Helicopter Money for Wall Street & the Wealthy: $2.06 Trillion in 5 Weeks. Regular folks, forget it.

By Wolf Richter for WOLF STREET.

Since the Fed announced its market bailouts and interventions on March 15, it has printed and handed to Wall Street $2.06 trillion. But here is the thing: This was front-loaded, and over the past two weeks, it has cut its bailouts in half, and it has stopped lending new funds to its SPVs that were expected to buy all manner of securities, including equities, junk bonds, and old bicycles. Those loan amounts haven’t moved in four weeks. What it has bought were Treasury securities and mortgage-backed securities – and it’s cutting back on those too.

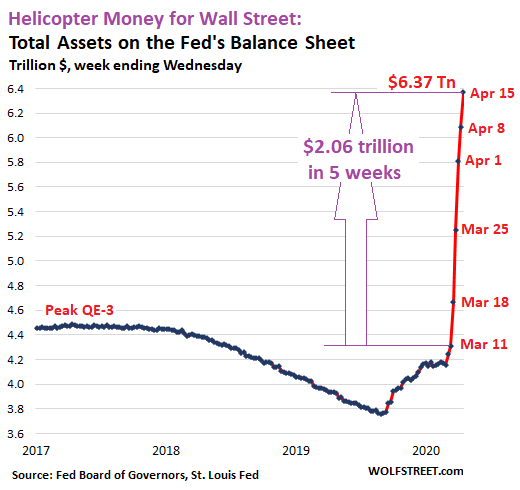

Total assets on the Fed’s balance sheet rose by $285 billion during the week through April 15, reported Thursday afternoon, to $6.37 trillion. Over the past five weeks, including the partial bailout-week which started March 16 and ended March 18, total assets increased by these amounts — note the big taper from $586 billion and $557 billion early on to $287 billion in the latest week:

- $356 billion (Mar 18, partial bailout week started Mar 16)

- $586 billion (Mar 25)

- $557 billion (Apr 1)

- $272 billion (Apr 8)

- $285 billion (Apr 15)

The $6.37 trillion of assets on the Fed’s balance sheet are mostly composed of Treasury securities, mortgage-backed securities (MBS), repurchase agreements (repos), “foreign central bank liquidity swaps,” and “loans” to its Special Purpose Vehicles (SPVs). We’ll go through them one at a time.

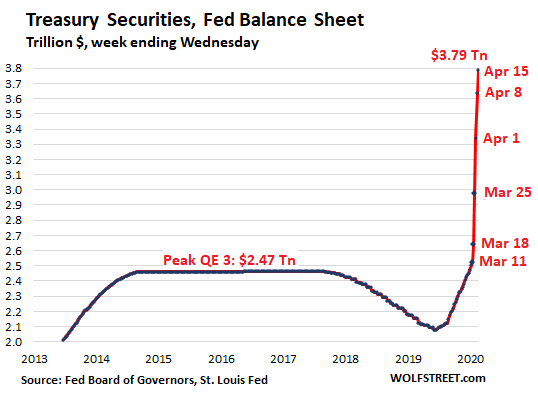

Treasury securities purchases get slashed.

The Fed added $154 billion in Treasury securities during the week, down 47% from the $293 billion it had added the week before, and down 57% from the $362 billion it had added two week ago. This is a major factor in the Big Taper of QE-4.

The sharp reduction in purchases of Treasuries confirms for now that the Fed is sticking to its announcement that it would drastically cut QE after the initial blast.

Fed Chair Jerome Powell in a webcast on April 10 said that the Fed would pack away its emergency tools once “private markets and institutions are once again able to perform their vital functions of channeling credit and supporting economic growth.” Whatever that means.

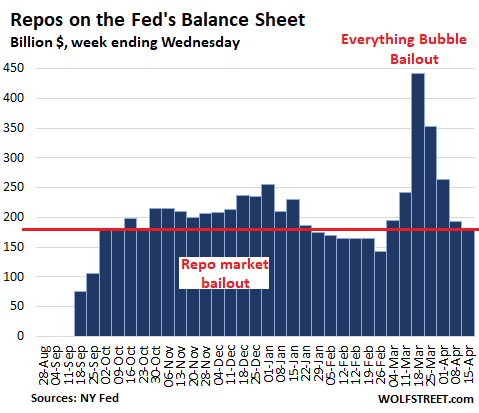

Repos fizzle further.

The Fed was offering gazillion per day in overnight repos plus over a gazillion a week in term repos. But since the beginning of its asset purchases, repos have receded into the background, and there have been few takers. The Fed has now reduced its offerings. And there is only a trickle of activity. Repo balances on the Fed’s balance sheet have now dropped to $181 billion. This decline in repos also contributes to the Big Taper of QE-4:

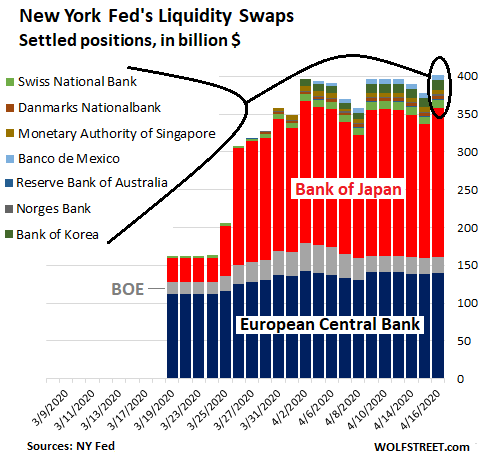

Central Bank Liquidity Swaps: BOJ & ECB

The Fed has “dollar liquidity swap lines” with the ECB, the Bank of Japan, and the central banks of Canada, England, Australia, New Zealand, Norway, Sweden, Switzerland, Denmark, Singapore, South Korea, Brazil, and Mexico. The total on its balance sheet increased by $20 billion from the prior week to $378 billion but has been in the same range all April. Of note:

- 83% of outstanding liquidity swaps are with the ECB ($138 billion) and the BOJ ($176 billion).

- The Bank of England is far behind ($22 billion).

- And there no swaps with the central banks of Canada, Brazil, New Zealand, and Sweden.

The chart below shows daily balances by country. The balance sheet is for the week ended Wednesday. But the chart also includes Thursday (right column):

Under these swap agreements, the Fed lends newly created dollars to the other central bank and takes their newly created domestic currency as collateral. The exchange rate is the market rate at the time of the contract. These swaps have a maturity of 7 days or 84 days. When the swaps mature, the Fed gets its dollars back, and the other central bank gets its own currency back. The Fed carries these swaps on its balance sheet valued in dollars at the exchange of the agreement.

Why do the ECB and BOJ want dollars?

The ECB and the Bank of Japan – the biggest users of the swaps – preside over export-focused economies that both have large trade surpluses with the US and through those surpluses obtain a constant flow of dollars.

In addition, their currencies are the second and third largest global reserve currencies (dollar’s share down to 61.8%; euro’s share at 20.1%; yen’s share at 5.6%).

Further, the BOJ’s foreign exchange reserves include $1.2 trillion in US Treasury securities.

In other words, neither the ECB nor the BOJ need the dollars for trade. They need them to support their banks and companies have large dollar-denominated debts and speculative bets that they need to refinanced with cheap dollars. And those swaps make that possible.

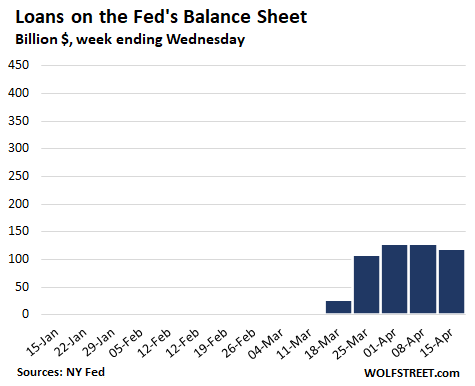

“Loans” stalled.

The category of “Loans” is a group of accounts that track what the Fed lends to its SPVs that it set up and what it lends to its Primary Dealers (the big broker-dealers and banks it does business with). The Fed can lend money to these SPVs which then can buy – even though it would be illegal for the Fed itself to buy – all kinds of stuff, including corporate bonds, junk bonds, equities, and what not. There was a burst of activity four weeks ago, but nothing has happened since then.

The balances of “Loans” fell to $120 billion (from $129 billion the prior two weeks). The chart is on the same vertical scale as the repo chart. After the initial burst, nothing:

As you can see in the chart above, the Fed has purchased practically nothing over the past weeks… just jawboning the markets. The loans by category:

- Primary credit: $41 billion, down from $43 billion. Expanded recently to include “fallen angel” junk bonds, but the Fed hasn’t bought any yet. The amounts outstanding predated the “fallen angel” expansion.

- Secondary credit: $0 (to purchase corporate bonds, bond ETFs, and even junk-bond ETFs). But none were purchased.

- Primary Dealer Credit Facility: $35.6 billion (up from $33 billion)

- Money Market Mutual Fund Liquidity Facility: $52 billion (down from $53 billion). This is the money market bailout where a few weeks ago the Fed bought corporate paper and other assets. No additions since the initial burst.

Note that “Secondary credit, which has been expanded to buy corporate bonds and junk-bond ETFs, has a zero balance. The Fed hasn’t bought anything yet. It has just been jawboning. And that was enough to trigger a huge rally in bond ETFs, including the iShares iBoxx high-yield corporate bond ETF.

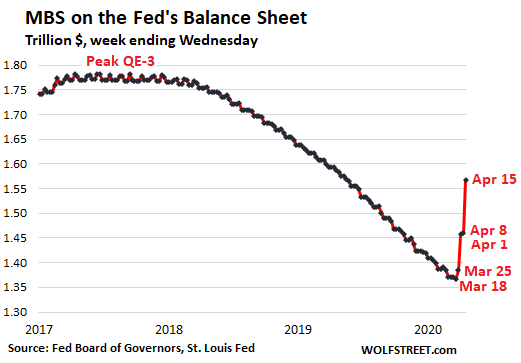

MBS.

The Fed has drastically cut its purchases of MBS over the past two weeks, as reported by the New York Fed:

- $157 billion (week ended Mar 25)

- $145 billion (week ended Apr 1)

- $109 billion (week ended Apr 8)

- $59 billion (week ended Apr 15)

But there are two complications with MBS.

One, holders of MBS, including the Fed, receive pass-through principal payments as the underlying mortgages are paid down or are paid off. Given the boom in mortgage refinancing due to the lower interest rates, these pass-through principal payments have become a tsunami. Just to maintain its balance of MBS, the Fed would need to buy a significant amount every week.

Two, MBS trades take a while to settle, and the Fed books the trades only after they settled. So what we’re seeing on the Fed’s balance sheet lags the actual trades by some time.

The increase of $108 billion is a mix of these two: purchases from the big burst during the weeks ended March 25 and April 1 some of which finally settled, minus the pass-through principal payments it received:

If…

Since March 11, the Fed printed $2.06 trillion and handed it to Wall Street and asset holders. The sole purpose of this was to inflate asset prices and bail out asset holders. The potential crumbs offered to small businesses or the real economy have not happened yet.

If the Fed had sent that $2.06 Trillion to the 130 million households in the US, each household would have received $15,800. But forget it, this was helicopter money for Wall Street and for asset holders – particular those with the riskiest bets – and for no one else.

“In May, what market? I don’t see no market”: Realtor. Read… How Will Covid-19 Lockdowns Hit the Housing Market? It Gets a Little Clearer

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Two thoughts. The Fed makes money available to loan, but someone has to be interested in borrowing or it really does not matter. Second, with so much debt going bad, and if it cannot stop what is happening, how willing is the Fed going to be to load their balance sheet with bad debts?

Yes, the problem we are seeing going forward is not so much the supply side, but the demand side.

The worst thing, at least for me, is uncertainty, which no amount of central bank activism can solve: how am I supposed to go out and spend to buy, say, new office computers or have a new climate control system installed if I don’t even know when I’ll be allowed out of the house for a ride? Right now my top priority is to rebuild the stocks we have used up, and add to them “just in case” if the lockdown is reinstanted and/or supply chains keep on breaking up, and have a water filtration system repaired: the repair technician can now come and do his job, but spare parts are apparently still stuck in a warehouse somewhere.

That’s about the extent of my present investment plans, and I don’t need to take out a 0% maxi stimulus loan backed by the ever suffering taxpayer to execute them. Until governments give me some certainty I refuse to spend a penny more.

Regarding debt… I’ll repeat what I always say: as long as creditors are fine with it, a company can pile debt to the sky and beyond and pay peanuts for interests. The problems start when creditors start getting cold feet, usually because they fear to lose a good chunk (say over 20%) of their principal in a restructuring deal or to be stuck with worthless shares in a bankruptcy procedure.

That’s exactly what’s happening right now with Norwegian Air Shuttle (NAS): after months of allowing themselves to be led by the nose, creditors have started to run around with their hair on fire. NAS bonds coming due in July 2022 are presently trading at 33 øre to the krone (Norse for “cents to the dollar”). And that’s after receiving the equivalent of over $250 million in bailout money from the Norwegian government, proving once again that sentiment, not fundamentals, is what drives financial markets. Until reality comes knocking at the door.

Jdog,

The Fed’s loans are primarily made available to companies that need to roll-over old debt. So if I need to pay off a $1 billion dollar loan next week and don’t have the cash to do it, I need to borrow it quickly. But in a crashing market, banks are highly unlikely to come up with that money for you. So the Fed is just making sure these companies can roll-over their debt instead of going immediately bankrupt. It saves the company, the jobs, and, to the Fed, most importantly, the banks that the money was originally owed to.

As to your second question, note in the process above, the Fed did stop it. For some period of time at least. And the Fed doesn’t care about taking on bad debt. The Fed is the creator of the nation’s fiat currency. It’s balance sheet is therefore infinite. Even $100 trillion dollars is microscopic compared to infinity. Yes that can mean hyper-inflation. But hyper-inflation is not in the best interests of the banks who control the Fed. Therefore, it is not a concern.

What the Fed is doing is exactly what it was put in place to do: to stop asset prices from crashing (which are collateral for loans), which keeps banks from calling in their loans, which would otherwise cause mass bankruptcy, bank failures and an economic depression. The Fed is doing its job, and doing it fairly well in my book.

The downside, as Wolf so elegantly states, is that it bails out the super-rich on Wall Street rather than you and me on Main Street. We could solve these problems differently: have a large federal agency that rapidly wipes out owner’s of debt and shareholders through bankruptcy and re-opens these companies with new shareholders who buy in at much, much lower prices. But that would require that us regular Joe’s provide higher levels of campaign financing than Wall Street does, and that’s not actually possible. So we have what we have and it works fairly well.

Kent said: “So we have what we have and it works fairly well.”

Yes, it works well if you are Jamie Diamond, Goldman Sachs or other priveledged beneficiaries. It also works to “debt slave” much of America. It also works well to grease the gears of globalization and subect American workers to the side effects of wage arbitage and outsourcing. You make an excellent cheerleader for the FED. Do they pay you for your service?

Well, no.

Kent says it clearly;

But that would require that us regular Joe’s provide …higher levels of campaign financing than Wall Street does, and that’s not actually possible.

…. and that’s not actually possible…

Us regular Joes only have a chance if we can find a way to outbid the Wall Street in their perpetual purchase of our governing classes.

Getting that type of money would not be easy, or possible even, so a way must be found, in the first instance, to ensure that each and every single “public official “ is held personally liable on an indemnity basis for any damage his/hers/them (see what I did there), “decisions“ inflict on those that voted for them.

But how to get to that point, through the endlessly corrupt legal systems everywhere, is another matter.

Kent has the markings of a FED shill. The FED always has room for more shills so feel free to join. The FED loves deception and prefers any slight of hand to make the public to think they are doing “well.”

The only way we peons have any chance of a fair distribution of wealth of this kind is when we insist that ALL elections follow a constitutionally mandated program:

The first and foremost mandate being all elections financed ONLY by public money. The second being some sort of solid/simple/transparent progression from wide open to all interested comers who put on the public website at least one page written by them in their own handwriting And one speech of say 10 minutes; from there to say candidates with 10 top vote totals, etc., down to final vote with top two voted for; and at each level, each candidate can put up another page or so and another 10 minute speech, with clear understanding any candidate getting a majority wins at any level.

This and similar, term limits, equal application/availability of all guv mint programs, etc., needs to be in a 21st Century Bill of Rights, following the ”Declaration of InterDependence.”

Until We the People vote only for folks supporting this, We the People are going to continue to be, in fact, WE THE PEONS, no matter which nominal political party is in charge.

Well in the meantime, we the people should not be apologists for the scumbag FED. Nor should we tolerate the apologists or useful idiots of the FED.

I choose not to be an apologist for crooks.

So, what happens when the debt that needs to be rolled over are all in the junk grades? Or, if the company’s debt is currently above junk grade, but has just gotten downgraded, or is about to be downgraded to junk?

How are the junk bond rollovers going? Any answers starting to come forth, Wolf?

This is what I want to know. Do we have any confidence that these emergency loans to big businesses will be paid back? If the underlying business is not innovative and profitable, no amount of propping up will save them in the end, and we are only supporting mal-investment.

Interesting political angle. Michael Bloomberg spent over $500 million in the democratic primaries splitting the vote to make sure Bernie Sanders would bow out. He evidently thought this was cheap insurance compared to the socialist threat (to his wealth) from Sanders.

The Fed can print oodles of dollars and give it away to their favorite banks, wall street houses and hedge funds.

The Fed can’t print farms. Or manufacturing facilities. Or mines. Or plumbers. Or hospitals. Or small businesses. Or trucking companies. Etc.

As these go bankrupt with the “lockdowns,” they are gone. And they are not coming back anytime soon.

Cheap and easy money can only very limited good. And a host of harm.

Should the Feds financial repression be lifted, and backing away from stimulus is a first step, though ostensibly involuntary, then you will see (inflation) and a surge in real economic growth. The proposed trillion dollar infrastructure bill never got off the ground. No one doubts the demand is there. Jim Rickards said there is no pent up demand, in a service economy. Once all of GFC is unwound, the economy transitions back to manufacturing, (domestic), which will be a difficult transition. There are two outcomes; the stock market goes to new highs, and people are in unemployment lines, or GDP soars, jobs rebound, and Wall St. (reallocates) tanks. Fed will transition but probably not until after the election.

Could it be that the “BRRRRRR” (money printing) meme is just a meme? Given that seems to have put a rocket under the markets, these gains could be a little precarious. Thanks Wolf — you are the only financial media I’ve seen that covers what the Fed ends up doing, not just its jawboning.

Good coverage once again!

Even if FRBNY started to purchase HYG, still wont make any difference as more default on their 98.8% unsecured underlying bonds (nearly 1% of HYG triggerd defaults this week by bankruptcies or missed payments: WLL [3 rolls of paper], JCP [2 rolls paper] ,FTR [4 rolls of paper], NMG [2 rolls of paper] out of like ~1000 toilet paper holdings in HYG) and nearly 43% of shares outstanding are sold short.

Watch for these 8 companies of 300+ in HYG; the used toilet paper below makes up ~13% of the notional value in HYG with ~8% of the toilet paper inside of it, and any credit event turns any of their unsecured trash into jeromes most expensive cheeks cleaner:

NGLS 10 [u’NGLS’, ‘TARGA RESOURCES PARTNERS LP’]

Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3

CHTR 13 [u’CHTR’, ‘CCO HOLDINGS LLC’]

B1,B1,B1,B1,B1,B1,B1,B1,B1,B1,B1,B1,B1

BHCCN 14 [u’BHCCN’, ‘BAUSCH HEALTH COMPANIES INC’]

B3,B3,Ba2,B3,B3,Ba2,B3,Ba2,B3,Ba2,B3,B3,B3,B3

NFLX 10 [u’NFLX’, ‘NETFLIX INC’]

Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3

THC 10 [u’THC’, ‘TENET HEALTHCARE CORPORATION’]

Caa1,Caa1,B1,B1,N/A,B1,Caa1,B1,B1,B1

TMUS 10 [u’TMUS’, ‘T-MOBILE USA INC’]

Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3

CSCHLD 12 [u’CSCHLD’, ‘CSC HOLDINGS LLC’]

B3,Ba3,B3,B3,Ba3,B3,Ba3,Ba3,Ba3,B3,Ba3,B3

NAVI 10 [u’NAVI’, ‘NAVIENT CORP’]

Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3,Ba3

Same is true for LQD holdings if any of that 45% BBB trash eats dirt…

The holdings for this ‘junk’ in HYG is like 0.1%

Thus even if you can find ten major holdings that BK, your talking maybe 1% of the assets, and besides the good-stuff keeps rising.

Most likely of course is HYG has already sold the losers, as they’re aren’t ‘High-Grade’ anymore

…

But this could be the end of the ETF, as you all know, they have to sell the good stuff first, because its liquid to cover redemption’s, then they’re only left with the trash, and thus the buy&hold crowd that holds an ETF, gets hurt really bad by waiting for the liquidation sale to take place

I guess the irony of all irony’s is “HYG” doesn’t mean what you think, as the high-grade is the only thing that sells during a bank-run to cover draw-downs.

Most likely the ‘cash’ that FED gives these ETF’s is not stock purchases, but just cash to cover people who want their money back NOW.

The last guy that leaves an ETF get’s the empty bag.

Winning, to quote Trump

HYG is “High Yield” aka all junk ok there are 3 trash in it that are BBB) so there is no “good stuff” because 98% of it is unsecured (reflective of the overall corporate bond market that is collateral light with about 85% unsecured). LQD is “Investment Grade” (96% unsecured paper in it) and they both certainly have more breath of coverage than say the cdx na hy or cdx na ig (both of which only cover ~100 companies instead of 300+ in HYG and LQD respectively) as index.

Or you can go to one of those private bond funds that will lock you out and still end up giving you back pennies on the dollar…

The overall corporate bond market is crap when it comes to getting back par post credit event, and the ETF holdings reflect that.

Gotcollatoral do you think hyg can go to zero?

Last time I looked ,

Energy comprised 12% of the HYG portfolio.

With inland storage likely to be completely filled in about 3 weeks, cash flow for E+P producers will tube as they have no choice but to cut back production .

He must have been looking at current value not par value (what investors lent) lol

May be Munchkins kickback negotiations are taking longer than expected for the SPV to kick in?

This looks more like deceleration of expansion. I’ll believe it’s a taper when those graphs start pointing down. So far that’s only happened with repos.

Isnt the drop in REPOs just an indication that other avenues of liquidity have been opened and those who were in constant need before are now using other facilities or new programs to ease their situations?

ie the Discount Window, which was supposed to be an embarrassing location for relief, with a penalty rate and public transparency, is posting a rate of .25……..with no penalty and no transparency. That’s pretty close to FREE money. Supposed to have a 50 basis pt penalty. Dropping that is a curious unreported perk for Wall St.

Michael Gorback,

“I’ll believe it’s a taper when those graphs start pointing down.”

No. That would be the “QE unwind.”

“Taper” as defined by the Fed in early 2013, is the gradual reduction of monthly QE purchases. When the Fed announced in early 2013 that it would “taper” QE Infinity purchases, which were still running full blast at the time, credit markets went into “Taper Tantrum.” And it took the Fed another year until early 2014, when it started “tapering” its QE purchases. It then tapered its purchases, reducing them every month, until Dec 2014, when monthly purchases reached zero and the balance sheet no longer expanded – meaning the Fed at that point was just maintaining its balances.

From Dec 2104 to Oct 2017, the Fed maintained its balance sheet at a steady level.

The decline in the balance sheet was the “QE unwind” that started in late 2017, which I heavily covered here.

Hi Wolf:

What is the Fed’s posture towards the Bank of China? Any swaps?

Thanks.

K

No swap lines with China.

Wolf,

Thanks for the overall summary and breakdown of Fed activity – please keep providing them every week or two.

The segmented high level activity is going to have significant effects going forward (I don’t think the Fed will be able to sustain jawbone-only mode too long…the unprecedented sudden stop will fatally dislocate too many large businesses that only survived the last two decades via ZIRP…but even ZIRP can’t save them from ZIP.)

The implications of each FED program’s rolling activity going forward are going to be complicated and worthy of in depth discussion (say, for instance, how Fed purchase of Treasuries likely sucked demand out of repo mkt…) but I’m too worn out from hunting for canned meat today to get into it right now…

(How do you hunt canned meat? Vwery, vwery, qwuietly.)

What would an Austrian School economics solution to the mess we are in look like?

Well the level from which we fell would not have been so lofty, for starters.

Wolf,

Great post. Thank you so much. Hope I didn’t wake you.

Is there any country in the world, now or in the past, that has adopted the Austrian School economics solution?

roddy

Do you mean free markets without central planning?

What specifically do you refer to when you mention Austrian School?

The choices are credit expansion until the total collapse of the currency or austerity. Americans don’t do austerity unless it’s forced on them.

Why is austerity the only alternative to credit expansion? I can think of other alternatives, and austerity is a proven failure world wide. Just look any country that lets the IMF set their policy.

Pretty much. I can’t recall such a situation in modern history. Perhaps Somalia, where feuding warlords compete without government intervention.

roddy6667,

Austrian school of economics is just vague non-sense, they famously are opposed to math and instead favor individual sovereignty. Individual sovereignty is the cure for everything in Austrian economics. With individual sovereignty, everything magically fixes itself, because, individual sovereignty is so powerful, math isn’t needed. Such a school of thought can only succeed in small tax havens/parasites, and that depends on large rich countries allowing it.

In general though, all the economic schools are simplistic, and in order to succeed you need to piece together a set of different policies for each individual country or economic Union, and those policies will probably have to change over time.

“With individual sovereignty, everything magically fixes itself,”

If I go to McDonalds and they can’t get their shit together enough to produce a hamburger, I never go back and they never get another dollar of my earned wealth.

If my kid goes to a public school district that can’t get its shit together enough to provide a decent education…they tax or take my house.

Or get DC to print money…which defrauds me of my wealth.

Institutional accountability is what makes things *work*.

And individual sovereignty is what makes institutional accountability work.

The same applies to bailed out companies – without a gvt empowered to defraud savers through printing there would be no possible bailouts.

Gvt fraud is the indispensable power in these now habitual farces.

But…but…”math”…which you don’t bother to describe, simply invoke.

Roddy

“Austrian school of economics is just vague non-sense”

Only for those who glance and turn their head.

Vehemently against central planning and a tremendous faith in individual analysis and decision making. For they make the irrefutable point (close your ears) that a myriad of people with excellent information and driven by their self interests and economic realities can discern and react to economic conditions, thus rationing and consuming, investing and divesting in a more efficient manner than unelected central planners in an oak covered board room, dictating behind closed doors, and insulated from the ill effects of their policies by inflation protected pensions provided to them by those who carry the brunt of their uninformed dictates.

Austrians? We would move do to a hard(er) money system.

It seems to me a large percent of the problems in the USA are due to aforementioned BRRR machine. It’s now obvious that the cat is out of the bag, “they are gonna print – they can’t stop printing – they have not choice. And NO ONE worries about how any of this will be paid back anymore.

So currently we are still Wil E Coyote suspended in air off the cliff.

Last time around in 2008 we *seemed* to get back on solid ground. But that *appearance* doesn’t seem possible to achieve this time.

Peter Schiff is a big speaker for the Austrians, and he generally says, “We need to take our medicine/pain now, and allow what needs to fail/go bankrupt, to do just that. And then return to a world in which money is tied to something tangible, so that it can’t just be generated out of thin air by those with the power to do so, in order to give it to their friends. Or later, when it’s worthless, to give to their enemies with the pitchforks and torches, in an attempt to avoid the guillotine.

I think the “Chicago Boys” were invited to design the ‘new’ economy in Chile after the ‘socialist’ Allende was assassinated. The result was an economic structure that could only be sustained by brutal authoritarian rule (the opposite of ‘Laissez Faire’).

So, there was a test (unlike in most cases), and it showed a massive failure WITHOUT foreign interference (other than support)!

More food banks and mass protest?

Does it help if you think of this Fed scam is just a suit wearing food bank lineup and some insiders are loading up friends pickups out the side door?

No, I understand the Austrian model means we are all supposed to be self-reliant and those durn food banks would have never been needed in the first place for individuals or corporations. I just think examples of graft and excess seem to be part of human nature and would have existed, anyway.

Austrian model does not shun food banks, it encourages private enterprise of all kinds including charitable enterprises, and some also promote government safety net. The Austrian model is more about government interference in interest rates ie countering Keynesian model. We would be well served by it.

Raise interest rates, cut government spending and taxes across the board. We need to purge the rot from the system not accelerate it.

The system is the rot. Debt forgiveness and nationalize the banks to start. Next we need Socialized Medicine. After that redirection of “Defense” spending to infrastructure. If we don’t, “Apres moi, le deluge”.

Well that is a long way from Austrian School economics but more like Karl Marx school of economics.

Assets would depreciate to values determined by the market. Fed supported crony bankers would cry. Pensioners would actually earn interest on their deposits. Wage earners would be paid according to their productivity. After a few years, everyone would be more productive and wealthy except the cronys.

Yeah, it’s a shame that the average person does not understand this enough to revolt against all this the way they should. Most just think the economy was “doing good” and stock prices reflected that and now all this is necessary to “save us”. If they really knew they wouldn’t stand for it as what is actually going on is just about criminal….they’re stealing from us to prop up those that have squandered it and now none of us benefit and cannot invest wisely with any confidence. It would be so much better for everyone if we just did it honestly but that doesn’t ever seem like a possibility.

I think the ‘average person’ in the USA does understand the situation that Wolf and others report so well on.

The tricky part of a ‘revolt’ against the actions of the Fed and the New York Fed is that it’s impossible to do anything about it. The two party duopoly is so entrenched and powerful, that it will not be broken in my lifetime – despite my tiny efforts to break it every time I vote.

As long as the red/blue status quo controls the Executive branch and Congress in Washington DC, nothing, I repeat, nothing will change.

Professor Mujahid Kamran, a theoretical physicist from Punjab, Pakistan sums it up spot on:

“The United States is a country controlled through the privately owned Federal Reserve, which in turn is controlled by a handful of banking families that established it by deception in the first place.”

“The tricky part of a ‘revolt’ against the actions of the Fed and the New York Fed is that it’s impossible to do anything about it. ”

Exit the dollar.

If it isn’t used, the power to dilute/steal evaporates.

And if some MMT’er spouting fiscal fascism comes to throw you in jail for refusing his fraudulent fiat?

Shoot him in the head.

From cover.

From a distance.

Rinse.

Repeat.

I still don’t get why currency speculation, dollar denominated debt, requires the Fed to step in with these swaps. When the decision to make this debt dollar denominated, a risk was taken. Why should the Fed step in to relieve those who are caught in a speculation? Especially nations like Japan who have huge trade surpluses with us?

And btw, NASDAQ 100 higher on the year….so the collapse that warranted all the helicopter money is tempered a bit, wouldn’t one say.

Otherwise the USD gets too strong relative to those other currencies, and it increases pressure on the Eurodollar system, and the Fed doesn’t want that.

As I understand it, here in Norway the central bank has been using those swap lines to auction off Dollars to domestic banks, buying local currency in return, in order to support the USD liquidity of domestic banks and the exchange value of the NOK, and bring NOK money market rates more in line with the central bank funds rate. The spread between Nibor and the funds rate was widening significantly with the price of oil crashing, government spending and deficits increasing, and as smaller and less liquid currencies like the NOK get abandoned during times of financial duress.

It’s absolutely ridiculous that we have to pay to keep the stock markets up when they are in known overvalued territory and not even down very much. Maybe if we had a 50% drop and valuations were crushed by historical standards but otherwise there is zero credible argument other than they are stealing from the tax base to prop up speculators and shareholders.

As I see it, a Japanese bank has a significant dollar balance sheet and needs assistance just as US banks do. The Fed doesn’t want to be caught bailing out Japanese banks. That job belongs to the National Bank of Japan. But it will swap dollars for Yen with the NBJ so that the NBJ can choose to supply $ liquidity to Japanese banks and with the credit risk born by the NBJ.

Second point – absolutely – market has bounced strongly so of course QE has slowed down. The question is what happens if the markets test the lows again. Probably massive QE again.

Why would any one behave prudently if you know that big brother is backing you?

problems and debt are getting bigger and bigger.

all fiat currencies eventually become worthless

“all fiat currencies eventually become worthless”

Being founded upon nothing more than the integrity and intelligence of a majority of politicians…of course they do.

And all empires eventually collapse — do you suppose this means that new empires never rise?

Of course not — which is why fiats, like religions, are always with us: whomever tries to operate without them get crushed by the larger agglomerations of humanity that they allow to form.

So get with the program, or get crushed by the program or its competitors/successors …

It may so far be jawboning in respect of junk bonds, but should the jawboning run out of steam then I’d guess that actual purchases will begin.

Also, and I’ll happily stand corrected if I’m wrong here, but isn’t the control of purchases by the SPV established to buy those junk bond ETFs with the Treasury and not with the Fed, in order to get around legal restrictions on Fed dispositions, with the Fed just obliged to fund the purchases?

In that case, unless there is some time limit established for the existence of such SPVs then I certainly can’t see politicians wanting to get rid of what essentially merges a portion of monetary policy control into a department under their power. The current US president will surely love being able to force monetary policy through such instruments.

Or aren’t the SPVs being administered by Black Rock so there’s a lag until these funding decisions are made and booked?

lenert,

What the Fed’s balance sheet shows is the amounts of funds (“Loans”) the Fed sent to the SPVs. And it has hasn’t sent any new funds to them over the past four weeks, after the initial burst. If SPVs get no funding, they can’t buy anything.

SPV, as I understand them, are off balance sheet tools and therefore would not show up on the Feds balance sheet other than a loan value. What the actual SPV is investing in would be hidden from the fed and prying eyes.

And with Blackrock in control, I would expect nothing of good to come from them.

If the Fed doesn’t fund the SPVs, the SPVs cannot buy anything. It’s as simple as that.

The Fed funds the SPVs via loans, and discloses those loans. And those loans, after an initial burst, have gone nowhere. In other words, over the past four weeks, there has no new funding for any of these types of asset buys.

What about the money the Treasury put into the SPVs? And who was actually to manage the purchases from the SPVs, the FED or the Treasury?

The Treasury provides a small equity slice for the SPVs as loss protection. The SPVs are leveraged 1 to 10. 10% equity from the Treasury and 90% loans from the Fed.

I hope so. Would Luv To See the Powell Fed leave the economically damaging Private Equity schemers high & dry and politically neutered by refusing to buy their junk bonds or leveraged loans. Why should We the People bail them out with our money? They and their damaging business model can work their way through the bankruptcy courts. That would be the honest solution, and as author Matt Stoller pointed out earlier this week would enable the economy to grow again.

Thanks.

Do we have any visibility into the $100B that was currently loaned to the SPV as to its disposition?

steve,

What the Fed itself discloses on its balance sheet, I summarized in the article under the “Loans” section, including the buying corporate paper to bail out money market mutual funds. The Fed also specifies what types and quality it accepts as collateral.

Thank you for helping people out like this, sometimes i wonder if people are even reading what you post

“and discloses those loans. ”

Presumably…but the Fed has now repeatedly acted in a way essentially unmoored from anything resembling “law” (beyond “do what thy wilt”).

Statutes that provide no prior notice of capacity or meaningful constraints upon action are meaningless as laws.

Jawboning? More like Jaws eating your bones.

*Insert JAWS movie theme here.*

Great info, Wolf. Thanks for this. This really helps to explain what the Fed is up. Real and imagined.

Thanks for this Wolf.

I’ve seen persistent assertions from ZH and others (ZH I take with a grain of salt but not always others) that the Fed is gobbling up junk bonds and ETF’s strongly implied to include stocks.

I mean, when they quote my former employer State Street that this is happening, easy for me to fall for it.

Thanks for the fact checking. If the facts are being fudged…well…that’s a whole different ball game. Not suggesting that but then there are Fed folks openingly advocating “opaque” reporting of information.

On the subject of Special Purpose Vehicles, here’s my outline to write to the NYFRB

Members of the Federal Reserve Bank of New York,

I am writing to request a loan of $250,000 to fulfill my Special Purpose Vehicle needs.

You see, my Special Purpose Vehicle needs to provide me with non-stop adrenaline. Recently, I have been able to acquire a Special Purpose Vehicle that can fulfill my needs when only two wheels are required, but as it stands now, when four wheels are required, my Special Purpose Vehicle cannot provide the needed acceleration to produce adrenaline in sufficient quantities.

Therefore, it has been determined by the Board of Directors of Romig Incorporated that a new Porsche 911 Turbo S is needed. As such, I respectfully request $250,000 from the Special Purpose Vehicle program be transferred to my Corporation.

Thank you,

-Dan Romig

Ha ha!

So getting the change out of the couch and the car and putting a few extra bucks on the mortgage won’t do much. How can I avoid this massive debt as all politicians hold a credit card with the name US Taxpayer on it. Their credit limit is always unlimited and they even max that out. I suppose if it doesn’t effect my day to day life it’s all good I suppose,

“How can I avoid this massive debt as all politicians hold a credit card with the name US Taxpayer on it. ”

Remove your name as a US Taxpayer by:

1) get good tax accountant (2+2=what do you want it to equal)

2) join the parallel cash or barter economy with no tax reporting

3) marry a wealthy spouse with non-taxable cash trust funds

4) use your C19 mask to rob banks

5) change citizenship

Uuuh, none of these methods are endorsed by the author.

A question for Wolf: My ongoing assumption is that nothing can be done via monetary or fiscal policy unless some insider-connected entity is making money from it. You’ve well covered which entities are profiting from receiving the helicopter money. But there must be transaction costs for all the Fed loans and purchases. Who is cashing in on these and are MBS and bond prices manipulated so the sellers get fat profits? Call me cynical, but I suspect there’s a layer of graft here that hasn’t been discussed. Thanks for the great reporting.

thankfully wolf sticks to the numbers and doesn’t get into the politics. he provides plenty of good leads if you are into looking at the sources of the graft you suspect.

Eye opening article that makes me think total manipulation of the markets is their ultimate game. Everything is fair in love and war and financial markets.

I wonder what Michael Milken is thinking about now as he was made poster boy to blame for creating this “junk bond” market that the United States Govt Federal Reserve is now ready to enshrine as AAA credit from CCC status in one fell swoop! Can you say chicken salad out of chicken s**t?

The name of the game with the Fed, judging by the fruits of their labor, especially since 2008, is protecting financial speculators from the consequences of their speculation, at the expense of retired people looking for steady income from bonds or CDs.

“protecting financial speculators from the consequences of their speculation, at the expense of retired people looking for steady income from bonds or CDs.”

if you look at it from the standpoint of someone who has been running a smoothly-ish operating ponzi scheme for several decades, this would seem like a reasonable thing to do,

it’s only when the original investors want their principle back that it becomes a problem. not so much for those running the ponzi, but for retired people and anyone looking for steady income from bonds or CDs. but, as they say, you can’t make an omelette without breaking some eggs…

FHA/VA/USDA bailouts are coming. Proposals all over the place but bottom line is all payments missed will be forgiven.

Soon enough this will be applicable to all mortgages, whether FHA or not.

No housing crash is going to happen.

Ok , I know what a front loaded bond fund is but I do not know what a front loaded QE is.

QE after the Financial Crisis was a fixed amount every month — and by today’s standards a small amount, but it kept going for years.

In this version of QE, the Fed printed $1.4 trillion in the first 2.5 weeks, averaging $110 billion per working day.

Over the past two weeks, this has been reduced to $50 billion a day… and in fact, if you figure in what is happened to MBS now (purchases are down to $10 billion a day), but which won’t show up on the balance sheet for weeks due to the lag in settling these trades, then the daily total is more like $40 billion.

This is precisely what the Fed spent the last two years saying: at the next crisis, they’ll front-load QE, and then taper it and end it, rather than let it drag out for years.

Here’s what I don’t understand: if it was pure jawboning that caused sharp spikes in the values of a number of junk bonds, then why would buyers not sell now, having digested this information? Confidence that the Fed WILL buy if they (again drop sharply)?

And, as others have mentioned, given the extra special opacity that was built in this time around, why should we assume that the official reports are accurate?

“given the extra special opacity that was built in this time around, why should we assume that the official reports are accurate?” Exacalacaly, as they say in Willy Wonka and The Chocolate Factory.

Tinky and timbers,

The opacity is about bank balance sheet disclosures. Not about the Fed. The Fed doesn’t want to hide QE, it wants to SHOW QE as part of its communication tools.

The Fed uses jawboning as its official tool. They don’t call it that. They call it “forward guidance” and “communication channels” and what not. That’s how the Fed accomplishes its goals. Jawboning is perhaps the single most important tool it has, and it has perfected it, and markets love it. It’s the common buy signal everyone wants to get.

BTW, no one, not even the Fed, can buy bonds or other securities secretly. These are electronic entries, and whoever buys them is known, and must be known because they’re receiving the interest payments. Same with stocks (dividend payments must reach the stockholder), etc. We live in an electronic world.

timbers – I take anything State Street says with a grain of salt – and keep my handbag locked up!

I’m not comprehending how FED jawboning could be bullish for gold? Seems like all hat and no cattle, more not QE, $2T but not $2T, it’s actually confusing.

Long-Term care is more expensive than heroin;

heroin is more expensive than religion.

Negative interest rates, negative risk premiums,

and helicopter money are pain relievers.

When your immune system is weak,

you get all kinds of viruses,

a wide variety, not just COVID-19.

The underlying problem is mental health,

homelessness, and street drugs.

Re stock market valuations- take a look at the chart of the Dow Gold ratio, when it falls to single figures then is the time to start planning what to buy, but wail until it hits 5 maybe 7, simples.

Did you just use your beer mug image to make the New York Fed Liquidity Swap graph?

Do you see any similarities? I don’t.

Just looked like the outline of a mug when I first scrolled down.

Been browsing here for the last couple years, rarely post, and wanted to thank you for demystifying the arcane world of finanace. I have really been able to maintain my wealth during the last couple years due to your insight. Cheers and God bless.

Speaking of mugs and graphs, would be neat to put some outrageous graphs on your mug. Six million unemployment graph comes to mind and jives well with the whole unemployment and drowining your sorrows theme. Sign me up for one if you make a few!

as long as we are on the topic of mugs, i think an “old bicycles” themed, kitten designed, mug just may be a thing to try out one of these days.

keep up the good work, wolf. i hope you are doing ok in these interesting times. i always smile when you talk about the fed buying old bicycles.

“Fed Chair Jerome Powell in a webcast on April 10 said that the Fed would pack away its emergency tools once “private markets and institutions are once again able to perform their vital functions of channeling credit and supporting economic growth.”

So sometime around 2120? Given how well things went when they even try to unload lightly their balance sheet last time and market threw a fit…good luck with that FED. You guys are the best

Yes. Just fancy talk and frankly, and out and out lie.

The Fed began it’s “Not QE” QE4 NOT in response to “private markets and institutions not being able to perform their vital functions of channeling credit and supporting economic growth” BUT because Mr Market thru a hissy fit and the stocks went down. Vital credit function and absolutely nothing to do with it.

Could it be that Fed (or rather Powell) is actually being a bit more sensible than we expected in our worst fears? Oh how I wish it is true.

I wonder why the many ocredit facilities are not being used (yet?). Maybe the internal Fed traders have been instructed not to bid on any junk bonds/ETFs (as an example) until the prices drop by X%? That would fit the theory that the main intent is to talk (jawbone as Wolf says) the debt markets but not actually intervene in any meaningful way (yet).

Good thing it is not Neil Kashkari that is running the Fed. With him he would have blown his entire wad already and created the worst bubble ever. So far, Powell has ignited an dangerous stock and bond rally, but it could be worse, and it looks like (fingers crossed) Fed is easing up on the reserves-printing pedal.

my worst fears are that they just authorized a treasury-backed, fed financed pile of dry powder for blackrock to leverage once that pennies on the dollar opportunity finally arrives.

If the not-yet-peer-reviewed Santa Clara County antibody prevalence study (*) turns out to be reasonably accurate, Fed/Powell is going to have to withdraw a LOT of credit “liquidity” come Monday.

The paper has been out since Tuesday but did not get much airplay until yesterday afternoon. The accuracy of the results are in question because the false positive rate of the antibody may be higher than estimated, and also there were potential problems that the selection of participants was not sufficiently random.

(*) https://www.medrxiv.org/content/10.1101/2020.04.14.20062463v1

As Nader suggests Powell is clearly under political pressure. The Fed is throwing political chum on the water. He has managed to distance himself at each and every critical juncture. He responded preemptively to trade war dislocations, and ignored the Covid crisis. He is a loyalist, not above letting the leadership call the shots and letting the chips fall where they may, while absolving himself. At the same time he allies himself with previous Feds, Yellen and Bernanke, which is dubious company while the great unwind proceeds. We haven’t had the 2009 moment yet, and looking at Powell, the lights are on, but nobody is home. The partisan divide widens, somebody has to take the side of the 99%. Trivial contributions are more likely to sow discord. Let them eat cake?

I’m sorry Wolf. I don’t understand the orientation of articles like this. So what if the Fed has cut back in recent weeks?

If things swoon again, they’ll just start buying again. What are you trying to say?

There is no “orientation.” I’m just telling you what the Fed does — now on a weekly basis. Before all this circus started back in September, I was telling you on a monthly basis.

1) Swap to Japan is swap to China.

2) Japan became a relay station transmitting dollars to China to swap

debt.

Any FRBNY $-swap line with any other central bank could do something similar, TBTF banks already have $-swap lines with many other country central banks/private banks so FRBNY is doing nothing new here that wasn’t already being done by the eurodollar market.

SPX weekly :

1) Jan 2018 high, is a resistance line, @ 2,872.87.

2) The midpoint between Mar/ Feb 2020 weekly (C) low [hi / lo] is 2,843.

3) If by the end of the week starting on 4/27, a (C) two weeks from today, the weekly (C) is above 2489 //

and by the end 5/4 week, three weeks from today, the (C) will be we are are probably going down.

4) Until then, in the next 3-4 weeks, a trading range.

5) SPX @ 2,843 & 2,873 are numbers to remember.

On a practical and personal note, I want to pull $100k out of an IRA to fix some liquidity issues under the Cares Act. One of my pension funds says they will have the CVD withdrawal forms available at the end of the month. Anyone know a quicker way to get some money out. “Autopilot” pension funds seem reluctant to let me access my own money.

Wolf said: ” But forget it, this was helicopter money for Wall Street and for asset holders – particular those with the riskiest bets – and for no one else.”

With the vast proponderance of the balance sheet expansion being through Treasury purchases, how does that reconcile with a bailout for Wall Street and asset holders?

This is a whole circuitous flow, not just one transaction. And each entity is just one element in it…

I sell the Fed my Treasuries that are now yielding near 0%, though I bought them when they were yielding 2.5%, and so now I make a big gain thanks to the Fed which forced down yields through its purchases, and I invest that cash in some junk bonds or stocks that the Fed said it would also buy, and so I help up drive those prices, and the junk bonds I already had in my portfolio suddenly jump in price by 40%, and the companies that I thought might have to go through Chapter 11 restructuring suddenly find the liquidity to borrow more and keep going and burning cash, and their bonds jump in price, and all this is owned by Wall Street and asset holders, and they’re dealing with each other and the Fed and the Fed’s newly printed money, and they’re driving up prices. Times 1 million. Wall Street banks paid record bonuses for 2009, the year of the bank bailouts, the unemployment crisis, the housing crisis, and mortgage crisis.

Thank you Professor Wolf. I am enlightened.

Wolf, can you site an example of an investor who would own treasuries, sell them, get the cash and then buy junk bonds?

Also, you pointed out a few months ago in one of your articles that the Toys R Us bonds were rated junk and traded at 98 cents on the dollar the day before they filed bankruptcy.

Can you explain to me how an investor could be so anti-risk that they’d be willing to buy US Treasuries and then turn right around and buy junk? This makes no sense.

Yes, hedge funds do it all the time. Highly leveraged deals that made a ton of money until the Treasury market went haywire a few weeks ago.

cb

Good question. Dots need to be connected there.

“..over the past two weeks, [the Fed] has cut its bailouts in half, and it has stopped lending new funds to its SPVs that were expected to buy all manner of securities…”

That’s because the Fed’s stock-price-reflation program begun when the holy DJIA threatened to break below the 20,000 mark has been highly successful – market rallied 20% at the same time over 20 million American workers were losing their jobs. As soon as the markets catch the next teeny whiff of the unholy price-discovery sniffles, you can be sure that the Fed will quickly resume the Ctrl-P-ing from its magical money-creation terminals over at Maiden Lane.

Amen but they will also act to bail out their cronies. Watch.

Speaking of currency swaps: I read on the Fed website somewhere that the swap exchange rate is generally the market rate of currency X (X per USD or X/USD) at the day of the swap. And it seems that the swaps tend to happen when X/USD (in the numerical sense, the number of X you get for 1 USD, a division) is a high number because the value of X is going down. Presumably because USD is (still) the most used (reserve) payment currency, flight to safety and all that.

I’m thinking this means that later, when the swap is undone, that Fed (or someone in the US) gets to make a profit?

Will the *traded* X/USD exchange rate that day be magnetically drawn to the swap exchange rate? Will X/USD, which may since have gone below the swap rate, suddenly rise to the swap rate? Somebody could be making a profit on this…but who?

Central Bank “CB-X” has to pay back the Fed (=CB-USD). They do that by reclaiming the USD from the CB-X client banks, who may then in turn need to get other USD credit on the open market? Or maybe not, maybe CB-X client banks have accumulated enough export payments from the US that they have no further need for the USD of the swap and can readily pay them back. I guess it depends on the strength of country-X exports.

Seems a bit complicated, but I wonder what *usually* happens?

Is the FED taking a pause to go into their sound proof chamber and release a primal scream?

Now at true zero rates, (with their low rate of support for high risk corporate bonds and near zero rates for govt debt), maybe now, they realize, they are the only bond buyer. Just like the ECB and BOJ found out; that for the first ZIRP $1 in, then they are all-in for trillions and trillions. But unlike, the patient Japanese citizens, or the desperate EU for a bailout at any cost, the USA public and the (private corporation) FED, have other perspectives.

“They” should be petrified. World wide.

Firstly, the magnitude of debt is staggering: a) Reported total USA debt is $70T since end of 2019 and now climbing by trillions. Or ~400% of GDP in reported govt and corporate and consumer debt. Then b) add in the crumbling $20T in GDP. Crumbling not just because of covid-19, but also from “their” demand crushing policies. And then c), add in the unfunded liabilities, (like pensions, social commitments, banker and corporate liabilities that are now but footnotes on their balance sheet). And then d), add in off book debt (banker & corporate). And then e) add in derivatives (?). It’s a staggering amount of debt for the private corporation (owned by the bankers), the FED, to willingly absorb. Maybe they should as that is their morale hazard; but so far they have captured taxpayer promised handouts for FED’s corporate funding losses. All in, at a guess, the FED could end up sucking up $90T; and the public losses could be tens of trillions; 20% could be $18T. And then world wide, the “reported debt” is $250T; (on ~$60T of GDP), plus the add-ons like the ones noted above. Staggering.

Secondly, so much for the argument that ZIRP would lower the USA dollar for international competitiveness and EM debt support.

Thirdly, then there is the political risk. The oligarchy is at risk of loosing (personal) control. With workers and voters at home, and some thinking about how pissed off they are, and how worried they are, about their personal and their families future. There is potential for political blow back; irrational or rational. Breaking a social contract is politically and economically expensive. This oligarchy said they were going to make American great again. They can not fail to deliver on that, when so many people are now at home worried about rent, food, health care, kids, and gamma.

l know some have suggested, a back to work order, is a way to solve this economic and financial issue. But like someone else here said, we really need to listen to the medical experts on this. Otherwise even more people will die; just ask denial Iran and China. That is why we want independent experts doing the best they can; and not just for health care, but for all areas too. However, more constructively, why is everything so yes-no binary in the USA, when there is a more humanitarian and moral solution. If corporations legally defined as “persons” can be bailed out, (FED backed for low rates and backed by the taxpayer for losses), then so can “real people”.

When we think outside the binary box, the real issue, is whether to ‘offer a deal and print’ for only corporations and bankers, or to also ‘offer a deal and print’ for main street too. And if we can get the FED and the bankers, the out of the way, then the cost to print, is now zero. That zero rate decision has already been made. The decision now is whether to support the public with the ZIRP and a deal. We all are going there anyways; as a “no ZRIP and no deal” for the public will cascade back at the bankers’ door anyways. So it is better to make a one time reset deal now. And make it at zero cost, by shoving the FED and bankers out of the way.

While here, for corporations, we should be taking deeply discounted major share positions, for bailouts, and sort them out later; what is their alternative; we should look at public bailouts like any other free market bailout buyer of last resort; didn’t someone say that the swamp needed a clean-out too.

For a controlled print, we need experts; independent and credentialed experts. Not the carpet baggers running the show now, who made this mess. And not most of the morons who are but wealth mangers for the wealthy, we call politicians, either.

This can be a one time debt jubilee reset; utilizing a two tiered rate structure (a zero rate and a realistic reset rate for new debt), a jubilee for both corporate (for share position) and public (paid as $???k per person), combined with a huge pile of new and stringent debt controls, and combined with a retraction of ‘their” GDP demand-crushing policies. But l am not confident this oligarchy; they certainly lack for pubic interest. And a reset is still painful. If done correctly it requires: a) Tough love on their indulged banks and corporations, (ie free market within a regulatory framework)(more shareholder rights); and tough love for consumers and government too. And B) a retraction of both their favorite pro-corporate-economic policies, and their negligent public-dis-interest policies; ( that got them & us into this mess, but that flooded the wealth from the bottom and middle to the top). The distortions are not just covid-19. There is a long list of policies, on many fronts, that have to be corrected to fix this mess. And we need a number of independent experts to assist in that; similarly: why would we hire the worse mechanic to fix our car?; hire an incompetent doctor to treat our kid?, hire the fox to look after the hen house?, or vote for greedy corporate wealth managers to run the place?.

IMO, solvable. But only with a rational and public-interest and fiduciary view.

Otherwise?

experts. that sounds like a plan, they’ve never done us wrong in the past. let’s all just obey.

Did you see any talking head on a financial show say…

GET OUT?

Nope.

Brilliant and well said!!

” maybe now, they realize, they are the only bond buyer. Just like the ECB and BOJ found out;”

Here are the interest rates, they say…. and now everybody play to those rules. NOPE!

It is TIME to ASK….are artificially low interest rates, rates below inflation, the cure or the CAUSE?

I think you confuse DJT with an oligarch. I disagree.

He is an interest rate hating, constantly leveraging individual who has a need for attention. No more.

Oligarchs are Soros and his lot.

The people who get the call when the ECB SNB or BOJ is about to cut rates…they are the oligarchs. DJT doesn’t know a LIBOR from a Fed Fund.

So buy calls or puts on HYG ??

Even if the Fed raises interest rates, corporate bonds will remain solid. If rates rise HY bond ratings by implication earn a better rating. If rates drop new issuance comes on line, just watch the spreads! (Treasury yields will never rise, the chase is on!) They have “revenue”.. JP swaps (T)reasury (P)aper for corporates, he knows. What lies ahead (at this rate) is the complete destruction of the US government finance system, replaced by the Corporate States of (Extended) America, a nation of rentiers, for rentiers and by rentiers. In the next pullback price makes a new low in SPY, but the low in HYG should hold.

Dear wolf

https://www.federalreserve.gov/releases/h41/current/

said that TS in increased 222,862 million but

https://fred.stlouisfed.org/graph/?graph_id=349387#0

FRED said that TS in increased 154,000 million

Could you explain this difference ?

Engin,

No, that’s not was the H.4.1 said. You looked in the wrong place. That $222,862 is under “Averages of daily figures” — so this compares the current balance on Wednesday to the average of the daily figures of the prior week, rather than to the Wednesday level of prior week (end of prior balance sheet).

You need to go down the H.4.1 to section 4. “Consolidated Statement of Condition of All Federal Reserve Banks,” which gives you the Wednesday-to-Wednesday figure = 154,472 million.

Dear wolf

Thank you

Seems like record low, 4000 year lows in interest rates…before the crash…are not the solution.

Any one ask……”Are they the PROBLEM?”

Wolf,

As always thanks for keeping score. Always appreciated.

Note that since the Fed tapered Treasury purchases from $75 B per day to “just” $15 B per day, reverse repo borrowings have collapsed. Guess it’s not worth the trouble for the banks at such puny daily purchase levels, even at zero % interest.