Fact is, home prices cannot outrun wages forever.

The market, if it’s allowed to, can fix the affordability problem that exists in many cities in the US by finding price levels were first-time buyers can afford to buy a home with the income they’re making. At its glacial pace, this is starting to happen in some markets, with sales volume dropping, and inventories rising, and sellers having to step down the aspirational ladder to make deals. In some of these markets, price levels have a long way to go before they make sense, where a household with a median income on the local scale can afford a median home. And there are now enough local housing markets that have turned south to where the impact is starting to creep into national averages.

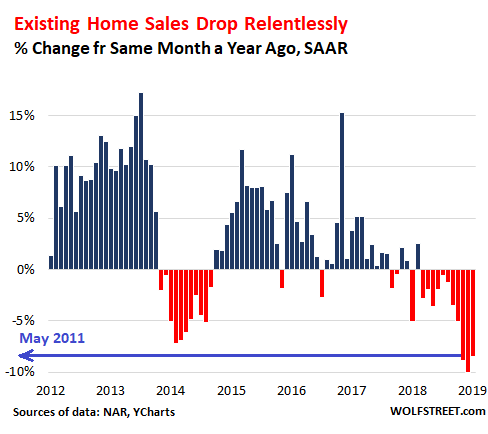

Sales of “existing homes” – single-family houses, townhouses, condos, and co-ops – across the US in January dropped 8.5% from a year earlier, to a seasonally adjusted annual rate (SAAR) of 4.94 million homes, according to the National Association of Realtors, after having dropped 10.1% year-over-year in December and 8.9% in November. All three were the biggest year-over-year drops since May 2011, during the final throes of Housing Bust 1 (data via YCharts):

This decline in sales volume is occurring despite the large drop in mortgage rates since early November. But hope continues: “Existing home sales in January were weak compared to historical norms; however, they are likely to have reached a cyclical low,” according to the report. “Moderating home prices combined with gains in household income will boost housing affordability, bringing more buyers to the market in the coming months.”

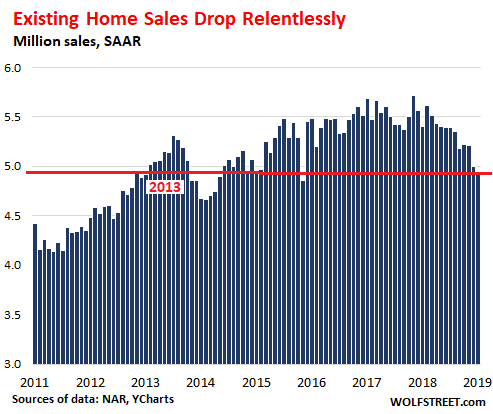

I’m not sure about the reasoning, but it could very well be that home sales ratchet up from here because nothing goes to heck in a straight line. The chart below illustrates the decline in home sales volume since late 2017 (data via YCharts):

By category, sales of single-family houses in January dropped 8.4% from a year earlier to a seasonally adjusted annual sales rate of 4.37 million. Condo sales dropped 9.5% year-over-year to a rate of 570,000. By region, with the West consistently in deepest trouble:

- Northeast: -1.4%, to an annual rate of 700,000.

- Midwest: -7.9%, to an annual rate of 1.16 million.

- South: -8.4%, to an annual rate of 2.08 million.

- West: -13.8%, to an annual rate of 1.00 million.

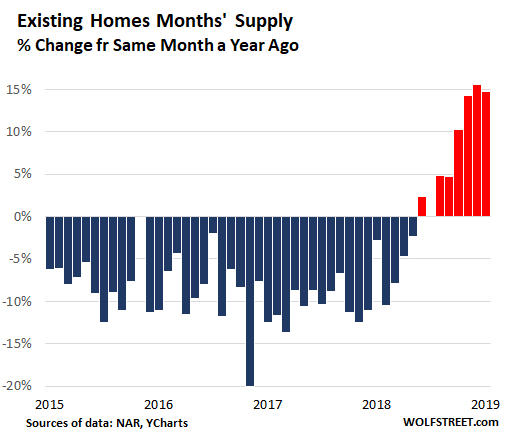

Inventory of homes for sale at the end of January rose 4.6% year-over-year to 1.59 million homes. At the current rate of sales, this represents 3.9 months’ supply. This is not a fiasco level, but it’s up nearly 15% from a year ago (data via YCharts):

Declining sales and rising inventories are gingerly starting to have an impact on prices at the national level – something we have seen play out more brutally on a local level.

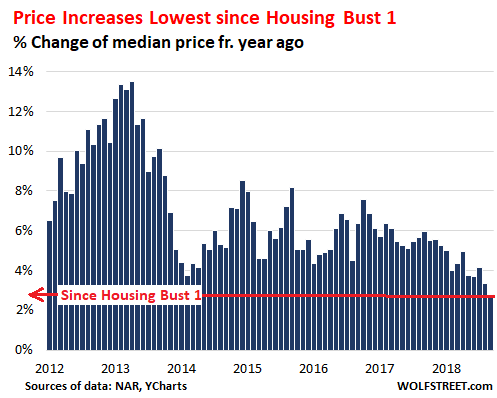

The median price in January, at $247,500, was still up 2.8% from a year earlier, the lowest year-over-year increase since 2012, with house prices rising 3.1% and condo prices remaining flat. This chart shows the year-over-year price changes in percentage terms (data via YCharts):

The chart above shows the disconnect: When nominal wages rise 2% to 3% and home prices surge 5% to 12% year after year, as they have done, sooner or later something has to give. Home prices cannot forever outrun wages – because it eliminates layer after layer of buyers. When there are no buyers at a price point, there is no sale. And for there to be a sale, the price has to come down.

Median home prices by region:

- Northeast: +0.4%% year-over-year, to $270,000.

- Midwest: +1.4% at $189,700.

- South: + 2.5% year-over-year, to $214,800.

- West: +2.9% year-over-year, at $374,600.

The disconnect between prices and where the buyers are was pointed out by the NAR report, though from a slightly different perspective. Inventories are rising and there is no shortage of housing per se, but it’s the wrong kind of inventory, after years of sharp price increases. “In particular, the lower end of the market is experiencing a greater shortage,” the NAR report explained.

That “shortage” at the low end exists because prices have outrun incomes. There is no magic to it. The market can fix that when sellers are motivated enough to make deals and cut prices across the spectrum to where the buyers are. This doesn’t happen overnight. It happens over the years, market by market. And eventually it shows up in the national averages.

There is a whole generation looking forward to the moment when they can afford to buy a home in these out-of-whack markets, though that’s still a while off. Those are the buyers of the future – and eventually prices will have to meet them (some good listings in Vaughan). There are a host of other economic benefits triggered by lower home prices, such as buyers having more money left over to spend on other things, which would give other parts of the economy a sorely needed boost. Gradually unwinding some of the home-price inflation of recent years is not the end of the world.

The signs are now everywhere. Read… Mortgage Applications Drop Despite Lower Mortgage Rates: Industry is Baffled

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Well said. This is a net positive in the long run

Baby steps to affordable housing…

Two actual steps that lead to affordable housing.

— Buy and wear a yellow vest

— Vote Socialist

Only your first point is correct. Socialist policies tend to result in a dearth of development of rental units. Landlords are discouraged when too many punitive measures make it simply not worth their while to invest in rentals.

Vote for socialist = bringing in Venezuela? Wish not!. Which socialist goverment in the world had the most even keel in policies?.

Housing Bubble 2.0 Pops! We are just in the first innings BOYZ

“Housing Bubble 2.0 Pops!”

And just not in the US.

Real estate sectors around the world are in a ‘world’ of hurt.

Canada, Australia, US, Hong Kong, UK. are just the tip of the burg!

Taken in conjunction with all the other globally negative economic/financial conditions, does not rule out a worldwide recession.

“decline in sales volume is occurring despite the large drop in mortgage rates since early November.”

But there’s “conventional wisdom” out there, saying that the answer to the housing sales decline will be the Fed’s interest rate policy, e.g:

“… the Fed may have no choice but to keep rates flat to avoid a housing market crash.” https://www.zerohedge.com/news/2019-02-21/existing-home-sales-crash-accelerates-buyers-cant-afford-house

Hope we get back to a real market with price discovery.

My concern is they are more likely to turn on the printing press and the fed will buy them all keeping this ponzi going; like last time…

Then the government will say here’s a house as long as you have a good social credit score.

Housng. Bble. 1 was caused by subprime mortgages.what is causing housng. Bble. 2 ?

It’s mostly a function of extremely low interest rates across all mortgage types, which has allowed people to increase leverage resulting in higher home prices (in other words, the same mortgage payment buys you more house – and thus house price moves to match).

With respect to subprime borrowers, the private mortgage business which fueled the last crisis no longer exists. The FHA and VA have filled that void (albeit not to the same volumes as in the past crisis). If we get into an actual recession, this will lead to significant losses to the taxpayer and will likely cause Ginnie Mae to collapse. This sets up an interesting conundrum… with private and public lenders crippled, who will lend to subprime borrowers after the next recession? This is not very clear at this point.

Maybe they will lend to each other?

And housing will vary by market which you all knew. Take for instance SV & SV, tech still moving forward, should there be a tech crash, that market will get decimated overnight although dropping prices would bring in speculators and investors looking to score a deal on rental properties. NorCal is an extreme example but its also an extreme economy out there. NYC and surrounding area have seen reductions in IBank employment and some other highly compensating banking careers (trading comes to mind) so employment in that sector could drop but its already come down from big highs. Can go down the list: LA, Seattle, Dallas, Chicago etc. Each has its own driver. Am curious what pops the bubble in Nashville although that one may lag the general market. This time what brings it down significantly over the broad housing market may be something unanticipated. Fed Hikes off the table for a good while now and perhaps another decade.

Primarily interest rates but reducing tax subsidies, clamping down on foreign investment/money laundering and potential recession in the near future, are contributing to the slowdown in houses priced over $1.0M. Inventory is building in the luxury and vacation home segments which will eventually trickle down to the mid and lower tier levels. Eliminate the prospect of annual 4%-5% price appreciation as a result of the above headwinds and qualified buyers like myself start waiting on the sideline looking for a deal.

Further complicating price discovery is the abundance of luxury apartments and rental houses hitting the market and driving down rents. it seems nobody is sure what the hell anything is worth if sellers aren’t realistic about price listings and rentals rates keep dropping.

Max – “the private mortgage business which fueled the last crisis no longer exists.”

My son and my nephew, in the last 6 months, both got a mortgage from a private mortgage business.

Maybe they are just being more selective to whom they lend.

@TXRancher

when I say “private mortgage” I mean a mortgage not guaranteed by the GSEs or GNMA. Since the financial crisis, those types of mortgages make up only a tiny portion of the US mortgage market.

Housing bubble 2 turned up significantly on 2 things – the Obama administration inviting hedge funds into buy-to-rent housing making it a truly global investment asset, and capital flight from China with the wealthy there looking to hedge their wealth in foreign housing.

That is why the focus of the boom was primarily in big cities with rural areas left behind, many still underwater from 2008.

Note that commutable suburbs near big cities also saw a spike as locals moved further out – a spillover effect from a city-focused housing bubble with a limited range.

My prediction is that big investors will put a floor under big city housing at some level that still locks out the lower middle class, influenced by a rising tide of central bank liquidity.

The price swings in the 50 mile commuter areas will be much bigger though because their primary buyers will avoid the nasty commutes if they can. They’ll drop first, faster and further, then they’ll climb later, faster and further – the metaphorical tail of the beast.

John – I totally agree with the first three paragraphs and have been a huge beneficiary of rising city real estate values. However, I see the complete opposite happening. Inner city real estate values have risen to astronomical levels and are going to be much more heavily impacted by rising interest rates, reduced tax subsidies, and the reduction of investment from international speculators.

The big cities have become massively overvalued to the point where homes 30 miles from the city center are valued at one tenth per square foot. I cashed out $400K in equity from selling my city townhome and can buy an identical unit 30 miles from the city or in flyover country for $250K . The outer ring burbs and flyover country have been beaten to death over the past 15 years so badly that two minimum wage workers can easily afford a median priced home. I’m seriously considering moving 30 miles from the city and buying a home all cash and demanding remote work or a part-time schedule.

Cities are already imploding while lower cost burbs and flyover country are holding steady.

Wash your hands of the whole awful house and apartment situation. I spend my earnings any way I please without being obligated to waste money on housing. Let home owners to pay the taxes to maintain the public commons – they got greedy let them tow the line meanwhile I will ride for free.

And, when I can no longer handle living in this horrible area (Seattle), I can simply drive away without entanglements – no overpriced house to sell or lease to break.

I was pushed out of house habitation by extortion level pricing. Now I’ve found vehicle habitation perfectly adequate and will never go back even if prices correct. The real estate industry is a corrupt racket, walk away and live in a van man.

I’m not homeless, I’m home free.

Van, why not get into a mobile home or RV? You get a lot more comfort (i.e., kitchen, bath, closet space, etc.) for a little added cost.

RVs attract attention. What you want is a white van, leave a hard hat and a clip board on the dash board when you’re not in it or asleep etc., no one will question it. Whereas, an RV screams “I LIVE IN HERE AND MAYBE EVEN HAVE NEAT THINGS TO STEAL”.

(HUUUUGE SMILE)

and THIS is PRECISELY why i miss you when you’re not around.

i miss Petunia something fierce, too.

x

Better yet get your CDL license and live in the truck, make money and see the country.

I bought a large (could have done all caps there) truck – Nissan NV2500 HD about 3 and a half years ago. It has a queen size bed and a 50 inch TV hanging from the roof. I’m loving it. When I want to transport my motorcycle, I ride the bike into the truck and away I go. I can fit a single bed next to the bike.

It was actually the 15 percent foreigners’ tax in Vancouver that destroyed all of Seattle. I told everyone right here on WolfStreet how to get rich buying up the the lots and homes that were the closest to all the elementary schools in Seattle before they had moved up in price. All the ones I suggested double or tripled or more in price will the rest of the residential housing gained around 40 percent. Had Trump not “put the blocks to China” homes in Seattle on average would be well over the one million dollar mark by now.

You are home free “on the coast”. You can’t enjoy that freedom in Minnesota. If everyone fled to the coast for this freedom it wouldn’t feel so free.

I know a couple living in an RV in Pacifica (San Mateo county – terrible fog bank weather). They are paying $1600/month for the spot.

It’s not that cheap.

Gee, housing sales down, auto sales down and auto loan delinquenies up, credit card debt growth lagging. And stock markets that have now demonstrated vividly that the only thing keeping them propped up are low interest rates. Sound like it’s time for negative interest rates.

Just wait for the 40 or 50 year, minimal down, government guaranteed mortgage to get rolled out. That’s the catalyst for next leg higher when this one stalls out.

There are still a few tricks left in the bag.

We don’t have to wait for that long. Just a few more years until AOC can get old enough to be elected, well, two presidential terms, but that’s nothing. Then it will be free housing for everyone.

:)

Ok, I jest, but the rate hike is going to resume at some point, and that’s going to let the air out of the stock market. Not to mention all of the negative externalities, Brexit, Trade War, etc. The market is poised for a downturn at some point in the near future. All that has to happen to for the final crop of IPO to finish off, Uber, Lyft, Airbnb, Slack, Palantir, and a few others. Then the pipeline is going to go dry for about a decade while things shake out.

A 50 year mortgage would be too risky for a bank. There is no way a borrower would be able to work for the required 50 years to pay off the mortgage. The 30 year mortgage works because it matches the estimated length of the average persons career. A 30 year old buyer will work for 30 years and retire with a paid off mortgage. Makes perfect sense for the bank.

What about 40+ year old buyers? Do the banks not extend them 30-year mortgages to these people today because they’ll be retired before mortgage is paid off?

I think banks will introduce longer term loans if the economics are there. I don’t know that it has much to do with length of an individual’s working life.

Well when you have half of households, not individuals but households, making less than $30k a year what do you expect?

If half the households in the US made “less than 30K a year,” as you said, the median US household income by definition would be less than 30k.

But the median household income in the US = $61,372 in 2017. Median = half make more, half make less. So by definition, half of the US households make more than $61K, and half make less than 61K. Not 30K.

I understand that this doesn’t fit into your dystopian fiction. But there are plenty of real issues with incomes. It’s not necessary to invent more.

The article linked below also has a chart of incomes by quintiles (20% layers) of household incomes, adjusted for inflation. It’s terrible in many aspects. It also allows you to estimate what percentage of households makes less than 30k.

https://wolfstreet.com/2018/09/12/real-earnings-of-men-women-income-distribution/

Wolf,

It is your focus on data and facts that make your articles of such great interest, and dare I say importance. That is very rare today and I, and I know many of your readers, appreciate it. The number of strangers, friends, and acquaintances who blurt out opinions (of all political persuasions) devoid of any data or factual support has gotten depressing. Your well researched and data driven articles are a breath of fresh air.

I also appreciate the professionalism of your response where you didn’t just point our the error of the statement, but provided the data to support your contention.

Having said that, and knowing nothing about Alex or his environment, it wouldn’t be surprising for people who have to deal with the large number of people who are struggling to believe that things are worse than the numbers indicate.

Thanks for your great work.

Old Engineer,

Alex likes to post dystopian fiction — see his screen name. Santa Clara County (southern part of Silicon Valley), where he lives, is wealthy with lots of very high-paying jobs. Median household income was $106,761 in 2017. I go there quite a bit. Yes, there is misery and poverty, but it’s only a small-ish part of what is there. He makes it sound like it’s all there is. He is at heart a (good) fiction writer with a dystopian bent. It’s fun to read, but it’s fiction. As such, I block most of his dystopian fiction because it has no place here. People might actually take it seriously.

That September article about men’s and women’s wages came out just after our household had a lively discussion on the topic. I printed it as Exhibit 1 to spring on my opponents next time the subject came up, but it hasn’t yet. Patiently waiting for topic to come around again on the divisive MSM circuit.

Agree with you about doomers. They distort the conversation as badly as the NAR shills, sans the silvery language.

In a good world, the NAR would clearly and simply inform people that, at $61k median income, the median house should be $183k, not nearly $250k. But this won’t happen because agents make more when prices soar. So do builders. So do banks. So do contractors.

But we don’t live in a good world right now.

This is why people listen to doomers. We allow the housing sirens to sing a seductive get-rich-quick song. There is scant counterpoint. Then we all lose credibility as the wrecks of hypnotized (usually young) buyers begin piling up on the shoals of market reality.

You’re doing your part, Wolf, and I’m happy about that. But the lies and deceit of supposed authorities will cost us all in the end as people flip from greed to fear and begin listening to a different, darker, siren song.

Wolf – I find that breakdown of household income to be incredibly confusing. It says the “median income of the top quintile” is $225K but what does that actually mean? Does $225K (all income sources) put you in the 90th percentile overall?

I’ve read as little as $130K in household salary income is 80th percentile. Households earning over $130K can rapidly accumulate wealth from higher savings rate and the resulting compounding interest.

Ed,

It means that half of the top quintile, so half the top 20% in household incomes, are above $225k, and half are below. Without thinking about it (I could be overlooking something), I would agree that if a household has $225K in income, it makes more than 89% of households and less than 9% of households. In other words, it would put that household at the bottom of the top 10%.

Your second point concerning $130K sounds about right, give or take. However, “accumulate wealth” with this income in an expensive area may be tough to achieve.

=>Sound like it’s time for negative interest rates.

Sounds like it’s time for TPTB to crash the global economy one last time, complete the subjugation of the sheeple, disabuse them of any lingering hopes for a finer future, and start culling the non-performing assets.

Did I say something?

(smile)

aaaah… Unamused… and there YOU are! finally…

it’s gonna be a good fine day indeed!

x

Wake me up when there is an actual meaningful drop in prices, say >5% yoy.

We are in LA and starting to see 5 percent drops or more. But sellers and buyers are pretty far apart. Some examples:

1. A house in a great neighborhood but in need of updates listed at 2.3m, we thought it was worth maybe 1.8. They dropped to 2.1 a few weeks after initial listing.

2. An updated house in a great neighborhood listed at 2.7m over a year ago. They are recently at 2 even and still no takers. Due to some quirks, we think it’s worth maybe 1.5.

We are expecting baby #2 and honestly not sure whether to lease or buy. Leaning toward leasing.

Max – LA is insanely overpriced. My guess is LA is propped up by foreign speculative investors and money launderers and China and US have both clamped down on this activity. Add to that increased interest rates and a huge impact from the reduction of SALT deduction.

Some parts of LA may be 30%-40% overvalued. Best case is houses stop increasing in value which alone eliminates any incentive to buy. My projection implies BOTH rental rates and house values will drop significantly over the next 5 years ( down 15%-40%).

Stay away from California real estate until mid-2020 / early 2021.

In San Diego the market for homes over 1.5 million has been going down a bit for awhile. But now prices have flat lined since summer 2017 for mid to low price range in our neighborhood.

What goes up for sale seems to sit until they have at least a few price cuts. It will be interesting to see what sells this summer.

Interest rates really haven’t moved much. You can still get a mortgage for maybe 1 or 2 points higher than I got mine in December 2017.

I am from San Diego and I keep a tab in my neighborhood and I see multiple reductions in asking price

You borrow for the house at 3-4% and enjoy 5-10% annual price appreciation. Meanwhile the money you’d otherwise pay down the mortgage with invested in S&P500 pays you another 2% dividend plus 10% annual gains. Thats like 14-18% return each year, win/win really, people get rich.

andy – There is very little chance that California will appreciate AT ALL much less the required 5%-10% appreciation. There is a much greater risk of California real estate dropping in value at this point.

We purchased a house in Antioch Northern California in 2005 for $590,000. At the time we were satisfied that the price was more than fair market value based on the prices of comparable homes that had just sold in a ultra competitive market. In 2007 it appraised for $735k. Flash forward to March of 2009 & that same house was worth $260k. That’s called “serious” deflation.

Unfortunately at that time, I lost my job & we had to say sayonara to the house, but 3 years later we were able to buy another house in a nicer neighborhood for $355,000. This house now has about $150k positive equity but that will inevitably all evaporate again & prices could even revert back to what the house originally sold for in the next great Reset. We’ve now come to view a house as comfortable shelter and not as an appreciating asset (as in the past).

The point is, we are coming to time real soon when all of the sins of the past are going to have to be paid for (pun intended). If you own a house, I’d look at maximizing the value of it now because values are only going to go way down from here & inventory will be ramping up as sellers become more and more desperate.

We just purchased 3 acres in Western Kentucky last November & are planning to build our dream home there, saying goodbye to all of this overpriced way of life & hello to a hopefully a nicer future in retirement. I think we all need to have a plan for what’s coming.

What a refreshing post from DoubleD; buying the property in Kentucky. As my first flight instructor said to me 45 years ago, “Don’t you know the 5 Ps? Poor Planning Precludes Poor Performance.” :-)

So here is a plan to knock down the cost of new RE for first time purchasers, and lower income purchasers.

* Look for a lot that does not have curbs and gutters built into the development costs.

*look for a lower tax region.

* Buy sensible appliances that are NOT financed into the mortgage.

* Nix the 2 car garage.

* You really don’t need granite or polished concrete countertops. Honest.

* In-floor grid heating in the bathrooms and kitchen isn’t necesary. You won’t freeze without it.

*a 25 year duroid roof works just as well as tile, and Bats don’t over-winter in them.

* One bathroom works just fine for a small family, but an ensuite will be wonderful for and during teenager years. You don’t need any more than this!

* laundry facilities can be built into the main bathroom (and guests won’t even know they are there).

* Build the back decks yourself, after you move in.

* Choose a location and design that will allow build ons, or better yet, an unfinished basement.

There, I just saved you 30% of cost without breaking sweat.

Great info. I did a lot of research before we purchased our parcel of land. The key is making sure you do your own due dilligence prior to making a purchase, & putting several contingencies into your offer in case something doesn’t check out.

We also plan purchase a Modular Home & have it installed on the prepped site. You get a much better final product over a site built house. The benefits are a much lower cost/sf than a comparable site built house, faster construction time (6-8 weeks) & better quality control as it’s 100% built in an environmentally controlled factory. In addition, a modular home appraises the same as a site built house (because it’s considered permanent real estate) as opposed to a manufactured home (which is not considered permanent). Most people equate modular construction & manufactured as the same, but they are not. Properly designed, asthetically a modular looks every bit the same as a site built.

My estimate for a custom 3 bdr/2ba 2,000 sf modular home + 1,200 sf steel building garage & including the land & land development cost is approx. $230,000. A site built house would probably be double that.

Why not just find a cave somewhere? The cost to build in most states (for an individual builder) exceeds the cost per square foot to buy a house. Reducing or eliminating amenities/ creature comforts will save a little money, but permits, taxes and fees will not be less. Then, try selling that albatross.

I would spend quite a bit of time in Western Kentucky before moving there. It is quite different than California.

Agreed. I’m a NYer/Long Islander who lived in Northern KY/Cincinnati for 10 years. It can all look good in theory – aka great value, beautiful country, etc. But most likely, culturally you will feel like an alien in your new “home” town. Not saying don’t do it… as I don’t regret my 10 years in KY/Cincy, it was the right place for the time – young family.

And probably it’s the right place at the right time for you too.

In better metro areas, like LA/OC, SF, NYC, Boston, Seattle, and DC, people earning the median income or less are renters. In these areas, only people making above the median income are buyers. This is sustainable. Where does this rule that median income people must be able to buy the median priced home in better metro areas? Sounds like a false requirement that can not be backed up with fundamental analysis.

In less desirable metro areas, which is nearly everywhere else not on the above list, you can buy a median priced home with the median income. But so what?

All of this is sustainable. No problem here.

There’s this attitude that anyone should be able to live anywhere they want at the price they want.

In the 60’s, you could buy a bungalow near the beach in Malibu for nothing.

That ship sailed.

Median means half is over and half is under. So when the median income is not nearly enough to pay for a median house, who is going to buy the median house? The Rich? Nope, they don’t want to live in a median house. The simple fact is, at some point you run out of buyers. That’s when sales volume plunges. Maybe you can recruit enough foreign buyers… and if that’s your only hope, the market is in real trouble.

“Maybe you can recruit enough foreign buyers… and if that’s your only hope, the market is in real trouble.”

pretty much describes manhattan. the only people buying regular apartments are wall street types and foreigners. people say manhattan prices never go down but i’ve met people who bought at the bottom in the mid-seventies who know better.

I understand as part of capital controls the Chinese government is chasing down foreign home buyers and forcing them to liquidate.

In the late 80’s and early 90’s, notices for foreclosure auctions for coop apartments in Manhattan and Brooklyn took up entire pages of the classified advertising section (remember them?) of the New York Times. My wife and I were too broke to buy at the time, but those who did made phenomenal gains.

The main point is that, if you think real estate in the prime coastal cities can’t decline in price, you’re quite mistaken.

My neighborhood in Northern Virginia is mostly foreigners. Somehow they can afford it, I rent below market.

If the market tanks, they can all just bounce back to what ever country (HELOC first!) and the banks would never have recourse.

There is NO rule of saying “median people” should be able to afford “median homes”. Let’s all take position and rent seek them into serfdom. Better yet, there is NO rule of saying slavery is NOT sustainable. Let’s revive that.

The equitable society providing the little guy with freedom and opportunity has degraded into a system of rent seeking and serfdom. Capital rules, labor serves. Rent seekers get rich and serfs goes into their tombs with unpaid student loan and mortgages.

All of this was sustainable for thousands of years on earth, why don’t we go back to that!

Hey, hey, hey, JZ, get with the times! Traditional slaves are far more high maintenance than debt slaves. They need to be housed and fed, and overseers and guards need to be hired to make sure they don’t run away or rebel and kill you, or go and slack off instead of working all their waking hours for you. Debt slaves take care of all of that stuff themselves.

I really like that comparison and agree completely. Avoiding being a debt slave is the #1 thing I repeatedly tell my teenage son

Rent seekers are morally superior. The rest of us need to shut up.

Mass moral decay precedes civilization decays. But let’s even ignore the moral issues under the name of capitalism’s basic principle of “greed drives civilizations forward, so let’s unleash hreedand all the wonderful things happen”. I have always maintained my focus on NOT hating the players but hating the gamwa. The game rule determines how players act and how greed is used. If greed is channeled to invention, society moves forward. If greed is channeled to rent seeking (tuition, house, health care), society starts to decay. Parasites (rent seekers) exists naturally and they serve the important functions. But the game rule has to be set up so that the parasite does NOT overwhelm the hosts. Let the rent seekers do what they do and let’s all compete. But there should NOT be FED’s policies, there should NOT be bailouts. Take out those two, parasites and hosts will die together if things are done wrong and maintain a balance. With FED and bailout, inequality, hatred, yellow vests, populism, socialism ….. happens.

The DC area is the province of rent seekers, whether it be lobbyists or federal employees ( I refuse to call them workers, since they produce no wealth).

There is more and more public sentiment to eliminate the 17th amendment to reduce rent seeking by lobbying and campaign contributions for senators.

The next step in reducing DC rent seeking would be to eliminate the 16th amendment which offers a variety of rents through direct taxation.

You speak as if there are no opportunities in the US for people who are motivated to become more than renters. Trust me, the majority of home owners and landlords were, at one time, renters. Precisely why we are being flooded with immigrants, legal and not so legal, they see and smell opportunity. Perhaps you should trade places with one of them and experience true poverty and hopelessness?

The fact is the market is dependent to some extent on the median income buyers as they usually make up the majority of the population. There are not enough upper income buyers to support the housing market.

The fact that purchasing the median Priced home requires 2 incomes for the median income household makes the housing market very vulnerable to recession as most people in the median income brackets cannot afford any sort of income disruption without dire consequences. A minor recession causing the loss of a job for 1 person in a 2 income household usually means a downward spiral in finances that will result in the loss of their home. Multiply this scenario by 10% or 15% of the population and the housing market is in real trouble.

socaljim – Explain how it is possible that a median income family cannot afford a median priced home? Either it’s cheaper to rent and the median family is logically renting or there are foreign speculators in the marketplace that will exit at any sight of a recession. Either way, houses are undeniably overpriced in major American cities and WILL go down in value.

Speculation is at the heart of every bubble. With the exception of shortages, anytime asset prices outstrip wages, there is speculation driving the prices up.

OK … I will explain it. In the LA/OC area, more than half of the people rent. Assume the renters make less than the median income, which is true. Then people making the median income and less rent in apartment buildings. Now, the upper half of the income distribution are the buyers, and the average income of the buyer is much higher than the median income of all residents. So, you have a much higher than median income doing the buying. That is how that works.

Considering that somewhere around two-thirds of Americans are house owners, a figure that has held fairly steady for decades, what you’re suggesting would be a major paradigm shift in this country.

Momentum has changed in housing. Very apparent. Appears to be because prices have outpaced incomes. Not only have incomes not grown along with house prices but incomes have been eroded by the unrecorded rising costs of health care, insurance and rising taxes.. Even autos cost more.

It appears that another factor may be that foreign buyers have also started withdrawing.

In the past the next issue would be sentiment. Once an asset starts to fall, many people will not want to purchase in fear of having it fall further. With the lack of incomes, huge other debts being carried by many young people and the psychology this could easily turn into long bumpy road.

I think we still have a lot of apartments and condos complexes under construction. I have read that many, maybe most, of these are for high end buyers. This should bloat the inventory even if the builders aren’t able to lower the prices enough to sell them.

Very entertaining.. I hope it doesn’t turn into a horror show.

It still seems like housing is gangbusters here in Seattle. Anything less than 500k is sold within a week, perhaps the higher end luxury housing is sitting longer but anything within striking distance of the middle class is gone fast. The housing stock in general in Seattle is quiet poor and these 500-700 SF bungalows should all be torn down. They have exceeded their life expectancy. I toured one a few weeks ago, sagging roof, toothpicks holding up the floor, roof shingles applied directly to OSB with no waterproofing membrane, essentially a glorified chicken coop, but low and behold it sold in 2 days. Totally crazy.

PS long time reader Wolf, thanks for posting these great articles and keeping it real.

Kidding? Seattle metro is perhaps one of the fastest deteriorating markets in the US by nearly any measure.

Based on the Case-Shiller data:

https://wolfstreet.com/2019/01/29/the-most-splendid-housing-bubbles-in-america-deflate-seattle-san-francisco-bay-area-los-angeles-san-diego-denver-case-shiller/

Based on the NAR data:

https://wolfstreet.com/2019/01/08/housing-bubble-trouble-in-the-seattle-bellevue-metro/

While I don’t discount your analysis and agree that prices have fallen, and the bidding wars of last spring are over, from the ground level prices are still astronomical for what one gets in this city. It will take a much larger drop to return to some sort of normalcy. Although I fear that falling rates will decelerate the decline temporarily. I think the “spring” selling/buying frenzy will shed some light on how sour the market has become. Thanks.

“It will take a much larger drop to return to some sort of normalcy.”

That drop will happen only when the seller accepts that the drop he is seeing now is not a temporary one and he may lose more if he holds longer. That will likely take some time coming so we can expect this to play out over time. This acceptance will in all probability happen first with investors (when they find it is a hot potato to hold on). It is here things will get interesting in all sorts of manner-Fed might intervene to boost house prices, buyers might refrain from buying thinking the bottom is still not in, sellers trying to get out of the door etc.

May be if we have an idea of what is a normal increase in home prices in an area, then given how much out of whack the present prices are should provide us some clues on what could be called normal prices (or slightly higher). The time to get there would still be a guess.

Price movement in the housing markets tend to be a long drawn out process.

House prices aren’t like the stock market. You won’t see the price of houses drop say 20% in a couple months.

Even the rental homes in the Seattle area are mostly overpriced crapshacks….and the ones that aren’t are gone in days. I thought Cali had the worst market for a buyer/renter….not until i saw Seattle’s market.

At least Cali had a lot of newer housing stock, not old mold and crazy painted interiors. I have seen so many rentals with stained and worn out carpet that are snapped up in days. I wouldn’t take my shoes off in those places.

Think it’s going to be awhile before price will be reasonable here.

Seattle’s an interesting case.

The market has probably gotten ahead of itself in a number of neighborhoods, especially north of the ship canal and on the Eastside. That said, rapid population growth is going to continue and the ability of expand outward is limited by geography and our atrociously bad transportation infrastructure. NIMBYs have also been really successful blocking higher density zoning. No way the Fed doesn’t support the housing market in the next downturn.

So, I don’t see someone losing a lot buying now, but I don’t see making a lot either. Given all of Seattle’s problems: high COL, traffic, tent cities and homelessness, garbage on the streets, panhandlers on every corner, property crime, and the weather and that even more people are coming and we don’t have the infrastructure to support the growth, the problems will get much worse. Why live here?

Lots of other places to live with better quality of life…

It wasn’t all that long ago (or am I just too old?) that Seattle was a highly sought-after destination, precisely for its quality of life.

That the terms of discussion for the city and region have altered so radically is a measure of how fast things are changing/deteriorating for most people in the country.

Sister lived just north of UW for a few years while hubby was getting his PhD. Both were sick constantly until they moved away. Landlord wanted to replace carpet before they left, no problem. The carpet folks pulled-up the old revealing extensive mold throughout the foam padding, which was completely black.

We bought in Normandy Park, just south of Seattle. Love it. Quiet, but we have two young kids so it works for us. But agree that within the city limits – lot of old craftsman homes which need a ton of work/have issues. One of the reasons we moved out of the city.

There is just not much inventory still. I know some first time home buyers and they cannot hardly find any houses to buy. I think home buyers are still competing with wall street investors

Depends on the area.

A minor drop in prices isn’t a problem because we all know that everyone who bought in the last few years put at least 20% down. And according to Senator Running Deer, all mortgages since 2010 were underwritten with extreme care and risk of default is practically zero. Speculation on housing is impossible nowadays and prices simply reflect lack of supply. ;-)

Well, there is a big difference in loan underwriting quality from 2002-2008 vs 2010-now.

No comparison.

Uncle Jamie and my bros at Wells have pulled back from shack lending, so it’s the cowboys at the shadow banks y’all need to worry about. We’ll see how sturdy all of those <10% down loans are as prices fall, hopefully sturdier than the termite-infested moldy shacks they’ve lent against at astronomical prices. Katy bar the door!

“underwritten with extreme care and risk of default is practically zero.”

If that is the case, then the prices have to be normal. Is it?

If not, it means underwriting has been a tad optimistic or in the expectation of housing price never falls nationwide. Meaning to say the risk of default is proportional to the optimistic assumptions in underwriting.

Typically the price for any good is out of whack if there is a supply-demand mismatch, with demand far exceeding supply.

Foreign buyers of US residential property:

4/16 – 3/17: 10% of total

4/17 – 3/18: 8% of total

Five states accounted for 53% of foreign buyer sales:

Florida: 19%, California: 14%, Texas: 9%, New York: 5%, Arizona: 5%

52% of foreign buyers purchased the property as a primary residence, so lets assume 48% left the property empty.

Source: Profile of International Transactions in U.S. Residential Real Estate, National Association of Realtors (2018)

Contrast with remarks by David McKay, CEO of the Royal Bank of Canada (3/7/18) just before Vancouver imposed both a foreign buyer’s tax and a vacant unit tax:

– Foreign cash is ‘gasoline’ on Vancouver’s overheated housing market

– We do not need foreign capital using Canadian real estate as a piggy bank

– We’ve got this cocktail of factors that are leading to unconstrained growth in home prices

Ah…were are our regulators and bankers when we need them!

i’d like to point out that most high end foreign real estate transactions in nyc are done through an llc so they won’t show up in the data. i believe the rules have changed so that may not be happening as much going forward. also, i wouldn’t discount the percentage of middle class housing that is bought in cash by a us resident that is actually funded by an overseas relative.

that being true, the feeding frenzy of foreign buying that has been going on here for several years appears to have slowed down,

Perhaps wolf maybe an article about who’s buying those $ 500 000 shacks

Gordon Bumshaft is talking about ,maybe there is a mystery buyer probably some mutual

Fund company or something like cough blackrock cough same in canada Lower end stuff being gobbled up baby boomers sitting on their 5 bedroom 4 baths house for sometimes over a year very strange indeed ,millenials can’t buy boomers can’t sell

Professional investors rarely buy at the top of the market unless they know they can make a decent profit renting. While they make mistakes like all of us (see Blackrock buying office buildings in Munich just when a slew of new developments around the Hirschgarten was putting downward pressure on rents), they usually know what they are doing.

Those buying these very average houses at high end prices are usually “small fry”, a mixture of poor souls who just have to buy at the worst possible moment, small time speculators including “mom and pops” types moonlighting as flippers, hapless foreigners dragged into the fray by general enthusiasm etc.

Robert Shiller, him of Case-Shiller fame, famously said the main driver of the real estate market, even before supply and demand and financial conditions, is the image media project on potential buyers.

I have been told real estate is “money in the bank” since I was five or six, but I’ve never heard the media saying that unless the market is white hot you need to wait an awful long time to get that money from the bank. Guess when 80% of us sell?

I’ve also never heard about the costs of ownership: mortgages may be amazingly cheap to service but property taxes, junk fees and maintenance aren’t.

This is a business for people who know what they are doing, not amateurs who expect a bailout because real estate and construction are “too big to fail” and “can only go up”.

The rest of us are just better off either owning or renting a single house for living and not pretending to have skills we haven’t.

Bologna – $500K is very affordable when interest rates are at 3.2% and you get a nice tax subsidy. Not so much when interest rates go to 5.0% and you get zero tax subsidy. 25% of households in America can afford a $500K house even at 5% interest.

“Fact is, home prices cannot outrun wages forever” is my new mantra.

According to recent news stories, there is supposed to be a migration of retirees from high tax states to low tax states. Wolf, is there any data to suggest prices in FL and TX are weathering the downturn better than other areas?

Wendy,

The problem with these stories is that they discuss only one or two elements in a larger equation. If there were that much out-migration from California, the population of California would drop. But it continues to rise, now at 40 million and still rising. What these stories conveniently ignore are other elements, such as the complete picture of in-migration which includes in-migration from other countries — in California, this is largely from Asia.

There are fears in the RE industry that this in-migration from Asia might slow down, and that the population in the Bay Area and other hot spots would actually drop, but that hasn’t been the case.

I guarantee you, the moment I see data on the population of California or the Bay Area dropping, you’ll see an article on it right here. I get monthly data on this. This is a potentially huge issue and I keep my eyes riveted on it.

In December, the Census Bureau released data for the 2017 migration patters. I covered this at the time (link below). For California, my article includes this paragraph:

“In 2017, net out-migration amounted to 138,000 people. But California’s population grew by about 241,000 people over the same period. The difference – around 379,000 people – has to come from somewhere. A small component of it is births minus deaths. And the remainder? Foreign migration.”

The article also has a chart of the populations in the big four states. California outgrew all of them. Granted, the Census data only goes through 2017. But even in 2018, from the monthly data I get, the California population continued to grow.

https://wolfstreet.com/2018/12/04/california-housing-market-in-for-serious-trouble-foreign-home-buyers/

A couple of notes re Florida growth:

1) We picked up an estimated 500K Puerto Ricans after the hurricane; whether or not they stay is TBD but that’s 5% +/- of the total population.

2) We’re seeing a significant influx of permanent residents from the Northeast, many of whom already had homes here (so they might not be “new buyers”). Sadly, now they aren’t going home at the end of the winter season. I suspect a lot of this is SALT-driven (no state income tax and relatively low property taxes here).

3) Internal migration is big here: as Miami and Lauderdale become (or remain) too expensive, large numbers of people are moving over here to the nice part of the state. We don’t need a wall on the border as much as we need a wall at the Broward County line.

Jamie sez: Any city where the median house price is >3X the median income will be in a world of hurt. W/ a median household income of ~100k in the SF Bay area, median prices there will eventually drop to ~300k. And condos are always the last to inflate in a bubble, but the first to crash. TIMBERRRRR!

That logic was true when rates were at 7%. At 4.5%, markets can probably sustain 4-5X medium income. Certainly not the 10X you are seeing in SF, LA, NYC.

Excellent points. The market will sort this out one way or another, and what we are seeing now in the data is a direct reflection of the Fed refusing to let the markets function.

Central bankers are deathly afraid of deflation, but functioning markets depend on it. 10 years of pushing, distorting, delaying and what do you get? Pent-up deflation looking for the escape hatch. This is where NAR is missing the boat. Pent-up demand is not the real story; It’s pent-up deflation. Yun is still hoping, as are most Realtors, that this is all just a temporary path back to “normal”. Good luck with that.

I suspect December was just the first inning of deflation to come. and the reasons should be obvious. What was the Fed’s first reaction to that pent-up deflation rearing its ugly head? They panicked, just as they always do.

It’s entertaining to watch the jawboning and hypocrisy, as they pretend to be data dependent, “independent”. Lower rates should give a little lift to the spring selling season, but I don’t think this story is over. There are simply too many distortions, imbalances in the system. The Fed can jawbone and delay the completion of the market cycle all they want, but they can’t prevent the inevitable conclusion.

The data for the new home market suggests there is no rebound yet, at least in North Texas, the largest new home market in the country. I’m looking at my screen this morning, with both closed and pending sales for new construction down about 8 percent from a year ago in January. This is on average prices that were just slightly lower, down one percent.

I suspect the February data will improve a bit given that markets were jawboned higher to keep the confidence game going. The tug of war between the Fed and the market continues.

This is a good comment, but what is the timeline? BOJ has managed to fight inflation for decades. One day it will blow up. Not today though.

ALP:

Could the decline Y-O-Y in North Texas have anything to do with “another Toyota” not moving to DFW and bringing employees from CA (with a lot of money to spend from the sale of their CA house) into the market?

There’s still a lot of money on the sidelines, waiting for a dip. Interested to see how the plays out…

Was in housing court doing an eviction yesterday…the court room was PACKED. Rents are high and people are having trouble.

Smart money is always on the sidelines at the top of a cycle. The fact is though, that smart money is a small minority, and the dumb money who have gotten themselves over extended and are unable to tolerate any loss of income are the vast majority.

During a recession, the number of properties coming onto the market due to foreclosure far outstrips the number of buyers, which is why prices fall dramatically. It is an endless cycle, and yet every time it happens, there are always those who are convinced this time is different.

Analyst made the point last night on PBS, as long as the investor class is willing to take up the slack, (slice and dice and rehypothecate) this market is not going anywhere

Not really, speculators are in the game to make money. At the point where fear enters the market, speculators are the first to get out. They do not have the incentive of needing a roof over their heads to risk toughing it out. When fear enters the housing market, the speculators will be the first to take their money and run.

You do realize there is no such as “money on the sidelines”, don’t you? To buy a house, people have to sell some stocks or bonds. If housing dips in price, stocks and bonds dip as well. This “money on the sidelines” thus evaporates into thin air as all asset prices drop.

You are correct. Bubbles are driven by financing, based on confidence that the financed asset can be sold at a higher price at some time in the future.

The funds are created by a signature, usually with a token down payment. Speculative home buying depends on the inflated rents that accompany inflated home prices.

Speculators fear recessions because falling rents quickly translate to negative cash flow. Most speculators cannot tolerate much in the way of negative cash flow before they become insolvent. Falling home prices mean lower rents, and more pressure on speculators to exit the game.

I had to drive to Courtenay the other day and saw a 350 sq foot ‘tiny home’ while enroute. Cute enough for a laugh because the bugs ear tiny house costs as much as a barnd new 1100 sq foot modular; a modular with 2X6 walls and room to swing a cat. They both have to rent pad space.

This society of ours, (Canada and US), even takes affordability issues and commodifies it into a fashion statement. It’s time to grow up and grow back into common sense roots, that longed for time when people had brains and judgement.

Oh well, now off to enjoy the day. I’m turning a carport into a garage using old growth yellow cedar purchased direct from the sawmill. It will cost me $400, a bit less than a contractor built item for 20K, and will look stunning when I get the Sikkens on it this spring. While I’ve been building for over 40 years, I am the first to say it isn’t rocket science. Do it yourself. There is enough information out there for anyone to tackle their own projects. It beats paying to go to the gym!

regards

Someone on this site, I believe Petunia, once called tiny houses a “glamorization of poverty.”

I wholeheartedly agree.

Been building my own studio office at the end of my garden.

Learnt how to lay foundations, build block walls, frame roof, steel beams, lay grp roofing, wire up the electrics, crimp data cabling.

Man, can this get any better.

Customers call and birds are chirping in the background.

And, cancelled my gym a year ago. My biceps are swollen.

I believe the Housing market is going to go strong with the Fed capitulating. In the Bay Area we will see all of the IPOs into this market while it’s still being levitated by the Fed, so that means housing should start to really shoot up once the IPO lockups expire, assuming the Fed can levitate for the full 6 month lockup period.

After the Fed gets assets up another level, they will probably start cutting rates and re-institute QE. Then we will officially be Japan and the balance sheet will grow at an enormous pace. Nothing in their minutes can be believed.

Please TrojanMan, go buy your house. The market won’t tank until the last lemon is squeezed. So you have to take position before it can POSSIBLY turn south. I am eagerly waiting for you to do so.

That aside, don’t we all agree that house price at this level is pushing W2 folks to the limit? Don’t we all agree on betting the direction is simply a game of poker? Don’t we all agree on FED has pushed “innocent” W2 buyers to a place where they have to play the “poker game” they are NOT good at? I have NO idea about the direction but I do know houses at current price level will suck in majority of my savings every year if I go in and pick up one. What hold you back? Is that the fear of missing out or is it the fear of being a debt slave? To me, it is simply no safety margin once I can NOT save 25% after tax every year. I now save 50% and at this price level and I buy one, I will probably left with 10% savings. I am NOT comfortable with that. I do NOT play the game of counting house appreciation for retire. I save to retire.

So you’ve levered 20 to 1 to play this pending housing boom, correct? No? Why not?

I tend to agree on the QE Infinity outcome thought. Seems baked into the recessionary cake within the next 24 months.

I think there is misunderstanding. I track my spending. Say I make 200K, After TAX is 100K, I spent 50K, and I save 50K. By doing this, Every year I work, I will save 1 year of retirement. At the house price today, if I buy a house, my spending goes up to 90K a year and I can only save 10K. That is too much risk for me. Many people say your house will go up and that is your retirement. To me, a house is like a tomato, I consume it. I bought my shack in 2010 and I never count any gain in that as my retirement since it is NOT reliable. I track my income statement and make sure I spent only half. Buying a house today would break that rule.

JZ:

I am curious as to how the simple act of buying a house (to live in) will increase your cost of living 80%. (from 50K to 90k).

You live somewhere. The cost of renting (or owning that property) vanishes when you move into your new dwelling. So, unless you are stretching into a much higher cost property (or you have a sub market rent or are living with friends) the math doesn’t make sense to me.

We recently did what you described. We left one paid for house in a high tax state (no mortgage) and replaced it with another paid for house in a low tax state. Including the cost of moving, costs associated with utility deposits, insurance differentials, etc., our cost of housing dropped – even considering having to do considerable repairs (ongoing) to the new house (that the old house would have soon needed anyway). When I say “dropped”, I mean by 50%. We also have the equity differential to invest which has added to our income. And, no, we didn’t move to some remote area of the planet – miles from the nearest convenience…. we’re now in North Scottsdale.

Regarding the net migration into CA: Not all migrants are H1B’s or educated. Many are uneducated and living in overcrowded housing. It would be interesting to see how the demographics of the outflow compares to the influx in terms of income.

Lastly…. falling home prices do not bode well for municipalities that have built their expense structures on the ever increasing property values. When the homes are re-assessed (or the valuations are appealed), the tax base and resulting revenue will start to fall. For the Utopias (as Bill Maher) that rely on high taxes (and they’re still broke) it can only mean disaster.

– You sound like the people in the 2nd half of the 1990s and the early half of the 2000s who thought that real estate never would go down.

– The FED doesn’t lend to individual households, commercial banks do. So, when commercial banks stop lending then real estate prices will tank again. like they did between say 2005 and 2013.

– The FED’s effots to (re-)inflate the markets are doomed when prices don’t go up (any more). When (real estate) prices fall then FED can huff & puff al it wants but then the amount debt stops growing. And when debt stops growing real estate WILL fall.

– Actually it’s a bit more complicated. As soon as the GROWTH RATE of debt starts falling (e.g. from say +2% down to say +1%) then an economy is already in a recession.

– Also think demographics. The US is ageing and older people spend less and pay down their debts (= very deflationary).

– Nonsense. Why ALWAYS blame the FED for everything ?

– Just look at the balance sheet of the FED and you’ll see that that balance sheet has been growing since the (very) early 1960s. But after those early 1960s the US had – at least – 5 recessions. In other words: all that “printing of money” didn’t prevent those recessions from happening.

– Between 1960 and 2008 the balance sheet of the FED kept growing but that didn’t prevent real estate prices in California from falling by some 20 to 30% in the first half of the 1990s.

As someone said of land: “They aren’t making anymore of it.” The only place to build is up, in many areas. Developers can go bust in a downturn, and those without much equity and large payments can too. However after the ’08 crash many properties were bought for cash. These properties i believe are imune to market fluctations. I can see a scenario where many units are vacant, yet prices or rents do not move downward. RE is safe place to park money over long term due to its hedge against prospects of hyperinflation ahead. In hyperinflation rent income could never keep up with value. The true value is the hard asset itself, not the short term income it can provide, but rather it’s ultimate projected value once some sort of reset is established. If and when debts are ever written off the books, then and only then will RE become a value based on its use, rather than a commodity for speculation.

Can’t agree more. Real estate is better than gold in many aspects. There is only one problem with it, whereas gold can be hidden away as an insurance policy, real estate is the easiest target for the government to tax. It’s the only drawback I see and in those tax the rich times, real estate will be the first victim.

Your hypothesis has a few flaws. While it is true that many properties were purchased for cash after ’08 ( I was among the buyers) many of those purchases have already been resold. The kind of speculators who pay cash, buy low and sell high. They understand and play the cycles. You are also wrong about hyperinflation, we do not have, never had, and will not have hyperinflation unless our GDP is somehow halted. Hyperinflation is not a product of money supply, it is a product of loss of production of goods.

Not true. Printing money creates inflation, unless it is done to offset sources of deflation. Common sense really.

Yes, it causes regular inflation, not hyper-inflation. Hyper-inflation if you care to study it, only occurs in cases where the countries production is severely curtailed driving the supply/demand ratio to extremes. The most famous example is post WWI Germany when large amounts of Germany’s industrial and agricultural production was seized by France, England, and others for war reparations. Like you say, common sense, when there are extreme shortages, it causes extreme inflation, or hyper-inflation.

I’m starting to come to realize that we haven’t actually had inflation since the early 1980s. Instead, what we’ve had has been a savings glut that’s pushed up prices on everything in the search for yield. The first half of that savings glut was caused by Boomer retirement funds, either self or via pension funds. The second half was caused by overseas capital surpluses, which ironically was spurned on by the retirement savings glut (i.e. capital seeking yield offshoring manufacturing).

You have some valid points here. People that bought at the right prices won’t take a low rent to fill a unit because bad tenants are costly to get rid of and ruin units. You’re better off less than full with people who take care of your houses. However this can only be done when purchased properly..

There’s another mathematical quirk – even if wages and housing prices increased in step – real increase is significantly different due to the base factor. I love that you use hard data Wolf. It is so rare.

If we take 2% inflation (from the seriously suspect CPI)

Median household wage: 63k – an increase of $1260 per year

Median House according to Wolf: $247,500 – 2% increase is $4,950

Or – even at 2% houses outstrip wages by $3,690 per year.

Maybe you are supposed to make that up in time by locking in a fixed price? Instead, wage increases are seemingly stagnant, and houses go 8% every year. You can goose that with interest manipulation (why? idk but that’s what they did). But tack on other increasing costs, nondischargeable debt, and other factors – you totally lose the ability to save a downpayment, let alone afford to keep up. The treadmill just becomes harder to jump on every year. To say nothing of property taxes and broke municipalities

I’ve abandoned sub/urban homeownership. The few young adults I know that do own are all complaining they are underwater and their budget is crushed. Call me when they are 50% down. I got burned on rental raising my rent – no way I’m setting myself up for that again. Job loss happens, and most luxury features are a facade. I’d move rural except farmland remains supremely expensive and have hard enough time finding a relationship as it is – though lower population density may bring some sanity to dating… Urban areas seem to remind me of Calhoun’s Mice Utopia experiment lately…

Inflation does follow any standard data. Asset prices rise and fall with demand, and the availability of financing.

Wages are a factor of supply of labor. The reason the standard of living is falling in the US and people struggle to survive is that the labor supply is increasing faster than demand.

Between automation and immigration, the supply / demand ratio of labor has been changed and wages in relation to cost of living will continue to diminish dispite the increase in productivity.

Wolf: Thank so much your honest and thoughtful articles. When the markets are up, all the articles I see are from bull perspective. When the markets are down, it’s all bear perspectives. It appears that most writers have ulterior motives in pushing their theses. You think for yourself and don’t promote a particular viewpoint. Thank you for being an honest broker!

I sold a coop in Brooklyn, and am renting now in New Jersey. I am sitting on cash, waiting for an opportunity when the market drops. It’s amazing to me that so many people forget history: booms are always followed by busts!

Manhattan is already down 15-20%. Low balls are taken seriously especially if all cash. There are very good deals to be negotiated.

And i do mean very good.

I don’t expect a crash and -20% was all we got in 2008.

Who knows?

In the end real estate is usually saved from disaster by inflation.

And if rates go negative RE will go up.

Wolf, this article gets one to think about macro level issues at a much higher level, and the tug-of-war that’s going on between price discovery and lack thereof……

“The chart above shows the disconnect: When nominal wages rise 2% to 3% and home prices surge 5% to 12% year after year, as they have done, sooner or later something has to give. Home prices cannot forever outrun wages – because it eliminates layer after layer of buyers. When there are no buyers at a price point, there is no sale. And for there to be a sale, the price has to come down.”

Everyone wants their cake and they want to eat it too….

Internal corporate captial flows continue to be funneled into buybacks rather than human capital (wages), Realtors want housing prices to continue to rise indefinitely regardless of stagnant wage growth, equity markets and realtors want low interest rates that feed the asset bubbles, and at the same time, everyone wants macro-inflation to be contained.

We pay an enormous price when we persistently thwart price discovery in our asset markets……

Bubbles cannot persist indefinitely in all markets. Something does have to give, over time…..

– Disagree. The subtitle of this thread should be

“Fact is, home costs cannot outrun wages forever”.

Reality and time solves everything that is skewed as Social and Financial engineering only manage to delay while amplifying pain. Homes are for domestic families NOT hedge funds and Chinese launderers.