First signs of a very slow-moving mess.

By Wolf Richter for WOLF STREET.

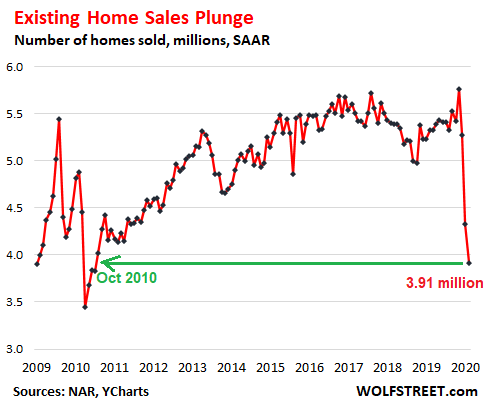

Sales of existing homes (closed transactions of single-family houses, townhomes, condos, and co-ops) plunged 29% in May compared to May last year, not seasonally adjusted, to 340,000 homes, according to the National Association of Realtors. The “seasonally adjusted annual rate of sales” (SAAR) – which is generally used as the headline number – plunged 26.6% year-over-year to 3.91 million, the lowest rate of sales since the depth of the Housing Bust in October 2010 (data via YCharts):

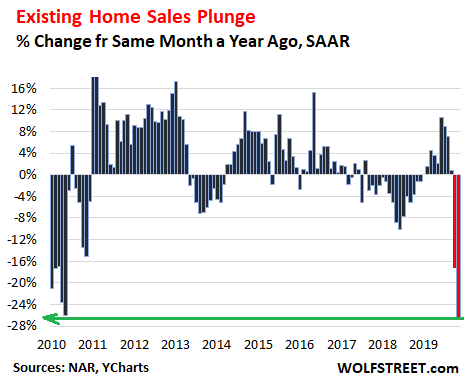

The 26.6% year-over-year plunge in the seasonally adjusted annual rate of sales was the biggest since February 2008, a sign of just how tough the real estate businesses has become (data via YCharts):

Condo and co-ops sales were hit much harder than house sales – but both were ugly:

- Sales of single-family houses plunged by 24.8% year-over-year, to 3.57 million units seasonally adjusted annual rate.

- Sales of condos and co-ops collapsed by 41.1% year-over-year to 340,000 units seasonally adjusted annual rate.

The “big move to the suburbs?”

Closed sales in May largely reflect contracts signed in March and April. So it’s a little quick to come to a conclusion as to why condo and co-op sales are collapsing like this, while house sales are only plunging.

The report – and the industry overall – points at pandemic-induced moves from multi-family buildings in big cities, such as condo towers with elevators, to houses in the suburbs, with commutes being made less arduous by work-from-home arrangements.

This would be a great trend because big cities are awfully congested, and these condos are awfully overpriced. But I’m not sure…. House sales still plunged, rather than increased, as a shift from condos to houses might imply.

And a lot of condos have been bought by investors, many of them residing in other countries. Investors’ reasons for buying a condo vary, ranging from basic capital flight and money laundering to renting the unit out, either as regular rental or as vacation rental. But finding new investors in condos in this environment has become tough.

So we will see down the road if a “move to the suburbs” is one of the permanent changes that the pandemic has initiated. The NAR in its report is in that camp:

“Relatively better performance of single-family homes in relation to multifamily condominium properties clearly suggest migration from the city centers to the suburbs.”

“After witnessing several consecutive years of urban revival, the new trend looks to be in the suburbs as more companies allow greater flexibility to work from home.”

Sales in May fell in all regions, compared to May last year:

- Northeast: -29.9%

- Midwest: -20.2%

- South: -25.1%

- West: -35.1%

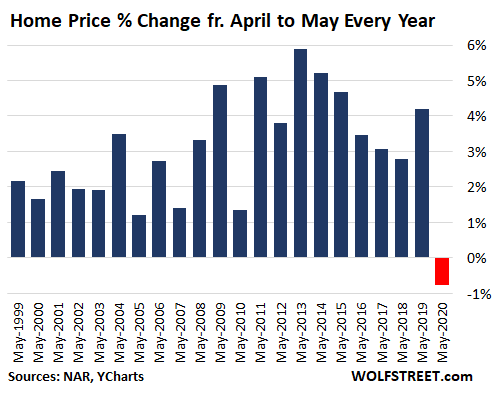

Median price drops from April to May for first time ever in the data.

The NAR report didn’t mention this because it was very inconvenient. The Median price dropped from April to May.

April to May price changes reflect the spring selling season in the housing market. Big increases in the median price from April to May are the norm. Even during the worst years of the housing bust, the median price increased from April to May. It just always does no matter how bad the housing market.

The month-to-month increases from April to May tend to be big. Last year: 4.2%. But not this May. This May the median price fell 0.8% to $284,600 – the first April-to-May price decline in the data going back to 1999 (data via YCharts):

This wacko April-to-May price decline chopped the much-ballyhooed (and pooh-poohed) year-over-year price gain in April of 7.4% to just 2.3% in May.

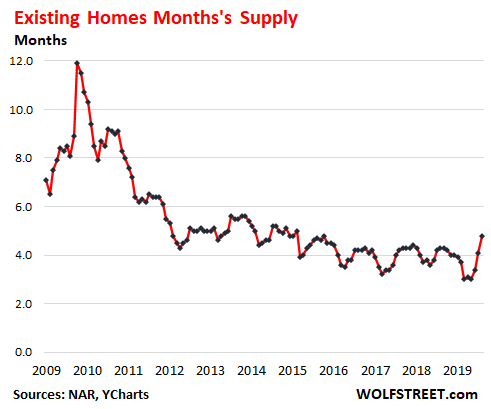

Unsold inventory is rising.

Unsold inventory of homes that are still for sale and haven’t been pulled off the market yet has increased in May by 6.2% from April to 1.55 million homes.

While still down 18.8% from May last year – as sellers were still worried about potentially contagious people running through the homes – sales have plunged a lot more (-26.6% SAAR), so unsold homes for sale rose to 4.8 months’ supply, the highest supply since July 2016 (data via YCharts):

Clearly, the housing market is in the first moments of struggling with the economic consequences of the pandemic. Housing markets move slowly. Things don’t happen overnight. Sales take a month or two to close. Everything takes time and data always lags. And markets are very local, each with very different dynamics.

And this time around, there is an additional wrinkle: Millions of homeowners, rather than defaulting on their mortgages, with 30 million people now on unemployment rolls, have entered into forbearance agreements with their lenders, where the lender agrees to not pursue its legal rights against the homeowner for non-payments. This too is going to be a mess for people who still haven’t found a job when the forbearance agreements expire. The market hasn’t even begun to wade into this mess.

The Big Shift: Fed shifts to propping up consumption rather than asset prices, and its total assets decline. Read... Fed Ends QE, Total Assets Drop. Liquidity Injection Ends

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

From my brother in law who’s a broker….”Yes, we are experiencing the same thing in Santa Barbara/Montecito. Santa Barbara is about an hour to an hour and a half from Los Angeles and there are a lot of people trying to get out of LA. Homes in Santa Barbara that have been considered very over-priced and have been on the market for over 500 days have sold to Los Angeles buyers. One of our listings that has been on the market for five years with a different agent, is pending sale now with an LA area buyer.”

Paging SoCalJim?

Please don’t page him

Thank you Fredrick, I, for one, appreciate your honesty.

I think you’re the outlier here but you’re welcome

negatory on the outlier F,,,

several folks on here are always ”banging the same drum” as in ”drummer” of olde

although, to be fair, some of the best commentors, and our fearless leader also that way,,, ”sometimes”

eh?

Me too, Frederick — without candor, this place would be just another yahoo board (note generic yahoo, although branded would be the same point).

haha I was waiting for that….I am sure when it comes to this stat, it doesn’t apply to West LA/OC & South OC/San Diego or whatever posh enclave of Southern California. We will hear many stories of how they just listed and 5 mins later sold for XX% asking price cause you know supply is still low and you know those demand, just roaring back cause everyone around here is hedge fund managers or super immune white collar workers. There will be plenty more to see here, think this movie just started and it will be a long one, 2-3 years and plenty of hindsight will validate which side of the camp is right afterall.

Sales in May fell in all regions, compared to May last year:

Northeast: -29.9%

Midwest: -20.2%

South: -25.1%

West: -35.1%

No!!!! I want to get a place in SB again in a few years. Hoping this trend changes soon.

I was thrilled to get away from the LA area once Covid struck. Now I’m required to drive in 2 days a week but with all the tourist and LAX traffic gone it only takes 1.5 hours to make the 90 mile drive.

I’m definitely going to get serious about wearing a mask to work with the surges we see though. I live with my 78 year old mother – and I’m hoping to convince them to let me cut that driving back to 1 day a week again. An extra 3 hours in the car is no fun, but I’d still put up driving 5 days a week if it saved me from living in a dingy, overpriced apartment or granny-shack in LA again.

A friend of mine, also age 40, did finally buy his first home here in Orange County though.

City living is definitely over for a while.

All those condos in Downtown SF will be in trouble soon. Imagine having to get into an elevator with people who refuse to wear a mask.

Many rich people will get dinged for sure.

It’s not a problem, it’s an opportunity.

I don’t know how many of those properties remain unsold, but the city literally ought to negotiate with those condo developers to buy those things cheap, and then turn it into below market rate housing. It would go a long way to solving some of the housing problems. It’s an opportunity.

As for the rich people, they can afford this.

Housing projects in the sky. Great views. One advantage, can’t open the windows and chuck bottles down on the street like they did at the old Geneva Towers, on Schwerin Street by the Cow Palace, which was built originally as upper middle class housing and degenerated into a needed implosion.

The problem with buying those condos on the cheap is that they are still a long, long way from cheap.

And the HOA’s still suck out the rest of your cash [for what?].

At this point, yes, but wait a bit until the developers get desperate.

Couple of things, one has to wonder how many open units do some of these condos have that has just sat there for the last couple of years. Also, how many unfinished projects there are. Cause the longer the developers sit on those, the more pain.

Great idea! Buy buildings from wealthy developers. But what to do? Raise taxes for the money? Float another bond issue for the money? Bailout the developers currently holding the bag. Cheap now, they maybe just be considerable cheaper in the future. BTW, even poor people read and watch TV and may not be in a hurry to move into a condo elevator death trap.

Lots of possible state laws, rules, and regulation may be different Lisa, et alia:

Potential trap for condo owners in FL is the possibility of a buyer owning a certain percent of the units being able to convert ALL the units to apartments, and otherwise ”cook” the HOA so that they are able to turn the whole complex very raw and demand HUGE special payments from all the other owners…

Trailer parks in FL with lots owned by occupants have been done similar, forcing everyone out so the buyer can build a high rise, etc.

(Though, in all fairness, one on the east coast, owner occupied, right on the Atlantic, developer paid each of 20 owners MM OR first right of refusal for a unit in the new construction.[ ‘course that was back when a MM was real money, not just ”chump change as it is today, eh])

The City has no money. But as you say, it might be an opportunity.

Raise the assessment value on those properties. Get paid a ton while waiting for their value to crash. Swoop in and purchase everything.

That a great way to run down the neighborhood.

Hate to say I told you so but Gold is breaking out 1758 right now

It’s simply too early tell how things will settle out in Sonoma County, people who relocate from SF to the wine country are likely to be well heeled and we may very well see a bifurcated market with nicer areas and more expensive holding value much better than lesser properties.

That’s usually the case in a downturn, but it may be more exaggerated than in past market corrections.

Once a market turns it usually takes a few years before the bottom is hit.

This time may be different, the pandemic is a wild card and as Wolf pointed out Mortgage forbearances are ending soon which could drastically affect the supply at a time demand has been hard hit.

Tom Stone,

One has to wonder how this covid induced ‘out migration’ will be affected, should any major fire-season conflagrations occur this year or the next. I’m sure the idea of one’s recently acquired ‘escape pod’ possibly going ‘up in smoke’ has not crossed the minds of at least some of those looking to relocate.

That would be quite the one-two punch in the gut!

There is supposed to be about 4.5 M in forbearance at this point, it would be interesting to see a geographical distribution here. It would be a good indicator of where some of the worst trouble spots are likely to be.

New research offers a glimpse into struggling households, discovers out of the 2,000 American homeowners polled, over half (52%) of respondents say they’re routinely worried about making future mortgage payments and nearly half (47%) considered selling their home because of the inability to service mortgage payments.

The study, conducted by OnePoll and the National Association of Realtors, determined 81% of respondents had experienced unexpected financial stress due to the virus-induced recession. Over half (56%) reduced spending so they could service mortgage payments.

zh

Vancouver Island anecdote.

We are selling a single family 3 bdr rancher on Vancouver Island due to a death in the family. This is located in a smallish city (40K). The sign goes up July 1, as we are still moving stuff out and cleaning, etc.

I have been told prices are down 3% in the area.

There is no inventory these days so sales are still brisk. People do not want strangers entering homes during Covid, so that our place is empty is considered to be an advantage. RE agent average time to sell is still around 18 days. From what I gather in my research we are still attracting city folks (Vancouver and back east) moving for relocation and lifestyle change.

In our rural home area, not only is there virtually no inventory, white elephants are even selling. A shitty old hotel (which needs to be torn down imho) recently sold on auction for 100K over the last asking price. It was an online auction through Ritchie Bros. The only properties not selling are those that are over built for the location. People don’t want fancy homes here, they want property….land, and a more modest home. Last week I was approached to sell some vacant property we own. It isn’t for sale.

On Vancouver Island we have no active Covid cases and haven’t had any for awhile. Except for tourism and hospitality, the economy is doing okay. For now. We’ll see.

Yes, we will see, in the 8 to 12 months. What’s that old song by the Carpenters….”we’ve only just begun”….in June a significant number of folks have not make mortgage payments, plus a boat load of other issues. We shall see how all plays out.

Badly, no doubt ..

I don’t forsee the ‘bank’s extending their forbearances any further .. out of a sense of ’empathy’, having already once done so .. unless compelled by government fiat. That doesn’t look too likely from my admittedly cloudy crystal ball.

So, seeing as it looks like millions of property/homes are going to be foreclosed upon, what will be the negative social ramifications ?

This could get ugly, Biggly!

Lack of adequte shelter.

Lack of sufficient employment.

Lack of affordable medical services.

Lack of sustenance (Food).

All BAD for keeping the Plebs from completely losing their sh!t.

If a bank forgoes a few months mortgage and tacks it onto the end of a loan, would that really show up as much of a loss?

Also, why wouldn’t everyone claim distress, get 4 months free of mortgage and put it all into the principal?

Not a good time to be living in or near a big city…..

So the “sold for 120% over asking price” real estate bubble has finally spring a leak but only in the city, not in the suburbs!

In the burbs, all real estate agents still selling houses “over asking price”!

Better hurry because remote suburban office space, without elevators, is selling fast!

This absolutely does not reflect what I am currently seeing in San Diego county.

Inventory is as low as it has been in history, sales higher than anytime and prices also are at their highest.

May was an outlier as people were ordered to stay at home but we caught up and some all the May slack in June.

Time will tell how this evolves, but right now market is red hot with bidding wars, I know it sounds crazy but it is what I am seeing, the only thing preventing this from exploding even higher is the lack of inventory not demand.

Wolf, can I start the ball ralling here :-]

I stopped counting new all time highs today.

Short traders just can’t help themselves venturing out in front of the tsunami of Fed’s liquidity. That’s how we get new record highs.

Meant to post not as reply.

Jeremy Grantham says this is the “real McCoy” bubble, 4th in his career. First being Japan, then dotcom, then housing.

Says US exposure should be zero, or less than zero if you can stomach it.

2-3 years ago he predicted melt-up to sp500 3400-3700, which would constiitute classic bubble.

Also mentioned Tesla is bigger than combined German auto industry.

andy,

My short is up about 0.8% at the closing price of the SPY today (since I shorted the SPY on Friday morning, not on Friday at the close).

“So far so good,” he said, passing the 14th floor on the way down ?

It would be interesting if there was an easily accessible list of all currently rated B/CCC companies out there…logically that’s the population that is most likely to hit the wall first.

But, a bit surprisingly, it seems the ratings agencies do a pretty good job of policing their IP…my casual googling has not turned up much in the way of one-stop-sources.

I wonder if anybody on the board has come across publicly accessible lists of B/CCC companies.

DOW futures down 400 points, oh no. Quickly, someone, call federal reserve.

Someone did, no? Bounced back right away, after Navarro came out and denied what he had said on TV about the China trade deal begin “over.”

Not what I’m seeing in Boston either. Boston is hotter than it’s been since 2017, particularly the outer suburbs. The question is, is this just the demand from March/April + May/June? Or is this actually a lasting boom? I’m thinking its the former now more than anything.

There is no inventory.. that is the problem here in the suburbs. And what is on the market is crap. It’s going to take awhile for any of that to change.

As a condo renter in Andover, MA (about 30 minutes north of Boston) I’m currently paying $1500 a month for a rather old and small 1 bedroom unit. I’ve been told this is an amazing bargain. Hoping for a big reset of property values, but how that might actually effect renters remains to be seen. As they say, it’s always the darkest, just before the dawn.

Would another inconvenient truth (in addition to the drop in median price from April to May) be the following: when the mix of properties sold shifts from condos to houses, the effect would be to skew the median higher. So if home sales merely plunged but condo sales were obliterated, perhaps some kind of mix-adjusted median value would have fallen even more from April to May? Or is the NAR number cited single family only?

SocalJason,

Yes, that shift in mix skews the median price, especially in places were condos made up a larger share of sales.

The issue is made worse when volume drops, because it’s the weaker buyers with less resources and more worries about jobs that drop out of the housing market, which means the higher-priced homes are more represented in the sales mix and shift up the median price of the mix.

In addition, according to the NAR report, the median price in May year-over-year:

Single-family house: +2.4%

Condo and co-op: -1.6%

This gives me a good excuse to post my favorite chart about how a “change in mix” of sales skews the median house price. The median price is the price in the middle, with half of the homes selling for more, and half selling for less.

The table below shows a very simple housing market. In April 2019, 9 houses sold, with a median price of $300,000. In April 2020, the same top 7 houses sold again, each at the same price as a year ago, but the two lowest-priced houses didn’t sell. So actual house prices did not change at all. But the median price jumped because the mix changed:

Hi Wolf,

Thanks for the additional insight and example! Interesting how the median, ostensibly designed to reduce distortion from outliers, can bring it’s own set of problems :)

It is not the money with little money that leave the market first but the flippers. They buy the houses that are cheap for type and location and than “upgrade” them

If you are a home owner or business owner in a long term controlled city, you are in trouble.

Restaurants, bars, etc. closed due to COVID power mad mayors. Looting and rioting. Degraded city services. Defunded police. Streets not safe.

The tax base has been voluntarily destroyed. But pensions will be paid. Your property taxes are about to go from insane to ludicrous.

Those that can get out are gettin out. To the outer suburbs or small to mid cities with some sanity left.

There is low to no demand to buy in a big city now. It will only get worse too. Very hard to sell a house with significant price cuts.

The most truly in trouble are those who purchased expensive and/or fixer upper with all life savings homes in “gentrification” neighborhoods expecting that sweet equity.

Cities died in the 1970s and yet here we are.

I think the effect will be short lived like 9/11. Americans have short term memory.

Many cities did die in the 1970s.

They didn’t start coming back until 30 years later.

Some never came back.

I agree with Harrold. I don’t see the long term trend, yet. Just how many people are going to be working from home permanently?

And if it does become a firm trend, I could believe people will be in trouble due to out-migration from cities that have gotten sky high like San Francisco or New York, if you bought in the last couple years, but for most of the cities in the country? Most cities have very few skyscraper condos compared to single family homes.

For instance, without claiming Austin is representative of coastal cities:

Austin metro: est. 2,168,000

Austin city: est. 978,000

Austin downtown: 12,000

The last figure is from:

https://austintexas.gov/faq/how-many-people-live-downtown

One could imagine that the “downtown” figure is off by anything short of an order of magnitude and you can see there just aren’t many people in Austin who will be fleeing the virus in an elevator.

If the bookies are right and Biden wins and dems take the house and senate they could crank up MMT and bail out the irresponsible cities and states who are mostly controlled by the Dems. Then property taxes might not go crazy. “Moral Hazard “ is the American way.

Problem is the Dems are the center party. For MMT to work you need a left party.

All the comments seem like they’re still stuck on the euphoric buyers buying the real estate. I would consider them “dumb money” If people are buying houses now, they’re in for a big reality check. It’s still early and by “early” I mean that defaults aren’t even calculated yet. We’ve only been in this mess for roughly 3-4 months. Defaults take time.

I know a lot of people don’t even look at the real esate market before even buying a house. Some people just want a house to live the “american dream” so they impulse buy and make irrational decisions. My cousin just recently closed her deal for her house in Tracy, Ca. I was just like…you’ve got to be kidding me.

Just my opinion.

Some people value a house for what it provides, a roof over your head without having to deal with neighbors above and below. I value a home with the next neighbor at least one acre or more away.

Not every decision in life is timed to make an optimal profit. If your cousin can afford the home and feels secure then it might be a good decision for her.

Your opinion is a very sound one

Yea, well, those of us that looked at it rationally lost out on 100% gains.

Still crazy here. I don’t see any job loss among friends. We had hundreds of layoffs where I work and everyone has been hired by other companies.

Trillions of money from uncle FED going to companies… you still expect lower prices… a lot people are making more money than before with the new jobs.

“Everyone has been hired by other companies” That’s a hell of an assumption.

“rational lost out on 100% gains” –What do you base that statement off of?

When I purchase property, it’s always at rock bottom prices when there’s regression in the economy. It’s not too hard to use averages to see when to jump into the market. Don’t be blinded by the greed of the people. I WOULD NOT jump into this real estate market with a 10 foot pole. There’s way too much divergence between the poor and the rich. Usually the rich live in the dream world totally oblivious to market regression. Can you imagine being so filthy rich that price doesn’t matter?

Tony I bought in NYC in 1980 when everything was going to hell in a handbasket and again in 1992 a Hamptons small farm which was a default by a Manhattan attorney Both investments have been superb and I agree Now is NOT the time to be buying real estate The crash will come and you can buy then My advice is to hold cash or better yet gold and wait

re: “My cousin just recently closed her deal for her house in Tracy, Ca. I was just like…you’ve got to be kidding me.”

Why? Tracy is a bedroom community for the SF Bay Area; not glamorous or chic, but not a dump, either. Are you saying your cousin should have waited for prices to drop?

OTOH, Mountain House, 5m NW of Tracy was one of the co-epicenters–along with Victorville–of the 2008-9 crash.

I’m selling my house in the mountains while it’s at top of the market..lots of cleanup and repairs still to do though. No more getting the house trashed by bad tenants.. the state of California has also been treating landlords as if they are evil and criminals . I’m hoping that the window is still open to sell it. The realtor says that the market is still good, maybe because people want to bug out of the city. My belief is that that window won’t remain open for long though. Four major reasons why, 1st the changes in loan requirements..20% down and a credit score over 700, the second is the massive job losses up to 40% or more, the third, foreign buyers are drying up as well, and the fourth reason is the market will be flooded with foreclosures and bankruptcies.. let me know if I’m incorrect on my views.

Or a slap across the back of a head.

In my little burg houses are selling before they’re even listed. Last month it was selling within days. Now from what I hear, agents aren’t even listing publicly. They send out an email to fellow agents saying I have this for sale. Bring offers. And then once an offer is accepted, the listing is put on the MLS with pending status.

There is virtually no inventory to speak of, under $500K. And if you want to buy new, it’s at least 6 and often 12+ months wait to buy something. The builders got smart after the 08 crash. No more spec houses, hence no inventory. You want a house, you get in line and in a year or so the house will be ready. Kinda like the Soviet system for getting a car.

In my little burg, houses are selling before the owners even thought about selling them. Buyers arrive with vans full of cash, and pay triple the price that homeowners would have accepted, and just rip the houses out from under the homeowners no questions asked ?

My house was bought by unicorns.

Did the buyers perchance to endow you with some of that magic powdered horn, for the needed incantations to be bestowed upon any new digs that might come into your favour?

Really strange to most folks: In my little corner of the world (not a “burg” -no other house within a mile) I’ve lived in my house for forty three years, after deigning and building it. Timber and cattle sales have reimbursed me for it, several times over.

I’m told there’s trouble in the cities. I wouldn’t know, first hand.

How did/do you get infrastructure utilities (electricity, water, wastewater).

Septic is common enough for true waste water and gray water can probably just be dumped outdoors.

Well water is also passably common (although there are upfront costs).

But electricity?

I imagine the connection costs rise very, very fast if you are really any distance from the existing grid.

Solar/etc are fine for the committed/disciplined…but how about the mass buying public looking to push out the frontiers of the exurbs.

I wonder if there are any good books for that niche audience (not true off gridders living far, far out…I know there are books for that audience.).

We are in Texas. We are just living in our houses around these parts. They are not worth much anyway, they are just houses.

Quite. Texas has a lot of flat, open land and building codes that are not restrictive.

It’s only gotten pricey in the biggest cities and, even then, not uniformly.

Investors bulldozed my house and started new construction before I could put it up for sale. ;-)

Don’t forget to say hi to Lawrence Yun for me, JSRG. Can you also ask him to show the hard data that backs up what you just said?

Hard Data to back up a shortage of real estate? LOL

You can google this yourself, you don’t need Lawrence for that. But it’s cool, you keep renting if it makes you feel better. But 5 years from now don’t whine that housing is unaffordable.

Right because housing is so affordable now especially with so many unemployed and so much uncertainty…good, at least I see where you logic is coming from…yup I get it, housing never goes down..now is a great time to buy..etc.

Better to buy gold and wait for the crash in housing It will definitely outperform in hyper inflation Look at Fairfield County Conn what’s happening to housing close to NYCity Taxes and lack of high level jobs is killing that market

Is your name Lawrence Yun?

All real estate is local, right? I’m in the Denver suburbs, inventory is extremely low, and things are selling within days at asking price for now.

But no one has any idea what things will look like if we are still at 10% unemployment in 6 months, if were looking to sell in my area, I would move very quickly, there is so much uncertainty, and if people aren’t promptly returning to work, this could be like Wile E Coyote spinning his legs for a minute after rushing off the cliff before he plummets down.

In my little burg houses are selling faster than lightning. Some people are trading organs and giving up their firstborn child to get the privilege of making the obscene payments each and every month because their jobs are guaranteed for the next 100 years with pay raises every year.

Bonus: There are oil and gold under each plot of land, so it is virtually a no brainer. People are smart now, they won’t miss on this.

As you point out, “a lot of condos have been bought by investors, many of them residing in other countries,” it’s hard to make predictions for the future. Condos and coops, (aka owned apartments,) have been a fast way to park or move money. They could snap back just as quickly. However, for the price of a small NY or SF condo, you can buy a 3BR house with a yard a few hours out of those cities. That’s why there is currently a buying frenzy in small towns throughout the U.S. (ie. Catskills.)

But what I feel is even more significant as an indicator is that U.S. home-mortgage delinquencies climbed in May to the highest level since November 2011 with more than 8% of all U.S. mortgages past due or in foreclosure. (Bloomberg, 6/21).

Here in Seattle it is a knife-catchers convention.

People coming here believe ALL the hype, or maybe they are just really desperate to leave their basement living dead-end lives and get in on the gold rush that is Amazon.

Now that it takes FIVE years to get that huge vested nugget Amazon gives you, instead of TWO, it will definitely put a damper on the idiocy that is my neighborhood, Queen Anne which is just up the hill from SODO, where a whole boat load of fools paid their WHOLE bonus to buy TOLL BROTHERS beginner townhouses, that were going for 1.4 million.

Prices got a little soft in the recent months. Now they are talking in their adverts that they are only a million bux for a glue-and-brick plastic window starter condo.

I can feel the sharp sweet slice as the knife enters your eschopagus, not mine of course.

Amazon is making more money than ever.

The story is the same in the Bay Area. Cookie cutter builder homes slapped together with glue and any half-decent feature available only as an eye-gouging “upgrade”. We got really competitive prices but need a view of the little sliver of green we call the “park”? 40k extra. Don’t want to face the super-busy and noisy street, 80k. Ready to buy? Now go to this website where the anonymous bidding starts at 8pm and ends at 10pm and go fight to the death while we laugh all the way to the bank.

Glad I didn’t fall for it.

It is hard to make predictions, especially about the future :)

In March I figured RE would tank with everything else, and figured anyone in the market just needs to wait 6-9 months for the bottom to fall and pick up cheap, but I am not seeing that yet for where I watch:

– I am in The OC (SoCal coastal), and things are humming along. I keep an eye on the 300 unit condo development where I had my starter condo out of curiosity/sentimentality, and they are having a “normal” spring season with a condo selling about once a week since early May after no sales during the depth of the shut-in. Sale prices about flat to what they were a year ago. I am frankly shocked that a new one keeps selling each week, then another comes onto the market, maybe RE agents are working to control inventory.

– Relative in Houston RE says things are insanely busy, with regular closings, no falloff in pricing, but note these are suburban mcmansions in planned communities, so where people are now migrating.

– I was already planning to flee CA in next couple of years, was already keeping an east side of Tahoe/Reno. If anything pricing there is going up now since my idea is not exactly unique now.

Our “suburban mcmansions in The Woodlands about 30 miles north of Houston are selling for $130/sq. ft. This is a 2,000 sq. ft. brick home on a builders lot in a nice community. Yes, there are more expensive ones that you can buy here for upwards of $200/sq. ft. But those are BIG houses (5,000 sq.ft. on up).

Houses are selling here.

Better late than never Merit. I knew it was pretty much over after the September 11th situation. 2008 just confirmed it for me

Any flight to the suburbs will not be very fast. Very few people can afford to buy a new house unless they can sell the old one for top dollar. If everyone is going to flee the cities for the burbs, who is going to buy the city RE so the escapees can afford to move. If urban real estate collapses in price due to this trend than suburban prices will have to be pushed down as well to allow people with diminished equity to buy something to live in.

I hope you’re right. The reasoning is sound, let’s hope the reality matches.

the big downturns in 1929-33, 1973-74, 2000-03 and 2008-09 were very serious, but these did not have the major shock to the system that was provided by this plandemic. My personal belief is that this one will get very, very crazy in the near future. You can only sell smoke and snake oil for so long…

What’s the half-life of Hopium ..?

Trinarcia:

+1000!!

I agree It’s all “ smoke and mirrors” and has been for awhile You forgot the 1981 downturn in your list and for me with a new house and an infant and homemaker wife it was the worst of them it

10-4 on ray guns effort in 80-81, to let us Peedons know that going forward the money was coming from the rich party by ”trickle down”, with similar family situation, including new off spring,,, but, being home a bit more, i was able to ”bond with the baby” as is now my opinion every daddy should do both ASAP and AMAP right from the get go,,, so silver lining on that one..

not so silver with the one in ’56 that family literally lost ”the farm” when dad had no work for six months or so.

I really and truly think it is in the best interests of WE the Peedons, as well as our masters/owners, to do NOW whatever it takes to get rid of the HUGE burden of the so called financial economy on top of the real world economy before we get a lot more ”woke/formerly confused” folks actually equating the financial malarky thefts proceeding now with their debts, homelessness, and slide toward poverty, and we do actually proceed to some sort of civil war as is being suggested these days by some on both sides of the aisles.

I am not sure about other larger cities, but ~60% of SF residents rent. Doesn’t take much to get a moving van, assuming they have been saving up for the down payment.

This past month-end was the most outgoing moving trucks I have ever seen since I have lived here (anecdotal just from walking around the city constantly with kids). It will be interesting to see next weekend. Most with young kids and/or newfound work flexibility are eager.

This is correct. If there are people fleeing the city for the suburbs, they will mostly be renters. Urban landlords look most likely to me to have problems coming shortly.

Market here in Ottawa is the hottest i have ever seen. I am not looking at condos. Single family in the suburbs and country are going for over asking and obvious bid wars. Is it an exodus out of the city combined with huge government spending?? I can’t order deck wood they are out of stock. Canadian Tire is packed. Everyone is shopping like i have never seen before. Is this the peak? Its craziness.

Aren’t Canadians getting C$1K per person stimulus until further notice? If that’s the case, the economy must be on fire.

No.

People who have lost their job have some stimulus funds for another month. It is month by month. Folks who applied for the stimulus funding and don’t qualify have to pay it back or be charged for fraud.

A friend of mine owns a mechanic business that didn’t qualify for the wage subsidy program as they took the receipts from March to assess his revenue losses, but March has always been his slowest month. He didn’t fit the stat filter so couldn’t get help paying his employees. He is still running but it is very very tough.

There has been eviction holds and rent relief in our province, but that is also ending.

Some places and sectors are booming, though. My son is in Ft Mac working full time in the Patch, and also runs an electrical business on the side. He is going flat out working twelves. And yet, others are laid off depending on their trade/career. This is all private sector work he is doing.

Here in NC mtns our building supply stores are practically ransacked by bored, stressed out people looking to fix the deck or patch the roof. Work is therapeutic.

Market up after Wolf goes short – no price is too high, we’re still in a bull market until (a) virus spike (b) Fed loses control. Not sure which will happen 1st

His is a longer term trade, not a one day call. Same like mine.

My short, which I took Friday morning, is still up 0.8%. So don’t panic yet :-]

The market also went up after Wolf shorted the last time, went sideways but somewhat up over the course of a month before it started to pay off. The nice thing about a bet like that is that it isn’t options. It limits the gains, but it also doesn’t get wiped out after a few months or a few years, unless the SPY doubles. Which is just not that likely. Because if it does double, then it really means that the US has become a banana republic.

Is there a way to short the real estate market ?

I live in Richmond, VA. The housing market here has not been hot for the past 15 years. Most houses appreciated only 10-20% for the time period.

I am currently renting. Many people may default on their mortgage in the next 6-18 months. That could be time for me to get into the housing market. The housing downturn this time is likely to occur more quickly.

A Miami real estate guy says it is harder now to get mortgages on condos there, they want 30% down or all cash. The special assessments are also a problem, many buildings have them, and some buildings have multiple special assessments. This could increase the cost to carry the unit to as much or more than the mortgage. Plus they have a glut of units too.

Yes, that’s a huge issue. Always happens to condos.

Wait for the special Earthquake Repair assessments in California!

Anecdote re ”special assessments” by HOA of condos:

a very funky/comfortable wood framed beachfront condo in SWFL, 60 units in 15 bldgs decided in 2005 to bring the 1970s built facility up to current standards and codes, with new stairs each bldg, new impact doors, windows, siding, metal roofing, etc..

The cost was approx $300K per unit, versus the $70K new!

They were much more hurricane resistant, far shore,,,

Mr. Richter:

The last two lines of your post says it all!

What’s it gonna be like??????

In NYC, the luxury retailer Valentino is suing their landlord to get out of their long term Fifth Avenue lease. Things are starting to shift.

I saw Rodeo Drive all boarded up last week and also saw a video of the Gucci store being broken into. I can’t imagine that’s going to make prices go up in nearby Beverly Hills.

One of the fanciest condo buildings in Portland ended up inside a 4 block zone that made Portland’s version of Seattle’s CHAZ. Ours only lasted for a couple of days, but I am sure negotiating with the anarchist leaders to allow the food delivery guy past the dumpster blockade made them think twice about urban living.

Where are the stock shorters? NASDAQ 10K? YES. ok, up and up we go. Down is no longer in the dictionary for the stock market.

So housing is just gonna go to the moon… wait for it.

Let’s see.. We just had the worst world wide pandemic in 100 years, and it is threatening to have a second wave which is only beginning. We have 20% unemployment. We have record business closings, spiking delinquencies, and defaults, and nose bleed debt, and asset valuation levels. We have a collapse in the commercial real estate market. We have several segments of the economy which are decimated and will not recover for years. We have riots and civil unrest on a scale we have not had since 1968. We are in trade wars with our biggest trading partners, and the threat of war is increasing world wide. All things considered, I think now is a perfect time to purchase ridiculously priced real estate……

You bet. And as a kicker, a 70K pick up truck to haul all the appliances you will need to live in it.

F#ckin A !

And don’t forget to sport those rear-guard cajones .. for the manly virtue factor.

Yeeeehaww!

In my experience, people who buy 70K trucks don’t haul anything bigger than a Costco pack of TP.

I have about had it with conspiracy theories by people who do not understand anything about the issue. The Hong Kong flu killed about 100K in the US over its entire run. This was during a time when medical care was primitive compared to today’s standards, and no preventative measures in place.

Covid-19 has killed about 123K so far after about 4 mos. and will probably continue to kill at least 10K per month for the foreseeable future. And that is with state of the art medical procedures, draconian prevention measures, and the entire world working at what is basically a war time effort to find more effective treatment. Covid is not a flu, or a respiratory disease in the common sense. It attacks the blood vessels. Once infected it attacks the walls of the cells which allows it to find its way to the circulatory system and travel throughout the body where it attacks nearly every single organ. Covid has caused injury and death from strokes, heart attacks, liver and kidney failure, and several other conditions. Even if you do not die from the virus, if you have a moderate case, there is a very good chance of having permanent organ damage in one or multiple organs making your susceptibility to complications due to “pre existing conditions” in the future. Anyone thinking they have nothing to fear from this pandemic is simply ignorant of the facts. Ask you primary care doctor if you should ignore the precautions and take your chances and see what they have to say….

Shamelessly, I hope prices drop to the point that people can’t move (viz. they can’t sell their existing homes to get the $$$ to buy elsewhere) — sort of like during the Great Recession. Why? I live in a beautiful place that, as I’ve stated before, is a place where boomers come to die. They retire here, bring in goobers of out-of-state money and have driven up real estate prices to the point that only folks from out-of-state can afford it. No locals can afford to live here. I hope the whole damn thing collapses!

(I feel better)

The boomers are a liability everywhere when they can’t go out to eat in profitable numbers in the new 50% occupancy world.

Mt,

As a native of FL who has seen many friends driven out of their homes, some after 3 or more generations in the same one, etc., by outside and ”easy” money, I empathize greatly.

And this is why we definitely need some sort of tax reduction or elimination for family homes to be stable places for our elders and our children going forward.

The property tax RAISE limits in place in various states are a good start IMO, but the ones I have seen and heard about obviously need both very careful editing and additional elements to provide a solid foundation for life, liberty, and the happiness of pursuit.

VV – the issue in my state is that there is no freeze on taxes, only on assessed value. The township raises the tax rate on the frozen assessment. Better than nothing but doesn’t solve the “sell your home because of increased taxes” problem.

I feel better too, Mi.

Yes. Some places in Northern Ca have a very very hard time getting volunteers for their fire depts because all the local younger people have had to move out. AND the lights are out in some downtowns- because foreign RE investors have bought everything up and do not live there OR rent them out. They just sit empty and rot.

It would be a good time for Homes not Jails to even the score.

I think what you are wishing for is called Karma and you should get your fill of that shortly from the looks of things

Nationwide home sales rose in May compared to April.

From Becker’s Hospital Review:

“Multiple Florida hospitals out of ICU beds amid COVID-19 surge,” by Gabrielle Masson, June 18

David Hall,

“Nationwide home sales rose in May compared to April.”

This is misleading BS for the brain-dead. There is always a seasonal surge in sales in May, of usually around 15% to 20%+ from April. This is part of the spring selling season. This year there was no surge at all. These are the not-seasonally adjusted numbers:

April 2019: 403,000

May 2019: 482,000 (+20% from April)

April 2020: 338,000

May 2020: 340,000 (+0.6% from April)

Duh!!!!!

That seasonal surge that didn’t happen this May is the reason the seasonally adjusted annual rate of sales dropped by 10% from April to May (from 4.33 million SAAR to 3.91 million SAAR)

Having watched and sometimes participated in housing busts going back to Houston in the early 1980s, I can tell you it always starts in condos. The low end consumer is where demand destruction begins.. same as this pandemic. All housing prices are based on the cheapest studio apartment and work the pricing system up from there, not from bill gates 50m

This is just another weight added to the balance rapidly tilting toward deflation.The Fed cannot let the property tax / bond and insurance fraud collapse.The Fed/Wall Street and Government grifter schemes have been fleecing home owners for years. The stock market is puny compared to this hustle. They are going to be forced to keep this bubble going . This fraud has been easy money. The Fed cannot allow deflation or game over for them. To prevent their demise they will destroy the economy at a rate much greater than it has done in the past with de-basement. This has been a gravy train with pensions to boot.

Real Estate industry was shut down in May – sales tanked – end of story. June so far is looking strong but there is still a lot of catching up to do because of missed sales in April and May. The masses are mistaken “bridge loan / aid” for “stimulus”. There is no “stimulus”. Only Desperate measures being taken Fiscal and Monetary to avoid a societal collapse. The whole working population has been placed on a fully paid retirement for a short period of time with money that is being borrowed from the future. And folks we cannot shut down a second time – not financially even close to a possibility. Soon reality kicks in … everybody counts their money … social tension rises once segments realize just how screwed they got in comparison to few who actually got rich from this (relatively) … fiscal prudence (or the semblance of it) returns … this will not be pretty.

Who, in their right mind, knowing this… would buy a home now?

‘And this time around, there is an additional wrinkle: Millions of homeowners, rather than defaulting on their mortgages, with 30 million people now on unemployment rolls, have entered into forbearance agreements with their lenders, where the lender agrees to not pursue its legal rights against the homeowner for non-payments. This too is going to be a mess for people who still haven’t found a job when the forbearance agreements expire. The market hasn’t even begun to wade into this mess.’

The ignorant will be punished for their ignorance (or their inability to understand what the above means….)

Around here PDX they might be moving to the burbs, but they are certainly not moving to the exurbs. In the last 3 months there has been a total glut of people selling horse estates, and small wine estates within commuting distance of Portland. For the last 30 years one of these 5 acre places complete with a mini-mansion with pool , winery and grapes or horse stables and arena plus 4 car garage and 2000 square foot shop has been the go-to for the well-to-do in the metro area. Now they are coming on the market at a record clip and they just sit there or have huge price reductions even though one of these places goes for less than a fixer upper in the bay area.

You are on to something. I spotted this trend in Toronto also. Suburban homes <$750,000USD GETTING SNAPPED UP exurb estates $3mil just sit. Trying to understand this trend. Found this article covers this issue in West Vancouver. Thesis is that wealthy Chinese buyers not able to travel to Canada to inspect the homes to buy. I am having trouble with that concept.

https://business.financialpost.com/real-estate/the-theory-of-immigrants-and-foreign-investors-driving-canadas-property-market-is-about-to-be-tested

I am in San Diego and I don’t like the urban feeling this gives me with match box size lots and bigger homes north of 1 million dollar or more.

I don’t see any impact on the ground yet. The inventory is super low and prices are holding firm or going up. The Mainstream media is all touting that the housing in socal would end this year with a high note. So, a lot of euphoria among people who are invested.

Let’s see.. Only time would tell..

This economy has fast become a depression for those buried in debt. Including businesses. Many people are already panicking about unemployment possibly ending soon. The buzzards are circling for so many people because the promised V shape ain’t happening. If the economy and home prices can boom without these 30+ million jobs and thousands of businesses, then more power to it.

My SF neighborhood in North Palm Beach County is selling like hot cakes. 4 miles from the beach, A schools, nice amenities, non member golf courses close by. HOA $150/mo includes cable and new high speed Internet. Large yards on cul de sacs. Every home on Realtor.com is listed as pending or contingent. Families are looking for yards!

Early days, early days.

Just a couple weeks back, half of the country was celebrating the demise of the virus…

Being early doesn’t always make you a winner.

The Fed’s now in a tough position. They can let:

1. Wolf, myself and a couple other guys shorting the market to profit or.

2. Start BRRRRing to infinity.

The RE Market here in Sonoma County is supposedly going to be rescued by people fleeing San Francisco.

What will they be buying?

And how many of them will there be?

We have the worst unemployment in 80 years here, Mortgage forbearance, eviction bans and Unemployment will all end by September.

And tourism is, if not dead, nearly so.

It’s not coming back soon.

We have lots of AirBnB properties in the county many of them owned by small time entrepeneurs who own multiple properties which they paid a premium for based on projected incomes that were 3-5 times what a long term rental would bring.

Short term rentals are allowed again, but there aren’t as many renters and several months of vital income have been lost.

Lots of headwinds, one tailwind.

It’s a PITA to sell a home right now, the property must be cleaned to CDC standards after each showing.

The same holds for home inspections.

Buyers are not going to pay for that, which means either the seller or the listing agent has to.

So you only show to highly qualified buyers and you absolutely have to pay a videographer to produce a quality video which can be posted on line if you want a sale.

House poor…

Sorry, but I just do not see a job market in the USA that supports ever increasing home prices.

How many new home buyers are confident that they can maintain their current employment status for 30 years to pay off their mortgage?

Garbage jobs a plenty somehow equates to a booming economy of course.

Wage increases and job longevity data should validate ever increasing home appreciation prices. Unfortunately, I never find articles that demonstrate that home prices are justified based on the underlying wage data. Magically, home prices continue to appreciate because they do.

The rhetoric that Small business is the backbone of the US economy is such a joke! 30 – 40 million American’s loosing their jobs should be crippling to the US economy, this has not proved true. Corporation losing billions should be devastating to the US economy, where is the evidence?

Debt is the US economy.

economy vs. people

It is devastating individual lives. People are lining up around the block for food. That’s what gets me about economists. They are all about theoretical shit, and “the evidence” is not in theories or in “the market” or in “the economy”. I suggest you do a little looking around George, for real effects. This has happened over and over, and I have been affected by every downturn in my lifetime.

It looks like banks lend their money to house flippers because the real estate is a collateral considered good enough.

And that is about the only real economy sector of interest for them.

Otherwise it is much more convenient to press the buttons moving the money between bonds and stocks. Very liquid, low transaction costs.

As for SME being the base of real economy – I’m still convinced of that, at least there is a obvious correlation between SME and the state of “real economy” which is a vague term.

People buy overpriced houses because they know that they can squat there for 5 years without being evicted. There are some things you can do to stop an eviction and foreclosure. There’s free money from taxpayers (via keep your house) blah blah.

There’s programs, and laws to keep people in their “homes” without paying the mortgage.

Well, I know of a sweet deal in central Vermont, if anyone is interested

I absolutely love Vermont My Uncle was a Veternarian in St Johnsbury when I was young and spent a lot of time up in the Northeast Kingdom It’s gotten alittle too left wing for my taste lately though

well, do let me know.

Well, I just bought a condo in San Diego County, Wolf… fractional that is. I’ll be in California two weeks every other year. Actually a repurchase, as I had sold a larger interval in 2016. Purchase price $250. Original price would have been $35-38,000. No one wants to pay the maintenance fee. I like every other year now, as it splits the fee in half, and it hasn’t inflated that badly….

Laurence:

How do yearly maintenance and other fees compare to say just staying 2 weeks at a hotel?

The COT report published last Friday shows record short positioning by dealers in the Euro contract. To me, this is the cheapest and safest way to short the market: short the Euro and hope that the dollar gains in strength as the market falls. Looking at history, I believe dealer positioning in the foreign currencies is one of the only reliable indicators of future price developments. It has worked well for the Canadian Dollar, Australian Dollar, Euro, and Mexican Peso.

I am now short the Euro as of a few hours ago.

May closings were from deals done during the stay at home orders. No big deal. July closings will be a much better story.

The foreclosures have not and will not begin for at least another 6 mos.

The people who are going to lose their homes will ride the free train as long as they can. The people who are trying to get out now, are probably fully mortgaged and just trying to save their credit, but cannot afford to sell below market due to not having any equity. You will not even begin to see the effects of what is happening for at least 6mos. and it will continue for probably 2.5 to 4 years if the past housing crashes are any indicator. My last short sale purchase in San Diego was in 2012, a full 4 years after 2008. The bank lost 200K on the deal and was not happy….

Anecdotal: in SW Florida, I knew people who hadn’t made a payment since 2009 who still had their house in 2016. The bank didn’t want to put the loss on the books until they had to, and the costs of maintaining an empty house could be close to $1000/mo.

Trade deal over

“It was at a time when they had already sent hundreds of thousands of people to this country to spread that virus, and it was just minutes after wheels up when that plane took off that we began to hear about this pandemic,” Navarro said this afternoon

It’s starting to look like WR is psychic. His first short was followed by news of the virus going mainstream. Now days after his second announcement, a high WH official accuses China of an act of war.

I’m not even going to ‘qualify act of war’ by adding ‘virtual ‘because ‘sent hundreds of thousands to this country to spread that virus’ is unequivocal.

So the second hole is shot into the market balloon while the first hole is still leaking helium and getting bigger.

Oh! Surprise! Navarro is trying to walk it back: says ‘trade deal not over’

What an idiot. When you have a position you think before you speak.

But then…

Nick,

Do you suppose Navarro and his putative boss guy are doing this kind of manipulation of markets deliberately so they and their masters can profit or position their portfolio according to what everyone knows is going to happen sooner or later.

While hopium seems as endemic as this virus these days, if memory serves, there has always been some sort of manipulation by the big boys, well publicized by MSM as now, to lure the moms and pops into markets before the inevitable crash is allowed. (Was ”in” SM from approx 1956 to 82.)

Danielle Martino Booth, x-Fed Reserve, was interviewed on the Quoth The Raven podcast a few days ago. This topic is covered ~ towards the middle. She went into the timeline of the trade deal, terms, other factors including international vs domestic flight restrictions. They absolutely had to know by early September.

Glad I didn’t buy in the Twin Cities – all the cool restaurant areas are burned down, all the new apartments downtown are empty and boarded up – with Now Leasing signs still on the sign of the buildings (so much for those expected $2,500+ a month rent). All the offices all shut from COVID and now boarded up from riots and all the small businesses that supported by them have gone under. Tons of shootings nightly – coming soon to a city near you. Apparently been a massive number of listings in the metro.

The facade of Everything cracked – the young adults who didn’t own anything were never invested snapped, the system kept pushing people around, and from where I am and what I see – it’s only the beginning.

Coming soon to a city near you.

I warned another commenter, on this site, that would be the case. He too lives in the twin cities. This criminality affects the demographics of a city in a negative way and lending and insurability dries up really fast.

All the insurance claims drive up the price or they just stop insuring in those areas. The data is shared or purchased by lenders, who stop lending in those areas as well. It’s a downward spiral.

There are boroughs in London which are both highly criminal, with immigrants of the very worst type and a lot of gang violence (not so much shooting of course as in the US, more stabbings ) and in which real estate prices have gone nuts since 2011. People just had to buy those 19th century houses which actually have decent gardens.

It will, given the permanent high unemployment which is the future of those boroughs in the wake of COVID, be most uncomfortable for those who have bought there, mostly young professionals with families.

One of these boroughs is the only place I have ever seen a dead man with a knife sticking out of his back, in broad daylight in the high street, and that was 20 yrs ago – it’s much worse now.

Many of these people who were involved in the riots and looting now feel empowered, and nothing is more addicting than power. The cops are angry and for the most part now standing on the sidelines and letting crime get out of control to prove how necessary they are. Things in the cities I fear are going to get a lot worse before they get better. If the elections do not go their way, things could go really sideways…..

I am really glad I am where I am…

They may get a lot worse before they get apocalyptic It’s a possibility we shouldn’t ignore

Thanks for pointing out the decrease in sales that NAR never mentioned.

It might mean something, unless the property buying REITs and foreign money people get backing. If they don’t- maybe less people will be homeless. And rioting.

Here in rural northern Ca the new entries on the market to houses sold are 3 to 1 and more some weeks, but asking prices haven’t gone down. They’re waiting for foreign buys to come back.

2 towns are selling like hotcakes- but they have for years. There seems to be one investor who buys up much of the housing. I think it’s a foreign buyer with a local address. Maybe he’s fronting.

The Tampa Bay area is hit hard.

“Pinellas’ sales were down 46 percent compared to May 2019, while Hillsborough saw a 28 percent drop and Pasco slipped by 32 percent…

Also unlike April, these drops affected nearly every price range…”

And perhaps most interesting:

“Local Realtors attributed the drops both to sellers’ hesitancy to allow strangers to tour their houses as well as buyers’ fears about financial stability.”

https://www.tampabay.com/news/real-estate/2020/06/22/tampa-bays-may-home-sales-saw-steepest-declines-of-pandemic-so-far/

I follow the prices in a few Florida cities, they are all overpriced. Reminds me of 2005-2008.

anecdotal local hood stpt report bmc:

a house just down the street sold early, buyers could not finance with new limits; sold again and closed last week at the same price; it was last one of any size until one couple block away with pool was listed last week for at least double what it was worth last fall (IMO)

and the ”tearer downer” a couple blocks away is now down, and apparently the new house to be built there, with occupancy in about 9 months is already sold…

certainly seems to be a WTF moment hereabouts,,, only thing i can think is that a lot of folks are anticipating high inflation, or very high interest rates as per late 1970s, and are attempting to ”hedge” with RE.

fortunately, we are ”homesteaded” with the elderly bump, so in spite of our yearly appraised ”market value” tripling in 4 years, property tax raise is limited

Agree with you things are crazy here! Off the hook RE market in Ottawa Canada. Starting to think its an inflation hedge as well. Should not have sold one of my rental properties in May. It has already gone up in value by about 10k comparing it to a few that just went on the market and sold within a few days… The lesson i learned is dont give into the doom and gloom but instead listen to your gut. My gut at the time was telling me housing would go through roof with all the printing going on. I even told that to a friend with properties in Toronto then i turn around and sell one of mine. My cash will end up trash unless i put it into the casino (stock market). Wish i held the RE.

Don’t fret. I am in the exact same position. I sold 4 rental properties in Phoenix as fast as possible April and May. Too early to tell if we were wise or not. USA / Canada in fantasy land right now. Canadian historically high Fed deficit $20bn blown out to $200bn doesn’t include BOC inflation created from balance sheet. Remember the Flow Of increased credit can boost and ASSET price – but that flow must be continuous and must be expanding in order to sustain and propel the asset price higher – that price will come down when the flow moderates or stops – that’s the Point of Wolff’s article – Fed Res is slowing the flow into asset pools

The headlines say home sales SURGE. One said they dropped but that was the bottom, so all of them are saying BUY. This process by which markets self propagandize themselves is fascinating. The amount of positive weight attributed to the presidents tweets on the stock market is comical. Of course I remember 43 repeating his mantra, “the economy is strong” right up to the GFC. So they all get paid to say it. The MSM used to comment on the economy (disconnect) but lately not at all. A bull market in stocks speaks for itself. Miracle as noted the Fed chief has used very little of his ammunition. He probably never thought he could save the world by jawboning markets. The markets by turn take it that there is still a lot of juice left, and lean into it even harder.Really amazing that the catalyst was a crisis not some amazing technological breakthrough. I don’t like real estate because houses haven’t changed in several hundred years, and waiting for Elon Musk to show me the way.

Your right they sure havent changed much- but they surely went up in value!!

of course i cannot say much about ”several hundred years” AB, but i can say a ton about the very clear differences in the vast majority of houses built in FL since i started working to build them in 1951 until today..

the house we own was built in 1950, a ”good solid block home” of the day,,, with NO connection between roof and foundation which is sin qua non these days just being the first very clear delta…

from the foundation up, houses in FL and CA and OR and TN and AL and CT that i have personally been involved in the manual labor of building are SO much better built today to withstand the weather, especially the extreme weather events that are now understood to be the usual/regular.

after the the quake in SoCal in ’70? that took down the VA hosp as well as miles of the freeways, the codes began to change to deal with the realities; after the loma prieta in 89 they changed even more and even faster,, similar in FL after Andrew in ’92 opened the can of worms, especially the corruption, and then the confirmation of the changes in 04 where houses built to the new codes lost a few shingles while the old house next door was leveled…

Been trying to get the ”better half” to let me build her a modern house that if cannot be actually ”hurricane proof” can at least be majorly resistant..

And, trust me, you don’t want to even think about the very very major changes to the electrical systems, HVAC, even PB systems of recent houses versus even 50 years ago,,

To keep up, you must flip MSM over upside down. It now reads WSW for We Sell Widgets. Print or electronic, it’s all just “air time”.

I live in PA equidistant from Philly and NYC. Our housing market is on fire right now. People are fleeing NY / NJ in droves. Housing here is substantially cheaper, as are the taxes. May numbers were down here but that’s because in most counties no one was able to show or sell houses. June numbers are going to be much, much better.

AZ must be backwards.

Home sales here are HOT! The realtors for a house on our street had planned an open house, but then canceled it, and now there’s a “Sale Pending” sign hanging.

The Chinese Virus is down nationwide but spiking here, even though heat is supposed to kill it and it’s 105° outside right now.