Investors are waking up after years of somnolent money-making.

Markets are in a tizzy. They’re finally reacting to the Fed’s rate-hike cycle, the slowest rate-hike cycle in history. It took three years to nudge up the effective federal funds rate from near zero to 2.40% now. Throughout, the Fed has communicated its goals of “removing accommodation” from the “financial conditions” in the markets — thus tightening “financial conditions” that had become loosey-goosey during years of zero-interest-rate policy and QE.

And suddenly, financial conditions in the markets started tightening in October. So let’s see where we are — and how this might impact the Fed’s decisions.

“Financial conditions” is a key term in the Fed’s official communications. For example, in the minutes from the November FOMC meeting, the most recent available, the term was used five times:

- Once, when “participants” discussed the interest the Fed pays banks on “excess reserves” on deposit at the Fed. This rate, it said, provided “good control of short-term money market rates in a variety of market conditions and effective transmission of those rates to broader financial conditions.”

- Two times, when it discussed financial conditions directly: “Participants observed that financial conditions tightened over the intermeeting period, as equity prices declined, longer-term yields and borrowing costs for most sectors increased, and the foreign exchange value of the dollar rose. Despite these developments, a number of participants judged that financial conditions remained accommodative relative to historical norms.”

- Once, when it discussed that its “policy was not on a preset course,” and that it could change its policy in one direction or the other, depending on the incoming data, including “the recent tightening in financial conditions….”

- And one more time, to make sure everyone gets it: “Financial conditions, although somewhat tighter than at the time of the September FOMC meeting, had stayed accommodative overall….”

These “financial conditions” indicate how easy and cheap, or how hard and expensive it is for borrowers to borrow. Tightening financial conditions mean that investors are reluctant to fund high-risk companies. This shows up, for example, as the difference (the “spread” or risk premium) between the yields of risky corporate bonds and “risk-free” Treasury securities.

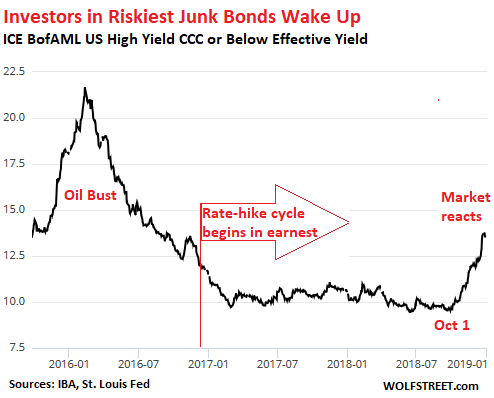

In the riskiest category of corporate bonds, CCC-and-below-rated bonds, just above D for default, yields started surging in October 2018, after being somnolent through the entire rate hike cycle.

The average yield surged in three months from 9.6% at the beginning of October to 13.58% yesterday at the close. In other words, for these companies, the cost of borrowing over those three months has surged by 41%.

Even more telling is the “spread” between the average CCC-and-below yield and the equivalent Treasury yield. It shows how much more investors demand to be paid to take on the extra risks of these junk bonds, compared to Treasury securities.

This spread has widened from 6.7 percentage points at the beginning of October to 11.1 percentage points as of yesterday’s close.

The fact that the spread (risk premium) has widened faster than the CCC-yield has risen over this period is impacted by two factors:

- The surge of the CCC-rated yield from 9.6% to 13.58%;

- The decline of the 10-year Treasury yield from about 3.2% in early October to 2.6% now.

In other words, investors are clamoring for low-risk assets. And they need to be induced with richer yields to invest in high-risk assets. This is a sign that “financial conditions” are finally tightening.

But this spread is still low compared to the Oil Bust when it shot up to 20 percentage points, and compared to the Financial Crisis when it spiked to over 40 percentage points – a sign financial conditions had become so tight that credit flows were freezing up.

So the current spread of 11.1 percentage points is nothing to get frazzled about. But it means that for these CCC-rated companies, the long-prevailing ultra-loose financial conditions have tightened significantly.

The same principle is at work in the category of BB-rated bonds — the highest speculative-grade category (here’s my color-coded cheat sheet for the corporate bond rating scales): The average yield has surged from about 4.1% at the beginning of October to 6.17% yesterday at the close. And the spread to Treasuries has widened from 2.1 percentage points to 3.61 percentage points. In the lowest investment-grade category, BBB, the spread to Treasuries has widened from about 1.4 percentage points in early October to 2.06% now.

So, yields on riskier credits are rising, and spreads to Treasury yields are widening at a good clip. This is exactly what the Fed has set out to accomplish three years ago.

But the well-known lag between changes in monetary policy and its transmission to the markets — typically between 12-18 months – was nearly three years this time around, in part due to the very “gradual” pace of the rate hikes that markets brushed off for the longest time. But no more.

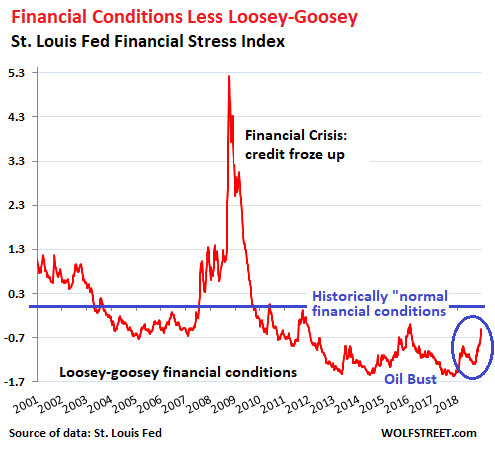

There are various indices that track “financial conditions.” One of them is the St. Louis Fed Financial Stress Index, released weekly, including this morning. It’s made up of 18 components: seven interest rate measures, six yield spreads, and five other indices. A level of zero means “normal” financial conditions (blue horizontal line in the chart below). When financial conditions are tighter than “normal,” the index shows a positive value. When these conditions are easier than “normal,” the index is negative. I circled the recent rise:

Note the enormous spike during the Financial Crisis, when financial conditions tightened so much that credit was beginning to freeze up.

In November 2017, nearly two years after the Fed had started its rate-hike cycle, the index dipped to record lows, a sign of the lag between changes in monetary policies and transmission to the markets.

By “normalizing” its monetary policy, the Fed attempts to “normalize” financial conditions in the markets to bring them back to historical norms. This means making credit more expensive and harder to come by for riskier enterprises. It means risk is getting “repriced.” It means that the Financial Stress Index ticks up to about the blue zero-line in the chart above.

Starting in May 2017, I wrote a series of articles about how the markets were blowing off the Fed. The theme was that the Fed would keep going with its rate hikes until the markets react sufficiently. Now they’re no longer blowing off the Fed. They’re reacting.

So now the question is this: When will the Fed consider financial conditions to have tightened sufficiently to where it can keep its monetary policy unchanged? This point is clearly approaching.

The Fed does not want to trigger another financial crisis where credit freezes up and mayhem breaks out. It just wants to “normalize” financial conditions.

Markets can react wildly, overshooting in both directions. And as we have seen, there is this lag between monetary policy and market reaction to those policies. No one knows yet how much further financial conditions will tighten on their own, even if the Fed just hangs tight.

The Fed’s “gradual” approach has been designed to avoid a sudden market reaction, such as a convulsion into another financial crisis, with all kinds of things collapsing left and right, which would then induce the Fed to once again go haywire with experimental monetary policies that no one can figure out how to undo afterwards without blowing down the entire house of cards again.

[Perhaps the latter part of that phrase is the perplexed state we’re in now.]From the Fed’s point of view, it would be far better if financial conditions tighten in small increments until they’re “normalized” — at which point the Fed could wait until the dust settles and until there’s better visibility. We’re not far from this point, after the recent market gyrations.

The problem that the markets have – and why they’re in such a tizzy – is that investors have been pampered and coddled for so long by central-bank policies that “normal” financial conditions now seem like cruel and unbearable torture. But they’ll get used to it if there is enough time.

How the Corporate Debt Bubble Will Crush Stocks. Read, or rather listen to… THE WOLF STREET REPORT

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The test will come when Powell & co flip to fully neutral with “risks on the downside”. Quite when this public statement will be made is up for grabs… with the determinants being a mixture of economic data calendar, market price action, and fed schedule. (plus perhaps enough time to undo some fed ego).

In a nutshell I don’t think the fed will allow markets to find their own feet.

C Jones

This is precisely the Problem, a replay of the “ 07-08” piss- weak, gutless move that the Fed are experts at now!

Not allowing the “ washing cycle “ to clean and rinse the dirt accumulated in the pricing of securities throughout the “ Greenspan and Co!

Very unfortunate set of circumstances that lead this bunch to such powerful positions, only to wreck havoc in average punter’s lives.

So yeah, the old movie will be screening under new title to the detriment of the

US’s citizens and probably the world financial markets at large.

Your thoughts on this señor Wolf “ for your Cuban audience “! :)

Thank You

Jack

There will certainly be winners in this cycle, and there will be many losers. The hard part is figuring out what to do to be a winner, and not a loser.

Wolf you’re a reasonable man in an unreasonable world. Spreads are wide because stock market sellers parked money in bond funds, pushing yields ridiculously low. Today its risk on again, and yields, and gold, are back down, as money flows into stocks. Financial stress levels are almost back to normal? HYG up 1 1/2% today. Okay maybe there are economic indicators separate from these? How about another

strong GDP number. The gradual rate hike policy is Yellen’s, not Powells. There is no credit crisis, instead the market will seize due to imbalances, should the 10yr go to 5% in a week? Far worse than a credit crisis. How will they unravel that? The untoward reality is that unless the stock market continues lower, we are all doomed.

The Fed should try to jawbone the market higher. If that doesn’t work, they should talk about how they might jawbone it higher. If that doesn’t work, they should schedule more meetings, where they might talk about jawboning it higher. Lord knows the stock market can’t be left to its own devices or god forbid actual price discovery.

Hey look, Fed jawboning and the market rallies almost 1,000 points! Who could have guessed? Isn’t it great having a stock market rigged to go up, no matter what. All we need is this Fed to say something “Dovish”. Heads we win. Tails, we also win!

Time to invest in the jawbone index!

CNBC is explaining the latest market surge (up this time) based on Powell’s remarks and ‘a blow- out jobs report’

Those are opposite factors not additive factors. The lower unemployment goes the less likely the Fed can deviate from its obvious course of normalizing rates.

These explanations make no sense. And in the middle of the chaos some

dolt is is saying that ‘the chart of X looks like it is set for a breakout’.

If ever there was a time to look at so- called ‘technical analysis’, it’s not now. Can anyone point to a tech last week saying Apple is set to drop 10% ?

Then after it did, sort- of- tech Cramer said it had a lot further to drop.

Then today it rallied 5%.

As Louis Rukeyser asked Head Tech Bob Nurock the day after the (not predicted) 1987 23 % crash: ‘So do you still believe in this stuff?’

nick kelly,

“…based on Powell’s remarks and ‘a blow- out jobs report.’ Those are opposite factors not additive factors.”

I’ve been hearing this all day everywhere – it’s hilarious really, for the precise reason you pointed out. It’s like people checked their brains at the door before they stepped into the radio/TV studio.

Employment had been fine for years. And the Fed has repressed rates for years anyway. It’s clear that the mandate for the Fed is to preserve price levels in the stock market. The economy cannot handle a losing market. It’s the tail that wags the dog.

Today is a sad day. The deep water Powell trying to hide got blown out of water and print a 2400 put on his head. All traders saw it. Now Powell has shown everybody his or the FED’s true color and that is, to tighten is to make the capital owning rich to have more negotiation power over labor, kill wage inflation and at the same time,

since the rich own 90% of the stocks, there is a 2400 put.

To have even one bit of hope that the FED will make the rich poorer to equalize inequality OR FED is doing what’s best for the economy is proven stupid. The stand-up Powell turns out is the same.

” Louis Rukeyser asked Head Tech Bob Nurock the day after the (not predicted) 1987 23 % crash: ‘So do you still believe in this stuff?’”

Rukeyser, who memorably hosted PBS’ Wall Street Week until 2002 used to have the experts issue annual predictions. In 2001 one of these was James Grant, whose hanging judge mien then as now added an air of gravitas. Grant predicted Dow 2600.

“2600?!” said Rukeyser in horror.

“Well, I am a bit of an optimist.”

Is a “blow-out” a good thing or a bad one? Not familiar with the term.

IMHO things won’t get back to normal until the levels of debt are back to normal. Best of luck with accomplishing that.

a reader, it’s all about the Debt Cycle & where we are in it. Right now, we are at the end of the Short Term & probably pretty close to end of the Long Term Debt Cycle.

Michael Hudson has some great thoughts toward that end, based on history. Debts that can’t be paid, won’t be paid.

Was looking at my mm statements …. within the last 4 yrs, received a whole, wopping, stupendous .. are you ready ?

34 quatloos …..

Wow ! I’m RICH, I tells’ ya ..

No free Fed Chips for mine or thine, but the conniving, thieving, lying banksters have had Their ill-gotten gain handed to them on a golden sack of skulls … no platter needed !

Guess I’m not corrupt enough to warrent the consideration … like about 80% of the populace, soon to be the 90%, once most of the credentialed class craters.

Sorry, but I’m in kind of a new year’s funk, and the paltry interest isn’t helping my mood … so when I hear about how the poor, frazzled, and whiney investors aren’t receiving their unicorn manna, I just get even moar pissed !

You speak truth. Central Banking Cabal = Parasites of Humanity !

The current Wall St barons are now addicted to cheap money and the Fed pumping huge amounts into the financial system.

Like with any addict, sooner or later they go through withdrawal. To the addict, this can seem quite painful, and the addict will describe this as “hell”. Sane people who are trying to help the addict express sympathy for the addict’s pain, but know that the addict must go completely through the withdrawal to be healthy again so they ignore the addicts pleas for more of the substance, in this case, more cheap money.

Investment grade funds are now suffering from major outflows of liquidity, as investors turn their backs on US corporate credit.

The total amount of consumer subprime debt is now in excess of the amount of subprime mortgage debt, at the peak of the 2007 bubble. Subprime auto loan/lease defaults outstanding, are critically high, with an even higher level waiting as delinquent.

There is no question that there currently exists a lack of liquidity in the system. What is more troubling, is that the assets supporting the debt are no longer worth the loan balance!

There are reports of Chinese officials “inspecting” loan organisations for their involvement in the financial derivative industry. There seems to be a “concern” (fear?) that these financial instruments are not performing as modeled.

When a counter party in a derivative fails, a net position instantaneously becomes a gross position. All that is required, is some small financial entity that has gotten in over it’s financial head, to default on a derivative and its game on! Contagion spreads as dominoes begin to fall, at an ever increasing speed. It can occur very fast.

There is currently a 39% chance (Fed Futures) of 1 rate hike or more in 2019.

And Dallas Fed President, Kaplan, has joined Bullard and Brainiac in requesting a pause or lower.

If Futures signal a 25bp cut, then a recession announcement will follow soon thereafter.

akiddy11, the Fed could even still take a pause and yet keep up with the QT which is a de facto rate hike in itself. Or, they could hike and the commensurately pull back on the QT and end up with both cancelling the other out. That, could literally be done on the QT.

These are the same people who put the chances of one or more rate hikes by the ECB in 2018 at 66% so I would approach anything the future market “says” on monetary policies with a bit of caution.

Also remember the Fed loves to play a game of “bad cop, good cop” these days to keep politicians off their collective back. Short of some catastrophic credit freeze event however it’s highly likely their policy has already been set for several quarters to come.

To quantify the probability of these future events to within one percent is absurd. They seem to come from persons not trained in the tolerance of measurements (not including MC01)

But I’ve seen worse and it’s common. I’ve seen a future GDP growth predicted to a hundredth of a percent! As in ‘we estimate next years growth at 2.55% ‘

They’re quoting a future result, affected by any number of factors known and unknown, as though they were measuring a piston ring sitting on the table here and now.

Well, if I were JP, I’d come out and say that I would raise rates three times instead of two, just to screw with DJT.

Honestly though, a little recession not need the Feds to drop rates anyhow.

As Wolf points out, the market is still way the heck up.

Will a broad China slowdown be the stealth market torpedo while everyone focused on rising interest rates? Commodity prices, hot foreign buyer RE markets, and perhaps a pullback on belts and roads next? Any articles out there on how much of the easy money has come from China in aggregate? Mostly just read anecdotal stuff on overseas RE and belts and roads infrastructure, or on domestic Chinese speculation. How much of a liquidity contagion risk is China aside from slowing market for Apple and the like?

Add the tariff issue on top of those and you’ve got yourself a doozie for the markets to digest. I’ll be sitting on my short term treasuries with popcorn.

“Any articles out there”…

From the South China Morning Post –

Authorities have changed the definition of what constitutes a small business and cut the reserve requirement ratio for banks, to encourage banks to increase lending. The cuts will release 400 – 700 billion yuan.

http://www.scmp.com/economy/china-economy/article/2180585/china-makes-us102-billion-move-aid-slowing-economy-will-it-be

could be china but me thinks it will start in europe. i wish i could enjoy the popcorn but i care to much for the smurfs who will lose their retirement funds. one close friend told me today that he’s already down 50% from his high. i think he was in faceplant, etc.

During Obama’s period of financial repression with cheap/free-money /credit, Wall Street’s fake financial markets grew insanely without any limiting boundaries to infinity and beyond.

When money is “free” people do really insane things with this free money because “free” has no value!

Now that “free” has been withdrawn from Wall Street’s financial markets, some insanity is being slowly removed until it is suddenly removed!

Ah that would be the continuation of the IR policy introduced by Dubya, then, necessary to mitigate right-wing policies of financial deregulation and the subsequent chaos they’ve caused. What short, selective memories people have when it comes to politics.

Go back one more presidential administration and one more fed chairman and you’ll have it.

Follow the money, because we have the best .gov that money can buy….. and political parties should be known as “parties the political class hold on our dime”.

Yes, Right-wing policies promulgated by republicans and democrats. Let’s admit the crime enablers and bands of merry criminals like the citi-bank gang were bi-partisan.

It is Robert Rubin who was recommended for indictment by the Financial Crises Inquiry Board.

But what area is there in the future for real economic activity to expand?

Blowing people up, and trying to keep people alive.

Mark my words these rate hikes are precisely what we need to kill off zombie companies that can only exist because they can pile on more cheap debt to keep servicing their old cheap debt. Wallstreet would have wanted this to go on forever, despite the fact that it would require a detachment from economic reality and I dare say the laws of physics. I will see the day Netflix, and Tesla actually collapse, and I doubt anyone will buy them out. Amazon won’t collapse, but they will feel the heat. Also, someone help, me out here but won’t these rate hikes stymie the wealth transfer from productive actives to the nonproductive financial system?

Agree. Many folks have compared this situation to a drug addiction. In any drug addiction scenario, there has to be an end game; indeed there IS an end game.

The problem with the FED is that it is beholden to the addicts. It is simulateously a producer, supplier and itself an addict.

What a world, what a world. . .

Yes and you’ll also get a zombie country too, just like Japan…same rampant speculation and gambling, same result. The only lesson humans beings learn from history is that human beings don’t learn from history

Why would our leaders learn to change when they are part of the insiders who financially benefit from QE and don’t feel the costs?

It’s a classic economic externality just like a factory making boatloads of money while polluting others downstream. The factory in that case will never “learn” to be a team player, it has to be regulated.

The (soon to be boiled) frog just figured out his fate…

Completely agree with this. The FED needs to stay the contractionary policy course and divest itself (sell) of toxic assets in order to prevent inflation from getting out of control.

Staying the course comports with the situation at hand, however the FED is under pressure by creditors (the FED being a creditor itself), investors, POTUS, banks, et al, to revert to expansionist policy. This is to be expected because if the FED stays the course on contractionary policy, the aforementioned and many intermediary financial institutions will be shown as insolvent. The FED itself will be shown as insolvent.

IOW, it’s not difficult to see what the right thing to do is, but the right thing is the most difficult thing. My prediction is, the FED will not do the right thing.

Wolf, something else in a “tizzy”!

The five year Treasury Note yield is now lower than the effective Fed Funds rate! The overnight indexed dollar swaps forward rate, has now plunged from 3.0 at the beginning of November, to now 2.05

What the heck is going on? Surly volatility has not reached this level?

OutLookingIn,

Part of the problem is that it’s still vacation week. Japan is still closed for New Years (Tokyo will open in less than an hour). There is not a lot of market participation. And the crazy stuff gets blown way out of proportion.

The 5-year being lower than fed funds rate is another sign that the yield curve has inverted at that end of the curve.

Inversions – plural.

The 2, 3 and 5 year Treasury yields are now all below the effective Fed Fund rate. The first time this has occurred since… You guessed it 2008!

Looks like the bond vigilantes are betting that the CB’s will have to step in and buy. If they do, it will crash the yields.

I just updated the article by adding this paragraph:

“Starting in May 2017, I wrote a series of articles about how the markets were blowing off the Fed. The theme was that the Fed would keep going with its rate hikes until the markets react sufficiently. Now they’re no longer blowing off the Fed. They’re reacting.”

Excess reserves and the interest they commandeer must be addressed or the pressure on the top section of short term interest rates will become trouble for the yield curve?

Question: if the FED allowed the securities on the balance sheet just naturally roll off, would it represent tightening or loosening with regard to planned QT? Difficult to tell?

Come on, how many times this week have you heard some wonk talk about the ‘strong economy’, ‘fundamentally the economy is strong’, and because the ‘economy is so strong’ this is precisely the correct time to impose Trade restrictions on China and on other countries that take advantage? (I’m thinking of the economist goof named, Stephen Moore).

This is how strong the economy is. Money and debt has to be free, or everything tanks. Wages need to be stagnant. Young people starting out cannot afford to buy a home. And, it takes two incomes just to get by. Yet, people continually parrot the strong economy propaganda and are apparently unable to critically assess what is going on; until they lose it all or finally realize all they ever had was debt serfdom and a bunch of hype.

Yeah, the Economy is always “strong” at the end of a cycle. Counterintuitively, this is when high equity prices and real estate typically fall. The prices for these assets are pricing in future growth, so that’s one component to these asset prices falling.

“This is how strong the economy is. Money and debt has to be free, or everything tanks. Wages need to be stagnant. Young people starting out cannot afford to buy a home. And, it takes two incomes just to get by. Yet, people continually parrot the strong economy propaganda and are apparently unable to critically assess what is going on…”

Totally agree with you. The economy is NOT strong and hasn’t been for about 10 years.

Growth rates past 10 years have been historically below par, and that’s coming off a deep recession which should have allowed for a huge spurt of pent up growth at way above average rates…had half way sane polices been followed.

We’ve witness the weakest “recovery” these past 10 years than it what…70 yrs?

The economy is only strong for the rich and rich gigantic corporations. And the “low” unemployment rate was achieved by suppressing wages so low, the labor force shrank from attrition.

Timbers, I put strong in quotation marks. I agree that this went on waaaaay too long with Bernanke & Yellen wanting to goose the Economy. ZIRP & QE were sound monetary policy tools that were needed in ’08-09, but should have been phased out once the economy was back off Life Support and not abused like they were. Don’t even get me started about the historical aberration that is NIRP.

I feel very sorry for Chairman Powell who is now backed into a very unenviable position. He seems like a honorable Guy who might have to pay for the malfeasance of his predecessors.

“strong economy” Wonk!

Paulo, they point to the US low unemployment rate and to the employment population ratio sitting at the 1986 level of 60.6%

Well now, if economic conditions are so supercalafragilistic, then why is the US labor force participation rate at the 1978 level of 60.6%?

Surly the population has grown since 1978? Where are all those folks working?

One statistic I follow is the “weekly with-holdings’. This is the amount of deductions (tax etc.) that employers “withhold” from their employees for payment later. These totals are horrible considering historical data! Proves that unemployment stats and the “strong economy” stories are from “Fantasyland”. Wishful thinking.

“The Fed’s “gradual” approach has been designed to avoid a sudden market reaction…”

Then IMO, clearly the Fed has failed, because there was nothing un-sudden bout the market’s reaction of asset inflation these past 3 years while the Fed was employing “hawkish gradualism” to stop it.

It’s not rocket science. Dear Fed, back to the drawing board because you failed and there’s a vast universe of alternative actions – like .5% instead of .25% – for starters.

The FED doesn’t have many options.

To fix asset bubbles? Don’t agree. Margin debt…and since when it only .25% the only game in town.

The Fed has millions of options.

The FED has billions of options. Even trillions.

Expect Powell to be fired in the very near future and Kaplan to take his place. QT will immediately be stopped and QEn will restart at earnest. Fed has always been stock markets bxxx since Volker times. Believing otherwise is madness.

We know Wall Street is a fraction of the economy yet they manage to take hostage the fed the media and the government. I want to throw up.

Forget about it: Yes Wall Street should be a fraction of the real economy but with free money they seem to have grown much bigger!

A long-term look on the money supply shows an exponential curve with a little bump around the financial crisis 2008.

Could it be that to keep the system going money has to increase exponentially with ever more and cheaper credit or the system collapses?

The problem seems to be international, rates for German and Japanese 10 year government bonds fell significantly with the us rates.

The current choice seems to be inflation over collapse.

Has any unbacked money system throughout history ever collapsed or disappeared or is the end always hyperinflation?

The so-called collapse they fear is simply the route Iceland took last crisis rather than the route Ireland took.

I’d say that ordinary people were much better off in the Iceland scenario, but the financial elites were much better off in the Ireland scenario.

Like the french franc and other European currencies ?

But a collapse in a currency means loss of confidence means loss of value, and as government doesn’t bother confiscating anything worthless (usually the opposite) the prices in that currency MUST then show inflation or hyperinflation.

However, I suppose it is feasible that price, capital, and social control could enforce the value of a currency that ordinarily people would not want. That would be like rationing, where your fiat is the token under a fully state controlled economy. To achieve this requires idealism, ruthlessness and a committed intelligence network.

So you see, currency and financial collapse are not nescessarily the worst outcome , what comes afterwards as an answer from the state may be.

In today’s world the transition might be gentler, say basic income from state for a redundant society, where inflation manifests in the competition of the rich over assets, but consumer inflation due to efficient productivity and low income (ultimately your basic income) balance. Due to government eventually providing that subsidy to the lower class, it must create it by debt as the profit goes to the asset owners (suppliers). That gives a circular transfer system where government finance is maintained by low rates and a certain inflation, which is “won” by asset owners, but devalues their total wealth by the same amount in real terms. Obviously that all represents a hierarchy or power structure, from which the subsidised are not likely to escape, maybe nor really want to, which is the same.

If this is synchronised between different countries there is no escape because there are no better options available to the individual.

Just a hypothesis over how or why this inflationary corner might be designed so that to avoid collapse people unwittingly embrace total management.

With the global dollars in circulation or in CB vaults, the Fed has limited control of total dollars, as more dollars exist outside our borders, and thusly cannot cause interest rates to rise. More dollars are outside the borders of the US (Eurodollars) and CB of these countries (also China) can determine where those dollars go. It they go back to the US, interest rates fall as bond prices rise. China converted dollars to yuan or bought US Treasuries which allowed dollars to flow back to to US, and thusly forced bond prices to rise and yields to fall. Notice US Treauries are at 2.56%, falling from the 3% range, even though the Fed is trying to raise interest rates. Like Greenspan said “ it is a condundrum”.

But they knew why is was a condundrum, but they could not admit it. Again Greenspan, a Maestro, please, he was a fraud.

Here’s just 1 of the many millions of things the Fed might do, to actually stimulate the economy. The real economy, not the fake Wall Street stock market economy.

1). Buy up all student loan debt, and announce a suspension of payments until further notice, or never. It might attempt to target this based on income. Or not.

2). Freeing so many consumers of such large debts could result in a flood of consumer demand – not fake monetary induced demand for stock, assets, and things that benefit Wall Street and stocks – that the Fed could discover it had better raise interest rates a lot more to ward off actual, real inflation.

3). The rising interest rates will right the balance, away form assets, Wall Street, and stocks. Financial institutions will howl in pain, but they are the ones who have been unfairly subsidized for decades and they need the pie take away from the so the rest of the economy can have it for a change.

4). Until Congress fixes it mistake of making student debt live slavery, and normalizes it like the debt, these Fed actions will dissipate over time. That is why the Fed must launch a full scale co-ordinated campaign to get Congress to reverse it laws granting special slave status to student debt.

Just one thing. I don’t know detail of the Fed’s vast powers. I’m sure it has many other possibilities to actually help the economy, for real instead of for fake like it did with suppressing interest rates.

That could definitely work. But, why stop at student loan debt? Why not ride that train all the way to the station?

Call it what you will- QE for the people, debt jubilee, debt forgiveness, debtor bail out, et cet, the problem is that there are too many bagholders, too many institutions on the other side.

The only way consumer or student loan debt forgiveness can be successful, IMO, is to reallocate existing wealth from the wealthy to the debtor. I don’t think that would go over very well with the wealthy 1%, so I don’t think that is a very realistic option.

The FED clearly only has two options, and of those, only one is viable. I think we all know what it is.

Kasadour,

Above, I just read your other comment, which said: “The FED has billions of options. Even trillions.

Now you say that “The FED clearly only has two options, and of those, only one is viable.”

I think I understand what you mean, but it’s funny anyway.

Here is reality: the Fed is worried about asset bubbles including in the credit markets that have gone haywire, and these asset bubbles are threatening “financial stability” — the banks! The Fed will be careful, but it will try to “gradually” unwind those asset bubbles and bring credit markets back to reality.

So don’t expect a U-turn. If “financial conditions” normalize, it will just hang tight with rates and continue the QE unwind on auto pilot.

However, if something big blows up, all bets are off.

Wolf, are you from the school of thought that the Fed sets rates, or that they simply follow what is already happening in the bond market…..

Jdog,

Absolutely neither.

1. The Fed doesn’t “set rates.” It decides on a target range for the federal funds rate (an overnight rate) and tries to keep the federal funds rate in that range via the Fed’s trading desk, via IOER, and other methods. I does set the IOER, which impacts the federal funds rate via the banks’ reaction to it. And then it hopes this will be transmitted via the broader markets to tighten or loosen “financial conditions” — as explained in the article above. The Fed tries to manipulate the credit markets in various ways, including interest rate policy, QE, and speeches. That’s all it can do.

2. The people who think the Fed just “follows what is already happening in the bond market” live in a another world.

Do I get reimbursed for paying cash for my daughters schooling, so as not to put her in debt….I hope so….its about time the sheeple learned about debtpushers…..

ideas like yours are what got us here, time for credit mooches and debt addicts learn a lesson……sorry that is the right the way to do it….not reward a bunch of 10 year students a free ride on taxpayers…….

That’s what they said about mortgage reduction to fix the massive bank fraud that led to the financial crisis in 2008…like you the rejected that solution….how’d that werk out fer yah?

great as I was smart enough to sell near the top…..When astrologers were wholesale mortgage reps for NewCentury making 300K a year and not understanding what tiered rates and a CDO is….get out….

I bought more credit than you could fathom, credit mooches and credit criminals need to be fed the hard lesson…..

I voted against TARP, the rescue of ghost banks etc…

you on the other hand seem to have your head in the sand…

No student loan rescue is necessary, just don’t rack up the debt….it will never happen to begin with…..than all hiring practices would have to exclude a diploma as part of hiring process as many smart folks learned a trade and didn’t rack up the debt…..

The Fed doesn’t have power in that area, but I’ve long thought that the Fed should be able to do a form of QE closer to Ben’s famous helicopter money, where every US citizen gets an equal amount of money claimable from banks based on social security number.

That would be simple and fair, and much of the money would either be spent and help to bolster demand or be used for debt reduction and help to rebalance the system.

In contrast, Ben’s actual QE was free money given to the banking system to lend out and bid up prices with, resulting in ever higher levels of debt. You can’t completely blame the Fed because they need Congress to approve any change to this system, but you can argue that the Fed should never have embarked on QE in it’s current form.

The Fed absolutely has authority. It has a clear mandate to act. The widespread fraud in student loans which well documented gives the Fed power to almost anything it will including what I just suggested.

you should learn about debt-credit-yield-LTV and charge off….

sounds like you bit to much off to chew, no 4 of 10 year college student deserves a break….unless you give the same amount to non students…

play with debtpushers and get addicted..

Crazy idea I had earlier this afternoon. If you had no clue on whether financial conditions will tighten or loosen, would it be smart to invest in a 50-50 mix of long term high grade corporate bonds and high yield corporate bonds? It would seem like they would counterbalance one another.

The Fed eased aggressively during the 2000-02 and 2007-09 collapses, both of which cut the stock market in half. They could reverse and ease again, but it probably wouldn’t work. Yield-seeking speculation is a powerful force, but it only works when investors are actually inclined to speculate. Cash again becomes the desired asset, regardless of what the Fed does.

One of the reasons why the yield curve is inverted is how the Fed is letting QT work . Instead of selling those longer term securities that they acquired during Qe , they are just letting shorter term securities mature without replacing them . This puts more short term pressure on a number of short term rates while putting less pressure on longer term rates. This has resulted in the ridiculous 30 year rate at %2.90 not far above its all time low. Of %2.11

Why isn’t all the Federal Borrowing out there in the 30 Yr?

uM, think you have a typo. “It took three years to nudge up the effective federal funds rate from near zero to 2.40% now.”

Shouldn’t it be 2.5 % ?

and 2 yr, 3 yr, and nearly almost the 5 year, are lower than Fed Funds rate.

So what bank in their right mind, would lend out for short term (margin debt anyone), when Fed Funds rate is above most of the bond market ?

The Fed is in a jam now, yessiree. They literally have to wait for the “accident” to happen, until they can reverse course, and lower. There has to be a major ’emergency’ for that to happen, bc if they suddenly did it now, or even a month from now, before any emergency, the entire market would either completely freeze up like a stone. Or it would plummet like a rock, and people would YELL get me out at ANY PRICE !

Heck, now they don’t even have time to go to ‘neutral’ and ‘posture’ for a bit, before admitting they need to lower rates. It wont be just Trump, but every governement on the planet will be screaming at them to lower, yet there just might not be a “Lehman” around to pin it on, or to try to make the case that its ‘contained.’ In 08, they also had ‘bullets’ they hadn’t expended. Now they don’t. Worse, now everyone will FINALLY question whether QE or massive printing will be the ‘solution’, since markets will have proven thusly, and it will be EVIDENT to even the most ignorant, that when they did it (QE, buying everything in sight) the first time, and yet we are back here again, even worse, that even considering QE may be off the table. So now what ? What magic trick do they have up their sleeve now ? A complete dollar reset ? Oh, that’d be cute. P.S. Got gold ?

Mike R,

To your question: “uM, think you have a typo. “It took three years to nudge up the effective federal funds rate from near zero to 2.40% now.” Shouldn’t it be 2.5 % ?”

The “effective federal funds rate” is a market rate that the Fed manipulates into the middle of its target range (currently 2.25% to 2.50%) via its trading desk, interest on excess reserves, etc. As of today, the effective federal funds rate = 2.40%

https://apps.newyorkfed.org/markets/autorates/fed%20funds

A month ago, Fed Fund Futures implied a 72.9% chance of at least one hike. They now imply a 38.9% chance of at least one (source: CME Fedwatch).

In the past I have found if there is at least 70% chance of a hike, the Fed hikes else it skips. Given that the chances of a hike in Mar 2019 is now 46.7%, it looks like the Fed is at the end of its hiking cycle for now. The other question is will the shedding of assets also come to a stop.

What are the chances of the markets again blowingoff the Fed once it stops? At this rate can the Fed wean the markets away from its money-spewing teats AT ALL? Looks like the cry-babies from wall-street want to feast for ever and the Fed will oblige as it has done during the last 30 years (since Greenspan).

The Fed is now in a fine pickle since it must realize weaning markets away without a market crash is a pipe-dream. Add ECB, EU, China, BoJ, Trade wars, EU, Brexit, China and uprisings like Yellow vest etc. to this and the mind gets blown away at the enormity of the task of normalizing things and the stupidity of the Fed in even thinking that it can be done.

IMO, we are at a cross-road of having to take a bitter pill (system blow up) now or later and we will choose the now for now.

Please see my comment above about these bizarre levels of apparent precision in these predictions.

A measurement quote of 46.7 % or a tenth of a percent is a quote to within one thousandth !

This is a tolerance associated with a machine shop using a micrometer on a item in the present. not a future event subject to unquantifiable influences known and unknown.

I’m not picking on you BTW, you are just quoting the experts.

It’s a bit puzzling how highly educated people don’t seem to grasp the level of precision they are pretending to have.

Could the whole field have missed the section of high school math where they discuss measurements and tolerances?

“we will choose the now for now”… should have been “we will choose later as usual”

BB is not investment grade, BBB is.

Sheesh! That B slipped right through the crack in my keyboard. Thanks.

The whole idea you can control something as complex as an economy by adjusting the base rate is madness. No engineer would try to control the electric grid, which is far less complicated, by varying the voltage. When you have such a complex system, especially one that’s plagued by swarms of black swans, you put a lot of effort into making it robust, you build in redundancy. That makes it look inefficient (uneconomical, if you like) in the short term, but in the long term it pays. A single black swan no longer brings the whole systems down, just part of it, and that part recovers more quickly due to the most other parts still functioning. So let’s sack the economists and replace them with engineers.

As it is, I wouldn’t bet against the FED eventually doing more QE.

I’m going to venture a guess that the Fed will raise rates two quarter points this year and keep QT going throughout the year. I think the stock market may stabilize somewhat going forward and provide the Fed the opportunity. Real estate will continue to decline but that won’t deter them.

The question I have is this: what is the impact of QT relative to a .25% hike? And 1 more …did the Fed ever justify their pre-designed rate of QT? Putting QT on auto-pilot is clearly not based on the data.

It does not seem unreasonable to assume that planned QT run rates are = or > rate hikes. If so, their pace of tightening has actually been very rapid.

The Fed doesn’t know with any reasonable degree of accuracy. If they did, then how does one explain that in the past their last rate hike was followed by a rate decrease in an average of only 6 months????

So Apple blows their pricing model, and the Fed is supposed to be accommodative?

We will not have honest markets or sound money until we end the Fed. Instead, we’ll have these engineered boom-bust cycles every 8-10 years that are the Wall Street-Federal Reserve Looting Syndicate’s most efficacious means of looting and asset-stripping the bottom 95%. Meanwhile, the Fed’s creation of trillions in fake money out of thin air to gift to its financier oligarch accomplices debases every dollar in your wallet and mine, destroying our purchasing power and quality of life.

Yep, it certainly looks that way. And if the Fed “saved us”, then how did year after year of 0% and massive QE fail to stimulate anything except the largest asset bubbles ever?

The average time between the last Fed rate hike in a cycle and the first Fed rate drop is 6 months. 6 months! Their track record is plainly abysmal …if viewed through the lens of their stated purpose.

Fed continues to raise rates till 3% is reached, boarder Wall is nominally built (or an event happens that makes Wall unnecessary) , DOD budget increases in real terms (stealth stimulus and saber rattling) , automation is subsidized, all prices increase substantially but especially import prices, blue collar wages soar. DJT Presidency becomes a blend of DDE and RWR.

312,000 increase in jobs in December, almost double versus what was expected. And people have been reentering the workforce in droves. Wages have been growing at the fastest clip in many years. Consumer credit is solid. Main street is strong …for now.

Looks like any downturn will be led by the Fed through the Corporations, not the consumer.

Market is rallying again this morning on “dovish” comments by Powell. I wonder how long before they throw another tantrum.

Oh lookee, here’s Mr. Powell finally buckling.

https://www.nytimes.com/2019/01/04/business/economy/jerome-powell-fed-reserve.html

“We’re always prepared to shift,” Mr. Powell said, adding the Fed could shift “significantly” if necessary.

“We wouldn’t hesitate to make a change” in policy, he said.

The markets are hanging onto his every word.

Wouldn’t bet my life on this, but this has been the MSM take on him before and so far he’s stayed the course. His “dovish tone” to use the cliche dujour could be the sugar to go with the medicine rather than actually changing the trajectory. If he said no we are tightening no matter what and ignoring any data/changes thatd be crazy. All he said was we are ready to change, but economy looks strong, with the implication of no imminent change coming. At least that’s how I took it and seems equally possible as waffling.

I do not think it matters so much at this point. Timing of the economic cycle is wrong to expect stimulus to have much positive effect. In order for economic stimulus to have the intended effect, asset prices need to be at the lower end of the spectrum, not overvalued as they are now. To stimulate prices at this point would only serve to blow a bigger bubble than we already have. To attempt to increase debt loads beyond the point they are currently at would surely create a massive colapse at some point in the future. In a debt based economy, you must at some point reconcile what is owed with the ability to pay.

My base case is slower growth with inflation. The fed statements this morning is important evidence supporting this base case. The strong job growth did not stop the fed statements. I think housing should be just fine, as long as the local employment picture is not too startup heavy.

This is why the response of the financial markets to Fed interest rates is exactly like what happens in the engineering control system world of operational amplifiers where there is a time delay on the feedback loop. Time delays on a feedback loop are inherently unstable and will always result in oscillations, where the up cycles and down cycles overshoot their targets.

The only way to dampen these up and down cycles is by putting in a low gain on the system, which is what we had for the period of tight financial regulation, high tax rates, and moderate to high interest rates, roughly the period from 1932 – 1981, i.e. New Deal tax hikes and Glass/Steagall to Reagan tax cuts and the start of financial deregulation

We now have a high gain, highly unstable system. Low taxes, little to no financial regulation, low interest rates (anybody remember the days when a standard savings and loan account paid you a 5-1/4% interest rate? Regulated and guaranteed by the Federal government?)

Multi-billionaires and vast paper fortunes arise overnight! The mighty engine of entrepreneurial capitalism at work! Blah-blah-blah!

The coming downside of course is the vast pile of debt, much of it really really bad debt, with no real assets behind it to recover the money, picked up in this overshooting up cycle. A big heaping stinking pile of garbage bigger than Kill Island NY.

Inflation is not a problem! Don’t keep raising the interest rates!

Right, if the Fed listens to this rising Greek chorus and stops its rate hikes, the only thing that will be accomplished will be to delay the inevitable crash of this bad debt, and most likely make the crash even mire severe. The last time the Fed held back from raising rates and unwinding QE, after the markets tumbled in 2015, all that happened was this vast increase in this Everything Asset Bubble and a huge increase in this junk debt.

It’s too late to prevent a crash. If the Fed doesn’t pop the balloon now, the balloon will just start reinflating again until the bad debt topples over by itself, and the deregulated financial system locks up again

This was the history of the financial system of the United States from 1800-1930, 130 years worth of regular financial crashes from bad debt every 20 years or so, until the vast suffering caused by the Great Depression finally brought forth the political willpower to change the system to a low gain financial system (ie, more regulation, higher taxes, and democratic socialism)

310000 baby boomers retired in dec. 2000 jobs were created.

Many of them had to unretire afterthe dot com crash

The Labor Participation Rate of 75-79s doubled (6% to 12%) from 1996 to 2016.

God help me if I actively seeking work at 79…

Meanwhile, the LPR for millenials keeps getting smaller and smaller.

The millennials are a larger generation than the boomers, and they’ve been entering the workforce in very large numbers. “Generations” are a constant flow not some fixed inventory.

All those companies that are Junk Debt Stars, because they literally cannot live without taking more more and more debt yet people think they are stars, are on the losing side, it will just take time for investors to stop blowing off the warnings.

Tesla has blow out the chances it has of being sold thank to Musk Continental sized ego.

Netflix is having to face more and more clones.

Apple is facing more and more competition.

Amazon might be growing too fast for their own good.

Alphabet is likely to recover.

Microsoft is actually doing quite well despite their Windows 10 update disasters.

And nothing is really lost if NVIDIA

crashes and burns (Anyone remembers Soundblaster or Woodoo? Nope? That’s what I thought.)

My take on this morning’s Fed show (I saw Powell, Yellen, and Bernanke, + interviewer, broadcast on CNBC):

quite a lot of self-satisfaction by the past and present Fed heads. And the conclusion, roundly accepted, based on the last 10 years: that virtually Nil Interest Rates should remain a tool in the Fed’s toolbox (not one remark re the fact that the ZIRPs will play out in retirement savings, and pension funds, for maybe 30 yrs. to come). A bit of looking askance at the Eurozone NIRPs as going a bit too far (we the Fed would never do that here, implied).

I did hear Yellen say that rise in price of house has put money in consumers’ pockets. That’s the seller, Yellen. Read some Wolf Street commentary for the would-be buyer’s side of that picture.

Finally, what has struck my interest lately, given the indebtedness of the average American consumer (again, see WS), is the interest rates charged on credit cards:

This is from a flyer sent me by Capital One, but is typical of all the big cc lenders: APR for Purchases and Transfers, following the intro rate of 0% lasting about a year: “… 14.74%, 20.74%, or 24.74%, based on your creditworthiness. This APR will vary with the market based on the Prime Rate.” Seems like these rates can only go up.

If the Fed has become wiser and more powerful over time, and their policies have always benefited the nation, why are they bothering to pay lip service to “normalization” ?

The single way, that I am aware of, that the middle-class American has been able to take advantage of VLIRPs, has been the home mortgage. The 3.33% APY, fixed rate, that spouse and I have been paying on an 11-year mortgage, has been good for us. Still, Wolf’s charts have pretty well substantiated the real estate bubble that the low rates have enabled.

Got a 30 yr fixed with first 10 years interest only in the mid 3s couple years ago. Think BNY discontinued the product bc they realized how stupid it was for them. Will make up for my conscious overpay of 5-10% with a plan to stay for the l-t. At least that’s the hope.

In theory isn’t this ideal for the Fed (and at least theoretically the markets/economy). Fed says market friendly things, keeps the bottom from falling out, while continuing on present course. Is this not the Fed call to the former Fed put? I read JP say that he’d CONSIDER ending BS normalization IF it showed to be a problem BUT saw no evidence it had anything to do with recent market turmoil. Seems like perma bulls hearing what they want to hear while the plan remains the same: orderly retreat while trying to avoid an implosion. Not saying they’ll be able to pull it off, but market (misplaced) optimism seems to give them more cover to push forward.

Rory Boyle,

I think you might be right. Powell may have just been saying what he needed to say to stop stock market bleeding and to keep Trump off his back. But I am getting the feeling Powell is not as sure and knowledgable about what he’s doing as I first thought.

He looked weak today.

Remember that the Feds balance sheet is only about 10% the size of the bond market. 10% can influence, but it cannot dictate.

The Fed will need to stay on the course of normalizing monetary policy, but to prevent panic they will need to periodically pause to let things settle.

We will know it is time to continue with the tightening when stock prices stabilize and multiples begin to increase again. Gradually squeezing out the speculation is not easy and frequently causes crashes. It will require a deft hand to manage monetary normalization. It will probably not be completed before a new recession arrives.