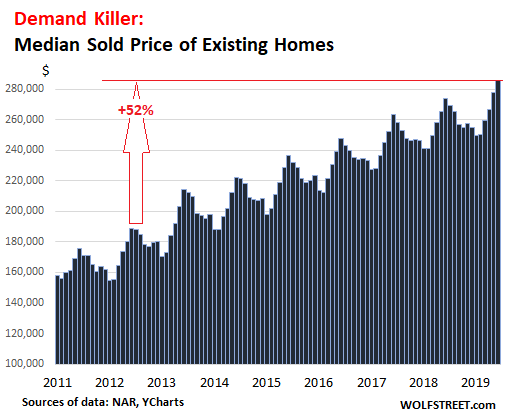

Surging prices are a demand killer, but real estate industry laments the medicine didn’t work.

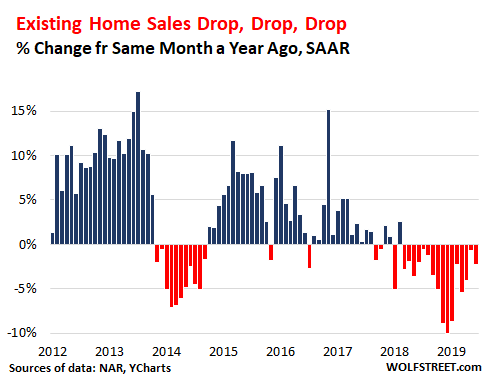

The relentlessness of falling home sales is starting to baffle the real estate industry that had expected plunging mortgage rates to fire up sales: Across the US, sales of “existing homes” (previously owned single-family houses, townhouses, condos, and co-ops) in June dropped 2.2% from June last year, to a seasonally adjusted annual rate of 5.27 million homes, according to the National Association of Realtors. It was the 16th month in a row of year-over-year declines (data via YCharts):

“Home sales are running at a pace similar to 2015 levels – even with exceptionally low mortgage rates, a record number of jobs and a record high net worth in the country,” lamented NAR’s report.

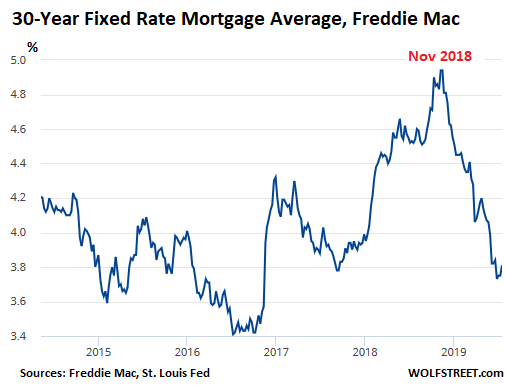

And the plunge in mortgage rates from the November high has been spectacular. The Fed has hiked rates one more time in December and so far has not cut rates. But yields across the curve have been dropping in anticipation of a veritable Niagara Falls of rate cuts and whatnot.

In June, the Freddie Mac average commitment rate for a 30-year, conventional, fixed-rate mortgage fell to 3.80%. This is over a full percentage point lower than the average rate in November of 4.87%:

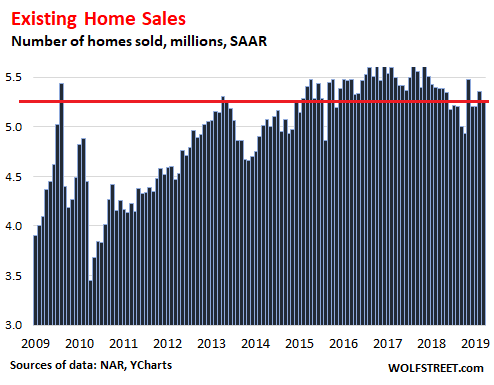

Sales of existing homes in June, at 5.27 million seasonally adjusted annual rate, are now back in the range where they’d been in 2015. The chart below shows how home sales topped out late 2017 and early 2018 at a pace above 5.5 million, as mortgage rates were already rising. When mortgage rates began ascending at a steeper slope, sales fell sharply, as you would expect, hitting the low point in December and January for deals signed in November and December.

But given the plunge in mortgage rates since then, expectations were that sales would resurge. While sales have ticked up from those lows, the move was, for the industry, confusingly feeble (data via YCharts):

The astonishment of the industry with these falling home sales despite ultra-low mortgage rates emerges in the report’s comment, as the industry is grappling with potential answers:

Either a strong pent-up demand will show in the upcoming months, or there is a lack of confidence that is keeping buyers from this major expenditure. It’s too soon to know how much of a pullback is related to the reduction in the homeowner tax incentive.

By home category: Sales of single-family houses in June fell 1.7% year-over-year to a rate of 4.76 million, and sales of condos and co-ops fell 6.5% year-over-year to a rate of 580,000.

Sales by region in June show the steepest year-over-year declines in the West and the Northeast:

- Northeast: -4.2%, to an annual rate of 680,000

- Midwest: -1.6%, to an annual rate of 1.25 million

- South: -0.4%, to an annual rate of 2.25 million

- West: -5.2%, to an annual rate of 1.09 million.

Inventory for sale in June was about flat compared to June last year. Given slower sales, supply at the current rate of sales ticked up to 4.3 months (from 4.0 months a year ago). This is plenty of supply. But it’s the wrong supply.

After years of price increases, home prices together have moved up the ladder, including the lower end that is now priced where mid-range used to be a few years ago, and there is no more “low end” in many markets, and the new low end has moved out of range for many buyers. High prices kill demand. And low mortgage rates, after years of low mortgage rates, are having only a limited effect on sales volume.

But the median price of existing homes sold in June across the US – median means half sold for more and half sold for less – rose 4.3% from a year ago to a record $285,700.

So here is the visual definition of a “demand killer”: Since June 2012, so in seven years, the median price has surged 52%. And mortgage rates in 2012 were in about the same range as now. No one in the industry should be surprised that sales are slow (data via YCharts):

By category, the median price of an existing single-family house rose 4.5% year-over-year to $288,900; and for condos, the median price rose 2.8% to $260,100.

By region, median home prices in June span the spectrum, with the West being 65% more expensive than the Midwest:

- Northeast: +4.8% year-over-year, to $321,200.

- Midwest: +6.7% year-over-year to $230,400.

- South: + 4.9% year-over-year, to $248,600.

- West: +2.3% year-over-year, to $410,000.

As prices rise across the board year after year, the low end of the market moves to where mid-range prices used to be and the middle moves up into the next price tier, and so on, though the homes don’t actually change; they’re still low end or mid-range. Only the prices change. And after years of price increases in many markets, there is nothing left where the low end used to be. And what used to be the mid-range is now made up of over-overpriced low-end homes, and there is plenty of inventory, but they costs too much for what you get, and buyers balk.

For the nine counties of the San Francisco Bay Area, the median home price in June dropped below June 2018 levels and back to June 2017 levels. Read... Housing Bubble 2 Lost its Mojo in the San Francisco Bay Area: House Prices Drop 8%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Only $410,000 in the West? Those number must clearly be distorted by housing outside urban areas. Good luck finding a decent house in an urban area of the western region for less than $1,000,000, if you find something it will be a tear-down or at least in need of several hundreds of thousands of dollars of work (no one even talks about the severe black mold and asbestos problems of a large percentage of homes in Seattle).

Who would want to get stuck owning one of these places, the traffic noise alone is bleak. How depressing to spend that much money to live in a basic slum. Plus you’ll have me (or one of thousands of others) camping out in my van right in front of the place.

How many working people can get a mortgage for over $1,000,000 even with rock bottom rates? And the bigger problem being once you buy the house you are stuck living in a pile of decrepit crap.

Dude, the “West” is more than just LA and SF and Seattle for crying out loud. $400K still gets you a nice house in a lot of the “West” like Boise, Salt Lake City, Albuquerque and in a lot of CA as well. I live in “the west” and even for $300K, one can find a nice house in a good neighborhood.

LOL +1000000000

Yeah if you want to live in the desert your crazy read the post above spot on!

van_down_by_river,

The West is huge and includes Arizona and New Mexico.

If I sell my home, there will be a 6% commission and all sorts of fees. The next house might need repairs as the home inspector might be part blind. The new neighbors might cause problems. I would be better off not moving. That means slower home sales. House price increases have slowed. Those 15% a year home price increases were too steep.

For sale by owner? Craigslist?

I paid 3% commission when I sold my house in San Jose April 2018. Broker was an independent who advertised the house on the MPLS and social media, and since he handled both seller and buyer he could give the reduced commission (save me $39K over 6%).

Look around; even ‘traditional’ RE agents will do 5% if you ask/insist.

Most will do 4% at least for higher priced houses.

For $410,000 you can get a nice home in AZ depending on your idea of “nice” and SF. But that is out of reach of a lot of people living in AZ, especially if you’re not living outside your means which I suspect many people are.

Van:

And, if that “pile of crap” becomes too large you can always rent a nice “comfortable” storage unit to store more crap. That’s the American Way! It has proceeded from American Apple Pie to American Pile of Crap!

Got a “giggle” on how you said, “….camping out in my fan right in front of the place”.

Years ago had a neat ’73 dodge van with raised ceiling; was totally exhausted driving down on hiway 5 from Oregon; stopped in Yreka and parked just like u described……after several hours of deep, deep slumber got a great pounding on my van door….Yep! The local police rousted me out…they were pretty good about it but the message was clear. LOL!

There are many places in CA that don’t require million dollar mortgages; just have to look. Foothills of the Sierras and the Central Valley have many. You just have to think and live differently.

The Greater Bay Area is a ZOO! But, that’s where the $$$$$$$ jobs are.

Have couple of family members/friends living in Santa Clara Valley in the mortgage business. The refis are insane right now. That’s where they are making their money now. (They’ve been in the business for decades and have seen and experienced the good, the bad and the ugly.

$410 sounds about right for Portland, but $410 is still plenty crazy for what that buys. But Redfin is my Candy Crush, and I see more “price dropped” and “back on market” notifications than anything.

“But the median price of existing homes sold in June across the US – median means half sold for more and half sold for less – rose 4.3% from a year ago to a record $285,700.”

But how can this be? I have been assured several times here and elsewhere that housing prices are falling precipitously everywhere.

They’re falling alright in some markets. Click on the article I linked at the bottom.

Buyers are lucky that sales are slipping because prices are only moving up a little more than 4 %. If home sales start rising, home prices will rocket higher, and the FED will put an end to the party. Best for homeowners if sales run at a rate that does not trigger the FED to raise rates … and that means falling sales.

Nonsense….”sales are slipping” is because of the buyers. Lets face it! No one wants to buy at peak bubble prices and there won’t be a FED engineered 3rd bubble to bail you out this time….save those commission checks Jim!

Sellers need to cut their prices. They’re still way too damn high. Sellers act like we haven’t just seen 50% to 100% appreciation over the last five years, and they still want more even as the market falters. Pigs get slaughtered.

that’s it in a nutshell,

too hard to predict tops, millionaires settle for much lower % on gains….

The relentlessness of falling home sales is starting to baffle the real estate industry

It shouldn’t.

It proves that the policy of enriching the wealthy at the expense of everybody else is working. People just don’t have the money to buy more houses, even though the country continues to get richer. Where did that increased wealth go? The rich have it. All of it.

What goes around, comes around, or not, as the case may be. The nice thing about reality, including financial reality, is that it will still be reality regardless of how the unscrupulous try to subvert it.

I think all the people who had the need and capacity to purchase a house did so over the last five years as mortgage rates have been low. There simply is not enough people left to purchase homes, especially at theses prices. Millennials would like houses, but they are priced out.

Plus, with all the nice new apartments coming online, there are plenty of places for millennials to live.

There’s plenty of foreclosures all over the country but these homes are not making it to market. They are being scooped up on the courthouse steps by the reits. These foreclosed homes were a traditional source for many first time buyers or buyers looking for a bargain, but no more.

It’s a shadow market that doesn’t show up in the real estate sales stats. The reits are also buying in bulk from developers at bargain prices. So if you buy a new home you may be in a rental community and not even realize it.

I think you’re on to something here — my first two houses were both foreclosures bought directly from the lenders, through agents. The lenders have no reason to pay 6% or whatever when they can just call a REIT and mail the keys.

I have been telling people that for years, before you buy see how many of your neighbors are section 8 which means maybe they bought the house and now they just live in it. All transactions are recorded at the assessors office. Previous admin used sec 8 to house immigrants and desegregate neighborhoods. Residents of Temecula, CA for instance, protested and turned back bus loads of these people.

All I know is that in the two housing markets we’re looking in, there has been a leap in prices post-2017. Like a 20-30% leap. Obviously sellers think the market has jumped enough that they can cash out and pay the broker commission. And no there haven’t been upgrades made to these homes.

Right on, Wolf. That is exactly what is happening right now in the north DFW area. “There is nothing left where the low end used to be. And what used to be the mid-range is now made up of over-overpriced low-end homes, and there is plenty of inventory.” On my “country” drive to work, I’m seeing builders still tearing and clear cutting ranch land to build new homes at prices that the “low end” can’t afford.

My hubby and I are saving our cash and waiting on the bursting bubble to regain a home we lost in 2014 due to the Great Recession.

Big hedge funds full of cash are also waiting like vultures for this “bursting bubble” and then they’ll swoop down and outbid regular people so fast, they’ll leave their heads spinning!

When the time comes, it won’t be like it was in 2008/2009, they’ve changed the rules of the game and banks won’t foreclose on any house that’s lost its value. They’ll just sit “off book” until the Fed reflates the next bubble and wait as long as it takes to get their money back.

So this time is indeed different!

LOL This time if Different Y’ALL

Hedge funds are run by morons who consistently lose money.

The Fed is trying to reflate the same bubble not the next one.

“And what used to be the mid-range is now made up of over-overpriced low-end homes, and there is plenty of inventory…” Agreed. This is true in many markets around the country, I think. In north DFW you make me think of the old Fox & Jacobs homes near 635 that should be in the high 100s but are selling for 350,000 plus (but with updated vinyl plank floors, of course). I am sorry about your home. Last time, I never thought the Fed would leave rates so low for so long. I wonder if they’ll have something new in their bag of tricks this go round to reflate assets.

Why Millenials aren’t buying houses

Why Millenials aren’t buying Harleys.

Why Millenials aren’t buying boats.

Why Millenials aren’t investing.

The [ ] is too damn high! Everything has been priced for Boomers who have of lots of discretionary income, because they were able to pay for much of their lives with “regular” jobs.

Boomers also didn’t major in 14th Century SJW Poetry Studies. They got real degrees, which led to real jobs which led to real incomes. They also didn’t buy $1200 cell phones, $15 craft beer or demand organic this and organic that at 400% higher price than the equally good and equally healthy “normal” version.

I’m not a boomer but I’m so sick and tired of seeing millenials blame all their problems on them. It’s pathetic.

Stop spending your life on Twitter, stop buying the latest i-gadget every 3 months, start saving some money, get an actual education that provides marketable skills and you too can buy a boat, a Harley and a house like the generations before you.

Just Some Random Guy – here’s a great chart of college degrees by major, data is a few years out of date but no reason to expect a change. The idea that millennials are all studying underwater basket weaving is patently false: https://www.npr.org/sections/money/2014/05/09/310114739/whats-your-major-four-decades-of-college-degrees-in-1-graph

Only real changes – Education as a major declined while Business and Health professionals increased. Millennials came of age at a time when Boomer’s refused to retire (mostly due to their own poor financial management). The labor supply also increased (lack of retirement, women in the workforce and then globalization)

As Wolf Reported, inflation has not been in wages; “Based on Census data going back to 1960 for median household incomes, median gross rents per month, and median house prices, all adjusted for inflation, it shows that nationally, incomes since 1960 have risen just 29%, while rents have risen 72%, and house prices have soared 121%:” https://wolfstreet.com/2019/07/12/changes-in-house-prices-rents-and-household-incomes-since-1960-in-the-us-by-region-and-major-metro/

Add in healthcare, tax, gas, and general inflation which inflation calculator states at 765.3%, and yeah – no one is buying. That cell phone would have cost $140 bucks in 1960. Personally, I have pretty much gone all-in on Dave Ramsey’s debt snowball – believing congress will never care – and hope to be debt-free in a few years at which point I will never use debt again, and I’m an engineer. Most young adults I know have completely given up hope on homeownership, it’s just not a thing – even among skilled trades and professionals. Those that did buy seem to generally regret it.

I looked at the graph on NPR.

Let me say at the outset, so everyone can be offended: One of the largest percentage and numerary increases is in business degrees. Business degrees are BS as in bull. They are inteded for the slack and disinterested to milk a business dry to satisfy lifestyle needs. True business are those who start building and owning businesses, not those who are expert at milking them through financial engineering.

Looking through the growth in degrees, some of the biggies are fitness, art and performance, communications/journalism, criminology, interdisciplinary, psychology, public adminsitration, other, humanities. I am also going to include computer science degrees in the long list of lame degrees since they do not increase the student’s body of knowledge, merely technique. This is partly true of many health science degrees too.

Some of the big losers are chemistry, physics,math, English, history, and foreign languages.

This is not the pattern of an improving society with people who can grasp fundamental ideas. It is a trend to the superficial, not the deep. Surface skating.

STEM has been hyped like crazy for decades and in truth, some of those degrees, like “fitness” can lead to a much more lucrative career. Try being in tech once you’re over 40! Not everyone becomes the Pointy-Haired Boss. Most techies post-40, if they’re lucky, end up driving a bus or some job like that around here. I’ve met tons of homeless people with tech backgrounds.

I agree on being scared to death of debt.

Chemistry took a big hit because there’s no money in it any more. Degreed chemists are making min. wage right now.

“Business” is a good degree because you get to say, “I have a degree” which is what ti takes to get in the door to a job that doesn’t require one, skill-wise, but a degree is used as a filter.

Let’s say I’d had the sense to stay away from tech and studied what everyone assumed I’d study, art. My life would have gone much, much better, I’d likely own at least one house by now, and instead of looking back on my 20s with bitterness, it might have been a rather fun time.

Alex,

You have been saying in the comments for years that you don’t have a college degree, and that you’re struggling mightily. You cited an income of $1,500 a month, in San Jose where the minimum wage is $15 an hour, or $2,500 a month. All kinds of companies are looking for people. The median household income in San Jose — meaning that half make more and half make less — is around $100,000.

I understand that things are tough for you right now, and I wish you the best, and I feel for you. But you’re not the person who is qualified to tell people not to get a STEM degree.

Add in healthcare??

I’m not spending a cent on healthcare until housing costs fall under 25% of income.

Housing + Healthcare should be at the most 30% of income. If the Fed inflated Housing Costs, then $0 goes from me to Healthcare. Fuck it!

Dreamer….great comment. However, I do take exception to your last assertion that those who buy houses generally regret it. I assume you are talking about recent buyers, but both my kids bought about 10 years ago and are now set up quite well. One is 35 and one is 39.

I do know quite a few engineers, and understand the degree is portable like any skilled trade/profession. You can slot in and slot out as the projects change, and live wherever you choose.

I’m 63 and retired at 57, solely because I bought a couple of homes along the way. They needed reno work and were located in areas that were affordable. Sweat equity and eschewing debt (I have always hated and feared debt), gave me freedom.

If you never buy, then you will be renting for the rest of your life, (which is a fine choice if you can afford it), but you also lose even more illusive freedom. I know a great guy in my area that was just told he has to move out of a home he thought he could stay in for another 5 years. He’s about my age and isn’t very healthy. The owner took ill and wanted to at least live in his retirement dream while he still could. Our friend received his two month notice only to discover there is nothing available to rent. He will now have to move away and he does not want to. A network is looking for him but ……

Buying a small piece of property in an area with lax zoning is a good lifestyle. Your neighbours might be a little rough around the edges, but no one will ever make you move unless you choose to. Or, it can be a good safety net if times turn tough. Hell, you can buy a place and rent it out to cover mortgage and upkeep/taxes. But not everywhere. :-) One day you can move into it, with no debt.

I wish you luck and want to echo your comments about debt. That might mean used crappy cars, or no car. I commuted by bicycle for 5 years, long before it was trendy (late ’80s). Bag lunches, local holidays, shopping the specials, and cooking at home paid for the house if the truth be told. Good luck on your journey.

But you’re not the person who is qualified to tell people not to get a STEM degree.

And yet, Alex happens to be correct.

I am so qualified. Do not get a STEM degree. Do not major in Chemistry. Instead, learn how to learn what you need. Even with a degree you will need to do so, and a degree will not help you if you do not. As the great Chopin noted, the primary purpose of an education is to enable the student to get along without the teacher. And no teacher ever learned anything for a student. That is up to the student. Teachers can be found everywhere, if you learn where to look.

But don’t mind me. As Auryn says, “Do What You Wish”. That’s not an invitation. It is a dire warning. There are consequences in any and all directions, and one must be circumspect. People have ruined themselves following Auryn’s directive improperly.

Whatever. I am going to go out to look at the stars again. It’s possible I may have missed something.

Unamused,

My friends, including my best friend, who have STEM degrees are doing just fine. They’re all boomers, and yes, they all face ageism. They all tried to deal with it in their own way. We all do.

And if, dear reader, you’re a millennial, you will face ageism in due time. At first you will face it because you will try to get rid of your older employees (if you’re in a management job); and then you will face it, when you hit that age, and the younger generation wants to get rid of you. This comes earlier than you think.

There are many things you can do to deal with ageism. My best friend works for a Silicon Valley company. He got that job in his fifties and has been able to do well and survive changes. But he knows when the layoffs start, he’ll be one of the first out the door. I started my own little media mogul empire. Other people start something else. Some work as consultants with old clients. It’s tough, and many doors are closed when you get that age. But this is not STEM related. It’s just plain ageism.

Wolf – I’m getting $16 an hour (1099 so no benefits though) half-time and a free place to stay.

Leaving here means living on the street, so I’m not about to leave.

I’ve been debating with myself whether it’s worth it to, if I’m going to end up on the street (the fate of most, just you wait and see, and my fate when something happens to my boss) at least be on the street in Hawaii where I grew up.

I’m sick and tired of millennial bashing. They are just fine, and thank God they are not like us. Boomers have had the softest easiest life in the entire history of civilization while being very materialistic and greedy. The world we have today is a product of the boomers and the two generations before them. The millennial generation did not make the world we have now.

JSRG, I’m throwing the BS Flag on your comment there. You need to study up on what’s really going down. The Boomers are eating their young. The WWII Generation might have been the Greatest Generation: the Boomers…uh, not so much. And this is coming from a Echo Boomer.

Dear Commenters,

In the future, I’m going to start deleting this generation-bashing nonsense. Millennial-bashing followed by Boomer-bashing followed by more Millennial-bashing followed by yet still more Boomer-bashing…

It’s not only nonsense. It’s also boring to read.

“Generation” of this type is a misnomer in the first place. People are born as others die. Generations are a “flow,” not a “stock.” These arbitrary lines in this flow were drawn as sort of a reference, but these are composed of millions of individuals who are all different, as people are. And to throw everyone who was born in a certain 20-year span into one bucket and assume they’re all the same because they were born in this 20-year span is just nonsense.

I have seen reports that Millenials are buying homes and many of them are buying suburban locations. Nothing ever changes.

What happened to the millenials only want to live in big cities leading to a new era of urbanization? Want to know what happened? Life happened. I saw it happen to me and knew what was coming for others.

These millenials that just 5 yrs ago were going to stay in the cities forever leading to a this new urbanization movement are figuring out that after having kids city living gets a lot tougher. Fighting for street parking, riding jam packed busses and spending half the day 4 blocks away at the nearest laundry mat is bearable when you have no kids but becomes a nightmare when one comes along.

Moving to the suburbs is the solution. This trend will accelerate in the coming years with detached homes nearest transit hubs with good school districts being highly desirable.

“What happened to the millenials only want to live in big cities leading to a new era of urbanization?”

That was the MSM’s fault in assuming a 26 year old would stay 26 forever. When I was 26 I lived downtown. I liked walking to bars and clubs and didn’t really care about school quality nearby (I’m not even sure if there were any schools nearby and didn’t care). Also didn’t really care about how safe my nabe was. I’m a big dude, some sketchy homeless people milling about don’t frighten me.

Then I got married and had kids in my early 30s and all of a sudden school quality and safety mattered, while the number of bars within walking distance didn’t. So I moved to the ‘burbs. Just like millions and millions of people did before me and will do after me.

Only difference about millenals is they’re doing it maybe a little later than GenX/Bommers. But eventually they will all move to the ‘burbs just like their parents and grand parents did.

Just Some Random Guy -The urban movement isn’t made up by the MSM. Each year, a higher percentage of young people live within 3 miles of a city center then the year before. The percentage of 22-35 year olds living near downtown has been increasing for 20 years and will continue to increase until peaking around 2025.

The birth rate is declining. The number of old people looking to sell houses is going to be greater then the number of young families looking to buy.

I agree with a previous poster that the only real estate that will not drop in value is A-rated school districts near transit/easy commute to downtown with some element of walkability.

I’m closing a loan for a millennial couple tomorrow.

I did their loan 3 years ago and now they are stepping up into a larger home, while retaining the current one. Equity increased substantially the past 3 yrs, and now they will rent it out and cash flow.

The down is coming from parents, but, she makes 110k and his business in it’s 2nd year is netting around 50k.

They started FHA with 600 FICO score, but now have doubled their income and increased credit to 740.

Just an example of the following:

Millennials can buy today

Millennials, and people in general make decent money

Poor credit FHA buyers are not guaranteed foreclosures (as many assume)

You can do quite well starting from the bottom and earning your way up.

They get a down payment from parents = they can afford to buy? LOL. (Despite their high incomes).

Are you hearing yourself?

There aren’t nearly enough people in their situation to stimulate demand, and it doesn’t change that housing is out of line with incomes compared to the past 50 years.

Your business is going to get a lot slower in the next few years, sorry.

>They started FHA with 600 FICO score, but now have doubled their income and increased credit to 740.

They got lucky on fed-fueled cheap debt appreciation. Good luck when the bottom falls out and they have to run to mommy and daddy to make the payment, because apparently they couldn’t save a down payment on that marvelous income.

Not sure how to respond to SC7 as the reply button isn’t showing.

In any case, there are more people in similar circumstances than you would think.

Dual decent income that can afford the payment but can’t come up with he down. So, ya, family steps in to help.

Lastly, you could be right or you could be wrong regarding my business and income in the future. That’s why I have 5 yrs reserves in the bank with 0 other debt outside the mortgage. I’m having a career YTD profit so far, and will continue to bank as much as possible.

Thanks for the concern, but, in my eyes I’m doing quite well.

Broker Dan – It makes sense that people with under 750 credit scores are mortgaging up and buying now! My wife and I make double your couple incomes with 850 credit score and can buy a house all cash. Never buying a home again. Not worth being tied down and wasting time and money doing maintenance.

SocalJim – They are not buying in great enough numbers to absorb mass selling from the boomers. Also, they are only migrating to certain parts of the country( South and West). Midwest and Northeast are completely dead. And no, Boston isn’t bucking the trend. Boston is dump and nobody not from Boston wants to live there. Even California can’t attract enough millennials and foreigners to absorb mass selling from the boomers.

Ed,

If you are an ivy league graduate looking for a 500K+ per year finance job, your only options are NYC and Boston. I agree with you that the rest of the northeast is deadsville, but as long as the finance industry continues producing the high income positions, NYC and Boston has a bright future. Boston also has a lock on biotech positions while NYC owns the ad business, but those positions usually max out in the 200K range.

Actually, you hit the nail.. Millennial are in no position to buy these.. and enjoy these expensive hobbies..Long run.. housing prices have to go no where but down.. no one knows when though..

these small dip in sales volume or prices are just noises.. or may be it is the beginning of the something..

Lots of building here – east/southeast of Tampa. Prices are very good – for now. We do have some stimulus here in the form of McDill AFB (Special Operations Command). Many people in my neighborhood work at McDill both as active duty military and contractors. My guess is that like NSA in Maryland (Fort Meade) over the years, there has been an explosion of government hiring and this has distorted the housing market. The private sector salaries here in the Tampa area really stink, so I know its not the non-government income that is the big draw here. I agree with most of the posters here – the market has run its course in most places and is now declining as everyone who can afford a home as already purchased. There are not just a few spot markets – maybe around military bases or high tech markets, but US housing is now tanking.

@Stephen,

The problem with living in a military base area are low wages. Military personnel do their 20-25-30 years and retire after picking up some good skills. Then, they often go back to work. However, because they have a decent pension they don’t need to earn a great wage. And that fact lowers everyone elses salary who have to compete with them. That’s been my experience.

That’s a problem in most of the Gulf Coast even where there is no military base: the “sunshine tax” keeps wages and housing prices lower than elsewhere.

Everyone can just relax! If interest rates go down down down the stream like life is just a dream…then mortgage rates will go negative too!

See, everywhere you turn your looking into the eyes of Utopia and Nirvana! Everyone will buy a house, there will be no homeless, and all because of negative interest rates!! They will save the World! Your monthly mortgage? no no no..they will soon pay you to live in your brand spankin new home! Why didn’t they think of this eons ago??

You’re smoking good stuff keep it up!

Clearly, a lot of potential buyers are renting instead of buying because the tax law changed this arbitrage … a surge of people are looking for rents. I am able to raise the rents on my single family homes by 10% without a problem. People thought the change in the tax law was going to cause house prices to go down with rents not changing much. Instead, what happened is rents are jumping while house prices continue to grind higher. I predict in 2020, home sales will be down while rents and home prices will be up. In 2021, I predict the same. Eventually, a recession will enter the picture, but as long as central banks are easy with the money, the probability of a recession is LOW.

LOL just keep thinking that Jim….

Let’s hope the rates go up above 6.5%. The true value of RE will be exposed!

Keep telling yourself that, Jimothy.

as rents were noted dropping in all of the basin…

your a funny one So Cal Jimmy

cd,

Recent reports show rents in LA are rising at the fastest rate in many years. Ditto for most desirable cities in the country.

SocalJim – Rents are plunging everywhere including LA, Manhattan Beach, NYC, Boston, etc. Nobody wants to buy a luxury home right now and developers have overbuilt apartment buildings.

You absolutely do not have pricing power in SFH rentals when all of your neighbors that can’t sell are trying to rent out their dump properties while competing with brand new construction.

Landlords are getting slaughtered on both coasts. Midwest is still a decent market I’ve heard

I would say maybe 5-10% of my buyers really mention anything to me about taxes and their impact when buying.

Think the most popular phrase is, “I’m tired of paying some one else’s mortgage”.

Truthfully, most people have no clue how the tax law has affected them nor how it will affect them after buying. I honestly don’t think they care, they just want to own their own place. So, the taxaggedon claim is very overblown in my experience.

I tired of paying for all your commissions….

I’m not a realtor, I’m a mortgage broker/direct lender.

I’m not a cheerleader nor a doomsdayer. I think I’m pretty even keeled and just like to report what I see in the lending world and the market in general.

Broker Dan – Clearly there has been a slowdown in the top tier. Every region in the country has a glut of luxury homes that are going through rounds of price cuts. Tax law has dramatically impacted homes on the market for over $750K. People that can afford these homes are smart enough to realize that hey are much more expensive than they were 3 years ago because the tax laws have changed.

Sure, the bozos buying $400K starters don’t notice a difference but the smart money certainly does and are A) trying to unload luxury properties, or B) holding off on purchasing luxury properties until the dust has settled.

Inventory for luxury homes is right around 3 years right now, so real estate will be a slow moving train wreck for much of the next decade. Why do you think the Fed is threatening to cut rates during the strongest bullish in history? Because they know what is coming and it ain’t pretty.

Ed,

You must live in the middle of the country. 750K is low end most desirable coastal cities. There is no 400K.

However, in midwest cities, 750K is a nice home. That might be why you think 750K is high end. Just guessing.

Ed,

Are they waiting till the “dust settles” when the new tax law you have referenced expires? You know that’s 2025, right?

Most of the first time home buyers I know here in Portland (many millennials) knew that the home they were buying (and could afford) was a bad deal if condition, size, schools and livibility were considered but were desperate to get on the property ladder before they were priced out. They figured that they could always sell for a higher price in the near future and move up to a better one. That was back in 2014-2017. But now their fantasy of constantly increasing home prices has been shattered and decreases in interest rates don’t restore their confidence in the golden property ladder. The ones I know that are still sitting on the sidelines are waiting for the market to deliver an actual house they want to live in. In the mean time, the growing glut of shiny new apartments with 3 months free rent and fancy amenities is making the wait more enjoyable.

But but but slumlord Jim said rents going up 10% on his poor tenants…. You better buy now before it’s too late!!!! LOL

Senecas Cliff – A thing I’ve observed for years is, when a person rents an apartment they think in terms of what they need, and tend to rent the smallest one possible. When they buy a house, this gets turned on its head and they buy the biggest place possible.

So now they’re shelling out at least 2X what they were for shelter, and maybe they end up with a shitty local government, Neighbors From Hell, or any of a number of other things that make their lives miserable, and they can’t move so easily.

Alex,

Constructive criticism here. You seem like a bright guy, but, you ALWAYS think the absolute worst about everything. People don’t want to hire or be around a negative Ned.

I truly think you could improve your prospects of you weren’t so Doomsday about everything.

Tech experience, ever thought of trying to do some consulting or a small biz helping people with CPU issues (think Geek squad and market online like Craigslist). But you got to market yourself and not want to talk people into killing themselves.

Broker Dan – I’ve pretty much seen and done it all, and my biggest niggle about myself is I’ve never been pessimistic ENOUGH.

Alex,

Thats the wrong attitude IMHO.

Broker Dan,

What if I were more pessimistic and paranoid? Firstly, I’d have stuck with what i know works, art. I grew up doing everything from “fine art” to painting faux car safety inspection stickers. I’d have “learned the Speedball book” (a book of fonts) like the hippie hangers-on we had around when we were on Welfare advised. I’d have done the math and realized that hustling little drawings etc would have made me more money, more easily, than working for $3.50 an hour doing fairly hard labor all day.

I’d have stayed the hell away from tech, to which I had a first-row seat, watching my father get poorer and poorer because he had the idiotic idea that you can make a living programming computers. His passion was carpentry, and he really should have gone with that.

Wolf is right, in that older workers are often best off starting consultancies of various types. He’s got this site, which makes some money somehow, and others can write books, etc.

As for Geek Squad type work, there are tons of kids right out of HS who want to, and can, do this work better than I can because they don’t actually hate computers. They actually like ’em!

I *am* looking seriously as developing brush lettering skill and picking up where I left off as an artist, because there’s dependable money in that. Lettering, pinstriping, signs… Look on Etsy and there are any number of people doing CNC stuff but hand-painted signs are rare, and good ones even more so.

Frankly I’d rather sell on Ebay but I can take a few years building skill, then if it looks promising leave my present employment and thus be out from under the “non-compete clause” I’m under now, and sell on Ebay on my own again.

I’m early 30’s – single dad – make close to $200k – 800 credit – no debt – tech industry. Buying a $500k starter home or condo in ATX would still stretch my budget (w 30 yr note) Of my 30 employees – I would guess maybe 2 could buy a home at these prices without significant outside assistance (eg family benefactor etc). People can argue over generational pretext / disposition all they want – bottom line (IMO) is wages go 50% as far as they did 15 years ago. We are now a 2 income mandatory society – even then we have to stretch. Who’s the marginal buyer from here? 3 income households?

Ty,

“We are now a 2 income mandatory society.”

I love that phrase. So true!

True, but sad… Actually stole that phrase from a mortgage broker friend. I asked him how many single income applicants he had (as was my case) – he couldn’t remember one! People would rather degrade each other’s financial literacy than accept the obvious fact that it continually requires more to achieve what was previously status quo. Thanks for the great content – all the best.

Nailed it TY.

That’s why in BC, newly arrived east Asians buy a house with all their relatives, pay it off, and do it again and again. Everyone works one way or another and the family ends up wealthy as lords. On the Prarries Hutterites do it and run their lives in communes. They are wealthy wealthy and more wealthy. Their neighbours hate their achievements but aren’t willing to make the same sacrifices.

I grew up in a small coastal town with a large Vietnamese refuge community – same story. Communal family wealth and a generational perspective to home/business ownership. Grandparents were literally dirt poor – kids my age are more/less secure for life. We are still a land of tremendous opportunity – securing that opportunity just takes more than it once did. All the best…

The hud’s and men’s have fans and haters in the prairies. The hater’s are jealous and the fans have connections for delicious honey and high quality colony labour. I am a fan, I no longer have my former connection to high quality labour these days, but I still get that delicious honey.

You should watch them reno a house, absolute work of art watching the whole machine of family and friends tic toc like a clock.

Ty, 200K income with a 20% down puts you in a home north of 1.1M. You should be good.

Can’t afford 500k ok 200k income with 0 debt?

Cmon guys, taking it to the extreme.

20% down and assuming 2% for property taxes, that’s a 2700/mo PITI.

That’s like 17% DTI. Extremely conservative there.

My HHI is a bit north of $200k, and I would never take out an $880k mortgage. Everything goes up when the cost goes up, including maintenence. If I was starting from the ground up now, I would still cap my purchase price at $550k-$600k.

@Broker Dan

I agree the OP might be a little too conservative, however, people are doing right to assume they may not be able to replace their income with a job paying the same as easily. Many people assumed before the 2008 crash that once you make a salary, you can always replace it.

500k is 2.5x income for $200k, so I agree with you it’s affordable. My only conern being the OP would be, if/when we enter a recession, how much below $500k is that house going to go. Just wouldn’t feel right to me entering the market as a buyer now.

SC7, never take out a 880K mortgage? I would, but only for a property that appears to be a great investment. For example, a beach close home on a quiet street near a job center is a no brainer. In the future, if you are over your head, that is a great rental that will pencil out in 5 years. However, for an inland location not close to a major job center, a 880K mortgage is stupid and can cause you to lose everything in a recession.

@socaljim

No thanks, not a fan of the leveraged debt-donkey lifestyle hoping for more fed-fueled inflation. What worked for you in the past 20 years doesn’t look nearly as good moving forward with the asset values blown up, and little more interest rate motion to go.

I would not be comfortable with that much debt on my primary residence. Extra income beyond a certain point offers me peace and comfort. I’d rather have my $450k home paid off sooner and life comfortably with other investments (potentially including other properties), than have that much mortgage debt where I live.

Also, the type of house I’d want to spend $1.1m on would be a house in a nice suburb. Those are hard to rent out (people who have $4k a month like to buy), and require a lot of maintenence. Throw in an increasing rate scenario where values decrease… not a lot of positives to me.

“Who’s the marginal buyer from here? 3 income households?”

This is actually happening. Husband+wife+parents social security/retirement = 3 incomes for a 4 bdrm home. It’s happening here in the Bay Area. Existing 4bdrm homes sell like hot cakes while many new construction is built with multi-generational in mind.

I honestly believe we’re heading back to multi-generational living especially here in the central Bay Area. Nothing wrong with it as long as you can deal with the inlaws. In house baby sitting, help picking up the kids from school, help with domestic chores, etc. Saves the parents a lot of time so they can work on their careers and make more money. For some it’s the only way to live here and for others it’s a cultural norm.

Yeah Ty, what you said facetiously is, in fact, the future: Multigenerational Housing. Maybe that’s good thing.

Or the immigrant way: Multi-family SFR…

Ty,

Sorry man but that’s BS.

Even putting $0 down, you could easily afford a $500K home on a $200K salary. PITI on a $500K home at today’s mortgage would be $3000 a month which is not even 20% of your gross income.

It’s absurd that we’re at the point where people earning $200K are playing the victim card.

So true. I understand trying to be fiscally conservative and make sure you have enough on the reserve take, but, can’t afford 500k on 200k income with 0 debt is a joke.

That’s swinging the pendulum way to far the other way.

Geez.

Senecas Cliff – This is so true. We bought in 2011 because there was a shortage of decent rentals and rent was going up 10% per year. After we bought, houses started going up 10% per year and rent started going down. We sold our house and move every year to a brand new building with two months free rent and incredibly nice amenities with 50% occupancy.

Now that there is a glut of luxury rentals and I have plenty of money, why should we ever buy a house and tie up liquidity? I like the freedom of being able to move and not have to waste time maintaining a house.

You move every year? That sounds horrific.

For us older people, there is a different challenge.

The locations of our homes are probably OK and the proximity to good hospitals and doctors, fine. But, there is a problem.

When you get older, there is a high probability that you will be asked to go to an ASSISTED LIVING home. Do you have any idea how expensive that is?

Anyway, the challenge is (as long as you are aging healthy) to remodel your existing house to be AGE-IN-PLACE certified. You will need money to do this. The trend is, unless your house is AIP certified, your judge MAY have a tendency to rule you be in a nursing home. Considering there is huge number of us aging, this is a money issue ignored.

This is another new housing topic for older people.

Where do judges kick old people out of their homes?

If you get old and frail, the judge orders you enter a nursing home and they take at least $50k per year from your assets.

The judges first name isn’t Jim, is it?

DawnsEarlyLight – it might well be, and this is not something to joke about. It happens all the time.

This surely isn’t true, is it? In Canada a senior’s family can step in but it is beyond hard if the senior is not cooperative; virtually impossible. If violence occurs, then the RCMP start a file on the senior and it can unfold where they are removed, but the senior has to be a danger to others and community. If people want to die at home no one stops them from doing so.

Big time agree w/Imafan. Having a McMansion out in the far outer burbs means lots of driving. When you’re 75 or 80, do you really want to get in the car to pick up your meds at CVS? Not to mention cleaning that 3,000sf house on the 1/2 acre lot. Either mow it yourself or pay someone when you can’t do it any longer.

Alternatively, find a smaller place close to health care; groceries; and public transportation. If you are close to the train or bus stop, it is a lot easier for Visiting Angels and the like.

Agree … furthermore, realtors tell me that older folks want single story because stairs are a killer for old knees and hips.

Hell, I am in my late 20s, in shape, and I prefer single story living. There’s far too much excess in this country.

sc7 LOL but do you belong to a gym and drive there so you can go on the Stairmaster??

My joke around our house when someone’s too lazy to get something up/downstairs is…Don’t you realize people are paying gyms to use pretend stairs? And you have real ones here, for free!!

But to Jim’s point, the reality is our downsizing-for-retirement home (soon) will be single story.

Iamafan:

Yes. As an “older” (really old) person I and one of my oldest and her husband have looked into the “assisted living” life and the picture is not pretty.

Our searches have been in CA Central Valley and in the Santa Clara Valley. For a nice place in the Central Valley (won’t mention any names) it starts at $3000 monthly for “unassisted” living; any assistance further means a steep escalation of prices.

The Santa Clara Valley searches will increase the cost a minimum of +$1,000.

Even with some good decent savings and a home it can go really fast. I’m still lucky that I can take care of myself; shop for groceries etc. But, my stamina is slipping fast.

We’ve decided that I will stay in my home until I have to be carried out. Period.

Then mercifully it will be over quick and I won’t have to spend all I’ve worked for overnight.

Other commenters have talked about the “multi-generational” living. As a first generation American that was the way most immigrants lived. That makes for a better society I believe but doesn’t make the capitalists very happy.

Everyone (including your pets) is a “market” in the US. “Communal living” puts the kibosh on that concept. Our form of capitalism (in my opinion) will devour itself if the medium to long term. There can be no other outcome.

Iamafan – More people should just kill themselves and leave assets to the kids when a nursing home comes into play. Not joking. I hope I don’t live long enough to have a nursing home steal all of my money.

Congress has just killed any hope of restraint with the raising of the debt ceiling. If the fed lowers interest rates next week QE will follow. Debt will be have to be destroyed before significant generational house buying occurs . Households are not forming . The liquidation of the boomers will follow. Youth will have to be patient but Time is on their side. We boomers will watch it from the nursing home/death houses while the liquidation is in progress. I myself hope I have lucid moments between the Benadryl dosing so as to get a giggle. Hell,they will probably have robots in the nursing camps by then and I can hurl insults at them until liberals give them minority status and victim rights for hate crimes against robots.

nice Dr. Doom….

they better have something better than Benadryl by then….

I’m stealing a sailboat to be a pirate and die at sea, why die with robots…

Dr. Doom and cd:

I believe the operative substance is Morphine…….that incessant “drip” that in escalation separates the mind from the body……

But eventually results in peaceful death from CNS shutdown.

As for this boomer, have no interest in long term care. Will make short appointment with geriatric specialist Dr Glock, at the time of my own choosing.

I heard about a new chain of nursing homes for old Republicans run by all young democrats. The name of the chan of homes is “Death’s Door.”

I think it’s undeniable that the Fed had re blown the housing bubble…to just one assets it’s re blown. Even my own lying eyes tell me this: my neighbor just get house well above what paid and just latest of many. And the internets says my house is worth 15% more done last December when the U Turn happened.

You keep citing the same neighbor’s same-house story time after time after time week after week after week. If that single event is your gauge of the national housing market, you’re on to something big, namely the Single-Sale Timbers Home Price Index.

Don’t forget his boss’ bidding war where he was one of 324 bids at 200% of asking price.

Haha, that was good stuff right there wolf.

Seems similar to the other popular phrase, “well my 2 other friends don’t make more than 50k/yr, so, no one in America can afford to buy houses”

Do tell which highly inaccurate site is making this estimate? Zillow has my shack in the burbs of Boston completely sideways. Shillow is also predicting a decline of most towns over the next year.

I think there is another bigger factor missing in this report. College Educated Millennial Debt. Typically, first time home owners in the past were primarily college educated new professionals starting their careers with higher than average wages with little to no significant debt. Now, recently college educated professionals come out of universities in debt with a minimum payment plan that will not be cleared for the next 10 years. This home sale slowdown is for the long haul. It is an economic systemic change. Home sales are going to stagnate for a very long while.

If people can’t clear a student loan debt of on average $34k in under 10 years, the problem is them.

I sometimes ask our STEM interns about student loans– not specifically, as that probably would be a privacy violation, but generally how it is affecting the students they know. The typical reponse is that neither they nor anybody they know has any significant student debt.

I know there are exceptions, and that student debt can be a worthwhile investment. But in many cases it seems to subsidize a party lifestyle.

I paid off my student loans from an “expensive private school” in six years, which weren’t too much because I only went after learning I had gotten a 2/3 scholarship. If I didn’t get that scholarship, it would have been public school for me.

It was a modest five-figure sum, and I went to grad school at night while working. Living modestly and accelerating payments did it, my income shot up after completing the grad degree which helped, but I was still on track before that increase.

As my social circle starts to move into our 30s, the only people I know still with any substantial student loan debt are:

-$100k for an art degree

-$130k for a social work degree

Two easily avoidable mistakes. The second one wised up and got some IT certificates and is now making good money. The first one, though… My point of all of this being, it is definitely the exceptions, and a government handout is not the solution to this issue.

Student debt:

Oldest grandchild 29 married, wife received her vet medical degree two years ago (8 years)….student debt upwards of $300,000. They both make decent money but that debt will ride them for years. They are the kind that will pay it off come high flames or death. But, it will also keep them from purchasing a “home” in the near future. Both very hard workers.

Part of the adding to the conundrum is millenials who want to move up in housing can’t because they can’t sell their existing houses. My son & daughter-in-law just experienced this. They are motivated to buy, thought they had their house sold & the buyers backed out. So that killed the deal on the house they wanted to purchase. A lot of potential buyers are skittish. They see the writing on the wall with the economy & their futures. It’s not a pretty picture. And maybe they have people like myself warning them about 2009 all over again. Buying at the top, losing your job & then seeing your house value crash in a matter of months. Back then, you could write off a huge loss due to the Debt Foregiveness Act that Bush Jr. was responsible for getting approved. That was a life saver. I don’t believe those experiencing a cataclysmic loss like that now would be so fortunate.

So the best advice I would give to anyone now is wait. Wait for the inevitable to become reality & then cash in on the “Fire” sales of a lifetime. It’s coming soon.

Double D – I think unfortunately a lot of the fence sitters are going to get burned in the opposite direction. You mentioned yourself that 2009 was ” fire” sale of a lifetime and you were right. None of us are going to be lucky enough to buy real estate again at rock bottom prices.

The Fed is telegraphing hyperinfation AGAIN and people are still scared to dip their toes in the water. The stock market is pricing in 75 bps in cuts and maybe even QE4. The Fed is turning on the money fire hose again that made so many people rich over the past five years.

I believe that luxury real estate in high tax top cities (NYC, LA, SF) is going to take a hit, but 2nd tier cities might be in for another 50%-100% gains now that the Fed has turned the hose back on.

The economy is red hot and outside big metro areas, i think real estate in good school districts might actually still be undervalued and affordable.

My guess is that hyperinflation in housing and child care is a greater risk than the median price of $284K going down even further. $284K is outrageously cheap at 3.8% interest. Any household earning over $100K per year is paying off that loan in less than 7 years.

Thanks for the charts, Wolf!

My Crystal Ball says when interest rates drop to the Oct 2016 levels and house prices drop to 2011-2012 levels, the sales volumes will go through the roof! Me included.

I’m predicting a retrace to 2001 prices. You heard it here first.

Inflation adjusted 2001 prices I could believe, that was before the first

bubble took off. No way we hit pre-adjusted values, though. There would have to be zero demand for that to happen.

SC7, that is a good point.

From Wolf’s previous post, the 1990-2000 housing drop was due to inflation. Housing prices were flat and wages and inflation were going up for a decade. The inflation adjusted decline in housing prices was actually worse than the 2008 crash.

If prices and interest rates remain flat for housing but wage inflation ramps up, we will see housing demand slowly ramping up over the next 10 years. House prices will be a bargain in 2029 if you account for inflation.

When I shake my Crystal Ball and turn it over for the answer, it doesn’t say how we will get there.

Right. Just like that guy on drhouseblog which I stopped visiting bc he had 25 different handles and repeated the same innane line.

Housing to crash 70% right around the corner!

It’s not feasible to have a decent conversation or debate which someone like that.

Senecas Cliff – I am willing to bet you a lot of money this doesn’t happen. Much more likely to double in value then fall 50%-75%. The Fed will not let that happen and they have proven they can inflate real estate by dropping free money out of helicopters.

What makes you think the Fed cannot inflate real estate through QE? Cutting rates during the biggest bull market is history is going to lead to hyperinflation.

In our oligarch-looted economy, wages and job security are insufficient to afford housing blown to bubbleiyious levels by the Fed’s deranged money printing and ultra-easy monetary policies.

Gold is getting a lift as the Keynesian fraudsters at the ECB get ready to huddle to plan the next escalation of their financial warfare against the 99%. Foregone conclusion from the confab: a gusher of new printing-press “stimulus” to further levitate the ECB’s Ponzi markets and asset bubbles. Their globalist handlers, meanwhile, are stepping up their looting and asset-stripping of the productive economy and demanding more austerity for the proles, while their media sock puppets bemoan the rise of “far right” movements – so utterly mystifying.

Single male, debt free millenial, 780 credit score here. Closing on my first home Friday in Tampa, FL.

Astonished at the process, i’ve never been involved something so inefficient in my life. This industry needs to get Uber’d ASAP. So much waste and inflated services and redundant jobs.

No one is building entry level affordable homes. Its all condos and luxury homes. People like me would never want to live long term in a condo where you share walls with loud neighbors.

However I do not think I am buying at the top of MY market: population (esp in Tampa) is rapidly growing and the supply is not. I feel that I got into a house at one of the best times in recent years given the crazy low rate I received –probably best time to buy since the big dip after the recession.

Boomers had it good – could skip college and get paid well, buy a home with a button and some pocket lint and get a pension at 50 to retire, SS at 65 and live easy. This will not be reality for any generations after them

Different experience for different people. When I bought my first home years ago I had 3 conversations: home owner for price negotiation, bank to get approval, lawyer to write up the mortgage sale agreement.

Last time I looked into buying I tried the realtor experience, complete joke. I don’t think the home owner was told about my offer, since the house sold for less than my offer a year later. My offer was low, but accurate for the time.

A bit of a small town luxury is talking to the home owners instead of realtors, I won’t deal with an agent next time I am in the market.

REGULATIONS are the reason for your experience.

P.S. Congrats on the new home

Are there any numbers on the homeowners using reverse mortgages? Once you get locked into that you aren’t going anywhere.

New rules/regulations have actually cut Reverse lending significantly. High equity and income/credit qualification needed.

HUD has been bleeding on losses from those from the past decade.

I’m in North Texas (DFW area) and I am waiting to buy. There’s nothing out there worth the money. Everything is waaaaay overpriced. It doesn’t matter what category. Builders are offering huge incentives and lot’s of free upgrades but, in the end, it’s still overpriced. I just can’t do it. I see inflation inflation inflation. The housing market is inflated so is the stock market.

Prices are slowly coming down, not fast enough for me, I need a house.

To “The Real Estate Industry”

Fool me once, shame on you.

Fool me twice, shame on me.

Take a look at Bozeman, Montana. You won’t believe what you see and the quality of life. It’s truly God’s Country and the best kept secret location in America.