But on Jan 1, it removed $64 billion in liquidity via gigantic “Reverse Repo.” And it continues to shed MBS.

By Wolf Richter for WOLF STREET.

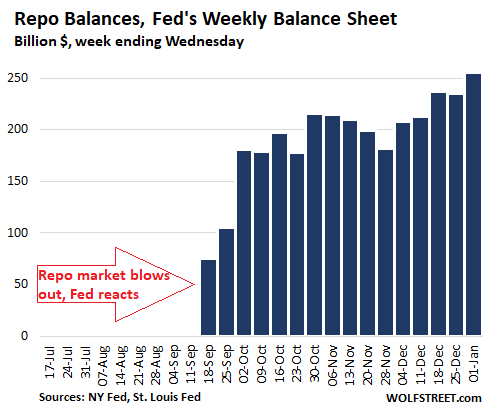

The big fear was that the repo market would blow out again at the end of 2019, as banks would be window-dressing their balance sheets by building up reserves to certain levels. In the process, they would refuse to lend to the repo market. And borrowing pressure on the other side – such as hedge funds or mortgage REITs that borrow cheaply in the repo market to fund long-term bets – would drive up repo rates. At the end of 2018, repo rates blew out, but quickly settled down without the Fed’s involvement. In September 2019, repo rates blew out again. At this point, the rattled Fed started dousing the market with hundreds of billions of dollars to calm the repo market and prevent another year-end blowout.

To do this, the Fed engaged in repo operations and also began purchasing short-term Treasury bills. This calmed the repo market, and at the end of December, repo rates didn’t blow out. But on January 1, the Fed did a huge $64 billion reverse repo, the opposite of a repo, thus draining overnight $64 billion in liquidity from the market. This astounding spike in reverse repo balances showed up on its balance sheet for the week ended January 1, released today:

In a reverse repo, the Fed sells securities and takes in cash, under an agreement to buy back those securities at a fixed price on a set date. A reverse repo drains liquidity from the market. When the reverse repo unwinds on the maturity date, as the Fed buys back those securities, it adds liquidity to the market. Reverse repos are liabilities on the Fed balance sheet.

In a normal repo, the Fed buys Treasury securities and mortgage-backed securities (MBS) guaranteed by Fannie Mae and Freddie Mac, or Ginnie Mae, under agreements to repurchase them at a fixed price on a specific date, such as the next day or in a longer period. This adds liquidity to the market for the duration of the repo. When the repo matures and unwinds, the liquidity gets drained. But a new repo can roll this over. Repos are assets on the Fed’s balance sheet.

Total repos on the Fed’s balance sheet on January 1 rose to $256 billion, up $48 billion from a month earlier (as of Dec 4 balance sheet):

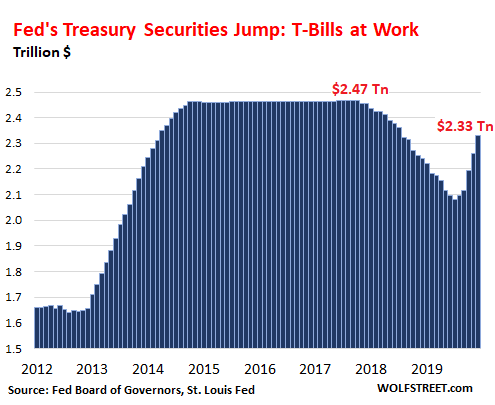

Fed gorges on T-Bills.

During the month of December through the balance sheet for the period ended January 1, the total amount of Treasury securities on the Fed’s balance sheet jumped by $69 billion.

Most of this increase was due to the Fed’s buying spree of short-term Treasury bills (T-Bills) with maturities of one year or less. The Fed carried $169 billion of T-bills on January 1, up from nearly nothing in September, following its announcement that it would add about $65 billion in T-bills a month until there were enough reserves in the banking system to calm its crybaby cronies in the repo market. This brought the balance of total Treasury securities, including T-bills, to $2.33 trillion.

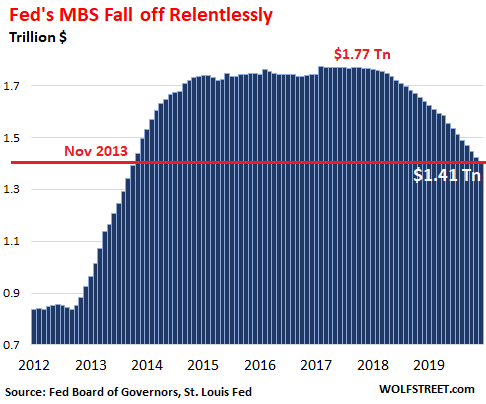

But the Fed continues to shed MBS

In numerous pronouncements in 2019, the Fed said that it wants to get rid of its holdings of MBS. The plan is progressing bit by bit. In December, the Fed shed $15 billion in MBS. Over the past eight months, it has shed $174 billion in MBS, or about $21.8 billion a month on average. Its holdings are now down to $1.41 trillion, below where they had first been in November 2013:

The Fed, like all holders of MBS, receives pass-through principal payments as the mortgages that back the securities are paid down or are paid off. About 95% of the MBS on the Fed’s balance sheet mature in 10 years or more, and the current runoff is almost entirely due to these pass-through principal payments.

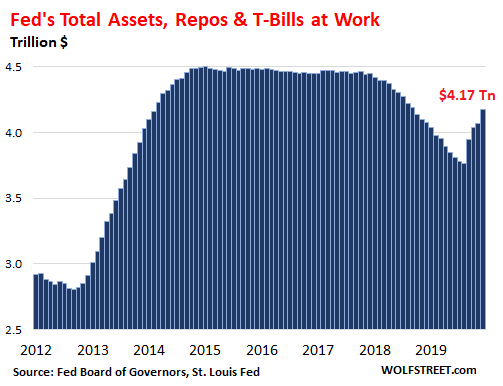

Total Assets Jump

In total, the assets on the Fed’s balance sheet – which include Treasury securities, repos, and MBS, among other stuff – jumped by $108 billion in December to $4.17 trillion. Over the four months since the repo-market bailout started, the Fed has added $412 billion to its balance sheet, the fastest increase since early 2009, when the banking system was on the verge of collapse and the economy in a tailspin. But this time there was no crisis, other than a hissy-fit of the Fed’s crybaby-cronies in the repo market, and they had to be pacified, it seems:

We got another one from the Fed, warning about all the right things. And then they do the opposite. Read… Here’s What Gets Me about the Fed’s Warnings of “Excesses and Imbalances that Are Hard to Deal with Later”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Won’t be surprised to see the balance sheet exceed $6 Trillion by year end as the government doubles down on deficit spending and the Fed agrees to finance the deficits. Will exceed Quadrillion by end of decade if we have not moved on to the new dollar by then.

Dual mandate: 1) fund government deficit spending 2) inflate assets

Everything else is just sound and fury signifying nothing. A banana republic but without the banana production.

Dual mandate: 1) fund government deficit spending 2) inflate assets

While delaying Detonation Day until their member banks are positioned to exploit it.

Pawn sacrifices are taken for granted in these chess games. Knights, bishops, rooks, even queens get theirs too. Those grandmasters do whatever it takes to protect the king and win the game. Feeling fianchettoed yet?

“All the real talent is siphoned off into the Arts and Sciences, and that leaves the dregs to put it all together”

-Bucky Fuller

“He just “yes”es you to death, and as he takes your dough He tells you “Yes, we have no bananas We have-a no bananas today.”

“the new dollar by then”

Yep.

“A banana republic but without the banana production”

Yep.

Correct.

We see a recession chance and must accommodate with added liquidity…Fed Governor

We have a larger economy and thus need a larger balance sheet…Fed Governor

In other words, PERPETUAL QE

Regarding “dual mandate”, the oft mentioned phrase, there are three mandates in that mission statement. The one ALWAYS left off is “promote moderate long term rates.” Moderate by definition means “not extreme”.

Record lows, 4000 year lows, in long rates is extreme.

Thus the Fed is in constant violation of two of its THREE mandates..the other being “stable prices”. 2% inflation yields 22% price rises in ten years. Stable?

Yes soon we Will get The new USD,, one old can be converted into one New If you are US citizen with money in US banks. Then foreign debts Will be paid with old USD…..

Wolf, are you of the opinion that some important bank or hedge fund would have already filed for bankruptcy if not for these repo operations? Are you of the opinion that the banking system almost collapsed on September 16?

Not banks. Banks can borrow at the Fed’s discount window at 2.5% currently, if they need cash. They don’t need the repo market once rates spike over 2.5%. Hedge funds and mortgage REITs do not have access to the discount window. And once they start funding long-term bets in the repo market, they have to have continued access to the repo market. And if that access closes, or rates spike too high, they will run out of options very quickly. I think that there is a good chance that a hedge fund or mortgage REIT could have gotten tripped up.

So you’re saying you think the Fed’s recent $412 billion Repo rescue was likely a bailout to Hedge Funds? So the Fed is now at the point of bailing out Wall St. parasites? Hm, not a troubling thought at all.

And I’m SURE they’re doing it for the good of the country.

I think he is saying “once ‘banks’ start funding long term bets.. they need continued access” The Greenspan Fed used REPO, with incremental interest rate policy. They in turn handcuff themselves in the event of a volatile shift in rates. They called it the Goldilocks economy, which required massive jawboning, and Greenspan to override committee dissent. None of that applies in the current context. Hedge funds are out of the loop. Some of this REPO business has to do with foreign banks and their dollar funding issues. It also has to do with monetizing spending (without revenue – a recent NY times art says lobbyists have gutted Trumps corporate tax cut provisions, which means even larger revenue shortfalls). Wall St’s irrational exuberance is an unintended consequence. The helicopter doesn’t care who is below them when they drop the money.

Thanks, very clarifying. Could this have something to do with WeWork or SoftBank…? (I know there is no way to know, since it’s a secret.)

Softbank can finance operations in Japan (much lower rates than in the US) and WeWork got a $1.7 billion lifeline from Goldman Sachs about three weeks ago.

My personal take is this was either a manufactured crisis to “force” the return of repo operations or a very large foreign bank (or a cluster of large banks) facing a “sudden” US dollar shortage. Either way something’s fishy as the Fed will only make detailed data about these present repo operations starting in September 2021.

@mc01

They never let a crisis go to waste.

This was an excuse to do not-QE and expand the balance sheet albeit at a very low interest rate.

Either way something’s fishy as the Fed will only make detailed data about these present repo operations starting in September 2021.

It’s a tell, but what does it say? When you discover that something is not what it seems you have to ask yourself what it really is. If it’s something good they’d say so, but they’re not saying so.

It’s perilous to trust banks but people do it anyway. Not that there’s any choice.

The Federal Reserve Board of Governors lowered the discount rate to 2.25% effective October 31st, 2019.

However, no banks use it because of the stigma associated with it. Under Basel III banks are supposed to have at least 30 days of HQLA to cover its outlay so in theory the have enough liquid reserves and don’t need to borrow from the Fed. They do it at Repo, though.

The problem has been exacerbated when the non dealer bank holding companies such as hedge funds increased their holdings of long term notes and bonds. Many became sponsored members at GCF repo and bought tremendous quantities as DIRECT competitive buyers at auction. They also most probably bought the dealer inventory overhang last year. Why? Because they bought the Druckenmiller bet that yields were dropping to zero. Meaning the price will increase and they will profit. The reverse happened and the yields suddenly rose!

Since this position was leveraged, they had to borrow mostly at repo. Since hedge funds don’t hold reserves at the Fed, they were stuck at borrowing at repo rates. Fed to the rescue because they didn’t want a fire sale of Treasuries by hedgies.

Thanks for the correction on the rate. I posted my comment in the middle of the night, and my brain was already whacked out, it seems.

That is an excellent definition of how not-QE works.

@ Iamafan nailed it. the real issue here is bank liquidity. my theory is the repo market has been keeping european banks on life support. the only way they can be saved longterm is for there to be an integration of eu sovereign debt. that can’t happen until after brexit, that’s what this is really all about.

It still amazes me that the supposed “risk management” part of these firms allows them to take these obviously VERY risky positions. If they did it because Druckenmiller said something (vs. some kind of objective and quantitative strategy), without proper hedging (risk management), then it is even more ridiculous.

The FED and FDIC (?), SEC(?) should immediately take enforcement action if this activity raised a systemic risk to the markets.

I will not be holding my breath.

I also wonder at who got caught by the Argentine default, hedgies here, and situation in Turkey’s banking system, that mostly concerning European banks.

Yes but then they have to adhere to regulations ie disclosing the identities of the banks that are accessing FEDs discount window. The repo market replaced the feds discount window for this and other reasons- to by pass regulation or ignore it completely.

It was a crisis because of the large amounts and the out of control interest rate arbitrage going on between these banks.

During the FC a large money market broke the buck. An FDIC like floor was put under money markets ($300K?), and FDIC bank’s floor went up to $250K. It is a RUN on anything by those that still have “extra money” to “invest” that our wannabe masters fear worst of all, but they are busy chipping away at that threat.

Make that “save or invest”. Since I’m just a CD, bare land, and Treasury type now I suppose I’m technically just a “saver”, (the land is for passing on if I can).

Fed is extremely fearful that short term interest rates will rise causing the Federal debt to become then very unmanageable and creating economy chaos throughout all monetary systems. However, Fed will lose the battle because market forces will eventually win out and cause rates to rise. They can’t stay low forever. There is just too much world debt not to have some accidental financial panic due to rate increases. What investors should do in that event would be a very good question.

Isn’t it just a matter of supply and demand? I mean there’s an over supply of debt thus it’s cheap, they’re almost giving it away. Some are even selling it at a loss, so I’m told.

Your analysis assumes that in a crisis interest rates will rise. They will do no such thing. They will fall and not rise. The greater the amount of Global indebtedness the lower interest rates must fall. The reason why we have the lowest interest rates in the history of the world is that we have the greatest amount of debt in world history. Any attempt to raise interest rates will crush the economies of the world like a bug.

Buy gold. Only gold can be trusted because it cannot be printed on demand.

Gold is definitely a hedge against ZIRP/NIRP and you’re right, rates are heading there in 2020.

The Fed’s balance slowly, or not so slowly, is working its way back to where it was before the runoff. But it is not QE!

Correct and the guy that called this years ago, Peter Schiff is dismissed as a clown by many so-called experts including I’m sure quite a few who post regular propaganda on here

Peter Schiff is a clown who’s been bearish for 10 years.

There is a lot of ruin in a country and a currency, and DC is committed to finding out exactly how much.

I don’t think I have ever used the term “clown” (clown absolutely terrified me when I was a child; I had a bad case of coulrophobia), but my opinion of Peter Schiff is extremely low and likely to remain so.

Whether I post regular propaganda or not I’ll let people decide, but if that’s the case I hope the Ministry of Information will send a few cheques my way. They have my address anyway. ;-)

isn’t peter schiff the guy who said there was zero chance the fed would ever raise rates right before they raised rates? i don’t need his analysis to know that if i don’t eat my veggies, i will eventually get sick.

He was wrong and right at the same time. They did raise rates, but it caused chaos in the markets. So the fed had to backtrack, lower rates and basically restart QE. What he probably means is “the fed can’t raise rates without destroying the economy.”

Schiff is a clown, a charlatan, perma-doomer.

M2 has been rising. It is higher now than in 1/19. None of these adjustments have stopped the rise.

Well who would have thought that after more than ten years since the 2008-09 Crisis, the Fed still has the same problem that caused it in the first place. It’s the debt problem and there’s no way to hide it.

The main purpose of Repo is to finance Treasuries and Agency. Both are government debt. Treasuries essentially are spent and simply go out into the ether. We pay most Treasuries by printing more Treasuries. But MBS are supposedly paid by mortgages that pay.

The simple problem is a mismatch between lenders and the amount of Treasuries that need to be financed at a very low rate. The market wants a higher rate for lending money but the Fed wants to keep that rate low and within its target Fed Funds rate. So the Fed needed to step in and became the lender at repo.

In my opinion this is a self limiting problem. If the government borrows more than the market can feed it, then the central bank must print the rest. The story always ends up badly because debt isn’t prosperity. It has to blow up sometime as it can’t go on forever. That’s why they are talking about a global reset. Reset of what?

Reset of the dollar, of course…

Yeah, because there aren’t REPO markets denominated in anything else with junk soverign collateral… lol

The dollar vs other currencies seems overvalued, based on several observations. I am no currency/exchange expert, so take that for what it’s worth.

Whether weakening the dollar vs other currencies would also weaken it against commodities is another question.

I think there are plenty of people working on this issue. One who definitely is aware of it is the POTUS.

When people talk about China currency manipulation, as just one example, this is what they are referring to.

Anybody with a functioning brain knew this would be the ineviteable conclusion And Epstein didn’t kill himself

But if you announced it was going to happen you got called a clown or worse. See comments above referring to someone who knew the Fed would eventually destroy the currency to allow the government to default on its debt – this person is called a clown for simply pointing out the “inevitable conclusion”.

Bad things are happening, at this stage its best just to react to the bad things to limit damage to your own wealth and not stick one’s neck out by trying to warn other’s who will turn around and attack you.

Looks like market is going to close green today. I hope anyone who made the mistake of shorting the market in exchange for collapsing currency has unwound that position.

I don’t see what Epstein has to do with finance and investing.

@Van – the sun will stop shining, that’s inevitable too. It doesn’t take genius to see the inevitable. The genius part is getting the timing right. Schiff has been early = wrong since forever. Guys like him and the other financial pundits stay in business because there’s always a fresh crop of people with pessimistic (or optimistic) outlooks who are willing to buy what he’s selling in order to alleviate their own anxieties.

The dollar didn’t kill itself…DC did.

The story always ends up badly because debt isn’t prosperity. It has to blow up sometime as it can’t go on forever.

Why not? It’s worked so far. It got the global economy past the last crisis, so why can’t it delay the next one indefinitely? If the minimum payments can’t be made just issue another credit card to pay off the last one and avoid default. Simply saying that it can’t go on forever doesn’t explain why it can’t go on forever. Besides, if things start going pear-shaped the banks can just foreclose on the global economy and then they’d own the world. It would piss off everybody but the banks would be okay, and that’s really all that matters. They’d be sitting pretty. The crucial insight, I think, is realising that free money isn’t really free. Even at zero interest costs are incurred which must be paid, and they have to be paid out of the real economy, however indirectly. The real economy is finite, has its own costs which must be incurred and must be covered ahead of debt servicing, forcing the system to break down. At that point debt can’t be covered with more debt, the defaults begin, and the dominoes fall. It’s hard to connect the dots when they’re so fuzzy, but I think it can be done. My best guess is 2026, at the latest.

“…debt can’t be covered with more debt”– unless, of course, there is a “lender of last resort.”

The problem will come when Treasuries mature and folks say, “No, I don’t want another Treasury, I want my principal returned.”

Why should the FED care if principal isn’t returned?

The Fed then directly monetizes said Treasuries, or does what they are doing now and buys from a direct dealer after a few days, giving out cash to pay that principle. They’ve already found their work-around.

> principal

Very true, the avg maturity date on HY is 2025-09-01, and IG 2032-08-04 (including junk but in name only at about 46% rated BBB).

>youtube-dl -f mp4 ‘ytsearch: The Fed Has Few Options, Says Danielle DiMartino Booth CFA Global Investors’

> 35-38 min

> non covanent -> from 40c/dollar in 2008 to 14c/dollar recovery in 20XX

> covanent -> from 71c/dollar in 2008 to 60c/dollar in 20XX

And with 80% non covanent, the issue is do you want to wait till these mature to get your 14c/dollar if the economy turns down before 2025?

2026 at the latest and for how far down??

And what is your best guess for the soonest, especially when considering 1. the likely effect on the 2020 election; 2. the likely agreement last week or so between the FED and the current POTUS; and 3. the possibility that the current run up in actual costs of construction can be sustained?

I need the info for my construction estimating, especially when I am asked to ”guess” as to longer term escalation allowances.

thanks

Just imagine, if the fed has to step in $USD denom, UST/ABS collateral… what about all those other repo markets using corporate BBB as collateral? How many times have those kind of collateral have been rehypothicated?

M. Singh of the BIS approximates the velocity of collateral to be about 2. That’s rehypothecation here in USA because its limited by law. But not in London. There is no limit to rehypothecation. That’s why Lehman took the money there.

I don’t think the Fed is interested in repo-ing non government or private securities. I don’t think that’s even a player in the 10 classes of general collateral anymore although you see ABS and some other private collateral mentioned in triparty. Over 85% is now government securities, right?

Good stuff.

>Over 85% is now government securities, right?

Who knows, a lot of stuff is OTC, like 55% of JPM derivative book is OTC. I can imagine many players overseas using all sorts of stuff as collateral (example: https://www.bseindia.com/downloads1/corporate_debt_repo_ppt.pdf). Gov securities-as-collateral is probably the tip of the iceburg globally.

It’s got to have a limit. They can’t go on creating an artificial or manufactured demand. It’s already quite crazy now.

Sifma has a good idea about the use of what kind of collateral is used in the different repos.

https://www.sifma.org/resources/research/us-gcf-repo-index-triparty-repo-and-primary-dealer-financing-reporeverse-repo/

Of course, you can’t measure what bilateral repo really does. Also the new electronic houses are large centers and I doubt they report stuff. Therefore repo is like measuring with a bucket with holes.

Yeah, you’re right, there is probably some theoretical limit, but its probably some kind of non linear system with a bunch of variables that aren’t all known (or mostly known) to all players ahead of time.

Sure, it would make it easy for CB’s/regulators to be like: “select ‘ISIN’ FROM collateral_b WHERE rehypothiction_multiple > 1”, and pass some more rules that actors figure out how to skirt via other exoitc means.

I do not have an accounting background, but in my opinion end of quarter or end of year window dressing is fraud because you are not faithfully giving the normal financial accounts of the business. I think Munger said that accounting dishonesty is the worst because you are falsifying the numbers on which people make investing decisions.

If accounting fraud worries you, then you had better not look to closely at municipal bonds.

According to GASB accounting, the states of CA, IL, NJ, NY, CT, MA are all supposedly solvent. At least as solvent as Lehman bros was anyway.

Moody’s thinks those insolvent states can just raise taxes, but all the productive taxpayers can just leave… and they are doing so.

Whenever the next recession hits, US society will be forced (not willingly) to confront the lack of chapter 7 bankruptcy for insolvent states. Massive defaults by state governments, even if the politicians label it something else, are inevitable.

The last time NYC went bankrupt, the politicians called it a restructuring. But NYC didn’t pay in full… it was a default.

No US state has officially defaulted YET, but several are insolvent and use debt to pretend otherwise.

That is accounting fraud.

Illinois — the bellweather state!

‘A democracy cannot exist as a permanent form of government. It can only exist until the voters discover that they can vote themselves largesse from the public treasury. From that moment on, the majority always votes for the candidates promising the most benefits from the public treasury with the result that a democracy always collapses over loose fiscal policy, always followed by a dictatorship. – Alexander Fraser Tytler

Much as I would like to bash New York State, it’s actually fiscally resposible compared to many other states. Their unfunded pension liabilities are fairly low. (below link)

I don’t think California even releases that kind of data, but it’s on the below map too. I’ve seen figures as high as $25,000 unfunded liabulity per individual in California , but it all comes down to how you measure it, and that gets complicated.

ttps://www.federalreserve.gov/releases/z1/dataviz/pension/funding_ratio/map/#year:2017

What are the assumed future returns on those supposedly solvent pensions?

Hint: warren Buffett has far more conservative assumptions for his company pensions, and he has a much better long term investment track record.

The states are insolvent

Wolf,

Sorry, I’ve gone off-topic, but the original article comments are so long now, I thought this would just get lost.

There’s a Jan 2 Market Watch article “A popular Wall Street blogger vowed to never short the stock market again — until now” about your December 30th “I, Who Vowed to Never-Ever Short Stocks Again, Just Shorted the Entire Market ” article. Mostly just quotes with a few comments and a link to your blog.

The most interesting thing I found was he didn’t specify that you were hammered in the dot com bubble, but that you were “destroyed by misplaced bets against stocks”. Because hey, click bait vs what could be learned over the intervening 20 years is so much better for a writer…

Given everything I’m seeing on Bloomberg, CNN, and MSNBC this morning, your timing may be astounding. I don’t really understand shorts enough to say more than that.

After what just happened in Iraq, Wolf’s short is paying off.

Wrong, if he shorted the SPY and QQQ on January 30 he is losing money and the losses are mounting. Give me one reason why stocks would drop today other than ripping off rubes and retail investors.

I don’t believe Mr Wolf shorted anything, its one thing to say but another to do, but if he did he’s losing wealth as the currency he received in exchange continues to drop as measured in stocks.

Looks like market will close green, this nonsense was just a transparent ploy to pull shares away from rubes and it barely worked (market down less then 1/2% midday.

Actually I bought S&P today at the bottom this morning. I will ride it maybe a day or two. Too good to be true.

I was too late yesterday afternoon to buy oil. I was going to, but stuff happened and beat me to the game.

“the Fed has added $412 billion to its balance sheet, the fastest increase since early 2009, when the banking system was on the verge of collapse and the economy in a tailspin.”

Wolf,

This quote sounds like cover for the thievery of the bailouts ….

the cover that’s continuously quoted by the the perpetrators, the FED, Geithner, Paulson, Bush, Obama, Cramer, (the crybabies you call out), etc. ….. but never proven, or even given scrutable support

Wolf, you might be hailed as a genius with the timing of the short announcement on bigger screen. Don’t let the fame change you!

Ha, that’s funny. Hailed as a moron one day, hailed as a genius the next, only to be hailed as a moron the following day… No, I won’t let this “fame” change me :-]

Wolf, I wanted to pull a bunch of money off the table, but was hesitant. After your post about shorting the market, I did. :-)

Insanity! If you sold your stocks what did you buy? The SPY pays 1.5% yield, you would trade that for a T-bill that pays 1.5% or less? Bonds are, in effect, currency and are not a productive asset (your yield is below inflation and does not grow over time).

Shorting stocks is market timing and, unless you have inside information, market timing is a fools errand – this has been proven repeatedly.

Many here are angry by the actions of the central banks, I suggest you not let your anger cloud your judgement. Do you think Buffet sold anything short on December 30? Do you think you’re a better investor than Buffet?

Shorting stocks last week was a bet on red at the roulette wheel but the ball landed on black. The house always wins (yes the game was rigged), accept the loss and walk away from the table before you gain a bad habit.

Just my humble opinion, but an opinion formed after losing at the Fed’s game – I will never bet against those guys again.

I agree with you about the FED. As long as the FED can print money with impunity, this money train is riding this rail all the way up to the station- so to speak. IOW, the central banks are ensuring that the top 1% take ownership of the entire S&P privatizing the entire economy, no matter the cost, the this class will be owning the earth and it’s resources in feel simple terms.

This is a watershed moment in history for the American economic system- will privatization lead to a system of peasants and lords or will it go the way of socialism/communism.

Wolf: im struggling with posting replies in the correct thread. Please delete the other post I copied at the end or start of the thread. Sorry. /-:

No, I won’t let this “fame” change me :-]

You’re fine just the way you are. Since you’re not running for office, founding a religion, or working out your karma, you don’t have to be all things to all people.

I’m okay with languishing in my pretensions, thanks for asking.

wolf, i don’t know, if you are right about stocks, but you were right about trader joe’s blueberries! i now add them to my homemade yogurt. delicious!

Seems I’m right about what really matters :-]

Look at today’s overnight repo= $51.150 billion.

Back to Dec 17th when repo was above $50b a night.

The embers are still lit.

Well, give it a few months. The various reasons and pretexts to goad the Fed into cutting rates, worked. And they will work again.

Plus, now they got the Fed to launch QE4ever.

We will some new reason to cut rates again. Someone has a hangnail, woke up on the wrong side of the bed, doesn’t like the color of their hair. There are always REASONS to justify cutting rates. It’s like a cycle.

Someone said the Fed isn’t done cutting rates until they are zero.

I agree.

We may have gotten the black swan of 2020, on Jan 3rd no less….

Wolf, I really wonder if the whole Repo thing wasn’t just a bankers strategy to get free or cheap money? In other words, no crisis, other than they might have to pay up and take a profitability hit. Now no hit, just more money to speculate with, and make rather than lose money, win, win for the banks. Moreover, In a world where the taxpayer is never told who the parties are or the terms of agreements, this is perfect for the banks. Just cry havoc and then the Fed throws you money and hides any details that makes either party look bad.

Augusto,

“I really wonder if the whole Repo thing wasn’t just a bankers strategy to get free or cheap money?”

Yes, I’ve been wondering about that too, from day one. By refusing to lend to the repo market, the banks (a handful of big ones) knew what they were doing and what the consequences would be, and that this would be a good way to stimulate Fed action.

So if the banks do what the Fed think what banks ought to do, why not nationalize them?

What’s the point of private banks if they don’t do what banks do and then keep all the profits to themselves by not doing what they’re supposed to do?

Socialize their profits not just their expenses so to speak.

And, there must be responses the Fed can do short of nationalization:

Stop paying bank interest on their reserves completely, or target specific banks that shun the repo market and not pay just those banks.

I’m sure their are other actions the Fed can take, short of nationalization.

But nationalization seems the most direct, logical response.

That, or breaking the bigs bank up into dozens of banks.

The horror of taking a stick to the Master of The Universe. Why must it always be carrots and sugar?

Because the Republican party is completely bought and paid for (we have a billionaire president for God’s sake!)

Half the Democratic party is bought and paid for.

And the few politicians (Sanders, AOC, Warren) who’s primary policy platform is putting the middle class back in charge of the country is obliterated in the press. …the same press all owned, from Fox News to CNN to the NYTimes, by the 400 billionaire families.

It’s mob tactics – take the billionaires bribe money or they’ll break your kneecaps 24/7 all the way fr Fox News to the NYTimes opinion section.

The only way for the truth to get out is on the internet in places like this. And the only way to fix the problem is realizing we have 300 million votes and they only have 400 votes and voting in politicians who will take the fight to the billionaire class (and stop voting in billionaires to be president!!!)

Yeah they could repo with the Fed, then relend at triparty, GCF FICC, and bilateral for a easy spread.

Look at the h.4.1. 1A. Memorandum Items.

Securities lent to dealers $41.450 billion overnight.

When the Fed lends out its Treasuries, this can be looked like a reserve repo. It really is lending out securities overnight for CASH. I could be wrong but I believe the rate is 1.45%.

Suppose that security was on special (like a new one that just came out of SOMA addon). How much can a dealer charge to lend out that security again for repo purposes since repo is at least 1.55%?

Wolf:. I don’t suppose we should overlook Mr. Dudley’s August call for his former staff at the New York Fed to create a recession as a possible explanation for September Repo crisis?

The USA has been a socialist economy for 20 years except it’s the stupidest type of socialism imagineable. We have socialism for the rich and pain& suffering for the middle class.

In USA socialism the middle class pays way higher tax rate than the rich. And then on top of it they’re stealth taxed with zero percent interest rate policies and huge national debts.

And where does all this go? Does the middle class get checks from the government? Does the middle class get to take out zero percent loans?

No! All that money is used to subsidize the rich.

If a middle class family needs to use a credit card and the rate is too expensive can they get it lowered? No, that’s an issue of personal responsibility! But if banks, hedge funds, and billionaires need money from the repo market and the rate is too high the conservatives use socialism to lower the rates down for them. You don’t get those government-socializes rates, only the billionaires do.

If a middle class family loses their job and can’t afford the mortgage payment then that’s an issue of personal responsibility and they shouldn’t have bought a house they can’t afford. But if a rich person buys mortgages who can’t pay up does he lose money on the deal? No! The socialist conservatives buy his bad loans.

If a middle class family needs a loan to go to college do they get 0% interest rates? No, only the rich and powerful get those socialist interest rates from conservatives. For the middle class it’s a lifetime of debt.

If a middle class family struggles, succeeds, works overtime and has a good year financially do they get low taxes so they can realize the gains? No! Only rich people like donald Trump get “carried interest” loopholes to avoid tax and Amazon pays no income tax. Amazon’s trucks tear up America’s roads and bridges but the damage is socialized and the middle class worker pays the taxes to fix them – Amazon gets a free pass.

It’s funny that you think there is a good type of socialism…. or that socialism somehow doesn’t ALWAYS favor the most politically connected.

Before the Soviet Union collapsed, did the politburo members live impoverished like the working class?

Venezuela’s Hugo Chavez wore fine custom tailored Italian suits, while average Venezuelans struggled to find toilet paper.

Bernie Sanders voted to shove Obamacare down YOUR throat, but like pelosi and Obama, sanders has congressional medical care (unlimited benefits, no deductible, paid 100% by taxpayers).

That is socialism, in all countries. If not for political indoctrination in US colleges, Bernie wouldn’t be taken seriously.

Socialism is all about the most politically connected exploiting the masses… ALWAYS. This time is not different

Socialism is all about the most politically connected exploiting the masses

Corporatists exploit the masses. You might like to wade through the archives here until the evidence persuades you.

Cold Water, you also forget to add, “(but) let not your heart be troubled.”

Hannity ALWAYS does after he points out exactly what you did.

To “A”….”the stupidest type of socialism”. Not if you are nearest the spigot of the FED…it is criminal, not stupid. But the people refuse to lead so the leaders won’t follow. The masses (asses) would rather be zombie shoppers and continue borrowing to buy crap. In fact, we’ve all heard that the vast majority of Americans cannot pay for an emergency of say…$1500 to $2500. So, the banks issue more credit cards…I’m not joking when I say that our cat (her first name with our last name on the letter) received in the mail a few years ago a credit card application….To this day, I don’t have enough knowledge of that system of how that could even happen? The secret, in my view, in leading a simple life free of stupid consumption by clearly knowing the difference between needs vs wants. The line is so blurred now and all the advertising is directed and blurring it even more. So, the “stupid socialism” (read criminal and immoral socialism) will go on until it finally crumbles at some point with lots of pain to go around. Personally, I have done and continue to insulate myself and family to the greatest extent possible. Gird your loins !!!

The secret, in my view, in leading a simple life free of stupid consumption by clearly knowing the difference between needs vs wants.

Very true, but I’m still keeping the schnapps.

of course the schnapps, not to mention the limoncello…gotta have a few simple pleasures….which are good for the spirit…no pun intended ! Just don’t want to go into debt for it.

Heads-I-win-tails-you-lose (for the already-wealthy) isn’t socialism but it certainly isn’t capitalism.

A good first step would be to overturn Citizens’ United, and since the Supreme Court won’t do it, the only option is for citizens to actually unite and take down the cronyists in both parties at the voting booth. Corporations can buy speech but if enough people get angry they can’t buy our votes.

Wisdom Seeker:

Not to far into the US future the general public will realize that “voting” is not going to “remodel” our system and then the “SCHITT” will hit the fan.

Personally I feel we are too far gone already; we lie to ourselves, our “elected” leaders lie constantly to all of us; we lie to the world etc. The latest (since ’08-’09) FED policies are just too far out in where even the weeds won’t grow forever and “we the people” will pay dearly.

It’s funny seeing how ‘Socialism’ has replaced ‘Communism’ as the ‘Ultimate Evil’ – the CIA must be changing their ‘evil regime’ targeting to a more western location than before.

Not surprising since a “centrist” Democrat is to the right of IKE, and one need only look to historical tax rates to see a big part of it, if not the biggest. But you are right, they seem to be becoming media equivalents. I’ve seen good articles on this “PR creep” for lack of a better word, and probably saved them somewhere.

An excellent stream of comments. I find Wolf’s articles and the comments are best after several days, I learn more, and find more people with the same take on things (and different ways to word them) that I have developed over many years, much study, and many experiences.

I believe the current funding problem is mortgage funding by non-banks such as shadow banking. Non-banks are doing 90% funding of all mortgage loans.

Before 2008 real estate crash, commercial banks were doing the majority of mortgage loans. Commercial banks have access to the discount window so they can borrow anytime but at higher rates!

Non-banks and hedge funds do not have access to discount window so they are forced to borrow from repo markets which sets a very fragile situation. Not even commercial banks want to loan to non-banks means trouble brewing!

Factory manufacturing dropped off a cliff last month and it’s a repeat of European malaise of manufacturing! China basically copied high tech manufacturing in Germany and is politely reducing German, South Korean, Taiwan and Japan imports!

Chinese want world domination with robotic manufacturing which will result in world wide unemployment in the name of 1% and their greed!

Stock market crash will come when the 1% panic with realization their unfounded greed catch up with them! Public pensions might fail with unrealistic property tax increase on yearly basis and this will force public bankruptcy. It will happen but when?

Foreign banks use RRPO; Fed gives collateral in exchange for cash. Charter banks use REPO; Fed takes collateral in exchange for cash. The carry trade goes through NYSE and the paper is monetized for purposes of government spending. Like giving your paycheck to the bartender and telling him, “give me whatever is left when I need it..” Jerome kicked it up to 50B this AM. Troops in Kuwait.

America’s response to Iranian attacks is rather mild,

in my opinion.

The Fed’s bailout of shadow banks has introduced

some incredible moral hazard; comparatively,

tent cities and food stamps are nothing.

Working the system, cheating, is quite popular.

Working the system, cheating, is quite popular.

It’s a fact of the dynamics of human interaction that those who cheat to win have an enormous advantage over those who do not, given the social conditions which enable it. That said, the Lesser Anthropic Principle more or less now guarantees the final stages of the devolution of your political order.

America’s response to Iranian attacks is rather mild,

in my opinion.

war is the one thing both parties and the media agree on.

will privatization lead to a system of peasants and lords or will it go the way of socialism/communism.

You already have a system of peasants and lords, and the lords have the will and the technological means to make it permanent. A lion doesn’t concern himself with the opinions of the sheep.

It’s widely believed by historians the the existence of a large and prosperous middle class has only been an aberration of history, brought on by overreach on the part of your overlords (and overladies) which caused them to temporarily lose control. Once they’ve completed converting the New Deal into the Raw Deal they can reverse the Enlightenment and the Renaissance and everything will be back to the way it always was.

“– such as hedge funds or mortgage REITs that borrow cheaply in the repo market to fund long-term bets ”

How is it that these can borrow in the REPO market? These aren’t banks.

The Fed is mandated to provide liquidity in banking emergencies, not daily “bets” by other entities as noted.

Who is watching …. and when did this all change?

Interest rates will rise. They cannot stay low forever.

I think this needs restating: “Reverse repos are liabilities on the Fed balance sheet” and ” A reverse repo drains liquidity from the market”. Liquidity in the market is by definition the liability of the Fed, no? A reverse repo reduces liabilities, no?

The Fed’s balance sheet — like any balance sheet – has three components: assets, liabilities, and capital. The sum of all assets equal the sum of all liabilities and capital. Or expressed differently, assets – liabilities – capital = 0. It balances, hence the word “balance sheet.” Always.

Reverse repos are carried on the Fed’s balance sheet as a liability. Cash in circulation and excess reserves are also liabilities on the Fed’s balance sheet. Treasury securities, MBS, repos, and the like are carried as assets.