Those counting on the Fed’s endless “Not-QE” or whatever to inflate the market might be disappointed.

By Wolf Richter for WOLF STREET.

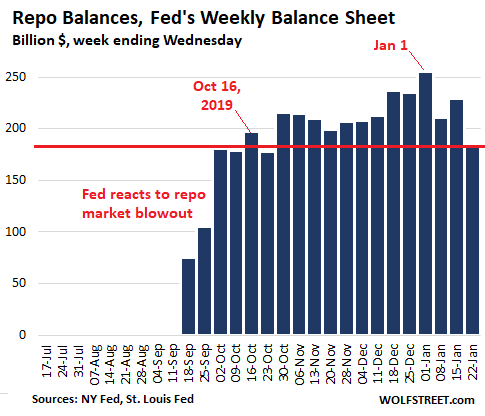

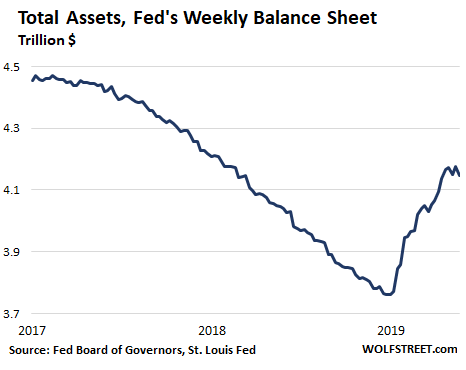

The Fed had doused the market with $410 billion in liquidity between September and January 1 through its repo operations and its T-bill purchases. Market hype had expected this blistering pace of money-printing to continue, but wait… While T-bill purchases continue, the repos on the Fed’s balance sheet are getting unwound, its mortgage-backed securities (MBS) continue to fall, and total assets on its balance sheet fell to the lowest level since mid-December.

Repos drop.

Under these repurchase agreements, the Fed offers to buy Treasury securities, MBS, and agency securities from counterparties with an agreement to sell those securities back to the counterparties at a set price on a specific date, such as the next day (overnight repos) or in 14 days or some other period (term repos). When a repurchase agreement matures, the Fed takes back the money it had handed out and returns the securities to the counterparties. This zeros out that particular repo on the Fed’s balance sheet.

When the Fed buys securities under a repurchase agreement, the amount it pays adds liquidity to the market. When that repo unwinds, and the Fed gets its cash back and returns the securities, it drains this liquidity from the market.

Every day, old repos unwind. And every day, the Fed offers new repos. This is a constant in-and-out. The balance changes every day, but it has been on an uneven decline since the peak on January 1.

The total amount of repos on the Fed’s weekly balance sheet as of January 22, released this afternoon, has now fallen by $70 billion from the peak on January 1 ($256 billion), to $186 billion. This is below where it had first been on October 16:

The $43-billion drop in repos over the past seven days was largely due to a 32-day $50-billion repo, dating from December 16, that unwound on January 17. It was not replaced by another 30-day repo, and there are no more 30-day repos on the Fed’s repo schedule or balance sheet.

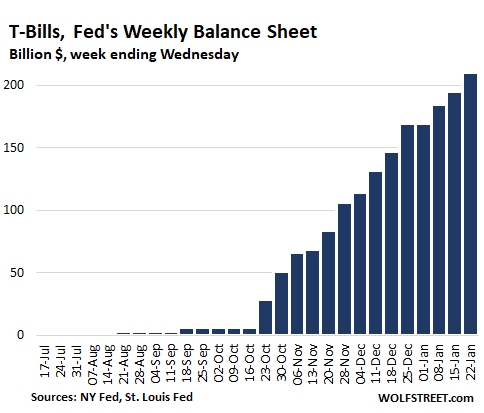

T-Bills surge.

Last year before the repo market blew out, the Fed said in a series of announcements that it would replace some of the maturing Treasury securities with T-bills (Treasuries with maturities of one year or less) and that it would replace some of the MBS with T-bills, if the roll-off of MBS exceeds its monthly cap of $20 billion. The stated purpose was to replace some of its longer-dated securities with short-term securities. Then the repo market blew out.

As part of its repo-market bailout, the Fed announced that it would buy about $60 billion a month in T-bills to push up the excess reserves that banks have deposited at the Fed, under the assumption that when excess reserves reach a certain level, the banks would once again eagerly lend to the repo market without hiccup. And then it would stop this $60-billion a month program. Since October, the Fed has purchased $210 billion in T-bills:

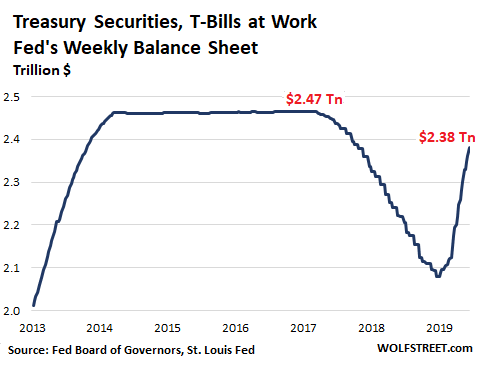

Total Treasury securities dominated by T-Bills.

Given the explosion in T-Bills from near-zero to $210 billion in four months, total Treasury securities (which include T-Bills) rose to $2.38 trillion, the highest since May 2018:

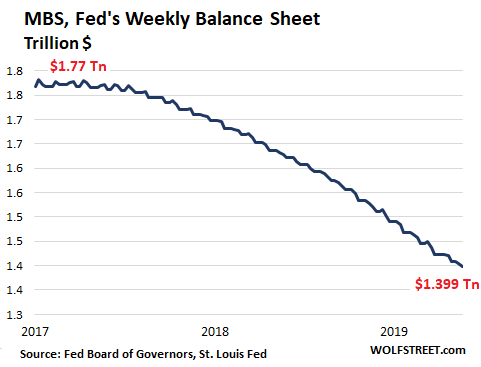

The Fed sheds MBS.

The Fed has made clear with numerous pronouncements in 2019 that it wants to get rid of its holdings of MBS at a rate not exceeding $20 billion a month (the “cap”). And it’s sticking to its plan.

The Fed doesn’t actually sell its MBS. Like all holders of MBS, it receives pass-through principal payments as the underlying mortgages are paid down or are paid off. About 95% of the MBS on the Fed’s balance sheet mature in 10 years or more, and the current “runoff” is almost entirely due to these pass-through principal payments that have been fired up by lower interest rates over the past year that triggered a surge of refis.

Over the first three weekly balance sheets in January, the net balance of MBS on the Fed’s balance sheet dropped by $10 billion to $1.399 trillion, below where they’d first been in October 2013:

Total Assets tick down.

Falling repos, surging T-bills, slowly rising coupon Treasury securities, falling MBS, and other activities reflected on the Fed’s balance sheet, all combined, have caused total assets to decline by $30 billion over the seven-day period to $4.146 trillion. This is down by $20 billion from the balance sheet four weeks ago, on December 25:

The various elements on the asset side of the Fed’s balance sheet are pulling in different directions: Repos shrank, T-Bills surged, coupon Treasuries ticked up, MBS fell, and on net, total assets are now down by $20 billion from four weeks ago.

The level of assets fluctuates from week to week, and the movement of one week doesn’t indicate a trend.

But the comparison of the past four weeks, when total assets fell by $20 billion, with the prior four weeks, when total assets surged by $123 billion, indicates that there has been a change — and more than a nuance of change — in what the Fed has been doing after it got the repo market through December 31 without blowing out. And that expected endless flood of new liquidity seems to have largely dried up.

Here is who got what from the Fed in 2019, including dividends. Read… Fed Pays $35 Billion to Banks, $6 Billion to Reverse-Repo Counterparties in Interest for 2019, Remits $55 billion to US Treasury

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Rates still gonna stay low for a long while. Uncle Fed ain’t gonna let rates rise until It sees the white’s of inflations eyes.

Why are people worried about rising rates if the fed has plainly stated its gonna print and print and print till it see its version of inflation.

Markets gonna rise. Commodities and services especially

While the bank cartel called the “Federal” Reserve, which is as much a government agency as my dog is a government agency, has managed to staunch the bleeding of whatever financier whale(s) needed the gigantic repo market loans, I doubt everything will be jolly in the future. (That is if the bleeding truly was staunched and “Fed” did not co-sign for another lender to help or do some other, secret trick to hide bail outs.)

The economy, like balls being thrown upward endlessly by a juggler, is not stable when it is being manipulated as the “Fed” manipulates it. Sooner or later, one of the balls is dropped. I think that the “Fed” has been fundamentally supported by other central bankers (particularly those that are also banking cartels mascarading as government agencies) and the “coincidental(?)” instability of other nations.

It is also helped by the normalcy bias again: whenever that ends, and foreign investors do not see the US dollar and US markets as the safest harbor to which to flee from financial hurricanes as now, the US economy will face a financial hurricane itself. While we still have some manufacturing, no country with (a) a government budget deficit of over a trillion a year, (b) total liabilities (just the US government liabilities, not even counting state and local government liabilities) of $210 trillion, (c) a secret, de facto guarantee of the banksters gambling bets on derivatives of over $200 trillion, (d) a gigantic trade deficit, (e) a reluctance to take on an unethical, corrupt, ruthless, murdering competitor that intends to sink it financially and replace it in the world economy (communist China) ,and (f) a corrupt government that allows the parasitic “Federal” Reserve to siphon off the earnings of Americans to corrupt banksters each year, will avoid such a financial hurricane forever.

To change the metaphor, we are like the ignorant passengers of the Titanic in the seconds after it hit the the iceberg who say: that was severe, but we are lucky that things are not too bad and the ship is not sinking. For now though, I too wonder if you are still short: betting against loaded dice seems unwise to me.

So my question to you Wolf is are you still short (QQQ and SPY)?

Of course. This is just the beginning, just a few weeks into it.

Wolf,

People really are silly, thinking that an invt position is taken with the expectation it will pay off in a few days, weeks, months.

This short-termism is behind a lot of the problems that the US has had for decades – plus I think there is a lot of anticipatory schadenfreude from very nervous perma-bulls holding stocks with PEs (if they have e…) Over 50…

On a post-related note – some new info regarding possible motives behind Repo rate spike back in Sept.

Specifically, the money ctr banks (having been hugely exposed in LIBOR rigging conspiracy) are being forced – this year – to switch to mkt transaction based index for the setting of trillions in floating rate bank loans.

Guess the market that will be used to set the new index rate.

Yep – the short term repo mkt.

So the big banks have every incentive to act to artificially goose up repo rates (like going on periodic creditor strikes, refusing to lend into repo mkt) so as to artificially goose up upcoming syndicated bank loan rates (ie, trillions in long term loans made to corporates).

Exit – LIBOR lies.

Enter – Repo/Syndi loan manipulation.

Why September?

Perhaps because new floating loan index will be based on average repo rates going back a yr maybe.

Look into it.

If true – f*cking amazing. The Bigs simply cannot act in any way that doesn’t make them look like a cat stroking Bond (loan?) villain

Wolf, the yield curve quietly inverting again.

Fed Bill buying (ie printing) shortly to increase…

At this distorted point in economic history, I don’t know if the Fed even knows why it should hate/fear/EXTERMINATE EXTERMINATE!! Inverted yield curves anymore – especially since the whole friggin curve is manipulated so far downward for so long already.

Why? Because the Treasury will be issuing more long term bonds and that will make the long term rate rise unless the Fed buys them and the rates will go down later.

Quietly? More like a lower high in number of inversions :P

https://i.ibb.co/TPmx9K5/num-inverted.png

There is alot of spread compression between maturities with the 30year and this time 3 month spread to 30 year is coming from the opposite direction. A break down in the 3month 30 year spread signals trouble for banks, and a break out in the 30 month 30year signals trouble for over leveraged corporates and banks (and non banks expose to financing such operations).

FRNBY can only sprinkle its magic repo pixie dust and hope it will all go away

By end of first week of February things will look totally different.

I hope not but I remain convinced Wolf will lose money if he doesn’t close the short position soon.

This stems from Wolf’s inability to believe that the a Fed is operating outside her mandate and will keep things going for a very long time. He is showing the same misplaced optimism when he was saying that the 10 year yield will hit 5% some years ago.

Just look at the Fed balance sheet, it has been increasing and it’s going up. Fed is even considering lending directly to hedge funds. It’s what matters. Some repo matured so what?

As soon as the market start to go down in a serious way the Fed will throw the kitchen sink at it.

Dow is going 30k this year.

I will take some money off when it hits 30k but in no way will short this market.

The natural growth rate is the increase in population plus productivity. Most of the growth in the past decade has been DEBT fueled. More of it won’t help. (L.B.)

B71,

What if it isn’t about helping…anybody but the Feds…stay in power…despite grotesque incompetence and corruption?

At the huge DC debt levels of 100 pct debt to GDP, each small 1 pct increase in interest requires an equal 1 pct increase in US GDP if the accumulated debt isn’t to grow, and enter a death spiral where the debt grows automatically.

So if the Fed allows the long term rate to go to 5 pct (it averaged 7 pct in the 90’s) then the US GDP would have to hit 5 pct (which it has not in decades), otherwise the Gvt’s debt automatically soars due to higher interest pmts.

Or the Fed can steal wealth from savers by printing money and giving it to the Treasury – thereby putting a cap on interest pmts.

All QE constitutes this massive theft that the Fed has engaged in in order to keep DC power intact.

Because the fed control is an illusion

Long term rates are safe in a world where the US is the only country offering positive nominal rates. The Fed realized their scheme has lots of gas left in the tank thanks to ECB, BoJ, BoE, etc pushing money into the long end of US curve.

Will this eventually blow up? Absolutely. But likely much further down the road than most people think. Just remember the Dow was 12K 20years ago! Real Inflation alone makes that number closer to 30k. The Dow fell to 7.k , 40% in 2003.. after 9/11 and wars.

So 29k doesn’t seem all that crazy if you consider there’s 4x more base money in circulation AND rates are 1/3 of what they were from 2000-2005 (4-5%)

This is great news!

The fed unwinding their QE, the bull market going on it’s own after a shot in the arm. Heck, stay on this pathway and get the fed funds rate up about 1% and I’m happy.

The Fed is not unwinding QE. In fact, they are increasing their balance sheet.

On today’s balance sheet, total assets fell to the lowest level since mid-December — the net of falling repos (1st chart) and falling MBS (4th chart) and rising T-bills (2nd chart). See bottom chart for total assets.

Why are repos down so much? A $50-billion 30-day repo from December unwound last Friday without replacement.

The assets of big bank holding companies usually drop at the end of the year. But this time it did mid January. I asked the question in a former post if the G-SIB snapshot was made in Jan instead of Dec?

Last week FICC GCF repo was also record low.

So the need for repo also dropped causing the Fed repo to also drop precipitously last week. We had 3 T bill 7.501b purchases though. Causing the actual level of Treasuries held by the Fed to rise.

Therefore, I believe this is a gimmick. Just look at level of bank reserves as they are very high. How they actually achieved this is secondary. So are week to week variations. We do have QE4, period. Kudlow says so.

I’m just gonna stick to the numbers, not Kudlow :-]

A cautionary tale about Repo was inscribed on a beer mug by the learned and wise which displayed that things do not go to heck in a straight line.

The fed says it will let inflation exceed its target for quite some time before they act………of course they also said they were going to stop QE……..did they lie or were subject to influence……..if yes……..could they raise rates immediately upon inflation starting…….you know. Just be honest with yourself. As low as rates are right now they would want to immediately bring in enough rope to at least have a chance to adjust money within a year and avoid an emergency increase of one point or more on one day.

How can there be inflation with stagnant wages, almost no unions left in the US to demand higher wages for their workers, visa threats/replacements for highly paid workers, scams to funnel more money to the chosen few, a shrinking energy pie, shrinking manufacturing base, and a debased currency through printing that covers everything up with extra zeros. Then, Doofus has announced he wants to control medicare and SS expenses in a service economy when the only bright spot is the rising medical sector (which costs 2X what other countries pay) so folks without employer paid plans have little to no coverage. Bear in mind, employer medical paid plans are a part of the wage package which means lower wages overall that might have actually funneled into the economy if people could afford to buy stuff.

Don’t worry though, there will be announced be tax cuts…soon soon, for the middle class, just before the election.

And next week is infrastructure week.

Sounds like deflation to me, hidden by currency debasement, and accepted under the guise of ‘exceptionalism’ and, “At least we’re not socialists”. This is collapse in slo-mo, until something kicks it into gear.

I look for violence in the streets long before inflation rears its head.

After the inflation hysteria of qe 1-3, what number are we on now? Followed by the failure of any kind of high broad level inflation in the consumer economy outside of a few malignant industries that don’t really operate under standard pricing models/behavior, how are people still worried about inflation going double digits is beyond me. We resemble Japan more and more every day.

Prices can’t rocket up without wages rocketing up to drive those prices higher. Otherwise what you’re looking at is a severe tightening of one’s budget constraints implying that the real economy is falling off a cliff. If you think the future holds much higher inflation then you’re predicting one of two things: much higher wages or a shrinking number of tangible goods and services available. I have yet to see strong evidence for either.

The fact that income inequality keeps shooting up while most workers get modest at best wage gains, even as unemployment levels continue to drop, indicates to me that there is something off with the labor market to this day and that’s exactly why you won’t see inflation. Employment to population ratios are still low and potentially misrepresented by multiple job holders, so jobs are not being created like they used to be or people simply cannot do the available jobs.

I will fear inflation on the day the fed stops buying securities (enabling excess government spending doesn’t seem to spur inflation much) and starts giving money directly to consumers.

I know Europe isn’t the US, but despite NIRP policy and relatively powerless unions the Netherlands has 2.6% CPI and wage increases that are the biggest in over 30 years. Large groups of government workers (teachers, healthcare etc.) got 10% or more income increase for the next 1-2 years. And for sure, inflation in housing, mandatory healthcare insurance, tuition etc. etc. is a lot more than the official CPI. Social security and old age allowance are adjusted for CPI, so those increase as well – only the middle class really suffers, and those on fixed income (but most Dutch pensioners have far more pension than they ever paid for, I have no pity for them).

If this can happen in Europe I don’t doubt it could happen in the US too if the FED lowers rates a bit again. No sign of deflation at all.

“How can there be inflation with”

There has been continuous inflation for decades now. Just look at the price of a candy bar or the level of the stock index. Ignore their propaganda. The use of their consumer price indexes or terminology like Quantitative Easing just spreads their misdirection. It’s properly called money printing and inflation – because that’s all it is – and purposely so.

How can inflation rocket up with the amount of debt being carried?

Debt drags down everything when it wasn’t used to produce value added enterprise. Most debt, especially stock buy backs, has been used for decades to produce consumption. So you borrow to consume and the production is used and gone and the debt remains to be serviced. Do this long enough and more debt just creates more deflationary pressure.

The FED is trapped. They created massive amounts of deflationary pressure and their only tool to fight this is more debt which creates more deflationary pressure. So they ramped up the monetary pressure to try and create inflationary pressure and all that has happened has been low wages and low investment and high asset values. All of which are out of balance with extremely limited market price discovery.

Yet with all the debt they helped create (and encouraged) they can not allow market forces to rebalance the system because that means massive defaults and massive dislocation. That means deflation which isn’t what they promised. They promised inflation to pay off the debts.

No matter what the FED wishes, gravity does exist and no amount of magical thinking or dialogue will change the rules of physics or economy.

Be careful.

So far, they’ve printed lots of money but it has gone only to the wealthy via tax cuts and stock prices. This hasn’t stimulated the real economy enough to create inflation; rather, it has only helped ward off deflationary pressures that are building. The next step could be some sort of tax cut or QE to put money in the hands of Average Joe, and that is something that could create inflation for a while.

The powers that be have been trying to keep the economy afloat by subsidizing the wealthy, in hopes that a minimal of wealth effect and trickle down demand will occur. It hasn’t worked. So, will they watch the system go under, or will they opt for their absolute last resort, which is helping Average Joe?

Take a anonymous poll at Davos, and the preference would likely be to hoard the wealth and move to a bunker in New Zealand.

The tax cut idea won’t work because to many people don’t pay any taxes..

Direct deposits probably won’t work because to many people live hand to mouth and don’t even have an actual bank account as the banks charge people to have an account… sort of like negative interest rates for the poor. Only what’s left of the middle class has bank accounts.

The government has very little control over wages as those are actually free market mechanism for the most part. The government does not actually like free markets and has made many rules to prohibit it.

The best and probably only answer is for asset prices to reset much lower after much of the debt has defaulted or severely written down (DEFLATION). After the monopolistic predators have been disassembled and done away with.

How can inflation rocket up with the amount of debt being carried?

By extending more credit. That’s the method that has been working for decades now.

– Here one W. Richter makes a BIG mistake.

– The influence of the FED is minimal. Just look at the data. In mid 2008 total US debt stood at about $ 56 to $57 trillion. But the balance sheet of the FED was a “mere” $ 800 to $880 billion. So, the FED had up to that point “printed money, created credit” that amounted to less than 2% (!!!!!) of total outstanding money/debt.

– Mistake #2: QT is NOT deflationary because then credit/debt is being swapped for money.

Do realise the FED is there for the FEDmembers in the first place.

Changing from MBS’s to T-bills means something.

What do they (fore)see?

CRV,

It may be as simple as what part of the interest rate curve the Fed wants to manipulate downward.

Long term rates came down with the Fed rate cuts this yr (altho allowing the MBS to run off pushes in the other direction – upward).

But for whatever reason, short term rates stayed high – causing a flat, occasionally inverted curve – which makes people nervous as a historic recession indicator (altho historic indicators are fairly useless in ZIRP world…)

So, in order to get short rates down…the Fed prints money to buy TBills that mature in under a year.

Pretty simple, eminently manipulative – fairly classic Fed behaviour in ZIRP world.

@CRV this shift out of MBS has been in the works for a long time.

The original Fed purchases of MBS in the Great Recession were technically illegal because the MBS were not (at the time) full-faith-and-credit obligations of the US government. Congress chose not to complain at the time, since they were busy saving their skins. But in the aftermath, it appears there was a general agreement to unwind the position. Getting the US government out of the MBS business will not only restore a bit of constitutionality, it will also eventually allow Fannie and Freddie to be spun back off again… no doubt to enrich a few favored insiders at public expense.

It’s the interest rates.

The Fed and the other central banks have tried to force the market to invest in the economy, to stimulate the economy.

That has worked to some extent, but a lot of money went looking for yield in Asia.

At 10% there is an ocean of repo funds.

The Fed is fighting market forces.

Statements like “Fed will let inflation stay low for a long time” or “Fed could raise rates immediately upon inflation starting” are confusing. They are confusing, because inflation is very high RIGHT NOW.

If you are referring to the Fed’s measurement of inflation this is and will be what the Fed wants it to be because these are deliberately manipulated figures that DO NOT measure what inflation actually is.

I believe a more accurate statement might be:

“The Fed may never raise rates, and will certainly not raise rates due to inflation, because inflation is already high as a result of suppressed rates and QE. Also, the Fed controls reported inflation figures and chooses to report inflation lower than it actually is. Therefor, we know with 100% certainty that the Fed is NOT “waiting” for inflation to rise to raise rates or for any other reasons.”

Agreed, regarding manipulated inflation measures.

It has been clear for quite a while, that DC will save the “government” by destroying the currency.

When it is all over, be it 2 or 20 years from now, over some long weekend, the then President of the US will morph from world leader to Chinese morning talk show host fawning over their then Dear Leader.

In the end, productive capacity (factories) are what determine economic power.

And for the last 20 years in this regard, the Chinese have exposed American “elites” as incompetent “leadershit”.

The inconceivable stupidity of opening US markets to the Chinese (while granting them the complete freedom to manipulate the Yuan so as prevent free US imports into China) will rank as one of the greatest political stupidities in the history of the world.

It was the moment when US superpower status passed from its hands – given away by America’s Ivy League inbreds.

That outsourcing/globalist policy was very clever obviously if you only care about the elites, and short term gains. The wealth transfer from middle class to the 0.1% (mainly in the US) is probably more than at any previous time in history. If it is wise policy longer term for the elites remains to be seen. Long pitchforks :)

The fed got what they wanted….the party started again. Now the mkt is going on its own. If the mkt should falter, the fed will be right back in business expanding balance sheet again. After twelve years of it, how can anyone doubt.

Morgan Stanley warns that April is the end of the buying by the fed. They there could be trouble in the markets. Give me a break. Either the fed will restart buying, or they’ll cut rates, or they’ll “hand off” to the ecb or another central bank to start buying the shit out of everything.

I’m not a defender of this stuff. My belief is that they are destroying the world. But i just recognize reality. Which is…….they are NEVER going to stop this crap until the currency mkt is dead.

Fed activities since October look very similar to late 1999, when Y2K worries prompted them to add huge amounts of reserves. The difference today is, we don’t really know the drivers of whatever liquidity issues they’re trying to solve today – or where they’re coming from.

So what you are saying is that it is the current float in the Repo market that is critical here? I must say I am confused because when they announce the daily Repo sales, it’s like we just added this new amount of money…they don’t mention that some of it rolled off or was cancelled? I hate it when the media tells one side of the story like one side of a financial transaction, but there also seems to be a lot of Fed haters repeating it? If I’m understanding this right?

Augusto,

“If I’m understanding this right?”

Yes, and how the media covers only the “in” part of repos and not the “out” exasperated me to the point where I slapped the WSJ, a big offender in this misreporting, directly across the face:

https://wolfstreet.com/2020/01/10/the-wall-street-journal-and-other-media-should-stop-lying-about-repos/

Thanks Wolf. One more question. The current prattle is that the daily Repo injection is jamming the market higher. Presumably it goes direct to the trading desk? But doesn’t the repayment side reduce liquidity, has to be repaid, not for trade, off the books, not for the traders, undercut the market? Of course, I don’t really understand the actual flow of funds, or what tricks if any traders can play, but still curious, if this is “true”?

Don’t listen to the “prattle.” Just look at the numbers. The charts above show you the numbers not the prattle ;-]

You tube : Fed T Bills jump =

Chongching fat pig bungee jump stunt.

Housing market, through its widespread tentacles, is the single largest chunk of the real economy. The Fed is trying to prop up the housing market. Look what is happening. The DTI requirement for mortgages is going away. The gigsters income is now counted as stable.

If the housing falls, the stock market won’t mean anything. The Fed will do anything to prop it up, including launching qe4 in the spring.

Trying to explain this repo more. Yawn.

Supply of Liquidity

On 19-Sep-19, Bank Reserves were only 1,394,122 (mil).

On 22-Jan-20, Bank Reserves are now 1,621,689 (mil).

In other words, Bank Reserves have recovered and are now very high.

In my opinion if this number is at least 1.6B, we don’t have to worry about a repo problem, TODAY.

The Fed can back off repo by simply buying more Treasuries.

Demand for Liquidity

Just how much bonds are there that need to be financed overnight?

Primary Dealers have about 201.7B Long Term Treasuries that needed to finance, just slightly above the 181.5B they had 2 weeks ago.

FICC GCF Treasury Repo was one of the lowest weeks for the last 12 months only averaging 31.34B per day for the week ended 1/15. For the week ended 1/22 the ave/day was 38.237B. Normally the average is in the 50Bs

Meaning, the is NO balance sheet size of the banks that need more financing than usual. Banks wanted to look and be smaller for regulatory purposes. You can countercheck these numbers with the h.8 report, page 3 Assets and Liabilities of Commercial Banks in the United States, item #3 Treasury and agency securities. Look at the columns Week of Dec 18, 25 and Jan 1, 8. They are all LOWER than November’s number. Same for #4 MBS, they are smaller, too. This means the banks SHRANK their end of the year Balance Sheet. They have LESS securities needed to be repoed.

Don’t forget Foreign liquidity coming in due to their negative rates in Europe and Japan. That’s another source of liquidity. Also the Fed REDUCED its reverse repo to 265,357 (mil) resulting in more reserves.

Bottom line, week to week varations really don’t matter much unless they affect the trend. But here is what I think will happen. If you look at the each CUSIP of the T bill purchases, many of them had 26 and 52 week terms. But nowadays you see the Fed buying 13 and 8 week terms also. I believe there is a limit to what the Fed can buy without disturbing the Money Market Fund (MMF) market because the growing MMF needs to hold SHORT TERM BILLS.

The Fed will be forced to buy 2 year and up notes if it keeps on going.

Same for the Treasury. They will have to raise new money from Notes and Bonds and not so bills. Guess who is the marginal buyer? The Fed.

Watch the liquidity levels like a hawk. When they do down, look for the stock market to tank. Just my personal opinion, ok.

You put one repo in

You take one repo out

You throw some dollars in

And spread them all about

You do the Powell-Pokey

And turn the market around

That’s what it’s all about!

HD,

That is actually pretty damn funny.

Bravo! Is this the anthem for our times? Maybe….

Today, the Fed just bought 5.723 billion of this T bill: 182-Day Bill CUSIP 912796WX3.

It was just issued yesterday. It will mature 07/23/20 and the Fed has all the intentions to ROLL it OVER.

So the Fed essentially PERMANENTLY added 5.723B to liquidity just this purchase alone. There are many others like it.

Now compare this to a RE-PURCHASE agreement or repo. They are typically only overnight or a term of 14 days.

After that date the other party (the borrower) must buy back the collateral. Meaning REPO is a temporary increase with a sure decrease of Liquidity at a later date.

Make sure you understand the difference since the FED is increasing or compounding the size of its PERMANENT purchases. Where does that liquidity escape – the stock market?

If the Fed buys a Treasury security hot off the press before the ink isn’t even dry, can you call that outright debt monetization? Or are you gonna be labelled crazy?

Sorry! It’s not “outright monetization”, because some bankers got to take their skim in the middle before it wound up at the Fed. /snark

More seriously, it’s not really monetization if the Fed is running off $5B in MBS the same week that it’s picking up $5B in T-Bills. What matters is the total size and composition of the balance sheet, not a particular transaction.

Anyway, in some sense the Fed’s entire job (since Nixon ended gold standard) is to convert a portion of the national debt into the national money supply.

If a MBS paid off early, it really needs to disappear and reduce the balance sheet. But no, they buy T bills with that but not over 20B. So re-buys, re-purchases, roll-overs are MONETIZATION. But they can’t have that.

Following this balance sheet increase is guaranteed stress. Need to keep cool and just ignore something I can’t control.

“Fed is running off $5B in MBS the same week that it’s picking up $5B in T-Bills. ”

Neutral in aggregate – but only for a year or less.

The MBS are long-term, altho a decade into the Fed’s “We Buy Crap” sign being put up, the huge MBS holdings are now maturing and not being replaced. This puts upward pressure on the long end of the yield curve.

Concurrently, the Fed is buying TBills on the short end – driving *short* rates down.

The two together put pressure on the market for a normal upward sloping yield curve. And keeps the aggregate Fed balance sheet somewhat static.

*But* – unless the Fed keeps the monthly TBill buying going indefinitely, the TBill mature quickly and the balance sheet shrinks again.

The twisting of the yield curve into normal shape seems to be the goal – made necessary because of the Repo spikes distorting the short end.

Same old Fed song and dance. The songs requests will keep coming, and it’s dancing all night long, till we can’t dance no more…. no more.

Wolf,

We are getting close(r).

Concentration – check.

5 companies are quarter of US GDP.

Acceleration – check.

Large cap up 5-10% year to date.

Irrational exuberance – check.

Tesla, Beyond Meat, Roku, etc.

Just need a bit more euphoria.

potentially >> 100.000 CoV cases within a month and major hit to Chinese (and other) GDP, check, bullish!

Maybe Mr. T has a problem selling all his US farm products to the Chinese if this gets out of hand, but no doubt he will have a “solution” for that like forcing them to buy anyway, bullish!! Is Paul Krugman already salivating about the economic boons of all this destruction?

1) The market is quiet, the Repo market is boring, because the year of the pig, 2019, had a 68 meter bungee jump.

2) The year of the Metal Rat will be celebrated on Jan 25

2020.

3) This party cost a lot of money.

4) Follow the Repo market in the next few days, because

there might be a lot of new demand, Chinese demand.

5) So far, $USDCNY is down in Jan 2020 from Sep 2019 @ 7.185 to 6.937, closing x2 gaps.

6) The trend is up. Up LT from 1.00 in 1980 to above 8 til July 2005, to start a correction. The USDCNY is approaching 8 from below.

7) China is not cheating. USDCNY 2005 to 2014 decline

was a temp correction in a bull market.

8) If the Repo market suddenly wake up, don’t blame China, please blame BA.

Fed is the banks, when they “buy” T bills and add to reserves, in order for banks to convert them to cash. The rise in equity prices is in no way antithetical to REPO. Do banks sell the stocks they bought if REPO closes, and Fed lowers (emergency) reserve requirements? If Fed lowers reserve requirements that should obviate the need to raise cash? With corporations buying at the highs and retiring shares, there is always a greater fool.

Only Wolfstreet charts have ONE clean parameter,

without three to six brothers & sisters parameters that fight and cross each other on the chart, with close undistinguished colors and few osc stuffed underneath for desert. The story telling is done on the blog, not on the chart.

Wolfstreet blogs are focused, short, clear language, with a punch lines. His English plain, not for the elite, so people around the world can understand.

Maybe I just missed it here on WS, but here is the WSJ tying the repo spike to the upcoming changeover from LIBOR to repo-based rates for setting the rates in the multi trillion dollar floating rate syndicated bank loan mkt.

https://www.wsj.com/articles/repo-market-tumult-raises-concerns-about-new-benchmark-rate-11569247352

Wolf,

Thx for the recap. Your point of media emphasizing the in but not out of Repo is consistent with the desired affect of Repos.

One down week does not a trend make, REPO bal is still around 185 Bil-200 Bil, same level it was in early Oct. I hope they keep retiring the 30-14 and 42 day repos.

Once again, I think the Fed has allowed the Repo system to facilitate arbitrage and to bail out over levered hedge funds.

In this way the Repo encourages this type of trade when their role should be to discourage it by allowing the players to take a loss not enable this model and more system fragility.

Plus I’m trying to short the hedgies debt and Repo is frustrating my aims so we’ll see whether the fed will continue to drain Repo’s out of the system.

I wished my family’s finances worked there way the Repo market worked.

Sadly outflows are not cancelled by inflows!

1) From the early 1970’s inflation was rising.

2) US 10Y was up from below 6% in Mar 1971 to above 15% in Sept 1981, forming a bubble.

3) For 30Y the 10Y was down with lower highs and lower lows.

4) Since May 2012 there was a stopping action, shortening of the down thrust.

5) The 10Y is in some kind of trading range.

6) For the first time in almost 40Y 2018 top is higher than the previous top, the 2013 top.

7) This stopping action might be over.

8) The current 10Y is at 2012 low. It might move up, or down, below 2016 low.

9) The downtrend is still VERY strong, because the 2018 retracement was shallow. The 10Y will proceed towards the zero line.

10)

MBS percentage of the collateral used in repo market has increased from 23% in Oct to 78% in January…..

Sorry Wolf, repo QE forever will only accelerate. Do you want to know why the Fed took over QE? It was so that the Federal government could fund itself. China isn’t buying bonds anymore and the Fed is using the short term market to bring in leveraged buyers of its debt.

Without the Fed sponsoring Repo, the entire world economy might collapse.

FRNBY Sponsored Repo == Bandaid over a stab wound

The FRBNY is a piss ant in the global repo market where junk collateral is routinely hyphothicated and transformed into rehypothicated UST’s which the notional value of said transactions routinely exceeds FRBNY repo daily.

When it comes to what is money:

Rehypothicated collateral > federal reserve notes

The Fed does two things when under pressure: they print money and drop interest rates, and everybody knows their game, and it’s their policy to signal their planned (upcoming) plays. The ultrarich buy what the Fed is buying and sell what the Fed is selling. The whole game works when the Fed strategy works. What we’re probably all waiting for is the moment when the game fails. That did happen in 2008, and again, briefly, in Dec 2018. Of course, the Fed just did more of the same in response. It seems to me that it’s hard to escape the analysis that the Fed is trapped. When the Fed loses credibility, market rates will rise, and printing money will help about as much as it did in Zimbabwe, Venezuela and Argentina. The Fed is winning every battle and steadily losing the war.

the FED (and the elites) will still win the war if the middle class (those few that are still more or less independent from central banking manipulation) are more trapped than the FED itself. It looks to me like that, especially in Europe – nowhere to hide from the unlimited moneyprinting.

Risk Premiums are so minuscule,

you need a microscope to see them.

( Risk-Free ) Fed Funds yield 1.75%,

higher than (risky) 10 year bond yield: 1.7%;

another ( bank destroying ) inversion.

If 2011-2017 were good years for you,

with things falling apart in 2018,

and bottoming out late 2019, this is why:

https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

78% the collateral used for repurchase agreements

are now (toxic) mortgage-backed securities.

Note the severe lack of capitalism.

The government, not capitalism,

won the monopoly game. Game Over.

There is certainly a severe lack of capitalism — a point that the political left has largely missed.

Agree, government and central bankers won – they are in bed and serve the same masters. Capitalism no longer exists, except maybe in some small pockets of the market.

What’s the rate on very long term Greek bonds nowadays (the country you know is never going to pay you back), 1.5% or so? What’s the rate on mortgages in the extremely overvalued Dutch housing market? about 1.0% … There is no risk in this market, only central bank money printing.

So the Fed will continue the T bill $60B/mo purchases till June.

That’s another potential $300B added to the balance sheet.

The bank reserves will be about $1.9 Trillion then.

Problem solved. No more need to repo.

The Federal Open Market Committee has not yet said that the purchases will continue until June. They said, on October 4, October 30 and December 11, “at least into the second quarter of next year”. They likely will clarify that on Thursday at the conclusion of their next meeting.

Check FRB H41 Table 11. Fed total balance keeps going up since 9/2019.

No they’re not. Now flat with mid-December. Look at the last chart above, which reflects total balance as per H.4.1

It ain’t a straight line as the mug says.

But I see your point. It’s a lot bigger since September.

The point is, repo was a symptom of the problem. It was caused by other things. Those things are already being addressed by more than ample reserve increases. Repo itself will disappear later.

Most of the recent decline in outstanding repos is not due to a change in the limits on the Fed’s offers but instead to the amount that the counterparties, the 24 primary dealers, are choosing to take up. For overnight repos everyday from 12/13 through 1/14, except New Year’s Eve, the New York Fed set an aggregate limit of $120 billion. For New Year’s Eve the limit was $225 billion, with $75 billion of that offered on 12/30 with one day forward settlement. The limits for 1/15 to 2/13 are also $120 billion. For term repos, they offered on 12/16 they offered 32 day repos with a $50 billion limit and twice weekly 14 or 15 day offerings with $35 billion limits. As mentioned in the article, the 32 day offer was not repeated in the new plan issued on January 30th but it still contains twice weekly 14 day offerings with $35 billion limits in January declining to $30 billion in February.

You can download the FICC GCF Repo and see the same thing:

http://www.dtcc.com/data/gcfindex.csv

There was less volume in Treasuries to repo.

You can also go to h.8 and look at the week-by-week change in the Govt Securities Held – Treasuries and MBS for those dates. They are smaller.

The big banks just didn’t have a bigger sized balance sheet.

“Last year before the repo market blew out, the Fed said in a series of announcements that it would replace some of the maturing Treasury securities with T-bills (Treasuries with maturities of one year or less) and that it would replace some of the MBS with T-bills, if the roll-off of MBS exceeds its monthly cap of $20 billion. The stated purpose was to replace some of its longer-dated securities with short-term securities.”

That is not quite accurate. The Fed did not say they would and has not replaced some maturing Treasury securities with T-bills. Principal payments from maturing Treasury securities are rolled over into newly issued Treasury securities on the maturity date. The Treasury does not issue T-bills on days that other securities mature and vice-versa so under that long standing policy no T-bills are purchased when Treasury bonds, notes, floating rate notes, and inflation protected securities mature. Now that the Fed owns T-bills as they mature the principal is reinvested in newly issued T-bills. The Fed is reinvesting up to $20 billion a month of MBS and agency principal payments in Treasuries purchased in the open market but only a small portion, 15%, up to $3 billion, of that is going into T-bills. The policy is that the reinvestment is allocated “to roughly match the maturity composition of Treasury securities outstanding”. 11%, up to $2.2 billion, is being reinvested in bonds with at least 20 year remaining maturity. The stated purpose is “to continue to allow [Federal Reserve] holdings of agency debt and agency mortgage-backed securities (MBS) to decline, consistent with the aim of holding primarily Treasury securities in the longer run.”

When the principal maturing Treasury securities are rolled-over, the allocation is in proportion to the amounts of the various types of Treasury securities being issued. For example on 12/31, the Fed received principal payments from maturing Treasuries totalling $12.047 billion. That day the Treasury issued $32 billion of 7 year notes, $41 billion of 5 year notes, $40 billion of 2 year notes and $15 billion of 5 year TIPS. So the Fed tendered $3,011,698,200 for 7 year notes, $3,858738,400 for 5 year notes, $3,764,622,900 for 2 year notes and $1,411733,500 for 5 year TIPS. (The total is not exactly $12.047 billion because there is a small amount of original issue premium or discount on each issue and the TIPS included accrued interest because while nominally 5 year they actually had 4 year 10 month remaining term as well as inflation adjustment. The face value of the purchased securities was exactly $12.047 billion.) Similarly on 1/14, $4,324,000,000 of T-bills held by the Fed matured. That day the Treasury issued $35,000,000,000 of 4 week T-bills and the same amount of 8 week T-bills. The Fed paid $2,162,133,300 for 8 week T-bills and $2,162,133,400 for 4 week T-bills.

Informative stuff above, thx Wolf and commenters.

I looked up “rehypothication”, just now, because it’s a recently new word to me. Ah, it looks like more of the same kind of stuff that goes on lately with money managers (read Central Bankers, and other bankers, brokerages, hedge funds, and so on)……wondering if the Fed’s repo activities are now considered as a type of rehypothication, or why not ? Wait, it seems like maybe rehypothication only applies to borrowing collateral without the owner’s knowledge/permission ?

Makes me wonder what the SIPC busies itself with, these days. Guess I will hope that the stock certificates that I hold have not been loaned out to anyone for their shorts- or other options, derivatives, etc.. These are certificates printed out on paper, with seals, etc..

As I understand it, from today’s word check (above), these should NOT be subject to any form of loaning out without my express permission. Whereas anything in the brokerage account may be on loan without my permission. Need to study this a bit more.

FWIW:

from Wall Street Words, 1997:

“rehypothecate To repledge stock as collateral for a loan. In practice the term means to pledge securities (by a brokerage firm) for a bank loan when the securities have already been pledged to the firm by one of its customers. The brokerage firm essentially passes along the collateral in order to obtain a loan to finance the customer’s account. ”

Silly me. I thought that I was “financing” my account when the brokerage firm took payment from me for the securities that I was purchasing. The purchase takes several days to settle in my account. But my cash balance immediately shows the drawdown for the purchase.

……………………..

“rehypothicate” appears to be a new spelling of the old word “rehypothecate”…….and “repo” an abbreviation of either word, appropriately applied to the Fed’s repo transactions