with some figure.

For the CPI, the BLS says, the cost of shelter of the owner-occupied home “is the implicit rent that owner occupants would have to pay if they were renting their homes.”

This explains the black line in the chart above that is completely out of tune with the reality of home prices: It tracks rent inflation, not house price inflation, and it essentially represents what homeowners think rents would be. So the rent CPI, which accounts for 7.8% of total CPI, and the homeowner CPI, which accounts for 24.2% of CPI, measure roughly the same thing: rents. And this thereby neatly and purposefully excludes rampant house price inflation from the index. And it also turns CPI into the sad joke that it is.

Durable goods inflation +3.3%. Food inflation +3.4%. Services inflation rising, but still held down by battered airline fares, lodging, event tickets, etc. — until people start traveling and going to events again. Read… Dollar’s Purchasing Power Dwindles to Another Record Low. Fed is Getting its Wishes

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

On purpose.

So Social Security and other indexed entitlements do not get increased.

And so savers do not even get paid interest to cover real inflation.

“And this thereby neatly and purposefully excludes rampant house price inflation from the index. And it also turns CPI into the sad joke that it is.”

Some people might think that this is a bitch & moan website .. hey.

Shouldn’t we be ‘good sports’ about the creative irregularity of the worlds economy !!

?

govt stealing been happening for centuries

how else are STUPID politicians gonna make living

interest rates should be at least 5%(which doesn’t even begin to cover the avg 10% annual DEVALUATION of fiat $dollar)

we have NO MORE MIDDLE CLASS

Yep, this is the way they are funding all these government boondogles. Depleting the value of savings of all Americans, and the incomes of retirees, and putting the working middle class up to their ears in debt.

ENJOY!

House price is always inversely proportional to interest rates.

In the Eighties, interest rates inched down from 18% to under 9%, but houses prices rose until early 1988.

Roddy,

Kam did say that falling rates parallel rising prices…just as you indicated.

The better test is what happened to home prices/sales volume during the ascent to those 18% rates in the late 70’s.

My guess is that sales collapsed (home builders mailed bricks to the Fed) and that prices fell (this was the heyday of seller financing…which is often employed to get a sale price that no independent bank will loan against).

He correctly wrote “inversely proportional”, meaning they rise when interest rates fall.

RTC DAYS opened up fact that BANKSTERS were lending to deep STATE investors

still remember TONY DORSETT putting $400,000 into DEEP real estate tax SHELTER were he could DEDUCT FROM IRS 4X times investment

IRS came back and SPANKED HIM for deducting $1,600,000 from income taxes and then penalized him for it

WHY RTC came about

I STILL APPLAUD GEORGE BUSH FOR DOING RIGHT THING – cost him election to CLINTON

by 1992 the economy was booming again – but not BECAUSE Clinton was running things

@kam Not really.

The usual way to do an appraisal is to add the value of the land to the value of the structure. The value of the land is an almost pure supply and demand sort of thing. A 1/4 acre lot in Palo Alto is currently worth maybe $1.5M. That same lot is Billings, Montana might be worth $12k, if it is on a paved road.

The value of a house is somewhat easier to figure. It is a mix of square footage, condition, construction quality, and local cost of labor.

It is true that high interest rates will suppress demand, which depresses price. This is an effect which is temporary, on a timescale of maybe 3-5 years. (Even with hideous interest rates, house prices zoomed up between 1975 and 1981.)

Similar comments for low interest rates, which tend to increase demand.

I would put interest rates as one of the top five factors which determine house prices, but would put it behind “Local Population Growth” and “Local College Graduate Salaries”.

Good points, although I weight the impact of ZIRP post 2000 much, much higher.

It would be interesting to get actual year by year sales/price data for SFH from say 1970 to 85.

I do know the 70’s were big on RE…but my guess is that fast rising rates choked that off starting maybe in 1978 (although the rise of questionable seller financing may skew the stats more than a bit…a sale ain’t much of a sale if the you’ve got to claw back the house in three or four yrs because the “buyer” drowned under 10%+ mtg rates.)

I just see 2000-20 as being a rotten 20 years in terms of employment/salary growth and, accordingly, population growth.

Certainly not healthy enough to double median SFH prices absent SuperZIRP.

That appraisal method you refer to is called the cost approach. Only FHA uses it. No one else does. Most use market approach.

Interest is the ‘magic’ ingredient.

On a 4% pa mortgage the house price has to double in 17.5 yrs to break even. People only talk about the sticker price and how much they’ve ‘made’ without deducting interest, maintenance, transfer fees’ etc.

It should simply be a depreciating place to live but a house has become about the only inflation proof asset Joe punter can easily get in our crazy debt fueled western economies.

The internets usually say my house goes up about 2% in one month not a whole year. This is what the internets say how much my house inflated.

Redfin:

$481,278

$166K since sold in 2016

Zillow (in a rare down month)

Zestimate

$410,660

LAST 30 DAY CHANGE

-$5,447 (-1.3 %)

I hate to say I see the logic in this. My friend is good with real estate. She bought about three years ago and got a good deal from a distressed seller. She probably is going to sell into the bubble. If she successfully sells, her equity gain will mean she lived there basically free including expenses. Her home would probably rent for $1600. Her house payment with tax ins was around $1050. How should you calculate housing inflation? It is complicated.

But any situation where you rely on an opinion of a nonprofessional about rent seems crazy to me.

As a professional, the professionals aren’t even paying attention.

If interest rate movements are behind 80% of home price movements (and I think they are) maybe it is better (more liquidity, fewer transaction costs) simply to speculate in interest rate futures rather than to do so indirectly via a house…

I think Wolf should pose a reporter and ask Jerome/Janet if they really think the cost of their house went up 2% in 2020?

Yet, housing starts are barely past their long-run average. Is there no profit in homebuilding? Heaven forbid mortgage rates go back up or they might stop building them.

Financing a house build and hoping a buyer will show up in five months is risky business and it’s easy for market to change in that time.

Interesting to note the lack of much (if any) of a hedging market for new home construction, despite large sums involved and significance to ntl economy.

Obviously, the non std nature of houses (size, design, location, etc) make a ntl home futures mkt difficult…but, there has been plenty of financial creativity (for good or ill) in other mkts.

rhodium

There are many places in the United States which are not in FL CA AZ NY TX WA OR or a couple other inflated states. In those states, it is still MUCH cheaper to buy an existing home and fix it up a bit vs cost to build a new one. Pretty much all of the Midwest and South comes to mind.

TX is not inflated like those other states (yet). You can still buy nice brick homes in great neighborhoods for well under $200/sq-ft. And those areas are not out in the boondocks. I lived in California for 12 years and saw the real house inflation on a personal basis.

I don’t know about Texas as a whole. Homes were practically free before. Now most (excepting certain parts like Austin and Collin County) are just around “MSRP” and reasonably manageable with the typical household income. I’d replace TX with NV and ID on your list. Boise and Reno have gone nuts for where they are.

Yes, I guess TX, except for Austin, Galveston and suburban D-FW are still affordable for existing homes. I agree with ID and NV (Vegas) being overpriced and thus susceptible to more NEW construction and boom/bust effects in the future.

However, to say ALL housing is over-priced is a huge reach. I bought fixer-uppers in KC MO for $20K+/- and had maybe $60K into them to make them beautiful turn-key homes. They can still be gotten for similar prices today and before you presume…..not all of them are in the “hood.” ;-)

Lumber, Copper, labor….

Building is becoming cost prohibitive because of the REAL inflation, the one that’s not reported.

Who wants to be exposed to lumber prices? Or fight with cities over insane zoning and infill regulations?

Yes, there goes my new deck! I guess I will just replace 25 yr old fence posts instead.

@rhodium

It is really hard to get a building permit in any good location.

The most desirable places already have a house on them, and the zoning guys will not let you build a “Granny Unit”, despite what the newspapers may tell you.

The reason why so many houses were built in Vegas and Victorville in the period from 2000-2006 is that these places were pretty much the only places where you could get a hundred building permits.

If mortgage rates go up all the builders will retire, labor will move back to Mexico, the timber and cement industries will shut down, white goods dealers will go bankrupt, and all the banks will liquidate from lack of loans.

Yep, because that’s how it always is when mortgage rates are above 3%.

I love the humor in Wolf Street comments. Delightfully witty and facetious all around.

Of course it is nonsense, purposefully. As home prices ratchet up, so does the down payment, as well as mortgage payments, ceteris parabus, as the payment is dependent on interest rates which can be manipulated. So do RE taxes, too.

Asking the home owner to estimate what the home would rent for is a flawed method, as the homeowner is likely not a reliable source for this information. And, it is irrelevant to what he is on the hook for anyway.

Also am quite suspicious of how health and medical care and education price inflation is calculated.

My new favorite latinism – ceteris paribus. THANK YOU!

I like “cave canem”

Nos condemnabitur

Oh yes we are.

Libera te tuteme ex inferis. In Wolfspace, no one can hear you scream, even in Latin.

I prefer “illegitimis non carborundum” (don’t let the bastards wear you down), especially since the fit hit the shan in 2008 and fiscal restraint became extinct.

“Ave Imperator, morituri te salutant.” – TINA

dulce et decorum est pro patria morii

or

de gustibus non disputandum est

or, in my case,

que bonita es hacer nada, y despues de hacer nada descansar

I like the original

Nihil vadit ad HECK in recta linea!

Nothing goes to HECK in a straight line!

?

Before the cheap and easy money era, it was a fairly simple calculation.

Average house cost was 2.5-3.0 times the average household income.

Average house total costs (PI, insurance, taxes, maintenance, etc) could take no more than 33% of take home pay.

Average house cost was about 100-120 times average monthly rent.

Fairly easy to correlate to US census data.

All gone today.

Bubble on Garth…

Now they’ll sell you a car at 2x yearly income.

Now they’ll sell you a USED car at 2x yearly income.

Fixed it for you!

When they calculate healthcare, do they use the total cost of services and medications or do they use premium prices? Do they factor in the increasing costs of co-pays and deductibles?

Why wouldn’t they use the mortgage payment as the imputed rent? Ugh.

How would that make any sense?

You mean, how would that make me any cents?

Wolf,

I get it. I understand there is inflation. I understand it is not measured, I don’t believe it will ever be manipulated or controlled. Maybe the Fed needs a new mandate like keeping interests rates low.

John…

WHAT!

Short rates are essentially zero, and the real return is negative.

The Fed is supposed to

“promote moderate long term rates.” Moderate means not extreme….that means too high OR too low.

Too low promotes what we have seen for several years…irresponsible debt creation, govt borrowing that is only pulling future wealth to the present, setting a debt time bomb for future generations.

IF there were moderate long rates, the balance between lender and borrower would be maintained, and short rates would return to the normal level that covers inflation, or exceeds inflation.

The Fed has been neglect in two of their three mandates….stable prices and promoting moderate long interest rates.

And Congress, the alleged overseer benefits from the Fed’s rogue behavior with free money for vote buying programs, the debt from which is burying future generations in debt.

Historic us

I get what you are saying. I said it meaning with all the debt that’s out there now, we might as well change the mandate. Low rates. World banks I believe will be buying our treasuries like the Euro.

John

‘ I don’t believe it will ever be manipulated’ !

LOL!

Maybe the FED should get rid of its 2% inflation policy!

This statement floored me.

“If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?” So homeowners have to come up with some figure.”

Why is the government using such an error prone methodology to come up with the data on rental rates which is available to any competent Real Estate professional with a user ID and password, and has paid the fee for access to the databases containing this information?

Rents here in the Maryland suburbs of the Swamp for houses are going up more than 10% per year along with the prices. As soon as a house is listed for sale it is gone the next day. The government CPI figures are 1000% total BS.

This is why I no longer pay any attention to government published figures on inflation.

I may have to publish my own inflation index. I will call it the Swamp Creature inflation index.

“This is why I no longer pay any attention to government published figures on inflation.”

Yup, you are damn right. There are several figures that I won’t believe AT ALL:

1. Unemployment rate

2. CPI

3. US actual debt figure

I would also add GDP(GNP) number since the INPUTS used to extract that figure are itself controiversial, tilted to the optism side!

Remember:

The chair person of Federal reserve who said ” we will NEVER a financial crisis like the 2008, in her life time” has become the Treasury Secretary!

“(Reuters) – U.S. Federal Reserve Chair Janet Yellen said on Tuesday that she does not believe that there will be another financial crisis for at least as long as she lives, thanks largely to reforms of the banking system since the 2007-09 crash.Jun 27, 2017”

More lies and deceptive numbers ahead!

Swamp…

“Why is the government using such an error prone methodology to come up with the data on rental rates”

I’ll tell you why.

Because the results of the survey are only known to them, thus they can publish whatever they want and there is no way to check the results of the “survey”. And does the survey even take place?

This statement floored me:

“To its credit, the BLS…”

What is today’s actual unemployment rate, anyway?

It’s not 6.2% that’s for sure.

Probably 18%, at least.

Low 20s, plus or minus.

I completely agree that owner-equivalent rent is an inane concept. A better approach would probably involve using Case-Shiller information, perhaps adjusted by some kind of formula that takes into account the prevailing market interest rate.

However, you should keep in mind that with respect to owners equivalent rent, the BLS is not really interested in respondents’ absolute amounts answers, only the rate of change from previous reporting periods’ amounts. Their thinking is that while respondents’ provided amounts may be error-prone, the error itself would be rather consistent across time periods, thus allowing the BLS to extrapolate reasonable rate of change information from the data set. At the end of the day, it’s that rate of change that they are seeking to track.

I’m going to put a different slant on the rent comment, if I may. Kind of turn it back around.

When someone buys a house, or is thinking about it, they need to determine if their prospective mortgage payment, (with a feared possible interest rate increase), is the same or less than rent of same house. Your estimated mortgage payments must also include taxes and maintenance. Another factor is your age and employment prospects. My favourite saying is from Art ‘the barge loader’, “ahh, you can afford that payment now, but can you make the payment if your not working for awhile”? (BC Forestry industry is very cyclical). Art loaded log barges and was extremely high paid for doing so, but he also was laid off when logging shut down for markets or weather..

Then, any ‘aware buyer’ might take a chance on a possible rise in house value appreciation, but at least able to put a dollar amount on an emotional decision for those times when people ‘fall in love’ with a particular property in the ‘gotta have it category’. If your criteria is not met, then you are buying “too much house”, are in the wrong market, or don’t earn enough.

I am in my third home after 42 years of home ownership. Emphasis on the word “Home”, not house, housing, or investment. However, in all cases my criteria was met, our mortgage payment was the same or less than rent of same property. Third home was for cash.

If this is not possible then you are buying into a market you cannot afford, and are speculating; relying on hope for a continual rising market that makes your purchase sensible…..to you. It is what keeps the market crazy high and RE agents in nice cars and hobbies.

Furthermore, from the days of T Pit I have argued on this forum that the goal of any home buyer is to get your house paid for as soon as possible so you do NOT have mortgage payments. This questions the very idea of 30 year mortgages as a means to affordability, to its’ core. Aim for a twenty, or even 15 year term, with options to double up payments or lump sum on anniversary dates. This concept is in direct conflict to other investment strategies that tout the returns on stocks, dividends, etc. I have been derided as a fool by more savvy and successful people who know how the Market works. (Or think they know). I get it. But I know housing, from how to build houses and apartments and how to fix them, having done it for decades. I also know this statement of Wolf’s, “For most Americans, housing costs are the largest item in their budget, ranging from 30% to 60% of their total monthly spending.”

Think about that. A paid for house is just like you were handed a 30% – 60% pay raise. In times like this, if you lose income but have your housing paid for, you just cut back a bit; no dining out, buy groceries that are only on sale or even as loss leaders, plan a menu, cook at home etc. It’s fun, actually.

I also tell people, when they ask and only if they ask, if you don’t have a paid for home you cannot retire. Of course this is different for many; millionaires don’t have to worry about the rent nut. But for normal working people, white or blue collar, monthly expenses are a somewhat larger factor in budget math.

Losing your health care insurance during a pandemic can’t be that much fun.

Good comment, as yours mostly are P,,, but you are leaving out one or more of the largest components of ”home ownership,” which has been pointed out here on WS many times:

No matter where you live in USA at least, you are in reality only renting your real estate of any and every kind from the GUV MINT, who will take it in a NY minute if you fail to pay them their rent AKA taxes and fees.

So, with Guv Mint taxes and fees, and realistic estimates for maintenance NEEDs — ( and not including wants such as new decks, hot tubs, the pretty gazebo, swimming pools, new kitchens, etc. ) — the remaining ”nut” is still likely to end up between 15 and 20 % of income for working class folks.

Realistic estimates of maintenance requirements vary of course, but I continue to respect the opinion of one of my mentors from the 60s who owned a ton of SoCal properties — enough to make even SoCal Jim envious– from San Diego to Santa Barbara, much of it purchased by his dad in the 1930s; he said it averaged out to 10% PER YEAR of the value of the RE.

He was also very clear about maintaining his properties as though he lived in them, or had a biz in them, so he rarely had a long term vacancy.

Also relevant, he did no manual work what so ever on his properties, unlike you and me and many others can and do.

Paulo – I still pay a mortgage. Within a few years my RE taxes will most likely be the largest item in my budget. I tried voting but I guess everyone else wants higher taxes. I have been told that if you don’t pay your taxes eventually a man from the government will show up with a gun and put your stuff on the street. I just can’t wait until I can vote again.

When asked if they have an IQ that is higher or lower than average, the vast majority of people answer “higher”.

They all must be from Lake WoBeGone eh, r2/3,,, where GK has made clear, ”all the kids are above average.”

Dunning-Kruger

Unfortunately half the people in the US have an IQ of 100 or less. Our modern educational systems are working hard every day so that half the people can have an IQ of 100 or more. /sarc When people fail to understand a definition there’s not much to be said.

roddy-it has always been my observation and understanding that half of the folks you meet (plug in your ‘talent’ or ‘capability’, here) are ‘below’ OR ‘above’ average. When encountering the self-assigning of oneself to one group or the other the perceived mileage appears to vary wildly against quantifiable results…(also known as ‘the human condition’).

may we all find a better day.

“Why is the government using such an error prone methodology”

For the exact same reason they use a dumbass methodology to calculate “labor force” (crucial denominator in holy (hole-y) unemployment rate.

Because crap methodology allows for Gvt manipulation of voter perception.

Yeah… that question leapt off the page to me as well.

As I used to tell my students… good research data is hard to come by… but it isn’t made easier or better if the questions you ask are poorly designed.

Spencer-this is why the American love-hate relationship with any kind of polling baffles me. Questions are not as often poorly-designed as they are constructed to generate a preselected ‘preference’ of the pollers from the pollees. (If forced into any kind polling situation these days, other than an official vote, my answer is usually ‘null question’).

may we all find a better day.

Underestimating inflation causes a lower yield curve … and this is very good for real estate and hard asset investors.

I don’t think this is good for anyone other then the bankers large and small.

Mr. Wolf is kindly pointing out more fraud and the repeated fraud which amounts to just more skimming the froth. Again “lights off for second third mortgages.

This second time a round will be child’s play for them squid.

Surging yields are going to lead to a liquidity crisis, (not good for those speculating in illiquid investments) and the end solution either way is to drop rates back to zero. RE likes that but the road from here to there is rocky.

For 25 years I lived in Salem Oregon ( state government town)and up until about about 2004 the average home price was almost exactly 3 times the average state employees annual income. Then like everywhere else they became disconnected from reality. There will be a world of pain for the house pumpers, re investors, flippers, and landlords when things inevitably return to reality.

The reason I like reading Wolf Street is that it seems to be the only place on the Internet where there are people who still believe in common sense. Nearly everyone out there seems caught up in mania or despair. These comments are a breath of fresh air for my soul. Hope for humanity.

What banker came up with the trope that a house should cost 3Xs annual income any how?

Is it the same guy that came up with the 4 year car loan?

@Harrold:

The “3x” rule was simply a guideline for the maximum house you could afford, not that it “should cost” that amount.

BTW, that “trope” served me well in my early years.

Neighbor stopped by, wants to buy our lot. Wants to build. He can get Big Dollar for his house he says. Wants to build before rates go up. Has he seen price of lumber? Well, he is in construction. His bro built a new house for $250k USD, not incl. labor. When dingalings spend $250k, WATCH OUT. Nvm, Uncle Joe Robin’it Hidin’ Buy-den will bail you all the F out?

Dish soap 25 oz. now 19 oz. W t f ?

No inflation.

I agree with Swamp Creature—-let’s publish our own inflation. Can we air it on MSM? Don Limon or Jake Cra-ppper huge intellects??

This time last year the lots and acreage were being snapped up around me, some of the lowest-priced land in the country (Ozarks). But building isn’t happening, materials are too high. Lumber 3x times higher in the same twelve months, copper wiring, heck, even plastic items are up. It’s all BS.

Flipping old houses are cost prohibited. Too much tear-out and replacement is not feasible. There’s going to be some real shoddy fixed-up houses with lipstick out there for sale. Watch out.

Like many my wealth has increased more from my home than from saving. But normally the increases come from

the various big cities. This the first broad-based real estate boom in my lifetime. Since it’s an anomaly maybe the cpi is correct not to include it.

Wealth that is encumbered by “home ownership” is not wealth, it is potential wealth. Same with “stock ownership.” Same with PMs. Even bonds unless held to maturity. When you have to sell to access your “wealth” you have only potential. Potential varies widely with time.

Seneca’s Cliff,

To better understand your comment re state employee’s AVERGE annual Salary (less taxes?) in Salem OR re the cost until about 2004….please tell us what that “salary” was in 2000-2004?

OR…what is the average state employee’s salary in Salem OR (the capital)

2019-2020 AND what’s the average cost of a home?

James,

my data is mostly anecdotal, but here it goes. My data for this thesis goes back quite a ways. In the late 1960’s the burbs of Salem had arrived at my grandfathers dairy farm, and he decided as he was near retirement he would get in the home building business. He subdivided part of the farm and built the house himself. He did the concrete forms, framing, siding, flooring, inside finish work and cabinets ( from scratch) himself. Nearly all these one story 3 bedroom homes he sold for about $17,000 as the average state wage was about $5600 a year. My wife and I moved to Salem in the 1980’s and bought a house in 1987 but the ratio was lower then due to high interest rates. All the middle class type houses we looked at were going for $45,000 to $85,000 and the average state wage was $36,000. Then in 1992 fresh off my wifes new job $75,000 a year job as the manager of the cities sewage treatment plant we purchased the “tour home” in a new subdivision for $230,000 but our equity took the mortgage down to $210,000. I was an entrepreneur with variable income so we did not bother with it to qualify for a mortgage. The next 8 years the subdivision filled out with most house prices strictly tied to the average state wage which during the mid 90’s was $56,000 and the average house price in our subdivision slow grew from $165,00 to $185,000 as state wages ratcheted up bit by bit. Things began to change in 2001 but Salem stayed sleepy and when we refied in 2004 our house appraised at $245,000. Then things came unglued and our theoretical house price jumped to $530,000 by 2007 while the surrounding houses jumped to the high $300,000 . During this time state wages only crept up at the pace of inflation. We left town in 2011 and only got $290,000 for our house because we were still in the tail of the subprime crash. After that I don’t know exactly how things changed but since then house prices have certainly climbed much faster than the average state wage.

For what it’s worth, our house payment went up 6.7% year over year due to increased property tax and insurance. This is in one of the non-housing boom areas of Montana.

You would think the data collectors could come up with a simple household survey (as they do in the employed/unemployed survey) by calling a percentage of home owners and asking them what their mortgage payment was last month.

Also, 2004-2008 in when Prez Bush prompted the idea that “everyone should own a home<' & the "Liar Loans" were feeding the greed & deception in the housing market ALL OVEr the US of A!

The flippers and film flam men loved it.

Then came the CRASH…so what's new?

Everything is BS in this country. Everything. The lies, the fraud, the graft – it’s despicable. And I can’t even tell where the lies end and the truth begins.

On one hand we’re supposedly in a depression, losing over 700,000 jobs per week for over a year straight, but on the other hand you can’t even buy an RV because there are none on the lot, and the prices have skyrocketed to absurd levels due to a never ending procession of wealthy buyers with a “pay anything” attitude. Ditto for boats, and houses, and $80,000 diesel trucks. And good luck finding an enclosed trailer, or a car hauler, or a dump trailer, or any iteration of a trailer – the lots are empty and they sell like hotcakes.

And everybody is a stock market genius, and everybody is wealthy on crypto, and on and on and on. This is the most fantastic depression I’ve ever heard of. Money flows like water out of everybody’s pockets. I’m sorry, but I don’t get it. At all. A depression isn’t an event where all of a sudden everybody is flush with cash and can buy the most expensive durable goods and hard assets in history.

And no, a $1,400 stimulus check isn’t paying for it. There’s some real BS going on right now. Somebody’s lying, but I do know it’s not the RV sellers and the empty lot local utility trailer dealer. They report their best sales EVER. Something stink to high heaven.

At least you get something tangible when you pay for a house or an RV.

NFTs (non-fungible tokens) are the new “in thing”.

An online video of Lebron James dunking sold for $208,000 (This is digital, not a hard drive). CryptoPunk images are regularly selling for over 25,000 USD.

What is a CryptoPunk image, you ask?

“The CryptoPunks are 10,000 unique GIFs. No two are exactly alike, and each one of them can be officially owned by a single person on the Ethereum blockchain. Originally, they could be claimed for free by anybody with an Ethereum wallet, but all 10,000 were quickly claimed. Now they must be purchased from someone via the marketplace that’s also embedded in the blockchain. Via this market you can buy, bid on, and offer punks for sale.”

Sold so far: 6,996

Average price: About 24,000 USD.

For a really ugly 24×24 pixel GIF of a strange-looking human. You pay more for Apes, Zombies or Aliens.

And recently someone sold a beautiful GIF of a Michelangelo quote for $57,000. You need to login and see your “artwork”.

’bout as healthy as sneaker fetish I suppose. …

I used to collect golden and silver age comic books as a teenager in the early 1980s. I once bought a copy of X-Men #1 in near mint condition for $200. Probably around 1982-83.

I decided to look up the price for it last night for the first time since the mid-80s. A mint copy sold for $340,000.00.

Guess I should have kept them! Even as a 14-15 yr old, I kept my best ones in mylar sleeves in a bank deposit box.

I saw that a NFT digital art collage was sold by Christie’s this week for $70 million… to an unknown buyer.

How do you find someone with $70 million to blow like this? Where do I go looking for such unicorns?

$70 million is no problem. Powell could have paid much, much more if he really wanted it. “What ever it takes.”

“And no, a $1,400 stimulus check isn’t paying for it. There’s some real BS going on right now. Somebody’s lying, but I do know it’s not the RV sellers and the empty lot local utility trailer dealer. They report their best sales EVER. Something stink to high heaven.”

In the words of Walter Sobchak: “I’ve never been more certain of anything in my life.”

No sarcasm meant or implied.

$1400 checks are peanuts , the big money has been in the PPP for businesses.

Personal anecdote, friend of mine owns a small business, employs about 20 people at most, bank calls him and approves for $1.2million ppp loan which will be forgiven if used for payroll.

He told me it was just free money, business was even better than usual during the Covid and he didn’t need money for payroll. He took the money and bought some real estate.

It’s hard to see your friends getting rich and keep your cool.

I think the excesses will become obvious when the dollar is worthless suddenly.

My bank is practically begging self-employed people with zero employees to get their free $20K, whether they need it or not. Just pay yourself, they say. It’s easier than ever, they say.

What do the banks get from this?

@Turtle:

Fees.

MM,

Very good point/illustration.

Wolf…could you put together a PPP in retrospect review post? Covering, for instance, if businesses could actually take the forgivable PPP while still remaining in full/partial operation?

I had kinda of assumed that the biz had to be shut down to get the PPP loans…but maybe that actually wasn’t legally required.

If so, PPP could have simply operated economically as a giant business grant

If so, C19/PPP is starting to look more and more like a huge inflationary reboot with a pandemic attached.

If so, it would also explain why the spending of March/April 2020 wasn’t done in stages…DC didn’t want people to think about it too hard or especially, too long

To get the first PPP loan and make it forgivable, your business didn’t even have to have declining sales. It could be a thriving business. There were some size limitations, and you couldn’t be a criminal, etc.

There was a ton of fraud going on with the 1st gen PPP loans.

The second-gen PPP loans are limited to businesses whose sales declined by 25% or more during the reference period. And there are some other safeguards. And there will also be a ton of fraud.

Now, in the new stimulus package, there are grants and loans for restaurants, etc., with the first couple of weeks being open exclusively to woman and minority-owned restaurants, after which time the money has likely run out for white-male-owned restaurants.

This whole thing is a huge mess.

I gave up trying to track all this.

@Wolf – thankfully we no longer have any racial or sexual biases in our government, this after many years of hard work and legislation for “fairness.” No longer equality of opportunity, it’s now equality of outcome. Won’t end well.

Wow…Probably the best post I have read in awhile that describes my feelings too.

Depth..

Dead on.

The Fake Fed rates are absolutely scrambling every metric of value and wealth.

No inflation, dont worry its only a spike….they tell us. We will “see through” the spike…they tell us. (ie they will let it run)

Central bankers are unelected yet they dictate, they control us.

Jerome Powell basically expanded M2 by 27% on his own…..WHAT!

Article I, Sect 8 of the Constitution gives Congress the right to “mint”. Powell’s digital minting is outside the bounds.

The Fed also pushes inflation on us…and that is a tax….and the same Constitution only allows Congress to lay taxes.

Who do we call? Apparently no one. For Congress loves the free money for their vote buying projects.

Depth Charge,

While I agree it’s disgusting and immoral, I don’t think there’s anything nefarious going on. I think it’s as simple as the government has transferred all pain that results from a recession to its own balance sheet. Let’s say the hit to GDP was 5-6%. The fiscal “stimulus” was 4-5 times the amount of economic activity lost, and that’s not even including the trillions of new printed dollars.

So, while in the past, people tightened their spending when the economy went into recession, here, very few people did. Many people were flush with extra cash from government largesse (whether from “enhanced” unemployment, stimulus checks, PPP, etc.) and those that weren’t, at least not directly, were very “confident” in the economy, as they are convinced that not only did the government have the ability to avert all pain, but that they were willing and able to do so.

Just think of the magnitude of the number. $6 TRILLION was spent by Congress in one year. That’s all of the U.S. debt from its founding until 2001 or so.

In the past, there was more of a sense of responsibility among our “leaders,” in that there was an understanding that all debt would eventually have to be paid back, and that debt shouldn’t be incurred unnecessarily. Now, they’re fully on board with MMT, and our reserve status and having been the world’s sole superpower for 30 years has allowed them to get away with it in the short term.

It’s as simple as that. That’s not to say there are no shenanigans going on with the BLS data, but the main reason for the empty RV lots, record Bitcoin prices, record house prices, and so forth is the $6 trillion that Congress borrowed to counter $1-$1.5 trillion of reduced economic activity.

Some day, there will be one hell of a hungover from this debt binge. I just don’t know when.

To paraphrase the hard money folks “when the Fed sets the rate of the treasury market” all other prices are screwed up.

Don’t worry, it can’t last. Reality will rear its ugly head as soon as it can. It always does. Many people spending (and gambling) their brains out with stimulus, forbearance, free rent and cheap loans will regret what they’ve been doing this past year. They think there’s a free lunch, but no there is not. I’m trying to stay sane through all this idiocy so I can pick up some of their pieces after the dust settles.

Depth

1000% correct

I drove through Louisiana last month, from about Lake Charles to Lafayette, I lost count on all the trailer and RV lots full of inventory. I think one was called RV World and they sure earned the name. Maybe you should give them a call or any on Interstate 10.

RV lots are full around here too.

The trouble with RV’s is many people think the RV lifestyle is fun and glamorous until they try it for a while and see how much work and cost is involved.

I liken it to getting a puppy. It’s not all fun and games.

Anthony,

So true, a friend has a low mileage 37′ foot “Coach” Cummins Diesel pusher. Him and his wife would come to visit 3 or 4 times a year. I have full hook up. Just about every time he came down he told me how he had to fix something on it, or was fixing it at my house.

Electrical panel, gas heater, cabinets, you name it. Luckily he is a mechanic, so he can do the work himself. But they still absolutely love the life style, they just bought a new one.

I am also mechanically inclined and can fix just about anything, but no way am I getting one, too much work.

When they visit, they have to check the wind conditions for the Benicia bridge, if it is too windy they have to delay there trip.

I have a brother who is doing that now. Monthly costs to park and hook up your R/V can be about $1200. Diesel costs between R/V lots is high. Minor repair costs are huge.

Our RV is for when the in-laws visit ?

Sorry, Petunia, but you’re making the same mistake a lot of people make – cherry picking and using personal anecdotal evidence to try to refute facts. I don’t know why people try to argue against something when they’re wrong.

“The maker of Airstream reported net sales of $2.73 billion, a 36% year-over-year jump, compared with analysts’ forecasts of $2.53 billion. Earnings per share of $2.38 beat forecasts by 83 cents.”

Thor is by far the largest RV manufacturer in the country. Again, RECORD sales, and my local RV people, who I talk to by the way, can’t keep inventory on the lots. You have to place and order and a deposit and wait.

I’m going to believe what I see and hear, and what’s reported, rather than somebody who told me they were driving down the highway and saw a bunch of RVs so it can’t be true.

@DC:

It is possible that those lots of RV’s seen along I-10 are consignment units – from people who bought them and had buyer’s remorse or had a job change (LA is part of the oil patch, is it not?) which made them unaffordable/repopped. They could have even been bought as temporary housing after the last hurricanes and are no longer needed (again… gulf coast).

Anecdotal, but an acquaintance of ours here in PHX bought an RV with 10′ of “toy hauler” space in the back. Used it exactly once (behind their $70K tow vehicle) and then took it to a consignment lot because they couldn’t handle it. They paid for both with the equity from their house (which they are now forced to sell because they couldn’t afford the new payment). Then there were the storage fees (can’t park them for free in a subdivision with postage stamp lots), insurance, and lot rot expenses. Sadly, their “Plan B” is even more ridiculous…..

However, that vehicle was sold by the manufacturer and dealer and both reported it as a sale and the resulting profit.

As a veteran of the automobile business, I’ve seen this movie before. All it takes is $5 diesel and those things become boat anchors.

DC,

I kept hearing, here mostly, that RVs were scarce, but when I saw more than I could count for 100 miles that made me think otherwise. I don’t think they are warehousing them in the middle of nowhere Louisiana to increase the prices, or maybe they are.

I don’t know about the sales of all the RVs and Trailers. I pass through northern Indiana/Ohio frequently, and see a great number of RVs/Trailers being transported to somewhere.

“In January, the industry shipped more than 45,000 RVs, a 40% increase compared to last January. Companies are expecting to see a record this year even though life is inching towards normalcy.”

All the info is out there, Petunia, if you want to take some time and read it. The bottom line is that RV sales have exploded to the upside, and many, many brands are on backorder. Don’t believe me? Just do some research. I’m not sure what issue you’re having with the data.

I see RVs on lots everywhere, there is no shortage. I was out looking for a fish house and asked about RVs and the dealer said they have increased sales but have plenty of inventory to choose from.

Great comment, Depth. But this is a K recovery. Some of those in RVs are now living in them, others are just worried about vacations. I see RVers living in them where I live, they just quietly park somewhere. On the west coast Canada a lot of Quebec kids out this way squatting out the winter, but then they stay. God knows how they survive? Yet our campground reservation service opened up this last Monday. By Wed the summer was totally booked by tourists.

My son rented out a spot on his property to some RV dwellers. They begged him for this place and against his better judgement he relented. They lasted 18 months then bailed this February, leaving the RV left on site smelling of cigarettes and poverty, sad broken lawn ornaments, and empty bird feeders. Not so easy to get rid of it, let me tell you. Too many cameras around to just tow it away and leave it for the vultures. There is a ‘process’.

I think we’ll rent out the pad to some German tourists we know, after Covid. They pay and don’t smoke.

Have you been to Germany?

Smokers everywhere!

These guys (we know them) don’t smoke. Come here every year and own a RV. :-)

I know. Thanks for your post. We live in an upside down reality.

“A depression isn’t an event where all of a sudden everybody is flush with cash and can buy the most expensive durable goods and hard assets in history.”

I agree heartily with your anger and confusion.

But one (awful) explanation of the pandemic death “boom” is directly tied to the large unemployment “premium” (ditto business forgivable PPP loans – in a harder to explain way).

Basically, a large number of people made more money last year (not working) than they did in 2019 (working) due to DC’s covid unemployment premium.

And that injection of printed disease money resulted in the same outcome that almost any injection of printed money (for any reason) would…a surge in nominal economic activity.

You mention the outright grants. They contributed to the disease boom…but the unemployment premia was the big money I think.

Has anybody on this comment board ever filled out such a survey from the Fed?

I haven’t.

In the back of my mind, I wonder if the survey is even sent out to normal people.

Bobber,

The surveys are not sent out by the Fed but by the Census Bureau for the BLS. Over the years, I have gotten three Census Bureau surveys about versions of this kind of stuff. Two were for my little company, and one was personally.

In my case, they sent me a postcard with a website and a login, and I filled out the survey online.

People are selected by address, randomly. Completion of the survey is “compulsory,” to avoid sampling error. But I don’t know what grievous thing they will do to you if you don’t fill out the survey. Maybe they will send you more postcards?

Wolf, you are a business owner and probably targeted for many forms. That puts you outside the norm.

I’d like to know if any employee wage earners ever answered the BLS survey question “what would your house rent for?” If average people aren’t getting surveyed, the sample is skewed.

If the BLS may is randomly selecting people to survey, many of your readers should have received a survey lately.

Lots of surveys over the years, always the census, and some random others Bobber, but never the ”what would your house rent for” one, and been owning homes and other RE in CA, FL, TN, and AL since the mid 1970s.

In fact, never heard of that question before.

Place the blame on the SUCKERS that buy into this. There are ALWAYS options.

I agree with that. Even though this is the hardest time to figure out how to invest or save, it’s probably the time that people will be richly rewarded if they play it right. Usually buying in this far into asset price rises is not the thing to do.

‘it’s probably the time that people will be richly rewarded if they play it right’

Sounds, great but can you elaborate on it ? thanks

I’d like to hear that too, Old School. I hope you are not thinking “Bitcoin”, though!

Bravo!

Best and sane comment on this issue!

AS long as the # is accepted, it is business as usual for ‘those’ getting benefit of continuation of status quo like Wall ST, Top 10%, Lawmakers who don’t have to increase SS befits++!

The job lose #’s are correct, which you state.

and these numbers are not getting better.

The lies started with the creation of the private European Banking System hundreds of years before America. Around 1917 or something ten or twelve extremely wealthy European, very, very wealthy destroyed this fair nation.

The rotten offspring from these bankers are here among us as perpetrators of most all financial crimes, that honest hard working community people clearly suffer from abundantly on a day to day level.

Yes you do get it. It is not about buying consumer big ticket items, or the mirage of such.

It is the thief’s , the theft by the billionaire class and their lower tier multi- millionaire creating the illusion of empty car lots.

Inflation is not the rising cost of goods, it is the over creation of currency. The endless printing by the money makers for the the central bankers enabling constant financial debt.

The only one lying anymore are the bank debt masters, their corporate crooks and lower tier wannabe lawyers, physicians and the money changing accounts.

Lots of tirades in the comments about bankers, families of very wealthy people, lawyers, politicians, the bureaucracies of capitalism etc. Are we just a bunch of cranky old men, pitchfork peasants egging each other on? Are we creating our own swamp instead providing the pipes to drain the current one? Time to wander out to the shed and fossick around in the shelves, find some pipes or something to fix it.

In Detroit a home sold for $50,000. I was not sure until I checked realtor.com. Probably a high crime city.

The U.S. apartment vacancy rate is 6.5% for Q4 2020. That is up from the 2020 low vacancy rate.

The Federal bonus unemployment money is being tapered. State unemployment systems vary.

Many homes in Detroit proper sell for peanuts…. largely because many of them are quite large, old, in poor repair, with lead water supply lines, and located in blighted areas (not necessarily ghettos, but surrounded by abandoned homes that had fallen into disrepair). If you can tolerate watching a HGTV show, take a gander at “Rehab Addict” who works on exactly those kinds of homes. The condition they are in makes you wonder.

There’s a new movement among the Millennials to purchase run down homes and rehab them. There’s a website following a young woman who bought a home in Wheeling, WV and is restoring it to it’s former glory. I think she bought it for something like $18K. Do a search for Betsy Sweeney. It’s quite interesting to watch her progress. She’s a preservationist who works for the City of Wheeling.

How much would it cost to create a government agency charged with tracking rental prices for single-family homes? They could literally just copy the Case Schiller pairs approach. Pay landlords $30 to send a copy of every new lease to this new agency. >90% participation, no problem.

10 yrs down the line, it would have a 30,000ft2 office in DC, with annual

multi billion dollar budget, run by a political appointment crony, with absolutely no idea about current rent rates.

1) The omerta is broken. FANG tsunami.

2) Gogol TSR is 10^100, but their Retained Earnings have zero momentum. The rest go for buyback and bonuses.

3) The FANG WFH bathe in the sun, walk in the park, jog, play video games, speculate ==> dolce vita.

4) Case Shiller RE CPI is 10.4%, but NYC & SF RE CPI is minus 20%.

5) That’s why we get $1.9T.

6) The liberal empire rule the waves and every choke points.

7) QQQ H&S and NR on the way to 280. After a bear market rally QQQ will plunge to : 240 – 250.

Nice to see you have returned to Wolfstreet, Michael Engel.

Yay, M. Nostradamus is back! And now with “The New Centuries”. Time to get back to translating old French, but what does a deceased Russian (Gogol) have to do with this? And how does it explain “To the Red One will the number of dead be determined”????

The “survey” allows them to report anything they choose.

Only they have the results, only they can “adjust”.

“Lies, damned lies and statistics.”

It’s called propaganda. These sick puppies make North Korea look honest.

Most of these government beaurocrats believe the lies they put out monthly. They are brainwashed. Met one at my breakfast diner the other day from the BLS. He was piping the bogus numbers and lies like they came from God almighty himself. When I tried to point out some of the flaws in the unemployment numbers he starter a rant about Trump, like that had any relevance to the discussion.

Actually it’s Putin’s fault. Or is that meme dead now?

I’ve never understood why “houses are an investment” is sound logic. Why is buying a house an investment but buying a car or a TV or furniture is not an investment?

They say you can rent a house instead of buying – well you can lease a car instead of buying too.

I honestly don’t see any logic here except “if we include home prices then inflation would be very high and we just want to pretend it isn’t high”

Your house and land can be leased/rented. Your personal car, furniture and most other durable goods not so much. There are some fine lines and gray areas in these definitions. BTW – I’ve always cringed when I hear people say “don’t consider your primary house and investment.”

BTW – I’ve always cringed when I hear people say “don’t consider your primary house and investment.”

That is especially true if you can do all your own maintenance and upkeep. A small home (ideally paid for with cash) is easy for one person to maintain.

A paid-for home on land not subject to any taxes is much, much better.

You can absolutely lease a car.

You can absolutely rent furniture.

You can absolutely lease electronics.

The only logic is “well most people buy those things instead of leasing them so common sense says we should have CPI be based on buying them” and that’s absolutely true! But then common sense would also say you should base CPI on buying a home since most people buy a home, not rent it.

The more you think about it the less sense it makes.

A little clarification. I meant buy car, furniture or a TV and “rent it out” as you would buying a house and rent it out.

My sister leased her car to a friend for a year while she traveled. Download a contract for free and make them sign a letter of responsibility. Make leasee show proof of insurance. Contact your insurance company, there’s no reason people cannot do that with cars that are hardly driven.

>“if we include home prices then inflation would be very high and we just want to pretend it isn’t high”

That is the reason. Bankers protect wallst easy money before instead of Average Joe’s Savings account.

CPI-E, which is the FED’s favorite measure, subtracts mortgage payments, food, and energy. For most Americans, mortgage+food+energy = 2/3rds of their budget!

“There’s no consumer inflation as long as we just ignore 2/3rds of things consumers buy”

“Other than that little incident Mrs. Lincoln, how did you enjoy the play?”

Or that comment from a Congresswomen from Minn, that on 911 “somebody did something. “

Son just bought his 2nd house. He’s 37. Rents out the upstairs and lives in suite (basement). He rents out his primary house to my buddy. All expenses are deductions. Rent mostly covers all mortgage payments, taxes, and insurance. (Gave a break to a good tenant). He does his own maint, and/or I help. It will all be paid for by the time he is 55, and in today’s dollars he would be earning 3500/month. Plus, he has the value of his homes as equity.

You can ask for a reduced rent payment in cash, if you are brave. :-)

Pretty sound investment on top of pensions, etc. He’s an industrial electrician.

Basically, if the house is bought in the right market tenant pays the mortgage. landlords are not in the business of charity, but neither are they crooks, (most of them). It’s just math.

My father in law retired at age 47 doing the same thing. He sold all the property and just put it in cash. He’s live in oceanfront for the last 60 years. The process works, but it takes time and sacrifice.

You and your son are the people causing the price distortions.

Indirectly, but in terms of moral fault, the central banks are. Rents are limited to what renters can afford to pay (which is basically wages and government transfer payments). Prices are based on the expected returns on other assets. Without the bond market being destroyed, there wouldn’t be any incentive to bid the prices of houses up.

“Rents are limited to what renters can afford to pay”

Nope. Rents are beyond what people can afford to pay, so now you have 10 people crammed into a 1 bedroom apartment, etc. They’re just as distorted as everything else.

Totally agree but blame the game not the players

I am in San Diego and everyone is a landlord and talks about real estate all the time

Agreed, everyone here in Swampland is gaming the system. Instead of being a place to live a house has turned into a speculative asset class. Gamble on something else, but leave people with a roof over their heads that they can call their own home.

A house is a place to live in. When people start gaming the system to make money off of this without adding any value, (like fixing up an old historical property and selling it for a profit, which adds value) I draw the line. I call this Real Estate speculation. I am not interested in what these people do and I will not lose a single night’s sleep if they all get wiped out.

A house is an investment if you buy to rent it, get the depreciation, and get someone to pay for it for you and get the write off for mortgage interest, maintenance etc. It doesn’t even have to appreciate but if it does that is a gain also.

Even if you break even you are gaining because your tenants are paying for it and if you keep it long enough, the house is actually free. Think about that for a moment

Every landlord I’ve ever known, save for one, has hated it and lost money. Fun fact : I do upgrades, maintenance and repair for them.

In my experience, most people who buy real estate to be landlords don’t know how to do anything. So they run their fancy models and see that their $1,900/rent covers the $1,200 mortgage payment, the $300 taxes, and the $100 insurance, leaving a nice $300/month profit. But they forget that if a sink breaks, they have to pay a plumber $200 to fix it, and there goes most of the profit. And that’s not even considering roof replacements, new water heaters every 10 years, and so on.

I don’t hate it and I know many that don’t hate it either. The last home I bought was in 2010, in the Bay area no less, and it has been two thirds paid for so far by tenants. It has also tripled in value (in large part due to my sweat equity) but even without that it is a great investment.

Regarding repairs. I rent homes that I have gone through and made right in every detail resulting in the absolute minimum of maintenance. I do the work myself (contractor) for a fraction of what it would cost to hire it out because I have the skills.

It is certainly not for everyone, but I know houses and have chosen them as my investments. I know nothing about the stock market and have never owned anything related to it.

If you have to pay to have any work done, pay for management, mortgage it to the hilt then no, a house is not a good investment for you.

@RightNYer, you forgot to mention they love the depreciation expense deduction until it’s time to sell the property and they have to pay taxes on the recapture amount. Bam!

Selling anything that has made a profit has its related costs whether stocks bonds art homes etc. Depreciation recapture is just one of the home-related costs sure.

Again, if you are in the rental game for a short run you lose, but planned correctly and with more of a long-term view, it makes money. And has historically beat inflation as this article shows clearly.

Home price appreciation is the icing on the cake for long-term landlords. Anyone that will criticize such a path without ever actually taking that path is really only a non-credible voice.

I can tell you how silly it is to have your money in the stock market but if you listened to me you would be as big a fool as if I listened to you.

To each his own according to his abilities and skilled tendencies.

Again, if you own it long enough (and manage it properly), it is a free house.

I started buying houses in 2012. By 2016 I owned a dozen properties, mostly 3/2/2 brick veneer standard issue suburban family homes. I was fortunate enough to really understand what I was doing (with the help of friends and others) before I jumped in.

Wife and I did almost everything, no property managers who will put anything with a pulse in your house. Buying right and qualifying tenants is job one. We only had one bad tenant out of about 40 so I think we did ok. We did our own cleaning/rehab because you really cannot find anyone who will do it right (there was this one team but they were always booked weeks in advance, and time is money you cannot let a house sit there when a tenant moves out).

For health reasons we started selling out late in 2019. We were planning one selling the rest over 2020 but when covid hit we decided to get out as soon as possible, and we did. We sold at 2% under market and our houses moved in days.

All told we made mid/upper six figures in profits via rental cash flow and price appreciation. It was a lot of work, and there are pitfalls but if I had started this when I was 40 I would be sitting amazingly pretty today.

My accountant (who was also my friend/mentor’s accountant) told him “no one makes money in real estate”. Well BS. (He is not longer our accountant ::)) It is like every other form of investing, if you do it right you can do well if you jump in without knowing what you are doing you will get properly rogered.

Probably because you need to live somewhere but you don’t need a TV, furniture or, in some cases, a car.

In addition, go buy a new TV and then immediately attempt to sell it “used”….. and see how fast and how much of a haircut you will take. Ditto a car. Furniture is even worse.

However, a house – on a percentage basis – usually will not depreciate at the same rate in the same economic environment (if at all).

You’re comparing liquid assets to an illiquid asset. Totally different.

As pointed out long ago by Karl Denninger, the CPI medical care index is also less than half of what it should be based upon OTHER data indicating the average percentage of household income spent on that.

The CPI is pure BS as pointed out long ago in the great book, Greenspan’s Bubbles. Also pointed out in that book: data manipulated for political reasons (ex., lower the CPI to lower COLA payments) is plugged into simplistic garbage computer models to run the world via artificially setting the price of money. In other words, they use their own manipulated garbage data as if one hand didn’t know what the other was doing… but there’s no way they can’t.

The only data that matters is on the teleprompter. ?

The correct way to evaluate home price increases is to look at a combination of the required down payment and the monthly payment. While nominal prices have increased by over 130% according to the chart above, the monthly payment has increased by much less because the mortgage interest rate has plummeted!

Regarding rents, when I was in Austin, TX last month, I checked out rents for houses. There are a few things going on there I have never seen before. Some rentals, posted on Zillow, charged for rent then wanted the renter to pay the HOA monthly fee as well. Some rentals added the HOA fee and a charge of about 2% for paying through a payment portal they force you to use. None of these fees were listed as base rent. On a $2K rental these fees could easily add a few hundred more to the rent. None of these added fees would be included as rent in the govt survey. More distortions to manipulate the numbers.

They’re included as rent to prospective tenants, so that sort of nonsense doesn’t work.

Great article. Certainly opened my eyes. How about a further article on the CPI wrt substitution. And another article on wage inflation vs productivity.

When rent rises does the landlord’s CPI decrease? Doesn’t that make it a wash? If the price of chicken goes up, because the price of corn goes up, and the price of fuel for the tractor, and money borrowed for seedcorn, all go up, that is inflation. Now that commodity prices are rising we might see some real inflation depending on whether or not the vendors or landlords can pass on their costs. In the case of existing housing there is a tough case proving that aging assets represent cost increases which can be passed on to consumers. If I sell fewer chickens can I charge more? (My rooster is tired). In some government conrolled businesses you can. Under rent control, and supply constraints, the underlying asset becomes worth more. When the cost of renting stocks is zero, the value of stocks goes higher, and dividend income does not increase, while companies put more of that asset value into growth??

How can there be rent inflation when rent is now free, as long as you rent in an expensive area, stop paying your electric bill for a single month, and can write a letter stating “the pandemic sucked for me?” I’m all for helping some folks, but it kind of looks like almost anyone can qualify for free rent as long as they folllow three steps. A millionaire could qualify if they moved to a billionaire location, stopped paying electric, and wrote a letter about how the pandemic sucks???

Per CNBC, how to qualify for the $35 billion initial rent assistance (with another $35 billion predicted to come soon):

Am I eligible?

To qualify, at least one member in your household has to be eligible for unemployment benefits or attest in writing that they’ve lost income or incurred significant expenses due to the pandemic.

You will also need to demonstrate a risk of homelessness, which may include a past due rent or utility notice.

In addition, your income level for 2020 can’t exceed 80% of your area’s median income, though states have been directed to prioritize applicants who fall at 50% or lower, as well as those who’ve been out of work for 90 days or more.

And what if I rent a $100,000 per month mansion? Guess that works for free rent too as there are no “Caps on amount of rent”, just a 12 month cap, for now (of course it will be extended as it would be “cruel” to not give free money out forever once it is started). Rent in Monaco is 510% higher than in the US, wonder if the qualifies as I’d love to rent a place there during the next F1 race…see the point, this program is not well thought out as millionaires could qualify, while it may be too complicated for poor people sign up…

Per CNBC:

How much could I get?

Many of the programs don’t have restrictions on the amount of funds you can receive, Yentel said. Instead, there will be a cap on how many months of rent you can get.

Some programs allow for 12 months of housing payments. Others may offer funding for as many as 18 months of rent.

The money is sent to your landlord. If your landlord refuses to accept the funds, you may be able to get them directly.

“The money is sent to your landlord. If your landlord refuses to accept the funds, you may be able to get them directly.”

It does not take a rocket scientist to see that the Landlord could cut a deal with the tenant, and refuse the free rent, then have the tenant pay 80% of the rent in the cash sent to them from the govt, and then write off 100% of the rent on taxes to make more than 100% of previous rental income. And there will be people from other coutries forging documents and getting free rent, just like the estimated $60 billion of fraud already from the previous stimmi. This is nuts, what would have been better is just send everyone with a pulse, all 330 million Americans, a check for $15,000 as that would have been cheaper than the $5 trillion stimmi sprayed in every direction imaginable…

Could you imagine each and every family of four getting $60,000 in total stimmi? That is how much we have printed, “so far”…

What happens to the real GDP, the one that really counts. Assuming no shady accounting, the GDP deflator should mirror CPI. If CPI is undercounting, the GDP goes from robust to crashing.

I hope they don’t find out Wolf Street have discovered error in their formulas, since they would see it as an opportunity print a lot more.

GDP (GNP?) itself is controversial b/c of controversial INPUTS to draw the real number.

Govt spending ( borrowed from future) is a positive input, even though one in 3 in the country depend upon govt hand out! It has become as fake as inflation#!

Yes, BLS data on CPI is corrupted (is it intentional or NOT, doesn’t matter), but who is going to challege it ? Consumer Protection Bureau?

Apparently there is NO out there interested enough to demand accountability of REGULATORS like BLS, on this stat either by the Congress or the MSM!

Where is the outrage?

Just business as usual!

I guess as long as there is free money heading everyone’s way, no need for outrage. Plus, the gov has figured out that it’s OK to lie to the general public without consequences.

Notice too that the Fed is coloring outside the lines….

Where is the outrage?

Congress benefits from zero interest rates and massive digital minting by the Fed…..and they are supposed to “notice”.

Owners of condos and single family homes buy another residence for household formation, scale up or down at most on four occasions for the median household. The owners equivalent rent ought to be based on that metric and factor in the ancillary expenses associated with maintenance and service expenses as well as capital improvements for the residence.

Rent on the other hand is an ongoing expense. It needs to be based upon data submitted on 1099s by landlords and/or require an annual expense submitted per each household that rents. Social security or TINs can be blanked out to protect confidential info.

Excellent article. You’re doing a great service in calling attention to this issue so widely ignored in the media.

Rents have declined relative to home prices due to declining cap rates … which roughly track interest rates. So ironically one of the same policies the Fed uses to try and raise inflation – interest rate cuts – actually has a depressing effect on the CPI due to this statistical choice. A topsy turvy mess.

And so they keep inflating bubbles, that will eventually crash and cause damage to the economy that is far greater than the benefit enjoyed going up. Great policy.

Here in the UK you can buy a house with a 5% down payment. In other words, your real estate bet is leveraged 20x. Who in his right mind would leverage, say, a stock portfolio 20x? But ordinary people buying a house in this bubble are doing just that!

What a surprise. The government lies. It lies about everything, and it lies all the time. If they are telling you something, they are probably lying to you. The next astounding revelation is going to be that the media lies……

Jdog-…just don’t forget that almost EVERYONE ‘lies’, even unwittingly, usually excusing themselves by professing an oft-imagined end-justifies-means moral or economic high ground masquerading some form of self-dealing (cue Nicholson roaring: “…you want the TRUTH? You CAN’T HANDLE the truth!!!” from Sorkin’s ‘A Few Good Men’).

Or, again, R.A. Heinlein’s: ‘…self-deception is the root of all evil…’, and what is self-deception other than lying to oneself?

We, the people, with all of our miserableness and magnificence put the ‘government’ in place. Paraphrasing Jefferson (all-too-human, brilliant fallen angel though he was): “…in a democracy (okay, ‘democratic republic’), the people get the government they deserve…”.

Or another take from the great Mort Sahl: “…the United States is the WORST country in the world…AFTER all the rest of them…”.

We make it what it is. The process has always been, will always be, too-slow, too-messy, and too-much of the pain-in-the-a** involvement required from the citizenry to make sure ‘government’ stays within the lanes we profess to want to keep it in-perhaps now for too many of us.

Franklin’s ‘if you can’ comment on the completion and ratification of the Constitution looms larger than ever.

Can we? Will we?

may we all find a better day.

Why doesn’t anyone ever read my posts.

Rents for any geographical area are available on line to any Real Estate professional who has user id and password. We’ve been doing this for 30 years. Does that not count for anything?

Many of the posts above are parroting the same garbage that the government puts out about a methodology for determining rents.

SC,

“Creative truth telling” was tradecraft of the intel community.. Now its infected all local, state, and federal [inclusive w/in for & non-profit biz/edu/religious + lobbying] entities.

Thank You for your insight, integrity, and professional knowledge you bring to this venue.

Everything that is going wrong in the country now I saw happening in the Intel Community after 2000. Everything! I experienced it all first hand. When I left 10 years ago to pursue another career I now see the same garbage that I experienced there transferred to the private sector. It’s like I never left.

Hi Wolf.

Do you have any data on what people spend on rent in aggregate?

In the work I do with low income people they usually spend 40-60% of their take home pay on rent. Presumably that % is lower among higher income groups.

But it seems to me the overall weighting of “shelter” in the BLS calculations is far too low.

—Erik