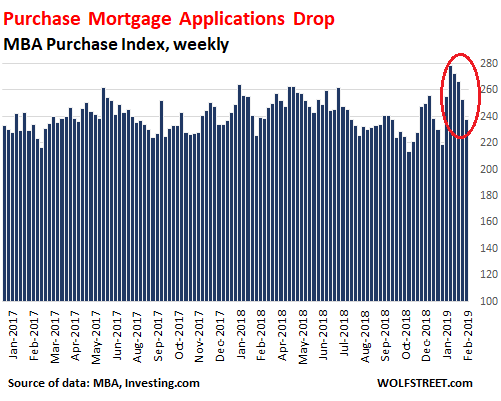

The hope in early January has been unwound.

A month ago, mortgages reappeared in the housing-hype circus, when it was widely reported that mortgage applications “soared” and “jumped.” Both types of mortgage applications did so: those used to purchase a home (purchase mortgages) and those used to refinance an existing mortgage (refinance mortgages). The jump in mortgage applications was ascribed to “plunging” mortgage interest rates. It was seen as a big sign that the weakening housing market was about to turn around. But that hope has gotten unwound.

Today, the Mortgage Bankers Association (MBA) reported that its purchase mortgage index – which tracks applications (not approvals) for conventional and government mortgages to purchase a single-family house – fell 6% from the prior week and was down 5% from the same week last year – despite falling mortgage rates, which should have cranked up home buying and mortgage activity. It was the fourth week in a row of drops:

The Purchase Mortgage Index is considered a reliable indicator of impending home sales, and so this decline, given the lower mortgage rates, mystifies the industry.

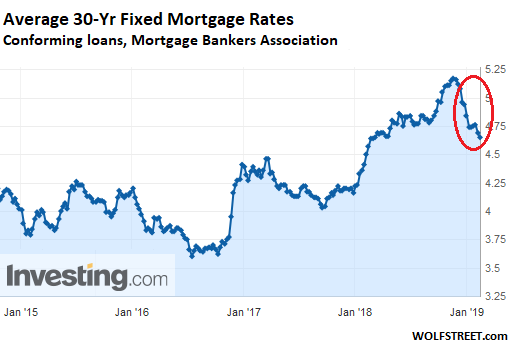

“Application activity fell last week – even with rates decreasing – as renewed uncertainty about the domestic and global economy likely held potential homebuyers off the market,” said MBA Associate VP of Industry Surveys and Forecasts, Joel Kan, in the report. “The 30-year fixed-rate mortgage dropped to its lowest level since last March, and was 52 basis points lower than its recent high last November,” he said.

You can practically hear between the lines, so to speak, the bafflement in his voice about this decline in purchase mortgage applications in light of the decline in mortgage rates. The MBA also reported today that the average interest rate for 30-year fixed-rate mortgages with conforming loan balances inched down to 4.65%, back where it had been last April (chart via Investing.com):

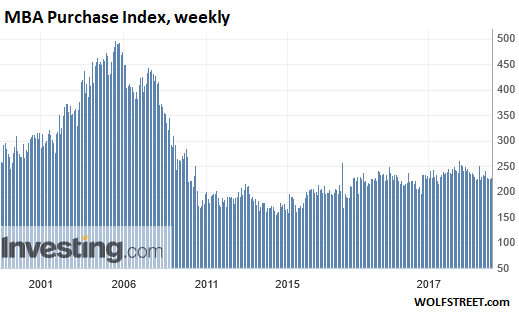

In the overall scheme of things, the MBA Purchase Mortgage Index remains way down from the peak mortgage craziness during Housing Bubble 1 (chart via Investing.com):

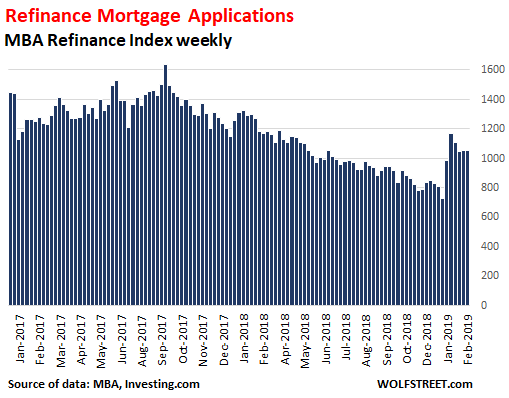

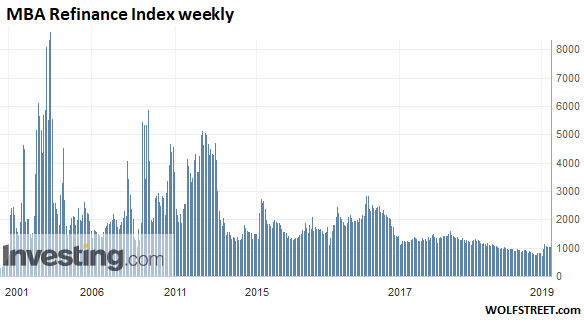

The MBA Refinance Mortgage Index has reacted in a very muted manner to the lower interest rates this year, after having fallen steadily since October 2017 as mortgage interest rates were rising.

Rising interest rates remove one of the economic incentives to refinance a mortgage, while falling interest rates increase the incentive to refinance. But the Refinance Index remains below where it had been last summer:

Seen over a longer period of time, mortgage refinancings are down by over 50% from 2016 and are just a shadow of their former magnificence during the mortgage craziness earlier this century (chart via Investing.com):

But don’t blame the government shutdown for the lousy mortgage applications activity. The MBA said that “government refinances provided a bright spark, picking up over 10%, as both FHA and VA refinancing activity saw increases over the week.”

The share of applications for adjustable-rate mortgages ticked down to 7.5% of all mortgage applications. They’d essentially disappeared from the mix of mortgage originations by 2009, since no one wanted to touch them, not even with a 10-foot pole, given the role they played in the mortgage crisis, During the peak of the mortgage craziness in 2005, over one-third of all mortgage originations came with adjustable rates. So at a share of just 7.5%, they’re back where they’d been in the 1990s.

Note, however, that various forms of adjustable-rate or variable-rate mortgages dominate in many countries, including Canada, Australia, Spain, and others, that have become known for their blistering housing bubbles, and in Spain’s case, also a devastating housing bust.

In New York City, 52% of the homes listed for sale last spring still have not sold. For sellers, “the situation calls for a clear strategy: cut prices.” Read... Liquidity in New York City’s Housing Market Dries Up

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“There’s nothing that price can’t fix”.

Oh, Tom, could you please stop making sense? Pretty please?

The saying in the business is that price cures all defects. Of course the govt/Fed’s solution was to “fix” prices to an artificial (aka unsustainable) level to cover up the last debacle.

It’s interesting to see the industry baffled by recent developments, but not surprising. Many in the industry are just as detached from the real economy as the new mouthpiece for the Fed, a multi-millionaire private equity alum who can’t see the forest for the trees. His view from the ivory tower, much like that of Dallas Fed’s Kaplan (former Goldman alum with beautiful penthouse views from his adjoining Museum Tower condo units worth over $4.5 million) provides a less than objective assessment of the reality for most Americans.

The real economy (and the middle of America along with it) continues to wither away with spiraling wealth inequality. With multiple industries exerting cartel pricing power and consumer debt ratcheting higher every quarter, of course something has to give. It would appear decades of can-kicking are coming back to bite the housing market in a serious way.

https://aaronlayman.com/2019/02/denton-county-home-sales-fall-out-of-the-gate-in-2019/

and years of ass-kicking, now the donkey kicks back….

I think that for some, their home is part of their retirement strategy (like a separate 401k). It may be hard for these folks to realize that their investment needs to written down and accept the implications of that

The smart money today is in cash, the stupid money is in everything else.

Tom Stone, So glad your doing well, CCLT….

Greater fool theory in action.

I really think you need to see 4.00% on 30 yr to see any pickup in housing outside of seasonal factors. Another 50bps and we are basically inverted however so either the Fed is cutting next or housing has a healthy adjustment coming. Maybe both.

Problem is we ran out of greater fools.

The fools are still there. It’s just that they have low paying jobs or crushing student loans, and therefore can’t afford these prices.

Yep it’s very hard to sell things to people for whom the things are just plain out of reach. This is happening with cars and it’s happening with houses. Notice how bicycle sales are trending upward:

https://www.statista.com/statistics/468241/us-consumer-spending-on-bicycles/

You’d not expect to see this with an aging population that’s increasingly overweight, which should drive bicycle sales down. You’d expect to see this in spite of those factors in an increasingly broke population that increasingly needs a bike to get around.

Oh believe me there are still loads of foosls left. I work in academia as a postdoctoral researcher in the u.k and two office colleagues have bought houses this last week alone. Both are on short term contracts (<2 years) and managed to borrow around 7x their paltry annual salary. One of them said the estate agent had told them that there had already been 4 offers on that same house that day and if he didn't put a high enough offer in by the end of the day then it would go to one of these mystery buyers. It's ok though because the price my colleague did pay in the end was, in his words, "well underpriced" and he amazingly bid the highest out of all the interested parties!

A bit off topic but at work yesterday we were looking on google maps at Pripyat/chernobyl. It took less than 2 minutes for someone to start talking about house prices in the area. I used to try reasoning with these people but it is an ingrained mental illness here in the u.k and i'm sure the same thing is present in other countries so all that's needed to boost mortgages is to lower lending standards because what could go wrong.

Most Americans realize the world is headed into a second great depression far worse than the dirty thirties. Home prices like almost all other assets will plunge in value.

The plot thickens. It’s tough to plan anything with the Fed constantly flip flopping on rates and QT, so called “patience.” Ok, so a lot of buyers (who if they waited this long are probably pretty savvy) will be patient until they can figure out what the hell is going on. Not to mention they are probably a little freaked out by the fact that the so-called “strong economy” can’t seem to withstand a little uptick in rates or a shallow attempt at balance sheet “normalization” (more like balance sheet propaganda if you watch the Fed sliding all around from month to month regarding QT). I think we will see a stalemate between buyers and sellers on price for a while and at the end of the year may come unglued. Meanwhile the DOW and NASDAQ are pushing back toward their all time highs. There are a lot of IPOs scheduled for this year. Those employees better hope the market stays inflated through the end of their lockups.

Ignoring the money launder, insti buying and price insensitive buyer group, just talk about W2 taking on mortgages. Only two parameters matter, income and rate. Back in 2009, unemployment was in teens, now 4%. Back in 2012 days, 30 year fixed was 3.5%, now 4.5%. I do not know what will happen, but I do know 2009/193x style deflation will kill jobs. I do know 197x inflation will push mortgage rate to 1x%. To me, with house fully priced under double income, full employment and historical low rate, either deflation or inflation will kill the W2 buyers. Deflation could kill existing W2 owners due to income loss and inflation may help existing owners if they can carry the debt through it. For owners, underinflation, monthly bills will add up due to food, gas and you can never refinance, sustain through it is the only way. I see NO good outcome either way and they better hope they can maintain the goldilock, not too hot, not too cold, just right, all the time for ever! No hard brexit, no yellow vest, no China devaluation, No Italy exit EU! Above said, income can rise dramatically under IPO, and that is the thing about Silicon Valley……..

Trojan Man, I don’t know how if I’d call myself savvy but I’ve been waiting this long and the ripples on the water are definitely making me think what’s the harm in waiting. Prices can’t sustainably go higher for much longer.

At least in Sothern Calif, I do’t see prices coming down in a meaningful way… although sales volume has come down a lot

Let’s wait..

Jon, this is like 2007 again. Real estate moves at the speed of Snail. Also dont expect a third housing bubble to bail you out or the Chinese money launders out this time.

It depends on many factors.

Good area

Updated/turnkey property

Realistic price

That will go quick with multiple offers.

Take the opposite of the above and it will sit and sit and sit.

Lets hope Dan has been saving his commission checks…

I’m actually a mortgage broker and not a RE broker.

Just had my biggest month ever thank you.

Just calling it like I see it. No the sky is not falling and a crash isn’t happening. Some areas are down some have plateaued. A pullback is healthy and needed.

Oh and yes you are correct, as all self employed individuals should do, save. I’ve got around 5yrs reserves with 0 debt (other than my mortgage)

Well the prices will come down when the civil-war begins;

I’m seeing in North Arizona where lots of my friends as a kid from LA, moved too, I bought a large acreage for the heck of it ( near flagstaff cash ) in 2001, I have been trying to sell 10+ years for 1/2 what I paid, so I know this stuff is worthless and demand is gone; Largely because the cost of water now is astronomical, it used to be cheap to truck water, and a well has always been out of reach for the “Tremors Crowd” ( AZ is the only place in my life I ever lost money on land/homes ); The problem there is taxes they charge out-of-state folks 2X,

I think Portland & Seattle are still doing fine, left LA in 1970’s and never went back. RE in PDX is up 30X from 1970’s. People still moving north from LA to ‘escape’

Some +90% of all wealth produced has been made in Real Estate, they dn’t make anymore unlike stock, bonds, and/or crypto.

But like AZ, the essential problem with most of South Calif is ‘water’

…

Lastly I think the drop is because people aren’t going to get their tax refunds, and now people feel poor.

Also Trumps new tax stuff hits a lot of the second home demand, so we’re going to see lots of re-adjustment;

IMHO RE is still the only way for a ‘kid’ to get rich and retire by 35, say if he starts acquiring ‘fixers’ at 20 on 15yr fixed.

Maybe put some solar cells or wind turbines on the land? – I prefer solar myself for the simplicity.

That way it can sit there and at least make *some* money.

“… renewed uncertainty about the domestic and global economy likely held potential homebuyers off the market,…” says Mr. Kan of MBA. In all my life I’ve never known a working guy who knew anymore about the domestic and global economy than the certainty/uncertainty surrounding his own job. That is a very funny quote and basically means that he doesn’t have a clue.

And although I know the data discussed is loan applications, I will mention that it appears the loan approval rate is going down. I still follow the state of real estate in our section of town and in the last couple of months I have seen 3 out of about 10 or 12 “pending sales” get put back on the market within a month. That is new. I have seldom seen that happen here previously.

I think if we were in a market where house prices were in line with the incomes of those in the local home buying community then an increase in interest rates would decrease sales ( or prices) accordingly and then when the interest rates went back down the sales (or prices) would go back up to match. But we are at the peak of a bubble market and prices are out of whack with buyers so the drop in sales (and prices) that followed the increase in interest rates crushed the delusion that many in the house buying market had that prices would only go up. So now they are less likely to stretch for an unaffordable mortgage (even with improved interest rates ) with the thought it would soon go up and they can flip it. Many people now have a new mindset and it will take a large drop in prices to correct that.

Home buying and selling is essentially a comment on migration, migration for jobs, warmer climates. Maybe everyone is where they want to be (for the duration)

Wonder what that chart would show for san Jose CA it seems this city is booming right now

Daniel r Gallardo,

Booming? Home prices in Santa Clara County took a big dive. For example, median price single-family house down 11.5% in December year-over-year, and back where it had first been in April 2017, according to the California Realtors Association:

Hate to say it, but it still looks as though a seven-year trend is intact, just touching the “support” line around now. That median would need to drop below a mill ere I’d call it a reversal.

“known for their blistering housing bubbles”…

You may now lump Canada and Australia into the housing bust.

In Canada’s case, the two hottest real estate markets of Toronto and Vancouver, have seen the pricing of housing dive, with fewer listings. The Canadian household debt is growing at the slowest pace in 35 years!

As for Australia, their real estate sector is in shreds, as are the financials that depended on ever increasing real estate values, that are now gone.

The weak real estate sectors in both these countries, started before the current concern in the American mortgage market. Most all of the global financial fundamentals point in one direction, down. The looked for and anticipated global recession is here. Most do not, or will not, recognize it as being such.

Some figures for Spain, remembering the market is still being propped up in various ways :

Although prices recently inched up, they are still a third down from 2008 peak in real terms

https://www.idealista.com/news/inmobiliario/vivienda/2018/11/23/769690-fomento-la-vivienda-se-sigue-encareciendo-pero-es-un-tercio-mas-barata-que-en-pleno

And the evolution of fixed rate mortgages is visible at

https://www.elconfidencial.com/vivienda/2018-09-10/hipotecas-tipo-fijo-tipo-variable-tipos-de-interes_1613084/

they now make up 40 % of new mortgages, whereas before were token.

Clearly the vast majority of existing mortgages are still variable, so what happens if rates rise is a guess as the knock on cost of monthly payments is large, and immediate. As people don’t much seem to want to refinance into a higher fixed rate now, it is therefore maybe unlikely they would want or be able to once rates start moving upwards.

So for now Spain is the housing bust that doesn’t want to be one but that hasn’t found how to escape beyond pressing the pause button.

Vancouver is in the midst of an all out collapse. The GTA could see a second leg upwards depending on what’s in the upcoming April budget speech.

I guess my biggest question about housing prices and mortgage interest rates is how much effect they actually have on monthly payments. When I bought my first house in 1982 I paid $52,500 for it from a person who purchased it for $86,000. I got a 30 year mortgage at 12.5 percent interest and still wonder if the person who bought it for $86,000 actually had a lower monthly payment than I did. If interest rates go up and cause a fall in prices, does it matter? Any thoughts?

It’s better to buy with lower principal and higher interest rates. Assuming the mortgaged principal is below the limit, you can write off the interest if you itemize. You can also refinance to a lower rate if rates drop, but you still have to payoff the principal regardless of rates. You can also get more house with your down payment if prices go down, so overall as a buyer I would rather pay higher rates and lower principal for my purchase (or best of both worlds after a crisis with low principal and low rates).

You also pay taxes based on the purchase price for as long as you own the home.

As an aside, agents prefer to see a credit for repairs rather than a price reduction because we are paid a percentage based on the sales price…

A higher interest rate will cause you to pay thousands (maybe 10’s of thousands) more for your RE purchase. Buy when rates are down and use the difference to pay off your mortgage faster. Paying interest is a waste of your money and is an investor’s dream. I make no money when you pay down your principal, so please, keep those interest payments coming. The tax savings on interest is minuscule compared to your spending on long term interest payments.

When interest rates are low the purchase price is higher. Its better to buybwith high interest rate and lower principal.

My coworkers that have completed their 2018 taxes, have remarked that home interest is no longer a deduction, because the new standard deduction is higher.

The interest tax deduction for a Home isn’t a tax deduction any longer for the majority of Americans due to the increased standard deductions.

You got a good deal on a house:

https://fred.stlouisfed.org/series/ASPUS

Most people don’t actually buy a house for the sale price. They buy a house for the PITI monthly price, based on their monthly cash flow. So if interest rates go up, Principal will have to decrease. It’s just a matter of how and when that decrease occurs.

Falling prices matter a lot for existing home owners. Because it eats up their equity which they would normally be able to use to trade up.

If you don’t own it doesn’t directly effect you. Though certain homes that would be sold by people looking to trade up probably wont as falling prices could trap people in their homes or make moving less desirable.

I agree with below that it is better to buy at a lower principle with high interest. Assuming interest rates are unlikely to go higher.

The only good reason to finance a house in a bubbly market is if you think you can unload it on another sucker at a much higher price in the not-too-distant future. That $hip has already $ailed. Hope you’re like me and your former home equity is sleeping $oundly in T-bills ready to buy at the bottom.

Perhaps everyone is just massively confused with all of the double talk from the Fed. Perhaps the consensus is that rates are headed lower now, but now wages are going up, CPI numbers look ok, so perhaps keep rates where they are at, or maybe hike a bit, or if we strip out the energy hit on the CPI perhaps we need more hikes, or…….and so on.

One the FED started catering and pandering aggressively to the equity market, and became massively political over the course of just 2 months, it just left everyone completely confused. Four to two to zero hikes with no material degradation in domestic economic data.

I heard there was a recent speech on the importance of the independence of the Fed from politics. This speech, in and of itself, is very hypocritical. More doubletalk.

No Chinese flippers, oops, I mean investors, means no gamblers buying at any price. With gamblers out of equation means RE agents can’t setup phony lineups, and multiple cash offers. That has a psychological effect on the local fools. So, now RE industry can’t even get the local fools to make offers.

Also, there are a lot of large scale layoffs that you hear about, but also a lot of large scale layoffs that no one hears about. For example, last year, Oath (which is Yahoo and AOL combined) laid off all its contractors. We are talking about at few thousand contractors; yet, you can’t find even one headline news about this layoff. God knows how many other large scale layoffs are happening that no one hears about.

The first chart shows some seasonality effects. January-into-February was a time of slowdown for both 2017 and 2018.

Sure. Hence the year-over-year reference of a decline of 5%.

Interest rates are only one part of the total picture. When I first became a Realtor in 1986, interest rates were 12%, and the market was hot. Average Days On Market (DOM) was 18 days. In took a few years for interest rates to wind down to 8%.

If people want a house and can afford it, the demand is there. Today’s first time buyers may want a house, but few have any savings or the income to purchase a house.

Roddy,

What about job instability and greater need for mobility. That’s doesn’t impact buyers and sellers? I know a guy who married late in life, stay at home spouse w 2 young kids. Won’t ever buy, worried about job stability and needs to always be mobile. Isn’t this the new norm? Renter for life.

Nailed it.

Inflation sure seems to be taking hold. Rents continue to rise. I am a landlord. A Manhattan Beach home I rented for $3500 ( 2Bd, 1Ba ) in 2014 is now rented for $5300. A Corona Del Mar home ( 2 Bd, 1.5Ba ) was $3600 in 2013. Now, I have it rented for $5200, but I have seen similar homes rent for just under $6000. Health insurance … I am 48 and retired. My Covered California insurance just hit $2100 per month for my wife and I. That was a $450 a month jump. I bought a brand new base model Toyota Highlander in 2014 for $26500 at the end of year. I am looking to replace it, and the price for the same vehicle is $32000. Small 3Bd/1Ba well located east Manhattan Beach homes were $850K in 2014. Now, $1.9M. In Corona Del Mar, a 3Bd/2Ba Irvine Terrace home was $1.7M in 2014. Now, $3M+. This is what I see. And, I still see a bid for these homes. If the Fed does not raise rates by a significant amount, I think inflation will accelerate. Not buying a home is a risk that inflation will damage your future. Good luck with that.

who are the fools paying you that kind of rent money for properties worth 1/2 that…..so many sheeple out there….Irvine is worth about 1 million at most…it will see under that in 2022…..

Buying a home at the top like right now will damage your future, there is no bailout of speculators coming this time……no one is buying homes right now because the up cycle is over, the down cycle has just begun, 2007 rewind

2020 it begins…so let it be written, so let it be said……

cd, you might be right. Or you might not. It is really all about where inflation comes in at. To me, I think the Fed does not have control of inflation like they did in the past. And, the Fed losing control of inflation is a risk all of us live with. I am betting it goes higher. Renters are betting it will fall. We would all be better off if the Fed figured out how to manage inflation.

As far as Irvine goes, average price is around 1M. But, that is a hard market to figure out. The Chinese control that market and I can not figure out how they view housing investments, so I stay away.

SoCa,

Inflation and interest rates in my mind are two different things. I think by your comments you would agree. Fed already capitulated, but based on data, rates should continue to rise and balance sheet roll off should continue but Fed I believe has a plan to cease rolloff should need arise…

PS – what are the demographics of your $5k / mo tenants and props to you. Nice cash flow.

At some point, artificial control of markets won’t be possible and then its 32 ft / sec / sec.

the 5 year moratorium on selling bulk purchases bought by PE is now over, the fed, treasury and govt. turned housing into investment, essentially backstopping PE, Hedge and foreign PE (obama changed tax rules in 15 to allow for more purchases). Take notice of what Geithner and Paulson are saying about rents killing GDP. Lets be honest, this was the biggest heist of wealth transferred to bankers in the history of mankind. I see this year as distribution because of the investment meme of housing now that the pigmen ruined it. Just like the libor, commodities, stocks etc.

Inflation is not going to rescue housing, you would need to see rates go up to see inflation, the fed has it backwards, low rates have cause deflation….its not the 1960’s anymore….

I will lose a lot of equity on my home but I just like the roof over my head right now with the rain coming down in the city…. I wish they would tar and feather these fed engineers who bilked a lot of un-savvy finance folks…..

But with the fed, you never know, supporting and bailing out the 1% since 1913

Bart,

They are professionals in their mid 30s to mid 40s who could but do not want to buy. They are want the freedom to move, and they want to rent in a nice area. Different mindset than my generation, which is approaching 50.

FACTS

Okay, after 10 years of low rate to lift asset prices, the house owners start to find difficult to offload houses to next suckers because rate can’t go down any more and worker’s income is still limited because they lazy fucks can only work 60 hours a week. Hmmmmmm house is NOT selling, soooo let’s jack up the rent to justify the cap rates! Use inflation to scare the shit out of those suckers and let the banks issue 60 year mortgages to transfer their next 60 years earning in my hand! Who says human can only work for 30 years? But here is the thing. Cars and houses are interest rate sensitive stuff. interest rate is a slave of inflation or the FED and the country’s currency dies. If in deed inflation happen, people using cash can buy houses but people use debt and monthly payment can NOT. More likely, people will put their down pay into other commodities that do NOT require borrowing money. Maybe gold will shine? By the way, when it gets down to that, don’t you think people here will behave like Venezuela people eating zoo animals and smash your properties? It will bring the worst out of all the people and release all the hatred out of wealth inequalities built up during the past 10 year underFED asset inflation policies.

The best way to fix this would be to deflate asset prices such that the mean assets will slowly drop to make the wealthy more like me.

I think the Fed is working on this with stock and house asset leveling or slow deflation. Inflation increases and wage growth will take care of the rest. Pretty soon the wealthy will be like you and me.

It’s not the wealthy’s fault that their Silicon Valley house they bought for 350K in 2010 is now worth 1.1M making them wealthy.

Or their Apple stock they bought for $10 in 2003 is now worth $700 with splits.

SoCalJim – Inflation is nonexistent outside of bubbly financial assets (stocks and real estate). Go to the mall or shop on Amazon and look how impossibly cheap all consumer goods are.

The Fed suckered everyone into stocks and real estate with QE and they hit the brakes after a sufficient number of suckers bought houses. The tax reform act will absolutely devastate RE prices in your neighborhood. Wonder why inventory is skyrocketing in Cali? Everyone is bailing and trying to sell their homes at the same time. I seriously doubt your renters will renew because rent and home prices are both starting to drop nationwide. Especially the in the luxury segment….Deflation is a much higher risk than inflation at this point.

Nothing better than a mortgage deduction cap and a 10k limit on tax deduction can’t do. Elevated house prices look down below.

Haven’t most responsible homeowners already refi’d in the last few years when 30 year rates were at 3.5%?

Even the people who did refi back then and need more cash now may be finding appraisals are coming in flat or lower so they can’t jump on these new 4.5% rates.

That is a reason for refinance volume to decrease in my humble perspective.

I’m a little surprised nobody is talking about the ripple effects of a housing slowdown.

It’s more pronounced in places like here on The Other West Coast of Florida, but when housing collapsed in ’07, so did the job market and the rest of the local economy. Since we’re a mecca for tax- and cold- refugees, the second home market drives everything else … so I’m expecting it to get pretty sporty here in the next year or two.

The only likely positive driver will be people making their second home their primary, once the SALT deduction makes New Jersey untenable.

Great article, I love Seattle! The snow up there was crazy a couple weeks ago! 2 to 3 feet in some areas from what I understand. Crazy! I hope you all are staying warm :)

Is the data Seasonally Adjusted or not? if its not seasonally adjusted, then it wouldn’t be a surprise at all for January purchases to decline, and that would change the analysis.

please let us know.