Durable goods inflation +3.3%. Food inflation +3.4%. Services inflation rising, but still held down by battered airline fares, lodging, event tickets, etc. — until people start traveling and going to events again.

By Wolf Richter for WOLF STREET.

The Consumer Price Index rose 1.7% in February from a year earlier, the fastest year-over-year increase in 12 months, picking up speed from the stall in April and May last year. Prices of goods are rising sharply, amid all kinds of shortages of durable goods after stimulus-fed red-hot demand, and food prices are rising too, according to data released by the Bureau of Labor Statistics today.

Price increases for services, the biggie, are held down by the battered discretionary services such as lodging, airline fares, and tickets for sporting and entertainment events, whose sales have collapsed.

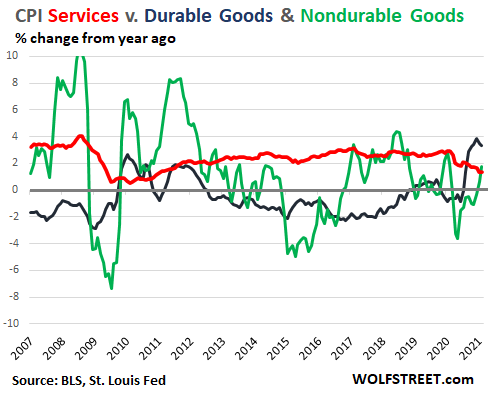

- Durable goods (blue line) account for 10.9% of overall CPI (laptops, new & used cars, appliances, bicycles, etc.)

- Nondurable goods (green line) account for 26.6% of overall CPI (dominated by food and energy). Spiking & collapsing energy prices caused the larges moves of the index.

- Services (red line) account for 62.5% of overall CPI (rent, healthcare services, airline tickets, cellphone services, etc.).

CPI for services (red line) rose 1.4% from a year ago, remaining at the lower end of the Pandemic range. This includes rent, homeowner’s equivalent of rent, healthcare services, insurance, but also airline tickets, and haircuts. Over the past decade, it has increased mostly between 2% and 3% year-over-year, but lost steam during the Pandemic as demand for services related to travel, personal care, events, and other areas plunged. For example:

- CPI airline fares: -25.6%

- CPI hotels, motels, etc.: -17.2%

- CPI admission to sporting events: -14.1%

Services, which dominate spending and CPI, is where inflation pressures will make themselves known because services account for two-thirds of the overall CPI.

Parts of the services economy have been hard-hit by the shift in spending from services to goods. And those sectors have responded by slashing capacity – and some purveyors of these services shut down for good. When this shift reverses, as people revert to buying airline tickets, staying at hotels, taking cruises, attending sporting and entertainment events, etc., this renewed demand will meet slashed capacity, creating price pressures that will feed into services CPI.

CPI for nondurable goods (green line) rose 1.7% from a year ago, the steepest increase in 12 months, after having dropped during the Pandemic amid collapsing prices of gasoline and other fuels. This category is dominated by the volatile prices of food and energy.

But gasoline prices are now rising. In February, the CPI for gasoline was up 1.5% from a year ago. And food prices in February rose 3.6%. This includes prices for food at employee sites and schools, where demand has collapsed, and where prices have plunged 24.5%, though I’m not sure how to track prices accurately when so many establishments of this type are closed.

CPI for durable goods (blue line) rose 3.3% from a year ago, remaining near the peak of the Pandemic price spike, amid reports of shortages, backorders, production delays, and transportation bottlenecks, as no one was prepared for the sudden and blistering demand for durable goods since spring.

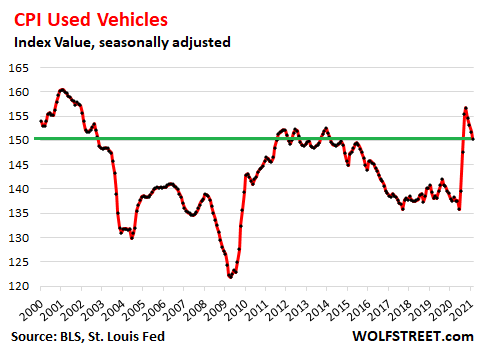

This surge in durable goods CPI includes the historic four-month spike in used vehicle prices, skyrocketing 15% from June through October, but that is now gradually backing off. The used vehicle CPI was still up 9.3% year-over-year.

The price surge in used vehicles was not a result of blistering retail sales – retail sales of used vehicles have been running below year-over-year levels for nearly the entire Pandemic, including in February, according to data from Cox Automotive.

Instead, the price increases are more likely a result of a change in pricing power at the dealer level, which has been documented by the record surging earnings despite flat unit sales at AutoNation, the largest auto dealer group in the US. And consumers are now willing to pay higher prices – those that can afford to buy.

But the method of how CPI is figured makes sure that, even as used vehicles get more expensive every year, the index value of the CPI for used vehicles, after various ups and downs, has actually fallen since the year 2000, thanks largely to the infamous hedonic quality adjustments.

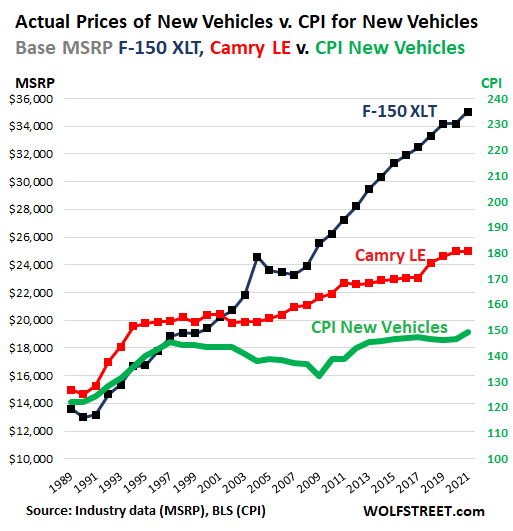

These infamous hedonic quality adjustments are also used to push down the new vehicle CPI, which has been essentially flat since 1997.

The power of these hedonic quality adjustments is demonstrated by my now equally infamous price index that compares the new vehicle CPI (green line) to prices of the F150, best-selling truck in the US, and the Toyota Camry, best-selling car in the US (I discuss the mechanics of these hedonic quality adjustments on new vehicles in detail here):

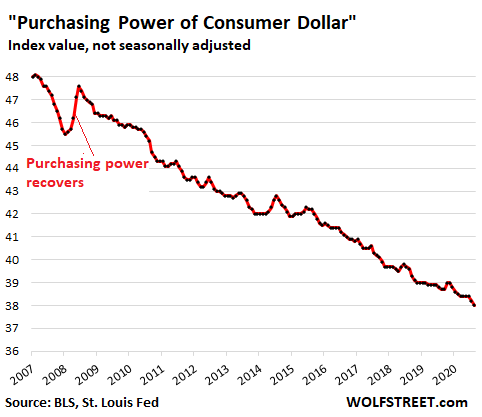

The politically incorrect term for consumer price inflation, which is what CPI tracks, is “loss of purchasing power of the consumer dollar,” and thereby the loss of purchasing power of labor denominated in dollars. And the purchasing power of the consumer dollar has dropped to a new all-time low in February, according to the BLS data today:

And now the Fed wants the dollar to lose purchasing power even faster, and thereby the Fed wants the purchasing power of labor to decline along with it. And by the dynamics now transpiring, it looks like the Fed will get its wishes fulfilled.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This means we’ll all get a big raise from SS;-) Oh sure.

Food is a killer right now for me and I’m one person.

WHERE’S MY GOVT CHECK!

Things are getting expensive!

I just spent my stimi check(that’s in mail)

oops – better get a loan to pay for it then

Yes, the $60-$80 sinhle brown bag (we don’t do plastic ones, courtesy of the econuts in Olympia, WA. – Yay!) ….. Pick any items under a dozen, matters not what combo – and BLAM! pay up suckers … We (FedHeads) knows you gots ta eat to live – absolutely nothing “durable” about that, right? you BANKSTA pea-stealin CONjurers !!!

Hope they all get ground into WALLnut pa($t)e!

Last year’s SS increase (plus) went for the cost increase in Medicare and the increased prices on drugs we need to buy.

All drugs would sell for generic prices without the patents but we’d rather have the drug company CEOs, CFOs, COOs, CMOs, CIOs, CTOs, and all their VPs get rich trading drug stonks.

Rightly said, actual investment in research and development is less then prior decades, some call it technical advancements but the bottom line is the higher paid get raises by cutting costs and monopolizing their product.

My parents who are both in their 90’s have been given probably ten years of added quality life by advances in heart pharmaceuticals. The drugs are now generic and will be so for the next hundred years.

Patents allow for pharmaceutical companies to earn a return on investment like any company on drug development. Pharma company investment has to compete with the rest of the seed corn out there and is not a guaranteed money maker as evidenced by Warren Buffet generally avoiding the sector.

If you don’t have patents then the government has to stump up the money like in vaccines, but the government doesn’t really have any money but must tax it or borrow it or steal it through inflation.

govt needs to NEGOTIATE 1 price for big pharma drugs

in fact if BIG PHARMA takes even $1 from govt for research then AUTOMATIC 50% discount should apply

these prices all over the place are ILLEGAL

same with hospitals – 1 price for everyone

Joe Saba

VA Hospital can negotiate drug prices with Big Pharma but MEDICARE also a Govt institution is explicitly FORBIDDEN to negotiate b/c law enacted by Bush Jr to protect their profits ( for which he received a lot campaign contribution!)

Some how the Medicare either ignorant or (?) to notice this ans should have raised hell nut are silent!? MSM is also complicit in NOT highlighting this!

AS I repeat ” TRUTH is never given but has to be sought”

@ Old school

Drug Companies & Doctors: A Story of Corruption (a well kept secret!)

Please read the investigative article from Ms. Marcia Angel at NY times Jan 15, 2009

(Marcia Angell is a member of the faculty of Global Health and Social Medicine at Harvard Medical School and a former Editor in Chief of The New England Journal of Medicine. (December 2018)

fyi: The Big Pharma spend MORE on Marketing & Ads than on research! Now they are raking it in!

In her 2009 article “Drug Companies & Doctors: A Story of Corruption”, published in The New York Review of Books magazine, Angell wrote :[7]

…Similar conflicts of interest and biases exist in virtually every field of medicine, particularly those that rely heavily on drugs or devices. It is simply no longer possible to believe much of the clinical research that is published, or to rely on the judgment of trusted physicians or authoritative medical guidelines. I take no pleasure in this conclusion, which I reached slowly and reluctantly over my two decades as an editor of The New England Journal of Medicine .

(wikipedia)

MD (ret)

We subsidize the world. I’d recommend that the Government regulate prices, but increase the patent life on the Brand drugs before going generic to basically reward these companies for the innovation. This idea that people and companies should work for scraps is unreasonable.

Regarding the one payer system, I am for this, BUT you cannot allow every illigal immigrant into America and their families to get everything for free. There has to be a balance. Neither the government nor the liberals or conservatives want anything sensible. Also, you cannot have 750 billion a year spent on MIC if you want more spent on yourselves. Lastly, there has the be welfare reform to push people to do work even if part time. I don’t care how unglamorous the job or if considered foolishly racist i.e. working on farms.

So, enjoy your chaos and live with the increases.

People whose jobs in rust belt states have been outsourced by mega-greedy corps now move to NC or CA to pick fruit and lettuce?

Yeah, but motorist carpal tunnel has been virtually eliminated from the ER by power windows, doors, mirrors, seats, trunks, tailgates, etc, and is now only seen in factories, and those, too, are being reduced. So Medicare costs could be worse.

Yup, I refuse to buy crappy dog food. CPI is the Dog Food Index.

Courtesy of zero hedge today :

“The blunt answer is that the Fed, in sync with the fiction writers at the Bureau of Labor Statistics (BLS), reports consumer inflation as honestly as Al Capone reported taxable income…”

Al Capone listed his occupation on his business card as

“Furniture Dealer”

Also think about what some people are doing to protect dollars from inflation such as buying stocks or housing.

Stocks. How much annual earnings do you get for a $100 purchase? About $3.50.

House. How much new house do you get for $200? About 1 Sq ft.

Those are already inflated prices to me.

But, but, if you’re new home comes with, like some cool outside decking, that’s ok.

Becoz that’s so only $50 a square foot with such an awesome hedonic adjustment, dude, bro…

I believe real CPI figures should run at about 10%. I have received invoices and quotes for my locker rental, my car insurance, and even Canada Post shipping, which have all jumped 10% higher than a year ago. Alas, I am not flying anywhere or renting hotels these days, where I could enjoy a discount.

Yes. Housing is 10%. Healthcare…need I say more? Cars.

The Fed wants us to think we spend all our money on food, which is hasn’t gotten around to classifying as in “investment”…yet.

We could allow for the immigration of qualified foreign doctors and dentists which would lower prices but the AMA has a better lobby than you.

Read that drug monopoly costs US $350 billion/yr. Universal single payer healthcare would save us $650 billion/yr says CBO. Obviously a lot of that is in our drug cartels.

What to shrink the deficit?

Support universal single payer healthcare for all Americans.

That would also slash US labor costs to US employers, and help us bring back American jobs exported to other nations…that the smartiest say can’t happen.

Yeah, the CBO is such a reliable source.

Timbers:

You are forgetting all of the hedonic improvements in food, such GMOs, shrinking food packaging sizes, etc.!

Re hedonic improvements:

Have you looked in the yogurt or “milk” sections in the last handful of years? There’s now a variety that perfectly fits you’re lifestyle & pleasure profile.

My BC/BS health ins premiums just went up nearly 10%. Not a word on the fake MSM news. Gas at the pump is up 50% from a year ago. A lot of things haven’t gone up at all. Most of these are things you don’t need or can cut out without much hardship.

Absolutely brutal. Why was I ever prudent?

This is like watching Lance Armstrong or Mark McGuire juice up before an event in front of everyone and win everything, while I stand around with a tri-cycle and wiffle-ball bat.

This is so grossly unfair.

How much do you want for the wiffle-ball bat?

Because you, like all of us here, ain’t in the club.

“Absolutely brutal. Why was I ever prudent?”

Is the tri-cycle a Big Wheel? How many miles on it?

It only needs to have enough mileage to hit smack-dab into a derelick Fedship …

So beware of any and all financially shifty leathery objects – they carry quite a bite!

I think the reality is prudent, responsible people are what makes America work. If you are prudent and responsible you are a resource for the government to help pull the wagon.

It looks like prudent responsible people peaked in the early 60’s with only 5% getting transfer payments. We have been going downhill ever since. How many people can ride in the wagon is still an unknown, but we must be up to about 25% or so.

The prudent are losing. They have been losing for a decade. Now even more so. The back wheels of the wagon are broken and it’s resting on the ground. At the front of the wagon the government expects us to continue straining in the traces. A few folks are beginning to notice, especially some of the kids.

As for responsibility – responsibility appears to be confined to BLM, illegal immigrants, LGBTQ, reparations, climate change, &c, &c.

I think the prudent ones will still win in the end. Just stay the course and don’t do anything stupid. Uncle Sam’s not going to be able to keep this party going indefinitely. These are my thoughts, though I am worried.

The beatings will continue until morale improves.

That last chart is very alarming; the slope looks relentless.

Local 7/16″ waferboard has increased another 10% in the past few weeks, now at $33 for ONE 4×8 sheet, with a limit of 90 sheets per order.

Guess I’ll wait til next year to build a new outhouse. Ha ha.

Scary info and corroborates what all of us know. Fuel costs are exploding here in Canada, even rising in Alberta. Food prices are crazy high and rising. Housing? Climbing big time. Building materials? Ouch.

Remember the 70s and early 80s? Costs skyrocketed. Pissed off labour demanded more money to keep up. We had wage and price controls imposed on us to cool things down and my mortgage rate shot up from around 7% to 18%. When I moved for steadier employment I barely broke even on my house. Sweat equity return was 0….my first house.

This could get really ugly, fast.

This has already gotten ugly real fast.

You know it’s true when a house in Reno costs $500K.

I just bought some lumber for the first time in almost a year and had real sticker shock at checkout.

When do people start recycling wood?So much waste in this country.People have rediscovered old style homebuilding such as adobe.

Note: for the record I do like adobe. But for the sake of argument – that would have us living in mud huts.

I think used lumber is the next big thing.

I seem to remember that you made a bearish bet on the indices some time ago. Are you still in the position? Have you added to it or hedged it?

These posts appearing in nearly every article are really getting irritating. First, Wolf stated in his original post that he would post another follow-up article when he decides to close the short. Second, he has answered this inane question multiple times.

Why do people keep asking questions to hear themselves talk?

I doubt Wolf put 50% of his money short the markets. It is all relative, as a huge percentage loss short could be very little in absolute dollar terms damage relative to investments held. For example, I’m getting crushed on my GOLD investment right now, yet my XOM investment, which was a much larger percentage than my GOLD investment, is up 87% in a couple of short months. VIAC up 268%, DKS up 97%, etc…which ends up pulling my average gain up even with a few huge losers. If you get lucky, like I have recently, a couple of heavy weighted winners will make up for any smaller weighted shorts.

I suspect Wolf won’t be on the streets with a signe that says “Will work for TSLA calls” anytime soon due to shorting the markets…HA Plus I hear the govt is handing out a lot of “free money”, so does anyone go bankrupt anymore…is that even a possible when the printer go Brrrrrrr….=)

Yort and Charles Ponzi,

Both of you are correct: Yes, I still have the short; and yes, it’s just a trade and won’t kill me.

Only an idiot would put all his eggs into one rickety basket on a rock-strewn road. Not happening. If the bet goes sour, it joins the many trades in my life that went sour. If it makes money, it joins the many trades in my life that made money. What made this trade different is that I publicized it when I made it. This gives everyone a well-earned opportunity to take potshots at me.

Sure is a lot easier to brag about winning trades afterwards :-]

No pot-shots. This, after all, is the weirdest market ever.

As I fight off waves of alienation and vertigo, I keep telling myself that “the market can stay crazy longer than you can stay…somewhat less crazy”.

Give it up, older folk on the blog – is this not totally whacking your sanity? All the stuff you learned is bonzo. Wrong. Anti-money-making.

To make money in this market, you have to pull a Costanza: “Whatever I would ordinarily do, I do the opposite! And it works!”

I’ve posted about this before. Yes, its been a bad bet to go against the Fed since the start of the “Greenspan put” era and afterward. I learned my lesson in 2000. The Fed is a previously unknown massively powerful entity now actively engaged in market manipulation. How long it will be able to dominate markets is unknown. But I will no longer “Bet Against the Fed” (and this includes gold). My current and future investment tactics will take this into account.

@Tom Pfotzer

I read at WSJ that the Bank of Japan owns 7% of all shares on the Tokyo Stock Exchange’s first section. The BoJ and the government fund for the country’s pension reserves together own one in every eight shares. Also:

“BOJ has almost always stepped in with afternoon buying when the market suffers a sharp fall in morning trading”

So the Fed still has a long way to go…

Wolf, it was my first time EVER joining the US stock market back in February 2020, and I have hold my short since March 2020. I need a 50% crash on Dow Jones to make up my losses.

I can easily write off my losses with my annual tax return allowance ($1500 per year, as a single person), but I don’t want to surrender. I strongly believe FED will lose when the foreign investors know the US dollar is no longer reliable.

By the way, Wolf, what do you expect about the gold price for the next 1-2 year? I expect it skyrocketing after Biden signs the 1.9 trillion COVID relief bill.

If I expect something to “skyrocket,” it’s surely not going to skyrocket :-]

Tom wrote: “All the stuff you learned is bonzo. Wrong.”

I figured out 50 years ago in high school that pretty much everything we learned in school is a lie. Still took a few decades as a computer consultant to understand the depth of the corruption, after seeing it up close and personal.

Now even the bondo has fallen out of the rust holes and anyone with eyes can see we are being towed to the car crusher. Time to find something to trade to the Amish for a horse and buggy?

I think with the last two stages of stimulus the housing market and the stock market is in the ‘fear of missing out’ stage. Just saw where past four months was highest money flowing into stocks ever right as it’s making new highs. Housing up 14% year over year.

Consumers can control this Stop Buying get food only on sale water instead of soda and healthier what fed is really trying to do is inflate assets to increase tax base my real estate taxes increased 3200 4600 in 5 years build the gallows

If everyone started an edible garden, the gov would tax that.

Perhaps not the garden. But some places try to tax the rain you “divert” to water that garden.

As a percentage of median pay:

1989 F150 – 47%

2020 F150 – 68%

1989 Camry – 49%

2020 Camry – 50%

In other words, it takes 45% more labor today to buy a new F150 than it took in 1989. Nothing to see here, folks. Just move on.

Couple that 45% more with 84 month loans and it’s a no brainer!

I have family members for whom that deal might actually save them money. One of them criticized me for driving the same 1986 Ford Bronco for 18 years… even paying a couple grand to put a new engine in it about 2/3 of the way. He replaced his white pickup truck every five years as soon as it was paid off… with another white pickup truck.

And to this day he thinks that I am the crazy one.

SpencerG, staying alive is everything. I would be scared if I crashed riding in an 86 vehicle. A big payment is worth it if you or your family survive a crash in a new vehicle. An old vehicle can be deadly because of safety advances it does not have.

Plus, I just bought gas in Wisconsin (7 Mi.) for $.50 a gallon less in Wi. than Il., and lake County Illinois where I live just passed an 8 cent per gallon tax hike. Taxes are ridiculous already and going up.

Illinois taxes have always been ridiculous.

Hey Ted,used to live a couple miles from border of Cook and Lake County.Dont you love all the IL. Taxes?IL. Has been experiencing mass exodus orecovd due to never-ending taxes among other things.IL. Rep. Just proposed illegal bill wanting to acquire police powers of arressting,detaining,and other nonsense with or without due process as he says,think Tavers is the name,Yay!! :-)

Gig workers are going to see some inflation in their taxes, yet airports get $8 billion in free infrastructure grants to “improve” their facilities…wowza The latest stimulus bill had a lot of non-stimulus “stuff” if you are “lucky” enough to have a gig, tucked away in the fine print, such as per Bloomberg below:

Business Taxes

Companies that work with “third-party” gig workers will be required to report more transactions to the IRS, likely resulting in more taxes paid by ride-share drivers and food delivery contractors. Under current law, companies don’t have to report transactions to the IRS unless a contractor is paid more than $20,000 and is a result of 200 or more transactions. The bill would lower that amount to $600, no matter the number of transactions.

I like the tax change. It let’s a lot of unpaid taxes from slipping thru fingers. Many subs work for cash, or under the table, now it’s like getting a 1099 for anything above $600.

Yort,

This is wrong. Completely bogus information. Companies are suppose to report anything over $600 right now. Not all of them do it, thank God. I’ve got 20 years of data to back up what I’m saying.

To vendors, yes, but supposedly this change is to PayPal and Etsy and facilitators like that. I don’t know the details, however.

You work hard, save some money, pay your taxes and there comes Chairman Powell to chip away at what is left.

How did it come to this?

Who gave this guy authority to steal my hard labor?

The same people You, I, and everyone else VOTED FOR, to FIX what ails us!

Well, they fixed it alright …all for THEMSELVES!

Just sit on your arse and eat popcorn, drink beer then take a knee. Rome 2.0.

Got dang the Purchasing Power of the Consumer Dollar in U.S. City Average is a sad sight to behold.

No wonder it’s so easy to move down in the world.

Meanwhile China is tightening credit. Cost of imported US goods could rise. The upswing in commodities means even locally sourced materials like lumber are more expensive. Copper is $4??

I recall copper near $4 a while back and I was working oil & gas projects then. Thieves were stealing copper cabling on deep submersible well pumps and cutting that very large diameter cable LIVE with 440 volts on it. Scary.

I recall a guy who was trying to cut power line cable in a field and got electrocuted while on his ladder cutting the cable (in the dark, no less). We found him on the ground in the morning and he was “toasted”.

Yeah… my area was having trouble with people getting electrocuted in power substations while trying to steal copper cables. It sort of corresponded with the meth epidemic that the South started having in the early 2000s.

Just ordered some toner for my laser printers. Got the box and opened it up. All of it was made in China. Need I say more. Can’t we make anything in the USA anymore!?

Nope. When I saw that the U.S. flags for sale in the gift shop at Monticello (Jefferson’s house in Charlottesville) were made in China, I knew that America had jumped the shark.

Even the some of the MAGA hats were made in China.

Let us start today.Many co.s will refill or refurbish cartridges.Everyone learn to tinker,hack,blacksmith,do coldframing,etc.Old school days,if you didnt have the regular thing you would create an alternative or work the problem to resolution.Everything does not need to come from a store or China.

I didn’t have Wolf’s courage to short the market, so I put 50% of my savings into European banks in September-October last year. At the time everyone hated them, despite the fact that they were making money. They’re up between 25 and 35 % since then and look set to increase even more with the coming inflation.

If slr waiver, whether extended or not, doesn’t come back to bite them or others.

The smartest money people I read say the Fed is on an extremely narrow path and can fall off either with inflation or deflation. Got to be positioned to survive either. One difficulty with shorting is the stock market is an asset that can compound by a factor of 10 in a couple of decades, so it can be devasting if you get trapped.

I am biased that stock market is worth 1200 or so but in reality if rates stay at zero for 10 more years who knows high it could go.

How can you position for both? It seems like a one or the other situation.

I think they try barbell strategy. Deflation end cash and treasuries. Inflation end real estate and precious metals. Maybe commodities.

”theoretically” rnyr, it would seem either cash on one side and housing on the other,,, OR, gold on one side and ”financial asset” of some sort on the other…

In reality IMHO, all of those are now SO subject to massive manipulation by various actors that we now are pretty clear are NOT acting in the interests of WE the Peedons who are careful and prudent and have spent our working lives building up savings, and have no debts, etc.

If I were in my 20s again, and knew that this horrible GUV MINT sanctioned theft was going to happen, for sure I would have done a lot differently than I did. Staying in the US Navy as a career for one, but there are many other such choices that were available to ensure a more secure old age that I did not choose, certainly similar to many folks who chose to continue to smoke and do other equally harmful activities.

I am going to be OK, but only because I am a short timer by any reasonable metric, and can stop any and all purchasing of items not really needed, looking at you ”liquidity”,,, no matter how much I might want them.

The freeze in Texas wiped out the vegetable crop in the ground. The price of blue jeans has not changed much since the 70’s. Bananas are cheap. The price of a bathroom renovation is expensive. I read a hospital was sold for $1.00. Another mall operator filed for bankruptcy.

At $1, even the price of jingle mail has gone up!

So you’re getting new 501 stove pipe Levi’s made in the United States and overdyed for $9.99 these days…what the hell planet are you living on? Are they still going to discos?

A little over a year ago when the repo market failed and the Fed stepped in and ramped up asset purchases I said get the heck out of cash because the Fed just crossed the Rubicon and they are never going back. I said buy the S&P 500 index, buy desirable real estate, even buy some gold. We now have QE Eternity AND direct payments to people. It may take a decade or more before get a spectacular crash-up (assets to the moon, dollar to the basement). This is not a drill. Now don’t go plow it all in at once. Keep calm and build up your investments in assets over time. It is easier that way. The pandemic was a great opportunity that just happened to come along at the right time. Some other calamity will happen and you’ll have a great opportunity again. Meantime, a little this week, a little next week, and so on. If the Fed still measured inflation like they did in 1980 it would look way worse than Wolfe’s charts. There is an awful cost of doing nothing.

I think this is more a reflection of what the Fed WANTS you to think than the power it actually has.

I still wouldn’t buy any stocks at current prices.

Yep. I know it’s more complicated than this, but here are three numbers to show how scary things are with asset inflation.

Paper assets $525 trillionillion

Real GDP 84 trillion

Estimate of corporate profits assuming 7% of GDP = $6 Trillion

That’s a lot of financial assets riding on $6 Trillion of profits. No wonder we are stuck at ZIRP.

Exactly. Enough people believe the Fed is all powerful and can backstop any market, it becomes a self-fulfilling prophecy for a while, as private investors jump in to buy.

But the Fed wasn’t able to stop the collapse in February and March of 2020, and at this point, it is out of “tools,” no matter the protestations of Powell. What will it do for the next collapse?

I am curious how much of the $1.9 Trillion stimulus just passed will actually end up causing inflation. Paying off debts of people will only result in savings of a few hundred a month over 10-20 years. For example, the stimuls gives minority farmers $4 billion to pay off their UDSA loans, up to 120% (to pay for any forgiveness income taxes), for any minority regardless of income, assets, net wealth, etc. Yet that $4 billion is not going to hit the economy all at once, it will be a few hundred dollars for a few thousand people over the course of 10 or more years. That is not the same as sending $4 billion to minority farmers bank accounts to spend as wanted, which could lead to inflation.

And as a second example, giving the states $350 billion could end up just paying for pension obligations and bond debt, again not going to all be sent to consumers or spend of police robot dogs and street tanks, etc.

I’m starting to second guess long term high inflation because of the $5 trillion in stimuls printed in the last 12 months. Sure inflation will spike over the next few months, but unless the stimulus becomes a universal basic income (UBI), it will slow down and stop someday, and then inflation will by nature moderate lower. The question becomes will it ever stop, as once you give out something free via govt, the voters tend to want it forever. It will take an unsolvable unintended consequence to stop the forever stimmi, QE, financial repression, etc. It could be as simple as too good to be true can’t last forever…and I suspect the hang-over will be somewhat painful at some point in the future…

My stimulus check is going out as soon as it comes in. The inflationary boost will be in the same month. End of story.

If the govt really wanted inflation, they would boost SS to above the poverty line for the lowest beneficiaries and give everybody else a real CPI increase. All that money would go back into the economy every month. The average SS payment is under $600 a month, which barely supports living in a tent.

FYI – From the very beginning SS was there to supplement your retirement savings, not be your retirement savings. However, the inflation adjustments to SS payments has been pitiful ever since Slick Willy Clinton and his gang changed the way it is calculated in order to “save” the system.

“retirement savings”

All it takes is one serious illness to devastate savings. If the illness is chronic and makes employment impossible, Social Security is all that is left. *IF* the person can get past the gatekeepers.

An illness wrecked my health. Society’s response wrecked my life. In the US, being sick for longer than a week is a Crime Against Capitalism. The punishment is brutal.

Petunia, “average social security check” for retirees is $1543/mo according to https://www.fool.com/retirement/2020/10/31/the-average-social-security-benefit-for-retirees-s/

The number I saw was for everybody including SSI. In any case, I won’t be getting anything close to the average anyway.

According to AARP, the current (Jan2021) average SS is $1,543 per month Pet, and I just checked to confirm.

M.I.L. is getting $6xx at age 90, but is OK due to savings and dutiful children keeping her at her home, etc.

My grandpa went back to work for a couple of years in the ’50s to get $100 per month, and did his best to live on that, by building and living on a sailboat, on the hook in Bahamas, eating a lot of fish, etc. Just to show us it could be done in style. Gave it up after 15 years at his mid 80s and went to the Rockies for his end game. He did appreciate us bringing him a very large sirloin when we visited!

My SS is definitely NOT keeping up with inflation in the last 10 years or so.

I’m not even planning financially on SS checks when I retire.

Glad to hear of a well-treated oldie! :-)

You’re right to second guess inflation. There is also the issue of structural inequality. I can’t speak for the USA, but in the UK there are estimates that about 50% of the stimulus money has just gone into paying rents.

Effectively the money flows up, and is eventually used to buy the same bonds that were issued to fund it. The net result is that asset owners suffer no losses, and have converted their private debts (due to the stuffed real economy) into taxpayer backed debt.

Pretty good deal for them, but this balance sheet process will not create broad inflation because the ~10% who are asset owners have enough food and clothing already.

There is also the drum of austerity being beaten again. UK has already announced tax rises for middle earners (basically the only people who have any spare money) and this will create quite a lot of deflationary pressure.

So across the work force you have deflationary pressure on disposable income, and the stimulus going to an ever shrinking cohort of wealthy asset owners. I do not see this as a recipe for inflation.

Now if Biden used QE money to fund a UBI, then yes, I think we would see inflation. But I really don’t see that as politically viable right now.

Friedman’s helicopter scenario assumed that those who collected the money actually got to keep it. The reality is that many workers are nothing more than serfs on the land and must remit any helicopter money they find to the lords of the manor.

Exactly. In the US April 15 is fast approaching. Simply endorse your stimulus check over to the IRS.

I suspect that the 1.9 T is exceeded by the loss in the value of commercial RE: incl malls and office towers. Not counting the loss of businesses.

There seems to be an equation out there that:

(Bail out due to Covid) is greater than (economic hit from Covid). I.e., it was a net bonus. A biological version of the old ‘let’s break windows to create jobs and raise GDP’. Speaking of GDP: all the money spent on PPE, the vaccines, the medical bills: all raise GDP.

So things are great! In fact once we get on top of this Covid 19, we’ll need more to keep the expansion rolling. Fortunately they seem to be in the works.

As for the Fed: if it is going to reward ‘irrational exuberance’ it is no longer irrational.

I don’t think it’s that hard. Fed has been playing games with money especially since Nixon took us off the gold standard. It allowed USA to soft default at the time.

Taking real metals out of coins was a treasury debasement of real money. NIRP is a soft default if they do it long enough. CPI manipulation is another game. Running huge deficits is another. It’s just the opposite of sound money and you can clearly see.the distortions in asset prices and the economy.

Too much of the phony money ends up with the already rich. Maybe the current plan is to shovel as much free stuff out of Congress to try to offset wealth affect of 20 years of Fed policy.

Well thought out, and as Wolf has posted consumer credit debt is lower since the relief dollars. People may be committed to lower debt and consuming less.

I’m not even planning financially on SS checks when I retire.

Probably like about all big government money drops it will cause short term bump up in everything, but screw up mid and long term as imbalances become larger.

Central bankers are not making the same mistake of dealing with crash of 1929, but they probably are making a different one just as big. We are a wealthier country now so they have a long runmay for screwing up. I suspect the biggest mistake will be that the Fed encouraged the everything bubble. Looks good, but let’s see if they walk away from landing the plane.

AS long as the Fed keep repeating:

There is NO bubble!

There is NO inflation!

rest of us doesn’t matter!

I have to wonder if the BLS includes the value of the USD in it’s CPI basket of goods as part of it’s permanent hedonic adjustments?

Ima thinking: basically all the printing ends up in some billionaire’s pocket, if not immediately, then in a month or two. And with no one in the deplorable 90 percent with cash to burn, what is there to drive deflation of the currency? Isn’t it possible prices will fall through the floor?

Good comments so far!

Check out the steel market right now. We are getting slammed by increases and shortages on most material inputs but steel is the worst so far. I don’t know how long it will hold this high but this run has already outlasted most early predictions.

Thanks for this report RG8.

Been out of the rebar and ”red iron” markets a few years now, but remember well those markets when estimating construction in the early oughts.

For a huge project requiring a couple hundred tons of rebar, all the quotes we received said in large caps, ”This quote is good for 24 hours.”

Maybe going to happen again?

Likely another commodity that can no longer be made in USA due to environmental concerns, similar to aluminum, so will be at the mercy of foreign sources who may collude for strategic reasons as well as economic reasons, since they have no need to comply with any such USA rules and concerns.

“When I use a word,” Humpty Dumpty said in rather a scornful tone, “it means just what I choose it to mean — neither more nor less.”

Pretty much describes the CPI and BLS statistics.

All you people bitching about inflation have only yourselves to blame. Inflation could not exist in a world where people only purchased what they could afford with the money in their pockets.

Inflation comes from consumers purchasing with credit. Period.

It comes from people living above their income using credit to fill the gap.

People want to believe they are wealthy and that they can afford to take lavish vacations and drive new cars and pay stupid amounts to eat out.

Average consumer debt is $92K without their mortgage!

We are the land of the stupid, greedy, consumer, and we deserve inflation and the poverty that will eventually come from it….

What about people who never buy on credit and save? No right to complain about being shafted?

Lots of folks on this forum eschew debt.

That’s right P,,, we have NO debt , including NO mortgage on our home base,,, but we are still getting ”shafted” with rises almost every month in various and sundry necessities or requirements from local and state GUV MINT.

OTOH, we have lived up to recently in a fly over state in a county where any politician or elected official who voted for or even proposed increasing any tax was voted out of office at the next election as should be done every time.

”CLEAN HOUSE, SENATE TOO,” until we have 100% folks who actually work FOR We the Peedons, instead of FOR corporations.

If you reject the use credit, you are such a small minority that your actions have no impact on the overall issue, although it does impact your personal situation. Complaining is a waste of energy. The only thing that will change the inflationary environment is a collapse in the economy.

We are witnessing consumer inflation simultaneous to mass unemployment. This is not sustainable, and the result will be ugly.

Being free of debt is one way to be prepared for what is coming, but it is not enough.

Yeah, I’m debt free except a moderate mortgage at record low rate. Definitely not picking up any more debt. Otherwise, my attitude is shifting from basic prepping to moderate prepping.

My gut feeling is that this is not yet the “big one”. The fed/govt will probably manage to put out this fire, but the tinder keeps building.

Don’t blame just the people.

The government has a lot of blame for this inflation. Printing money, monitizing the Fed deficit is just one major cause. The other, as I posted before is the 2017 tax bill, which distorted the housing market creating an artificial shortage of houses for sale. People who move often keep their previous home as a rental income property. What better investment with 1% or lower risk free interest rates. We are seeing a lot of empty homes where the owner is refinancing! Because of the 2017 tax bill a lot of the tax advantages of owning a home cannot be grandfathered in and are lost once the home is sold. All these contribute to a shortage of homes available on the market and hence much higher prices as well as rents.

I’ve found the opposite, that the non deductibility of full SALT decreased home prices (at least until the May 2020 surge).

That hasn’t happened here. The factors I listed above offset the lack of SALT deductability. Prices are still going up.

Monetizing the debt does not contribute to consumer inflation. It simply effects the asset values and interest of the assets the Fed purchases.

Other government policies which encourage consumer debt, do have a big impact however.

Wow! You can’t go stating the truth like that nowadays you’ll get de-platformed.

Only also add that Govt spends more and borrows more than the people do. When J M Keynes was asked by a cynic what happens in the long run? He gave a typical smart–s Oxbridge reply that, in the long run, we are all dead, but what he really meant was that his generation was dead and the problem was offloaded to the next gen which is smart but not moral.

Got to love ‘hedonic’ adjustment. Is that why I can’t get a simple car without a mobile office and all the other BS anymore? Maybe it should be ‘hedonistic’ adjustment.

Weak $ makes american goods more competitive on the world market. That’s a boost for the US Economy. Oil goes up, XOM can use a break after a devastating year.

US Farmers planting new record of corn and soy beans. Weaker $ will create huge foreign demand. Like Canadians buying american properties in 2011. Dollar also was weak back then.

Let’s not forget, there is two sides to every transaction.

Drunk Gambler,

You’re talking about exchange rates not inflation. Inflation makes US goods more expensive overseas because they cost more in US dollars.

But yes, inflation means companies are able to raise prices, which is good for companies and bad for consumers.

But we barely make anything. Having our assets like real estate more desirable to foreigners is NOT a good thing.

We have to be able to feed our cheap labor force…..china.

Well thought out, and as Wolf has posted consumer credit debt is lower since the relief dollars. People may be committed to lower debt and consuming less.

Food prices are remaining pretty stable here in Thailand. Still able to get a tasty decent quality Pad Thai w/shrimp dinner for about $2 in the local restaurants.

There is the Mercedes or BMW driving upper class, but most people maintain a thrifty lifestyle which keeps inflation down.

Yup, same in Indonesia.

$ still strong here.

Oh, you make me miss Thailand so much. I was teaching in a small northern village back in the aughts. Not much to spend money on and that was fine. Splurged occasionally in Chiangmai. I don’t want to romanticize the poverty and corrupt government but there were fewer people living in the streets than there are here in my northern California town.

If Americans spend these latest $1.9 trillion dollars as surveyed by Bloomberg below, inflation might not pick up as much and as long as many predict. Savings (much higher than last stimulus rounds), food, house payments, seems like they people are replacing lost income, versus stimulus for “pent-up-demand”. Are consumers getting wiser and looking at longer term horizons now? Kudos if so…

Per Bloomberg today:

Spending, Saving

About one-third of Americans plan to save their check, according to a survey by Morning Consult commissioned by Bloomberg News, much higher than the prior stimulus money. Around the same share said they’d purchase food, and one-quarter cited housing payments.

My daughter and her husband are going to save this stim check.

I’m going to use mine to pay 1/3 the cost of the upcoming dental work I need that Medicare won’t cover. For all not on Medicare yet: from the neck up, Medicare doesn’t cover (glasses, contacts, eye exams, dental work, dental surgery, hearing aids, etc.)

Brain surgery is covered, but by that time, the brain is not working very well anyway.

It’s shocking that Medicare doesn’t cover the very things that old people suffer from. Hearing loss is associated with the onset of dementia, dental problems interfere with chewing nutrient-dense high-fiber foods and cause serious infections if left untreated. There are deductibles and only partial coverage for everything but hospitalization. It’s basically catastrophic level insurance which I had when young and under-employed. Cost about the same.

I put mine in GameStop.

Yort, that 1.9 trillion does not all go to stimulus checks. Don’t forget that. I look and look and can’t find the total cost of the direct checks. Almost like they don’t want to report that part…

The $1,400 payments cost around $422 billion. The previous $600 payments cost around $174 billion. The costs are not linear in nature as different amounts and type of people qualify for the $1,400 vs $600.

For example a family gets the full amount $1,400 per person up to $150,000 AGI (adjusted gross income). Between $150,000 to $160,000 the amount goest from “full amount” to “absolute zero” (drops off about 14-17 million people versus previous stimmi). The $600 previous stimmi “STARTED” to taper off at at $150,000 yet it had no “true” hard upper income limit, depending on how many dozens or hundreds or thousands of kids you might theoretically have in your family (thousands possible for Bezos to adopt..maybe millions…HA). A family would lose $100 in stimulus for every $1,000 in AGI above the $150,000 AGI income limit.

Now what the media made into a stimmi envy circus was constant articles stating that people making $300,000 qualified for stimulus. While “possible yet not probable”, it is both rare and difficult as a family would literally need a herd of kids in their house to both make $300,000 and get “ANY” stimulus at $600 per person. So even if you have 23 kids, and two parents, then add that 25x$600=$15,000 stimmi…yet if you do the math you still get zero stimmi, with 23 kids if you make exactly $300,000 of AGI income —>($150,000 cuttoff + $25x$600x$10 = $300,000 income is stimmi cuttoff for 23 kids and 2 parents)

There is a reason they do not “do the math” when writing MSM articles about how the rich $300,000 income families getting stimmi. Fear sells, math not so much. In order to keep the population distracted, those in power need each income, wealth, race, etc groups to be distracted and in social conflict at all times. That way, nobody has the time to pay attention to those who really do the most damage to society, so they enjoy the life that 99.99% could only dream about.

The more you consume, the more you are impacted by inflation, and the more harm you do to the environment. Take jobs or walks. Lay on the beach. Play cards or board games. Read. Chat at the coffee house. Watch movies. Go camping. Thrift shop. Downsize. Watch high school sports or playground sports. Better yet, play sports. Farmers market. Public education. Public transportation. Public libraries. And much more. All for free or low cost. Don’t worry what the masses are doing. The masses aren’t happy.

Durable line looks black on my system. Or is it just really dark blue? Thank you for a super site.

Dark blue. But your screen determines what it looks like to you.

Once this inflation starts to kick in with a vengence as a result of all this fake money printing, I can see these brain dead morons that are now running our country instituting across the board wage and price controls, just like Nixon, Burns and his Treasury Sec did in 1971. This will lead to shortages and long lines everywhere. You can take this prediction and put it in the bank.

SWAMP

yep.

But those working for the government will get COLAs …so from Yellen and Powell down to the postal worker, all taken care of. But what of us?

What we have here is inflation pushed upon us by those who are insulated from its ill effects due to govt employment.

What we have here is a TAX being laid upon us by those who have no right to tax.

What we have here is a Congress who loves the free cost of borrowing so they can spend and spend and buy votes and fund pet projects.

“A democracy cannot exist as a permanent form of government. It can only exist until the voters discover that they can vote themselves largesse from the public treasury. From that moment on, the majority always votes for the candidates promising the most benefits from the public treasury with the result that a democracy always collapses over loose fiscal policy, always followed by a dictatorship. The average age of the world’s greatest civilizations has been 200 years.” De Toqueville

I used to have bumper sticker on my car which read

“Minimum wage for Congress”

While I was driving over the George Washington Bridge over the Hudson River NYC, stuck in slow traffic, I was getting high five’s from nearly every motorist and trucker that passed me.

Wasn’t said/written by de Toqueville, or Alexander Tyler.

How about I went to buy a work truck with cash from capital gain on house sale, and dealer wanted to penalize me $1500 for paying cash. For best price you need to finance with us with at least 4 payments, then you can pay off. What kind of bizarro world is this??

Not too mention finding an actual work truck with 8ft bed was tough enough….

Now you’re Armageddon-it Dave. No more briefcase full of blues or greens. No doubt the “pay off” would require that transfer in electro-credits or check. Everything happening makes total sense when you realize they are just trying to kill off your privacy by killing the money. The future United Wards of the States. A tool stops being a tool when you whack your head with the business end.

Saw something on one of the public car retailers that they made just over $2000 profit on the car sale and just over $2000 on the financing for a total of about $4500 or close to 10% of sale price. So they were trying to get both pieces out of you. Welcome to a financialized economy.

You never tell a dealer you are paying cash until after the contract is signed. They always assume you are going to finance, and it is priceless to see the pissed off look on their faces when you whip out your checkbook and begin writing the check…..

Yeah, but often they’ll say “How much do you want to pay per month” and when you tell them “Let’s negotiate the price, not the payment,” they’ll figure it out.

The last time I bought a car from a dealer and wrote a check, the people I was working with, were not sure how to do it, as if they had never had anyone pay cash before. It was kind of amusing..

The local Honda dealer here in Bethesda MD, assumes that anyone paying cash for a car is a drug dealer laundering money. This actually happened a few years back and they were severely prosecuted and fined.

Been like that for a while DK,

Was going to pay cash for a new pick up in 07, but was offered $500 if I financed it for three months, which I did, then paid it off.

Similar offers the last couple of new trucks, including the ”Classic” Ram 1500 regular cab 4×4 w 8′ bed that I use to drive across USA to see family and friends all the way across, then camp in the outback for a couple of weeks,,, usually at least partly in the top of the Rockies still in snow in June, sometimes even July.

Greatly missed that trip last year due to the virus event making the social situation so sketchy many places, but still hoping for this year.

So government workers get a COLA…..

and money for “relief” when they didnt miss a paycheck.

The working families of this nation will be pounded and ground down by this inflation…..and the govt worker will be okay. Thus the bifurcation of a nation.

CPI up .4% in a month…..6 month Treasuries yield .01%.

And why is the Fed buying $120 billion a month of treasuries?

So, is having to resume mortgage payments going to make a dent in home prices? Housing seems out of whack for more reasons than one.

All this currency debasement is not just bad policy. I feel it is immoral too. It’s nice to have a (flawed) economic model to base your policy on, but they are destroying people’s savings. That is money that people have worked for all their life.

Why does nobody ever highlight the moral angle in this?

Because they’re sociopaths. They’re born without consciences. There is no “moral” to them.

It really is insidious. Not much different than someone sticking you up at the ATM. At least with tax hikes things are explained. This is just trickery.

Tax hikes, unfortunately, are often trickery too.

I fight for awareness at the local level because this is where your vote actually matters.

Take public school laws in Missouri as an example:

1) Debt service levies.

A school district has a cap on how much it can levy (i.e. tax people’s real estate) without having to go to the ballot – which costs money and sometimes social standing. The higher the levy a school wants above the cap, the higher majority it needs (e.g., starts at 50%+, then 55%, 60%, etc.). BUT the debt service levy gets around this obstacle.

If a school takes on debt, it can go to the ballot and ask voters for a “debt service levy”, which only requires a 50%+ majority. Once approved this extra levy can be assessed ON TOP of the normal cap, so for instance if the normal 50%+ cap was a 4% levy, the debt service could allow an extra 1.5% levy for a total of 5.5%, which normally would have required a much higher majority at the ballot of 66%+ of the votes, but in this case only required 50%+. (Numbers are hypothetical)

Even worse, voters are given the impression that a debt service levy is temporary, since the debt service levy revenue only goes to paying off the debt. In reality, the school makes the debt service levy permanent by making darn sure that it always takes on new debt before the old debt expires.

One can hardly blame the school with such a perverse incentive.

The law basically says, “If you want more tax revenue, go into debt, give a cut to the banks, and the voters won’t know what hit them.”

The district of which I am a board member pays out $1 million in interest per year to banks, not education. That’s pure tax dollar waste that accounts for about 2.25% of our budget.

Try explaining even a quarter of this to a layperson before their eyes glaze over.

2) Bond Issues.

The normal person doesn’t know what a bond is. There is a member of our Board – a very successful small business owner – who has recently admitted he doesn’t understand bonds, and he voted to have the district put a bond issue on the ballot four years ago!

School districts are seen as prime targets by certain architectural firms, however, precisely because nobody understands bonds. They come to schools saying, “We will manage a campaign to get your bond issue passed, you’ll need to borrow, oh, $12 million, just makes sure all the work comes our way.”

Then, as promised, they “frame the message” for voters with that infamous slogan, “No Tax Increase”. While this is technically true, it is the height disingenuity. Voters think that the bond issue is somehow “free money”, like a grant. They don’t realize that it’s borrowed and the interest gets paid out of their pocket.

The reality is, if the bond issue gets passed, the school takes on new debt, so it can keep the debt service levy in place for another 10 or 20 years. And when that debt comes close to maturity, they pass another bond issue. And so on.

If the bond issue didn’t pass, the debt would mature and the levy would have to go back down to the normal cap. So, a more honest slogan would read, “No Tax Increase, But No Tax Decrease Either.”

Again, try explaining this to voters in 5 minutes without gross oversimplification.

The thing schools should teach but don’t (yet, I am trying!) is practical financial literacy and practical civics. They teach broad theory at best in both areas.

3) The Missouri Proposition C Rollback Waiver.

Okay, I should stop before this post goes on forever, but suffice to say that the Prop C waiver “tax” is a legal Frankenstein’s monster resulting from two sets of legislation separated by ten years and a lot of hocus pocus.

Anyway, look into your local taxing bodies and you might be surprised at what you uncover. I didn’t until I was 30, which was twelve years of voting in ignorance that I regret.

When I moved to California in the 1980’s……we have Prop 13, MEANS LOW TAXES. OK, we buy house for $200,000….prop tax is $2,400/year. (sounds great!)

Get tax bill…… Prop Tax = $2,400, repayment of issued city redevelopment BONDS = $2,700!! Yep, pay low property taxes but I pay for the bonds too!

Thanks MJ for the detailed comment. Very, very much appreciated.

YuShan

Morals, Ehics or scruples is NOT part of teaching in Economics, Finance, Wall St brokerages or in MBA curriculum!

Its because there is no morality left in this country. Its every man for himself. Or to paraphrase what a worker in a factory told me on my first job:

Its “Hurray for me and f… you. ”

If you can create a little circle of virtue and sanity in your life your are doing good.

I won’t contribute to this stock market and bonds are useless. So I’m “losing” money every day. But – I feel good about not being a prostitute or a pimp. I’m old enough to be able to put value on my morals and ethics.

@Lisa_hooker And maybe, with that “losing” money, you’ll be able to pick up some nice pieces on the cheap after this all falls apart. But when?

“the Fed wants the purchasing power of labor to decline”

So the solution is to bring in more cheap labor.

Too bad we can’t kick out all the high cost middle class labor. Except for the massively productive government workers massively boosting GDP of course.

FOLKS:

Fed says there is NO bubble and NO inflation!

So keep buying on DIPS!

(sarc)

BTW All bubbles bust like in 2000 and 2008. Some take longer than others! Higher they go, harder they fall!

Been in the mkt since ’82. NOT seen anything like this SURREAL mkt!

Has any Country in human history prospered by spending Debt on Debt?

I guess we will soon find if the US economy can have its cake and eat it too. We have economic policy (wealth transfer scheme) which generated huge returns. (US net worth rose $14T last year alone to a total net worth of $130T). Now we are embarking on social spending programs (which are long overdue) to help combat the poverty and extreme wealth inequality being generated from the current economic model. We aren’t raising taxes in any meaningful way, we don’t seem concerned with interest rates and asset price inflation, we don’t seem concerned with deficits of any kind. Apparently no heavy lifting will be required for any future spending and it is smooth sailing from here. It just doesn’t seem possible that it is this easy to safely manage an economy. Will every future economic stress be dealt with in this way, i.e., don’t change the system just throw more money into the (IMO) rather corrupt system?

They will keep on kicking the can, as long as possible or until the payment on the DEBT will exceed the budgets of DOD, Medicare and SS#!

Since there are $16 Trillions earning NRP, interest on any US Bond is still positive, many outside are willing customers!

The guard rails have truly been removed. There is only the desire to spend, borrow and print money. Digital money will change that even more IMO. If they find a limit the government doesn’t just meet that need it smashes through it. We used to have these limits in place but because of the COVID they are spending with an excuse. But when the pendulum swings the other way the Republican’s will have to get an even bigger stimulus because who will ever try to do a Billion dollar plan when Trillion dollar deals are now the normal

There is a new question on the 1040 Tax form that asks if you every invested in a digital currency. What the hell is that all about?

@SC – But we can’t have a question like “are you a US citizen?”

Wolf, thank you for another excellent article. The “big one” (services inflation) is as you point out the crucial swing factor and perhaps the arena which markets have not got their heads round yet. Yes, as you write, in a reopening phase, the supply capacity taken out will mean a price spike upwards of this “big one” because of all the demand. But this might be a 2022 phenomenon (it takes a long time for full re-openings to occur?) But in 2021, I was thinking that surely a lot of the price adjustment to airline tickets etc occurred in the first lockdown phase (Q1-Q2 2020), so a lot of those big negative numbers you quoted will get taken out of the year-on-year comparatives. And, by magic, even without a full re-opening in summer 2021, the crucial red line levitates upwards well beyond 2% year-on-year, overall. This will contribute to inflation surprises in Q3-Q4 2021. And then, the Fed has a problem because a full re-opening into 2022 will see services inflation established well north of 2%, perhaps 3% yoy. I also have a conceptual problem with the Fed’s “transitory” claims for oil/commodity inflation because it is well documented that in previous cycles, it takes 12-18 months for such commodity price rises to feed through to the consumer economy. A nasty surprise is coming?

30 year US treasury bond yields are going to 3% by summer maybe fall 2021. This is why I sold all my long bond ETF’s 6 months ago and went to cash. I took my 41% profit, interest+ capital appreciation of the last to 3.5 to 4 years from yields I bought in the 3.85% to 3.92% range.

Now, even as I sit in cash making little, US 30 year treasury bond yields are in the 2.28% to 2.29% range. I will go back in due time when it is right. I give it another 6 to 12 months when yields will be 1% point higher than today’s yields.

Here in Canada, we have 2.15% to 2.25% 10 year GIC’s fully CDIC deposit insurance. The main disadvantage I can see if we get higher interest rates in coming months, years and limited to $100,000 per type of account, RRSP, TFSA, RESP, RRIF, non-registered etc. and no possibility for any capital appreciation like with bonds.

Drake Hillsdale

If you have followed today’s 30y bond action ($24Billions). it sailed through without a hitch. the yield slided from 2.29 to 2.27!

With 16Trillions+ in NRP for global bonds out side USA, rates of 10y ($1.51) & 30y yield will remain attractive, at this point, assuming ‘inflation’ remains the same.

This is the key point sunny129. Now with multi trillions stimulus spending, deficits, debt from all governments, mostly the US government, inflation will creep up and stay up.

Last year most predicted 2% US 30 year treasury bond yields would take a years. It took less than a month.

Today, all yields are jumping alot again. The 5, 7, 10, 20, 30 year are now 0.85%, 1.29%, 1.63%, 2.30%, 2.39%. Most long Bond ETF’s are taking a big hit last few months.

This will be the next speculative bubble. Wait till just before the next recession and buy long term treasuries with only 10% down. 90% borrowed money. When the crash hits the long treasuries skyrocket, and with 10 to 1 leverage, you make a killing.

It used to be called “Shooting the Treasuries” .

While you’re waiting you collect the 2 to 3% interest on the bonds.

Sort of like what Michael Burry did with MBS short only this time you’re long. You have to time it right.

And here in the UK; I can report that fresh fruit and vegetables seem to have fallen in price sine the UK left the EU and we are only 2 months out.

I think I have sadistic tendencies because I am enjoying watching the EU falling apart and advising people to avoid buying EU products and buy Japanese cars and wine from Australia etc.

I’m enjoying watching America fall apart.

It all depends upon, whether you belong to top 10% (who own nearly 90% of Wall St wealth) or in the (compared to 3%) the bottom 90%!

America is slowly falling part since mid 70s, if not earlier.

– Nearly 50 trillions got transferred slowly, from the bottom 90$ to top 10% during this period.

More income stream going to those with (increasing!) Capital assets, away from Labor – lower and middle class, in the bottom 90%. It got worse since 2000 (+globalization!)

Trends in Income From 1975 to 2018

“The three decades following the Second World War saw a period of economic growth that was shared across the income distribution, but inequality in taxable income has increased substantially over the last four decades. This work seeks to quantify the scale of income gap created by rising inequality compared to a counterfactual in which growth was shared more broadly. We introduce a time-period agnostic and income-level agnostic measure of inequality that relates income growth to economic growth. This new metric can be applied over long stretches of time, applied to subgroups of interest, and easily calculated. We document the cumulative effect of four decades of income growth below the growth of per capita gross national income and estimate that aggregate income for the population below the 90th percentile over this time period would have been $2.5 trillion (67 percent) higher in 2018 had income growth since 1975 remained as equitable as it was in the first two post-War decades. From 1975 to 2018, the difference between the aggregate taxable income for those below the 90th percentile and the equitable growth counterfactual totals $47 trillion. We further explore trends in inequality by applying this metric within and across business cycles from 1975 to 2018 and also by demographic group”

Rand Corp

Remember, most of that “wealth” is not hard assets, and assumes a functioning society. The top will be hurt too when this all implodes.

Wait, I thought they were saying you wouldn’t even have food if you left the EU.

Re: “Purchasing Power of Consumer Dollar”

Is it possible to add foreign currencies in their native countries?

Does the data exist or would cultural differences skew it?

Those countries whose currency is pegged to US $. will (more or less) have the same efffect including petro-dollar. Most of them have LESS stability and credibility compared to US $

Thanks for your responses!

Another great post! Along with the Purchasing Power of the Consumer Dollar graph should be overlaid the median wage of the consumer, or perhaps better, the median wage of the laborer, normalized to the dollar’s value.