The ECB promised “to monitor markets closely.” Then it came out with a new bond buying binge.

By Nick Corbishley, for WOLF STREET:

Bank stocks in Europe plumbed fresh mutli-decade lows despite the release of a hurriedly improvised one-paragraph announcement by the ECB pledging to do just about whatever it could take to keep the banking system in tact. The ECB will continue “to monitor markets closely”, the message read, and is “ready to adjust all of its measures, as appropriate, should this be needed to safeguard liquidity conditions in the banking system.” In other words, the ECB is willing to throw what remains of the kitchen sink at the problem.

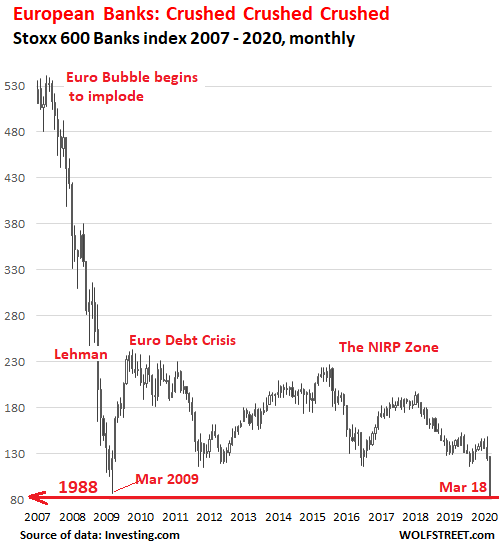

The message may have been intended to reassure investors, calm market jitters, and stop the sell-off of sovereign bonds and bank shares but if anything, it had the opposite effect. The Stoxx 600 Banks index, which covers major European banks, fell 3.7% to close at 83, below even the multi-decade low of 87 in March 2009, at the bottom of the first Financial Crisis this century. Today’s close was the lowest since February 1988, during the sell-off that followed Black Monday in October 1987. The index has collapsed by 85% since its peak in May 2007, after having quadrupled over the preceding 12 years:

The almost vertical collapse of those shares over the past four weeks is but the latest episode in a 13-year story of decline. The Stoxx 600 bank index has slumped by 85% since its peak in May 2007,

But what is the ECB going to do to rescue bank shareholders? Not much. The ECB is primarily concerned with keeping the Eurozone duct-taped together. Unlike the Fed, whose 12 regional Federal Reserve Banks are owned by the banks in their districts, and to whom bank stocks are therefore hugely important, the ECB couldn’t care less about bank stocks, as long as the banks themselves don’t collapse. So it has thrown just about everything it has at the problem of keeping the Eurozone in tact, including conjuring up €4.7 trillion ($5.2 trillion) of fresh money, and pushing its policy rates and many bond yields into the negative, but with largely undesirable consequences for banks and their shares.

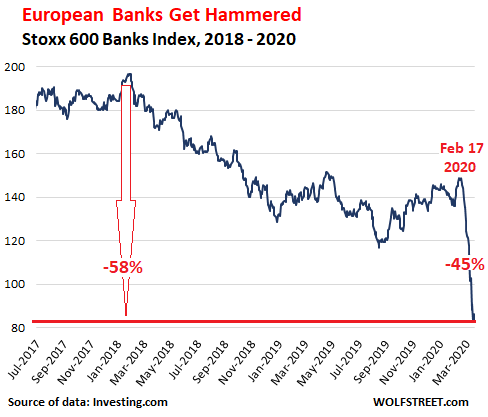

On top of it comes the impact of the coronavirus. The Stoxx 600 Banks Index has plunged 45% since February 17, going to heck in a (nearly) straight line, and is down by 58% since January 2018:

By all appearances, we are headed into yet another full-blown financial crisis, triggered not by the banks this time but by the response to the coronavirus, which is now reverberating throughout the system and hitting the already weak banks. So far, neither the Fed nor the ECB have managed to get a grip on this new crisis, which is moving far faster than the last one.

Bank bonds are selling off, particularly the “senior non-preferred bonds,” a new creature road-tested three years ago by France’s biggest bank. These bonds lured many investors with the promise of a slightly positive yield. It’s “bail-in-able” debt. In return for the tiniest of returns (say, a yield of 2%), you basically get to hold debt that can be turned into worthless equity or be cancelled the moment a bank begins to wobble. Not surprisingly, investors are trying to offload them as quickly as they can, reports the FT.

Today, the ECB, in a bid to reassure investors, said that it is directly intervening in sovereign debt markets with a €750 billion bond-buying binge for the rest of 2020, including Greek bonds for the first time, and Italian bonds, whose yields have spiked sharply in recent days. Italian bonds are held in huge numbers by banks all over the continent, particularly Italian and French ones. The more they fall, the weaker the banks’ capital buffers get. Despite the ECB’s intervention, the yield on the ten-year bond still rose by over 5% today to 2.43%, its highest level since last last June.

The ECB also walked back prior remarks by Austrian central-bank governor Robert Holzmann that suggested that the ECB would take little further action beyond cutting interest rates even further into negative territory, which has been decimating banks’ interest margins for years, and providing emergency liquidity lines for the same banks that are being slowly killed by the negative interest rates.

No publicly listed lender, big or small, has been spared by the latest rout. Below, in descending order, is a list of the worst-hit large publicly traded banks in Europe. The first percentage is the amount by which the bank’s shares have fallen since February 17, when the Coronavirus began spreading like wildfire through northern Italy, causing everything to go to heck. In parentheses is the amount by which they have fallen since Jan 1, 2018. We’ll leave it up to your imagination what the percent-drop from the peak in May 2007 would look like:

- Société Générale (France): -56% (-67%)

- ING (Netherlands): -54% (-73%)

- Credit Agricole (France): -53% (-57%)

- Santander (Spain): -52% (-64%)

- Barclays (UK): -53% (59%)

- BNP Paribas (France): -52% (-58%)

- Unicredit (Italy): -51% (-57%)

- Deutsche Bank (Germany) -50% (-68%)

- Credit Suisse (Switzerland): -49% (-62%)

- RBS (UK, majority state-owned): -39% (-54%)

These ten banks are Europe’s financial flag carriers. Though some of them have been shrinking in size, complexity, and risk, including Deutsche Bank. Nonetheless, they are still recognized as global systemically important banks (G-SIBs) due to the size, scope and inter-connectedness of their assets. If any one of them collapses it will set off a shock wave throughout the global financial system.

Many of Europe’s second-tier banks, whose collapse would have significant repercussions at the regional level, at the very least, have also seen their shares plunge in the past four weeks. Spain’s BBVA is down 52% (and 64% since Jan 2018), Germany’s Commerzbank, in which the state still holds a big share from the last bailout, is down 54% (and -75%). Italy’s Intesa Sanpaolo is down 44% (and 50%).

While the recent share collapse of seventh and eighth-placed Unicredit and Deutsche Bank has been slightly less pronounced than many of the region’s other large banks, their overall decline since the global financial crisis has been far greater than any of their other peers. Deutsche Bank has lost more than 95% of its market value since 2007 and Unicredit more than 98%. By Nick Corbishley, for WOLF STREET.

Most importantly, we have our health (touch wood) and each other. Read... Welcome to Dystopia: My Life Under Lockdown in Spain

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The hits just keep coming, don’t they? I will not even try to imagine what Italy’s economy or banks will look like after this storm has passed. Here in Belgium – already burdened with an impressive national debt – we just entered a lockdown period. How long can an economic system survive under these circumstances, I wonder?

Trumponomics in action

How many billions of the Fed QE is going to bailout foreign banks?

Lots of articles hint at it – but no real data.

Failing banks and modern-day Hoovervilles

remind me of 1930’s America — Grapes of Wrath.

The similarities are amazing.

The world is in a deep slumber,

ready to be awakened.

That’s why it’s a good time to start thinking about what comes next.

Many of us want something quite different from what we have, but we don’t seem to have defined what this “else” actually is.

This is an ideal moment for the imaginative-and-practical – I know you’re out there – to take out a sheet of paper and sketch out what this next economy might be.

Good use of lock-down time.

How about a zero rate inflation policy and let Mr. Market guide the market.

Tom Pfotzer:

Easy one…

A system that does not allow “free market capitalism” to ravage society.

A system of rules.

A legal system that works for all and that backs up those rules. That means a legal one that does not have multiple levels of “justice”.

A philosophy of not raping the environment on this crust of dirt hurtling thru space to wherever!

A system where “greed” is not good.

A system that embraces “community” versus “individualism” (or outright narcissism)

A system where the 7 deadly sins are corralled.

Political term limits and also the same for any kind of “Supreme Court”.

I’m sure others can add to this list but thanks for asking.

Simple.

Please start with paying ”fair” interest rates to retail savers, similar to what allowed my grandmother to live fairly comfortably for the last 30 or so years of her life without so called social security or any other help from the taxpayer/working folks. (She had worked many years as a public school teacher, and was a very thrifty Scot, but she had a new car when she wanted one.)

And, to be sure, many other basic, repeat, basic concepts of fairness SO very different than the continuing and worsening crony/corrupt capitalism of the last few decades.

NZ Government is urging everyone to come home ….

Expecting a halt to all flights as airlines are ‘no longer economically viable’

i suspect that all international flights will be halted shortly.

https://www.stuff.co.nz/national/health/coronavirus/120404655/coronavirus-ministry-of-health-to-provide-update

This is the end, beautiful friend

This is the end, my only friend

The end of our elaborate plans

The end of ev’rything that stands

The end

I hate to do this but – I TOLD YOU SO :)

Seems you’re slightly confused. An airline shutting down temporarily is not “the end” of anything, not of the airline, and not of the world.

The beginning of the end then?

Every airliner will be flying just about empty on international routes now.

NZ just shut out all non passport holders and they issued a warning today stating ‘we urge all of our citizens to immediately return home — airlines around the world are not running viable businesses (interpret that as there will be no international flights soon so you either come back now your you do not come back at all)

Air NZ had already slashed 85% of their flights — today’s announcement surely means Air NZ will halt their remaining international flights.

Virgin Australia has also halted all international flights.

Millions upon millions upon millions are being laid off across the world.

The Central Banks are pushing on multiple strings now — you cannot bail out the entire world.

I am simply amazed that people are oblivious to what is playing out before your very eyes.

“The beginning of the end then?”

yes, of the bull market and of the Everything Bubble. Don’t transfer what’s happening in the financial market to society at large. We’re in a recession, and recessions are routine. If the shutdown last more than a couple of weeks, we’re going to be in a deep recession, but even deep recessions end, and life goes on. So get off this “everyone dies” them that you love so much.

I would be utterly, and pleasantly, surprised if the lockdown did not last a couple of months.

Some don’t understand that their suffering is just beginning.

And Lufthansa circles the drain now too:

Elsewhere, Lufthansa Group said on Thursday it would shrink its flight schedules to levels not seen since 1955.

The German company will also ground 700 of 763 aircraft.

Stay tuned as the global airline industry implodes.

Hotels to follow?

What about the auto industry?

I don’t think the panic buying that is emptying shelves around the world will apply to autos. Nobody needs a new car when they are planning for a doomsday scenario.

I don’t recall anything remotely similar happening in 1987 or during the dotcom bust or the GFC.

To put it mildly, we are in uncharted waters — with reefs everywhere.

I am a small importer in NZ, air freight is still coming in but delayed about a week and the cost had doubled over night. Sea freight out of the US is 12wks backed up as there are no containers (not sure why this would be).

All the empty containers ended up in China.

NZ strikes me as a uniquely unsuitable place to ride out the pandemic. Cutoff from the world, supplies will run low, prices will skyrocket.

First of all, they have plenty of food on the hoof and growing on only grass, so plenty of ”reserve” food, much like USA and many other countries.

Not been there, but had some really good friends from there in the East Bay, and, if they are any indication, the Kiwis will pull together to make sure people get what is needed to survive.

Much more likely to be extended chaos in USA due to lack of community these days, IMO THE most important aspect of this event and all such events, though I must admit that I grew up in a different era when I saw folks sharing (and partying) together to deal with extreme events, no matter what their socio economic status.

What is the counter-party risk for US banks? Is this a cascade of Lehman Brother type failures across the continent?

I can see the private jets flying over our house on a regular basis as they approach the airport (we live just outside of Queenstown on a large rural property).

Half of Silicon Valley is in town by now I bet.

That would make about about 2 million folks. I was in Queenstown. Beautiful place, but small, so you’d notice 2 million new people for sure.

As mentioned, there are not 2M people in the Valley with private jet money.

I doubt there are even 200.

But now you changed the definition from “half of Silicon Valley” to “people in the Valley with private jet money.” And you might still have to changed it to “billionaires who started EV companies” or something like that.

“Beautiful place, but small, so you’d notice 2 million new people for sure.”

Ah but you’d notice silicon valley rats fleeing, if they each had $100 million in their pockets ……

As bad as the European bank stocks have fallen, it is nothing compared to the drop for senior gold mining stocks. I would be happy if they had only fallen 50%!

Why am I not surprised that as the EU, UK, Japan, China and US all went farther and farther in not-fixing the problem, the worse it got?

Who’s the new Credit-Anstalt?

“In May 1931, a Viennese bank named Credit-Anstalt failed. Founded by the famous Rothschild banking family in 1855, Credit-Anstalt was one of the most important financial institutions of the Austro-Hungarian Empire, and its failure came as a shock because it was considered impregnable. The bank not only made loans; it acquired ownership stakes in all kinds of companies throughout the sprawling empire, from sugar producers to the new automobile makers. Its headquarters city, Vienna, was a place of wealth and splendor, famous for its opera, balls, chocolate, psychoanalysis, and the extravagant architecture of the Ringstrasse. The fall of Credit-Anstalt—and the dominoes it helped topple across Continental Europe and the confidence it shredded as far away as the U.S.—wasn’t just the failure of a bank: It was a failure of civilization.”

From same article (from 2011 – Bloomberg – I won’t post link here):

“Once again, Europe’s banking system, and by extension its social fabric, is threatened by bad loans.”

The Austrian-Hungarian Empire (sometimes called the Dual Monarchy) died and was completely broken apart/dissolved by 1920.

Read a novel called, “The Winter Soldier” recently that gave what certainly seemed to be a first hand ”historical fiction” account of Vienna during and right after WW1. So, if in fact it had been rebuilt to the standards of excellence that existed prior to that awful war, IMO there would have remained in 31 a terrible deficit of many tangible and, perhaps even more intangibles such as confidence underlying any appearances.

Certainly part of the basis for WW2, no matter how much the Austrians wanted to assign all the blame onto the nazi and other such parties.

That parallels exist in the world today goes right to the heart of this current crisis; I hope and pray it does not lead to similar war or wars.

VintageVnVet:

“Winter Soldier”:

Our current read for our book club here in the Sierras……

Why is banking still in a private enterprise after 2008? I get it that everyone luvs capitalism etc. But lets get real, a private sector bank is merely a creditor tax on the general population at this point. Creditors’ rights appear to be superior to the civil society’s right to coexist as a whole.

Was the Greek bailout really Greek? What about Argentina?

Whom does the World Bank and IMF serve?

Asking for a friend…

Sorry, what’s capitalist about the banking sector?

Takes other people’s money to spend it on impressive high-rises, to pay executives and management handsomely and to make more money with existing money.

When they’re loaning money to keep dying businesses afloat there’s nothing capitalist about it. Many banks should’ve died long ago.

It is my understanding the IMF loan history is all about softening up the victim by imposing directives, such as Greece selling off vital Govt assets to remain in compliance. It often seems to be that helping hand with a, “I’ll pull you out of the fire right after you hand me your wallet with your other hand. Carefully”. And then a mysterious purchaser arrives for the now for sale airport, ferry service, whatever.

Tony Soprano in action.

It’ll take some real pitchforks to stop the future wealth transfers from unfolding. Queensland? NZ havens? There must be no hidden safe havens for proven bandits, imho.

give me a second, so i can find my tiny violin. i think we need a song to perk up our spirits.

I suggest “Brother, can you spare a dime?”

I wonder what’s bazooka #3.

NIRP in the US?

I wonder when will people learn.

Got to get to QE10 first.

I’m a small business owner of many years.

10 years ago I lost A business in relation to the horse ranch industry. Most of the small business owners here in Southern California that I see all around where I live even the ones that are successful or not gonna be able to last much more than a month or two. I’ve told a few of my friends to immediately go to the landlord and negotiate a decrease in the rent and I do everything they possibly can. But in reality I know having been a small businessman for many years that most people eat what they kill. It is a contradiction to tell people to stay home and at the same time have a small business that needs people. The fools that set us up with China have made all their money and now I’m happy to see that we’re going to have to decouple from China. God help us all

Geno,

My nephew and all his friends were just laid off, yesterday. 5 hour wait time to talk with an emergency unemployment officer.

I have friends with small businesses, one owns a highway restaurant and pub. She is selling some takeout. A local auto parts store takes orders from mechanics, you call them when you arrive at location, they unlock the door and set the parts outside on the sidewalk. This is what, day 3 after the dire actions were implemented?

CA governor Newsom (I’m a non partisan voter and couldn’t care less about either major political party) sowed mass confusion up and down the Bay Area with his “6 county shelter in place” order that has fallen very heavily on the small business in the area. I do believe the situation is pretty serious. But not believe that tens of thousands of workers will be laid off soon is to be day-dreaming. Prepare for an onslaught of the unemployed.

Tesla is trying to give the finger to the gov. but in the end they may have to succumb also. There alone is about 10,000 jobs.

To add to the confusion two days ago the Ca news was that (from Newsom) the public schools will probably be closed for the rest of the year!

Tonight on the news the talk for so many (at least from the Sac. news channels) is that “….schools may be closed until the middle of April!)

Who writes for these guys???????

Maybe we shouldn’t have built a Ponzi economy, that could evaporate 30% in a few weeks, in the first place?

If anyone runs out of toilet paper you can probably find some of those 40 billion WeWork stock certificates lying around.

The ECB can’t help itself, how could it help commercial banks.

You should get yourself a Much Younger Wife like some of the other posters around here.

He who holds the goods win. What will you do with fiat money if you have nothing to eat.

Randy,

It’s kind of nice to have someone at home during this period of isolation. Just sayin’. My wife and I have lunch together and check in, we keep our spirits up and look after each other. I can’t imagine a life without her. Synergy…the sum is greater than the parts, even if you add in some of your bon…… er, meant to say, headaches.

The government can buy beyond warrants and own everything. Q4ever.

Hopefully this event will get everyone to save up some money (3-6 months worth of pay) in the future for an event like this. Fortunately my job is needed at my company, but I am guilty of not saving also. My only saving grace is I have enough credit to get though this if needed.

Savings accounts were opened for each kid by the teacher in our classroom and we were encouraged to bring .25¢ to deposit each week if at all possible. It was all taken to the bank by the principal. This was in the 40’s following WW2. Some kid saved up $12 for the year and we were all green with envy and admiration. I think that was in 3d grade. Kids were taught to save everything they could. Now…I doubt anybody saves, anything.

Wait till you get old and retire. Without my savings I couldn’t pay all my utility bills and buy food, let alone luxury items. I no longer have a cell…or a car. This would be a nightmare for most younger people.

Hey John,

We appear to be similar age, and I must disagree about at least some young folks today not saving as you and I have done to our long term benefit.

I know of several next gen family in late 30/early 40 age group who might very well ”retire” if they chose to do so, which, of course, they do not, yet. Majority will likely retire in their 50s. Each of them are in what are being called ”essential” work or public sectors.

Some others in that cohort of cousins are not at all in good shape, but are younger and still learning; all but one are good workers, and in spite of their spendiferous habits, IMO will learn from this event, maybe even learning what it feels like not to eat for a couple of days at a time, as I did in 68, when I had to quit driving a cab around LA and calculated that I could make it to my next paycheck from new job if I didn’t eat for 10 days. (Had to stay in bed the last 3 days, but it was an interesting experience and gave me some likely much needed empathy.)

Nick / Wolf – serious question, given this point “The Stoxx 600 Banks Index has plunged 45% since February 17” and the impressive league table of losses by named banks, are they not all insolvent? Seems to me that losing half – give or take a little soupcon here or there – of your capital structure and without reducing leverage and outstanding would not not cut close to the buffer and top end of Tier 1 capital but slice into it like a hatchet.

If they’re insolvent, then as we used to say back in GFC days, “you can’t fix a solvency problem by hosing liquidity at it”. So what’s the ECB actually capable of doing in the current climate?

C