Fed leads in trimming its balance sheet; Bank of England governor publishes the reasoning for central banks to shed assets – before raising interest rates. A big shift!

By Wolf Richter for WOLF STREET.

The Fed has been cutting back for weeks on its asset purchases, and on its last weekly balance sheet, its total assets actually fell by $74 billion. Now Bank of England Governor Andrew Bailey published a piece on Bloomberg Opinion today in which he wrote that these massive central-bank balance sheets – he was talking in global terms – “mustn’t become a permanent feature.”

“As economies recover, it’s likely that some of the exceptional monetary stimulus will need to be withdrawn,” he said. And this shedding of part of the bonds that had been purchased would happen before the central bank raises interest rates, he said.

This is the opposite of how the Fed did it last time: It started raising rates in December 2015 and started shedding Treasury securities and MBS in October 2017.

This time, the Fed front-loaded $2.8 trillion in QE and has already started shedding some of it even as FOMC members don’t see interest rate hikes through 2022. This is a big shift, of reducing the balance sheet first, and then raising rates.

In Bailey’s piece, there was no word of negative interest rates or yield curve control. What he is saying is that the balance sheet became the primary tool for adding stimulus and will become the primary tool for withdrawing stimulus, as interest rates remain near-zero.

And he is saying that the BOE’s balance sheet isn’t going to stay this massive for long and that it will undo some of the accommodation as the economy figures out where the new normal is.

The Fed is leading. The BOE is publishing the reasoning for other central banks to do the same.

Bailey started out doing the same thing that Fed chair Jerome Powell has been doing for weeks: patting central banks on the back for the massive money-printing binge that was designed from get-go to make sure asset holders wouldn’t have any skin in the crisis, that they’d get bailed out lock, stock, and barrel. Bailey emphasized how important it is for central banks to act independently and freely to bail out whoever they want to.

Central banks have “made big decisions and implemented them rapidly in the face of an unparalleled crisis, coordinating with governments to maximize policy effectiveness,” he wrote. “This capacity to act must be reinforced and not mistakenly called into question.”

Yup, don’t even think about reining in central banks. And suddenly he pulls the rug out from under any hopes for QE infinity.

“But the financial system mustn’t become reliant on these extraordinary levels of reserves,” he said.

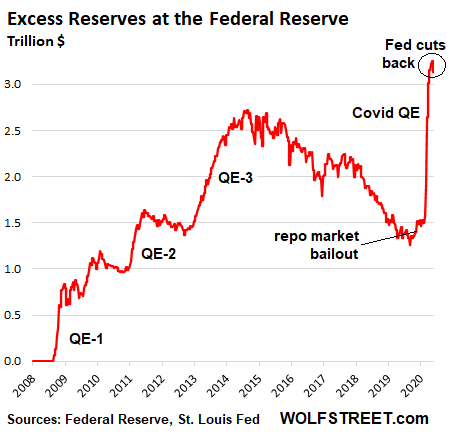

Asset purchases of all types – such as the Fed’s buying Treasury securities, MBS, corporate bonds, junk bonds, and the like – end up in a huge pile of assets on the Fed’s balance sheet, and they also engender a huge of pile of “reserves,” which is cash that the banks have put on deposit at the central bank, and that the central bank carries as a liability.

For the Fed, “excess reserves” have surged during QE-1, QE-2, and QE-3. Then they began to unwind through mid-2019. This includes the period during which the Fed began shedding assets. During the repo market bailout starting in mid-September 2019, these reserves rose again – and that was one of the stated solutions to the repo market issues. When the repo market bailout ended on January 1, 2020, reserves flattened. Then in mid-March, the Fed unleashed the money-printer’s fury, and reserves skyrocketed:

These reserves held at the central bank, that resulted during the asset-buying binge, “are the ultimate liquid assets,” Bailey wrote.

“But the role of central bank reserves shouldn’t always be taken for granted,” he said.

“Rather than having to keep relying on central bank support for all aspects of the financial system, we need a robust assessment of the latter’s weaknesses,” he said. “The role of money market funds, and the risks to financial markets that they posed at the height of the disorder, is one area to examine.”

“Finally, the current scale of central bank reserves mustn’t become a permanent feature,” he said.

“As economies recover, it’s likely that some of the exceptional monetary stimulus will need to be withdrawn, including by reducing reserves,” he said.

But there are limits as to how far the balance sheet could be trimmed. “This wouldn’t take us back to the very low levels of reserves before the financial crisis, which sometimes failed to recognize the role they play in ensuring the stability of the financial system.”

Central-bank balance sheets need to be trimmed down because “elevated balance sheets could limit the room for maneuver in future emergencies,” he said.

And the big shift: Reduce the balance sheet first, before raising interest rates – which is the opposite of what the Fed did last time. Now, according Bailey, the BOE at least would do it in the opposite direction:

“When the time comes to withdraw monetary stimulus, in my opinion it may be better to consider adjusting the level of reserves first without waiting to raise interest rates on a sustained basis,” he said.

And the fact that he didn’t even mention negative interest rates indicates that the BOE is not seriously weighing them, after the Fed has already taken them off the table.

The Fed shifts to propping up consumption rather than asset prices, and its total assets decline. Read... Fed Ends QE, Total Assets Drop. Liquidity Injection Ends

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Fed is worse than me when it comes to budget. Zero discipline.

Plans, and more plans, not to mention the fact that decision makers could change later this year. How can they resist printing to keep interest rates down and to control social unrest?

(Mutters “Not this again?!” under his breath)..mate, low interest rates are not controlling social unrest, they are creating it. How did you ever come to believe otherwise? Cognitive dissonance? For the millionth time, low interest rates cause skyrocketing asset prices which locks people out of not just home ownership, but an equal place in their own society. Also, investments which rely on compound interest to grow are neutered.

In addition, they enforce poverty on people that steals their freedom, their hopes and their dreams. Such is the situation in third world countries. This also makes libertarian predictions of the government enslaving you sound all too credible.

These are all bad things and make people desperate. They have no stake in society, they do all the shitkicking jobs and all they get in thanks are cops on their ass night and day. Thus, they riot. Have you got it now?

Wooh fat chewer he’s right and you’re right.

Raising rates would bring social unrest and economic armageddon.

Of course the continuation of these asset price inflating policies does bring social unrest and eventually something really bad …

Am I right ??

Excellent point, when I discussed this with some friends, they called me a socialist. It’s just common sense in a democracy. If common sense is socialism, then, yes, I am a socialist.

One more point, what’s going on right now is a “rebellion”. If you are 0.01%er or are, like I was, a professional attending to the 0.01%ers financial needs, be afraid, very afraid down the road. More to come in the next few years!

Here are some simple ideas that could help our troubled world.

End the Federal Reserve and allow market forces to set the cost of capital

Move away from fiat currency to one that is backed by gold and or other national assets

Eliminate the income tax and move to a system that derives revenue for the state based on usage fees. For example, transportation using public resources would pass their costs on to consumers

Decriminalize the usage of currently illegal ‘drugs’

Eliminate laws that are in place that do not directly protect individuals and their property i.e. get rid of laws for victimless crimes etc.

Get rid of public sector unions including those that fight against change in policing and education

Have a citizens’ oversight boards for every law enforcement agency

Provide equalized funding for K-12 education and allow said funds to be spent at the will of parents – have competition for the current K-12 state run school monopoly

Enforce claims against the state when it violates the Bill of Rights

End all state subsides to corporate and non-profit entities

Well said!

Amen

Hmmmm…..

So….time to short the FTSE? :-)

“The Fed is leading. The BOE is publishing the rationalization for doing the same.”

Like I posted previously…if…IF the Fed insists on making the stocks go up, better it should just buy stocks and be done with it, rather than stinking up the whole world wide darn economy and pervasive redistributuib of wealth in every corner with ZIRP and QE.

Maybe someone could mess with the Fed by creating an etf that bought or sold the sp500 based solely on monetary policy. Call it SP500FED. Their marketing could be “Fundamentals are for losers”.

The intermediary transactional costs of making the stocks go up with QE & ZIRP are phenomenal and QE and ZIRP carry with then highly socially destructive affects. The transactional costs of buying stocks are minimal. The Fed should just buy the darn stocks and end the charade.

Much better: let the equities and real estate market collapse. The environment needs American households to stop consuming like drunken sailors ASAP. Nothing is more effective than a massive double crash to achieve this. We will all benefit from a livable planet.

Siberia is burning as we speak, it’s almost game over without a double massive crash that forces Americans’ consumption levels down to South American levels. There’s no other way.

Sure there is. People will continue to survive, even thrive, if the planet is a degree warmer. It already is now.

Yes, that’s what should have been done 2008-2009.

But if you don’t throw the the banks a bone with the transaction fees, how could they survive? They would have to offer 24% revolving credit instead of 22.99%.

Fed shouldn’t be buying stocks either. What needs to happen is all mega holders need to call their hand. Who is solvent, who is not solvent and who can become solvent is the question. Those not solvent need to be declared bankrupt and the company goes into receivership on behalf of the bond holders. The bond holders should have a chance to reorganize the company with different diectors and executives. Those who can become solvent need to enter into high dose mediation between their bond holders and creditors to come up with a plan to get the company back on track. If bond holders dont meet the goals of the mediation agreement, they are declared bankrupt. If creditors breach, monetary offset on the debt.

All of this financial manipulation eventually leads to civil unreset and war because the imbalances affect every day life, every moment of every day. We have been seeing this play out in real time over the last 20 years, not to mention 2020, the year of years.

When you say negative rates are off the table, do you mean for the “foreseeable” future? I find these things off the table until they become suddenly on the table.

When rates eventually rise what happens to their massive treasury holdings, lose value on the longer dated issues?

Looks like the fed, with coordination from the other important cbs, are trying to find a sweet spot with regards to how much excess liquidity is in the system. Might expect to see weeks of shedding accompanied with weeks of expanding over the next year.

Its hard to tell which way it goes with central banks effectively conering markets across the globe.

Pretty much what you say. These central bankers are the ultimate headfakers or should we say liars? Its been that way as long as I can remember. Look, the sky is falling, so ordinary folks tighten the belt, while the insiders buy everything in sight. Like those same insiders telling you that SS is broke, and you’ll have to manage without, but they can come up with 3 trillion to save the rich.

John…….you nailed it pal.

Hear hear!

SS is broke. This massive money pit they have unleashed will cause consequences. One of which you nailed. If the government is always able to find another Trillion here or there what really stops them from funding WHAT EVER THEY WANT that day/week/month/year. What excuse do they have for putting all the senior citizens on food stamps when they have proven that they will print when it is comfortable

Trump could be one and done and the Fed is likely adjusting to this new reality.

I do not like Trump and I definitely do not like Biden.

The Federal Reserve is standing on a mountain of US debt and desperately must reestablish it’s primary directive as the central bank of the US and the world.

Jerome Powell must be replaced as his decision have been obviously compromised. The autonomy of the Federal Reserve must be restored.

As much as I can agree with your choice of candidates your comment that the FED’s autonomy must be restored rings untrue as it suggests it was autonomous prior to Powell. The FED has always had an agenda that was not beholden to the “people”.

Wolf, let me save you some trouble with my updated Hawk-O-Meter, which I call the Talk-o-Meter, a BASIC program to predict Fed action.

1 If stock_market does not equal ‘tanking’ then talk

2 Else If stock_market equals ‘tanking’ then print

3 Goto 1

For an example of the ‘talk’ outcome, see this post. For an example of the ‘print’ outcome, well, we all know what that looks like.

I don’t think the Fed is intentionally stopping QE at this point. The QE schedule is still there and the Fed is asking for 500 billion a day. The QE repo failures we saw last week and this week are due the fact that the banks ( primary dealers ) do not like new bid rate and don’t bring any collateral to the window.

>>and the Fed is asking for 500 billion a day.

Huh?? That made no sense.

Raise interest rates? I’ll believe it when I see it. How Can the Federal government possibly handle higher interest rates on their debt “out the wazoo”? I think he’s blowing smoke.

I’m not sure this applies with the BOE, but it certainly applies with US debt. Though it must be said that this may not be dire as the numbers show, as the FED simply just gives the interest earned back.

Though to be a contrarian to my own thoughts, while the interest can be given back, if the fed is to shrink the balance sheet, it has to accept the currency from the treasury in order to take currency out of the marketplace. This is currency that will not be able to be invested in useful places that will propel more growth.

I’ll call it a circus.

I have to agree, as much as raising rates seem to make sense, JP has all but ruled it out. He cut last year when there was no reason to. He could have conserved firepower in February and March, but he didn’t.

Now we have to wait.

“As economies recover” since when ? What standard or specification reflects “recover”. Bernanke basically said the same thing after 2009. He trotted out the Big Lie in front of the whole world nearly a decade ago that this was all just temporary and the Fed would be withdrawing liquidity and “normalizing interest rates”. Jerome tried and failed and then reversed course.Only a fool would now believe the BOE or the Fed can “normalize” interest and withdraw liquidity , no matter the sequence .Do the simple Math , their Debt Machines have done their damage.The BOE and the Fed are doing a check to see how many suckers and fools that will believe a past fairy tale. They are trying to buy time. The Fed and BOE have ruined their respective countries economies.Their respective governments have aided and abetted the fraud.The Fed and the BOE are going to be wounded by deflation first ,then die on the sword of inflation .This matter is quickly slipping out of their control. It will be taken to the streets.

AS long there is ‘confidence’ in fiat of Sterling and Us dollar’ the SHOW of EXTEND & PRETEND’ will go on. Rhetoric is the entertain for the masses!

Remember jawboning technique!?

Gold and Gold miners are inching up, every day!

“As economies recover”

Yep … there was no recovery post GFC…. there was just more and more and more and more stimulus.

And then we got covid which was a fantastic excuse for nuclear stimulus.

It amazes me that people are still hopeful…still believe the BS.

Step back and look at this picture. How many businesses GONE – forever… massive numbers of unemployed and on UBI…. mortgage holidays are epice… as are other debt holidays….

There is NO way we can ever recover from this. The global economy has been smashed to pieces and is on life support. It’s barely registering a pulse.

This is not something you recover from. The Central Banks are pretty much done… they have mainlined BAU with trillions of gallons of morphine ….

And most of the 8 billion people on the planet are in a drug-induced daze… clueless to what is really happening .. and hallucinating about an economic recovery — any month now.

Correct. None of the impact of these once “extraordinary” measures can ever be gauged until fully wound down. Much easier to extend and pretend and let inflation silently do it’s work.

They will raise rates

…. to defend the currency.

But when you need to resort to such measures, it’s pretty much the end.

Mr. Powell has already declared NO RATE increase until 2022. No need to defend the currency. The US $ is the least dirty shirt sought after everywhere in the world. US Treasury bond is the largest with liquidity unlike other bond mkts!

Who wants YUAN or the Ruble?

Even if the China sells it’s treasury tomorrow, it will be mopped by the rest of the Countries where Trillions are in NIRP!

Least dirty shirt amongst filthy fiat perhaps I’m trading all mine in for real wealth as soon as I get it And no, I don’t mean Bitcoin

Did that, starting 43 years ago (used debt leveraging during the startup period, limited by non-greedy judgement of when “enough is enough”). Now continues with every fiat dollar I get and don’t need to spend on necessary consumables.

It will eventually go to my kids, since taking it with me would corrupt heaven and be useless in hell.

There are more than one reasons for high liquidity. But for one reason counts this: high liquidity is needed if you intend to get rid of something as soon as possible. That is when you don’t trust it to hold it for long. In things you do trust, you don’t need high liquidity.

Rubbish. Just because no one wants Yuan or Ruble does not mean that there are no better currencies out there. How about Swiss Francs or Norwegian Krone.

Both of those countries have Debt to GDP at around 40%.

You forget the USD has lost more than 90% of its value.

How can anyone think interest rates are going to go up? Too many powerful people owe too much money . Rate rises will cripple them. Therefore rate rises will not happen. It is the same with US$ losing value. 70% of US$s are used as currency in foreign countries whose citizens have zero confidence in their own currencies. It will not lose value until this confidence has gone.

Sit23:

That’s why the US has 12 aircraft carrier divisions constantly prowling the world!! LOL!

Raising rates at the low end would be consistent with YCC policy. Just have to wait and see.

“Finally, the current scale of central bank reserves mustn’t become a permanent feature,”

They have been talking ‘the same, again & again’ since 2013 and NOTHING has changed! Fed is trapped by it’s own design.

I just watch the chart on BlackRock Corporate High Yield Fund, Inc. (HYT), HYG and LQD. Actions speak louder than words!

LQD is just a dollar below it’s 52 week high!

Fed just CANNOT afford to abandon the Corp credit mkt at this point and to the end of year or till GDP goes positive territory!

If the Corp credit mkt cracks, there goes the Equity mkt!

When you are facing the Long Emergency …. you do whatever it takes.

I am not expecting a withdrawal of stimulus. Ever.

Follower of Peter Schiff huh? He says the exact same thing and has been proven right over and over again

I live in Turkey now and yes there is always someone who wants to acquire your gold I bought it at the gold exchange in Istanbul and I can sell it there as well

Peter is 100% correct about owning gold It cannot be inflated away by bankrupt central bankers

By the way gold is at an 8 year high as of right now and on its way to much higher numbers In USD anyway

These crooks will never stop stealing and the worst part of it all is the media puts out the mantra that high interest rates=bad, low inflation = bad and continually uses the phrase ” pumping money into the economy”. There is no criticism, no discussion and only celebration that the typical mortgage payment might be coming down £3 a month. Forget the shrinkflation, prices of items that aren’t in the inflation basket like housing FFS!

To my knowledge this bullshit has been going since around the mid nineties. However, i suspect it has been going on for much longer than that, i just had better things to do back then ;)

For someone who has just had their upteenth letter saying my savings account interest rate has been reduced to 0.05% is the ultimate kick in the teeth to someone who has done what my dad would have called ” the right thing” by saving for the future.

You still have the money you saved. What you are lamenting is that you don’t get to continue to ride for free via interest. Go out and work some more if you need more money.

“You still have the money you saved.”

You are not considering inflation.

Inflation is at very low levels for ordinary living expenses. Yes homes and medical costs are too high, but that is a problem separate from interest rates.

I am not saying that I don’t think that people who work hard and save should lose their equity; but I think it’s possible even in low interest environments to save enough, you just have to work and save enough to cover your costs of retirement without relying on savings rates.

It’s what I plan to do. I’m going to save enough that I am not counting on savings interest to carry me to the end. And I fully expect to have to do some work if I run low.

hey Z,

don’t know where you are finding low inflation for ”ordinary living expenses” but certainly not true in FL state in USA, where I am back again to support taking care of my 90 yo mil, 75 years since my start here.

Besides the house ”market appraisal” triple in 4 years: gasoline is approx 9-10 times what it once was, same for motor oil for car; a simple bicycle is same or more, not to mention fancy ones; used to buy a loaf of bread for $0.10, yeah, a dime; used to buy a coke for a nickle, pepsi too; used to buy a quart of fresh squeeze OJ for a quarter; we used to buy six shopping carts of groceries for the price of one 60# bag today,,, etc., etc…

Now, don’t get me wrong, some things, usually intangibles such as sunsets are still the same price and just as good as ever..

Everything else is at least triple just a couple decades ago, and very likely to triple again sooner with all the financial malarky we are seeing these days.

Better prepare for massive inflation right after the depression coming sooner…

They pretend they know what they are doing and that they are in control. He probably knows that they cant raise interest rates ever again. So he is lying as Jay Powell was in his infamous 60 Minutes interview. It might also dawn on him that their “policy effectiveness” was and is ZERO. “Adjusting the level of reserves first” is just talk, since it has no consequences for the real economy anyway. Even in the competence free zone at CBs it gets more and more difficult to ignore the “effectiveness” of their policies in Japan and the EU.

Back in the days every schoolboy in France was taught about “Les Dernières Cartouches”, an episode from the War of 1870: as French resistance was crumbling during the Battle of Sedan, a group of marsouins (French marines) fortified a hotel (Auberge Bourgerie) and, together with stragglers from other broken units, kept a whole Bavarian regiment pinned until they had just eleven cartridges left between them. At that point the surviving officers demanded the honor to fire those last cartridges, with the final one fired by commandant Arsène Lambert, the highest ranking officer still able to hold a rifle.

The French defenders narrowly escaped being summarily shot by the Bavarians, who had been under fire from local francs-tirerurs organized by the Abbé Baudelot and were in no mood to take prisoners, thanks to the intervention of the Bavarian general staff, highly impressed by the canine courage of commandant Lambert and his men.

Central banks, after over a decade of needlessly firing their cartridges in all directions to squeeze every last ounce of growth right now instead of waiting a couple of years, are now in the same position as those brave marsouins: they have a handful of cartridges between them and face a horde of angry enemies.

The big difference is commandant Lambert and his men bravely exited their improvised fortification to face the consequences of their actions and met an enemy who had to reluctantly concede they were brave men indeed.

Central banks instead have not even the courage to tell politicians who have promised trillions of dollars in “stimulus” to cover their own panicky overreaction to go and face the music: to give an example the Italy treasury will have to find buyers for a mind-boggling €500 billion in newly minted debt in H2 2020, and that total doesn’t include the promise made yesterday to slash VAT for “at least €10 billion” since “the economy hasn’t restarted”. Call me not surprised.

It’s obvious these hapless politicians expect central banks to merely wave their magic wands and make all that debt go away, and without causing consumer inflation. People tend to get restless when vegetables and milk go up in price faster than their wages and pensions.

When the executives of a company prove themselves to be “fools and knaves” shareholders usually send them packing without much ceremony. Our whole leadership worldwide, weakened by a decade of complete complacency, has proven to be nothing but a bunch of fools and knaves, and I am still being gentle.

It’s nigh time to send them packing.

I always enjoy your comments, MC01, but you’re at your best when you get really pissed!

The Federal Reserve is not out ammo. That s not true.

They can at every moment stop any inflation dead in the track.

Inflation is when the sum of Debt in the economy rises faster the the real GDP. This causes Demand too surpass Supply. Prices are rising.

By the way: QE is not inflationyry because it first increases the monetary base. I could be when banks follows to spur credits to biz and consumers. But only then.

But Gouvernment debt is inflationary. Ofcourse it creates demand out credit. The Fed can stop the Gov with interest and the banks additionally with rising reserve requirements. The FED would be very restricted if Reserves reach one day 100% (all debts monetized). This is the precondition for every Hyperinflation. But this could be the cases if trust in the value of cash and deposits wanes and everyone rushes in foreign currency, assets or anything but cash. the explosion of money velocity is then the dead of a currency. But its not as near as some hope here. ;-)

The Fed wants asset prices to inflate. This increases the taxes on the house you live in . If you have public utilities to your house that is also an asset and both are a cash cow for Wall Street and the bond market. The Fed does not give a damn about the 40+ million or whatever the number is of un-employed. They are our problem if they live in your county or state or in your family.The Fed and Wall Street and even our own Government is de-coupling from the America that does not en-rich them directly. Look at governments indifference toward property owners and businesses including the denial of public rights of way in the occupied riot zones.The Government has made sure that Americans have not gotten their share of Productivity Gains in the form of wage gains for decades.Instead those gains have by-passed the inflation mechanism of the wage earners economy and went directly to Wall Street. The fools talking on the nightly news ain’t the ones paying the bills.

It can’t be done. For interest rates to rise in Australia, wages would have to significantly increase and the cost of living would have to significantly decrease. Otherwise, it would send a large proportion of the middle class to the poor house. Now, how exactly do you arrange that with monetary policy alone, since our politicians are acutely aware of the electoral ramifications of even a breath of change to the status quo? “Oh, I know, I know, sir! More infrastructure on the credit card!!” More rorts for the elite. And the beat goes on.

“Now Bank of England Governor Andrew Bailey published a piece on Bloomberg Opinion today in which he wrote that these massive central-bank balance sheets – he was talking in global terms – “mustn’t become a permanent feature.”

I’ve read more more believable bedtime stories to my kids.

Whatever happens they’ll kick some kick the can along and a new paradigm will emerge.

Get ahead of it.

Be widely hedged now to avoid disappointment.

Wide hedges just block the view.

The question that no one seems to be willing to ask…Should we hold all debtors, top to bottom, accountable for their own actions and allow final settlements to ensue? Savers holding hard assets in hand would benefit from allowing land values to collapse back to the real level where the land is worth what it can generate as farms or factory sites. Why the hell should we worry if the so called middle-class, living on inflated wages and financing a lifestyle on mere expectations that what they do holds importance, should end up bankrupt along with the overextended firms that they work for? I don’t care if you are Warren Buffet or Joe I.T. or Doctor Feel Good. If you don’t have hard assets to pay for it as value drops, you have no right to claim that it should be yours because you once lived as though you were better than the guy who scrimped and saved. Time to evict all the damn deadbeats and fools who think their stocks and bonds are money…smart ones would get themselves out quick before the musical chair game came to a pause. Then we’ll see things run by people who don’t kiss ass to market manipulators and interest charged and paid out might come back with real meaning. Tough sh*t debtors!

Buysome:

Suggest you and others familiarize themselves with the music of the “1812 Overture” and why it was written…….it will surely be the background sounds as the citizenry come for those who have sold out this country pointedly since WW2.

The politicians, the bankers, the brokers, the dirty shirt paper salesmen, the union busting legal firms along with their street thugs….and on, and on……prepare yourselves!

“As economies recover, it’s likely that some of the exceptional monetary stimulus will need to be withdrawn…”

What a joke.

There was no recovery after 2008, and there will be no recovery from COVID at all–this is a new paradigm being forced upon us. The central bankers are signaling the fact that they are going to let it all fail to so that the “reset” can happen, as planned.

Hi Wolf,

I’m a bit confused as this analysis does not match what the Federal Reserve has stated it will continue to do:

“The Fed also said it will continue to increase its bond holdings, targeting Treasury purchases at $80 billion a month and mortgage-backed securities at $40 billion.”

https://www.cnbc.com/2020/06/10/fed-meeting-decision-interest-rates.html

While some components of the balance sheet such as Repos may decline, won’t the Fed’s planned purchases of $120 billion a month be greater than the decline in some components? Even if the Fed slowly reduces the planned purchases of $120 billion a month, the balance sheet will continue to grow for some time.

Steven,

Yes, agreed, you’re “a bit confused” — by the braindead media coverage of the Fed. You sound like a first-time reader here, so welcome to WOLF STREET. But you therefore have not seen any of the analysis I do regularly of the Fed’s actual balance sheet.

You need to look at the Fed’s actual numbers, on the Fed’s balance sheet, and you need to understand how a huge bond portfolio works.

The Fed has a $7-trillion portfolio of securities. These securities mature on a given date. This includes 30-day Treasury bills that mature every 30 days. When securities mature, the Fed is paid for them, and the securities come off the balance sheet. And so there is a constant massive flow. Just to keep the balance level, the Fed needs to constantly buy new securities to replace the maturing securities.

In addition, MBS have a feature called “pass-through principal payments.” All holders of MBS receive principal payments as the underlying mortgages are paid down or are paid off. The current boom in mortgage refinancing due to low mortgage rates is creating a torrent of pass-through principal payments – which has the effect of reducing the Fed’s holdings of MBS.

To compensate for the pass-through principal payments and keep its MBS balance flat, the Fed needs to constantly purchase a large amount of MBS. If the Fed buys no MBS, the balance of MBS on its balance sheet would fall sharply.

This article has the latest analysis of the Fed’s weekly balance sheet and charts. This is data straight from the Fed. To understand what the Fed is actually doing – rather than just saying – you need to read this article:

https://wolfstreet.com/2020/06/18/fed-ends-qe-total-assets-drop-liquidity-injection-ends/

Yes, the Fed’s balance sheet is more complicated than the hype on CNBC, but I make it easy for you and included a lot of charts that are easy to read.

This is one of the charts. It shows total assets on the Fed’s balance sheet, and total assets declined by $74 billion in the last week. Note how the Fed front-loaded QE in March and April, how it then systematically cut back in May and June, and how the balance sheet actually declined in the week ended June 17 (so DO READ the article I linked):

Thanks.

I only follow the craziness at the fed generally, not closely. These are my observations from the cheap seats. The US Treasury has amassed a huge balance of reserves with the fed, $1.6T. This is enough money to do serious damage to many players in many markets.

The BOE’s statement is a huge indicator that folks are definitely nervous out there, both about the money and the bonds. The $1.6T was raised by selling treasuries. I don’t know who brought what, but the BOE’s worries indicate it could be global central banks. US treasuries are negotiable instruments in any market and all of a sudden the BOE wants everybody to sell their bonds. Selling these bonds en masse would lower their price and increase yields naturally.

Somebody is trying to manipulate something in a big way. That’s what I think.

Folks are nervous. The Fed holds this stuff, regardless of the registered names. In a world of fraud, this isn’t much. If I wake up tomorrow and find I own several million in treasuries my first thought is whoopee, then I consider the liabilities. Making everyone own a share of the debt isn’t much of a fraud, it actually makes sense.

In my pending old age I wonder if I will ever be able to earn decent (4-5 percent) interest on savings again. CD rates have trended down from the 90’s, when they were 4-6 percent, in the “naughts” they were 2-4 percent. Now we are at essentially zero percent and we all are relegated to finding our place at the wall street gambling casino. FU to Carlyle Group alumnus Jerome Powell. (With a special FU shout out to the architect of this monetary nonsense, “the maestro” Alan Greenspan).

Take comfort that your 20 yr sacrifice via ZIRP has facilitated the re-election of DC politicians too cowardly and stupid to make difficult decisions and the perpetuation of a DC political class whose entire wealth is founded upon those politicians.

And that’s what it is really all about, right?

(Sarc)

just curious why you added the sarc tag c10?

certainly seems to this old boy that the sentence above that tag is correct, fundamentally, forcefully, and forward looking lee…

equally certainly this is NOT about making sure We the Peedons actually have enough to eat, drink, and be merry,,, though some of us old folks who have been what is now referred to as suckers, AKA savers — in spite of the ludicrously low interest rates — are already experiencing sufficient ”liquidity” to be merry each and every day!!

Let me get this straight, interest rates were kept down because they needed to service the interest on their government debts.

However, the tens of trillions of money printing is probably costing us $10 trillion by year end not to mention what they been doing since 2008-2020.

Didn’t they just spend the same money which the debt is up 136%+ in 13 years. This is a 7.7% increase from $11 trillion to $26 trillion on the U.S. national debt.

They did not save anything. The deficits and debts exploded the same. It is all a sham and lie, they just did not want to pay higher interest rates to savers, fixed income, bonds etc. Just I have always expected, they want to give all their money to their buddies and this is nothing to do with helping the overall U.S. economy.

The U.S. Federal Reserve, ECB, Bank of England, Bank of Canada, Bank of Australia, Bank of Japan and other central banks going down the low interest rate train are the biggest hypocrites in the world.

The government bureaus that produce major understated inflation to keep their interest charges and indexing of social security etc. are the other biggest hypocrites. They al l work together to financially screw us all.

I think every now and then Wolf turns a toy loose in a room full of cats just to see what happens.

Ahh, but which of the kats keep their second eye on the limited kibble in the bowl rather than the air-filled empty bag?

The biggest BS issue at the FED is their use of bank reserves. Reserves can come from many places and be held in many places, (they are everywhere) and while markets are ATH is a run on the bank really what worries them? There is no lockbox for reserves they find their way to the trading desks, because they are after all, cash, and their accounting is a shell game. Are they going to do (post W2) YCC, the virus is a war, right? Salient quality of YCC is Treasury control. Fed buys what Treasury issues. Most likely they will be all over the place, maturities and yields, they are now. Depends on what happens after November. My guess is Powell will stay (just as Bernanke filled out his term). They will blow the numbers off the current balance sheet, with more direct stimulus, or MMT. The immediate reason for YCC or OP Twist, is to rescue the financial stocks, and at least today they are keeping pace with the rally. If financials can’t make money in this environment, there are serious problems ahead.

The American public needs to get behind the idea of ending the Fed.

The Fed does not act in the best interests of the American people and instead works for the banking industry and Wall St. It has impoverished the American people with its interference in our economy. It has encouraged the Federal Government to go so far in debt that future interest service on the National Debt will require much higher taxes on the American people, further impoverishing the nation.

The Constitution never gave Congress the power to delegate its duty to coin money to another institution that is not answerable to the people in any way. The Fed is an unconstitutional bankers scheme, and needs to be abolished.

“The Fed is an unconstitutional bankers scheme, and needs to be abolished.”

Many decades ago when I was a youngster I heard this sentiment a lot from old timers – working types. I think these old timers had wisdom. You also.

I guess ANY AND ALL bank reserves are counted as excess reserves, now that, since 2020-03-26 (link below), the reserve requirements for banks have been reduced to 0%.

It appears to be the case, just look at the vertical wall in March on the ExRes figure in the article.

Reference:

https://www.federalreserve.gov/monetarypolicy/reservereq.htm

Required reserves at the peak before the rule change were only $200 billion.