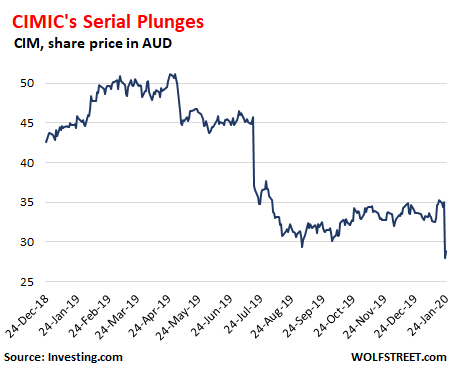

Shares plunged 20% on the spot, and are down 44% in nine months.

By Nick Corbishley, for WOLF STREET:

The shares of CIMIC, Australia’s largest construction company, plunged 20% on Thursday to a four-year low, wiping AU$2.2 billion (US$1.5 billion) off its market value, following news that the company was abandoning its Middle Eastern operations with the sale of its stake in BIC Contracting (BICC). The firm expects to suffer a AU$1.8 billion ($1.23 billion) charge-off after failing to recover debts owed for projects built (or in some cases, barely built at all) at the tail end of Dubai’s property bubble.

CIMIC’s stock has plunged 44% since April, when the Hong Kong-based research group, GMT, had released a report that accused the company of using reverse factoring agreements with banks and financial institutions to create the illusion of cash flow, reduce the appearance of debt, and lower its leverage ratios:

CIMIC (formerly known as Leighton Holdings before being acquired by Spain’s Grupo ACS) builds many of Australia’s biggest infrastructure projects, including Melbourne’s $6.7 billion West Gate Tunnel and Sydney’s Metro City. It is also the world’s largest contract miner. The company is majority owned by German construction giant Hochtief, which itself is majority owned by ACS, the world’s seventh largest construction and services company (by sales), following its acquisition of the German firm in 2011.

The shares of both Hochtief and ACS also plunged on Thursday, by 8% and 5% respectively, and are now down 24% and 21% from their 2019 highs.

From 2005 through 2007, CIMIC’s shares soared from around AU$9 to a historic high of AU$58. This was the period leading up to most of the company’s investments in Dubai that would end up costing it billions of dollars in losses and write-downs.

CIMIC’s parent, ACS announced it will book a €400 million charge. For its part, CIMIC said it will cancel its final dividend for 2019, which is likely to further enrage shareholders, and it anticipates spending around AU$700 million ($470 million) in 2020 on financial guarantees of liabilities associated with BIC Contracting to facilitate the sale of its stake in it.

CIMIC’s disastrous Arabian adventure began in 2007 when it entered a joint venture with Dubai’s Al Habtoor Group, which came to be known as Al Habtoor Leighton. Like many other global businesses and investors, the Australian company had hoped to tap the United Arab Emirates’ booming construction market, but the timing could not have been worse: by 2009, the boom had turned to bust and Dubai had little choice but to ask its more conservative, richer neighbor, Abu Dhabi, for a $20 billion handout.

By that time CIMIC — then called Leighton — had shelled out AU$870 million for a 45% stake in the Al Habtoor’s building arm, Al Habtoor Engineering, which had some US$4.4 billion of total work in hand with predicted earnings of US$2.75 billion for 2007-2008. Those projects included luxury hotels such as Burj Al Arab and Kempinski Hotel & Residences Palm Jumeirah, a 73-story residential skyscraper called the Dubai Pearl and the St. Regis Saadiyat Island Resort, in Abu Dhabi.

When the Global Financial Crisis struck, property prices in Dubai and other parts of the Emirates plummeted and more than half of the projects in the country were cancelled, including many of the projects CIMIC had hoped — and paid over the odds — to participate in. The hugely ambitious Dubai Pearl development, for example, has stalled since 2009 and is barely off the ground. Even today, Dubai is blighted by a massive housing surplus and property prices have failed to come even close to recovering their absurdly inflated pre-crisis levels.

For CIMIC, the pain has merely grown over time. Between 2010 and 2012, the company was forced to take AU$2 billion in write downs. In 2012, its former chairman Stephen Johns told the Australian Financial Review (AFR) that he rued the day the company had ever entered the venture. “With hindsight, no, we’re not happy with [Al Habtoor Leighton], we should never have gone into it,” he said.

The partnership came to an acrimonious end in 2016, with Al Habtoor Group exiting the venture just weeks after the arrest by Dubai police of the CEO and managing director of Habtoor Leighton Group (HLG), José Antonio López-Monís, who was subsequently released without charge. CIMIC’s new Spanish owners continued to try and recover the money CIMIC had frittered away on its Arabian dream, but to no avail.

Today, it officially threw in the towel. One former employee said that ACS had tried to “kick the can down the road for as long as they could” but have ultimately been forced to accept that CIMIC will never recover its losses.

CIMIC — which has been dogged by opaque finances — insists it has enough money in its cash and loans to meet its obligations, but not everyone agrees.

In its report on April 30 2019, GMT Research alleged that CIMIC began minimizing the impact of its losses from the BICC joint venture in 2018, probably even as those losses grew significantly. This avoidance of JV losses, coupled with “aggressive revenue recognition and acquisition accounting,” had enabled the firm to inflate its profits by around 100% over the previous two years, according to GMT’s estimates.

In 2016, Morgan Stanley raised questions about the apparently irreconcilable figures the company was presenting for its operating cash flow. “Contrary to CIMIC’s comments at the first quarter that there was a a 28.5% improvement in operating cash flow, our assessment of Hochtief’s accounts implied that operating cash for Asia Pacific (which largely consists of CIMIC’s activities) actually deteriorated around 19% year on year,” said Morgan Stanley analyst Nicholas Robison. By Nick Corbishley, for WOLF STREET.

Brick & Mortar melts down on mall owners in the UK. So “repurpose” malls into housing? Read… What to Do with Malls? Teetering UK Mall Giant Intu Asks Investors for £1 Billion. Shares Drop to Near-Nothing

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It was as if thousands of Wolf Street readers suddenly shrugged their shoulders and cried out, “…meh, we could have told you… this will end in tears…”

One of these days, fear will finally overtake greed. (apologies for the tortured Obi wan quote too)

Who will be buying all these distressed debt?

someone with access to cheap credit?

The Bank of Australia would be my guess

someone with access to a printer

Smart meet Dumb!

CIMIC debt is not “distressed” for the simple reason nobody outside the upper echelons of the company has a firm grasp on the company’s finances. That includes regulators, auditors and shareholders.

A company that turns a 19% cashflow loss on their main market in a 28% cash flow increase overall should be immediately called to task by shareholders, and given CIMIC shares have been halved in price in less than a year this is likely to happen.

Given construction and real estate are Australia’s official religion it’s likely regulators will turn the other way, at least as long as they can. But if CIMIC has cooked the books as much as it seems they’ll have to act, for no other reason if left unchecked this thing will blow into their faces at the worst possible moment.

But, again, the first watchmen should be the shareholders since, well, they own the company. But given shareholders tend to think of “their” company in the same way as frat boys renting a car for spring break with their parents’ credit cards backing it this is unlikely to happen.

MC01-great analogy vis shareholders! Applies to the citizenry of any country with the right to vote, as well…

May we all find a better day.

And work on the west gate tunnel in Melbourne has ceased as who will pay for disposal of contaminated soil hasn’t been resolved. Guess CIMIC is not able to, there goes the State’s economy and government if the project is cancelled, and there goes the State’s credit rating if it picks up the tab.

My question is how the hell did these geniuses not do adequate soil testing before they started. All around Melbourne were factories of all types and they were “leaking” all manner of things into the ground for almost a century. There were no regulations then. All this is well known. Many inner-city backyards are contaminated with lead, mercury and other heavy metals. So was this a case where the bidder just put in the lowest quote and hoped for the best. Of course, the Victorian govt loves to keep various “activities” away from public scrutiny. This is not the only project with massive cost overruns. I remember the disastrous Myki (transport card) project, the software of which blew out by billions. Then there was the (electricity) “smart meter” debacle where the Auditor General said that there was absolutely no benefit (only cost) to the (overpriced) electricity customers. That was also billions. There is also the older Burnley Tunnel project, which was plagued by lots of problems during construction, where lots of freshwater needs to be pumped in daily to stabilize the geology around the tunnel. There is also the current rail crossing removal (elevated train lines) project which is massive. So the Victorian budget is stretched and the state cannot afford to absorb yet more billions in losses. This is why there is currently a court case to determine who will pay. In the mean time, hundreds have lost their tunneling jobs. All hail the “efficiency” of politicians the world over!

It would be unreasonable not to expect problems when embarking on huge infrastructure projects. Victoria’s infrastructure spending, is a saint to our economy. The level train crossings have been rolled out very quickly and to an outstanding quality. (Even my Father, a Conservative voting engineer compliments them regularly)

The State of Victoria is just another Province of China. It to may have to be quarantined from the rest of Oz given its economic S-bend adventures. MelDanistan as we call Melbourne downunder is a pro-leftist utopia lead by a Marxist addict. One good thing about Victoria, it can cure constipation.

Well, Will all that needs to be said is it take a Genius to know a Genius!

If you think more Geological Tests can meekly solve this problem, you are NOT the GENIUS, your pen suggests!

We all know there are massive quantities of “Contaminated Soil” not only in Melbourne, but Globally!

The QUESTION being asked here is WHO IS RESPONSIBLE for it, and WHAT TO DO WITH IT?

Wonder if this outfit wasn’t on the hook for the fire at the eponymous Torch Tower and any other skyscrapers whose cladding are prone to burst into flames?uu

In this vein I wonder how long before some of China’s ‘Belt and Road’ projects end up in default , or worse, repudiation. Does China really believe sovereign nations are going to turn over their ports, railroads and other infrastructure just to satisfy Chinese creditors?

Why not. Ownership is not control and Chinese loans are s(lightly) less oderous than those of the IMF

I doubt China would agree. We pay your laundry, we wear your clothes when we choose. We own. Master, servant arrangement.

The Hambantota port in Sri Lanka was not confiscated by China over unpaid debt. The story is much much more complicated than that and likely to have far more to do with old fashioned corruption than some dastardly scheme by China to “take over the world”.

Hambantota was financed by a 6.45% loan from a consortium of Chinese investors. This alone should raise some alarm because the World Bank and the Asia Development Bank finance that kind of projects below 3% and the latter give extremely generous grace periods for repayments.

Hambantota was not merely “handed over” to China: the Hong Kong-based China Merchants Group paid the Sri Lanka government $1.5 billion in cash for an 85% stake in the port. The Sri Lanka government said the cash was needed to avoid “defaulting on foreign debt” but never gave any details on which debt issues were at risk of default. Fascinating.

The issue is not merely extremely complicated by the dynamics of Sri Lanka politics, but also by the copious amounts of disinformation disseminated by the US and Indian media, no doubt under orders from the respective governments.

Both countries consider the Indian Ocean their own backyard pool and completely freaked out at the idea of Hambantota becoming majority-owned by a Chinese SOE. Scare pieces hinted at a long string of catastrophic consequences, from locals being fired to be replaced by Chinese nationals to Hambantota being filled with PLA aircraft carriers and marines. So far nothing of this has happened, albeit the Sri Lanka government has proven unable or more likely unwilling to provide full financial details of the deal. Again, fascinating.

I strongly suspect the present climate of “China taking over the world” is nothing more than a modern day rendition of the Yellow Peril, albeit Fu Manchu is a far more suitable antagonist than Xi Jinping.

China does want to take over the world. The problem is they are just a paper dragon. President Xi along with his most direct followers imagine Xi as a Stalin like figure who will turn China into a superpower. The problem, everything Xi has done since he got in has backfired; the latest thing, possibly allowing a global pandemic to happen. Xi = Kim Jong Un.

The trick is if you let China build a port you cannot run, they take it, and then they’ll build something else in your country. Corrupt officials love it. Eventually though, if China’s power begins to wane, those countries could just nationalize everything.

Fiat money + FED = crony capitalism

“Ever since 1791, when Alexander Hamilton got the Federal government to take over state debts, which his cronies had bought for pennies, and then when he got the Federal government to authorize a monopoly for a privately owned central bank, the Bank of the United States, the real Mob has been plucking the feathers of the public.

The goons are Congress and the enforcers in the executive branch. The victims are taxpayers and investors who think the goons represent them. The Mob is the corporate system.”

“Government and business should be “one big happy family.” This was Henry Clay’s American System.

the basis of what is called the government-business alliance. In early modern European history, this was called mercantilism. In 19th-cenrtury America before 1865, this was called the American System. In the mid-1930s, it was called the New Deal. It was called fascism in Italy.”

It is same system in Australia.

excellent post

“using reverse factoring agreements with banks and financial institutions to create the illusion of cash flow, reduce the appearance of debt, and lower its leverage ratios”

Who the hell do they think they are…Greece?

Actually, this is exactly the kind of financial f*ckery-pokery that *can* cause “sudden stops” in the otherwise inviolate corporate debt rollover market (which habitually re-finances hundreds of billions each year, regardless of how crappy the macroeconomy or the corporate financials.)

Creditors are happy to help corps deceive retail shareholders but once the corps start lying across various creditor classes…the jig is up and credit suppliers as a class pull the plug.

Also, the law in UAE is feudal. If a deal goes bad with someone in power or connected to royal family, your best bet is to flee the country.

Hochtief used to be the envy of the German construction sector. Not without its (many) bribery scandals, that comes with the industry, but very good at all things construction. A pity to witness the decline of Hochtief since the takeover by ACS.

When the oil recedes one can see who has been swimming naked. This story needs to be seen also in connection with the recent wave of bankruptcies in Texas.

It’s called capitalism the end of an era mr. Putin has $150 billion in spending the West has no money looks like capitalism has failed

There have been quite a few Australian construction giants collapse, the industry is incredibly corrupt in Australia.