Then there’s the sinkhole of $1.5 trillion in MBS and $617 billion in Treasuries that mature in over 10 years.

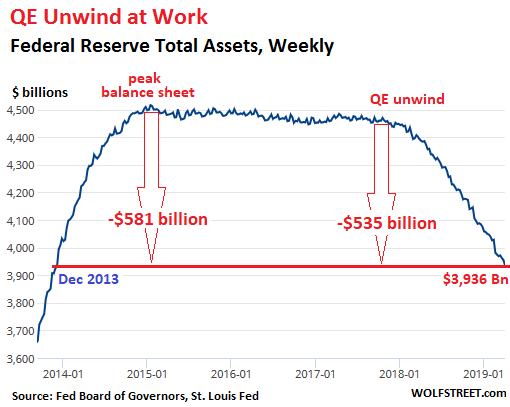

In March, the Fed shed $34 billion in assets, according to the Fed’s balance sheet for the week ended April 3, released this afternoon. This reduced the assets on its balance sheet to $3,936 billion, the lowest since December 2013. Since the beginning of the “balance sheet normalization” process, the Fed has shed $535 billion. Since peak-balance sheet in January 2015, it has shed $581 billion:

Last month, the Fed outlined its new plan for its balance sheet. The autopilot of the balance sheet runoff will be tweaked starting in May. A totally new regime will start in October. There are all kinds of changes in this new plan, primarily, that the runoff of Treasury securities will stop at the end of the September, and that the Fed wants to entirely get rid of its mortgage-backed securities (MBS), including by selling them outright, to replace them with shorter-dated Treasury securities. This strategy will finally begin to address a massive maturity-sinkhole that the Fed has carved out for itself and slipped into ever deeper. More on that in a moment.

According to the Fed’s old plan, which is still in effect, the QE-unwind autopilot is set on shedding “up to” $30 billion in Treasuries and “up to” $20 billion in MBS a month for a total of “up to” $50 billion a month, depending on the amounts of bonds that mature that month.

Treasury Securities

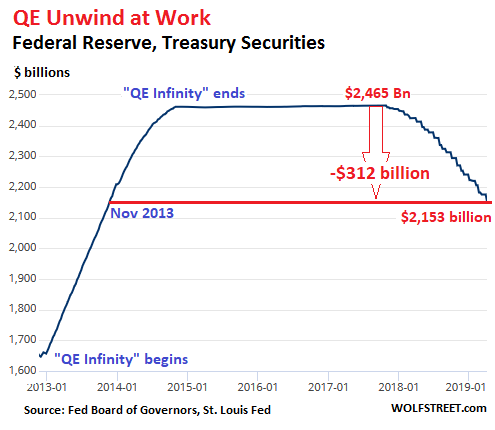

The Fed doesn’t sell its Treasury securities outright but allows them to “roll off” without replacement when they mature. Treasuries mature at mid-month or at the end of the month.

On March 15, no Treasuries in the Fed’s portfolio matured. On March 31, three issues of Treasuries matured, totaling $22 billion. This was below the $30 billion “cap,” and the Fed allowed all $22 billion to roll off without replacement. This brought its Treasury holdings down to $2,153 billion, the lowest since November 2013:

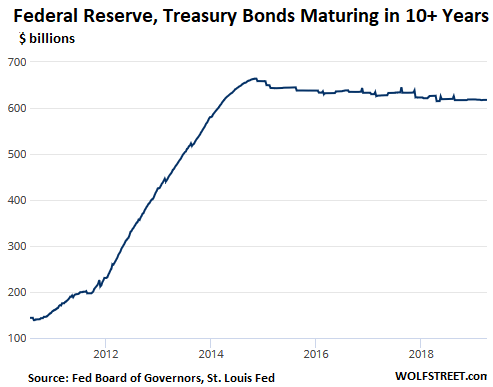

Of those $2,153 billion in Treasury securities, $617 billion are bonds maturing in over 10 years! This amount has not moved at all since August last year, though over the same time period, the balance of total Treasury securities has dropped by $183 billion. In other words, the average maturity has risen further. And as we will see in a moment, this is a much bigger issue with MBS.

Mortgage-Backed Securities (MBS)

As part of QE, the Fed also acquired residential MBS that were issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. All holders of MBS receive pass-through principal payments as the underlying mortgages are paid down or are paid off, such as when mortgages are refinanced. The remaining principal is paid off at maturity.

These pass-through principal payments cause the balance of MBS in the Fed’s portfolio to decline in an unpredictable manner. To keep the balance steady after QE had ended, the New York Fed’s Open Market Operations continued purchasing MBS in the market.

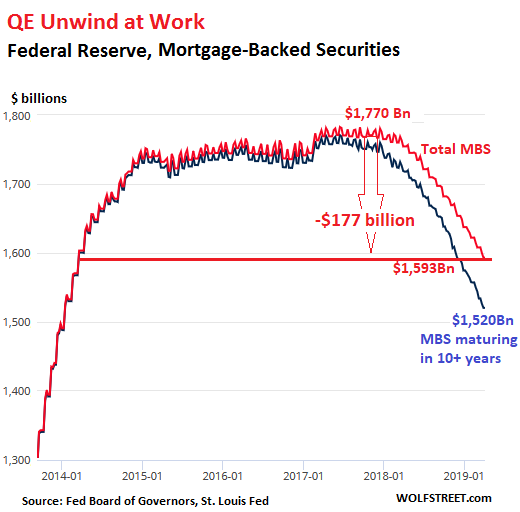

In March, the balance of MBS fell by $15 billion to $1,593 billion, the lowest since March 2014. Since the beginning of the QE unwind, the Fed has shed $177 billion in MBS.

But of these $1,593 billion in MBS on the Fed’s balance sheet, $1,520 billion mature in over 10 years!

The chart below shows the total MBS balance (red line) and the balance of MBS maturing in over 10 years (blue line), which has been shrinking slowly in part because of the pass-through principal payments:

Under the new plan, the Fed will continue shedding MBS at the current maximum of $20 billion a month until they’re gone. But that might take a long time, given their long maturities and the slow pass-through principal payments. So the Fed said in its plan that it may sell MBS outright to speed up the process of getting rid of them.

After September, it will reinvest the principal payments from the MBS into Treasury securities, likely with much shorter maturities, such as Treasury bills, of which it has none currently. This should have the opposite effect on yields that its current procedure has, with some upward pressure on long-term yields and mortgage rates, and some downward pressure on short-term yields. This would steepen the yield curve a tad.

The Fed has not yet decided on what the maturity composition of its portfolio should be or how it will get there. This decision is yet to come, it said.

And there is another twist in its new plan: In relationship to GDP, the Fed’s balance sheet will continue to shrink until some magic unknown point is reached. Read… Fed’s New Balance Sheet Plan: Get Rid of MBS

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Interesting to see the QE unwind still going despite the dovish fed talk.

In my view, as long as the Fed stays where it’s at it will push dollar strength and asset price vulnerability. Worldwide QE has dwarfed all other economic effects on the market. So my thoughts are to stay liquid and wait until the Fed eases a few times, perhaps to 1% yields with QT on hold … In other words, be patient and invest when the flood Gates of QE are open again. I have no doubts that the Fed will ease up in the next year or two, so that’s how I plan to play along.

That being said, I think we badly need an asset price correction … the dark downside of QE is much worse. I hope the Fed stays tight just like I hope to rent a decent apartment or maybe even own a condo some day. As the #1 market mover Powell said though, I gotta be patient.

Patience is a buzzword that can mean anything. I don’t get why some people think the fed is going dove besides mwybe doing one or two less rate hikes that planed.

Also the 2019 slowdown was prediced about half way in the past year.

As far as the FED is concerned, there is no reason whatever to change their plans in 2019.

‘Strong jobs number dashes recession fears and shows Fed it does not need to move on rates’

PUBLISHED 4 HOURS AGO UPDATED AN HOUR AGO

CNBC

In other words Larry Kudlow should know better than to listen to his boss.

The question is how much damage has been done by the Fed’s rushing to soothe the market’s attack of the vapors?

Waiting for Godot

A word on patience:

It is a basic tenet of Economic Theory that when governments print money, ruinous inflation follows. Think Zimbabwe or Venezuela.

I’ve waiting since 2009, where’s my inflation?

Also, markets front run reality.

Buy the rumor – Sell the fact

Your inflation is there, clear as day. It’s in asset prices.

Median workers see rapid cost of living increases in things like rent, healthcare related costs, and so on. That kind of “investment” combined with massive consolidation of businesses doesn’t lead to wage gains. Workers have less discretionary income, so CPI stays low.

Steepen the yield curve and sell off MBS is correct. More please.

Good job Wolf!!! I love your articles but just one comment on the amounts which are actually in the trillions. (ie $2.153 billion should be $2.153 trillion vs. $617 billion is correct) These amounts are so large it’s difficult to believe we printed this much money! What a bunch of fraudsters! Wind this nonsense down!

In my article, that little thing after the first digit is a comma not a dot. But when you wrote it here, you made dots out of my commas and thereby converted the number to trillions, and suddenly everything is off.

So if you read my version out loud, it sounds like two-thousand one-hundred and fifty-three billion. This equals two trillion one-hundred and fifty-three billion.

The reason I do this is to keep all numbers in billions, rather than having to switch from trillions to billions and back to trillions all the time. All my QE articles are that way.

OK I get it! Thanks Wolf for the clarification!

Ron

Thirty year mortgage pools usually have an average life less than ten years, which is why they can be funded with shorter term money. If they are selling MBS with ten year maturities it is because the life of the pools is shrinking due to home sales, refinancing, or DEFAULT.

Silly question but if the Fed were to sell MBS who purchases them?

Investors around the world. These MBS are guaranteed directly or indirectly by the US government.

Then why didnt they buy all of it then if these were so good? Why is this in the Fed if foreigners wanted them?

The FED bought treasuries too which are even safer investments. Part of the point of QE was for the Fed to gobble up super safe investments to both cause asset price inflation and to (gently) force money out of so called “safe haven assets” like treasuries and MBS into riskier assets to try and stimulate economic activity through risk taking.

By selling MBS the FED will be gently encouraging a slight reduction in risk taking by providing a previously cordoned-off wad off lower risk assets to the market which will thus move some money out of higher risk investments and into MBS as their prices fall due to their effectively increased supply.

This had been my question as well. And if there is a housing price correction and individual defaults leak into the tranches, what happens then? Didn’t the last guarantees by Fannie and Freddie require Govt intervention…..big time? Of course it did.

Guarantees are great when they aren’t needed.

It will be interesting to see the slicing and dicing for investor dicovery; what the MBS actually contain and who actually owns what?

My Dad, in another lifetime, used to occasionally buy/back 2nd mortgages of young families he knew that were trying to get into their first house. This is when you could buy a damn fine starter home for 25-28K and wages were rising rapidly (early ’70s). But, he held those mortgages on people he knew personally, and who also had a track record of stability. He never ever suffered a default and the financing was usually very short term. This modern way of doing business, financializing everything, reeks.

Iamafan,

Why didn’t they buy all Treasuries if they were so good?

They bought way too many of both … and now they’re trying to unwind this without blowing up the market.

The private-label MBS that imploded during the mortgage crisis have largely disappeared. Most MBS issued since the Financial Crisis are those issued and guaranteed by the GSEs Fannie, Freddie, and Ginnie Mae and sold to private sector investors. The Fed has bought just a portion of them. This is a huge market.

By buying these MBS or Treasuries during QE, the Fed was trying to drive down long-term rates in the credit market. Buying MBS drove down mortgage rates. While there is a big market for both MBS and Treasuries, without the Fed buying in that market, yields are likely to rise a little. That’s all.

yes but the dollar is not

By how much would the market be affected by the massive dumping of MBS by the Fed? Shall we assume banks can front run the Fed and make a profit?

Are all these MBS implicitly guaranteed by the government agencies? If yes, that raises the philosophical question – why should taxpayers guarantee someone making good on their mortgage payment?

I Am not very sophisticated in my thinking of Qt , and perhaps have drawn wrong conclusions due to it. To me QT is the final destruction of the evidence of bailing out the financial fraud of a decade ago.It represents the loss of a basic elemental requirement of human economy which is the HONEST time value of money,often referred to as the natural interest rate.We get old our work output from the past needs to equal at least the present or we risk being wards of a state,without dignity.I see the hollowed out interior of the country every day and it reminds me of the description from the declaration,of independence of our substance being ate out.

Tranch everything and put anticipated earnings on a spreadsheet for buyers, try and control inflation by keeping wages suppressed, actually fudge the discovery numbers that indicate the real health of the economy….what can go wrong?

Meanwhile bridges are falling down, no one can get into the housing market, and we’re worried about “me too” and “personal space”. Toss in a rising opioid addiction rate, lower life expectancy, continued globaization and real jobs decline, and let’s do tariffs.

Don’t worry, Dr Doom, next week might be infrastructure week and an election looms. It’ll be okay.

=>next week might be infrastructure week

It only takes a day to promise voters the moon in the morning, put it off for a couple of years in the afternoon, claim to have done what nobody else could, and then go cheat at a round of golf.

There are many examples.

I strongly suggest your read Walter Bagehot’s “Lombard Street” and see that central banking hasn’t really changed at all since at least Victorian time.

You can get the book for free on the internet. If you’re posting here, you show interest in these things, and this book is worth the time to read.

What you describe is nothing new, and will happen again.

LOL,

The unwind can continue, because the massive balance sheet really has served no purpose for years, so shrink it until it actually matters again.

After all, it is utterly ridiculous to see EVERYONE equate that large balance sheet with instant flipping inflation.

The reality has been a big overshoot in asset prices that have almost nothing to do with inflation, and everything to do with demographics.

In short, without a real push for wage inflation, which could only happen if we shut down illegal immigration and only allowed skilled immigration for decades.

In short, all the old folks grew up in the boomer years, and think it is Nixon taking us off the gold standard.

Meh, just think about how it has been, and where is that massive inflation- you might ask your farmer friends, where costs keep marching up, and yet the product is stuck in the past for pricing.

And those sky high values are the grave of investors….

LoL

Unemployment claims at lowest level since 1969. Nixon was president the last time it was that low!

Weird how there is virtually no mention of this on any of the bear blogs out there. Wonder why…..

Just Some Random Guy,

“Wonder why…”?

Because it has been in the neighborhood between 200k and 240k since 2016, jumping up and down in that range, week after week after week after week after week… How long are you going to bore your readers with it? Reading the headline in the news is more than enough. No analysis required.

A recessionary environment approaches when these claims are above 350k. During the worst of the financial crisis, there were above 650k.

But since you’re into “bear blogs,” here is something you should read for your own edification:

https://wolfstreet.com/2019/04/03/this-is-not-a-rate-cut-economy/

US Presidents have next to nothing to do with employment levels.

But also very low job growth, so we’re at full employment just waiting for something to happen, good, bad, or otherwise.

Maybe, Matt P. But I remember a similar housing boom when I was starting out as a carpenter’s apprentice. The Carpenters Union business agent came around the jobsite and confirmed I was working as a third year. He looked at my pay stub and noticed I was being paid more than the negotiated rate, we all were. He shrugged and said, “Nothing in the agreement that says an employer can’t pay more than union rate”. And now? Why they got rid of unions of course, but houses cost more than ever and the rich are getting richer. Hell, I hear some folks even bribe elite universities to get their kids in. hmmmm wonder what is really going on?

Feudalism, here we come! Next thing you know poor folks will join the military for opportunity and fight overseas for national conquest. Oh….

@Random Guy

A. Tell us how great the job market is when labor participation returns back to %66 or better. You don’t find what you ain’t looking for and these people have disappeared from the calculations since 2008.

B. I would hope you are not referring to Wolf’s site as a “bear blog”. He is quite balanced is will be the first one to explain why the sky ISN’T falling. He does so on a regular basis.

If you want feel good news please turn your attention to any of the MANY finance sites where permabulls cheerlead the good data while playing down the negatives or outright ignoring them. Hell, go to Yahoo finance and read about great the cherry picked housing data is.

If you want to be told what you already “know”… This might not be the site for you.

Is Yahoo still around? :)

The MSM is in non stop recession talk. Watch 60 mins of CNBC and at least 45 of those minutes will be “experts” debating how severe the recession will be. You can see the scorn on their face when reporting positive economic data.

If you count robots the participation rate probably is 66%

Good near time sci fi novel-“Amped” by Daniel Wilson gets into such happenings, except even further into the forthcoming animosity between hybrid humans and “normal” less productive and skilled total humans without enhancements. A world with the merging of robotics, prosthetics and Crispr into the workforce.

Capital expenditures write- offs will find their way to the other side of the ledger, and will be taxed, and consciousness will not be the determination. Politicians need to keep an affluent life style somehow.

I don’t think the Fed will even consider stopping until long-term interest rates go up. The bond market is signaling that there is plenty of liquidity, so the Fed is free to proceed.

If long-term interest rates rise sharply, and the stock market tanks again, then they will ease off.

Whats wrong with letting the MBS just roll after 10 yrs? Whats the hurry?

Absolutely agree. There is no need or value.

The Fed is in thrall to a neo-Keynesian/monetarist economic theory that says the unemployment rate is a function of Fed set interest rates. Too high, and unemployment goes up. Too low, and wage increases become a driver of inflation.

I think the Fed thinks they are close to the sweet spot, with relatively low unemployment, and little in the way of wage increases. So, as long as it doesn’t have a big influence on interest rates, I’d expect them to take a very moderate approach. Which is probably the right thing to do anyway.

Is it not more relevant to focus on excess reserves?

Until they tighten up Im not sure QT is more than skimming off excess liquidity. We do have a lot of TSY issuance though. I suspect its more a 2020 story TBH surrounding the Fed being behind the curve and there still being scope for the velocity of money to accelerate into Trump reelection bid

The algos are programmed with a positive bais to manufactured media declarations. The apparent media declarations in September will use the Fed. policy to declare the economy is getting better as shown by the induced reverse of yield curve inversion- steepening. The scam goes on. Truth is in the eternally hopeful eye of brainwashed masses. It is like a controlled reality cross between Huxley’s1984 and Asimov’s Foundation Trilogy, where reality is painted and planned out for the next future virtual reality. However, the inflection point is the Talib’s timeless swan when reality is now, and they can’t plan for it. Forgive my optimism.

Implicit, can you be more explicit? I do not understand what this means: “The apparent media declarations in September will use the Fed. policy to declare the economy is getting better as shown by the induced reverse of yield curve inversion- steepening”.

Sorry for the delay. Work called.

In September, the Fed starts buying the short term bonds with the funds from the roll off of the long from bonds and MBS. This will be a force against the short yields rising and long yields falling, thus steepening no flattening towards inversion. Will it be a strong enough force will depend upon what other bond market participants do. Probably play along by front running early on, but later who knows.

Stupid Question Department: How does anyone know if the Fed is even telling the truth?

Why, I guess that depends on what they say? Some days they tell the truth and some days they lie. Depends on what the interest rates do and how the Dow fares. :-)

Best comment award to you, Mr Mike Are.

=>How does anyone know if the Fed is even telling the truth?

To quote mayor Rudy, truth isn’t truth. So it’s all good.

Two half-truths make one truth. But sometimes you have to add up all the little pieces.

Or as my boss once told me “there is more than one way to tell the truth”.

Shut off the MCAS !!!

To repeat Otto on the Simpsons,”no can do little Bart dude” ….MCAS disabling ain’t in the manual,This bitch is going down. The fed and the banks got the ‘chutes ,to hell with me and you.

What is MCAS?

MCAS Massachusetts Comprehensive Assessment System

MCAS Marine Corps Air Station

MCAS Matrícula Consular de Alta Seguridad (Spansh: High Security Consular Registration)

MCAS Microsoft Certified Application Specialist (Microsoft)

MCAS Michigan City Area Schools (Michigan City, Indiana)

MCAS Massachusetts Child Abuse System (standardized testing)

MCAS Mediterranean Center for Arts and Sciences

MCAS Mobile Servicing System (MSS) Common Attach System

MCAS Mississippi Coast Audubon Society

MCAS Midair Collision Avoidance System

MCAS Mission Capability Assessment System

MCAS Micro Communications and Avionics System

MCAS Multispectral Collection & Analysis System

MCAS Member of the Chinese Academy of Science

The Fed’s reduction in it’s balance sheet has been too slow .

The market is rising on good news, bad news, any news, no news.

This is a sign of too much liquidity. We’ve had too much liquidity for 10 years or so. The Fed has changed nothing. Nothing has changed.

The Fed made the same mistake on interests. It raised them too slow. Now it faces increasing pressures to cut rates.

If it does not cut rates soone, new FED voting member who favor QE and 0% rates will replace those who don’t.

And an election is coming.

Wolf says this is not an economy for rate cuts. What does that matter? The economy of the last 10 years was not an economy for QE or 0% interests, but the Fed did in anyway.

For 10 years.

@timbers

If the equity market tanks even a bit, especially going into 2020, they will cut. It’s not necessarily right, but it’s unfortunately how things work today. I wish someone would have told us this back in 2009.

Is it the Fed’s job to maintain permanent stimulus?

I don’t see that in their mission statement of mandate.

MBS is a hot issue now. VP’s guy, Calabria is there to fix it :-)

https://www.whitehouse.gov/briefings-statements/president-donald-j-trump-reforming-housing-system-help-americans-want-buy-home/

There have also been efforts underway in Congress (where ultimately this has to be decided) for the government to get out of the mortgage business. But there is so much opposition to reform from the RE lobby, financial industry, etc., that these efforts so far have produced no results.

Good luck getting elected on a platform of making it harder for Americans to own a home.

I full agree with you. The govt should not be in the mortgage business. Or the student loan business. Or the health care business. Or about 1000 other businesses it is in.

But reality is once the govt starts handing out money to people (whether to buy a house, “free” health care, etc), it never stops. Like it or not, the govt will be in the mortgage business forever, regardless who is in congress or in the white house.

Why does it matter? At this point, none of the millennials can afford a house anyway. Even a gigantic subsidy from FNM or FRE is too much of a stretch.

Mortgages need to be assumable. The industry doesn’t want that but screw them.

Government “ TAX PAYERS “ should never ever be the underwriter of any private dealings and commercial transactions conducted between two parties within the economy.

The only underwriting the government/s should be legally able to do is to keep their budgets balanced . Budgets ( in non war time) should aim to provide dignified living for its citizens.

That is the role of the government (in Economic sphere) , Full Stop.

Look at us! A far cry from that!

The US tightening experiment is over. It was not popular. The majority of the 0.01% (Wall street, our leader, Govt. and the media), do not like it.

At least that is one thing they are all in full agreement on.

Let us not forget that the 0.01% majority rules in a democracy !!

We have a $80 trillion global economy that needs lower rates. A few $$Billion of MBS on or off the balance sheet will impact very little.

Moreover, i am beginning to hear the word “Japanification” more and more. The EU is as good as Japanificated at this point… And it seems to be crossing the pond on it’s way over to the USA.

When Central Banks over-medicate the patient, that’s it. Yes it appears that the pudding has been over-egged.

There is no undoing to be done.

The Japanification can get far worse in the USA. Let’s hope we don’t go there, but the trend doesn’t look good, especially with the current Administration in place…..

Returning to a normal interest rate should be called something other than “tightening”.

How about “removing the stimulus of fake and forced interest rates”?

The financial history of this nation is that Fed Funds equal or exceed inflation.

If the Fed wants 2% inflation (in violation of their stable price mandate), and others want it as well, then all those who do so are asking for HIGHER INTEREST RATES as well.

I would be more concerned with what MBS in the aggregate is doing? As long as rates on new paper are lower and or there is less of it; selling old MBS is a nobrainer. The last ten years of a 30yr bond is a 10yr bond, and 10yr rates show a dip in the curve. If Treasury pushes that issue, rates stay down, and the Fed unloads. Funny how things work out.

To insure his re-election, Trump is floating QE4. Since, Obama got QEed into a second term, it is only fair that Trump gets QEed into a second term. We are in political season now. You have got to admit Trump has done a great job reducing regulations to offset QT damage. That was a good trick. As far as investments, long real estate. Stocks will continue to rise until inflation outpaces wages … QE4 should be inflationary.

Every trader bets on what he thinks will happen. As long as there are plenty of levered bets out there, the market will take the path of least resistance, When the levered shorts have been margined out, they will go after the levered longs, thus the initial 10-20% vertical pops up and down. Nobody levered gets out alive.

Eventually, the angles of up and down soften and the market begins a slower move in one direction or another for an unknown length of time and direction. Place your bets

Since political season is starting, would be great to see a debate about market impacts from the election circus. It will be volatile. QT and QE have become political issues.

Wolf!

I’ve heard all sorts of discussion about the treatment of the principal payments made to the Fed, but what about the interest payments they collect on said securities? Are they extinguished upon payment to the Fed or are they reinvested?

Thanks!

Tom,

The interest payments that the Fed receives (from MBS and Treasuries) are revenues to the Fed. In 2018, it received $112 billion in interest payments. Here is what the Fed did with those revenues in 2018, roughly:

– It paid its operating expenses.

– It paid the banks interest on required and excess reserves: $39 billion

– It paid (“remitted”) the remainder to the Dept of the Treasury (hence to the taxpayer): $65 billion.

Here are the details for 2018:

https://wolfstreet.com/2019/01/10/fed-paid-banks-38-5-billion-in-interest-on-reserves-in-2018-slickest-annual-wealth-transfer-from-taxpayers-to-banks/

The Fed has lost all credibility when it made the decision to stop QT, just because the stock market had a little decline and Mr Trump had another fit. Everyone of those Treasury traders that I have talked with would not be surprised if the Fed changed its mind again later in the year or during 2020.

There currently are 2 seats open on the Fed. Stephen Moore a so called conservative economist who has criticized the Fed in the past and has now changed his feathers and wants the Fed to drop its short term rates by 50bp immediately and Herman Cain , who is chairman of Goddathers Pizza are the probable nominees. There is a good probability that neither one will pass the Senate.

By stopping QT and holding their portfolio at very high levels , the Fed has done what many Austrian economist said that they were doing, they have monetized the debt . This is is a similar action that happened in Zimbabwe although the degree and the mechanism of transmission are far different.

Inflation is rampant , but not in most areas where the consumer is dominant. Inflation has happened in those areas where credit is dominant, like housing and the stock and bond markets. The Fed is directly responsible for the highest GINI coefficient since the 1920’s

The former Fed chairman Janet Yellen has recently suggested that the Fed be allowed to buy stocks and corporate bonds. This seems to follow the script of the ECB.I challenge anyone to show me legitimate economic studies showing how such a program has benifitted the economies of either Euroland or Japan. In Europe unemployment in the southern tier has remained sky high and populism on the far right is rampart. Zombie companies ( those who can not generate enough cash to pay the interest on their debt are kept alive by the asinine policies of the ECB

And in Japan real estate market and stock market still have not recovered from highs set in the late 80s. Japan’s bond market does not de facto exist because of the complete dominance of the ECB. It’s stock market is on the same course with over 50% of the ETFs held by the BOJ.

Now maybe some of may consider that the 10 year Treasury with a real rate of 61bp and an implied inflation rate of 1.90% and the thirty year Treasury with a real rate is 99bp and an implied inflation rate of %1.93 are good buys but I believe that the next 10 years are going to be radically different from the previous 10

It seems like the typical mechanisms are slowing in a Japanesgue manner.

The fed will do everything that Japan, the ECB and themselves have done before to keep things from getting too volatile and uncontrollable.

The government will not be able to make the interests payments on it’s debts if rates rise too much; and too much would have been considered low 15 years ago.

However, As Mark Twain said “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

So the Fed is playing the “patience” games to confuse the market even more than what ( it ) had done in the past under the “ evil geniuses“ A Greenspan, Bernanke and Yellen “?!!

There in lie the ( Clear Fact ) that under such blind stewardship “ We” that We denote ( you and I and every Joe Blow) will sooner rather than later end up in the re run of the 07-08 financial Olympic Games!

Only 10 times the size, and 100 times the pain. The Feds patience games will only end one way, In TEARS.

The problem is they won’t be shedding them, we will.

Wolf has mentioned that the Fed holds 617b of Treasuries that mature in 10 years or longer.

If you look at the Feds holdings in a little more detail , you will find that virtually none of their holdings are in the 10 or 9 year maturities. Almost all of their 617b in longer term bonds mature in the years 2038-2042

Do we really need a FED? Would are country be better off without it? I doubt the banks that own the FED would be better off, but what about the poor or middle class?

our country.

The US banking system is a fractional reserve banking system, meaning banks can lend out far more money than they actually have. Prior to the Fed, corrupt banks would have a run and bring the whole system crashing down. The Fed was instituted to hold all of the reserves while regulating the banks to avoid bank runs. If one happened, they would theoretically have enough money to stop it.

It failed miserably during the Great Depression. Following that, the Federal government stepped in with its own regulations and the system worked spectacularly for decades.

Then the government started getting out of the bank regulation business and we got the Great Recession.

So I think if you want strong economic growth and stability, you should look towards the policies of the post war period. If you enjoy massive global meltdowns, go with a Fed and unregulated banks. If you want wild swings go with the pre-Fed days.

Its really just a political choice among demonstrated alternatives.

If Donald Dow Jones gets his way will have negative rates and QE4 by 2020.

Call me a cynic, but I have my doubts. Seeing US govt debt decrease is like seeing a Dodo Bird. However, I have seen and heard the govt and the fed lie MANY times.

Draw your own conclusion.

It hardly seems like paint drying, there must be some sort of effect on prices from this process.

Why do the charts presented only go back to 2013?

This entire matter began with the ’07 ’08 debacle.

The balance sheet starting point should be about $850 Billion.

So now it is “all the way down under $4 Trillion”? Whoopee…

It will never go below $3 Billion again….

For the “stimulus” has become the “crutch”…and crutches cant be removed.

historicus,

NO, the balance sheet should NOT be “about $850 billion” now. The balance sheet has always grown and must always grow with “currency in circulation” which is a liability on the Fed’s balance sheet. Currency in circulation are paper dollars and coins. This amount is determined by demand for currency through the banking system. The dollar is stashed under mattresses around the world. Currently currency in circulation amounts to $1.72 trillion.

The sum of the Fed’s assets is always larger than the sum of its liabilities (the difference is capital). It also has other liabilities, including “reserves” that banks deposit at the Fed. So about $2 trillion would be the theoretical MINIMUM of the balance sheet today. Then there is the issue of “excess reserves….”

All this is discussed here with charts going back to Adam and Eve:

https://wolfstreet.com/2019/01/11/feds-powell-balance-sheet-to-be-substantially-smaller-how-small-he-gave-big-clues-my-dive-into-dynamics-w-charts/

So when the Fed buys Treasuries and MBSs, where do they get the money?

They borrow it from the Treasury and place the securities purchased up as collateral.

Try this somewhere else in the real world.

No. When the Fed buys securities, it creates the money to buy them. When the Fed sheds securities when they mature, it receives money in the amount of face value for those securities and then destroys this money. This is how QE and now QT work.