The dollar lost purchasing power with regards to houses at the fastest rate in six years.

By Wolf Richter for WOLF STREET.

Prices of single-family houses jumped 8.4% in the US, the biggest year-over-year jump since March 2014, according to the Case-Shiller Home Price Index for October, released today. The index is based on the “sales pairs” method, comparing the price of a house that sold in the current month to the price of the same house when it sold previously, going back decades. By comparison, the National Association of Realtors’ house price index, which is based on “median prices,” has skyrocketed 15%. In this terrible economy with 9 million to 20 million people out of work, house prices have been fired up by record low interest rates, the $3 trillion the Fed has handed the markets, the shift of working from home and not wanting to live in an apartment or condo tower, and by a dose of panic-buying.

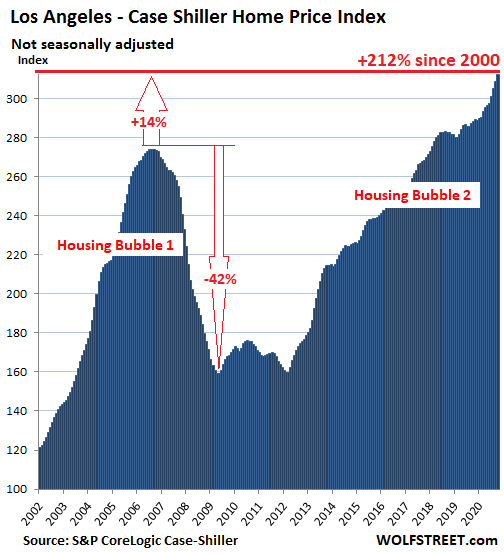

Los Angeles – the most splendid housing bubble of them all:

House prices in the Los Angeles metro rose by 1.1% in October from September and by 8.4% year-over-year, which put them 14.1% above the peak of the insane Housing Bubble 1. The Case-Shiller index was set at 100 for January 2000 across all 20 cities it covers. Today’s index value for Los Angeles of 312 means that house prices in the metro have more than tripled since January 2000 (+212%), making it the most splendid housing bubble on this list.

Today’s release of the Case-Shiller Home Price Index, named “October,” is a rolling three-month average of closings that were entered into public records in August, September, and October.

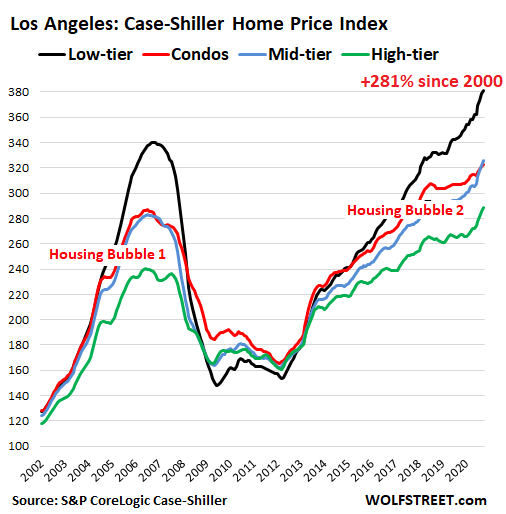

The Case-Shiller Index provides sub-indices for some cities. For Los Angeles, in addition to overall house prices, it provides data on condos, and for high-, mid-, and low-tier house prices.

Prices in the low-tier segment (black line) jumped 10.4% year-over-year and have nearly quadrupled since January 2000 (+281%). During Housing Bubble 1, this segment surged the most, and during the Housing Bust, it collapsed the most (-56%). High-tier prices (green line) jumped 8.0% year-over-year and are up 188% from January 2000. Condo prices (red line) have been increasing at the slowest rate of the four categories (0.5% month-over-month and 5.0% year-over-year):

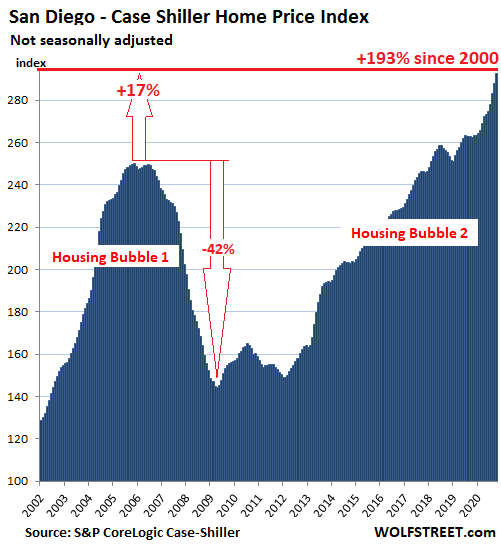

San Diego:

House prices in the San Diego metro jumped 1.7% in October from September and by 11.6% from a year ago, having nearly tripled (+193%) since 2000:

This is “House-Price Inflation”: The Dollar lost purchasing power faster.

The Case-Shiller Index – by comparing the sales price of a house in the current month to the price of the same house when it sold previously – tracks the amount of dollars it takes to buy the same house over time, thereby measuring the purchasing power of the dollar with regards to houses. This makes the Case-Shiller Index a measure of “house-price inflation.” And what we’re looking at is the phenomenon that the dollar has lost purchasing power with regards to houses at the fastest rate in years.

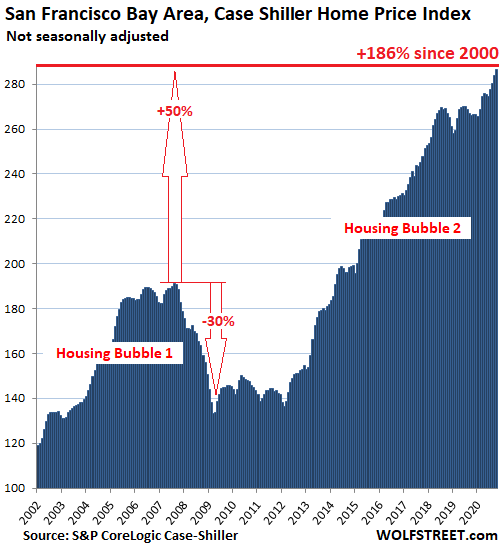

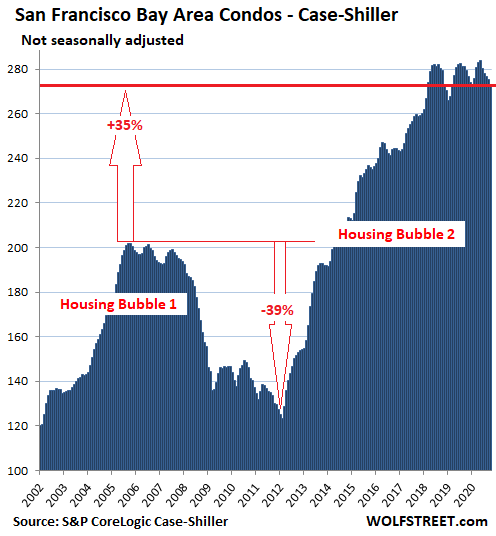

San Francisco Bay Area:

The Case-Shiller Index for “San Francisco” – the Bay Area counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay) – rose 0.9% in October from September and was up 7.7% from a year ago. The index is up 50% from the crazy peak of Housing Bubble 1 and has nearly tripled since 2000:

San Francisco Condo Malaise:

But condo prices in the five-county Bay Area fell for the fifth month in a row and are down 2.3% from a year ago, and below where they’d first been in March 2018, amid a historic all-time record condo glut in San Francisco itself:

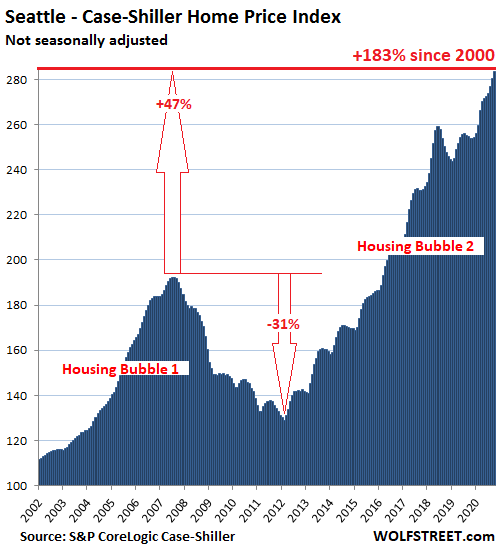

Seattle:

In the Seattle metro, house prices jumped 1.1% in October from September and 11.7% year-over-year, having surged 47% since the peak of Housing Bubble 1:

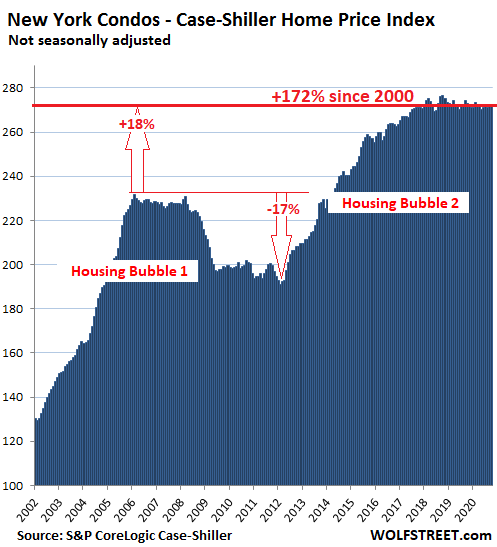

New York metro condos:

Not to be confused with Manhattan condos that are now undergoing a reckoning, Case-Shiller’s index for New York City condos includes all of New York City plus numerous counties in the states of New York, New Jersey, and Connecticut “with significant populations that commonly commute to New York City for employment purposes.” In these vast and diverse markets, the index for condos has essentially been flat since late 2017 and is down a smidgen year-over-year and from the peak in October 2018:

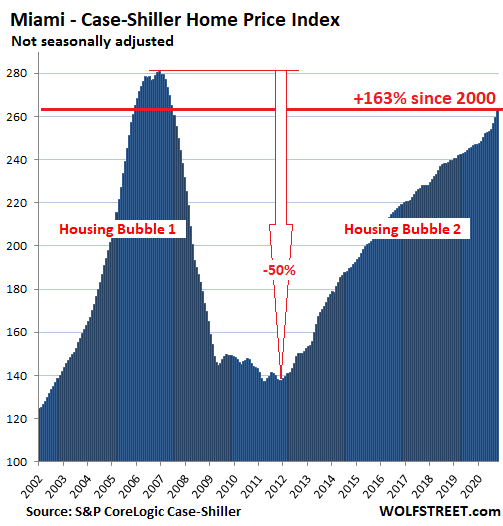

Miami:

The Case-Shiller index for the Miami metro jumped by 1.5% in October from September and by 6.8% year-over-year, pulling within 6.1% of its totally crazy peak of Housing Bubble 1:

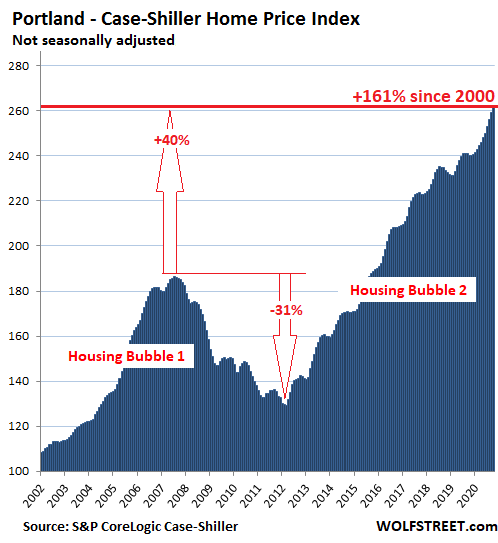

Portland:

House prices in the Portland metro rose 0.7% in October from September and 8.9% from a year earlier:

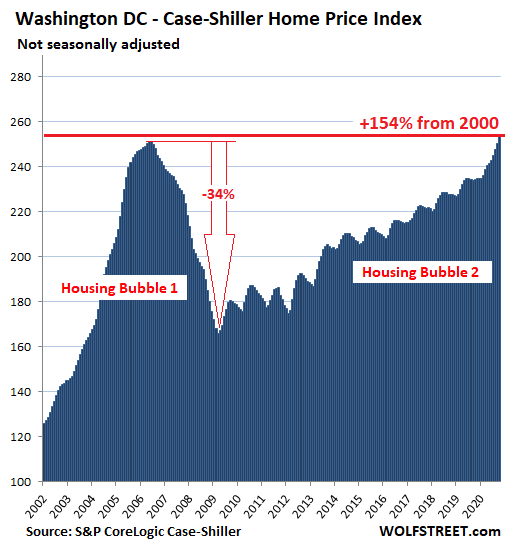

Washington D.C.:

The Case-Shiller Index for the Washington D.C. metro rose 1.3% in October from September and was up 8.2% year-over-year and thereby finally surpassed the crazy peak of Housing Bubble 1, hallelujah:

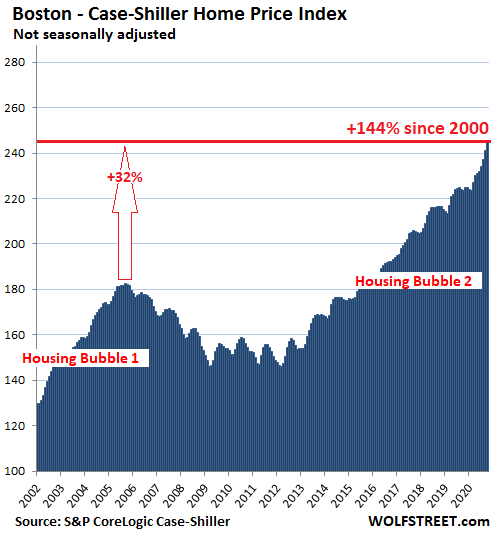

Boston:

The index for the Boston metro rose 1.5% in October from September and 9.4% year-over-year:

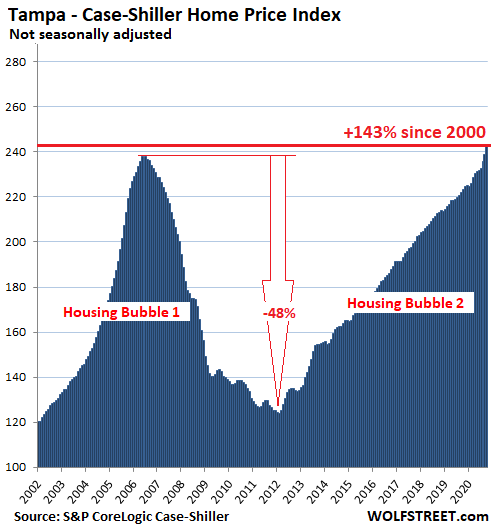

Tampa:

House prices in the Tampa metro rose 1.6% in October from September and 8.6% from a year earlier, and are now 1.6% above the crazy peak of Housing Bubble 1:

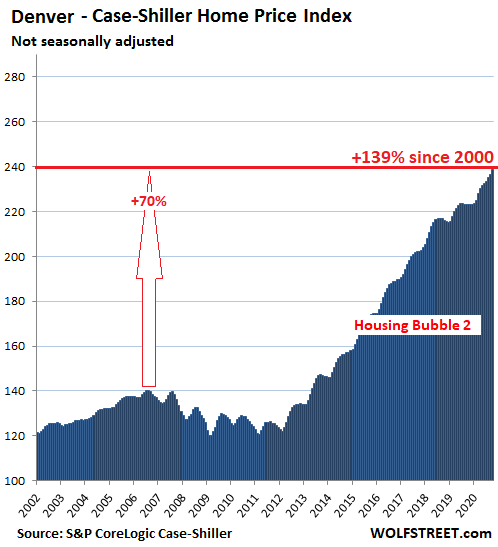

Denver:

The index for the Denver metro rose 0.9% in October from September and 7.0% year-over-year:

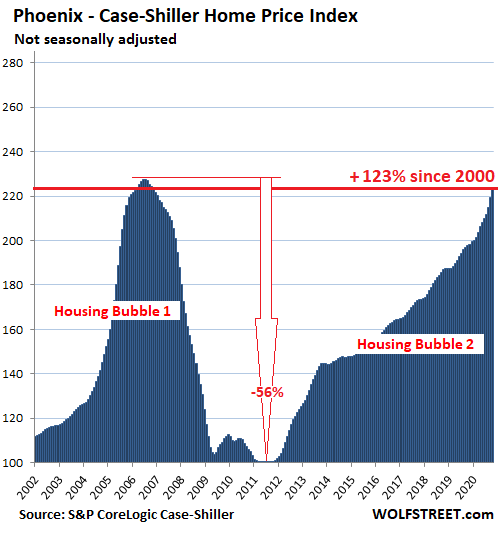

Phoenix:

For the Phoenix metro, the index rose 1.7% in October from September and 12.7% year-over-year, making it the market with the currently hottest house price inflation on this list of Splendid Housing Bubbles, ahead of San Diego (11.6%) and Seattle (11.7%). And prices almost caught up with the crazy peak of Housing Bubble 1:

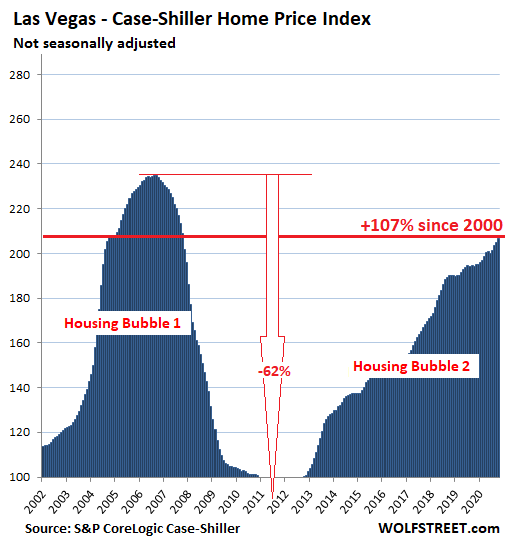

Las Vegas:

The index for the Las Vegas metro rose 0.8% in October from September and 6.4% year-over-year, but remains 12% below the crazy peak of Housing Bubble 1:

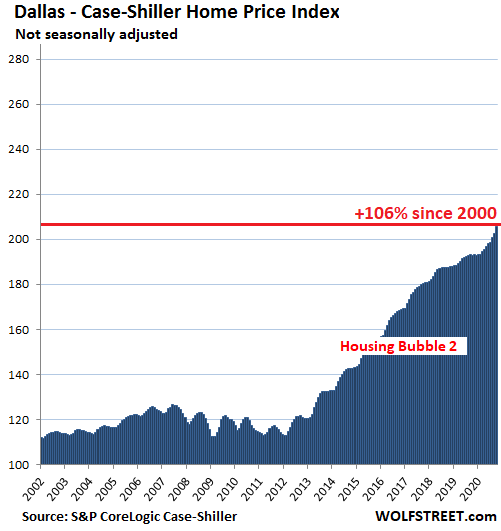

Dallas:

House prices in the Dallas metro – counties of Collin, Dallas, Delta, Denton, Ellis, Hunt, Johnson, Kaufman, Parker, Rockwall, Tarrant, and Wise – jumped 1.4% in October from September and 6.5% year-over-year, having more than doubled since 2000.

This makes the Dallas metro the tail light of the Most Splendid Housing Bubbles in America, with the remaining markets of the 20-City Case-Shiller Index not having reached that point yet where it takes over twice as many dollars to buy the very same house than it took 20 years ago.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This would all explain why Burton Malkiel recommends that everyone should own some real estate (or an REIT).

I personally recomend owning a mortgage. It’s self-diversified thru owning real estate tax (they can’t take it from you).

Only problem with purchasing a mtg pool is the brokers have access to systems like “YieldBook” which accurately price them at a fair OAS. Then, they take advantage of the retail investor … they can locate mortgage pools trading cheap to the benchmark in the institutional market because of idiosyncrasies in the collateral and prepayment patterns, then sell you a piece with a significant markup, and you will never know you got taken for 25 to 50 bps, or even more. The problem is even worse if you invest in private pools.

You are better off in a mortgage ETF, as long as you were not counting on a ladder investment.

You are talking a 1/4 to 1/2 percent. Is that significant?

How much should a broker make for placing a mortgage to a retail investor?

I will give you a little more info … retail investors make mtge product purchase decisions on yield. But, that is a mistake. Institutional investors make mtge product purchase decisions on OAS.

A smart broker can find mtge products that look good on yield, but are terrible deals on OAS. These guys buy these deals in the institutional market, then trade them on yield to retail buyers.

Since you don’t have YieldBook, you can not figure out if you are getting a good deal, and you usually do not. The game is rigged against retail and I never saw a good deal on mtge paper sold in the retail channel. I would stick to ETF when it comes to mtge.

Debt is in a “bear market”, and represents a bargain. USG subsidizes mortgage debt, but two questions. How does a bear (commodity) market in debt resolve itself? Does the debt I own have equity, or am I just holding the coupon? (picking up dimes in front of a bulldozer?) Before debt enters a bull market people go bankrupt. Typically the bond holders get a haircut. Why would this be any different? Assuming forebearance is not all unicorns and rainbows.

makruger,

The big issue with that philosophy is that some areas will be winners and others losers. For many, those houses in losing markets are anchors.

Wolf,

Housing Gone Wild…. you could further expand out the Wolfstreet Media empire with a series of videos, on VHS, literally. It’s a new spin on an old theme. And keeping it on VHS will bring back the nostalgia factor

Housing Gone Wild (by Wolf Richter), and sell if for $19.99.

It’s 1984. The above charts are what the Fed calls stable prices trending a little on the low side. All government language has been corrupted.

Treasury= Debt management department.

Defense Department= War Department

Stimulus= Dance a little longer Cinderella

Interest Rate= Paying people to hold your money so you don’t spend it.

Social Security= oh we didn’t plan for everyone retiring when they hit 62

Here’s the inflation that the Fed claims isn’t happening.

Right on RNYer.

And more inflation in the cards.

Go to the grocery store, an auto parts store, or a restaurant as it’s already there.

Well yes and no. The velocity of money is declining and I read that people are going to be saving their “stimulus” if the can, for when the fit hits the shan. See Wolf’s most excellent piece on the number of mortgages in “forbearance.” When that explodes like a pressure cooker (no way left to let it out slowly), there will be masses of foreclosures, short sales and AH4R and Blackstone and the usual suspects will be there to buy them at say 65% of par. They will take them to foreclosure and either book their profit on the sale or take them away from Joe and Susie Sixpack and the others who “bought” with like 2.5% down. A 5% dip makes you a tenant with a mortgage. See http://www.peoplevmoney.com for an interesting read on the gross conflicts of Florida appellate judges who owned “bank stocks” and hammered down owners installing the “rocket docket” and other fudgery post 2008. Why people aren’t in the street rioting I dunno or maybe they will be. In France they’d be rioting. Here, everyone is too anesthetized with whatever they ingest and are in their silos. Bezos gained $340 billion in more wealth in this dumpster fire of an economy and even the Hot Waitress index doesn’t work anymore because small restaurants are getting decimated. Congress screws the little people and Fox and their ilk pit people who make $100k a year against poor people/working class while all the benefits flow to the top .0001%. Today, the top 1 percent of households own more wealth than the bottom 90 percent combined. #BITFD

Velocity of money is ignored pretty much everywhere… except for a few of us that notice that cash flows aren’t what they used to be, and debt is growing fast than “money printing”…

speaking of inflation, I went to UPS to ship 2 medium-sized packages from Florida to Florida and paid over $55 for that. I remember paying 15 dollars per package cross country 5 years ago.

Yep. That’s how Amazon is controlling online sales, through shipping rates. A small retail website can in no way compete.

Buy the decals online, print them at home. The in-store purchase I think has higher fees attached? Keep the profile of the box as small as possible. Corps get a bulk discount rate as well. 3rd parties like Paypal might be able to sell you shipping via UPS cheaper.

Bubble wrap retail prob costs more than OLED TV screen per square foot, save the packaging from purchases.

Amen! Also see health care and college tuition.

Yes. I do not see how the higher end of the market can long keep climbing. Remember that we have a demographic cliff coming up: the baby boomers will have to sell their homes sooner or later, even if it is only after they die.

There will have to be a lot of foreign investors stepping in to buy the inventory, because so many baby boomers did not save enough, so they will need to cash in the capital in their homes and live in cheaper places thereafter to have reasonable qualities of life. Otherwise, there will be a collapse in prices on the upper end RE in the coming years.

The lower end will likely remain desirable in most places that do not face shocks to their areas like factory closings, etc., because there will always be relatively prosperous members of the poorer, younger generations that can afford that.

Who knows when this will play off? I would guess within five to ten years at most.

Inflation will climb and that might hide the likely real, decrease in RE prices in more expensive RE.

Notice that in today’s YoY figures released by Case-Shiller, Boston is the only Northeast city with a healthy YoY. Why? In my opinion, the biotech and drug industry, as well as the health care industry, which all have a heavy presence in the Boston metro, is raking in billions from govt COVID spending. That spending could last for years and years.

Also note how cities with large tourism revenue relative to GDP, like Las Vegas, Miami are underperforming YoY.

Boston is a ghost town.

Hopefully a reset to make things more affordable for next generation and a slow and steady (rather than boom bust) growth pattern that supports entrepreneurs and small business get back on their feet.

A 1BR nice condo at 450-550k should indicate a bottom.

True. Core city areas like South Boston, Back Bay, Fenway, are suffering … people want out of the high density condo and apartment life. And, they want out fast.

But, not too far away, where the single family homes start, it is white hot demand. I have some single family rentals just outside of the city limits and the demand is so extreme that I can’t figure out what the rent is … and I have cold feet with massive rent rises on my current tenants. I do have some morals. One is a family headed by a single mother … I don’t want to throw her out so I can jack the rent by 50% from the 2018 lease … God will get you for that one.

Evict her and give half the rate increase for the new tenants to charity, tax deductible.

450-500k gets you a nice 2BR Condo in the Swamp..

I agree that the lower-level RE will keep its price. However, you have to compare the average annual earnings of the bottom 70% of Americans versus the prices of such real estate.

The younger generations are usually at the bottom of the economic ladder. Not all, but the bulk of their bell curve is not well off. Frankly, I do not think that many post-baby-boomers will be able to afford even that price you cited unless the “Fed” helps them out with more inflation, which would lower the real dollar value prices of those condos.

Thus, I think that either inflation will be promoted more to benefit the banksters by their “Fed” or even those prices will be too high compared to the average earnings of people in Massachusetts of $74,188, which includes the top 10% of earners, with huge earnings, so you know that the lower 70% earn much less. Remember that if they earn $45,000 per year they have to pay increasing food, transportation, very rapidly rising HEALTH care costs, rising property taxes due to inflation, rising taxes due to inflation, etc.

The ultra-rich can deduct most of their expenses by claiming them as corporate deductions for corporate condos, corporate jets, corporation provided autos, corporate provided secretaries-mistresses, etc. The expenses of the bottom 70% have been made non-deductible: they are effectively taxed on their earnings regardless of their net disposable income.

Thus, there will be a major real dollar decline in real estate prices at least in the high end and probably in the middle too. I just hope that we do not have a communist revolution when things become too intolerable for most.

lots and lots of Biotech and Pharma around Philly area, one of the nations Pharma hubs actually.

According to the genengnews website, these are the top 10 biotech/pharma hubs:

1) Boston/Cambridge – 18 of the top 20 firms

2) Bay Area – Lots of startups going public

3) NY/NJ – Mostly NJ

4) Maryland/Virgina/DC

5) San Diego

6) Philly

7) LA/OC

8) Raleigh/Durham

9) Seattle

10) Chicago

My opinion … SFRs close to office centers featuring Biotech/Pharma should work out well over the next decade. Can’t miss. Many of my recent rental applications ( Boston ) are for people working in this industry.

Real estate is very affordable just outside the urban areas of Raleigh-Durham. Property taxes are unbelievably low.

The Research Triangle brought all the high tech jobs and all the service jobs to support them. Duke is a major medical research facility, also.

Interesting to see how San Francisco proper would dragdown Case-Shiller Bay Area, were it separated out.

“100 for January 2000 across all 20 cities it covers. Today’s index value for Los Angeles of 312 means that house prices in the metro have more than tripled since January 2000 (+212%),” Is that two a typo?

100% means double. 200% means triple. Not a typo.

I think the inflation aspect to focus on here, is how current disinflation pandemic factors play into prior and current housing inflation. This is a crazy time, when dollar purchasing power isn’t making total sense. I think the future value of money will be worth less and perhaps that plays a part in people buying now, even at inflated levels. It’s hard to wrap a head around this, that future value is being discounted by todays lack of inflation. Buying inflated assets today is thus cheaper than buying future assets with higher inflation. As mortgage rates slowly drift higher later in 2021, that will not be driven by falling home prices — if anything, rates will go up because of too much demand for low rates.

I feel safe that nobody has a clue what’s happening and that most predictions and assumptions will be wrong.

Well, we’ve just started climbing the demographic hill of the millennials where each successive year for the next twenty a larger population than the previous enters what are typically prime earning years, forming families and increasing demand for housing, typically single-family-homes. Maybe builders are right to be bullish.

Flip side of that demographic equation is Baby Boomer (currently 71.6 million Boomers aged 56-74 years– entire generation) homeowners downsizing from their standard cookie-cutter McMansion or ranch suburban homes and going smaller, or going to assisted living facilities or apartments, or (over time) to the cemetery.

Perma housing bulls are out in force these days. To them this time is different, we are at a permanently high house price plateau, and there has never been a better time to buy real estate.

A look at WolfStreet charts for this grand Housing Bubble 2.0 will not even faze them.

But remember at least how Housing Bubble 1.0 in previous decade turned out. And remember that anything that can not go on sustainably will not.

The other issue is that the Millennials and Gen Z aren’t making the wages to continue the trend. They’re struggling, and either living in small apartments or living at home, while working jobs with no real wage increases while interest rates are kept low to protect their parents’ assets.

RightNYer,

“The other issue is that the Millennials and Gen Z aren’t making the wages to continue the trend. ”

So, will housing prices eventually decline? Probably so…

I know of very few boomers who are downsizing. I’ve heard from realtors that the opposite might be taking place for those well-off. McMansions being sold to retired couples, usually chosen by the wife. Perhaps with visions of showing off to guests. The other driver might be sort of a mania, “investors” seeing prices increase and thinking it has to continue. Probably correctly as long as the Fed keeps pumping that bubble.

MC

Your statement “…I feel safe that nobody has a clue what’s happening and that most predictions and assumptions will be wrong….”

is about the most accurate prediction of the economic future I have heard in the past 12 years. :-)

Now is the time to buy what your business or your family will need long term. Once Biden’s in, you won’t be able to count on anything being available, and if it is, certainly not at today’s prices.

Thanks for making me LOL!

Considering the dumpster fire that just happened w/bungling the Covid response, massive tax break to corps that didn’t need it, outright grift/corruption with zero shame, pardons galore for his crime family (When before did the question: Can the President pardon himself get asked? Never.), the nation run by a corrupt, incompetent charlatan, etc, etc…. I’d be hard pressed to worry that the next guy could possibly be worse.

Come on man! You made me spit my coffee on the puter screen.

Ah yes, the bungled COVID response with vaccines the Left said were impossible by the end of the year. Now that they’re here it is non stop complaints that only 3 million are out of something they kept claiming would not exist (of course if they opened the gates to first-come, first-served all would be out).

So what country would you say didn’t bungle the COVID response? Germany with 1,000 deaths yesterday? What about Belgium, which has the highest per capita deaths anywhere?

Seriously, which politician would you said did the best of stopping a virus? What metrics do you use to show you’re consistent? Then show your data. Then let’s see how time holds up with politicizing a virus. Even if you say S Korea your views may not hold in another month.

1) NY governor delayed evictions for two more months, saving tenants from being thrown to the cold. NY governor shift cost to the landlords. Section 8 Apartments will add cost to NY tax payers.

2) The lagging banking sector will be under stress, yearly in 2021, from mortgage payers.

3) Jan – March lake effect snow will freeze volume up north.

Short term thinking. By the time NY kommissars get to evictions it will be winter again.

It can take years to evict someone in NYC. In fact, I have never seen anybody evicted in NYC. If a tenant is late paying, the courts give them time to catch up. If they are not paying due to repairs, they don’t have to pay until the repairs are done, or they send the money to the court.

I know people who were constantly 3 months behind in rent, in NYC it’s a lifestyle choice.

Everyone seems to be counting on inflation without any growth in wages; and increasing assets prices with declining velocity of money. Can infinite debt substitute for real growth? We shall see.

The alternative theory — that this economy is going to explode in a deflationary bomb — seems more plausible to me.

2021 will be interesting.

The high cost state to low cost state migration is distorting both the high cost markets and low cost markets. Eventually, both housing markets will come down.

Those cashing out in high cost areas are mostly paying cash for what they consider cheaper homes. In many cases locals accuse them of overpaying for properties, but cash buyers can always overpay for property and come out ahead. It looks like inflation for awhile, but it is really deflationary.

For example, the average $300K home purchased with a mortgage pays an extra ~$150K in interest. If a cash buyer overpays by 10% ($30K), they will still be saving $120K on the house overall. The temporary inflation turns into longer term deflation/savings.

Even if the buyer gets a mortgage and overpays for the house, they are still saving relative to their old property. The mortgage will be smaller and the taxes and insurance as well. Still deflationary.

The higher cost area the buyer migrated from will eventually crack from lack of demand and that is also deflationary in the long run.

I’m hoping the Texas Gold Rush, currently underway, will push my paid for 2,000 sq.ft. brick home value from $242,000 (current appraisal value in The Woodlands, Texas) to a cool million.

Thanks to Californians making this possible, we will have enough for future assisted living costs for us and maybe a quick trip to Disneyland when we cash out.

I saw a chart recently that listed the Woodlands as one of the high mortgage default areas. So far house prices are high, but when those defaults go into foreclosure, watch out.

Exxon has 8,000 jobs here.

Also here are Occidental, Phillips, Chevron/Texaco, and two dozen other smaller oil companies. Then there are the oil service companies. But we do have a lot of Biotech firms too.

Great comment, Petunia. My problem as a buyer who needs to retire soon on a moderate budget, is that the long run is getting to be a very long run. I’m running out of runway.

Tough times cause individuals to make tough decisions. Moving for a better opportunity or to cut living expenses is one of them.

“. . . or cut living expenses.”

In 2020 my wife and I made half of what we did in 2019 but we still were able to save. (Taxes already accounted for.) So it’s a matter of where to “invest” that savings. And then we’ve got two $600 checks coming from the government that I’ve got to worry about too. Decisions, decisions.

It gets worse, the Wolfs past, data would suggest that to some degree:

> Even if the buyer gets a mortgage and overpays for the house, they are still saving relative to their old property.

and

> The higher cost area the buyer migrated from will eventually crack from lack of demand and that is also deflationary in the long run.

are the same buyer (2 chains… now we have folks called 2 mortgages… lol), they have moved from high cost metros to escape the Lock-down Olympics while mostly still holding on those leveraged high cost bags (old mortgage they’re still on the hook for)…

The buyer that expects to eventually go back to the high cost area and didn’t sell will be sitting on big losses. I didn’t address that scenario because it is the worst possible outcome, two overpriced homes that don’t sell.

I would have thought coronavirus would have burst housing bubble 2 but that doesn’t seem to be the case somehow. If that doesn’t burst it, what will?

This year has been about bidding up SFH away from the cities. Next year is the reckoning for all the condos and co-ops left behind (but still accruing fees and taxes).

What mucks it all up is the printing.

“If that doesn’t burst it, what will?”

A 1% rise in interest rates…

That’s exactly it, with the kind of runaway debt and inflation we are seeing now, the Fed will eventually lose control of interest rates. Even an increase of a point or two will crush the housing market. It will then turn in to a roach motel with no escape possible for the bag holders. I am not sure why people think buying at the lowest historical interest rate in history is a good idea. I bought my first house with a 10.5% fha loan but only cost $45,000. Over the next decade I could just refinance whenever the rates went down a couple of percent but my mortgage stayed the same size. Eventually my mortgage payment was less than my car payment. When you overpay at the lowest possible interest rate the only way out is the poor farm.

That was my theory when rates were instantly slashed to zero amidst the financial crisis. I never dreamed of QE or that this could still be going on a decade later.

Thanks, Seneca.

It is funny that during an era when the internet provides an unprecedented level of *detailed* historical economic data (free, except for the cost of a few keystrokes) people will hazard many, many thousands of dollars…without doing a dollop of research.

And memories of the 2009 implosion don’t even require Google.

But, in fairness, the G’s ZIRP scheme machine is more and more clearly running out of gas…each subsequent bubble appears to be built on fewer actual transactions.

Perhaps the Fed’s wealth effect Nirvana is for 1 hyper inflated transaction to take place…and then for tens of millions to spend based off their Zillow Zestimates.

“the Fed will eventually lose control of interest rates. “

I grew up thinking they only controlled short term rates. But they now control long term rates too as we see this year and did the past 10+ years too.

What will make them lose control?

The reason for younger folks jumping on the property ladder at what you describe as a bad time (debatable), is mostly that we have to. As previously stated by someone above, there is a demographic wave of millennials starting families. Some are blind to the risks, but most my peers are all aware how silly this housing market is. We are all just feeling the pressure to find a family-friendly home in a place with gainful employment.

Your situation of buying at a high interests rate and a low price just to see rates fall over your lifetime was luck. It was the state of the world around you, not genius. We get a little resentful hearing this stuff time and again from those who grew up facing different challenges than we are now.

I feel as though the entire financial system has been in crazy land since I began adult life around 2012. It’s frustrating to me to have to participate in a system that feels so illogical, but time marches on, and decisions have to be made even when many of the options are bad.

Patience is very important to make good financial moves but sometimes you just have to jump and hope for the best. Maybe this bubble will collapse and many will end up underwater as deflation hits home prices. Maybe the fed will achieve its goal of destroying the dollar to pay for decades of unrealistic promises to retirees…and these houses bought at 2.5% and paid for in depreciating dollars will be a smart move in the long run. Who knows.

Dave,

The Fed will lose control when fewer people around the globe use the USD as a store of value (DC has created 20 yrs of ZIRP at this point…essentially taxing away 50% to 100% of the earning power of USD savings).

Be it gold, the Yuan, bitcoin, or anycoin…savers won’t endure this forever (why does anybody think bitcoin is a thing in the first place? Because, unlike fiat, it cannot be diluted at the will of a political class).

In the end, USDs are the only thing that DC can create at will…as people use it less (because of DC’s behavior), its power evaporates.

USD collapse is the darkness that DC has been flirting with/french kissing for two decades all so it doesn’t have to make a single hard decision about reducing (by even 1%) the political payola it employs to maintain power.

Dave, the value of the dollar will. If the market is demanding higher interest rates for 10 year treasuries than .95%, the only way the Fed can “keep them down” is by buying more treasuries, which means printing money and devaluing the dollar. This makes foreign imports (nearly EVERYTHING we consume) more expensive, which the government won’t be able to hide. As you can see over the past year, the dollar has dropped by 10% or more and it seems to be accelerating.

In other words, the Fed can only control interest rates for so long as it can print money without affecting global demand for those printed dollars. But markets are ultimately larger than governments, and the fact that we are the reserve currency means that we have more runway, but not an infinite runway.

It’s the historic demand for U.S. dollars that has allowed Congress and the Fed to get away with the shenanigans it has over the past 20 years. But I get the sense that facade is finally being exposed.

Trillions and trillions of government intervention saved the asset markets. They are busy saving the patient right now. We will see what his quality of life is when this is over.

Somebody is going to be getting a lower standard of living than they were counting on. If you are not in a politically connected group it’s coming out of your pocket in the future.

When its over the rich will get richer and the middle class will move down to the lower middle class, the lower middle to the poor, and the poor will be homeless or living in tent cities. We will be no different than a third world country. In a lot of respects we are already there. Most of Washington DC away from the monuments resembles a third world country,

I have lived in DC my whole life. Which neighborhoods in DC have you visited in recent years that look at you say?

Of course he hasn’t, Dave. The favored past-time on these forums is crapping on places you’ve never been and telling people you never knew how unwelcome they are to move to your area.

DC now is far more wealthy and developed than it has ever been.

No tree grows to the sky

Only the money tree my Dad once talked about.

1) SF Bay area and Condos are shortening the thrust. NYC Condos are in a trading range.

2) There is no sign of correction for the rest.

3) Vectors up to a new all time high, or to a lower high. Up in a strong momentum, or in a moderate momentum, but there is no sign of weakness in the RE business, except in the heavy weight RE markets of SF & NYC.

Peace and prosperity thru asset price inflation. Monetary policy so easy, even a caveman (named Jerome) could do it!

Ah, but he doesn’t appear to wear any of those off-brand Neanderthal genes … so tis the pity, NOT!

These inflated housing prices are the direct result of several factors:

1. The Fed keeping interest rates artificially low. The home prices are discounting this effect, since the monthly payment is lower than it would otherwise be.

2. Secondly, the 2017 tax law discourages selling your home when all your debt is grandfathered in and can be lost when you sell if you try to take out another jumbo mortgage. Unlike 2005/2006 I don’t see a lot of homes in the swamp (DC) up for sale. Realtors are complaining about a shortage of listings. Back then the “days on the market” when up the 2005/2006 meltdown began. Shortage of listings means higher prices.

3. The builders compound the problem by building monster homes that appeal to the millenial generation that are much bigger and more expensive than the homes that were on the lot, which were torn down. I wonder if the Case/Shiller index takes into account the much larger sq footage of the home than the one that was formerly there. If so then this index is inflated. Its comparing apples to oranges.

4. The government has not cut back on its workforce to any significant degree. While much of the country has suffered under lockdowns, layoffs, and business closures the fat cat government workers and the lobbiests and contractors that feed off the Fed government here have not suffered one bit and they are still living on the gravy train. They are the ones buying these expensive homes and bidding up the prices.

#3 Especially relevant in our hood in St Pete, FL SC:

Just saw the new 2500 SF home sold for $785K, before it is actually constructed on the lot, that the builder bought with the 1950 old house for $195K a couple months ago.

And similar all through this hood where houses were selling for less than $75K in 2013-15,,, now on ZippyLo for $200-225K.. or more. Only houses currently for sale are older ones, remodeled and waaayyy over priced for this hood,, all others are gone in one day.

So, Wolf et al:

1. Does the Case-Shiller differentiate between the houses on a lot, or does it just go by the address of the lot?

2. Does the C-S differentiate between the house as it was at the last sale and how it is with the 1,000 SF addition added between sales?

Curious to know, as it is a big difference for some of the houses I see in my bicycling.

VintageVNvet,

#1 and #2: Yes and Yes. From the Methodology, page 7:

“Price Anomalies. If there is a large change in the prices of a sales pair relative to the statistical distribution of all price changes in the area, then it is possible that the home was remodeled, rebuilt or neglected in some manner during the period from the first sale to the second sale. If there were no physical changes to the property, there may have been a recording error in one of the sale prices, or an excessive price change caused by idiosyncratic, non-market factors. Since the indices seek to measure homes of constant quality, the methodology applies smaller weights to homes that appear to have changed in quality or sales that are otherwise not representative of market price trends.”

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf

How can C-S compare the 125k invested in new bathrooms, kitchen, rec room, garage, &c, when the exterior and yard appear the same. Shouldn’t compare original home with extensive remodel of only the interior. I.E. pandemic and 9 months of Home Depot with a flush bank account, or a pile of Tesla/Amazon.

Read the Methodology. It’s really pretty interesting. They’re having to deal with all kinds of complications, such as those you mention.

Hey VintageVNVet,

I’m down in Sarasota…tried to buy a few places in St. Pete back in before the last bubble burst and homes were going under contract the first day on the market. I bid $10K over asking price on one and somebody else offered $20K. It was a frothy insanity and this sure feels just like that.

After the last crash, a friend of a friend started buying up dozens of homes in S. St. Pete for $8-20K/each, fixxer uppers, and they’re now full of tenants.

Those same fixxer uppers are $179K asking price today and selling fast. RE is a trailing economic indicator (normally) of course, but it’s inconceivable to me how “this” lasts much longer.

Finally, people are taking my advice and buying quality real estate and stock market indexes (S&P 500 way up this year too). Fed is printing like mad, so the only thing you will regret is not buying more.

I would regret not selling near the top. When will that be?

My favorite Warren Buffet saying:. If Cinderella had known it was 5 minutes before midnight she would have rode home in the carriage.

There is no top with quality real estate and the S&P 500 (or gold and silver). There is however a bottom for the US Dollar, and that is a very small number.

Nobody knows for sure but guaranteed it’s better to sell too soon than too late! Like George Carlin’s joke about “buyer beware”….

Wolf,

I wonder what the above charts look like if magnified to focus only from about October 2016 (when the 10 yr T was about 1.6%), to October 2018 (when the Fed allowed the 10 yr T to rise to a “huge” 3.2%).

(Students of American Decline note…the annual 10 yr T never went below 3.2% from 1959 to…2008)

My guess is that the metro roller coasters were flat at best, to downish (transaction volumes fall before prices do).

For all the RE bulls…picture if the Fed were compelled to allow 10 yr Ts to rise to 5%, 6%, 7%, 8% (all very common for 50 yrs) …contemplate how monthly mortgage affordability evaporates if rates return to historical norms..after the Great Fed ZIRP slaughter has caused home prices to double or triple.

“For all the RE bulls…picture if the Fed were compelled to allow 10 yr Ts to rise to 5%, 6%, 7%, 8% (all very common for 50 yrs) …contemplate how monthly mortgage affordability evaporates if rates return to historical norms..”

We are in a situation where they cannot let that happen. And won’t. The national debt plus the fed balance sheet is what 30T? 5% is 1.5T in interest annually alone. That’s real money to be paid. They will QE like their life depends on it not to have to pay that interest. ….and most major central banks are in the same situation.

All I see happening is most central banks continuing to print and they will inflate until everything breaks across all fiat currencies. No idea when they will break. But at some point.

The statistics on inflation will inevitably be manipulated if they are not already to keep the big lie going.

I actually think true hard assets that generate income with low leverage long term debt are one of the best plays out there right now.

It’s always good to read the history of John Law and the Mississippi bubble from time to time. All it took was a few Germans going over to Mississippi and finding the the whole French financial paper money system was backstopped by swamp land that brought about the bust. John Law went from smartest to dumbest guy in the country within a year.

That and Dutch folks deciding to not buy anymore tulip bulbs.

We can’t bring back Paul Volcker, the greatest Fed chief in US history, but in his honor we can bring back his 18% mortgage rates and 21% prime rates.

Lets get it on and have the slaughter now rather than later.

Lets see how these greedy homeowners, stupid lenders, home flippers, fare in that environment.

Lets separate the men from the boys.

We, ( the family We in this case,) agree with you, like totally SC!

Bought a house for $40K with 18% mortgage a few decades back,,, sold it, majorly rehabbed, 2 years later for $105K with 9% 1st for buyer from bank,,, and we held a small ”purchase money second” at 12% for a couple years to help them make the deal.

Same house sold a year or so ago for $800K, and the new buyers literally ecstatic to get it for that measly sum in SF Bay area, from what we heard…

And so it goes, as K Vonnegut said many times, eh?

And for all on here, just keep in mind the bubbles and crashes have been going on for eva, in every location,,, and that’s exactly why we must get rid of the Fed asap, so that all the fine young folks, including these younger so called boomers, can come to really and truly appreciate an open market in at least one venue, if not all markets when the frauds and con games going on in all of them are exposed for what they really are.

RE mkt formerly always seemed to level out, due IMO to these very bubbles and crashes, but this time IS very likely to be different, between the slurp financing and the exacerbation of the extra bottom support supplied by the PE and hedgies getting into the SFRs this time as they did last time.

As a cash buyer at the end of the last crash, we were challenged to find anything that could close quickly, as we were in direct competition with these folks financed and more or less in bed with the banks. Finally found one that the hedgie bird dog had seriously mis understood.

VV, we shouldn’t get rid of the Fed as they are quite useful (go play around in FRED). We need to get rid of a Congress that creates spending bills as though the amount of money doesn’t matter. Don’t blame the Fed or the Treasury, they’re “just following orders.” Perhaps real usury laws for the banking system.

Benjamin Franklin observed, “Tis easier to build two chimneys than to keep one in fuel.”

By the time you subtract repairs, taxes, insurance, utilities, brokers fees, etc. the housing appreciation is not pure profit. The bigger the roof, the greater the cost of roof replacement. New flooring/carpet is another expense. Termites are a threat. The A/C repairman replaced a motor controller fried by a lightning powerline surge. Cracks appeared in the driveway. The washing machine died. It seems more economical to own than to rent, unless you move frequently.

People buying homes now because they believe the price will only be higher in the future – can we now say we are in a period of asset hyper-inflation?

Or a period of dollar collapse perhaps People understand what’s happening and want hard assets not hot air

Sure, but housing as a hard asset is famously subject to worse-than-wealth-tax property taxes.

And, equally famously, immobile.

And, illiquid.

If you want reliable hard assets, look to what millions of refugees have used over centuries of government oppression.

Today’s world…brought to you by DC.

Blackstone and the Fed will make sure that there’s always a floor to home prices!!!

The Zillow says my house increased 4.4% last 30 days. Up from around 2% a month lately. But that’s not inflation.

There is an appraisal issue here in DC. Some houses are being bid up so high the appraisers can’t even come close. When the appraisers tell you the value isn’t there, it must be real bad. Because they have been pretty consistent in making anything fly.

The values are not there. The appraisers are correct. There are three ways to appraise a property.

1. Market approach

2. cost approach

3. income approach

When ‘1’ outpaces ‘2’ and ‘3’ as is now the case that is a sure indication that we’re near the top of the bubble. The buyers of these houses will have to wait a long time just to break even if they are lucky. If they are unlucky they will have to walk away and leave the keys with the banker and have their credit ruined. This could be triggered by a normalization of interest rates or a 30 to 50% reduction in the Federal Workforce.

Gravedancer Sam Zell in a recent RealVision interview. Sitting on a pile of cash. “When everyone is going left, look right”. Does not believe COVID and the WFH fallout will have a lasting impact. People will want to be where the cultural action is, not the Kansas pig farm. Does not believe Zoom will permanently replace face to face get togethers. The trick might be to buy RE at the right time before he and Blackrock buy everything.

Otherwise if the Fed loses control of interest rates……

Unless you are a big investor, there won’t be deals for you.

Keep an eye at the commercial listings out there, there ain’t no bargains, everything is listed at prices beyond belief. It will stay this way as loans will be packed and sold at 10 cents on the dollar to black rock and cie at some point. Get some black rock shares instead.

Black rock and cie will eventually get its own police department to evict recalcitrant tenants, it will be a state within the state managing housing policy.

I think in Germany there was talk to ban big landlords from purchasing more than a certain number of units, maybe it’s not such a dumb idea.

Boomer,

Zell owns a lot of apartment buildings. So yes, he sure would try to make everyone think that way.

That said, many people – but not all – will return to the city centers because for them, living out in the suburbs or the sticks just doesn’t cut it long term. That’s a different lifestyle than living in a tower with a doorman where everything is taken care of, and where you can walk to 100 favorite restaurants and other venues within 30 minutes. That lifestyle remains appealing to many people — once the restaurants are up and running again.

I’m wondering how many people go back. I was a diehard NYCidiot, but two years in rural New England have been wonderful.

I’m friends with three households back in NYC, two have moved and another can’t until his condo sells. We’re all early 50s though.

People are running the numbers on city living – they don’t make sense unless you’re rich (or young, really young). Possible this reflation sticks, but restaurant culture ain’t all that. There’s something so nice about the scent of baked goods wafting through the house, ya know?

As someone who spent most of his life in the NYC area, I concur with this. Manhattan living is great if 1) you’re rich enough to be able to afford all of the “culture” and to avoid the inconveniences, like dealing with the awful subway system or 2) you’re young and single, and like the idea of being able to get drunk and mingle at hundreds of different places not far from home.

It gets really old otherwise though.

“That’s a different lifestyle than living in a tower with a doorman where everything is taken care of, and where you can walk to 100 favorite restaurants and other venues within 30 minutes.”

Wolf, that is a carriage class lifestyle that is accessible to fewer and fewer people economically (unless the building goes BK, fires the doorman, and cuts rents by 50% to 75%)

If I want culture and restaurants I take the train or car to the city – 55 minutes. Walking to some park in the city is not the same as sitting in your backyard in the forest with a few, very few, good neighbors. But to each his own.

Yes, “each his own.”

“…sitting in your backyard in the forest with a few, very few, good neighbors.”

I’d love to do that for about 2.43 days during vacation, and then I’d go nuts ?

“People will want to be where the cultural action is, not the Kansas pig farm.”

Kansas pigs are greatly offended by that remark.

Kansas pigs can take up issues affecting their community on the daily pig report, on the radio, which is part of the Kansas cultural scene. I heard it with my own two ears, unfortunately.

Serious food for thought. If the Government borrows $2000 and gives it to you, should you?

Loan it back to them by purchasing t-bills?

Buy gold and stash it away?

Pay off $2000 on your debt?

All three of those would not be what the feds want you to do with it in my opinion which probably means you should do one of the three.

I’m not smart like the other folks on this board, but I would first ask what kind of debt, at what interest rate?

I was going to say mortgage at first. My thinking was the gov. just borrowed $2000 for you at about 3/4% and gave it to you. Since they screwed you by borrowing it, how should you make the best of a deal you didn’t ask for.

The only people screwed harder are those of us who had $2,000 borrowed on our behalf and given to other people. But I’m not complaining. The government inflated my stock holdings by 40% since July, and it’s a whole lot more than $2,000. I’m just hoping that it’s actual gain and not inflation, and also that it will still be worth something when I retire.

I am glad to see Wolfe say that housing prices are rising due to the falling purchasing power of the dollar.

The value of houses always falls over time just like cars.

I fully expect money velocity to start increasing as people no longer want to be left holding large amounts of fiat dollars for any great length of time, preferring instead to buy a real asset as quickly as possible.

The first sign of hyper-inflation is a falling currency.

The second sign of hyper-inflation is increasing money velocity.

We are seeing early signs of both.

Gold and silver prices can not be used as an early indicator for signs of hyper-inflation because when governments are printing money, it is no problem for them to keep suppressing metal prices with the printed money, 8up until the moment there is suddenly no gold or silver to buy at any price.

Once the dam breaks, it is then too late to protect yourself.

” the value of houses always falls over time just like cars”Yes, all houses are a depreciating asset, but the LAND is not.

Not so sure about that Sooty.

Lots in prime SC golf communities that were sold for 98K in 1998 can be purchased for 5K today.

Up until last year you could buy a house in a south FL golf community for as low as $10K. The mandatory memberships were $70K and maintenance another $2K a month.

Take a look at what happened to RE in Detroit from 1970 forward.

Very true The physical metal, which is what people will want will NOT be there and whatever there is will sell at very high premiums over spot

1. Marriage rates dropped since the 80s.

2. There are less millennials than the boomers.

3. Boomers must transfer their wealth to sons or sell it to cover medical bills

4. Even if the dollars loose the purchase power, kids (Millennials or Gen Z) will get the houses or stocks

5. Some immigrants might buy homes or they are not so interested in houses similar Millennials or Gen Z

6. Either way price discovery mechanisms will workout and the properties will find their rightful prices and owners.

7. Ok, even if foreigners from Chinese soil or non-residents are buying up these houses, eventually, they sell it for a price or their kids will own them

8. Happy new year everyone!

Another Michael Engel in training?

Is there a volume of transactions adjusted Case Shiller index?

I would think prices are high because volume is low.

I might consider selling my house now but then I thought of all the covid risk I’m taking both buying and selling. Too risky and the logistics are poor.

Robert,

In general, sales volume has been very high in recent months. Highest since 2005 and 2006. Nationally, sales volume in Sep, Oct, and Nov was up around 25% year-over-year, according to the National Association of Realtors:

https://wolfstreet.com/2020/12/22/housing-market-goes-crazy-everyone-sees-it-can-last-and-then-the-first-dip-appears/

The Case-Shiller has counts of “sales pairs” for each market. For example, the number of sales pairs for Los Angeles was up 24% from a year ago.

Thanks!

What I’ve seen in my upper-middle class northeast neighborhood since covid is fewer listings, but once a home is listed the homes sell quick and at elevated prices relative to last year. In fact, the sign in front of the home typically starts out as ‘under contract’. And of course not all homes have signs.

So I thought, limited supply is pushing home prices higher. But this would be occurring in the context of lower net volumes. I guess all real estate is local.

Yes, there is limited supply because people are buying a home first, nearly in panic, before selling their current home; so now these people own two homes. They’ll eventually put the original home on the market. And also because many big-city apartment dwellers have left those apartments and have bought a home. This all came very suddenly.

Those who can get out might get out. The question of what causes this to go from potential to kinetic are ponderous chains indeed, many of which have been noted repititously. But perhaps the big wedge under their butts is not one of the things noted (see that looking right versus left problem noted by Boomer). Are we looking for love in all the wrong places? That said, I wonder exactly how much of the population in the “those who can’t get out” sector are using the circumstances to arm themselves. Real or not, a concern over what could be happening nearby may just be that one little thing that leads people to want to buy an escape at whatever the price must be their burden. Wall Street keeping statistics on how many new guns are being held as reserves in urban rental boxes?

It is impossible to do a proper appraisal of houses during this Covid-19 crisis. The appraiser can’t go into the property if it is occupied because of the toxic air inside the property. Been there, done that and almost wound up in the ICU. The appraiser has to use pictures supplied by the owner. What a joke. Who in their right mind would lend someone 1 million $$ without even looking at the collateral for the loan? This is total corruption and stupidity. Why are they allowing these cash out refinances when we’re in the middle of a pandemic? Greed! I hope all of these lenders go bankrupt. They will not get a bailout this time like they did in 2009/2010.

God bless you, you made me laugh.

They will get a bigger bailout than in 2009, they already are, Fed is buying billions in MBS every month.

Good thing this isn’t widespread because real estate is local and there is only so much land and water and foreign buyers that are looking for a way to launder money and people are moving to the suburbs around places like Bakersfield and Waco and El Paso and all those desirable locations where there are so many tech jobs .. oh wait maybe everywhere is like everywhere else

And maybe real inflation would be reflected in precious metals- (auto spelling)

1) The RE casino is global.

2) There are two bubbles : the first one was created between 1995 and

2006. // The second started in 2012 and cont until these days.

3) The safest market in US is NYC. // The most manipulated markets are Las Vegas & Phoenix.

4) Buy& Hold properties between 2003 to 2020 is very risky in most cities. In extreme volatile markets, with small down payments, owners are likely to lose their houses.

5) Buy & Hold before the 90’s is safe.

6) The condo market in NYC lost 17% between 2006 and 2012. Las Vegas lost 62%. // Phoenix was down 56%.

7) Between 2012 and Dec 2020 NYC Condos were up from 190 to 270,

or up 42%. Las Vegas more than doubled, up from 100 to 210. // Phoenix is doing better, up between from 100 to 220.

10) One small business owner bought a half a dozen properties in the early 2000’s. Phoenix RE was better than his business. He indulged himself with debt. He got into troubles with his banks and his suppliers, lost his RE and his business barely survived.

“ 2) There are two bubbles : the first one was created between 1995 and

2006. // The second started in 2012 and cont until these days.”

There was an earlier bubble in the 80s. That’s when The Great Inflation began – Reaganomics.

No bubble at all.

1. No Subrimes with changing high interest rates. Mortgages not available for everyone who asks. You need proper income to get a loan. Fixed mortgages.

2. Low inventory, unlike in 2006. One of the factors driving prices up.

3. RE not growing 15-20% a year nationwide. Like in 2002 – 2007 period. Even 8.5% seems prety moderate, giving Covid Exodus 2020 fenomina.

4. New record on median down-payment, roun 20k, means people actually have money to buy.

5. Fed Monetary Policies. Nobody was printing trillions of $ in 2002 – 2006. We see assets inflation of all kinds now days.

6. Low interest rates, major reason for price growth, unlike in 2002 – 2006 when int.rates was pretty high, up to 8% on some mortages.

Forbes has an interesting take on number 2. The low vacancy is because the eviction moratorium does not allow for the natural movement and eviction of those who would normally move on to a place where they could afford. When the moratoria ends they will not be able to pay the back rent owed to the landlord. Both are in a bad spot.

In other words, the scarcity in housing has everything to do with the fact that the natural flow of movement of properties is being blocked by the government like a clogged toilet, and the bowl keeps filling up with pent up demand to move through the pipes. Everything is flooded, everything.

Drunk Gambler,

FHA insures mortgages with 3% down, to people with non-stellar credit ratings. November delinquency rate of FHA mortgages = 17.5%. Seriously delinquency (over 90 days) = 12%. But due to foreclosure bans and forbearance, you’re not seeing these homes being foreclosed on.

VA delinquency rate in Q3: 8.2% — again forbearance deals and foreclosure bans keep these homes from being foreclosed on.

5.5% of all mortgages are now in forbearance. That’s 2.7 million mortgages where homeowners are not making payments.

Active duty military are last ones to default on loans. If they do, the negative information goes into their annual performance evaluations which affect their careers. Reservists, retired and ex-military who also qualify for VA loans have good fiscal habits which they built up during their active duty service and are usually good credit risks. So this 8.2% delinquency rate is very disturbing. I’m interested to see the Q4 rate. If it is higher, then its another indicator that the RE bubble is unraveling.

Wolf,

I’m hearing when the forbearance ends, all mortgage holders who want to add the forbearance amounts to the mortgage, will be asked to re-qualify for the loan. This is going to be ugly.

By the way, noticed the lenders themselves are not paying their bills on time. I’m going to start posting their names to my friends and blog site. They owe us over $5,000 in receivables for work that was done 2 months ago. We had a very austere Christmas as a result. We don’t have the time to go after these low lifes. They don’t even answer e-mails. Most of their employees who handle accounts payable are on vacation or calling in sick. If you go in there to get a loan at an inflated interest rate they welcome you with open arms. If some of them went bankrupt like they did in 2008/2009 I wouldn’t lose a nights sleep. I wouldn’t give them a nickel in bailout money.

Does that 17% include forebearance?

It includes all FHA mortgages that are delinquent. When an FHA mortgage is delinquent and then, after it became delinquent, enters forbearance, it is included in the 17.5%. But if the mortgage entered forbearance when it was “current,” it is not included.

Forbearance does not “cure” a delinquency. Forbearance just means that the lender has agreed for a set period of time not to execute its legal rights under the mortgage (foreclosing on the property).

Every bubble is slightly different from the last one. This one is due to ‘2’ and ‘6’ above. These will unravel at the same time.

‘3’ not factoring job losses on income needed to qualify for loans

‘4’ is bogus – VA requires no down payment

‘5’ contains its own seeds for destruction – inflation will lead to higher 10yr note = higher mtg rate = lower sale price.

Being a Cleveland Browns fan and seeing Cleveland as #5 appreciation price city (Zero Hedge report today) on the list proves the US is in a highly serious bubble.

No worries, Browns lost to the Jets and will “choke” against the Steelers to keep their playoff drought intact. Book it!!! Hey, it’s the Browns…..

Wow NFL talk on WolfStreet, never thought I’d see that. Steelers fans here, but I always have a soft spot for the Browns, that is a fan base that deserves some success, and I’ve been saying for years that seeing the Browns win a super bowl would be more exciting than yet another for Pittsburgh. I will be rooting for the Browns this Sunday …

Bad omens! If->”Have to pick the Browns in the playoffs.” Then–>>>”Yeah, well they’re playing the “quite game” in Columbus now.”

The Case-Shiller index sounds more like the home flipper index. I’m constantly seeing the same trash houses selling and re-selling for higher prices every 2-3 years. It’s like a game of musical chairs and the winner loses.

It all sounds like sour grapes to me at this point.

“5.5% of all mortgages are now in forbearance.” Do we know, at this point, how many people will default on their mortgages, when forbearance program is over? Cuz some people will resume their payments when it happens. So they treat forbearance like a legal break from the mortgage. Saving plenty of $ meanwhile.

If I’m not mistaken, you still owe the $ to the bank after the forbearance period ends.

I haven’t found any definitive explanation as to what happens next when forbearance finally ends (and that itself is up in the air because lawmakers can extend it on a whim if they choose).

Eventually (if amounts owed during forbearance are simply moved to end of mortgage loan payment schedule and not due at once) delinquent owners do get a break.

If other delinquent mortgagees still can’t make payments after forbearance then foreclosures or short sales commence, unless again legislators step in and give them generous eviction grace periods, say 6 months or more.

In these batsh*t crazy times anything is possible.

No one knows what will happen. We know what has happened: some homeowners came out of forbearance and resumed payments. Others came out because they sold the house and paid off the mortgage. Others got their mortgage modified and came out. Others came out of forbearance with no solution, and those mortgages are now delinquent, waiting for something to happen. Many mortgages extended their forbearance.

Since November, more mortgages went into forbearance than came out because the total in forbearance has been rising again (after declining over the summer/fall).

It’s called inflation.

Yes, in the title of the article and throughout the article … house price inflation… dollar losing purchasing power.

As a long time home builder in Austin, I can testify the Wild West is alive and well – 2020 Covid style. Instead of an 1850s gold miner bursting into a saloon with a golden nugget yelling, “I’m rich!”, tradespeople swap stories (truths and exaggerations) after work of quick, fat paydays.

The reality is the Austin housing market was already hot a year ago. Now with Covid and the mass exodus from CA, central Austin is a bubble within a bubble. I’m not saying it’s going to pop but it’s an alternate universe.

Skilled construction labor has been waning for years. All labor in motion is simply moving up the food chain towards the luxury construction projects. Those clients have the financial means to get their houses built and those projects reset the labor rates.

Information moves so fast now that there is not a lull to capture the spike in residential real estate pricing and then decide to build at labor rates that don’t exist now (speculative construction).

Here me now and listen to me later: Skilled labor is King. It’s been taken for granted for years and it’s quickly changing. Everyone has access to internet and everyone is learning and keenly understanding the added value they provide to the equation. Good for them – they deserve it.

Our homes, for decades, have been affordable because they were built with cheap labor. Kids play video games now. They don’t build birdhouses or tree forts. No one goes into the trades and the consequences are becoming quickly apparent.

Do you think 3D printing will change that? I saw a demo when I lived in Austin, and it struck me how “disruptive” it could be.

Did The Independent sell out? I lived in its shadow for a while.

I’ve heard that the housing industry has been slow to modernize to increase worker productivity and efficiencies. Old methodologies and practices are hard to change. Stick-built houses are still the standard.

One solution for people who want a minimalist lifestyle is the ‘tiny house’ (TH) movement. Some are touting TH as an answer to climate change because of their smaller carbon footprint. I think it is just an excuse to drop people’s standard of living and call it a virture.

Even those TH products are way overpriced these days– in some cases around $50K for what amounts to a 200 sq ft trailer.

I’m well aware of the 3D printed houses you mentioned. What sounds good on paper does not make a viable product. Lots of kinks to work to make the process more efficient and affordable.

Kentucky:

Skilled labor should always be King!

My 100 year old Sears Craftsman bungalow was bought from Sears Roebuck for $600. When I explain that my home was built by the original owner(s), and cost six hundreds bucks, I like to say, “Back then, people knew how to use a saw and hammer!”

Agree 100%. My point is labor has not been appreciated. (nor really the quality of construction). Ignorance is bliss. Technology has directed people into less hard working opportunities. As a result, skilled labor is becoming a more sought after commodity. There is simply less of it.

In CO, construction and other skilled labor is essentially completely people from Mexico.

In suburban large-metro Florida prices have been rising about 1% per month since last fall. Feels like a typical RE bubble forming and you can see the commensurate parabolic move in Wolf’s chart.

With the Fed printing gobs of money and government assistance and market intervention at a high point it’s difficult to to predict when it ends and what comes afterwards.

A dirty truth is you can’t have stable asset prices with cheap money. All bubbles are built on borrowed money.

1) Beware of the biotech bubble. Rt 128 corridor have a long history of bubbles. From Berkshire Hathaway to the minis. The minicomputers industry was a short lived phenomenon. Digital Equipment Corp, Data General, Prime, Wang and many others, declared BK many decades ago. Thanks to the “innovator’s Dilemma” : bigger minicomputers for electronic engineer’s pleasing themselves when the PC was born. Is that EV & self driving cars and luxury pickup trucks in the next recession.

2) Las Vegas osc down 62% and up over 100% between 2012 and 2020.

3) NDX osc down from 9,700 to 6,700 in one month and up to 13,000 in Dec.

4) Are those markets osc & speculations inflation/ deflation.

5) Do u want to be the last bagger during the markdown. That was the fate of Las Vegas and Phoenix last baggers between 2007 and 2012/13. They had hope, praying for god, that their holdings will not sink further down. But it was not up to them. they lost control.

6) We, the guppies, can sell our entire stock portfolio in few minutes. No commissions, no bankers, no lawyers meetings involve.

7) Large institutions selling tens of thousands stocks between $150 and $3,500, need time. They need top wall street experts to do the job for them. Most bottoms in the stock markets are sharp.

8) Las Vegas & Phoenix tops suddenly collapsed. The bottom lasted between Mar 2009 and 2012/2013. The banks, taking over from the last baggers, needed auctions liquidators.

9) The auctions liquidators were very active during the saving & loans crisis in 1989/ 80. It was a great time for B&H.

I read a lot of Buffet’s stuff and like to think of myself as a value investor. It’s basically rational investing looking for safety of principal, but a higher return than you can get on a safe bond. Right now there just isn’t much out there because it’s all been bid up with cheap money, at least that is what Buffet says.

Most likely scenario for the future of is low growth since we are now encumbered with high debt to gdp. I think what they call the money multiplier from debt is down to nearly zero. What they call the natural interest rate is at near zero. Maybe if rates stay at zero you can justify the sp500 on the 1.6% dividend yield, but I don’t think so.

There is no value investing any more. Everything has been bid way up and everything will go way down. The best thing to do now is just try to protect what you got and if you lose a little due to inflation then so be it.

Rational investing has no place in a Congress-funded economy.

lol, u have been calling bubble since 2013. After 7 years of skyrocketing u still think that u are Michael Burry?

Xi Ping,

You see the bubble if you open your eyes and look at the percentages and charts. But that’s probably too much to ask of you. And no, not since 2013. But maybe since 2017… I think that’s when I started this series.

I’ll admit it, I downplayed the impact of monetary inflation for much of the last 20 years. On too many occasions, I could not get the models (anything – DCF, operating metrics, dvd) to foot to market.

So then I looked at money supply growth and compared to the S&P 500, and I realized 1. Okay, now it makes sense, and 2. Equities have not kept up with inflation

I read the book “The Big Short” and saw the movie by the same name. Michael Burry was right on the money but he was a little early. He almost lost his shirt. I heard, forget where, that Michael Burry is predicting a severe war between the counties in California over water rights if there is a major drought in the next year or so. Invest in water???

Twelve years ago someone bought the SP500 for $666. Today someone will pay $3700. Someone got a lot more for their money.

Sign of financial bubble. Tesla who doesn’t make money and bitcoin which is a financial speculation both are worth more than Berkshire Hathaway which is AA credit rated, earns around $20 billion per year and has 50 plus years of weathering every economic environment.

Either you can borrow at zero.zilch from the gov or not. And pay only the interest, hoping to receive a check soon when interest rates go negative.

With that borrowing power, you can buy up the foreclosed properties for pennies, rent them out to the peons who lost them for whatever they can pay. Everyone is happy.

since I hit 30 I could have bought a home but didn’t. I didn’t understand why people bought when they did. It was a case of if I’m right then everybody else is wrong. Maybe that’s true for Galileo and Columbus but I was pretty sure it wasn’t true of me.

Here’s the problem. People wait for low rates and then go house hunting. This creates high demand for houses which causes bidding wars which drive up prices. And people end up with low rate mortgages on high priced homes.

I thought it would be much better to wait for high rates. This should cause a dearth of buyers which should drive down home prices. If I could find a motivated seller that would drive down prices even further. In a few years I could refinance the mortgage and end up with a low priced home with a low priced mortgage. In comparison, most people end up with a high priced home and low priced mortgage. They’re settling for half of what I’m getting.

I have to say – I’m right and everyone else IS wrong!

The internets say all is well markets end year at all time highs future very bright for assets economy recoverying central banks accomadating. Everything is awesome.

Somewhat related and worth pondering (for those are freaking out):

From Barron’s, Feb. 12, 2019:

“For economic historians Japan is really a fascinating case. If you took a snapshot of the nation’s finances and demographics today with no previous knowledge of the country’s journey over the last 30 years since its asset bubble burst, you would wonder how the country isn’t in a constant crisis. Debt to GDP is the highest in the developed world at 236%. The BoJ holds around 43% of all JGBs. Core prices in Japan are also virtually identical to where they were 20 years ago and 10yr JGBs have fallen from 2.21% to -0.03% over this period. Nevertheless, Japan is an example of how long a crisis can be averted for under extreme measures.”

Japan has had a massive trade surplus with the rest of the world, and holds large amounts of foreign-currency denominated assets, and has kept consumer price inflation near zero, all of which prop up the yen.

If the yen were to dive, Japan’s cost of labor would come down further compared to other countries, and it could sell some of those foreign currency denominated assets for yen, and this would likely stop the yen’s decline.

Having a huge trade surplus is a large benefit to the economy.

The US has a huge trade deficit, and its position cannot be compared to Japan’s position.

The pandemic has given me lots of time to chase more stuff in circles. The following paper had some interesting things about trade and debt, bubbles, etc. … Japan hasn’t had too many housing bubbles lately and ZIRP seems to be sailing along. There is a section in here about the productivity of Japan, which makes them unique, in terms of being able to sell stuff that the world wants.

The Policy Trap

By the cool people @

Brookings Institution

To put Japan’s dilemma in other terms, the workers and suppliers who

are paid in yen to earn excess dollars do not produce anything that is ulti-

mately exchanged with other Japanese. They produce things for foreigners.

If the foreigners in turn produced things that were bought by Japanese, that

would not be a problem. But they do not—that is what it means to have

endlessly accumulating trade surpluses. And the deposits that go to pay the

Japanese who have produced things for foreigners without return represent

a drain on the Japanese economy …

By holding its reserves in dollars, Japan has more or less encouraged the

United States to spend and import more. The United States does not need

to pay for imports—that is, earn foreign exchange through exports or asset

sales—as long as exporting countries such as Japan are satisfied to receive

claims on the Federal Reserve as payment. If the U.S. currency were still

backed by gold, the chronic deficits with Japan would have seen the transfer

of American gold holdings into Japanese accounts. But instead, because of

the willingness of Japan to receive claims on the Federal Reserve without

ever exercising those claims, American deficits with Japan are automatically

financed

And another thing, I was just looking at FRED (again):

University of Michigan: Consumer Sentiment, Index 1966:Q1=100, Not Seasonally Adjusted (UMCSENT)

About a year ago, that sucker was around 101 and it’s closer to 77 now, and falling, as we go into our super pandemic explosion. Although mismashing data sets probably doesn’t matter, it’s still worth keeping sentiment somewhat linked to things like the 2-yr Treasury rate and or VIX. The economy and all the warped data and political polarizations during the pandemic are not going to turn-around into some perception of normal — if anything, the mindset in-place now is a mix between people going insane at a casino and people frozen in fear — not exactly a nice safe stable place.

The V-Recovery hype is reflective of stock market insanity while the near-Zero Treasury yields are reflective of slow growth ahead. As such, housing is still very much in demand, as are stocks that are linked to bubble valuations.

Will the wintertime maple-syrup slow-flow of vaccine make a difference in the next 6 months? Time will tell, but people and their behaviors during the pandemic and the overall chaotic reaction to social restrictions, suggest that a return to normal is something not to bet on.

The writings of Nostradamus, post Christmas, pre New Year 2012

What do consumers know? Most believe (still) in the Russian Collusion hoax, the Kavanaugh gang rape hoax, and continue to consume MSM propaganda. For the record, lest I be accused of being a Trumper, I campaigned for Bernie Sanders in 2016, and did not vote for either major party candidate in this or the last presidential election.