In addition to logistical difficulties of selling a home in the era of social distancing, there is the explosion of a historic unemployment crisis.

By Wolf Richter for WOLF STREET.

By the end of April, there will be 4.2 million mortgages in forbearance, or 7.6% of all mortgages, the American Enterprise Institute estimated in a note, based on forbearance data through April 19 released by the Mortgage Bankers Association yesterday.

These homeowners whose mortgages are in forbearance will not make any mortgage payments for some months, as spelled out in the forbearance agreement they have entered into with their mortgage lenders or servicers. The missed mortgage payments will be added to the remainder of the mortgage, so it’s not free.

But the cash – interest and principal payments – of those mortgages has stopped flowing up the chain. Mass forbearance of this type has thrown the entire mortgage market into chaos – and what keeps it from imploding is the US government, which is purchasing or guaranteeing most mortgages written, and the Fed which is buying mortgage-backed securities issued by these government entities.

The government is on the hook for this forbearance: As of April 27, 5.9% of the mortgages on the books of Government Sponsored Enterprises Fannie Mae and Freddie Mac were in forbearance, according to the AEI, and 10.5% of the mortgages on the books of government agency Ginnie Mae were in forbearance.

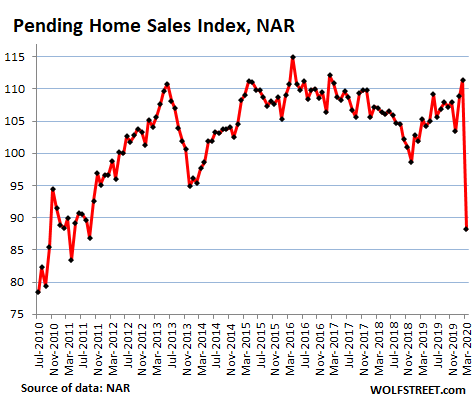

March deals plunge.

Pending home sales – signed contracts that haven’t closed yet – are an indication of closed sales a month or two down the road. These contract signings on existing homes in March plunged by 20.8% from February, and were down 16.3% from March last year, according to the National Association of Realtors today.

But this decline is an average of the first half of March which was likely in the normal range, and the second half of March, when the lockdowns were implemented, and when sales volume plunged more steeply. Nevertheless, it took the index back to the 2010-2011 housing-crisis range. And many of these contracts might not close; failure rates can be high even in good times, and are likely higher now.

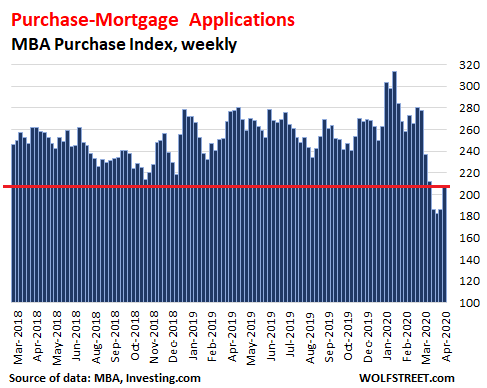

April deals plunge.

The number of mortgage applications to purchase a home in the US during the week ended April 24 ticked up from the dismal levels of the prior three weeks, but were down 20% from a year ago, and were down 34% from the peak at the end of January, the Mortgage Bankers Association reported today. It was the sixth week in a row of year-over-year plunges. For the first four weeks of April, the index has plunged 31% compared to the same period last year.

The purchase mortgage applications data – based on weekly surveys of banks, nonbanks, and thrifts that cover three-quarters of all residential mortgage applications – is an early indication of demand by regular people who need or want a mortgage to buy a home.

But this does not include demand by buyers who don’t need a mortgage from a lender in the US, including some formerly prolific buyers that have now pulled backed and their disappearance is not reflected in the mortgage data:

- Nonresident foreign investors who bring cash or finance their purchase overseas; they have largely been locked out due to travel restrictions.

- Large US buy-to-rent investors that fund purchases at the institutional level; they’re now struggling with turmoil in the lending markets and uncertain demand for rental housing.

- “iBuyers” that buy homes and flip them at steep losses. They include Zillow [Z], Redfin [RDFN], Opendoor, iBuyer, and Offerpad. They have all shut down their home purchases, and demand from them has collapsed to zero. And they’re now trying to sell the homes they got stuck with.

But the drop in demand from these buyers is not reflected in the mortgage application data. This drop in demand will show up later in the home sales data.

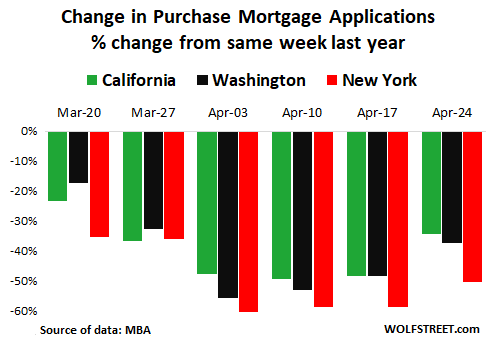

New York, Washington, California.

In the states that kicked off the virus-control measures first, mortgage applications dropped earlier and more than the national average, according to the MBA.

Of the three states – California, New York, and Washington – purchase mortgage applications plunged the most in New York, with year-over-year declines that reached 60% in the week ending April 3. Since then, the year-over-year declines have backed off a tad, but remain huge: -50% in New York, -37% in Washington, and -34% in California:

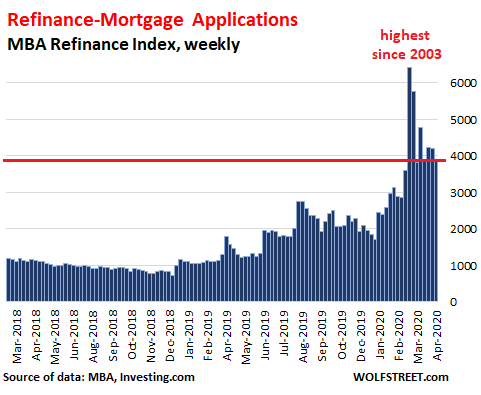

Refis not quite as hot, but still hot.

Low mortgage rates have motivated homeowners with existing mortgages to refinance their mortgages in past weeks, but the enthusiasm of early and mid-March has waned a bit.

Applications for refi mortgages in the week ended April 24 ticked down from the prior two weeks and were down 39% from early March, but were still triple the volume of the same week last year. Refis accounted for 72% of all mortgage applications.

Real estate brokers and their potential customers are now trying to use online tools to the extent possible in the sales process, with virtual open houses, e-signings, and the like. And some deals are being made.

But for many people, this just isn’t a great time to buy a home: Initial unemployment claims have already reached 26.5 million over the past five weeks and will reach 30 million over the next couple of weeks; and many people who’ve lost their income are not eligible to file for unemployment and are not in the unemployment claims data.

Other people are looking at their jobs that they still have and that used to be promising and are confronted with layoff news that keep rippling across the screen, such as those now at Uber and Lyft. People whose jobs have vanished – even if it’s presumed to be temporary, and even if the income will be replaced by unemployment insurance – and people who are in the process of losing their jobs, just aren’t going to buy a home, and even if they wanted to, they wouldn’t qualify for a mortgage.

In addition to the logistical difficulties of selling a home and closing a deal in the era of social distancing, there is the issue of economic uncertainty and the explosion on the scene of a historic unemployment crisis. And that explains the volume declines we’re now seeing in the various preliminary measures of the housing market in the range of -20% to -50%.

Unsecured bonds of Macy’s, the largest still existing department store in the US, crashed 53% since Feb 14. But Macy’s has been living off its real estate portfolio of “owned boxes” for years by selling them. Read... Can Macy’s Survive this Crisis Without Filing for Bankruptcy?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

YEA ! – First to comment! WOW – I can’t believe it!

Yup – ours in fb as of today!

As the poet wrote, “April is the cruelest month”

I don’t think I’ll ever trust a virtual open house as a prospective buyer.

Me neither. One thing I make close note of when inspecting a house for rent or purchase is smell (is something decomposing in here)? Cain’t do that virtually yet.

How many buyers will you trust traipsing through your property in a day, week, month? What will you do before and after the showings?

“is something decomposing in here”

Yeah, the rate of return on your savings…for the last twenty years.

You want to buy a house based on ‘virtual reality,’ you go right ahead.

I sold a house in the SF Bay Area I’d lived-in for 22 years in 2018, at what appears to be the peak of the market (I’m not bragging, I just got lucky). Bought at $245K, sold at $1.305M.

Really good that you provide a full context to the “bullish” news you see on MSM outlet like Yahoo or CNBC trying to convince people the market will rebounce nicely soon from tick up in mortgage application. I had to re-read MSM article on the application up and still didn’t spot a crucial little detail left behind as in your article. Good stuff

“The number of mortgage applications to purchase a home in the US during the week ended April 24 ticked up from the dismal levels of the prior three weeks, but were down 20% from a year ago, and were down 34% from the peak at the end of January, the Mortgage Bankers Association reported today”

Instead of Yahoo I see this…

“Digital mortgage lender Better.com also reported a 36% increase year-over-year in April purchase applications. The top state was California, which made up 14% of the month’s total purchasing volume.

“With $8 billion in applications since April 1, Better.com continues to see increases in applications across the board,” said Sarah Pierce, head of sales for the online mortgage lender. “While the majority of application volume is refinance, towards the end of the April, we did see an uptick in purchase applications, making up around 12% of our volume in April.”

Among lenders surveyed nationwide, the MBA reported a 17.2% spike in California mortgage applications, compared with a 2.9% increase the week before. Washington and New York witnessed increases in purchase applications of 16.1% and 13.7%, respectively.”

Sounds about right. I quit trying to predict. I assumed our work to drop off a cliff. It still may do that. Until then we keep going.

Past 1.5 weeks we have certainly had an uptick for new home construction, and real estate sales. I deal with sh*tters, so the demand has also increased with replacement systems. Lock downed serfs are wuhaning

their systems.

Who would have thought bidets would be big business?

Mortgage, shmortgage – as with the not-since-Great-Depression unemployment and GDP plunge, stawk markets only care about the bullish headlines at this point: “hope for Covid-19 vaccine!”, “hope for early lift of lockdowns!!”, “Tesla reports positive fake earnings!!!” Wolf, man, stop harshing on our endless-rally party with this glum real-economy news. :)

Tesla…haha. It’s been great seeing insanity in a form of a company stock. Aftermarket right now at $878 a share. I know when I am starving and have to choose between feeding my family or buying a hipster approved cool electric car, it will be a easy choice. Sorry family is gonna have to starve so I won’t miss out as being part of the future and make sure EM hit his pay package real soon.

Pssh…Tulip bubble? You got nothing on Tesla I am afraid..

Walking about SF I do see street parked hi-end Teslas, p95 and such. The door lines do not match the body, sunked in. Plastics are dim for 3-year old car. I suppose it accelarates very fast, so there is that.

I did follow one p95 tesla cutting across lanes, he could not shake me for miles and miles, but he did try. That was fast and fun. I lost my car since then, unrelated.

There are P85’s, P90’s and P100’s. Never heard of a P95 Tesla. You were probably chasing a motorcycle of some kind.

1). Go to Zillow or Trulia or your choice and check out the historical distressed mortgages in your neighborhood. I know mine isn’t like this, was much lower pre Covid:

“By the end of April, there will be 4.2 million mortgages in forbearance, or 7.6% of all mortgages, the American Enterprise Institute estimated in a note, based on forbearance data through April 19 released by the Mortgage Bankers Association yesterday.”

2). Now do a quick calculation in your head how many of your neighbors aren’t paying their property taxes in your town because forbearance.

3). Now ask yourself why you didn’t support Federal bailouts for local and state governments.

Unless you plan on hiring your own security service, trash collection, street light, etc.

Wall Street, investors, buy back corporations, the rich all got their bailouts and free money.

The rest of us might well be sh*t outa luck.

I pay for my own security (it’s sitting here on my desk), pay for my trash pickup, pay for my street lights, etc. Other than occasional road repair, I’m not sure what my local or state governments provide.

My condolences. My local government in Boise, Idaho provides a lot of public services including excellent parks, trails by the river, trash pickup, firefighters, ambulances, public school programs (though I don’t have kids). I pay for these, but I appreciate them.

Yeah, Boise parks are pretty good, but the greenbelt trail and the foothills in general aren’t what they were even ten years ago. Half of the year, the river is either flooding the trails or the river is 2/3 dry, making for a really uninspired view. A lot of the vegetation along the river now consists of non-native invasive crap like cheat grass, escaped apple trees, black locust trees and even poisonous cow parsley, but few people understand or care. The sagebrush, bitterbrush and other native plants are almost gone from large parts of the foothills thanks to drought, fires and understandably hungry deer. What’s left is garbage like alfalfa, wild mustard and cheat grass smothering everything. It’s sad and gross. The city is becoming increasingly hostile to dogs, and the hiking trails have been overrun by aggressive mountain bikers who treat the foothills like their private playground. The new “bike skills park” (located in an upscale part of town supposedly to serve lower income kids) is an example of the increasing number of economic boondoggles that the taxpayers are now on the hook to maintain until forever. Sorta like that hideous and poorly used JUMP “community center” downtown. Overall, the downtown has become overcrowded and ugly, and the views of the foothills have been all but obliterated from most areas of the city, creating a sense of disconnect from place. Instead, we have really crummy tall hotels, condo complexes and faceless small skyscrapers to look at. Whoopee. Air service sucks and every inch of open space is being smothered with crap shack housing including acres and acres of cheaply built apartments that will become tomorrow’s slums. Anybody who thinks the schools (especially Boise State, or B.S.) are worth crap, is totally delusional. Oh, and let’s not forget the waves of lovely immigrants who are overriding and runnnig down certain parts of town, now. Some days there are areas that look more like Little Mogadishu than a formerly nice American western city. And our housing prices and property taxes? Up and up and up they’re going. The “privileged” have gotta get their asses out of bed every morning and get to work to pay for the food, housing and health care for the growing ranks of ‘underserved’, you know. And don’t get me started on our burgeoning homeless problem… Boise is turning into every other bad city in America. Just give us a little more time, and we’ll get there.

Sparrowhawk is right. Im even worse off living in Nampa. If these housing prices dont crash im moving out of the state.

Do you pay for your kids education? Water? Roads? Do you think your situation is the norn? And why do you think road repair is occassional? Are suggesting Texas is really that backwards?

Ranches pay little in the way of property taxes and with no state income tax he probably pays almost nothing.

He is probably posting via tax payer subsidized internet connection :)

Payed for their private education, paid for my well, payed for my septic system.

Have no issues paying my property taxes. Be it for private service or public. Commercial and diesel taxes for my equipment .

I get ya TX. But our era is over.

It is now trust in govt era.

Like you, I have plenty of security on my property.

can u send a link that shows / explains how SS or Medicare or Medicare or whatever it is you said the other day, have never been a net drain on the balance of accounts for the US govt.

Btw security isn’t police….but since you apparently don’t have education down there, maybe you didn’t know that…

Any service provided by the city could be provided by private companies at a fraction of the cost with exponentially better service and quality.

But then who would pay the political kickbacks?

I think he’s talking about a firearm

Yes, it is only the big cities that are looking for a hand out from the rest of the country…. Sorry we don’t owe you anything….

Same here I’m from Chicago it’s not brake here , no help , no bailouts, no forbearance if we don’t pay the property taxes we loose the property quickly, Instead our Mayor is taking more care of refugees than the workers tax payers .

Shameless government

Question about forebearance in relation to property taxes –

If a monthly mortgage payment includes a a portion for the property taxes, then is the entire payment part of the forbearance? Is the bank paying the property taxes directly out of their own pocket during this time? If so, this is going to get more interesting than I thought, especially for high property tax financial basket cases like Illinois.

The servicer of the loan will advance the taxes and insurance, if any.

Yes, they are the ones with the biggest interest in the property. They will make sure it is not subject to liens for taxes.

It will be interesting to see stats on non performing loans going forward.

Simple jump-off point. No more cash-for-corporation program. Make it money-for-monorails. Guv. plays swap game on aging inner properties for outlying existing homes. No more new housing starts, only structures which encompass the new transport system. Then dump most of those lousy busses, streamline the roads, and start working on problems with the environment/population/etc., etc, etc. Build for the future when we’re all gone. Might help if we stop wasting resources on pointless pursuits. Loans do not automatically equate to Liberty. And I’m not even a liberal.

Stop making sense! :)

Maybe you are a liberal ‘cos I agree with you 100%. ;-)

Them’s fightin’ words..man yur spud launchers and prepare to be boarded. I’m just realistic about where this is headed over time…better to make a fair deal trade on what started as public lands to be sold to farmers than have a hooligan smash ‘n grab. I’d rather not end up living with a commie microphone stuffed up my butt. Sorry true conservatives…I’m willing to show our Indian friends I’ll fight to the death over Republic versus feudal tribal commune, but I don’t think I can load shells fast enough to hold onto a piece of dry dirt hillside that will just end up as a cemetary monument for dead horse soldiers with curio hawkers outside the gate turning a buck on sellin’ Chinese pot metal crap to gullible tourists. Guess it’s nearin’ time to kick the money changers out of the temple of freedom.

China has a strategic plan. It depends to 2 pillars.

1. Cheap, high-volume Chinese steel. No pollution controls, dubious quality.

2. U.S. dollars from exports to the U.S.A.

And China’s communist government has out-maneuvered all Western governments, including the USA.

Since all Western economies now depend entirely on subsidized money (low interest rates, no risk premium since Governments backstop stupid corporate/banking decisions) via ballooning debt, so we can pretend we have a real, functioning economy, then housing will never truly be priced by supply and demand. It will continue to be dependent mainly on Government.

Be wonderful if it could be that romantic. The lucky ones will be the small farmers with arsenals. Tragic faced drifters will seek an egg and barn bed security if they can be offered a job or two. The stories on whatever media may be left will stretch ironic limits. Folks just had no idea things could get this bad.

Cities/Suburbia are the body/temples of capitalism, oil its blood and finance its brain. Killing its head is the easiest, but disturbing the others is way more fun. Something a radical told me in 1970.

Been scanning the horizon for capitalism. No sign. Just some old clothes in the attic.

The second order effects are what the stockmarket is missing right now. This is a second order effect, and it will lead to third and fourth order effects by June.

Every action has an equal and opposite reaction. People do not seem to understand the laws of physics and mathematics are linked and the laws apply to finance as well as physical sciences. We have ignored physics and mathematics for decades, and now they will assert themselves, without mercy.

the only solution i can think of to this problem is to buy some more microsoft and facebook stock.

You aren’t alone…what do you think is (barely) holding the mkt up?

Microsoft at a 30 PE (not truly insane, except when you realize how big MS already is in terms of revenue and penetration)

And Google at a 27 PE (see MS)

And Apple at a 23 PE (see Google)

And Amazon at a 100 PE (truly insane).

Those 4 stocks account for over 40% of the entire value of the Nasdaq *100* – so their fate is the fate of the mkt.

That is not the definition of diversification.

They own the most important aspects of their industries.

PE is a function of interests rates generally. Just like any asset it’s all about comparing the return vs risk free rate. 30 is a bargain if 10yT stays below 1% forever-ish.

The main risk would be double digit inflation. If that happens then PEs come down to account for that erosion of purchase power. Since money velocity is slow and price of goods and services suppressed that will be a long way off 4-5years. By then the 30PE company may have doubled revenue and profits and thus it will be a 15PE by the time inflation hits.

It’s not always about looking at historicals

Like drowning rats frantic for dry land. And yet, a hard rains agonna fall.

Yes, it is always a good idea to drive looking out the rear window….

Get back to us in a year and let us know how that worked for you

Don’t worry. The 2K check per person will help I am sure. I mean it will not get people to go out and see houses, but it will help somehow ;)

I now have a job although my pay has been cut, but I feel somewhat punished.

Yancey…interesting idea(s)… Could you flesh out your 2nd , 3rd & 4th “ORDER EFFECTS,” for those of us who aren’t quite sure what you’re referring to, please.

People get forebearance, people stop paying rent (2nd order effects from the lockdowns). Landlords and mortgage originators stop investing altogether putting builders, maintenance organizations out of business (3rd order effects). All these newly unemployed feed into the decline of consumer spending, which then becomes the 4th order effect.

My point is that the decline feeds on itself, and quickly at this point. Who really thinks 4 months of missed mortgage payments are suddenly going to be paid any time in the future? Who is going to make the political decisions to lift the mandated forbearances?

It’s like a… derivative…in reverse.

“Who really thinks 4 months of missed mortgage payments are suddenly going to be paid ”

They aren’t gonna paid “suddenly”. The missed payments are added to the end of the loan, to be paid as before.

Actually, many of these forbearance’s are being written with a balloon payment due at the end of the forbearance or shortly thereafter. What could go wrong?

There is now guidance from the GSE and Ginnie to allow balloon payments but don’t require them, and offer mortgage modifications that add those missed payments into the mortgage either spread out over the remaining term or at the end.

Hate to say this but there wont be a $2000 check.

RE is going into Hibernation.

At least some more worthless Agents will disappear from the business.

That will be nice

In Utah, demographics not the covid-19 virus run the show.

In Utah county specifically, home building continues unabated.

I guess I am now a Harry Dent guy as Economies seem to start and end with demographics.

Classical, Keynesian, Austrian, Supply Side, Communistic, Socialistic Economic models never start with demographics and so they never end with demographics.

Correct economic theory can aid demographic realities but not define them.

China, uses a little of each but their goal is capitalism.

The USA seems hell bent on following Rome down the path of Imperialistic destruction.

“Economies seem to start and end with demographics.”

But economics feed back into demographics…witness the collapse in birth rates following 2009.

Most people hold back on having children in bad or deteriorating economic circumstances.

Supply sees things differently and correctly…

D.R. Horton, Toll Brothers etc they are all here in Utah and building like crazy, building as if the coronavirus never existed.

Demographic demand for Homes in Utah will continue, the coronavirus will not.

At the national level, SFH/apt supply has been insufficient – that is how housing prices have been able to soar despite near stagnant incomes for over two decades.

Utah may be a different story – but it is not the national story.

You can Google “new home construction (or completions) by year” to see the annual stats for yourself.

Price is just the intersection of supply and demand…if we had more supply, housing prices would not have soared over the last 4 or 5 yrs (relative to income at least).

Same with birth rate by year – easily Google-able and Utah’s story is not America’s story.

All of the developments you describe began before anyone even heard of Covid-19. Yes, Toll, DH Horton, Shea, etc., are building like there’s no tomorrow here in Scottsdale, AZ too. However, they are not selling and the “free upgrade” discounts have begun. Resales have screeched to a halt. Our friends with a Huntington Beach, CA manse listed at $2.2M had their third “backup” sale blow up. Could not obtain financing.

Scottsdale seems hell-bent on paving over the entire desert. Homes in another new development popped up over the past week (was previously only infrastructure). Another slow selling development went into hyper drive to get built out (60% of the homes took 2 years to build…. the remaining 40% two months trying to close out the development). Another large boondoggle of California cookie cutter snout houses is being slapped up down the road by Shea and Toll Brothers. Of course, Snotsdale hasn’t upgraded the roads… nope.

There was a local news segment last evening covering PHX AirBnB hosts that are being forced to sell as the full time rental income won’t cover their nut. The realtor that runs “Sellyourhomein24hours” was also on there acknowledging the flood of sellers.

We bought out in the weeds (horse country) for the views, the fresh air, and quiet. Many of those who have moved into this development have been spending obscene amounts of money to take a simple vacation home and turn them into luxury resort homes. I think they’re in for a rude awakening. One home nearby ours is languishing on the market at $3.1M….. of course, they paid $5M for it…. and they have no takers. There’s example after example of people who got their teeth kicked in on the last market inversion and sold at rather painful losses (it didn’t recover out here until 2016) but no one pays attention to history.

Interesting times.

You’re assuming most people have IQs above room temperature That’s not a great assumption

Well, I know that a certain political party holds that view – its political power is founded upon it.

But actual statistical reality says that people respond to the economic environment by having fewer children when times are bad.

Interesting fact: the Antonine Plague allowed the Roman Empire to avoid the first existential threat of its history. While it hit Rome hard, it hit the Germanic people pressing against Rome’s northern limes much harder.

Marcus Aurelius had been campaigning against Danubian tribes like the Quadi and Marcomanni for years with not much success. He could drive them away from the borders but they always came back, and each new attack led to more and more desperate fighting. Military expenses were spiralling out of control and the need to transfer troops from the Near East to the Danubian limes helped the Antonine Plague (probably smallpox or measles) to spread throughout the Empire.

But ironically enough the plague hit the Danubian tribes much harder than the Roman Empire: the plague mined the power of the Marcomanni, the most bellicose of Rome’s enemy. Their subjects and allies saw their opportunity and infighting started.

After Rome signed a peace treaty with the Danubian tribes in 180 the Marcomanni progressively sank into irrelevance and became subjects or allies of other confederations such as the Alans and the Huns.

Sic transit gloria mundi.

All those second, third, and extra wives all get food stamps and aid to dependent children. So yes, it is demographics with revenue sharing added to it.

The only thing holding up demographics now is immigration which is making up for low birth rates. If the coming depression ushers in a new nationalistic fervor, then immigration will dry up and so will the need for new housing.

We also have the issue of a glut of commercial property that will be vacant and in need of re-purposing. I remember in the 60’s and 70’s there was a glut of commercial property in CA and hippies used to rent whole floors of abandoned office buildings for really low rent.

Whew! Things are not nearly as bad as I was expecting!

What was that old song by the Carpenters….”we’ve only just begun”…the best we can hope for is stagflation “a la Japan” once the effects of this initial shock settle into the system. Currently, the system is confused because of the massive injections of liquidity, which at the end of the day, are still debt. My parents and my wife’s parents lived through the depression as young children followed by WW2 in Europe and were also bombed, and suffered food shortages. This left an indelible mark on them, they lived a simple life and they never spent money they did not have. The were truly content. My wife and I “inherited that same indelible mark” and it has served us well and we are grateful. Unless most folks…namely the ones who helped exacerbate the situation by talking out too much debt, are slam dunked in the most brutal way by the depression that seems to be headed our way, nothing will be learned and bad behavior will continue. The best thing that could happen to society is to be blessed with that “indelible mark” so we then have the chance of returning to some semblance of sanity. It will be a painful road, but the other end will be liberating. Most folks simply don’t realize how liberating it is to be blessed with that “indelible mark”. Gird your loins. Anecdotally, I report with great sadness that I’m already seeing people panhandling in areas where I had not yet witnessed the phenomenon…so sad as I believe many fine and innocent people will also get hurt by this.

April 30 employment loss will reflect downstream jobs which are are much higher value jobs and benefits than the preceding week.The following week will be greater than the week before. Last on the list will always be government bureaucrats ,college professors ,politicians and other rènt seekers . Employment numbers do not treat the loss of a $100k a year job different from a $10k a year job.they are both counted as a equal loss. The first large wave of the un-employed were mostly renters and proportional less mortgage holders as will be the reality of the losses of April 30. We are now getting into the “quick” of the economy. The basic resistance of reversing an equillibrium once reached such as when job job losses equals job gains will be a forceful resistance to reversal which will have a much higher threshold value than going from more orderly (more jobs) to lower orderly (less jobs) This is the entropy conundrum of the physical and natural world and human economics. Entropy is a bitch. The stock market is a case study of the irrational behavior of humans and yields the same results. Job loss mitigates this behavior variable as most people do not want to lose their job until they have another one . This irrational behavior is a mechanic that can be ignored in this cycle of job loss . The nut-cutting of it is that the longer we go before equillibrium the shit storm gets increasingly harder to reverse. Ask yourself how long and how difficult would it take to get another mortgage if you defaulted.

April 30 already? I love UE Thursdays. Almost as much morbid fascination as the old Bank Failure Fridays in 2008. If Bill McBride starts up BFFs again then that’s another leg down, mark it.

Good point on UE compositional – any analysis of second and third round effects of the raw numbers should differentiate and disaggregate by “what kind of job was lost?” Not just by sector, but by bracket. Gives more of a sense of significance and impact, like a VaR summary for labor.

C

mebbe Societe Generale Friday coming soon…?

Families who live in their houses as a primary residential home will try to keep it. However, the second home rented via some Airbnb will be sacrificed to keep the primary residence. So, homeless population will not increase overnight. Economy and GDP might be affected. Hustle is not good for now. Loss of second and third homes, vacation rentals might really open up buying opportunity for real middle class people in future. Or, the rich can scoop up the properties via their banks wholesale.

The SFH/apt supply was sufficiently tight for years before C19 for rents to soar in the presence of barely growing incomes.

What is really needed is a major hike in supply – but not at ZIRP-hiked 300k “starter home” price points…but at something much closer to pre ZIRP 150k price points.

For the last two decades, ZIRP enriched builders have grown addicted to delivering half the homes at double the price – there is a huge market opportunity for traditional builders using mass production techniques a la Levitt Town 2.0.

But that requires work – not just the multi decade destruction of interest rates through money printing.

In my Southwest Metro area the cost to build very basic apartments was north of $140 psf, without land, in 2019. So no delivering lots of 150k houses to the market with those costs. There is some movement towards new modular building techniques that have might eventually deliver Levittown 2, katerra company is an example.

The silver lining is that the labor and materials costs are sure to drop..

Okay, but my pt is that we have been conditioned (largely via gvt abuse of the currency/interest rates) to think that it is somehow conceptually “impossible” for prices to fall for certain sectors (housing, med, educational, etc).

Even as aggressive “deflation” (gasp! GASP!) rules in other sectors (electronics, etc)…sectors that have actually managed to improve human living conditions – in contrast to the progressive immiseration “provided” by those sectors that gvt has “saved” from deflation (otherwise known as productive efficiency in less insane parts of the world).

That productive efficiency is the essence of your point about modular housing – there is no holy writ that demands $140 psf costs (or 2500 sf McMansions for that matter…Levitt Town homes were maybe 1500 sf) – those costs are a function of supply and demand, both modifiable (if heavily screwed up by endless ZIRP).

Land costs are more intractable…but even there, prices are heavily influenced by end use value…which is heavily inflated by ZIRP.

And I agree with your pt about idled labor possibly being redeployed to produce less costly housing – although it is a major, open question why such a redeployment did not occur over the past 20 yrs of mostly stagnant employment, even as home prices doubled as incomes stagnated.

Clearly there were impediments to increased housing supply, and I suspect they were largely generated by the traditional incest between private/gvt vested interests (incumbent interests are almost always the enemy of new supply…it lowers the value of those interests already in being).

Neighbor is home builder, told me last month or so $120/SF for ”plain jane” 3&2, i.e. std family starter home, SOG, block ext, basic finishes, but he had run out of available lots in tpa bay area, and did we want to sell him our 1950 2&1 900SF cottage for the lot? No, we do not…

In const biz in CA, FL, TN, other areas since 1950s era, and can tell you that many folks just do not want to work in const because it is hard work at least some of the time.

As commented, modular is helping reduce cost of larger projects, esp multi family, and have seen apts/hotels based on ”podium” model with mods stacked high (22 stories in one case) above, etc., going around $100/SF in TX, FL, norCal last couple of years.

One mod manufacturer told me he could deliver and place units faster than we could ”hook them together” if given time to prepare.

Other concept gaining ground is actual 3-D printing of small homes, approx 600 SF out of concrete for less than $40/SF for structure only, establishment highly resistant so far, but I do think it will become important component eventually, right up there with modular homes.

Last mod commercial in SF, last year, all union, was about $120 installed with everything above dirt…

Meanwhile, homes I worked on in early 60s in SWFL, built for $12.50 now selling for over $1,000/SF!!

VVN,

“In const biz in CA, FL, TN, other areas since 1950s era, and can tell you that many folks just do not want to work in const because it is hard work at least some of the time.”

Agreed…but my guess is that if builders had increased wages anywhere near as fast as they raised ZIRP inflated SFH prices, they would have had plenty of US citizen applicants.

But, like a lot of other US businesses, they formed an unholy alliance with vote harvesting Democrats to import illegal alien labor by the millions.

There was an article on WSJ yesterday about Airbnb hosts who are overextended. It was interesting to see at least one anecdote about a host who rented apartments and then used it as Airbnb. But looks like an overwhelming majority has bought more houses through leverage.

There were snippets about people who had been getting supplemental incoming those properties generated, some of it was quite large. And now those bookings have vanished, and there may be a wave of offloading coming.

So I suppose that’s one way of getting primary residence ownership up, but on the other hand, it might mean lower rent. Both of which might be good for the market, but there will be a lot of air let out of that asset bubble over time.

Sonoma County will take a big hit, I drove through Sebastopol today and thought about which Restaurants will make it.

Do they have enough space inside or outside to make a profit if social distancing is required?

Do they offer a menu that will tempt more people to order to go?

My guess is that at least half will be gone in a year, many of which have been in business for a decade or more.

When it comes to housing, deals are still being made.

We still have a housing shortage and a shortage of active listings, but a LOT of buyers are gone and we are going to see a lot of places coming on the market.

A friend listed a very nice place in a first rate neighborhood at $1.2MM, it just closed at $1MM, all cash.

Christopherson Builders, who do first rate work and who are very sharp put a rehab on the market the first of March, reduced the price by 8% after 30 days and it has not yet sold.

Both of these properties were listed at, or very near the then Market price.

If you plan to buy a home in Sonoma County ( Or anywhere else in California) you had best not be counting on real appreciation for the forseeable future.

A home is an expense and a place to live, a hedge against inflation and a forced savings vehicle.

An income property is about income.

Period, full stop,

If it appreciates during the holding period, great.

However if it does not make sense based on the income it is NOT historically, a good investment.

The numbers work or they don’t.

PITI, maintenance and management are your costs.

And don’t fool yourself that Taxes and Insurance will be fixed costs during the holding period.

Maybe it’s just me, but I have multiple people in my life talking about selling a property they bought between 2016-2018 and they’re talking about selling it super casually, as if it’s a stock or ETF.

I’m very curious what happens when all these people who think it’s going to be the easiest thing in the world to sell a house (because prices only go up!) meet the reality of supply and demand.

Still a lot of flipper tv shows perhaps?

Flipper…Are you referencing that big old fish, or that stuff that smells like big old fish?

“I’m very curious what happens.. ”

Median price falls by half (give or take) – just like in ZIRP-Up 1.0.

Fewer boom Era homes built this time, arguing for lower hit.

But real economy impact of C19 almost certainly worse, arguing for worse hit.

CA and NYC are always the high volatility flippy tip of the Fed’s big swinging ZIRP.

Me too.

The construction and real estate industries should be allowed back to work on Monday already here, but this week many were allowed to start checking their construction equipment, picking up material, clean up etc. They are already licking their chops.

But how many sales will they make over the next months?

People here are absolutely terrified the lockdowns will be reimposed shortly on the flimsiest reason so they won’t exactly be rushing out to buy or lease a house. The top priorities right now is go out for a walk, go and say hi to grandma and grandpa and if we manage to get there without being locked up again perhaps get a haircut and some takeaway food. Then we’ll go back home, sit tight and hope and pray new cases don’t cause our politicians to completely panic once again.

Buying a house is not exactly on the book right now, and at least until there’s some certainty we are really in the “post-emergency phase”.

So we’re all here pointing out how absurd the stock market and housing is when you look at fundamentals but the world at large is only fixated on the headlines. E.g. remdesivir (sp?) trial yielded a median 4 day reduction in recovery from coronavirus and perhaps a negligible reduction in fatality rates per the data shared today. That’s what the market is so excited about?? Give me a break. I’m about to give up trying to understand what’s going on. The Fed has pumped so much liquidity that nothing makes sense anymore. The moment they said they’d buy junk bonds (even tho as far as I know they haven’t bought any yet) it was game over. Best case we end up like Japan with decades of low rates and low growth. How does this all end? Why do we keep thinking it’s ok to make future generations pay for the mistakes of the present? Ok I better stop here…

“they’d buy junk bonds (even tho as far as I know they haven’t bought any yet)”

And haven’t any of these equity-heads noticed that the Fed had no problem letting individual industries go to the BK blade in recent memory (oil, post 2014, with hundreds of BKs…) without directly intervening.

If cruise lines, casinos, oil companies, and the Gap turn crap (and little else systemically) I don’t know if the Fed will feel compelled to actually act.

It ain’t like they are *banks*, operating on slender equity cushions and – much more importantly – the private sector cats’ paw that provides cover for the Fed’s economic control via multiple monetary expansion.

You can’t use the Gap to control interest rates…

It is only when enough industries actually turn t*ts up to endanger the banks in toto (or really just the Big 4) that the Fed feels it has to buy and bail everything.

So far, just jawboning.

The Fed is probably paying a helluva lot more attention to housing across the nation…a major hit to that will take down almost all banks (again) because of all the MBS crammed on banks’ balance sheets. The only item banks’ have more exposure to are DC’s Treasuries.

Only select banks have very heavy exposure to retail, casinos, oil, etc – but they are all Wiley Coyote when it comes to housing/MBS.

Me too on the about giving up part AB.

Been on here a couple of months trying to get some education re bonds, muni bonds in particular, and do find a ton of info here, and that’s good.

But, when a leading puppet politician says just let the states, munis, etc., to BK, that’s bad, very bad.

One of the frequent commentors here suggests the worst thing is the uncertainty produced by all the puppets pronouncing one thing one day, another thing, apparently opposite the next — from the same puppet!

So Wolf et al, what do you think of the tax free muni bonds with the current events in mind?

Thank you.

I wouldn’t go long on anything at this time. Sitting on cash here, living like a miser, and biding my time.

Same here, for a while now, and, not trusting banks, I had been and am thinking about ”something” other than RE…

Question is, how likely are we to see BK of municipalities wiping out their bonds?

Even low interest bonds are sure to be more than bank int., eh

Stocks have gone psycho. Bond risk is greater than the reward, not to mention yields suck. Rentals are a pain in the ass, especially now. Forget flipping if prices are expected to come down. I’m thinking a recession proof business like a pawn shop, prepper shop, or weekly motel. Have to deal with the riff-raff , but at least you can kick them out right away. IDK,,probably best to do nothing until the bottom sets in.

“what do you think of the tax free muni bonds ”

Be very, very, very careful – huge public pension shortfalls at both local and state gvt levels – Google to get details (there is a ton of it online).

Ask yourself if a $40k 2 earner household will happily pay increased taxes so that some 50 yr old ex-DMV worker gets his “guaranteed” $80k per yr in pension pmts…every yr, for the rest of his non-working life.

Revolutions are made of such stuff…and state/local bankruptcy of some fashion is one mechanism to undo those politically purchased pensions.

20 yrs ago even talking about undoing those political pensions was a third rail…now there are multiple long standing websites dedicated to the topic, even well before the SHTF in depth.

Those pensioneers will try very hard to feed everybody (including muni bondholders) into the wood chipper before they give up a penny of those politically purchased pensions.

Google Vallejo, San Bernardino, Detroit public pensions…you will see the trench warfare soon to come to many/most US municipalities, school districts, and states.

“But, when a leading puppet politician says just let the states, munis, etc., to BK, that’s bad, very bad.”

Some guy from Kentucky, a state with 4.6 million pop calls the shots for 330 million people? We need a political reorg badly. The unthinkable slouches towards us.

Of course March numbers plunged. Power hungry governors in several states shut everything down. Most if not all realized housing is you know – ESSENTIAL – and allowed real estate to start again. Plus the initial shock of the ‘Rona in March froze people. If all you did was watch CNN you’d think the world was about to come to an end in early to mid March. Buying a house wasnt exactly #1 on your list of things to do.

That insanity was gone by the end of March into early April. The economies of most states are now open.

If April 2020 is as bad relative to April 2019 as March 20 was to March 19 then that will be meaningful. But March is such an outlier that I don’t think it means all that much.

April is already worse than March was overall. First half of March was pretty good, the second half sucked. In April, all of it sucked.

For once, I would like to hear some Federal Reserve’s spokesman make a statement like that instead of their unnerving newspeak drivel, you know, something along the lines of: “You really want the truth? Well, it sucks. All of it. Big time.”

Whenever the Fed starts referring to a” challenging environment”, what they really mean is that the sky is actually falling. “Unlocking value for shareholders” is another good example in the private sector. After all, “daylight robbery” is such a crass concept.

Wolf,

Agreed.

But I wonder what you think might be the 1 or 2 fastest-turn leading indicators of national real economic activity?

Rail car loadings? Too bulk commodity influenced?

CA shipping container offloadings? Too subject to exporter push vs. Actual US demand?

Or weekly aggregate unemployment levels…considering that not much is going to move very fast if tens of millions have no ongoing income.

At their hugely inflated levels, I vote for unemployment levels…there is no way for GDP to grow at these levels.

It isn’t like the stock market where you can huff paint and convince yourself of almost any future valuation.

If gross household income falls 15 to 30 pct because of unemployment…groceries don’t get bought, gas doesn’t get burned, etc.

There is no way for that to not show up in GDP, no matter how manipulated the methodology (although DC will try…).

And employment/unemployment numbers seem to be generated among the fastest.

In my subdivision there has been no let up in construction. Several homes have been finished and people have moved in during the ‘Rona times. And just ball parking it, there are about 12-15 homes under various stages of construction right now. Which is typical.

And really everything is typical. Other than restaurants, things are back to normal all around as far as I can tell. Even traffic is back to its pre ‘Rona ways. I miss the brief time when I could drive 70 at 5pm on a weekday.

I went to Walmart this afternoon. It was funny how there are signs everywhere about staying 6 feet apart while everyone is ignoring them. Other than employees, maybe 1 in 10 people had masks on. And the 6 ft rule is long gone.

The entire s**t show is just about over.

re: “I went to Walmart this afternoon. It was funny how there are signs everywhere about staying 6 feet apart while everyone is ignoring them. Other than employees, maybe 1 in 10 people had masks on. And the 6 ft rule is long gone.”

I started to reply: “Well, it IS Walmart.” Then I remembered I went to a Lowe’s yesterday and, same story.

Oh, my favorite are the people wearing masks, covering their mouths but not their noses.

You mean like Congress creatures?

Masks are still efficient even if they don’t cover their noses, they protect others when you sneeze. I go to local Walmart, Costco and Home Depot here in San Diego and I can tell that all people have masks, I haven’t seen anyone without some form of mask for the last two weeks.

Yes, the fear show is over and most people will forget quickly. Just look at the stock of Norwegian Cruise Line Holdings, up over 75% since April 24th. Doesn’t matter the reasons why. Tesla showing a profit and accelerating to an all-time high stock price.

I should have bought everything during the 7 day dip in stock prices. Foolish me for believing negative spin websites like Zerohedge.

I had a house built a few years back and had to get it done quickly after first builder pulled out. It still took four months from signing. So since four months ago was before any of this, construction will still be going on now even if all housing starts stopped three months ago.

When you are looking at a house under construction you are looking in a rear- view mirror at decisions taken a minimum of 3 months ago.

As for ignoring distancing, the kids who gathered on the Florida beaches decided to return to a normal spring break: ‘if I get sick I get sick’

Some did.

Houses in question go up in about 2 months. These aren’t custom built homes, working with a contractor that take 6-12 months to complete. It’s subdivision cookie cutter houses. Granted somewhat upscale homes, but still cookie cutter, assembly line homes.

My county’s death toll from the ‘Rona is in low single digits. We’ll be fine.

Over ? Or intermission? Anyone who thinks things are going to return to pre rona times is delusional. Too much damage done.

During the 1918 Spanish flu the people of SF deciding the pandemic was over all threw their masks in the street and began to celebrate, filling bars and restaurants. Withing a few weeks the flu numbers spiked and they had to lock the city back down. Human behavior seldom changes….

Was at Costco in Lafayette La. on Tuesday. Fully stocked shelves (pallets). Employees all had their masks and gloves on. Only one out of 20 or less of the customers had masks. Interesting it’s located next to a couple regional hospitals / medical centers and I observed at least a dozen people in scrubs (save to assume medical professionals) and NOT one had a mask.

Elsewhere in town it looked like business as usual except for a few retailers and restaurants.

Forbearance is such a complicated world. Maybe “mortgage payment postponement” (possible adding, “with interest accumulating”) would be a better phrase?

word not world

Forbearance means patient self control, endurance or even fortitude. From a legal perspective it describes the action of refraining from exercising a legal right, especially with regard to enforcing the payment of a debt. But I agree with you, we should keep it simple….mortgage payment deferral, or something similar would be more descriptive.

Thanks, deferral is probably the better word.

A couple of realtors in the Redding area say the phone has been ringing off the hook from Corona scared Bay Area buyers wanting to buy a house in the country.

Hmm, see if that pans out?

Everyone was going to move to Canada after Trump won. I remember the same type of headlines “Canadian Realtors Phones Wont Stop Ringing From American Democrats Scared of a Trump President”.

How many people actually moved to Canada? Nobody.

I suspect this phenomenon is the same thing. People are calling, looking for homes online, etc. But in the end I doubt many people from SF or NY or LA move to flyover country over this.

Just Some Random Guy,

Yes, kind of funny, actually. Every year there are surveys that say that 30% or 40% or whatever of the renters in San Francisco (I think over 60% of the housing units here are rentals) want to leave. And they don’t leave, and the city keeps growing… Fake wants :-]

Well, until the bust… when laid-off workers cannot afford to live here anymore, and they actually leave. This is happening now. It happened the last two busts. I already saw this in the March labor force numbers, and this is going to be an even bigger number in April and May. Happens at every bust in this boom-and-bust town. Very predictable.

In the past, these folks went back to where they’d come from, including mom and dad’s place. This time, some of them may head to less expensive places in California hoping to keep working here but do it as work-from-home. Redding is a cute historic gold-mining town, and fairly close to Mount Shasta and the lakes around it, and there are other towns like that. If you have to commute to SF only twice a month, it’s doable. Just get ready for some real heat in the summer.

Yeah there will be some of that. But I was referring to people moving to Redding (or whatever) because of Corona itself, ie feel safer in a small town vs big city. Not due to economic reasons.

And you’re right about those surveys. 1/2 of SF wants to leave yet the city grows every year. It’s the bar that’s so crowded nobody goes there anymore.

You nailed it Wolf. I hated living in CA the last 10 yrs. I was there, but it was where my job was, and people have to live where they can make money. As soon as I no longer needed my job I was gone in less than a year.

CA is a great place as long as you do not have to commute and as long as you have enough money

What makes you think you can just move to Canada if by move you mean permanently and to work ? Check Can Immigration.

PS: I personally know two people who tried.

Of course I mean Americans. Half the world wants to get into either country. Both had jobs waiting.

CAN immigration has been a bit looney for a long time NK,,, I tried to immigrate there as a ”landed immigrant” in 1970 when they were welcoming some folks, but was turned down — at the border — because I was NOT AWOL or draft refuser, etc… I was going to homestead some of the land offered up there at the time, already a vet, with farm experience including behind a mule drawn plow, etc., had cash and all the basic tools needed to start, !!

A long time screws loose situation up there…AKA ”loose cannons” eh?

Makes ya wonder how long it will bee until those provinces will be part of the United States of America, eh??

(OK Paulo, have some fun with this!!)

Wish you’d made NViet. Should have said u were a draft dodger. Our loss.

Choosing to accept forbearance from your servicer will have long-term ramifications for those that choose to do this without need. Fannie, Freddie and the major banks are already rolling out new guidelines making it impossible for a consumer to refinance their mortgage if they have missed payments. Sure, you won’t be reported as making late payments, but you won’t be able to refinance that mortgage.

I do not know, but I would assume it would have some negative effect on your credit record as well.

I read the headline before I had my first coffee. I thought it said “mortgage forbearance ballrooms”. It all made sense. A lot of people dancing because they didn’t have to pay their mortgage.

Wait until they have to deal with the big lump payment at the end. They’ll go from dancing the gigue to singing the Blues.

I submitted my application for a 30 year fixed last weekend. Looking to buy in the Bay Area in the next four months. I’m excited to finally get out of an apartment!

1) The American corp balloon was pricked. The old pyramid have shrunk. US corp is frugal.

2) America became more competitive without knowing about it.

3) Things are not the same. there is a change of character.

4) The cost of an engineer is the cost of his salary & benefits plus the cost of the whole pyramid above him, divided by the number of engineers in the co.

5) Include the cost of the finance department, sales dept, HR, RE…

all the way to top management up to the CEO.

6) Since Mar 2020 bonuses, dividends, options, buybacks are mostly cut.

7) Many employees got pink slips. The rest work on furlough. Many on 70%-80% of previous salary.

8) The cubicles are dead. Old RE was a fad. Employees work from home, on conference calls.

9) American businesses is using employees apartments or homes, that cost a lot, without paying them a dime. Don’t dare complaining.

10) There are plenty good engineers, MBA’s and other professionals out there looking for a job.

11) New engineer salary, fresh out of college, is about $80K/Y + benefits. An experienced engineer salary is $100K/y- $120K/Y + benefits. With 20%-30% pay cut the difference is rectified.

12) Who need under trained new engineers during a recession.

13) The pyramid have shrunk overnight, We became more frugal and efficient, but the competition is a moving target.

Interesting point you make. How will a corporation train a new engineer hired straight out of college? “Congratulations, welcome to Intel. Now go home and read our new employee handbook. When you have your work-from-home setup ready we’ll get you started on designing new chips.”

The old lady who own a 5,000 sq.ft McMansion, in an upscale place, for x2 long months, have to clean the house by herself, since the maid who used to do it for the last 10 years, is not coming and there is nobody else around.

It takes time to clean a big house like that. Its really a hard work. but there is no hurry.

She needs to form herself into a LLC, take on casual contractors, pay herself, and expense a large room of the house to company functions as an office, while hitting up the SBA for support., and letting the garage to WeWork.

Sheesh. Where has the entrepreneurial spirit gone?

I don’t believe for a moment that corporate america has suddenly become more competitive or frugal, or that the balloon in the shape of a pyramid or whatever has been deflated or upended. This is still the honeymoon phase. August might be a different story. The only thing that occurs to me that would help wring out corporate excess is liquidation. Start again with assets remaining and recovered, goodwill in some cases, and rebuild the business model from the ground up.

C

I love the mentality some people have. They’ll go into a Costco with 1000 other people in the store. But they’re afraid of a maid coming into their house? LOL

My cleaning service is still coming every 2 weeks. Pest control was here this week too, did their quarterly service both inside and outside.

As for going to 2 months without cleaning? Pffft. My roommate and I went 6 or so months without cleaning our apartment in college. Both our girlfriends – with good reason – were disgusted with the state of affairs. So one day they came over and cleaned the entire apartment top to bottom for us. Today if that happened I think we’d both be arrested by the MeToo police, LOL.

So she lost the butler, the maid and the servants three? Will definitely need to knock down some pills now.

In the 90’s a property management company used to ask to see a paycheck/stub to make sure the person(s) applying to rent an apartment had a job. These people do not have jobs and are not required to pay rent due to rent forbearance. This makes it difficult for the real estate investor to pay the mortgage.

McDonald’s saw a drop in Q1 earnings. Shell (RDS.B) cut its dividend for the first time since WWII. They are down over 8% in premarket trading.

The best way to see how much someone wants to rent your place is to have them write out a stack of predated rent checks you can deposit each month. That will just about sum it all up.

Wolf, I know you don’t ordinarily let your disciples draw attention to their writings on other blogs, but I ask you to let this one ride:

https://lenpenzo.com/blog/id58566-grandfather-says-some-thoughts-on-building-a-life-long-homestead.html

It seems to me that this crisis might be the time for some of our enterprising youngsters to find a way to get up and out of the ratrace.

(kitten’s: phrase: “find a way”)

Also profoundly felt by Johnny Cash in the In Memoriam movie

“Hurt” by Mark Romanek

Thanks for the favor, Wolf

If you ever need spiritual counseling, I’ll provide it, free.

Wolf,

Thanks Wolf it all has been expected, even the fed was expecting it, not like the financial crisis. I see it as opportune times. Opportune times what the heck to push back a little and borrow on your great and incite full writings, which has helped and educated me. I do appreciate your contributions as a human being even though I haven’t purchased a mug. I am an icurable optimist even in these times, but more cautious thanks to you. Well, they are cutting dividends, Royal Dutch anyway. Large share count comparable to others and lots of natural gas. 45 k gas stations. Spread pretty thin there, too many in these times. IMO. Pulling the sector of others down a bit. Opportunity., time wise?, probably. I don’t get home builders going up though. Noticing some conflicting narratives on oil companies not finding engineers and how they can’t fill the positions because oil is bad. Big oil with digitizations doesn’t need them. Thanks again. Third day with my sister, she received I believe 2 c packs tested, waiting for results. Eight confirmed and three suspected. Hoping! It’s not bad for her. Will share anything as time goes forward.

30 million Americans filed unemployment already (for the last 6 weeks).

If you aren’t scared already, wake up. That $1200 check won’t last long.

I wasn’t around last 1929 so I have no comparison, just concerned. My parents were small kids then but the feeling stuck in their heads. My dad and his sister are in their nineties and still alive.

I remember my dad’s story he told my mother, then she told me. My dad started saving as a little boy. He had a wooden box. The savings was for a higher education. But after the war, the family spent his savings for his older brother to go to school in University of Michigan. My dad didn’t complain. He just saw his dream end up in smoke. Years later he got a full scholarship to Harvard and MIT at the same time. He studied German so he could read the chemistry books. He had no money, so he lived in the guest house of the kind Massachusetts governor at that time.

He worked for oil firms in the refining operations, then drug firms because he was a chemist. Why this story? Because I have a feeling we will see a generational reset. It will be time for savings and hard work again. I never heard my dad complain. Time for real life again. Do you know how to milk a cow?

Those 30 million Americans now with no healthcare. During a pandemic.

That’s a huge amount of money that will no longer be flowing to the insurance companies/hospitals/doctors/pharmacies.

Medicare4All may be here finally.

How to pay for it ? The tax burden on the remaining workers will be even greater yet.

The old who will/how to pay for it conundrum… The big money crowd loves workers who keep that old fashion ethic dear to heart. Primarily so they don’t have to.

Paying for the “right” things is easy.

Brrrrrrt go the printers. Predictable how some complex problems get solved so quickly with an endless supply of greenery.

The remaining workers should refuse the burden. Instead, they’ll likely roll over and beg for the usual scraps until even those don’t remain.

That’s widely believed but, in fact, there’s no way taxpayers can cover the astonishing increase in the national debt, which is actually what “pays” for it.

reduce the ‘defense’ budget by an order of magnitude. or two.

I hope this, even if I am already in Medicare.

No need not to give it for all Americans. Just a matter of priorities.

I know how to milk a cow. That does not mean I should milk a cow, as I have always been considerate of cows. Knowledge does not imply skill. But I know what you mean. I do have a problem with removing horns from young goats.

1) Macy’s CEO is scared. How can Macy’s attract customers back to the

ugliest building in the mall.

2) Landlords are scared of a renters strike. Renters are scare, accumulate arrears plus penalties. They want to go back to work and not to gamble anymore. The old lady in her 5,000 sq.ft McMansion is scared. She is alone for too long and hope to get out of her big fancy jail.

3) Market makers are scared. QQQ can tell us a little story about how scared they are.

4) QQQ, Nasdaq 100 ETF, 5 min :

yesterday before the close, QQQ turned sharply lower.

5) The last bar, before yesterday close, QQQ produced a very large volume, in red, the highest volume on the 5 min chart.

6) Market makers said : QQQ stop it now, u are not going down.

7) Today QQQ gap higher, produced an upthrust, turned sharply lower, producing a big red, high end full bar, x3 times the size of yesterday last bar size, on lower volume.

8) Yesterday high is resistance. Today high is an UT. The next bar lower, the 9.35 bar low is support.

9) 80% of the time markets will be in trading range.

10) That’s what QQQ is doing now. QQQ is building a cause.

11) Yesterday big red was a selling bar. When the next big red supply bar,

on high volume, will breach the trading range, this supply bar when it comes, will change QQQ character. It will show weakness. Its a signal from market makers. Until we get their signal, we don’t know what the market will do.

12) hit #1 started a trading range.

13) Hit #2, a signal from market makers, will change QQQ direction from up to down.

Asset and housing deflation? Not likely over time. In addition to stimulus discussed here relentlessly, expect a Trump defeat to turbo charge immigration. Nothing wrong with asset prices that 20 million more consumers riding a wave of UBI won’t cure, per year. If you listen to our rulers, they have been acting for many years on the belief that the US is underpopulated. Too many bean counters and not enough ideology in consideration.

Asset deflation is guaranteed. It is impossible for deflation not to happen.

The laws of economics mandated it.

The allure of all pyramid schemes is that they appear to defy the laws of nature. They seem magic, and therefore are somehow excluded from the natural laws that dictate the behavior of everything.

People are very susceptible to the fantasy that they are special, and that the rules can be ignored without consequence.

That is where we are at.

Debt based economies rely on inflation to create money without production. They rely on the promises of payments in the future for consumption today. They rely on the greater fool theory being the road to wealth. But mostly they rely on the belief that the pyramid scheme of inflation is forever sustainable. At the point where people begin to no longer have faith, the system collapses and true asset values are discovered.

The fact that debt based economies inflate asset values faster than incomes insures the collapse of the system at some point. The collapse is guaranteed, but until it happens, and even after it actually begins to happen, peoples greed will drive them to continue to believe that this time is different and that they will be able to defy the laws of economics….

Good one JD.

And I agree with you except for the part in caps I inserted below

”Debt based economies rely on inflation to create APPARENT money without production.”

IMHO, when and only when We the Peeons insist that our money not be stolen by the various and sundry and extensive corruption of the ”ruling classes” will we be able to grow in reality as opposed to the fantasy world we have been living in the last 4 or 5 decades.

jdog – the problem is that faith and belief are cheap to manufacture and don’t require much in the way of material resources. That plus the ever-present greed and hope means that this show can still go on for quite some time. Even worse if you include an inrush of naive, poorly educated immigrants.

The credit / inflation pyramid scheme can only function as long as people service their debts. When default begins to happen on a large scale, the forced of deflation begin to reverse the scheme.

I’m sure they’re giving you forbearance but if people get in a bind where they don’t make their payment for three months. I’m sure the list Penders will be filed from the date of your first forbearance.

No one can argue that mall real estate is not down considerably over the last year .This is a combination of online sales and the financial fragility of a number of national retail chains.

No one can argue that commercial real estate is not down .considerably over the last year. This is a combination of fewer foreign buyers , a collapse of demand from companies like Wework and recently the trend towards working at home using software like ZOOM.

No one can argue that the number of unemployed has not soared over the last year and will still be much higher even after the shelter at home orders are modified over the the next few months

No one can not argue that hostility towards China has not increased over the last year.

No one can argue that many mortgages are going to in be in “technical “ default, even if articles regarding forbearance are becoming more common.

No one can argue that rents and housing prices are taking up an increasing % of after tax income, even as after tax income is under pressure

No one can argue that jumbo mortgages are not harder to obtain than was the case previously

YET MANY REMAIN BULLISH ON RESIDENTIAL REAL ESTATE.

Based on comments I have read on this site I would also say…

that no one can argue there are residential real estate buyers

who have been sitting on the sidelines hoping for price drops.

Is this their time? Do they still have a job?

No one can argue that the Federal Reserve will not continue to suppress interest rates well into the future. No one can argue that the Fed will not create any amount of “liquidity” that they deem appropriate. No one can argue that these actions will not continue to distance the economy further and further from reality.

The Fed does not really set interest rates, it follows the bond market.

The Fed can create as much liquidity as it wants, but it will not find its way into the economy unless there is demand for credit.

In short, the Fed’s powers are much more limited than people think.

Belief in the Fed has grown to be a fanatical religion based more on faith than on actual understanding and facts…