Most of the losses come from established income-based repayment programs that include debt forgiveness at the end. No one has ever put a number to it until now.

By Wolf Richter for WOLF STREET.

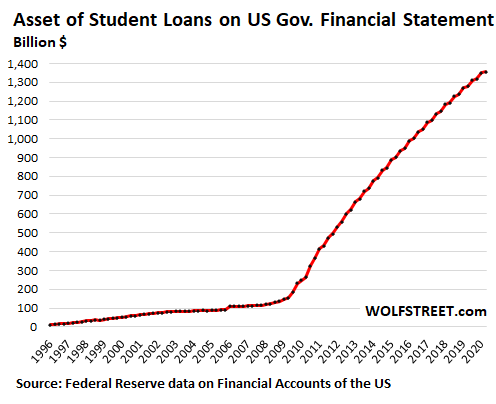

In 2009, the US government entered the business of reckless, no-matter-what lending to students, even to older students with subprime credit ratings and to students at iffy for-profit colleges with dubious degree programs. And then tuition soared, and student housing went upscale and became a global asset class with its own commercial mortgage-backed securities (CMBS) that are now experiencing record delinquency rates. And Apple and textbook publishers and everyone began feeding at the big trough, with students just being the conduit for this money. Student-loan balances on the government’s financial statement skyrocketed from $147 billion in 2009 to $1.37 trillion at the beginning of 2020, despite the 11% decline in student enrollment since 2011.

Taxpayers face a loss of $435 billion on the $1.37 trillion in student loans on the government’s financial statement at the beginning of this year, even if no additional loans are issued going forward, according to an internal study by the Department of Education, reported by the Wall Street Journal which reviewed the documents. Most of the losses would come from the already established income-based repayment programs and the debt forgiveness at the end of their term.

The expected loss of $435 billion is far larger than the rosy estimates released previously, including the Congressional Budget Office’s estimate in May 2019 of a loss of $31 billion, including administrative costs.

The student loan balances in the chart above do not include student loans carried by private lenders that are guaranteed by the US government and that will produce additional losses for taxpayers.

The Department of Education, fearing that government staff had underestimated the losses on student loans, brought in FI Consulting to build a computer model for a much more detailed analysis. And it brought in Deloitte to review the model.

The study found that most of the losses are already baked into the cake through the income-based repayment and loan-forgiveness plans, which see to it that effectively many loans do not get paid back in full before the remainder is forgiven.

Only a small number of borrowers owe a gigantic part of the student loans: 7% of all federal student-loan borrowers, mostly those that went to graduate school, piled up $500 billion of student loans – meaning these 7% of borrowers owe 37% of the federal student debt, according to a report by Moody’s dated January 2020. Each of them owes more than $100,000.

But a majority of borrowers don’t owe all that much: At the end of 2017, the “median” amount owed by the 45 million federal student-loan borrowers was around $17,500, according to the Moody’s report. “Median” means half owe more and half owe less. It means that there were 22.5 million borrowers who owed less than $17,500 – about the price of the cheapest new car available in the US.

And these 50% of borrowers combined owed only $200 billion of the total federal student loan debt.

Student loans are a top-heavy affair, with the vast majority of borrowers owing manageable amounts, and with a small number of borrowers, mostly with graduate degrees, owing very large amounts. This distribution skews the “average” student debt (total debt divided by total number of borrowers) that is often cited in the media as being over $30,000, compared to the median student debt of $17,500, with half of the borrowers owing less than $17,500.

But student-loan forgiveness is already the rule through income-based repayment plans, which allow borrowers to make monthly payments of only 10% of a special income measure composed of gross income minus 150% of the federal poverty limit. And the remaining balances are then forgiven after 10, 20, or 25 years, depending on the program.

Borrowers in income-based repayment programs will repay only 51% of their balances on average, while borrowers in other plans will repay 80% of their balances, according to the analysis by the Department of Education.

The idea – particularly for borrowers with huge debts, such as former graduate students – is to drag repayment out as far as possible, and make it as slow as possible, and to pay the least amount possible, and then have the rest forgiven. Students with smaller balances too use this strategy to avoid default and minimize payments.

This is in part responsible for the surge in student loan balances, according to Moody’s; as new loans are being added, old loans are simply not being repaid.

And these income-based repayment programs and the debt forgiveness that comes with them are a major component in the projected $435 billion loss to taxpayers on the loan balance of $1.37 trillion, according to the analysis by the Department of Education.

At this point, federal student loans are not easily discharged in bankruptcy court, but they’re forgiven at the end of the income-based repayment programs. And this is already baked into the cake. And taxpayers are on the hook for these losses.

The fact that student loans began surging only a few years ago means that this tsunami of losses stemming from loan forgiveness at the end of the income-based repayment programs is still in the future, but can be estimated.

But who ultimately got this money, since students were just the conduit? The educational-financial-industrial complex, of course, the entities that have lined up to clean out the taxpayer via these student loans. Billionaires have been printed in the process, enabled and encouraged by the government since 2009. Any solution to the student-loan crisis needs to include measures that shut down that money-transfer and return the government’s role in student loans to where it had been before 2009.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I know of many student ‘borrowers’ who took on large debts for aviation programs. This included paying for qualifying flight time which can run in the hundreds of dollars per hour for multi instrument training.

My nephew asked me several years ago for feedback regarding his buddy who was considering such a degree. My reply was to ask if he was crazy?

Hmm, wonder how it all worked out?

What did Ben Franklin say in Poor Richard;s Almanac? “A fool and his money are soon parted”. In this case who was the fool? Taxpayers? Borrower? Institution?

Paulo,

When I started flight training many moons ago, everyone in my class was pay as you go. No one took out any loans, but my fellow classmates were, like myself, business owners looking for a more efficient means of transportation. After 9/11 aviation course costs escalated dramatically, and many students took out loans in anticipation of the “pilot shortage.” I always thought it was dangerous to put all your eggs in one basket as far as careers go, but I often hear nowadays that you should follow your dreams at all costs.

All I can say is good luck to anyone in such a predicament.

The commercial airlines hire mainly ex-military pilots as they have years of experience. They may not hire from pilot training schools.

That was not a problem for my cousin years ago, when he finally gave up trying to feed his family being a magic/musician.

He went to his first pilot training on his last few dollars, then went with, IIRC Eastern, Pan American, and one more that I do not remember before he retired to Miami and enjoyed ”the good life” until he kicked that bucket we all have in front of us…

He would call me when coming into SFO, and we would sorta/kinda party, but he would not touch a drop of alcohol because of flying the next day, enjoying vicariously making me do his part as well as my part,,, but on his nickel, as I was a ”struggling student” at Cal, paying my way by working pretty much full time will taking a ”full load”…

Good guy, absolutely earned his ”capt” stripes in spite of not being in any of our wars,,,

A lot of pilots in the wars never made it back for their last “safe” landing. The ones that did deserve a good civilian job and respect in life.

“A fool and his money are soon parted.”

That should mean there is a shortage of stupid rich people?

Different types of smartness.

Smart enough to hop on a publicly financed gravy train clearly made plenty a fair bit of money over the last decade.

we call it STUDENT LOANS

end them today and all will become right with higher education world

by end ALL student loans we can then forgive yesterdays follies

but under new world order we educate them(state calls them jobs for youth) sink further into 3rd world country

merica WAS great – but now is sinking faster than Venice

While the banksters are not exactly top physicists, they have a cunning, so sadly, the people who are truly dumb are those masses of Americans who believe them. I never thought that what some Europeans told me (which was offensive) might be hard to dispute: that more Americans than Europeans were not the brightest intellectually.

However, what happened during this pandemic is hard to refute. See The Atlantic’s excellent “Hospitals Know What’s Coming” So did I and various neighborhood doctors and nurses — in February.

I forgot to add: I truly wish that the student problem defaults that are oncoming were even among our top five, greatest national problems.

In this case.. whether you like it or not … YOU are the FOOL.. all losses will be socialized..

We are in a delusional period where the consequences of Debt and Irresponsible Behavior.. are Delayed..

When society sees no consequences.. you get the behaviors we see today..

In the world of Free Money.. the only fool.. seems to be the one who does not have his or her hand in the pot..

When it all Collapses (As it inevitably and mathematically must)

I guarantee. this same group will all be singing the famous song

WHO COULD HAVE SEEN THIS COMING?

Two words for all of this: Moral Bankruptcy

Money printing morality: Repress savers with Zirp and forgive loans of debtor. Many savers noncollege educated hard working older people paying for university student partying. Shameful.

25 years of not making “too much” in order to minimize the amount you pay back and maximize the amount you stiff the taxpayer doesn’t seem like much of a “win.”

“But student-loan forgiveness is already the rule through income-based repayment plans, which allow borrowers to make monthly payments of only 10% of a special income measure composed of gross income minus 150% of the federal poverty limit. And the remaining balances are then forgiven after 10, 20, or 25 years, depending on the program.”

The word missing is officially, as in “too much, officially”.

10% of your income above 150% of the poverty line is a lot less money than what you might be paying on loans normally. Doing some quick math, for me that would be a little over $300 a month. I’m currently paying (in full, I might add) about $1350 a month on student loans. At least I got a useful degree and a good job (with real cheap health insurance) out of it.

Gotta tell you LC, that when I paid off every cent of my private loans from a cousin, and he told me I was the only one of his several relatives to do so, it absolutely made me free of SO much ”psycho-spiritual burden” that I still cannot describe it other than as a very great relief.

Immediately after that, my business started to grow immensely, and continued that growth for many years.

Now comfortably retired and although not by any means ” affluent/ rich”,,, I am able to project that my spouse will be able to keep on keeping on without me,,, and/ or send a bunch to the grands to help with their educations, as our kids, 40+, are self sufficient as we hoped they would be due to our so called ”tough love” child raising, that was nothing more than the common sense our parents utilized…

I fully paid off my student loans as soon as I could. None of this delay nonsense. Call me stupid. But being debt free is a liberating feeling. I second that psychological effect.

However, I also know the value of going into debt to grow a business or make an ROI that exceeds the interest on the debt. Not for me.

It is about minimizing your income. I can pay extra to my student loan, or I can put it into my IRA and reduce my income, ditto for 401k’s (TSP for feds). While you would not want to increase your income via overtime, as it may not be available in the future, getting promoted is still advanteous, as you still keep more. Heck, you may keep even more if you invest. After ten years as a govt employee, the debt is discharged without a tax hit. The 25 year plan counts as income. Oh, income you pay on your federal loan can be deducted up to $2500 to reduce your income on your tax returns.

Another benefit to this is it enables a work life balance. I got a law degree, but I only need to work 40 hours a week to have my loan paid off. Compare that to the kids working in law firms slaving themselves away. There are real benefits here, provided you planned ahead.

Back in the day you could get a summer and a school year part time

job that would be enough to pay for your education.

Today that is all but impossible .Hence the need for student loans.

It might be cheaper for the gov’t to pay for undergrad

and be done with it ,

You do realize that “getting government to pay for it” started the higher education affordability crisis in the first place?

The same can be said for medical care.

gorbachev,

That would just make the problem worse, the problem being that the government is feeding hand-over-fist the educational-financial-industrial complex and printing billionaires in the process, at taxpayer expense.

It would be a lot easier if the absence of no-questions asked student loans (meaning going back to pre-2009) would:

1. cause universities to cut their tuition and remove the on-campus-residence requirements, offer cheap online classes for theoretical topics, and sell part of their huge campuses in prime locations to fund those tuition cuts.

2. cause textbook publishers to cut their rip-off prices to ebook level.

3. cause remote learning for some semesters to take over, removing some of the student-housing costs.

4. cause students to focus their studies to get the heck out of there as soon as possible;

5. cause students to avoid expensive degrees that lead to low-income jobs.

6. cause graduate students, who want to invest $100k in their future, to be prepared for using part of their high future incomes to pay off the big student loans. A young doctor making $8k a month can pay $1k a month in student loans, for 10 years, no problem. And that would more than pay off a $100K student debt.

I’ve worked for the Department of Education on every level since 2010. I’ve worked every department from default resolution to Income Driven Payments Plans. I could not agree more with all of your points especially number 6. Many have been denied the opportunity of a higher education due to expensive tuition cost. As a collector and counselor, I’ve dealt with borrower’s loan debt in the upwards of 50k to 300k and 99 percent dodge all efforts of repayment. These are your Doctor’s, Attorneys, Politicians, and self employed licensed workers. There isn’t a system in place to go after this bunch. I’m willing to bet they make up a significant percentage of debt that no one wants to talk about. They take from social security! The system is screwed and I’ve seen it first hand. I owe loans and even I disagree with allowing some one to pay $5.00 a month. The benefits are terribly misappropriated and whoever made those decisions…. Nevermind I could go on.

I got a MS in Semiconductor Physics some years ago. It was kind of expensive, but I paid off my student loans 4 years after graduation (maybe 5). Of course, you can get a pretty good job with that degree, if it comes from a real University.

The problems here come in two flavors:

Fake colleges, which produce graduates who can’t get a job.

People who get a PhD in Medieval History, but do not have a trust fund.

What needs to happen first is that we have to crack down hard on the fake colleges, and then we need to explain to the PhD programs that they will encounter “burden sharing” if they continue to produce more PhDs than society needs.

(Anyone who has been a Graduate Student at a fancy University knows that we produce WAY too many PhDs in this country.)

An even bigger problem than too many phd’s, is that quite alot go to college, because, they were told office jobs will be the only meaningful jobs available in the future. Because, so many were told to go to college, companies hiring office workers and various other workers were able to require college degrees for jobs that didn’t need them. These employers of course didn’t raise the jobs pay to match the new requirements.

That’s the main reason an average student will go to college and get any random degree (including most business degrees). It doesn’t matter what the degree is in for most jobs, but, for every job you apply for, for the rest of your life. One of the determining factors will be, whether or not you have a college degree. It is much harder to get one later on. As more and more young people got college degrees, it became more and more necessary to have them.

I started college at the tail end of the 2008 recession and there were some various middle-aged laid-off people at the college who all basically said they were high performers at their company and most missed out on executive positions in last 5 years (Back then), because they lacked college degrees. They were then laid off during the recession, while, the ones with the degrees who got those executive positions did just fine. It’s always hard to tell how true those stories are, but, I’m sure that it does happen exactly like that for some.

Alot of the fake colleges have already been shut down, it will be necessary instead, to limit college to fields where it’s actually necessary and greatly reduce cost for the now smaller number of students. A wealth of free educational resources of all kinds can be given for free online and would cost almost nothing in comparison. For those already with debt, there would be a massive write down and new graduates would have much less debt (and be fewer). The ability to get student loans could be restricted upon the program the student is taking for private colleges.

Totally agree. In my field, PhD’s are sales people. And no, they do not need that extra 5-6 years of schooling to do the job. Most don’t want to slave through one or two post-docs with no guarantee that they can secure a decent academic position.

These jobs had been and can be done by bachelors degreed folks. I even sense a sort of entitlement from these folks when they do encounter a non-PhD, even when the record shows they actually underperform the lesser educated folks.

Forget about the PhDs we produce in the country which is Minuscule if you compare it to the number of phD‘s and engineers being produced by countries like China and pump into America debt free.

When I read articles like this I wonder to myself how stupid can American people be? No wonder the world is laughing at us!

I have a good friend who has a Ph.D. in History. She has no debt from the Ph.D. because her University funds Ph.D. programs. She frequently says so few people get their Ph.D.’s in history even though it’s free because the work is so daunting w/nothing guaranteed post-grad. I’m not sure how common it is for Universities to cover the tuition costs of their Ph.D. candidates but I bet a lot of student debt comes from MBA’s not history degrees. It would be nice to debunk the “basket weaving degrees are useless & draining to society” talking point.

A lot of those PhDs filter down to teaching at the JC level. You could make the point that you don’t need a PhD to teach begininning chemistry.

PhD’s?

You should have seen all the worthless, useless, idiots with PhD’s that came to teach in Japan when the yen surged in value from the 250 – 300 yen level to the 75 – 80 yen level per dollar.

Idiots that didn’t speak a word of Japanese and could not read either that were hired because the Japanese universities wanted a ‘brand name’ PhD.

I had the ‘opportunity’ to observe a number of these people ‘teaching’ at various universities and wanted to throw up. Most of the students hated them and their classes.

Private universities paid these dolts a decent dollar wage that in yen terms were less than half the previous salary that was being paid to current teachers AND made them teach twice as many classes along with more office hours, extra work AND the requirement to be on campus 40 hours a week for 52 weeks a year except for school holidays and a couple weeks vacation a year.

Universities made out like bandits when the yen went up in value.

A perfect example of globalization ‘wrecking’ a job market.

My daughter is getting a PhD in Mechanical engineering and getting paid for it (as a stipend). In the UK her undergraduate debt gets paid off by a payroll deduction equivalent to AFAIK roughly 10% of income above a approx. £20000 threshold then written off after 30 years. Considering that fees tripled overnight without warning i think that’s probably fair enough for now.

Haha btw grad programs for “cheap” in state programs cost $70+ per year and they go up the max amount every year because the university needs more money due to greed. These programs leave students with 300-500K + in debt. Not to mention the undergrad degree costs that came 4 years before at pry 100k. So… I think your numbers are way off. Oh and don’t forget the lovely 7% interest they charge us. The gov let it happen cuz this is the best money maker since they found out wars make money for them. One guys opinion.

California resident undergraduates at all UC campuses pay $12,570 in systemwide tuition for the year 2020/2021.

This does not include grants and other forms of financial aid.

Minnesota resident undergrad tuition is $13,318 for 2020/2021. Add a surcharge of $2,000 for ‘School of Management’ or ‘Science and Engineering’.

But don’t forget the $214 ‘Loan Fee’. As: “Students who choose to take out a federal direct student loan incur origination fees set up by the federal program. Students who choose not to borrow do not incur any loan fees.”

Forty years ago at the U of MN it was $1,151.

An undergrad degree in a favored subject area will cost A$3950 from next year in Australia. That is around US$2800 a year.

And by the way, undergrad degrees here are done in 3 years, not four.

OZITRALIANS are sooooooooooooooo much smarter than those in the USA as they take four years to do an undergrad degree!!!!

Thanks for smacking me around a little bit.

I think I needed it.

That is as solid a list as any I’ve seen on this topic. Two thumbs up Wolf. I think you should include these types of “solutions” in the article itself.

Wolf!! Have you been taking your MEDS?

Your suggestions are Cogent and MAKE SENSE!!

If Twitter and F/book get wind of this…

Lets not even consider the dangers..

A wave of good sense could sweep the national conversation..

whoo…

Good thing I caught it early – Right??

So how about you hear from a real Emergency Medicine Resident Physician before illustrating us as worthless people who by some here seem to think we are idiots.

My debt from Med School is 350K, and I make 47K per year after taxes thank you Medicare (No Hazard pay or increase in wage). I can’t touch the interest of my student loan. So over 4 years, with my interest @ 6.5% via the federal government I will have tallied ~40K over 4 years and my debt is now 400K. All while we “idiots” wasted 8 years (basically our 20s undergrad included so med school is so competitive) while most of you enjoyed marriage, families and vacations. I still cannot start that process because i do not have the means.

Now I will be earning 250K, pretaxes and will have to make ~4K monthly payments for the next 8.3 years just to pay my debt.

Appreciation and a sense of duty is why I volunteered to come back into the ED and ICU during my off-rotations, clearly neither of which seem to matter to every post I read here. Also if you are unaware the pace of tuition for medical school is 6x that of undergrad and both currently outpace the rate of inflation.

R,

Look, you invested in your future. These are decisions YOU made in order to earn $250k now as a young doctor, and much more in the future. A quarter of the workers out there make 1/10th of that. So it was a good investment. Now you want ME to pay for your education that then allows you to earn $250K a year as a young doctor, and $350k in a few years, and then you clean out my pocket a second time when I get my medical bill? Don’t even get me started about the racket that is our health care system that now consumes nearly 20% of our economy.

As a retired engineer, I never made $350K per year…..actually, no where near that! I now pay about $4K per year for Medicare and my supplemental policy. My wife pays the same. Drugs are extra. Our out of pocket for “healthcare” is about $12K per year and we are in our 70’s. And it keeps rising.

Oh, when I got my degree, I paid my own way, but I needed less dollars back then. And the GL bill helped, but that cast me 4 years of my “free time”, plus had to dodge bullets, real ones.

Tough s***.

A private in the US Army makes US$20,000 a year or so in basic pay.

@R…Are you for real right now?

I wish one solution to all this as a compromise would be to charge the Fed funds rate for student debt instead of writing it off.

That way they get a break like the banks and all of corporate America but still have the responsibility and we don’t have to pay for it. If the gov’t wants to provide loans they should do it at that rate anyway and maybe that would be an incentive for us to not have it artificially suppressed all the time.

The cost should also be addressed as the root problem as salaries and amenities are ridiculous. Our state schools should be better funded to compete but just spend the money on good teacher salaries and classrooms only.

I support all this, but I want to add the cultural element: we can stop telling everyone to go to college and treat it as some status symbol or mandatory rite of passage.

I remember growing up in that culture. I started college in 2001. I wasn’t ready. I went back and finished it after having some life experience under my belt (and a burning drive to take it seriously).

The community college experience was people a decade my junior who didn’t seem like they wanted to be there, and who knows who was paying for them to sit there and get C’s and D’s.

My teacher would sometimes show the grade distribution, and it was always disturbing. So was running across cheaters… in an ACCOUNTING class.

But I’m guessing in today’s service-based economy, a college degree is serving the function that a high-school degree used to serve.

“It might be cheaper for the gov’t to pay for undergrad

and be done with it ,”

The colleges, which have now shown for decades of phonied up tuition inflation that they have zero ethics, would simply more deeply rape the taxpayers than they already have.

Ask the alumni what they think of the business morals of their schools.

Its the supply of free federal money, loans, that cause the increase in demand for that money, fees. A near infinite supply of Federal loan money means there is no limit to what a customer can pay. Same as in medical care with insurance money.

There is no real need for atudent loans, you can get a University education in another country way cheaper than in the USA. Is just validating that degree in the USA that’s a problem. If you do it using a student exchange program however the degree is usually recognized.

Of course that works outside of Global lockdowns and pandemics.

Make all the elitist college endowments cover all the losses from student loans. They can easily cover this with money to spare.

I agree, they are the bloated entities with overpaid professors. I hear there are many if not most who rarely show up in class. The schools should be made to co-sign any loan.

Nope. Not going to happen.

“A Cal Football Player Opted Out Because of the Virus.

Then Came the Tuition Bill.” (NYtimes)

Btw I’ve no idea what’s being fed to young kids, but 6’6″ at 330lb?

Totally agree!Lately these elite,insanely Wealthy schools talk alot of equity this,sustainable that,opportunity,blah,blah,blah while charging middleclass and financially struggling students Bigbucks.Hypocrites/posers!community college should be free/slidingscale,state colleges slidingscale with a good required ratio of poorer students admitted,accredited decent online/forprofit scools should have requirements to offer slidingscale tuition to a percent of the students. Yes,studenthousing became Wallstreeted,but the Real trouble xame with Reagan who cut Grants while pushing loans.Additionally,if state/Fed. Funding of higher ed. Is reviewed,it becomes clear that this was cut or neglected concurrent to grantcuts and increased focus on Campuslife,I.e.,loans taken out to build fancy and unneeded facilities such as state of the art gyms,theatre,fancy dorms,etc.Same time of these lovely developments,class sizes increased with more T.A.s teaching-or trying to!Costs of constantly revised,required textbooks add to the misery.

Trouble came with Reagan? Are you living in upside down world?

These reforms were crammed through by the D’s in 2009 and have everything to do with paying off the higher ed constituency, this is a purely produced product of the Democratic supermajority in 2009.

An endowment tax is actually something of a political winner.

Although the schools will all screech the predictable false arguments, the simple truth is that these phony “non-profits” have had compounding endowments essentially untaxed for many, many, many decades.

Their under employed alumni have little love for them and the general public has long since sussed out the odor of pretentious fraud that emanates from many areas of academia.

The “elitist” colleges with large endowments often have student loan default rates of <1%. Their graduates aren't the problem.

You're not suggesting Harvard's endowment pay for defaults of lower quality schools, are you?

SC7,

Are you suggesting that these phony non-profits have not profited from decade after decade after decade of untaxed income?

Do the math and see what a huge difference being untaxed makes to the final endowment amount.

Compounding is a b*tch.

Harvard might have to cough up $10-15B by itself.

As a FYI:

“As of late December, just 262 people had managed to get their student loans wiped away through PSLF out of a total of 38,460 applicants, according to reports citing Education Department data sent to Congress last week. This equates to an acceptance rate of less than 1%.”

Student Loan Hero dot com

April 3, 2019

2banana,

Do the math. The PSLF = Public Service Loan Forgiveness is a very unique program for people who go into public service. After making 120 qualifying payments (at least 10 years), they get the remainder of their loan balance forgiven. So by Dec 2018, the date the article you cited references, qualifying payments would have to have started before Dec 2008. The first qualifying payments under the program were at the end of 2007. So this was just the first trickle of the program that 10 years later had the first batch of loans forgiven.

more recent numbers:

https://www.forbes.com/sites/robertfarrington/2019/09/20/public-service-loan-forgiveness-pslf-numbers-are-improving-but-is-it-enough/

So, Banks + Loanshark.Gov … + Recruiters × ‘$tudents in a dire need of leaving the Nest ÷ Alma mater/Parents

—————————————————zzzzzzzz——————————–

!FOOTBALL! .. !BASEBALL! .. !BASKETBALL! .. !WRESTLING! .. !SOCCER!

– PAYING JOBS ÷ IMPOVERISHED TAXPAYER = hella grief for Greater

Plebian Financial-Ratchetstan….

Avg. cost for an ATP from Embry-Riddle was additional 150k on top of the ER ‘foo-foo’ degree cost.

Start adding lots of 000’s when turbine time spools up.

Easily paid off flying cargo in the hinterlands for $27,000/yr. /sarc

Automation will end those opportunities: Drones will do a better job faster and cheaper. Besides, robots can keep secrets!

What of all the people who…

decided not to go to college because the debt was too high

the families that did without to pay for college

the people who worked two jobs to pay for college

the people who actually paid off their debt

The PROBLEM IS college costs too much for no reason. Learning carries little cost. Dispensing knowledge and facts is a repetitive process ….recorded lectures and teaching assistants getting tuition breaks isnt expensive.

The Dept of Ed budget in 1978 was zero…it is now over $63 BILLION a year. That increase in spending is in exact and direct proportion to the increase in the cost of higher education. Imagine if each state could KEEP $1 Billion A YEAR for their schools. For simplicity of argument, $1 Billion per state (times 50) would still leave $13 Billion for some trimmed back Dept of Education in Washington.

The entire scheme, from higher tuition to loan forgiveness, all goes to the people who are indoctrinating our young people. And they are getting rich doing it.

If wasnt long ago that the ratio of a good entry level job salary to annual tuition was about 4:1. Now what is it? 1:1? 2:1?

I am gonna guess these aren’t the kind of folks the politicians are looking to buy their votes anyways.

“decided not to go to college because the debt was too high

the families that did without to pay for college

the people who worked two jobs to pay for college

the people who actually paid off their debt”

The problem is companies have set a college degree as a minimum requirement ( and are quickly working towards requiring a Masters ) for jobs that formerly required no degree.

Want a job as a receptionist? Those now require a bachelor’s degree.

Essentially, a highly overrated college degree (minimum 4 year BS) has replaced a high school diploma as a minimum entry level qualification for many jobs.

I call that credential inflation. Everyone seems willing to accept it as a fact of life.

But what can’t go on will eventually stop, and higher education’s gravy train of feeding off gov-backed student loans must eventually collapse back on its bloated carcass.

Wild card here is if Congress crosses the Rubicon and goes all in on debt forgiveness and prints to the moon.

If that happens one wonders what the fallout is likely to be. Will those responsible people and their families who payed off their student loans quietly accept this injustice?

And what about going forward, will student loan forgiveness morph into guaranteed free higher education for all?

Frankly (as a BS credentialed person myself) I see a rosy future in online degree certification (with perhaps some classroom/internship training for certain fields).

I would love to see the fat cat academics and administrative types squirm their knickers in a knot at that outcome.

It might be political suicide to cancel student loans. There’s a lot of former students out there, including me, who took out loans and repaid them, and I graduated in the middle of a recession.

These back-door bailouts of government sponsored loan programs are unfair. Don’t get me wrong. I’m all for higher education, but if public funding is going to be involved, it should be approved up front by legislators, not bailed out on the back end, so that everybody has an equal chance of benefiting from it.

Want a job in Oz to serve coffee at a coffee shop or to even wash dishes you need a resume……………………references and the lot……………

Cuz there was no Dept. of Education in 1978. There was the Office of Education in 1979 that had a budget of $12B.

Ienert

Nothing gets by you.

You caught on. And that’s right.

And yet the nation survived, sans Dpt of Ed (and 42 yrs of subsequent runaway tuition inflation) pre 1978.

Once the official bureaucracies get entrenched, the political kickback machine goes into ultra high gear.

Yes, these people are pissed

How many people saddled their kids with college debt when the could have paid for it?

How many of those people had second homes, boats or yachts, or went to Europe for vacation?

I know people who did all those things…and told their kids, “don’t worry, the debt will eventually be forgiven.”

Forgiveness is WRONG WRONG WRONG.

Why should an ADULT who can:

Vote

Join the military

Drive

Get married

Have kids

Etc.

Expect to have their parents pay for an expensive lifestyle choice?

It’s important to remember their parents are the reason college is required and why it is so much more expensive than when the parents were college age.

And WHY is it so much more expensive?

The cost is the issue that creates the magnitude of the debt.

“And WHY is it so much more expensive?”

Student loans where the lender takes no risk because the taxpayer will bail them out. Prices rise to what the customer can bear. Only bought and/or stupid governments wouldn’t know that exactly what has happened was certain to happen.

College prices used to be limited by what the parents of the student had saved up for college or what the student could earn with a part-time job while going to school. Not any more…

Pay your Debt

Truth: Debts that cannot be paid, will not be paid. My question(s) A: are all these debts securitized? B: If the Feds are guaranteeing them, then the Fed should have a say in the tuition cost, right? The Ivy League is paid for it’s high powered social connections. Education? Not so much.

These debts are owed to the US government thanks to the “reforms” of 2009. Thanks Democrats.

How about those who went to trade schools and learned a craft, and took a loan? Do they get the forgiveness also?

And what of those who borrowed (it was allowed) for apartment rental and “incidentals”?

The entire mechanism was designed to PUMP UP debt. Imagine that from the Government?

And, recall, the first thing Obama went after when he was elected first term,…..taking control of student loans. Now why would that be on the top of his list? Anything to do with fluffing the mechanism that indoctrinates our youth and funnels money to those who are engaged in doing so?

WOLF

You posit

“…Any solution to the student-loan crisis needs to include measures that shut down that money-transfer and return the government’s role in student loans to where it had been before 2009…”

Is your response to gorbachev the way it was prior to 2009….or…..was it something different ?

It’s different. For example, textbooks have always been a ripoff even in my time in MBA school (huge ripoff). But now with ebooks, textbooks should cost $10. But the big issue today is that there is no discipline because the government pays for it. There was at least some discipline before 2009.

And they constantly ‘churn’ the texts, so last year’s can’t be re- sold.

But shouldn’t a text have the latest news?

NO! Especially at the undergraduate level. Profs complain that students have a weak grasp of basics.

There is no good undergrad text that is obsolete less than five years out.

As for Grey’s Anatomy, or Romantic Poets…

Gee Nick, how can my perfesser (that I see a few times in a semester) maintain his $250,000/yr lifestyle if we don’t have revised (required) $200+ textbooks every other year? Those consulting fees are just too erratic.

I got a 2.500 dollar lown 2.500 you read it right they sold the loan at least 20 times this all started 1983 most of the time i didn’t even know who to pay.? To date i have paid just over13.000 and still owe over 9.000 they will never get another penny from?me

And unless you pirate them, there is no way to buy “used” ebooks. In careers whose books don’t change much, buying used textbooks that saved some money.

Yes, these digital rights management techniques are nasty. But it’s less of an issue if the textbook costs $10 instead of $150.

Back when I was buying used textbooks — and yes, they saved a lot of money — they worked for a year or two. And then Chapter 12 became Chapter 8. And other changes were made to where it was really tough using the text book, and it became essentially trash, though the info was the same.

That entire industry was a scam. I remember in the 90s, buying my texts from used book stores and such. It was never cheap, and heaven help you if they changed an edition, I have no idea how many times I would see the used book, but then when I checked the syllabus, I would see it’s a new edition.

It’s like they had the pages all made in advance, and then they just swap things out every couple of years. Remember hearing of at least one instance, where a few students got together, they chipped in, bought a text, and then xeroxed the rest. I might not agree with their method, but I understand the reasoning. $85 for a calculus book, give me a break…. (that was in the 90s)

My mom was an editor at West Publishing of St Paul, MN for 18 years starting in 1974. Title: Senior Production Editor, College Text Book Division.

The toughest class for me to get my physics degree was a senior-level multivariable differential calculus class – which I’d put off until the end – and passed with only a C grade.

A few years after graduating, Mom gave me new copy of the book I’d used for that class as it had been revised and edited by her. Damn expensive and not sure why it needed to be revised, but it looked good & there were no typos!

“That entire industry was a scam. I remember in the 90s, buying my texts from used book stores and such..”

In the 90’s huh?

How about in the 70’s?

Books were expensive back then, but theuniversity bookstore always cheap second hand ones…………

That was fast:

“$147 billion in 2009 to $1.37 trillion at the beginning of 2020.”

In places like Scotland and Germany, governments eliminate the middle man (or woman or LBGTQ) and make colleges free.

Nothing is ever free, and in government-run systems the government IS the middle man (and many of ’em!).

The goal should be to reduce the overall systemic cost of a high-quality education, not just the direct cost to the student.

Finally, the student needs to have skin in the game… incentives to choose an educational path that isn’t an economic dead end. One might argue that the educators needs some skin in that game too.

… incentives to choose an educational path that isn’t an economic dead end. …

Trying to follow the Soviet ideals of centrally plan “where the jobs are going to be” five, maybe eight years into the future is not going to pan out the way “everybody” thinks it will, even when rebranded!

Education must be for the benefit of the individual. The most successful of those individuals will create ways to use their education that maybe didn’t exist before, getting in front of the “next thing”, tangentially benefitting “business” and “society”.

Starting out with demanding that education is shaped to make the individual benefit “business” and “the state”, then making it “an investment in the future” is putting the cart before the horses so to speak and will only do one thing well: Getting trained people behind the “already fading thing”! Like all those “Multimedia Designers”!!

PS:

The people pulling down the biggest salaries are from “Humanities”, the people driving shittier and shittier cars, while getting no-where, are mostly STEM candidates from the naughties!

Yes, look at a campus in Germany. Drab office buildings. No sports arenas. No cheerleaders. No 50-meter pools. No on-campus residence requirements, etc. Students there get an education. Here, they get an education too, if they want to, but they get ripped off by the educational-industrial-financial complex via tuition, housing, textbooks, etc., which has been enabled by the government via student loans.

German higher education (university level) is reserved for students that are proven qualified for that level of learning (as opposed to US where every kid and their dog can probably be admitted to all but the most prestigious universities).

There is a dual track education system in Germany whereby students who can’t qualify for university or lack the aptitude can follow a vocational training path that would eventually lead to an internship and well-paying job.

Is it any wonder that Germany used to produce some of the best scientists, teachers, and technicians in the world?

Are you saying that US institutions of higher learning shouldn’t tilt the playing field to support BIPOC and whatever other acronyms you can come up with so that they can look like they are filling some diversity quotient?

How dare you sir…. I’ll have you know that the US model a merit based society with a critical eye toward equality and justice for all. Higher education institutions in Germany has a lot to learn from their peers in the US about things like how to be equal and how to be just and such things. Germany may have come a distance from their roots in WWII, but they still have a long way to go to meet the US standard.

You know, the standard where we don’t educate anyone, rather we brainwash them and turn them into debt slaves at the same time. US institutions are a model of excellence in this field, and we are equally focused on screwing over every ethnicity possible.

College is an “experience” Wolf, a rite of passage in America. It’s not supposed to be drab education. If you wanted education, you can get books from the library and read them, including higher level math and science stuff. :)

Young people should forget higher education and get straight into the workforce, learn a trade earning as you go. Might not earn much to start but in the long run you will be much better off. Also no student loan to pay back for a useless degree. The best life skills are learnt on the job.

Sure.. you just create a list of people that want to train them in said trade, and line it up to the number of high school graduated there are in this country. You tell me which number is larger.

The economy should make enough jobs for them, then.

Good luck with that, especially with many trade jobs being outsourced and now increasingly automated so they don’t even need extra workers.

Considering the banks got bailed out in 2008-9, they should have insisted that they not charge over 3,5% interest on the student loans. Many students, old and young, watched as the loan amount skyrocketed through compounding interest rates of 7-9%.

Using the IDR program is just another bail out birthed from the moral chicanery that started with the removal of Glass-Stegal bank limitations their subsequent bailouts.

Banks don’t lend to students,,,, it has been totally taken over by the federal government!!!

This isn’t the banks, it’s the Federal government.

Well if I pay off their loans as a taxpayer I should receive a check also where is accountability no free lunches

Are you a farmer? If so, then you to will receive a check.

Have a close friend who teaches (Higher Ed, 4 year State University). Her department has 23 educational ‘professionals’. Approximately 11 of those individuals only teach 1 – 3 hour course per semester. She normally teaches 4 – 3 hour courses per semester.

Her pay is right around $54k a year. Plus she contracts (added $8k a year) vwith the university to do a specialized job that the university would have to go out & hire .5 FTE ($60k a year for a FTE).

Total comp is approx. $62k a year, plus health bennies. Add 40% for bennies (another $25k). So $87k total.

She has (current semester) 146 students in all 4 classes, so 146 x 3.00 = 438 credit hours. The current composite billing rate per semester hour is a very, very, very closely guarded secret, but best estimate is $1250 per hour (and that’s on the low end).

So, that’s $1250 x 438.00 = $547,500 for this current semester. And that’s with 75% of the year being remote learning.

So, $547,500.00 x 2 semesters per year = $1,095,000.00 – $87,000.00 = $1,008,000.00 PROFIT.

Looks to me like Higher Education has become one giant scam, and we are the ‘scamees’.

She LOVES teaching. But it’s tearing her up with what she feels are the students being cheated and indebted, and with a lot of her colleagues being imperious toward the students, and just ‘phoning it in’. She does not see this ending well.

Some of that $1,008,000.00 profit pays for the parking lots, building cleaning, HVAC repair, campus cops, the pool and gym, sports teams, teaching assistants, library staff. Some for students who don’t pay based on skin color too.

Published audits with all overhead and other cost numbers shown should be required to keep getting student loans.

Don’t forget the multiple mortgage payments on the stadium and swimming center and plush student union.

Everyone keeps talking about how the Coastal Cultural Elites (Democrats) need to start listening to everyone else. That would include people who never went to college, people who went to State instead of out-of-state, people who lived with Mom’n’Dad (yuck) so that they could afford school at all, and people who put on the uniform – risking their arms, and their legs, and TBIs – to earn their tuition under the GI Bill … while defending the people who now want their civvie ride to have been for free.

This is appalling, and is a huge mistake.

Terrible. Profiting from debts that are so exploitative that many can never be repaid is not a good way to make money. Bloomberg also touched on this a wile back:

“though they’re meeting their $1,300 in required monthly payments, their balance has remained roughly the same over the last year because Vicky’s outlay doesn’t cover all of the interest on her loans. For all their education and career success, the Wilsons can’t envision repaying their school debts—ever. And forget about buying a home or opening a college fund for their 3-year-old son. “We don’t even think about it,” Jon says”

and

“few know that this generation of borrowers is chipping away at their debt so slowly that some may not escape it until they’re dead. That’s the grim assessment of a new Bloomberg Businessweek analysis, which found that U.S. student loan borrowers as a group are paying down about 1% of their federal debt every year. It’s as if a former student were reducing the balance of a typical $30,000 college loan by only $300 annually. At that rate, it’s almost unthinkable how long it would take to repay the government: a century.”

https://www.bloomberg.com/news/articles/2019-08-16/you-may-be-dead-before-you-pay-off-your-student-loans

What about MMT in the near future to cover student debt, pension shortfalls, big city debt , UBI, reparations etc. politicians will never talk austerity until one day it is forced on us.

So in other words the student debt is a perpetual tax not a loan. Perhaps by design?

A partial solution would be to make sure that all members of the “the educational-financial-industrial complex and printing billionaires” pay their full share of taxes and become taxpayers like the rest of us.

You mean like Buffet and Gates pay their full share of taxes… hahahaha.

I think that is just one of the biggest lies of all. Buffet has bragged for years about how he doesn’t pay nor taxes than his secretary, was that because he knew how to cheat on his taxes? No, he just employed a bunch of lawyers to set up family offices, “charitable foundation,” etc to make sure he pays nothing. The tax code then lands right on top of the middle class or the upper middle class while Buffet, Gates, and their pals all laugh their way to the banks.

There is literally nothing stopping Buffet or Gates from whipping out their check books to write a massive check to the IRS, except… they have no income, their bank accounts are pretty standard. Of course they have multi billion dollar family offices and charities to make sure that they pay nothing. Wonder how Bill is making out with his investments in vaccine makers or with Impossible foods.

I wouldn’t mind being part of that scam.

Buffet wasn’t bragging, he was telling lawmakers to raise taxes. What difference does it make to the tax code, or the deficit if Buffet writes a check for a billion?

And that Gates guy, funding vaccines just for the write off! What did Trump fund to end up paying 750 dollars in 2019?

Maybe the answer is on ZH.

He was, and it wouldn’t affect him one bit. That was the entire point.

Buffet says I make too much, I should be taxed more, but in reality, his team long ago set up protections for all of his assets. If he was so insistent on being magnanimous to the government, he’d just write a check, that’s the point of him being a hypocrite on this matter

Ummm, so Trump paid $750 in taxes?

Really?

How much taxe credits were applied to the tax bill to leave a $750 remainder?

Yes really. Widely reported, never disputed by Trump. Not to say they won’t be investigated after January.

One write off: Payments to Ivanka for consulting.

Sounds like yet more Extend & Pretend.

There’s a moment in the movie depicting the Apollo 13 mission where the politicians are bemoaning out loud the current state of

the appearance of the greatest disaster in NASA history when the

Director of Mission Control, played by Ed Harris, corrects them: “With all due respect, Sir, I believe this is going to be our finest hour.” This is what the student loan mess combined with Covid-19 restrictions has the potential to produce. It is not just another debt to be paid; it is an opportunity to make substantive changes in how our children are educated at every level.

So, surprised the students turn out to simply be a special type of SPV – a conduit – in this mess? You shouldn’t. This has always been a stimulus program. Just take a look at our wonderful pre-Covid economy everyone glows about – the so called ‘good old days.’ What did you think was propelling growth since 2010? Instead this was just another manner of pumping money into the economy without both the needed transparency and the wisdom to stop and consider who the ultimate beneficiaries of that economy were. Be pissed. Just don’t go

blaming the 18 year old who was taken advantage of after having been cheated out of a K-12 education. Aim correctly. Like we did with the 2017 tax cut for the 1%.

What are we promising these kids anyway? A trade? A career? A class distinction for marketers? To be marketers? Aim correctly. What should College provide? How much government mandated format/curriculum do we want? What should having a College degree indicate to employers?

I have an idea: it should mean the kids have been taught how to measure, evaluate and present contrasting opinions/ideas to others. How to effectively use math, words, science and social theories to follow the logic of competing ideas. How to honor but constantly test our social contracts to find where these kids best fit in the world. College should be making them ready for the changes coming over the course of their lives and how to find tools to fit and re-fit and re-fit again as our social

contracts change and, by and large, improve upon the original promise made: of, for and by we the people. There are lots of ways to do these things. The first one is to talk about them. Perhaps we need trillion dollar losses to get our attention these days.

To do this you need to commit to the process of using a government system of incentives to tear down a lot of ossified college departments and services and re-set higher education upon a central theme of educating a kid for the challenges of a changing world. No small order when the colleges are full of professors and administrators who have been taught extraordinarily narrow specialties in school then how to protect turf once becoming a professor and/or administrator. Instead demand that we teach these College grads to do something really important: teach them to think. They should have been taught about compounding interest in 12th grade.

But you could say this about a lot of careers. Doctors come to mind immediately – the smartest kids in the class, most destined to mindlessly check your blood pressure or to proscribe antibiotics depending upon the color of the mucus. Lawyers are no different – the clever but lazy ones who now mostly fill out simple forms to be rubber stamped by the union down at the courthouse.

{SideBar: In many ways our fight with Covid-19 has been the finest hour for many in the medical field. A fight with an unknown before, unseen until dangerous, and evolving enemy demanding we step back, take off the shackles of routine and truly think with the thought skills we have been provided in College to look for patterns where none seem evident, treatments where none seem effective, vaccines in time periods thought to be impossible, throwing up more and more ideas while arguing for

acceptance based upon facts then known. But mainly thinking in ways which do not even see the box they are thinking outside of}.

So drill down into and through this student loan veneer, find the social contract, discover who got the money, why, and how it was used. Did the tax payer ultimately benefit? If not, why not? Logically follow facts to a remedy. Just aim correctly.

And don’t blame 18 year old kids. The student loan mess is one of those times where the kids are the last ones to blame. It is also one of those times where we can demand the country strike out in a new and hopefully more transparent direction. Use it to expose the hypocrisy – if such a thing is possible – and then educate the Congress. Show this to be one of our finest hours in demanding a better education for our kids.

Apparently, the Affordable Care Act allowed the federal government to take over about 90% of student tuition loans (2010). Private lending dropped by 90% as a result of the ACA. As of 2018, the tuition loans accounted for almost 40% of federal assets. Is that the $435 billion? I believe it was Elizabeth Warren who complained that the feds were charging up to 8% in interest on their loans (i.e. those graduate degrees I’ll bet). If that 8% is compounded there is no way in Hell these loans will be paid back. They shouldn’t be paid back. The reason tuitions are so high is because the major lender (The feds) let the good times roll for their favorite university. Per usual, where there’s billions made, there’s crime involved. Fraud in this case, would be my guess. Anyway, if the ‘debt’ is on the feds balance sheet, it can be forgiven. Reduced to zero. Just because your kid got screwed, doesn’t mean all the future kids should be screwed too.

I think in setting interest rates the rate is set at the treasury rate plus the estimated default rate plus a slight premium to make it worth the effort. If taxpayers are going to lose money the rate wasn’t set high enough to cover the default rate.

Some predatory degree mills counted on their fast-talking approach to rope in gullible 18 year olds. They showed slick marketing brochures and promise pie-in-the-sky careers, while having those youngsters sign away to get locked into their system.

That worked for a time, as many listened to classmates and signed the loan documents. They got a crash course in debt servitude, along with a useless ‘degree’.

Happy Ending: One such diploma mill got caught and had to sign a consent decree forbidding such shady practices. They later went bankrupt, but not before trying to rope in more youngsters. Their sales people must’ve had loans to pay back, too.

Other people’s money + printing money = savers eat rice and beans.

Quite well said. I would disagree with: ” They should have been taught about compounding interest in 12th grade.” They should understand compound interest in 9th grade. By 12th grade they should understand a mortgage amortization table and the net present value of an income stream. It is not rocket science. You also used some words apparently proscribed for many students: science, math, and most especially logic.

The hilarious part of all this is that the rich are probably going to go bust along with everyone they detest. It’s a long fall from the roof when the string of Christmas lights proves to be a poor rescue plan….one by one the fasteners rip loose. Don’t let the shingles hit you in the head on the way down!

There is a bust, and then there is another bust.

$5,000,000 -> $500,00 = living more uncomfortably.

$50,000 -> $5,000 = homeless.

Numbers? 1/3 Preoccupied. 1/3 Loyalists. 1/3 Very PO’d. Result: Goodbye King & Parliament. Put 100 million in jeopardy and that 500 grand won’t mean shite. Don’t think they aren’t getting very nervous in the clouds…one mis-step and this game goes tilt. Funny little bugs.

I find it repugnant that a system even exists that loads up citizens with 5-figures or even 6-figures of debt as a price-of-entry just to be given the opportunity to find work in our country.

A:

Your comment is +1000!

It’s all about money.

We are all, including our pets, “money fodder” for the oligarchal business interests. The country was never anything otherwise. It’s now becoming more evident because all the money making (snake oil) schemes are becoming exhausted….the only thing left is the selling of debt. Once M. Milken made it shiek to own debt it was another step into financial oblivion.

We are a disgrace as a country.

As long as the perception in the bond market is that deficits do not have any cost , the government is going to bail out the student loan program , among many others such as state and local pensions

Maybe being able to sell 30 year government bonds “in the market” at a rate of -2% has something to do with it?

Think about it, you are the UK government, short about 100 Billion in 30 years, -2% yield bonds due to Corona. Then interest rates goes back to, say 5%. PoooF, goes all that debt, when you issue 30 years, 5% bonds to buy back the -2%’ers at pence on the pounds nominal!

Now, If “they” had used Free & Gratis money wisely, then it would have been “our finest hour” indeed. Of course, they will waste it all on their cronies!

That seems to be the plan. The easy money policy is just allowing uneconomic things to go on and on. Might be faster just to say a leaf is worth a dollar and if you need something go out and grab some.

I thought at the time that getting banks out of the profit chain was a good thing, but the devil was in the details of defaults and forgiveness. I do not support federal loan forgiveness, especially at the paltry income-based payments instituted. If there is any possibility of forgiveness, of course you leave the student debt unpaid while paying off your car or house instead, or just buying more stuff.

I have known people who spent their students loans on weddings, ATVs, foreign travel, and, lastly and obviously, degrees that have no worth. I know government employees who paid the minimum loan payment all these years because they are counting on the public service student loan forgiveness program, although they haven’t read the fine print on it. Do I want them to suffer the consequences, even if it was a system begging to be played? Absolutely. As for public service loan forgiveness, it perversely attracts the biggest debtors, not the best and brightest, to government jobs.

I do support forgiveness for many of the people steered into public and private loans by for-profit colleges. Forgive their debt if the program was worthless and put every last former and current administrator of those places in jail, along with their buddy Betsy DeVos.

Because few dare to attack the increased rot in the educational system, and hardly anyone ever dares to drastically defund it, it now attracts even more sociopaths to its administration, where they can play their power games and make bank so readily. It’s too easy to rip off taxpayers through schools and non-profits by exploiting the public goodwill towards them. Bogus credentialism is a huge part of the problem. An Ed.D. is a degree in fraud against taxpayers, but now school districts and universities often require them for deans, principals, superintendents and college presidents. The only hard skill they have is inflating their own salaries to the stratosphere. Get them out of the system by delegitimizing the Ed.D. (although in the status quo it’s still one of those graduate degrees that does pay for itself). Yes, there are overpaid faculty too, but not all and not everywhere. As for defunding the bloat in universities, legitimate and successful programs always get the ax before administration, because administrators make the choices. Alaska demonstrated this recently, pre-pandemic.

Developers and landlords also benefit from the debt. How else could students pay $700-$1000/month for rooms in luxury dorm-style apartments going up everywhere? The correlation with billionaires being made is the local population in smaller places not being able to afford limited housing, and the abundant students driving service wages down toward the minimum. Student loan-inflated rents thus create more homelessness and economic hardship. The knock-on societal effects really are endless.

Drastically reducing the federal student loan limits would be a major shock to the system, but it’s a needed shock.

Thanks for mentioning the little noticed fact that, according to my info, student loan money can be used for many other things than tuition, room and board, and textbooks.

Do you really expect 18-22 year olds to be miserly and penny-pitching with a largess of other people’s money?

Taking beach vacations on spring breaks? No problem– Uncle Sammy is there with cash. Clothes and jewelry? Why not?

That is the darkest fraud of the student loan scam (along with the middle men Wolf mentions that skim off the whole stinking mess).

A lot of apple products and plane tickets and even some stock gambling were paid for with student loans (my son did that). Money is fungible you know.

How quickly people forget that this was how Obama reduced the unemployment numbers.

Student enrollment has been declining since 2011.

Financial consequences have lead me to make infinitely better choices in my own life. I feel sorry for those who have financial consequences “vanquished”, as I believe paying debts build character and long term mental fortitude. When things are “free”, humans do not make good long term choices as only the present matters, thus the future and past become irrelevant. If my own college had been free, I would have most likely not have graduated a year early, and would have taken easier classes, and perhaps a junk degree as it would have been more of a “life experience” versus a means to future stable lifetime income. Because I had to pay 100% of my own college, I could not afford to fail or spend years of my life getting a useless degree. Paying all of my college was net positive for me (took 5 years). I feel sorry for the current generation to be honest, who have the moral hazard removed from making poor financial choices. It sets them up to make a lifetime of mistakes that could have been changed via natural fiancial consequences. What started a decade ago with “trophies for everyone” and “no red ink on test papers” has now morphed into a finacial consequence free society. Perhaps it will work for the younger generation, yet I personally know that my fiancial failures are what made me, me…and I’d be less financally successful currently without “paying” for my past fiancial choices. So for the 11% of college debt holders who are paying their bills at this moment, I applaud you because long term, you will make better fiancial choices via current financial consequences. I believe all humans need “consequences” to force better long term choices as “consequences free” by nature is unhuman…

So all those degreed Europeans who received free tuition are dummies because of it? Not on your life. The real dummies are on this side of the pond.

Touché.

Again, they didn’t get “free tuition”. They got an education paid for by someone else. In Europe the high taxation rates and other elements of the social contract ensure that those students will pay for that education by other means, or pay it for the next students at any rate.

Yort (and others)

Just what is a “useless degree”??????????????????

Explaining that to me will show me what kind of human being you truly are!

Degrees granted to people who aren’t able to further their professional lives and make society better would fit that bill. Degrees that don’t prepare people for work in some fashion also. What exactly does a person get with ethnic studies, marketing, sociology, or psychology in most instances? Is society as a whole, or that individual better for their 4 years and 100K? I think we all know the answer.

Heck, my granddaughter just got one from Sam Houston State College:

4 year degree in “Health Services”.

She couldn’t get a job for months, then landed one at a non-profit doing “fund raising” (cold calls) at $14/hr.

Great future in that…….

I agree with how student loans have let universities raise prices uncontrollably.

But the raising of dollars of debt you cite is largely caused by getting rid of all the privatization but still fed guaranteed debt.

Student loan debt is not discharged in bankruptcy. Most of those in the forgiveness programs will pay a large share of debt thru them.

I am mostly concerned with the students who went into debt for sham degrees and no career prospects. Many of these folks will have the debt follow them their entire lives. For ever!

Speaking of sham degrees .. Why should students getting theology or social work degrees be able to borrow the same amount at the same interest rate as kids getting a medical or computer degree ? Some fields have near 100% of their graduates employed at high income, others have a surplus of degree-ed people not even earning enough for a car payment.

The kids at my college who were getting student loans were the ones with nice cars, nice apartments and frequent trips. Many were women with kids who entered college just to get the loans to support their kids because the fathers could not or would not pay child support. They never had any intention of paying them back. Others were going to med school or law school and my ex girlfriend (law school) never intended to and never paid anything significant back. The nation might be better off with a national child support program since most men cannot pay enough in child support for a woman to raise a child. This is a national issue since over half of the children born in the US are on Medicaid meaning they are financially impaired. If we are going to allow unlimited childbirth in the US we need to come up with a way to pay for it. Studen loans are not an efficient way to do it.

My Golly, Miss Molly. Half a trillion in govmit encouraged debt down the drain. Why it almost makes you wanna think maybe Mr. Powell oughta be thinking ways to encourage savings and discouraging debt. Like normalizing interest rates. Now. And jawboning risk and lower asset prices instead of baby talking them up and giving markets free $trillions$ to play with for kicks & giggles. But then what do I know? Shirley Mr. Powell’s knows what he is doing with his plan to encourage more and more debt forever and ever and ever.

1.37 Trillion, Wolf? are you funning us?

137 is a pure number, Alpha. The cosmic constant.

… Ok, so the Vertex-Ascendant, I see it, it’s been awhile, the 137°arc.

it’ll be next year, like, hello we’re here, sorry for crashing.

Forgive loans get more loan applications.

Count me in.

It will be a howler to see the national debt next year. About 1/6 of collected taxes are wasted now on interest on the debt even at these ridiculously low interest rates.

Of course under MMT, the interest is paid by the treasury to the Fed which pays it back – less corruption fees.

Big changes coming for everyone, virus lockdowns, job loses, bankruptcies are just the start of the ramp-up. Calm before the storm. Don’t laugh, 5 years ago you would not have believed what is going on now. Water is heating up frog.

Milking the government coffers is an ever-growing percentage of the economy.

Are you seeing the commercials where old sports stars are telling seniors they are probably missing out on many benefits Medicare provides? Oh heck yes, let’s make an industry out of squeezing out every dime possible instead of just using the insurance for actual health concerns as intended.

Meanwhile, the politicians won’t touch this hot potato, much less care.

M-I-D-A-S Disease. When I worked at Merrill Lynch, an older broker came over and put his briefcase on my desk. “There’s a million dollars in this briefcase. I want you to invest it for me. What you are feeling right now is greed.” He then pulled out a pistol and held it up. “If you lose any of my money I’ll come back and shoot you dead. What you are feeling now is fear. The lesson? The only thing that will control greed is fear.”

I’m very surprised Wolf didn’t mention the Student Loan Asset Backed Security (SLABS) industry. Similar to morgages in the runup to the financial crisis. Whole white collar armies helping to securitize the loans into bonds.

It’s not so different this time. Bailouts for “students” will go to SLAB holders.

My nieces ex husband was (still is?) the loan restructuring business as an office manager of the those who make the phone calls. From him I learned:

1. The company gets a fixed fee ($1,500 ?) from the government for everyone they sign up.

2. It is a one time only deal for the borrower. If they decline or fail to follow through they don’t get another chance.

3. If in the plan they are reviewed once a year for payment adjustments.

4. They are not in default even if they pay only $1/month.

5. Meanwhile the loan balance keeps growing.

and lastly and very important:

6. When the loan is forgiven after 20 years it is reported to the IRS as income. And they can go after everything, including parts of SSI.

My friend’s brother made a very nice living as a manager for Sallymae and then one of the big banks in the student loan business. I was always a little jealous being a design engineer that he made a lot more money than me probably about 4 times by pushing debt on young people.

My whole work life was basically a period of debt expansion and people got paid well to push the debt out.

“But who ultimately got this money, since students were just the conduit?”

I’d say 25%-50% of the money went to students so they could pay for food, rent, I-PAD, Beer, car insurance, vacation, eating out.

There is absolutely enforcement of where the money goes.

[iffy for-profit colleges with dubious degree programs]

Honesty those colleges should have all definitely be shut down. How? They ALL take government loans so the government really should look at who they are lending to.

While the USA government making loans that are básically charity is not something new, they really shouldn’t be lending money to scammers.

What about this expanding blackhole, which is an even greater joke with the pandemic:

Today colleges’ assignable square feet is estimated at about six billion and growing, and there are about 13.2 million full-time students. That works out to about 450 square feet per student. “The space per student has in some cases tripled since the 1970s,” Mr. Parsons says.Apr 17, 2009

Student loans are just another stimulus program for the cities.

Except for this site, why is it that I can’t find any news about the economy that isn’t a bunch of cheerleaders?

Maybe because we live in the new Amazon-world of cash-conversion-rate, winner-take-all, things have become different. Maybe future value has become less and less important as short-term immediacy has turned our economy into a real time casino, where debt plays less a role, as people wish away future obligations, pretending that our fantasy world has sustainable underpinnings. That philosophy may be part of the reasons that our education system is more and more worthless, as it churns out pointless diplomas, for this that hang in there to actually finish programs that are linked to mountains of debt.

Although my mishmash FRED charts are not perfect, the following visual paints a picture that explores the current relationship of debt and casino mentality:

Left axis: (a) Assets: Securities Held Outright: U.S. Treasury Securities: All: Wednesday Level, Millions of U.S. Dollars, Not Seasonally Adjusted (TREAST)

Right axis: (a) Wilshire 5000 Total Market Full Cap Index, Index, Not Seasonally Adjusted (WILL5000INDFC)

I obtained my college degree long ago via a ‘quid pro qou’ program. That is military service, including a year in SE Asia during the Vietnam War, in return for the GI Bill.

I did too (4 years served). And the GI Bill is still available. And you don’t have to go fight anymore. Plus, you can get $50,000! I got $222.00 per month for 4 years.

It, with a part time job, got me through 4 years of engineering school. NO DEBT!

Actually, GI Bill II is available. The first one was killed and replaced with VEAP which you had to contribute to. That was a failure (inherent design flaws), so they brought back GI. Of course, they don’t want anyone mentioning the mistake.