Turmoil in the housing market and its impact on the “median price.”

By Wolf Richter for WOLF STREET.

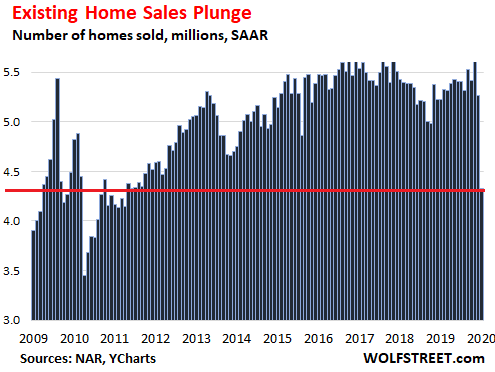

Across the US, despite record low mortgage rates, sales of “existing homes” – closed transactions of previously owned single-family houses, townhouses, condos, and co-ops – plunged 17.8% in April from March, after having already plunged 8.5% in March from February, to a seasonally adjusted annual rate of 4.33 million homes, last seen in September 2011 (also 4.33 million). The last time sales were lower was in July 2010. This knocked April’s sales volume down by 25% from pre-Covid February (data via YCharts):

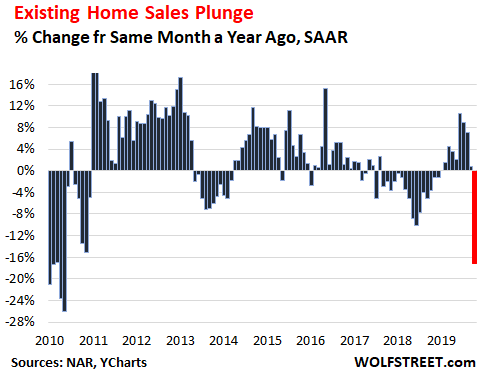

Compared to April 2019, homes sales dropped 17.2%, according to the National Association of Realtors today. It was the sharpest year-over-year drop since August 2010, during the Housing Bust (data via YCharts):

But condo sales were hit much harder than house sales – and that’s crucial for the discussion of the median-price head-fake in a moment:

- Sales of single-family houses dropped by 15.5% year-over-year, to 3.94 million units seasonally adjusted annual rate.

- But sales of condos collapsed by 31.6% year-over-year to 390,000 seasonally adjusted annual rate.

The “Change in Mix” causes the median price to do a head-fake.

“Changes in the composition of sales can distort median price data,” the NAR cautions in its footnote #3.

This is not normally a huge issue unless the market goes into turmoil when sales volume plunges and the bottom is falling out of the low end, because tens of millions of people have lost their jobs, and lending standards have tightened up for riskier mortgages, which is now.

We’re seeing evidence in the NAR report that the bottom is falling out at the lower end: the 31.4% collapse in condo sales. We’ll get to that in a moment.

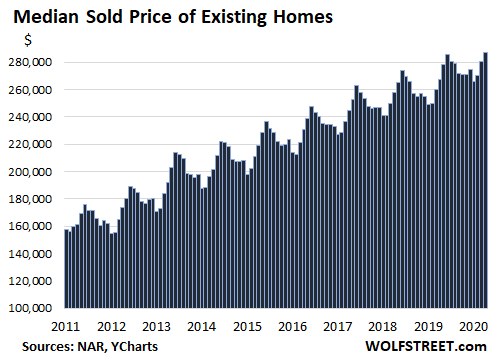

First, the median price jumped 7.4% to $286,800, which would be astonishing, given the turmoil in the market and the unemployment crisis, but this being a median price, it’s not astonishing; it’s expected:

The median price is the price in the middle, where half the homes sell for more and half the homes sell for less. The median price metric can be distorted by the price-mix of the homes that have sold, as the NAR points out in its footnote #3.

When sales at the lower half of the spectrum plunge while the upper half is hanging on better, then this changes the price-mix of homes that have sold, with a relatively smaller number of lower-priced homes in the mix, and a relatively larger number of higher-priced homes in the mix. This change in mix pushes up the median price of all homes sold, though actual prices of individual homes may have gone into other directions.

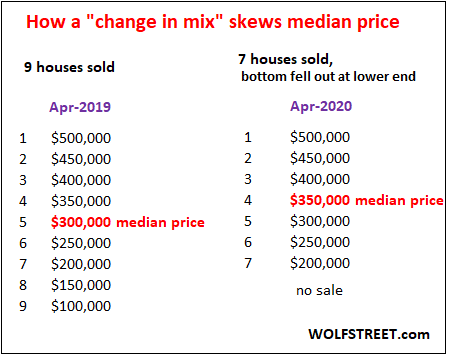

How a “change in mix” skews the median price:

The table below shows a very simple housing market. In April 2019, 9 houses sold, with a median price of $300,000. In April 2020, the same top 7 houses sold again, each at the same price as a year ago, but the two lowest-priced houses didn’t sell. So actual house prices did not change at all. But the median price jumped because the mix changed:

That a median price index can be heavily skewed by changes in the mix is its primary disadvantage. That’s why the Case-Shiller Home Price Index uses “sales pairs,” comparing prices of the same home over time, multiplied by thousands of homes in each market. The Case-Shiller index essentially delineates how the price of the same home changes over time. It is not impacted by mix.

But the Case-Shiller Index is a three-month rolling average released with a one-month lag. The last data set, released on April 28, was the average of sales prices that were entered into public records in December, January, and February – useless for the Covid-19 market.

So we’re stuck with the median price index for now. But we need to understand that changes in mix skew the median price away from actual changes in home prices.

And this is what happened in April.

Condo sales plunged 31.6% year-over-year, more than twice the decline of house sales (-15.5%). Condos generally are somewhat lower-priced than houses. The fact that condo sales plunged more than twice as much as house sales shows two things: One, the mix changed, resulting in a larger share of houses in the mix and a smaller share of condos; and two, it indicates that the lower half of the price scale is seeing relatively larger volume declines – both houses and condos – than the higher end.

This dynamic makes intuitive sense: Volume plunged as tens of millions of people have lost their jobs and are out of the housing market, and those that still have jobs but are not at the top of the income scale and have perhaps lower credit scores and need riskier mortgages to buy a home, well, they have problems getting approved for a mortgage because now riskier mortgages have become harder to come by, and because lenders are getting more skittish about lending on condos, which are perceived as riskier.

So when there is a drastic drop in volume accompanied by a drastic change in the price-mix of what sells, the median price is not a reliable indicator of how actual prices changed.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Some condos don’t qualify for FHA mortgages because the building or community has too many defaults, or bad financials. I’ve seen this stated in some listings, where they tell you the unit doesn’t qualify for financing, cash only.

just got burned for 1400 dollars plus lots of stress condo purchase fell through bad for us

Sorry for your stress Joe but look at it on the bright side Soon you will get a much better price on a condo Just try to be patient and good things will come to you I’m sure

You’ll get a much better price on anything real estate soon.

The biggest factor no one is talking about, Immigration, both legal, Illegal and deportation.

Immigration is on hold, 100,000 annually into NYC.

Illegals immigration is down, significantly.

Deportation is still on, plus many Illegals lost their jobs some are heading back home.

@budhu

You forgot to mention immigrants that return home. A lot of expats already did that. And it will be IMHO the biggest number

That’s interesting. I thought that couldn’t be done anymore, as it sounds like red lining. If it’s cash only for a place with huge defaults, it better be worth cash price.

FHA is a government agency, not a bank.

Redlining laws apply to banks, not governments.

There is definitely something wrong with that.

The FHA has had a redlining past built in.. look at what they did in the 50’s:

https://en.m.wikipedia.org/wiki/Levittown

Levitt refused to sell Levittown homes to people of color, and the FHA, upon authorizing loans for the construction of Levittown, included racial covenants in each deed, making Levittown a segregated community

The FHA had as official policy for years that mixed race communities were not allowed if you took their support.

The so called “plunge” in sales has mostly to do with the very low levels of homes listed for sale, unavailable for purchase not a glut on the market.

No, it has mostly to do with there not being buyers. Months supply jumped to 4.1 months, from 3.4 months in March and 3.0 months in February.

Wolf,

I wonder if a volume-weighted median sales price metric of some sort would help reduce distortions.

I think that I’ve seen volume weighted price metrics in the context of stocks.

The bottom line problem seems to be that demand evaporates a few months before price capitulates. Volume data helps highlight this dynamic.

Same situation in Queenstown.

Houses for sale are piling up — nothing is moving.

Also at the beginning of the week there were 182 houses for rent – that’s now at 202 https://www.realestate.co.nz/residential/rental?by=featured&lct=d300&ql=20

I bet most of those 202 are not sleeping very well wondering how they will service the mortgages…. those houses are not going to find tenants because the economy has been flattened by two months of lockdowns…. and it’s going to remain flattened for a long long long long time

3 days ago the Westpac mortgage rate on a 1 yr fixed was 3.05%… today it is 2.79%

Australia recently announced a 6 month mortgage payment holiday (interest and principal… no need to pay either)

What’s that stench??? Smells like dead rat…. oh … it’s the smell of desperation wafting across the country.

This is the calm… before the storm. Do we get a global mortgage holiday?

I am thinking we do — because otherwise we are going to see the Mother of all Financial Crises as millions of mortgages go into default.

The economy is not flattened by lockdown but by corona. Acting like the lockdown is to blame is lying and blaming the wrong thing. See Australia, which i think is already out of lockdown

In my city, i have never seen the inventory this low. A metro of 1.2 million people normally has about 9k to 11k home for sale. Right now there are only 3.5k. Thus using zillow’s price per square ft, this metric has gone from $120 per square ft to $140 since February until now.

I wonder if price per square foot is going up because rentals can’t enter the market (moratorium on evictions) but AirBnB’s and ‘flips’ can – which may be in nicer condition per square foot…

The much more expensive homes stay under normal conditions longer on the market than the average home. They are also much more likely to unoccupied or lived in by second home owners. So if only uninhabited homes come on the market than you would see something like this

Amen. The supply and demand curves are going to be meeting at a lower price point for most RE. Most major investors will soon try to liquidate and look around for safer places to invest.

As David Stockman correctly pointed out, underlying problems mean this dead cat will not bounce. RE FMV prices will ultimately plunge. The bankrupt sellers will be desperately rushing to sell when most potential buyers are also bankrupt.

Yeah ,but he also advocates no virus control measures.

Dangerous voice.

That is true as to virus control, which I also see as crucial. Sadly, except for Nouriel Roubini, there are many commentators whose views are correct and acceptable on one thing and less agreeable on other things.

Human lives have an inherent worth aside from income production for the economy, which some do not consider. Many also have limited knowledge of medical matters and do not see/understand the consequences– to be fair.

Real estate depends on the overall economy. States that handled Covid wrongly will see their economy crash and with it RE. States that handle it rightly will only be hit by the world economy and a change in how the economy function.

@M

It is not that i find other peoples life inherently worthwhile , but other people fond their own life worthy. Which means that there behavior during corona is markedly different than during normal times. This incurs big costs for the economy. Very likely bigger costs than a lockdown. And for a longer time because covid would be faster over with a lockdown.

A lockdown is the cheapest way to handle covid.

And BlackRock will buy up All the real estate again. In Canada the PM has put this private eq firm in charge of its newly created Infrastructure Bank (fox-guarding-henhouse!). Desperate owners will sell just like in the Depression of the 30s. The question is, where will people go?

Interesting if you think the mortgage market has been QE’ed. Banks are writing REFIs at record rates, while new home buyers are blocked from the market. A system top heavy with pension obligations has not blinked once, while people still working have to queue up online to submit and resubmit UI forms. Post GFC corporations weren’t hiring, or expanding, while companies with no revenue were borrowing at rates subsidized by Fed QE policy. Companies with revenue were buying back shares, all others fell through the cracks.

Not in my hood in tpa bay area JS.

There was one for sale sign in Dec, sold before it even got onto Zillow; now at least a dozen, including some of the ones that sold in the three or four months previously.

Nearest was sold in March, but back on mkt due to buyer not able to finance with the new rules, and that owner getting ready for a haircut, as that house was inherited and his wife just inherited a much nicer one.

And so it goes again, and the RE pros keep right on tooting a horn of plenty of sales, solid values, etc., while the market continues sliding away again.

Gotta love how Wolf breaks it down so we can decipher what’s really going on counter to what msm is trying to sell to the masses. If I strictly believe in talking head on various network or worse yet Lawrence Yun, I probably just eat up what Zillow or RE association is telling us and buy into the most 3-4% drop in price by next year at most and how there’s just so much pend up demand once we get our V shape recover, people will lining up to buy houses.

I think I still have a few of those NAR bumper stickers in storage. You know, the ones that read “Now Is A Good Time To Buy A Home”. Left over from 1986 when I first got my license.

Roddy:

My favorite bumper sticker is of 1982 vintage seen in Sydney, Australia.

Eat Kangaroo Meat! 50,000 Americans Can’t Be Wrong!

In reference to Jack-In-The-Box meat scandal.

My favorite bumper sticker is welcome to Nevada now go home. Maybe the 90s

After that I referred to them for a while as Yak-In-the-Box.

Yak’s more chewy :)

Exactly And this is why MSM is dying and sites such as Wolfstreet are growing exponentially. People get it.Some people anyway

“Data released May 12 from the National Association of Realtors (NAR) shows that house prices increased in the first quarter of 2020 despite the ongoing coronavirus pandemic. The NAR’s quarterly report on metro home prices shows that the median single-family home price increased year over year in 96% of U.S. markets in the first quarter of 2020, versus 94% in the first quarter of 2019.”

96% is a big number. Many of the US markets do not have many condos.

I think it would still make sense that the low end got hit more than the high end. Most job losses are at the lower end after all.

The real change will happen during the recovery though. When jobs start coming back, it won’t happen evenly. We’re likely to see a significant number of people moving into some areas and out of others based on how that shapes up.

If big tech companies keep a strong shift towards telecommuting, areas like San Francisco could easily weaken as workers move further out. Even 200 miles isn’t a bad commute if it’s only once a week.

That’s exactly my take on this Low paid people aren’t buying homes presently. Frankly I’m surprised that anybody is buying homes presently

> Even 200 miles isn’t a bad commute if it’s only once a week.

A lot of people commute to SF from Bend, Oregon on an X-days-every-two-weeks schedule. Bend has an airport with nonstops to SF and widely deployed fiber optics. If you’re a gambler, look for other places like that (Wenatchee has the fiber+airport but you have to connect in Seattle)

How do you tell if NAR is lying….. You don’t need to, they are always lying…

Their lips are moving.

They also lie when their lips aren’t moving

Is this typically a lagging indicator for home values? Supply/Demand

I just did some numbers. Turns out that 10 single family homes are sold for every condo. So, the median is not being affected much by the change in sales mix … the condos are only 9% of the sales … they can not impact the median that much.

Also, the report mentions first time buyer activity rose slightly from 1 year ago. First time buyers are concentrated at the bottom end of the market. That also throws cold water on the median being distorted by the bottom end falling out.

What we have here is prices rising in a slowdown because supply is falling fast.

A few weeks ago the Zillow said my house went up 4k from previous 30 days. Today it says up almost 6k past 30 days. At this rate I’d make more money if we keep the economy closed forever. The internets are smart. I think Zillow is owned by the Fed and everyone there is drinking coolaid.

Nah, they’re at the moonshine..

I was absolutely shocked at some of the houses that Zillow bought last year. The sellers must have laughed all the way to the bank. The houses bought by Zillow had more than a few problems not reflected in the sale price.

As I pointed out in the article, condos are a sign that the lower half is where sales are falling the most — not just condos but houses too. I have seen this in other data, including in the North Bay data I posted a while ago.

Excellent and Educational article as usual Wolf. Thank you.

One factor today and after the last crash that I did not see in article or comments is how much the PE and hedgie folks have distorted the market for SFR.

As cash buyers in 2015, our competition was PE and hedgies per our very competent realtor; we looked at dozens of properties in our price range, found very few that could close as fast as we wanted, most were owned by banks that really did not want to sell, as they wanted to finance a sale for some kind of tax benefit I suppose.

Is there any good data re how many SFR are owned today by these rich companies as opposed to owner occupiers?

Bloomer says they are waiting again, with tons of the fed’s free cash, to jump into the market ASAP. Any info on that aspect?

Thnks again,

The banks prefer the mega landlords because they buy in bulk and don’t require inspections. The inspections are a big deal because most of these homes would come back with some big code violation, like termites, lack of wiring, roof problems, etc., which are hidden in the bulk purchase.

Meanwhile, around here, during the shutdown, the contractors have been working furiously to complete the condos started, no doubt to get the rest of their money while some can be still got. I anticipate a whole lot of defaults and lost deposits when builders come to the pay window for their mullah. Also I live a “seize or sue” jurisdiction which means the banks or hedge funds will have a heck of a lot of condos to sell, as buyers/depositors throw them the keys.

You can lead SoCalJim to water, but you can’t make him think…

“first time buyer activity”

Define “activity” – that can mean anything from actual buys to bowel movements.

I’ll assume that if they were actual buys/purchases…the NAR would label them so.

“Activity” has the scent of BS wafting about it. It could mean website browsing…

It’s mostly people of lower incomes that lockdowns are demolishing. I suspect that has a lot to do with it.

SocalJim’s tricky lies of the day, trying to make us believe that process are not dropping

1. Jim used Q1 (which ends in March) closed sale data when Covid19 did not have an effect until April closed sales.

2. Jim claims only 9% of sale are condos, without specifying which local market or nationwide. So calling BS on that one, too.

3. Then there is the usual year-over-year price trick. Also based on Q1 data, which proves NOTHING. An always remember, realtors love to YOY gains when month-to-month has losses, and vice versa.

Buy now or forever be shut out !!!!

Condos are an example. The same is true for cheaper homes but those data are more difficult to extract.

A friend of mine who lives in the North Bay just sold his house at a price above the asking price

Just a thought but could be FOMO if it’s anything like the stock market. Times like this you will always get people that think it’s bargain time. Especially for housing with lower interest rate being an extra incentives. FOMO is defintely one factor in the stock market, read something about 800k new accounts created with likes of Wealthfront and Robinhood during this crisis from retail investors. All piling in now in hopes of stock bargain. Also i wonder about some of these peoplw buying houses now, i guess the very thought of potentially losing their well paying white collar job is not a concern, might not happen in a month or two but if this drags out you have to think what’s the long term implication..

I know some friends are scrambling to refi now because they are fearful of losing their job and not being able to refi.

I suppose some renters are scrambling to buy now also. While they still have a high paying job.

There are those who believe in the myth of the V recovery and think they are getting a deal… (a sucker is born every day…)

Reopening reality check: Georgia’s jobs aren’t flooding back

A month after easing lockdown restrictions, the state is still seeing a steady stream of unemployment claims, economic data shows.

https://www.politico.com/news/2020/05/21/georgia-reopening-coronavirus-jobs-273070

Because people make more money sitting at home due to the CARES Act than they would if they went back to work. That’s why the jobs “aren’t coming back”.

Here in Scottsdale, local small businesses have a plethora of “now hiring” signs in their windows. Only takers are those who can get paid more than they can get for free on unemployment. One restaurant owner, who was featured on the evening news, was bemoaning the fact that her staff won’t come back to work for the above reason and she has to offer $20 an hour to get anyone to accept a job….

Wages have needed to rise for some time. I don’t see a problem with people holding out for better pay while they can. It’s about time for a modern labor movement in this country. It really is about time.

In silicon valley cashing out stock options to buy a home doesn’t trigger any suspicions that you think the options are a worse investment than a bad RE deal. The RE will still be worth something in the future, while the options can go to zero. By doing this, you get to look like you believe in the future of the company, especially if you really can’t get a better job.

So many things are changing, none of these numbers can be used to project the future.

Some things to consider:

FHA minimum credit score is now 620 vs 585.

Most conventional loans now require 20% down.

Jumbo loans are virtually non-existent. Wells Fargo requires $250,000 in LIQUID deposits.

However, as Wolf always says: “All real estate is local.”

Here in the Dallas area showings are shooting through the roof now that lockdown is over.

Even during lockdown vacant houses were selling. And now we are back to multiple offer scenarios (4 and 5 in 3 days on my most recent 2 houses earlier this month).

Note, these are in good, updated shape, but in the “affordable” price range here.

At the same time, in the same working class neighborhoods, there are lines of 20-40 cars every day at the churches and food banks. And no surprise, most of them are late model vehicles much nicer than what I drive.

Yes, 40% of the people making less than $40,000 are out of work. Even though that goes a lot further here The ripple effect is going to be huge.

It seems like lots of people have gone Covid cabin crazy and are trying to return to normal. Restaurants are packed because the 25% occupancy rule is not being enforced.

Am I being too paranoid or are too many people living in a dream world?

I agree, it’s hard to know with so much going on. Will say this: The Fed has injected trillions to benefit the rich. That has to go somewhere. It’s going into stocks. I’ve long said there will be no real estate crash unless we have a stock crash. We had a stock crash, except its basically already over because the Fed gave it trillions at wrap speed to reinflate the everything bubble prices. So maybe that means no real estate crash?

Well, individual public companies are still going BK so the Fed Firewall is not being applied universally.

‘We had a stock crash, except its basically already over because the Fed gave it trillions..’

The bear market has just begun and like all the others has big rallies. See 1930.

A number of big players on CNBC who are normally bulls are predicting another big leg down soon. Guy with last name Orlando who became a billionaire buying distress figures we have a 10 % move down in June.

The disconnect from the shut down of the economy is total in the world of trading stocks. You click a button and buy a stock. They might as well be trading baseball cards or tulip bulbs.

My guess is that sometime in July, when Wiley Coyote looks down, we see a 5000 pt one day hit as we begin the next leg down.

July 29th is the day the DOW drops 3,500 points.

Wait until those AirBnb investors can’t make their mortgage payment. There’s going to be a lot of repo’ed condos for sale in downtown/uptown Dallas.

Schadenfreudeulous.

Bring it.

Just saw on the news today that 70% of people are going to stay home for Memorial Day weekend. That is huge. The hospitality industry is in serious trouble, and that has a lot of spill over effect. But unfortunate they are only one of many industries facing devastation.

It will take a while for the reality of this all to set in. Right now people are frozen, not knowing what to do, and allowing their normalcy bias to influence them.

They are like an animal staring into the headlights of a vehicle ready to run them down, not being able to understand exactly what is happening.

A few months from now, the temporary measures to delay the inevitable will end, and fear will begin to set in. The fact is that about half of our population was only a few paychecks away from living under a bridge before this whole thing started. Now with the inevitable asset deflation that is coming, many people who thought they financially solvent will discover their assets are not worth what they believed they were and they are really broke.

> “All real estate is local.”

Yeah, because obviously all PANdemics are local.

RIiiight.

The effects on your surroundings may be different in Queens compared to Pitcairn Island…

Wolf,

Thank you for your useful information.

After 2008, with a big student loans, low pay work ( if you could find one after graduation), and rising house prices, most of us where thinking that maybe in the next crisis will be another opportunity to catch the train and buy a home. I am so sorry to say that maybe we should just keep dreaming. Because seems like the house prices are not coming down. Or maybe I am wrong.

I am not sure about the statistics, but on my cycle of friends, and friends of friends, everyone born in 80s wish that they could afford to buy a home. I can say that since the last crisis ( 2008 housing bubble), Millennial are still running after the train that they missed it.

With all this struggles, and at the same time seeing the baby-boomers

that are living the american dream, owning a payed off huge size houses and still complaining about the pensions, are making me think that we really are poor generation.

My user name (Educated but poor Millennial) says a lot about our struggles.

I definitely understand this,

As Max Kaiser said “paraphrasing”, most millennials are going to get their homes as the boomers and older die off or have to unload their homes at a discount as they move into retirement homes.

Nah, they will reverse mortgage, hire a granny nanny, and eat all their equity first. The Me Generation is spending their children’s inheritance, and laughing about it while slurping up free health care as their grandkids suffer, never being able to afford a doctor or hospital visit.

Have a nice day!

That is their plan, but, it won’t last. The boomers are hoping, everything will hold together long enough that they will outlive the system breaking apart, but, we will see. A-lot could happen in the near future that will be very hard to predict.

My grand kids, and they are grand, have better healthcare than I ever did before I found the VA,,, all on a ”state” (actually two different states) program, and from what I hear, those programs will basically take care of all medical services until they are 22 or something like that depending on various factors; also will continue indefinitely if they are disabled before then.

Folks do not seem to realize the vast extent of guv mint medical services plans already out there these days, especially for children, but really for most everyone IF poor, etc., until we are old enough for medicare to take care of us if we want it…

Sorry millennial, why don’t you pull yourself up by the bootstraps like boomer will tell you? cause in their view, you are either too lazy or not smart enough to make it big. How dare you of dream of owning a home? That’s entitled mentality but it sure is different when boomer can buy a house back in the days when income to house price ratio is actually reasonable.

I feel for the millennial generation, even though I am not one myself, I can imagine being in a generation where you’re screw twice, first from great recession and now this and all while being the scapegoat and everyone’s favorite punching bag generation. Is there lazy and entitled among millenials? Of course there is but so do every generation, looking at my boomer parents, I see plenty of entitlement right there. Look at who is in charge of this country now, talk about entitlement…

People forget that the parents of the millennials are the boomers.

The Me Generation begat the Selfie Generation.

Funny how that happened.

Don’t get too down about it if you can help yourself. I’m an older millennial (right on the dividing line) so I think I’m better off than the younger millennials, but I too missed the good or at least sensible time to buy a house. I don’t fault anyone else for my not buying earlier. I have similar feelings and frustrations. I have no idea where this is going. I do think the young millennials are really getting screwed though.

The growing divide between haves and have nots in this country is getting disturbing. And I’m not deluding myself as I know I’m one of the haves regardless of not being a homeowner.

Totally off-topic, but relevant to your complaints.

I had my teenage years in the eighties and there were all sorts of problems. I too heard day after day the world was doomed by: “The bomb”; hous prices through the roof, despite interest rates being above 10%; smog-polution; lead in petrol, the ozone hole, to mention some. Some people sit down and cry. Others encourage themselves to do something. I chose to study environmental chemistry in the hope to be able to contribute something.

It’s not a generation thingy. It’s actually very personal. I see it with my children. The boy (14) just complains about everything. The girl (12) assesses the problem, decides if it is worth her effort to do something with it. She either leaves it as it is, or starts working on it. No surprise she is the more productive of the two and has more free time.

The people complaining seem to seek all the attention (in the media). The do-ers, just do and get on with their lives (and get blamed and taxed for it).

I teach my children not to study for a job, but to study for skills and knowledge which will give them flexibility. That’s all i can do. They have to decide if thy take the advice or not.

I don’t feel guilty for what i and my wife have worked for. We bought our home in 2000 for 500.000 dutch guilders. In comparison: my parents bought theirs (similar in size) in 1980 for 50.000 (which was considered to much). See the difference? We worked hard and the house will be payed for in 3 to 4 years. And i’m sure some people will blame us for that too, because we are so well of. As if we got it for free.

Better to stop comparing and feeling sorry for yourself and deal with the situation. Nobody will hold your hand and give you everything you want. Nobody of the plebs is entitled to anything but to work for his wants and needs.

To add another critique. You call yourself educated, but is seems you skipped writing and spelling classes. This just pisses me off. You complain about the generations before you, who also had to work for their stuff. But can’t be bothered to do some grammar and spelling checking.

Hi

You forgot to mention the part about the unpleasant effects on purchasing power of moving from the guilder to the Euro.

CRV,

Sorry for my spelling mistakes.

Not only were you off the topic, but also you even didn’t get the point. I am not talking about myself and my own problems, as you do speak here about yourself. I am trying to paint an overall picture, where you may possibly see the problem. (If you can see it)

Don’t feel bad EBPM, most of the nostalgia laden “boostraps” generation boomers are psychologically incapable of genuine introspection or accurate analysis of current issues affecting younger people. The damage to their self made image would be too uncomfortable. Even a slight nod to the economic advantages they enjoyed would damage their superhero sized egos.

I agree with CRV on one point. Just move on from trying to get them to change the system. Figure out how to adapt and bang on the system that exists. These greedy dinosaurs will never wake up nor give anyone anything but sh*tty self-aggrandizing advice.

Yertrippin,

good lordy, this boomer-millennial crap is really getting boring and old.

I was born in 1980, have 3 children, and we are looking to buy our fourth house; an upgrade so kids can each have their own bedroom. Since we were born, mortgage rates fell from nearly 20% to 3% and house prices quadrupled. Hell of a headwind for purchasers during that time, unless you bought in 06/07. I don’t know how the Fed will pull that rabbit out of the hat again.

tailwind

Some generations ARE poorer. It’s not a generations fault. My parents were WWII, and they were poor and lived through the depression. It was just a cycle of history. Of course, if you made it through the depression and war, people of the WWII generation also generally lived through the most prosperous times in US history (1945 – 2000).

Now, we are back to depression. My advice to myself and others. Be the exception. America has ALWAYS had poor and rich people. Keep yourself healthy and know that the depression will end at some point. Ride the next wave of prosperity or better yet, become the exception and have prosperity during the depression.

Even this 1960 boomer here agrees with you totally. I’m a skeptic and cynic, though. I believe that is why many of the politicians, big corporations and mainstream media constantly promote social and wedge issues in order for the millennial generation to not follow the money scent. The Fed of course since Greenspan only knows asset / debt bubbles, inflation and CONfidence, not production, earnings, savings, so they have to keep the asset/debt bubble going at all costs. It will collapse, sooner than later because of their recent actions, so hang in there.

Both of my kids are in their mid-30’s and ALL of their peers who “own” homes got help from parents, grandparents, etc. I don’t know of any of their friends who bought a home on their own. Many are still subsidized by mom and dad. The fake wealth created by the Fed has to go somewhere and much of it is going to kids of “wealthy” parents, and propping up the housing market as well. Kind of a two’fer for the Fed, I suppose.

‘Mis-Educated’ might be more accurate.

I would guess that if you can muster 20%, you can probably get there, but you need to be realistic, and work your way in if you happen to live in an expensive area, start up at the condo or townhome level, then work your way up. I remember that when we bought a TH in 2007 near the peak, it was quite nerve wracking for a few years watching the value fall, and wondering how big a mistake it was.

Also, don’t run after the train, let it come to you. In 2008, the bottom didn’t get there until 2011 or so from my recollection, that was in the bay area. Just relax and be patient, if things keep going the way they are, there are two pieces to consider; first, rent is likely to get a bit cheaper due to a bunch of different dynamics. second, home prices will get cheaper over the next few years, it should give you time to save up for the 20% if you aren’t there already.

The lesson I learned is not to stretch your budget just to buy a home.

Very Good comment MCH, and in my extensive experience, right on the money!

Today is not the time to buy RE in this current event, MOST PLACES,,, and, to be sure, every location will have different situation per day, week, month, or even over more than one year…

As posted elsewhere on this wonderful site,,, please be patient, etc., but, perhaps most importantly,,,

PAY ATTENTION to all the various signs and similar;

it really is a lot easier in these days of the fast and furious, if not always exactly correct communications through our world wide web,,, etc…

IMO, you are going to be well informed in you read at least a dozen domestic news sources along with at least a dozen international sources,,, then make up your own mind,,, go back and research deeper on any subject on which you do not feel clear, etc., etc.

Relatively easy to ”cross reference” any news or other information these days, with SO many sites offering access, usually free now, to first class research results.

NOT to do your homework is up to you, but please do not blame others if you do not do YOUR homework, as others commenting on here clearly have not done…

MCH and all good people here,

Thanks a lot for your positive comments. Sometimes, when I am indicating facts, it sounds like I am complaining or want to be negative.

For sure, I will be more patience, will watch the market, and try to stay out of debt. Similarly, I have told to my fiends to be out of debt.

Last winter, one of my friends was buying a $400k , 1bed condo (built in 60s) in Los Angeles. Now, he is happy that I discouraged him.

I have very recent front line experience in the Bay Area. Nice homes that are priced and marketed correctly are flying off the market. There are still bidding wars, I know I lost one.

Be careful. The chairman of a huge tech company was on CNBC saying that all tech companies are rationalizing costs now. You now what that means. The tech industry uses a lot of contractors, and they can be let go quite easily. Cost cuts takes several months to flow through to home prices.

Thanks, I’m good. Whatever happens happens, but right now homes are flying off the shelves. Literally every home I was tracking on Redfin from mid April to mid May had gone pending. Most spend maybe a week on the market, and some would sell faster but the sellers want to dangle them out there long enough to generate buzz for a bidding war. I’ve really noticed the pickup in both sales and inventory since the beginning of May.

You have to remember this is the Bay Area market. So many people here have cash to throw around and reserves to get them through a downturn even after buying a home. The virus situation will get better and until then a lot of people here will work from home and believe it or not they have lots of work to do.

The rich are doing better than ever;

-only- the poor are suffering.

It’s silly to blame it on a virus,

completely ignoring bad habits.

Virus or not, obese geezers weren’t

going to live long anyways.

Our youth are suffering too;

half of them are unwanted,

unneeded, “nonessential”, lost.

Hence the low fertility rate;

women are having fewer kids.

The bluer the state, the worse it is;

people are voting with their feet.

Europe is worse off than America.

This was like almost a string of six haikus.

Speaking of my post, Mr. “Debt Wazoo” commented:

> This was like almost a string of six haikus.

I think I’m turning Japanese, I really think so.

You can just sort of imagine ancient disasters driving the development of Buddhism.

@Jeff – you’re giving me The Vapors.

Mr. Clete replied ( to me ):

> you’re giving me The Vapors.

As soon as they had created “Turning Japanese”,

before it was even released, “The Vapors” knew

it’d make them a “One Hit Wonder”.

At the time, 1980, I think it was

mostly about Japanese cameras;

today, it’s more about living alone.

Tim replied ( to me ):

> You can just sort of imagine ancient disasters

> driving the development of Buddhism.

All religions are about pain relief;

alcohol, drugs, low interest rates, and

low risk premiums are also about pain relief.

Our world is strung-out, high as a kite.

If you’re an alcoholic, and it’s harming you,

you might join a “12-step” para-religion.

What’s amazing about Buddhism is that

it doesn’t require a supernatural “sky daddy”.

“God” is nature; nothing more, nothing less.

Excessive desires, lust,

including a lust for life itself,

increases suffering.

Really? Another generation of “why us?”. Feelings hurt or are you pissed off enough yet? Those “boomers” often work hard to get that stuff and protect children and grandchildren, all to drop dead before they can enjoy much retirement. Some of those jobs gave rise to health issues. And many of them saw the road coming at us with worry, and a concern that younger generations were walking into a trap ever so willingly. What’s it gonna be..sit back and take it, or get up and fight? None of this mess was not known, but now it’s becoming clear.

‘Some of those jobs gave rise to health issues.’

That’s not the way I see it. The epidemic of obesity, diabetes and heart disease in the US and around the world is a choice.

Yes I have heard that the PR/Ad men made everyone sick but at the end of the day it’s a CHOICE.

Don’t blame it on your job. Or the cat. If you are falling to bits then that’s the consequence of piling crisps and other rubbish into your shopping trolley year after year – and all those trips through the drive through.

Healthcare systems worldwide have maintained a long series of what are called “occupational illnesses”, meaning those working a certain job have a higher, or even much higher, chance of falling to it than people working other jobs since the 60’s. To give you a nasty example workers in the chromium industries have a very incidence of cancer to the whole breathing tract (including the nose) and of skin diseases, including ulcers.

People suffering from these diseases usually have access to extra benefits like, say, a little extra pension benefit and/or priority in medical care and/or an increased pension for a surviving spouse.

The list I have right now runs at 23 pages of plain small text.

Trust me on this: I come from an industrial district and there’s a good reason you won’t hear people complain robots are “stealing” their jobs. Let the machines handle cadmium, manganese, chromium and a host of organic compounds I don’t even want to think about.

Of course, increased workplace safety has curbed the excesses, but the chances you’ll pay the price for the job you do down the road are not negligible even today.

Diesel Fuel! Aviation Fuels! Asbestos! On and on. Do you think the employers told these people that they knew how dangerous their chemicals could be? Freak cancers don’t always come from diet, drinking, or even smoking. An employer might even ship a drum of corrosives in air freight in violation of laws back then…think they cared if someone’s life was endangered down the line? You need to stop dreaming that you’re on Christmas Tree Lane. The bulldozer just missed a few pines while it was shitting over the enviroment for your cement pad. This game has costs and not all information is revealed in the pricing.

It’s easy to blame illness on everything but one’s bad lifestyle choices.

Take a look around you (particularly in America)… how many fit people do you see?

And don’t confuse being fit with not being grossly obese…. that does not qualify.

When you go to the grocery store, have a look at what people have in their carts.

I’ve seen people with cases of Red Bull. Not only do they guzzle that crap themselves — they feed it to their kids.

Sure some people suffer from exposure to chemicals in their workplace — but the vast majority of people are sick because they made bad choices.

I don’t see things this way either.

Treat your body well (eat real food, don’t smoke, stay physically active everyday) and diabetes, obesity and heart disease don’t happen to you.

*Or at least you stack the deck enormously in your favor that you avoid chronic diseases like these.

Bad things still happen, but far too many people act like their health problems are caused by issues external to themselves instead of their own poor health self-care decisions.

Crap happens to everyone at some point.

That, that, should be taught in high school.

What I have yet to see is the long term follow on effect of the Fed recently creating more money on house prices.

At some point this increase in money supply will be reflected in each dollar being worth less. It will then take more devalued dollars to buy the same depreciating house.

Could it end up being a race between falling house prices and a falling dollar?

If for example, house prices fall 10% but the dollar falls 20% in value, then housing prices in nominal prices could increase 10%.

In this case, the possibility of attaining home ownership for many will remain forever elusive.

WES

I agree. people talk all the time about deflation. With this much additional money in the system, I don’t see how deflation can ever occur.

Mr. BearDawg wrote:

> With this much additional money in the system,

> I don’t see how deflation can ever occur.

Oversupply ( from China ), and

under demand ( from disabled Americans )

is a recipe for deflation.

Every time a loan is created,

the money supply goes up.

When a loan defaults,

the money supply goes down.

Can bankers create loans faster than

people can default on them ?!

No surprise…………if you were a seller would you want sick people going thru your home to view it……..if you were a buyer would you want to go thru all the meetings required to move……new carpets, appliances, closing, looking at homes all exposes you.

Only the young, someone that needs to buy or the wealthy are in the market.

The big ticket homes will stay healthy……most of those folks can work from home or have wealth that is not dependent on the economy……its the poor folks that work at JC Penny, Nordstrom etc that are losing their jobs and have lost their ability to purchase homes. No job…..no loan. As the unemployment rate goes up the home market will stall……but as it declines the home market will lead the recovery.

I suspect this will be one of the first areas to recover…….with interest rates near 3 or lower.

The real key is that with the fed and government now in a position which requires them to monetize the debt……inflation is a sure thing……so……for the average Joe a home is one of their best plays…….its just a matter of time until the vaccine hits and the monetary fix hits the market. Savers be damned. The US is still 30 trillion or so from monetary loss of control so they will print print print until homes are sold.

Let’s see – sales for existing Homes are plunging while the median price for same is rising.

Where I live the home builders are all busy, actually very busy. There’s no spec building here.

Drive around the neighborhoods and you’ll see one, maybe two, homes for sale. No one wants to sell. If you want a home you’ll end up at the new home subdivisions. Lenders have definitely tightened up on underwriting criteria. High FICO required, 20% down, etc. They keep selling the new houses. Existing homes not so much. I’m confused…

Housing starts fell off a cliff in April

“Privately-owned housing starts in April were at a seasonally adjusted annual rate of 891,000. This is 30.2 percent (±11.0 percent) below the revised March estimate of 1,276,000 and is 29.7 percent (±8.1 percent) below the April 2019 rate of 1,267,000. Single-family housing starts in April were at a rate of 650,000; this is 25.4 percent (±9.6 percent) below the revised March figure of 871,000”

Where I live (Nanaimo, Van Isle) the builders of condos and rental apts are incredibly busy, almost insanely busy. (The most bizarre is a very difficult site, they’ve been test drilling for a week for a high rise hotel with Chinese money. They had to start work to keep their option open so it’s hard to know if they are insane enough to proceed.)

I would say that our supply of apartments is set to at least double in the next 3 to 6 months.

Why are they going ahead? Because the decisions to proceed were taken in 2019. With the price of lots these days (only the lot appreciates faster than the CPI) you can’t stop once you’ve taken the plunge. It only stops when the bank pulls the plug. And these are multi-sites with all the approvals etc.

Some may have been committed to in 2018.

If the houses aren’t spec, they are custom. Unless the buyer just walked in, pointed at a plan and said ‘that one’, they probably spent a month looking at plans and debating, after buying the lot. If the houses were spec, that would be a vote of confidence. But, again, with the price of a lot equaling the cost of construction, the builder who bought lots on spec may be forced to proceed. Show me a builder buying lots NOW to build spec and I’ll show you a brave builder.

The fact that a custom house is being built 8 weeks after the stock market took its first big hit just means nothing stops at once.

Great article Wolf, it seems to have brought the House pumpers out of the woodwork spinning their yarns.

What are mortgage application numbers looking like? I saw an article that said May was 98% of applications last year so far month to date.

Cash out refinancing is part of the mortgage application activity.

https://www.mba.org/2020-press-releases/may/mortgage-applications-decrease-in-latest-mba-weekly-survey

“The Market Composite Index, a measure of mortgage loan application volume, decreased 2.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 2 percent compared with the previous week. The Refinance Index decreased 6 percent from the previous week and was 160 percent higher than the same week one year ago. The seasonally adjusted Purchase Index increased 6 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 1.5 percent lower than the same week one year ago.”

As someone who does work in finance, albeit indirectly to mortgage lending I have a couple of thoughts about where this is going to go:

1. Currently alot of states, CA and NV included, have a ban on evictions so there is alot of people who havent been kicked out of their rentals and houses.

2. I know a couple Airbnb hosts who have 2,3 + mortgages and about half might have to default or figure something else out on at least 1 property.

3. What happens to future home lending for all these people that lost their jobs? You have to assume that they wont have that concurrent 6 or 2 years work history that lenders need to buy a home and with alot of industries cutting jobs that wont be coming back, this is going to take alot of potential home buyers out of the market.

I live in the Bay Area and have been watching the housing market for a while. Prices are definitley going down a little. And I’ve seen lots of price cuts in Modesto which has more blue collar workers and much cheaper houses than the Bay Area proper. What Wolf is saying here makes sense.

We must be in a strange world where house prices, at least seem to be going up, when the USA has over 50 million unemployed. I’m not sure what the starter home is, in the USA, but without that first rung on the ladder how can people selling second or third homes sell. I do know, for the poor Millennials who are waiting for house prices to drop, that it is very hard to get a mortgage if the lender thinks the house will drop further. Strange times….

There may also be the added pressure of over- extended households downsizing, at some stage.

1) How do u start a car : push it uphill with your hands.

2) Click a starter, a 20% incentive on brand new houses in Levittown.

3) $100K x 0.20 = $20K for #9.

4) $150K x 0.20 = $30K or #8, for brand new houses in Fl, GA,Mi, PA & SF…

5) Crank $4K starter on cars with more lives than cats & dogs.

6) Click $20K starter on a $40K brand new F 150 and Silverado, to clear the swamp.

7) Click on Made in US phones.

8) The Fed will click shares of DOW components with Red, negative equity of co like Boing, MCD, HD. Hook jump start cable to small/ mid size US industries. Replace XLE dying battery & cables !!

9) Paint (electronically) Baba back. Build a wall on the devalued Yuan after China sack HK.

11) Stop feeding cooks & crooks.

I don’t, uh, what the, huh?

@Otis – Good, I thought it was just me.

Gave up trying to figure it out. We just keep cranking the hours/days

until the work slows, or snow & frost drive us out of the field.

We are slammed with work. Builders I dig for are buried.

Our business has been through recessions & the great housing depression.

This time around with the great imprisonment ..totally different…at this point.

There is no shortage of pain on main street. Shut downs were squarely aimed at them. So we spend our $$ in their shops/stores/cafes/bars.

End of today it will be Friday fish fry & old fashions at the local watering hole.

A 1,500 sq ft mall store pay base rent + a cut from the cash register

to the landlord.

When the mall is closed, rent fall.

COFFEE prices are trending down for many years. Grande coffee cost is up, since yesterday, because SBUX shareholders equity is negative.

Going to see a wave of Honk Kong buyers again, trying to get their money out of the country.

Hong Kong only has a population of 7.5 million, most of whom can never leave. The ones who could get out, got out long ago, or already own property overseas as an insurance policy. They have a lot of options Australia, Canada, EU, USA, etc…. However, I do agree a wave is coming.

but its a tidal wave hitting a housing bubble resting of piles of leveraged dynamite. There is no saviour coming down from the heavens for the housing or condo markets.

And most of them are sitting in Vancouver, BC trying to figure out how to bring over the rest of the family and milk the Canadian Gov’t.

There are about 300,000 Canadian citizens resident in Hong Kong. Travel right now is difficult but I expect a significant number will leave HK as a result of the CCP crackdown that is coming.

On balance, the HK people have brought a lot of capital and talent to Canada so I don’t buy that they’re milking the system any more than the locals. Somebody voted for the NDP.

In British Columbia, the main problem going forward is what they plan on doing for a living since every major industry is in serious decline.

I already know of a couple of millennials who have dumped their rental condo’s and gone back to stay with Mom and Dad because they lost their job and can’t afford the rent. Also, surprise, surprise, they don’t want to spend 24 hours a day locked in a sardine can. Many condo dwellers like the lifestyle, that is a small place to live in the downtown core, spending their money on bars, restaurants, clothes, etc…rather than cutting grass and fixing the plumbing like their parents. Who wants to live in the downtown core now, locked in some imitation jail cell by power mad bureaucrats. You add in all the AirBnB condos, all the speculators flipping condos and there is one holy disaster coming for Condo owners. And for condo renters and future buyers , the dawn of a good day, providing the politicians don’t destroy their cities for good,

From USAToday:

Delinquencies among borrowers for past-due mortgages are soaring, a sign that Americans are struggling to pay their bills amid a wave of layoffs and lost income from the coronavirus pandemic.

Mortgage delinquencies surged by 1.6 million in April, the largest single-month jump in history, according to a report from Black Knight, a mortgage technology and data provider.

Don’t worry. SocalJim and those people in Boston will lap the foreclosed properties up ;)

1) Hertz is trying to lift their head > the choking swamp.

2) Hertz offer their fleet of 2019 Corvette Z06 for $61K to $64K.

3) Today, Z06 wholesale price is $55K.

4) Hertz should click Corvettes for : wholesale price minus 15% – 20% discount.

5) Hertz is joking. $63K is : wholesale price + $8K, or wholesale price plus a 15% markup.

Wait for few months and buy them for ~$50K :-)

I read all the above comments. I think that we’re still too early in the ‘curve’ to see how all of this will play out. Factors such as rent- and mortgage-payment freezes, eviction moratoriums, personal and business bankruptcies, depletion of savings (if any), and others all take time but will culminate in the months ahead. Gonna be tough, especially if there is a ‘second wave.’

I used to teach high school and community college US history. We do not lack for a precedence.

My personal opinion is that the educational system in the U.S. has failed Millennials and that’s why many of them flail. The “old fashioned” skills of “useless” classes like home economics that taught about budgeting, the true cost of interest on revolving credit, or teaching simple mathematics without the use of calculators. Many of them can’t do an estimate of materials in their head. They don’t learn life skills and, while there’s a plethora of information on the internet, it’s no replacement for common sense, critical thinking, logic, and instinct.

If you want to torture a Millennial at a checkout, pay them in cash, let them enter the amount into their register, then give them the change portion in addition to the original bill. Watch the panic set in as many of them can’t do the math in their head.

OK Boomer

Katz:

Better still (in Canada), talk inches and feet, since they only know centimeters and meters!

El Katz,

“If you want to torture a Millennial at a checkout, pay them in cash,…”

BS. I pay in cash all the time, every time I go to any store, even Costco, where it’s hundreds of dollars each time, and the cashiers can handle it just fine, because they’re trained to handle it. Quit making up stuff about millennials.

Those newly unemployed Millions have wonderful opportunities to better themselves while enjoying a lavishly paid vacation.

Learn coding and get a highly paid job, guaranteed!

Or, if you are a real go-getter start flipping time shares using OPM for fun and profit.

There are opportunities galore for those willing to seize the moment!

Correct A MUNDO Tom!

In 2008-10, a friend was buying nice little houses at the courthouse steps in a small town for between $2 – 5K, fixing what needed fixing, usually about the same $$, then selling them for $20-30K and holding the note until folks had the income to finance through credit union or bank. Or just renting them out to pay a note he financed at his bank to buy the next one.

He was not rich then, and still is not rich, did OK, but mainly said he enjoyed working with the people who needed housing.

(fly over country, of course, with those numbers, eh)

Whenever I see the statistical expression Median, I think back about a dozen years ago of a rambling conversation on another forum, where we took the Median age of the participants to produce an amazing analysis. We even brought up Marshall Mcluhan’s Medium is the Message to provide further weight to the app!ication.

Excellent observation about interpreting median. A great statistics lesson.

I’ve often said you can prove anything with statistics, but only to people who don’t understand statistics.

Lawrence Yun is the Baghdad Bob of real estate.

“I’ve often said you can prove anything with statistics, but only to people who don’t understand statistics.”

My new favorite phrase (and/or business model).

With median analysis, it is taught in Statistics, remove the outliers. So for a example, a sample of 15, remove 1,2,3 and 13,14,15.

I’m just going on memory here. It sounds like in the analysis above, this wasn’t done, instead a warning about Distortion.

Median, Mode and Mean, Wolf

Perhaps next time around we can look at Mode? This would be an analysis of articles that count the times the same number or series comes up. Like what was spotified a few weeks ago, when 11, 22, 33 kept repeating, over and over..

Mode night not be relevant to price analysis, but it teaches us other things, like the number 8 re-appearing in transactions in Asian real estate. For a time anyway, before it ended a few years ago.

Rosebud,

You’re confusing median and average. It’s the “average price” that is distorted by outliers and where you can remove the outliers.

The median removes outliers by definition. That’s its advantage over average. And that’s why it’s used in housing. The median price is the price in the middle. It ignores all other prices. But the median is distorted by mix. Look at my table in the article. It shows you how the median works.

In summary:

– Median price is distorted by mix.

– Average price is distorted by outliers.

There are other methods in the housing market, such as “sales pairs” (Case Shiller in the US or Teranet in Canada) or “benchmark price” (the method used in Canada) or average price, and the like. They all avoid the issues of median price – being skewed by mix — but have their own issues. I like Case Shiller’s “sales pairs” method, but it’s so far behind it’s useless when the market goes into turmoil.

People used to have relatively small houses. Is there any hope of that trend returning? Large but poorly built houses don’t help people to get a leg up in society.

I was born in the early eighties and I own my own home. But, I’ve never had a good job (health issues have dogged me & self-employment has been my only earning power). I lived with my parents until I could buy the home, and I needed a loan from them to help me. But I paid cash, and the bank can’t take my home from me.

Generational leverage is many people’s only real path to any sort of independence. I think that was once understood, but now seems to be seen as some sort of twisted badge of shame (aka living with one’s parents). Mortgages give banks way too much power. It would be nice if there were good starter home options for people to buy with cash, after saving for a few years, instead of getting into the rent / mortgage cycle, and one or two paychecks away from disaster if unlucky.

I should add that my home is about 800 feet and quite old, but in good condition, and has resale value since it’s a one-story near amenities and hospital (aka retirement house possibilities). I feel very fortunate. But I think more people could be fortunate with good financial counselling (aka save as much as humanly possible, avoid unnecessary debt), live with your parents as long as you can both stand it.

My income this year is likely to be quite low. That’s how things are sometimes. I won’t lose my home over it, though. I have some savings, I’m being careful, and I have family if I need help. But many people don’t have the option of living in their own home or asking family for a little help if necessary. Many families are so leveraged it’s like a house of cards.

I hope that everyone can get a good financial education in the easiest way possible, not the school of hard knocks, and that they can be fortunate, too.

It would be nice if there was a path to home ownership for people my age and younger that didn’t involve being extremely lucky and extremely careful, but there it is.