In fact, QE started reversing at the end of 2014.

The Fed’s balance sheet would be “substantially smaller” after the Fed gets done with its QE unwind, Fed Chairman Jerome Powell said on Thursday. How far the Fed might go in shedding assets is a red-hot topic right now that causes a lot of fretting and howling on Wall Street and in the White House. Here is what Powell said at the Economic Club of Washington, D.C – and then we get into the dynamics and charts of what he described and what “substantially smaller” might mean:

“Yes, we wanted to have the balance sheet return to a more normal level, which is a level no larger than it needs to be for us to conduct monetary policy,” he said. When asked what level that would be, he said:

“Don’t know the exact level. That would depend really on the public’s appetite for our liabilities, specifically currency. To us, that’s a liability. And the public has a large appetite for currency….”

“So it will be substantially smaller than it is now,” he said. “But nowhere near what it was before, and the reason is, currency was well less than $1 trillion before quantitative easing started and now is moving up toward $2 trillion.”

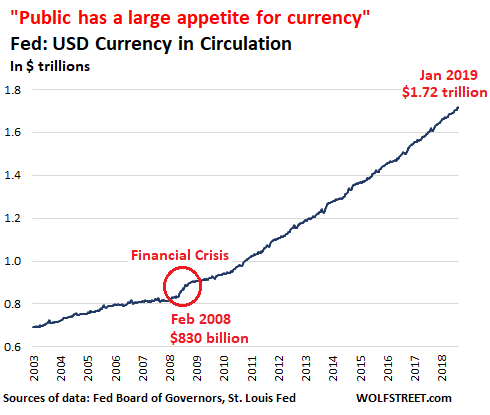

“Currency in circulation”

The line item on the Fed’s balance sheet called “currency in circulation” is composed of Federal Reserve Notes – as it says on the wrinkled and thinning wad of twenties in my pocket — and coins. In other words, hard cash. And as Powell pointed out, this is a liability on the Fed’s balance sheet, not an asset.

The Treasury Department produces the bills and coins. But the Fed manages the amounts in circulation via the banking system. Currency in circulation grows when there is a lot of demand for paper-dollar cash. There must always be enough paper-dollars in the banking system to satisfy the demand by customers for the physical dollars. And as Powell pointed out, “the public has a large appetite for currency.”

This demand for dollars is on a global basis. People globally are hoarding this stuff, and some countries use it as their primary currency, or as an alternate currency alongside their own trashed currency. When the Financial Crisis set in, folks started hoarding more of it, and demand increased at a steeper rate.

This chart shows currency in circulation. The amount more than doubled from $830 billion in February 2008 to $1.72 trillion now:

Note the steeper curve during the Financial Crisis — and afterwards. I also went to the bank and withdrew some extra paper-dollars and stashed them away, just in case. And this, as it was done by hundreds of millions of people around the globe, increased demand for those paper-dollars.

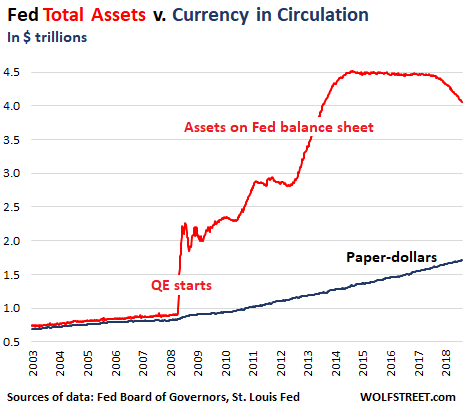

Currency in Circulation and the Fed’s assets

But banks don’t get paper-dollars for free. They have to trade for them with the Fed dollar-for-dollar. So when currency is put into circulation via the banking system, the Fed records the currency as a liability, and what the Fed gets in return from the banking system dollar-for-dollar becomes an asset on the Fed’s balance sheet. This asset is mostly Treasury securities.

Until QE blew up that whole equation, the asset side of the Fed’s balance sheet was always slightly larger than currency in circulation and has grown in parallel with currency in circulation.

The reason the Fed’s balance sheet was slightly larger than currency in circulation is that the Fed has other assets on its balance sheet, including gold, and it has other liabilities than currency in circulation. But before QE started, currency in circulation was by far its largest liability.

The chart below shows the relationship between currency in circulation (black line) and total assets (red line). Until QE started, they grew in parallel, the red line slightly above the black line. But then QE blew the whole equation apart:

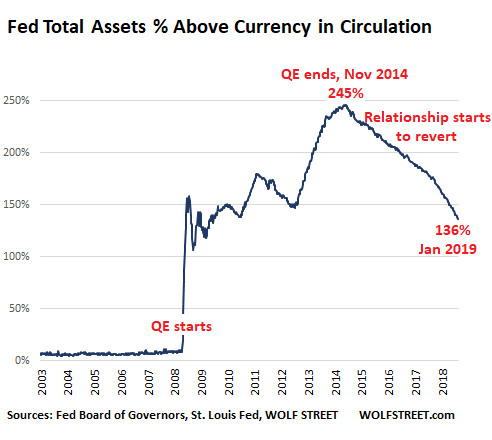

Normalizing the Assets-to-Currency Relationship

Another way of looking at this is via the percent difference between total balance sheet assets and currency in circulation:

- How much larger in percentage terms was the balance sheet before QE?

- How far has QE exploded this relationship in percentage terms?

- And how far would the balance sheet have to drop, given the continued rise of currency in circulation, until something close to the old relationship in percentage terms – for example, a balance sheet that is 10% larger than currency – is reestablished?

The chart below shows in percentages by how much total assets exceed currency in circulation. The peak of the QE distortion was in November 2014 when balance sheet assets were 245% higher than currency in circulation, up from 8% in early 2008. Due to the continued rise of currency in circulation, and more recently also due to the QE unwind, total assets are “only” 136% higher than currency, down by almost half from the peak:

By not adding more assets after QE had ended in late 2014, the Fed allowed the relationship between assets and currency to start reverting, or — to put words into the Fed’s mouth – “gradually normalizing.” In other words, from this perspective, the QE unwind essentially started in November 2014.

Even if, hypothetically, the QE unwind stops at this very moment, and the balance sheet assets remain level, eventually – perhaps in 20 years – the old relationship would be reestablished. But the QE unwind speeds up that process by a lot.

The relationship between currency and assets is key. This is what Powell referred to when he said that the level of assets “would depend really on the public’s appetite for our liabilities, specifically currency.”

And so, he said, the balance sheet “will be substantially smaller than it is now,” but given the surge in currency in circulation, it will be “nowhere near what it was before.”

At the demand rate for currency over the past 10 years, there will be about $2.2 trillion of currency in circulation in 5 years. That means that the balance sheet, if it is going to be just 10% larger than currency in circulation, would need to be near $2.4 trillion in order for the old pre-QE relationship to be re-established. This means, the Fed would have to shed an additional $1.6 trillion in assets over the next five years.

And it has already shed over $400 billion since the QE unwind started. Read… Fed’s Balance Sheet Reduction Reaches $402 Billion

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Very interesting that Powell is maintaining his hawkish stance on QE unwind, even as it appears that he is being a little more dovish on the FFR (federal funds rate) increases.

Perhaps Powell is more of an anti-bubble hawk than what the media has made him out to be in the last 3 weeks?

I think Wall St has misinterpreted Powell yet again, perhaps intentionally so, in order to make the public believe there is a “Powell put” for the stock market.

Justme,

Powell was never a fan of QE. And he even mentioned that in the interview.

What’s interesting is that even uber-dove Bullard want’s the QE unwind to go on. It seems they really want to get the balance sheet back to some sort of normal level that allows them to do monetary policy in the classic way.

Wolf – I’m assuming you have seen the NY Fed forecast of liabilities for the SOMA Account (Chart 30) produced in April 2018? It provides a forecast for 2025 (in billions) with a low of $2,706 and High of $4,034 with median forecast of $3,466. Other Assets are obviously not relevant so looking at the liabilities with a current As of mid-November the total of liabilities was $4,106 billion.

I think the focus will be the excess reserves given the interest rate cost as you pointed out yesterday. They will try to get that to zero but everything else will be growing including required reserves. The interest on excess reserves is going to pop up as major political problem again though Congress can’t actually do anything about it.

Is there a relation in the Federal Funds rate and the assets / currency circulation? The federal funds rate has traded in its lower range every time the rate was raised. According to a former Fed banker he sees this as the monetary policy having slack i.e. looseness. He thinks that as QE is decreased the Federal Funds rate range will tighten. If this occurs he thinks that the Powell Fed will have a better understanding/grasp with respect to returning monetary policies to “normal”. Steve Mnuchin alluded to the use of the asset side instead of using the Federal Funds rate to normalize policy.

That is great to hear! The classic way is more transparent to us all.

I also scrutinized that comment. Could this financialized global market stand a “….return to the classic”….(model)? Or would that model prove to be too restrictive? Hmmmmm.

Ultimately, the “Classic” way to extinguish an unserviceable debt bubble, is a currency devaluation. History pretty much proves this out.

We are likely entering the point where the Fed finds itself captive to markets and politics.

It’s been implied that the unwind was part of an agreement for QE3 to get everyone on the board to vote for the policy.

I’ll make another observation that I think is interesting: It is very difficult to undo dollar bills!! FRB can undo reserves by letting the underlying bonds roll off the balance sheet (i.e. expire) , but you cannot undo dollar bills except by extreme measures such as invalidating them wholesale, and then printing a new and physically different dollar bill.

They tried to undo paper currency in India two years ago and it was a sham and waste of epic proportions.

Justme, +5 for this! “I think Wall St has misinterpreted Powell yet again, perhaps intentionally so, in order to make the public believe there is a “Powell put” for the stock market.” So the asset-gatherers can retain some income, and so the insiders can unload soon-to-be-worth-less assets on the unsuspecting public.

P.S. The bankers can’t “undo” dollar bills under mattresses, but they can certainly snag and remove the ones in circulation. The banks do it all the time in order to recycle tired, worn bills. Also to shuffle the bills to whatever part of the country has a shortage. Or to send them to Puerto Rico after hurricanes, or to Iraq after an invasion.

Good point. And how do you deal with the vast quantity of currency held outside of IOUSA?

“So the asset-gatherers can retain some income, and so the insiders can unload soon-to-be-worth-less assets on the unsuspecting public.”

Exactly, the Fed is dumping up to 50 Billions a month of their Sliced & Diced Mortgages that they bought up from all the cheating banks after the 2008 Financial Collapse.

America’s top banks fined Hundreds of Millions to Billions of dollars in fines for Fraud, Corruption & Manipulation of the Markets after the Collapse.

Now 21 Trillion in Debt – Trillions Missing & Unaccounted For – Pensions Underfunded.

Nobody Goes To Jail – FED Refuses to be Audited

America’s House of Cards is Burning Down While Everyone Pretends Otherwise.

That is one reason people like physical representation. I wonder what banks do if there is a reverse flow and cash gets deposited, do they exchange them for CB assets? Poor CB, has to give up interest paying securities for its own paper which it then flushes after use…. O.K…. not poor CB… let’s say poor taxpayer for less eventual remittance to the treasury?

“Poor taxpayer”, every which way you lose :-(

Are you not confusing the dollar with dollar policy? They are one in the same.

Powell knows who the boss is. Trump. After Trump expressed his dissatisfaction with his policies, Powell straightened right up and brought the markets back. When Trump runs the show, it will be anything it takes for more GDP, even if that is inflationary. Easy.

He actually seems to be doing all he can – that jibes with his base – to drive GDP down. The trade war, the ridiculous wall, policies that are ultimately going to end up with us like South Africa, shunned by the civilized world.

Very interesting stuff. Currency as Fed liability is virgin info to my brain, thanks.

One thing we have learned from Powell’s several years at the Fed:

Raising rates towards neutral as the rate the Fed has done, is much too slow to be desirable. We can confidently know that now, that 0.25% increases are just too small and a failure. Increases of .50% would be indicated as the next level to use, should anyone be at around 0% again (Europe are you watching and learning?….I think not….though Europe could be different). Also, starting from 0% if ever again, I can’t see why the first increase can’t be a full 1.00 if only to play catch up and slice years off the 3 years Powell spent.

It seems as if physical currency is a small fraction of money supply as hardly anyone uses cash anymore, at least in this country. Most money is created via credit. Just keystrokes on a computer. Once debt is created the only thing that supports its existance is the promise to repay it unless it was used to purchase a colateralized asset. If the debt is defaulted on, the money simply dissapears.

Is this true? I think the money still exists somewhere, right? If someone takes a non-collateralized debt then defaults, the issuer is out the $, but the $ is somewhere. If spent on anything, it was transferred to vendors, service providers, employees, etc.

I was recently having a conversation with a relative in central Florida who makes the cash deposits for a busy local gas station with minimart/subway type shops. I was shocked by how much cash he deposits for them. He says that since the area is relatively low income, a lot of people don’t use credit cards.

Also you may have noticed that many gas stations now give a neat little discount for “cash” purchases. I used to watch the “older generation” way, way back in the days of 1940’s, how small business owners treated their cash…..transactions that almost always included a “sharing” of part of the cash deal with a small undeclared “cut” for the “house.” Those were the days of “cash discounts” beyond the….”…..30 days net”. Yes, the “commons” usually has access to cash but no credit cards….which might be a blessing for them (us?).

Anna and Sierra7,

I have seen a few gas stations that offer a 3 cent per gallon discount for gas for cash. At $2.00/gal, that is about 1.5% discount. Since gas stations pay about 4% to the CC companies, this is a win for the gas stations and cash paying customers.

However, some CC companies are offering 3% cash back for gas when you use their card. ie Costco.

As long as that is happening (and I can float my gas expense for free for a month and get 3%), I will continue to use my card. Well, at least while I am working and can pay off my 1 credit card on time to avoid the 28% interest on the card.

I am not yet lured into shredding my credit cards while they are still unsuccessfully trying to tempt me into the oblivion.

The Feds Liabilities other than excess reserves are in Table 1 – Factors Affecting Reserve Balances of Depository Institutions (continued) of H.4.1.

They say that a vast majority of the currency in circulation about $1.71 Trillion are in the hands of foreigners (I guess under their mattress). Why dead money has to be backed 1 to 1 with Treasuries is beyond me. I guess if we go cashless, then we won’t need this much currency in circulation.

Anyway, I think we can maintain the current liabilities (excluding reserves) at near $ 2.543 T or even less than that if we go digital.

The autopilot Roll-Off for the next 5 years (not counting additional maturities from 2Y 3Y and 5Y Treasuries) are about $916 Billion. A reduction of that amount is a little more than the $806 Billion in Treasuries added in QE3 (only). So all we are doing is rolling back QE3 in about 5 years and essentially leaving QE1 and QE2 balances intact.

The loud objections against Quantitative Tightening is pure whining. All the complaints against less liquidity is about the crowding effect (against the stock market) by the massive amounts of added Treasury auctions moving forward.

If you are a saver wanting higher yields then shout out “bring it on”.

“So all we are doing is rolling back QE3 in about 5 years and essentially leaving QE1 and QE2 balances intact.” QE3 was all about “signaling” anyway, according to Bernanke. They wanted to send the TINA (there is no alternative) message and force investors away from cash with another $1 trillion dollar tranche. It worked, and now its being walked back.

The demographic trends seems to be a major factor. Now that about 95% of the world’s population growth is coming from less-developed countries, it could be that people in those countries consider credit, or even credit cards, as more of a novelty. Nor are they as digitized as we are, implying that any computer larger than a smartphone is unusual. As you noted in the article:

“This demand for dollars is on a global basis. People globally are hoarding this stuff, and some countries use it as their primary currency, or as an alternate currency alongside their own trashed currency.”

Jump ahead 10 years to a movie called “Internet Down”, and it could show a world where few would give up any of that “stuff” for a piece of plastic. If the grid is at risk, then the web is at risk.

This absolutely. I’m all about cash and so are most people. You leave far less of an info trail using it, it’s easy, quick, can’t be disappeared on a computer, can be hidden under the mattress (banks of Sealy and Serta are my two favorite banks).

You mean the private equity investment firm of Simmons Sealy Serta Stearns & Foster. :-)

I believe there is a much larger use of cash than most people realize. The ramp up after 2008/09 in currency can’t be attributed to “hoarding”. Sure there was hoarding during and for a period after the Great Recession, but I seriously doubt it is going on now.

The increased use of cash in the US is supporting the hidden economy of the bottom 50%. Those people aren’t probably reading this website like us.

Cash equals no taxes and it also is used by those that can’t or don’t want to set up a bank account (most notably illegals in the country). And we know there are bunch of those folks here for the duration.

Outside the US, people use cash to avoid currency effects and crisis within their countries. The cleanest dirt shirt.

Mostly this jawboning by Powell is to simply establish some reasonable expectations about the lower bound of reducing the Fed’s balance sheet.

It’s not going back to anywhere near where it was before. In this case, he wants to use the cash needs/preference as the rationale, but it probably is based on the fact that the economy will go into recession well before they get there. Whatever his reason, it sure sounds like making some excuses before the reality hits.

Very true. Use of US cash is growing (especially world wide), as the need for privacy increases daily. Credit card companies, and any kind of lending, is just not a good thing, and people are realizing that more and more each and every day. Bitcoin got its start bc of that need for privacy and avoidance of the system, but people ultimately discovered it was not nearly as private as they wanted. The problem is digital. Something digital ALWAYS leaves a ‘trail.’

And when I say cash, I’m talking physical dollars, not checks or anything else. There are more people daily who desire to stay completely out of the banking system as much as they can. Further, the Fed needs to stay on the path of increasing rates, and do so for a very long time to come, since especially QE went on far too long, and from so many central banks, so that will keep the dollar stronger for some years ahead vs other currencies. Thus oil price will be kept in check , and buying power of other countries goods will be kept in check. I’d argue they are still way behind the curve, as evidenced by the real inflation in all sorts of goods and services, and it continues to be a major hazard. They are still too dovish and accomodative, and that is spreading inflation into every single crevice on the planet. If stocks take a hit because the Fed is more aggressive on its hikes, then that means it needs to happen that much more. The bubble in stocks is gargantuan. If this is the Fed’s idea of letting air out of that bubble slowly, it means we need another 5 years, and 20% corrections each year to get back to any reasonable valuation. Of course that cannot be controlled. So eventually the market will decide suddenly, the slow prick, only delays the inevitable, and everybody will want out quickly, to ironically ‘preserve’ as much of the gains as they can, which will further heighten demand for cash and US dollars.

Well Mike Are,

This Canadian just returned from a 6 stop town run. I bought paint, electrical, some stuff for a van I am outfitting, (a van by the river :-), groceries….all paid with cash. I visited the credit union to restart a RIFF; at a withdrawal rate just low enough to keep me in a lower tax bracket. Forgot to pick up more cash. Note to self: get some next week. I have a small rental which tenant pays for in cash. I spent 40 years operating out of a high tax bracket, and as a wage earner taxes are deducted at source so there are/were few reductions to enjoy like the wealthy have access to. Now that I am retired I really really enjoy paying for everything with cash. It’s up to the seller to declare the sale for taxation purposes. I don’t like Big Brother watching what I buy or do.

Two weeks ago we had a massive wind storm. The power was out and a local restaurant kept open to provide hot meals for stranded drivers. My wife was one of them. All their till machines and computers were out as the internet was down. They took IOUs and cash. Good lesson for everybody.

Hell I made a payment on my phone (have a $30 a month pay as I go plan) and the Verizon store only took cash!

Most gas stations here in Long Beach, CA i’m noticing are increasingly accepting only cash or debit. Had to drive for a bit to find one that took credit.

Yes kinda’ miss “Van by the River” comments. Wonder if he still listens in.

I contribute to the cash statistics in the plots. Built up cash reserves at home just in case…maybe something like the threat from yellowvest in France to make a bank run on cash.

He made a comment on another thread a couple days ago, then went off grid again.

Powell, in discussing Fed Fund rates, has gone from “a long way from neutral”, to “just below neutral” a few weeks later.

He has gone from three rate increases in 2019 to two increases in a short period of time to “the Fed will be patient” meaning two increases are now off the table.

The Fed will be looking at “datapoints”. GDP? Inverted 2/10? Phillips Curve?

No, the DJIA.

So much for the independent, monetary hawk who will undo the Fed lunacy of the last decade. A phoenix resurrection of the Greenspan/Bernanke/Yellin Put.

DJIA aka “pressure from Trump”.

It’s awkward for the Fed but they really do respond to pressure, if they think there’s any chance that there would be more than talk.

The great fear is that Congress will rein in their independence in some way. Trump would sign that kind of bill, if Congress presented it, I’d say. Recent previous presidents would not have done so.

I should say I think pressure works at the margins — I mean that it won’t change things unless the Fed is a little bit undecided in the first place, but that much can matter, of course.

I wonder how much of the Excess Reserves have been tacitly re-hypothecated (in some sense), used as collateral for shadow loans or other off-the-books schemes?

Excess Reserves are fundamentally no different from the famous Chinese Warehouse schemes in which a warehouse full of metal is used as collateral for multiple loans. Idle assets are scam magnets.

Any bank that could get paid 2.4% for the “Excess Reserves” AND collect the going rate for whatever scheme they have in mind… would want both. Especially if no punishment was likely or there was a pre-designated scapegoat ready to hand!

Wisdom Seeker,

This observer thinks you may have nailed it.

The past 10 years? From this vantage point, the term applied has been “The Great $USD Re-hypothecation”.

Now we’re witnesses to the unwind of this re-hypothecation. Went exceedingly poorly for EM’s and the EU last year and started to fall apart for the U.S. at the end of the year.

Still in the early innings and QT indeed on auto-pilot. Massive disruptions and dislocations still to come. Keeping the pantry stocked with plenty of popcorn.

i had brought up this idea on a previous post but wolf seemed certain that the reserves could not be used as collateral. if this is indeed possible, i would love to know how it’s done.

The Fed is going to crash the stock market.

Wolf, to what extent does external – non-USA – demand for currency enter into the Fed’s consideration of balance sheet size?

I ask because of Jay Powell’s statement “… it depends upon the public’s demand for our liabilities…” , and the fact that the Fed has engaged in a large number of swaps and repos with foreign Central Banks, as well as an unknown number with foreign commercial banks.

Currency in circulation is really just physical paper-dollar cash. It is not related to the Fed’s swaps and repos. These are separate animals.

That said, as you alluded to, much of the demand for physical dollars comes from overseas.

From this article:

“This means, the Fed would have to shed an additional $1.6 trillion in assets over the next five years.”

From the prior article:

“Therefore, the amounts in interest expense the Fed pays the banks on their “Excess Reserves” and “Required Reserves” … was huge in 2018: $38.5 billion!”

And

“Excess Reserves are the amounts that banks voluntarily deposit at the Fed to earn risk-free income. The amount peaked in September 2014 at $2.7 trillion and has since fallen to $1.5 trillion.”

Hmmm… need $1.6T, “excess” reserves of $1.5T…

Seems like we could solve a few problems here.

When he says “the public’s appetite for OUR liability,” he means the taxpayer owns it. If printing cash creates a public liability, what happens when there is a run on the bank? The cost of printing cash comes back out of our pockets. In simpler terms it is inflationary, by exchanging 30yr T bonds for cash, in the case of China, that would be inflationary, (and when gov discounts bonds that’s exactly what they do). When he says OURS he means YOURS.

THE asset in question that is used to back cash is government debt, as it is the ultimate reserve on the issuance of cash within any meaningful fiat system.

The value of government debt or its cash derivitive is at its simplest based on two paradigms.

Firstly, as you say, it is the ability of government to extract redemption of its debt from the public via taxation – liability . If there is a run on the banks and reserves must be increased to cover the issuance of cash, normally the yield on government debt will decrease. This alone would be inflationary as the government would be paying less interest and so have more margin for a larger principal. However a run on the banks ironically would likely signal a loss of faith in the financial, and hence in consequence, the monetary system. People would just be rushing to claim what they could before the door closes. So of itself you are maybe looking at a hyperinflation and a breakdown of the value system of the currency. That the backing is a public liability will not be part of anyone’s thinking, as they are grasping at the residual value the currency once had in society, or whatever is left of it. In hand with this goes a lack of control of the market by the central bank. Transactions become effective without intermediary, and visible devaluation of the currency becomes self reinforcing until it reattaches or is reattached to a viable or understood asset. Hence government debt might be issued at levels to keep up with the runaway inflation, in essence a loss of monetary control or meaning as the real economy takes a life of its own. I expect in such circumstance guarantees ( QE and FDIC are examples) , and if not capital controls and price setting , would be used to contain the market. I think to leave Weimar property was used. So what I am saying is that the public liability here actually adds up to the hypothetical cost of system failure to society, where any financial savings become worth much less. There is nothing backing fiat except the promise of more fiat, the obligation of legal tender, and the gist that it is all for real because it touches on the real economy by obligation of taxation. Because that very last sense is crucial for fiat to exist, as it integrates the power structure of governance into society and lends legitimacy to government debt , you are right to say the liability is of the public when cash is created. A run on the banks is more akin to saying forget everyone else and the public and the government et al though – there is no more government and public, just paper that might be used. Maybe there is a halfway where authorities reap the tendency towards cash keeping it managed to own benefit, but if so, if that is really the game at work, then the system is more vulnerable than it appears, being on a perpetual tenterhook of sorts. Either way, any increase in government debt IS a public liability, no matter if it is redeemed via future taxation or active debasement of the currency itself.

The second paradigm is simpler, it is the method of expanding government debt that sees the real value of currency deflate. This could be seen as the cost to the public of a non productive sector, and there you have all the arguments you can think of of whether government is overall positive or simply parasitic – one thing for sure is that it is opaque and the unhelpful will be mixed with the helpful to such a degree that you cannot discern one from the other. As the base funding of this is via the productive economy, and the debt is grafted on to that in a non voluntary manner (by force via taxation), I think it can only be concluded that the whole fiat monetary system, cash and all, is based on transferring the liability of the currency onto the public so as to extract their worth, so as to value their worth in that currency, and so as to be able to then manipulate those values to a degree, in the name of management.

If people accept all of that well who am I to say better.

Thank You Mr. Wolf Richter. You have helped me with your writings beyond sense.

Does anyone know what the impact of this would be to a cashless future? What happens in extremely cashless economies like Sweden? Do they suddenly start having lower and lower liabilities?

James: First you have less choices! Less choices means less freedom! Are you sure you really want to go there?

I was asking, what happens to Central banks. Do liabilities decrease (or slow down rate of increase) in cashless societies? Does it affect rate of monetary increase in future?

Powell has said so many different things in such a short time that I am now discounting whatever he says. I will wait and see what the Fed does and mostly ignore what they say. The technical term for this is “loss of credibility”.

What they have done so far is stick to their schedule of a rate increase every other meeting, and until December they stuck to their QT schedule, but as Wolf points out they didn’t have enough maturing paper to max their unwinding schedule.

That seems to indicate to me that they are holding no one-month bills anymore, and by February they will be holding no 3-month bills. Is that a misunderstanding?

At any rate, it seems that the pace of QT unwinding going forward will be less than what they had previously promised due to a shortage of expiring paper. And we won’t see what they do on the Fed funds in two months for another two months, so it’s all jawboning in the mean time.

Eastwind,

The Fed hasn’t had any short-term Treasuries (bills) since the days of Operation Twist years ago. They replaced all their bills with longer-term paper at the time to push down long-term yields. Over the years, whatever matured was replaced with longer-term paper.

Actually, the Federal Reserve doesn’t have any gold. Instead, they have gold certificates ($11 billion worth) they received from the Treasury when the gold was confiscated. Take the $11 billion divided by $42 per troy ounce (the statutory exchange rate-holy Hitchhikers Guide to the Galaxy) and by the 32,000 oz per ton, and you get, voila, 8 thousand tons.

Wolf, thanks again for sharing more insight to the Fed:s doings!!

With regards to QE/QT, I am surprised that so few analyse the detailed mechanisms and flow of liquidity due to these programs. To me it looks fairly obvious that the liquidity effect of QT (and QE) affects markets directly, as the credit channel does not easily replace liquidity withdrawn from financial markets (mainly managing savings I assume). And as you noted 400 billion is alot of mpney (the bank system created in aggregate net about 500 bn last year)

Some argue that QE provided excess liquidity and QT does the opposite, without any practical use and with small real effects on markets. But I would argue that 1) liquidity is always and in any form a risk management tool and therefore you should not assume it does not play a role just because it ends up as excess liquidity (and excess reserves at FED). And 2) there is in any case the ‘flow effect’ that affects financial markets since that is where liquidity is withdrawn.

Wolf, could I ask for your view/opinion on this relationship – does QE/QT influence markets as directly as I personally think or is it a smooth way of reducing excess reserves and as interesting/relevant for us market participant as “watching paint dry”?

Cheers!

Fred

Frederik,

In general I agree, but I’m not sure that I would go as far as saying “QT influences markets as directly,” because “directly” can mean different things to different people. But with QT, the Fed “indirectly” via the Treasury Department drains money from the market and destroys it. This has the reverse impact that QE had. But the amounts of QT are smaller than the amounts of QE were. Here is how it works in basic terms:

Step 1: When the Treasury securities that the Fed holds mature, the Treasury Department transfers the money for the face value of those securities to the Fed. If the Fed doesn’t buy other assets with the money, that money just disappears.

Step 2: Since the Treasury Department doesn’t have the money to pay off maturing bonds – as the US government runs a big deficit – it raises this money in advance by selling new bonds at regular auctions.

Step 3: By buying the new debt that the Treasury Department issues, the bond market gives its money to the Treasury Department that the Treasury Department then gives to the Fed to redeem the Fed’s maturing bonds.

Step 4: Because private bond buyers replace the Fed by the amount of the QE unwind, these bond buyers have to sell something else to raise the money to buy those bonds.

It’s by this mechanism via the bond market and the Treasury Department that the QE unwind drains “liquidity” – or whatever else you might want to call it – out of the broader markets.

Kind of like the old street/schoolyard playtime: “Ring Around the Rosy”?

Again, Mr. Richter you have elevated my knowledge of the financial system a micro-degree with each article!

Wolf:

Thank you for your site; it’s uniquely specific in a journalistic world sorely missing out on data and reliable resources.

Could you, please, point out the finances behind the current government shutdown, please?

My best bet is we are still speeding away on the financial highway to hell, but it would be nice to see the details…

Thank you in advance.

A shutdown doesn’t change the finances of the government. All the arrears it doesn’t pay now (salaries, etc.) will be paid as soon as it re-opens. All government employees will get paid their salaries that they earned during the shutdown, but they’ll be paid late. This impacts the personal finances of people who live paycheck-to-paycheck, but it doesn’t impact government finances.

I am aware of that. However, they are not spending our money while they are not working…

As per one source,the USFR is hiking the rates to save the US Pension System,which seems to be in a bad way.Some say already DESTROYED by low rates,ZIRP.Other reasons for QT,as per sources :–

1.To bring the value of Collateral,which is HIGHER in a BUBBLE to par value.

2.Excessive Corporate Leverage.

My hunch is that Powell is trying to help pension funds

stay afloat. The PF’s want an assured cash flow of 7-8%

and not “maybe” capital appreciation.The chattering

classes on CNBC seem loath to address this notion for

fear that the Fed is removing the punch bowl and the

equity markets are about to get trounced.

Projected the two curves on the first graphic and came up with the intersection of QT and the cash at about 2.5-3 years out, which interestingly is the same timeframe (mol) that a basic chart of the recent S&P 500 downtrend at the usual velocity (not the last month) intersects the long term uptrend that started around 1983 which touches several major bottoms/correnctions along the way. Most recession predictions I see are in this timeframe too. Am curious to see if these trends play out but the next few years is looking like a good time to invest in popcorn and watch the fireworks.

Sorry, the second graphic…

I’m wondering what was more damaging to the economy: QT or quantitative tightening or the spike in interest rates. Are the two independent of each other or does QT lead to higher interest rates?

Here is a clue.

Most of that money is drug money. There is at least $900 billion in US that is used for drug money.

Where are all the “experts” that said 2% (or a little more) would be a good thing? Did they not think interest rates would also rise, or did they expect negative real returns forever?