Kudos to the private equity firm. These things don’t happen overnight for companies. They happen overnight only for investors.

Golden Gate Capital – the private equity firm now infamous for asset-stripping its portfolio company Payless ShoeSource into bankruptcy and liquidation – strikes again with another of its portfolio companies, Clover Technologies, whose $693-million leveraged loan has suddenly gone to heck.

Slices of that leveraged loan are traded like securities. But because leveraged loans are loans, not securities, the SEC doesn’t regulate them. No one regulates them, though the Fed wrings its hands about them periodically. And there are $1.3 trillion of them.

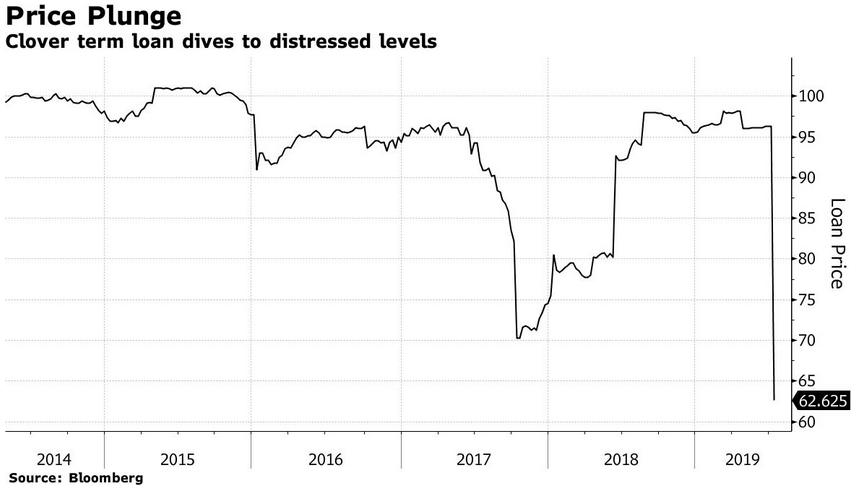

The market for them is very illiquid, even during good times, and before Clover disclosed some issues on July 9, the loan still traded at 97 cents on the dollar, according to Bloomberg. This was the day investors, such as leveraged loan mutual funds and institutional investors that held these slices, suddenly woke up with the foul odor of debt restructuring and bankruptcy in the air. Within just a few days, the price of the loan plunged 35% to 62.625 cents on the dollar.

The loan was “covenant-lite,” giving fewer protections to investors and allowing the company and its owners to get away with all kinds of things. This included the absence of certain disclosure requirements.

Not that we feel sorry for investors that suddenly got whacked: They knew that leverage loans are risky, that they’re issued by junk-rated over-leveraged companies with iffy cash-flows, often to fund their own leveraged buyout by a PE firm, and to fund special dividends back to the PE firm. Both factors apply to Clover’s leveraged loan. Investors don’t care. They’re chasing yield no matter what the risks, in a world where yield has been repressed by central-bank policies.

These slices are not liquid and they take a long time to trade, and trading is thin even in good times. But when investors want to unload, there are suddenly no buyers and the price just collapses (chart via Bloomberg, click to enlarge):

Clover Technologies, founded in 1996, is “the world’s largest collector and recycler of imaging supplies,” it says on its website, such as printer cartridges. It also recycles and refurbishes smartphones in facilities in the US, Mexico, Europe, and Asia for wireless carriers that then resell the refurbished phones to their customers.

So on July 9, Clover’s parent, 4L Holdings, disclosed to investors that Clover was losing two big unnamed customers. One was in its printer cartridge business. The other was a wireless carrier that was buying Clover’s refurbished smartphones, but has “decided to fulfill requirements for refurbished older units by purchasing them directly from the OEM,” such as Apple or Samsung. That customer remained unnamed, but “people” told the Wall Street Journal that it was AT&T.

In its disclosure to creditors, the company said that it had hired restructuring advisors, which is often an indication of a pending debt restructuring or bankruptcy filing. It invited creditors to organize and hire their own advisers. And it proposed a meeting for the week of July 22.

This was the moment investors woke up. When investors tried to sell their slices of the loan, they found that buyers at these prices had evaporated, and to sell the loan at all, they would have to take a big haircut.

When a highly leveraged company in an already tough business is threatened with the loss of revenues, there is no margin for error, as cash flow needed to service that debt can just dry up, and the results can be catastrophic for investors.

And even if the company can muddle through, at some point the debt matures and has to be refinanced, and when no new investors can be found to bail out the old investors, it’s over. This is what Clover is facing.

The $700 million leveraged loan is coming due in May 2020. Clover tried to refinance it last May, when it might have already known about the potential loss of customers, but had not yet disclosed it to investors.

It offered a juicy yield of nearly 9%, but investors balked and wanted a better price (higher yield), “people said,” according to the Wall Street Journal. Now, after the disclosures of the loss of customers, refinancing the loan is off the table altogether.

But Golden Gate, which had acquired Clover in a leveraged buyout in 2010, wasn’t shy about stripping assets out of Clover via $278 million in special dividends it extracted, according to Bloomberg: $100 million in 2013 and another $178 million in 2014.

That $178 million dividend was funded at the time by Clover issuing a new leveraged loan, the current one, whose proceeds were also used to pay off the prior loan (new investors bailing out old investors) and to fund an acquisition.

Golden Gate got its money out. Clover had more debt. Old creditors were bailed out by new creditors. The banks arranging the leveraged loan made a ton in fees. And everyone was happy. But now these new creditors – which include unwitting investors in those funds – ended up holding the bag.

On July 11, Moody’s chimed in with a devastating three-notch one-fell-swoop downgrade, to Caa3, just a couple of notches above default (here’s my plain-English cheat-sheet for the corporate credit rating scales by Moody’s, S&P, and Fitch).

“The downgrade reflects the likelihood of a default is high given the recent downward revision in earnings guidance following the loss of business and pricing pressure in both the imaging and wireless segments combined with the maturity of the first lien term loan in May 2020 that will put pressure on the business,” Moody’s said.

“The company’s hiring of restructuring advisors, request to meet with lenders in a few weeks, and challenges refinancing the term loan indicate a restructuring will occur soon,” Moody’s said.

“We also remain concerned about the longer-term business viability as a result of more limited visibility into forward financial performance and related uncertainties given the unexpected operating developments,” Moody’s said.

The near-default Caa3 rating reflects “the high balance sheet restructuring risk” along with the “near-term debt maturities,” and “the ongoing business and execution risk as management evaluates its strategic options,” Moody’s said.

These things don’t happen overnight for companies. They happen overnight only for investors.

The company had already suffered revenue declines and pricing pressures in its major businesses, according to Moody’s. Clover is also heavily dependent on just a few big customers, two of which are now leaving.

The secular downtrend in the printing sector and the competitive challenges in the smartphone-refurbishment sector, along with Clover’s high customer concentration were known to investors, but given the glory times we’re in, fundamentals no longer matter – until they suddenly do.

Moody’s also lambasted the company’s “aggressive financial policies, evidenced by its private equity ownership and history of shareholder distributions and large debt-funded acquisitions” — a reference to Golden Gate Capital.

Moody’s slash-and-burn downgrade, and the subsequent plunge of the loan deeper into distressed territory turned more institutional investors into forced sellers as they’re limited to what extent they can hold distressed debt. But it’s no biggie. It’s just other people’s money. And that loan is now a plaything for hedge funds specializing in distressed debt, and they’re hoping to make a killing. However this turns out, kudos to Golden Gate. They’ve done it again.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wow. A company that specializes in refurbishing products, with no intellectual property of its own, just screams of disintermediation.

I’m surprises AmazonBasics hasn’t come after the ink side.

A shell within a shell. The refurbished tech market is big, and about to get bigger. You wonder if equity extraction is just their way of booking profits early. If you like the business why not like the bonds? Something for everybody in this deal, consumers, bond investors (and equity vultures).

“How did you go bankrupt?”

Two ways. Gradually, then suddenly.”

― Ernest Hemingway, The Sun Also Rises

I find this whole process fascinating. People weren’t really loaning Clover money to expand their business. They were giving their money to Golden Gate with the hope that they would eventually going to get it back with interest from the now weakened Clover.

But were they really even doing that? Suppose this is all just playing with other people’s money. Maybe the money managers received some form of compensation for “investing” other people’s money into an enterprise they knew would fail.

Wouldn’t it be nice if we could find out the names of those making the decision to make the loans? Certainly impossible, but maybe repeated public embarrassment would cause them lose enough customers that they’d have to find a way to fly straight.

Who will pick up what left…Chinese? Oem? Management buyout?

Yes. Step right up folks.

Pick your lucky number and lay your money down.

Round and round she goes,

where she stops nobody knows.

Better luck next time Chump!

“What’s business? Simple. It’s other people’s money”

-Alexander Dumas

Famous 0.1 (or less) percenter of his time in business. (among other things)

Last part of quote was spun by the likes of Thatcher/puppet Reagan, and many, many others to this day.

You can depress interest all you want, but how about sales, margin, and gross profit let alone labor or material costs. I think the Fed FFR decrease Wall Street is wanting is nothing but to sugar coat debt service. I think something’s going down.

Lots of good insight

Do those things really matter now..? I honestly don’t think they do.

Due to far too much power being handed to the financial sector by the ‘big boom’ deregulation (and with it the associated glorification of greed associated with Thatcher/Reagan) – gleefully continued by the so-called left wing of the 90s – we now have been left with a form of vulture capitalism, further enabled by manipulated IRs to hand the vulture capitalists lots of cheap borrowed cash, which concentyrates on nothing apart from short-term stickholder returns.

Neoliberal dogma legitimises this greed and self-interest by declaring the ‘trickle down’ effect of all this stockholder wealth will bestow riches on us all. Naturally, this hasn’t happened.

Add into the mix the fact that a a lot of these stocks are traded on ‘momentum’ (ie bigger fool theory) by machines, and you have a situation wherein stockmarket indexes really have nothing whatosever with the real wealth and prosperity of a nation.

The most dangerous aspect of all is that out politicians really do seem to believe that they do – because NOT to do so would mean that 40 years of ‘there is no alternative; thinking (end of history ‘n; all that jazz) was in fact nothing more than a route to crippling debt, and soon-to-be third-world status.

What amuses me is that these supposed “real smart” people such as the likes of Thiel (sp?) all have their “bug-out” palaces in New Zealand. There are tons of poor people in Auckland, and it won’t take them long to find out where the lights are still on.

I see so much absurdity here:

– Rating agencies who rated the instruments higher than it should have been. I am not even sure rating agencies have enough expertise and resources to accurately rate all the instruments.

– Investors chasing yields blind to the risks. Isn’t it conventional wisdom to not invest in things they don’t understand?

– Fed keeping rates so low for so long to push investors towards riskier instruments.

– Lawyers and schemers who know where loopholes exist and aren’t shy of exploiting them.

I think Marx had something to say about what happens when money becomes the economy (and by extension I guess when debt becomes a product) – what we now refer to as ‘financialization’.

Maybe soon he’ll be proved to have had a valid point.

I think the word “finaglization” is what is taking place.

You’ve just outlined the rules of the Wall Street Casino. Buying leveraged loans is the dumbest thing I’ve ever heard of. Having worked as a collateral working capital lender in my 38 year career, and having participated in more than a few bankruptcy work outs, buying a piece of a leveraged loan is insane. Advance rates are calculated on a “going concern” basis and can be adjusted downward if risk increases. Should the client go bankrupt the realized recovery can be 10ths of a percent of the initial loan. Buying a slice of that loan without daily or more updates on the client’s financial condition is throwing dice at best, or throwing money away at worst.

GB….you have hit a couple of good sore spots. Leveraged loans came in under the radar of even the private derivatives markets because the stake was a mere few trillion dollars instead of tens of trillions of dollars. A desperation for yield, matched with overt speculation to obtain that yield and more, has taken over the mind since rates were cut so far in 2008 to save the major banks and insurance companies. The bond market, by itself, has been a disaster since 2009: Limited supply matched with plummeting yields and spreads. That premise opens the door for “creative” under the table financing that will go unnoticed as long as it doesn’t pose a systemic threat…….like the CDS markets posed in 2008.

This should scare the hell off Japany CLO investors.

Imafan,

These Japanese banks that gorge on CLOs only invest in the highest-rated slices of the CLO, they say. The lowest-rated slices of the CLO take the first loss. So the calculus is that even a good-sized loss won’t make it up all the way to an AA-rated or AAA-rated slice because there is some collateral backing the underlying leveraged loans and so there should be something there at the end. That’s the gamble they took and count on winning.

Wolf, I think I’ve heard the same story (or at least similarish stories) on Wolfstreet several times over the last year. It is amazing that LBO and private equity firms continue to do this, from Sears to Toys R’Us to this. It’s like an endless parade of vulture capitalist sucking out cash and then throwing the workers out on the street, after which, people point to Amazon and claim its their fault.

All abetted by these rating agencies that give AAA ratings up front. I’m somewhat surprised that no one from these agencies ever looks at how the first set of loans gets used.

Well unless you have INVESTOR losses, Wall Street does not care. Workers don’t count.

MCH,

I agree, this has happened so often as to hardly be news. What amazes me is that the people who bought the loans apparently aren’t aware of the frequency of these things going south. You would think that the behavior patterns of the riskiest lenders would be obvious.

It must be that the country is so awash in cash that the principle is irrelevant. All that counts is the monthly interest payments. And if the lenders get a few years of payments before they lose a big chunk of the principle, they don’t care, they have more money to invest, so they do it all over. It’s like living in Alice in Wonderland.

These are NOT investors. These “people” or entities do NOT care whether business will be good. They only care whether there will be somebody else willing to buy from them with a higher price LATER.

You can criticize them making wrong judgement on businesses or do wrongs to employees. In the end they “TRANFER” money into their own hand. Building business is for suckers. Churning bond paper and merger acquisition using zero rate fund is king.

Wolf’

Will you comment on the following:

1. Do you see a similarity b/w 08- 10 housing crisis and a potential PE Acquisition / Leveraged loan crisis sometime soon?

2. How would / could one tske advantage of this situation if it happens? Find PE sponsor, source opportunities and negotiate w debt holders? Would be interested to hesr all your ideas

Thank you

Andrew,

The first question is easy: the magnitude is different. In the housing crisis, mortgages were a $10 trillion problem. Leveraged loans are a $1.3 trillion problem. And many of them will be OK, just like many of the mortgages were OK. “Only” about 10% or 12% or so of the mortgages defaulted. So if 20% of the leveraged loans default, the problem loans will amount to $260 billion, and there will be some recovery, so the actual losses will be smaller, and the world can digest that. These are investor-owned loans, so the banks will largely be off the hook.

I’m not talking about derivative products here. That’s a different story, and it could provide for some surprises if leveraged loans run into trouble.

The second question is hard. When leveraged loans default, creditors can take possession of the collateral. And then they might try to sell the collateral at fire-sale prices. So there will be some opportunities there. But this is something where you have to go and inspect the collateral. This might be some equipment or inventory or some other physical assets.

The PE firms that backed these companies are shareholders of these companies. So they will probably not be your negotiating partner :-]

There are plenty of “distressed debt” funds, and if you’re financially heavy enough for them, you can join one of their funds when they go fundraising.

In terms of buying stuff with the click of a mouse in this situation — that would just depend. A publicly traded company that defaults on its loans will likely wipe out its stockholders, and the stock will get cancelled in bankruptcy court or become nearly worthless. So that’s not a buy. If the company also has some senior bonds, you could gamble and buy some of them through your broker, if you can. But you need to know what you’re doing or you’ll get shredded by the pros.

If there is a leveraged loan crisis that is large enough, the stock market will get into serious trouble in general because many publicly traded companies have issued leveraged loans, and suddenly these companies are in trouble. So if you time it impeccably, you may make a buck buying their shares – or lose your investment :-]

That sounds almost verbatim what they said about CDOs just 15 years ago, right up until the super-senior tranches weren’t so super. How much does one trust that AA or even AAA rating? At the end of the day, do investors really know what’s in their tranche? They say history doesn’t repeat, but it sure does rhyme (CDO…CLO…what-next-O…).

Calm Horizons,

The scary thing is they’re now saying everywhere that today’s CLOs are no comparison to the CDOs that collapsed at the time, that they’re far superior and not nearly as risky, yada-yada-yada.

If there were at least a modicum of self-doubt by Wall Street about these CLOs, I would be a lot less worried.

The good thing is, foreign investors (Japanese!) are big into them. So if these CLOs blow up, they’re going to splatter into someone else’s face… come to think of it… that’s not a good thing… that’s why a US financial crisis becomes a global one – because this crap is everywhere.

but they are more likely to have less covenants this time? That is definitely a con.

That’s what people thought would happen with the housing-related alphabet soup back in 2008, when the holders of the higher tranches suddenly found themselves holding a bag full of toxic excrement. Corruption of the rating agencies also played a big part in the debacle, as much of what was rated AAA really wasn’t.

No surprise that the same thing is happening again, since nothing really changed.

As you say, it works until it doesn’t.

My guess is this is just a warning shot for more leveraged loans to default. There are hundreds of zombie companies(i.e. firms that have insufficient cash flow to service their debts) that have been able to access the capital markets over the past 10 years. When the music stops playing, the liquidity will be gone.

In the case of Clover, I have to applaud GG Capital for being very transparent in fleecing the “smart” money. I would love to see the prospectus for the latest loan that provided the special dividend to GG investors.

I would be interested to hear the ‘investor stories’? Are they individuals chasing yield, or are there ‘financial advisors’ buying on behalf of investors? My neighbour lost 125K in 2008 when the “financial advsior” (son of another neighbour) didn’t sell in time. Supposedly. “He cost me 125 thousand”, goes the accusation. Or, do people park money with so-called experts and walk away with an expectation of reaping rewards without doing homework or exercising due diligence?

Did the financial advisors/buyers get a pat on the back with commisions, leaving their clients holding the bag?

Greed, and chasing yield seems to be too simple of an explanation for people getting fleeced in this instance.

Following the Epstein trial/investigation unfolding in NY. Along with several mansions, two private jets, a safe full of diamonds and cash ect…. he also had a bank account holding around $100 million in cash. Now why was a clever hedge fund guy like Epstein heavy cash? …. something is brewing.

A couple of things to note. Epstein is not a hedge fund guy….at least, not now. His association with any hedge funds is tenuous at best. He is really what he has been cast to be in some quarters…an intelligence asset. Why would he need large amounts of cash? Well, to run operations. The Epstein case is unique because this is actually a war within the deep state and one part of the deep state wants to expose the pedophilia and other nonsense. They want to expose it not because they are good guys, but because they realize that the legitimacy of the entire political and economic system is at stake these days. If the ‘system’ decays and confidence is totally lost, everyone will lose. Watch the developments and who gets tossed into the vat next. It could get very rough. Big stakes here.

Now why was a clever hedge fund guy like Epstein heavy cash?

In his line of work one needs to be prepared to take the money and run. And avoiding extradition can be expensive.

Paulo,

Leveraged loans are hard to trade directly for individuals. Individuals are on the hook if they have money in a loan fund, or in another type fund that has some slices of this loan. Or they’re on the hook if an institutional investor, such as a pension fund of which they’re a beneficiary, has some slices of this loan. These individuals will never know what happened. Their return just went down a little, or their pension fund has a little more trouble in the future funding its liabilities.

In Canada some years ago, the charter banks were flogging ABCPs, Asset Backed Commercial Paper, directly and through their brokers, which were presented to retirees and others as Safe Investments, with Investment Grade Rating by the agencies. The whole market just froze one day in late 2007, no bid, everything went to zero, and people lost hundreds of millions. This sounds like what happened to your friend. The reason the agent couldn’t sell in time is because there was no bid.

The usual sort of financial nonsense caused the liquidity crisis: borrowing short (i.e. selling the ABCPs to clients) and lending long

(private and commercial mortgages, credit card debt along with other ‘assets’, which turned out to be mostly credit default swaps). When the holders didn’t want to roll over the ABCPs but wanted to cash out, the whole mess collapsed overnight. Everyone wanted out.

It was only through aggressive campaigning and organization that any sort of compensation schedule was achieved after managing to get the government interested.

…….

This was also the time the big 5 Canadian banks got bailed out to the tune of about 115 billion; all were underwater. Even the US Fed kicked in over 33 billion, the Bank of Canada over 40 billion, and CMHC over 60 billion. The individual numbers don’t add up to 115 billion because each amount represents a peak of their contribution.

And the legend of the Canadian Banks’ solidity carries on … , while leveraged to the hilt with inadequate loan loss provisions to cover even a normal business cycle.

‘No Canadian bank was in danger of failing, the Bank of Canada lent banks money on market terms and the Canadian Mortgage and Housing Corporation bought safe, insured mortgages from the banks, all so that the banks could continue to lend to consumers and businesses to help the economy through the recession. Important programs to be sure, but not a bailout.

And was this all a secret? Well, no. In fact, these programs were publicly announced by the government when they were introduced and included in two federal budgets voted on by Parliament. The Canadian Bankers Association issued statements welcoming these programs and they were covered extensively in the business media. So now you’re in on the “secret” too.’

From the Waterloo Record in response to an as usual alarmist bit from the leftist Canadian Center for Policy Alternatives which is endlessly recycled.

The first paragraph of the quote from the Waterloo Record is the definition of a bailout. These actions are periodically necessary.

As I said, the legend lives on … particularly in discussions about financial institutions. It’s never solvency, it’s ‘liquidity’, and the news about it is usually on page 3.

Well, here we are: in the VERY shallow end of the investor & regulator gene-pool.

This is like watching drunks douse themselves with gasoline & jump over the camp-fire to see who flames up first.

Regulators bend themselves out of shape to NOT DEFINE leverage-loan trades as securities. However, on the other hand, regulators bend themselves into shape to DEFINE crypto-currencies as securities.

1) It should be securities fraud for an LBO company to strip out more assets than the take-over-target’s free cash flow for some safe-harbor period (say 5-years)

2) It should be illegal for regulated banks (ie taxpayer backed banks) to make “cov-light” loans (if the bank really wants to make this risky loan, it must be 125% secured by target-company assets)

3) It should be illegal to securitize “cov light” loans

4) No part of the regulated financial services infrastructure (read: backed by taxpayers) should be allowed to trade these dog-turds

WARNING – CAPITALIST COMMENT TO Follow (snowflakes please go quake in a corner): I have zero problem with vulture funds aggressively recycling failed companies, but LBOs are a scam for knowledgable fund managers to pump money out of regulated (ie: taxpayer backed) banks to temporarily fluff-up returns and/or sell this garbage to investors with IQs below that of a mature carrot.

LOL, this whole comment reads like a poem. Thanks for the chuckles.

DOW might kiss 2015 peak, @ 18,351.36 from above.

If the Fed does NOT lower rates in the end of July, there will be more pressure for leveraged loans. Remember their rates are floating.

Even if the Fed lowers the RATE(s), if the business model with leveraged loan cannot produce ‘enough’ income stream to pay the interest or the funds needed to roll over to a new one. they will still sink!

There is no value here.. tell your buddy to stay away..market is under attack from Chinese and oems

Wolf,

Many thanks for covering this. Much appreciated.

One paragraph in particular stands out:

“When a highly leveraged company in an already tough business is threatened with the loss of revenues, there is no margin for error, as cash flow needed to service that debt can just dry up, and the results can be catastrophic for investors.”

That about says it all for corporate entities the world over in this post-QE world.

Cash flow is king. Once it falters, extend and pretend has reached the end.

Cov-lite is like throwing gasoline into the fire.

Your post resonates with me. My wife and I worked our last ten years for JCP, in the supply chain. We had our 401K’s loaded up with company stock when it was on the way up. One day it did not go up. I walked to the nearest computer at work and dumped all our JCP stock. It was at $82. Now it is about a buck (a Penney stock). The company’s huge debt and antiquated and inefficient supply chain are it’s problems. They lose money selling the same products as Walmart, Target, Kohl’s, Macy’s, etc.

They forgot that the goal of retail is to sell for more than what it costs. Cash is king, like you said.

Especially when key ‘facts’ are hidden from investors and or advisers!

I bet there will be more similar stories, ahead, when the tides start going down!

While the SEC regulates the bond market, the commercial paper (unsecured loans) market is unregulated.

Moody’s downgrades three notches on the news that…

‘The company’s hiring of restructuring advisors, request to meet with lenders in a few weeks, and challenges refinancing the term loan indicate a restructuring will occur soon,” Moody’s said.’

Ya I guess doing that would raise doubts alright.

Does Moody’s EVER smell smoke before the flames shoot through the roof?

Well, at least Moody’s had rated it B3 before that downgrade. That’s the lowest B-rating and is pretty deep into junk already. You have to give them credit for not having rated this thing A or even AA :-]

This is a case where Illiquid investment debt collides with market price discovery reality.

No more greater fools, to fall prey in their on going ponzi game!

I’m surprised that Wolf didn’t get deeper into the players of the Payless Shoe fiasco. Blum Capital is Richard C. Blum, husband of Senator Diane Feinstein. So much for the Democratic “People’s Representative”. Why does an 83 year old billionaire need to put thousands of common people out of a job? Why does Mitt Romney, of Bain Capital, need to help wipe out 30,000 jobs at Toys-R- Us and Babied-R-Us? These LBOs and subsequent Vampire Loans need to be made illegal. This should also show you that Big Money is the common thread in both parties. Nobody cares about the working person. Billionaires will own everything thanks to cheap money from the Feds.

Stan Sexton,

I’ve been writing about PE firms and how they operate for years, including their portfolio companies that went bankrupt, all the ones you mentioned, plus dozens more. But there is no need to stick partisan monikers on this topic because it is bipartisan or rather non-partisan.

There are thousands of these PE firms, and lots of people worked for them or ran them or were partners at them, including David Stockman (the Blackstone Group and later his own Heartland Industrial Partners) and Jerome Powell (Carlyle Group). I know people in this business. They’re everywhere. This isn’t personal. It’s a system. They’re doing what the system strongly encourages and richly rewards them to do, including the tax benefits that come with it. So I think it’s silly to stick last names to this. What’s to blame is the system.

The system can be fixed pretty easily. But the beneficiaries of the system don’t want it fixed, and so it doesn’t get fixed.

The obvious challenge is that politics is intertwined with capital markets. Fixing the system means getting rid of the swamp.

politics + capital markets is probably the simplest definition of neoliberalism.

These are not businesses. These are scams from the start.

Billionaires will own everything thanks to cheap money from the Feds.

Weaponising the financial system works. You can’t really have an efficient kleptocracy without it.

Not to worry. They’ll still let you vote them into office.

Here’s the gist. For as long as the risk dose not stay in the banks – they sold the loans off to investors and ETFs, then the Fed could care less to rescue. Only the banks are too big to fail.

That’s what securitization does. Banks Sell the risk to you, since you’re dying for higher yield.

This time around the banks aren’t the ones driving this frenzy. Remember they have been under the microscope since 09 and have been largely shut out of holding these toppy deals on their books. They will arrange them but not hold them. The driver of this is the staggering amount of risk that has been pushed into unregulated vehicles (BDCs, CLOs, debt funds backed by PE firms) where there are no rules or oversight. These terms are ridiculous, but these deals are oversubscribed because demand for any yielding paper is so high.

So when this rolls over, I think we will see that the banks come out in much better shape as they are better – capitalized.

The implosion will be in the shadow banking market. And that’s when we will see how uneducated some yield-chasing investors are regarding this asset class. People are trying to grab yield anywhere, and when you offer an entry into a leveraged loan fund for retail investors, many people see the coupon and don’t understand the risk.

As long as it’s not FDIC – insured money, the government has taken a hands off approach. Caveat emptor.

Lets do check the more. is a time to gift.

This included the absence of certain disclosure requirements.

It’s easier to make money if you don’t tell your victims, er, investors, that you’re out to cheat them. That would be unprofitable.

Nothing like BKLN. More liquid than the underlying loans in the fund. I never understood that. Anyone with a brain would stay away.

Some think the floating coupon on the underlying loans makes BKLN a nice place to be when rates rise … what a mistake.

FRONTIER bonds are exploding today.

That’s my local carrier and the office is nearby. Dying.

If you think you are a SECURED lender, then check this out:

Apparently NOT in India.

https://www.bloomberg.com/opinion/articles/2019-07-16/essar-insolvency-ruling-risks-damage-to-india-debt-market

Should affect the debt markets.

Private equity firms and LBOs should be illegal, I wonder if any country will dare yo take the first step on that? Maybe China… but probably not. The most they will do is become a billion atm octopus and insist in having a tentacle in any business in their country.

not sure what happens now. These are the first lien bonds that are collapsing. The private equity fund already extracted most of the cash from the company, so liquidation might be the next step. The assets of the company would go up for sale, and whatever cash they can get will go to the bond holders. Maybe you can get a loan to pay off the bond holders and take over their business!

These arent even the bonds, this is the senior debt. Ans these are cash flow/enterprise value loans, there arent enough assets to even get close to everyone out whole.

Likely the PE firm informs the lenders that they wont be putting more equity dollars in to support the Company. In the old days, the company would blow a covenant and give all lenders the ability to weigh their options (i.e. call the loan, exercise rights/remedies, restructure debt for equity, etc.).

With covenant light, the lenders get to sit idly by because without covenants, the Company isn’t technically in default until it misses an interest payment, at which point things are pretty dire. So by that time, the sponsor is likely gone (or has taken option value on the company because it has its initial gain out already), throws the keys and lets the waterfall take its course. The senior debt will get first dibs, the subordinated debt likely converts its debt to equity and is the proud owner of a crappy turnaround story. Meanwhile, you’ll have vulture loan-to-own funds piling into the debt on the cheap looking for that equity conversion. And you’ll have a pissing match between loan-to-own who want to preserve the business, and angry lenders who just want their money back and to go home.

It’s a fun process.

@GSW You are well-versed in this subject…guessing you did some time in Special Situations, Troubled Debt Restructuring and banking in general.

Thank You!

I would like to take this opportunity to introduce my new investment vehicle: gambling-debt-backed securities. Backed by the full faith and credit of compulsive gamblers. Moody’s rated AAA.

LOL

Wait… Just got a call from my buddy at Blackstone. Said they’re already working on it.

Hedged using card and dice futures?

Thank you wolf for the response. Great insights