But the problemita of pulling the rug out from under the entire banking system still needs to be addressed.

“As cash use continues to decline, the question naturally arises as to whether central banks should provide a digital alternative to cash that also provides some privacy features,” says the blog post, titled “Monetizing Privacy,” by the New York Fed. The post is based on a 26-page academic paper on digital payment methods that have been used broadly, the current market structure of digital payment methods, the data-gathering that occurs, versus cash payments that preserve privacy – and versus the “digital dollar” now being worked on.

Each time a digital payment takes place, the companies involved gather voluminous amounts of data and hang on to it because it gives them a competitive advantage in selling more goods or services to this particular consumer. This data has a lot of value for these companies – a key point we’ll get to in a moment with regards to the “digital dollar.”

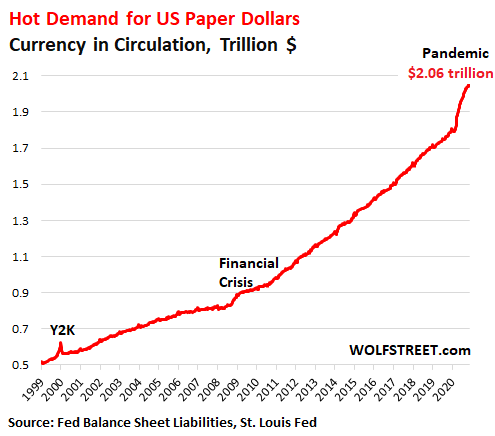

While the share of cash in transactions has declined, US dollar bills are being hoarded like never before. “Currency in circulation,” which the Fed reports weekly on its balance sheet as a liability, has soared during the Pandemic, reaching another record last week of $2.06 trillion, having doubled since 2011:

The amount of currency in circulation is demand-based: Banks have to have enough currency on hand to satisfy their customers’ demand for currency, and during a crisis, people load up and hoard cash, much of it overseas, and to meet this demand, banks have to buy more currency from the Fed, usually paying with Treasury securities for this paper.

The digital dollar is not going to replace “currency in circulation” for hoarding purposes. Dollar bills will continue to fulfill that function. Instead, the digital dollar will be designed to compete with digital payment methods and checks.

The digital dollar – or more broadly, a “central bank digital currency,” or CBDC – has been on the back burner or on no burner before the crisis. But it has now been moved to the front burner.

Numerous Fed heads, staff, and former staff have stepped forward since the Pandemic began, expounding the possibilities of the digital dollar. In late September, Cleveland Fed president Loretta Mester, said that the Fed is now even looking into harnessing the digital dollar to send money directly to households, even those that don’t have bank accounts.

So now the New York Fed is touting the digital dollar in an entirely different sense: privacy and pressuring companies to pay consumers for the data they collect.

OK, we’ve got to get this straight: The digital dollar, if designed properly, would protect the user from the prying eyes of Corporate America and its vast data collection apparatus. For this purpose, it would be like paying with cash. But it would not protect the user from the Fed’s prying eyes.

This consideration of privacy from the prying eyes of Corporate America should go into the design of the digital currency, the article says, adding that “a privacy-preserving digital payment method may improve consumer welfare,” in ways that are somewhat unexpected.

Central banks, such as the Fed, don’t have a profit motive since they can create money at will. So they have no motivation to use the consumer data that they would obtain from their digital currency, and, the article says, are “better positioned, relative to private intermediaries, to commit to safeguarding data from outside vendors.”

The concept of “Monetizing Privacy.”

So bear with me for minute. I’m trying to lay out their argument here.

The digital dollar would run in parallel with cash and the current digital payments methods. The logic goes, according to the New York Fed, that consumers would have a choice between Corporate America’s payment systems that collect volumes of data in order to use it and target that consumer, and a central bank digital currency that also collects data but does not use it.

With a digital dollar, consumers have suddenly power, the argument goes. They can tell Corporate America that they will henceforth pay with the digital dollar, thus depriving companies of the valuable data they collect from the payments system. And if a company wants consumers to use its payment system in order to enhance its competitive advantage, it must offer consumers incentives, discounts, or rebates (such as the familiar 2% cash back for using a credit card).

In effect, consumers could pressure a company into paying them for the data it collects, under the threat that if the company refuses to pay for the data, consumers would switch to the digital dollar, thereby depriving the company of the data that gives it a competitive advantage.

This is how consumers could “monetize privacy” – they could effectively get paid for their data, turning their data into money for them, not just the companies that harvest it.

“By helping consumers to monetize privacy, central banks would not be proposing a radical transformation to the payments landscape,” the New York Fed article says. “Rather, they would be preserving aspects of payments that existed prior to the digital revolution” – meaning a digital version of dollar bills.

The creation of a digital dollar is not going to be easy, however, and there are some unresolved problemitas, such as the entire banking system, the article says:

- “Offering ubiquitous and direct access to central bank money, let alone one that is privacy-preserving, requires a reliable and robust system.

- “With the commitment to privacy, regulators and lawmakers would have to rethink how to adapt current anti-money laundering practices.

- “Finally, the impact of CBDC on the existing banking system and financial stability must be considered.”

The last point is particularly tricky because the digital dollar would in theory eat into some of the core functions of the banking system, such as processing payments, including credit card payments and all the fees that come with it, taking deposits, and possibly even some lending functions. And the Fed isn’t going to pull the rug out from under the banking system. So, it seems, some details still need to be worked out.

But the idea that a digital dollar would apply competitive pressure on Corporate America to pay consumers for their data, or lose those transactions to the Fed, and that thus consumers would benefit from the digital dollar even if they don’t use it, is one more piece of evidence that the Fed is very seriously paving the way for this creature, and is pitching it in different ways.

Online sales jumped 37% in Q3, after 44%-Spike in Q2. Online food-and-beverage sales were up 160%. Read… Online Sales by Category, in Weirdest Economy Ever

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

No matter how I view this, I am nothing more than a digit!

I fear the Fed, as usual, has this completely wrong. People-as-digits aren’t just bank accounts, they are also physical addresses, cell phone numbers & locations, social security numbers and many other digits. Companies like Amazon will still be able to associate purchases with people via addresses and other contact information, because an order has to go somewhere. And in the physical-store realm, enterprising banks will still be able to match customers with their purchases by creative tracking and sharing of data. When a bank gets a real-time debit from the Fed for $123.45 for Joe Sixpack, all they’ll have to do is check where Joe’s phone is to know what store he’s buying at. Note that on Joe’s banking app or monthly statements he’s still going to want to see the bank confirming when & how much he spent, so he can verify receipts and make sure he’s not being defrauded by a scammer spoofing his card, too. How’s the Fed going to handle payment-fraud claims?

The only way for the Fed to make even a tiny dent in the flow of customer information is if they take over the basic banking function of providing everyone with a checking account, and cut the banks out of that whole business. Which may be the point?

Furthermore, even if transaction privacy were increased, the giant oligopolies will not simply stand still and have their profit margins eroded due the lost value of customer data. They’ll just raise prices on “digital dollar” transactions to compensate. “How you pay” always gets rolled into the price one way or another – gas stations and many others already charge a premium for credit transactions, and many other businesses offer tacit discounts for cash. Make the transaction less rewarding for the oligopolies and all you get is inflation in your cost.

Finally, I question the premise that people are simply “hoarding cash”. There should certainly be some of that, but it’s also entirely possible that there’s a surge in the black-market economy due to near-totalitarian anti-COVID policies. Businesses that have “officially” been shut down were serving real and often enduring popular demand. They can force hairdressers to shut down, but as Nancy Pelosi demonstrated for us all, they can’t stop people from finding ways to get their hair done if that’s what they really want to do. Some of those transactions will be legit via Venmo etc., but others may very well be doing everything off the payment network in order to avoid getting sent to jail for violating the COVID rules – and in order to collect unemployment and other benefits on the side. The more restrictions in place to prevent people from satisfying their needs & wants, the larger the off-the-record economy becomes.

Central banks, such as the Fed, don’t have a profit motive since they can create money at will. So they have no motivation to use the consumer data that they would obtain from their digital currency, and, the article says, are “better positioned, relative to private intermediaries, to commit to safeguarding data from outside vendors.”

Uh,..no. The Fed is a cabal of private banks headed by obscenely rich and powerful men. Carnivores at the top of the food chain,…

Tom moore,

Uh,… no, the Fed is a hybrid. The Federal Reserve Board of Governors is a US government agency. Powell and any other member of the Board of Governors are federal government employees appointed by the President and affirmed by the Senate. They have government salaries and healthcare and pension plans. But the 12 regional FRBs, such as the New York Fed or the San Francisco Fed or the St. Louis Fed, are owned by the biggest financial institutions in their districts. Most of these financial institutions are publicly traded.

He still got the ‘cabal’ and ‘rich and powerful men’ part right. Once the fed has people on their electronic cash, there is not very much to stop the government from easy confiscation like they did in Greece. Saying the government will do nothing with the data is laughable.

“Publicly” traded merely means that there are a lot of suckers that are minority owners of the stock of a financial institution. The real owners are the “control group” who often own a majority of the shares but often merely control a majority of the shares by getting proxies, e.g., from public/private pension funds, university endowments, and union pension funds.

Ever wonder how some pension administrators are so rich and union leaders get so wealthy despite modest salaries? Proxies are very valuable.

The “Federal” bankster Reserve cartel was masterfully designed and called the “Federal” Reserve or the “Fed” to conceal the fact that it can be controlled by a cabal of obscenely rich and powerful men through their control of the Federal Open Market Committee: bank presidents that get selected from the district banks (controlled and owned by local, private banks owned by banksters) and control of just enough of the presidentially-appointed directors to get majority votes for banksters’ wishes.

Pliable persons appointed to head the “Fed” can get rich. The banksters have taken care of their families and will take care of their families for years to create a bribery-culture in which those who do what the banksters want will have guaranteed futures and their children’s futures will also be guaranteed.

It is just like in China in which CCP members’ children are hired or made partners by persons who want to government to protect, lend to, and support their business. It is just more tacit and less express.

However, it is just as massively corrupt. 95% of Americans are thereby the victims of the banksters and their pliant, cooperative cronies, who are like acting like the monkey figurines: covering their eyes to see no evil; covering their ears to hear no evil, etc. Other organized criminal organizations are playing with pennies, comparatively.

It’s ALL part of The Great Reset authored by Karl Schwab, Bill Gates/Other Oligarchs:

Digitizing money is merely the first step in realizing The Great Reset.

A subject matter, it appears, has never been discussed here.

“But it would not protect the user from the Fed’s prying eyes.” ‘Nuff said? I favor plucking out a lot of peeping eyes above the level the rest of us live on. And a new presciption for the ones that are supposed to be watching the truly wicked.

The proposed “digital dollar” wouldnt provide any privacy from anyone, because, there would still be a list of transactions containing who bought what products or services, as well as, various other ways to identify people. Those companies could still sell that data to everyone, including governments and not just your own government.

If you care about privacy, the ONLY OPTION for most people is cash (and technically gift cards and disposable credit cards if bought with cash, with all money spent in store). Of course if you “research” anything you are going to buy or at any point ask questions about it online or it accesses the internet in any way, there might be a record about that. Protecting privacy right now is almost impossible in America, although you can certainly achieve no privacy whatsoever if you are lazy about it. I could go on and on, but, as it stands, no form of digital payment provides any privacy, don’t assume cash does without extensive precautions either.

Track 1, Side 2 of Thin Lizzy’s ‘Johnny the Fox’:

Jimmy the Weed for greed was taken aback

Johnny the Fox you old sly cat

Cleverly the Fox concealed his stash

Crisp dollar bills leave no tracks

Thomas’ warning is so true. Facial recognition cameras, which in times of mask wearing are not as accurate, may be at the cash register where one shops.

I wonder if anyone has done any work on spending digital currency. It’s documented that people spend more with a credit card than with cash. It’s rare that I purchase on line, but I do buy and sell financial assets on my smart phone. Very easy to move six figures around and if you are tired or giddy you can make an emotional mistake.

I know for restaurants, particularly, fast food ones, they have actually done studies how much people spend when using cash vs credit cards. The result, those using credit cards spend on average 30% more than cash spenders at fast food restaurants. Debit cards spenders are in between. Card spenders always spend more, but, the number varies alot.

I imagine digital cash would be roughly equivalent to debit card spending.

let me know how it goes when POWER IS SHUT OFF

Same with other digital payment systems. Or try to get into your bank account when the power is shut off. Try to turn the light on when the power is shut off. When the power goes off, there are a lot of very basic and fundamental things you can’t do anymore in modern life.

Thus it is always good to be at ground-floor level, simpler that way … the fall hurts less, with fewer scratches and cascading contusions.

In other words: Complexity is it’s own Hell!

What if there is a local power outage which affects the blockchain’s computers?

Yeah, no power, my electric dog polisher won’t run. Takes forever doing it by hand.

Inflation is poised to rise sharply and soon. Article makes a compelling case. Please research this.

That’s why it is always smart to keep a chunk of cash in a safe at home. Then if the lights really do go out, you are one very small step ahead of the vast majority of people in the short term.

Less is more, simple is good. People just can’t seem to learn this, which is why I believe we have a crisis of the spirit. As a result, I know something very unpleasant is heading our way; I believe folks who lead a simple life will simply weather this storm much better.

I worked in operational banking back when the Earth’s crust was still cooling. We had mechanical teller machines with an attachable hand crank that worked with no electricity. Our dailies were on the old green and white striped, tractor feed computer paper. We could still operate when the power was out. Then came the electronic teller machines and microfiche. Power goes out, lock the doors.

Well, as the software developers, who’re invovled in development of software for financial institutions, say – cash never crash ;-)

Even if cash is banned – officially – the Street (to use William Gibson’s term) always will find another way to trade. A way that won’t involve financial sharks.

Try paying for anything at the grocery store (or at any other business) even with cash if there’s no power to operate the register.

Power went off in S. Florida in 2004. Generators were brought in to get the cash registers working. Cash on hand was used since the credit card machines were not working. All electronic systems have many vulnerabilities and not just from power outages. Fraud, cybercrime, malfunctions, complexity, control, all go up.

But check kiting is a lost art.

Electricity is simple to generate. Gilligan did it with coconuts shells and saltwater from the lagoon -with the professor’s help.

That was only DC. You need Chinese gooseberries for AC.

Isn’t this how the Fed makes “money”?

Gilligan for FED chairman!

Monetizing data is a silly idea. There has never been “privacy” in the sense that the advocates claim. Companies have been collecting and buying and selling mailing lists ever since postal systems existed. Even if you get a few pennies for each collected item, this doesn’t help your privacy at all. It only fools you into complacency. And that’s the real purpose.

Fed wishes to reinvent its control on the real economy.

Currently the Fed’s dollars are usable mainly of the banks echanges, and banks transfer too little of it to the real economy for the profitability reasons.

Multiple studies have shown that you can’t have privacy in the internet. Even when companies such as Google claim that they’ve scrubbed the identifying information, the studies showed there’s ways to get back the original information.

When doom is approaching, there are two options:

1. Throw sarcasm at it, hoping that it will slow down. That’s my way.

2. Introduce another complexity to the system hoping somewhat that it will save the day. It won’t of course, but it might serve as a convenient scapegoat.

Additional new complexities invariably create opportunities for new sarcasm. Sometimes irony, even satire. MB your observations are always treasured.

Scott McNealy, co-founder and CEO of Sun Microsystems, said in 1999 – “You have zero privacy anyway…Get over it!”

So detail all the personal information of Mr Scott McNealy for us and show how personal information is not protected. I’ll bet you can find very little. Just as there are 2 justice systems, 2 economies, there are 2 security and privacy systems. Unfortunately we get the short end of the stick with no trust funds, foundations, holding companies, private security guards, private schools, or private French Laundry dinners.

But I do agree with black humor as a psychological defense. Soon we will all be Russian ;-)

Sounds suspiciously like Fed coins; only now, it’s even more stringent than our default fiat currencies.

And instead of the banks, the payment processors, Facebook, and Google tracking us, we can now all centralize it with the government. And let me guess, they’ll outlaw various cryptos like bitcoin, etherum, etc, along the way.

Let me just say, no thanks. I would prefer not to have the government with the ability to instantaneously cut off means to access my funds because they didn’t like something I did or said. If they want to do that to themselves, fine, but for me, I’ll just stick to the paper currency.

Please excuse my pessimism, but I don’t believe we have the choice to say “no thanks”.

Our local (population 1,100) lumberyard stopped accepting dollars and caused an uproar, but, next town over is 30 minutes away.

Unless a miracle occurs, I fear digital payment, chipped vaccines for tracking and finally, a communist regime is ahead. God have mercy on our freedom loving souls.

Why? They should be happy to accept Canadian dollars, nothing wrong with that.

And we always have a choice to relocate… Australia… or may be New Zealand. Land of Middle Earth and the uber rich?

New Zealand is going to be hell on Earth soon. Your window of opportunity has already closed.

Cash is a real pain in the butt to process every day. Count it, make deposits, maintain change funds, etc.

Credit cards sales are much simpler. No change, the CC machine gives you totals and makes an automatic deposit. It is well worth the 2% or so that it costs.

Unless cryptos can literally clean up their act outlawing them may become an environmental necessity:

I agree — Fedcoin coming and, with it, crypto currencies will become illegal because they compete and protect the users from inflation.

I am a retired CPA.

Besides side lining the Banking system, what about the authority of Congress, only who can legislate to pay ( to spend) the consumer directly, like stimulus?

Will Fed take over all those authorities?

Too good to be true!

The Fed will need approval from Congress. There will need to be legislation, and there are already efforts underway (since March).

Of course, Mega Banks are the primary dealers for FED in selling/buying treasuries/bonds(?) Will they just sit on the side?

Wolf you still short in all this mess?

I shorted at 360 and I was feeling good until I heard: Janet Yellen.

Every lunch is free in Janet’s universe, and it only goes up.

I’m not so sure Yellen will be good for stocks. I think Biden picked her because she is the least intimidating figure to convince the general public that tax hikes are good for us. The general public will not second guess her motivations, and everything she says will go down easy like one of Grandma’s peach pies, with a dollop of ice cream. To the layperson who knows nothing about finance (i.e., the average voter), she presents a trustworthy contrast to people like Lagarde, Powell, and Mnuchin.

What a disastrous pick. She’s the embodiment of the spoiled, entitled Boomer who wants to keep disastrous policies of QE and ZIRP so that her selfish generation doesn’t have to make any sacrifices.

“disastrous policies of QE and ZIRP so that her selfish generation doesn’t have to make any sacrifices” What would be different for the Boomers? I can point out one very bad effect from FED operations in the last dozen years, extremely low yields from safe investments like T-bills, CD’s, Moneymarkets, etc. It has forced the Boomers that saved for the future to either eat into savings or lower the lifestyle, or…gamble with riskier investments. Some Boomers have signed reverse mortgages to survive, big market these days for the marginal savers, I know one.

You probably see the stock market gains for your reasoning of the benefits, but many Seniors don’t want to be there with the risk. I have no worries as I mostly have my money in money made from elements or high purity alloys, I think the FED has benefitted me.

Yellen ended QE, the mere threat of which caused the Taper Tantrum, then she raised interest rates, and then she planned the QE unwind and started it in late 2017. Trump got rid of her in early 2018 probably for those reasons.

True, but in my view, she should have started normalizing in 2014 right when she took over. By then the economy wasn’t in the state it had been. Maybe I have unrealistic expectations for these people.

She raised rates once, .25, and then stopped because the stock market had a sad. We’ve been paying attention Wolf, we know who yellin is. Another crony who will do everything to help the top 10% and give “capitalism” to the bottom 90%

Mr. House,

“She raised rates once, .25, and then stopped because the stock market had a sad. We’ve been paying attention …”

BS. You have not been paying attention. She raised rates in Dec 2015, Dec 2016, and 3 times in 2017 = 5 times. Trump got rid of her in early Feb 2018 before the March 2018 rate hike became effective, though it was baked in and well communicated. By the time she left, the effective federal funds rate was 1.42% up from 0.12% in Nov 2015.

Replacing Yellen is a political solution to exculpate the previous administration, and preserve ACA. If you are correct then maybe Treasury will let the market set rates at auction. That would be a positive turn.

chasebank,

Yes. But last week was nice. Why didn’t you ask that question Friday night? These questions only crop up on days when the S&P 500 is up 0.6% or something ;-]

Today S&P is 1.62%!

S&P pe is now over 35%!

Hurrah for the DIP buyers and those who believed in simple narrative (unlike the rational analysis) that STOCKS always go up!?

More easy-peasy money on the way along with MMT, right?

The digital dollar or whatever you call it will end up having exactly and precisely the identical privacy as does the internet, phone, and mail systems. Which is precisely zero privacy from government = corporations.

This all presupposes a recovery is, “to the moon, Alice. To the moon”.

Oh well, we just beefed up our house cash envelop we keep for emergencies. I don’t mind using debit for in-store cash purchases, and a cc for online, but I have yet to see anyone turn up their nose at cash, especially when I say, “No receipt”.

These guys get too cute and a lot of the economy will burrow underground, especially in renovation and repairs. My best friend used to have a high end furniture store. He had an old fashioned cash register that made a lot of noise and spewed out a receipt….in addition to the more modern debit and cc machine. He said it was all in the bells and drawer lever. Ka ching ka chunk. The cash went into his pocket much of the time.

And that is why you should, can and ought to get a cash discount. Self employed man pays around 50% of profits in federal, state, local taxes and fees, with 15% social security, plus medicare and unemployment.

Ask for a 25% cash discount. He still makes 25% more than running a credit card, check, or Apple Pay payment through the greedy paws of the taxman.

“But your taxes pay for things you get.”

Just what are we getting for our taxes these days?

National healthcare? Nope.

Winning wars overseas? Nope.

A national passenger railroad system? Nope.

Government issued PPE? Nope.

A functioning and effective pandemic response? Nope.

A functioning FAA, preventing aircraft crashes? Well yeah, but who certified the 737 Max?

Yes, national parks are nice but there are entrance and parking fees now. Clean water? Talk to Flint.

“These guys get too cute and a lot of the economy will burrow underground,”

…yep…exactly.

oh and BTW – Yellen is going to be appointed to merge the Fed Res and Treasury into a single entity.

1) Fred : US gov debt = $26.5T.

2) For 16 years SPX was rising from 1982 low to Apr 1998 Buying

Climax high, slightly > 1000. // Oct 1998 low was the quick response, slightly 11 years.

5) From Mar 2009 low to 2020 high another 11 years. The total is 22 years.

6) A 100 years old Japanese theory predict that the next low will be

either in the next 11 years (2032), or 22 years.

7) What Zanet can do if in the next 11 years US GDP will shrink in stepping stones at about minus (1%/y – 2%/y) ?

8) USD osc around 100, backing up, since Mar 2015, for 6 years.

9) SPX will correct, – “something” slanting block it’s advance, forcing SPX to turn around since Jan 2018 – USD will popup in the next decade.

10) US10Y will flip to ==> NR.

11) The global smart money will flow into Zanet invisible hands, seeking refuge in the vaults of US Treasury, but space is limited and it will cost more money : TY will rise !!

Wolf, thanks for the interesting article.

“…the digital dollar would in theory eat into some of the core functions of the banking system”. Kind of an understatement I would say. Demand deposits are the cheapest (lowest interest cost) form of bank liabilities used to fund loans so loan funding would dry up, and interest costs to borrowers would increase for the remaining loans. It would decimate the banking industry and the economy. Time to go back to the drawing board.

Maybe this explains why the crypto currency XRP has doubled in the last few days. The “bankster coin.”

Yellen confirmed as Treasury Secretary. The only thing left is to merge the Fed and the Treasury.

Hyperinflation is now 100% guaranteed.

Yippeeee!!!!

How many times do I still have to repeat this? (time to write an article about it):

Yellen ended QE, the mere threat of which caused the Taper Tantrum, then she raised interest rates, and then she planned the QE unwind and started it in late 2017. Trump got rid of her in early 2018 probably for those reasons.

You mean that it would be possible to start shorting now? Or May be on the day she is confirmed.

I don’t care if it’s a dumbo in office or a jackass, as long as they help my account in some way, they are my friend.

Wolf,

I’ll guess we’ll see Wolf.

The whole “DC Consensus” of the last 20 years (“Screw Savers to Save Our Ass”) suggests the opposite and the whole Fed to Treasury dipsy-doodle does reek of nothing so much as continuing/deeper monetarization of astronomical debt-to-“GDP” levels.

We’ll see.

Forgive me for not seeing events as you see it. Yellen became Fed Chairwoman in 2014. She could have started the process earlier. Before that she was also quite happy parroting Bernanke’s flawed thinking.

+1

Quoting from Jim Bianco in a Bloomberg Interview:

“Risk markets are celebrating Yellen as Treasury Secretary in a way that suggests she is heading both the Fed and Treasury. They are celebrating ‘easy money’ Treasury Secretary but technically the Treasury Secretary doers not set monetary policy and is not supposed to influence it.”

Hyperinflation 200% guaranteed.

Dow 100K

S&P 10K

Nasdaq 50K

Bitcoin 100K

Great stuff.

Wolf, are you indicating you think she is a good pick? A return, however slight, to sound money? A portion of the Dems seem to believe in the MMT magic tree, and the rest seem to be trying to grow a veneer of socialism (although they are the same corporatist sharks as the rest underneath) which means spending. Here in the UK Johnson seems to be as incontinent with the cash as Labour. Nobody seems to care about deficits and debt like they are trying hard to blow the whole thing up. I can’t see how a tighter fiscal reign is around the corner, Yellen or not, I wish it was.

Ian,

She won’t do monetary policy. Now she will execute more or less what Congress tells her to do and spend the money Congress tells her to spend and fund this spending by collecting taxes the way Congress tells her to collect taxes, and by borrowing the rest, as Congress expects her to. That’s a very different job. And she will lobby Congress to get some things done. I’m neutral on her in this job. At least she doesn’t have all this filth in her history the way Mnuchin has.

I am with Ian on this one, sorry. Yellen’s supporting the repeal of the Glass Steagall Act caused the gigantic bailout of the banks in 2008 and will cause the upcoming, third bailout in 2021, since they already got a second bailout from the “Fed” purchasing $ 2 TRILLION in MBS. She then argued to prevent the re-enactment of the Glass Steagall Act– after she was one of the ones that caused the crash!

The US congress will probably not be able to act together and just argue, as always. A treasury secretary has power in being able to funnel federal funds, contracts, etc., to cronies and claim that the world will end if the banksters do not get more bailouts. That happened in 2008. Remember the 2008 stock market crash that led to the $700 BILLION TARP bailouts urged by the then treasury secretary, who “coincidentally” came from a big financial institution?

What a load of Fedbullshit. People can demand that corporations pay them for their data now, or they will use cash. How’s that working out?

What’s to keep the IRS and law enforcement from getting access to this fedata?

I like cash. It’s anonymous, portable, doesn’t need a reader, computer, electricity, can be used by anyone, handed off to others, isn’t taxed, therefore earning me a discount from service providers, can’t be turned off; “four former Air Force drone operators-turned-whistleblowers have had their credit cards and bank accounts frozen”, cannot be charged negative interest like money in a bank or some kind of fedcredits etc.

Yeah, try buying anything online with cash. The digital dollar would not be a replacement for cash anyway, but a replacement for digital payments that are currently used. That was one of the key points in the article. Seems you totally missed that.

“but a replacement for digital payments that are currently used.”

They could call it something friendly and reassuring.

Like, “FedPal”

Or,

“Big Brother Bucks”

(I’m getting those images of Saddam pawing that kid in ’91…)

Yes, I missed that focus of the article.

Still think that it’s a slippery slope to elimination of cash with the attendant controls and other negatives.

Buying online? What makes you think I have a computer?

“What makes you think I have a computer?”

?❤

I lost my bitcoin wallet key.

I don’t understand block chain technology. We already have a digital dollar but not yet a crypto type dollar. To me any crypto dollar created will require a shared key.

How does a digital currency stop the power of a cookie?

The world runs on credit not dollars. Merchants don’t care if I pay with credit/debit rubles are renminbi. I am a demographic that bought x product, what difference does it make how I paid for said product?

Whatever I buy needs to be delivered somewhere. Pretty sure companies can figure out who we all are from a delivery address.

There is no reason to base the digital dollar on a blockchain platform.

Actually, the blockchain can track a digital dollar through the economy. This will allow them to see the journey of any particular dollar. It’s a bit much, but it’s more data for the surveillance state to drown in.

Blockchain is very cumbersome if you have billions of transactions per day, day after day. Small scale is fine, but for a global currency like the dollar? The Bundesbank did an experiment with it and found that there was no benefit to blockchain: it worked, it was cumbersome, and it was unnecessary.

Yes, well, blockchain tracking and locking would tend to screw with that whole “dilution friendly” nature of the USD…

Nothing is getting more diluted than cryptos. They went from 1 (bitcoin) to over 3,000 now. And each one of them is constantly getting diluted through more “mining,” every single day. Blockchain hasn’t stopped any of it. That’s not what blockchain does. It’s just a record-keeping technique.

Isn’t true that there is a limit to Bitcoin? 21,billion IIRC.

I’m happy that it’s going up. I’m a hodl.

Wolf,

The structure of Bitcoin (and other similarly designed electronic currencies) is that the ultimate number of “coins” is fixed.

Before that point, it becomes progressively harder and harder for “miners” to mine new coins, by design.

This is in contrast to the USD, which (as QE made self evident, if not necessarily legal) the USD has few, if any, dilutional protections.

I’m not championing Bitcoin or any specific electronic currency, but conceptually and so far in practice, they have more built in protections against printing/dilution than the USD.

That is the core of their appeal for non pure speculators.

DC has done this to themselves and to us.

Before reading comments I thought: someone will think this is a version of Bitcoin.

Whatever BC is, we know one thing: it isn’t a currency.

Root word of currency: ‘current’ as in currently acceptable in transactions. The Ruble is currency in Russia but not here.

There is all kinds of speculation in BC, and virtually no payments for stuff.

A few years back, Craigs List etc., trying to be edgy, would ask if crypto was ok as payment. Long gone.

Why? Who, making a substantial payment, does not want a third- party record of such? Otherwise, it’s ‘But I sent you the BC man!’… ‘Never got here dude, so I sold the car to a guy with cash’

One guy made a few bucks on using BC on Silk Road, the market for illegal stuff. The vast majority of transactions that aren’t hand- to- hand cash are legal, and this is the target ‘market’ of the Fed’s ideas.

I am not an expert. However, I understand that a full-fledged quantum computer will be able to crack the computer security schemes, such as the security schemes that protect bitcoin and other coins.

If so, those “investments” will be valuable but readily stolen. I would particularly doubt that they would be safe with anything associated in even the slightest way with the “Federal” Reserve — i.e., the one entity that has been funnelling $2 Trillion dollars to save its banksters since 2019 was setting them up.

Have we not had digital currency for many years? Since we have many more dollars in existence than we have currency in circulation, we have a great abundance of digital dollars, and have had for many decades.

cb, you make a good point, I guess they used to call them ledger dollars or some such jargon before the digital age, or maybe no one ever questioned the scheme until it was unraveled by you.

Fractional Currency Creation

“we have a great abundance of digital dollars”

____________________________

a cookie for anyone that knows how many ………….

Once the Yellen Treasury and the Brainard Fed Chair team together, I suspect a Central Bank Digital Currency (CBDC) will be implemented quicker than most think possible. The privacy concerns are easy to avoid as there will always be an alternative form of barter, if not simply the items you barter themselves as the only transfer of payments. What could make the CBDC a human three ring circus is if they use special types of digital currency that are time dated to expire, or even product specific . In theory the Fed could give citizens digital currency that would only buy say an American made SUV, for a limited amount of time. Or if housing needs a kick start, $30,000 for any house purchased in the month of December. How about $10,000 to be spent at Home Depot or Lowes to energy proof your home in the next three weeks? Such policy has already been enacted by various tax and rebate schemes for autos, houses, and energy proofing homes. What makes a CBDC different is it is so simple to enact that only the Fed would be required, and they could do consumption promos 365 days a year, using constant feedback data from the CBDC past purchases to tweak future purchases to optimize future GDP. And how does one Opt-out, other than move to another country? Consumerism would become the religion of all religions in America with constant “CBDC coupons”. The government would control what you buy, when you buy, how you buy, who you buy for, etc. Citizens would have to play along else they would get behind financially if their friends and neighbors got all the “free stuff”. People would be lab rats, and the FOMO would be similar to what we see currently with the stock markets. And as long as the govt enacted such policy over enough time, most would not figure out what is happening. Sure we now have boss day, fathers day, mothers day, daughter day, son day, grandpa day, grandma day, etc and that took decades to “evolve” into constant “Hallmark Moments”. It happens over many years and the next thing you know there is a reason to spend money for “mandatory” descretionary stuff every day of your life, as some “special event” requires your monetary attention 365 days a year. At what point is that not a human zoo? Consumers think they are on the outside of the zoo bars, and that is the genius of the corporate states of America materialism complex. If we only bought what we “needed”, capitalism would fail for the super rich. So here comes the Fed and Treasury to save us little plebs via UBI, MMT, and CBDC??? Do you trust “I am with the government and I am here to help”? Or is it more like “All your base are belong to us”…HA

Well said, Yort.

Yort, first off, allow me to wish you a Happy Unbirthday! (Odds are 365:1)

CBDC is the perfect solution. No Bureau of Engraving. Save trees. The citizens will not need suitcases or wheelbarrows. Instead of being paid twice a day they can be paid by the millisecond. It will bring a new meaning for the word exponential.

You’re describing corporate-ization. The Fed bought the entire economy in 2020, and we found out how small the real economy is compared to the financial economy. GOP thinks there is too much (main street) aid, and there is, but junkie needs another fix. China has products to sell. US has Tbonds to sell, (who will buy them, doesn’t matter just type in a name). The Wall St vision is to make every poor kid in India who lives on $100 a year a full fledged consumer. This is where the Fed wants the money to go. Meanwhile the only way that kid gets anything is to work in a factory while Wall St steals the profits. The field levels and his wages and your wages start to converge. Enter big orange man says $100 a year kid is stealing from you. Wall St falls over laughing. Fed pumps up money base, you live without working, he works without living.

It never made any sense to me that private banks or other investors could create or buy loans backed by a gov’t gaurantee. They have every incentive to push the debt as far as it could possibly go. That creates false demand surges that artificially push prices up (college) (housing) getting high interest payouts that don’t match the low risk. The gov’t would be better off loaning to consumers directly for those items since there would be no incentive for gov’t to inflate the costs with loan surges since it wouldn’t increase the value of the loan portfolio to lend to high risk borrowers. Not allowing exceptions to bankruptcy and not offering taxpayer backstops to private lending activity acts to create price stability by preventing private investment behemoths from moving markets in their favor by preventing them from risk free manipulation of supply/demand. Price levels would then reflect debt that can actually be serviced through wealth creation in the real economy, not rabid gov’t subsidized financialization.

“creates false demand surges”

For a Keynesian, there is no such thing as a “false/wasteful demand surge” if there is unemployment.

If the G is paying people to dig, and then fill in holes, (or receive, then fill in, absentee ballots…) then the economy is being run along the optimum trend line.

Any equilibrium below this theoretical construct is a Keynesian sin.

As if those things were/are the real goals….

The digital dollar offers no privacy to users at all. The “know your client” rules apply to all banks, and in the case of the fed, the fed can guarantee your payer identity using govt databases(irs, ss, va).

As for the data corporate america collects, it will be exactly the same, except they will have more protection/confirmation as to the payer’s identity. The payment info links to the customer account where the customer activity resides, no difference at all. The sellers only care about selling and getting paid. The digital dollar will assist in that with the added protection that the fed is guaranteeing the customer’s identity.

Customers will have zero privacy to go along with zero control over their money.

+1.

Privacy? See FinCEN and Form 8300 and SARS report, and not least the Federal Financial Institutions Examination Council. Do we have half the employed working for government yet?

I doubt if congress would pass it. I’m guessing too many hands in the black market and offshore cookie jars. I would guess most arms sales are on the up and up, but what about the drug trade? How many billions is that? Is there any chance politicians don’t have their hands in that? Rumors are some of the very wealthiest families in the US got their starts in that in the 1920’s.

How would llcs in the Cayman islands and Macau intersect with it if all data goes through the government??

There is no digital dollar privacy unless the seller is willing to accept it. Look at all the ‘term of service’, EULA’s, and so forth. Even now, it’s common practice for sellers to slant digital purchases towards their advantage.

Roku is a good example of this sort of thing. After paying for a Roku device, one must accept 17+ pages of legal contracts which, among other things, requires that the owner provide accurate PPI such as name, address, phone, email, payment information… or Roku has the right to disable the device (which the owner bought.)

Sound far fetched? It’s on the Roku website – if you look hard enough.

Never heard that.Heard of roku long time ago.So glad I gave them 0$!

I’m trying to understand the rational behind it (beyond the stated one). My understanding is that banks get a very high percentage of their income/profits from debit card transactions, so wouldn’t this idea hurt banks a lot?

The digital dollar system is more efficient in the sense that it eliminates all middlemen and creates a more realtime system for funds transfers.

For example, a large employer could pay all their employees by depositing wages in accounts at the fed, instead of at hundreds of different banks every pay period. Some of those paychecks now go to small banks, which in turn get them from their larger correspondent fed member bank. Digital dollars can go directly from employer fed account to employee fed accounts.

Hi Petunia, glad you’re back!

Digital dollars go directly out too. Sent an estimated tax payment for $1500 to the IRS (amount clearly written in text on the second line). IRS OCR mis-recognized my “1” as a “7” and electronically presented the check to my bank for $7500 – twice, no one looked at it after it bounced the first time. I have a separate account I use for checks and only fund it with a tiny bit above the check amount. They would have taken the $7500 and I can only imagine how long it would have taken to get the $6000 back.

Oh, and then the IRS levied a $150 penalty for refused payment. I’m still working that one out.

Switch to ACH direct debit/credit. Handwriting and handwriting-recognition systems will no longer interfere :-]

i’m glad you’re back, too. i was afraid you went and died and i had a moment of panic because we haven’t even begun yet.

x

Micheal,

Thank You for all You (and others…especially Senor Wolf for these forums) provide with integrity, intelligence to convey extensive & intricate financial knowledge that (even) I can assimilate & comprehend.

All The Best to You and Your Loved Ones this holiday season.

ie Comment targeted to Micheal Engel, and thankful to all contributors.

Wait a minute. Are you saying that you can actually understand what the dot point cryptologist is saying? That is no small feat! Could you give us an occasional decrypted translation? That would be great! Many thanks!

ME is actually the Central Bank Skynet trying to warn us from the future.

That is the why behind the line numbers and oracular statements.

He also says, sell any stock with a PE above 40…

Couple it to your social credit score, and now we’re talking.

Yort,great insight!Many people would just get the deeplydiscounted whatever and actually trade or sell it via another venue just like the looters have been doing!Get the goods and sell it or trade in a myriad of ways!”I’ve got a guy.” Comes to mind along with the image of Chicago streetguys hawking everything out of their car or their coats.Take your pick of the various hyperlocal online sales sites,craigslist,varagesale,whatever!

“a privacy-preserving digital payment method may improve consumer welfare,”

Unless you’re going to get a nameless digital dollar card you can use as a credit card at physical stores I don’t see how DDs are going to improve privacy. Online, well you still need to have your purchases mailed somewhere – the store will know who you are.

Since I don’t believe the Fed gives a rat’s a** about consumers, much less their privacy I assume this is just one more way to print more money with less accountability. Don’t these people have something better to do with their time?

“just one more way to print more money with less accountability”

Ding Ding Ding!

Give that man, ahem, well,…a dollar…hmm.

And no one, other than for marketing, gives a rat’s ass about the personal lives or information of 99.9 % of the population. The level current level of paranoia, if it wasn’t currently in vogue would seriously alarm a psychiatrist. After hearing from the client that govt computers were being used to gather his personal information. the pro might ask as gently as possible if the client ever heard voices telling him this.

I know someone, with a degree, 500 K house paid for. juicy govt pension. who only pays cash for his booze because he thinks a record of such purchases could damage his credit rating! In short, a nut, but in most other areas very sane.

Because I make inquires about boats, having owned a few cheapies, I will get pop-ups telling me about the new 50 footer or yesterday, a marina for luxury yachts a million and up. So ya some dumb as f54k AI algo ‘decided’ to feed me this. So what?

My brother now retired from the Coast Guard, was entering the final stages of the recruiting process 40 years ago. It was time for the crunch. The board asked: why have you been in communication with the Soviet Embassy?

He had no idea what they were talking about. As it turned out, as part of a Social Studies project, in Grade 9 or 10, he had written to it, asked for info on Stalin and got back the standard brief blurb.

So this was dealt with and dismissed with a few chuckles.

A few people have expressed horror at this true tale: Big Brother is watching etc. Actually it is an example of an appropriate interest: the .1 % that govt is supposed to be doing, even in Canada.

The US has always thought, correctly, that Canada is the ‘soft underbelly’ for alien penetration of the US. An extra juicy example was the case of the

‘soccer mom’ and hubby, the perfect US Barbie and Ken suburbanites. After a decade in the US, they turned out to be long- term Russian moles, illegals, whose entire ‘legend’ about early life in Canada was faked.

The couple, with no immunity, were swapped. Decorated, the Mom especially is a celeb in Russia. Their kids, biologically theirs but basically props in the 20 year project, knew nothing. After long appeal, their Canadian citizenship has been restored.

But you have to wonder what Hal will say if they try to enter the US!

You could have your ton of manure delivered care of 20th Street and Constitution Avenue, N.W., in Washington, D.C

So, what is a digital dollar?

Trillions of dollar denominated transactions are conducted daily and yet none of those transactions are conducted using “digital dollars”?

Is a “digital dollar” intended to represent a cash transaction?

Example.

I have a $20 bill in my pocket, I walk into a 7-11 and spend it on a case of beer. Next time, I have a $20 digital dollar, I walk into a 7-11 and spend it on a case of beer. In both scenarios, there is no 3rd party involved in the transaction, unlike if I had paid using a debit/credit card etc?

George W,

Think of a digital dollar as a paper dollar. Each has a form of a serial number and can be tracked throughout the economy with that serial number. With a paper dollar, you would need a serial-number reader every step along the way. With the digital dollar, it’s automatic. Each digital dollar exists as an electronic unit with a sort of a serial number, and as it changes hands, it gets tracked. It’s closer to cash in that sense, rather than a payment with a credit card.

The digital dollar would protect the consumer from the prying eyes of Corporate America.

The information would be safe with the Government. Until the Government profits, by selling the consumer’s information to Corporate America.

Seems to me that the Government just wants their cut.

California DMV makes a pretty little profit selling Californian’s personal info to businesses. If I remember correctly, the CA DMV makes 50 million per year doing this.

Have you forgotten the hacking of Office of Personal Management (OPM) containing the huge data on ALL Federal Employees, in or prior to 2008(?)

I worked for VA hosp around 2006-2008 as a Temp. After that hacking I have been provided with LIFE-LONG protection monitoring on my credit and personal identity!

NO ONE is hack-proof!

The digital dollar is not the same as a paper dollar and the transactions you describe will not be the same. With paper money you can buy your beer and be on your way with no third party deciding that you have drunk enough beer this month.

The digital dollar will eventually be tracked and a third, fourth, and n th party will be deciding what you should be doing with your money. If you were overweight at your last mandated doctor visit, it will be no beer for you, or no meat, or no snacks. If you have a dispute over a payment, who resolves it, it better not be with a big political donor.

Am I the only one that feels like we’re approaching the end game here where the wheels come completely off the bus?

They are lining up to print trillions, start issuing fed coins straight to the serfs. Meanwhile, the middle class is being eviscerated by lockdowns despite explicit guidance from the UN and WHO that lockdowns are counterproductive. Suppose if you get fed coins invest them in disconnecting yourself to escape serfdom?

Supposedly these new digital coins will be at least partly based on Ripple (XRP) and Algorand (ALGO) and I guess this will be linked to the new roll out of the LIBOR replacement SOFR by the ISDA in January of 2021 (perhaps linked to the Reset that shall not be named). Not sure how true any of that is, but it does seem to be at least rooted in fact.

Nope, you are not the only one. About five years ago I started seeing projections that the budget numbers were going to look really ugly by 2030 and wondered what would the playbook be. Then covid hit and made a bad situation worse.

I definitely played the last five years wrong as the play was to leverage up and take risk even when risk assets were pricey. I am not sure what to do now, but until I figure it out I will just stay mostly risk off and just consume less. As Buffet says “Never risk what you need for what you don’t need”.

Subscribe to Martin Armstrong’s blog. Your intuition is correct.

This is no longer a problem. The bus now has no wheels as it is now a hoverbus and can slide around randomly in any direction.

How it relates to the control of money creation and commercial banks this is the key question. Everything else about privacy etc are secondary. What they are talking in effect is to take the power from the commercial banks to create money and give it to themselves. As Wolf writes “pulling the rug” from the commercial bank’s feet literally. They are already eating their lunch in the bond and credit markets under the pretense of “inducing inflation” and providing liquidity through asset purchases. The whole argument the Fed makes is nonsense. Digital dollars have decades in circulation most of money supply is digital already, one bank digitally credits an account, physical cash in circulation has never been more than 5% of the total money supply. So we already have digital money around the world not just in the US. What the Fed is saying is that they want to be the ones crediting accounts not commercial banks. They will give you some app to make it seem innovative and ingenious but it’s the same thing basically. It’s a very dangerous development if true.

Yes, for banks. Banks have always been a necessary evil,but maybe digital disruption has claimed them too. Maybe they have become an UNnecessary evil.

Sir P,

Outstanding, I think you hit the nail squarely on the head.

Just think of the FRB as the Highlander. “In the end there can be only One.”

WTH happens to BitCoin if a digital dollar is implemented ??

These cryptocurrencies – there are now over 3,000 of them, bitcoin being one of them – exist in their own universe. They don’t have a function in the real economy. They’re just an empty medium for speculation. So whatever is going to happen to them is going to happen to them, whether or not there is a digital dollar.

As long as the medium exists and can be converted to fiat currency, there is a place for it. I think the biggest attraction for bitcoin is that there is a limited supply, and its value will not diminish over time. Although transacting in bitcoin is painful.

Will they crash and burn? Not as long as the current store of real value is not easy to move around. Of course, the biggest problem with cryptos are the fact that it needs electricity.

The limitation of the amount of BC is a bogus argument.

You can divide them indefinitely. In theory you could do that with a gram of gold also. But you will come to a point it can’t be handled physically/ Solution to that is to dilute/mix it with base metals (1 micro gram in a dime for instance). And history has shown us what happens eventually. Bitcoin will go the same path.

“I think the biggest attraction for bitcoin is that there is a limited supply, and its value will not diminish over time.”

That is the core appeal of *all* the limited supply alt-currencies.

It is absolutely no accident that they are arising at the precise moment in history when decades of Federal fiscal incompetence has forced DC into the money printing business.

20 yrs of ZIRP has taught savers exactly what to expect from DC.

Mount Gox

WOLF & MCH

Thanks for your take on BitCoin and Crypto in general.

I (and others I believe) remain interested in a prospective article discussing the viability (or non-viability), or perhaps the correct term is “probability” that BitCoin / Crypto can become a bonafide currency, whether in the US or elsewhere.

With PayPal, Venmo and many merchants already taking the leap, it makes the discussion quite intriguing.

The intro of PayPal provides the missing link in the blockchain, a third- party record of payment to protect the payer. But the whole reason for BC is supposed to be it’s not traceable, thus it’s use in criminal site Silk Road, probably the closest BC ever came to actual use as a way of transacting.

RE: the limited edition of BC and hence its ‘value’.

The same applies to art. Whatever you or I might think of Pollock’s splashes of paint, there are no more, and so they are valuable if people decide they are.

Perhaps BC is not so much an improvement on a currency as it is on the chain letter. The chain letter eventually collapses because the numbers swell geometrically. But what if they were numbered, and were a limited edition?

Civilization is digitization. Language is digitized thought. Writing is digitized language. Printing is digitized writing. History is digitized events. Musical notes are digitized music. Recorded music is digitized performance. Science is digitized knowledge. Telegrams are digital correspondence. The internet is digitized correspondence, news, television, libraries, adveretizing etc. Social media are digitized relationships. And so on and so forth. Every step introduces a level of abstraction and carries within it the power and potential of an exponential leap in what can be tansmitted at what speeds to what distances as well as over the ages with minimal loss. The flip side of this is that what is digitized becomes data viz. subject to processing, storage, analysis, manipulation, impersonation,.. recording and transmission against the will of those originating the signal etc. Every technlogy is double edged. Every gain in possibilities comes at a cost of new threats through new levels of exposure. There is no stopping this process. Everything that can be digitized will eventually be digitized. Our responsibility is to not abuse it, to not use it against each other. We all know how that’s going to unfold.

I should add that money is digitized wealth. And while it allows transmission of wealth through space and time etc. it already comes with said threats.

And toes are digits too.

That’s the etymology as presciently noted.

Nature does it best. DNA is digitized life. To cheating death and transmit life it must be digitized. The part of you that is not digitized will die with you. The part that is, may have a new life.

Goldlarche, I appreciate your very interesting comments and I if I may, sincerely ask you to comment on ATP or more generally energy. Thank you.

Digital currencies are inevitable. China is now doing trial runs with the Renminbi, perhaps the most underreported story of the last decade (due to what it will mean for the dollar’s international decline).

However, there is a plus side to digital currency in the US: the roughly half trillion in underpaid taxes per year (mostly from small businesses) would be theoretically easier to capture.

Fully agree with this. The Chinese story is under-reported and could prove to be a massive game-changer a few years down the line.

For China this is much more than a monetary experiment. It’s a geopolitical strategic thing, as they are hostage to dollar funding and a payment system (SWIFT) that is actively being abused against them or their allies to impose sanctions (ask Iran, North Korea etc).

I think the implications for the US$ can be enormous when this takes off, though it can take quite some time before it gets big.

Good point. Who takes the risk when I want to move some of my rubles into my FRB account?

Up until covid-19, credit expansion in China dwarfed that in the US. In fact it is the most rapid in history.

As I commented years ago on WS, (and was echoed on CBC) China’s discovery of credit and unlimited currency creation resembles the Sorcerer’s Apprentice in the Mickey Mouse cartoon. He dives into magic without knowing what he’s doing.

The Big Story in China in the last month are huge SOE’s defaulting on their bonds. SOE banks attempting to collect from SOE steel and aluminum plants have been called on the carpet by the CCP and told they are obstructing the Party.

The big question in China: will the govt default on its own debt?

The fundamental challenge for China: it has moved on from Maoism. Can it move on from the CCP?

It highly doubtful that the Chinese govt will ever have to default on its debt. It owns nearly everything re: state own enterprises and these enterprises are profitable for the most part. China’s balance sheet is solvent (when compared to the U.S.), and it has relatively low levels of future (unfunded) liabilities.

Incidentally, American corporate debt sits at ~$3 TRILLION BBB /$1 Trillion high yield/speculative. U.S. Govt debt is at ~ $25 Trillion and long growing out of control.

That’s OK. I complained about the choices available in this last election and was told I was obstructing the Party.

And you’re still at large to tell us!

Doesn’t work that way everywhere.

‘China’s economic growth in recent years has been hobbled by the many long-term money-losing firms, often state-owned, dubbed as “zombie companies” because they are effectively insolvent but kept alive only by continuous bank loans and government subsidies. From 2008 to 2018, China’s nonfinancial corporate debt grew more than fourfold, from $4.56 trillion to nearly $20 trillion, according to the Bank for International Settlements.’

From PIIE via Reuters

There can be differences of opinion as to who is deeper in debt, but the idea that China is running a clean, lean, relatively debt- free economy is utterly bizarre and cannot be found in any published source, even a CCP source.

China does have one big advantage: prosperity is so recent and so little shared by those designated ‘rural’ that it could tighten its belt easier than the spoiled younger US generation. You do not have to be very old in China to remember facing starvation. (It was older Chinese who cleaned out the rice in supermarkets in Canada in the early covid panic.) If you have nearly starved, it is not seen as hardship to not order food delivered 2 or 3 times a week.

The NSA collects digital data on us 24/7 so I don’t see a how it would be any different under a monetized digital system. There really is, or should be, no expectation of privacy under such circumstances.

Comments re the article makes me think a whole lot of people don’t understand the basics and differences of ACH, AFT and Credit Card transactions.

Is there an estimate of the savings to consumers and merchants by not paying the credit card company tax?

Well Renminbibibi is taken and Edsel won’t work, so I suggest they call it the Push Ups. That way future President Douglas C. Neidermeyer can greet us every morning with “You’re all weak and worthless. Now drop and give me fifty! And tuck in those pajamas!!” All demerits will be automatically deducted so prepare to tow the line. Of course until they finally can use it to kill the evil paper, sporting good stores will do well on baseball bat sales with the rise of offline banking. Somewhere near the end the precious metals dealers will get their take. Do I smell an amazing recovery in the morning, or is that napalm?

The NY FED states that cash will still be used. But what if they abolish cash overnight, like they did in India with certain notes? They would get rid of a 2 trillion liability in one stroke. That’s tempting, not?

What this is really about, is that central banks have painted themselves into a corner with ZIRP/NIRP and are looking for a way out. So they are now preparing the way for debt-free money that can be credited directly to the accounts of whoever they want to ‘stimulate’.

Of course to sell this to the public, they will have to make the case that it is in the interest of the public, so they come up with all kinds of strange sales pitches for it. This is another one of those. Once they have introduced the CB currency, they have crossed that Rubicon and can expand the reach further and further. As I wrote here before, I expect to eventually end up with a full reserve system based on Central Bank Digital Currency. Full reserve, because then the central bank will be the sole creator of currency which will give them the greatest power.

Think of the possibilities: much easier for G deficit spending, because the CB can directly monetise some or all of it. Targeted stimulus possible. 100% traceable, killing much of the black market. They can even introduce personal interest rates (positive for boomers, negative for millennials, etc) because every dollar you own is traceable to your name. And as the currency is not a commercial bank liability anymore, no need to backstop banks in times of crisis.

It will really eat into the profits of traditional banks, so they will resist it. However, their power is already diminishing as they get eaten by fintech, who will end up being the ‘guardians’ of your Fed account and they will become the interface with the customer. The Fed is not going to make their own ‘app’.

The more dystopian it gets, the more the need to prevent flight to alternative currencies. Cryptos like BTC are still a fringe thing, but if it ever becomes a viable alternative to their monopoly they can kill it any time they want. Just require any entity that accepts BTC as payment or converts it to dollars to provide detailed information about the source of the funds and tax owed (any crypto transaction is already a taxable event today) that is so bothersome than it’s not worth it for them, effectively killing much of the convertibility to the real world.

Sung to the tune “A Spoonful of Sugar” as Mary explains to the children.

Exactly.

However, I don’t think commercial banks will resist as with ZIRP they can’t make money their traditional way, by lending. There will be a different arrangement allowing the main players to stay fed.

Wolf,

Thank you for the heads up, interesting. Seems like they want to get around the banks and their hoarding of dollars. I would think consumer credit would have a say in this for the fed to do this. Seems like the fed is trying to figure out a way to help the middle class. Here comes the inflation, right?

I can not remember spending a $20 bill in months. I switched to a 2% cash back plastic card. I put recurring monthly payments on auto payment linked to my checking account. Not writing many checks. Wrote a check to pay my property tax. They charge a fee for using plastic. The roads, bridges, schools, police, fire department and court system are not free. Who could have thought paying more for better school systems is a good idea?

“Who could have thought paying more for better school systems is a good idea?”

we have been paying more for increasingly crapified education at pretty much every level for quite some time. it’s almost like saying we should pay more for a better healthcare system.

Wolf, thanks for deleting my earlier comment in whole… at least now, I know which side of the coin you fall on.

Everyone knows the day of reckoning is near with so much of :-

– Fake economy

– Fake stock market pricing

– Fake unemployment stats

– Fake GDP numbers

– Fake Science

– Fake news

– Fake votes

– Zombie companies with fake accounts

– even Fake Gold (see recently NASDAQ de-listed Kingold)

– Fake (printed) money – all of debt-based fiat currencies issued by CBs.

– USD reserve currency faking it with no gold anchor since 1971

And the FED is telling us this new digital dollars will be their “new deal” GRAND solution to wipe clean all that has been faked? lol.

kevin,

You asked me to delete it if I couldn’t let it stand as is. It contained a YouTube link, which I almost never allow, and you knew that, and you gave me a choice, and I chose. Normally I would have just taken out the link.

Yes and I thanked you for it. I’m just saying I’m aware that all of us will inevitably fall along a spectrum of needs… and loyalties.

To be fair, that includes myself too – We are all either eager, willing, quietly acquiescing of forced participants in this charade of a FAKE system anyways. Cheers.

Wolf, what about the aspect of the Fed selling the data directly to Corporate America, thus creating a revenue stream for themselves? Now the Feds, Corporate America, and U.S. Government would all have access to the same data, one for selling goods and services, the other for policing, and the Feds for exchange with other central banks across the globe (i.e., complete consumer transparency across countries if other central banks create their own digital currencies).

Erik,

The Fed creates its own money and doesn’t need to create additional revenue streams. That takes the profit motive out of the equation. And that part I can see. But I could still give companies or banks access to this info, and there is nothing that would stop it if it wants to do this.

1) Zanet entered the World Trade Cage to teach China how to behave,

but Shaolin Xi gave her tiger claws in her face.

2) Zanet raised interest rates, but in 2020 the yield curve is

hugging zero.

3) Zanet speak in a language nobody understand, but monetizing

airlines restaurants and NYC wouldn’t help, because corp US ability

to raise debt is limited and Midwood Bkly’n obey their own God.

“Zanet speak in a language nobody understand”

Pot…kettle…

I think Yellen is probably about as good as we could expect, but god it’s painful to listen to her. A mumble a lisp and some weird accent ( New England?)

Maybe digital currency is a matter of where form following function? This is not your grannies economy:

1. Bloomberg reports that during a student webinar, the head of the Bank of England acknowledged that they are looking into the possibility of issuing a digital currency

2. Amazon P/e 2012-09-30 @ 3633.14 [(EPS 7 cents) share price @ $252.44]

Amazon P/e 2020-11-23 @ 90.73 [(EPS $34.15) share price @ $3098.39]

Did any one else notice all the new vehicles in the “soup line” on the Consolidated Corporate Controlled Press outlets ? The Fed will need to push a lot of their D$’s into those folks accounts to keep them riding in a SUV to pick-up food . In my opinion, if you are on social media you have already agreed to be a data cow , and be milked for free . My 2002 Siverado rust bucket with 350K+ miles on it would be shamed out of line. I’m rebuilding the Mill in the ol’ bucket this summer if I can get the parts.

I’m still driving the 2002 Jeep Grand Cherokee, and so far so good. Just put on new tires all around; am under 300K mileage, so love to read the higher-mileage reports from other 2002-Club members.

Good luck with the rebuild- I know that my library keeps Chilton’s in the stacks…wondering if Warshawsky’s still exists.

Pulling the rug out of the banking system is a feature, not a bug. Destroying commercial bank money enables massive creation of central bank money without inducing too much inflation.

The commercial banks use their control of the payment system to preserve their parasitic rent. Central Bank electronic currency main goal is actually to remove this chokehold. That is of course assuming that Central Banks work for their shareholders instead of being just a springboard for its executive to a lucrative employment in a commercial Bank…

Incidentally, there is a theoretically sound way to have anonymous central bank currency, at least at the buyers level. Check taler.net , the GNU payment framework.

that central banks work for their shareholders is probably about as sound an assumption as one can make.

Bitcoin being confiscated by feds got Silk Road for 1 billion illegal actives so not secure fedcoins same scenario this won’t end good remember WE THE PEOPLE quit. Electing same billionaire idiots to. Steal r country

Dow hit all time high and just under 30,000. Tesla is over 500 Billion market cap.

Wolf, what are your thoughts on the market.

In this Thanksgiving season, I am thankful for The Wit of Wolf Street. Without that dark humor to look forward to, it would be impossible to try to keep up on the world’s economic/financial news. Thanks, Wolf, and best of the wordsmiths.

Great read Wolf, I just wonder if money laundering rules aren’t the problem. Federal law on MJ for instance? The entire purpose of owning bitcoin is avoiding these obstacles, hence the premium. While I get as agitated as anyone over financial privacy, while we enter a period after democracy sat perilously on the edge for a few days, that money transactions NEED TO BE scrutinized more closely than ever. The virus of sedition requires vigilance.

Why not simply lower taxes on the lower and middle class? Too politically unpalatable? Seems like a lot of work for the same effect.

I guess people will feel like they are getting money when actually their spending power is going down at a faster rate than the fed reserve money coming in.

Mr. Cramer on the mkt

Shockingly (who never bad mouths Wall St) Mr. Cramer described the existing environment as the “the most speculative market” he’s ever seen. He even likened the circumstances to a “slot machine” that always pays out.

Go Figure!

Mkts are zooming based on 3 major assumptions:

1. Various C -19 Vaccines ( assuming they are reliable and credible!?) will turn around the Economy! When is the question NOT asked. IMHO It will be around April if NOT later.

2. Infections, Hospitalization and Mortality rate will come gradually DOWN. Morbidity can haunt many who survived the infection. for months/years to come.

3. Easy-Peasy Spigot from Fed withhand in hand with Treasury.

There are a lot of IFs, BUTs and What & WHY Nots in the above scenerio!

NOT a comfortable thought.

“Central banks, such as the Fed, don’t have a profit motive since they can create money at will.”

False. Just as false as the statement that corporations pay taxes. PEOPLE pay taxes, and the PEOPLE at the Fed are not there because of some community minded ideal. Instead they are creatures of two institutions: banks and government, and they will serve those two masters above all others.

There is no reason why the currencies could not run parallel.

A currency is defined by whatever the national government accepts as payment for taxes. Once the entire federal budget moves to its electronic currency, the majority of the economy would follow. Then it only a matter of time until value of the “old dollar” is manipulated into oblivion. It’s done all the time with foreign currencies when their debt payments are due.

One year the IRS says you get a 10% discount on your taxes for paying digital and the deed is done.

‘It’s done all the time with foreign currencies when their debt payments are due.’