The QE unwind has started to rattle some nerves.

For the past two months, the sound of wailing and gnashing of teeth about the Fed’s QE unwind has been deafening. The Fed started the QE unwind in October 2017. As I covered it on a monthly basis, my ruminations on how it would unwind part of the asset-price inflation and Bernanke’s “wealth effect” that had resulted from QE were frequently pooh-poohed. They said that the truly glacial pace of the QE unwind was too slow to make any difference; that QE had just been a “book-keeping entry,” and that therefore the QE unwind would also be just a book-keeping entry; that QE had never caused any kind of asset price inflation in the first place, and that therefore the QE unwind would not reverse that asset-price inflation, or whatever.

But in October last year, when all kinds of markets started reversing this asset price inflation, suddenly, the QE unwind got blamed, and the Fed – particularly Fed Chairman Jerome Powell – has been put under intense pressure to cut it out. Yet it continues:

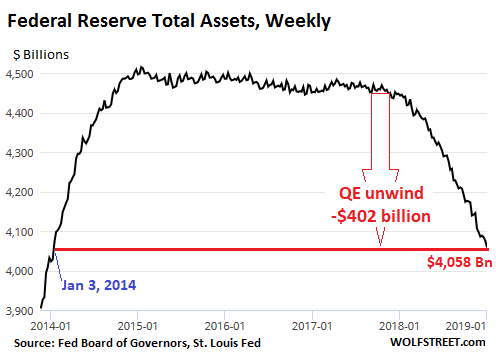

The Fed shed $28 billion in assets over the four weekly balance-sheet periods of December. This reduced the assets on its balance sheet to $4,058 billion, the lowest since January 08, 2014, according to the Fed’s balance sheet for the week ended January 3. Since the beginning of this “balance sheet normalization,” the Fed has now shed $402 billion.

According to the Fed’s plan released when the QE unwind was introduced, the Fed is scheduled to shed “up to” $30 billion in Treasuries and “up to” $20 billion in MBS a month – now that the QE unwind has reached cruising speed – for a total of “up to” $50 billion a month. So how did it go in December?

Treasury Securities

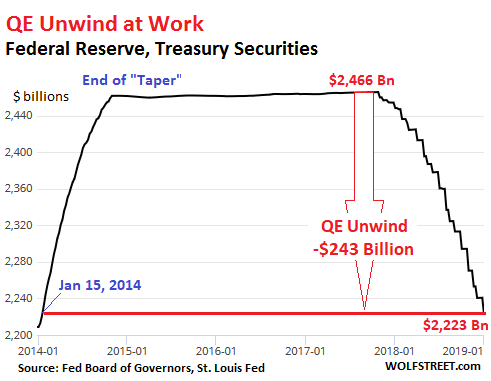

Over the four weeks from December 6 through January 3, the Fed’s holdings of Treasury securities fell by $18 billion to $2,223 billion, the lowest since January 15, 2014. Since the beginning of the QE-Unwind, the Fed has shed $243 billion in Treasury securities:

The Fed sheds Treasury securities not by selling them but by allowing them to “roll off” without replacement when they mature. When Treasury securities mature, the Treasury Department transfers money in the amount of face value plus any outstanding interest to all holders of those securities. The fact that Treasuries mature mid-month or at the end of the month creates the step-pattern of the QE unwind in the chart above.

On December 15, no Treasuries in the Fed’s portfolio matured. On December 31, three issues matured, totaling $18 billion. This did not reach the cap of $30 billion. So for the month, all $18 billion in Treasury securities that matured were allowed to roll off without replacement. And the Treasury Department paid the Fed for them.

The Fed creates money, and it destroys money; but it doesn’t hold trillions of dollars in cash. So when it received the $18 billion from the Treasury Department, it destroyed them just as it had created them to purchase these securities during QE.

For those wailing and gnashing their teeth about the QE unwind: Going forward, there will not be all that many months when enough Treasuries mature to reach the cap of $30 billion. For example, in January the Fed’s maturity schedule shows that four bond issues will mature totaling only $13.3 billion, including one issue of TIPS.

Mortgage-Backed Securities (MBS)

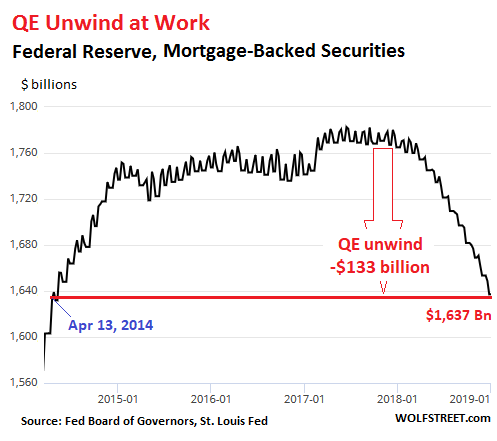

The residential MBS that the Fed acquired as part of QE were issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. Holders of these MBS receive principal payments as the underlying mortgages are paid down or are paid off. The remaining principal is paid off at maturity. To keep the balance of MBS from declining after QE had ended, the New York Fed’s Open Market Operations continued purchasing MBS in the market.

The Fed books MBS trades at settlement, which lags the trade by two to three months. Due to this lag, the amount of MBS on the weekly balance sheets in December reflected trades in September and October. In September, which was the last month of the ramp-up period, the cap for shedding MBS was $16 billion. In October, the cap rose to $20 billion.

In December, the balance of MBS fell by $16 billion, to $1,653 billion, back where it had been on April 13, 2014. Since the beginning of the QE unwind, the Fed has shed $133 billion in MBS:

So December was a somewhat slow month for the QE unwind, with $18 billion in Treasury securities and $16 billion in MBS rolling off the balance sheet, for a total of $34 billion that went back where it had come from during QE – namely ambient air.

Investors are waking up after years of central-bank inspired somnolent money-making. Read… Markets Are in a Tizzy. So What Will the Fed Do?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, what are the implications for the Fed’s corporate welfare program via IOR (Interest on Reserves) to the big banks?

We should get the new numbers in a few days for the amount the Fed paid the banks in 2018 in interest on excess reserves (IOER) and interest on required reserves. This is going to be a big pile of money. I’ll cover this when I get the data.

The Fed uses this as a tool to keep the federal funds rate within its target range. I get that. But the other implications are many — and the Fed never mentions them.

Some of the Fed writings explain how IOER had set a floor and effectively replaced the corridor they had floor rate setting or in effect monetary policy. It’s wonky but worth reading.

As far as the rolloffs are concerned, try this for comparison. Wall Street cheered as companies budgeted 1 trillion in stock buybacks in 2018. Yet they complain about the QT which will reduce less than that amount in 5 years. Ridiculous if you ask me.

In this modern world, the partygoers hold a riot should any adult dare to try to take the punch bowl away. And that of course always works out well, right?

Thank you.

Mr. Richter,

I am trying to wrap my mind around the impact of the Fed normalizing its balance sheet while raising rates.

While reading about past recession I have led to the paper Gold Sterilization and the Recession of 1937-38 by Douglas A. Irwin to gain an understanding of simultaneous events which created the recession of 1937.

He posits that the recession was only slightly the result of an increase in reserve requirements. But, the real culprit was the U.S. Treasury began sterilizing gold inflows. “[W]ith sterilization, instead of replacing its withdrawn balance with a gold certificate in equal amount, the Treasury kept the certificates in an “inactive” account where it could not be used for the expansion of credit.”

He believes the growth of the monetary base was stopped and created the recession.

Would you mind addressing how the combination of Fed actions could impact the monetary base and once again create a recession?

Thank you

Joe

https://economics.yale.edu/sites/default/files/files/Workshops-Seminars/Economic-History/irwin-110926.pdf

Recessions (busts) are created by booms. Both are created by human nature. Or do you mean ‘trigger’ a recession?

One snowflake or vibration can trigger an avalanche, but you need a massive build up of snow on a slope to create one.

Please include the 6% interest some banks get on their Fed Stock.

That’s not how it works.

The 12 regional Federal Reserve Banks are owned by financial institutions in their districts. For example, Wells Fargo holds shares of the Federal Reserve Bank of San Francisco. The FRB of San Francisco pays a dividend (not interest) to its shareholders. The 6% you mentioned is based on the value of those shares. But the shares are not publicly traded, and the value of those shares is not disclosed. If the value is relatively small, that 6% of a small value doesn’t amount to much.

The book value of the Federal Reserve (“Capital”) is only $39 billion — relatively small because the Fed remits almost all its profits to the Treasury Dept.

So if the book value is an indication of the share price — Wells Fargo currently trades at a price-to-book ratio of 1.1 — that 6% dividend is not a large dollar amount, unlike the IOER.

Basically what IOER does is to convert reserves into interest-bearing securities so they don’t behave as hot potatoes inflating asset markets. With IOER, the economy is behaving as if the Fed’s balance sheet has already been cut to $2T. Is the Fed creating huge risks by allowing its balance sheet to shrink by $50B per month? No, because excess reserves already earn over 2%. If they hold T bills instead, what do they care? We are still on the flat of the liquidity preference curve, so there is still a long time before T bill rates rise appreciably above the IOER rate. When it’s down to $2.5T, the T bill rate will be about 1% over IOER.

IOER is really RRPO, or Reverse Repo, which they would prefer you didn’t think about. There was a spike in REPO rates on the 31st which brings it all into question. REPO is the discount window, RRPO the guy in the window reaches out and grabs you by the lapels. When the Feds albeit higher rates are superceded by the markets, you have to assume the Fed real position is to pin their rate below the market, which resulted in a market rally. Hence real rates remain negative. I continue to expect a sudden rate hike, see Powell’s prepared statement.

The market has a “negative rate” needle in its arm….

and Powell is trying to pull it out….

Where are those who felt the Fed promoting 2%+ inflation was a good thing? Did they not think rates would rise to meet that rate???

Is there another site on the PLANET that’s bringing this news forward???

Thank You Wolf.

no. this info is invaluable. thank you wolf!

Oui! Merci M. Wolf.

No

Central banks have rebuilt the banks balance sheets by stripping hundreds of billions of dollars in interest from savers. At the same time, governmental deficit spending, is simply a scheme for the confiscation of wealth.

Massive leverage was the root cause that drove up asset prices. As the Fed continues to “normalize” liquidity is withdrawn from the system and the overall level of debt shrinks. Money is destroyed.

Asset markets will eventually regress to their long term mean valuation, often over-shooting to low side, before correcting to the average.

This regression to the mean economic fundamental value, is proving to be extremely painful to the markets. Welcome back to reality!

Wait a minute. It isn’t wealth if the Fed created it, which it did. What “wealth”–considering we are all pawns in a Ponzi scheme–are you talking about? Are you, by any chance–Billy Graham?

“Central banks have rebuilt the banks balance sheets by stripping hundreds of billions of dollars in interest from savers.”

Yes, but substitute trillions for billions. Several trillion …redistributed and punishing prudence, especially older fixed income savers. Just had an elderly relative pass away and my guess is ZIRP cost just 1 little old lady who was a simple wage-earner for 50+ years over $250,000 (conservative estimate).

And yesterday Yellen and Bernanke sit there with smug satisfaction acting like celebrities.

Robbing banks gets you in trouble. Robbing for banks and you achieve celebrity status.

Right on!!

And based on the effects of the wailing and gnashing of teeth on the Fed, it appears that the “great” unwind will turn into a small, snail paced untightening. As evidenced by statements from the Fed board members this last week or so and the chairman today. The dropping stock market and the president’s threats have begun to get to them. I don’t think they have the courage to let the air out of the bubble at a rate fast enough to prevent the bubble’s eventual bursting.

It will matter not what the Fed does going forward. Conditions have moved beyond their attempted control, or for that matter the Treasuries control.

For the past three plus decades, the markets depended on the Fed put. When stocks went down, bonds go up. Each time the Fed came to the rescue by cutting interest rates and goosing bond values.

The present market participants are due for a big surprise, in that this stock/bond relationship has ended. The conditions that made the Fed put possible have changed. The conditions that exist today, are now the opposite of what has been. The markets are now facing the double whammy of a combined, stock and bond bubble meltdown.

So it matters not what the Fed does. The myth of their “put” is dead.

The Fed has long put on a “bad cop and good cop” show, chiefly to get politicians off their collective back. In reality I am pretty sure they have already set a course they intend to follow long-term unless there’s some catastrophic credit freeze event: they could not care less about President Trump hammering away on Twitter or the pathetic temper tantrums by supposedly grown men and women.

These guys are not Greenspan or even Draghi.

However remember what the great Marx (Groucho, that is) said “Politics are the art of looking for troubles, whether they exist or not, diagnosing them incorrectly and applying the wrong remedy”.

The monetary policies we have suffered through the past decade are the result of this. And make no mistake about it: the Fed knows fully well they cannot afford a full scale recession because it would mean losing control of monetary policies to the same kind of people that got us (and them) into this predictament.

But stock and bond prices deflating from their obscene 2018 heights are not a recession regardless of what Wall Street says. Again: these guys are not Greenspan or Draghi. They won’t back down just because the Wall Street Journal editors told them to.

The steady balance sheet reduction and the small but steady interest rate hikes are the price to pay to avoid politicians (and those who voted them into office: those expensive SUV’s and those obscenely overpriced concrete cubes are bought on credit) from come charging in guns blazing to the sound of pans being beaten and cause us all more problems.

Rest assured the Fed is watching very intently what’s going on in Europe, where the ECB gave in to the collective temper tantrum originating from stock market traders, automakers, real estate speculators, big exporters etc and now it’s left with an economy that’s dead in the water and zero monetary tools left. More stimulus? They have already done it: it worked for about a couple of years and all it achieved was more distortions that now will have to be purged out of the system or added to the “to be bailed out for the next decade” list.

While this so called “qt” obviously reduces the Feds balance sheet , it is not a reversal of of QE.

By not replacing maturing notes , the FED is engaged in a double barrel of front end tightening . This contributes to all types of distortions with short term rates, while at the same time encouraging long term rates to trade at yields too low. This is also a major if not the major factor in yield curve inversions.

If the Fed actually started to sell those securities that they purchased under QE , pressure would be reduced on the front end, long term bonds would decline and yield realistically higher rates and talk of a yield curve inversion would disappear

A huge factor in the yield curve inversion is the shift by the Treasury Department toward issuing securities with maturities of 5 years and shorter, and back off issuing longer-term securities such as 10-year notes. This has been a well-communicated shift early in 2018, and they’re doing it, issuing truly massive amounts of 5-year and shorter debt. This drives up yields at the shorter end, and by not issuing enough 7-year plus notes and bonds, it causes supply bottlenecks and lower yields at the longer end.

It’s as if the Treasury Department wants the yield curve to invert, in order to force the Fed to back off.

Powell mentioned the issuance problem during the press conference after the last meeting. He is fully aware why the Treasury Department is doing this.

Instead of “Left hand” vs “Right hand” sometimes it looks like the different branches of the USA government are all heads of the same hydra that want to eat each other.

Speaking of many headed hydras, did we forget the last great president that killed such a beast? Certain powers would like to rewrite history and prefer that we forget what Andrew Jackson’s Bank War was all about. But lets not kid ourselves. If you think France is bad with the yellow vests rioting, imagine heavily armed yellow vests. That is the picture that will be painted when the powers that be drop the ball here in the US. As they say, it ain’t gonna be pretty.

As a consequence of their focus on short-term debt (thereby alleviating the effects on the long end and mortgages), it turns out they have to rollover more than $4T in debt in the next 12 months. This will continue to pressure the shorter-term interest rates.

Great. So not only are Trump and the Congress spending lots of money that they don’t have, but they are financing it with short term loans.

With long term rates still well below historic levels, and with a tiny premium to be paid in terms of a very slightly higher interest rate for the long term bonds, this of course makes no sense at all. Like everything else those con-people and crooks do.

Not to mention there’s no demand for treasuries on the long end.

I have a question tho- if the FED takes a loss on 10y and 20y treasuries, are not the tax payers on the hook for that?

Remember the Fed can create money (Federal Reserve Notes) out of thin air. It did this when it bought the Treasuries in the first time place. When it sells them the money goes right back where it came from – nothing.

Kasdour,

The Fed gets paid face value when maturities roll off. So if it paid face value for them, there will be no gain or loss.

The Fed bought numerous long-term Treasuries at a discount in the market as yields had dropped from the time they were issued. So it makes money on those securities when they roll off because it gets face value.

On the other hand, it will lose money on securities it bought in the market at a premium. These gains and losses are not huge, considering the size of the balance sheet.

The Fed likely raked in $100 billion or so in 2018 in income from the securities it holds (we will get this number in a few days). And gains/losses from the roll off are minor compared to this interest income.

The bigger issue is the amount the Fed paid the banks for IOER. This may be around $35 billion in 2018 (we will also get this number in a few days). This comes out of taxpayers’ pockets because the Fed remits most its “profits” to the Treasury Department, and the money it paid the banks on IOER is money it won’t remit to the Treasury Department and the taxpayer.

While there is about 80+ percent tilt on the less than 1Y weekly auctions, TBAC says that the average age of marketable securities is about 69.2 months as of 9/30/2018. It was below 50 in 2008-09. So, the average maturity of marketable debt outstanding is getting OLDER.

Surprising.

I’m not sure what to think of the yield curve inverting at the 1Y term.

There’s more 2Y to 7Y auctioned that 1Ys. Maybe that’s why.

You’re looking at the average maturity of all securities currently outstanding. These are mostly securities issued before 2018, before this shift took place.

“This drives up yields at the shorter end”.

I must be missing something here …the 3 month, 2 yr and 5 yr Ts have almost identical yields between 2.4 and 2.5%…and all are also about the same as the Fed’s overnight rate.

If you compare yield on the 5 yr. and the 30 yr going back a couple of years you will see it pretty clearly:

At the beginning of 2017 yield on the five yr. was 1.94%. At its high yield just a couple of months ago it was 3.09%. 115 basis points higher than it had been 22 months previous.

At the beginning of 2017, yield on the long bond was 3.05%. At its high yield just a couple of months ago, it was 3.45 %. Only 40 basis points higher over the course of 22 months and during a hiking cycle.

That’s news to me, although not entirely shocking they would pull a stunt like that. Perhaps it won’t effect Powell’s decision making but will it affect everyone else’s I wonder.

You know, bank’s business is borrow short and lend long. If the yield curve inverts, banks hurt. FED is the mother of all banks. If Trump can NOT do anything about the mother, he can hurt the children. Art of the deal.

This is hilarious. Trump wants stawk market to go up, and the way to do it is to let the FED pause. In order to let the FED pause, Trump asks Manuchin to front run FED at the short end and force the FED to pause because everybody is agahst at the inversion and since FED is data dependent, yield curve inversion could be part of the decision making.

So could the Fed come up with another Operation Twist? to target the middle of the yield curve. (That would require some coordination with Treasury?) In Powell’s remarks Friday he praised Yellen and compared the current situation to 2016.

Wild!

the goal here is to “normalize” without creating a liquidity crisis. if i was the fed, i would slow down the rate hikes, because that’s what makes the headlines, while continuing to roll off the balance sheet.

I’d accelerate rates hikes. I would have been where we are 5 years ago, in 3 or 4 hikes.

Or the FED could simply have allowed rates to normalize freely and naturally, that is, if the FED’s objective is to promote economic healing and inclusion on all socio-economic strata. But who are we kidding?

I postulate that any monetary policy the FED acts upon is predicated on the continuing expansion of the credit markets. In terms of money and profit centers, these very markets have supplanted industrial ambition with financial engineering, turning once productive companies into hedge funds and asset stripping operations.

If that is case, and it probably is the case, then raising rates quickly would be disastrous and don’t ever look to the FED to do that. Raising rates even gradually “to prevent a liquidity crisis” simply provides cover for the FED to cut them again when the credit market(s) face any existential threat to their expansion.

Of course it is – it has to be when you’ve de-industrialized and decided to base your economy on debt-fuelled consumption and speculation [easy, lazy way to build an economy] rather than production and export [requiring patience and planning].

What other route can there be apart from further credit expansion, given that perpetual ‘growth’ is required..?

In reality, of course, the economy is now mirroring that of Japan’s in the early 90s – and will now be permanently on life support [corporate welfare ie. socialism for the wealthy], as there can be no other end game for a system that requires perpetual growth, but perversely also constantly seeks to pay the vast majority of people less and less.

The Fed must perform a balancing act with smoke and mirrors that maintains the wage slave / debt based system.

The trick is to make the wage slaves believe they are getting ahead, but at the same time make sure they die broke and that their entire lifetime of productivity only goes to support the elites at the top of the food chain. Their tools are inflation and manipulation of asset prices. Creating asset bubbles induces the masses to buy assets on credit, deflating the bubble induces them to sell those assets at a loss while retaining the debts. Economic cycles are simply the masters sheering the sheep.

I don’t dispute that.

As a solution, I think the Fed should be required to look at the New And Improved True Inflation Measure.

The New And Improved True Inflation Measure will include:

1). The Dow Jones Averages

2). The NASDAQ

3). The S&P 500

4). The Russell 2000

The Fed will be required get concerned and perhaps enact interest rate increases any time these indices rise over 2% annually.

The Fed will also be required to consider policy changes if wages increases dip below 2%. At that time, the Fed will be required to take measures to increase wages.

The Fed will also be required to use Labor Participation Rates in calculating unemployment. The Fed’s job will be to increase employment.

Having grown up as a kid in Minnesota, I have vague memories of the News (which at that time was not concentrated as it is today by the Telecommunication Act of 1996 allowing mergers of media outlets into a hand full of mega corporations with agendas that now distort are news and fake it up), so I really the News going on a lot about Humprey-Hawkins REQUIRING the Fed to focus on unemployment and workers wages.

To my knowledge, Humprey-Hawkins still requires the Fed to do this.

Why does the not not obey this law?

I’m shocked – SHOCKED that gambling is going on in the establishment called the Fed!

“”In terms of money and profit centers, these very markets have supplanted industrial ambition with financial engineering, turning once productive companies into hedge funds and asset stripping operations.””

But that has been THE policy for decades! It creates:

A service Economy

Disappearing middle class

Super Wealthy Diletantes

Politicians Milking the Citizens

etc. etc.

A way out is to supplant the Consolidation of Capital in the hands of the Few, with Vibrant Economy, Energy Production,

Widespread wealth—ie—very large middle class—-70% of population.

Forgot to mention I majored in Pol Sci—-then put that to use as a Gen Contractor for 35 yrs……no economics, but then if you want several differing opinions, just ask an Economist.

Seems appropriate that the last four letters are ‘mist’

@ M. Eiford

To understand what an economist is you have to return to the root of the word economy, which is essentially a philosophical or moral approach to the management of wealth. For example (slightly clipped version)

https://www.academia.edu/3375908/Oikonomia_Redefined

So it really relates to household (in the wider sense) management, and is also companion to orthodox theology.

Hence “an economist” is a bit of a vague concept itself , meaning along the lines of say “a theologist”… someone who examines and hypothesises on theology maybe.

However to practice an economy is a very real concept is it not ? I don’t think you have to be “an economist” to do so, nor even “an economiser”, just working working with moral boundaries, common sense and a decent measure of reason.

You cannot expect others to provide those for you.

“Or the FED could simply have allowed rates to normalize freely and naturally,”

The U.S. Government granted a Monopoly License to a Central Bank- the Fed. That ended all “freely and naturally” occurring interest changes and liquidity.

Baker, Spending money we don’t have is largely a bipartisan activity, i.e. there must have been a continuous supply of con people for quite a while.

One thing that cannot be disputed – we have the politicians we have elected. Oh, but some will say I didn’t vote for that “side”, i.e. simply blame a “side”, which has allowed the con to continue.

Every time Mr. Richter says ‘QE,’ a kitten gets a ball of string.

the New-Era theory of valuation: dividend discount model

The dividend discount model caters to speculative frenzies.

in a world of fiat money, the interest rate is controlled by the central bank.

it becomes clear that the Fed exerts an enormous influence on stock prices and valuations if and when investors make use of the dividend discount model.

There are two important ways through which the central bank and its effectively inflationary machinations influence stock prices.

First, a lowering of Fed interest rates reduces the discount rate with which investors discount expected future dividends, thereby increasing the “fair” values of stocks.

Second, lowering the Fed interest rates brings down firms’ credit costs. This, in turn, lowers firms’ interest expenditures, translating into higher profits, thereby also increasing a firm’s present value and thus its stock price.

Artificially lowered interest rates cause consumption and investment to go up and savings to go down. The economy starts living beyond its means and is put on an unsustainable path. The credit-fueled economic expansion can only be upheld if and when the central bank succeeds in pushing interest rate to ever lower levels.

central banks’ inflationary machinations lead to a squandering of scarce resources and cause a great deal social and political problems. As Ludwig von Mises was well aware of the consequences of the boom. He noted: “The boom produces impoverishment. But still more disastrous are its moral ravages. It makes people despondent and dispirited. … In the opinion of the public, more inflation and more credit expansion are the only remedy against the evils which inflation and credit expansion have brought about.”

As soon as firms realize that their profits fall short of expectations, they cut production. Jobs created in the boom will be lost. The artificial boom collapses.

https://mises.org/wire/how-central-banks-stoke-stock-prices

“The Fed Giveth, and the Fed Taketh Away”

It has been seventy years since Mises moved to the US and became the spokesmodel for a certain political economic slant.

When if ever did anything Mises propound upon ever come true in actual fact, supported by data? Isn’t his theory a kind of Teutonic wishful thinking for a morality fairy tale that ends with some catastrophic event at which his followers get to say “neener neener neener hyperinflation!”

It seems more likely that we will stagnate, our institutions will try to behave according to their mandates, and the next technological revolution will come and save the world (Beanie Babies will become currency! Bitcoin!) until it sours and we start looking for the next big thing or begin speculating in climate change futures?

Does the recent increase in “Reverse Repurchase Agreements” on the Fed Balance Sheet sanitize or somewhat soften the blow of this months QT ?

SecondMouse,

Good question. I’ll give it a shot.

In terms of a five-year time frame (used with the charts in the article), the recent uptick in reverse repos is rather small. They’re down by half from their peak at the end of 2016. Also, the amounts are very volatile, with huge jumps and declines, so I don’t think that the recent moves had all that much impact.

Here is the long-term chart:

https://fred.stlouisfed.org/series/WLRRAL

In a reverse repo or “RRP”, the Fed borrows money from primary dealers.

So in effect this reduces liquidity or money in the market.

December had on Rollover (SOMA) purchases but had a RollOff of 18,209,480.4 (in thousands). The Fed will probably reduce the excess reserves of banks by the same amount (meaning less to IOER).

So the dealers get CASH (during RRP) and loses CASH in terms of less IOER during Rolloffs. But is it a wash? 2.4% of 18.2 Billion is about $437 million LESS Cash from IOER. But on December 31 and January 2 there were 41.84 Bil. and 19.481 Bil. of Reverse Repo. So that alone is more than 60 Billion of extra LIQUIDITY or MORE Cash into the system. It is more than a wash but for 1-2 days only.

You can see reverse repos here:

https://apps.newyorkfed.org/markets/autorates/tomo-results-display?SHOWMORE=TRUE&startDate=01/01/2000&enddate=01/01/2000

This is excellent exemple of manipulation by central banks. Created problème and destroy problème. Created terorist and destroy terorist.

QE was feared to cause massive inflation, but it didn’t.

QT is now feared to cause massive deflation (bursting of the everything bubble, etc), but will it?

Everyone in 2011 piled into gold thinking it was only a matter of time before the QE money printing started a hyperinflation, but that trade fizzled.

Now, people are crowing that QT will cause a collapse in “everything”, and what do you want to bet the consensus will get it wrong again.

Where is the trade in this????

Going to all cash??? Doesn’t seem right, with real inflation near 3%.

Going to gold???? Doesn’t produce an income, and people worry the market can be manipulated by the fed.

Going to short term treasuries??? Maybe.

Going to long term treasuries??? Seems logical, but you could get killed if rates reverse.

Keep a well diversified portfolio, and rebalance??? Seems to be the only choice that makes sense, even though “everything” is supposed to collapse with QT.

QE did cause inflation in financial markets and on main street in some areas like housing, art, classic cars etc. and QT is causing deflation in asset prices but I agree that it doesn’t necessarily mean a collapse. There are many people spreading doom porn to sell books, subscriptions, precious metals etc. Doom porn is very profitable and contagious.

If enough people believe that a collapse is going to happen then what actually happens doesn’t matter. Gold and silver are rising for that reason, the miners too. It’s an issue of monitoring perception rather than reality, you just have to keep a close eye on the situation so you don’t get burnt. So yes I think the PM space is the place to be right now but watched like a hawk.

QE did cause inflation, that is why stock, bond, and real estate prices inflated. It did not cause consumer price inflation, because Joe Sixpack did not get the money.

We now have an everything bubble in assets. Reversion to the mean will take care of that, at some point.

Dennis…do you consider the price of Food part of the consumer price inflation? I can tell you that with a family of 4 the cost of going to the grocery store has increased dramatically on all food items…

“Going to gold???? Doesn’t produce an income, and people worry the market can be manipulated by the fed.”

It IS being manipulated and not by the Fed:

https://thedailycoin.org/2017/06/03/deutsche-bank-trader-david-liew-rats-manipulation-lousy-jobs-numbers-launch-goldsilver-higher/

Wendy,

With these two statements/questions, both correct in a way — “QE was feared to cause massive inflation, but it didn’t” and “QT is now feared to cause massive deflation (bursting of the everything bubble, etc), but will it?”– you are conflating two different types of inflation.

You’re correct, QE did not cause consumer price inflation. But it caused asset price inflation (stocks, housing, commercial real estate, bonds, etc.).

So QT will likely not cause consumer price deflation. But it is already helping along the current asset price deflation (but there are many reasons for it, such as inflated asset prices, that would on their own trigger asset price deflation).

And, there is another QT of sorts going on: it’s called RMD’s. The Boomers are starting to hit 70.5 and this parallel form of QT has really just begun.

I really think the new model will be a Japanification of the Western World. The Boomers sell Assets and the FED & other CB’s just buy them up.

Also, when Folks retire, they tend to spend less-way less. In the beginning of most People’s Retirement, though, they actually spend more which is in the short term inflationary.

On another note, how does one know if there has been a response to their comments on here without going back and tediously looking through the comments section?

So, my next question is:

If assets continue to roll of the balance sheet, but the FED pauses interest rate increases, is this still considered QT or another form of QE?

Is it possible the have the Ray Dalio “beautiful deleveraging” by balancing the QT of asset balance sheet roll-offs, with a pause or a slight dip in interest rates going forward? The Dalio portfolio suggests 40% long term bond exposure, but this seems nuts to me.

And again, where is the trade in all of this??

I want to make money, or at least not lose money, so going into cash (short term T-bills) is the only option? Is the recent rise on gold a suckers rally, or a real bankable trend? Is bitcoin really dead now that all the non-believers have left the room?

Somewhere, there is an asset class that will turn out to be the best investment for 2019, but in all the fog, I cannot see it, and when I do, it will be too late to get in.

Wendy, here is my take. I do a W2 job to make money. I ladder 1 year treasuries to try to defend against inflation. At the same time, I am sick of these digits in the bank that are being manipulated into something I do NOT trust. There is 20% of me that do NOT want “money”, I want something nobody can do anything to it and that is GLD. Even GLD can be converted into “money” when things gets tough, so I get CEF. I understand to hold physical, I need to store AR15 or AK47 as well, so I do NOT bother.

Wendy I believe all your questions were answered in the December 16, 2018 WOLF STREET REPORT. Go to main page and click achives on bottom left.

Wendy:

Everyone in 2011 piled into gold thinking it was only a matter of time before the QE money printing started a hyperinflation, but that trade fizzled.

The thing is, UBS and JPMorgan Chase, (et al?) have been manipulating the COMEX and NYMEX since 2009 so it impossible to discern any fair price for PMs on these exchanges.

In his guilty allocution, one trader stated in court that he learned this deceptive trading strategy from more “senior traders” at his bank. He about to turn states evidence.

so much for that rogue trader defense.

Kim

Wendy

Jan 5, 2019 at 8:50 am

QE was feared to cause massive inflation, but it didn’t.

Um, yes it did, stocks and housing have hyperinflated

They are already significantly slowing down the QT. Looks like they rolled off 18billion instead of 30 of treasuries this month, so that is a 40% reduction which is significant in the already small baby steps they are taking.

At this pace the whole program will end next month.

Forget about it,

No. Please read the article before posting nonsense like this.

The article explains this very thing. And it explains why only $13 billion in Treasuries will roll off in January. The reason is that only Treasuries that mature in that month can roll off. The Fed’s Treasury maturity schedule is posted on the Fed’s website. You can check the amounts of Treasuries that will mature in future months. This is totally on schedule. You can check for every month in future years to find out how much will roll off that month. This is totally on automatic pilot.

https://www.linkedin.com/pulse/why-has-global-liquidity-crashed-again-michael-howell/

If you can get to the conclusion notice how the contemporary view of QE and QT are reversed.

Wolf, any way you can publish the Fed Total Assets chart (top of post) going back to 2010 or so. Picture worth a thousand words, and I’d like to see the scale of reduction to date to the total increase in Fed assets, not just back to its 2014 equivalent.

Thanks. Amazing info.

Sean,

This would be totally misleading because the Fed’s assets always rise roughly in line with the liability, called “currency in circulation,” (on the other side of the balance sheet) that has to be balanced with securities on the asset side.

“Currency in circulation” is physical cash, called “Federal Reserve Notes,” as it says on every dollar bill.

When QE started, there was $880 billion of “currency in circulation” on the liability side, and about that much in Treasury securities on the asset side.

Now there is $1.72 trillion of “currency in circulation” on the liability side. So $1.72 trillion in Treasuries on the asset side would currently be the MINIMUM.

Currency in circulation is based on demand for currency that is distributed via the banking system. Since the Financial Crisis there has been a lot of demand for physical dollars globally, with people hoarding this stuff. The Fed needs to see to it that there is always enough physical currency in the banking system to meet customer demand for it.

So an appropriate long-term chart would be one overlaying Treasury securities and “currency in circulation.” And I will likely put together an article about this someday. Good idea. Thanks.

It will show that in the not too distant future, as currency in circulation continues to rise, the Fed will HAVE to stop unloading Treasuries, though it can completely unload its MBS.

Wolf, what does all this mean for ‘main st’ (i.e. small businesses) or the average working American?

I’d say it’s a mixed bag. And fairly complex and layered. Here are a few thoughts:

Small businesses and average working Americans in most parts of the US who don’t hold financial assets such as stocks or bonds will likely barely notice a gradual 50% decline in the stock market if they ignore the to-do in the media.

Some specialty professions will feel the pain. For example, I have a friend who has a small law practice that specializes in corporate transactions (such as M&A), and everything that goes with it. She told me that when the M&A boom ends (and she sees it ending), her business will take a hit. But she is not the average American worker bee. Her bill rate is around $500 an hour.

When QT bleeds into housing, workers may notice it in terms of slightly less un-affordable housing (rents and purchases). And they will welcome this. QE has jacked up the cost of housing. QT and higher interest rates might bring a little relief.

On the other hand, homeowners who bought near the peak in prices (depends on the local market) will feel the squeeze if they’re trying to sell the home.

There are some areas in the US, such as San Francisco and Silicon Valley, where a large decline in the Nasdaq will translate into VC funding drying up, and into money-losing startups shutting down in large numbers. People who work at these outfits will have to go find real jobs somewhere else. But the Bay Area is used to this cycle. It’s ugly. It entails effects such as a shakeout in restaurants. But it happens regularly, and is predictable. It cleanse out the excesses and deadwood. And makes room for another boom later. Boom and bust, always.

Since this is “Everything bubble”, what should we name the yet to arrive bubble?

The bubble to end all bubbles, but you can shorten that to Weimar if you prefer.

I’m still having trouble understanding how QT transmits it’s effects into the economy. QE I think I get: when the Fed buys treasuries and mortgage bonds it puts currency in the hands of investors that have to find another income-bearing home for it in stocks or real estate. QE also keeps interest rates down by creating higher demand (prices) for treasuries, hence lower yields.

But with QT, by allowing bonds to roll off the balance sheet without replacement, there don’t seem to be any agents involved except the treasury and the central bank. How does this affect anything? Its probably obvious, and I’ll figure this out eventually, but can anyone help?

In basic terms, the QE unwind drains money from the market like this:

Step 1: When the Treasury securities that the Fed holds mature, the Treasury Department transfers the money to the Fed. If the Fed doesn’t buy other assets with the money, that money just disappears.

Step 2: Since the Treasury Department doesn’t have the money to pay off maturing bonds – as the US government runs a big deficit – it raises this money in advance by selling new bonds at regular auctions.

Step 3: By buying the new debt that the Treasury Department issues, the bond market gives its money to the Treasury Department that the Treasury Department then gives to the Fed to redeem the Fed’s maturing bonds.

Step 4: Because private bond buyers replace the Fed by the amount of the QE unwind, these bond buyers have sell something else to raise the money to buy those bonds.

It’s by this mechanism via the bond market and the Treasury Department that the QE unwind drains “liquidity” – or whatever else you might want to call it – out of the broader markets.

Wolf,

Am I correct in saying that when QE first began, the Fed purchased both treasuries and MBS from the big banks , and in return gave cash to those banks who used it to provided credit to investors who then bought assets (i.e. stock, real estate.).

So prior to quantitative tightening (QT), the FED continued additional purchases of bonds from those same same banks as the MBS and treasuries matured, thus providing them the ‘needed’ credit for continued asset inflation.

This would seem to make the actual amount of QE over time far greater than the ‘amount of debt’ on the Feds books at any given time.

Therefore, now that QE is being reversed, all assets must adjust downward, for an amount comparable to the initial QE+ recycling (which is a lot).

Or am I completely wrong?

Wow! Excellent, Thanks for taking the time to explain things in a way that makes sense! I have a degree in Engineering and many years of studying high level math

and i still haven’t understood QE and QT and all the monetary and Fiscal processes! But.. it’s coming..thanks to your articles and taking the time to explain it in depth!

I try finding it on the internet, but i can’t find a clear in depth explanation. But you tell it, good..and Free!

I think i may have this down correctly..if anyone can just verify:

In QE: The Fed buys the treasuries and MBS from the commercial banks and private institutions (?) . This is the Feds base money and it gets recorded as bank reserves electronically (not physical cash ..unless they request it).

This is called open market operations. These purchases of treasuries and MBS are recorded as the Feds Assets.

The currency in circulation though may not rise at all cause the Fed paid digitally as bank reserves to buy them, and its only if the banks request cash form the Fed for the Bank reserves that it will be record as cash in circulation.

I am not even sure if the Fed buys treasuries directly from the Treasury dept. or if they just buy from the banks? And if they do buy directly from the treasury won’t they have to pay in cash cause the treasury needs physical cash to pay there bills?

Now, that’s what I think is correct, but I am not sure? I am hoping if someone reads this and can tell me if it’s correct then i will save it in my LT memory and not wonder if it’s right or not! Thanks to whomever lets me know!

Wolf,

Did excess reserves have a roll in inflating asset prices? Were they used as collateral for the banks to purchase financial assets?

I do not pretend to understand all the ramifications of QE and QT. I think it will all come out in the sewer pipe at some point!

However, I am most curious about the U.S. federal debt at over 21 Trillions of $$. Surely this will increase over the course of the next several years no matter which of your two conservative political parties has control. But I cannot imagine that that $$ will ever be repaid, especially since the Baby Boomers have usurped their role in providing lots of $$ through taxes that the next generations cannot hope to duplicate.

The QE pumped up the economy, and created a lot of useless activity. Now that it is being removed, the economy will start to shrink, and the howling for a rate cut will grow. A decent thing would be to do a one time economic write-off due to fake QE effect, and start counting from there. That way the economy would keep growing, and the interest rates could keep going up. I have no idea how to do this, but I am sure Dr. Bernanke is on hand to figure it out.

Peace dividend ! (Like they used to promise every 24 months)

And who will take the brunt of the ‘one-time’ the middle class for sure, not the Dilettante Wealthy.

I wonder, is there a similar chart showing a natural monthly roll-off of the balance sheet, or even a yearly cummulative?

Step 1: When the Treasury securities that the Fed holds mature………What are they?, what do they consist of?.

For example are the MBS part of them originally the worthless multi tranche bonds and the associated rubbish of CDO and CDS that the treasury brought from the banks and have made seemingly acceptable by re-namig to MBS with the implied backing / authority of the Treasury who held them for a while?, in which case in the end the fed is taking this crap from the banks via the Treasury and destroying them continuing with the bank bailout third hand, or am I getting this wrong??

Can you write an article when you notice that the FED has stopped QT and reversed to QE? Or is there a link you can post so we can see it ourselves.

Thanks Wolf, great articles.

I cover this every month, and have been from the day it started, and will continue to do so. So yes, we will see right here what the Fed does — if it sticks to its plan and lets the QT run on autopilot, or if it switches from autopilot to manual lever-pushing.

Autopilot is stopping at March 19-20 meeting, and QE5 likely starting July 30-31 or September 17-18… The street pressed and Powell blinked. They are gonna keep credit frozen in Junk’s until defaults to force Fed hand, kinda weird the Federal Reserve works for the Big Banks, given how they try to portray themselves

High Yields maturity’s of January-Feb will defaults, credit froze in junk and there is no way out except defaults, the fed is clearly aware of this in there November Report, but Fed under-estimated how quick it can dry up in there when they aren’t buying everything

Btw, your site is Money… Keep up the good job

QE5? Whoever thinks this will be in for a rude awakening. Wall Street’s wet dream. Not going to happen unless something really big breaks — and I don’t mean a 30% sell-off in the S&P 500 … that’s not big, that’s fairly common.

Ignore the FED heads double talk. Watch what they do not what they say.

Powell’s early blink was so telling at the same time he was being pressured by the street and overt firing threats from Trump. So, pretty historic pressure.

The rolling off process seems to have slowed from its delayed, already meager, and predicted pace; which is tantamount to a QE4(b) and sends a signal for a willingness for more QE support.

The Fed wouldn’t dream of pulling the punch bowl; perhaps dabble w/ the recipe. Nothing to worry about.

Stan Getz,

“The rolling off process seems to have slowed from its delayed, already meager…”

BS. Read the article before posting this nonsense.

Interesting Wolf… You think Powell has a high pain threshold ?

With the Corporate Bond Defaults starting very soon, how long will the Fed let it drag ? Regardless of what happens with tariffs or Brexit, if nobody is buying new Corporate Bonds, with maturity’s due it’s a no brainer what happens starting end January.

Please let me know your take on this, with 95 % + algo trading, they can sell off into oblivion within a few weeks nowadays once panic really sets in

Reading this blog is like having a free course in macroeconomics and money, credit and banking.

So I make sure I occasionally give a few bucks to encourage continuation. For those who haven’t thought about this, to see how, look at the top banner under how to donate. The information from Wolf, and from his remarkably well informed followers is well worth the money.

curiouscat,

THANK YOU!! In forbidden all-caps :-]

Wolf,

Thought this month was one of the biggest roll-off months of 2019?

$18.2B in Treasuries rolled off on Jan 2nd. Another $1.8B slated to roll off on Jan 16.

On the MBS side:

$18.3B rolls off Jan 16.

$ 3.4B on Jan 23.

$ 8.9B on Jan 30.

Cannot find on St Louis Fed website the incoming maturity’s of Federal Reserve, would you mind linking it ?

Thank you

Ricky Tan,

Here you go:

https://www.newyorkfed.org/markets/soma/sysopen_accholdings.html#tabs-1

Well, December was only the third month in cruising speed (up to $50 billion). So you can’t compare it to the ramp-up months. In December $34 billion of up $50 billion rolled off. In other words, $16 billion didn’t roll off. In November, $46 billion of up to $50 billion rolled off, including $30 billion of Treasuries, at the max-out level.

As of 1/4/19 implied inflation rate by Treasuries

5 year-%1.57

10 year-%1.75

30 year-%1.80

This in a future bond environment of increasing deficits in ALL developed countries( including China),where an increasing number of companies are zombies and need to borrow more at higher rates just to service their current deb, where default of some kind is inevitable in numerous states and municipalities, where the convexity in dollar terms is gigantic and where the largest US creditor (China) will inevitably sell some of its Treasury horde in the ongoing trade war

I found it interesting in Volcker’s autobiography, “Keeping At It” (2018), he said the new red line for policy: a 2% rate of intertest in some carefully designed consumer price index is acceptible, even desirable, and at the same time provides a limit. He is puzzled about that rational and he knows of no theorectical justification. It is difficult to be both a target and a limit at the same time. And a 2% inflation rate would mean prices double in little more than a generation.

I must say Volcker used his position to help our economy without trying to promote himself, unlike The Great Maestro- Greenspan, who always caved in to Wall Street. So far I believe Powell is also not caving to Wall Street’s crying and trying to get assets back to reality without crashing the Main Street economy.

Hi Wolf,

not able to understand following,

total QE unwind = $402B

Treasury security unwind = $243B

MBS unwind=$133B total=243+133=376.

how to explain (402-376)= 26B difference

Is there some other component

Also, last total unwind was $374B (https://wolfstreet.com/2018/12/06/feds-qe-unwind-reaches-374-billion-balance-sheet-normalization/)

so, difference from last month ($402B-$374B)=$28B

But Dec TS+MBS unwind = 34B

So, how to explain (34-28)=6B difference

There are other components on the Fed’s balance sheet, as I have explained before, including in the article that you linked. They include the impact of activities beyond Treasury securities and MBS, such as swaps with other central banks. You can see this by the fact that total the balance of total assets is always larger than the sum of Treasury securities and MBS.

I report on all three: the total balance sheet reduction, the reduction in Treasury securities, and the reduction in MBS, in case people wonder – and they do, as you can see from some of the comments under the older articles — if the assets just get shifted around, for example from the MBS account to another asset account. The way I do it gives you all three numbers, including three charts: total balance sheet, Treasuries, and MBS, plus the total for just the reduction in Treasuries and MBS = $34 billion this time around, which was higher than the total Balance sheet reduction = $26 billion this time around. Other times it’s lower.

Huge rallies in stock and bond prices last week. So if not the Fed, where is the money that the Plunge Protection Team is using to support stocks and junk bonds coming from?

Dip buyers buying stocks? And especially during holiday week when there was thin participation. And what about the big sell-offs? Ha, and this: Each time someone pays $1,000 to buy a stock, someone else receives that $1,000 for selling that stock (minus some fees). What changes isn’t the money, but the buying pressure or the selling pressure.

Precious metals are surging as investors belatedly figure out that the Keynesian fraudsters at the Fed and central banks have lost the plot, and the full consequences of their monetary malpractice, especially their creation of 16 trillion dollars in “stimulus” out of thin air since 2009, will soon be fully exposed for all to see.

Unless helicopter money is instituted as a mainstay in America interest rates will end up permanently negative.

For the first two quarters of QT (Q4’17 and Q1’18) the Fed’s “tightening” through allowing maturing treasuries and MBS to roll off was more than offset by the reduction in Fed overnight domestic repurchase agreements, and thus net liquidity by the Fed to the commercial banking system was actually increasing (by $35B in Q4’17 and $26B in Q1’18). As overnight domestic repurchase agreements by the Fed declined to negligible levels in Q2’18, tightening of Fed net liquidity actually commenced, though at levels quite a bit below those targeted in the Fed’s 2017 anticipated schedule. The actual numbers for Q2’18, Q3’18, and Q4’18 were $93B, $101B, and $133B, below the targeted $90B, $120B, and $150B, respectively. Pressure on financial markets should continue as long as the Fed does not reverse course, though there is a possibility the commercial banking system increases leverage in the system independently while the Fed tightens Fed reserves, as Fed reserves are still enormous and not a limiting factor for potential expansion of commercial bank balance sheets.