Seattle House prices fall year-over-year, as do New York & San Francisco Bay Area condo prices. Los Angeles, San Diego tick up. Denver, Boston hit new highs. Las Vegas, Miami, Phoenix aspire to their crazy peaks of Housing Bubble 1.

Year-over-year declines have spread to house prices in the Seattle metro, after having cropped up in condo prices in the San Francisco Bay Area and the New York metro in prior months, according to the CoreLogic Case-Shiller Home Price Index released today. These are the first such declines since Housing Bust 1 that followed our fabulous and crazy Housing Bubble 1. In many other markets, year-over-year price gains continued to wither away. So here we go.

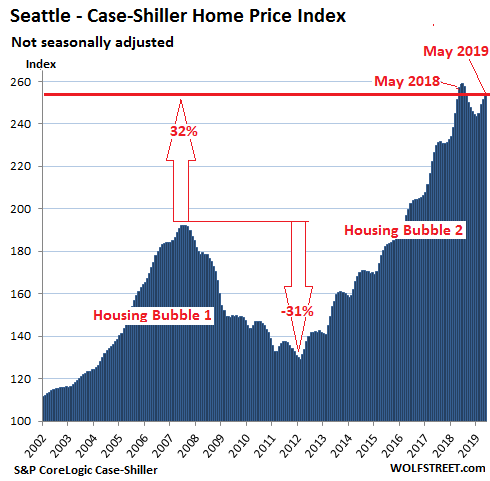

Seattle House Prices:

Prices of single-family houses in the Seattle metro ticked up 1.0% in May from April, which was less than half the seasonal increase last year. And so the index fell 1.2% from May last year, the first year-over-year decline since Housing Bust 1.

The Case-Shiller Index is a rolling three-month average that is released with one-month delay; today’s release represents closings that were entered into public records in March, April, and May.

The index was set at 100 for January 2000; a value of 200 indicates prices have doubled since January 2000. Every housing market on this list of the most splendid housing bubbles in America has an index value of over 200 in its history, either during Housing Bubble 1 or during Housing Bubble 2. This is the minimum requirement to make this list.

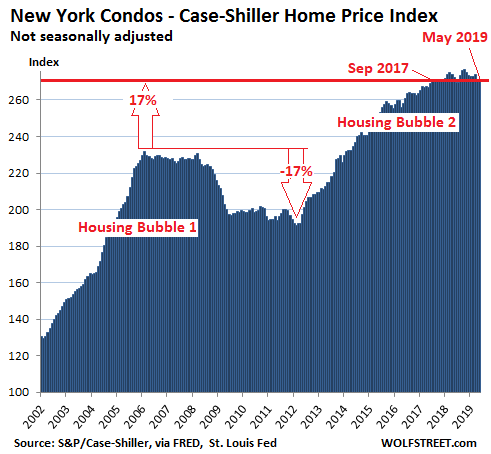

New York Condo Prices:

The Case-Shiller Index, which in most cities only covers single-family houses, also covers condos in a handful of big condo markets. The index for condos in the vast New York City metro, instead of booking a seasonal uptick, remained flat in May compared to April. This left the index down 0.3% from May last year, the fourth month in a row of small year-over-year declines. The index is now back where it had first been in September 2017:

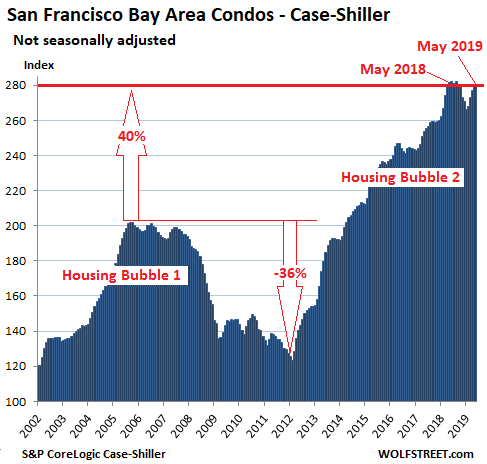

San Francisco Bay Area Condo Prices

Condo prices in the five-county San Francisco Bay Area – the counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay) – rose 1.3% in May from April, according to the Case-Shiller index. But it wasn’t enough. Compared to May last year, prices slipped 0.4%, the third month in a row of year-over-year declines – the first such event since April 2012 at the end of Housing Bust 1:

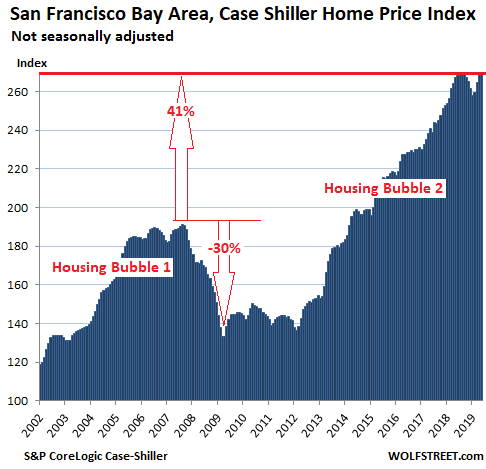

San Francisco Bay Area Single-Family House Prices

Single-family house prices in the five-county San Francisco Bay Area inched up 0.3% in May from April. This was merely one-third of last year’s increase in May. And it further eroded the year-over-year price gains, down to just 1.0% compared to May 2018 and left the index a tiny tad below its peak of July 2018:

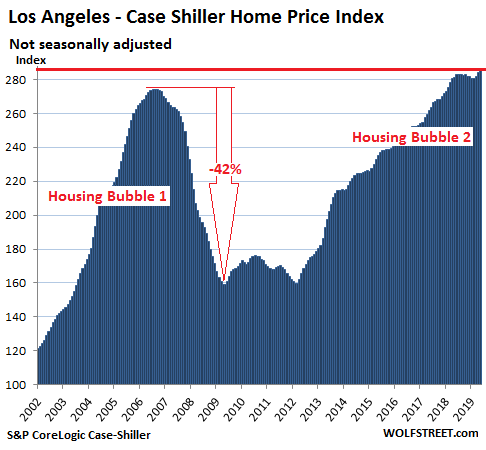

Los Angeles House Prices:

The Case-Shiller index for houses in the Los Angeles metro rose 0.8% in May from April, thus inching to a new record. The index is up 1.8% from May last year:

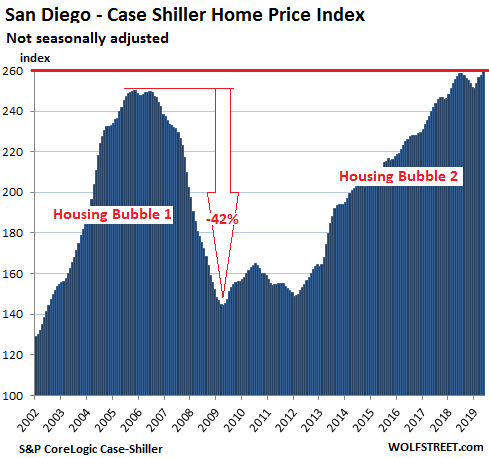

San Diego House Prices:

In the San Diego metro, house prices ticked up 1.0% in May from April, and eked past the record set in July last year to a new record, with the index up 1.3% from May last year:

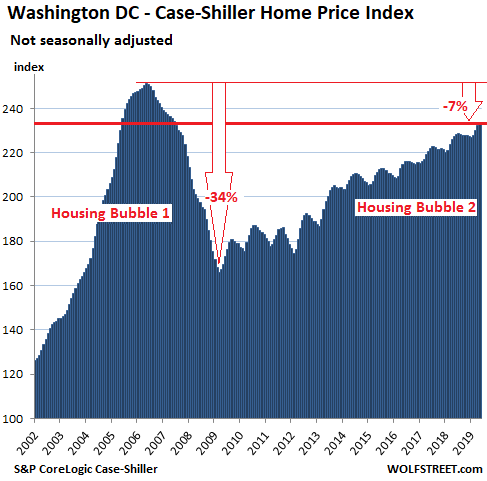

Washington DC:

House prices in the Washington D.C. metro rose 0.7% in April from March, and 2.9% from May last year. The index remains 7% below its crazy peak of Housing Bubble 1:

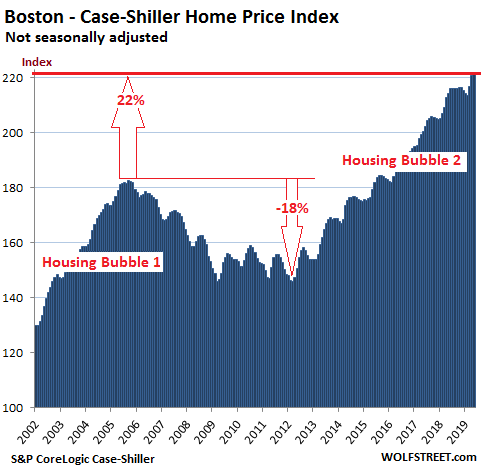

Boston House Prices:

House prices in the Boston metro ticked up 0.5% in May from April to a new record, according to the Case-Shiller Index. The year-over-year increase was whittled down to 3.6%, the smallest year-over-year increase since June 2015:

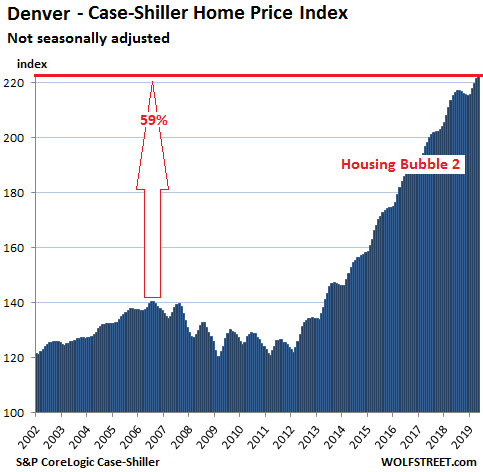

Denver House Prices:

In the Denver metro, house prices rose 0.6% in May from April, and this whittled the year-over-year gain down to 3.6%, the smallest such gain since April 2012:

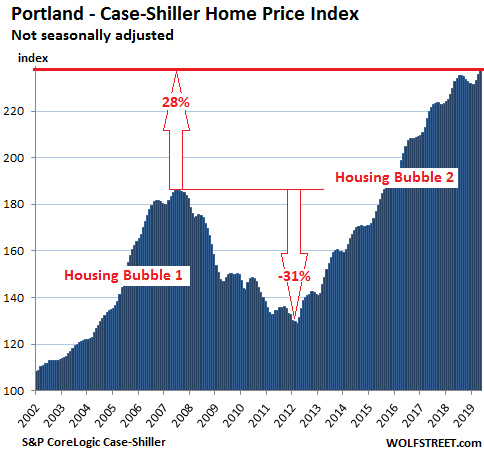

Portland House Prices:

House prices in the Portland metro rose 1.0% in May from April and 2.4% from May last year, the smallest year-over-year increase since September 2012:

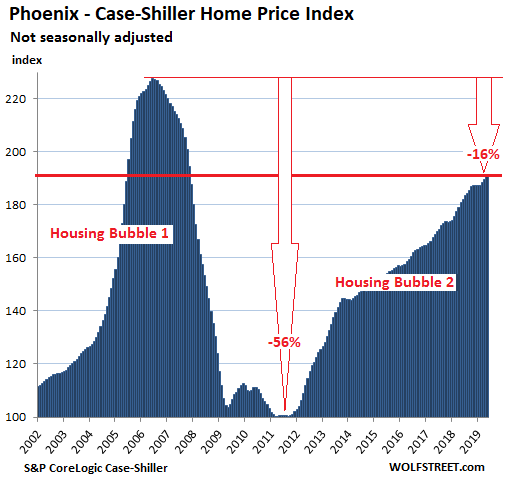

Phoenix House Prices:

In the Phoenix metro, house prices rose 0.7% in May from April and 5.7% compared to May last year. The Case-Shiller Index remains 16% below its totally nutty peak established during Housing Bubble 1:

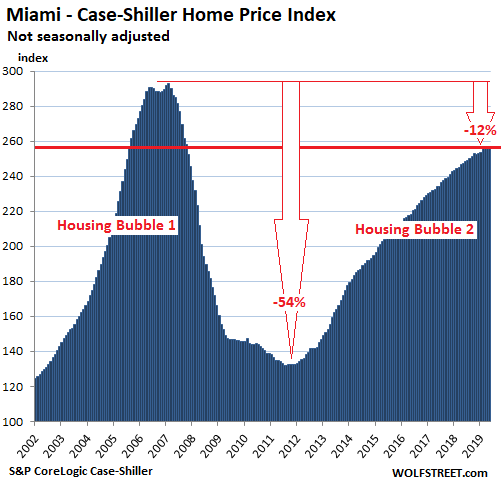

Miami House Prices:

House prices in the Miami metro ticked up 0.4% in May from April and were up 3.8% from May last year. The year-over-year gains in May and April of 3.8% each were the slowest since May 2012. The index remains 12% below the peak of Housing Bubble 1, when the entire housing market turned into a besotted casino, with house prices shooting up 140% in just five years, before they inevitably collapsed. So now the market is desperately trying to get back to those happy days:

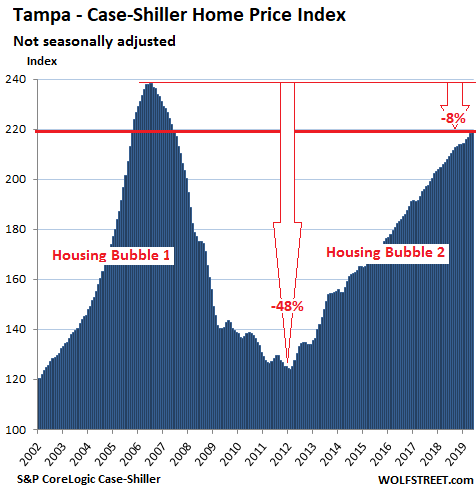

Tampa House Prices:

In the Tampa metro, house prices ticked up 0.1% in May from April. This whittled the year-over-year gain down to 5.1%. The index remains 8% below the crazy peak during Housing Bubble 1:

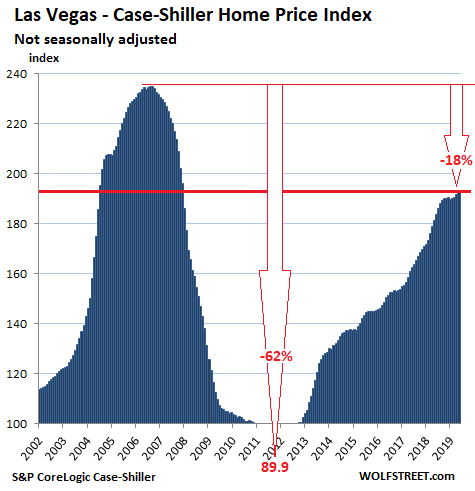

Las Vegas House Prices:

House prices in the Las Vegas metro rose 0.6% in May from April, whittling down the year-over-year gain to 6.4%. As high and out of whack this year-over-year gain may seem, it was the smallest such gain since February 2017, which shows how big the price increases have been. The index remains down 18% from the crazy peak during Housing Bubble 1:

The Case-Shiller methodology of “sales pairs” compares the sales price of a house in the current month to the last transaction of the same house years ago, thereby tracking price changes of the same house over time. When the price increases, it’s not because the house got larger. It’s because it takes more dollars to buy the same house. So the index tracks the purchasing power of the dollar with regards to houses and therefore is a measure of one type of inflation: house-price inflation.

Surging prices are a demand killer, but real estate industry laments the medicine didn’t work. Read… Ultra-Low Mortgage Rates No Relief for Home Sales

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Please have Chicago metro area for Less Splendid.

Thanks

Tomorrow!

Please Charlotte as well in the same category.

Atlanta please!!

1. Does case schiller reflect value/price or just the aggregate price in a region.

It dosnt seem to reflect a regions

Sq. Footage/price

Quality(intangible)/price

Replacement cost/price

Local municipal bene like water quality improvement to price

Local income plus

income growth/price

Mortgage rate/price

Treasury price/housing price

Alternative investment price/ price

Realtor inventory in sq. Ft/ price

In a nutshell, the schiller school of thought cries bubble everytime a price index rises. This assumes past prices were correct and modern time expensive.

One could suggest irrational pessimism exists and peaked in 2009 or 2010. Sellers bubble .. inverse irrational exuberance.

What if the observable time period in an indice starts from prices that were excessively cheap and in poor condition such as the prevelance of lead anf aesbestose.

Im going to suggest prices of real estate, nationwide arent terrible when adjusted for size or quality factors which isnt yet measurable..

In 1972, the ave. Home was 1200 sq. Ft and lead paint.

In 2014 ish it may be 2400 sq. Ft and not much lead or aesbestos around.

But fact check that please.

Its not a bubble everytime prices go up when you ignore the gold standard and embrace some more useful minerals to digest.

Perhaps what matters more than price is

( alternative rent)/(total cost of overhead of ownership.)

What savings are realized owning a home today versus renting a compairable property and that savings relative to a bond.

If it costs $1400/mo to rent that costs about 17,000 rent per year..

Owning the same property, you might have some variable costs for tax and maintenance.. 6,000 to 9,000 to keep a property maintained per year with tax.. maintained property is fairly liquid at the rate of inflation usually but depends on cost basis…

So an owner might be able to manage about 50% margin of savings over renting more or less…depends..

A bonds yeild about 2.5% today… real estate is long duration..

One could rationally argue to pay as much as 320000 for this good…

Considering the yeild of the alternative risk free rate..

It depends on quality too.

Im not going to assume its a bubble.

One could argue you should be buying up the property and charging rent at this rate of risk free asset.

G,

The Case-Shiller Index compares the sale price of a house that sold in the current month to the price of the SAME house when it last sold (maybe years ago). The index is amalgamation of price changes between “sales pairs.” It shows how prices of individual homes changed over time.

The index adjusts for improvements and other things. You can check out the methodology. It’s linked in the last paragraph.

As an apartment dweller in the San Francisco Bay Area, how does this affect me? From what I understand the both house prices and apartment rents are supposed to track together, but that seems, like everything in whacked economy, not necessarily true anymore.

Also when this bubble pops what will happen to the rest of the economy, and to the other bubbles? Are we looking at the Second Great Recession or maybe a Second Great Depression?

I know trying to understand, forget about predicting, the presently insane economy is somewhat difficult, but if anyone could give me some ideas I would appreciate it.

“house prices and apartment rents are supposed to track together”

There is only a very tenuous relationship between them. Sometimes they track together, and sometimes they don’t because they’re subject to different dynamics. For example, interest rates play essentially no role in apartment rents.

The most recent nationwide Case-Shiller month to month housing price rise annualized appeared quite steep.

I would look at a rent vs buy calculator, if I were to change locations.

The recent rises were seasonal, and were smaller than in the same season in prior years. That’s why the C-S YOY increase has diminished further.

Jbird4049 – Just a quick thought here … house appreciation is the closest thing our system will allow for “helicopter money” for the middle class.

If you’re not an owner, forget about it. But since a fat part of our population does own their house, the appreciation is a way to drop money into their hands, to, for the most part, go out and spend.

This money isn’t going straight into the hands of the proletariat, but it is in a backhand way in that the house-owners are then spending it in the coffee shops and mini-malls where we work, buying strawberries from us on the street corners, etc.

In 2008 we saw what happened when that “helicopter money” came to a stop. Everyone hung onto that one dollar bill they had, and everyone (except the oligarchs) lost their jobs.

So, yeah, Great Depression II, complete with war as a ploy to get out of it.

It will be a Recession but will feel like a Depression. The domino effect of people losing their jobs, can’t pay the mortgage, can’t pay the rent, living in their cars, moving in with their families. It’ll be very difficult. Much worse than the 2008 crash.

Thank you for posting this Wolf!

With Seattle, I am awfully curious what the numbers will show for June, July and August.

Hoping that peak home selling season will show a slump in sales.

It won’t, at least compared to supply. The Seattle market is in balance at the moment, with active inventory staying essentially flat the last couple of months. As opposed to rising like it did in summer of 2017 and 2018. This doesn’t mean prices will jump or anything… just that the balance of inventory has stabilized for now at a level higher than prior years.

Note, today;s pending home sales print shows pendings moving up, YoverY, and MoverM.

Yes! Those buyers, if they do NOT buy now, they will NEVER get this price again!

I would not go that far, but in Boston, it is being reported that:

“Yet the volume of sales fell sharply, with single-family homes down 9.3 percent from last June, according to the realtors association, as buyers struggle to find houses they can afford. The real estate trade group said there were fewer homes for sale last month than in any June since it started counting in 2004.

And new listings — homes that were put on the market last month — are slumping again after rising earlier this spring, suggesting there’s little relief on the way for prospective buyers.”

The entire article can be read in the BostonGlobe.

The title “If you don’t already own a home in Massachusetts, it may be too late”

Wow. Just got a serious case of Deja Vu reading that title line.

Boston area home prices I think is benefiting and rising smartly from those areas of spending that are growing:

Healthcare

Education

War & Aggression

Finance

Add to that in areas that I live in that have buyers I assume benefit more from lower interest rates that stock market bubbles, and that explains what I’m seeing locally.

Markin, that one is over the top, but I thought everyone would enjoy the article. Google the title if you want the story. The comments on the Boston Globe article are a fun read.

I just don’t understand Boston. It is a bastion of wealth, seems like there’s a university within a one mile radius of anywhere, has great sports teams, a great symphony, fine architecture throughout the city, etc. At the same time, the summers are way too hot, the winters way too cold, the transportation system is dated, crowded and not weatherproofed. Outside of Miami it will probably suffer from climate change more than any other city in the country. I just couldn’t see me living there if prices were halved.

Time to get those rates down, right Jim!!!

Actually, if rates go too low, inflation goes up, and the Fed will move rates up to protect the USD. I prefer a string of small to mid single digit price increases because they are sustainable. A 3% price increase yearly compounds to a 35% return in 10 years … I like that one. Double digit price increases causes a hawkish fed … in a 10 year horizon, that could do some damage. Easy does it.

Keep pedaling your bicycle because if you stop you fall.

Always interesting to see the Portland data. The market around here continues to defy logic.

I would really love to see hard data on what percentage of the buyers are out of state. Anecdotally the hot market is driven by in-migrating buyers. Both foreign nationals and people moving from out of state. A lot of locals are priced out, yet prices still go up.

I truly think the market here will crash (or deflate) in a lagging fashion that follows the California markets.

If you look closely at Wolf’s city by city charts you will notice that Portland’s chart almost exactly mirrors San Francisco’s ( except scaled down). So you are right that when San Fran goes down Portland will follow almost immediately. People seem to harbor the delusion that certain places will be safe from the next real estate downturn, but a quick look over all these charts show that things go down together, some just more than others.

Anecdotally, I see a LOT of out of state license plates in my neighborhood here. (You can’t see my CA plates because I registered my car in Oregon soon after moving.) There’s also a ton of new housing (of the condo persuasion) slated to come online in the next year to judge from the state of completion I observe.

I do have friends considering moving to Portland, but I’m not sure there will be enough bodies to fill all the inventory that will be available. I don’t mind taking a bath on my house if it helps housing become more affordable for people here–because it’s way too expensive for incomes.

“So the index tracks the purchasing power of the dollar with regards to houses and therefore is a measure of one type of inflation: house-price inflation.”

Given that housing expenses are mandatory (one must live somewhere) and given the growing disparity between housing and wages/earnings, it’s a mystery that consumers have any money left to spend. Is population growth the engine feeding the housing bubbles?

There are no bubbles in Lake Mead. No water either.

OK so where should I move? I don’t want lots of snow or scorching heat. I don’t want hurricanes or tornadoes. I don’t want forrest fires and floods. I don’t want to be near fracking or the Mexican border. I haven’t even talked about distance to a good hospital. That doesn’t leave me with many choices. Help.

A small town near a big city in the UK?

Or Australia?

You blokes don’t quality. You have ferocious “forest fires” and “scorching heat” and “hurricanes” (you call them “cyclones,” like the one that about wiped out Darwin), though admittedly, you’re “not near the Mexican border.”

How about Greek Islands? Are Americans welcome there? I guess USD will go a long way.

Check out Charles Cather just put that name in, on YouTube. He’s bullish on Serbia, and frankly he makes it sound pretty good.

There are also small towns in areas like upstate NY.

You could come here, wherever that is. For obvious reasons, we don’t advertise.

Do not go to the Greek islands. They’re mired in poverty, loaded with tourists, and it’s a very long commute.

Ex-spooks love Panama.

Are you not happy where you are? Do you own? If you like it, why move?

Moving costs money.

Or if you must, you could move to Toronto – it’s fairly temperate, and prices are down about 100K in the last month. And the Canadian Peso is only 75 cents US!

Toronto temperate? ha ha ha…Aprils Fools.

FAIRLY temperate, with a couple of cold months a year, after Xmas.

The upside: it doesn’t rain 200 days a year, like some places.

When I was there was told one could walk across Lake Ontario to Buffalo.

Toronto hasn’t found bottom yet and the Great Lakes create some rough winter weather, one day a tee shirt will do and the next day a blanket of ice will keep you warm with frostbite.

That’s Calgary.

Seattle, obviously.

Become a Cheerleader, and travel with the team! ;)

Hmmm… Antarctica should work. It’s a cold desert so they don’t get much snow there. Confirmed also on no heat, hurricanes, tornadoes, fires, floods, fracking and Mexican border.

Lake Chapala, Mexico. Low cost of living, mild weather, plenty of expats and it’s over 500 miles from the US-Mexico border.

SF, let me dare u :

1) Normal corrections are between 38% to 62%.

2) From the bottom of the 1970’s, assuming the start was 50 area, SF had a bull run. Since 1995 it went vertical, reaching 190.

3) SF up : 190 – 50 = 140.

4) The 2007 correction was only (-) 30%, ==> the trend is strong.

5) It hit a bottom at 130 in 2009. Add : 130 + 140 = 270.

6) The whole move from 1970’s to the peak was : 270 – 50 = 220.

7) A 38% correction will send SF to 2007 peak.

220 x 0.38 = 84 // 270 – 84 = 186. The uptrend is still strong.

8) A 62% correction will send SF to 2009 bottom.

220 x 0.62 = 136 // 270 – 136 = 133. The trend is weak.

Possibly not reaching, or exceeding 270.

9) Good luck !

When will this central bank driven debt fueled funny money madness end? Normal people can’t survive anymore on wages. Yet we cannot afford to risk our entire financial well being speculating in idiot central bankers’ worldwide asset bubbles and business models making unicorns out of businesses that sell dollars for 75 cents.

Amen amigo.

For what it’s worth, you aren’t the only one dismayed by this madness.

And if the speculators beat us in the end, you won’t be the only loser! :)

GCISF:

And that, good sir, puts you at their mercy. And they don’t have any.

Don’t take it personally. It’s just business.

Getting Crushed – Move out of the SF bay area. There are good jobs all over the country right now thanks to the Fed which you hate so much. Never take a position against the Fed. They have the power to perpetually inflate the stock and real estate markets via credit expansion. If you can’t afford SF, move somewhere cheaper and get on the gravy train. Buying a single family home in a good location has been a gold mine for the past 50 years. Stop swimming against the tide.

I always thought that we would imitate closely Japan after the big RE bubble deflated. Now with interest rates going to zero, prices of homes will skyrocket again putting homes beyond reach for most working people.

Look at Japan, homes are getting smaller and smaller and people are living in containers, in EU, most people are renters for life. I think we are heading towards the same situation. A landlord class with easy access to financing that will owe most housing stock and the rest who will rent forever.

Don’t bet on prices of real estate coming down. The Fed made the mistake in 2007 as they weren’t sure about the legality of QE and prices went down for some time, but now their tool box has everything they need to prevent deflation of asset prices, they can print 100 trillion if needed and purchase everything if they choose to do so. There is no limit to their power. I would bet on higher housing prices and Dow to 30k by the end of this year.

But the fed isn’t here to protect your perceived home value but rather load you up with cheap credit then slam you with higher interest rates ,I shouldd remind you that the last move was up and they are still doing roll offs as per wolf’s articles the fed always crashes the system so dummies who loaded up default then by it back for pennies on the dollar if I was a banker that’s what I would do ,,,I would bet that because it’s already happened before in the past

It’s like economic checkmate. No solution accepted. Keep slugging on.

https://www.google.com/url?q=https://www.ft.com/content/e26d36e6-918b-11e7-a9e6-11d2f0ebb7f0&sa=U&ved=2ahUKEwizwozVk97jAhVmT98KHa8EDdAQFjADegQIChAB&usg=AOvVaw2AxoqH9WoW-MgbIKQZs9fF

Jonathan Tepper’s Fourth Turning describes the generational cycles these go in.

Right now the country still revolves around the boomers who own homes and want high asset values while cheering for low wage inflation to keep their spending power high.

Soon enough, priorities will change to the young, housing affordability will be a major political issue, and wage increases will be demanded and cheered.

According to the theory, the turning point should be about the time Gen X’ers are starting to retire. Those who bought at the peak to try and build some equity before retiring will end up getting crushed.

Overall we are still looking at a market that is going up albeit a lot more slowly than previous years. Will it come down? When will it come down? And by how much?

Things won’t start coming down until unemployment goes up and takes out demand. We will stagnate until there’s a recession.

If anyone has a crystal ball, please share your thoughts on where tomorrow’s Fed rate cut will take home prices. As I understand it, homes in Tokyo are approaching their 1990 peak, now that the BOJ has gone negative. I think I agree with Kyle Bass’ statement that “once an economy falls into the tractor beam of zero rates, it’s almost impossible to escape them…”

I am just being more specific with a question:

When will we be able to buy decent homes fo $50,000?

“When will we be able to buy decent homes fo $50,000?”

My parents bought their first house in the mid 80s for $86K. $50K is as likely as movies going back to being a nickel.

There are decent houses available for $50k. The problem is that they’re in places with little or no work, away from the coasts, minimal “entertainment” or spare time amusements, and lacking in modern infrastructure. Frankly, they’re cheap because nobody wants to live there. But they are decent, and cheap.

When my parents retired they sold their Southern California property, went back to the old homestead where most of the family still lived, bought five acres and a house for cash, and lived on the proceeds. That can still be done.

There’s a really good reason that American retiree’s are looking outside the USA. Like the Chinese, they have cash and don’t really care where they live since they are not looking for employment. Who needs Malibu or Miami when $100k will buy you a beachfront condo in southern Spain?

When the ‘new dollar’ is created, 1 new one for 10 old. Accordingly, the minimum wage will be 1.50. And a cheap car is 2,000 bucks.

Hmm, that sounds like the 1960s.

I read Wolf’s reports and insights with great interest, and also appreciate the comments from all of you.

My 10 cents (maybe 5 cents) is around keeping in mind that real estate can be very local as we see trends in general markets.

For example, Tampa real estate is showing down by 8% from top of Bubble 1, and yet beach front has significantly appreciated since.

Maybe the housing prices show higher because more of the more expensive homes are selling.

Stan Sexton,

“…because more of the more expensive homes are selling.”

That is an issue of “mix” that dogs “median price” indices. But the Case-Shiller Index is based on “sales pairs,” comparing the price changes of the same home over time, so comparing its sales price today to when it sold last time, perhaps ten years ago. So “mix” does not impact this index at all.

Fed rate cuts are essentially the equivalent of being a kid getting a candy cane after sitting on Santa’s lap — buying into the North Pole and a massive sleigh delivering toys to all the tiny tots on Christmas eve — it’s all a wonderful little game being a naive toddler inside of a dreamscape. The Fed ferry tale will deliver a short term impact and then, as homes go up in value and stocks break records — suddenly out of nowhere, Santa and the magic will vanish and tears will be cried. It won’t make sense.

I have to say, I really enjoyed this website and articles a lot more when we were talking about rate increases. Now it is just really depressing. I have been waiting and waiting, and now it looks like waiting some more. For crying out loud, it’s been 10yrs of this garbage. It is starting to feel like it will never end.

“For crying out loud, it’s been 10yrs of this garbage. It is starting to feel like it will never end.”

It’s just that old “permanently high plateau” for everyone.

Again

I feel you man. It is an absurd situation.

Just try to remember that unstable states last longer than you ever thought they could, right before collapsing more suddenly than you ever thought possible.

Right now it may make sense to call them “Housing Bubble 1” and “Housing Bubble 2” but really it is just one continuous bubble with a saddle in the middle which all started in the mid ‘90s. Housing prices never deflated significantly or for very long and it has taken criminal activity on the part of banks and .gov to reflate the market to even more insane levels today. Anyone considering making a levered purchase of housing today should have his head examined.

It’s a little off topic, but not much. House is a long term asset like a stock. If stocks inflate it’s possible to sell and buy a house so the assets can be connected.

The overall stock market can be valued by the cash flow (dividend). You can use an on line calculaor, but there are three variables. Dividend, nominal growth rate of gdp (=long term div growth), equity risk premium. Long term risk premium had been around 3% over 10 year treasuries. If you plug in the current dividend $56 and 10 year average of nom gdp of around 4% and 5% for the risk premium you get around $1350 for SP500. What gives? The Fed has lulled the investing public into taking too much risk so that there is no risk premium right now. It’s not a nice thing to do as eventually they will lose control and risk premium will go back to 3%, but might overshoot first which means market could fall below 1350.

I am saying this because when stock market falls it will drag everything else with it including house prices. The Fed is not ad powerful ad we are led to believe. They can control interest rates, but they can’t control people’s behavior completely.

Stocks are not considered long term assets. Or there wouldn’t be day traders as a whole industry. Maybe mutual funds?

I think your premise needs a little reworking but interesting idea.

These graphs succinctly shows how house prices have ballooned through the years making them very unaffordable for many as average incomes didn’t go up by similar levels. I assume this problem will be similar in most every city in the world. The dips or corrections are too small to call them “affordable”. This worldwide problem demonstrates how mankind has used housing as more than just savings but for speculation everywhere. I don’t think there is a solution since good location (land) is a scarce resource.

The solution involves government regulation. No need to wring our hands snd hope things get better.

Carrots and sticks. There is no reason a city “must” allow global capital to distort local housing markets. Vancouver finally had the balls to try and disincentivized foreign “investment” and vacant housing in its strained housing market to benefit citizens (aka workers) in need of local housing.

More Communities should do what works for them, not the highest bidder.

From the graphs, it is safe to say that real estate prices go in cycles. Unlike stocks, which can be dumped indiscriminately in a panic, real estate houses people, so if it is sold, you need to move somewhere else. This tends to put a damper on price declines. The first bubble, was truly a bubble with liar loans, and chants that real estate never goes down. The second bubble is different, and perhaps more of a reflection of the loss of purchasing power of the dollar combined with historically low unemployment, but liar loans are gone forever. Will it correct with the next recession? Sure, but there will be no 50% off sales. Even a sideways market for 10 years with 5% inflation will correct value, but prices will remain “the same”. The price of your home will be the same as ten years ago, but a Big Mac will cost $12.

I’ve been cashing out my stock gains in this run up, and using that to pay off mortgages. First the primary is gone, now knocking down the beach house. Depending on how long this goes will allow me to reap the benefits of paid off rental properties which become cashflow machines, and hopefully protecting myself from inflation. Other than this, I really don’t know how to take advantage of the run up.

One of the interesting things I’ve noticed about this site, having pondered the problems, many of them severe, raised in hundreds of posts, is that there very much appears to be no feasible solution to any of them.

Solutions, yes, feasible solutions, no. It should be obvious that this is by design, because these problems couldn’t occur naturally or randomly. It’s easy to be discouraged by this, but that also seems to be part of the design.

If I ever decide to become an Evil Overlord, I will keep my minions locked in a mindless trance by providing each of them with free unlimited Internet access and social media accounts. Unfortunately all the existing Evil Overlords seem to have beaten me to it, which one must admit does tend to explain rather a lot.

Ha!

When I start to get a little miffed at all the Evil Overlords appeasing me with free unlimited internet and social media accounts, I just put on my favorite Pulp album with this little ditty:

“You will never understand

How it feels to live your life

With no meaning or control

And with nowhere left to go.

You are amazed that they exist

And they burn so bright,

Whilst you can only wonder why.

You’ll never live like common people

You’ll never do what common people do

You’ll never fail like common people

You’ll never watch your life slide out of view

And then dance and drink and screw

Because there’s nothing else to do”

I’ve always been impartial to a good drink and a little dancing.

Are the graphs done in constant dollars?

Zippy,

PLEASE read the last paragraph, which explains that the Case-Shiller index is itself a measure of inflation, namely home price inflation, since it measures how the price of the SAME house changes over time, and therefore it measures the purchasing power of the dollar with regards to houses.

House price inflation is one of the many types of inflation that also include consumer price inflation (measured by CPI or PCE), wage inflation, wholesale inflation, etc.

You don’t express CPI in constant dollars either. That’s absurd.

How does Case Shiller define “Seattle”? Because what’s happening in the Pugent Sound area is Seattle proper’s prices have stagnated. But everything around Seattle – Tacoma, Bellevue, Issaquah – is still increasing. Turns out the ‘burbs aren’t dead after all, despite what the MSM would have you believe.

Looking at all your charts, a clear pattern emerges. Prices dropped by a small amount last year. Then this year it’s back to increasing prices. How anyone looks at those charts and concludes a housing crash is happening is beyond me.

Case-Siller uses the Seattle-Tacoma-Bellevue, Metropolitan Statistical Area, which includes the counties of King, Pierce, and Snohomish.

That’s why the C-S for Seattle metro is down only so little, because it includes areas that are stronger and areas that are weaker.

Didn’t anyone note the impact of housing supply? I think this factor, esp. in SF and LA, among other areas, is a critical reason why prices have continued to appreciate. Low interest rates, a rising stock market and steady job growth have contributed to a strong demand, but the bottom line is, people have to live somewhere, whether they own or rent. Rental prices have soared in these cities as well, again due to a massive drop off in new construction post-2008. In LA, where I work as a Realtor, demand continues to outstrip the available supply. This is another indication of the key flaw in this analysis of the current market as a Housing Bubble 2.0- when supply is low and demand is high, pressure on prices will correspondingly increase. As supply increases and demand cools in some of these areas, prices will drop, but the factors that led to the 2008 crash are not the same so I don’t expect a similar drop but more of a typical correction.

Will Flannigan,

This is sheer Realtor propaganda, down to the iota. I mean, perfect. They pay people to produce this. Almost all of the quantitative qualifiers you used are wrong.

To start at the top, there is plenty of vacant housing, some of it on the market and some of it in the shadow inventory. But the asking prices are too high, and sales volume as dropped because potential buyers are just not willing to pay these prices willy-nilly.

To get a feel of where things are, if you even want to see the numbers, read the articles on this site, including the one you posted on; yesterday’s article on rents — which shows a decline in asking rents in LA and other places; and concerning the SF Bay Area, where house prices are down 8% year-over-year, according to data from the C.A.R. to which you belong:

https://wolfstreet.com/2019/07/18/housing-bubble-2-lost-its-mojo-in-the-san-francisco-bay-area-house-prices-drop-8/

If the bubble is about to burst, is there any downside to selling your house right now before the burst? I live in Vancouver (at low end of detached market) & have been watching my house price decline at least 100k per year since 2016. Thought this may turn around soon but based on this site seems this may only be beginning? Thinking about selling, renting, then buying into market at lower price in future. Selling a few years ago would have been ideal but is selling now too still a smart time? Wolf and commenters would love your feedback. Thanks.

Ciena,

Timing a housing market in this manner successfully requires a large amount of luck and a willingness to live where and how you might not want to live. It’s easier to try to do this with investment properties than with your home. Two different things :-]