Leaks about money laundering, a resurgent Pandemic, China risks, exposure to Turkey’s financial crisis, all in a negative-interest-rate environment that is toxic for banks.

By Nick Corbishley, for WOLF STREET:

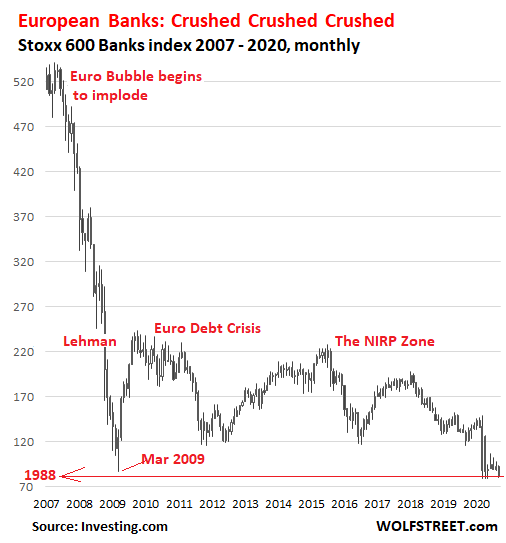

The Stoxx 600 Banks index, which covers major European banks, slumped 5.7% on Monday, to close at 81.1, just a smidgen above the multi-decade low, of 79, set in March. The last time before March that the index was below today’s level was in February 1988, during the sell-off that followed Black Monday in October 1987, when it also slumped as low as 79. The index has collapsed by 85% since its peak in May 2007, after having quadrupled over the preceding 12 years. Here are the wondrous European bank stocks going back to 2007:

Not even the promise of more industry consolidation, facilitated by shotgun mergers of big, struggling banks with smaller struggling banks, has stemmed the slide of Europe’s banking shares. Three weeks ago, Spain’s third largest lender, CaixaBank, announced plans to buy majority state-owned Bankia, with money largely provided by the State, to form what will be Spain’s largest domestic bank. Spain’s MSCI rose only slightly in response and is now lower than it was.

Today, it wasn’t just banking stocks that had a rough day. European stocks overall were down by 3.9%, as concerns grow over a second wave of the coronavirus. But banks were particularly hard hit.

One reason for the rout was the release of a report by the International Consortium of Investigative Journalists on lenders that had facilitated $2 trillion in suspicious transactions. HSBC, Deutsche Bank, Standard Chartered, JPMorgan Chase, and Bank of New York Mellon, were implicated. Over almost two decades, the five banks had “enrich[ed] themselves and their shareholders while facilitating the work of terrorists, kleptocrats, and drug kingpins,” the report said.

Here’s a sampling of how the bank stocks reacted:

- ING: -9.27%.

- Deutsche Bank: -8.76%

- BNP Paribas -6.37%

- Santander: -6.22%:

- Unicredit: -6.17%

- HSBC: -5.26%

Deutsche Bank appears to have facilitated more than half of the leaked $2 trillion of transactions, which were flagged to the U.S. government but rarely read by investigators, let alone acted upon, according to Deutsche Welle. Experts said that some banks treat Suspicious Activity Reports (SARs) “as a kind of get-out-of-jail-free card”, filing “numerous reports on the same clients, detailing their suspected crimes over the course of years while continuing to welcome their business.”

HSBC is alleged to have allowed WCM777, a particularly pernicious Ponzi scheme, to move more than $15 million despite the fact the business was barred from operating in three states. The scam pilfered at least $80 million from investors, mainly Latino and Asian immigrants, while the company’s owner “used the looted funds to buy two golf courses, a 7,000-square-foot mansion, a 39.8-carat diamond, and mining rights in Sierra Leone.”

The latest allegations could further complicate Deutsche Bank and HSBC’s business in the U.S. Deutsche Bank has already been mired in a host of scandals since the financial crisis: Its front-line role in the subprime mortgage crisis, its manipulation of interest rates, the services it provided Jeffrey Epstein, and its involvement in numerous money laundering scandals.

HSBC’s position is fragile, given it has already signed three deferred prosecution agreements (DPAs), an official form of probation, with the U.S. Department of Justice in the past eight years. But patience is running thin, especially since the bank’s decision, in June, to embrace the Chinese Communist Party’s crackdown on Hong Kong, which prompted U.S. Secretary of State Mike Pompeo to accuse the bank of aiding China’s “political repression” in Hong Kong.

HSBC’s relations with the CCP are also strained. No matter how much the bank kowtows to Beijing, it could still be sidelined as punishment for ratting out Huawei to U.S. authorities last year for breaching U.S. sanctions on Iran, which eventually led to the arrest of Huawei’s finance director, Sabrina Meng Wanzhou, in Canada.

This weekend, fresh reports surfaced that China could put the bank on the list of “unreliable entities”, a punishment meted out to foreign companies seen by the Chinese government as compromising national security. Given HSBC’s massive dependence on the Chinese market, which together with Hong Kong accounts for the lion’s share of its profits, if that were to happen, as unthinkable as it may seem, the impact on the lender would be huge. HSBC’s shares are now down 52% so far this year, at their lowest level since 1995.

Other banks have similarly stellar performances this year, pushing the Stoxx 600 bank index down 43% so far this year:

- Spain’s Santander (-59%) and BBVA (-58%)

- France’s Société Générale’s (-63%).

- Italy’s Intesa Sanpaolo (-32%), which recently took over its domestic rival, UBI Banca;

- Switzerland’s UBS (-17%) and Credit Suisse (-30%). They, too, are thinking about merging, to create a European megabank that is capable of competing with giant U.S. lenders;

- Deutsche Bank (-3.5%), ironically the best performing European large bank this year, after its shares had collapsed last year, and Commerzbank (-29%). The two banks’ shares are down 94% and 99% from their respective peaks, in 2007 and 2000.

The risks continue to accumulate for Europe’s banking sector, which never properly recovered from the last two crises — the Global Financial Crisis and the Euro Debt Crisis — and has been chronically debilitated by the ECB’s evermore aggressive monetary policy, pushing its policy rates and many bond yields into the negative, with largely undesirable consequences for banks, such as obliterating their interest margin and destroying their capacity to generate a healthy profit.

Europe’s doom loop — when shaky banks hold too much of their country’s shaky government debt, raising the fear of contagion across the financial system if one of them stumbles — has actually deepened by €210 billion since the start of the pandemic, according to a new report by S&P.

Another risk that appears to be growing is the outsized exposure of some European banks — particularly those in Spain — to struggling emerging economies, including Turkey.

But the biggest risks are at home. Although Europe’s furlough schemes and forbearance programs have helped forestall the pain, it cannot be put off forever.

To give banks a little breathing room, the ECB has relaxed banks’ leverage requirements until next July. The ECB’s plan to keep Europe’s banking system afloat is to push through a massive wave of consolidation that will weed out many of the weaker, smaller banks and reinforce many of the larger banks, many of which are also weak.

“Before the Covid crisis, the need to adjust costs, eliminate excess capacity, and restructure the banking sector was very important,” and the pandemic intensified those needs, Luis de Guindos, the ECB’s vice president, recently said. Banks need to consolidate “quickly and urgently,” he said. The hope is that with less competition, they’re able to survive in what is for banks a hostile interest rate environment that the ECB has created. By Nick Corbishley, for WOLF STREET.

For Turkey, borrowing in dollars & euros was cheap until it wasn’t. Read… On Concerns about Turkey’s Financial Health, Lira Dives to New Low, Cost of Insuring Turkish Sovereign Debt Nearly Doubles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Time to buy up Europa

Is it? I will stick with metals and cash thanks

DITTO!

Surely this time it’s the bottom

The only bottom I know as far as monetary, banking and fiscal policy is concerned is ZERO.

Ask the Venezuelans, The Zimbabwe inhabitants, the ( very ) old Germans who lived through Weimar, The Argentina population, the French ( assignats ), …

Stock market did great during the Weimar Republic.

The Zimbabwe stock market (INDZI) is up 594% year to date!

No. I mean, who would want to ($)wipe all those dirty cheeks?

Educated but poor Millennial, you are on the right track.

Chances are you won’t be poor by the time you reach middle-age, if only you can listen to your own advice and dip buy into Europa.

No one knows when is the bottom, so just accumulate as your financial means allows. When I was your age, I had little spare cash to put into stonks too, but what I’ve managed to put in over the decades more than paid off in terms of dividends and capital gains. If I could travel back in time, I’d tell my younger self to put more into stonks rather than buying stupid stuff, but I know its a hard sell to my younger self when my earnings then were meagre.

Despite what everyone feels right now, remember the darkest time of the night is just when the dawn is arising.

Or think of it this way: Let’s say we imagine a worst case scenario where the news reports that a giant asteroid is heading to Earth and that there is a 50% probability that it will smack into our planet and wipe out everyone, so much so even our dear corona-viruses will not survive. So what do you think is the correct thing to do?

If such a literal worst-case scenario were to happen, and the market crashes really hard, I mean… its the end of humanity right?

Counter-intuitively, I will sell everything and buy every Stonks I can get my hands on! because I have 50% probability that the asteroid misses Earth, and then I will become fabulously wealthy as Stonks markets recover; and if I’m wrong, so what? it doesn’t matter anyway, get it? lol.

What is a “STONK”

A STONK is a stock that stinks.

kevin,

“Chances are you won’t be poor by the time you reach middle-age, if only you can listen to your own advice and dip buy into Europa.”

OK, maybe in the future. But not in the past… if you look at the Stoxx 600 bank chart above, you will see that this “dip buy” and hold would have destroyed your wealth going back to 1988. What you would have to do is dip buy and sell on the bounce — in other words, trade and time the market and time those bank shares and know in advance when the next crisis comes — to get rid of those shares before they drop to the 1988 low again.

Yes of course, its forward-looking advice for the future.

And especially for millenials with most of their lives ahead of them. Why would they bother with the past (or our past? lol.)

My comment is based on buying a BROAD market ETF, not advice on any specific sector or company. One can always cherry-pick any sector (i.e. banks, tech, industrials, consumer staples etc.) and show on some arbitrary timeframe, that each will come to grief depending on when you invest and divest – on hindsight.

No one is saying its an easy-street to riches or a sure-win lottery ticket.

That’s why I said to the millenial “Chances are….”

In fact, you could also pick say, Japan and rightly conclude that had you invested in a broad Japanese ETF in the 90s, you’d still be losing money today.

My point is that the broader your investments are (by that I mean real estate, equities, bonds, PMs etc. No Bitcoins for me yet) and the longer your time horizon, the better your chances of winning.

My own experience is that US of A was a pretty good ride for me despite some inevitable corrections every now and then, but looking ahead, it might not be a such a good deal for millenials buying in at late stage versus looking at other opportunities to get in on the bottom.

Wolf,

Good advise but it is extremely hard and dangerous. I tried to buy deep ans sell the bounce. However couple time I timed the market incorrectly and lost a lot. Do you remember I asked about the airline stocks? I got burned badly?lol?

Being consistent and doing it for long run is a key to success. If you dont have a lot of capital at the beginning. Good for you that you started it at some point. Thanks for you advise.

No thank you, it is like a cheap ticket on the Titanic on April 15 1912.

A dead horse is dead. You cant kill it more. If it is gloomy for europa all I can say is after dark there is a sun shine.

Young person, after you do this awhile you’ll learn to distinguish a fall from a bottoming process.

?

DB’s Covid low should hold and this low should provide capitulation.

“Attempt no landing there.”

What about the total gross obvious literal dishonesty exhibited by all concerned? If I acted like that, I couldn’t sleep at night, my children would criticize me horribly for my sleaziness, and I would lose all my decent respectable friends. Surely there are websites that just publish what has happened, and can give the names of the banks’ decisionmakers. They have to be publicized, even though we all know that in classic Dilbertian manner, all bankers have to be hidden and protected from those they lie to and steal from.

SiT23,

All these banks listed here are publicly traded and their top executives and directors are listed in public documents for everyone to see. There are no secrets here. If you want to know their names, just look them up. You can google them too, such as: ceo deutsche bank … his name along with his bio will pop right up at the very top of the page. Executives of big banks are very public figures.

Wolf, be that as it may, I haven’t seen much in the way of either contrition, nor endowments into the provisioning of orange prison threads, for all these ‘execs’ who .. if they were not protected due to their power positions, would be rotting behind thick steel bars .. kowtowing to Bubba .. instead of conniving with their tight ‘loot-to-share holder’ buds!

‘penance for thee, but NOT for Me!’ …

… same for the sovereigns who enable them to continue with these ongoing chicaneries!

I love september… cdx rolled and now banks sitting on those netted pos figuring out how much of it is a an asset or liability… lol

I wonder when companies like HSBC will begin to spin off their Chinese operations.

We’re already seeing it forced by the US with Tiktok. China could easily go tit for tat with Facebook or others.

Many companies are struggling to manage the PR between governments with opposing views, and may decide its less risky overall to split these entities on their own terms. Most companies already split their operations based on country or region anyways.

Will they be able to quickly enough if the Chinese government moves against them rapidly.

To what degree would a move to unreliable status affect their continuing to do business on the mainline.

what’s China going to do to Facebook? Ban it? Declare it illegal and forbid it to operate in country?

LOL

Apple and Amazon on the other hand could be in trouble. But in both cases, it would hurt China too. Because as much as Apple is exposed to China, the other way is true too, a massive amount of supply chain is exposed to Apple. If Apple goes down, a good number of companies in the supply chain would scream bloody murder. The advantage is that China couldn’t care less about those companies.

Facebook and many other major US internet firms are blocked at the Great Firewall, so they don’t have exposure. They do try, witness Google’s recent efforts in that direction, to tap the Chinese market, but without success.

US firms built the Great Firewall of China.

On Dutch TV it was explained that a polish subsidiary of ING helped russians to buy US stocks with ‘dirty’ rubles, then sold the stocks and got dollars back which somehow laundered it that way. Don’t know how that works exactly and it wasn’t explained either.

So i expect the US markets to go lower, because those ‘trade routes’ will dry up. At least until they find another way. Other banks will have been in the same kind of scheme a guess. They all do the same dirty tricks.

I also expect precious metals and stocks to go up again, because of the fear that is created now.

Well, yes.

In the meantime the may be a few week/months of pain for gold and silver bugs. This may be persistent price decline. May simply be pronounced volatility over the next 6-8 weeks.

Is the current correction likely to change the views on precious metals underpinning inflows into physical metal and ETF’s by more than retail investors? Same question with the money raised by several Gold miners recently.

I would like to think, even if Gold loses overall, it may end up next year less than other asset classes.

In any event, it’s hold your hat time.

I have 200 golf courses, what do you have?

I have a 150,000,000 square foot mansion.

I have a 999.9 carat diamond.

I have mining rights in every African country.

I have the largest super yacht in the world.

I have all the satellite rocket launch sites.

I have all the communication satellites around the planet.

I have free travel to Mars and the Moon.

I have bottling rights to every water spring on Earth.

I have all the seed rights to all the staple foods on the planet.

I have all the patents to zero point energy vehicles.

I have all the mind controlling pharmaceuticals.

I have all telecommunications networks on Earth.

I have strategic command of all space weapons.

I have control of the weather in any country I choose.

I can print as much money as I want.

What would you choose to do with infinite money supply?

What did I miss?

You are not GOD and you will die with nothing to take with you. I also will die and go to heaven to be with GOD. And live forever.

GOD: “Welcome to Heaven – here are your wings!”

ME: Honey-Mustard or Garlic-Parmesan?

GOD: “GET OUT!”

Remember one of the arguments that they gave against Bitcoin was that criminals will benefit from it… not as much as from using the global banking system I think. I’m not a fan of bitcoin but the hypocrisy of the people running the financial system is incredible.

There’s the ‘right’ criminals and the ‘wrong’ ones. Only the right ones are allowed to benefit.

You mean those crooks with ‘pull’ are friends and those without are criminals…?

Nooo, say it ain’t so..

There are criminals and then there are criminals.

Falling share prices – couldn’t happen to a ‘nicer’ bunch of businesses!

Just another reason to avoid anything in Europe.

I din’t see any Japanese banks in the lists. I wonder if they were involved or not. (Lots of cash used to go on the ferry from Japan to North Korea until the service was stopped in 2006) There was some discussion about a couple of Australian banks involved, but not much detail.

On the other hand, the banks make it very difficult for ordinary people and businesses to get loans.

Last spring the a Trump organization asked for a delay of payment on a loan owned Deutschbank due to the coronavirus. Trump has a record of defaulting on loans.

And DB with a whole slew of potential enforcement actions ongoing at William Barr’s DoJ.

On one hand these stocks are cheap. But the systemic risk of all asset classes ruins any investment opportunity. It’s still buy and hope. Yet inflation is on the horizon. The Fed wants it badly – and – wages are going up before my eyes. I live between NYC and Philadelphia. There are numerous warehouse job advertisements on billboards. They offer $18 per hour. I have never seen such demand for labor. And then we have increased cost pressure from tariffs. But TIPS are selling for 125. Maybe real estate is an option. In all the years I have never seen such a “hopeless” market. So the depression aside, Mr. Wolfe, is there anyway to understand the magnitude of all those derivatives? I believe they equal 10xs the value of the markets. But how can we gain some insight? Thank you sir.

“… numerous warehouse job advertisements on billboards. They offer $18 per hour. I have never seen such demand for labor.”

Everything having to do with ecommerce is hot. Ecommerce is booming like never before. Ecommerce means supply chains, specialized warehouses (fulfillment centers), and specialized transportation (delivery).

You live between two of the most affluent malls in the country, Shorthills and Valley Forge. Go out and take a look for yourself.

My personal opinion is that even the luxury sector is struggling. I’m not even buying the good deals anymore, for what, not leaving the house most days.

You’ve also never seen such an overabundance of available labor. Expect downward pressure on wages for a while.

Consolidating the European banking sector will only make matters worse by creating systemic banks.

‘….a massive wave of consolidation that will weed out many of the weaker, smaller banks and reinforce many of the larger banks, many of which are also weak’

LOL!

Aren’t they doing this over 19 yrs simce 2008? May be the WEAK ones wil take over the weakest!?

Is it not the end to ‘extend & pretend’?

I also work in the logistics sector, for a large international forwarder with fairly diversified operations. I can tell you with great certainty that there is no overabundance of warehouse labor. Anyone with a pulse and a pair of hands can land a 15+ /hr job at any one of a dozen pick-and-pack operations in Lockbourne in about a week.

Our Distriburion operation, which is 95% exam fulfillment, is hiring out the wazoo. All through various employment agencies catering specifically to the sector. Labor will not hesitate to jump ship if a neighboring operation offers up 2 or 3 / hr more.

“Europe’s banking sector…has been chronically debilitated by the ECB’s evermore aggressive monetary policy…”

Surely the powers-that-be knew that their policy would hurt the banks. Did they not care? Was that part of the plan? Or simply dismissed as unfortunate collateral damage?

Makes one wonder.

International trends in central bank independence: the ECB’s perspective

https://www.ecb.europa.eu/press/key/date/2019/html/ecb.sp191112_1~f304b47e14.en.html

“To give banks a little breathing room, the ECB has relaxed banks’ leverage requirements until next July.”

= Change rules as needed. In the meantime “weed out many of the (pesky) weaker, smaller banks”.

Sounds like the plan is going even better than expected.

Two unrelated thoughts:

The good news about Deutsche Bank is that since it has near zero equity (after write- offs for negative good will, pending fines etc.) its nationalization would be cheap. So why not do it? This is Germany after all where few people are going to start screaming about communism if the government takes over a bank whose name alone is an embarrassment to Deutschland.

Second: HSBC in trouble for ‘ratting out Huawei to U.S. authorities last year for breaching U.S. sanctions on Iran, which eventually led to the arrest of Huawei’s finance director, Sabrina Meng Wanzhou, in Canada.’

This is a major embarrassment for Canada. I know we aren’t supposed to get political on this site but the entire fiasco is political. Canada and the US have a joint extradition agreement but obviously for Canada, now knowing what the US regime can stretch to interpret as crime, the agreement needs tuning. Step one: ask if it would be a crime in Canada. Did the guy injure or rob or extort someone in the US? That would be a crime in Canada, so extradite.

The US admin is almost completely isolated on these Iran sanctions, not just from the rest of the world but from its own career officials and its former cabinet officers, who have mostly been fired by tweet. Rex Tillerson. Gary Cohn, Mattis, all, said that Iran was in compliance, and was being inspected so you would soon know if it wasn’t.

But that is a US problem. Canada’s problem is how to avoid being sucked into US bipolar mood swings. We declared war on Germany 2 years before the US, but stayed out of the Iraq tragedy (ironically, Iraq WAS the counterweight to Iran )

So it can be done.

Good honest comment, Nick.

This is not a political site, but since when has politics NOT taken marching orders from the rich and powerful in either/any country. Sometimes, politics and dollars are indistinguishable, hence ZIRP. I’m still waiting for a banker to be jailed. If Angelo Mozilo can stay out of jail, nothing will happen to any crooked banker from what I can see. Not here, there, or over there.

regards

I’d rather see the banks struggling instead of the working class. We should just have federal banks managing the money for zero profit. Also insurance. There should be no profit in it.

Along with rent seekers these are all parasites.

P.S. I didn’t read the article yet, this is just a troll comment.

We better get a handle on this covid thing before it causes problems!

NINJA loans are back in the New Orleans area and maybe in the rest of the country too. An article yesterday in NOLAdotCOM quoted a mortgage broker saying loans are being approved for furloughed workers on the grounds they will be called back to their jobs. If they don’t have a job to go back to, the broker creates a file with all the documentation and completes it, if and when they get a job.

Houses are reported to be flying off the shelf. This in an area hard hit by the crisis. The higher prices are causing real estate taxes to rise as well, just when most can’t afford it.

And this while the state has exhausted its unemployment fund and has to borrow from the feds to replenish the fund. This will cause them to lower their already low maximum unemployment benefit another $26 a week, going from $247 to $221.

I think something else is going on too. I’m in rural California. I’m seeing some very unlikely properties going 3 days after being on Zillow. I’m seeing adds for buying multiple properties for cash. 2 I tracked as nation wide, although one hid itself as “local” in hundreds of places nationally. I’m seeing blog reports of agents for companies posing as newlyweds and then trying to flip the properties. I’m seeing properties appearing then disappearing then appearing again with no sales or pending sales recorded. I’m seeing properties resold within a month.

I’ve been looking at listings under the microscope as I was finally, finally, in a position to buy a home. Then prices rose 20% within a month. Something smells rotten. I don’t think it’s only people leaving the cities. I think some of that 3 trillion went to major RE acquiring companies or individuals.

It is fishy, indeed. I noticed it.

Prices started to go up suddenly and they blame it on lack of supply. But the game behind the curtain is not so hidden.

Can you believe the bank asked my friend about his apartment value without hiring a appraiser, while he was refinanacing? He said 600k, 100k more than actual value and the bank accepted it. He refinaced the loan. Banks are trying to keep the homeowner happy with lower rates with ziro cost to refinance.

I saw all the zillow, redfin , … CEOs advising people to not to sell, why?

They know the bubble was deflating since 2018 and now they have chance to blow way more air into it and let it inflate temporary. Will it explode.?

They are trying to strech the rubber band even more. I expect a sharp and harder backtrack because they pulled the rubber band too far.

Please, share your thoughts. Thanks.

“I saw all the zillow, redfin , … CEOs advising people to not to sell, why?”

I haven’t seen that- where did you find that? What key words- can’t use links here.

I’m in far northern Ca. Where are you? Real estate agents here are saying, quote” real estate is hot hot hot, so sell NOW”. Haha.

Another thing I noticed is banks seemed to be slowly letting out their left over 2008 recession foreclosure homes onto the MLS. They stopped a few weeks or so before the price jump. All of those homes were supposed to be put on the market quite a while ago…

One positive thing I saw on what I think was an internal memo to RE agents from the Ca RE org was that sales have been softening a little bit for 3 weeks.

I wonder what percentage of homes in the US are owned by either corporations or by foreigners, especially Chinese, that are not going to be put back on the market.

Also, I wonder how many homes the banks are drooling over and hoping people can’t pay for. Heck, what do they care? they’ll get bailed out.

Buying European bank stocks is not investing in a business. It is investing in the whimsical support of government entities. Without continual government interventions such as changes in capital requirements, too big too fail mergers etc., these entities would fold. The current market value of these equities is a sliver relative to book value of equity, and it’s microscopic relative to the book value of their assets. They have as much chance as an 85 year old man stepping out on the a professional football field. If they don’t adjust the playing rules to protect this man, he’s done.

Unfortunately, this is largely true for the broader stock market as well.

The money laundering report is political flotsam, extraneous information from the investigation of the presidents’ finances. Financial weaponization (sanctions and money laundering rules) along with central bank interference, has ruined the banking industry. If that doesn’t spell the end crypto currency will finish them. Should the Euro hold up I would prefer this banking index, and short banks which deal in dollars, and that fiscal mess post 2020.

Anyone notice Fed telling Congress they need to spend more and CBO telling Congress they better start spending less.

The question is ‘ any one listening’?

Bank stocks have ALWAYS been poor investments.

Back in “the good old days” when we actually had functioning capital markets, bank stocks sold at P/E’s that were barely in double-digits and had dividend yields of at least 4-5%.

Anyone who has been buying these stinkers since 1999 (or before) is either an idiot or a compulsive gambler, or both.

“Anyone who has been buying these stinkers since 1999 (or before) is either an idiot or a compulsive gambler, or both.”

Really?

Take a look at the performance of Australian bank shares during and after the mining boom in Australia. They performed better than the mining shares and provided a huge return in capital gains, dividends and for Australian holders franking credits.

For example, CBA, Commonweath Bank, the biggesst bank in Australia.

Even the last ten years have been outstanding. Let’s look at the ten year performance since 2011.

The price was around A$45 a share in 2011. Four years later in 2015 it hit a high of A$92 or so. Since then it has moved up and down and the most recent high before all the crap started here in Australia with the banking commission investigations and then the virus was A$85 or so in January 2020.

It hit a low of A$61.82 in March with the big sell off and then hit A$71 before starting to fall again. Current price is just above the March low of A$63.

And all during that time they have been paying huge dividends. This year around $A3 a share and another A$1.30 or so in tax credits per share. Previous years have seen about A$4 a share in dividends and the associated tax credits.

So even if you bought and held over those ten years you’d have a 50% or capital gain and around $A40 or so in dividends per share and at least another A$15 in tax credits. Not bad for a conservative investment in a bank share. ($A18 in capital gains, A$40 plus in dividends, and A$15 in tax credits for a total of at least A$73 over a ten year period.)

Are they going to be a good investment going forward?

Who knows.

And you want to know the reason why?

It is because of increased earnings caused by two factors:

1. A big increase in the variable rate loan mortgage book for residential real estate and even more important;

2. Commercial banks were able to increase the net interest spread charged on these variable rate loans over the RBA discount rate thus increasing earnings. Spreads have exploded upwards on these loans.

These variable rate mortgages are huge cash cows for the banks. Even if the total interet rate margin of the banks has fallen, these loans have provided the ‘juice’ for the banks to cover their other losses to companies and commerical real esate as well as huge fines and other write-offs.

You can’t get a 30 year fixed loan here in Oz for a house from an Australian bank and I don’t that there are even 10 year fixed loans anymore either. I know there used to be five year fixed loans, but the interest rate banks were charging were around the 7% area when the variable rate mortgage loan was around 4%.

They did this by increasing rates by more than when the RBA increased the discount rate, by reducing rates by less when the RBA cut rates, and by having out of cycle increases of the rates as well. The banks also delayed passing on any cuts too.

So you have a bigger base to earn interest on and a bigger margin on that increased book.

No banking leaders ever get prosecuted so why would one think the behavior would change when then central bank is flooding currency to this blessed group.

Bingo. Remember when the old grey wise heads said you couldn’t prosecute after 2008-9 because the banking system was too “fragile”.

The foxes were advising the hens not to enforce the law and the hens went for it.

Yeah, I hate banks and the whole fractional-reserve banking scheme…

But the chart would be much more informative if it was based on market cap, similar to the second chart in the Aug. 26 article about Airlines; not based on an unscientific, loosely-defined index.

All these indices are essentially market cap indices. I can convert my “Giant 5” market cap chart, expressed in trillions of dollars, into an index that starts at 100. It’s just a simple formula on a spreadsheet. That chart will look the same, except the vertical axis will be measured around 100 instead of trillions of dollars.

Maybe anyone interested in investing in bank stocks, can come to my country! Here, banks are even more indebted, much more dysfunctioning, and incredibly more corrupt than their troubled european peers, but their stocks are blossoming! (Yes, even in dollar terms)

Iran pays really high positive interest rates so looks really attractive if you do not believe you are going to lose your capital on Iranian currency devaluation or the bank simply going bankrupt.

This money laundering is going on all the time.

The center of the world for it must be the City of London.

Hence no effort to eliminate it.

One can set up online a UK limited company in 24 hours for US$16.

Open a bank account within three days.

Make a few transactions.

Close the bank account.

Let the company be struck off by Companies House after 18 months for failure to file the Confirmation Statement or if one feels generous pay US$13 striking off fee to close the company.

Cyprus used to be a great place to open an overseas company bank account as well by simply taking the UK company memo and articles and certificate of incorporation to a Cypriot bank in Cyprus or once you had your contacts open the Cypriot bank account by getting documents verified by a Cypriot London branch.

The possible reason for this Money Laundering news is all about fines and monies for the government.

The banks have huge losses brought forward form 2008 fiasco so they have no corporation tax to pay on profits currently and hence no taxes to the government.

However a fine is the solution for the government to get some monies off the banks.

HSBC is a buy, they’re very agressive on the canadian market. Oh and they’re one of the TBTF ( Too big…).

Disclosure: I just bough some today.