Normally, this would be ironic: The Fed doesn’t need to borrow; it creates money when it needs some. So it wouldn’t pay interest. But these are not normal times.

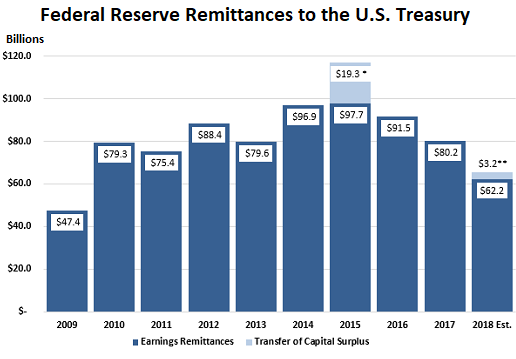

The Fed reported its preliminary results this morning for the year 2018. The headline is that it sent $65.4 billion of its profits to the US Treasury Department in 2018, and that this amount had plunged by 18.5% from the remittances, as they’re called, in 2017, and by 44.1% from the peak of $117 billion in 2015.

The Fed earns interest income on the huge pile of securities it holds. After covering operating expenses, interest expenses, and some other items, it is required to remit the rest to the Treasury Department – to the taxpayer.

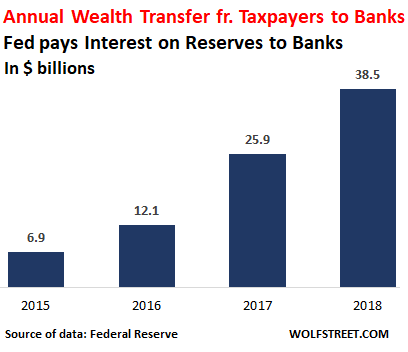

Therefore, the amounts in interest expense the Fed pays the banks on their “Excess Reserves” and “Required Reserves” comes out of the taxpayer’s pocket and its transferred to the banks to become bank profits, and thereby bank executive bonuses and stock holder dividends, funded by the dear taxpayers. And this amount was huge in 2018: $38.5 billion!

Here is what the Fed reported:

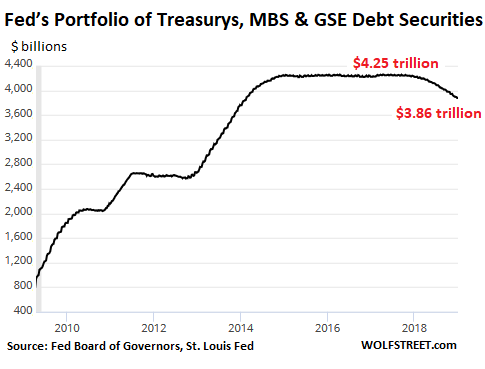

Interest income: $112.3 billion. This is the amount the Fed received in interest payments on the securities it holds, including those acquired as part of QE: Treasury securities, mortgage-backed securities (MBS), and government-sponsored enterprise (GSE) debt securities (the latter is now almost nothing in the grander scheme of things, just $2.4 billion, and down from $169 billion peak in 2010).

The chart below shows the Fed’s combined holdings of Treasury securities, MBS, and GSE debt securities. The QE unwind (which started in October 2017) whittled down the balance of those three types of securities by $392 billion.

“Interest expenses”: $38.5 billion and $4.3 billion.

Normally, these line items would be ironic because, obviously, the Fed doesn’t need to borrow money – it creates money when it needs some – and therefore, it wouldn’t need to pay interest. But these are not normal times.

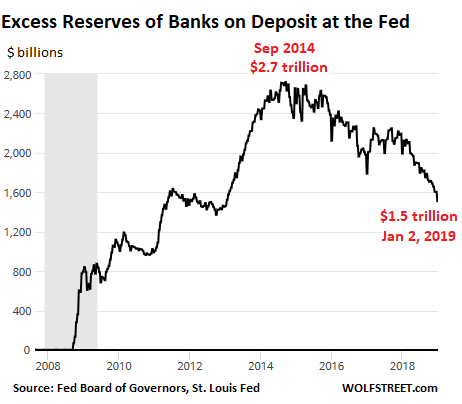

The $38.5 billion: This is what the Fed paid US banks and foreign banks in the US on their Excess Reserves and Required Reserves on deposit at the Fed.

- Required Reserves are the amounts that banks have to keep on deposit at the Fed for liquidity purposes. This is relatively small, $192 billion at year-end, and was roughly flat in 2018.

- Excess Reserves are the amounts that banks voluntarily deposit at the Fed to earn risk-free income. The amount peaked in September 2014 at $2.7 trillion and has since fallen to $1.5 trillion. Of that $1.2 trillion drop, $510 billion occurred in 2018.

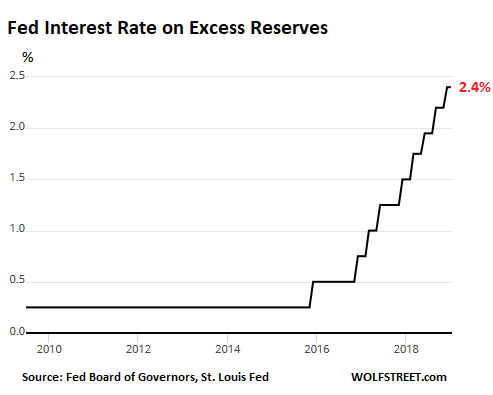

The interest rate that the Fed paid on both types of reserves was 1.5% at the beginning of 2018, and was raised four times with each rate hike during the year, but less than the 1/4-point hikes of the Fed’s target range for the federal funds rate. At its December meeting, the Fed raised this rate to 2.4%.

So the balances of Excess Reserves have plunged, and the interest rate the Fed pays on those reserve balances has jumped. Both factors combined caused the Fed to pay a record $38.5 billion to US banks and foreign banks in the US. Here is the sordid history of this annual wealth transfer from taxpayers to the banks via the Fed:

The $4.6 billion: This is what the Fed paid in interest expense on securities that it sold under agreement to repurchase. This too came out of taxpayer’s pocket.

The total the Fed sent to banks and others in interest that came out of taxpayers’ pocket amounted to a combined wealth transfer in 2018 of $43.1 billion.

Operating expenses.

The Fed, including the 12 regional Federal Reserve Banks, had operating expenses of $4.3 billion in 2018. They also made $444 million in income from services. And there were some additional expenses:

- $849 million for producing, issuing, and retiring currency

- $838 million for Board of Governors expenditures

- $337 million to fund the operations of the Consumer Financial Protection Bureau

The thing that is always fun but minor, given the huge amounts the Fed pays the banks on Excess Reserves: the 12 regional Federal Reserve Banks, which are owned by the largest financial firms in their districts, paid statutory dividends of $1 billion in 2018 to their shareholders.

So what does this leave for the Taxpayer?

The Fed remitted most of the remainder – the difference between its interest income and its expenses plus some other items — $65.4 billion in total, to the US Treasury Department, and hence finally the stiffed taxpayer. It was the lowest amount since 2009 (chart via the Fed):

The Fed also disclosed:

The payments include two lump-sum payments totaling approximately $3.2 billion, necessary to reduce aggregate Reserve Bank capital surplus to $6.825 billion as required by the Bipartisan Budget Act of 2018 (Budget Act) and the Economic Growth, Regulatory Relief, and Consumer Protection Act (Economic Growth Act).

These are preliminary results, the Fed said. Final results will be released in March after the annual audit of the Fed’s financial statements.

But all bets are off if something big breaks. Read… Rally in Stocks Takes Heat Off Fed, Now They Talk Rate Hikes Again, Market Expectation of a Rate Hike Spikes

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Does the Fed pay IOER on the “Par” Value of the security or does it do it on the “haircut” or market value of the security or excess reserve? Sometimes they use % of Total Outstanding and I get confused what for?

Iamafan,

IOER is an interest payment on a deposit. This is not a security. It’s like your bank pays you (wishfully thinking here) 2.4% on your savings that you deposited at your bank.

So according to Zhaogang Song and Haoxiang Zhu, the banks made about $650 million front running the Fed, sold the securities and got paid by an interest bearing (2.4%) deposit account. More than a gift!

The end consequences of “too big too fail” and “too big to prosecute.”

Thank you for shining light on this.

Paying interest on required reserves seem justified. But paying interest on excess deposits sends wrong message and creates wrong incentive. Banks can lend excess reserves to other banks and try making money that way. Use power of free markets?

IIRC, It was worse during housing crisis: banks were not lending to each other (or pretty much to anyone else) and kept their bailout money at the Fed.

The IOER is basically a bribe to the excess reserve-holding banks not to lend it out. Every dollar in excess reserves would result in $10 in additional M1 money supply. If all excess reserves now were used for loans, the M1 money supply would increase by a factor of 4x.

This would certainly increase economic activity. But the inflation would be amazing.

Note: This is all explained in a Federal Reserve note, though in their example they used a 1.3% reduction in excess reserves to cause a 20% increase in M1.

Dale, thanks, makes sense.. except, according to the above excess deserves shrunk by 510B in 2018 but according to st. Louis Fed website M1 money supply stood at 3.75T at the end of 2018 and at ~3.6T at end of 2017 so it did not increase by 5.1T (-10x change in ER) but by less than -1x !

Even M2 only went up from ~13.8T to ~14.45T. Why did your theory not apply in 2018? And why would it apply now?

Thanks, SW

M1 only increases if banks convert excess reserves into loans. IOER is a risk-free payment to the banks not to make those loans.

In addition to QT, the Fed has been working on other ways to sop up excess reserves. But QT is the best and necessary way to achieve this. Even if the Fed delays an FFR hike or two, they need to continue QT. I believe that Jerome Powell understands this.

Dale, good analysis, but I have a question. Bank net interest margin on loans is around 3.5%. Why would they forgo a loan at that NIM in order to keep $ at the FED earning less?

Two reasons:

1) There’s no risk if the money’s at the Fed. The NIM on the other loans is subject to risk, so actual returns are lower than NIM.

2) The banks have ALSO made all the other loans that are worth making. They aren’t foregoing a bite at either apple here.

In 2018 $35.8 billion dollars was paid to the Federal Reserve (via US taxpayers) and then to the Federal Reserve Regional banks which was then paid in dividends to the public owned banks since they are private shareholders of the Federal Reserve Regional Banks. And that the Federal Reserve will not disclose the identity of those public banks that own their shares. Did I get that right?

“[Amount remitted to US Treasury] was the lowest amount since 2009 (chart via the Fed):”.

I am curious how much interest was earned by the Fed in each of those years? It might be the case that a lot of of high-coupon rate bonds have matured and overall interest collected has reduced over the years.

Double-whammy: lower interest collected by the holdings, higher interest paid on excess reserves

GP,

The difference in interest income is minimal after QE maximum was reached. For example, in the peak profit year, 2015, the Fed earned $113.6 billion in interest income. This is just $1 billion more than in 2018. The main difference is that in 2015 the Fed paid only $6.9 billion to the banks in interest on reserves (due lower interest rate); and in 2018, it paid $38.5 billion.

They sort of did disclose it a while back. I think I read GS was the largest and JPM made the most in spread earnings.

Sadie,

Note quite. The Fed’s interest on reserves is unrelated to the dividend payments from the 12 FRBs to their shareholders. These dividend payments totaled only $1 billion in 2018, which I also point out in the article. But this is a separate item.

In terms of the interest on reserves coming out of the taxpayer’s pocket, this is how it works:

1. Fed EARNS interest on the securities it holds: $112.3 billion in 2018. This is revenues for the Fed.

2. In terms of expenses: the Fed PAYS banks interest on the Reserves the banks keep on deposit at the Fed: $38.5 billion in 2018.

3. These $38.5 billion in interest payments that the Fed pays to the banks were an interest expense for the Fed, and reduced its profits by that amount.

4. The Fed has to remit its profits (income minus expenses) to the Treasury Department. This is us, the taxpayers.

5. This amount of profit the Fed pays the Treasury Department (= taxpayer) is reduced by the Fed’s interest expense, namely the $38.5 billion that the Fed paid the banks.

The interest payment comes out the taxpayer’s pocket via this triangular relationship – Fed sends it to the banks instead of the Treasury Department. It is money that the Treasury Department (taxpayer) is not getting because the Fed gives it to the banks. And taxpayers have to make up for it either via paying more taxes or shouldering more public debt.

Thanks for the clarification Wolf. The $38.5 billion was IOER.

Well that’s not a very good arrangement!!

Thx again for a very informative writing about the FED/Treasury/Public relationship. I suspect anything this complicated….for the layman public!

You got it right- if Wolf would print it in all caps every day, it might help defang the monster. (and worth recalling that the last President with the guts to take them on, Andrew Jackson’s portrait occupies a place of honor in the Trump Oval Office (but the bad news is Trump does not have the guts to take the Fed on.)

Holy smokes. After paying for any required graft, swag, and vigorish, it looks like there would be enough left over to fund The Wall. How was this missed by the minders?

It’s as much as the Tariffs. Those poor poor peasants….oops, that’d be us. Oh well. Just the price of doing business, I guess. Everyone needs their cut. Ain’t capitalism grand?

Is this then the rare instance where the government actually follows the constitution?

“No Money shall be drawn from the Treasury, but in Consequence of Appropriations made by Law”, Article 1, Sec. 9

Trump can’t spend the money until he gets an appropriation of an amount for that purpose. Yes, ideas like democracy can really mess up a wanna-be dictator who’s trying to push a giant, expensive construction boondoggle for his friends.

So, annual government debt is 1.4trilliom, FEF is paying banks 40 Billion, and they say 5.8 billion for a wall is big budget deal and we should spend carefully and guard TAX payer’s funding of government.

Hi Wolf, do you have any opinion why the dollar amount of excess reserves dropped so significantly since Sep 2014 (from 2.7 trillion down to 1.5 trillion)?

The banks can make more money buying Treasury securities. Even though yields have come down recently, the 1-year yield has been around 2.6%.

Why not have the banks use their excess reserves earning IOER to buy treasuries and fund the deficit?

If the Fed didn’t pay IOER (which is a new concept created in 2008 to help set the floor on rates?), wouldn’t banks just buy the 1-year treasury yielding 2.6% as you suggest above?

The end result is that tax payers are paying 2.6% directly from the treasury to banks, rather than 2.4% from the triangular relationship of the Fed, banks, and Treasury?

Why not just eliminate the Fed? Why should the government allow the Fed to create the nations money supply and then lend the money to the government at interest? The governments debt to the Fed is the reason the income tax was implemented.

The Fed is a corporation, who’s stock holders are the member banks. Corporations work in the interest of their shareholders first and in the interest of customers second.

Wolf. You are on a roll. 2019 is your year. You own 2019.

+1

\\\

What new euphemism should we use to call this grand gesture of good will towards the suffering financial institutions?

\\\

“Cash for Stash”?

\\\

The mission of the Fed has always been to first enslave the citizens, and then to transfer all assets from the working people to the wealthy.

In order to not completely demoralize the workers, they allow periods of false prosperity to encourage productivity, and then follow with recessions to confiscate the fruits of that productivity. It just amazes me the majority of the people never figure out the game…

Let’s say you’ve figured it out, what can you do about it?

Call Geico

Nothing unless the majority of the people educate themselves and force government to abolish the Fed. I am not holding my breath waiting for that to happen.

You know, when people are busy making ends meet, psychologically stressed to a point of anger, here in America, they start to shoot neighbors they don’t like or kids in school. How come the European guys knew better? They gathered around ECB headquarter. The yellow vests in France now are talking about organized mass cash widthdraw from the ATMs.

I hope Congress questions why these interest payments are necessary. I’d like to see the Fed explain why it pays $38B of taxpayer money to banks when it doesn’t have to.

According to Dale, it’s so they don’t lend it out into the economy thus blowing up M1 supply and create inflation. So the fed’s bailout money stays at the banks, solving their liquidity problem until gradually withdrawn. Thus, the actual bailout will have taken the form of interest paid to banks over the period on the nominal amount they got from the fed and kept at the fed or in T bonds until the wind down, all the while avoiding dreaded inflation. If this scheme was deliberate and predictable and controllable then it could potentially make some sense. Except for the asset price inflation and junk bond trap and the lost decade of austerity leading to trumpism etc. But is there reason to think this was sort of the plan?

The Fed doesn’t really have to pay the interest to the banks to restrict lending. All they have to do is raise the “reserve ratio” – say, from 10% to 20% or higher.

Similar with putting a brake on stock trading – they can change the “margin requirement”.

What difference will it make? They pay interest on required reserves as well.

You seem to be under the mistaken impression that the Congress works in the best interest of the citizens.

“I hope Congress …..”

Ok, sure … pull the other one.

‘Congress’, such as it is, works NOT for me, nor thee .. they’re a Big Club … and we, the plebes, are the target .. hence the FED !

I think the Fed should be prohibited from paying a bank any higher rate than the highest rate it offers its depositors.

Rare words of wisdom. So would demanding Congress live by the same laws they impose on the rest of us. (or demanding the wall around Nancy Pelosi’s mansion be no higher than the lowest part of the Mexico wall.)

So, what is the banks’ cost of funds? They are required by law to have these deposits at the Fed, but they may not be getting the money for free. It is likely that the much of this interest is just passed through to depositors.

Unless you have a minimum of $10K to put in for at least 18 months about the best you can do is around .1%(that is 1/10 of 1%). No, it isn’t getting passed on to their depositors.

Looking on the Fidelity CD web page, I see you can get 2.25% on a 3-month CD from a number of banks. Minimum deposit is $1000.

“The bankers own this place” , IIRC, that was Sen Durbin (IL).

Note, he did not say “The taxpayers own this place” as one would expect in a democratic form of government.

Buy a Yellow Vest.

and a pitchfork!

Ahhh! Progress is being made! Who said that reading the WS Report would not educate us????

Let the games begin!!

And why doesn’t the Fed extend the same tax payer funded ‘gift’ to us Americans? I’d like be able to ACH some cash to the Fed’s online savings banking and get 2.4%. I bet if pressed, they’d say they’re prohibited by law, but don’t how it’s any less illegal to offer the same risk free return to banks.

Might happen in the future with TreasuryDirect (not Fed). TreasuryDirect would work better than E-verify and the US Government needs more onshore funding. Could eliminate earned-income-credit and replace with southern-border-wall dividend. Quick way to monetize debt while bypassing the Fed and Wall Street but pleasing to most banks and credit unions. Citizens love free money. 21st Century version of war-bonds.

The Fed has no mandate to act in the interest of the public, as we saw clearly during the 2008 crash. They are a private corporation with no accountability to the American Citizens. Their only accountability is to their member banks.

That is why they do not have to subject themselves to audits. No one elects anyone at the Fed. They attempt to maintain the appearance they are accountable by the clown show of allowing the President to appoint the Chairman, but in reality, the President can only choose from a small group of insiders who are already deeply imbedded in the system.

Now you understand why dumbing down the public- which is going on relentlessly on TV at any rate- is so essential.

My hat is off to the French- these are the people who not just stormed the Bastille, but took it apart stone by stone.

The dumbing down begins in the government schools. By the time the average person graduates high school, the government has not only instilled in them what to think, but how to think. That is what is really scarry.

What happens if the Fed reduces or stops paying interest on excess reserves? Do the banks then start making with the excess reserves? Why is this not being done?

The Fed fears that if stops paying IOER all of a sudden, it will lose control over short-term interest rates (federal funds rate), money market rates, etc.. The balance sheet is too big, and it distorts the Fed’s efforts to conduct monetary policy (manipulating interest rates). This is already a problem. But they’re gradually trying to whittle down those excess reserves by reducing the incentive for the banks. Note that the rates hikes are now smaller for IOER than they are for the target of the fed funds rate. These are micro steps, but they’re sitting on a powder keg and micro steps is all they’re going to do.

The taxpayers are not paying interest because of the fed, they’re paying interest because they’re BORROWING MONEY. If the member banks didn’t deposit their money at the fed, they’d be buying the treasuries themselves.

The fact that the Fed bought Treasuries has nothing to do with reserves. Banks are required to have reserves to offset loan losses.

The only thing this setup does is allow the FED to use reserves to buy bonds. Banks cannot hold reserves in bonds because their duration is too long.

Your argument that the “taxpayer” is funding reserves if circular thinking. Taxpayers wouldn’t be paying any less if there was no fed.

Also, the argument that banks can’t lend reserves because they’re tied up at the fed is a nonstarter. Banks don’t lend reserves, they create money. They reserve reserves.

Nonsense. Banks lend out the “cash” they get from deposits. A “deposit” in our common language is actually a debit and a credit on a bank’s books: one is an asset called “cash” (the $100 you put into your bank account); the other is a liability called “deposit” (this is the $100 that the banks owes you). This is basic double-entry accounting. The bank lends out the asset called “cash,” which is your $100 bucks. This converts the asset “cash” to an asset called “loan.” And the bank retains the liability called “deposit,” which is its $100 debt to you.

The reserve requirement stipulates that the bank send a portion (such as 10%) of the cash it gets from deposits to the Fed to be put on deposit at the Fed. This is done so that the bank cannot lend out all of its cash from deposits and has instant access to some cash (liquidity) in case there is demand by its customers for cash (when they remove their deposits), as is the case in a run on the bank.

Banks are not restricted by deposits. Alan Holmes, a former senior vice president of the New York Federal Reserve Bank, wrote in 1969, “in the real world banks extend credit, creating deposits in the process, and look for the reserves later.”

If bank lending is constrained by anything at all, it is capital requirements, not reserve requirements. The banks don’t need your money; it’s just cheaper for them to borrow from you than it is to borrow from other banks.

Jdog,

Oh lordy, everything gets twisted in these nutty discussions about banks: The purpose of required reserves is NOT to restrict lending, for crying out loud, but to make sure that a bank has LIQUIDITY on hand (10^% of its deposits, waiting at the Fed) to meet customer demand if there is a mini-run on that bank. That’s the purpose of required reserves.

But then you have 100 deposit in bank A, 90$ loan out to become deposit in bank B, then 81$ loan out to become deposit in bank C and then 72$ loan out to become deposit at bank D ….

Jdog, say BOA wants to make 90$ loan but have NO cash, say BOA immediately borrow 100$ from CITI, and now BOA can lend. But Citi has to have 100$ cash to lend to BOA. There is a deposit required somewhere but after all of these interbank lending and borrowing, it gets very hazy and hard to know the true limitation on reserve or capital requirement. One thing I do know is this. If BOA wants to make loans and NO other banks are willing to lend to BOA, the FED will lend to BOA. Ding! Ding! Ding! Money created from thin air. All the other regulations on banks and these “systems” are just created to hide this “last resort” which is a printer.

JZ,

Interbank lending is down to almost nothing in the US. Even before the financial crisis, it was never a large source of funding, given the gigantic size of the US banking system. But interbank lending has since plunged to near-nothing. So your elegant theory doesn’t really apply.

>>The reserve requirement stipulates that the bank send a portion (such as 10%) of the cash it gets from deposits to the Fed to be put on deposit at the Fed.

I would like to revisit that statement a bit, because it is not quite accurate as written. The member banks do not have the power to *create* reserves for themselves by “sending portions of cash deposited” to FRB. Reserves are created ONLY when FRB buys bonds (generally US Treasuries, sometimes “agency” MBS) on the open market and issues (credits) reserves against the bonds to the primary dealer bank that was the ultimate mediator of the bond sale, from whoever was the owner of the bonds, to the FRB.

Any given bank can accumulate more reserves only if another bank sheds reserves, unless FRB issues more reserves. The main concept to keep in mind is: Reserves are the currency of interbank daily debt settlement. Daily settlement of interbank debt is the main function of reserves. Most banks end up with a quite small NET settlement imbalance every day, because most banks most of the time have only a small imbalance of withdrawal versus deposits (or outgoing versus incoming payments, if you will). But when a bank customers (or banks themselves) have losses, as when there is a financial crisis, a banks reserves can dwindle. Then the bank has to find another bank that is willing to lend them the difference overnight, which will replenish the reserves of the lossy bank because, well, the loan takes the form of an incoming payment that reduces the net transfer of reserves out of the lossy bank. Oh, and finally, if the lossy bank cannot find a counterparty that will lend to them, then they will go begging at the FRB discount window, where FRB will create temporary reserves against some collateral (bonds) offered by the lossy bank. And if things get REALLY bad, FRB will do “permanent” (POMO) purchases of bonds, to create more reserves. One example of such is the QE1 program. But each individual FRB member bank does NOT have the power to *create* reserves.

The above illustrates the mechanics of reserves as the currency (or unit of account, if you will) for interbank debt settlement. It also illustrates that when loan losses are bad, FRB will create more reserves by accepting more bonds, and often of a lower quality than UST bonds, in order to let weak banks build up their reserves to a level required by their liabilities. But it is also clear that FRB member banks do not CREATE reserves themselves by “sending portions of cash deposited” to FRB.

Justme, I think all you are saying is that the banks have account at FRB in same way you and I have account at bank of america. The banks settle at FRB like you and I settle at Bank of America. The reserve we have is BOA is like banks reserve in FRB

FWIW, the source for Jdog’s Alan Holmes citation is https://www.bostonfed.org/-/media/Documents/conference/1/conf1i.pdf .

Please read the article: you totally missed many points including that there are two kinds of reserves: Required Reserves and Excess Reserves. The first account for only about 12% of total reserves, the second for about 88%. Excess Reserves are voluntary. They’re based on a profit motive by the banks.

And this article has nothing to do about taxpayers paying interest. It’s the Fed that is paying this interest to the banks, instead of handing this money to taxpayers.

What else would you expect a corporation to do? Its primary responsibility is to its stockholders, the member banks.

Wolf, I have to quibble here since usually you’re better than this statement: “And this article has nothing to do about taxpayers paying interest. It’s the Fed that is paying this interest to the banks, instead of handing this money to taxpayers.”

That’s a distinction without a difference. The Fed+Banks created a scheme. The Fed made up “interest on excess reserves” and now that new “interest” is going to banks INSTEAD of taxpayers. It’s entirely fair to rephrase that as taxpayers are (effectively) paying interest to banks.

Prior to 2008 there was no IOER, and all Fed holdings paid interest to taxpayers. Now the Fed “pays interest” to banks (that it doesn’t legally have to!) and pays less back to taxpayers. Mathematically that’s equivalent to taxpayers paying interest to banks.

One wonders how this was even legal.

Thank you. Without a formal accounting, how do we know what the Fed “expenses” are that you mention? Isn’t that an area of uncertainty regarding their profits? Thank you.

The Fed has a “formal accounting,” as you say: its audited annual report. The audited 2018 version will be posted on its website when it’s ready later this year, and you can dig though all the numbers.

All its audited annual reports are here:

https://www.federalreserve.gov/publications/annual-report.htm

Off course everything gets twisted in banking conversations, by haters, who can niot understand banking necessities, so hate banks and the fed simply as its a “cool” thing to do.

These people are sad, they do not Hater the Sewage Systems that make their cities inhabitable, but they hate the banks that make their financial systems work.

Banks are exactly the same as Toilets and Sewage Systems.

Something a modern financial system, can not function without.

The problem is not the US bank’s, or the people that operate them.

It is the People in the US who Enact the regulations for them.

Blame the FED blame the Banks. Much easier than actually solving the US Bank problems. In CONGRESS.

Why blame the Fed (and banksters) when we sheepies are always at the ready, begging to be fleeced? They are doing God’s work!

Okay, so if I understand this right, the Fed here is just acting as a pass-thru between the banks as lenders and the Treasury as borrower. Overall the banks are lending their “excess reserves” to the Treasury and earning interest on them. Of course the Treasury is paying interest on its debt.

The problem as I see it then isn’t that the Fed is acting to funnel wealth from taxpayers to banks – taxpayer costs were decided by Congress when it ran up those massive deficits – it’s that the banks aren’t paying squat to the original lenders, their depositors. Net-net people are lending vast sums to banks who in turn are lending to Treasury, and Treasury is paying big bucks in interest but it’s not flowing through to the ultimate lenders of those funds.

Dear Wolf,

There appears to be a circular arrangement between the Fed, banks and Treasury which appears to be designed to distribute profit to banks at zero risk.

I do not fully understand how this apparent circular arrangement works, permitting banks to “siphon off” profits.

It would of great help to me if are able to describe the full cycle in a manner an “ordinary” person can understand.

With regard

$849 million for producing, issuing, and retiring currency

Seems like a lot of money to convert air into paper.

I’d like to know the figures on how much was produced, issued, and retired lol…

I see dollar demand is down to around 60% on global markets that leads me to believe the world is moving out of dollar reserves.

Could this be a cause for the fed paying banks this interest?

There is a huge demand for USD currency globally. Demand has picked up since the Financial Crisis. Folks are hoarding this stuff. There is now over $1.7 trillion in USD currency stashed away globally. This is double the amount before the Financial Crisis. This is called “currency in circulation.” This $1.7 trillion is a lot of paper. It wears out and has to be replaced, etc.

BTW, currency is not an asset on the Fed’s balance sheet, but a liability.

Thanks Wolf, I noticed you did an article on it back on Dec 31 which covered 3rd quarter data.

Ah well, much better than spending that 65 billion on social programs to improve society. After all, that’s horrible socialism, and we don’t do that unless it benefits the wealthy.

Real test of the Yellow Vest movement will be to see if they can pull off this deliberate bank run on the weekend. If they succeed a new global tactic will be born, if not the Yellow Vest movement will be a bit of a fizzer

Yup! A great idea indeed!!! I very much hope they pull it off.

Couple of advantages to this idea…

1. You bring one down, you can get a cascading effect

2. It can be replicated all over the world.

As Maxime Nicolle, said a “tax collector’s referendum.” Indeed!!

Really time to bring the banks down along with the banksters, central bankers and politicians. They have had a ball fleecing us for the last decade (on top of bailing out banksters in the guise of helping common man). Time to get our own back!!

Problem is, “The guv’mint” will embargo private accounts and limit withdrawals, e.g: Greece, 2015.

Then the yellow vests will have to decide what to do next. There are those that believe that a full-blown revolution is the only way the oligarchy can be removed from power.

“….Problem is, “The guv’mint” will embargo private accounts and limit withdrawals, e.g: Greece, 2015….”

Panic early and beat the rush

they will just be skimming off excess liquidity for at least another 20 months… which takes up to Q42020 and sub $500bn excess reserves.

Wolf – what is the total paid to banks (foreign and domestic) in IOER since QE started? How does that total compare to the increase in net capital over that period for those same banks? Basically I’m asking how much of the recapitalization of the banks over the past 10 years was simply a direct subsidy from taxpayers.

The chart I included (4th from the top) goes back to 2015, which is when the interest payments got serious because the Fed started raising rates. Over the span of the chart, going back to 2015, the total amount in interest paid on Excess (IOER) and Required (IORR) Reserves was $83 billion.

Note that the Fed didn’t use to pay interest on required reserves before all this started.

This came too late to recapitalize the banks. By the time this flow became big, the banks were already allowed to buy back their own shares and pay dividends, which goes against recapitalization.

Banks should be nationalized. They have become even fewer, even bigger, and more “too big to fail” be design since 2008.

Wolf, it would have been helpful for your article to include some context on what the $38 billion in IOER means to the banks. It looks like US banks’ profits in 2018 were in the $200-$250 billion range, so the $38 billion handout from the Fed is maybe 20-25% of total bank profits. Not bad money for taking no risk at all!

But now the banks “earnings” (hard to call it that, in this case) and hence stock prices are dependent on that flow. The Fed is draining the Excess Reserves, and appears to have paused on raising rates, so the flow is drying up. Unless something else improves, bank earnings will drop 20-25% over the next 2 years as IOER vanishes!

Perhaps this explains much of the Wall Street Crybaby behavior? Obviously they can’t directly complain that “you’re taking away our taxpayer subsidies!”, so the whining is coming in other forms… And there’s more to cry about anyway.

Will come back later today and read through this post thoroughly; for now:

Wolf, as I think about the topic of the Fed, and how its actions affect/have affected different economic strata, I am repeatedly very much impressed by how accurately and objectively you cover this subject.

Again, thank you very much.

What about the billion spent on board of governors’ expenses?

Craft brews? Why didn’t they invite me?

Who are the owners, if I may ask? Get specific.

It is a little more complex than is being made out. Justme gave a clear explanation on how reserves are created, they are an interbank tally at the central bank, and cannot in themselves be cashed in or out of directly – the central bank creates and destroys reserves.

As to whether banks profit or not (well they do if only because the value of the market they trade/own is monetised and accounting made whole) is a different kettle of fish. Banks mostly acted as intermediaries in the asset purchases that were used to create new reserves, so the question is how the monetisation of the asset classes and the cost of bank intermediation plays off against IOER.

https://economic-research.bnpparibas.com/html/en-US/QE-bank-balance-sheets-American-experience-7/23/2015,25852

Explains (first three pages only for basis) how depositors and households (read the financial sector) were rewarded, how much excess reserves landed with foreign banks based in the US etc. Basically it looks like the fed monetising and guaranteeing “the system”, it’s all skewed and towards whatever ends so don’t ask me to explain, and thanks for all the fish, you’re welcome I’m sure.

Yes, they guaranteed “the system”.

They did not want another Depression.

Choices were made by the boys in the club.

I certainly didn’t agree with those choices, but they worked.

All water under the bridge, lets pay attention and figure out what their ongoing plan is.

First and foremost, they created, Confidence.

This imho, is why the Markets will continue to rise.

I know Wolf and most others disagree, supported by

irrefutable fundamental facts and charts, which in the long run won’t matter for the general Markets.

The FED has the Markets back. Yes it is not fair, but at the same time the Markets will benefit all that are invested in it. Most especially Pension Funds.

I have had the mindset that the Markets can’t possibly continue upward based on the evidence available, until Trump got elected. Love him or hate him, he is no savior, we already had that with Obama.

Trump altered the status quo, and that’s when it hit me that the FED did the same in 2008.

When we get the retest of the recent lows, I will slowly start buying back in for the long haul.

Of course I’m no genius so I’ll have my sell stops in place, just in case.

Looking forward to Wolfs upcoming article on Kraft Beers, and how they are changing the landscape of the beer beverage market.

They’re really rich and live in penthouses with tons of computers and nerds in the floors below and often have walking sticks and start wars.

Your turn.

We could buy 8 border walls with that money and have enough left to reopen the government!

Hahahahahaha….

Right, I’m laughing too.

So the Fed – how shall I put it ?- has a great deal of control over interest rates. They present themselves as moderators, a force against excursions into extreme, destructive economic territory.

In that light, I find Barry Ritholtz’s chart of “Long-Term Interest Rates Back to 1790” (for the U.S.) instructive. It’s a simple chart of interest rates, the y axis showing rates, and the x axis showing years. Nothing logarithmic, no higher math involved….but what’s that parabolic curve ? …oh, I see, but this can’t be right, that wild excursion occurs AFTER the creation of the Fed (“Federal Reserve Created” is indicated on the chart)…..

What are the governors spending $838 million on? Nearly as much as it costs to do its work

Just curious – who completes the annual audit of the Fed??

KPMG

We will not have honest markets or sound money until we end the Fed. This criminal private banking cartel has been rigging the game in favor of its oligarch handlers and our corrupt financial sector elites ever since its misbegotten creation as “The Creature from Jekyll Island” in 1913.

Who voted on this?

Milton Friedman was for the Fed being paid on required reserves….but was he for payment on excess reserves?

The Fed also pays 6% on the required stock ownership by member banks.

And where is it written that the Fed must pay more and more interest on these excess reserves?

The Fed has self authored their powers all based on the “emergency” of 2008.

Wow! There sure is a wide range of opinions expressed here on how basically the FRB functions. I’ve gotten the impression over the years that even among those politicians who are supposedly running things we would also find a wide range of contradictory opinions.

One isolated fact I think I know: Before the Fed started paying interest on excess reserves in 2008 the practice was to sell the banks enough T-bills to keep their reserves fairly small. Reserves that payed no interest at all would tend to be lent to other banks at any non-zero rate, pushing rates down and sometimes interfering with the Fed’s objectives in setting the rate. When QE came in the FED was trying to net buy T-bills, which inevitably increased bank reserves and led to the need to pay interest.

Key Goodwin,

This is funny…. But you see, the Fed should have never ever done QE in the first place. It was the biggest wealth transfer from labor to capital and from young people to asset holders in the history of mankind. It destroyed the value of labor with regards to assets, such as housing, and capital-intensive services, such as rent. “Housing crisis” – meaning middle-class people, such as teachers, can no longer afford housing – that’s the result of QE whose sole purpose was, according to Bernanke himself, to inflate asset prices to produce the “wealth effect.”

So now, you defend and justify the Fed’s paying the banks $38 billion a year in easy profit, taken from the taxpayer, because it allowed the Fed, in your view, to push and maintain this wealth transfer? I’m not sure you realize just how funny this sounds to others.

Hey, I’m not justifying anything. That post is just an explanation I’ve read of how the Fed used to operate and how it had to change because of QE. No approval was implied.

I think that the Sub-prime Mortgage crisis was a debt bubble financial crisis like others before it. A standard Minsky Moment, but bigger this time, facilitated by mortgage fraud becoming a standard practice throughout the industry, regulators failing to act, ratings agencies helping to hide the fraud, and so on. Ever since, the powers that be have been trying to find a way out with minimal damage, especially to the powers that be. Of course what should have happened was that all the banks should have been shuttered with their shareholders losing everything and their management punished. But politics would not allow, so we’ve got unconventional monetary policy instead.