After truck manufacturers eat up their backlogs, then what?

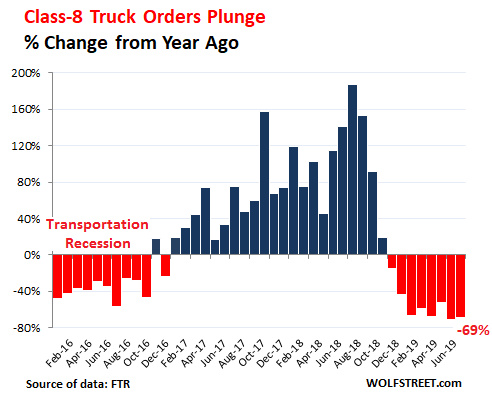

Orders for heavy trucks plunged by 69% in June compared to June last year, to 13,000 units, after having plunged by 71% in May, to just 10,400 units, FTR Transportation Intelligence reported today. It was the eighth month in a row of year-over-year declines. So far in 2019, the year-over-year declines in orders for Class-8 trucks ranged from -52% to -71%, which, as FTR said in the statement, makes it “the weakest six-month start to a year since 2010”:

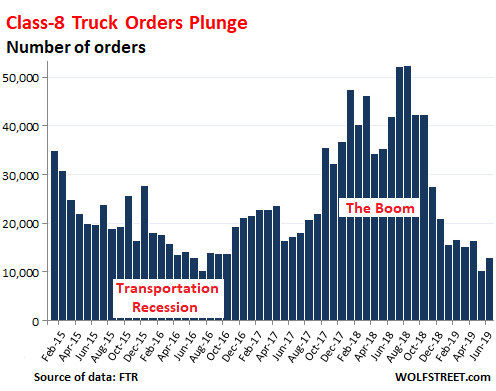

Orders for Class-8 trucks experienced a historic boom last year, reaching over 52,000 orders in both July and August, in a burst of ordering amid what was then called a “capacity panic.” But this boom is now getting unwound:

A year ago, nearing the peak in orders, FTR explained how the circularity of surging orders and subsequent delays in getting these trucks built, as factories are operating at capacity, leads to even more orders and even greater delays – the boom-and-bust cycle of the industry:

“There is an enormous demand for trucks due to burgeoning freight growth and extremely tight industry capacity. However, supply is severely constrained because OEM [Original Equipment Manufacturers] suppliers cannot provide the needed parts and components required to build more trucks fast enough. This bottleneck is causing fleets to get more orders in the backlog in hopes of getting more trucks as soon as they are available.”

Now the cycle has turned. These trucks that were ordered during the ordering panic last year to meet the capacity crunch last year are now on the road, and this increased capacity comes just as freight volume is falling, leading in practically no time from “capacity panic” to overcapacity.

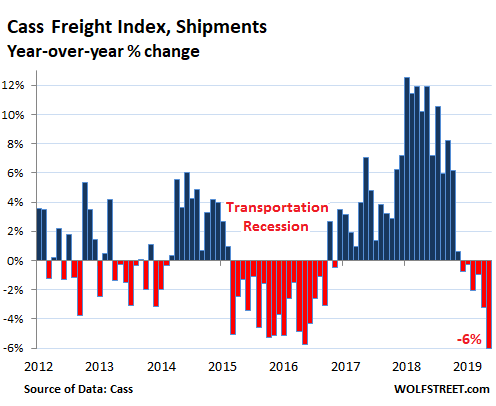

Freight volume in the US by all modes of transportation – truck, rail, barge, and air – has been declining on a year-over-year basis since December last year. According to the Cass Freight Index for Shipments, volume fell 6% in May, the sharpest decline since November 2009:

Increased capacity and declining demand are putting pressure on freight rates. The national average spot rates for hauling flatbed trailers and van trailers in June plunged about 18% from a year ago, to respectively $2.31 per mile and $1.89 per mile, according to DAT Trendlines. Contract rates, usually available only to large trucking companies with big stable clients, such as national retailers, have begun to edge down as well.

The decline in spot rates squeezes smaller trucking companies that depend on them. With fewer loads available to haul and less money per mile, it’s going to get tough for some of them, and the idea is to hang on until the cycle turns.

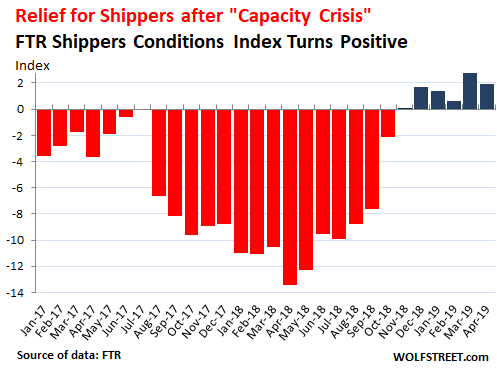

But there is always another side to it: Shippers – such as manufacturers or retailers – are breathing a sigh relief after last year’s crunch. The FTR Shippers Condition Index, which tracks shipping conditions from the shipper’s point of view, had been deeply negative until late last year. Then as capacity increased and freight volume began to back off, the SCI for November turned positive – the first positive reading since August 2016. The most recent SCI, released June 24, showed the sixth positive reading in a row:

The SCI tracks freight demand, freight rates, fleet capacity, and fuel price and combines them into an index value. A positive index value signals “good, optimistic conditions” for shippers. A value around zero represents neutral operating conditions. A negative value signals “bad, pessimistic conditions” for shippers. According to FTR, “double digit readings (both up or down) are warning signs for significant operating changes.”

The frenzy in transportation last year was caused in part by companies trying to front-run potential tariffs by ordering more merchandise. This sudden surge in orders led to all kinds of capacity problems, and it also led to the subsequent inventory pile-up in warehouses around the country that will eventually be worked off via a reduction in orders – and therefore a reduction in shipments.

The tsunami of orders for Class 8 trucks last year created a historic backlog for manufacturers – Peterbilt and Kenworth, divisions of Paccar [PCAR]; Navistar International [NAV]; Freightliner and Western Star, divisions of Daimler; and Mack Trucks and Volvo Trucks, divisions of Volvo Group. The plunge in orders since them means that these truck makers are now living off that backlog, and that the backlog is dwindling. FTR expects the backlog to fall below 200,000 units.

This is the time of the year when the model year changes, with truck makers ending production of 2019 models and opening up orders for 2020 models. But this is now fraught with its own issues, due to the uncertainties of the tariffs. In the statement today, FTR’s VP of commercial vehicles Don Ake says that one truck maker already started taking orders for 2020 models, but that the other truck makers “apparently did not.”

“Most OEMs are reluctant to quote future trucks due to uncertainty over material costs,” Ake said. “Until the tariff situation is resolved, it is risky to quote prices for 2020. Fleets are also reluctant to accept material surcharges with this much ambiguity present.”

This adds to the industry-wide cacophony from trucking companies and railroads that the threat of potential tariffs last year, and the imposition of actual tariffs, and now the uncertainty over tariffs have not only contributed to the transportation sector’s outlier-boom-year of 2018 but also to the undoing of this boom in 2019. Read… Trucking Swerves Deep into Slump, from Red-Hot Boom. Smaller Truckers Hit Hardest

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Clearly, the Fed will just have to buy all of the excess trucks, and then a few more. Otherwise, shipping costs will fall. (Of course, the Fed wasn’t concerned when shipping costs going up, because 2%.) The resulting artificial demand for trucks will generate a wealth effect among truck owners. All will be well.

Dale, I’d suggest a more ambitious solution: Department of Transportation buys any used trucks on the market at cost price, the operators get a tax amnesty on the resulting gain relative to book value on the asset disposition, and the Fed adjusts its planned treasury market actions to absorb the treasury issuance resulting from the program.

This should provide stimulus to both producers and operators, propelling economic growth, whilst simultaneously satisfying two segments in the transportation industry. It could be called the Transportation Asset Replacement Program, and being an asset swap, objections from some intransigent alarmists can be simply brushed aside as lacking in understanding of the process.

Furthermore The DoT could be tasked with appropriating adequate storage facilities at cost price for the aqcuired assets, targeting areas currently undergoing a transient period of difficulty in the property market, thereby also providing relief and stimulus to temporarily depressed areas.

I’m sure industry representatives in Washington would helpfully provide many further useful and stimulative refinements to the program over the course of a few rounds of golf and some lunches, and the appropriate, and the suitably indecipherable details can subsequently be forwarded to Members of Congress for approval, together with assurances that their respective constituencies will derive great benefits, and that indicators show that the outlook for their campaign funding appears bright.

SALTCREEP – Genius! – I would add one more layer. (Respectfully) – Human Capital Global Transients (HCGT) are overloading the border facilities at all ports of entry. The Border Patrol, and the Central Banks print a one time issuance of the “OC Bond (Occasio-Cortez). Trillions of Cortezios, are distributed into the US economy to land, settle, educate, and integrate 20% of Global population into the continental USA and the Two “other states” – Class 8 Trucks have Trailers, that can easily be refitted as Tesla, Mobile Dwelling Units. These Dwelling Units finance the repatriation of many many jobs and “stuff” from China. Funds from the unlimited wealth generated, are recycled, to repay the OC Bonds. Everyone Wins.

You are welcome America

Problem Fixed

Next?

That is good because there are way to many trucks around that kill the business ,lots of hillbilly trucks killing our rates and shippers and fricking brokers a too bad too bad.

Quota system

Another data point:

“Recently FedEx reported its international shipping revenue was down and cut its full-year earnings guidance. Its CFO blamed the economy, reported CNBC.”

https://www.forbes.com/sites/johnmauldin/2019/04/08/fedexs-report-confirms-recession-fears/amp/

Many data points – All negative.

These are FUNDAMENTALS.

US factory orders are down, the lowest reading in three years. While the service sector has declined to the lowest level since December 2017.

Jobs growth has been dismal at best. The small business sector, companies with 1-19 employees, has seen a plunge in employment, as worse as 2008. The Empire State Manufacturing Survey has suffered its worst MoM drop in the surveys history! With the number of employees and hours worked leading the way.

Restaurant Performance Indices are negative. Retailer earnings are down. The farming sector is an absolute disaster for this crop season, due to abnormal weather. Agriculture employs 24 million workers, many of whom have been laid off.

Add these fundamentals to the gloomy global freight flows, along with all the other negative economic fundamentals, and you have a word that is spelled R-E-C-E-S-S-I-O-N

Could this be filed under the “broken window theory”?

You had best get your ‘Old Crow’ before the price goes ballistic.

Big fire at Jim Beam destroys 40,000 barrels of whisky.

The horror!

Changes in trade affect transport. Roubini said the trade war might cause a recession. Since Roubini is usually pessimistic, this alone is not cause for panic. People will be watching the jobs numbers. An aging US population and a decline in work force participation percentages is a source of worry. Boomers are retiring.

Actually, it is not. it opens opportunities for less senior members of staff to replace them. Also, we are constantly being told that Robots are going to take our jobs..not.! So where is the worry?

Robots are not going to take our jobs. Hmmmmm

https://www.delawareonline.com/story/life/food/2019/07/01/sci-fi-meets-seafood-new-newark-robot-restaurant/1573695001/

Robots are used Clyde, Ohio at Whirlpool. Decent amount of people on layoff from robots. Also Jeep in Toledo was using robots pull parts on top hats to the line. Yes still need human to physically load. But can easily switch robot to loading.

Proles in our oligarch-looted economy are tightening their belts and cutting back consumption. This belies the “greatest economy ever!” meme pushed by the White House, or the “Everything is Awesome – Buy Moar Stawks” cheerleading from the corporate media.

Given the epic boom over the last couple of years, the present decline seems almost like an equal and opposite reaction. Your chart of the Case Freight Index over the last eight years seems to say it all. What goes up…

Greatest. Economy. Never.

We all know there is a recession coming. The questions are, what will be its nature, timing, depth, and duration. This is where the economic divide is really important. The investor class and those with a toe-hold in it are obsessed with timing: they want to know when to go liquid. They also care about the nature of the recession: in what asset class does it erupt from. That’s about 15% of the population. The rest, well, they have no stake in that game. They have no assets, other than perhaps a house with a fat mortgage and maybe a paltry 401k account (although over 1/3rd of Americans don’t have that). Those people care about the severity and duration of recessions, not its timing and nature. Problem is, the people who write about recessions and report on it in the media are all solidly in the 15%, so their focus is skewed by their position in the pecking order.

I could be wrong, but I swore I read somewhere that some of the truck orders were to beat EPA mandates on newer and therefore more expensive models that caused a spike in orders. So the industry jumped on board to save a few bucks knowing they’d be ahead of needed purchases for the coming year or so.

Glenn McClendon,

I don’t think there was anything like a new and major EPA mandate like this happening in 2018 and 2019 on a national level (there is some California CARB stuff going on though). However, Electronic Logging Device (ELD) requirements began getting phased in in 2016 and are still being phased in. But this device doesn’t require a new truck. The device tracks how long a driver drives. It is designed to enforce rules that limit how many hours drivers can drive. This phase-in caused some issues and added to the capacity constraint in 2018, at least until trucking companies worked out the kinks.

As the owner of a trucking company here in Los Angeles I can definitely see it slowing down and the rates are somewhat lower from last year. Some companies or owner operators are still having to replace trucks with newer trucks here in Calif due to Calif Air Resources Board aka CARB rules.

This is the time for us to have cash in the bank and no payments on equipment as it looks like its going to slow down even more. Our biggest expense or problem is land and having a terminal here in LA, very expensive and I am competing with carriers based in AZ or TX who pay much less.

MSM/blogs: We’re in a recession!!!

Stock market: Nah bruh.

Yes, plus: Treasury market: We’re in a depression :-]

That’s a good one! ;-))

Assuming this transportation recession will be worse than the last and worst since 08 where is the economy heading? 16 was a mini recession, perhaps a stealth market crash, except for global liquidity. Two assumptions to be challenged, the sea of money will continue to levitate economies, and there is a firewall between mainstreet (consumer led recession) and wall street. Business needs to make long term plans and tariff by whim is causing whiplash. Fed will find that closely manipulating interest rates using data in real time will acerbate the swings in volatility. They are right to go back to core PCE but the lapse in confidence in their policy (or the markets ability to control Fed, which is not a bad thing). I mean suppose the Fed didn’t pay attention to markets at all?

FYI?

“U.S. trucking costs are up 25% vs. the previous year,” Procter and Gamble spokeswoman Jennifer Corso said. “A key driver of this has been increased demand for trucking and a driver shortage. These increased costs obviously put pressure on margins, hence our continued focus on productivity throughout the company to help offset these costs, as well as rising commodity costs.”

The problem is basic supply and demand. Trucking in particular has been squeezed for years between an aging workforce of drivers and increased tonnage demands.

Kevin Burch, president of Dayton trucking company Jet Express and American Trucking Associations’ past chairman, called the situation a “perfect storm.”

“This bottleneck is causing fleets to get more orders in the backlog in hopes of getting more trucks as soon as they are available.” That sounds like a terrible way to run a business: they must know this guarantees they will get too many trucks in the end. Or am I missing something?

Cash for Trunk Clunkers…anything older than 3 years old.

I do lots of time series analysis, including economic. The first thing I do when I see very cyclic data, like the chart going back to 2012 is to take the integral to see the cumulative increases. If the cumulative increases after 7 years is positive, and a reasonable number, then the overall economics of that system are good, and you have to learn how to live out the swings by using credit/debt in your favor (buy low, sell high). If it is such a regular pattern as this chart has, it is pretty easy to execute that. The problem is that most in this industry don’t have the resources to play that game, so they get into trouble in the down cycle, and go too crazy on the up cycle.