“In 30 years, I’ve never seen anything like this”: CEO of warehouse operator Pacific Mountain Logistics.

Sales at merchant wholesalers (except manufacturers’ sales branches and offices) fell 1% in December 2018, compared to November, to $497.2 billion on a seasonally adjusted basis, and inched up only 1% compared to December 2017, according to the Census Bureau estimates this morning.

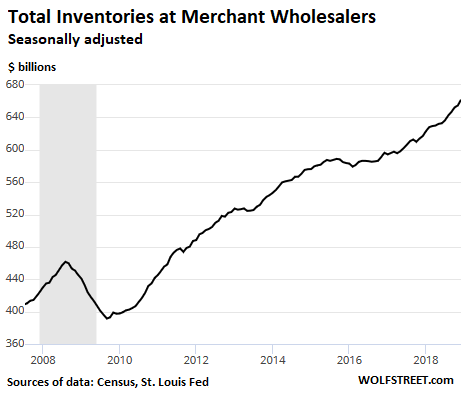

But inventories at these wholesalers rose 1.1% from November and jumped 7.3% from December 2017, to $661.8 billion. Over the two-year period through December, inventories have risen 11%. This includes inventories of durable and non-durable goods (we’ll look at them separately in a moment):

This surge of inventories on soft sales caused the inventory-to-sales ratio to spike to 1.33, up from 1.30 in November and up from 1.25 a year earlier.

This is a familiar pattern. As inventories are piling up, and as inventory carrying-costs rise, companies eventually react: They whittle down their inventories by cutting orders. As we have seen in 2015 and 2016, this hammers the goods-based sectors of the economy. In 2016, it dragged GDP growth down to just 1.6%, the worst growth rate since the Great Recession. The overall economy was barely kept out of a recession by the service sector.

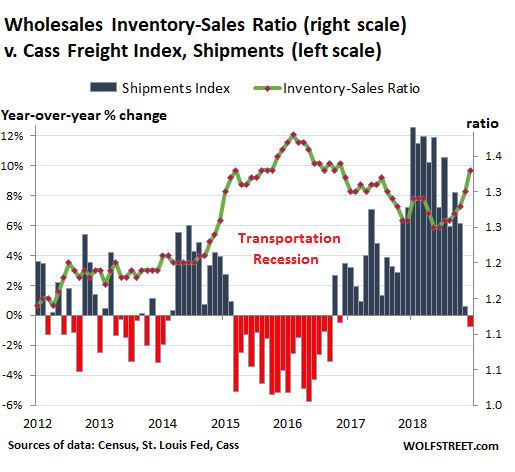

The transportation sector tracked this perfectly as it fell into a steep recession in 2015 and 2016. Now a similar pattern is starting to form: A surging inventory-to-sales ratio as inventories are piling up, while shipment volume of goods, as tracked by the Cass Freight Index, have started to decline on a year-over-year basis.

The Cass Freight Index covers consumer and industrial goods shipped by all modes of transportation — truck, rail, barge, and air — but does not cover commodities such as grains.

I overlaid the two data sets: The Cass Freight Index for Shipments, expressed as percent change from the same month a year earlier (columns, left scale), and the inventory-to-sales ratio (green line, right scale):

Non-durable goods not helpful.

Sales of non-durable goods — food, gasoline, apparel, agricultural products, etc. – at wholesalers fell 1.4% year-over-year in December, even as inventories ticked up 2.2% to $251.2 billion.

The standout here is the category of petroleum and petroleum-products inventories. Inventories and sales are valued in dollars, and the sharp drop in crude oil prices since August caused the dollar amount of petroleum and petroleum-products inventories to drop 12% year-over-year in December. Between September and December, inventories plunged 21% in dollar terms to $20.4 billion.

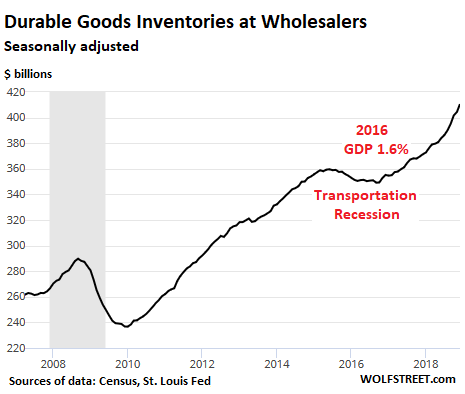

The problem is in Durable Goods Inventories

Sales of durable goods by wholesalers ticked up 3.5% year-over-year in December to $245.6 billion. But inventories of durable goods at wholesalers surged 10.6%, to $410 billion – the steepest increase since 2012, the period of inventory restocking coming out of the Great Recession:

Here are some standout categories, in terms of percent change in December 2018, compared to December 2017. Note the three categories with double-digit jumps, two of them relating to the construction sector:

- Furniture & Home Furnishings: +8.9%

- Motor Vehicle & Motor Vehicle Parts & Supplies: 7.3%

- Machinery, Equipment, & Supplies: 12.7%

- Hardware, Plumbing & Heating Equipment & Supplies: 12.1%

- Lumber & Other Construction Materials: 14.9%

- Household Appliances & Electrical and Electronic Goods: 6.5%.

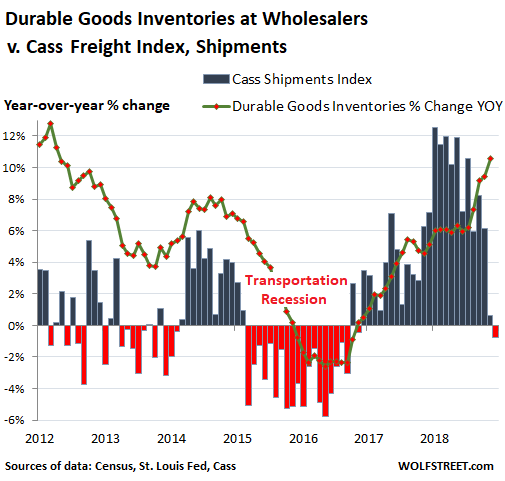

The chart below compares the year-over-year percent change in durable goods inventories at wholesalers to the year-over-year percent change in the Cass Shipments Index. Note the turning point in shipments late last year. Inventories follow with a lag.

This situation of ballooning inventories on soft sales is showing up in the warehousing industry – and it’s getting blamed on companies trying to front-run trade tariffs. The surge of imports ahead of the potential tariffs – coming on top of the usual increase of inventories ahead of the Chinese Lunar New Year – has left warehouses and shipping terminals in Southern California “overstuffed and distribution networks jammed,” the Wall Street Journal reported.

“That stacked-up inventory is straining logistics capacity around the neighboring ports of Los Angeles and Long Beach, which together comprise the biggest U.S. trans-Pacific gateway,” the WSJ. It quoted BJ Patterson, CEO of warehouse operator Pacific Mountain Logistics in San Bernardino: “In 30 years, I’ve never seen anything like this,” he said.

Increasing inventories is counted as a business investment and is added to GDP growth; This is what has been happening much of last year. But conversely, the inevitable decline in inventories will be subtracted from GDP growth.

Apocalypse not now

The goods-based sectors comprise the smaller part of the economy. The services sectors dominate. The biggest of them are healthcare, finance, and housing (rents are services). In the US, you cannot get an overall recession with just the goods-based sector slowing down, as we have seen in 2016. It will pull down overall growth in the economy but won’t push the US into a recession. For a recession to happen in the US, the services sectors need to approach the zero-growth line, while the goods sectors are in decline – and that is not yet in sight.

Something has to give. Read… What Trucking & Freight Just Said About the Goods-Based Economy in the US

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

LoL, oceans of stuff made in China, Mexico, Vietnam, etc…

So I guess if housing slows down, the goods economy suffers a meltdown.

Meh. Assets are the biggest bubble, and if they slide again, no guarantees are going to be sufficient to reignite a bubble.

The Fed should have promoted the 3-6-3 world of the 1950s and pushed taxes back up to balance the budget. Stop the wars, etc. Now we are going to have a war exhausted economy that won’t respond to stimulation.

GLTA, and now asset bubble prices will have to be supported out of domestic savings.

Ha!

CitizenAllenM! Wow, blast from the past. Good to read you again.

Has been several years since the CR comment section. Hope you are well.

Oji

Hi also remember CitizenAllenM from the good old days – perhaps Calculated Risk?

Did you see the video of the Chinese shipping container transformed into a house in 10 minutes? Of course this wont happen en masse for our homeless because of the Currency parameters.

No, but I have seen lots of houses transformed into shipping containers. The currency parameters are regulatory (permissions, fees and taxes) and resource ones (e.g. land or services), because you are able to build as good or better without container for same cost. Add to this that the wealth, convenience and social activity tend to be concentrated around large cities which act like magnets, but ones which don’t resolve the result of their being so. I don’t know, maybe it needs an idea for setting up ok quality towns/communities in much cheaper areas where there is still some kind of focus and activity involved. At the end of the day it’s up to people to make their neighbourhood , so avoiding just creating ghettos is another problem.

Ridiculous…10 min conversion,,, must be some good stuff you’re smoking

China Expandable container house —10 minutes one house!

https://www.youtube.com/watch?v=mya2cMDACKg

Well, they don’t build it in 10 minutes. And it’s not a shipping container.

It’s a prefab house folded and packaged into the shape of a shipping container. The thing is manufactured somewhere else, trucked to location, and unfolded into a basic house in 10 minutes. No telling how many weeks it took to manufacture this thing.

In his next speech Poloz will say he was reading the internet and discovered a contraption that prints modern money faster than anyone thought possible.

Montainer, an American company, has been doing this for a long time:

http://elmacontainercabin.com/

They aren’t cheap, but they acutally comply with the building code (IBC 2015), which is pretty astonishing if you think about it. They even pull the permits for you.

Channel stuffing, not supposed to work like a lot of other things. When a company does it illegal, when a country does it?

The stuff here was ordered here.

We’re not in a recession officially, which is a joke.

Back off the annual US federal deficit of about $1.2T from GDP growth and you’ll see the recession. It’s been going on for many years.

Increases in debt, in excess of GDP growth, are masking a recession.

Wolf, you should start citing an adjusted measure of GDP growth, which excludes the annual deficit. They like to use the term “Real GDP”, but maybe we need a “Real Honest GDP” or “Real GDP, Ex-Fluff”.

Yes, GDP is a terrible measure among other reasons because it measures the flow of an economy (dollars being spent or invested) without accounting for where these dollars came from (earned, borrowed from the future?).

Nor does it measure whether the spending is actually ‘healthy’ for the economy. The cost of providing pointless or counterproductive regulations is a good example of that. It’s the bureaucratic equivalent of the ‘broken window’ fallacy. GDP also ‘rewards’ inefficient spending in business.

The word “economy” used to mean an efficient use of one’s resources.

Now the economy “improves” when more money is spent, whether it’s on yachts, 3rd homes, or to repair a whole state wrecked by a hurricane. GDP counts it all without caring for well-being or the future.

To put more color on it, preparing for a hurricane properly by, say, not building in low areas or building strongly and on stilts, which husbands resources, counts for less than repairing to the same vulnerable state, if it’s more expensive to repeatedly repair the property . . . like some idiot who doesn’t care because the rest of us are paying via insurance, some of it taxpayer-protected, i.e. taxpayer-paid.

Gross Domestic Product is such a good description, I wonder if it was given that name on purpose. Add in Easing, Excess Liquidity and a bit of Trickle Down, and the reminder is “better leave the plumbing to the pros”.

Disclaimer :

I am not in any way associated with Rudy Barf and Co. Sump, Pit and Sewer Merchants Est.1934

“The welfare of a nation can scarcely be inferred from a measure of national income.” Kuznets

Would not GDP also pertainto our resourse wars, or unfactored externalities pushed by Big Corpserations as they relate to the destruction of the biome on both a local and global scale, or of the DeathCare facilitators e.i. the Pharma, Medical, Insurance Triad, with their abiltity to rake in $$$, effecting positive outcomes for everyone but the serfs … ect. ect.

This is still the good times but they are getting less good that they were before.

“not yet in sight”.

The expected and looked for recession has been postponed.

Ain’t gonna happen! Not until after the 2020 election cycle.

The powers that be, will most certainly see to that.

The economy must be seen as healthy and growing to the paroles.

To be viewed otherwise, would cause those who depend on “happy time stories” to have their propaganda disbelieved. Can’t have that!

The indexes are tracking the value of these goods, but what about the actual numbers. Are there ever increasing stacks of washing machines, etc, or is it just about the same number that are nominally worth more?

And what are those valuations worth if they aren’t selling? Does the correction to value only happen at the point of sale?

If there are more physical numbers of goods, where are they stuffing them? Disused malls and factories? Logistics companies I have worked for have their space calculated pretty fine, and can’t just store double the physical volume of goods.

I haul out of a distribution center that serves a certain big box home improvement chain. They are stacked to the hills with and shipping way less than they were a year or so ago.

Stores measure MOM sales by dollars, not units. An assumed increase in sales can be just a higher price. I worked in a large retail distribution center for ten years. They are not concerned with price, but with units per month and cost per unit. They can give you the real numbers.

Yes, just talking about the dollar amount doesn’t tell the whole story. Goods not moving in a just-in-time system hits producers in no time.

Aren’t almost all sectors of the economy effectively offshoots of the finance sector?

So inventories were consistently rising since 2009, just like the stock market. Winning.

Who is taking the most risk on these inventories?

I really would like to know if the cost of residential construction is likely to come down?

Inventory is up around here in the DFW area, but people are still moving to Dallas and it’s crowded here. I wish I could make it stop.

45% of new residents in the last few years (I think 5 years, maybe 10, I’m not sure…info from Community Impact local newspaper) came from overseas.

I need a house, I have the land, but construction cost is way up.

I do my own house construction. I’m in Canada but some basics are the same. Lumber costs are up, regulations are always increasing, inspections are slower and more expensive, and there are not enough good tradesmen. None of this will change any time soon. I suggest building your own, as I do. You may want to get professionals in for foundations and the like, but framing is easy. Alternatively, find a handyman special. If you don’t have the time, find some recently retired skilled tradesman who needs the money. He’ll want to work slow but will work good.

This article about Texas says just that:

https://www.statesman.com/business/20180907/shortage-of-texas-construction-workers-leads-to-higher-costs-delays

“I suggest building your own, as I do.”

Me, too.

Wolf,

Thanks.

No real surprise here. Just-in-case inventory management pulled out of mothballs to front-run the tariffs. Corporations ordered everything that might ever be needed…just in time for the next recession.

Yes, there may not technically be a recession at the moment but strip away inventory building and the U.S. economy is likely at stalling speed ( sub 1% growth).

The inventory build is over. Let’s see what GDP looks like by Q2. Might be close to flat-lining.

QE pulled forward too many years of demand. Here comes the void.

Wow. The graph of durable goods vs. freight index tells the story perfectly, doesn’t it?

Agree on economic impact, though. I don’t think people realize manufacturing represents less than 10% of jobs these days. It would take some pretty epic layoffs in the sector to bring unemployment back to “normal” levels.

One downside to heavy automation is you can’t layoff a robot. It’s way better to run it at breakeven than mothball it, which requires write-offs.

Everyone tried the “go upmarket” silver bullet over the last couple years. Now, the game will be “keep the robots running”. This means means round after round of de-contenting until manufacturers meet the market where it actually is, rather than where they’d like it to be.

It also means margin compression and the attendant stock price corrections.

Little doubt retailers are front running tariffs.

A sag will happen whether tariffs occur or new trade deals are signed.

Central bankers will do the only thing they know, print more money!

– But Central bankers don’t lend to households or companies. Whether or not households or companies can borrow money is a decision made by the commercial lenders/banks etc.

I strongly suspect “tariffs” is the US version of “Brexit”: the adult equivalent of “the dog ate my homework, honest miss”.

I have this lingering feeling the reason is a whole lot of people massively overestimated sales growth or, to be more precise, the ability of a conjunction of factors to sustain 2017 levels of growth indefinetely.

Now that they are stuck with growing piles of unsold goods that should not have been ordered in first place, the game is on to find a ready-made culprit.

Wolf,

I think there is one critical difference between this slowdown and the slowdown in 2015-2016. That slowdown was imported from a weakening global economy, while US consumers seemingly in pretty good shape then supporting the domestic economy. This slowdown the consumers don’t seem to be as supportive as indicated by Total Vehicle Sales, Housing Starts/Permits/Existing Home Sales looking as if they are rolling over in a very bearish way. The Dec. Real Retail sales was disaster…. I wonder if this gumming up of inventories at the warehouses is just another sign of consumers in the early stages of a retrenchment from a loss of confidence. If so then this weakness we are seeing is likely to be recessionary. But with employment numbers so strong it’s hard to make the case for consumers retrenching.

Bing Wong,

December retail sales, according to the initial and somewhat dubious estimates, were not good, to say the least. We will get revised retail data for late 2018 over the next few months, so we will see if December retail downturn is confirmed. Here is what I wrote about it:

https://wolfstreet.com/2019/02/14/why-im-not-in-panic-yet-over-dreadful-retail-sales-that-fell-most-since-2009-but-nervously-look-at-the-trend/

“But with employment numbers so strong it’s hard to make the case for consumers retrenching.”

94% percent of jobs created recently are part time or temporary. That’s new.

Employment numbers are most definitely not strong. They are weak. Very weak.

If they were strong, wages would be rising. Wages are not rising.

Go look at the methodology for the employment numbers. Government wants people to think employment means a well paying full time secure job, with benefits.

Full time means 35 hours a week. Pay, job security, benefits are not considered.

As for openings, I have one job application open with the Government where the funding for the post was put on hold. I sat tests for it. The post is still “open” three and a half years later. Because the funding may be restored any time, it counts as a job opening.

..and if you think that Government creating thousands of “job openings” for which they will never actually have to hire and pay is in any way accidental, then I have a bridge to sell you ;)

I am pretty sure private enterprise does the same thing. They keep advertisements out even when they are not actually hiring.

Sometimes they do it just in case the “perfect hire” shows up. Sometimes, for their most common jobs, I think it’s just as easy to keep the ad up as take it down for a little while or easier, saves a couple of phone calls.

I know my last company had hiring freezes from time to time but still had open ads while in the freeze.

“Wages are not rising.”

?

https://www.bloomberg.com/news/articles/2019-01-04/u-s-payrolls-rise-312-000-wages-top-estimates-in-jobs-blowout

With all the ‘wages rising’ stats, you have to know wages per hour AND average weekly hours AND taxes housing costs AND real inflation AND population growth. Cherry picking any one or two of those that happen to look good that month is just that, cherry picking.

Literally everyone I know, bar one, in 4 countries, has seen their actual disposable buying power decline steadily since 2008, typically at 2%-3% per annum. Most have been promoted at least once in that time, which provides a jump, but they are worse off now that they were in 2008.

The one who is better off sold his 3 travel agencies in 2007 and retrained as a plumber. He has more work than he can do.

If not direct offshoots, financialization means that the financial sector has become a too large part of the economy, having grown 4x or 5x in only a few decades. Then there’s central bankster manipulation…

Bing Wong bing light methinks…

Are you sure that companies are not stocking up with Chinese goods in the event of import tariffs on Chinese imports to the USA?

Wolf mentions that as the reason.

He also continues to point out that this counts as GDP today and will count against GDP in the future, which is interesting.

@Wolf Richter:

– Can you redraw the first inventory charts but now with “change/delta (yearly/monthly/quarterly) inventory” ?

Yes, I could but…

Inventory is very seasonal, and the data gets revised sometimes heavily for the next few months (always does). MOM percent change data is only as good as the seasonal adjustments. And the revisions impact it the most. I mentioned MOM in the article but it’s essentially useless data except for getting perhaps some additional color. I can create a chart based on MOM but it would be a useless chart.

QOQ is only a little better than MOM.

YOY percent change data is not impacted nearly as much by revisions. It eliminates the impact of seasonality. So it’s a lot more on target than MOM percent change data or QOQ percent change data, in data sets like inventories and retail sales that are very seasonal.

– With interest rates so low the cost of storing all those imports is also very low. Just guess what the storage costs/inventory costs would be when rates were at say 10%.

– I that regard it would be VERY helpful when rates were much higher. But the FED follows the market rates and those are very low.

– I recently came across one other disturbing figure. The Purchase Managers Index of the metro Milwaukee area dropped from 71 in may 2018 down to 53 in december 2018. That’s a HUGE drop. Ouch.

Not yet, but darn close considering debt, rising living costs, housing, retail, restaurants etc.

For what its worth, in my (extremely) niche market – which nevertheless correlates very closely to macro-economic performance over the last 20 years – orders from the US, our biggest market, have simply cratered since early 2018, having started to turn down in late 2014.

One long slide, as far as I can see, with a marked downward jerk in 2018……

And orders from China, which was less significant but growing, have simply vanished in the same period.

The problem with an economy that is service based is that services for the most part do nothing to build wealth. Money spent on goods, is invested in something tangable in which at least some value is stored in the asset, and can be resold. Services are intangable, and usually not an asset which can be resold.

Based upon your charts and information it looks like import inventory could be trying to front run potential tariffs for future demand while the transportation sector is looking at a slowing demand from the retail sector.

Slowing demand from the corporate sector also. A lot of companies are becoming wiser on their inventory holdings also to improve cashflow reduce their stock holdings. Buy only when required, rather than for the sake of it.

I really like the CBO.gov- 2019-2019 budget projections and some of the other charts on the same page for the full picture.

darn, the excel won’t copy, but here’s the link when you compare revenues, and taxes etc for 2018 to 2019, it sure gives the real focus, of reality.

https://www.cbo.gov/about/products/budget-economic-data#3

Click on that Jan 2019 ikon under the 10-year budget projections. Sure makes it easy to then not have to be swayed too much by the interim “demand” predicaments, a lot of the daily, weekly, monthly variances just seem to be interim- flushes-down-the-drain.

Alongside the 10-year economic projections- pretty much shows where we’re heading, it’s pretty obvious. The daily “news” is pretty much confirmation of the “plan”.

https://www.cbo.gov/about/products/budget-economic-data#4

Quarterly updates- so long as there isn’t another Gov shutdown, which in my book is probably just to not have to update any of the books again for a while, to keep all the ones that are supposed to be kept in the dark, really in-the-dark to the max! That’s just being negative about the whole grand plan.

Judging from the longer term picture, these inventories appear to be a minor matter. So you discount on your current inventory, get rid of the excess and use tighter controls in the future. I assume that’s what you did when your car dealership bought too many cars.

This appears to be cyclical and normal. Boom and bust.

https://fred.stlouisfed.org/series/S4236SM144SCEN

https://tradingeconomics.com/united-states/wholesale-inventories

To me this article screams that it is only massive and unsustainable deficit spending that continues driving our economy forward. The bottom-line is that we are in the midst of a “false economy” and it is only by the grace of this huge deficit spending that we are not languishing at the bottom of a deep economic pit.

Today late cycle indicators are on the rise, moderating growth, tightening credit, declining earnings, the peak of consumer confidence, rising inflation and more. Deficit spending is not a silver bullet without consequences and with each step forward we get closer to the end of the road.

This is why investors would be wise not to accept America’s recent GDP as verification the economy is hitting on all cylinders.