The heavy weight of debts denominated in foreign currency. Borrowing in dollars & euros is cheap until it isn’t.

By Nick Corbishley, for WOLF STREET:

In recent months, Turks have been buying up gold — their traditional safe haven asset of choice — in even bigger quantities than usual. The average daily volume sold at Istanbul’s Grand Bazaar, one of the world’s oldest still-operating markets, surged tenfold between the start of the lockdown, in March, and the end of the lockdown, in June, according to traders cited by the Wall Street Journal. Turkey’s domestic gold production was not nearly enough to meet demand, so $15 billion of gold had to be imported from January to August, up 153% from a year earlier.

They can hardly be blamed for wanting to buy gold, the best-performing currency against the lira over the past ten years, given how quickly the currency in their pockets and in their bank accounts has been depreciating. Ten years ago, it took one and a half lira to buy a dollar. Today, it takes seven and a half. In one decade, the currency has lost 82% of its value against both the dollar and the euro, and 90% of its value against gold.

On Thursday, the lira fell to a fresh low of 7.55 against the dollar, of 8.91 against the euro, having shed 21% of its value against the greenback so far this year and 26% against the euro.

The cost of insuring Turkish sovereign debt has almost doubled. The latest rout follows a decision by Moody’s to downgrade Turkey’s sovereign debt by one notch to B2, five levels below investment grade. It also maintained its negative credit outlook for the economy, citing concerns about Turkey’s rapidly vanishing currency reserves, which “have been drifting downward for years on both a gross and a net basis but are now at a multi-decade low as a percentage of GDP because of the central bank’s unsuccessful attempts to defend the lira since the beginning of 2020.”

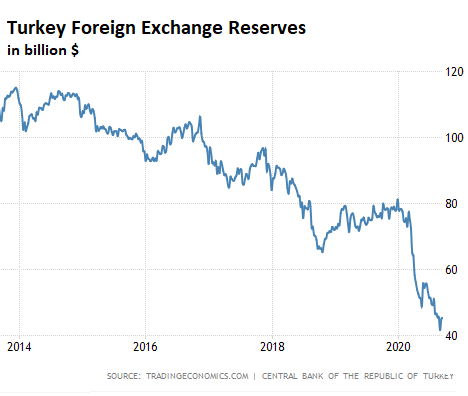

Turkey’s central bank has burnt through over 40% of its foreign-exchange reserves trying, clearly unsuccessfully, to prop up the lira, leaving the reserves (excluding gold) at $44.9 billion (as of 4 September). This, as Moody’s says is an “exceptionally low buffer when measured against upcoming external debt payments.”

Turkey’s central bank has been borrowing vast sums of foreign currencies from domestic banks and then selling those currencies to buy lira. These currency swaps ratcheted up the central bank’s net short position in the swap market, from $30 billion in March to $53 billion at the end of July. If they were not rolled over, all the commercial banks’ reserves at the central bank would be insufficient to cover the short position.

Turkey does hold substantial gold reserves. Like it its citizens, it has bought up large amounts of gold in recent months. Due to this increase in gold purchases as well as the recent increase in the gold price, Turkey’s gold holdings are now broadly equal to FX reserves ($42.7 billion at the beginning of September). But it’s still not much of a buffer.

Turkey’s gross foreign exchange reserves are now at their lowest point since November 2005. The lower Turkey’s gross and net reserves fall, warns Moody’s, the more likely the country is to experience “a severe Balance of Payments crisis, causing acute disruptions to economic activity and further deterioration in the government’s balance sheet.” (Chart via Tradings Economics):

During prior periods of acute currency weakness, Turkey’s tourism industry has served as an important counterweight. The lower the currency has gone, the more competitive and attractive the country has become as a tourism destination. Today, with the virus crisis upending global travel and tourism, that is not an option.

One upshot of this is that a lot less money is flowing in to government coffers, at the same time that the government is spending more than ever, partly to counteract the devastating effects of the coronavirus crisis but also to maintain Erdogan’s expansionary monetary policies. The result has been an ever widening gulf between government revenues and government expenditure. In August, Turkey’s 12-month rolling current account deficit surged to $14.9 billion, its highest level since early 2019.

Other problems are stacking up. The economy suffered a 10% contraction in the second quarter as the collapse in tourism and the lockdown wiped out a big chunk of the nation’s revenue. The plunging lira is also making it hard, once again, for companies and the government to service their dollar or euro-denominated debts, which in April still accounted for 37% of the total debt owed by Turkish borrowers.

Inflation, at 11.8%, remains high and still well above the benchmark interest rate (8.25%), meaning that the real rate of interest is deeply negative, which puts additional pressure on the currency. Even as the lira continues its descent and inflation remains high, Turkey’s president Recep Tayyip Erdogan continues to oppose a rate hike, since it would stifle the one thing that has underpinned Turkey’s economic growth model under his rule: constant credit expansion.

On Wednesday, Moody’s delivered a second blow by downgrading 13 of the nation’s banks, including big state-owned lenders and a number of foreign-bank subsidiaries, such as Garanti BBVA, which is majority owned by Spanish lender BBVA; TEB (BNP Paribas); Yapi Kredi (Unicredit) and HSBC Turkey.

Many of these banks, as well as Turkey’s large state-owned lenders, are likely sitting on a mounting pile of non-performing loans (NPLs), though, as Fitch has warned, the scale of the problem has been largely masked by the recent explosion in lending and the forbearance rules introduced by Erdogan’s government. Thanks to those rules, the worst NPLs, or so-called Stage 3 loans, are now classified when 180 days overdue rather than the previous 90 days. By Nick Corbishley, for WOLF STREET.

For many, squatting is a desperate last resort. For others, it’s a lifestyle choice or political statement. Barcelona, ground zero of the phenomenon, attracts squatters from all over Europe. Read… How Spain Became a Squatter’s Paradise

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is gonna be a contagious event, soon the cracks will become big enough to bring down a few European banks, they have massive exposure, it’s like Iceland in 2007, then Northern Rock(UK), then Lehman & Bear Stearns, this will be a massive problem, you can already see desperation when Turkey tries to drill for gas in disputed or Greek zones, they are already angling for a battle which could falre up to a war, Greece already buying French fighter jets and other military equipment. A full blown collapse & financial crises is already happening below the surfice, remember it took a year from Iceland banks to Lehamn before the penny dropped & markets collapse, today we have mass unemployment, debt no payment holidays, trillions of stimulus, fake unemployment statistics, and whatever else, the list is long, wait & see hundreds of hedge funds go bankrupt, funds get locked down with no withdrawls allowed for years after huge losses, banks go bust, bailouts, stock crash, property crash, the whole works. It’s already happening if ya look close enough. So expect a full blown financial crises which they will use once again to bail out the banks, there is no way in hell they can absorb the defaults comming, then add the commercial property disaster.

It’s gonna make 2008 lokk like a picnic :)

That is the irony.

All these shenanigans were done in 2008 to kick the can.

Now, to get another kick, mutiple times the shenanigans.

Exponential curve.

It’s too bad America didn’t allow a real recession in 2008.

America would be so much better off.

It’s not a real recession that’s needed so much as a real rebalancing.

Incomes need to be allowed to rise faster than debts.

This can be done by a recession where incomes plummet and debts plunge faster as they are restructured through bankruptcy, or it can be done with the likes of stimulus we haven’t seen since WW2. The kind of stimulus which makes the government find use for those disposed of as worthless to the economy. Hopefully they can be used for more productive purposes.

I tend to think this kind of stimulus will come somehow whether it’s another CCC or some amount of UBI, because the alternative depression will not be democratically acceptable, and kicking the can down the road with QE is generating ever more anger and political instability. This is a “Forth Turning.”

Yes but all the money sloshing around at present will still be sloshing around after the dung hits the fan. A lot of people will be on a position to make a lot of money.

There are points of contention. The current admin is pushing Turkey out of NATO and towards Russia. Probably one reason they weren’t included in the dollar swap line. China is lending them money as well. Not sure if the realignment matters to Turkeys financial problems. What if they decide to issue debt in Yuan? China has shown better acumen at running a command credit economy so far. The extension of colonial rule by way of IMF loans, fails to maintain traction. Western investment pulls back but too much money everywhere, where does it go?

“The current admin is pushing Turkey out of NATO and towards Russia.”

Turkey has been a *hugely* unreliable “ally” for years.

They have pushed themselves out of NATO.

As for Russia…Turkey and Russia have been mortal enemies for centuries…check out Wikipedia.

Turkey isn’t going to play cuddles with the Bear next door.

They much rather give the finger to the US, with the backstop that we will die for them via NATO.

Perhaps Turkey could just default like Argentina. They could go to the IMF, please poverty, borrow $50 billion, and not pay it back or offer to pay back pennies on the dollar. Doesn’t seem to matter in South America whether you pay back your loans or not.

Excellent article. Thank you!

talk about argentina have the same problem but x10!

Makes USD cleanest dirty shirt – yet again. I guess we don’t trade with Turkey (much), so we (USA) are probably not benefitting much financially from their pending BK. Hopefully the gold can keep them afloat.

Gold will see $500, safer than Lira but not a place to hide, they are better holding a basket, Dollars, Euros, GBP, CHF & 20% gold, or pay off property debt.

I think you forgot a “2” in front of the “5” and should be :

“$2500”

They probably meant a zero *after*: $5000

‘On Thursday, the lira fell to a fresh low of 7.55 against the dollar, of 8.91 against the euro, having shed 21% of its value against the greenback so far this year and 26% against the euro.’

So euro cleanest by quite a bit.

But neither can be proud of being cleaner than ‘sick man’ Turkey. At some point all shirts are too dirty. Against the lira, gold has outperformed both the US$ and the euro.

The difference between the valuation of the Turkish lira vs the dollar or Euro is not an indicator of the strength of either of the later. It simply shows the valuation of the dollar vs the Euro at this date. (Basically it takes more lira to equal a Euro than a dollar.) It would be an indicator of strength if there was 1:1 parity between the Dollar and the Euro.

Should the Euro drop (which will happen due to Brexit) that valuation will change (I’m guessing 10% in favor of the dollar). Should the Euro ever hit 1:1 parity with the dollar the EU will probably fold.

Your first paragraph repeats my comment:

‘Basically it takes more lira to equal a euro than a dollar.’

OK.

And then adds ‘but valuation isn’t strength’. In the here and now, that is what it is, by definition. What you seem to want to say is that the euro’s strength is temporary and that parity with the dollar will signal its demise.

The euro was below parity with the dollar for two years.

But if the euro was to fold, and Germany returns to the D- mark, the US dollar becomes a distant second- tier currency as a store of value. Before Covid, Germany was running a 2 % budget SURPLUS.

More likely than Germany having its own currency is it being an anchor for a new euro

union of the ‘frugal five’. If the euro could dump Greece, Italy and Spain, that would be send it (or whatever it’s called) soaring.

German manufacturers would scream but they survived a towering D-mark pre- euro.

I am going from memory but I think euro started at $1.15 to the dollar and has traded between about $0.80 to $1.35 or so.

Point KG, so conceding it, looks to me like there isn’t enough between them for the first comment to proclaim ‘king dollar’

I’d still call them neck and neck, even given the problems of running a multi-state currency, a handicap the US$ doesn’t have.

Given the Italian banking crisis, the Greek debacle, etc. the Spanish flirtation with civil war, it’s amazing how strong the euro is.

So if we imagine a D- Mark or a frugal five without those laggards, it wouldn’t be close.

Ok, Nick let’s do it as perfect math.

$1/7.55= 0.1324 (or the Turkish Lira is worth 13 U.S. Cents)

E1/8.91=0. 1122×1.19 (the current exchange rate dollar vs. euro)= 0.133 (or, in plain English, the Lira is worth 13 U.S. cents).

The valuation in straight percentages (7,55 vs. 8.91) does not equal purchasing power because there is a difference in valuation between the two currencies (dollar/euro) which, when added in makes the value of the lira the same.

In actuality the value of the lira shed would depend on the currency and the exchange rate at the time of the transaction, or it could be measured against the average valuation of the various currencies annually. This is preferable as it smooths out any major changes in adjustments in exchange rates.

Ten years ago the Euro was trading 1.48:$1. It is currently trading 1.19:$1. The low this year was 1.08:$1. So, looking at pre-covid numbers (ie the Fed printing lots of dollars to cheapen the currency) the Euro had, over the past 10 years, lost 27% of it’s value.

See above

The expression I like is “the healthiest horse in the glue factory”.

Yeah…he’s using the OJ Defense: If all else fails, play the race card!

Those dirty Greeks!

That will only be for a while. What if all those countries have to sell their dollars to get some stability at home? (Which they will not get). The US dollar will become the dirtiest shirt there ever was.

In one of yesterdays articles somebody wondered what next event would topple the whole upside down piramid. Most likely it will be an event like Turkey that starts the domino’s falling then something under the US jurisdiction. The US could deal with an at-home event, but not so much with a far-from-home one. It’s always something one didn’t expect, because if it was expected, or identified as a potential problem, one would prepare for it. It will be a thing we didn’t prepare for that hits the fan and starts everything coming down. There is no way of knowing in advance, because then we would prepare for it. You see the problem? We know of Turkey, so that will not be it.

If you see a problem somewhere, don’t tell anybody, but take position and wait for it to happen. But beware, you might be wrong. ;-)

Thanks Nick, it’s interesting to read about another nation’s problems as it shows us how the U.S. stacks up and where we might be heading someday soon. Let’s hope not!

and Turkey has potential conflicts on 6 fronts.

Cyprus, Greece, N Syria, Libya, Iraq and Armenia.

Plus an internal Kurdish revolt.

Plus demographics off a cliff.

“Other problems are stacking up…”

Those are 6 fronts that Turkey is facing- and can control its level of engagement.

Turkey’s biggest external threat comes from the north across the Baltic.

Who benefits from these foreign relations debacles:

UK vs EU

Poland, etc vs EU

Turkey vs Greece, etc

Saudi vs Iran

China vs India

On and on

So if the dollar takes a run higher, are they finished.

Historically platinum has been more expensive than gold. It is much less common than gold. Currently the price of gold is close to double that of platinum.

Interesting. The “Platinum as an investment” page on Wikipedia says:

“… during periods of sustained economic stability and growth, the price of platinum tends to be as much as twice the price of gold; whereas, during periods of economic uncertainty, the price of platinum tends to decrease because of reduced demand, falling below the price of gold, partly due to increased gold prices.”

Looking at a graph of the two, prices for gold and platinum were roughly the same from the 1970s until 2000, when platinum became more expensive than gold. They started coinciding again in 2008 until diverging in 2015, this time with gold being more expensive.

Platinum has lots of industrial uses.

Demand goes down in a worldwide recession.

Isn’t the biggest use of platinum catalytic converters? As electric vehicle sales displace combustion engines… This might hurt value.

Platinum ist already replaced by palladium in catalyctic converters.

I’ve wondered about what if we don’t go back to a gold standard, but a platinum standard instead. That would take a lot of people by surprise. Never underestimate the element of surpise.

How might the immigrants that Turkey is currently hosting (holding back from Europe) play into this?

TSO,

Good point. This is a wild card and one that doesn’t seem to get the attention it deserves. I anticipate that Turkey, should it decide unwisely to take some sort of military action against Greece, will first unleash hordes of unwanted immigrants (unwanted on both sides) toward Greece to sort of tie up their hands for a bit.

Maybe the immigrants are a source of revenue. The EU pays them off, and although the immigrants must be expensive to maintain, I would expect the Eu is making it worth the while of the insiders in Turkey.

I am more interested in the’collateral, damage to Spanish and other European Banks!

Is this first DOMINO to fall in the tightly knitted global banking system, like Bear Sterns in early 2008!?

Interesting development!

Bear Stearns

The word is..China cant wait to step-in and further Help such a Strategically located Country…lol Ah yes the ‘Silk road’ is Alive and Well..amigos

China has already stepped in:

“Erdogan Is Turning Turkey Into a Chinese Client State”

9-16-20

https://foreignpolicy.com/2020/09/16/erdogan-is-turning-turkey-into-a-chinese-client-state/?mc_cid=943eb0e2c2&mc_eid=d58018eddc

The BRI – Belt & Road Initiative.

1 Turkish Lira = 0.89 Chinese Yuan.

Not a huge difference there, almost 1:1.

Prescient! I think that China has every intention of ‘helping out’ Turkey, but first wants to see the Turks in a bit more desperate position.

Turkey have millions of refugees from Syria and Iraq! It must be an enormous cost and financial drain!

1) Turkey Bonds are getting better thanks to Erdogan talented family in the central bank. The front end used to be 27%, way above the 10Y, with a gump, but now full recovery ==> 1Y = 11.8% // 2Y = 13.53% // 3Y = 13.33% // 5Y = 13.63% and the 10y = 13.75%.

2) When the USD will popup, the Turkish Lira will dive further down.

3) Their mighty industrial workers have the lowest wages in Europe.

4) Turkey need gold to buy oil from Iran & Kurdistan.

5) They sell oil for profit to Europe, to enemies and friends.

6) Foreign trade is more important than blood, but if u disrespect Erdogan, , or protest against the gov, u are gone.

I like this comment, you might get 13.75% but of what, worthless Lira, I think inflation in Turkey is about 13% & the Lira loses about 20% a year, reality is at least burning ya money keeps you warm :)

“When the USD will popup, the Turkish Lira will dive further down.” You mean after pulling $5 trillion out of thin air just this year- whoopie! I can’t wait to see how strong the dollar gets when the national debt goes up another $5 trillion. This may be one reason the Chinese yuan is doing so well- we have always been told “there’s no telling how many they’ve been printing!” but no one told us the USG would be printing an extra $5 trillion either. (One question you never see asked in the MSM: “Why did there used to be a gold standard?” (” a wampum standard?” “a cowrie shell standard?” “any standard?”)

Wolf, I’d really appreciate it if you could publish a graph of the lowest debt per capita nations- I think those are the currencies I might start buying. Thanks!

Robert,

“I’d really appreciate it if you could publish a graph of the lowest debt per capita nations- I think those are the currencies I might start buying.”

The cause-and-effect relationship is the other way around: Countries that have destroyed their currencies through inflation CANNOT borrow in their currency because no one wants to lend to them. So these countries like Argentina and Venezuela etc. have very little government debt per capita (in their currency). So go ahead, buy the Argentine peso. It loses about 40% to 50% a YEAR of its value against the USD. Check this out, including the chart of the ARS to the USD:

https://wolfstreet.com/2020/08/04/why-wall-street-loves-serial-defaulter-argentina/

Iran and Turkey have lots of infantry.

1970s tanks.

Decrepit air forces and navies.

No logistical infrastructure to project and sustain power.

No, they are not. The Kurds, who are not a nation, regularly have both those countries stalemated. Israel flat out terrifies them. War takes money, and neither Turkey or Iran can afford one.

Best thing for Turkey is to get rid of Erdogan. Easier said than done though. It was a nice tolerant country at one time. Erdogan is turning it into an Islamic state.

It’s a pretty good lesson not to borrow or invest too much outside your home country as currency value might go against you.

If countries run good policies you should not need to hold precious metals, unfortunately when government is corrupt and trying to survive it’s about all that will preserve your wealth

2banan

Absolutely wrong !

Nick says, ” $15 billion of gold had to be imported from January to August, . . .”

I wonder if this is a significant enough amount to explain the recent run-up in the gold price.

So I saw this on Wikipedia:

“The EU further incentivized Turkey to agree to the deal with a promise of lessening visa restrictions for Turkish citizens and by offering the Turkish government a payment of roughly six billion euros. Of these funds, roughly three billion euros was earmarked to support Syrian refugee communities living in Turkey.”

I believe someone in Turkey is “making bank” in what could become the next big thing, warehousing migrants.

Yeah, erdogan

I am retired in Turkey, my investments are in Turkey and my money is in tl. This is a worry for me. What would be my best options as my capital is nose diving.

Rich Turks are very sophisticated. Turkey has always been a major platform of the physical Gold market.

And they own a LOT of Gold.

Physical gold.

Actually with respect to the poorer Turks they are richer than ever.

Turkey’s interest rates on their bonds of 2, 5, 10 year maturities are in the 14.1% to 14.2% range. This reminds me of the 1980’s in Canada with high inflation and GIC’s in the 12% to 14% range.

Look at this guys, imagine how a few days things can change in the interest rate game. Peter Fanza listed here Turkey’s interest rates on their bonds, 2, 5, 10 year maturities are over 14%.

Look at them today, September-25-2020, Turkey’s bonds, 2 years 13.45%, 5 years 12.95%, 10 years 13.01%. These are 1% percentage point drops in just 3 days. These are huge drops in just 3 days, for example the 10 year maturities means 11.90% total less interest total or almost 1 years less interest.

This is also simple interest not compound interest which is a huge difference and would be 37.5% less total interest in 10 years or roughly 3 years interest less. This is either the market not so worried about future inflation expectations or a massive financial intervention, manipulation from Turkey’s central bank, government.