Then there are the dividends it pays its member banks.

By Wolf Richter for WOLF STREET.

In addition to a lot of smaller activities, the Federal Reserve does two financially huge things: in 2019, it held about $4 trillion in interest-bearing assets, mostly Treasury securities and mortgage-backed securities (MBS); and it owed banks about $1.5 trillion in interest-bearing reserves. Among its other activities, are its reverse-repo activities, and the costs of its own operations. On Friday, the Fed reported its preliminary results for 2019, including how much it paid the banks ($35 billion), how much it paid the counterparties of its reverse repos ($6 billion), how much it remitted back to the US Treasury Department ($54.9 billion), and how much it paid in dividends.

The Revenues:

The Fed earned $102.8 billion in interest income from the Treasury securities and MBS it held in 2019. This was down 8.5% from the $112.3 billion it earned in 2018, in part because Quantitative Tightening, with extended into July, reduced the pile of interest-bearing assets on the Fed’s balance sheet. It also earned $444 million from “services.”

The Expenses:

What it paid the banks: The Fed paid its member banks (there are over 3,000 of them) interest due on required and excess reserves that banks have on deposit at the Fed. Those reserves on deposit at the Fed — liabilities on the Fed’s balance sheet — averaged about $1.5 trillion in 2019, but had been declining through September. Also, starting at the end of July, the Fed cut rates three times, including the rate it pays on reserves. So the interest the Fed paid the banks on these reserves fell 9.1% from a year earlier, to $35.0 billion.

Note that if banks had not deposited those funds at the Fed, they would have likely bought Treasury securities for at least part of it and would have earned about the same or a higher rate of interest from the US government. When banks sit on large amounts of reserves, they’re going to try to make money off them, one way or the other.

What the Fed paid its reverse-repo counterparties: The Fed paid $6.0 billion in interest to its counterparties on securities it sold under reverse repurchase agreements (the opposite of repos). Reverse repo balances are liabilities on the Fed’s balance sheet. The Fed has been doing reverse repos for a long time. Balances started surging in 2014, peaking at over $500 billion. Then in 2017, balances started declining. In 2019, they averaged around $270 billion.

The Fed’s own operating expenses amounted to $4.5 billion.

Other expenses: The Fed also incurred expenses of $837 million related to producing, issuing, and retiring currency; $814 million for Board of Governors expenditures; and $519 million to fund the operations of the Consumer Financial Protection Bureau.

Net income and where it went:

After it was all said and done (income minus expenses), the Fed had an estimated net income of $55.5 billion in 2019. Final data will be published in its audited annual report.

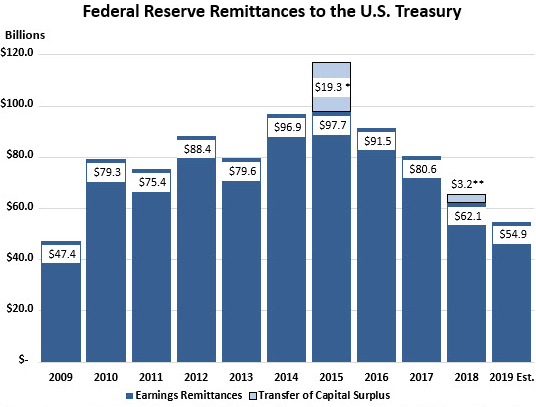

Every year, the Fed remits nearly all of its net income to the US Treasury department. For 2019, it remits $54.9 billion. This is down from a remittance of $65.3 billion for 2018 (chart vie the Federal Reserve):

The circularity: The US Treasury borrows money to fund the US deficit. This borrowing takes the form of selling Treasury securities. The Fed buys and holds a chunk of this debt, and like others gets paid interest on this debt. After it funds its operations and pays interest to the banks and counterparties, the Fed then pays the US government back what’s left over.

Dividends to its member banks. The 12 regional Federal Reserve Banks are private companies whose shares are owned by the financial institutions in their districts. The Fed pays dividends to the shareholders of the 12 regional FRBs. These dividend payments are determined by federal statute. For 2019, the Fed paid $714 million in dividends to these financial institutions.

Though $714 million in dividend payments sounds like a lot, but compared to the $35 billion the Fed paid the banks in interest, it’s practically a rounding error. Anything denominated in millions is a rounding error at the Fed where the big things are denominated in trillions. That’s the times we live in.

My patience has been exhausted. Read… The Wall Street Journal (and Other Media) Should Stop Lying About Repos

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

We live in ridiculous interesting times.

You can’t live on the interest of your savings yet billions are tossed around like candy by the un-elected few. Nightmarish.

Absurd, grotesque,maybe, but nightmarish? Oh no, things can get very much worse. This will no doubt be looked back upon as a kind of Golden Age in comparison to what is to come.

,

We are all of us here well-fed, housed (except for the guy with a van) and clothed: in the coming decade or two, this middle-class comfort (every day less and less secure, of course) will evaporate for most.

Yes, observable prosperity is unpresedented. Everyone expects helicopter money but I propose helicopter money was here for years.

They failed to rain money on me. I had a rain catch out and everything.

Over the past years I have sometimes ruminated that in the future I will be able to tell the young’uns about the days when I could take a hot shower whenever I wanted one.

Savings have little yield when there’s so much money the money has little “value.” The only ways to drain money from the system are losses and bankruptcy. Credit money that simply “appears” could go back where it came from.

Actually there’s a third way, and millions of foreigners are doing it: hoarding cash. All else equal, massive hoarding would create deflation, but the Fed is not playing along. They’re making more!!!

Why is the US dollar like Doritos nacho chips? “Eat all you want. We’ll make more.”

How do we know the Fed actually paid those amounts? What else did the Fed pay in secret? Why should anyone believe ANY Fed reports?

WHY HAVE A ‘FERENGI’ RESERVE AT ALL .. ?? Lotta good they’er doin for .. or should I say ‘to’ .. the mopes.

But if you’re one of the Big Playas .. it’s Gravy Time as far as the lyin eyes can see.

Yes,, where are The helicopter money Bernanke promised If?? Only banks and Wall Street getting it.

It’s a small club.

And you ain’t in it.

Yes. However, the fact that the “Federal” Reserve is the world’s largest parasite is not conveyed by the article. The key point to remember is that the “Federal” Reserve is owned by its member banks with only its directors government appointed from bank cronies, yet can print (digitally create) US legal tender in unlimited quantities without paying ANY INTEREST WHATSOEVER to the US on the legal tender so printed: that is what was done for the QE and Repo market operations.

The fact that it was authorized to do this by its political cronies for nearly a hundred years does not change the huge benefit that the banks thereby can receive. It is as if you could get a credit card from your uncle and he paid all of the interest, so you could charge whatever you wanted at ZERO interest with no fees, and only had to pay back the principal, plus a share of the net profits that you made from the gigantic charges. If the “Federal” Reserve has printed $3.6 trillion as of now, and the FMV annual, interest rate on those sums were 5% (as an example), then it is avoiding paying interest of $180 billion.

If the “Federal” Reserve bank cartel had to go to some independent entity, e.g., the World Bank or IMF, that is the minimum amount that it would have to pay. Also, As reported in the New Republic in “This Is the Fed’s Most Brazen and Least Known Handout to Private Banks” on March 9, 2014, “But you will never hear about the Fed’s direct subsidy to private banks that costs over three times as much as the total CFPB budget.”

“The subsidy comes in the form of a 6 percent dividend, paid on stock that over 2,900 banks purchase to participate in the Federal Reserve system. Very few places where ordinary Americans park their money offer such a risk-free benefit. In 2012 (the last year with available data), the Fed gave away $1.637 billion in dividends to banks, tax-free in the majority of cases. And the Fed has been doing this for the last 100 years. It’s one of the many unknown ways the Fed extends special benefits to Wall Street.”

The Federal Reserve has no right to promote ANY INFLATION.

The second mandate under which they are ALLOWED to operate is STABLE PRICES…(first mandate is maximize employment)

The 3rd mandate is Moderate Long Term rates…..not record lows.(for extreme is not moderate by definition)

Thus, the Fed is in constant violation of two of its three mandates…..and not a word….because it makes stocks go up….and disguises the real cost of massive debt creation by the government. (The Fed is apolitical?)

If inflation is a tax (and it is per Friedman) Congress has that power, not an unelected panel sitting behind closed doors. Would a 2% tax on dollar holdings pass a Congressional vote? OF COURSE NOT. So why do we sit and watch the Fed do this?

Hopefully Wolf will see your comment and realize their hedge fund subsidiaries are getting free money to buy and jack up the prices of the overvalued QQQ’s he shorted. In today’s Bloomberg dot com, two daggers aimed at his heart: “Tesla Tops $500 a Share as Oppenheimer Boosts Target to $612” (by Courtney Dench), and “Apple shares could

Tesla is a minuscule part of QQQ.

And I specifically did NOT short Tesla, and gave reasons why not.

Correct me if I’m wrong — I don’t think I am but I’m too lazy to double check my notes right now — but the dividend is only 6% if the price of the last auctioned 10 year is higher than 6%, so as of now, the banks only receive dividends on their shares equal to the rate of a 10 year treasury. Just go the the federal reserve act and control f the key word dividend. It should only take about 5 minutes

Actually I found it for ya

A) DIVIDEND AMOUNT.—After all necessary expenses

of a Federal reserve bank have been paid or provided for,

the stockholders of the bank shall be entitled to receive an

annual dividend on paid-in capital stock of—

(i) in the case of a stockholder with total consolidated assets of more than $10,000,000,000, the smaller of—

(I) the rate equal to the high yield of the 10-

year Treasury note auctioned at the last auction

held prior to the payment of such dividend; and

(II) 6 percent; and

(ii) in the case of a stockholder with total consolidated assets of $10,000,000,000 or less, 6 percent

https://legcounsel.house.gov/Comps/Federal%20Reserve%20Act.pdf

Yes, it is, and this club is getting ready to be shut down. Not by the authorities, who serve the club, oh no, and not by presidents, judges, or anyone else in the club.

The club has a big surprise coming, one it never, ever considered due to its obscene arrogance.

Yes. They system will begin to operate around the central bankers.

Be it crypto currencies or something else….

the game will have a surprise ending.

1.5 trillion seems a bit much for the Fed to require in bank reserves. Lowering the reserve requirement should relieve pressure on banks needing to borrow overnight money to meet these reserve requirements. That, in turn, would resolve, or reduce, the stealth QE in the repo market.

My understanding per Wolf’s writing is that banks don’t use the repo market, shadow banks and hedges funds etc do. Banks actually serve as repo counerparties and when they wouldnt do the volume needed is when fed ad to steped in sept.

Is this true about shadow banks and hedge funds as the main customers of the repo market? I’ve been trying to understand this facet for awhile with and I can’t find a clear answer. Who makes up a plan to borrow a couple hundred million with the intention to pay the money back, with interest, within 30 days or in some cases, much less? And with some consistency. Is this loan for speculation or a business plan run amok? I’m just confused who gets to take advantage of this scheme?

4 banks own almost all of the excess reserves at the Fed. They can use these excess reserves and LEND at the repo market.

Not directly. The Fed “IS” the charter banks. They are an umbrella organization, controlled by Congress which has certain authorities, most of which are fluid and can be defined according to need. There is a push to bring charter banks under “greater” Fed control. Fed spoke of implementing the next QE using charter banks. At issue is the degree of “nationalization” in the US banking system. Under these new parameters shadow banks will use the “charter” banks as GSEs, to oversee lending practices, (this is same process which blew up mortgages in 08, loan originators were passing bad loans to money center banks.) The change should provide oversight on shadow banks, and buffer the system. It may be some of the charters resent the intrusion, it does in part prove that corporate debt is not going to get downgraded. If backing stodgy corporate paper puts banks at risk, they are also allowed to monetize Treasuries. The issue of reserves is non sequitur. Some like Ellen Brown, http://www.webofdebt.com/ and Tom Steyer want independent community banks as counter to the Federal Reserve system.

You repo for short term money to pay interest on long term debt while you arrange to roll over the long term debt into another loan. If you don’t arrange a new loan you do another short term repo.

I don’t believe that concept of repaying “principal” ever enters their vocabulary.

chillbro,

Banks can but don’t have to borrow in the repo market. Unlike hedge funds and mortgage REITs and the like, banks can borrow cheaply from each other in the “unsecured” federal funds market (no collateral required, which is a better deal), and they can also borrow at the Fed’s discount window. So when repo rates go to 3% (they spiked to 10%), bank would (1) stop borrowing in the repo market and (2) lend big time to repo market. The first part likely happened; the second part didn’t.

But Wolf, in a previous article, you did mention, and specifically, a REIT that was a big player in the REPO market.

How is it that non bank entities have a seat at the REPO table?

@historicus

Repo comes in different flavors, but the main ones are:

GFC repo with the FICC where the big dealer banks exchange goverment securities as general collateral and netting occurs at the end of day with the central clearing party. In 2019, the big members can sponsor smaller members but they must net their sponsored members clearing payments.

GFC repo had agent dealers that keep the identities of borrowers and lenders secret since each deals with the central party instead.

Triparty repo. Has more players where borrowers and lenders repo about ten classes of securities with DTCC as the central clearing party. Because it deals with classes of securities it’s generalized and non specific collateral following the rules of the DTCC.

Bilateral repo. No central counter party. Any two borrower and seller can do it. They make their own rules and agree on any collateral.

In addition to the 3, there is the Fed Repo where the lender is the Fed. It’s it own Repo but it uses the Triparty repo to settle the transaction. Only the primary dealer are allowed to do Fed repo.

Therefore, the primary dealers borrow from the Fed, then they lend others in the GFC, triparty, and bilateral repo. The Mreits can borrow in the triparty or bilateral from the primary dealers.

Just like India, we have stratas and classes at repo.

From what I’ve read the Fed repo window is primarily used by banks, while there exists a second type of repo facility used by hedge funds. I’m not sure if the hedge fund repo facility is sponsored by the FED. It may be private.

If Wolf could give some clarity on this I’d be grateful.

Blue Light,

There is no “repo window” at the Fed. There is only a “Discount window,” which only banks have access to.

@blue light

The Fed only really deals with primary dealers

https://www.newyorkfed.org/markets/primarydealers

when it repos.

But the Fed also regulates BANKS and require them to have RESERVES. Banks can loan each other by borrowing reserves at the Fed. But that is a small compared to repo.

https://apps.newyorkfed.org/markets/autorates/fed%20funds

The real market between overnight borrowers and lenders is the repo market run by the DTCC called Triparty (and its subsidiary, the FICC for only Gov’t securities called the GCF). These two are the private centrally cleared repo, where the DTCC/FICC are the counterparties of the lender and the borrower.

The Fed also has a separate repo. They only deal with primary dealers though. So try not to get confused.

Almost all the primary dealers that really matter are owned by Bank Holding Companies, so primary dealers = banks.

I think so many here can be helped by a basic primer on Repo.

I got very confused, too, so I decided to read a lot on it.

While the banks are gambling in derivatives/other investments, effectively government guaranteed, the FDIC has only a tiny reserve to bail out insolvent banks, and other banks are only thinly capitalized (so the FDIC requirement that they bail out sister banks is meaningless), $1.5 billion (or $15 billion, if it were required) would be like using one load of squirrel pee to fight a forest fire. The banks have $250 TRILLION in outstanding derivatives.

Even the banksters are aware of the risks.

The current repo situation is not due to some mysterious and unsaid emergency, nor quarterly taxes, nor the new year “turn.”

It is an intentional mechanism the Fed is using to sidestep laws preventing them from monetizing debt directly – by funneling repo money through crony intermediaries who have enough of the right kind of collateral to facilitate the Fed’s large T-bill purchases. This funds the US budget deficit which is half defense spending.

Term repos make this easy. Correct me if I’m wrong but I think it works something like this:

1. Entity (Bank, hedge fund or reit) sells MBS garbage or treasury instruments to the Fed.

2. Entity uses cash to buy T-Bills.

3. Within the term of the repo or generally a few days, the T-bills are flipped to fed.

4. Entity bags guaranteed risk free profit.

5. Entity repurchases collateral.

6. Repeat steps 1-5.

Seems the Fed is using its repo market to monetize national debt, enrich their bros on the street, and simultaneously suppress interest rates. WHat a racket!

Nope.

Defense spending as a percentage of Federal Budget – 15%

Entitlement spending as a percentage of the Federal Budget – 62%+

“This funds the US budget deficit which is half defense spending.”

https://en.m.wikipedia.org/wiki/United_States_federal_budget#/media/File%3A2018_Federal_Budget_Infographic.png

2banana, that’s a big Negatory on all fronts.

Most of social spending like Medicare and Social Security are not only self funding, they run massive surpluses.

Your total libertarian 100% BS ignores that these programs have taxes incorporated into the from their original conception into law.

Please identify which or our military wars, military armies/navies/air forces, which or our military budgets and weapons programs have taxes directly linked to their budgets at their point of conception into law?

You can’t.

Because our military is 100% non funded except through deficits or the income tax.

I would recommend you check your predilection for libertarian

Fake News at the door. Because if you don’t, sharks like Timbers Bimbers will eat you alive.

“Most of social spending like Medicare and Social Security are not only self funding, they run massive surpluses.”

Timbers,, you got that way wrong,,,, they may have run massive surpluses in the past but no longer,,,, certainly you have read or heard of government reports that SS (2035) and Medicare (2026) will run out of money … they presently are spending more than they take in…

And those are the “optimistic” official reports…

BTW,,, can’t believe you are too lazy to do a simple google search for such info… Also note… way long many years ago, Supreme Court made two important rulings,,, SS and Medicare taxes are just that, and not insurance premiums, and two, government can change what they give you, including making it a big fat ZERO…

Personally will live long enough to see both of these programs go belly up bankrupt… will enjoy every moment watching these two giant ponzi schemes die…and oh yes,, don’t forget,,, those other entitlement programs, medicaid for example, aren’t financed by anything except government borrowing.. Lots of it,,

Top-Gun

No, I am 100% correct. Every penny of Social Security and Medicare are pre-funded by a tax. They have huge surpluses.

Mr Google is filling your head with falsehoods.

Not that you know this to be true, it is YOUR choice to break out of your Fake News Bubble.

In contrast, as far as I know not one single penny of the military is pre funded in any way.

The military – not social spending – is the Number One cause of spending related deficits.

I said that at $740 bilion the defense budget is half of the $1.4 trillion U.S. budget deficit but I get your point.

Otishertz

The military war and aggression budget is most definitely not any place close to $740 billion.

It is probably closer to $1.5 trillion/yr.

Official US government claims of the military budget are false. They do not include classified military, war and aggression, and security spending which at the very least is hundreds of billions a year.

Ok, I was wrong. $1.4 Trillion was the amount of the Spending bill that passed on Decembber 19..

The budget deficit for 2020 is projected around $1.1 trillion so defense spending is 67% of the budget deficit.

defense spending is 67% of the budget deficit.

That was years ago:

https://www.globalpolicy.org/component/content/article/153/26227.html

It is higher now. But you could also argue that very little of that is actually for what is euphemistically called ‘defense’ because most of it is to maintain and extend a global military empire.

Similarly, Federal Reserve and Federal government financial operations are organised to maintain and extend a global financial empire on behalf of transnational corporations with no allegiance to any country, certainly not the US. That said, you could also argue that the US does not really have what is euphemistically called an ‘economy’ because it is essentially a self-serving collection of international corporate racketeering operations.

The US Social Security program is a trust fund. It is managed by the US government separately to protect it from the corporate predation afflicting all other federal financial operations. Obviously, corporatists like to whine about SS and other social programs because they want those trillions too, even though they still get all of it when it is spent. Still, they prefer to control those trillions more directly by cutting out the middlemen, having the right pretexts to turn the rest of the US into Haiti.

All will be revealed once they drop the pretences, which you have to admit are pretty flimsy anyway.

Arg,

I hate it when people blame defense spending for taking half the Federal budget. The real truth is that 50% figure comes from the DISCRETIONARY part of the Federal budget.

Discretionary Defense spending actually made up just 15% of the TOTAL 2019 Federal budget. Another 15% of the Federal budget made up the rest of the discretionary part of the Federal budget.

70% of the Federal budget is MANDATORY spending –

Social Security – 24%

Medicare – 14%

Medicaid, CHIP, ACA subsidies – 12%

Interest on debt – 9%

Other mandatory -12%

https://www.cbpp.org/research/policy-basics-introduction-to-the-federal-budget-process

Moral of the story: if you REALLY want to cut Federal spending, you don’t bother with cutting Defense spending, since that’s only 15% of the TOTAL Federal budget, what you want to do is throw Grandma and Grandpa to the wolves, since Social Security and Medicare make up 38% of the TOTAL Federal budget.

Gandalf, you win the:

100% Fake New Post.

And your post is a big Negatory on all fronts.

Social Security and Medicare not do NOT contribute a single penny to deficits, they in fact contribute huge surpluses.

Most of social spending like Medicare and Social Security are not only self funding, they run massive surpluses.

Please identify which or our military wars, military armies/navies/air forces, which or our military budgets and weapons programs have taxes directly linked to their budgets at their point of conception into law?

You can’t.

Because our military is 100% non funded except through deficits or the income tax. I

Funding the military is a necessity.

Funding endless wars with no mission, with deficits that are absorbed by the Fed….that is not good.

Imagined if perpetuating endless wars was cost prohibitive….

Sometime in 2019 or 2020 Social Security (including all things under the SSA) the net cash flow of tax receipts and disbursements becomes negative.

“The shift in 2010 from primary surpluses to primary deficits was notable because it marked the year in which taxes under pure pay-as-you-go financing would have risen above currently scheduled tax rates. In the era of primary surpluses that has now ended, the baby boom generation paid higher taxes than it would have paid under pure pay-as-you-go financing. In the era of primary deficits that has now begun, workers (including many born after the baby boom) will pay lower payroll taxes than they would have paid under pure pay-as-you-go financing of the same benefits.”

Current article at: https://www.ssa.gov/policy/docs/ssb/v75n1/v75n1p1.html (Social Security Bulletin > Vol. 75, No. 1)

Gandalf,,, you are 100% right…

Timbers on the other hand is very wrong,,, don’t know why he would want to spread the LIE that entitlements are fully funded with massive surpluses… that are ponzi schemes and will blow up… and BTW, there are a lot, every State, of other retirement ponzi schemes that are underfunded ponzi schemes, both public (Chicago city and State of Illinois ) and private (multi state employer funds) teamsters for example…

Absolutely right, thanks for a definitive statement.

Gandalf,

There is a difference between the *budget* and the *budget DeFiCiT*

I thought this was self evident.

That defense budget comparison wasn’t even part of the whole point of my post which you completely sidestepped.

Sorry, I thought you were 2banana but the same thing about budget vs budget DeFiCiT still applies.

You are spot on, otishertz. Libertarians conjure the deficit spending, not accounted for by previous or present tax revenue, as equal or a sum of the total federal yearly outlay. I bet they don’t do that with their personal budgets! “So I want to gamble more, then I must drain my savings, (entitlements) to further my vice”. If the S.S. trust and Medicare trust had been receiving the same interest as the banks and F.R.B. for all these years, the projections of a shortfall in the trust wouldn’t exist. Entitlements are taxed immediately or before receiving them, unlike WW2 or any defense expenditure. Heck, War bonds helped pay for the huge defense budget in the 40’s, not taxes.

I find it hard to believe a military that “runs out of bombs” because of how often it uses drone strikes is cheaper than SS. You should look into how much money is spent on fueling those drones alone, it’s insane.

Isn’t that where all that See EyE Ay Afghani heroin money comes into play .. off-the-books funding .. for whatever Chaos du jour needs to happen … you know, like cookies, color revolutions, and assassinations ??

Yeah, but the savings rate in the US is about 2-3%, Seems insignificant to me but it also is Huge HuGe Yuge yooooge money on the “sidelines” or so I’m told on TV.

Right. The Fed cant directly take down auctions…

SO they must operate through dealers that will then get a cut, and what is really going on will be disguised.

Three dots…the Treasury, the Fed, the dealers…and we are supposed to not see …not connect the dots?

Three dots.

Are we electing representatives or turning over ownership of the country to our ‘Leaders’.

How do you think someone who never had a job (except as a community organizer) and, as president, earned $400,000/year for eight years, can afford a $16 million beach front vacation home?

I guess he had a pretty good down payment!

I generally don’t get baited into politics, but I find it particularly annoying when people misstate facts. Because the person you’re talking about did in fact work as a community organizer for some time before law school, but then went on to become a practicing attorney, law school instructor, state senator, and US senator – these jobs all making up far more of his life than some post grad community work. But, I guess we should all just assume this is the only time you’re making things up out of whole cloth and take you seriously the rest of the time. Cause this is just a little fib to make a point about wealth acquisition. Am I basically on point?

Wolf, I love your site but I gotta stop scrolling down. The facts diminish the further I go.

“Wolf, I love your site but I gotta stop scrolling down. The facts diminish the further I go.”

True.

I scrolled down with my nose plugged, and finally decided to post this reply to 2nd Banana.

Entitlements, he said….take up the vast majority of the budget.

Definition Entitlement: “the fact of having a right to something.”

The only entitlement I see in this article is the expectation that banks will be protected at all costs, and the FED is an agent to get this done. All the political arguments are diversions to divide and conquer and ensure money continues to flow upward.

“Well, we’re going to start in a couple weeks with our budget adjustment bill. The first step is we’re going to deal with collective bargaining for all public employee unions, because you use divide and conquer.”

Scott Walker

“If you make people uniform, you can control them. If you teach people to read, and think, and question things, you lose control. So, the best idea is to separate people if you wish to maintain a monetary system. It’s called divide and conquer. By dividing people, they’re not a threat, you can control them.”

Jacque Fresco

But if you can teach them to read and not-think, even better!

Universal education has always been viewed as a means of control, not a gift from benevolent fairies.

But we can take comfort from Solzhenitsyn, who said that even in the worst system there will be sane and decent people who make life bearable.

Like the artillery colonel who shook his hand when S. was arrested and sent to the gulag: that simple human gesture could have got the colonel killed, but he still did it. Now that’s a man.

Those that argued above should simply look at their pay stubs and look at the lines stating FICA deductions.

Both Social Security and Medicare. No point arguing.

But, but, but, he has a Nobel prize!!!

In the last twenty years, bank assets increase 2.2 times; but C&I loans only increased 1.89 times.

The amount of Gov’t. Securities banks hold increase 2.76 times and CASH (includes excess reserves) increase 5.01 times.

I forgot, and they can’t even get repo squared away despite all these trillions.

Top-Gun,

No, I got that 100% correct. It is you who are wrong. These programs not do NOT contribute to deficits, they have MASSIVE surpluses.

Please explain how a surplus is a deficit, let a lone a deficit so large it is 24% of the total deficit!

Also, any future short falls (which are not deficits) are due deliberately freezing the revenue side below what it was planned to be.

I would recommend you:\\

1). Brush up on arithmetic.

2). Stop reading Fake News and start reading Reality Based blogs.

Yeah, he’s speaking in the future tense and not addressing your statement in the current time frame to which you referred, timbers.

“””Certainly you have read or heard of government reports that SS (2035) and Medicare (2026) will run out of money “”‘

That quoted 15 and 6 years from now.

He quoted that twice in one minute, lol!

It’s the Treasury that has the short term liquidity crunch because it switched its funding to short term T-bills.

The repo market is the mechanism that allows the Fed to conduct arms length transactions and circumvent the law intended to prevent direct monetizatiion.

The Fed can’t buy the debt directly but it can buy the debt from its crony homies a few days later no probs and finance it with a nice vig to boot. A bit a farce but there you have it.

The repo market will only grow over time because the needs of the US government for short term financing will only grow.

Agree. Therefore treasury kind of dictate fed policy (indirectly, via market). And this tbills mature around summer I think.

Does repo has anything to do with

Fed financing federal debt…

Since September, Fed balance sheet has grown nearly by the same amount of US Federal debt growth.

https://fred.stlouisfed.org/series/GFDEBTN

https://fred.stlouisfed.org/series/WALCL

Dealers buy tbills.

Fed buy surplus tbills

The Fed will never unwind its financial interventions for the same reasons the proposed ‘down payment’ on the US federal debt by POTUS 42 was so soundly rejected twenty years ago: transnational corporations want governments and quasi-government agencies to take on stupendous debts, hand over those trillions to them, and leave the 99% holding the bag. Money laundering is perfectly legal if it’s big enough.

As the Ancients observed, steal on a small scale, and you are a ‘bandit and pirate’; on a large scale, you are king or emperor……

Just out of curiosity, how much money did US banks pay in interest to everyone who had a checking account or savings account last year?

Interest rates on checking accounts are usually zero these days, and if any is paid it’s rarely more than 0.5%.

Savings accounts are getting maybe 1.5% at best, often less.

I wonder if the average “little guy” savers with hundreds or a few thousands of dollars in their local banks are getting paid significantly more than the Treasury gets from the Fed.

To look at the big picture, when the Fed can literally create trillions of dollars at will and hand it out to whomever it damn well pleases, a few tens of billions of dollars in interest payments are very small potatoes indeed.

The Fed has greater financial power than Congress, as the federal government spends “only” about 20% of GDP per year. The Fed can create up to 200% of GDP in any given year, out of thin air, at will.

The ability to control THAT much money is the real power in the US today. If the Fed gives the Treasury a few crumbs that are left over, it’s really more of an afterthought rather than much of a benefit.

The banks that own the Fed simply couldn’t get access to that much money in a truly free market for money, with the premium needed to compensate for the risk of losses correctly calculated.

They are paying a pittance for the power that they exert over the Fed, and by extension over the entire planet.

That’s easy. Interest on reserves at the Fed is 1.55%. Interest high yield on the 28 day T bill that you and I can buy is about 1.5%.

I think what Ensign is trying to say is how much is the total interest paid to all the average people. Individually they don’t have much but there’s a lot of them. There are way more people that don’t know what a T-bill is than people that do.

Thanks for clarifying. This is a very good question then.

Banks pay close to nothing. So here is how I do it.

I compute the minimum amount I need for a payment balance monthly. At that is the level (plus a small buffer) I keep as a minimum at the bank.

The Fed actually had a PAYMENT CLEARING RESERVE requirement a while back.

But the concept is similar. I need a bank account to write checks, do ACH, etc. In other words a source and sink for PAYMENTS.

Anything else is SAVINGS. To earn some interest, I put my savings in Treasury Direct and link it to my bank account. You can spread investing in T bills maturing in different weeks to improve your liquidity.

Sometimes, I keep a CASH balance in my Treasury Direct Certificate of Indebtedness (CofI) account that earns no interest, to stage where I want my savings to go and and act as an emergency buffer because it is safer than the bank and can move to the bank within a day.

Hope this helps.

Exactly Iamafan. One should only keep what is immediately necessary (plus a buffer) in a checking account. The rest of the money needs to move seeking yield versus risk. Bummer, but that’s the way things are. A couple of times a month I move what’s needed into the checking account to cover disbursements. Credit cards (paid off every month) and electronic online banking makes life easier. But I think quite a number of people can’t be bothered.

I’m with you on that because holding “cash” in individual demand deposits is a service now for the banks. Current payments are the only reason to have a checking account.

Banks don’t need your deposit to make loans with all the fed facilities and bailouts available to them. They could care less about your hard earned deposits. Take .05% peasant. /s

Thus we have negative real interest rates (and nominal). People are now paying for the use of cash. Look at it like a transaction fee. NIRP is a transaction fee like putting a quarter in a video game.

The only value in a modern currency is it’s transaction value. Currency regimes are walled gardens where you pay to play. Fiat currencies don’t store value but destroy it by design.

You know if the Fed really wanted to help the little guy all they have to do is set some rules around minimum interest rates on savings accounts and place limits on bank charges. Otherwise, no free interest. I get so tired of the lies, they are so concerned about “savers”, or worries about socialism and MMT. And all the while in between the song and dance of hand wringing, moans and groans, they keep paying the banks more. Of course these banks and hedge funds that benefit from their largesse is where their friends work and where former Fed officials will go in the future. Ordinary people, savers, just so much carpet making material

If the Fed wants to help the little guy, it could offer us a bank account with same day electronic payment abilities and pay IOR on my balance.

Yup, fair is fair. I’m perfectly willing to accept the FED’s IOER rate on quite a bit of my savings, provided they are backed by the FED itself and not some insolvent FDIC.

Better yet, I’m a repo player:

let me PUT dubious packaged mortgage investments on the books since 2009 to a guy, call him the Fed. That guy then gives me 100% margin on my “collateral” to speculate on T-bill flipping to finance the treasury and guarantees a risk free return to keep the monetizing of US debt rolling.

You can look at this a couple of ways:

1) In 1929 and 2008, the banks, in their arrogance, still did not know what they were doing and caused the immense crash and pain for the middle and poorer classes. Today, the Fed will save us all because they have all of the knowledge and enormous computers to prevent what happened in the past. Trust technology and the Fed!

2) There is a 1% capitalist cabal that will win this game of Monopoly at ANY cost. We will become India and China where there is IMMENSE wealth at the top and people dying Down By The River with no money to bury them.

IMHO: Who drives up the deficit by Trillions to drive up the stock and housing market by lowering interest rates during supposedly the “Greatest Economy Evah”?

The homeless “Down By The River” side of #2 seems to be growing. It is probably a safer bet.

The repo crisis is caused by the Fed paying interest on excess reserves, which they began in the GFC and never stopped. See https://osf.io/preprints/socarxiv/ve3uw/

If the Fed did NOT pay IOR, excess reserves would leave the Fed and simply buy Treasuries. The Fed will be forced to accept Treasuries for cash. Massive Repo. Make sure you understand who is the boss – the Treasury is the government’s.

Should we be concerned that excess reserves would leave the Fed and simply buy Treasuries? How would that hurt us?

And, why would the Fed be forced to accept Treasuries for cash?

REPO today is 60B, 20B more than Friday, which is very close to QE under the previous program, 85B. Of course they can drop it 20B tomorrow. If 10B is seed money on Jan 1, and I raise it to 20B and hold it there until the 29th, then reduce it back to 10B, is it 10B for the month? By the recoursing method REPO is nothing. It all gets paid back. So why do they keep bumping it higher? We should figure how much the limit is raised and for how long, because clearly having more today than you had yesterday means something, even if you do pay it back.

Very good comment.

Yes, REPO must be paid back.

Overnight is easy to compute since you need to repo the same amount (or more) tomorrow.

But TERM repo is tricky because what was issued up to 42 days ago suddenly has to be paid back.

Therefore, in order to provide liquidity to the repo, the Fed has to buy Longer Term securities and stuff them to (eventually) bank reserves.

That is the design of our monetary system today. We need a massive amount of excess reserves (maybe 1.8 to 2.0T) to keep the scheme going.

Eventually the Fed will have to make the over $200b repo fund PERMANENT while keeping the Treasury TGA high at about 400-450b (low of 200-250b), and Reverse Repo at 250-300b. If the foreigners buy LESS Treasuries at auction, expect the numbers to go up. I think tax cuts may be quite interesting.

This is accounting and finance 101.

Right on Iamafan.

Much as a snowball rolling downhill keeps getting bigger and bigger. Then it hits the bottom.

“Fed will have to make the over $200b repo fund PERMANENT” Either Fed has gone completely over to the dark side, bending to insane policies they have publicly disputed, or Fed is morphing into a central bank authority. Fed REPOs the charters who in turn buy stocks, and then Fed makes the facility permanent. The stocks are closely held on THEIR balance sheets, they have GSE backing. We are all one entity, your reserves are my reserves, kumbaya. Maybe JPM wasn’t singing when rates blew up.

Back to your observation this morning repo = 60.725B.

You know why?

Because YESTERDAY’s repo was 40.875B AND

a 25.000B Term repo done last Monday, December 2, 2019

matured.

Therefore they need more than 60B of new money.

They are now scraping the bottom of the barrel of liquidity.

LOL

dark humor appreciated

on that note, I think I need to go now and listen to my Ezio Pinza CD……

Here I sit watching my trees grow in girth and therefore in value, independent of their vacuous fiat price….and enjoy the deep deep discussions about the vacuous money system …

If you look at the POMO this morning, all the outright Coupon Purchases mature after 2040.

Maturity/Call Date Range: 02/15/2040 – 11/15/2049

Are we thinking that far ahead?

We are thinking that that’s so far ahead we don’t have to worry about it now. We’ll just fix it when we get there. Same as it ever was.

Just in case you haven’t noticed, this morning’s 13 and 26 week auctions got the largest ever recorded Fed SOMA Addons ever for this term.

The 13 week got 2,965,307,700 and the 26 week got 2,541,692,300.

Why is the Fed doing ROLLOVERS in short term T bills?

Because the latest Not-QE T bill purchases are already MATURING and the Fed has all the intentions to roll them over.

Watch, there will be a new Operation Twist because these really need to be kicked down the road a lot longer. The Fed can secretly do QE by doing NOT-QE + Operation Twist.

What about the yield curve?

The FOMC has managed to suppress long term rates for ten years now. They are now working on the short term rates absorbing the excesses to suppress rates. One overlooked point in the Repo market is the very short maturity dates. By providing cash, the FOMC is effectively giving them time to mature or turn to cash at or before expiration. This points to a very interesting phenomena and that is the shortage of cash or liquidity on a daily basis. Remember that a transaction must be turned to cash to book a “profit”. This is very suggestive to where we are in the credit cycle.

Debt ceiling jump ==> $400B in the bank.

1) FRED : US Treasury General Account Deposit , Wedsday :

2) On Wed 1/30/2019 @ 411.4B ==>

3) But on Wed 8/21/2019 the war chest is down to 131.4B.

4) Repo rates crisis on Sept 17.

5) On Jan 1st 2020 404B // $SOFR was 1.52%.

Currently up to 1.55%.

1) The Fed isn’t the only player in the repo market.

2) 200B FED/ 4,000B market is 5%

Foreign entities borrow both from the FED and the Repo

market.

2) From the FED :

FRED : Reverse Repurchase Agreement Foreign Officials

and International Account, Wednesday :

3) On Jan 8 2020, the latest reading, 272M, Millions.

4) The peak was on Sep 18 2019 @ 306M.

5) The trend is definitely UP.

From 2005 til mid Sep 2008 a TR low level of : 22M – 40M.

6) A jump to 89M in Sep/Dec 2008.

7) A TR between 2011 til Dec 2014 : 85M – 105M.

8) Since Dec 2011 til Feb 2016 a vertical jump from

under 100M to 250M. Who is in troubles?

9) A TR was form until Apr 2019, but from 10/10/2018(L)

a significan jump from 215M to 306M on Sep 18 2019.

10) The cause ==> foreigners.

Interesting take on the repo market’s ongoing action from Wall Street On Parade. Specifically mentions Wolf…

“Last Friday, the usually reliable and fact-intensive financial website, Wolf Street, threw a hissy fit over how the Wall Street Journal (and by extension, Wall Street On Parade) is reporting the tallies for the repo loans that the New York Fed has been pumping out every business day since September 17, 2019 to the trading houses on Wall Street.”

These people are STILL clueless and still don’t get it because they simply REFUSE to look at the numbers. The numbers are published. You don’t need to make up stuff. The other day they ran a piece that said that the Fed held $6 trillion in repos. Total bullshit. I wrote my article to debunk this bullshit. And they still don’t get it. But now at least they’re getting a little closer to getting it. But they’re still not there. Link deleted because this is garbage.

Wolf.. care to counter?

These people are STILL clueless and still don’t get it because they simply REFUSE to look at the numbers. The numbers are published. You don’t need to make up stuff. The other day they ran a piece that said that the Fed held $6 trillion in repos. Total bullshit. I wrote my article to debunk this bullshit. And they still don’t get it. But now at least they’re getting a little closer to getting it. But they’re still not there. Link deleted because this is garbage.

So, how can I collect all those bits and pieces of $$ that are rounded off that no one pays attention to? Or how to profit on them?

1) Banks make money on overdraft accounts. The FED is

a bank.

2) US gov account might osc one day, in a recession, between (-) 1,000B to (+)500B.

3) FED profit will be return to the gov, after expenses.

4) The FED will enable “flexibility” from political pressures.

All this is just too scrambled or non understandable unless u use it every day. I may love the brand of sausage but really. Don’t need to know what goes into the making. Much kudos to those who can untangle all these comments. This sausage is too long on the shelf and odorous.

Context for the board

https://www.zerohedge.com/markets/944-trillion-reasons-why-fed-quietly-bailing-out-hedge-funds