Not a rate-cut economy.

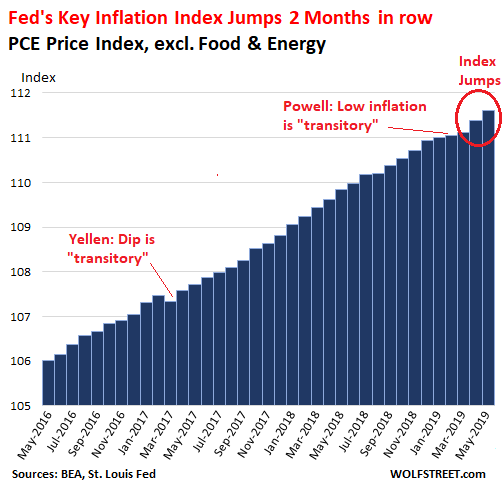

The inflation index that the Fed has anointed to be the yardstick for its inflation target – the PCE price index without the volatile food and energy components – rose 0.19% in May from April, according to the Bureau of Economic Analysis this morning. This increase in “core PCE” was near the top of the range since 2010. It followed the 0.25% jump in April, which had been the third largest increase since 2010:

Fed Chair Jerome Powell, at the press conference following the no-rate-hike FOMC meeting last week, gave a clear and succinct summary of the US economy. It was mostly in good shape, he said, in particular where it mattered the most: “All of the underlying fundamentals for the consumer-spending part of the economy, which is 70% of the economy, are quite solid,” he said.

He acknowledged that there were some problems, including the slowdown in manufacturing and the current bust in the vast US oil-and-gas sector, and that the Fed would be watching for further deterioration in the economy, before it would take action. But “low” inflation was another matter.

Sustained “low” consumer-price inflation – as the Fed defines it – worries the Fed, though it’s a godsent for consumers. If inflation, as measured by the core PCE price index, drops in a sustained manner below the Fed’s pain threshold, wherever that may be, the Fed would likely adjust monetary policy no matter what the economy does.

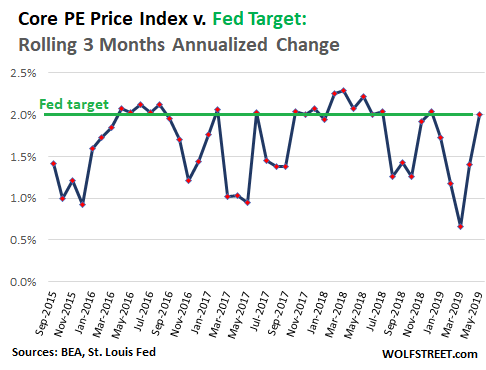

The Fed’s “symmetric” target is a 2% annual increase in the core PCE index, meaning the increase can fluctuate some above or below the target without causing the Fed to act.

Core PCE inflation was in the 2%-range for much of last year. But early this year, the increases softened. So in his opening remarks at the press conference, Powell said that “committee participants expressed concerns about the pace of inflation’s return to 2 percent.”

So that everyone understood, he added: “We are firmly committed to our symmetric 2 percent inflation objective, and we are well aware that inflation weakness that persists even in a healthy economy could precipitate a difficult-to-arrest downward drift in longer-run inflation expectations.”

In other words, a trigger for a rate cut would be a “sustained” period significantly below the 2% target. Inflation data is volatile and jumps up and down. Earlier this year, when core PCE inflation fell significantly below 2%, Powell said that the factors behind this low inflation were “transitory.”

Janet Yellen, when she was still Fed Chair, also used “transitory” to describe the factors that in early and mid-2017 were causing an actual dip in core PCE – which hasn’t happened this year. And a few months later, she was proven right.

After today’s data on the increase in the core PCE index, following the jump in April, the three-month increase – March, April, and May – has now hit 0.50%. Annualized, this amounts to 2.0% core PCE inflation over the past three months, in the bull’s eye of the Fed’s symmetrical target, with the last two months being substantially above the Fed’s target. But note the sharp decline in January, February, and March, and how it has now reversed:

This data is volatile, and is likely to move in either direction. But the “low inflation” scare early this year seems to have dissipated. And this gives the Fed one more reason to be “patient” and observe developments as they unfold before making a move with monetary policy at its meeting at the end of July.

What we’re watching here are the “cyclical” dynamics of inflation, which move on a monthly and yearly basis.

But there are also “structural” factors why inflation has been “low,” by central-bank definitions, for years. Powell mentioned this in the press conference. These factors, in place for over two decades, have to do with the internet, globalization, the search for cheap labor, efficiencies in manufacturing and transportation, and the like.

These factors have led to a sharp split in inflation: Services such as healthcare, rent, and financial services have experienced red-hot inflation; and consumer goods have experienced ice-cold inflation. Here is the data, and what my couch, jeans, car, PC, sheets, and phone are saying about globalization and the internet, and how they impact prices. Read… My Perspective on the Murk of Official Retail-Sales Inflation, with Some Surprising Illustrations

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Ha, core CPE inflation data. Does it reflect reality anymore? Making decisions based on that looks silly.

Are there better metrics available (proprietary or otherwise)?

I would also question why the target needs to be 2%. Why not 1% or 3%?

GP,

Core PCE is the Fed’s yardstick with which it measures inflation against its own target for inflation. What you and I think real inflation might actually be is totally irrelevant here. This is not about some kind of real inflation but about the Fed and the July meeting, and the data the Fed looks as it makes its decision.

If Powell doesn’t cut the interest rate in July by min 25% (an he will, probably by 50%) Trump will fire him. Mark my words.

Words marked. Markets didn’t stop him from raising them before, they won’t force him to cut them now.

Memento mori,

Yes, good chance Trump might try to fire him or demote him.

Kashkari, ridiculously failed and utterly incompetent gubernatorial candidate in California before he parleyed that run into a job at the Fed, is brown-nosing up to Trump with talk of 50 basis-point cuts. He is trying to get Powell’s job. So now we have elements of a palace intrigue.

This Fed is fixing to decide whether it’s going to be stooges of the White House once and for all, or “independent.” There is more at stake than just Powell’s job.

If I remember correctly the procedure for removing a Federal Reserve chairman, failing a blatant act of treason or another serious crime, is very complex and revolves around multiple hearings in front of both houses where Powell can simply point at his mandate and at data and say he’s following said mandate to the letter. Trump knows this as well. He’s just being the showman he’s always been.

Mr Kashgari deserves special mention here.

Elvis Presley famously said “Ambition is a dream with a V8 engine”. It worked for the King.

In Kashgari’s case giving him a V8 engine would at best result in an expensive car being written off and at worst in a horrific pileup on the highway. Better take the keys away from him and buy him a bus ticket.

Powell already said flat out in a 60 minutes interview that Trump cannot fire him and that he intends to serve out his full term, so, I have no idea why you are still floating this idea. All.the MSM outlets totally shut up about this possibility after that interview.

Based on this interview, here’s the scenario if Trump does try to fire Powell. First he won’t do it himself, he’ll tell one of his hatchet men, probably (cough, cough) acting chief of staff Mulvaney to make the phone call:

Mulvaney to Powell: President Trump has decided to fire you

Powell: He can’t fire me. I’m not leaving

Mulvaney: He’s the President, and he just fired you

Powell: the President has no authority to arbitrarily remove a Fed chief, and I am not leaving

Mulvaney (crying): I can’t tell him that! He’ll fire ME!

Powell: Good, now go away, I have work to do

The 60 minutes interview is available online and on the CBS News apps for all the phone, Firestick, and Roku platforms

Time destroys the speculation of men, but it confirms nature.

– Cicero

A US President has NO AUTHORITY WHATSOEVER to fire any member of the 7 member Federal Reserve Board Of Governors of which the Chairman of the Federal Reserve is and must be one of the 7 members. The Federal Reserve policy decisions are NEVER made by unilateral decision of whim by the Chairman but rather are ALWAYS made by the 12 member FOMC (Federal Open Market Committee) which is comprised of the 7 members of the Board Of Governors plus 5 of the 12 Regional Federal Reserve Bank Presidents.

Right, then, bet on Kashkari becoming Fed chair. Keep in mind the glorious leader hired that Kudlow guy from off of the radio.

With 100 percent certainty. A priori is Trump getting re-elected everything else is secondary no matter what it is.

There are better metrics available. Core PCE uses a ridiculously distorted basket of goods compared to what the average American actually spends money on, and notably ignores the effects of fraud on healthcare costs, which have skyrocketed. It also weights housing at half of what CPI does, which is material for anyone who is spending a disproportionate amount of their income on rent or a mortgage.

Before there was an inflation target, the consensus amongst academics was that it should be 1.5%. Only Frederic Mishkin seemed to think that 2% made sense. Mishkin co-authored a paper on the topic with Ben Bernanke in 1997 positing inflation targeting as a hypothetical. Somehow, once Bernanke actually implemented it, 2% became the norm. It’s a nice round number. There’s no external evidence to suggest that it makes any sense at all.

It could be argued that the entire empirical basis for the Fed’s policy is the arbitrary whims of academics who look at bad data on a regular basis and treat it as gospel. But that’s probably being too generous.

“…bad data on a regular basis and treat it as gospel.”

All the gospels I know are based on data that only make sense in mythical kingdoms. The Fed’s gospel could very well be one of them.

What are the better metrics you speak of?

Just came from the plumbing shop – there was a notice at the cash of price increases from a range of suppliers.

They were all ‘4% – 5%’

Time frame was not indicated.

I recently bought a Purtech water softening system. I hesitated for a month before moving ahead. In that time the price went up 2%.

So the above increases can NOT be assumed to be annual.

Inflation recently jumped. Looks like Staples jacking up prices with smaller packages! Fool your eyes!

Nailed it. One has to wonder if they actually there to insure the slow orderly decline of the dollars value into the waste bin of history.

Just a reminder that the US has been known to do nicely with inflation far below 2 %.

1960 1.7 1.7 1.7 1.7 1.7 1.4 1.4 1.0 1.4 1.4 1.4 1.7

1961 1.7 1.4 1.4 1.0 1.0 0.7 1.4 1.0 1.4 0.7 0.7 0.7 1.0

1962 0.7 1.0 1.0 1.3 1.3 1.3 1.0 1.3 1.3 1.3 1.3 1.3 1.0

1963 1.3 1.0 1.3 1.0 1.0 1.3 1.3 1.3 1.0 1.3 1.3 1.6 1.3

1964 1.6 1.6 1.3 1.3 1.3 1.3 1.3 1.0 1.3 1.0 1.3 1.0 1.3

1965 1.0 1.0 1.3 1.6 1.6 1.9 1.6 1.9 1.6 1.9 1.6 1.9 1.6

These are the annual inflation rates by months with the average at the last place. The average for 1960 was dropped when I pasted.

If one of the Fed’s “mandates” is “price stability”, why isn’t the target 0.0%. Annualized inflation of 2.0% is ~ 22% (compounded) in a decade, and over 200% in a century. How is that price stability?

The Fed has debased the dollar to such an extent that a 1913 dollar, when the Fed was founded, is now worth ~ $0.03. Again, how is this “price stability”?

The Fed’s legal mandate is “zero per centum”. They simply choose to ignore this US law.

Yes, the way the Fed — and the other central banks — get around the meaning of “price stability” is by calling its mandate “price stability of 2% inflation.” Problem solved.

“The Fed has debased the dollar to such an extent that a 1913 dollar, when the Fed was founded, is now worth ~ $0.03.”

Dont you have that inverted?

Should it not read ” the $ has been so debased that today’s $, is worth around $0.03 1913 $’s.” ?

Do you even read what you write? Inflation up to 2.00 from 1.90? Like that’s important? Or even real? Woooooowww! These figures are 100% fake fraud propaganda. Asset inflation is far higher and that where the money is going. Inflation is not anywhere near 2.00 it’s much much higher.

@timbers, Your and my perception of inflation is irrelevant in relation to this article which is about the Fed’s perception of inflation. The Fed could give a rat’s ass about any of our perceptions. The are looking at the whole economy and trying to keep their strings untangled as they do their marionette manipulations. Yes, it will all blow up in their faces one of these days but not tomorrow or before their next meeting.

timbers,

This article wasn’t about what you imagine inflation might be. It was about the Fed, and what the Fed is looking at, and if the Fed might use inflation as a reason to cut rates. If you want to understand what the Fed might do, you need to look at what the Fed looks at. Core PCE is the Fed’s yardstick to see whether or not it reached its target of 2% inflation.

41 days without junk bond issuance is driving this fiat wagon. Jerome blinked. Historically the fed has had 5.5% of head room for a recession and the mandate is whatever the fed needs to do for the reserve banks,to hell with us ants.

If all inflation is monetary there is no policy, other than to wait and see how much money washes up on the shore, from distant lands where central banks have control over monetary policy. While they are at it Fed should predict the annual rainfall, since global monetary stimulus and climate change are handmaidens of global policy. If Trump did try to fire Powell Congress would take up the issue. They have more control over Fed than Prez.

Kind of reminds me of the famous line in the “Godfather” when a “capo” (who ended up testifying before Congress denying he was involved in any nefarious activity whilst his brother from Italy was being held “hostage” by the Godfather in the hearing room):

“Io non mangia in Las Vegas” Trans: “I don’t ‘eat’ (profit from) in Las Vegas”.

Today:

“Io non mangia a la tavola de Reserva Federala!”

Trans: “I (as an ordinary consumer) don’t eat at the table of the Federal Reserve!”

So their “inflation” is irrelevant to my life except in extremis.

Wolf, do you actually believe what you just wrote??!!

The Fed says all kinds of things that they know are not true.

First, they want and know that inflation is much higher than the “advertised rate”. This is because we have so much debt in the system and the only way to deal with that is through heavy inflation. Who benefits from all this high inflation? Why of course the US government does. The average smuck, not so much. The inflation that is ongoing is a race between our national supremacy in the world against the little guy in the US being decimated. The Fed is simply in the middle trying to keep it all together.

Mike Are,

Seems to didn’t read my comment. You’re replying to something else and about something else.

The individuals that are negatively impacted the most by inflation are those who rely on fixed incomes. Powell and the FOMC know this quite well. We have one of the largest retired populations on record and this is to going to increase in the near future.

You’re not seeing any inflation if you hold your savings in bitcoin or gold. The U.S, dollar is a junk currency. Just don’t hold any dollars and you have nothing to worry about. Only exchange enough of your gold or bitcoin, or other money that can’t be debased, as you need to meet your immediate needs. The Fed said they wish to destroy the value of their own product, that would be like Ford telling you to drive your car as much as possible because they designed it to fall apart after 2 years. They have designed their currency to fall apart. Dollar going to zero, this nonsense is going to get out of control and it will happen quicker than Powell thinks, That’s how hyperinflation events occur.

Van_down_by_river: We are both pretty much in the same boat.

Yes ,my gold mining stocks have rallied very modestly after being dead for nearly 10 years. After all gold has rallied less than 10% so far.

One worry is that my gold mining stocks will soon die again when the market realizes that Powell won’t be cutting interest rates in July or anytime soon like Wolf says.

Unfortunately I am now being forced to slowly but surely liquidate my gold stocks at rock bottom prices.

My biggest worry is I will have sold everything before gold really rallies.

Watch out for the next Bre-X. There still are gold mining scams running around BC

The USD is but one asset in a world of assets. Indeed, the dollar is performing brilliantly…. In some places, mainly emerging and developing markets. You need to get out of the van, it’s a big world out there.

Don’t know about gold but bitcoin, yes. It’s a lot more convenient that gold, and secure. I’ve been hodling [sic] since 2014. Last bought some in 2015 and took the wallet offline then. Am now looking into running two wallets, one offline (air gapped) and the other a watch only wallet (which has online access). Using these two makes a very secure system. Takes a bit of time for it all to sink into my old head but it eventually does. As I keep saying, the revolution will not be centralised. The sovereign individual is on the rise.

With the disastrous situation in the farm belt I’m just really glad that core PCE doesnt include food so inflation will stay low.

Maybe the upside will be a shortage of high fructose corn syrup and Americans will lose weight. That will decrease morbidity and mortality due to obesity-related diseases and lower health care costs, reducing the amount GDP devoted to health care spending.

Every cloud has a silver lining.?

Farmers welcome higher prices. Not all of them got flooded. Ag commodity prices have been hit very hard in recent years, and there has been a wave of farm bankruptcies due to low ag commodity prices. Corn is now barely above $4 a bushel. Overproduction in the ag belt has been the rule. So don’t expect food prices to jump.

I used to grow corn on my farm

We were thrilled at3.5 a bushel in the mid 90’s. My question is farmers still a that price level but a box of cornflakes has doubled and the

box has shrunk by at least 30%

Who is making the hay?

This has driven farmers mad for decades. The commodities stay very similar in prices with a few spikes and troughs, but the finished product gets to enjoy steady price inflation for the costs of processing, packaging, freight, etc. The farmer and the consumer aren’t enjoying the ride as much as everyone in the middle.

Read a comment from a farmer in the flooded region around Iowa, that most of his neighbors who were underwater were growing GMO crops, which are used for livestock feed. He held the line on growing this stuff, and came out okay, ie had a market for what he had grown. Wonder if the boutique approach to ag has put more farmers at risk, and do American consumers really understand what is happening?

– In 2007 & the first half 2008 inflation kept rising. But short term rates kept falling and the FED kept cutting rates as well. That’s why I still expect the FED to cut rates.

anything above 0% is debt monetization. that’s what this is all about.

What rate cut? Who needs to make it “OFFICIAL” when the yields of Treasuries have already dropped.

Year-to-year, the High Rate for June has already fallen almost 1%:

2Y: -0.843%

3Y: -0.803%

5Y: -0.928%

7Y: -0.92%

10Y:-0.832%

For T bills, the High Rate in the last 6 months have also fallen at least 25 basis points to more than half a percent:

4 wk: -0.255%

13 wk: -0.37%

26 wk: -0.475%

52 wk: -0.56%

This comparison is not even Peak-to-trough.

As a treasury investor, I definitely know I am getting a lot less yield.

The FED does not have to change the Fed Funds Rate to lower rates.

As I have noted many times before, all they have to do is do a lot of SOMA re-investments (rollovers). That’s the real hidden QE.

And the Primary Dealers, they are playing a “dangerous” game. Their treasury inventory is pregnant today. Probably they bid high so the yield goes down. Take about rigging. LIBOR rigging was caught. How about Treasury rigging?

Inflation worry, the Fed? I’d be surprised if the market doesn’t get their quarter point cut in July. They really want a half point, and will freak if they get nothing. Personally, I think this market owns Powell and the Fed. But Powell and co are essentially nervous nelly bureaucrats at heart, fussing over their models, bed wetting at a .001 move this way or that, hanging their heads at any critical headlines of their performance, or hiding in the rules to justify failure. They will never move too fast, not in their nature. They still haven’t turned off quantitative tightening? No faith in these guys to do the “right thing”, that is get off this easy money merry-go-round. That December panic was one for the history books, what a cave. They say Powell is a nice guy, but we need a tough guy….please come back Paul Volker….

The fed is going to be shocked when higher rates crate higher inflation (when their textbook says it should lower it).

Companies have been subsidizing low prices to consumers by taking out near-0% loans and then passing the savings to customers. But when those loans start rising the company has to stop taking out the loans and raise prices instead AND ALSO raise prices some more to pay back the loans they already took out.

For example, a Netflix subscription today is 40% more expensive than 4 years ago – now THAT is inflation.

And this is happening everywhere in the economy. Uber loses money on every ride and makes up the difference by taking out a cheap loan. Those prices are going up 40% too once they can’t get a 0% loan from Daddy Fed.

Mark my words the 2% inflation today will jump to 3% next year then shock everyone by being 5% in two years. There’s going to be a financial crisis when the fed has to spike rates which will obliterate all the money people hold in bonds and real estate.

This is the biggest asset bubble in history, so big that the bubble itself created low inflation. But the end is coming.

Higher rates won’t lead to higher inflation because the higher rates will reduce demand and consumption and borrowing. People have tried making that argument forever (higher rates = higher costs = higher inflation) and it just never happens that way.

Just got a notice in one of my utility bills. The tax cut act has created a surplus for them and they are refunding us ~$10 next month and $1+ for the next 24 months. Oh, and by the way we just requested an increase of ~$0.80 a month.

So the decrease is about to be clawed back. They give no particular reason for the increase requested. So it must be because they can and we obviously don’t need money we were spending anyway. This is how America works in a nutshell.

The Trump associates and hires that have obsequiously done his bidding (Manafort, Spicer, probably Barr,…) have not fared well and have more-than-tarnished reputations. Those that have stood up to his capricious demands and unsound policies (Sessions, Tillerson, Kelly, Mattis,…) have preserved some of their integrity. Based on Powell’s history (Jesuit education, investment in sustainable energy, work to regulate “too-big-to-fail” banks,…), I suspect he’d rather belong to the latter group. But no one knows for certainty what will happen at the July meeting. And predicting Trump’s reaction–given his reckless behavior thus far in office–is foolhardy. Finally, there is considerable debate over whether Trump can demote or fire Powell. An independent Fed (and, yes, it has been largely independent) is essential to preserving the dollar’s value and security. Do the powers that be really want to give that up?

Interestingly, Trump could have retained Yellen and didn’t. Her Fed increased rates only 1 time, from 0% to 25bps. For 7 years rates were ~ZERO …which silently transferred literally trillions of dollars from small savers to folks with the big money. And then rates are raised like 8 or 9 times in 2 years (and QE reverses) so Trump is screaming because rate hikes are economic brakes after 7 years of Fed pedal to the metal.

So what Trump thinks of the Fed is meaningless, though he is competitive enough to put up a fight. But, he is a temporary nuisance to them and they are over 100 years in power. Very few even know enough about what the Fed does to have an opinion. He can scream, while they whisper and carry a very big stick. For example, after he settles in and tries to put his selections on the Fed, all are summarily shot without a final meal or even a cigarette. The opposition came quickly from key people in BOTH parties.

Now when both parties unite on something, that is worth the effort to try to understand why.

He should be getting rid of the Bear Stearn guys, Kudlow and Malpass. Those two are his real problem.

Getting rid of Powell is a waste of time because the fed has become irrelevant in our broken markets.

Would anyone else like to see the Fed stop trying to cause inflation? How is it even legal that the Fed’s mandate of “stable prices,” to them, means 2% inflation? Webster says stable means “fixed,” “not changing.” A 2% inflation rate means prices double every 35 years. In about an average person’s lifetime, prices will quadruple.

Wolf, great article but you are making the mistake that the FED is in control of interest rate policy.

The market controls all interest rates (even indirectly the over-night rate), and the FED must respond to it, otherwise it risks losing control of monetary policy. As. you’ve noted, the market can ease credit conditions itself without direct cuts, but the FED must ultimately deliver on the markets demands.

The yield curve has inverted and the market has priced in several rate cuts. The FED must respond with rate cuts, otherwise it’s ability to counter future weakness will be undermined.. There is NO ambiguity here about whether the FED will cut, which is why Mr. Market is going into its rally mode (I think it’s nuts too).

The FED doing anything else but cutting would cause a credit crisis and undermine the system. This is not the 1970’s and Powell is not Paul Volker. He is an enabler of asset bubbles like his predecessors. The reflation trade is going full steam this summer.

While it may do a quarter point in July, followed by a quarter point in Aug I think it’s 100% (not 99%), that by the end of summer the 0.50 % rate will be cut done.

Miner,

“…you are making the mistake that the FED is in control of interest rate policy.”

I know exactly what the Fed “controls“: IOER (2.35%), primary credit rate (3.0%); and overnight reverse repos rate (offering rate 2.25%); and what it has pretty good control over (federal funds rate); and what it is trying to manipulate with its verbiage, “forward guidance,” and other tools (the vast rest of the credit market).

Here is the short form: The Fed tries to manipulate the credit markets with its tools. But manipulating is not “controlling.” It only controls a tiny sliver of the credit market (as outlined above).

Look at this for example — and please read the whole thing and not just the headline, and make sure you understand what I say about the “transmission channels”:

https://wolfstreet.com/2019/06/27/the-feds-stealth-stimulus-has-arrived/

And you’re wrong with this: “The FED must respond with rate cuts, otherwise it’s ability to counter future weakness will be undermined.” The market has been nearly always wrong about what the Fed will do until the date of Fed action gets pretty close, and then the market adjusts (mostly). When the market doesn’t adjust beforehand, it adjusts afterwards.

Don’t believe me? Look at the chart that shows market expectations (federal funds futures) and what the Fed actually ended up doing. The chart goes back to 2001. And markets were almost always wrong about the Fed:

https://wolfstreet.com/2019/06/11/the-market-is-almost-always-wrong-about-what-the-fed-will-do-chart/

Re: primary credit rate (3.0%); I think this is called the discount rate. There’s a stigma from using that.

yes :-]

Trump fired the director of the FBI, the deputy director of the FBI, the attorney general, the assistant attorney general and numerous White House staff. He tried to have Mueller fired. No doubt he was looking for a way to fire Powell. Trump is a fat autocrat. Constitutional law might not decide in his favor.

We are in a period of modest inflation – 1.8% annual CPI inflation.

Interesting history here:

The first hundred years of the Consumer Price Index: a methodological and political history

Although the public’s demand that the federal government address social and labor unrest caused by drastically higher prices in the late 19th century seemed to solidify the prominence of the Bureau’s nascent retail price index as a national economic statistic, countervailing economic conditions in the early 20th century, as well as political decisions by the Roosevelt administration, made the future of the Bureau’s pricing program anything but secure.

https://www.bls.gov/opub/mlr/2014/article/the-first-hundred-years-of-the-consumer-price-index.htm

Also See: A related (inflation) measure is a retail price index, which measures prices of goods sold at retail outlets. In Hong Kong,

CPI and Retail Price index are highly correlated (Leung, Chow And Chan, 2009, Chart 4

I don’ understand. If powerful forces such as internet, global labor supply, technology, etc. are causing deflation, what is causing inflation to approach 2%?

There must be big inflationary pressures related to debts that are rising faster than GDP. Is this healthy for the economy in the long run? It must be if the Federal Reserve is encouraging it. //sarc.

Bobber,

There is a lot of inflation in services (healthcare, financial, rent, etc.); Non-durable goods (food, etc.) are seeing some inflation too. But many prices of durable goods (furniture, electronics, etc.) have fallen over the decades (deflation).

So the internet and globalization impact mostly goods. Services don’t face much of that type of competition. And so prices keep rising.

In terms of debts and inflation, we have to separate:

1. Consumers with debts are helped only by wage inflation; but consumer price inflation makes it harder for them.

2. Businesses with debts are helped by consumer price inflation (they can raise their prices and increase revenues) but are hurt by input inflation and wage inflation.

Wolf: You and Fleckenstein have the best readers I know of. However, today seems to be an off day, as no one is actually discussing the topic you raised, which is basically, “What will the Fed do?” If our views on inflation do matter, and if it’s actually higher than how the Fed measures it, which all of us here probably think it is, one assumes that at some point, it will show up in their measures too, despite the fact that Fed-measured inflation is designed to exclude the things that are inflating most (which are basically things we have to have). I don’t see any likelihood that the Fed will see dramatically higher inflation soon, though they may down the road. So could they do an “insurance” cut? That is now Stockman’s view, and he’s been around the block a time or two. Basically, Trump is telling them to do a cut, so they are trying to make him happy. It will certainly be a shock to everyone if the market returns to driving rates at some point…..

The FED will do what it always does.

Sit on its hands until the long-term DATA, or a sudden crisis, tell it what to do.

The FED tries to be proactive, but in reality it is a reactive entity, just like most of the legal system.

Higher inflation and lower interest rates just mean they can wipe out the entire middle class a lot faster. This has to be one of the reasons for these rates cuts in the future. With rate cuts the middle class loses even more to the inflation rate each and every year. Negative interest rates squared or to the power of 2.

Morning…. Good discussion and article. Re Trump and his team… All of the worry re inflation pales in comparison to people not knowing what they don’t know…. Ref to “The Fifth Risk” by Michael Lewis..

I think it’s well past the point that most layfolk trust that the FED’s stated target inflation metric is the actual threshold or catalyst for FED funds rate policy. It apparent how the FED chairman’s assumed position (dovish v hawkish) is sufficient to affect desired rate adjustment . Taking on such a position leading up to the FOMC is a brilliant and effective way for the FED to set policy without any real commitment. This strategy of merely adopting a position allows the FED to avoid blame should a policy mishap occur, but take credit for market gains and this without actually doing anything to materially support this position at FOMC and Jay Powell can call for patience as long as he adopts a strongly dovish tone.