A pandemic of house price inflation.

By Wolf Richter for WOLF STREET.

House prices jumped 7.0% across the US, according to the Case-Shiller Home Price Index released today. Other indices have indicated similar price surges. House prices are going nuts despite a terrible economy. They’re being fired up by low interest rates, $3 trillion in liquidity that the Fed threw at the markets, fear of inflation that drives people into hard assets, work-from-home that causes people to look for a larger place, the urge to-buy-now before putting the current home on the market, and a shift from rental apartments and condos in high-rise buildings to single-family houses. And condos, as we’ll see in a moment, are not universally hot.

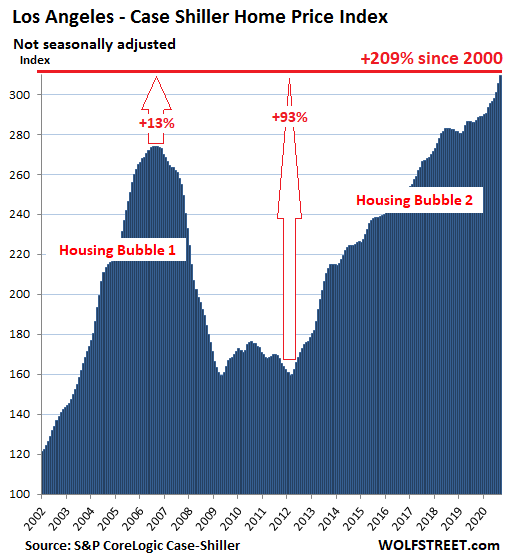

Los Angeles House Prices:

House prices in the Los Angeles metro in September jumped by 1.3% from August and by 7.7% from September last year. They’re now 12.9% above the peak of the totally crazy Housing Bubble 1, have nearly doubled (+93%) since early 2012, and having more than tripled since January 2000 (+209%):

The Case-Shiller index was set at 100 for January 2000 across all 20 cities it covers. Today’s index value for Los Angeles of 309 means that house prices have surged 209% since January 2000. This makes Los Angeles the most splendid housing bubble on this list.

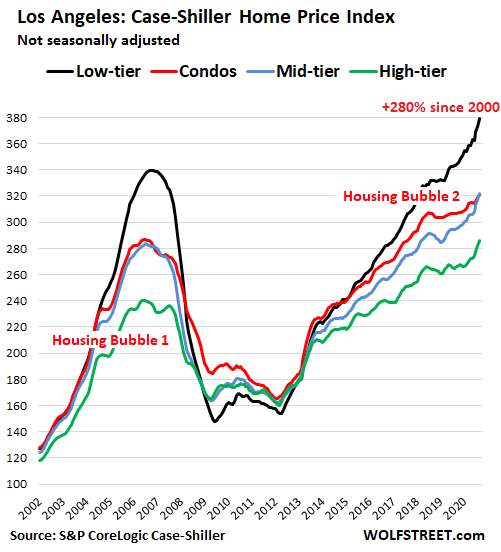

For Los Angeles, the Case-Shiller Index provides sub-indices for condos, and for high-, mid-, and low-tier segments of houses. In the low-tier segment (black line) – where people can least afford price increases – prices shot up 10.2% from September last year, having nearly quadrupled since January 2000 (+280%). During Housing Bubble 1, the low-tier surged the most, and during the Housing Bust, it plunged the most, -56% from peak to trough. High-tier prices (green line) have risen 7.6% year-over-year and are up 186% from January 2000:

The Case-Shiller Home Price Index avoids some of the distortions inherent in median-price and average-price indices because it is based on “sales pairs,” comparing the sales price of a house that sold in the current month to the price of the same house when it sold previously, and it does so going back decades. Today’s release for “September” is a rolling three-month average of closings that were entered into public records in July, August, and September. So that’s the timeframe we’re looking at.

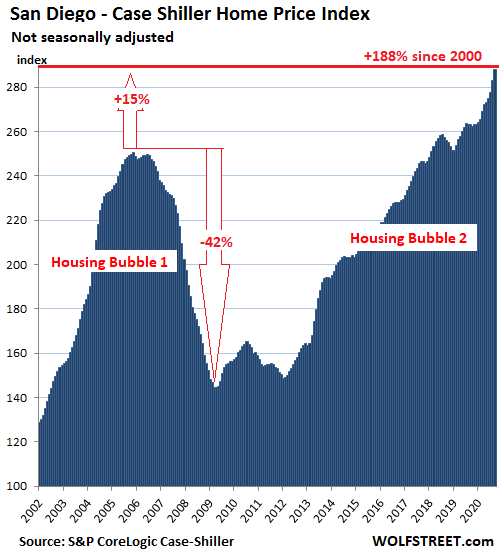

San Diego House Prices:

The Case-Shiller Index for the San Diego metro jumped 1.8% in September from August and was up 9.5% from a year ago:

This is “House-Price Inflation”: Loss of purchasing power of the dollar.

Because the Case-Shiller Index compares the sales price of a house in the current month to the price of the same house when it sold previously, it tracks how many dollars it takes over time to buy the same house. In other words, it measures the purchasing power of the dollar with regards to houses. This makes the Case-Shiller Index a measure of “house-price inflation.” And that’s all this really is – the loss of purchasing power of the dollar with regards to houses.

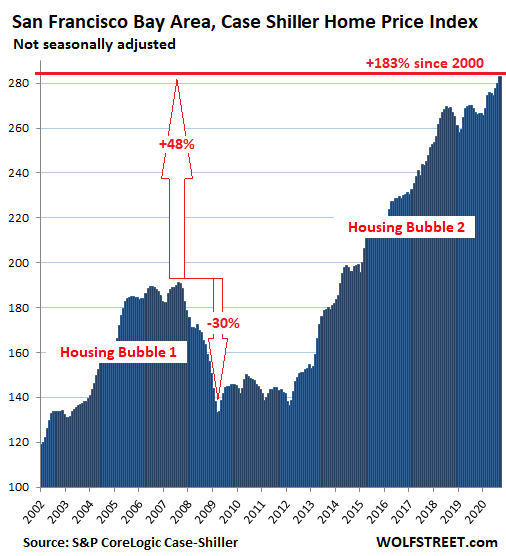

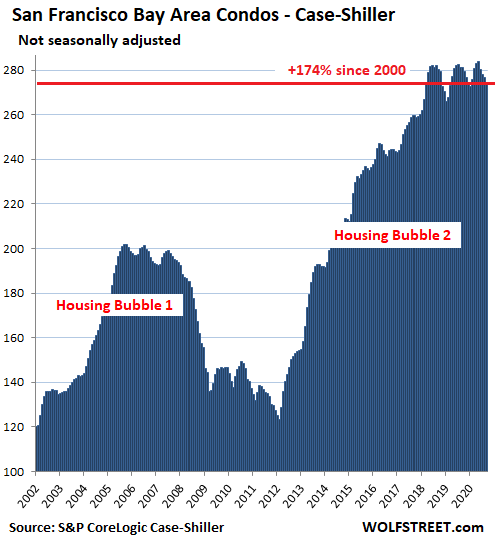

San Francisco Bay Area:

House prices in the five-county San Francisco Bay Area – the counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay) – rose 1% in September from August and 6.0% from a year ago. The index has more than doubled since 2012 and nearly tripled since 2000:

But condo prices in the five-county Bay Area fell for the fourth month in a row and are down 2.3% from a year ago, and are back where they’d first been in March 2018. Condo prices in San Francisco itself have fallen much further amid a historic all-time record condo glut, with the median price down 12.8% year-over-year. But the Case-Shiller Index covers a vast area around the Bay, including those where San Francisco refugees are moving to, and some of them are seeing rising condo prices:

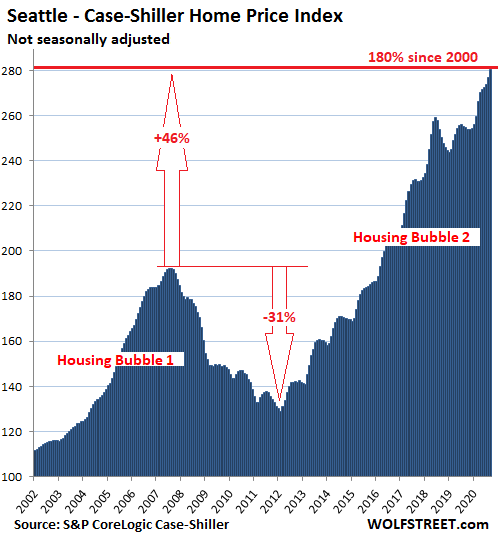

Seattle House Prices:

The Case-Shiller Index for the Seattle metro jumped 1.2% in September from August and 10.1% year-over-year. It has more than doubled since 2012 and exceeds the Housing Bubble 1 peak by 46%:

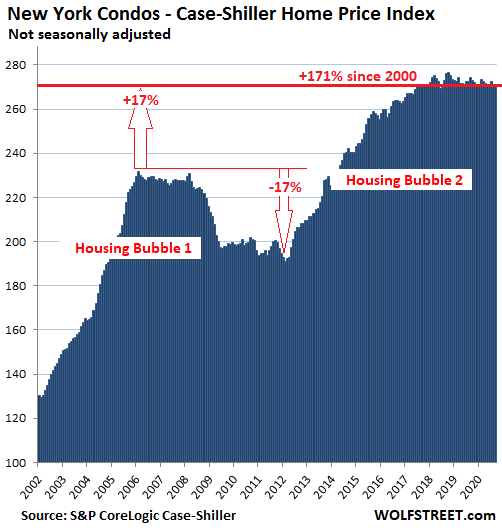

New York Condo Prices:

Case-Shiller’s area for its New York City index includes numerous counties in the states of New York, New Jersey, and Connecticut “with significant populations that commonly commute to New York City for employment purposes.” This area is far more diverse than Manhattan by itself. Condo prices in this vast metro have essentially been flat since September 2017 and are down 2% from the peak in October 2018:

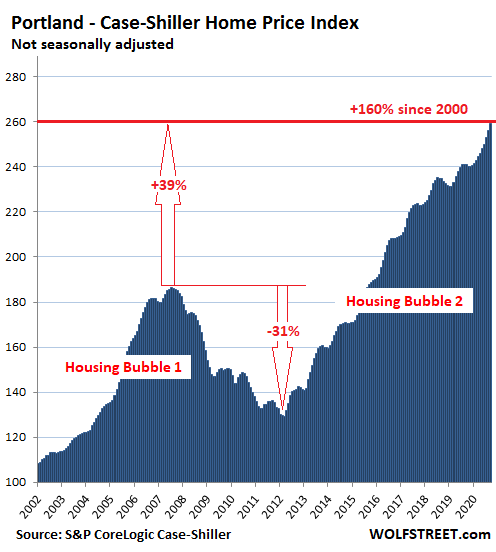

Portland House Prices:

House prices in the Portland metro jumped 1.3% in August from September and 7.6% year-over-year and have doubled since 2012:

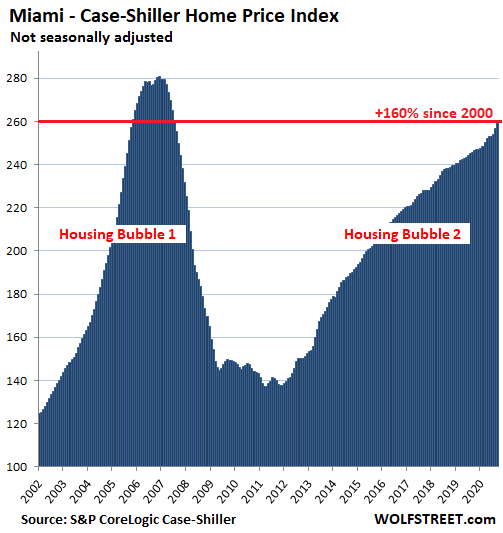

Miami House Prices:

House prices in the Miami metro rose 1.0% in September from August and by 5.6% from a year ago. The index is getting closer to its ludicrous Housing Bubble 1 high, lacking just 7.4%:

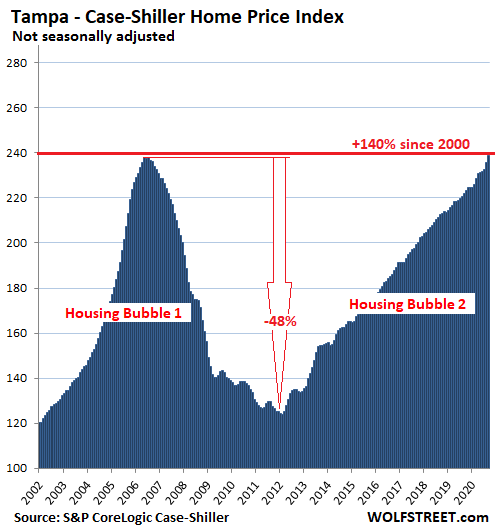

Tampa House Prices:

The Case-Shiller Index for the Tampa metro jumped 1.4% in September from August, and is up 7.5% year-over-year, and has thereby surpassed its prior crazy bubble peak of 2006:

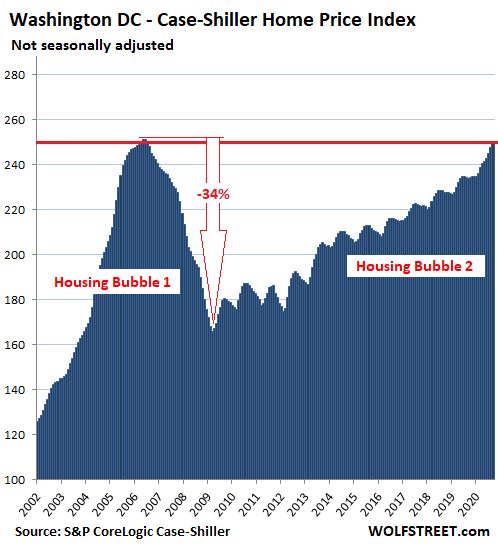

Washington DC:

House prices in the Washington D.C. metro jumped 1.0% in September from August, and 7.0% year-over-year but are just a smidge shy of their Housing Bubble 1 peak:

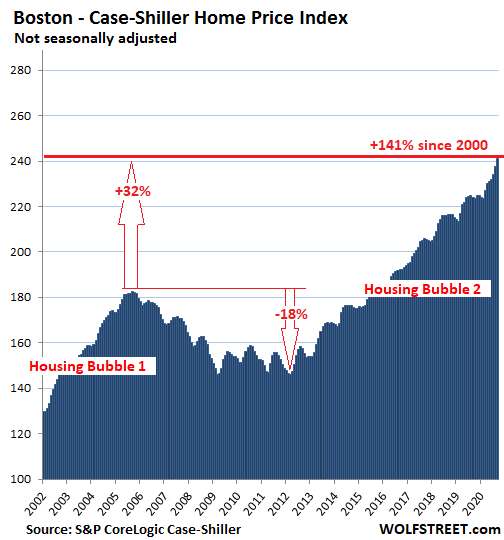

Boston House Prices:

House prices in the Boston metro jumped 1.5% in September from August and 7.7% year-over-year:

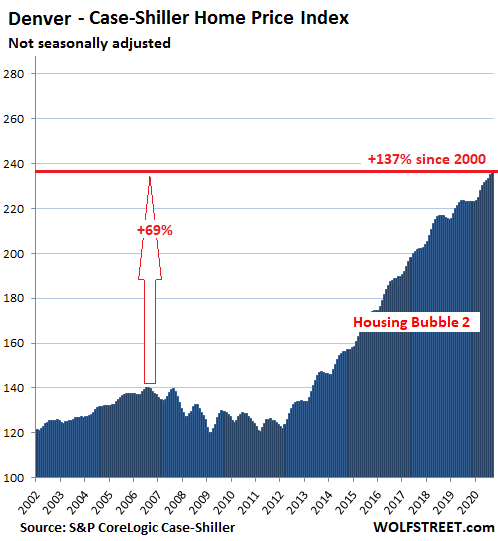

Denver House Prices:

House prices in the Denver metro rose 0.6% in September from August and 6.0% year-over-year. Beautiful Housing Bubble 2, but not much of a Housing Bubble 1:

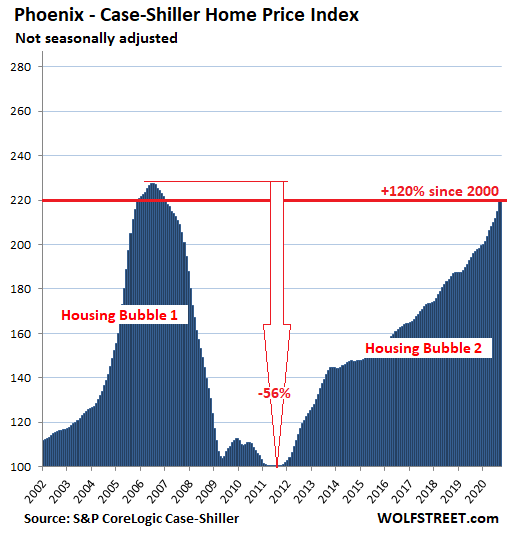

Phoenix House Prices:

House prices in the Phoenix metro soared 1.9% in September from August and 11.4% year-over-year, the hottest house price inflation of all the markets on this list of Splendid Housing Bubbles. But the index remains down 4% from its Housing Bubble 1 peak in 2006:

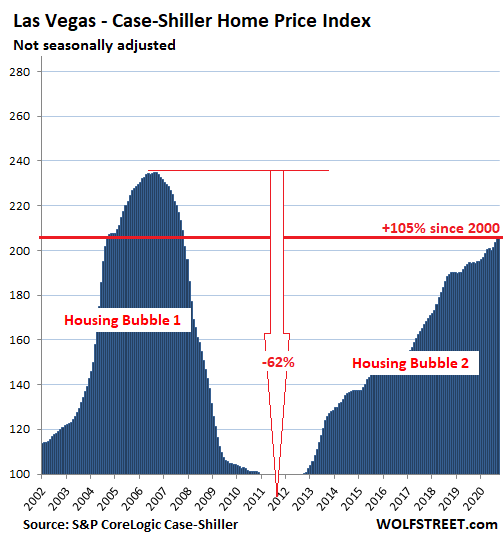

Las Vegas House Prices:

House prices in the Las Vegas metro rose 0.8% in September from August and 5.4% year-over-year. But they remain down 12.6% from their ludicrous Housing Bubble 1 peak:

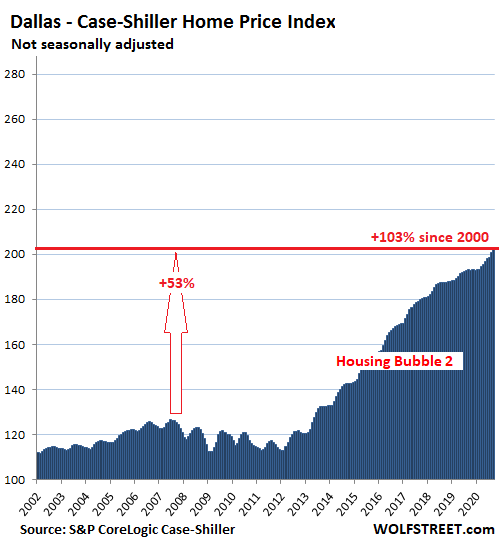

Dallas House Prices:

The Case-Shiller Index for the Dallas metro – the counties of Collin, Dallas, Delta, Denton, Ellis, Hunt, Johnson, Kaufman, Parker, Rockwall, Tarrant, and Wise – rose 0.9% in September from August, and 2.6% year-over-year, the coolest house price inflation on this list of the most Splendid Housing Bubbles:

Dallas is also the last entry on this list, with house prices having “only” doubled since 2000 – meaning house price inflation of 100% in 20 years. The remaining cities in the 20-City Case-Shiller index have experienced house price inflation of less than 100% over the past 20 years and didn’t make the cut.

Work-from-anywhere, unemployment crisis, oil bust, people chasing a cheaper less crowded place to live, the land rush to buy homes. Read… I’m in Awe of How Fast Rents Plunge in San Francisco, New York, Boston, Los Angeles, Other Expensive Cities. Rents Decline Even in Houston & Dallas. National Average Turns Negative

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Housing, the stock market and college costs have not even had a hiccup in this terrible economy.

How disconnected parts of the economy have become from reality.

“House prices are going nuts despite a terrible economy…”

So its just a mania? or are all fiat currencies devaluing in unison with one another vs hard assets as the government steps in to fill the demand void that has cratered from private industry?

so are we getting deflation or not?

Fiat currencies are devaluing in unison with one another vs hard assets;

Take a look at The Los Angeles Case-Shiller Home Price Index peaks for all housing types in 2006 and in 2020.

For example, when you price them in ounces of gold, they’re actually cheaper. Even though the y-axis for Case-Shiller is not based on $10,000 my point is still valid.

2006 2020

Home Price oz. Au Home Price oz. Au

$340,000 400 $380,000 201

$280,000 329 $315,000 166

$280,000 329 $315,000 166

$240,000 282 $285,000 150

Au $/oz. $850 $1,894

Anything the government directly or indirectly subsidizes will increase.

I’m a 32 year real estate veteran. The gutter level current mortgage rate is a danger sign to anyone looking just beyond the housing market horizon. It might seem reasonable to rationalize that your payments might be below or close to rents but consider this. What happens to the value of your $500,000 (+) home if interest rates rise by just one half of a point? Say 3.5% or 4%? Rates still below what had been healthy economy rates. Suddenly fewer buyers will qualify for higher priced homes. A slow market be omes a buyers market. Think about it.

What happens to the value of your $500,000 (+) home if interest rates rise by just one half of a point? Say 3.5% or 4%?

Depends what’s causing the rise in rates. If it’s a stronger economy overall than wage growth and lower unemployment will lead to more demand.

As an experienced real estate investor you should know that what crashed a real estate market every time is speculation. If you’re seeing a lot of it in your market market be careful.

Get real…look around you. The economy is definitely not growing and new unemployment claims was over 709K last week. I’ve never seen numbers this high.

The question Thomas is when and how much interest rates rise and if rising rates are even possible given the ramifications beyond housing. I get your point though, people buying for a low payment and then a job loss and or a move and not enough cash to bring to the table to sell.

PS, in general, are mortgages today non-recourse?

Bart,

There are 12 states in which “purchase” mortgages are non-recourse. But refi mortgages in those states may be treated differently. In 38 states, mortgages are full recourse:

https://wolfstreet.com/2018/06/20/us-style-housing-bust-mortgage-crisis-in-canada-australia-recourse-non-recourse/

Bart,

people forget how fast a market can change on a dime. The bond market is no different than any other market. Once bids dry up or defaults happen a meteoric rise in rates will happen. Go back and look at the South American countries’ bond rates when they had their crisis. Brazilian banks were paying 10% on a savings account.

I’ve been pounding the table for years about this happening. I’m glad there is another genius out there like me.

I blame HGTV.

I have noticed on some of the episodes of HGTV that they are tearing out granite counter tops to install quartz. Its their money, but gee whiz is it so hard not to have the latest thing.

I’m getting quotes to replace my quartz with unobtainium. It’s the next thing. Don’t be left behind.

?

Here in Canada the whole house is made of unobtainium… so there!!

Next year they will tear out the quartz countertops and install some made of unobtainium.

We are going back to Formica counters since it’s “back to basics” around here!

Great time to get a very very low cost used granite countertop. Talk to your local counter man and offer cash.

Granite countertops were a fad mistake. They’re hard to keep clean. Literally no one has the mental capability of resealing them annually to prevent water and other liquids from seeping through cracks and staining the countertop. I’ve seen 50 year old tile counter tops that still look decent with minimal maintenance, even with a lot of use.

Bonus: Busy granite countertop patterns make it difficult to find small objects you drop on the countertop. If you really want to flaunt your wealth, get marble countertops that need to be resealed every 3 months!

hikusar,

“They’re hard to keep clean. Literally no one has the mental capability of resealing them annually to prevent water and other liquids from seeping through cracks and staining the countertop”

You’re confusing granite with marble, a common mix-up.

Granite is an ancient hard rock (age measured in billions of years) that when polished is like glass, and is non-porous. You can clean countertops with Windex. Granite countertops will last thousands of years in perfect condition without re-sealing unless you break them.

Marble is a soft relatively young limestone (age measured in millions of years) that is fragile and porous and needs lots of maintenance, including re-polishing from time to time, and re-sealing.

Wolf, the more exotic natural granite that is “grained” and has a lot of crystalline structure does collect “stuff”. I cut my own countertops out of large exotic scraps- an installer’s mistake. Some of this stuff just has a lot of grain and tiny cracks throughout. While technically, mine don’t stain easily (or at all) over time oils do seep in, even with sealant. This leaves a slightly darker color which sort of saturates throughout the piece. I gave up and just applied coconut oil to the whole thing.

You can blame them for environmental waste as well. Every time they walk into a perfectly functional kitchen, the lady says “this has to go”, as though kitchens are part of the wardrobe. I shiver to think how much of the environment is wasted because of peoples’ need for “style”. What’s wrong with something that performs its function well?

Yeah, and most women don’t even cook anymore!

not so fast AA:

Don’t know much about your environment, etc., but the only woman I know who doesn’t cook is my 90 yo mil, who has two daughters who are loving the opportunity to cook for their mom, and share with any of the family around them…

Even a (4.5 yo) grand niece is really getting into it with her grandpa, a former pro chef, etc., now retired and loving the opportunity to cook with his grandchild…

Of course, I don’t know ”most” women, only a couple of hundred IIRC, so maybe should just consider my self fortunate that my retired chef spouse continues to love to cook.

Brutal! But nesting is a thing, I guess. Keeping up with the Jonses. Maybe sick consumerist culture taken to an extreme.

I don’t know if I have granite or quartz or whatever countertops. I just know I moved from an s-hole Studio in a bad part of town into a 1-Bedroom that’s much nicer. That’s enough for me who is used to barely having anything.

VVN, you are a lucky man! Restaurants are FULL nightly around here so I know those women are not at home cooking!

Hubby cooks. He hasn’t asked for a new stove – yet.

Slightly off thread:

I nabbed a $25.00 slab of formica (affixed to 2 glued -3/4″ dense particleboards, to form a 11/2″ base) from the local Restore outlet, and proceeded to fashion a combo hat/coat rack/room divider screen above, with open firewood storage cabinet below.

Said formica surface actually looks like polished granite .. with both matt and shimmery sheen incorporated within the laminate, simulating both quartz & mica .. and was completely blemish free. The unit is better than anything manufactured, as it suited to our prticular household needs.

I my point is that I had created a unique piece of ‘furniture’ utilizing both new and used/salvaged elements. Fun to build, and highly functional as well. Had it been offered as a store item, it easily would have cost double, or even triple the price of materials alone.

The labor however, was ‘cheap american’ ..

‘;]

Speaking of ‘environmental’, granite off-gases radon and adhesives for gluing the countertops to cabinets off-gas VOCs. Cutting, drilling or sanding stone yields silica particles.

Bobber,

I totally agree. Having said that, you are just a curmudgeon. (sarc)

Agree. The amount of waste with home re-selling is mind-blowing. I’ve heard of sellers putting in entire new kitchens ostensibly to sell their home and the buyer tears it all out – wifey or realtor didn’t like it or it doesn’t meet their ridiculous standards. Thanks to copious marketing in the last decade or two, the masses now believe they are entitled to “luxury” at any cost. It’s your god given right!

Consumerism run amok. Planet shmanet! Who cares about the planet when you can tear out a perfectly functional but perhaps “outdated” (the horror!) kitchen and install a gleaming, cool and clinical white and gray kitchen that looks like it came from a spa or urgent care center? Gotta keep up! Be like everyone else or what will the neighbors think? Or better yet, outdo those darn Joneses across the street!

I have been checking out a few real estate gurus’ websites, and nearly all of them have said they have been making more money than expected due to the HGTV effect, where newbie investors see these flipping shows on HGTV and spend more money than the should on fix and flip properties.

You should see what “flippers” are paying for crap houses with major, major structural and safety issues around here.. 1940’s electrical, severely sunken slab foundations, old “renovations” removing structural walls, grow houses with extra drywall recently applied right over the moldy stuff. I even saw a mock perimeter foundation comprised of cement basically just troweled right over post and pier.

Saw a friend bought such sunken foundation foreclosure and put a wall and pillar underneath. I don’t know if that will cure the problem. How can new buyer find out this structural defect?

If you believe inflation is in the cards, what better investment than a house.

First you get a 30 year mortgage at unbelievably low rates that you certainly will pay back in inflated dollars then on top of that value of the house goes up protecting you from said inflation, double whammy indeed. The best time to buy real estate is alway five years ago.

The ‘time to buy’ is when no one wants anything to do w/RE.

When [not if] rates rise, there will be epic write downs.

Not as drastic as the 80’s, though everything goes in cycles.

Patience Grasshopper….

Addendum – recently noticed an abundance of existing entry level ranch design (3bd/2bth) thats seen no activity past 60 days. Adjacent ‘hood is Macmansion developments near Nike & Intel operations

An anomaly, or something else unfolding?

As always, may the sun & wind be at your back.

Nah, not if you are geo-arbitraging you sell for $400/sf and buy for $100/sf. Its a K-shaped recovery. If you have a reliable job/income stream, you can get a lot of house for a very low monthly payment. in some instances, the annual mortgage payment is less than past yearly property tax payments.

? What are inflated dollars?

Toilet paper.

h1730, actually, toilet paper is going up versus those inflated dollars

One example using a metric that everyone can appreciate:

The 2020 dollar that buys you a tiny candy bar versus a 1970 dollar that bought you 20 larger candy bars.

People who had 15 year fixed rate mortgages originated from the mid-60s to mid-70s rode the inflation wave from mid/70s to mid-80s.

Yeah, only if you think no one will ever have to pay rent and their mortgages ever again… lol

I think more people will rent as real estate becomes more expensive.

But this is the major trend our society is evolving to, you don’t own anything anymore, just pay a monthly fee, like your phone bill.

Once we rent everything for a monthly fee, private property will cease to exist.

That is by definition communism by subterfuge. For the plebes only.

but on the plus side, we will be happy once we don’t own anything.

And with one bullet in the head of the owner… you can easily transfer from renter to owner… and the scheme you layout falls apart… as it always has… lol

Memento mori,

That sounds like feudalism, as for house prices it will depend on location. After the pandemic ends there could be massive layoffs, especially, for those working from home, and the question will be where will people move? Anywhere a significant number of people move away from will see a massive drop in house prices. There is also a lot of people who are about to enter retirement age who might try to offload houses. There also has to be enough money and credit for house prices to jump.

I live in China, where everybody owns their own home. And don’t believe what you read on the Internet about owning land. In China you have the right to exclusive possession and sale, just like in any US condo, association, Planned Unit Development, co-op, or HOA. This agreement has a set period. When this is up. the city can buy you out or it rolls over. It’s just another type of Eminent Domain.

I don’t see many countries where this “communist” type of ownership exists.

Makes me think of Doctor Zhivago.

roddy6667,

Most people are referring to the Soviet Union. As for China, the local governments in China can take back land at any time to resell and they usually pay those living on it, little to nothing. Alot of people rent and even when you do buy property, the building developers almost always bought it as a, usually 70 year lease. None of those leases have ever expired yet, so no one knows what the end result will be when those leases expire.

For the creditor class who own all that private debt. Pretty sure they aren’t communists. Pretty sure they are almost 100% capitalists. The fabled One Percent!

I do agree with you on the 30 year mortgage as that is not a natural interest rate and could only exist at these rates with government subsidy.

A lot of people don’t realize they are using more leverage than wall street if they are only putting 3 – 5% down. I don’t really know how I feel about leverage on a house. There are pros and cons, but when you are young you don’t have much choice usually.

In my parents day it was all about paying the house off as quick as possible. They bought one house. Paid it off in ten years and have been living without a house payment for 55 years. Taxes are now about twice what their house payment was 65 years ago. Their cable bill is 3 times their original house payment.

I recall my father’s $107 home payment for everything – PITI. In the 60’s, contract not mortgage.

The Fed certainly is propping up the risk taking. Anyone that put 5% down in these areas got 100% plus year over year paper return on investment, just like it works on Wall Street. Got to know when to take profits if you are a speculator.

When to take profits? We call that a home equity loan. A mortgage is a non recourse loan in many states — if you default they can only take the home and nothing else.

Second and subsequent mortgages, e.g. HELOC, typically have full recourse. You’d have to take your profit to another country before default.

Lisa,

Good catch regarding deficiency judgments on defaulted mortgages.

One really big question that is rarely addressed.

During the housing implosion, about 8 million home “owners” defaulted (out of about 50 million with a mortgage, out of 75 million SFH total).

What ever happened to those potential 8 million deficiency judgment obligees?

Lenders always want their damn money back and are not lazy about angling to get it…but there was very, very little commentary from 2008 to now about all those deficiency judgments.

(Not to mention the fact that those 8 million households almost certainly couldn’t get another mortgage with a deficiency judgment against them outstanding).

There were too many (millions), it just wasn’t possible, and these defaulted borrowers didn’t have assets to go after, and so banks essentially gave up. They just didn’t have the resources. And the political will had turned against them.

But in the regular course of business, when banks have only a small number of defaulters, they’ll take them to court following the foreclosure sale if there is a deficiency.

“If you believe inflation is in the cards, what better investment than a house.”

If you are an investor then you’ll need to run more or less complex financial simulations to decide every single investment in housing.

If you need a house to live, the biggest question is whether you plan to live in it for the next 10 years. So, unless you are a house flipper (gambler), the question of buy/rent boils down to you capacity to commit to no mobility/upsizing for at least 5 (better 50) years.

World’s only getting faster. The only people staying still are the retired or the people who never leave their small communities and stick close to their families.

I can’t imagine owning a home ever. Lifelong renter. If I do get some type of permanent residential asset, it better have wheels.

You’re better off owning a duplex or small apartment building and doing house hacking where you live in one of the units and rent out the rest of them and have the tenants pay your mortgage.

You know there is more than one way to put a roof over your head.

I myself got out of the stock market and retired at 47, mostly due to my 6 rentals. Thus, I’m a fan of people who choose to rent.

Yeah. Buy now at the peak and ride the crash into a life of being upside down in your mortgage. Every day you will see homes much nicer and larger than yours in better neighborhoods for 30-50% less than what you owe. But you can’t sell. You can’t even move to another state to take up a lucrative career advancement. You just have to sit there and make the payments. What better investment than a house?

Been there and done that.

Aaand while you’re waiting for the 20% drop in 5yrs, houses would have appreciated 40%. Aaaand when the market drops and you’re trying to deploy that dry powder, no bank will give you a loan bc housing is now “risky” and you have to compete with all of the deep-pocket investors at the courthouse steps who are itching to get into vast SFH rental. This idea that you’d be able to swoop in for a deal when we’ve been under-building for 10yrs and boomers have another 20 before dying en masse, is a pipe dream.

Oldest Boomer is 74. They’re starting to die en masse right now. 18 years worth.

Buy a new house then walk away from the bad deal.

Like people did during the last crash.

All I want to know is when and how does it end…

It all ends when lockdowns have forced everyone into default, while the CBs run out of things to buy with free money.

– “while the CBs run out of things to buy with free money.”

The way out is found for CB buying:

material things are finite,

services are infinite (based on self-regenerating worker’s time) – whether useful or not.

Engin-ear:

“services are infinite”. Yes I think you are onto something. I made a similar comment a while back.

Let’s see:

I form a startup to lend my engineer buddies’ time to big tech @$200/hr., say fifty of them.

Then, issue $20M AAA rated bond back by future income stream.

Sell the bond to the FED.

Divvy up the proceeds among us, close down the shop.

Everybody happy. Right?

It’s always a supply/demand imbalance that moves the markets. Whether it is stocks, bonds futures, forex, housing, etc. It matters not the market. Right now in Phoenix it’s more of a lack of supply that started the price increases. Then Covid strikes, WFH becomes the rage and now every Realtor in town is practically begging people to list their home because of a surge in buyers moving in from Cali. Now its a refusal of homeowners to sell their property coupled with a overnight doubling of buyers and voila- instant bubble. Home builders are slow walking their developments, no starter homes here, just big ass 4/3 and 5/3 homes with hefty price tags.

So to answer your question ” when will it end?” My guess is it will end when the supply and demand equalize. That could take awhile. I don’t see a collapse though, more of a boom/plateau. The underwriting standards are fairly high and the buyers are serious buyers with an intent to occupy the home unlike the last RE boom/bust.

SATYA

I concur. Most Buyers are qualified in a traditional sense but there’s just nothing out there for sale.

Defaults/foreclosures will be nothing like 2008-2011. As such, any price correction, with interest rates at perpetual ZERO, will be minimal even when supply does begin to meet demand.

A couple in SoCal just bought a $1.5M home.

They earn somewhere between $240k and $280k per year, before taxes.

This couple has a little over $100k in student loans and an additional $30k in credit card debt.

Payments on the cars are $800 for another two years.

Down payment came in the form of $250k “loan” from family.

Bank needed to see nine months of payments in their bank account, so they raided their 401k accounts.

They will be spending $200k to remodeled the home as soon as they can refinance and cash out equity when the six month requirement is up.

Daycare cost is in the $1,800k/month range and it will go up as baby gets older.

Property taxes are in the neighborhood of $1,300/month.

Lifestyle choices include(d) international trips, wine clubs, and takeout from “nice” eateries.

How do I know all of this? Because they must have a need to confess, in the hopes that everyone they kniw with is also drowning in debt.

These are the kind of “credit-worthy”, “qualified” people who are buying properties that banks are all too happy to underwrite loans for.

Good luck having to make a $12k nut every month – and I don’t care how low interest rates go – that’s a prison sentence I won’t sign up for no matter how crazy the housing frenzy gets.

BHSL,

It’s almost like they perceive no risk in buying a home. The National association of Realtors must be estatic there commercial propaganda has so throughly entrenched in purchasers minds.

Funny how I hear many Chinese buy property with the same mindset knowing the CCP will backstop any housing market failures. What could ever possibly go wrong? :) I guess Americans can take solice in the fact that contractors would mix cardboard into their concrete that will fall apart in 3 years or less. Although I don’t want to give them any ideas

If you are retired you can still find cheap housing in rural areas if you are familiar with the state (NC). Got to do your due diligence to make sure you are in low crime, low tax and good cultural fit. Newish mobile homes are well built and will last at least 50 years. $70,000 or less depending on age. Small brick ranches were well built in the late 50’s and 60’s and can be found for around $100,00. Usually you can find the above on a 2 acre lot 30 miles or so from metro area.

Good Start OS:

Middle/later part of the last crash, (middle of ”nowhere/flyover”), a friend was paying cash at the courthouse steps for 2/1 small houses in our county seat, putting in another $2-5 rehabbing, then either renting and refinancing, or selling for $25-30K…

Similarly, in SWFL, in 08-09-10, I saw waterfront houses, good ol’ ranches, on canals, but with dock and ”sailboat water” to the GOM going for less than 30% of their high $$$ in 05-06,7?..

This crash appears to me to be hugely distorted by the pandemic/work from anywhere, etc., and it only suggests to me that the time to bottom will be a bit more than last time.

V V,

Unlike the last crisis which was an employment and credit crisis, the next one is one of political corruption and ineptitude.

People are not leaving CA because they have lost their jobs, they are leaving because they are overtaxed and over regulated. Chicago will become the next Detroit due to high crime, crazy real estate taxes, and dumb governance.

The bottom is falling out all over the place. Sometimes it’s a whole state, sometimes a whole city, or it can be more local, like a certain section of town. It is different this time.

Boom/ plateau, is that wat Fisher said about the stockmarket in 1929?

Hey Petunia,totally agree.Grew up in n.w. Burbs of Chicago,ex. Is in west town of Chicago.Bankrupt,leftist,pro-looters are terms coming to mind.Lightfoot just today came to crap agreement with citycouncil on More taxes!! Property taxes,I believe will go up,because they do not pay emough!?Gas taxes hiked and some other goodies so they didnt have to cut city jobs.I wonder how Equitable it will be to the struggling homeowners and small holder landlords????

“It’s always a supply/demand imbalance that moves the markets.”

Well said!

@ Satya Mardelli

The growing disconnection between assets bubble including housing prices and the reality which is being brought slowly by descending 2nd Covid spike is unnerving to say the least!

Every one here, thinks there will be a ‘soft’ landing unlike in 2008. No chance of collapse blah, blah. Same thought was prevailing in 2006-’07!

There will be at best K shaped, not V shaped. How many businesses and Jobs are going to be lost permanently? How many sectors of the Economy will come back to pre-covid levels by next spring/Summer?

Every one and his uncle think Vaccines are “here’ and pandemic will be story of the past by spring/Summer?fall!?

REALLY?

Watch the Economy and the mkts for the next 8-10 weeks!

Compare the level of DEBT ( private/public) now vs 2008. Fed(CBers) have been kicking the can year after year. This year’s deficit is over 3 Trillions! MMT will take care of it, right?

2nd stimulus NOT in sight. Even it comes it will be small and not effective until March. Global Economy is already tanking.

More will join the unemployment in the 8 weeks! More renters will homeless. More defaults and bankruptsies!

Covid infections, hospitalizations, mortality & morbidity increasing by weeks if NOT days! GDP could be negative for Q4 ’20 and Q1 ’21.

However housing industry will be barely get affected right? I am NOT that hopeful. The problems in global Banking industry which brought us GFC, NEVER got addressed, just masked with more debt. The ticking time bomb just got bigger!

Golly, it is like the “technology” necessary to build sub $200k houses (big wood boxes basically) has been lost to the American mind.

So little to no extra housing supply despite an extra 10 million looking for work.

Incredible rigidity is destroying the American economy.

The when is easy- it ends when you die.

“In the grave, my boy, in the grave.” – Mr. Natural

I’m waiting for the graveyard plot bubble. Then you know things are messed up.

Well, there’s been a run on refrigerated mobile morgues in NYC and El Paso.

It ends when the people trying to end America finally succeed…

I live in the Dallas area and my house has gone up about 73% in the past 11.5 years, however after taking into consideration the amount of things I needed to fix (new windows, HVAC, roof deductible, plumbing repairs, pool pump, etc.), and after considering sales costs when I sell soon, the increase is really “only” 30%. Raw math that is only about 2.6% per year. Still better than wasting money on rent over the past 11.5 years.

Maybe better than renting, maybe not. Depends on what you would have done with the down payment money that you have invested in the house instead of a different type of investment.

Zantetsu:

I don’t agree with your outlook. The “different type of investments” have their own problems.

If rent and mortgage are equivalent, and the down payment is small, there are very few scenarios where renting makes more sense. And you do eventually pay off a mortgage and own a home, with rent, it never ends.

Ultimately, I buy houses to live in. If I make money on it when I sell, great, if I don’t, well, I still had a place to live.

Don’t forget the high TX property taxes paid, which may or may not have been deductible.

And the mandatory insurance costs if you had a mortgage.

Won’t find a dog or marijuana plant suffering homelessness.

I knew a guy. He smoked marijuana for his medical condition, and he had a beautiful golden retriever. lived in his van with the dog. His nurse felt sorry For The Dog, and bought it from him. Lol. Let’s not give the guy a place to live, so he can take care of his dog. But this was 6 years ago, and some things have changed.. But more like a rotation of people through the system. He’s dead.

This is about house inflation. And you get this bizarreness because home is where the WiFi is. Did you read about the woman taking a bus two hours to a place to charge her cell phone? Electricity and WiFi. And heat, that’s about it. And a fear of Kraken. Which is fear of homelessness, but this is code. fairly deep political code, considering the people involved and what they are doing.

I have no idea what this has to do with housing prices.

I think it had to do with reefer…

dogs and plants, apparently, can afford to overspend on housing and therefore drive up prices? that was my take.

dog,

If and when you are ”un housed” (the current PC version of homeless,) you will know what it has to do with housing prices and availability, and I speak from long experience in residential real estate and the construction industry, and having been on the streets a bit in my wilder younger days…

These cycles of RE markets first came to my attention in 1956, when dad had no work for six months to the day, right after buying 3 properties, then leaped right back to work into the beginning of the next boom.

That one was due to the let down from the Korean war IIRC, but, no matter, fact is that these cycles have gone on for eva,,, and the actions of the federal bank have just made them worse and worse, and will continue to make them worse and worse until the whole shebang falls apart, which, as has been said on Wolf Street many times, eventually it must.

When will it end? Never IMHO, just have various lows and highs and timings, mostly local as commented earlier; so, basically, watch carefully where you want to buy, and keep your powder dry.

So if I decide to start living out of a car, I should spend some of the savings on rent towards a chronic chronic consumption?

I tell ya, the stuff does allow you to put up with a whole lot, including four years of insane politics. However, murders productivity.

Dur,did she not think of a B.K./Mc.D.,or library/community center?

Yeah. If the percentage of people who are homeless increases as much again as it did in the last recession then everyone is going to have a problem. Except the dogs. Most homeless dogs who are still with their people look pretty happy to me. The people- not so much. Twice as many homeless people won’t potentiate anyone’s carefree enjoyment of resources.

I’m not sure Seattle is having a housing bubble. Inventory is very tight. The economy is great. If there is one part of Seattle that could be argued is in a housing bubble will be on the north side by Everett. The 787 production is moving to South Carolina so all those jobs and supporting job will disappear so that area could implode.

I’d love to know your basis for saying Seattle’s economy is “great.”

It’s a boom town for car enthusiast movie makers, who like to display their restored classics cruising the entirety abandoned downtown of Seattle. The cars look beautiful roaring through empty tunnels, floating by forgotten and boarded up business and malls. The homeless left last, but there is nothing left downtown for them. I filmed my video in March but have seen many of them on youtube by now

Wow, I just had a flashback to 2006

+1

Most every one here, has a some kind of ‘rosy’ outlook on housing and the economy which has to support it in the coming months. Been in the mkt since ’82.

Every day Indexes are zooming with no real concern of the economy on the ground. I get an unsettling of approaching ‘an ice berg’ soon and a replay of titanic and 1929 together!

I hope I am wrong!

Check out the Harry Dent interview on Kitco. Lands like a cocktail shaker tossed into a dry crowd, the running and screaming always comes after the oohs and awes.

Very very good article. In particular the 1st paragraph laid out so many of the fundamentals of rising house prices. And yes, a good house is an excellent hard asset, and while there might be dips and dodges going forward, the trend as long as I have owned a home is ever upwards, and housing value has kept pace with inflation. I bought my first home at age 24, and 40 years later…….

Of course the rise also reflects the decline of currency, but is all relative.

Besides, a person has to live somewhere and if a mortgage payment is close to rents, buying is a no brainer.

Resisting the temptation to trade up and refi, will set a working man/woman up for life. Of course this also depends on your taxation area, but that factor should have been figured in at the beginning.

My son just closed on a home, in Campbell River (Vancouver Island). It is one house up from an unobstructed waterfront view, and has an excellent view itself. Being single and stretched with the purchase, wary of the economy, he will finish off the basement suite and rent the upstairs out for Jan 1st. For now. The rent will cover the mortgage and most of the taxes. He has another home which he also rents out. That rent also covers the mortgage and taxes. This place includes 3 acres of riverfront and near Dad. Son is 36. In twenty years he will be 56 and the homes will be paid for, by the renters.

Today’s market is different than the 08 bust. I no longer hear about liar loans and insane flipping. Speculation. It might be impossible to get into a ‘top tier’ market, but there are many many good places to buy that are affordable.

I don’t think you could find a house in BC that the rent will cover your mortgage and taxes, and I challenge you to find a listing not now, but within the last 15 years that meets such criteria.

BC prices have been beyond bubble the last 20 years mainly supported by money laundering activities from China and they are completely decoupled from any reality of rent vs price metrics.

Memento, I was looking for properties around Mission, Agassiz with a little land. Forget it. Very overpriced. Awhile back I read about the Chinese sending out their money with BTC and converting it and buying homes. Some are empty shacks. Yesterday there was an article of wealthy Americans scrounging for 2nd passports. I’m one of them, but not a wealthy American! I love BC, Canada, but overpriced, but as long as the money is there the prices will be supported.

This time is different.

@ Paulo

‘Today’s market is different than the 08 bust”

The structural problems which brought us the GFC, NEVER got fixed just covered with more debt on debt along with financialization of most of the economy, with a lot less going towards productive economy on an organic basis.

For examp: BA spends 43 Billions in buy-back shares(’09 – ’19) , but spends NOT a dime on fixing the festering problems of 737 Max.

This is NOT 2008, true but there was no C 19 infecting over millions and over 1 millions deaths world wide and 230, 000+ counting in America.

2nd spike of the virus has just begun! The amount DEBT 2-3X over the value of the collateral asset both in private and public sectors.

Global DEBT over GDP is 255+Trillions/ 100 Trillions ( 25-30 T more since ’09) 50% or more of Corp Debt is close to junk grade.

Deficits and Debt don’t matter right.

MMT might take care of Public debt. What about private sector debt? unless the coming new Secy of State might recommend buying STOCKS ( she said on record!) also in addition to all Corp debt, right?

Interesting weeks, ahead!

“ever upwards”

In the 2008 implosion (“brought to you by ZIRP 1.0”) 8 million households (out of 50 million with a mortgage) defaulted.

That isn’t ever upwards.

Wait until you see what ZIRP 2.0 hath wrought…

“House prices jumped 7.0% across the US, according to the Case-Shiller Home Price Index released today.”

The internets say my house is rising 2% per month. That about matches my observations of sales and new listing in my neighborhood.

Like I’ve been saying for years, real estate is NOT going to decline unless the stock market declines.

And the stock market is not going to decline unless the Fed’s recently acquired power of QE is taken away from it and interest rates are normalized.

Just like I said long ago we a Debt Jubilee is needed and would benefit the economy. Guess what: We’re living a defacto Debt Jubilee, it IS benefiting the economy, and formalizing and legalizing a Debt Jubilee further benefit the economy.

Just like I said we can’t win a trade war against China because China has options. Guess what, we lost our trade war against China.

You know that you’ve got a problem if home prices rise 2% a month,right? Because wages don’t rise 2% a month. They might not even rise 2% a year. So after a while of these kinds of house prices surges, demand at these prices collapses.

Even worse is crazy rapid increases in home sale prices with average rents decreasing.

I friend just left a job after 24 years and his new job pays him $1 less /hr, accounting for inflation, than I made in 1986…….with 3 years experience.

Real wages have gone nowhere for decades. RE is completely out of reach for the average person in Socal.

The purchasing power of the American middle class has backslid to 1967 levels.

Right, and that’s the ultimately problem with the government’s inflation numbers. It excludes so much that we don’t have a choice on, like housing, education, health care, and groceries. Upper middle income people can generally deal with it, but it doesn’t do much for the true middle and lower classes who can buy cheap gas (to not drive anywhere) and cheap LCD TVs.

I agree with this, government inflation stats vastly understate inflation for the most important things.

But you do have a choice with education. The educational costs for my children (public schools K-12, inexpensive state and private schools for college, all children successfully employed) has been a fraction of some of my colleagues, literally 700K less in one case.

That’s what banks are for Wolf. With their fancy derivatives and custom Excel spreadsheets, in theory nothing is too expensive!!!

I have a feeling that investment gains are, in addition to wages, a significant driver of housing sales at the higher end. I’ve been sitting in a chair the past few weeks watching my brokerage account rise reliably like the morning sun (yet, there is no good reason for this), and this stock market success has me thinking about upgrading my housing situation. If people “earn” cheap money in the stock market, I think they aren’t afraid to take additional risks in the housing market. In my case, absent stock market gains, buying an overpriced home would be the last thing on my mind.

Sell some Amazon or Tesla, pay the taxes, buy a multi-million dollar home for cash. Repeat for some cars and maybe a boat. Stock market only goes up and there will always be a buyer. Scares the hell out of me.

Bobber, I suspect there are many in your boat. But that actually illustrates well the artificiality of it all. People aren’t selling those stocks to get the money for these housing upgrades; rather, the paper wealth gains causes them to spend OTHER money they have. But of course, if there was any significant amount of selling of these stocks, prices would plummet. So the “wealth effect” is that everyone’s wealthy and should consume only works so long as no one is selling.

NYer,

“So the “wealth effect” is that everyone’s wealthy and should consume only works so long as no one is selling.”

Excellent point too rarely made.

Ties in with how marginal pricing of stock shares creates a false impression of what true mkt cap is.

Resist that urge!

Cas127, exactly. I’ve had that argument with coworkers about valuation. The fact that someone is willing to pay $1 million for 1% of a company (valuing it at $100 million) doesn’t mean that you’ll find someone willing to pay $20 million for 20%.

Your point about marginal pricing is a good one. If there are 10 million shares outstanding, if the volume in a given day is 20,000 shares, the price is only a function of what sellers and buyers for those 20,000 shares were willing to sell for and buy. We have no idea what the holders of the other 9,980,000 shares would require to sell THEIR shares, and how much the other buyers in the theoretical “buyer pool” would be willing to pay.

To buy the whole company, you might have to pay $140 million — a 40% premium. Slack jumped 38% today after rumors emerged that Salesforce is in talks with it to acquire it.

The more demand for the shares, the higher the price. If you want to buy 20% of the shares of a company, the price is going to soar. Look at the Buffett announcements.

Wolf, correct, but that’s generally in the case of a smaller company for which you’re paying a premium for control.

I doubt any large institutional investor would want a majority stake in Tesla, for example, at current prices.

The majority of Tesla’s stock is already owned by institutional investors and Musk :-]

To see the largest institutional owners, and their percentage ownership, click on the link and go down to “Activist 13D/G Investors”:

https://wolfstreet.com/stock/tsla

Yup, but do we know what they bought in at? Haha. Even if a State Street thought it was overpriced, how much could they realistically dump without driving the price down?

Exactly correct!1)Not only do many wages Not keep up with Real Inflation,but they are reduced in the form of less 401k matching,loss of paid sickdays,less overtime,smaller or no bonus,higher insurance deductible/copay/drug prices,hours reduced-take your pick.It is also not just the home prices,but now the propertytax assessor thinks you are made of $ so of course assessments go up on top of actual property tax rate hikes due to shrinking biztax base and maybe less tourist$.While home prices have gone up in many parts of many markets,I noticed a trend toward buyingup of the cheaper homes several years ago. And strong sales in pricier,but not necessarily the Mcmansion homes.Bifurcated home market like the rest of the economy.

“The greatest shortcoming of the human race is our inability to understand the exponential function.”

Albert A. Bartlett

I would add the mistaken belief that all random distributions are Gaussian and symmetrical.

lease a,

Fill me in please,,, are not all Gaussian distributions symmetrical?

Thought that was the definition of Gaussian distributions as opposed to Gaussian functions??

Not to say there is not tons of confusion out there regarding all kinds of math, statistics, and other similar kinds of ”conventions,” including time, etc., etc. to and including infinity, eh?

@VV – You got me. Lots of distributions are symmetrical. I used Gaussian as an easily recognizable name, shouldn’t have. The human error is to assume symmetry for aggregated events. (See Kurtosis risk and Taleb distribution.)

He was talking about population growth, especially versus resources, which shrink arithmetically. All the exponential debt in the world doesn’t create new resources, it just makes them more expensive.

Love his bathroom analogy: “A two bedroom house can get away with one bathroom…but not a ten bedroom house. The earth is the bathroom.”

“We’re living a defacto Debt Jubilee”

I don’t see any homeless people celebrating. Hours-long lines of people waiting for food aren’t celebrating much either. Looks to me like only the billionaire class are living it up. The millionaire class may be partying today, but only because they are too blind to see they are next on the chopping block.

Real estate only goes up? Detroit and Camden NJ residents hardly agree with that idea.

Pretty sure Philadelphia also de-annexed fair chunks of its jurisdiction because a shrinking economy depopulated so many areas that it wasn’t cost effective to provide police/fire/trash.

It is done on purpose. If Fed wanted to save economy, they could mildly change things that will prevent a crash. But indeed they wanted to crack the walnut with a bulldozer. Simply by eviction ban. Forclosure ban, low interest rate for everyone, …. Again on purpose!

At least someone gets it…

Insightful Millenial!It IS purposeful.For what endgame?

Build Back BETTER! – to the sole benefit of all those cloud-floating Schwabians living in Greater Avaricioustan ….

How ‘bout that delinquency and forbearance rates? What of the landlords without rent? How ‘bout 10% (at least) unemployment.

Ask yourself, “would I feel safer buying 200,000 dollars worth of platinum today or 200,000 dollars of land?” That settles my mind.

I just look at everything and see crack up boom.

“crack up boom” and “bubble” are kind of the same thing. Just a different metaphor :-]

I make this distinction:

Late 1998 through March 2000 wasn’t a crackup boom- it was a bubble. The economy itself was still fundamentally whole even if the stock market was a joke, and when the bubble imploded, the wreckage was almost completely contained to the destruction of fake companies.

This market feels fundamentally different to me- when it implodes, it will be 2008-2009 on steroids. We have completely hollowed out the economy and even the philosophical underpinnings of the system. I am reminded of a phrase I first heard during Ken Burn’s documentary on the Civil War- we are in the “age of shoddy”.

This boom just cracks me up.

Wolf, if you want to see some insane pricing in housing look at the coastal areas of Orange County.

We were doing the central London dual income thing before COVID. Lots of fun for sure, but as we got older we realised that you can’t actually win that game. You are basically competing with multi-generation inherited wealth at best, and the casino finance guys at worst. We got close to buying a shoebox ex-council flat with a whole bunch of problems. I’m so glad we didn’t.

COVID made us realise that it’s time to get out. We will trade off career prospects for better cost of living numbers. Even if we dropped an entire income there are a whole bunch of places we can live much better than we were in London. And other people we know are doing the same, which means that we don’t even have to say goodbye to all our friends.

I sort of suspect this is going to be a big effect of this misplaced attempt to boost asset prices as a way to ‘save the economy’. Folks like us who were already feeling like it was rigged have an easy decision now. They will drive the best and brightest out of high productivity jobs.

That’s going to smash their GDP per capita, which in a sane world would be the actual thing that matters. No doubt they’ll try to boost asset prices even further to compensate so they can squeeze more out of those who remain. It’s going to be a mess.

That is why we are still swamped and hoping for an extended fall

so we can keep the machinery in the field going.

So far mother nature has blessed us with a mild fall.

The phones keep ringing, the chicago folks keep coming.

^

This. Ultimately, could afford here. Hate this place (Insert major metro name).

Own some land. Looking into well and septic. After a home is there, will gladly move and take income drop just to have space from dogooders, excessive regulation, and most important… space from people who are incredibly close minded and judgmental, but think they aren’t based on what side they’re on.

People need more space (distancing);

so they move to the suburbs, or farther.

Single-Family housing is soaring because

people can’t tolerate housemates anymore.

Shared Housing in Seattle should be worth nothing,

given the eviction moratorium, drug abuse,

squatting, property damage, violence,

Covid-19 fears, and general lawlessness.

10 or 20 years from now,

the pendulum will swing the other way.

The violence isn’t necessarily any less in the suburbs. Or rural, especially rural. Not anymore. It’s just different.

The Ads I see today; Amazon Prime, How to Retire in Costa Rica, there was an ad for a condo, lending tree, and one for clothes.

Odd I don’t remember looking for dog type clothing or housing lately.

The web 2.0 advertising brokers just fill their frames with whoever is paying at the moment. Doesn’t have to be targeted.

Werent we just talking about how rents in San Fran were plummeting?

Housing prices are way stickier than rents. Rich people have a lot at stake(and a golden parachute), so they hang on to loser assets through temporary stuff like a pandemic, because they can’t bear to take the raw end of a deal or admit they suck at finances(a small 10m loan from my father at 18, otherwise I’m a bootstraps story!).

Thanks for the last phrase bob,,,

Made me laugh to the point of almost choking on my current liquidity position!!

Wonder how we would have survived without the Fed keeping stable prices over the last 20 years?

Remember when mortgage rates were higher than home price inflation? ;-)

At least we are near the end of this ponzi. 2.5% mortgage rates are being advertised on my feeds. You can’t go any lower than that. It costs 1-2% just to issue and service a loan, then you have at least a 1% default risk.

Steadily reducing interest rates will be a thing of the past from here on out, and this WILL take out that incremental demand from first time home buyers.

Rates will remain low until no one else has any money left to compete with those who wish to own everything.

Adjusted for wage growth in absolute numbers as well as affordability in terms of mortgage rates and in most places housing is way up from the lows but is no where close to 2005 2006 levels.

There are exceptions, but for the most part it is not as severe a bubble at this point as last time.

The odd thing that gets me right now is I see in some micro markets where people want to buy because of Covid some homes are fetching 20% more than they could in January.

Why would anyone commit to a long term price by purchasing an inflated value house based on a short term pandemic that will be over in a year or so?

I am purchasing a home a Denver suburb. The inventory is insanely tight. Only one or two properties in the school district for sale each week. They usually immediately go under contract.

I could wait and maybe prices go down. But meanwhile I am stuck in a 650sqft studio in the city having to wear a mask to go anywhere for the foreseeable future. In the grand scheme of things I am not gonna care that I paid 20-40k more for a place 15 years from now. That is only a couple months of my income.

Fear and Greed.

Is there some element of loan qualifcation fraud going on? Not the blatant NINJA type stuff, but where the banks’ going-by-the-books screening process is missing substantial risk?

And under a Biden administration, I expect we will see the flood of Chinese and H-1B buyers resume.

Why is it that people think that liberals are somehow more amenable to selling out the country? No one mandated that any of the Fortune 500’s had to be greedy and betray their country. Nor did Americans have to choose the Chinese item that was 15 cents less at WalMart when you had the option of buying American.

I work in tech, and I assure you that none of my H1B colleagues are making a slaves wage, these people are not competing with Americans for jobs in skilled tech. We’ve tried. There’s a lot less paperwork and Americans cost the same. It’s simply a matter of education and drive. At this point the middle of the country treats ignorance as some sort of virtue, and thinks of universities as places for liberal indoctrination. And these immigrants and foreign investors are buying properties in nice places (cities) where people in red states claim they’d never set foot in anyway. How do you educate and employ Americans when they think that exploration, problem-solving, and being open to ideas and facts is “liberal propaganda”? It’s truly hopeless.

“Nor did Americans have to choose the Chinese item that was 15 cents less at WalMart”

Americans didn’t choose Chinese items, Walmart did. I lived in Walmart’s backyard (Northwest Arkansas) in the 90’s when the Clintons moved to the White House. It was just about that time that Walmart removed the giant “MADE IN AMERICA” banners from the front of their Springdale flagship store.

Walmart’s strategy was simple: they ordered their vendors to cut their prices to Walmart. Vendors responded, “We can’t without moving to China”, and Walmart said, “Better hurry”.

Our Dear Leaders certainly are not going to take the heat for wrecking the manufacturing base; much better to blame the victims, tell them it’s their own fault for not buying stuff that is no longer made here.

Very biased view of the world you have there. My son-in-law lives in rural town in red state. Bachelor degree in computer engineering, masters in electrical engineering and passed navy nuclear certification program. My daughter has bachelor in electrical engineering and spanish. Both very successful working in the utility sector. It’s a much more stable employer than tech. They have the big home and nice cars and like the rural lifestyle.

^

That’s most of my family (Close minded, but think they aren’t because they’re on one side of the nonexistent aisle).

Because only people with incredibly low IQs know how to grow wheat, raise pigs, work structural steel, etc, etc.

Mike Rowe said the dirtiest secret of dirty jobs were how many of the people on the show were multimillionaires.

But I guess if they don’t look or talk like Gates or Jobs they’re not worthy of learning from.

Both Jay and C the Peasants fall for the rhetoric.

I work in tech and I’ve personally seen instances of H1B used to hire foreigner relatives, friends and/or for roles that easily could be sourced from US talent. It’s definitely abused in my opinion/experience.

I’m a leftist, not a liberal, and completely agree with the foreign investors thing. We have a wave of new homelessness coming up and should be discouraging or penalizing foreign investment in our housing stock. We don’t need more empty “investment” housing. We need deflation of housing prices.

Just so you know, for some people that 15 cents or dollar they save on several items enables them to buy food which they would otherwise be unable to. Yes, really. People are not lining up for several blocks at food banks or living in tents for the fun of it these days. And for others it enables them to pay rent or their mortgage so that hopefully they won’t have to live in a tent in January.

One can only hope that someday more people will have that choice to buy something that benefits a local small or family manufacturer.

Interesting thing about home prices. Recent new purchase, and also refinance of existing summer home. Refinance is for a lower rate, dropping my payment about 250 monthly. I’ve bought houses since 2000, and now more than ever qualifying is much more stringent. While some people will surely be in trouble, they aren’t giving everyone loans like before.

In 2006 the US minimum wage was $5.15 an hour. In 2020 the US minimum wage is $7.50 an hour.

The median price of a single family home in Washington, D.C. recently surpassed $1,000,000.

FYI…MA minimum wage is $13.75 hour. overrides Federal. Also, only places like McDonald’s pay that low…everyone else is $18-$20/hr

$10. Hourly minimum in IL.

Mmmmm… property taxes.

Yeah I’d prefer slower growth in home prices as someone who isn’t moving and would rather not get killed on property taxes because of a bubble.

I’m up about 79% on a house built new 10 years ago, yet if I include all the upgrades, maintenance and the property taxes, I’m down about 9% total over those 10 years. Houses are consumables over the long term, and at best a sort of forced savings vehicle.

To be honest it seems like houses are zero sum as they go up in value, yet unless you plan to substantially downsize or live in a van, when you sell you still have to buy another house that has most likely also risen just as much in value. Plus with property taxes high in some areas like my own, you never own your house, you constantly rent even when you have no mortgage. And many houses where I live have seen their property taxes double in the last 10 years, rising $1,000 to $2,000 extra a year on $400 to $800k valued homes. It gets extremely expensive to property tax “rent” your house when property taxes are rising 8-12% a year and incomes are only rising 3-4%. So many people, to their future retirement detriment, re-finance and pull out “free equity” to make up the difference. As long as one never plans to ever retire, I guess that works long term???

Yort, thank you for pointing out that “homeowners” “rent” their land from the Government. That fact is not mentioned often enough.

As mentioned earlier in the comments, that’s a main reason Costa Rica, Nicaragua, Thailand etc. retirement ads are appearing with no apparent connection. They are targeting people who have yet to realize they are screwed. Tech knows your situation and future moves before you do. At least within an acceptable margin of error. Better get in quick on those tropical deals too. They are filling up fast with ever increasing RE prices prices due to the early “I’m totally screwed” adapters. America’s only retirement plan for many… leaving. Van living outlawed in 3..2..1.

nah yrt,

Best deal currently is to go to the back of no where in USA,,, AKA flyover country, and pay cash for a small home or ”homestead” of the kind with enough dirt to grow almost all of your food,,, and the rest will be distributed directly by the future guv mints who have to do it to at least pretend to keep up with FDR’s wonderful system that made folks continue to vote democratic for eva in those areas…

Other than that,,, if you have any ”mechanical ability” best bet is to live ”on a boat on the hook” somewhere outside USA, while still getting your SS payments regularly into your bank account,,, spend nothing outside your CC, and pay it off every month so as to pay NO interest, etc…

Grandpa did it for years, intent on living on his SS of $100/month, and still saved enough capital to move to the southern Rocky Mountains and buy an adobe for his last 10 years or so.

Funny how they market increasing home prices as a boon for all homeowners.

Eviction and foreclosure moratoria are ending 1/1/21 and the conservative estimate is that we will see 5.8 Million Americans become homeless.

This will affect quite a few aspects of daily life for every one, and not in a good way.

if you are buying a home in this market you’d be well advised to be really careful about where you buy…

Might depend on Two senate run off races in GA!

Sorry Wolf in advance. I hope I haven’t violated terms. My only point is more government cheese will have an impact on asset value!

There is No Way the moratorium will end in the middle of winter!Even if it is a state by state extension such as the ones occurring in IL.Additionally,just today I saw that utilities extended their disconnection moratorium because they care So much about their customers!Debt will be used as a forceful leverage on people to do what they do not want to,like maybe take an unproven,dangerous vaccine.

Off topic, but I really appreciate your charts Wolf. They make the data more accessible, not something easy to do.

You outta copyright them!

:)

Keep up the great work/service.

Everything on my site is copyrighted, including the charts. See the © notice at the very bottom of the page. People can republish my stuff only with permission. But lots of people just steal my content and republish it anyway :-]

Most people have no common sense only waypoint of this messis default everyone will start over everything will lose 90 cents on the dollar history repeats be prepared roaring 20 s rich never suffer they are prepared good luck

Most people will lose 90 cents to the dollars. The rich won’t. Then they’ll sweep in and pick up everything 10 cents to the dollars and everyone will be a renter. People will no longer own anything. Everything else they supposedly “own” will be on the cloud, where ownership can be easily revoked.

Welcome to the American Dream!!!

The wealthy “Rentier Class” is cannibalizing the bottom 80%, and with the help of the central banks, soon to be the bottom 95% of American society. “Rent-to-own”

applied only to poor people in the 1980s (and was shunned by the middle class as a joke), but today nobody thinks much about “Rent-to-own” on almost any discretionary product and/or service.

For example, Lululemon has a program called “AfterPay”, which allows addicted LuLuLoopy consumers to buy a pair of child labor $100 exercise tights utilizing four installment payments. Whaaa? And this works, even when the founder Chip Wilson had to step down after supporting child labor publicly….whaaa?

“AfterPay” is appropriate as most consumers will still be paying “AfterLife”…=D

from what my grand father said, many many ”rich folks” jumped out of windows or found other ways to do themselves out of life from the first major crash of the SM to the last Ron…

Some, as you say, just ”partied on dudes and dudettes” as has been done by some during all the crashes i have experienced since 1956.

And as has been said by some sage or another, ”you can’t control what happens, but you can control how you react to what happens…”

Many folks at all socio-economic levels came out of the crash formerly known as the Great Depression OK, and some even better than they had been.

This one will take over as the ”Greatest” depression sooner or later IMO, but, as Wolf has made very clear to me,,, that depends hugely as to how much, when, and IF the guv mint continues to intervene, and continue the ”extend and pretend” for another round/decade.

Bee very interesting to see,,, hope I can stay kicking for at least a few more years!!

So many things, economic or otherwise are built more and more with distorted, manipulated or incomplete factual certainty, Housing valuation, as a discretionary process, is not unlike presidential/election forecasting, i.e., very open to interpretation. The pandemic is a game-changer within a world of inaccurate modeling and forecasting. Nonetheless, current valuations seem frothy and exuberant and unsustainable, yet, fewer people are looking at future value in anything, ignoring risk and debt and focusing on immediacy, believing that any bet in any casino is a sure deal, backed by government bailouts and rescues, and moral hazard extremism.

One glance at these Wolfstreet charts of Case Shiller Index growth for these cities shocked me into one conclusion: this is indeed a housing bubble on steroids, and we are near a peak.

This is hockey stick economics, with an inflection point around 2012.

If you go along with this ‘psychosis of the masses’ belief that house prices can inflate much longer then you must believe in unicorns too.

As was once famously said, people go mad in herds and recover their senses slowly, one by one.

Although lots of folks with skin in this exhilarating housing game can rationalize until the cows come home just how these nosebleed house prices can be justified– I would ask them just one question: Does gravity still work if you should fall down or can you float in the air indefinitely?

Be careful. Financial prices are man-made, not natural forces like gravity. If desired, the Fed can print money to keep asset prices high. The question is – will they? If they do it, we’ll undoubtedly see increased wealth concentration, more scamming, and decreased standard of living for the middle and lower classes.

Financial policies and related social effects are chosen. Unfortunately, the current financial leaders view our financial system as a game, and they choose to play three at once – Russian Roulette, “Who Wants to be a Millionaire?”, and “Screw Your Neighbor”.

That’s an interesting thought, that man-made constructs like finance and economics can defy natural law.

Fools always think ‘this time is different’. They can ignore the real world but they will never escape the consequences– even if financial elites try to keep juggling plates in the air longer.

There is no such thing as a free lunch, resources are always scarce on the planet I live on, and trees do not grow to the sky.

It’s not just an interesting thought. It’s partly reality. Covid19 is a natural phenomenon, and our stock markets are partying like there’s no tomorrow.

“This time it’s different” works both ways, both on the long and the short.

The only way to win … is to not play. You’ve lost out on some monetary gain, but you also escape the moral quandaries.

I don’t think you get it yet.

Your debt (which is somebody else’s asset) can be wiped away by simple decree from a group of “leaders”. There is no natural law preventing that. Debt are simply contracts developed by men, and they can be extinguished by men.

The government can take your earnings through decisions about taxation. They can take zero, 10% or 90%, unimpeded by the winds or the shape of the galaxy.

Men in power can decide to expand the money supply by 50x this year. That would destroy the value of your past efforts (i.e, your savings), but they may feel some swindler deserves the fruits of your labor more than you do.

In short, your financial success is what people in power decide it should be. The only natural law applying is that humans tend to get fed up when treated badly, and they revolt at some point. They can vote people out, they can stuff money under the mattress, or they can cut off some heads. These are a few natural behaviors that can impact a financial system. But even these natural behaviors are not guaranteed to surface over a lifetime. For example, over a billion people can’t vote in China, because that’s the way a few leaders dictate it.

Capitalism, socialism, communism. These are all just ideas that are forced on people when “leaders” find them convenient.

Don’t get me wrong. I hope you are right and there is a reversion to the mean. But I fear we are witnessing a gradual silent shift from capitalism to psuedo-socialism, complete with never-ending money printing, interest rate repression, high inflation, and high asset prices. Our universal basic income checks will be deemed to compensate us for the lack of competition, opportunity, and mobility in society. Under that scenario, there is never a reversion to the mean, just a continued departure from it. Why? – because the powers that be want it that way.

The financial industry knows that this paradigm shift is taking place, but they aren’t complaining. They are benefiting from it.

Thank you Bobber for a concise and thorough summary of the reality of life, today and almost always from my extensive reading of history and the best of herstory, so far…

While long ago I lost an extensive argument with a first cousin (once removed) that the only real measure of progress was the ability of millions now to hear the music of Bach, Mozart, etc., etc., as good or better than the dozens/barely hundreds of their era,,,

IMO the dearth of progress toward a true democracy based first and foremost on an education system devoted to actual clear results, rather than political correctness, etc., is signaling the possibility or even probability that our species will soon be replaced on this planet by another species much more adaptable toward a true democracy, rather than the kind of ”representative republic” and all the corruption from that system now evident,,, in which USA and many others find their country ”stuck” today…

The Fed can print Federal Reserve Notes, but they can’t print trust in them. Once trust evaporates, it’s hyperinflation time.

So far Dear Leaders have destroyed the public’s trust in politicians, establishment media, election results, medical experts, vaccines, virus numbers, virus control policies, police, crisis management, and each other. Federal Reserve Notes can’t be far behind.

Well-put!

Bought my 3 BR Colonial in a nice suburb of DC in 1999 for $315. Added 100k over the years (20) to fix all the things that were broken when we bought it (as is) and fell apart (maintenance) after e bought it. So we’re up to $425 as a basis for the house. Now based on the tax assessed value and the Comps in the area we could sell it for $695 as is (We still haven’t fixed everything that was wrong when we bought it). Now add the depreciation of the purchasing power of the dollar in the 20 year period (50%) and add the costs of selling and moving and guess what. We haven’t made a dime on this house, even though we bought in a good neighborhood at a good time. We paid off the mortgage and have a nice place to live. That’s something to be thankful for. But as far as making money, forget it. That same goes for most residential housing if you figure in the costs listed above.

Now, if you would have spent 315K in Manhattan Beach, CA, or Newport Beach, CA you would be looking at more than 2M without any improvements. In Santa Monica, CA, you would be at 3M. That is lot value. You have to be careful where you purchase.

now you’re full on gloating, Socal Jim.. YOU be careful where you gloat and to whom. aside from practically begging for a cosmic beat down, it’s not very attractive or kind. this is what your one other beer friend is for. (it’s lonely at the proverbial “top,” Jim)

Interest rates are so low compared to the inflation rate that it truly has paid to go deeper and deeper into debt. The staircase down in interest rates over the last 35 years has been a site to behold, but then again, we lost massive amounts of good paying manufacturing jobs and gained massive numbers of cheap H1-B workers and others. And if you complained about this, the maestro said: “It’s not the job that counts, but your buying power”. If the staircase continues down and we get below zero interest rates, I truly believe we have entered the 21st century’s version of feudalism.

But, Sire! If you take yet another eighth of the grain we may starve!