SPVs to nowhere.

By Wolf Richter for WOLF STREET.

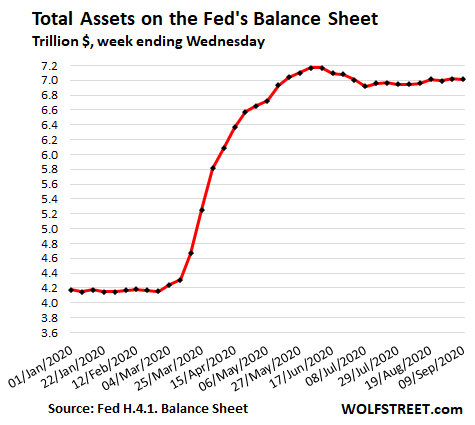

Total assets on the Fed’s balance sheet for the week ended September 9, released this afternoon, fell by $7 billion from the prior week, to $7.01 trillion. Since the peak on June 10, total assets have declined by $158 billion:

The Fed has numerous asset accounts on its balance sheet that are unrelated to QE. Some of them fluctuate from week to week. Others, such as its holdings of gold or SDRs (IMF’s Special Drawing Rights) do not fluctuate. But to see where the Fed is going with QE, we look at the five major QE-related categories on the Fed’s balance sheet: Repurchase Agreements (repos), Special Purpose Vehicles (SPVs), central bank liquidity swaps, mortgage-backed securities (MBS), and Treasury securities. In total, balances of the five categories combined fell by $11 billion on today’s balance sheet compared to last week:

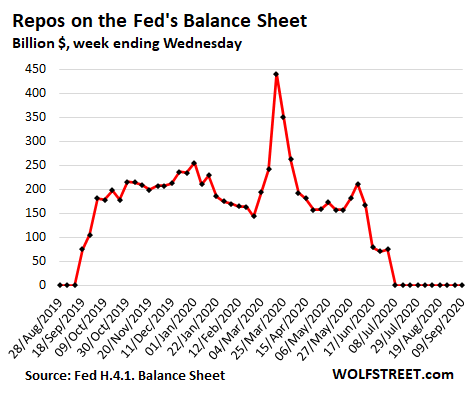

- Repos: unchanged (at $0)

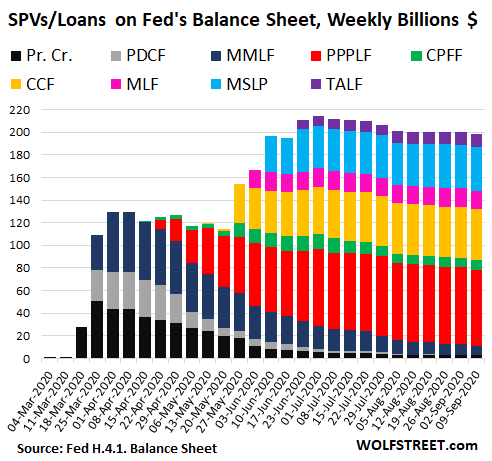

- SPVs: -$2 billion

- Central Bank Liquidity Swaps: -$17 billion

- MBS: unchanged

- Treasury securities: + $7 billion

Repos: at $0 for the 10th week:

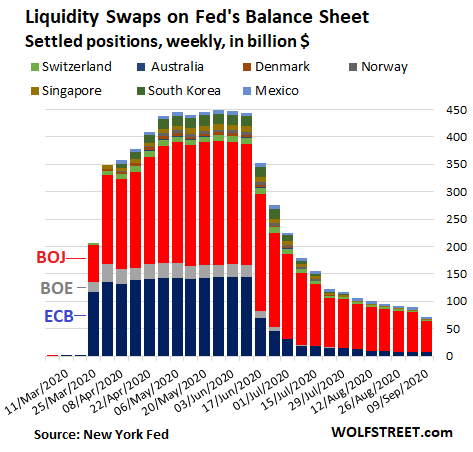

Central-bank dollar liquidity-swaps: -$17 billion.

The Fed provided dollars to a few other central banks with these swap lines, but they are falling out of use and balances declined by $17 billion during the week, to $72 billion, from a peak of $449 billion in May. The Bank of Japan accounts for 79% ($56 billion) of the remaining total. Swaps with the ECB fell to $6.5 billion. Swaps with the Bank of Mexico have been at $4.9 billion since July. The central banks of Switzerland, Singapore, and Denmark had small balances left. The rest are gone:

SPVs: -$2 billion, to $198 billion; -$16 billion since July 1.

The Treasury Department provides the equity capital to the SPVs, and the Fed lends to them. The SPVs then buy assets. The amounts shown on the Fed’s balance sheet include the loans the Fed made to the SPVs and the equity capital contributed by the US Treasury:

- PDCF: Primary Dealer Credit Facility

- MMLF: Money Market Mutual Fund Liquidity Facility

- PPPLF: Paycheck Protection Program Liquidity Facility, with which the Fed buys PPP loans from banks

- CPFF: Commercial Paper Funding Facility

- CCF: Corporate Credit Facilities: Buy corporate bonds, bond ETFs, and corporate loans.

- MSLP: Main Street Lending Program

- MLF: Municipal Liquidity Facility

- TALF: Term Asset-Backed Securities Loan Facility

SPVs to nowhere.

For example, the CCF (yellow) with which the Fed buys corporate bonds and bond ETFs, is showing a balance so of $44.8 billion, essentially unchanged for weeks. On September 9, the Fed disclosed that it had bought not a single ETF in August, and that ETF balances actually ticked down, and that its balance of corporate bonds edged up by only $435 million with an M.

This is an indication that the Fed has essentially stepped away from the corporate bond market. Its total holdings of corporate bonds and bond ETFs amounted to $12.7 billion at the end of August. The remaining funds in the CCF account are unused.

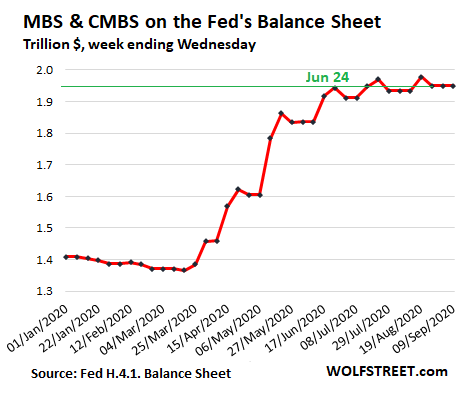

MBS: unchanged at $1.95 trillion, level with June 24.

The balance of MBS shows an erratic pattern due to two factors that push it in opposite directions: One, holders of MBS receive pass-through principal payments when mortgages are paid off, and in today’s refinancing boom, this torrent of principal payments reduces the MBS balance by large amounts every month. And two, the Fed’s MBS purchases take 1-3 months to settle, which is when the Fed books the trades.

Since June 24, the Fed’s MBS balance has essentially remained flat at $1.95 trillion, as the Fed’s purchases just replaced the declines from the pass-through principal payments:

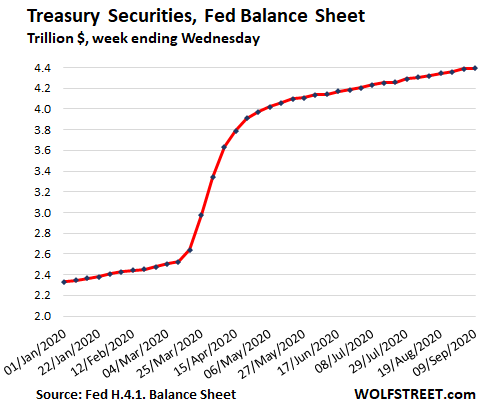

Treasury securities: +$7 billion, to $4.39 trillion.

Since late May, the Fed has increased its Treasury holdings at an average pace of $14 billion a week. This is the net of purchases minus maturing securities that the Treasury Dept. redeems. This week’s increase of $7 billion was within but at the low end of the range:

So it seems the Fed has pulled back from bond-buying. Its Treasury purchases would amount to QE of similar magnitude as seen during QE-3. But the government is issuing so much debt so rapidly to raise the funds for is various stimulus efforts – counted in the trillions – that the Fed is essentially just funding a slice of that spending by buying Treasuries. And that seems to be a signal that the Fed is letting the markets fend for themselves for now. How does that old saw go? Don’t fight the Fed?

There is still a lot of fawning coverage of the Fed in the media, but big dissenters are now given prominent spots, and loaded questions are used to politely hammer Jerome Powell into telling obvious nonsense. Read… Have You Noticed How Push-Back Against Powell-Fed’s Actions Is Getting Louder in the Mainstream Media, from NPR to CNBC?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

They’ll come in after -30%, maybe -40% this time because it’s marched so much higher since March? I’m sure the PPT is watching it very closely. :)

I doubt we’ll see a fall-off-the-cliff just yet but the top I do have a feeling may have been reached, both for NASDAQ and the Dow Jones, although I could be wrong. What the market IMO has NOT priced in yet is:

1. Second wave of lockdowns (despite what some might think, I will maintain that this is still probable, cold weather and viruses are very good buddies )

2. Financial crisis precipitated by knock-on effects like missed RE, CC payments causing bank defaults, credit crunch etc.

Either one of these IMO has the potential to deliver a knock-out punch which can cause the markets to make new lows. I also wouldn’t rule out military conflict between Iran-Israel in the ME or China-US in the South Pacific or both, if not before the elections, then after.

A second lockdown is possible, but, I see no particular reason war will break out this year, especially, with Irran, who is suffering quite alot from CCP-19, but, has to cover it up in order to get that new oil contact with China. Near China it’s also unlikely right now, because, the Chinese are going to be hesitant to do any big moves, they might try to do small moves, but, physical confrontation is unlikely, especially in the coming months. The attempted overthrrow of Xi is the biggest risk factor in that whole situation. If anything physical happens it will be on the India China border. That’s the bigger powder keg right now.

As for that second lockdown, every state is doing it’s own thing, so some probably will, others no. We will likely see actual tested vaccines being injected into people in January, healthcare workers and politicians (unfortunately) will likely be first and then the general public rollouts would begins in phases. Because, many have adapted to work at home and that end date is in sight, I don’t expect many lockdowns. Measured additional restrictions in certain states is most likely. As always anything can happen (we have to remember we moved over into the Twilight Zone some time ago), the more money given out, the more likely lockdowns are, as well as, if a major outbreak happens.

Yo, Wolf, hope yer well. For some reason I though of you during the Black Orange day that was yesterday. Kyushu dodged the big storm.

A second lockdown is extremely unlikely. People are still isolating in unprecedented ways and workplaces and socializing is a fraction of what it is normally.

Or, ahem, make it a great time for a wolf short…

“And that seems to be a signal that the Fed is letting the markets fend for themselves for now. How does that old saw go? Don’t fight the Fed?”

Fed intervention so close to an election is unlikely.The biggest fear of the Fed,of which there are very few,is the appearance of being political.

Entire market hinges on Russell 2000. It’s like on the edge which way to go. Long story short. It crashes.

The thing to worry about is the weak economy and the lack of adequate stimulus. We need 2t now and that may not last until January. It now looks like zero or a couple hundred billion if we’re lucky and quite possibly nothing until after inauguration.

The Fed may aid asset prices but it can’t drive the economy.

I’ll bet that I’m not the only market participant to see it. No stimulus no economy.

In that case the fed will be powerless.

Peloton putting up great numbers makes me think that the economy is decent for people with assets.

Wealth effect?

Coworkers have those bikes. *Huge* markup, ongoing revenue stream via subscription service, and everyone is stuck at home looking to exercise.

Easy to duplicate idea but no one has done it well.

Exercise equipment is selling heavily.

When was the last time the “market” was correlated to the REAL economy?

The “market” IMO is only driven by interest rates (bond prices), buy backs and sentiment. And the PPT, in case it is going down 3%.

Time to take a community approach to common law and look after each other locally by democratic vote. Issue a local currency and take back sanity and peace. To see where the FED is going one only has to close the eyes.

Issue local currency?

Backed by exactly what?

Or do you mean create thousands of new fiat currencies…

I would assume by local currency he isn’t talking about everyone creating a bit/fiat replacement. Just local credit unions based on local deposits and local tax revenues. People would be forced to spend based on what they have, not what the Fed manipulates into the system. I could be wrong though, and he could be talkin about that stupid bit garbage. But I would like to see more accurate spending from more accurate spenders. Not wall street and the Fed, that farce is up.

Bartering; assets and skills were money before fiat creation, like trading gold, silver and manual labor- the most basic skill.

Ellen Brown has several solutions including state run banks which can borrow from the Fed directly. The central bank system has nullified itself, greater numbers of people are falling out of the tax system. Covid will pretty much shut the door on the IRS..

9 milli metre or 7.62 by 51 millimetre community approach?

I suppose that may result in a silence of sorts, eventually.

You see, once people start to ‘take things back’, democratic voting can become simply a pesky inconvenience. Just gets in the way making people do what conviction and their guns think is right…

Isnt that what we have now?

Powell on interest rates at the NPR interview on Sept 4th:

“…And the reason is, you know, there’s some economics behind what sets an interest rate. There’s a real return and there’s an expectation about inflation in every interest rate. So if you go back and look at the U.S. Treasury, it would have been yielding 5 or 6% 40 years ago. And now the 10 year treasury is yielding less than 1%. And now why is that? And one of the reasons is that people expect inflation to be much lower. And also the level of savings that people as the population has aged, they create a lot of savings. And when people invest, that means they drive down interest rates. So that also means lower interest rates. So a big part of why interest rates are low is nothing to do with the Fed…”

So buying trillions of treasuries has nothing to do with why interest rates are low. Does he really think what he says?

Memento mori,

“So buying trillions of treasuries has nothing to do with why interest rates are low. Does he really think what he says?”

This passage you cited from the NPR interview is precisely what motivated me to add to my “Have You Noticed…” article yesterday this phrase in the subtitle:

“… and loaded questions are used to politely hammer Powell into telling obvious nonsense.”

I believe I will in my lifetime witness Powell being humbled in front of congress in the same way the maestro was with his famous “..I found a flaw in my model of how the world works..”.

But the damage will be too severe to draw any satisfaction from it.

It’s psycho-babble… less verbose than Greenspan but no less ridiculous.

Always that savings-glut bullshit… Why is nobody ever challenging that? If there were so much savings, then why is the Fed doing trillions of QE? Let savers buy the treasuries instead of the Fed.

I agree with you completely YuShan. Old people saving instead of spending their earnings are always easy to blame for slow sales.

Maybe the banks pushing loans to companies that will never be able to repay the loan, but will pay the bank’s fees, are the problem. After all, the Fed will rescue the banks.

The savings glut is the exact result of the Fed’s creating the credit-money in the first place.

Every dollar in existence has to be owned by someone at every point in time.

That oversupply of credit, relative to demand for loans, is what drives down interest rates. The “savings glut” is just the visible channel by which it happens.

Exactly

HAha. So true. Only If the general public really knew what is going on.

Big difference paying back fake money creation at 5%, the fed and others would not be able to pay back the interest without creating more debt. Ponzi

This is why it blows up eventually.

Yeah, don’t fight the lack of stimulus in a recession either. Fed this, Fed that, but fiscal response is just as important, and it is starting to look like a no-show.

Moreover, I’d say that the whole is greater than the sum of the two parts, and Powell is smart enough to know it. He takes a lot of abuse but I really doubt he relishes the position he’s in and is probably angry about the whole situation.

He should be. Mitch plays politics while the economy burns and puts the integrity of the central bank on the line.

Do you smell desperation? I think I do and it’s coming from the GOP.

Today Senate Resolution 688 designating Sept. 25, 2020, as National Lobster Day passed by unanimous consent.

Meanwhile the Resolution for Steak and Blowjob Day has been referred to committee, again.

If he didn’t relish the position he was in, he could have stood firm and allowed raised to normalize, rather than cave every time.

It has very little to do with Mitch or Nancy. That Congress didn’t pass more stimulus isn’t a reason for the Fed to print more money.

The stimulus already passed is unprecedented and has our national debt higher than at the end of WW2, more debt is NOT the correct answer although it would prop up our current overvalued situation for a while.

The really frustrating thing is we literally have nothing to show for this trillions in debt and stimulus. We still have a bloated military, a bloated and inefficient health care system, a crumbling infrastructure, and so forth.

We got the carnage, doe, as promised.

If you read Buffet’s stuff you know he doesn’t believe in speculating and only believes in buying things with predictable earnings. He got out of airlines with a loss because the future earnings dropped like a rock. Anyway, my take is he is sitting on a very conservative portfolio because future earnings for most things are unknowable until the virus is defeated or most stock prices just don’t pencil out to a reasonable return.

Now for the Fed, it would be funny to see all of their faces photoshopped onto a portrait of Soviet Union Central planning committee working on their 5 year plan for the economy.

I wish, I wish they were working on a 5 year plan instead of these 2-3 month plans.

Last paragraph Wolf,

Yes please

Trillions. Glad to see them count Trillions. It is a Trinity of Trillions, and Two Proofs, still to come. Any more stimulation and we’ll fry the high wires.

Hi wolf,

What is the significance of a relatively small reduction in balance sheet? We know Fed can balloon its sheet fairly quickly by treasury and mortgage security purchase to keep asset bubble from bursting. Your opinon seems at odds with peter schiff. Love to see you debate with schiff on feds balance sheet

Richard Ou,

The significance isn’t the reduction in the balance sheet; it’s that the balance sheet has stopped ballooning, that the Fed has stepped away from the corporate bond market, that it’s just buying enough MBS to replace the pass-through principal payments, and it has stepped away from the repo market (by raising the bid rate), etc.

Sure, the Fed can always step back in, but it could always do that, and has done it over the decades, but we still got crashes. So when credit markets freeze up, the Fed will step in – we know that. But they’re loosey-goosey now, so the Fed is leaving the markets to their own devices.

But, but, but … that would be like … Capitalism.

Been combing articles for the past few years trying to find the point of this fiat charade. The pass through principal on the central banks “balance sheet” is the income entry that screams fraudulent accounting. We know central banks don’t have to follow accounting rules but the big piece of the puzzle that everyone seems to be missing is when primary dealer banks stopped having to follow accounting rules. Which happened last September. Deloitte, in a brief report, outlined that bank trading accounts now no longer have to comply with the “accounting prong” for their trades. Beginning on January 2020 banks no longer have to follow any sort of accounting rules when complying with the Volcker rule. This is regulatory capture to the point the thing being regulated, bank trading accounts, are protected from laws by the regulation intending to force the law.

I’m not sure if linking articles is allowed but search “deloitte Volcker rule change 2019”. The rules changed before Volker’s body was even cold.

Between primary dealers no longer having the “accounting prong” on their trading accounts and unlimited QE there is literally no possible way to unravel this mess from an accounting point of view.

It’s times like this I wish we had a decentralized ledger to keep track of accounting flows.

Millie Brown,

EVERYONE who holds MBS gets these pass-through principal payments. They’re a standard feature of MBS. Your bond fund that holds MBS gets them too. And your bond fund replaces these pass-through principal payments with new MBS, just like the Fed does.

One thing that’s a little concerning if you try to figure out where we are going. Inflation as measured by CPI clocked in at a pretty stable 1.6% on average the last 10 years (even after all the deficit spending and fed magic money). You would think the Fed would see that as a success in the big picture of things. The congressional mandate is stable prices, and how is stable prices greater than 2% better than 1.6%? But no, the Fed I’d telling us that they have to make up for that sorry 1.6%.

It seems such a hall of mirrors where up is down and everything is distorted. Only thing I can figure is we are getting into the fourth quarter of the US being the reserve currency.

Agree with you. Stable means price does not change. Unfortunately no congressmen challenge Fed on this. It will be better the mandate is to keep the purchasing power of dollar stable, which unforunately is opposite of what Fed is doing. It is sad people are not educated on this.

The Fed has been allowed to choose an inflation measure and rate that vastly understates real inflation. Congress needs to get off their rear and end the Fed, or demand real stability. This will never happen.

Wolf – can you confirm if the “Chapwood Index (dotcom)” is realistic, because it shows at their website a 5-10% yearly real inflation rate in our largest cities on the 500 items humans actually purchase in real life:

The Chapwood Index reflects the true cost-of-living increase in America. Updated and released twice a year, it reports the unadjusted actual cost and price fluctuation of the top 500 items on which Americans spend their after-tax dollars in the 50 largest cities in the nation.

Yort,

First, you have to distinguish between “price increases” and “inflation.”

Inflation as measured by CPI is a monetary event: You buy the same thing of the same quality and size over time, and it costs more. This means your dollars lost purchasing power. That’s inflation.

But cars have gotten a lot better over the years, and even the cheapest cars have safety features (6+ airbags, antilock brakes, side-impact bars, crumple zones, etc.), convenience features, performance features (6-speed to 10-speed automatic transmissions), and other things that you could only dream of in 1985. Cars also last a lot longer than they used to. This costs money and adds “quality” and “value” to the car. This is not a monetary event. Your dollars are NOT losing purchasing power in that respect. You’re getting more and you’re paying more. This is a technological event (and it is taken out of the inflation calculation via “hedonic quality adjustments,” though there is lots of room to argue over how aggressively those adjustments are applied).

But because you cannot buy a car without those features, you end up having to pay more for a car. So you can add this price increase to the “cost of living.”

Here is a detailed explanation of this with fun charts using the Ford F-150 as an example over the decades:

https://wolfstreet.com/2019/12/15/my-pickup-truck-price-index-crushes-cpi-for-new-vehicles/

I consider the Chapwood index a bad hoax in terms of measuring inflation as a monetary event (loss of purchasing power). I don’t know what it measures, but it doesn’t measure inflation, that’s for sure. 10% inflation a year means 60% inflation in five years or 100% inflation in 8.5 years. That’s just BS.

1) Jeremia Powell will flip again and adopt Andrew Mellon policies.

2) He will refuse to install a new carpet for wall street bankers and stimulate their fun games.

3) JP will become an undesirable opposition and let the chips fall down as they may. A new real Jeremia.

4) He will refuse to resign under pressure and become the next Fed Fall

Guy.

5) He will defend himself and the Fed, blaming the chaos and panic at the top.

6) He will become the only adult in the room and the results are going

to be ugly.

What’s your basis for this, just out of curiosity?

Nah, he will declare himself a hero, a la Ben Bernanke, and will show “courage to act”, i.e. print, print, print, and print some more.

Will the challenger fire him before the election? Should he? The man is a political toady. You think he can moonwalk everything he has done? 44 kept Bernanke on for the duration of his term. Or can JP perform bipartisan groveling?

Question: re MBS comment in article “and in today’s refinancing boom, this torrent of principal payments reduces the MBS balance by large amounts every month. ”

Why is there a ‘torrent’ of principal payoffs in a time of such low low interest rates and the ability to lock in?

Is it security fears? Pass throughs?

Don’t get me wrong, I preach no debt and paying off mortgages, but it seems counter to the surge in refis etc.

I don’t understand the vehicle as an investment option, I guess.

Refinancing. The old loans are being retired, hence the principal payments, but the new loans aren’t yet sold to the Fed.

Got it. Thanks. Makes sense to me now. In other words, more pretend and extend.

Pretty much. LOL

Paulo,

It’s just the way mortgage refis work. Every time someone refinances a mortgage to get a lower interest rate, the old mortgage is paid off in its entirety, and that lump-sum principal payment is passed through to the holders of the MBS, such as the Fed. The new mortgage is then rolled into a new MBS.

Thank you. It makes total sense and I should have figured it out. I always mistakenly think it is like the old days when a financial institution simply held your mortgage and didn’t sell it as an investment product. I also remember when people did not ever refi because the object was to not have a mortgage and adding to a mortgage was not done lightly. :-)

Its deflationary, so Powell can say he is trying to shoot for inflation, but he sees the numbers like princ. loans being put to sleep, and people paying down credit cards.

He is “up on the high wire, one side is ice, the other fire”

as Leon Russell puts it

So if you opened a mortgage with some really solid bank, and you REFI through a shady online lender, you just bought a world of trouble, for a few cents, or you are just fine because the Fed now owns MBS II??

Mortgages are pooled and sold off by the originators ASAP. Within a month if not weeks or days. I’ve been trying to find a local bank with a mortgage portfolio for years with zero results.

The borrower is just fine. The risk is with the lenders/investors/taxpayers.

Nice hot read on CPI this morning. Jerome should be giddy that our purchasing power is going down.

You cannot believe anything the private federal reserve says or puts in print because they lie, steal, and loot for their friends in high places. It is no wonder that everyone is confused when they see what’s actually happening and what we are lead to believe. Why are lumber prices and Dr Copper doing so well? Outside of oil, many other commodities are doing well and the financial engineers are overwhelmed with work. Why? Interest rates are at fake low levels, and it one of the major driver’s of home sales and refinancing. Real estate defaults will be bought by the fed and resold to hedge funds cheaply, so that there will be a “shortage” of houses for sale and ultimately, commercial real estate will be handled the same way as houses in 2010. Argentina was a major economic power with a well educated populace in 1900. By 1940, it was a disaster because of looting by its politicians. The US has been looted for the last 40 years

RightNYer,

My DOW analog.

What do you mean?

Although the value of some SPVs have receded, the value of the SPV for corporate bond debt has plateaued at its high.

It appears the Fed is not selling a single FAANG bond. Perhaps the Fed has concluded it does not need to do much more than retain its FAANG bonds to keep the market balloon from bursting or deflating rapidly.

You skate to where the puck is going to be, not where it is. Things get worse, the Fed will step in, and things will get worse. (Otherwise how are they going to get better?) Without this virus the market would be 20% lower than it is now, and a lot of people would be unemployed, like they are now. This selloff may extend until the Fed gets into the game. The markets are very adroit at manipulating the Fed to action.

The fed will always matter.When America can borrow

3-4 trillion a year with little visible results and a currency that

still holds its value -that is the power of the fed.It is a backstop

along with the military no one can match. The one fly in the ointment

is the 150 million Americans who are broke.As long as

they are too numb to vote for their own interests then things will be fine.

Dont wake them up.

Haha, steady as she does on the repos until…

Keep your eyes on Australia. Goddamn Austrians need to dig deep in their pockets & put their money to work by buying stocks already! But we see.