The housing market faces ferocious headwinds.

By Wolf Richter for WOLF STREET.

Pending sales of existing homes of all types in April – contracts on houses, condos, etc., that were signed in April but that haven’t closed yet – collapsed by 33.8% from April last year, after having plunged 16.3% year-over-year in March, with the index plunging to 69, according to the National Association of Realtors today. An index value of 100 represents the pending sales level of January 2001.

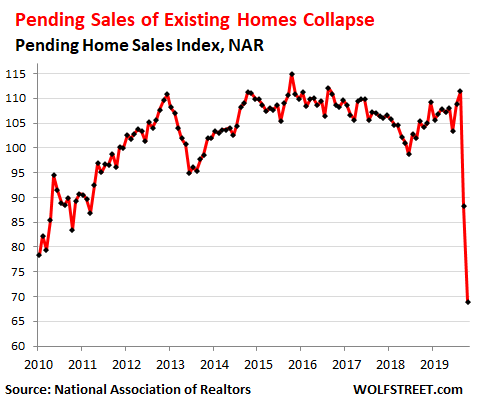

Pending sales are an indication of what closed sales will look like a month or two down the road. So this is an indication of the direction that May’s closed sales are heading into.

We already know how pending sales in March translated into closed sales in April. Pending home sales for March had plunged 16.3% year-over-year. And on May 21, the NAR reported that closed sales in April plunged 17.2%, the sharpest year-over-year drop since August 2010, during the Housing Bust.

Based on this relationship, closed sales of existing homes in May might be down by 30% or more, year-over-year. This will be reported in June.

The plunge of the pending home sale index differed by region, ranging from a breath-taking collapse of -52.6% in the Northeast to a plunge of “only” -26.0% in the Midwest:

- Northeast: -52.6% year-over-year to an index level 42.6.

- Midwest: -26.0% year-over-year to an index level of 72.0.

- South: -29.6% year-over-year to an index level of 87.6.

- West: -37.2% year-over-year to an index level of 57.1.

When sales volume collapses to this extent – no matter what the market is – it changes everything. It represents a market that has essentially frozen, with few buyers and few sellers, and lots of uncertainty. This is what happened in many other markets in the US, including otherwise very liquid markets, such as the wholesale market for used vehicles.

In May those markets have begun to unfreeze. Market participants have figured out how to deal with the requirements of social distancing. Keeping everyone reasonably safe during a pandemic that has already killed over 100,000 Americans in less than three months is a primary objective.

In the housing market, this has led to a change in the way business is conducted, including forays into accepting technologies, such as virtual open houses. This technology has been around for long time, but the pandemic pushed it into the foreground – like so many other technologies in so many other industries. And people are finding out that it sort of works.

But the market is facing ferocious headwinds, including 31 million people now collecting state and federal unemployment insurance.

More mass layoffs by big companies are announced every day, such as American Airlines’ message to its employees late Wednesday that it would cut its management staff by 30%. Delta came out with plans today to shed staff via early retirements and buyouts, along with Chevron that said it would cut up to 15% of its global workforce of 45,000 people, and Boeing which said it would cut 7,000 workers. Just one days’ worth of work, so to speak.

These are not restaurant jobs. These are jobs that come with good paychecks and benefits.

And this constant flow of announcements does two things: It creates uncertainty among potential home buyers that kept their jobs; and it removed potential home buyers from the market that have lost their jobs. This is a gigantic unemployment crisis, interspersed with a tsunami of bankruptcy filings, of even large companies such as Hertz, each accompanied by more layoffs.

Eventually – next week or next month or whenever – the job losses will end as more workers will return to work, and employment will start to rise, but from abysmally low levels, and even after rising for a while, employment will still be abysmally low – just less abysmally low.

So the housing market – in terms of sales volume – has two separate things to deal with:

One, the issues around keeping buyers, sellers, brokers, and others safe. The industry is addressing these issues in multiple ways, and is harnessing technologies to overcome the issues, and there is progress, and more deals are happening.

Two, the employment crisis that has already taken millions of potential buyers off the market. Even people who return to work after a stint on unemployment cannot instantly turn into homebuyers because it’s hard to get a mortgage, right after having been unemployed.

So volume will pick up some because the immediate issues of the pandemic are being dealt with successfully by the industry; but volume will not return to normal levels until employment has returned to normal levels – and having lost over 30 million jobs so far, this is just going to take a while.

More than plenty of supply: 6.3 Months’ unsold inventory of speculative houses. Read… Despite Record-Low Mortgage Rates, New House Prices Drop to Lowest April since 2015, Sales to Lowest April since 2017

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Have my popcorn ready, let’s see how many comments we will get from the usual suspects posting how their area are different and there are multiple bidding wars all happening in their observed neighborhood. All disciple of Lawrence Yum school of RE forecasting.

A very close thoughts to mine. In this condition, the unemployment will be a nightmare of higher paid workers, soon. You can see few examples in wolfs blog about the next round of cuts, which are permanent, indeed. Hold on to your hat, we are falling down.

And, now it will really effect the housing prices, too.

A lot of the older workers will never find comparable paying jobs.

That’s very true. This is true for tech jobs. I’m sure it’s true for many other industries.

That’s right. I’m currently working from home… crossing my fingers, knocking on wood, biting my nails, finding religion etc etc.

Harvey, and all ”you young boomer people” (pointing at YOU)

First and foremost, be using your time to update your digital skills as much as you possibly can, not just doing something to the pooch, etc

Those updated digital skills, combined with your long and ”real life” experience,,, really will help you find NEW work going forward in your current or recent field OR work in a NEW field.

After 7 years away from my primary professional ‘office’ work, albeit years spent in the field the same industry, at age 71 I was able to land a really good job at a really good company working with really good people on the basis of my experience being wider and longer than anyone younger in that company, though they did have some folks older than I was at that time, and I may have been hired with respect to their excellence.

Most contemporary software provides tons of free tutorials, and most also has actual paper books available for those of us who learned to learn with such antiques!!

Have finally promised someone to ”hang it up” this year, stop ”gallivanting around the countryside,” and have also promised to spend ALL of my ”stimulus” tax refund on improving my ”liquidity” position, so I really hope the comment about wines on this thread is correct this time too…

I also hope Wolf will come with a new larger size mug!! Hopium springs eternal in the heart of we Wolverines, eh

My son is in his forties, job wise has been always been an underachiever. Found a government job in maintenance, no chance for advancement until the foreman dies. I asked him once about their union, and he said they never pushed anything, if they win a too big pay raise next year they are all privatized. Take less and you have still have it when everyone else is losing theirs. I remind him he can still get privatized, and after letting your career skills languish, finding a new job gets much tougher. If you are the guy who always settled for less maybe that’s a resume highlight?

Plus remember Moore’s Law. Computing power will double every 18 months or so. True but physics are hard to deal with in nanometers. It’s still the same with job creation and loss. The longer you are out of work the more technology speeds destruction of old jobs and creation of new ones. 18 months and half the jobs have changed or disappeared…

Hey, anyone remember Tony Vu? I think that was his name.

Late night ads, 1980s,a young Vietnamese guy surrounded by babes in bikinis, hawking real estate phlegm.

Ya haven’t thought about him in a while. He’d have an arm around each blonde and say: do it for your family!’

Then there were the two midget (dwarfs?) brothers.

Let’s hope there is a mass extinction of these reno shows. They were OK until they turned into couple shows, and a constant $ refrain of how much they’ll get from the suite which justifies another 100 K mortgage. And sometimes the babe NEVER stops talking.

Tom Vu. Come to my seminar and learn how you can afford yachts and expensive hookers. He is now a professional poker player.

One of the many things I miss about the absence of F1 at Monaco is seeing the nice little boats docked in the bay by the tunnel the cars go through.

Not sure about the expensive companions, but it’s always nice to enjoy the race from your boat while drinking champagne with ladies who are getting some, but not too many, tan lines from the mid-day rays.

There’s always next year …

Actually, with the state of my city, I should relocate. Monaco is probably just outside of my budget though.

That was Tommy Vu, that guy was hilarious, ” you got enough guts to be rich like Tommy Vu? I got so many cars, I don’t know what to drive!

Buy my seminar!

Nope.

If I had a more useful collection of brain cells, this article is exactly as I would have described it.

Similar things are going to happen in many different parts of the world.

I wish it were so, however, here in Northern NJ, a lot of rich NYCers are buying high priced homes to leave the city. They have the money and have the motivation. I drove around my area and see plenty of “Under Contract” signs here. 40 million unemployed, and I don’t know one person who is. I’d like to believe the above, I guess I’m not seeing the proof of it. Not trolling here, but it seems around here like life as usual.

Its really lucky prices never go down in Toronto. Or my neighborhood. Would you believe on my street?

NoCalJim and SoCalJim do not approve this article!!!

CenCalJim might though ;)

Freejim checking in. Here in wide open flyover country, main street is busy.

We are swamped with field work. Sh*t digger so I’m tied to the real estate & construction.

I have no idea of if/when things slow. The last day of our imprisonment,

business was down 15% from 2019. As of today, we have caught up with 2019. That is a hard feat in my business. No popcorn for me. I’ll settle for a Friday fish fry and a few cold ones tomorrow night.

So basically the “imprisonment” was good for you:

1. You got to rest.

2. Your business is now up for the year, since previously you were down.

Not sure what you are complaining about. In fact based on what you said, more “imprisonment” will be even better.

Nope, no rest here.

I wrote that the last day of imprisonment we were

down from 2019.

Prior to being wuhaned, jan. & feb. were burners.

Not sure if we were deemed essential or not.

Did not bother reading the edict from the king.

No rest for us. Equipment has & will keep moving.

No complaints here.

Watch out, round two is coming to places that weren’t hit by round 1.

LM, you are correct as far as you go, but you don’t really go far enough IMHO.

As a retired analyst, ( of time, labor, materials and logistics) with a science related college degree (entirely paid for myself, btw re earlier articles) I have been watching this virus event since it was first mentioned in the south china morning post in early January, and my conclusions at this time:

1. We have a long way to go, locally, nationally, and globally; exactly how long is not knowable now, mainly because of the bad data so far, as has been commented on this site earlier.

2. The new cases, and following deaths, will not stop until this virus has killed all the likely cohort, of which I am one, mainly meaning all of us with the ”underlying” health challenges AND many younger folks with some sort of unusual condition, genetic or otherwise, BUT, it is clear that it has been slowed down by the various lock downs, and it will continue to be slowed down by the good practices now widely known, including especially the wearing of face masks to reduce the aerosols that appear to be the main method of contagion.

3. The economic damage from the social changes wrought by this virus will continue to develop for a long time too, perhaps a lot longer than the likely ”waves/surges” of the virus over the next couple of years.

4. Basically or base ball E, we are in the first inning with this event after what really appears to be the first 7 months — (based on various reports of the virus likely in November 2019 ) — so, the visitors, this virus, has had ”open season” a couple of places facing some really under prepared Teams/pitching in the top half of the inning, and now, in the bottom of the first, the home team is catching up a little,,,

5. So, 8 more innings, and since we all know full well that there is a wide variety of time per inning, let’s just say average will be 4 months, so 32 MONTHS to go before this first game of this series is over, eh?

I LIKE POPCORN BUT HAVE SWITCHED TO CRUNCHY COCKROACHES LIL COCONUT OIL & YOU CAN SURVIVE ATOMIC WAR OH! ADD SOME KAVA?

Please try to locate your CapsLock key and press it once. Solves your ALLCAPS problem.

Wolf, if someone comments in caps lock you should shrink their comment to size 6 font. Then put in regular font size (COMMENT WAS SCALED TO THE APPROPRIATE DECIBEL LEVEL).

Great article. In San Diego (Spring Valley to be specific) where I have been shopping for a home for four months, high quality homes that are well-priced sold quickly at asking price or slightly above asking price in March, April and May (sold or under contract). These homes are in the $500,000 to $750,000 range. I know it is a very small sample size in a specific area, but people are buying at prices that are still about double from 2013/4 levels. I assume the market will turn down with all of the headwinds, but I am in the market everyday and I have not seen it yet.

Eric same here in Ottawa, Canada. In the 650-900k single family home with a yard market, good luck unless you pay asking and have zero conditions. Otherwise do like others seem to be doing and pay over asking if you have conditions. Makes me sick. Nothing has changed here with Covid and the lock downs. Fewer homes going on the market but demand is insane. Maybe we will see a correction or maybe we wont. My gut is telling me year after year buy now otherwise you wont ever have the chance. Luckily for me i own a home and want to upgrade so im hedged. Feel sorry for my kids.

And the Primary Industry in Ottawa is…….drum roll please…….GOVERNMENT.

Of course demand is great in Ottawa. You are in the land of “every helper needs a helper, ad infinitum”

Yes you are correct. I should not be complaining i have travelled a lot and would not want to live any other place.

It took 4 years for housing to find bottom during last downtown in 2008 2009

So you need to wait atleast a year for price discovery

I am not saying its gonna go down or go up . My comment is specifically for price discovery and its take a year or two I guess

I am in San Diego btw and in a expensive neighbor where average home price is close to million usd..

I see the same softening price but not fireable going on

I think I have figured out why these folks ( if they are not imaginary) are rushing to pay full price for houses in the middle of this crazy period when most thinking observers realize that prices could be on a roller coaster ride back to the year 2000. These buyers are rushing because they have heard the rumors that their entire department is about to be downsized and they realize that if they hurry they can qualify for a mortgage before it is too late. My wife and I did the same thing back in 1987 when I quit my job to start my own company and my wife took a year pregnancy leave. The difference is we bought a house with a $450 dollar per month mortgage and these poor rubes are buying houses with $4500 dollar per month mortgages.

Eric Livingston

You’re really SoCalJim, aren’t you?

No. That was only my second comment on the site.

Uhauls are starting to pepper the streets of SF. It is a transitional period indeed and speculation about where the market is headed will soon be evidenced by hard data.

I was ready to start the first-time home buying process at the beginning of March and now I’m holding off. Hoping for prices to ease and the return of a buyers market soon–or at some point in the not-so-distant future.

We have been house hunting in the Lamorinda area (Orinda, CA) and what we’re seeing is that homes all go pending within a week with multiple offers. We passed on two homes that recently had deaths in the home and we were sure that these homes would have an issue selling but sure enough both went pending within 9 days. So at least for the Bay Area, I’m not seeing the market cool one bit and it’s still very much a seller’s market.

SF sales plunged 60% and supply is the highest in 9 years. That’s the data. The rest is stories.

Orinda inventory is up 20% from March but down 38% from 2019. You don’t like reading any comments that are counter to your articles do you?

So you use some data from an area west of Berkeley and you expolate that to means bay area is hot or seller market. Might as well said this time is different.

I meant to say east of Berkeley. If you said based on anecdotal evidence or observations, Orinda is a seller market, then I don’t think anyone including Wolf should have issue with that. To say an area where the median price is $2.5 millions is doing ok means the whole bay area is doing great is not just misleading but false.

I hear ya Elle. I am observing the same as you in Ventura County CA.

Real estate certainly varies from region to region. Or as Wolf would say “Nothing goes to heck in a straight line”.

Also matches what we see in Eastside Seattle. However, I think it dangerous to extrapolate. Wolf’s data is accurate but it does hide lower level (temporary) dynamics. There is a small set of highly motivated buyers here in Seattle that are (they think) immune from the econ impacts because they are in tech. Small number of marginal buyers, motivated, and a very small inventory of desirable homes in great neighborhoods during prime buying season.

These homes will get multiple offers and sell within a week. But the trends and data indicate this will be temporary. Go long buyer’s remorse.

RE is slow in Texas….real slow. Besides the CCP virus, oil & gas is in the “tank” so to say. Stay in CA though, we have enough immigrants.

Elle

Just to calibrate things, Orinda is a cute little town in the East Bay hills just west of Berkeley.

It has a population of 19,500 and median (not average) household income of $165,000.

The anecdotal stories might be accurate, but they sure aren’t statistically representative, which is where Wolf was going. But I’m guessing you knew that.

Why rushing to jump into conclusion? Wait a few months ( 6-12 months) and you will see the inventory level. Now people feel more comfortable to put their home for sale. And, they know they have to rush before anyone else does, and go toward the exit door quick.

Concept is very simple Elle, soon they will do a panick sell.

Wolf, respectfully people are feeling SF for cities like Orinda and Walnut Creek.

Wolf,

On the data, where is this data based on? Is it tax records recording property and title transfers? Just curious, I wonder how many transactions are going through without realtors through the iBuyer programs now. I can’t imagine it would be many, but would like to get a sense of magnitude.

Didn’t hear about the Chevron cuts, but that’s not surprising. If transports are going down, so is the oil guys. Thanks for sharing some real news as opposed to the barrage of garbage we get on TV.

Question: all things being equal, should one expect prices to go up or down post Covid19?

Answer: Down, due the facts in this and other articles published by Wolf. Thus, if the buyer is patient, the buyer will be rewarded with a lower price. The offer price doesn’t go down automatically – it only goes down when the seller starts to cave-in / give up on a sale at the current price level.

Both RD,,, lower after a few months of this event ”shaking out” so that all can see the damage happening every where when the fed et alia, having protected the banksters, etc., stops goosing the various markets;

Much higher when the long term effects of the dilution of value of our money becomes apparent.

Just one example from the last crash: When we understood that we had to move in early 14, I began watching the RE market where we had to move to, and found it down about 60% from 06; by the time we actually did move in late summer 15, that RE market in our specific area was already back up quite a bit, approx 40% in 18 months; the house we bought was up approx triple by dec 19, and although some z site says up another 10% since, IMO that’s fantasy.

Seems like this might be a good time to start negotiating, but that is SO location specific that it might not apply where you are.

VVN, I don’t disagree on the inflation aspect. But that is a pricing model that is probably beyond most of us.

i.e.

A situation in which there and extreme levels of unemployment AND inflation, simultaneously,

Thus, there’s little demand, yet the price keeps moving up due to the money printing.

Maybe we need 3rd axis for inflation on the traditional supply / demand curve.

Actually, no, I just figured it out…the houses get priced in gold or barrels of oil, if not tmrw or next year, then eventually.

I wonder if it has anything to do with Orinda being on the list of the 100 wealthiest cities in America? The rich are weathering the pandemic quite well from the statistics I’ve seen

Nels

Having lived there before retiring to FL, your comment is spot on.

If you llve inland in S.CA prices will plummet more as demand is less in those areas. Of course the fear of change and excuses will keep many from moving or selling once again.

Compton is 13 miles as the crow (or ammunition) flies from Manhattan Beach…you betcha prices plummet if you live inland

i have been seeing some nice houses come on the market that were originally purchased at the peak of the last market in early 2008. The poor saps that bought them have been trying to sell them high enough to break even on and off the last 12 years. Now they are finally accepting that they will have to take a hit to their equity and discount them enough to unload them. Most people buying a house right now at full price will probably take that same unhappy ride.

While workers “cannot instantly turn into home buyers because it’s hard to get a mortgage, right after having been unemployed,” it might be different this time. After all, being unemployed is not the same as taking time off for a pandemic sick leave. And banks might simply lower down payment requirements if the person had been employed with the same employer for a certain amount of time before the pandemic.

Curious: the big problem is exactly how many of those furlough’d workers will return to work right away, not merely in the US but all over the world.

Presently European airlines (I consider US airlines a very poor metric on the matter) expect to let go anything between 15 and 30% of their total workforce, the bulk of which is presently on furlough. It’s likely that those people will be hired back relatively quickly, if not by their old employer by somebody else, but in the meantime those folks will be truly unemployed: no job and no wages.

I don’t think overall unemployment will stay as catastrophically high as it is right now for very long: in many countries politicians seem to be finally coming to their senses. But it will be heartbreakingly high, at least until uncertainty remains at or near present levels. 10+% unemployment is bound to become the norm for quite a while and even countries with traditional low unemployment like Germany and Japan are bound to be heavily hit: a lot of people may be effectively immune to the virus but they are not immune to the reaction to it.

Traditional banks are bound to be extra cautious with consumer credit, at least until the dust has settled and they know who’s getting to stay and who is let go. In many countries there’s very strong resistance to taxpayer backing this kind (and many other) loans.

Smaller banks and shandow banks however may indeed behave differently: the former may believe they will be bailed out even if they are not “systemically important” while the latter may just feel the extra yield is worth the extra risk.

Again, the dust has barely started to settle so there’s no way to know how things will play out: my take is we are bound to see something in two/three weeks and to have a more complete picture in July, but those damn politicians just give me the creeps.

I wonder about the impact of distance work and distance conferencing will have.

Among other things:

-the demand for travel, hotels and dining when companies have discovered that a lot of meetings are smarter to handle online.

-people working more from home, less demand for services ( diners etc ) because people not turning up at the office ? Less demand for workers at these service providers ?

-need for large offices ? Less people around, less office space needed ?

Just a few points of mine.

We ended the (hard) lockdown here on May 4 but many businesses were allowed to re-open on April 13 already (as long as they kept a low profile to avoid people rioting).

“Distance work” right now is only used to allow parents with small children to stay home with them, but it is supposed to end soon as summer camps and “child parking” should start next week. There’s strong pressure from parents to re-open schools on schedule and normally in September which is turning into a political battle of the kind the government cannot win. But…

The big problem is right now there’s not enough work to warrant a full office staff working full time. Law offices are presently working at 30-40% capacity despite courts and archives now operating as normal. Notaries (needed for large transactions such as real estate sales and ironically for inheritance procedures) are operating at even lower capacity.

As we say around here, if notaries haven’t got any work we all should be really worried. :-(

Travel is a completely different bag. It may just be an European thing but airline bookings post July 1 (when quarantines are supposed to be dropped by all European countries bar Norway; let’s see who blinks first) are much higher than anybody expected. Granted, it will be a miserable Summer for so many folks but we should see a small recovery by August already. Hopefully, and if politics don’t intervene.

Now the big challenge is to allow hotels to re-open: it would ironic if hotels had to stay closed while “grey market” Airbnb and the like made a killing catering to travelers because they are the only game in town…

It is odd this situation, ideally there would be a keystone to a situation like this which can be restored to bring everything back to normal. But that’s just not reality, our economy has been transformed so much over the last 30 years that it was built on interdependency, take down one piece and everything comes tumbling down.

Kind of like the global supply chain, pick the choke point and gum up the works and everything falls apart

BTW MC01, haven’t seen a transportation related article from you in a while. Anything new coming out?

I am waiting for the dust to settle a tiny bit: pretty much all European carriers have announced larger than expected return to service from June 15 onward but there is a ton of craziness going on at the moment, with announcements denied the next day and confirmed again the other.

I want to provide at least a modicum of correct information.

Oh, and all internal travel restrictions in Italy will be dropped next Wednesday so I will be hopefully out riding a bit more. The moment international borders are re-opened though don’t expect to see me around much more. ;-)

Hey MC01,,, BEE CAREFUL,, AKA CAR aware!!

We are looking forward to seeing more of your insightful articles and posts, and do not want you motor cycled or recycled, eh??

Thank you.

Then there’s the “involuntary” salary reductions put in place by many employers. The company I once worked for applied a 2% to 10% reduction (based on salary level) in addition to “reclassifying” jobs and rewriting the job descriptions with adjustments to the pay scales (and they didn’t go up).

In addition, there were “involuntary furloughs” without salary for 2 weeks on a rotational basis that recently ended. Simultaneously, they offered an early retirement, a voluntary buy out for those not yet able to retire, to be followed by an unvoluntary reduction in force if they do not attain their targets on employee reduction. This will play out over a long period of time (the VBO’s will have to be complete by December).

There’s a lot of invisible carnage that has yet to become evident in any of the data.

And, by the way, the company that I am referring to is based in Southern California South Bay area and has a rather large footprint there. They also have presence in the U.S. from coast to coast (as well as in Canada).

Honeywell? Northrup, Raytheon?

The only homes that arent selling are junk. Bad layouts, open floor plans, ancient kitchens, on busy streets, asking $100k over market value, etc. The ones that are move in ready in desirable locations where the owner is simply asking the zestimate value are selling fast. A lot of people are waiting to sell which will end up being a big mistake.

That’s just NOT true I’ve been following New Canaan Ct area and there are magnificent homes on large properties an hour from GrandCentral listed for half the 2006 prices You must be talking about Commiefornia area

Anthony i think i made that mistake. I sold a rental property at the start of Covid for what i thought was reasonable at the time. Since then other exact units have sold for 20-30k over what i sold for. I wanted the money to upgrade from my primary residence but the market i am searching in is so hot you basically need to pay asking and no conditions to even have a chance. I am located in Canadas capital city which has a lot of gov jobs so cant speak for other locations. To sum up i wish i held that unit because i feel RE is only going up around here in the mid to longterm. Seems people are moving out of high rises etc and moving into the suburbs. No data to back that opinion but just my gut. Cheers

Hurry Anthony, buy 10 or 30 houses quick!!!!!! LoL

Buy now or forever be priced out right?

What’s so bad about 2015 and 2017 levels? Wasn’t that a healthy RE market?

2017 level? ???? You missed it, it seems.

Employment is already down to levels not seen since the 1990s as of mid-April data. Mid-May data (to be released early June) will be a lot lower:

I meant the 2015 and 2017 home sales levels you referenced in article. The unemployed in CA right now are adding $2400/month in Federal money (stimulus/ pork) to California’s bank accounts. If forbearance plays out such that we end up with 6-12 months of payments (our largest expense) pushed out for a couple decades, we will end up doing ok for the year. Not sure everyone realizes how easy forbearance is to get. Answer 5 questions and you are in for 6 months with 6 more available if needed. And many need it. But many many jobs will come back. The problem is uncertainty with govt. programs. If they extend unemployment through end of year with new outbreaks popping up, and then covid disappears/plays out, and next year is getting back to normal, that sounds like an ok scenario to me.

Lets clarify some information here. You are confusing forbearance with deferment. I don’t know how “easy” it is to get forbearance but I know investors that brought these MBS don’t want to get an ass pounding. Imagine you brought some product or service, and you tell the lender you’ll pay them back in 20 or 30 years. Why on earth would anyone suckers, I mean investors, pay for that? If I use your service for buying a house, are you OK with me paying you the commission 20 years from now? Hence, lenders are tightening on loan standards. Yes, I know it’s like closing the barn door after all the animal escaped already.

https://www.bloomberg.com/news/features/2018-05-24/small-time-bankers-make-millions-peddling-mortgages-to-the-poor

Second, some jobs will come back soon. Some jobs will come back in a year or two. Unfortunately, some jobs are lost forever. When you have a once in a century global pandemic, this affect your perspective and things may never be the same again. Just look at this article on saving rate.

https://www.cnbc.com/2020/05/29/us-savings-rate-hits-record-33percent-as-coronavirus-causes-americans-to-stockpile-cash-curb-spending.html

I would never in a million years think US debtdonkey (I mean consumers) would do this. Will the consumers have short memory? Will they go back to their usual ways of buying junks they don’t need with money they don’t have? We will see. I actually think this is good for the economy in the long terms. However, election is coming plus aren’t we all dead in the long terms.

I’m not sure you should promote forbearance without listing the possible consequences.

Forbearance seems to make it the responsibility of the borrower to work out an agreement with the mortgage provider. This sounds to me like refinancing the loan or a loan modification. This will be at their terms and there will be additional fees involved.

I would guess when this forbearance actually shakes out there will be a lot of people that end up losing their houses.

Nothing is going back to normal, because it was not normal to begin with.

I guess it was your other headline I was referencing.

https://wolfstreet.com/2020/05/26/despite-record-low-mortgage-rates-new-house-prices-drop-to-lowest-april-since-2015-sales-to-lowest-april-since-2017/

Heheh, Wolf, I think you need to slap on a denominator for with that chart, probably vs the total # of people in the US as a function of time. That will make things a bit more stark. The chart you show is pretty tame if one assumes the population stayed the same… which it hasn’t.

This chart is insane. We are NOW below car sales total from back at the depths of 2009. Cash fer clunkers coming???

https://fred.stlouisfed.org/series/TOTALSA

yes, population adjusted, it would be worse. US pop:

1999: 273 million

2019: 328 million

If it’s anything like the stock market, housing prices should skyrocket. Nasdaq with 2 or 3% of an all time high right now.

Are our hidden overlords more or less making a full confession that the trading volumes on the stock markets have just been fake all along?

I was watching the tape on SPY the other day and happened to see a 3million share sell order hit the market mid-aft. Bids disappeared and SPY’s fell 2$ in 1 minute as all the machines and their phantom liquidity stepped out of the way… before gobbling it all back up again.

My point being that our ‘hidden overlords’ aren’t manipulating volume, the machines are by passing fractional shares back and forth a million times per day; on the other hand, the overlords have literally become the market, pumping and/or dumping to arrive at areas of actual liquidity as it suits their narrative.

So yeah, nothing’s changed.

Mark:

“….our ‘hidden overlords’ aren’t manipulating volume, the machines are by passing fractional shares back and forth a million times per day; on the other hand, the overlords have literally become the market, pumping and/or dumping to arrive at areas of actual liquidity as it suits their narrative.”

Very nice!

I thought the stock market was only crazy because of the retail investors? Driven by RobinHood and the reddit people trying to buy the dip?

I saw articles that it’s throwing off the institutional investors who thought they knew where things would go. Then bam, 800,000 new Robinhood/similar app users.

@Ethan It takes only the barest perusal of a Commitment of Traders report to realize that the truth here is paradoxical. Institutional traders are always hedging and therefore mixed in sentiment, large non-commercial traders speculate and dictate direction in an endless search for liquidity, whilst retail although occasionally driving a market, will hold their positions long past the point of efficacy and often end as net losers; and that’s the paradox – can retail drive a market? Sure. Do they often end as cannon fodder nevertheless? Yep.

Presently:

-institutions are nearly fully hedged right now and eating the market share

-there are more than double the retail positions long than short the indexes

-large traders are in contrast, largely short

Deep pockets that scale short into retail rally’s are worth noting. Follow the money.

House are and have been overpriced. Prices falling should be good. No?

Who wants a country full of debt/rent/house slaves?, just so landlords, speculators and hedgefunds that used cheap money to buy housing can get rich.

I’m surprised, in the face of a lockdown, things didn’t slow a lot more.

There are no “houses” anymore. At least in the traditional sense. Houses used to be for living, but now it’s just another thing to lord over people just like your 401(k) balance, etc, etc.

Basically everything is now fair game for the “high school is never over” meme.

It’s the opportunity to avenge your high school self against your tormentors

Well stated MB.

Umm… If “high school isn’t over” for your crowd, you CAN change your social circle.

Plenty of grownups out there, if you look. Suggest trying the smaller homes in the nicer neighborhoods. Those are likely to house the people who don’t feel they have to keep up with their neighbors in order to be happy.

Very good observation and true here in our hood WS.

In a hood with all the houses on the block built exactly the same per neighbor born and raised in house across the street, and his brother in the house next to him.

Lots of adult conversations on the street we all walk our doggie pals on, bike on, etc., as much as we can, including safely at all hours.

Very mixed hood in all respects these days, with some newer homes twice or more the $$/SF of the older ones, but also many folks here from all walks of life and all ages, etc., etc.

More houses for sale today than in late fall 19, and some have been pulled; will be interesting to see how it works out in my every other day bike ride…

Real estate is not a rational market.

And a home is the biggest investment most people make.

Got friends whose stable jobs just went away?

Think prices are going to drop?

Maybe it’s a good idea to wait a little bit, see how things settle out…

Buyers control the market price of homes, and Real Estate is priced at the margin.

NO ONE ever has to buy, someone always has to sell.

It just takes a while to play out.

Is it a good time sell?

Yes.

Is it a good time to buy?

That depends on your particular circumstances.

I agree with you. I have a family of five; with 3 small children. We sold our house a few months ago and moving/renting has really upended our life. I don’t have several years to time the RE market. I need to find someone who will take a discount for the uncertain future and make the best decision I can in the next few months.

“NO ONE ever has to buy, someone always has to sell.”

That’s a good sentence, I need to remember it!

Covid-19 State Foreclosure Moratoriums and Stays

Nevada (non judicial foreclosure)

Governor’s Declaration of Emergency, Directive 008, March 29, 2020

Prohibits initiation of foreclosure and evictions based upon default under a mortgage until emergency declaration dated March 12, 2020 terminates.

https://www.nclc.org/issues/foreclosures-and-mortgages/covid-19-state-foreclosure-moratoriums-and-stays.html

“In Arizona, banks and mortgage servicers, in conjunction with the U.S. Department of Housing and Urban Development (HUD) and the FHFA, have agreed to suspend evictions and foreclosures for at least 60 days from March 30, 2020, with the potential to extend that period for as long as state and local emergency declarations are in place.”

https://www.nolo.com/legal-encyclopedia/coronavirus-foreclosure-relief.html

Homeowners can get forbearance. When there is a forbearance deal, the servicer can’t forclose anyway. Gotta wait until the homeowner defaults on the forbearance agreement.

What if there’s enough Fed bailout money sloshing around to buy up all the distressed RE? Seems like we might be a nation of permanent renters soon.

Permanent is long time, but what’s wrong with renting?

Does “Stop making your landlord rich. Buy your own home with a magic bank loan worth hundreds of thousands of dollars! The mortgage payments are roughly the same as rent!” sound familiar? Considering that it has been drilled into our heads since the 90s, it should.

Yeah problem is that interest payments and outgoings used to be almost equal to rent in many places. Now rent is massive compared to interest and outgoings. If you buy your flat in London where I am on interest only loan you’ll pay maybe 1/4 the rent for the same place. When rent is eating 50-60% of your net income that is life changing.

The catch is you have a humongous debt liability. If prices go up then you get a massive tax free cap gains bonus due to the leverage. If prices go down you are financially stuffed for life.

So do you take the gamble or not?

I don’t know the answer anymore. This is what stupid monetary policy has done.

A nation of renters, an oligarch’s dream

Is it because renters can move easily? For better work oprtunitities, to escape unfair taxation, crazy neighbours, etc.

“When sales volume collapses to this extent – no matter what the market is – It represents a market that has essentially frozen, with few buyers and few sellers, and lots of uncertainty.” So why it’s Powell buying real estate, homes? The alleged function of the Fed is to prevent “freezes” in “markets”, or at least freezes to your Almighty God, the Credit “Market” God to which mankind must bow down in eternal servitude and deference. Why isn’t the Fed in “freezing” our homes the same way it’s unfreezing the assets of the Fed ultra rich friends?

Okay, so this is very confusing. Yesterday Liz Ann Sonders put out a Tweet quoting the US census bureau on a very different RE stats: According to the US census bureau:

“April new home sales came in at +0.6%, way above -23.4% est. & -13.7% in prior month (revised up from -15.4%); median home price -8.6% y/y to $309,900; average selling price at $364,500.

So what is the Census bureau talking about? How could NEW home sales be so different from EXISTING home sales? I can’t fathom why that would be. Anyone??

Lisa,

you’re talking about NEW HOUSE SALES. Very different from PENDING EXISTING HOME SALES.

Read all about the NEW HOUSE SALES and prices as reported by the Census day before yesterday … right here, including charts:

https://wolfstreet.com/2020/05/26/despite-record-low-mortgage-rates-new-house-prices-drop-to-lowest-april-since-2015-sales-to-lowest-april-since-2017/

“Lisa you’re talking about NEW HOUSE SALES. Very different…”

No Mr. Richter, I was actually POINTING OUT that New HOME SALES were widely divergent from EXISTING home sales and asking what the reason for this is. Do you have an answer? I went to the link you provided and read that whole article, which did not really explain it. To say that new homes are sold by ‘pros’ and they’re more flexible in their pricing doesn’t really explain this huge gap as represented by the US Census Bureau. Typically brand new homes during a RE slowdown will sit for months & months before the “pros” drop the price. Especially the more high end ones.

Lisa,

One reason for this may be the difference in timing between the close of ”the deal” for new houses/condos and the completion and close of the final real closing where the people can move in, versus that for existing residences.

Used to be that houses in ”tracts” would sometimes be sold months in advance of the start of construction, and I know that was true of many condos where they wouldn’t start anything vertical until most or in some cases all of the units were sold, with deposits in escrow, etc.. ( Never did this myself, but have bought ‘existing’ RE in 5 states, all of which we could close in 30 or less days.)

Another reason may be that builders, and, gasp, maybe even their bankers, have seen this coming, and were already prepared to sell quickly because they had been stuck holding too long during the last crash.

The new home builders will throw in “upgrades” that normally would add thousands of dollars to the price (but, in reality cost the builder next to nothing). The existing home buyer cannot afford to do that.

Putting in a “premium landscaping package” or “upgraded lighting package” (aka some additional can lights), upgraded flooring – granite -appliances are not uncommon practices. Those add incentives to purchase. As in the case of a flooring or appliance upgrade, the builder can give you an “allowance” that doesn’t show up in the sales data.

Thanks for the thoughtful replies, VintageVNet and El Katz.

Katz, in my area (mid peninsula) the new home prices are staggering and though they do look cosmetically impressive with brand new SOTArt kitchens and perfect lawns w/new landscaping they’e on average a half to a million dollars more than a similarly sized and VERY nice older house. You pay hugely for the rather superficial difference. In our last downturn 2007 – 20012 NEW houses in my neighborhood often sat on the market for months. Existing houses almost always went within weeks or days. Also, the idea that the contractors who build these houses are “pros” at selling and the professional realtors are less “pro” is not something I’d agree with (that’s referring to Mr. Richter’s take on this).

I still don’t why existing homes would maintain their high level of sales when were we’ve been in an economic crisis since Mid March. My first inclination was to question the government stats on this.

Lisa,

There is NO divergence between my two articles. In both cases, sales volume was massively down compared to a year earlier.

But “pending home sales” in April is one month more current than “closed sales” in April.

My article on May 26 discussed “closed sales” of new houses – most contracts signed in March or earlier. Sales volume was worst April in years.

My article published on May 28 (this one) discussed “pending sales” of existing homes in April – all contract signed in April. They’re therefore timelier than “closed sales” in April.

So pending homes sales in April plunged a lot further that closed sales in April because it was one month deeper into the crisis than closed sales.

This lockdown is clearly driving people out of high density housing located in cities into the ‘burbs. Both to escape the conditions most likely to catch COVID and because so many jobs have shifted to working from home. At my main hospital, the secretaries that coordinated our schedules, work issues, and finances are still working from home.

Most all the new housing for sale will be in areas with open land, i.e., the ‘burbs. Lots of that new housing was being built before COVID, and with the clear paradigm change to shifting OUT of tightly packed cities (Wolfstreet just had another article by John McNellis about how this is going to affect high rise office buildings), people able to buy a house and looking for a house are going to go for these new homes in the ‘burbs

P.S. I used to live in Ventura County. It’s a wonderful place to live if you have kids, not so great for singles. Great schools, very low crime. There were already people with jobs in Los Angeles who chose to live in Ventura County and COMMUTE 3-4 hours everyday to work. Now that many have discovered that they can work from home you can bet that more people will be moving out to Ventura County, even though most of the cities there are tightly growth controlled with few new houses being built (Oxnard being the main exception)

So Wolf, the key here is to apply ALL THE LOGIC from John McNellis’s article to realize that some areas will definitely benefit from this COVID pandemic. Not all housing markets will crash. This totally explains previous posts about Orinda, CA and Ventura County housing markets doing well

This is why I read the comments today: guessing someone would highlight and explain this dissonance

LaMOrinda is a unique area….. and not everyone can afford to buy in those enclaves. The terrain limits the amount of property that can be developed in those areas. They are also located on the BART line – with their own stations – serving downtown San Francisco/Oakland/Oakland Airport/SFO.

People who are completely relying on remote employment may find a few things:

Trends shift…. working from home may not continue forever. What then? As far as those Ventura county folks, I had a woman direct report who lived in Ventura County and attempted to make that commute…. then, eventually, started sleeping in her car near work and showering at the gym…. and finally burnt herself out and got fired because those 2-3 hour one way commutes weren’t always that short… Same with the folks in LaCanada-Flintridge or even Anaheim Hills (due to the 91). Location still matters as does access to employers and transportation (airports/rail).

I would imagine (knowing how corporations work) that the career track for someone working from home will be inferior to one who works within the office – even forgetting aptitude. It’s a lot easier to steal people’s ideas and present them as your own when the more talented person who came up with the idea isn’t sitting across from the boss making the pitch or there to protect their work product. The ability to suck up one-on-one has it’s benefits. Relationships still matter.

Some of the supervision of remote employees will be taken over by automation…. and the need for “management positions” will be diminished. This will further limit career growth as the “next steps” won’t even exist.

El Katz,

Your story of that woman sounds more like she lost her home completely (remember something called the GFC of 2008, caused by …. subprime mortgage defaults?) rather than that she chose to live out of her car to avoid the long commute. It’s far more likely that a lot of things were coming apart in her life to drive her to that state of dysfunction, and if you were her direct boss you obviously lacked the ability or empathy to try to figure out what was going on and try to help her, and instead just fired her.

One way commutes in SoCal of 1-2 hours (2-4 hrs total) are very common, with commutes in the 1 to 1-1/2 hour range being extremely common. Commutes longer than that are life sapping for sure and so rational people looking for better places to live time the commutes and base their home locations based on those numbers.

The eastern most cities of Ventura County, Oak Park and Thousand Oaks, are especially well positioned for people with jobs in the LA area. My kids went to school with many kids whose parents were employed in the Hollywood or TV entertainment industry, which are mostly based in the northern LA area. Two parents of kids I knew worked for Disney in Burbank, one was a secretary, the other an upper level lawyer.

Our next door neighbor was an entertainment lawyer who worked somewhere in LA

Simi Valley had a large number of cops who worked either for LAPD or the LA County sheriff’s office

Cops and actual film making aren’t jobs that can be done remotely, but many of the ancillary work, HR, finance, accounting, etc. can easily be done remotely with video conferencing. It’s way more efficient than spending 3 extra hours of commuting every day, which lots and lots of people in SoCal do.

My original point was about why Ventura County could only benefit from people wanting to escape from the crowded conditions of LA, mostly people with kids. That’s a dynamic that’s been there for a long time already, and the COVID pandemic will only accelerate that process

1) First, the corona coma.

2) Plague #2 : Antifa unleashed its potential Ilhan energy.

3) Car dealerships are next.

I haven’t seen any softening of price here in Tustin in Orange County next to Irvine. Condos that were 750000 two years ago are now going for 950,000. That is just for a condo that sold in 2011 for 250K. Basically prices tripled in this area in ten years. No one wants to sell because if they buy something else their taxes will go up. I see the real estate price explosion as a proxy for massive dollar devaluation. Like the stock market all rational pricing metrics seem to be thrown out the window. That has been California as long as I remember. The last real real estate recession was in the mid 1990s.

The Chinese have kept the prices up in the Irvine area.

This is all you need to know:

“While coronavirus mitigation efforts have disrupted contract signings, the real estate industry is ‘hot’ in affordable price points with the wide prevalence of bidding wars for the limited inventory,” Lawrence Yun, NAR’s chief economist, said in a statement.

It is hard to sign a contract when you are ordered to stay at home.

Totally!

The NAR is definitely the people you want to listen to when it comes the RE market. They were amazingly prescient in 2007.

On a side note, a drug dealer told me that meth usage would lead to whiter teeth and a healthier complexion.

Meth 2020!!

Lawrence Yun, totally trusted “economist”. I can always count on him to tell me the truth about real estate market, just as he was super truthful about the state of the market before 08 and after. I trust him about just the same as big Tobacco companies or Facebook, I am sure all of them only have our best interest in mine.

C’mon VA and PI, give ‘so called J’ a break; he’s really too easy !

OTOH, the sarcasm is too broad to win Wolf’s ”best dark humour comment of the day” award, even though it is very amusing..

And for Felix above, a friend bought a house in CA in 2013 for a little less than half of what it had sold for in 2010, and although it may have been a little under the market, it wasn’t much under in that locale, and sold last fall for well over double the 13 price.

Jim, are you in the business or not? Docusign has been around for quite a while, and I have personally used it 4 times in the last several years. I have been thousands of miles away when I sign the contracts.

What gives?

Where do I get a drag on that weed !? Stay tuned as I believe this is following the 1929 pattern….

SocalJim

What I don’t understand is, with your RE insight & expertise, you’re obviously filthy rich (maybe even richer), yet you manage to take time out of you busy day, and hand out pearls of wisdom to us little people.

Hint: it’ll free up more of your deal-making time if you mastered digital signatures; eliminates hours of riding around in the lime to physically sign stuff.

Here is a pearl of wisdom …

If you are have decent health, you surround yourself with family and genuine friends, and you have a good enougn job, then you are wealthy. Too many people waste life chasing material wealth only to find that brings emptiness.

We’re into month three of actual “distancing”. So far people have been living on savings and credit. The “stimulus” was spent at Wal_Mart and Target, not on essentials. 31 million unemployed isn’t going to hit overnight, there’s too much momentum in the economy. What’s not going to be pretty is six months from now when the savings are gone, the kids college money is spent, retirement funds are raided, and credit cards are maxed out. And God help us if the Gov’t thinks they can help by printing $2 Trillion a month for six months.

The canary I use is toys; and one of my favorites to watch is boats. And it’s happening now. Look around (even on Craigslist) and you’ll see boats for sale, lots of them. And getting cheaper. Likewise berthing space. Heck, they’re giving them away. I’ve seen several nice 25’+ sailboats given away in the past month for free.

Another indicator is wine. Yes, there’s a “normal” discount, but when you start seeing boutique wines selling at less than 50% of retail (not restaurant pricing) then you know the cash is getting tight. In 2002-2003 you could buy a case of really good stuff at discounts of upwards of 90% as wineries flat ran out of cash. And back then restaurants and tourists (major customers) were still open and visiting.

Now is the time to hold cash and do anything it takes to maintain your job and hope that massive inflation doesn’t suck you in.

Great observations, all is not well. Corporations are taking the chance to slim workforces with thousands of layoffs; this is becoming a daily event. Give it a month or two, when medical insurance, back pay, furloughs turn into layoffs, credit cards are maxed….mortgage payments are due….the riots in Minnesota surely have an economic dimension, the misery will spread. Then we’ll get the second wave of COVID19 in the fall.

Cash is not trash.

Walmart is now selling used clothing thru an affiliation with Thredup, a reselling site. That’s a big indicator to me, they are competing with Goodwill.

I used to love going to GoodWill stores to hunt for old video games and early computers (Amiga, Atari ST, Atari, etc.) The stores would have piles of random surprises.

Now Goodwill stores are all upscale. Fake hardwood floors. Curated goods. Fancy signage. Goodwill passes off the computer donations to Dell which takes and destroys all the vintage computer treasures (some kind of eWaste contract.)

Pretty easy business when you get your product for free I suppose and not surprised other people are coming for their business. But I miss the old thrift store days.

In this economy with all the unemployment there are sure to be a lot of garage sales this summer. Happy hunting.

Where are these cheap boats!? I’m seeing almost zero inventory for used wakeboard and pontoon boats in California. (Medium to low end all bought up for isolating on the water) Prices much higher than 5 years ago for same boats.

Michael Engel, your haiku-like lists have usually been entertaining, but you’re clearly drifting into murky territory, sounding more like a conspiracy theory addled White supremacist.

They are scheduled to partially reopen Disney World on July 11th. I do not see the bottom dropping out of the housing market in the Sunshine State at this time. Some landlords are going without rent. The cruise ships are not sailing out of Port Everglades.

Disneyland Shanghai has long re-opened but there are no takers: the once unstoppable Chinese consumer is too concerned about the future to go to an amusement park. And that’s without the ever-increasing daily dose of doom-mongering peddled by our Western media: low morale is turning into downright defeatism and that’s hardly conductive for Mr Mouse’s antics.

Cruise ships are another matter: the big problem right now is incredibly not the virus but crewing and staffing them.

Getting crews home has proven to be extremely hard, chiefly because their own governments have proven to be incredibly uncooperative: it must be incredibly good to bully your own citizens stranded the other side of the globe but apparently a good chunk of the population supports shooting the other chunk and starving it to death.

In many cases hundreds of Filipino and Ukrainian nationals have been stranded for weeks in limbo after completing their quarantines because there was no way to get them home.

Getting these folks back to work would prove to be perhaps even more challenging, especially now that everybody is screaming “second wave” and the mere mention of a bunch of folks (legally) drinking beer in a bar is enough to send people in a rage.

I genuinely honestly don’t know why airlines even bothered announcing a re-start of service or why cruise lines haven’t just shut down and liquidated, there’s no point doing anything in this climate.

And people want to buy an extremely expensive house now?

Now is perhaps the best time to buy a house, a buyers market.

Not a buyer’s market yet. I’m stalking a “toy” car to replace a practical one. Prices have softened somewhat but not enough to entice me to pull the trigger.

As pointed out by others…. wait. Few will time the bottom, but those who stalk neighborhoods may find a gem. My daughter did in 2010 in East Bay of SFO. Held it 6 years and doubled the purchase price and tripled her money (and lived there for half the cost of her apartment in Lafayette for a SFR with double the square footage).

You just have to be prepared to move quickly. And a lot of cash to waive in front of their face doesn’t hurt either.

I passed in front of a large realtor’s office this week.

While they have started re-listing properties, prices haven’t budged at all: business as usual one may well say.

Nobody expected crazy high discounts to be advertised right away but a 5% off the asking price could be a good start in this climate.

There may be good deals to be had down the road, but right now there aren’t any.

Staterooms could be turned into floating condos.

Wolf how do you think state and local government shortfalls will play into this? Rob Bonds yesterday was looking for ideas for revenue increases aka taxes. Gov. Newsome mention cuts to schools, police and fire. San Francisco has a massive shortfall along with Oakland

State and city budgets are now a huge mess. We’re just a couple of months into this, and they’re now grappling with it. This is not something that will go away quickly. Obviously, they will try to get more money from every source, borrowing and taxing. But they will also have to cut spending. And those spending cuts are going to be felt in the local economies.

I don’t know about this. “Spending cuts” is just not American. It’s been a while, but did California cut its spending when it was paying people with IOUs. And spending cuts tend to be temporary anyways.

If states were to default on their pension obligations, then that’s a big changer.

Everybody knows those are already defaulted. That is why I laugh why people get hyped up over them. It’s basically money that never is going to be paid.

Can states and local municipalities default on their pension payments?

Palo Alto is talking about cutting 70 non-union employees. They are still negotiating with unions about cuts but I’m not holding my breath. There have been numerous cuts to services as well. Source: https://paloaltoonline.com/news/2020/05/26/facing-budget-shortfall-palo-alto-agrees-to-cut-more-than-70-positions

Can they??? This isn’t SS which can modestly raise payroll taxes, have Congress reimburse the money they took or lower health care costs boosting nominal savings into the trustfund. These legacy pensions were nothing more than PR started after the post-war ii era by states to recruit labor which was in short supply. Only a fool thinks all that was kosher. Much like cities, they will be slashed and not much can be done.

You have obviously never lived through a real recession….

And so there likely also goes the big raise in gas taxes we approved in the 2016 election that was supposed to be spent ONLY on the sorry a** roads that have become SO common in CA, the state that used to have the very best roads in USA during the governorship of Ed Brown, Jerry’s dad.

There has been some significant improvement of the 101 recently, especially in the Salinas Valley general area, but there is SO much more needed that I can only hope and pray the puppet politicians in Sacto don’t steal this voter approved tax money once again.

There are already spending cuts. My local town just cut its capital budget based upon indications from the state that local aid will be reduced. These aren’t job cuts like school teachers, but they are very real and will mean fewer people engaged in public works at at time when we need more, not less.

“at time when we need more, not less.”

The problem is that the political class **never** discovers a time when “we” need less, not more.

The seed corn is gone.

When you ZIRP savings, there is no savings growth.

And then another emergency happens, latest in a long proclaimed line, powering the one way, upward ratchet of spending.

Not a problem…just raise CA income tax to 20% top rate…it will only be double of 2010…

They are indeed. I see it firsthand. Prevailing view, which I also hold, is that once the real pain starts to bite the unions will win the day at the Federal level. State/Local bailout comes early next year after Dems retake White House and Senate.

NOTE: This is not a political support based comment… just an opinion of most likely pathway as I see it and others believe within government.

The Minneapolis city council will have an emergency meeting tomorrow at 12:30 (pm CDT). My neighbor is on the council and I imagine he and other members are under a bit of stress right now.

Dan Romig,

I wish everyone the wisdom and courage to sort through this properly so that it can be resolved quickly. All the best!!

You can always count on government to extend and pretend. They will kick the road with accounting gimmicks and raise taxes. Look to Illinois as the model.

The State assembly and unions are already pushing back of Newsom’s 10% cut proposal as too extreme. My guess is that 10% is actually a token amount an not enough.

They will keep digging the hole deeper until the situation is too large to avoid massive layoffs.

You have to remember that with the shutdowns gone, total

deficits won’t be that large in aggregate.

Rage,

The deficit already exists because while the private sector was sheltering at home and not spending so tax receipts collapsed. Meanwhile all those public employee and project costs continued to be incurred regardless if they worked or sheltered at home. So there is already a big hole in the budget. If tax receipts do not balance out spending that hole gets even bigger.

Tax receipts are not going to immediately return to anywhere near the pre crisis level . Some jobs have totally disappeared. A best it will start out slow and gradually pick up momentum.

The public sector leaders want to avoid the pain experienced in the private sector. The decision to make no adjustments will create a bigger adjustment in the future.

States cannot deficit spend. How the problem plays out is another article. States can refinance their current debt at lower rates, while new muni bond issuance will compete with Federal Treasury issuance. The key for state revenue is property tax. If home values fall and property tax revenue, the issue gets more difficult. States with higher property tax rates (poorer states) have no room to raise taxes. In the great D taxes is what drove people off the land. 2008 however gave us a blueprint, the live-in foreclosure. The Fed has already opened up the REFI market which will be used to tap locked up collateral. Will outside entities like Blackrock be allowed to siphon away the money. Ellen Brown has suggested a state run bank. a regional equivalent of the Fed. The Federal banking system has a number of challenges.

Be interested to see some actual data re taxes driving folks off their RE in the depression formerly known as the greatest AB.

Not dis agreeing because I have seen quite a few properties foreclosed and auctioned for failure to pay the property taxes even when they were otherwise lien free.

These days, the potential for various loans usually enable folks to duck and cover for a while longer, but those kinds of deals did not really exist in USA in the 1930 era from what I have read.

Wolf, any data available through your channels for this?

Thank you.

They could cut Curtis Ishii’s CALPERS pension of over $418,000.

Illinois legislators just voted themselves an $1,800 pay raise effective July 1st.

I suspect the old 19th century term: prepackaged bankruptcy( the 19th century version of a bailout) will make a comeback. One of the problems of allowing dead hulks like wells fargo, bank of america and Citigroup to remain around on its retail side is it increased the amount of corporate zombies and laid the foundation for the subprime junk bond/ loan bubble, which they hated.

They should have crammed down in 2008-9 beyond Bear Stearns. For many reasons, many they would see as altruistic, they didn’t. One is, the contraction would have been worse initially, eating into the “white white minority’s” living standards, damaging a faithful servant. Once you lose them, it’s a political hot potato, this the expansion needed rebooted quickly.

I find it very interesting and telling that prior to this event, the all cash home buying corps (Open-door, WeBuyUglyHouses, etc.) advertised like mad on local phoenix radio stations. It was incessant. For the past month and a half, silence.

They moved to TV…. no one listens to the radio if they are not in their cars (and commuting was greatly reduced). Watch the night time news (Channel 3) and you’ll see the 2 local guys and one national still making the pitch.

It’s “early days” so far……wait until the end of August at least to get a “slippery” handle on what is/has happened. Unless fed/states extend support payments I believe there will be very dark economic clouds what will forecast the near future. Just wait.

Nah…July 4th. If they have to place a general ban on fireworks out of fear that 100K+ may have heart attacks due to anything loud that might send them over the edge in this climate. That’s your first telltale of bad conditions ahead. And that move in the Gld/Slvr ratio might suggest forward concerns if it continues the current trend….if.

Inland to dump.

Coastal to hold in Ca.

The mistake too many are making is the assumption that home prices will fall in a recession. Historically, this is just not true.

Sometimes they fall. Sometimes they level off. Sometimes they rise.

That is what history shows. History also shows that rarely do home prices fall in a recession if they fell in the previous recession.

Yeah well show me your historical record of 0% interest rates for a decade and QE/S

your funny, home prices fell in 90-97 and then again in dot com bubble…then in the great recession….

Prices held up, and in many cities, actually rose slightly in the dot com bubble.

Jim, I lived thru it, please…… crowded tops are very dynamic and leave victims..

u got a 2 plex in balboa in 2001 on a motorola sales job salary….

This is generally true, the Fed lowered rates below the level of inflation and what was a dot com bubble turned into an RE bubble.

SocalJim,

LOL….I bet you are a Realtor trying to save the market, LOL

If you consider latest recessions, they have fallen at each one, specially in Los Angeles. 2001, 2008, and… Now. Yes, Now.

It is falling, in Los Angeles, the prices haven’t gone up for past 2 years and now it is down slightly.

A lot of multi family duplex and triplexes are cutting the listing prices ($50K on $900K houses), after siting in the market since last winter. These are great income properties.and wait for the home owners to put their houses for sale in a massive scale and then you can see the drop.

One dumb trick some realtors are using is that they keep the property as pending, where they re-list it at the same time !!!! Just to show that they have a buyer.

I see the PPT are hard at work this afternoon…

1) Pending Home Sales history : 2013 high and low are the trading range.

2) There was no sign of weakness in 2016. It was smooth sailing.

3) The upthrust of 2015 led to persistent falling sales, until Dec 20018.

4) The last attempt to recover from the 2018(L) led to a lower high in Feb 2020.

5) CV lock down led to a waterfall collapse.

6) In Kass R/R a similar situation, but the 2016(L) was much deeper.

7) When transport breached the 2016(L), there a waterfall collapse.

8) Chicago IL Boing HQ and Motorola HQ (MSI) led to the sharpest PMI

decline since the 1980’s.

9) The current weekly NDX is a black hanging man candle, at the top, a lower high. May 26(H) is an upthrust !! An UT might start NDX correction in June.

Only fools buy at the top….my cousin is now doing it in Las Vegas after selling 6 unit property in SLO….I don’t get it other than his wife is a con…..

buying real estate today shows most have no patience……top buyers are retail…..10 to 1 odds PE is selling their fed price fixing ill gotten cheap homes now….

Large southern city here. RE market has significantly picked up in the past couple weeks. I have Zillow searches set up for several areas. They’re showing both a big increase in listings, and lots of “pending” tags just days later. No real price cuts except on properties with issues that weren’t selling back in January either.

No idea if this will continue. Nor what the rest of the country looks like. But so far it appears here at least that C19 is looking more like a big speed bump than a train wreck.

I’ve been using the NASDAQ as a leading indicator for the direction of Las Vegas real estate. I had a conversation with my realtor last week and she said something about the real estate market here being correlated to the NASDAQ. I guess it’s obvious to many that both have historically had a similar degree of volatility (down 75%, up 350%, that’s all normal). Now that almost all asset prices are rising together, the NASDAQ tells me how much to ask for the house.

I know this all looks terribly bleak.

But doesn’t anyone else feel like it’s just another excuse for “the biggest stimulus ever”… just as it’s increasingly always been?

I’m certain it’ll be bad. 2007/8 was bad.

Many seemed to imagine we’d be in years long depressions, a great reset. Blah blah.

But then look what happened.

Idiocy ruled supreme.

Don’t fight the fed.

BTFD.

Buy into the dream, not the reality… Tesla etc.

So what makes this crash so different?

I won’t believe we’re in a multi-year depression and bear market until

I see it.

I’m in on a BIG BTFD opportunity coming up, as much as a long depression.

Just because we can’t imagine what stimulus we’ll see to extend and pretend, and keep the proles ‘confident’ to keep spending, doesn’t mean it won’t come.

Once UBI comes on then the risks of deflation will be near zero.

UBI could deflate all past debts to insignificance.

UBI would give confidence for tens of millions to spend in gay abandon.

ZIRP would mean more Wall Street gambling and consumer spending. Why save with UBI around?

Extend and pretend still has teeth.

Don’t call an end to the show until the CBs and govs have played their hands… which I think they’re still keeping quiet about while they make another killing on ‘bad news’

This is only anecdotal, but, my purchase business has exploded the last 3-4 weeks.

Received 5 new purchase contracts this past week, and, pre-approved 5-6 new buyers.

My referral agents are getting very very busy, after the lockdown lul. It feels like people are fatigued from waiting, and are now moving full steam ahead with their purchase decisions.

Lender guidelines are also loosening back up. Not to the pre-covid point, however, definitely removal of the very conservative restrictions imposed at the height of the lockdown.

Remains to be seen what happens over the next 30 days, but, no joke it’s somewhat of a frenzy right now (from what I see).

There has been a lot of residential and commercial real estate construction in Korea in the past few years, too much for any possible demand imo. But just the past few days have seen some banner ads (very common in Korea on the streets) for excavators, something I’ve never seen before. Think the housing boom is over.