But seeing the frenzy, the Fed has stepped away.

By Wolf Richter for WOLF STREET.

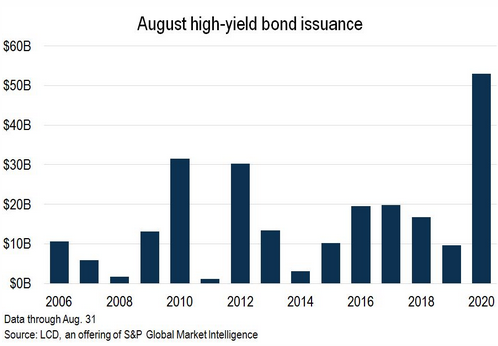

For the US junk bond market, August was the month of superlatives and records. Companies issued a total of $52.9 billion in high-yield bonds, by far the most ever for any August, which is normally a slow month, and the second highest amount for any month, behind only June, which had set the all-time record at $59.9 billion, according to S&P Global. August issuance was five times the volume of August last year, when there were already worries about the economy, a possible recession, the corporate debt overhang, and a trade war between the US and China:

Each of the past four months – May, June, July, and August – set a record in junk bond issuance for that calendar month.

Another type of record was set on August 10, when Ball Corp., an aluminum packaging company that makes things like beverage cans, sold $1.3 billion of 10-year junk bonds at a yield of 2.875%, the lowest-ever yield for a US junk bond with a maturity of five years or longer.

And there was such demand even at this low yield that Ball Corp. upped the $1 billion offering to $1.3 billion.

These bonds were rated BB+, the highest junk-bond category just below investment grade (my cheat sheet for corporate credit ratings), and therefore qualified for being purchased by the Fed’s Special Purpose Vehicle (SPV) for corporate bonds. But as of August 31, the Fed doesn’t hold any Ball Corp. bonds.

Bloomberg opined that this rally in junk bonds was triggered by two factors, “the Federal Reserve’s historic support for the market and heavy inflows into funds that buy the risky debt” – and the latter, the act of chasing yield, was a consequence of the first. It all comes down to the Fed.

“The debt deal comes amid a surge in issuance from high-yield borrowers seeking to cut interest expense on existing debt as yields approach unprecedented lows,” Bloomberg said.

Indeed, there has been a huge flow of liquidity into junk bonds, trying to find something with a noticeable yield, and so there was huge demand for new issuance of junk bonds.

The day those Ball Corp. junk bonds sold at a yield of 2.875%, so on August 10, the 10-year Treasury yield was at 0.59%, and 10-year yields of top-notch corporate bonds were also below the rate of inflation. Apple issued 10-year notes on August 20 that yielded 1.22%.

So where do you go to find a yield that beats inflation? Investors went chasing after junk bonds, hoping to be front-running the Fed that would buy these instruments by the gazillions, pay an even higher price, and allow everyone to make tons of money the easy way.

Alas, by that time, the Fed had already stopped buying corporate bond ETFs altogether – it had bought its last ETF (a measly 9,626 shares of Vanguard Intermediate-Term Corporate Bond ETF) on July 23 – and it had cut its corporate bond purchases to near nothing.

Junk bond issuance over the first eight months of 2020 – on the boom in May, June, July, and August – jumped 71% from a year ago to $292 billion, according to S&P Global. Citing projections by BofA Global Research credit strategists, it said that full-year junk-bond issuance is on track to reach $375 billion. And this “would shatter the current record total of $344.8 billion in 2012.”

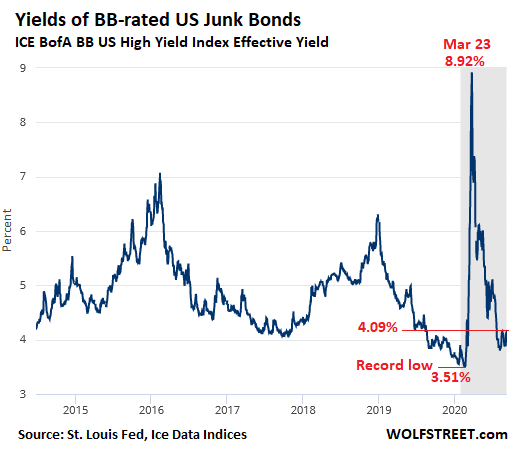

Since those heady days of early August, when the bond market was still under the illusion that the Fed would buy all these junk bonds, the average BB-rated yield – the high end of the junk-bond spectrum that qualifies for Fed purchases – has ticked up from around 3.80% on August 5 to 4.09% currently (ICE BofA BB US High Yield Index).

In mid-February, just days before all heck broke loose in the markets, the average BB-rated junk-bond yield had dropped to an all-time record low of 3.51%:

In August, secured junk bonds accounted for only 23% of total junk-bond issuance, and unsecured bonds accounted for 77%, showing what risk appetite investors have, especially when they were still hoping that the Fed would have their back.

In terms of issuance, the high-end of junk dominated, with bonds rated BB accounting for 57% of total issuance. About 19% of total issuance was rated BB/B; and 21% was rated B-, according to S&P Global.

What most issuers did (79% of total issuance in August) with part of the money raised through the bond offering is pay off existing debts, particularly leveraged loans. Leveraged loans are secured by collateral and are higher up in the capital structure than unsecured bonds. In a restructuring or bankruptcy, holders of leverage loans recover a portion of their capital, perhaps 40%, while holders of unsecured bonds may get little or nothing.

Companies that issued unsecured bonds to refinance secured leveraged loans replaced debt that is higher up in the capital structure with debt that is lower in the capital structure, a smart move by the companies because it will leave them room and collateral — when push comes to shove and investors get nervous and balk at buying unsecured debt — to issue secured debt to get out of a jam. And investors, who are now exposed to greater risks at a lower yield, went eagerly along with it.

That’s what Ball Corp did. It issued $1.3 billion in unsecured 10-year notes, used $600 million of the proceeds to pay off a secured leveraged loan, and the rest of the proceeds is for general corporate purposes. This means an increase in debt of $700 million, all at a minuscule cost of capital for a junk-rated company of 2.875%, hallelujah thank you Fed. But wait… that’s why the Fed has stepped away from the frenzy in the bond market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Which is essentially what’s happening with the stock market. Everyone is buying because they assume that everyone else will keep buying because of the supposed “fed put.” But it seems like the highs are on, as people realize that the Fed is not going to buy stocks, and not going to take rates negative.

2020-09-11-13:11!!!

Remember this date and time, when all three major indices went red, along with the infamous day 19 years past.

But, if and only if the big boys have finished unloading the SM onto the suckers on the so called retail side of that market.

SM and most if not all markets ”insiders” been doing that for eva according to what I have read about times previous to 1956, when the consequences of that activity were experienced first hand

And, simultaneously at precisely 14:00, buying on Friday afternoon comes to the DOW, SP500, and NASDAQ.

Nothing to see here. Move along.

Lisa, I don’t know how long you have been in investing, but myself has been doing so for 45 years and this is the most dangerous market I have ever seen. To think we are not putting in a generational top in stocks here is to not have studied the markets and the economy on a day to day basis for decades. How can we be setting new highs when the economy will have shrunk no less than 15% for full year 2020. You can rest assured that the Big Money is selling with both hands and two feet to those that don’t know any better than to buy companies that will not meet their debt service requirements in 2021. It starts at the top line called REVENUES and they have literally collapsed almost without exception as the economy was locked down, the dumbest move I have every seen. V-shaped recovery??? How about a bridge to nowhere.

David – my nothing to see comment was intended to be sarcastic. I totally agree with you that today’s market is the most dangerous we have ever experienced. Much worse than the Roaring Twenties, the oil crises of the 70’s, the home balloon of the mid 2000’s. No one, and I mean no one, has any idea of where this is going.

Wolf,

Do you think Fed has stepped away for good? Incase things get worse, and they will, is Fed going to come back and resume bying junk corporate bonds?

Can you point to the paragraphs in the Fed’s Charter as issued by Congress starting in 1913 and amended through legislation where they have the authority to buy any thing less than investment grade corporate debt???

They are much wiser than I thought.

If only I could form a company with my one home and float myself as junk, but I guess I might as well fly pigs since I doubt I’d make enough to pay 24.99% or whatever premium I’d have to fork out for a /DDD+ rating that would need to be created for megajunk me, sadly.

Why we put up with this state of affairs amazes me, while thinking its because most don’t read you wise Wolferines! If only all lives mattered instead of the 1%ers, but as said, pigs, or be selfish and think only of oneself and damn the rest while watching it all go to heck in a very unstraight line, sadly.

I really dislike this state of affairs but I’m glad there’s Wolf, and time.

It is my understanding, and I am open for correction, that the Fed is bound to deal only in federally backed securities.

The SPV is an “end around” that restriction, and up for much debate as to whether that is a violation.

When has the Fed ever been held to “restrictions”?

Each “emergency” expands their powers and makes more distant the mandates under which they are allowed to wield such powers.

I certainly don’t disagree with your legal interpretation, but one must ask who with any legal standing would have any incentive to stop them? Its in all parties (read politicians) current interest to keep their hands off. A crashing market/economy is not good for current incumbents regardless of whether you are a republican or democrat. And I suspect if any isolated congress people started openly questioning it you would see all types of scary scenarios portrayed to scare them into submission. Only if the tactic fails at some point will fingers be pointed.

I don’t think the Fed ever does anything “for good” except whittle down the purchasing power of the dollar :-]

So, if credit markets freeze up, the Fed might increase its purchases — but that could just be Treasury securities and MBS or it could be corporate bonds too.

The fact that the Fed has put a termination date (now extended to Dec 31, 2020) on corporate bond purchases shows that it doesn’t plan on doing this forever. This is just a crisis tool. Neither the Treasury purchases nor the MBS purchases have a termination date. But the SPVs do.

After the termination date, the Fed will either sell the securities, such as the ETFs, or hold them to maturity. All of the corporate bonds it bought have maturities of 5 years or less. Some of them have already matured and are gone now. So I expect this stuff to be off the balance sheet in a few years. But there really isn’t much on the balance sheet in terms of corporate bonds and ETFs in the first place, just $12 billion.

Wolf,

Excellent, well targeted article (as usual).

Very helpful to get the (hopefully actual) termination date of theoretical Fed corp debt backstop.

(Interesting to note that enough economic suckers/political cynics exist on institutional invt buyside to allow for sale of 5 *yr* junkish corp debt…even though Fed backstop will allegedly/hopefully end Jan 1…your thoughts, Wolf?)

Also very interesting/useful to get numbers on BB rates pre/post Fed f*ckery-pokery.

This is crucial stuff you are focusing on Wolf.

Another interesting post might consist of the highest profile corps currently falling *outside* the backstop and what their rollover financing rates/financials look like.

At least the Fed isn’t debasing the currency even more to protect the absolute sh*ttiest companies in America.

Yet.

And, in truth, it really doesn’t matter since the greatest degree of debasement is due to the continual bailout of the grotesquely incompetent Federal government…whose pathological corruption has stretched over decades, always and forever underwritten by the Fed, by means of global systematic theft from savers.

‘This is just a crisis tool’

QE1 was suppose to be a crisis tool too!

Now we arein QE4 extended version.

Anything goes ans WILL GO under the hood of ‘ global financial stability & smooth functioning of the mkts’

The Fed’s response will be to buy if it starts turning south. The Fed’s very existence depends on playing it to the bone. Near zero interest rates continue to inflate the bond bubble.

Maybe DD, but IMO only until 4Nov2020; after that, and assuming the pals of the FED have done their work to CYA, it is very likely all the printing comes to a full stop, while the insiders go short and let the punters take their medicine for daring to try to swim with the big boys.

Six months or so after that, the carnage will start to become much more clear to us Peedons, and we can start to put the pieces of our pies back together.

Meanwhile folks, ”keep your powder dry.”

After the election will be a perfect time for asset price deflation to emerge with an austerity policy. The big boys want a strong dollar with deflationary conditions. They have been loading up with covid bucks for just this event.

Dr. Doom

Can you explain why will anyone want to buy bonds at near zero interest rate? I can’t.

Low interest is exactly why I’m not a bond customer.

Would 0% be ideal because its so low?

Simple , because they expect that rates will turn negative

On 2/28/20 real Treasury yields for 10 year Treasuries

we’re 0%. Today the same yields were -(1.01)%.

I get it!

The perfect financial product for those that just have too damn much money.

Bonds are no longer investment, but charity. Who are these suckers?

In my small world I see no point in bonds. Arbritage by large holders however can exploit any differential or margin that would be useless for me.

What else are you going to buy?

With 0% bonds you are losing 2% loss per year to inflation, but with stocks or metals you are exposing yourself to a potential (and quite probably) >50% loss within a short period. Many funds and individuals simply cannot afford that kind of risk.

Pick your poison, but personally at this stage I prefer that 0% bond.

We’re talking about junk bonds here… unsecured junk bonds at that… investors will lose as much on those as stock holders lol

Fair enough, but do you really think metals (what are you referring to here? Gold and silver?) would fall that much? I seriously doubt it, and they’re a more straight forward long-term inflation hedge.

Metals may not have a theoretical ROI, but they cannot be printed, giving them an advantage over fiat, and compared to stocks at least they can’t have sudden or prolonged losses in revenue or go bankrupt. The only downside is how the govt taxes them, but still an excellent treading water long-term investment for desperate investors trying to protect their savings.

@GotCollateral:

Sure, that’s what the OP is about. But I was reacting to Ralph Hiesey’s post where he refers to 0% yielding bonds, which I assumed he meant to be investment grade / Treasuries (all yielding slightly above 0%).

Regarding unsecured junk bonds at 3.xx% I totally agree with you.

@rhodium

Gold and silver are not a good practical inflation hedge. Just check the last decennium: gold has moved roughly between $1000 and $2000 in both directions. That is much more variation than the thing you are trying to hedge. Silver is even worse.

It made sense until the end of Bretton-woods when we were essentially on a gold standard that could be devaluated against. After that, there was a massive rise for about 10 years and then a collapse that lasted 20 years, followed by a 10 year recovery, basically hedging nothing for 30 years. Even at today’s record high gold has massively underperformed bonds for the 40 years since ~1980, which is essentially a lifetime of investment. So it is hard to argue that gold is a viable inflation hedge.

Don’t get me wrong: I do see the case for gold. The most important being the lack of counterparty risk.

I can also see the case for a revival of gold as an alternative currency. However, this is all just speculation and in that sense no different than any speculation in certain stocks that you believe are going to be successful in the future. At this moment I see it as all part of the same bubble.

If anything, the gold price is probably more correlating with real interest rates than with inflation. That would make sense because it lowers the carry cost of gold. Current situation (priced in already?) seems a goldilocks situation for gold, with even junkbonds yields only just above inflation. But I don’t expect that to last. With unsustainable debt everywhere one would expect real interest rates to go up once the economy shows some recovery. Then you could easily see the goldprice cut in half again, as happened between 2011 and 2016.

@YuShan RE: IG

Yeah, well even with $ denom IG, 97.5% of it is unsecured, with 46% of it rated BBB with nearly 35% of the notional dated 10 years or more in just ~6% of the companies companies ( ~33% of the ~6% are banks, and look how good they have been historically with accurately predicting reasonable loan loss reserves… lol), and all them with severely dampened cash flows for the foreseeable future as long as they keep increasing their debt with no top line growth (or even contraction)… Junk all in but name only lol

I rather lose 100bps on inflation over a decade than +1000bps in a year trying to chase this trash…

But sure if someone wants to chase citigroup US172967EW71 S-NT paper at +177… be my guest lol

But what’s wrong with your mattress? it also also pays 0%.

Sounds like the equivalent of getting an unsecured loan to pay off a mortgage so when I default they can’t take the house. Where do I get one of these in UK please? Or am I just not understanding right?

Thanks for the recs for political news, phoenix and Oji.

They have some. Wells Fargo wants 24.99 percent interest on an unsecured line of credit. No low interest rates for Junk rated human beings.

My reply above should have been here. Sorry.

Unless politicians get involved.

See the GM bankruptcy for an recent example on how secured “first in line” bondholders got destroyed so that certain unsecured favored creditors could be made whole.

“In a restructuring or bankruptcy, holders of leverage loans recover a portion of their capital, perhaps 40%, while holders of unsecured bonds may get little or nothing.”

“See the GM bankruptcy”

Never, ever, forget that premier example of Feds true commitment to rule of law…

Between that and twenty years of ZIRP, it is pretty hard to think of DC as anything other than an incipient third world sh*thole.

I think the 1933 confiscation of gold at $20.67 an ounce, and the subsequent revaluation at $35 an ounce in 1934, and then using the profits to create a slush fund to allow the US to intervene in the currency market, all qualify as even worse things that the US government has done in a time of economic crisis.

https://en.wikipedia.org/wiki/Executive_Order_6102

The precedent has been set for the US government to do pretty much whatever it *wants* to do to private property. “Law” is just another word for the whim of the federal government at any given moment in time.

If you know of a clear article on how the BK was structured please provide the title. I’ve read articles; a whole lot of generalities without specifics.

I agree that junk bonds are risky and referred to junk for a reason.

However, I use Ball canning jars to can my garden vegetables and Ball Aerospace makes military satellites so is fairly secure (and hiring like crazy).

Ball stock is currently 5% higher than Pre-Covid highs. That makes sense since they are in the survivalist canning business and the military aerospace business.

Maybe that’s why they could sell bonds at such a low rate?

Ball is consolidating debt at a low rate. Like I’m doing with my refi.

It would be more like a cash-out refi, where you refinance your $600k mortgage and cash out $700k on top of it, and where the $1.3 million mortgage exceeds the value of your home by a huge amount.

But in reality, you cannot compare corporate debt to a home mortgage.

I’d like to do that, and then I’d take the money and “invest” it into the stock market, I heard that has better odds than Vegas….

Too bad, nobody would let me, cause if I can’t repay that loan, will just declare bankruptcy, what’s the bank going to do, take the house… ha ha ha ha.

Too bad reality is set up differently where governments and companies can do this sort of things, ordinary suckers… I mean people, can’t.

Shareholders are paying the CEO $25M to produce an earnings yield of 1.3%

If they are doing so well financially with canning jars flying off the shelf since no one ever gets sick from canning their own food and a new spy satellite is being sent into space weekly, WHY IN THE WORLD ARE THEIR BONDS BEING RATED AS JUNK, JUNK, JUNK. TOO MUCH DEBT, DEBT, DEBT IN RELATION TO SALES, PROFITS, CASHFLOW, ANNUAL DEBT SERVICE REQUIREMENTS …… ON AND ON AND ON. Someone in the rating agencies is looking at their true financial condition and not relying on the Wall Street media hype.

“Maybe that’s why they could sell bonds at such a low rate?”

Wolf’s chart on pre/post Fed backstop rates for BB debt index (made up of many companies) pretty much proves the opposite.

The correlation in time is too neat.

“Free market capitalism, efficiently allocating precious capital”.

LOL…..

This will not end well.

At all.

Wolf, the last 2-3 days we are seeing VIX lower while stocks trade lower. Like now VIX is down 10% as I write.

I suspect this is the flip-side of the manic call buying you wrote about.

Wonder if same self-reinforcing loop will work on the downside now.

The VIX is now a main street indicator of general market health to the maddening crowd, and could someone like Blackstone or the Goldman Squid or Morgan be selling it short to depress its price to keep the Sheeple buying stocks and bonds with wild abandon??? But in a democracy we have free and efficient and fair capital markets, right?? No longer.

That’s cuz Trump & co are shorting the VIX heavily & the Dollar to stop a collapse, every time you see market fall they go in heavy & flood the VIX with shorting & the Dollar to, watch it close, when this unwinds & they get blown out the VIX will hit the moon, the amount of short positions in the VIX are now massive, that is why you see an abornal fall in the VIX, they get scared they will lose the elction & flood both especially the VIX with massive shorting, the calls are now collapsing in volume, puts are rising, the VIX would have to off had it not been for the massive shorting, all it does is surpress the VIX like a spring & they will lose control, that VIX will go through the roof shortly and blow the whole stock market to pieces, same with the Dollar, both will explode higher than Feb to March.

Andy,

So that would be a result of something rather than a cause.

If call options expire worthless, the call writer can sell the underlying stocks because the hedge is no longer needed. So that would be the opposite of what we had in August.

Also, I think there is now more balance between calls and puts, as lots of investors have jumped in with bearish bets over the past few days. And that could impact the Vix.

ITM option skew on SPY chains from now to 6 weeks out still skewed +500k ITM calls near the 334, though down from about +1.4M ITM calls from the 340-350 strike…

Still plenty of +gamma to unwind, but yes, more balanced.

Different story with the QQQ’s, that flipped to -gamma now but just barely at the 270.5 strike with +5k ITM put skew from now to 6 weeks out. This is pretty much balanced now.

Once again proving that the low rate of interest is forcing investors to gamble on companies that should be compelled to use bankruptcy to resolve their debt issues instead of being bailed out.

Prudent savers are penalized as their funds lose value thru asset inflation and increased taxation and taxpayers are stripped of their buying power to pay off the debt incurred in bailing out zombie entities.

I honestly believe that, if they had to “help” consumers, instead of sending everyone a check in the mail the Federal gov’t would have benefited more by just giving taxpayers a $1200 deduction on this years taxes. But that wouldn’t have looked quite as good at voting time.

“Here, take this check and spend it. Just ignore the $21,000 in Federal debt we just tacked onto your tax burden.”

I say we all get together and launch a Class Action Lawsuit against the Fed for robbing us of Trillions of Dollars of lost interest income in our bank accounts, money markets, and savings accounts (dead asset class the latter) when the true inflation rate over the last 12 years since 2008 has been over 5% on average, not the ridiculous 2% the Fed is pining for without a scientific or financial reason why that is a Magic Level of Inflation.

If you do that, the Fed will simply print Trillions of dollars to compensate you.

Either way the Fed prints money.

It’s pretty great actually to be the Fed.

If an institution can not be held to account, it’s probably better to just abolish it.

“launch a Class Action Lawsuit”

1) No judge in the the US would ever rule fairly in such a case. The Feds would exert every conceivable form of pressure (up to and including murder) to prevent an adverse ruling.

Without the unquestionable “right” to print money, DC/meth addicted US economy would collapse in ruin within a month.

DC will commit murder to prevent that.

An entity that has stolen tens of trillions to prop up its grotesquely incompetent power, won’t stop at murder.

2) The best we can hope for at this late date is for an ever wider circle of better informed people, who will form the basis of an infinitely healthier post-DC based economy, using a currency based upon something/anything more reliable than the “word” of a sociopathic political class.

Just came from Home Depot, I paid $3.33 in March for a 2x4x96.

Exactly same 2×4 is $6.27 today.

That’s almost 90% increase.

But remember, the official inflation rate, esp. for giving Social Security cost of living increases! is around 1.3%! Me smells something rotten in Denmark. Don’t measure the actual dimensions of that 2×4 or you will really get mad.

The 2 X 4 has never been 2 X 4 and has never changed in at least the last 50 years.

Couple things re 2x4x8 @ $6.27:

1. Buy it as soon as you can mm, cause they are going way up with today’s commodity mkt close being an all time record, having more than doubled this year.

2. for nk: 2x4s used to be not only that but frequently more, ”back in the days” when used rough or mill run; I have taken apart old houses in SF Bay area with studs ranging from 2.0 to 2.5 inches thick, 3.75 to 4.5 wide IN THE SAME HOUSE! Walls were made flat with the plaster being from 5/8 to 1.25 inches thick between the scratch, brown, and finish coats, mostly in the scratch coat, when a six or seven foot darby was used to level the wet mud.

3. NOW a days, the 2×4 is a nominal measure of the rough cut, and then the piece is planed to be exactly 1.5×3.5, with slightly rounded edges for safety, and the gypsum board is exactly 1/2 inch or 5/8 inch. There was an attempt to make USA lumber fit metric sizes a while ago (decades?) but it didn’t fly any more than trying to make everything here metric; apparently, if it was good enough for King John in 1215 or whenever, it is good enough for USA…

You can still buy rough cut that is 2×4, but most places it is now special order, and with the interruptions of the supply chains might take months to be delivered.

Then the houses you took apart were at least 100 years old. Can you imagine the language if 2 x 4 ‘s with that variation were shipped to a site fifty years ago? The house I’m in was built in 1928.

My nephew has a mill specialized in those super thick slabs that are ‘in’ for tables. I’m in central Vancouver Island where small mills are everywhere and will saw whatever you want. I’m talking, obviously, about going into a large retail lumber yard 50 years ago as I was doing 50 years ago and where it was what it is today: 1.5 x 3.5. The guy I was replying to was implying the practice of shrinking the portion. Common, but not in the 2×4.

Carpenter here. Did someone mention wood?

Seriously, global market so prices on the rise everywhere…even here on Vancouver Island. Forestry is frickin’ booming here. Booming.

I will say this, $6 a stud is way too high. Maybe 4 something, but not $6 plus.

It will go higher with RE still rising and burned structures to replace.

I bought some BBB rated bonds before the pandemic at a YTM of 5-6%. They went up in value. The S&P 500 dividend yield is higher than the 30 yr treasury yield. I hold shares in a fund invested in that index. I would not invest in antiques, gems or art as I do not know those markets. Someone who knows pearls might make a fortune investing in them. To me they are useless.

Yes, Mr. Hall, but when a currency fails as the debt drowning Dollar is destined to do, even a loaf of bread holds its value longer than the stinking Greenback. Read the book, “When Money Dies”. About hyperinflation in post-WWI Germany which set the stage for the rise of Nazism and Hitler. In times of currency collapses, tangible goods such as those pearls become more valuable as the currency they are traded in hits the skids.

Ball is an interesting subject, a minor consumer product maker, a major DOD player? Not hard to imagine an economy with fewer consumer products, and more baseline security industries. Congress never cuts off funds for military spending, NEVER.

This isn’t grandma’s ball jar, doe. This is an essential, mission-critical food service and satellite delivery platform operating globally in a highly competitive inter-galactic market.

I wonder how many companies are issuing debt to buy back their own shares?

If it’s not happening now, it will begin again soon. Except for the banks, I don’t think the Fed cares what the companies use their debt issuances for.

The Fed absolutely cares how those issuances are used. For investment, it’s a big no no. For share buybacks? 100% support from the Fed.

But buybacks are good for shareholders because of the favorable capital-gains tax treatment which is all under the Fed’s control.

If buybacks are good for shareholders, why don’t the company simply buy back every share?

No, buybacks at these crazy high prices are NOT good for shareholders! They are good for management with stockoptions and other pay that is linked to the share price.

The company ends up with even more leverage and even higher vulnerability in the next downturn, which could mean a total wipe-out of the shareholder. Of course the management still keeps their millions.

Their ultimate goal is to take the company private, usually at a premium. Your company is worth trillions all held by “other” people, in the form of public shares. You buy them back at zero cost to you, Borrow a dollar to buy a dollar, and retire those shares. You rob shareholders of their equity. They bid up prices until shareholders cough up their shares. The float shrinks, the company pays off the remaining investors, who no longer have an investment. There is no stock market left, and the government nationalizes their output. It all comes about after the Fed cannot regulate debt, or zero interest policy. What has happened to the banks, then happens to the entire market.

The Fed may have stepped away for now, but NO-ONE believes the Fed won’t step in to bail them all if the stuff hits the fan. And they have good reason to believe that. 30 million un-employed, not the Fed’s problem. But if hedge funds and banks start taking a hit, the Fed’ll step back in. That’s what’s keeping the junk bond’s going.

Punish the little guy with zero to negative interest rates at his meager savings and make sure the big boy have access to 0% financing.

No, the Fed has absolutely nothing to do with the widening of inequality in this country.

If you took your marbles home and didn’t play, maybe they would be worth more.

In what parallel universe is a junk bond yielding 3%. I wouldn’t consider a junk bond yielding 3% in a perfect economy, in this economy 25% is not enough. They call them junk bonds for a reason.

I think in a universe where the Fed is the guarantor. At least for certain holders of them.

OK, we have entered another dimension….the twilight zone.

1) Remember 9/11/2001 ?

2) SPX Sep 2001 plunge was stopped by the July (H)/ Oct (L) 1998 TR.

3) That Trading Range (TR) was SPX backbone for the next 13.5 years, until Dec 2011.

4) For 7 months SPX tried to breach the July 1998(H) resistance line, but it was a thud.

5) SPX collapsed util the 2002/2003 lows and reached Oct 2007(H).

6) Hopefully the 1998 TR is ancient history.

The movement of the Fed to MMT is nothing new. It is just that the policy now has a name in academia and places like this website. Neither party seems to seriously care about the debasement of the US dollar. I think this will all blow to hell. The confidence game is going strong in 2020. It will not continue forever. Powell knows it and is trying to keep the game going any way he can, however absurd the means he must use. The number of people in the USA and elsewhere who believe the dollar is a sham will only grow.

Confidence? I just listened to a podcast on the upcoming election. These guys were discussing investment strategies for the possibility that both sides would claim victory. Really? I can’t believe they expect markets to remain open in that s***show.

I bought May 2021 80 puts on HYG today for $3.25, This seems like a pretty cheap price. By contrast, the February 140 puts $10 out of the money on IWM were $7.

The market is pretty docile on junk bonds. My take is that between now and May, something is going to happen. Not sure what the significance of GDP growth is when you have a $3 trillion deficit, but 29 million people are on assistance, not counting welfare.

We’re in a depression, Bonds are going to default.

I agree… great place to build up a tail risk post if you can keep rolling it over. In HYG, 91.7% of the bonds do not have any collateral, 46.6% are rate B or below. Much cheaper than trying to do the same on equity despite equity being lower on the capital tier (even though unsecured HY is pretty much similar to equity).

Even worse statistics on the underlying than going into march.

Corp credit Bond is the foundation upon which Equity mkt is built up.

Once the credit bond gets a seizure, it is a just matter of time if will affect the equity mkt. Think of Bear Sterns and Lehman, 2008.

50% of grade bond ( LQD) are junk bonds of varying grade including HYG and JNK.

Right now HYG is around 85 and was at 68 on March 23rd. It is within 0.5% of it’d 52wk high.

Once it slide below 80, Fed will intervene. Or else both LQD and JNK get affected fast tightening liquidity.

So Fed will jump in, unless they want Mkts to slide more than in March.

Mr. Powell is not only a hypocrite but also intellectually dishonest just like any other politician in DC.

sunny129,

You need to look at a long-term chart of HYG that goes back to 2007. You will see that after each bond-market blowup, when there were lots of defaults and bankruptcies — 2008-2009 (Financial Crisis) and 2015-2016 (Oil Bust 1) — HYG dropped sharply due to the bonds becoming worthless or getting haircuts, and then bounced back, but never got back to its prior highs:

High 2007: $106

High 2014: $95

High 2020: $88

So now, the new defaults are coming in, and all this takes a while, so I expect next year’s high of HYG to be below $80. And that would fit the pattern.

You may be right.

But as I am saying CREDIT mkt is the foundation upon which Equity mkt is built!

With SPV relief funds out there, once the HYG slips below, Fed will there to rescue, unless they are willing to let Mkts slide more than in March. Wait & see.

1) In July 29 US saving account in the Fed was : $1.817T and now it’s

$1.611T, or minus $206B within a month.

2) In Aug, QQQ jumped over the July 13(H) to a new all time high, and

now QQQ is back inside the previous box. It’s a normal correction, even if QQQ will dive slightly lower.

3) This type of spending before election can be tolerated, but beyond Jan

2021 it must stop.

4) Some kind of unexpected and unpredicted events, can affect US, or

her good friends, beyond mid Sept .

@Michael Engel

‘Some kind of unexpected and unpredicted events…’

It has to come outside USA which Fed cannot influence, easily (with dollar swaps like etc) like a major global Bank/conglomerate failure.

Covid is NOT going away after election or even after Dec 2020.

More significant credit events ahead!

‘

Fed policy has promoted yield chasing and desperation investing.

Which the Fed will be called on to support the effects of those desperations with stimulus, etc.

They couldn’t prevent dot.com bust in 2000 or Housing bust in 2008 just postponed the SAME problems with insane CREDIT creation for the last 11 years.

But Covid 19 was unexpected and has a triggered an even they cannot kick beyond Dec 2020! Until then they will continue their circus of ‘EXTEND & PRETEND”

“So where do you go to find a yield that beats inflation?”

I’ve said it before and and I’ll say it again: look at Japanese companies.

Good, solid companies with real earnings, lots of cash on the books, trading at low PBR ratios, and many of them even have yields of around 4%. The exchange rate risk is, of course, one of the problems, but that can be hedged.

And if you really want to get some high yields on non-Japanese companies you can take a look at Australian bank shares. The big daddy of banks, Commonwealth, pays around 4.5%. Risky? Maybe – maybe not.

The Reserve Bank of Australia has earmarked A$200 billion for the commercial banks here to borrow at a rate of 0.25%.

The banks promptly cut the rates they pay to savers even lower, but zero changes to variable rate mortgages. Banks here have to be making huge profits off of loans that are being serviced, but this will be somewhat offset by any defaults mainly in the commerical areas. So once gain those with variable rate mortgages are filling up the banks’ profit centers as others mount up losses.

Don’t know what is going to happen here in Oz with the lockdown/curfew going on in Victoria and the requirements needed to be met for a lifting of restrictions which are so strict that it appears that pubs/restaurants will not open this year.

Many other activities have been hit as well such as visits to GP’s, routine health tests, ER visits, people can’t get drivers license tests so no new drivers around the city, and public transport use is down some 91% compared to normal.

Still no travel allowed between states as borders are closed except for ‘special’ people such as singers and athletes. Want to visit you dying dad in Queensland? Forget it, as the politicians in Queensland have said it doesn’t involve money for the state.

Real estate sales in my postcode have basically crashed with few properties being listed for sale and even fewer selling. Those that show up as ‘sold’ were listed and went through escrow and paperwork months ago as the standard closing time here is about 3 months (except for cash sales which seem to list and sell within a week and close in about a month).

With all this subdued economic activity the deficits at the State level from a huge reduction in state revenues from lower RE activity and huge payments to everybody and a lower than expected share of goods and service tax from the Federal government are going to soar.

The Federal deficit for the year is going to be around 15 to 20% of GDP which is a huge number.

It appears that the international markets are totally unaware of this data. Australia has gone from a country with virtually no government debt when John Howard left office in 2007 to a country that should be rated as a junk borrower now.

Our postcode currently has zero active cases of the CCP virus and that is down from a total of two at the start of August. Total cases during this entire ‘virus crisis’ number 60 which works out to a rate of .001 or less depending on the current population numbers.

And it stil amazes me that 135 years ago people were able to send letters and postcards between Europe and the middle of nowhere in Australia in a period of 35 days without the use of planes.

Fast forward to 2020 and it takes a letter 12 days to get from Melbourne to Sydney, packages that need to go 400 kilometers are being sent on a 2500 kilometer trip around Australia before being delivered 15 to 30 days later and postal services between many countries have stopped.

And where there is service, it takes so long that businesses are refusing to ship overseas anyway. None of these impacts has been factored into the future business and social costs and impacts of the curent ridiculous restrictions in place in many countries.

Hi Lee

Watch the ‘Walk The World’ You tube channel by Martin North. A guy from your neck of the woods.

It’s getting grim for you guys pretty fast.

But the honest truth is, it is for us all. It’s just that the data from australia is more readily available than for many other places.

Stay as safe as you can.

It’s no surprise to me. After years of screaming about the debt in the aftermath of the GFC, we don’t hear a word about $7 trillion of debt from the very same people who did the screaming about a debt that was an order of magnitude less than their own contribution.

Most of that money went towards paying for the slime that now feeds on government giveaways such as think tanks, contractors and advisors.

The same thing goes for ex-PMs. They hounded three labor prime ministers out of office, then once they got into government they hounded three of their own PMs out of office. Simply because their donors in the coal industry forced them to in order to defeat any and all climate legislation. Australia has been a joke ever since.

They are the worst government in Australia’s history

The New Billionaires will all be JUNK BOND KINGS.

Financed by the FED of course.

I’m old but was hoping to leave something to my grandkids.

It’s beginning to look like I’ll be lucky to take care of myself

for the few years I’ve got left. Not an ideal state of mind in

ones retirement.

The whole situation is really ridiculous. A central bank is supposed to promote a stable financial system.

Instead of promoting junk debt issuance for stock buybacks and such, they should be pushing companies to take advantage of the euphoria and record high stockmarket to issue stock instead of even more debt.

This especially because government deficit isn’t going to disappear anytime soon because of stimulus and decreased tax revenue. To keep this game going for as long as possible, they should increase the capacity of the economy to absorb the increase in government debt. So ideally you would like corporations to issue stock to replace much of their debt so they can survive the downturn without government help and create capacity in the bondmarket for absorption of more government debt, which is unavoidable at this stage.

That would dilute outstanding stock and reduce stock prices. In turn this would adversely affect bonuses tied to stock prices. Furthermore it would adversely affect the value of company stock options and grants to employees. Can’t have that. Stock prices are about today, debt is about sometime tomorrow.

YuShan,

“A central bank is supposed to promote a stable financial system.”

That’s what they say. But the reality is that the purpose of a central bank is to fund wars.

Low rates imply a higher grade of debt. A junk bond at subnormal yields is not junk. The real junk is US treasuries, where the deficit is off the charts. No one has done a study of what Covid is doing to tax revenues? If Treasury bond vigilantes have a counterpart, it is corporate bond buyers. By implication they raise the quality of corporate debt, pushing the implied interest rates on Treasuries to NIRP levels. Sub zero rates imply loss of dollar purchasing power, which we see in stock market asset inflation. Then the huge corporate tax cuts, which are political policy to destroy big government. Drunkenmiller laments the commingling of Fed and Treasury since Covid. Ya think so? Should Treasury rates rise those corporate bonds are even “less” junky than before. Corporations have found an off balance sheet source of finance which can never be traced back to them. When the going gets tough American corporations go Multinational, with the blessing of US corporate libertarians. SHTF when American workers have to compete globally.

‘Corporations have found an off balance sheet source of finance which can never be traced back to them’

!?

Flash back to the days of Enron and it’s auditor Anderson!