Fed shed MBS. Loans to “SPVs” flat for fifth week. Repos in disuse. Fed still hasn’t bought junk bonds, stocks, or ETFs. But it sure sent Wall Street dreaming.

By Wolf Richter for WOLF STREET.

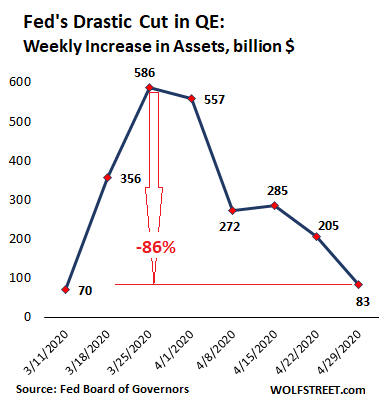

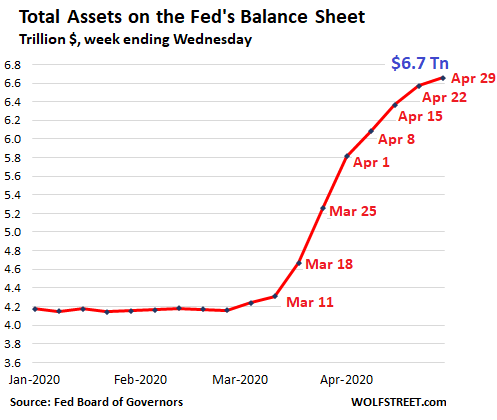

Total assets on the Fed’s balance sheet rose by only $83 billion during the week ending April 29, to $6.656 trillion. That $83 billion was the smallest weekly increase since this show started on March 15, and down by 86% from peak-bailout in the week ended March 25. This chart shows the weekly increases of total assets on Fed’s balance sheet:

The Fed is thereby following its playbook laid out over the past two years in various Fed-head talks that it would front-load the bailout-QE during the next crisis, and that, after the initial blast, it would then cut back these asset purchases when no longer needed, rather than let them drag out for years.

On January 1, the balance sheet stopped expanding as the Fed’s repo market bailout had ended. However, in late February, all heck was breaking loose, and the Fed first increased its repo offerings and then on March 15, started massively throwing freshly created money at the markets, peaking with $586 billion in the single week ended March 25.

But since then, the Fed has slashed its weekly increases in assets, which shows up in the flattening curve of the Fed’s total assets in 2020:

The Fed cut its purchases of Treasury securities. The balance of its mortgage-backed securities (MBS) actually fell. Repurchase agreements (repos) have fallen into disuse. Lending to Special Purpose Vehicles (SPVs) has not gone anywhere in five weeks. And foreign central bank liquidity swaps, after spiking in the first two weeks, only rose modestly, with most of the increase coming from the Bank of Japan, which is by far the largest user of those swaps.

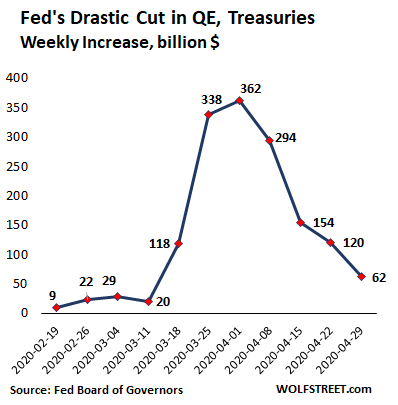

Purchases of Treasury securities get slashed.

The Fed added only $62 billion of Treasury securities to its balance sheet during the week, the smallest amount since this show began, down 83% from the $362 billion during peak-Wall-Street-helicopter-money. This chart shows the weekly increases of Treasury securities on the Fed’s balance sheet:

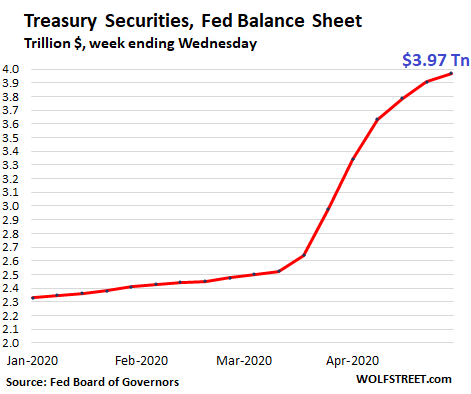

The chart below shows this effect: The curve of Treasury securities has been flattening over the past few weeks, after the massive frontloading of purchases in March. The total is now $3.97 trillion:

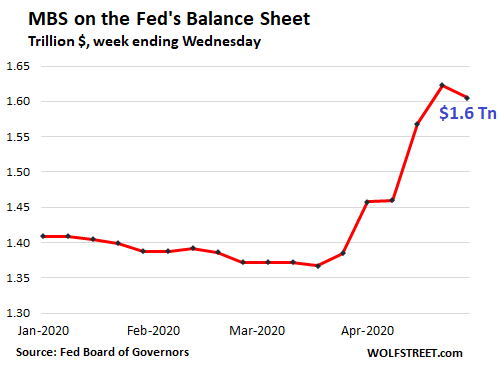

MBS purchases and balances fell.

The Fed has drastically cut its purchases of mortgage-backed securities over the past five weeks, as reported by the New York Fed transaction summary (net purchases, for the weeks ended):

- $157 billion (Mar 25)

- $145 billion (Apr 1)

- $109 billion (Apr 8)

- $58 billion (Apr 15)

- $56 billion (Apr 22)

- $38.5 billion (Apr 29)

MBS trades take weeks to settle. All of the $38.5 billion in MBS the Fed bought this week will settle in May. Since the Fed books the MBS trades only after they settle, the balance sheet lags by some time the actual trades.

In addition, if the Fed buys no MBS at all, the MBS on its balance sheet will decline due to the pass-through principal payments that all holders of MBS receive as the underlying mortgages are paid down or are paid off. There is currently a boom in mortgage refinancing underway, which creates a torrent of these pass-through principal payments. Just to keep its MBS at a steady level, the Fed would need to buy a significant amount of MBS.

This combination of drastically lower purchases, the erratic settlement dates, and the torrent of pass-through principal payments caused the balance of MBS on the Fed’s balance sheet to fall by $18 billion, to $1.6 trillion:

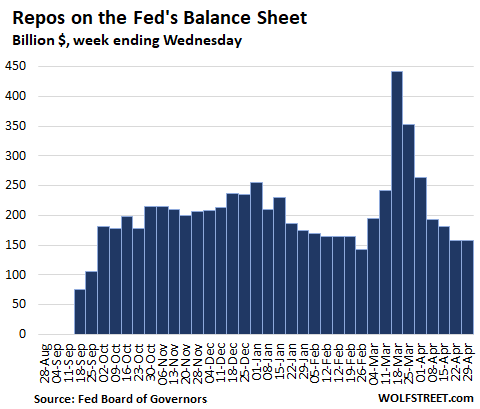

Repos fall into disuse.

In recent weeks, there has been no demand for the repurchase agreements the Fed offers in the repo market. The repo market itself is running as it normally does, a multi-trillion-dollar affair on a daily basis. But the Fed’s repos are only being nibbled on every now and then. What’s left on the Fed’s balance sheet are several term-repos from weeks ago. Repos are in-and-out transactions. When repos mature, the Fed gets its cash back, the counterparty gets its securities back, and the repo balance for that entry goes to zero.

There are $158 billion in repos left on the balance sheet. I’ve dug up most of them. Over the next two months, they will all mature and roll off the balance sheet:

- From April 29: $2.0 billion, 1-day

- From April 13: $14.5 billion, 28-day

- From April 6: $6.3 billion, 28-day

- From April 3: $1 billion, 84-day

- From March 20: $31.2 billion, 84-day

- From March 13: $17.0 billion, 84-day

- From March 12: $78.4 billion, 84 day

Total repo balance, at $158 million, is down 64% from the peak ($442 billion):

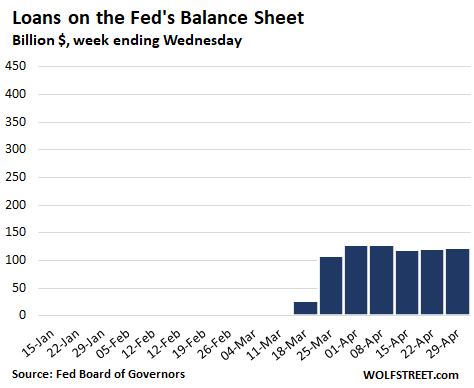

“Loans” to SPVs & Primary Dealers went nowhere in five weeks.

The Fed’s alphabet soup of bailout programs are in effect loans to Special Purpose Vehicles (SPVs) that the Fed has set up in conjunction with the US Treasury Department, and to its Primary Dealers (the big broker-dealers and banks the Fed does business with). The Fed in essence lends to them, and they can buy whatever the Fed directs them to buy or lend to entities the Fed directs them to lend to.

This scheme is a way to get around the limits imposed on the Fed by the Federal Reserve Act. Congress could stop these schemes but applauds them.

When the Fed announced the first batch of its alphabet soup of bailout programs, “loans” on its balance sheet ballooned. But over the five weeks since then, they have remained essentially flat at around $122 billion:

The Fed shows these loans by category:

Primary credit: fell to $32 billion, from $34 billion last week and from $43 billion three weeks ago. This SPV was expanded to be able to buy some “fallen angel” junk bonds. But the balance has dropped since the expansion and the Fed hasn’t bought any fallen-angel junk bonds. Some of the positions have unwound, and the SPV paid the associated loans back to the Fed.

Secondary credit: $0. Designed to purchase corporate bonds, bond ETFs, and even junk-bond ETFs. None were purchased.

Seasonal credit: $0

Primary Dealer Credit Facility: fell to $25 billion, from $36 billion two weeks earlier. Amounts the Fed lent to primary dealers to buy stuff with. After the initial burst, some of the positions have been unwound, and the loans were paid back.

Money Market Mutual Fund Liquidity Facility: fell to $46 billion, from $49 billion last week, and from $53 billion three weeks ago. This SPV bought corporate paper and other short-term assets to bail out money-market funds. After the initial burst, the positions have started to unwind, and the SPV paid back some of the loans.

Paycheck Protection Program Liquidity Facility: Jumped to $19 billion from $8 billion. This is where the Fed lends to the SPV to buy from the banks the government-guaranteed loans they have issued to “small businesses” (hahahaha) under the PPP program. This SPV does nothing for small businesses. It just takes some loans off the books of the banks after they’ve extracted their fees for processing the PPP loans.

These loans show that the Fed has not done any of the things with SPVs and Primary Dealers over the past five weeks that the markets were drooling and raving about – they didn’t buy junk bonds, ETFs, or stocks. The markets just haven’t figured it out yet.

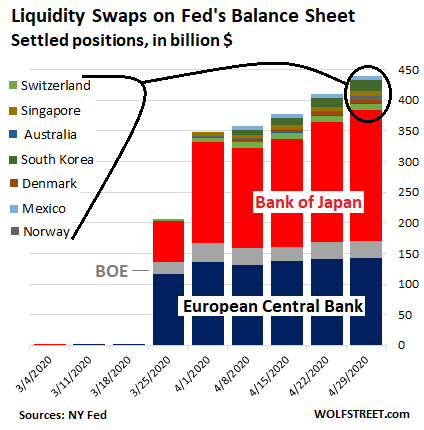

Central Bank Liquidity Swaps.

The Bank of Japan is by far the biggest user of the Fed’s “dollar liquidity swap lines.” Swaps with the BOJ surged by $18 billion from the prior week to $214 billion and now account for 49% of the total swaps on the Fed’s balance sheet.

The ECB is the second largest user of the swap lines, with balance of $142 billion, 32% of the total. The Bank of England is far behind with $28 billion.

The Fed also has opened swap lines with the central banks of Canada, Australia, New Zealand, Sweden, Denmark, Norway, Switzerland, Singapore, South Korea, Brazil, and Mexico. There are no swaps with the central banks of Canada, Brazil, New Zealand, and Sweden. And the remaining central banks are small fry (see chart below).

With these swaps – maturities of either 7 days or 84 days – the Fed lends newly created dollars to another central bank, against domestic currency posted at the Fed as collateral. The exchange rate is the market rate at the time of the contract. When the swaps mature, the Fed gets its dollars back, and the other central bank gets its own currency back.

The combined amount of those swaps – the country data is released by the New York Fed – increased by $29 billion from the prior week to $439 billion.

If…

Since March 11, the Fed has printed $2.34 trillion to inflate asset prices, restart the chase for yield to where investors would lend to companies with deep-junk credit ratings, already too much debt, and business models that have run aground. It did so to bail out asset holders and Wall Street.

If the Fed had spread that $2.34 trillion equally over the 130 million households in the US, each household would have received $18,031. For many households, this would have gone a long way to helping them through the crisis. But this was helicopter money for Wall Street.

In addition to logistical difficulties of selling a home in the era of social distancing, there is the explosion of a historic unemployment crisis. Read... Mortgage Forbearance Balloons, Home Sales Plunge

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The FED got embarrassed that the market had its best month in 30 years while unemployment hits the highest in 30 years.

As Loretta Mester of Clevelend Fed pointed out all they did is to make market pricing work more correctly – see John Hussman for exact quotes.

Meaning no actual market.

Only up not down

Is that what happened in March? What are the YTD returns for the indexes?

I’m far from being a fan of Fed intervention, but pumping out easily disproven factual inaccuracies isn’t going to help non-interventionists.

“…make market pricing work more correctly…”

And this was meant seriously? Really?

You can’t make this up.

Even Lenin would raise his eyebrows at a statement like that.

Jos,

Lenin’s favorite car was a Rolls Royce.

You’ve got to fine tune these things for public perception. You can’t have people thinking this is a plutocracy after all, otherwise more of them will want to become Bolsheviks.

And if wallstreet was more than just occupied for a week, and more like burnt to the ground, then they’d have failed at their game of getting richer. Surely another market crash would be in their better long-term interests. Or maybe they really are clueless about the terrible “populism” streak, heaven forbid the people try to stick up for themselves.

I’m sure there is truth in the mass perception image as a variable the Fed wants to paint with. Beyond that it is a wise move to do it now, It would be very embarrassing to keep adding more and watching w street dance close and happily while everyone maintains distance.

Also the economic equation using: %P = %M + %V – %Q

“The destruction of monetary velocity is offsetting inflationary pressure” P=price of things, M=monetary base, V=the velocity of money Q=real output. Read

The Crosscurrents of In/De-Flation

Written by Michael Lebowitz and Jack Scott | Apr 29, 2020

Convincing data for deflation early and big inflation later. However, rates have to stay low or nobody will be able to even pay the interest on all the debt, that’s my view.

… they will buy bonds until they can’t

A,

“had its best month in 30 years ”

Most people on this site are smart enough to know that if mkts fell 1200 points in March only to recoup 600 points in April…it isn’t like some illuminati triumph for shareholders (and wait for Q2 results in July/August).

Facile manipulation of measurement periods/percentage changes is skeezy when stock brokers and politicians do it…commenters too.

You seriously believe that? Why do you ignore that given the fundamentals, no “recoup” is even remotely reasonable?

The market is probably even more overvalued now that it was prior to Covid.

And it’s ball due the bailouts and the Fed.

Cramer’s head in the picture of both the market record short term gains and unemployment stats said it all.

Darn Pope Gregory XIII inventing the Gregorian calendar in 1582 just to make the FED look bad!

It is a formula tool, that is all, not a moral judgment unless you want it to be. Use it or don’t.

“My words but a whisper, your deafness a shout” Ian Anderson :>{)

Exactly the market knows where the bread is buttered and the toast always lands on the floor dry side down.

Jello spine Powell will do whatever our Commander-in-chief tells him to do.

Nice to see the FED attempting to “flatten the curve”!

You can keep your satisfaction over supposed alleged embarrassment (are even capable? I doubt it). I want heads to roll. I want Jerome in jail with the rest of his criminal bankster fraudsters with no social distancing allowed.

The fat cats need another “taper tantrum”

But wait. Is QE the appropriate tool for this covid-19 inspired problem?

Maybe that’s the problem. When you have a hammer, everything looks like nails.

QE is almost *never* the right tool.

But it is the easiest for DC to employ, so it is now habitually used to paper over the rapidly expanding dry rot in the American economy.

Plus, QE triggered inflation has the beloved political advantage of being readily blame-able on top-hatted Capitalists rather than money excreting politicians.

Thanks for the update, Wolf. No yuuge amounts of added helicopter money needed this month since markets been on a sugar high the whole time. As soon as the crack addicts realize that a miracle cure for the pandemic is not in fact going to be available next week and start selling off again, that balance sheet will resume ballooning. Fed, as result of the post-GFC “there are no limits to what we can do” mindset, has lost all inhibitions – they will literally print a GDP-multiple of helicopter money to throw at the stock indices, if that’s what thy think it takes. Their only measure of “the economy” is the indices, and operationally, their only mandate is keeping those numbers in bubble mode, to be able to point to them and say, “See? Prosperity!”

How exactly is the Fed involved in the PPP.

The Treasury said $349 billion was approved for loans by the SBA though a lending partner.

If the money eventually comes from an SPV, how much money did the Treasury actually put in. Who put the rest?

The way I understand it. The business borrows from a bank, and the SBA guarantees it. That’s the PPP.

But the Fed lends the bank under a different program called the PPPLF.

Source:

How is the PPPLF different from primary credit, the main discount window lending program for depository institutions?

The PPPLF differs from primary credit lending to depository institutions in a number of ways. The primary credit program accepts a wide range of collateral—including PPP Loans—but the PPPLF only accepts PPP loans as collateral. The primary credit program is open only to depository institutions, while the PPPLF is open to all eligible PPP lenders, both depository and non-depository institutions. In addition, primary credit loans are made with full recourse to the borrowing institution, while extensions of credit under the PPPLF are non‑recourse. PPPLF extensions of credit are extended at a slightly higher rate than primary credit loans (a fixed rate of 35 basis points rather than the current primary credit rate of 25 basis points), are for a longer term (PPPLF loans are for two years while primary credit is available for up to 90 days), and the amount of the PPPLF extension of credit is determined based on the principal amount of the underlying PPP loan.

So where exactly did the $349 billion come from?

In a fractional reserve financial system like the USA, all loans from banking institutions are money “created out of thin air”. Imagine 2 banks each creating 1 million dollar loans (out of thin air) to two different companies. Then those 2 companies deposit its million into the other bank. The banks now owe each other 1 million each, and transfer it at night. $2 million was added to the economy by private banks.

Money doesn’t “come from” a place. It comes from a banker’s belief in the value of a business proposition. The belief that you’ll actually sell all the inventory your loan will buy or that that house in California will be worth more next year if they have to foreclose.

3 reasons for the taper

1. Jawboning worked

2. Market is northward bound, which as per the Fed is the way it is to be

2. Even the Fed cannot keep adding $500 billion every week

In short, the market rose and therefore the Fed walked back. If the market falls in May, the Fed will come roaring back.

I think the chief reason for this display of force was to prevent security yields from blowing up. That crisis has for now been averted and private investors effectively lent shaky companies like Boeing enough money to get them through the end of the year even at the present level of cash burn.

The European Central Bank is doing the same: a lot of honey’d words but the promised flood of liquidity hasn’t materialized yet. The Bank of Japan is doing exactly the same: preventing yields from blowing up like they always do in moments like this. As long as investors think somebody will buy those Carnival Cruises bonds from them no matter what, all is fine.

If investors still want to buy stocks at an obscene markup it’s all gravy.

Why are central banks doing this? I think the two chief reasons are these.

First, for all the talk about 2% CPI inflation targets central banks know perfectly well the reality on the ground is completely different. Financial sector inflation is one thing, garden variety inflation is another matter completely. We cannot afford pushing the latter kind higher, period.

Second, central banks know perhaps even better than governments the true enormity of the crisis we face. Remember that behind public faces like Jay Powell there are a lot of very intelligent and very skilled people with access to raw data we can only dream of. They know perfectly well politicians need to stop wasting time and take a decision: adopt an aggressive containment strategy for the virus, like Korea and Taiwan have done, bite the bullet and soldier on, like Sweden is doing, or just declare victory and move on, like China is doing. Plainly put there won’t be anything left to stimulate if we don’t start rebuilding as soon as possible. Central banks can help manage economies (whether in bad or good fashion) but cannot create them out of thin air.

Here here.

Notice no mention of backing off in QE, only reduced increases:

“The Fed is thereby following its playbook laid out over the past two years in various Fed-head talks that it would front-load the bailout-QE during the next crisis, and that, after the initial blast, it would then cut back these asset purchases when no longer needed, rather than let them drag out for years.”

Each now unapproved market drop will be met by vigorous Fed “front loaded” QE which will never be rolled back only increased until the next unapproved market drop, followed by another “front loaded” QE.

At some point one might well ask when do all these front loads become back loads?

Japan has kept it going for a while. Their public also buys their bonds due to their exporting prowess.

Everything on a much larger scale for the US. In the mid term, will the public continue buying bond in the US , or just continue to buy to front run the fed?

The Fed will always be the buyer of last resort, and last resort could be anything above 3.5% on the 10 yr to keep things from getting out of hand-large amounts of debt not being able to pay back more frequently to prevent swan flocks waiting on the periphery from visiting.

Two words: Mission Accomplished

…..string pushing

It appears as if the religion of Fed fanatics is strong enough at this point that all the Fed needs to do is prime the pump a little and stand back and let the greed of the fanatics take over.

I cannot get past the feeling though that smart money is taking this opportunity to liquidate now, knowing that at some point soon, the economy is going to weaken to the point no one will be able to justify owning stocks. I guess I should not say no one, there will still be fanatics justifying owning stocks even at triple digit PE’s but I cannot believe that will be the majority…. I guess it is possible though, it would not be the first time I underestimated the idiocracy of the masses….

The Fed started lowering rates when employment was record high and the market was hitting all time records.

I’m just glad their models can predict black swans like a pandemic 3-6 months in advance.

Dr.Powell. flattened that curve.

On a serious note my assumption is that all the above instruments currently sitting idle were put in place to be ready for use when the actual crisis hits. Like a 3-course meal we’ve only been served the entree. The main course and desert will be to die for.

Also, some SPVs haven’t been set up yet, including the one that will handle TALF and the munis. They may be more complex to set up and it may take a while. Setting up an SPVs requires the Treasury to agree to it and put in equity capital, which may also be more complicated, politically. Mnuchin was talking the other day about this.

Aarrgh! The TALF! Now with extra design features from Munchkin!

To quote Hugh Hendry: “I recommend that you panic”

Or run for the hills, unless the TALFs and the SPVs are coming from the hills, in which case run away from the hills.

C

Derivatives cubed of real wealth that destroy others’ real wealth squared that in turn destroy dollars to cause inflation and collapse eventually.

Really real wealth consists of real things like gold, silver, rare earth metals, basically the periodic table including the real derivatives of them-things made from them and then art, software, intellectual property, teaching etc..

No one gets bailed out from buying, shorting too much, or making bad decisions, unless friends and family care to help. Got to start over somehow. Money needs to be finite just like everything including the universe

The Fed’s PPPLF only shows 19.488 billion on h.4.1

The Treasury said all the $349 had been loaned out.

What gives? Did the banks just invent $330 billion out of thin air and let the SBA guarantee it.

Iamafan,

The Fed only buys the loans from banks that want to sell those loans.

My prime candidate is Wells Fargo because the Fed put limits on its assets as punishment, and WF bumped into those limits and couldn’t expand its lending. So when PPP came along, WF said, sorry we cannot play because we cannot carry those loans. So the Fed came along and said, OK, we’ll take those loans off your hands, so you can lend under the PPP program.

PPP is supposed to end around June. Since PPP is a loan forgiveness program, in theory the SBA will have to pay the banks 350+300 = 650 billion. I don’t think that will happen that way. PPPLF will be the garbage can for PPP come June.

PPP is already considered “spent” in the Treasury budget as if 100% of the loans would be forgiven. So the taxpayer is paying for this, not the Fed. That’s how it was set up from the beginning — as an expense to the US taxpayer. The Fed is just helping WF and other banks that had bumped into regulatory limits on the amount of assets (loans) they can carry.

Wolf, I was trying to find this “spent” expense on the Treasury earlier before your comment. I could not find it. I can’t even find the SBA expense budget.

Need your help to show us how this actually works.

Iamafan,

The $377 billion for the PPP is part of the $2.2 trillion stimulus package which has been signed into law and is now part of the official US budget to be spent. The Treasury is already issuing bonds in huge piles to pay for it, as you have noted here earlier. You can get more visual detail as to what else is in the stimulus package here:

https://www.visualcapitalist.com/the-anatomy-of-the-2-trillion-covid-19-stimulus-bill/

Thanks to you and Wolf for the rigorous exchange

Mr. Richter, correct me if I’m wrong but the PPP loans are a work in process. They will eventually show up as debt sold by the treasury. Will the Federal Reserve eventually buy them and put them on their books?

Incidentally, the banks are paid up to five percent to process the SBA loans. That’s probably better than what they could have gotten if they loaned money out for good collateral.

While the expenditure was already budgeted (we know the President signed the bill on March 27), the SBA itself does not have the money yet. That’s the point I have been saying. In fact, the Treasury is still raising the large budget by selling a lot of cash management bills.

So the PPP money today is coming from the banks. Note they have massive reserve balances anyway due to QE4.

At the end of two months, the loan is either forgiven or not. If it’s forgiven, then the SBA must refund the banks. Normally, this is simple transfer payment from the Treasury TGA account at the Fed to the bank’s reserve account at the Fed.

But as you and I are suggesting, the fed can simply buy the loan using the PPPLF program instead and the Treasury can extend and kick the can down the road. They don’t have to pay the banks after 2-3 months from the TGA. The Fed pays the bank by buying the loans. Extend and pretend.

One other note: There are two options to the PPP. The payroll option does not have to be paid back if used for two and a half months of payroll funding. If the money is used for other than payroll it then becomes a loan for 1% which will have to be paid back. The SBA is underwriting both and the banks will transfer them accordingly.

Minor adjustment….2nd reference on Total Repo Balance reads $158 million rather than billion as noted a few lines back. [Don’t ya just hate all those blue pencil editors out here?]

The Fed has satisfied Wall Street and made the oligarchs whole for now. If there is any threat to the oligarchs assets sinking the Fed will be called back service to transfer more wealth to them. The Fed will not stop because it can’t . The Fed must play till the last hand is dealt. We are in a late stage fiat game and the last hand has to be played to the bone.It’s illogical and insults ones intelligence to think otherwise .

Dr. Doom:

As Wolfe said, the Fed restarted the stalled “chase for yield” game.

So now you have to venture further out on the tree branch, to a place where you know the branch can not support your weight!

They will need a computer.

“…till the last hand is dealt. ”

“”…Jacks ,Queens, and Aces, their faces in wine; do Lord deliver our kind”” Grateful Dead

In the Great Depression they did it all wrong by raising rates and causing 25% cascading unemployment.

In the Great Great Depression they did it all wrong by lowering rates and putting 25% out of work in one fell swoop.

I’m convinced now more then ever that the fed has not printed enough! They will quickly discover that they need to print 5x more to offset the deleverging cycle we’re about to experience.

I propose shovel-ready projects to pump oil back into earth, for future use.

Pedro:

Not to make light of your comment, but Mish Shedlock agrees that the Fed’s current money creation is likely not going to be sufficient to offset the decline (contraction) in overall credit as lenders reduce their lending.

Guess we will know in time if popping bubbles are deflationary or inflationary.

The question is: have the bubbles that have formed into one superbubble, with more bubbles soon to join the superbubble to create a hyperbubble, actually been popped? This has gone way beyond economics. It is going to take enormous political will to truly pop these bubbles. Will we don’t have. Are you prepared to see families living on the streets such as the Depression caused? No? Thought so. Are you prepared for engineers to be made redundant, their firms go under and their skills atrophied thus reducing national manufacturing output for as long as it takes to pay off 6.5 trillion in debt and get the economy back into equilibrium? Didn’t think so. WE are the obstacles to equilibrium. Our opposition to such outcomes ensures that there is no other option but to keep blowing up bubbles. Until the final hand is dealt as someone said earlier. That final hand will be marked by the whole house of cards falling in a heap, but that is the way it must be. One thing is that after it all falls down, a much needed new age of understanding of the limitations of capitalism and central banks will come about. God knows when though.

It is not the contraction in lending that is offsetting money creation, it is debt default. Inflation is caused by credit purchases. Deflation is caused by credit default.

When the amount of money being destroyed by credit default is more than the amount being created by credit purchases, deflation occurs.

Leverage works in reverse also….

Yep, when 1 borrowed dollar put into the system creates a negative dollar of output.

Hope so because my gold will hit at least the 3k that BOA predicts Or probably MUCH higher than that when the parasitic FED is done destroying this country and it’s currency

Your gold won’t be worth anything in dollars because you won’t accept any dollars after the country and currency are destroyed.

Bartering with real money. The start over of a fallen economy

The Fed hasn’t bought any. But are we seriously supposed to believe that they will continue Operation Jawbone?

The sequence of events in the future might look like:

1. Market drops 15%.

2. The Fed steps in for real and the market rallies 20 to 25%.

3. The Fed steps back and even reduces their balance sheet and the market stabilizes for a while.

4. Repeat step 1 to 3.

Yup! I wonder why we call it “the market”. And the temerity of the Fed to say market is working. And we have to believe it is capitalism. Essentially a crock of s***

The omnipotent Fed speaks and allows the majority who believe in them to do their dirty work for them.

the fed keeps two books.

I don’t think this is the case but even if they are doing it, who’s going to arrest them? Like seriously. Anyone getting jailed from Goldman, etc, after the mortgage debacle?

In America, if you are a banker, you pass Go and collect 1 billion. The rest of us?

It doesn’t need to. It’s not subject to an IRS audit.

And it would be useless because every single asset is an electronic entry that is registered, and it is known who holds those securities or loans so that interest and dividend payments and pass-through principal payments can be sent to the holder. Two sets of books are totally useless.

The time of having a suitcase full of paper bond certificates and a suitcase full of cash is over.

Why do assume electronic equals can’t be fraudulated?

I didn’t say electronic “can’t be fraudulated?” But you cannot hide it for long. So it would be low-level stupid to try … only a true moron would try to do something like that. And the people at the Fed are not morons, that’s for sure.

The audits bear that out.

/sarc

C

I think there’s plenty of negative things to say about the FED. I am just curious, has that been one significant thing the FED has done in the past 50 to 100 yrs that most economists, historians and the majority of general public consider a good decision on behalf of making this country and the financial system better? Really out of curiosity here out of my own ignorance.

Read about Paul Volcker, the last public servant leading the Fed.

Then Greenspan’s BS wealth effect, unfortunately, took hold of the Fed, the idea of transferring wealth from the young to the old, from workers to asset owners.

The federal guarantee of bank deposits is definitely a good thing. The panics and bank runs before where ordinary workers could lose their life savings overnight were terrible.

But it is also fairly easy to argue that it made both banks and depositors more careless/reckless.

IMO, fed guarantee of bank deposits did not make depositors more reckless.

Depositors became more reckless in response to repeal of Glass-Steagall. If I understand correctly what that caused, is allowing huge investors to park assets never intended for Fed guarantee in a way that they somehow were guaranteed.

FDIC didn’t make depositors more reckless. Reducing the yield on bank accounts to less than 0.25% made ex-depositors reckless.

Fed is meant to work in tandem with fiscal policy. In the postwar period, the problem was that govt realised they could soak up any level of unemployment with fiscal stimulus. But this leads to inflation if not done in a responsible manner. Politicians proved to be quite irresponsible. Hence central banks were made independent during the great inflation, so they could pull a handbrake on the govt if spending got out of control. Politicians accepted this, because they could then blame all bad stuff on fed. This setup worked okay for about 20 years.

But due to many factors (demographics, inequality, austerity ideology, automation, globalisation), we do not have inflation pressures like before and govt refuse to generate it. Hence central banks are trying to fix a problem they were not designed to fix.

All they can do is ‘push on the string’ by feeding liquidity into the financial system in the hope that some of it will magic into new employment that will stave off deflationary collapse.

So it’s not really the fed’s fault that its policies are making things worse. It is trying to fix a problem that only fiscal, taxation and trade/industrial policy can solve – i.e. competent political leadership.

Hear, hear!!!

Don’t be an apologist for the Fed, which has chosen to go well beyond its mandate into experimental areas. There is a reason the Fed doesn’t have the tools to direct the economy for long periods. It is not supposed to have those tools, and it is not supposed to direct the economy and set prices. The Fed grabbed hold of new powers without specific approval of anyone. It lied about the economy and its intentions the whole way.

The Fed is the dentist who demands to perform heart surgery on you while your heart surgeon is on vacation. That dentist is not performing a service for you. He is putting you in harm’s way.

“So it’s not really the fed’s fault that its policies are making things worse”.

Here’s some comparable excuses:

-“Sorry officer, the gun just went off”.

-“It’s not my fault, I was on cocaine”

-“Sorry neighbor, you weren’t paying attention to your wife, so I had to fill in”

Central Banks are never in the best interest of the citizens of the country.

There was a reason our forefathers warned us against them.

So long as you have a Central Bank, the country will always be in debt and the people will always be wage / tax slaves.

Do you think it was just a coincidence that the Federal Reserve and the Income Tax came to be at the same time?

I call this manipulation of the free capital markets.

It would be much better if all stock prices will rise 5 fold or more by any manipulation thus the investors will feel rich and spend more.

If manipulating, then it shall be useful for millions.

This useless virus will be around for years; be realistic

So you really want Asian triads and tongs, the Mafia and South American drug lords to be involved in the “free capital markets”, do you? You don’t know what you really want. You have been brought up to mouth this ignorant nonsense, but you have absolutely no idea what a truly free capital market looks like. There is no such thing as a truly free capital market because it would create anarchy. It is merely every libertarians’ wet dream. Imagine going to your local pawn broker, taking out a loan, only to find that your local pawn broker is actually a Mafia front and your legs are going to be broken if you don’t pay up. That will be very convenient in the near future when pay day loans will become equivalent to cash, if they haven’t already. That’s your free money market.

I disagree with your basic understanding of libertarians. Most are not anarchists and merely believe in classical liberalism. i.e. free markets and limited government

Imagine going to your local pawn broker, taking out a loan, only to find that your local pawn broker is actually a Mafia front and your legs are going to be broken if you don’t pay up.

In this case, most libertarians would support the idea of going to a pawn broker as an alternative to a bank but would expect law enforcement to become involved if a crime was committed.

Free markets are not anarchy!

Actually libertarians do believe in anarchy, in theory.

It is just most people do not understand what anarchy is.

They erroneously equate anarchy with chaos.

Anarchy is simply life without government. The belief that government is not necessary.

People on the other side of the argument believe that without government chaos is a given. That is a fallacy. Probably perpetrated by government.

Libertarians believe in the non aggression theory, and that all government by its nature is based on violence.

I agree, libertarians believe in opportunistic anarchy. “Take everything you can and give nothing back!” Globalist corporations favor this ideology as well. Always lobbying (in House, Senate and in commercial media) for their rights, concessions and privileges yet they go silent when it comes to their own responsibilities.

Fed to bankers: “You can have your billions, but first you have to work a month in a Tyson chicken processing plant.”

At least there would be some public benefit to all this.

Or take a leisurely swim in a Smithfield hog waste lagoon.

If the Fed has this ammo at the ready but not yet deployed, there does not appear to be a need to print more QE, just release the existing inventory….no? If the markets have already priced in that “releasing,” it seems more likely the markets will stay flat as the releasing occurs….no ??

The Fed is going to have to start buying with both hands once the Treasury starts auctioning long bonds at a staggering pace to keep up with the exploding deficit if they don’t want an epic bear steepener.

https://www.cbo.gov/publication/56335

“The federal budget deficit is projected to be $3.7 trillion.”

Now that is debt out the wazoo, and it only gets us to October.

1) Apr 15 tax return was delayed until July 15.

2) 2019 was a good year.

3) Last year, by Apr 19 2019, total returns received was 132.233, 000.

4) The average refund was $3k.

5) This year, by Apr 17 2020, only 115,961,000 tax returns were received. 106,637,000 were processed and 81,349,000 got their refunds.

6) 50,000,000 filers will receive their $3K refund in the 3rd & 4th

quarters. They will have $150B cash in their pocket to spend.

I suspect the early filers were those taxpayers expecting a refund while those that owe will wait until the July 15th deadline. That being the case I would be surprised if the average refund of those yet to file is as high as $3K.

To Concerned American

Here is an illustrated difference between our two countries. My wife and I filed in Canada a few weeks ago. She received a $1719 refund and I owed $1131. The day my bill came in I paid it online, her refund was already direct deposited. I did not have to pay until Sept 15th because of Covid, but I paid right away, anyway.

Reasoning for supposed early payment? We’re doing okay and our Country does not need an addition to the deficit during Covid mitigation. Now, many of you may laugh at this apparent naivete, but I look at it this way. If we get sick we are treated for free in a world class hospital. If my children lose their jobs, they will have a lifeline Govt program to keep food on the table and a roof over their heads. (Plus, we would also help if they were doing their best and still struggled.) Yes, it often appears that Govt policy in every country is inefficient as they try to be everything to all people who have many competing viewpoints, but I submit they are not always our enemy.

When did the US Govt and policy become the ‘enemy of the people’, and why? Did it start with founding based on revolution? Is it because of the gun rights in the constitution? Abortion rights vrs religious fundamentalism? The draft was discontinued. Why is the Govt now always bad? Or, are people just whipped up by negative media that bombards us day after day? Is this a symptom of a Country in decline? Or, is it healthy criticism? (It doesn’t sound healthy to me).

In Canadian elementary schools students are imbued with a constant mantra for certain behaviour outcomes to make the classroom and school function. It is developed every year, in every class by the students, and is posted at the front of the room as a big poster to be referred to as the year unfolds with inevitable hiccups and clashes. It is called (wait for it) “Rights and Responsibilities.” I have never seen a classroom without it, posted high, front and center. My wife was an elementary teacher, and last night when we were watching the news about protestors demanding a re-opening she looked over at me and asked, “Why is it always about rights down there? How come they never talk about responsibilities? It’s always me, me, me and what I want”? (Good questions).

Taxation now sounds like extortion. A Stay at Home order is tyranny and worthy of protest. Many states and cities will go bankrupt and all I read about are those damn Govt and private pensions, when the pension contributions were negotiated in free and PUBLIC collective bargaining but without the the teeth requiring yearly funding. It was part of the wage package for employees, but the money was spent, every year, to top up budgets for roads, schools, libraries, fire departments, policing, court services, etc., often in states without even a sales tax, but for ‘stuff’ people expect and demand.

Is everything a scam and ripoff? Everything? Really? Look at the news today. From university to Kindergarten everything is a rip off. Every tax paid and every pension someone receives is now a travesty, something ‘I don’t have and they shouldn’t have, either’. Hospital charges, co-pays, permits for whatever, taxes, tolls, are always portrayed as, “You Jane, take from me. Tarzan”.

Crazytown. My American sister said last night on the phone, “I just hope when this is over we end up with a decent medical system”.

She should have added banking to the list, but maybe a bigger concern in 2020 is staying alive or not going to hospital.

regards

Wake up and smell the Operation Coffee Cup – it’s morning in America all over again just like it never used to be.

Paulo:

Always enjoy your posts….

It’s called, “American Pie”!

It’s an illusion.

It’s steeped in propagandized narcissism: “American Exceptionalism”.

The “Pie” is rotten to the core……unfortunately.

Bankrupt government

Corrupt financial system

Destroyed public education

Out of control, “Military Industrial Complex” along with the “secrets involved in our foreign policies and “black” covert/intelligence (now there’s a word!) operations”

That’s just a small part of the list that is hanging around our country’s throat.

All the while bleating “Democracy and Freedom”

White man in the US speaks with forked tongue, still.

Don’t worry they will deploy!!! You know corporate America needs them to buy junk bonds! Watch the market will tank and here comes the the Fed!!!!

The Fed is independent. In the absence of penalty for lying, the Fed

can promise to be nice to the market and give their cheap talks.

7) $150B withheld from filers until the 3rd & 4Th quarters.

$150B will make a small dent in that $5T loss in the GDP this year.

\\\

They won, they have all the fields. There is nothing left on the board. Everybody else is just hoping not to land “on their property”. They even have all the “Get out of Jail free” cards. You name it, they have it.

\\\

I have a cunning plan! We make them a plack saying, “Congratulations you won!” and then we explain to them how it was all a big game, and that we have to start again from the beginning. You think they would give back the money and assets?

\\\

“At the end of the game, the king and the pawn go back in the same box.”

Wolf,

Does not sound good. No other option for myself but the long term. My sister is on day four of the corona virus, tested positive day three. Given one z pack and vitamins, with oxygen. Headache today with a little trouble breathing. Vitals are good.

Good luck! And watch out for the second week. That is when our friend really got smashed.

I’m just wondering…Mrs. Watanabe is buying expensive Hermes handbags by big enough numbers to keep Hermes’ Japan numbers in the black in Q1. Housewives buying $10K handbags are not watching every penny.

There are women in Asia who collect expensive handbags. The bigger the better. I have been to some Asian homes that have wall-to-wall shelves displaying very expensive French bags. It’s a status symbol over there.

I have a friend who visited Asia to pick up his “sister” in Asia on the way to Paris. He showed me pictures. Each day his sister had a different colored bag (huge ones making her look like a small person).

You can go to an Asian mall and the stores have handbags priced from $15-25k each. They are cheaper in Rue St, Honore.

I don’t have such ambitions. Just watching.

My comment was really about how Hermes made a profit in Japan in Q1 while losing money in the rest of Asia. Except for the new Japanese swap lines, not much seems to be different there.

The Case-Shiller Index shows housing prices are continuing to rise.

I suppose the Fed buying mortgages made real estate prices rise more. The cost of a home is not included in the Consumer Price Index.

While on vacation I discovered an American expat community in Costa Rica where home prices are low. A friend found Americans retired in Thailand. I have seen recent rental ads in America with apartment rents close to $600/mo.

David Hall,

The CS index is a three-month moving average that lags one month. The CS figures we got the other day were the average of Dec, Jan, and Feb. They’re totally irrelevant for the current crisis. The CS won’t show any impact until it covers Feb, March and April, which will come out on Jun 30. I won’t cover it until then because it is irrelevant. But I will cover it starting with the Jun 30 release.

The Fed is trying to control sudden unpredictable changes in the velocity of money caused by the lockdown. IMO, the money velocity had been going down since 2008-2009 and causing disinflation. The Fed seems to be instituting the same yield curve control they did in WWII. This would allow the the growing government debt to be financed at almost a zero. The bond vigilantes forced bond purchases. Now the stock and corporate bond vigilantes also want their money spigot opened. If bonds and stocks both tank, the Fed with the SPVs is already set up to submit. Japan has evolved and it might be America’s turn.

When you spend more than earned in the good times, and suddenly……

This is what happens.

I don’t see how this will ever be fixed through manipulation? Hopefully, the next reserve currency country will have a few history books to refer to, or there will be a basket of currencies with group oversight not manipulated for limited benefit.

This could change, everything. Think about it, this has only been 6 weeks in NA. Resurgence? Not good.

How is the economy supposed to grow if your saving enough??? Paradox 101. Then you can’t. The only time when America saved was during the post-war bubble

Fwiw, SPV’s are controlled by the dealers. If they aren’t buying, it won’t show up on the balance sheet.

There will be savers and spenders in any economy. Let those (individuals and companies) who want to borrow pay for it. If they go bankrupt let them. We do not want the Fed to meddle. Period.

The helicopter money will have to return very soon because donald is screaming at jerry to open the spigots full blast because we cannot have the stock market with all of its multi-national corporations going down in price. Isn’t it unconstitutional?? These corporations will need even more money to import their products into this country if the new tariffs on china are imposed. It will be just like a couple of years ago when so many things doubled in price to accommodate the price increase due to these previous tariffs…….No need to try and manufacture things in this country…..not even medicine, masks, nor ventilators.

We already manufacture a bunch of that stuff. This post……..pay attention.

GM was ready to import the masks and ventilators from China. They had no intention of manufacturing them in this country, even though they were bailed out by the fed in 2009 and are getting money from them now. And even though the government devalued the dollar in 1987, GM did not increase production in this country even then. There is no loyalty here to we, the people nor to Trump. Trump had to invoke the Defense Production Act to force GM to manufacture in the US .

https://nypost.com/2020/04/08/gm-to-make-30000-ventilators-to-help-us-fight-coronavirus-pandemic/

Require corporations to buy treasuries similar to the pension funds (buybacks limited), and make them move their supply chains back to America. Future solved till the next crisis.

Bond prices are down pretty much across the board today, as can be seen by looking at various bond ETF prices. Why? Is it the China kerfuffle and a fear that China will unload US corporate bonds in retaliation?

I ask because iany window to get a good deal on corporate binds is very narrow. Look at BND around 12-19 March 2020 for an example

Concrete numerical example: I was looking at VCLT ETF today at price 100.80 roughly, after dropping 1.34 today, of which only about 0.31 could be attributed to dividend being paid out as of yesterday.

SPV’s? Who needs them? Apparently, not the Fed because if the below is correct, the Fed is very likely already buying stocks and junk bonds.

Indirectly.

“In our comment to the Federal Reserve last week we pointed out how the Fed is handing out money almost no effective conditions. Public credit can be tapped for all kinds of deal funding, by private equity, and without retaining employees.

Now the Fed has outlined new credit rules for $600 billion in “Main Street Lending” that will make things even worse.

First, they added a new avenue for heavily indebted companies to access public credit. Many of these companies will be private equity owned. These companies can borrow up to six times their adjusted 2019 earnings — we know these “EBITDA” metrics are often manipulated.

Then, they watered down the already minimal requirements for borrowers to promise to retain workers when they get loans, and removed any requirement for companies to attest they need the money because of the pandemic crisis.”

There is no indirect buying. They cannot buy junk, they only can set up vehicles that banks who will buy junk but that won’t work. This board never changes. It simply doesn’t get it or the limitations of the fomc operational manual.

Wolf, I read somewhere that the Fed is pretty much restricted by its charter as far as what it can and cannot purchase, and that before it could buy something like junk bonds it would have to have Congress amend its charter. Is this true?

Jdog,

That’s why the Fed is using SPVs. The Fed lends to the SPV, which appears to be within what the Federal Reserve Act allows the Fed to do (emergency loans), and then the SPV uses to funds for whatever purposes.

To set up the SPVs, the Fed needs the Treasury’s permission and an equity contribution. That’s how it is being done.

So if the Fed wants to buy old bicycles, it can ask the Treasury for permission to set up an SPV for that purpose. If the Treasury says OK, and here is $1 billion in equity contribution from the taxpayer, the Fed can lend $10 billion or whatever to the SPV and buy up all the old bicycles in the US no matter what the Federal Reserve Act says.

Congress could stop this, but doesn’t. They all have stock portfolios, and they want to get as rich as possible while in office, so the more Fed shenanigans, the better.

And congress wholeheartedly welcomes the ‘cover’ that the Fed provides thus saving the elected ones from risking voter blowback to any actions congress would otherwise have to take in the absence of Fed largesse.

So basically we have a cabal whose only aim is to get rich while they can, aided by buddies with one hand on the printing press and the other on interest rate. Crank one up and crank the other down, moral hazard be damned. That is what I call good leadership.

I really do not see how this can continue, the amount of money needed to prop up everything just seems to be too much even for the Fed to backstop.

Between the States, Counties, Cities, corporations, taxpayers, pension systems, and stock and bond markets, the amount of funding needed to bail out everything seems astronomical. Then when you consider these are all loans that need to be repaid, how do they believe they are going to pull it off ? Perhaps this is the end game where they bail in all citizen assets to pay off the debts…. In which case we are all screwed.

The selling of one out of 10 houses in your neighborhood foreshadows the price of other nine. The Fed doesn’t have to control all the prices just an effective amount to control the sentiment.

The Fed’s next target will be the states and their pension system. Sales taxes are the sweet juice of leverage to keep the pension racket going. Sales tax ain’t doing very well right now and property taxes might be in jeopardy if this Fiat Ponzi Scheme delivers deflation (fiat kryptonite) instead of inflation . I can’t wait for the snot slingin’ fit when Mitch bails out state and local pensions by taxing those that do not have

a pension. If Congress can’t get enough taxes ,no problemo, their Henchmen and Henchwomem at the Fed will shake the rest out by De-basement. I’m filling up the Ol’ Heck Mug , putting my feet up and I am going to tune in to what follows. It will be great.

You know, I have no idea why the Fed has to keep on Q.E.ing at all albeit much smaller daily amounts in the billions. Banks are awash in cash already (earning excess reserves). So this might be done as taking the sick dogs behind the shed moments.

Iamafan:

There’s a significant difference between a liquidity crisis and a solvency crisis we are at the beginning of the latter.

Wolf,

Your first chart in this piece is on Chris Vermeulen’s piece on investing.com today.

Thanks.

If the FED is owned by private banks and it is “buying” treasuries, at what point does it make sense to default on treasuries leaving those banks hanging?