“A development that is surprising during a strong economy and labor market”: New York Fed

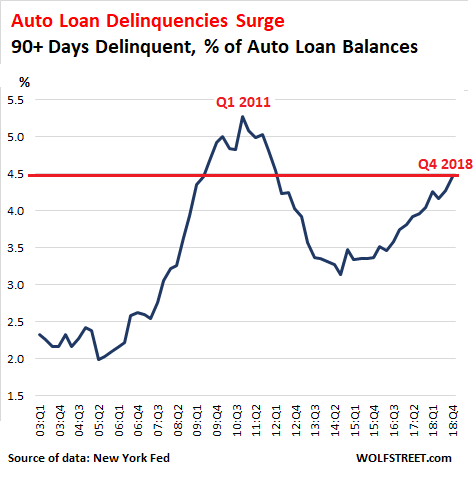

Serious auto-loan delinquencies – loans that are 90 days or more past due – surged to 4.47% of total auto loan balances in Q4 2018, according to New York Fed data this morning. This put the auto-loan delinquency rate at the highest level since Q1 2012 and just 0.6 percentage points below the peak during the Great Recession in Q1 2011.

At the end of 2018, there were over 7 million Americans with auto loans that were 90+ days past due, 1 million more than at the end of 2010, at the peak of the overall delinquency rates, according to a separate report by the New York Fed. It added that “the substantial and growing number of distressed borrowers suggests that not all Americans have benefitted from the strong labor market.”

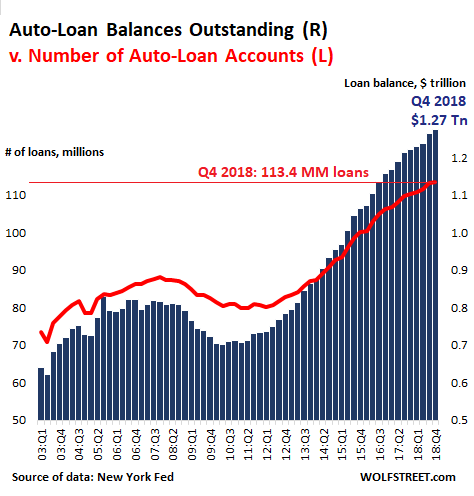

The dollars are big. Since the prior peak in Q2 2008, total auto loans and leases outstanding nearly doubled to $1.27 trillion (this is slightly higher than the data reported last week by the Federal Reserve Board of Governors as part of its consumer credit data).

But the number of auto-loan accounts rose only 28% over the decade, from 88 million accounts in Q2 2008 to 113.4 million accounts in Q4 2018, even as the loan balances nearly doubled.

The chart below shows the dollar amounts of auto loan balances (blue columns, right scale) in trillion dollars and the number of auto-loan accounts (red line, left scale) in millions of loan accounts:

The percentage of vehicles financed, as compared to the total number of new and used vehicles sold, has remained roughly steady between 50% and 60% over the decade, according to the New York Fed. The remaining vehicle sales were paid for in cash.

Here come the subprime auto-loan delinquencies

The share of total auto loans outstanding that was originated to subprime borrowers – with a credit score below 620 – inched down to a relatively low 22%. However, the New York Fed pointed out, as auto loans have surged, that:

- “There are now more subprime auto loan borrowers than ever, and thus a larger group of borrowers at high risk of delinquency.”

- “The overall performance of auto loans has been slowly worsening, despite an increasing share of prime loans in the stock.”

Hence the 7 million Americans with auto loans that are 90+ days delinquent.

And the flow of loans into serious delinquency is picking up steam. The share of loans that were current or in early delinquency in Q3 and became seriously delinquent in Q4 ticked up to 2.4% of total auto loan balances.

But among subprime auto loans, the share of loans that transitioned into serious delinquency rose to over 8% of their balances in Q4, “a development that is surprising during a strong economy and labor market,” the New York Fed added.

For loans to borrowers with credit scores one step up from subprime (620-659), the share of loans that transitioned into serious delinquency was about 3%. For borrowed with credit scores between 660 and 719, the rate was just above 1%. And for higher credit scores, the rates were minuscule.

Who’s originating the subprime auto loans?

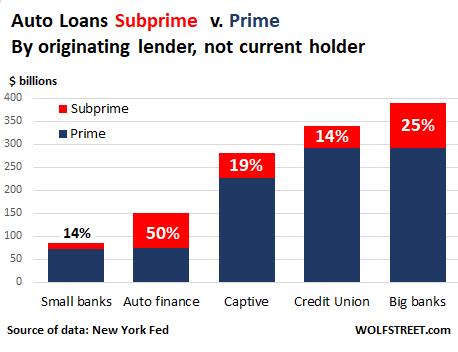

There are about $273 billion in subprime auto loans outstanding. So who has originated them?

Specialized auto finance lenders – among the many non-banks or “shadow banks” – have piled into this sector most aggressively. While they originated only about $150 billion of all outstanding auto loans, half of their loans ($75 billion) are subprime.

These are auto-loan balances by originating lender type, and not necessarily who owns them. Auto loans that are securitized are held by investors. And specialized auto lenders try to securitize most of their loans.

Big banks – those with assets above $500 billion – originated the most auto loans ($389 billion), and 25% of them are subprime.

“Captive” auto lenders, such as Ford Motor Credit, originated $281 billion in auto loans, but only 19% of them were subprime. Small banks and credit unions had the lowest risk profile, with only 14% of their loans rated subprime. But credit unions are the second largest auto lender after big banks:

So who gets in trouble over subprime auto loans?

Not the credit unions, with their clean loan book: only 0.7% of credit union auto loans are 90+ days past due. And not the small banks and the captive lenders.

The “big banks” – banks with over $500 billion in assets – originated $97 billion in subprime auto loans. But some of those loans were securitized and are now in the lap of investors. The exposure that remains is small compared to the size of these banks. There are only six of them in that group, ranging from Morgan Stanley ($852 billion) to JP Morgan Chase ($2.5 trillion). And each of them is big enough to digest the losses that might occur in the sliver of subprime auto loans it may still hold.

It has been and is going to be a little rougher for specialized auto lenders – a number of which have already collapsed in 2018 – and for investors in auto-loan ABS.

Consumers are doing their job only in a lackadaisical manner. But the student-loan scheme is hot. Read… The State of the American Debt Slaves, Q4 2018

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wow those stats are terrible. And no surprise seeing prices on the most basic boxes. A bare bones FWD 2.0l crossover with a stick shift ‘starts at’ $20k, immediately clicking the summary button and bingo, another grand (5%!) tacked on for ‘destination’. I assume a significant part of the balance growth is buyers who roll over negative equity on trades or decide what the heck, it’s ‘only’ another $150 a month 5 years long for the Denali package. But damn, can’t we get a little downward pressure of the bling in the base models.

Why start pricing at crossovers?

Midsized and compact cars start at as low as $14k new. And you can easily stay at $10k or below used for a 3 year old used model.

For that matter a small used crossover like a Hyundai santa fe is only $16k before tax and tag.

Car prices are only a problem if people think they are entitled to a new F150 or a luxury car.

good point, where should i shop?

Because there are no bare bones old school station wagons or sedans anymore for a family which may need actual room. A comparable sedan might be a Camry/Accord class. The crossover I’m referencing is a glorified tin box mounted on a car chassis with barely enough power to get out of it’s own way, in other words a bling filled piece of crap.

I stopped buying new cars years ago, buying one to 2 years old with warranty and low mileage. Let someone else take the hit for driving it off the lot and save 20-30%. I suspect some of these defaults are the downside of that new car smell.

That new car smell is toxic adhesive offgassing.

We buy new when incentives are high, typically amounting to 15%, and drive them to the junkyard.

GM credit card, pay the balance monthly, collect 5% towards purchase, then they sweeten it up even more around model year turnover. Trick was finding a bare bones model on the lot anywhere within 200 miles.

You’re smart. Sometimes more than 30% for just a handful of miles. It’s a no brainer

” This put the auto-loan delinquency rate at the highest level since Q1 2012″

Or, Q2 2008. It took a crisis to hit peak, and we’re already at levels seen in 2008.

Yes. But unlike in Q2 2008, the labor market is still strong. So this is going to be fun :-]

Does that mean the coming downturn (maybe pushed out thanks to the Fed’s recent dovishness) will be worse than the previous one?

Stop worrying, Wolf, stock market on a tear, everything is awesome… sing it with me… everything is awesome.

If that doesn’t work out, the Chinese middle class will save us. Then if that fails, more QE with the Fed. Finally, the fallback to the fallback to all the fallbacks. The NEW GREEN DEAL… gawd, makes me wanna sing: America… F*** YEAH…

It could never be the case that those “headline” numbers are cooked more and more every year and what is “Strong” today is maybe based on a “slimmer”, and more exclusive, set of statistics that it used to be?

There is an unreal quality to news-items moaning about the lack of skilled labour all the while that wages are not going up, businesses do not hire trainees, they do not hire marginal candidates (people who could work after a while) and everyone are laser-focused on only hiring the exact same demographics, with exactly all the skills listed on the advertisement. The mythical unicorn candidate is still being sought after.

We should see compromises being made if the labour market was indeed strong, as in there being a “hard” demand for labour, but we don’t see that “around here” (Denmark).

Interesting that you said Denmark – your description sounded spot on for the US situation (I’m in Los Angeles, the city of tents)

The labor market NUMBERS are better but are the jobs? Is there any possibility those securitized loans get thrown back in the lap of the banks? The 2008 housing unwind is a bad example of how to unwind debt.

Wolf,

I don’t mean to be a jerk on your blog but is the labor market really strong and for that matter, is the economy really strong? Unemployment is low but for a vast swath of workers, good jobs (solid middle class wage and job stability) are difficult to find. Me thinks the low interest rates have juiced things which in turn has helped GDP. If the economy in my opinion were truly strong, it could handle interest rates at least 1.00%-1.25% higher than they currently are. As it stands, after the last rate hike, Mr. Economy got wobbly knees. In my opinion, the economy has been on life support and the defibrillators are wearing out and keeping it going with chest compressions is going to be exhausting and unsustainable.

Yeah, I get all this. And there are big problems in parts of the country. But overall, it’s the strongest labor market I have seen since 1999.

This observation might just say how lousy the labor market has been since 1999, and that it’s just less lousy today :-]

Don’t look now but I know of plenty of engineers and tech workers who routinely get tossed out the door when they reach their 50’s. Good luck on your job search if you are in that boat. Age discrimination is flourishing … thanks in part to the Supremes who of course have life time tenure. After a while they don’t even get counted as unemployed.

The point of sale is trying to hold the gross margin as high as possible, naturally. A good example might be navigation; actual cost low, what they will pay to get it…like $1100 on a new car. And the mark has a redundant system on his smartphone!

One thing of interest is that good sales people know that half a loaf is better than none. So, for the subprime buyer, hold as much gross as you can, but give it up big time just to get that subprime person to sign. No matter if he can afford it of course; we ain’t holdin the note. Some really thin deals are done to get subprime done.

Inflation in the car business is good. Sharp finance people can work it!

Header today on MSNBC: A record 7 million Americans are behind on their car payments.

I wonder how many Japanese are behind in their payments?

Note: it is the Japanese govt that is deep in debt, which is mostly held internally. Japanese households are very thrifty with over 20 US$ trillion equivalent in savings.

A more “gradual” rate of increase in delinquency this time around, but then it is said fortune knocks but once while misfortune has much more “patience”.

Until 2008 housing as a whole never truly diminished in value (on a national level) which is why they were considered an excellent investment because the underlying value of the asset was considered stable (until the subprime mortgage crisis occurred).

However, for vehicles, the underlying asset depreciates very quickly so in the case of a repossession due to default only a fraction of the loan outstanding may be recovered.

Nonetheless, if big banks and investors wish to expose themselves to risk to bolster their balance sheet, theoretically its no skin off my back.

“Subprime lenders are willing to take a chance on these risky borrowers because when they default, the lenders can repossess their cars and persuade judges in 46 states to give them the power to seize borrowers’ paychecks to cover the balance of the car loan.”

https://www.nytimes.com/2017/06/18/business/dealbook/car-loan-subprime.html

In other words most are recourse loans, though I don’t have the percentage figure of that.

Bankers my apologies I didn’t realize this was the case, pardon my incredulity however such practices appear barbaric for a civilized nation.

Surely it would more equitable to require lending institutions vet borrower’s to an adequate degree rather than involving the courts?

A civilized nation..?

There’s so much that points to the fact that the USA isn’t a civilized nation, it’s difficult to know where to start really…

Its premier is a massive clue, though!

No apology needed, although I realised something like this was the reality I still had to search it up to be certain.

It is very hard to pin the moral,or lack of, in the above equation. Is it predatory lending or ignorant self serving borrowers for exampe ? Should the unreliability of payment from subprime be reflected in interest rates which punish the poor , it must… or no?

The fact that the system is broken and often immoral should give people reason for deep thought. Probably making debt non recourse would rectify this, or that avenues of claim were obliged expressly mentioned in contract and individually signed by the borrower would raise awareness. The way things are is that all market prices are affected by current law, when you try to change it, you change the market and prices and earnings – there are lobbies against that also.

Something to consider I suppose.

“[T]here can be no doubt that the standard of commercial honesty would be much higher in the absence of laws for the collection of debts.”

— Henry George

I used to think this, but it seems the way it works is, overcharge up front, usurious rates of interest, fees tacked on, etc, etc, THEN repo eventually. Theyve done the math. The repo is so simple now that until residuals go well south of where they are, it’s still profitable to lend to just about anyone. The problem is, in a downturn, given the number of cars that were leased that are already coming back, and the number that will be on lots as people default and get repo-ed, and the pile up of overproduced new cars sitting unsold on lots…those residuals are going to plummet. Then, as they say, we will see who was swimming naked. For now, it’s dance while the music is still playing.

Gee, don’t forget a strong down payment with the usuriuos rat that is lost by buyer es and once repo’d the vehicle is often sold again by the same dealer. Sometimes multiple times.

Last time I have the dog help me with a post!

Howard, “vehicles, the underlying asset depreciates very quickly ”

I was a recent purchaser of a new SUV. And maybe I am just not normal but the idea that vehicles lose a huge percentage of their value when driven off the lot sure didn’t appear that way to me. Low mileage used SUVs didn’t seem to be a great deal to me.

I calculated that the price difference had more to do with mileage on the vehicle than any thing else. And the risk that a low mileage vehicle turned in could have a lot of negative reasons, like no maintenance while owned, or reoccurring problems. Or else why turn in a perfectly good vehicle?

So for me paying only a few thousand more for new seemed to be more sensible than buying a few year old used for almost as much. I keep vehicles a long time.

I’m sure part of why the cost / value is staying high is that money is available to finance everything while the new vehicle mfgs are still unwilling to lower the prices on new. So those who can’t qualify for new go for what they can afford to purchase keeping prices high. Just like in homes. I’m sure that families making over $200k/yr would rather buy a 3/2 2500sf home yet in SF are stuck with a shack because that is all they can afford where they can make $200k / yr. As long as there is abundant money to borrow, all prices will remain high.

What the dealer will sell you a used card for is not what it’s worth. Since you wont get the same price they get except maybe in a very lucky private resale. But you are right late model cars with under 20k miles are not a particularly good deal always.

In general people will pay the dealer more because of trust.

Every car depreciates a bit differently. A Honda pilot who olds its value much better than an Audi sedan. So you can find new vehicale that dont lose 30% of their value once you drive them off a lot.

Also with late model cars, they are so rare to find used that the dealers sell them at almost new prices.

Hyundai lose value quicker. I was able to get a Hyundai Santa Fe, 2 years old with 20k miles with a full tech package for $20k before tax and tag. That package was 30k new after incentives which means tax was higher too.

Another factor along with higher stickers and 7 year payments: the rising cost of repair which I suspect is running above inflation AND perhaps even as a percentage of sticker.

Some of these auto transmissions are racking up big repair bills. A relative just had an Audi trans bill for 13K.

I keep reading about the need to carefully maintain the CVT types, to make sure they get their $100 oil ever 30 K (or so)

We keep hearing that the trade- in car is increasingly ‘underwater’ so the new loan is bigger than the cost of the new car.

I suspect some of these second or third- hand cars are going to turn out to be not economically repairable.

The repair scam/warranty dodge is what keeps the buyer tethered to the dealer. The gift that keeps on giving. The work is done by a $20/hour apprentice and the shop charges $110, plus parts markup.

The apprentice doesn’t do transmission work, the low wage apprentice does oil changes and tire repairs. Go to any shop that has been open for more than 5 years. The older experienced tech is so expensive they can’t be bothered with tires or fluid changes (in automotive repair shops those maintenance tasks are considered loss leaders), and on the flip side the cost of R&R for transmission work is too risky to have a failure to put a flunky on the job.

The real scam for tech work is quick lube places, avoid them like the plague.

The scam for dealerships is the third party warranty, it covers everything on paper but when you go back to claim it they find a way to deny warranty every time.

In my case the 3rd party warranty worked out. If I had not gotten it I would have been scr%$wd! I purchased my 2011 Kia Forte which I had originally leased, and I assumed I would have had the entire 10 year 100,000 mile Powertrain warranty, only to discover, when I needed repairs at just over 60000 miles, that the Rick Case dealership in Atlanta where I originally leased, then purchased the car from, had pulled a “fast one” and “purchased” the car from my lease, then “resold” it to me as a “used” car, thereby negating the factory 100,000/10 year warranty and leaving only the 60,000 mile warranty (which by teh time I needed repairs had run out). Fortunately when I “bought” it, I opted for an extended warranty as, I wanted the protection of EVERYTHING being covered, not just the powertrain (which I had assumed would be covered to 100,000). Anyway as it turns out it was a REALLY good thing I did, since Rick Case sole me a USED car. At 65000, the front axle had to be replaced, at 90000 the power steering went, and then at 102000, the transmission went. All the above WAS covered by the extended! If I had not gotten that, I would have been SOL.

Moral: NEVER EVER deal with Rick Case KIA, Always verify that if you are buying your car off lease, make sure it is recorded as a NEW car purchase (I had never leased a car before and don’t know if this is an “industry Standard – I had ASSUMED I was buying the car as a NEW Vehicle since I was the ORIGINAL lessee) and most importantly – I will NEVER EVER buy a Kia Again – ever. There is no reason at all why these issues should have arisen at such low milage, except KIA a cheap piece of SH!T

Lessons learned, and buying the extended save my A$$!

Aaronbav2019,

It seems, you have a misconception about what constitutes a “new” and a “used” vehicle in a lease. So some info is needed. When you lease a new vehicle, you engage in a 3-party deal. It works like this:

1. You chose a new vehicle that you want to lease and make a deal with the dealer.

2. The dealer then SELLS the new vehicle to the LEASING COMPANY. This could be a bank or a captive like Kia Motors Finance, or another lender. The leasing company pays the dealer in full for the entire vehicle. The amount is not disclosed to you.

3. The leasing company tags the car and puts the title in its own name, such as “Kia Motors Finance.” At that moment, the car becomes a USED vehicle.

4. The leasing company then leases the vehicle to you, and you go on your merry way.

5. Much of this happens behind the scenes as the dealer works with the leasing company to arrange the lease.

6. While you drive the vehicle, the leasing company is the owner of it.

7. When the lease ends, you have an option to buy the vehicle. This is what you did. But it’s already a USED vehicle. It became a used vehicles two or three years earlier at the beginning of the lease when the leasing company tagged the vehicle and put the title in its name.

8. If you don’t buy the vehicle, the leasing company sells the vehicle at an auction as a USED vehicle. Some other dealer buys it and then sells it as a USED car to some customer.

There is no such thing as a leased vehicle that is legally considered “new.”

Mr. Richter (I’m replying to the earlier post as I wasn’t sure how to reply to your comment to me.)

Re: New or used – I don’t care if the car was sold to me as either New or Used except for the fact that that was there justification for saying the car only had a 60,000 mile warranty.

It specifically states in the Kia “Warranty and Consumer Information Manual” that came with the car: (pg Page 6 under Original Owner) “If the KIA Vehicle was first placed in service as a lease Vehicle, AND THE LESSEE PURCHASES THE Vehicle at the end of the lease, the 120 month/100,000 mile Power Train limited Warranty REMAINS in effect.”

Fortunately I had purchased a 3rd party Warranty that covered the repairs. If I had not purchased the extended, I would absolutely have taken Rick Cast/KIA to court over it, because it is SPECIFICALLY and PLAINLY spelled out in the manual. Like I said – I never leased a car before and then purchased the car AS THE ORIGINAL Lessee, so I truly don’t not what all the GOTTCHAS are for that. IMHO there should be legislation passed that specifically spells out what the dealership and the company is required to cover TO PROTECT UNAWARE CONSUMERS

I was absolutely under the impression that, as the ORIGINAL Lessee, I would have the full Power Train Warranty. Otherwise WHY would KIA have specifically said that in the manual? If KIA doesn’t want to cover warranty claims of Original lessee’s that purchase the car afterwards, then they should remove that paragraph from the manual, because I do think it would be actionable in Court. Purchasers of off lease vehicles, when tehy are the original lessee should be made aware of this DECEPTION/SHADY BUSINESS PRACTICE. If there was and aeterick * or “fine print clause” involved, then it should be pointed out and signed off on by the buyer that he KNOWS that the original factory P.T warranty is negated because the DEALERSHIP sees the original lessee as the “2nd owner” (which is I believe in direct contradiction to what KIA says . I got lucky that I had purchased the extended Warranty, but if I hadn’t I would have been totally PO’ed…

Anyway, fact remains I feel Rick Case is a Shady Dealer for nor spelling out/telling me directly when I purchased the vehicle, that despite me being the original Lessee, they would NOT cover Power Train repairs under the original 10/100,000 KIA Power Train Warranty EVEN THOUGH it is what is written in the manual. I just have to wonder how many people got scr3ewed by this deception. I now try and warn anyone I know that if they lease a vehicle and think they may want to buy it afterwards to be very careful.

I was happy with the car when I decided to buy it after the lease (only was 3 years old with 45,000 miles) but am totally pissed that the thing that started breaking after 65000 miles. I will never buy a Kia ever again after this experience and warn anyone considering it to just NOT do it and get a Toyota instead.

Sorry, I am still more than a little ticked by this whole experience, even though if worked out for me (because I did buy an extended 3rd party warranty)… So again, in reply to the post above, not all extended warranties are a scam…

Never keep an expensive car beyond drivetrain warranty! That said $13K for a rebuilt transmission is laughable even if dual clutch.

Yes,

When my son and his wife were struggling financially, I told them that they could not afford a used car…had to buy new.

Wolf,

Many thanks for the update on subprime auto loans.

Seems to this observer that the one to watch in this sector might be Credit Acceptance Corp (CACC). 95% of the firm’s auto loans are sub-prime, if memory serves. The shares have nearly doubled since the end of 2016. Company has been wildly profitable. Average yield on the portfolio just over 22%.

Yet when the company published its 2018 10-K recently, noticed that they LOWERED the provision for credit losses by more than 50% from 2017. Find that difficult to believe at this late stage of the credit cycle.

Continental Illinois Bank (1984) did the same thing. They knew they were holding bad loans but instead of increasing loan-loss provisions to account for the potential loss, they LOWERED loan-loss provisions to keep the balance sheet appearing healthy. They fooled plenty of people for quite awhile, but when it collapsed it rocked the financial world.

If you think CACC is doing the same thing, short the stock and wait. Big pay day if your right

CACC doesn’t need to reserve much since they acquire the loans at a 30-35% discount from the selling dealer. Their losses are running between 25-30%, so that leaves them with plenty of cushion. Shorting their stock would be shorting yourself.

Why would a dealer sell a loan at a 30% – 35% discount?

The only loans that trade at that type of discount are highly distressed and on the verge of default.

I looked at CACC’s financial docs awhile back and they made no sense to me. Will CACC get bailed out? If not, its a good short. The chairman was selling Puts on his company so that should tell you something.

If he’s selling puts, then he’s bullish.

Are being sarcastic? A put is the right to sell at a given price which means if the price declines you are in the money because you can sell above market.

A put option is purchased by someone who thinks the stock is going lower.

@nick kelly: Read the above carefully.

Buying Puts = Bearish (right to sell the underlying at a predetermined price, believing the price will go down).

SELLING Puts = Bullish – you’re on the opposite side of that trade, meaning you *don’t* think the price is going down and you’re trying to collect income from someone who does.

Got ya . But why not just buy call options

I’not sure what constitutes a “strong” labor market in the Fed’s view. But what I see is more and more jobs that are being converted to 24 hour jobs and more jobs being “outsourced” to contractors who only provide 24 hour a week employment. While most of the professionals (engineers, scientists, contractors) who support the Federal government are 40 hour jobs, more and more jobs are only 24 hour jobs. This includes medical, educational, service, local government and others.

I’m assuming this population is probably where a lot of the subprime loans are. So it isn’t surprising, with the rising costs of rent, local taxes, food, cars, child day care, etc. that they are struggling to make the payments.

By the way, credit unions loan primarily (exclusively?) to their member clientele and because of the nature of credit unions most of the members are most likely professionals with 40 hour jobs. So I’m not surprised that their subprime loan rate and loss rate is low.

By the way, my own economic yardstick, the number of panhandlers I see, seems to be going up again. Over the past 20 years there has been an ebb and flow in the number of panhandlers that correlates to the local economy. And after 4 or 5 years of almost complete absence in the last two months they seem to be popping up again.

Strong labor market? Uh, yah, right.

The jobs report – like the inflation report – is 100% Fake News, fraud, propaganda.

94% of the “jobs” created under the previous President were part time jobs. And inflation is measured by striping out or underweighting those parts that have experience massive inflation.

No income growth.

That is not a strong labor market. No way, no how.

Again, the jobs report as is the inflation report. are 100% fraud, propaganda, and Fake News.

My current employer has never been more profitable. Yet, the managers retiring are not being replaced. Their work is being spread around to those that remain and by hiring part time workers to share the rest. Whenever they can they hire one or more part timers to cover the work of a full timer. The flattening of the corporate hierarchy is very real in the private sector, even in our strong economy.

Yes, that is the question. How does a company acquire experienced labor without paying for it? What frustrates me is that companies will hire five or so young analysts, who are well (overpaid?) paid and task them with the project of how to get experienced labor cheap. I worked the last part of my career in IT. Our company would pay consultants (who didn’t understand the business) $150/hr. versus paying an Analyst $150,000 annually (includes benefits). Basically twice the expense. The business justified this approach as giving them “Flexibility” to hire / fire at will. In California where I was based, it can be VERY expensive to terminate experienced professionals (usually persons 40+ years of age). Note in California if you haven’t gained experience in your profession by age 40, you usually switch careers and run for a political office.

Bottom line, so much expense paid to minimize salaries and benefits costs, the project time lost training outsourced labor, and the failed results due to inexperienced labor. Always amazed me.

The job market is strong if you take into account of the fact that the most successful companies around are the ones that find ways to suppress labor cost.

Read this interesting article from Bloomberg, and it doesn’t surprise me one bit.

https://www.bloomberg.com/news/features/2019-02-11/apple-black-site-gives-contractors-few-perks-little-security

The quest for corporate profit is universal, never mind whatever the CEO is saying about human rights or such. One should not be surprised of course that companies like Apple applies these practices regularly. Outsourcing of functions has happened in every industry, but Apple under Jobs (directed by Cook) was a pioneer in this field. Not so much the concept of outsourcing, but how to maximize its effects and locking in the contract manufacturer or service providers. Cook is a master at perfecting every little part of whatever non-creative process there is to maximize profits.

For example, Apple more or less perfected the idea of owning the manufacturing tooling while minimize the human expenses. Most of the critical manufacturing tooling for the iPhone in a place like Foxconn is paid for by Apple through front companies. (same is true for Amazon and others) While the CM deals with labor by ruthlessly suppressing costs. It is a frigging miracle, when it comes to profitability. Apple uses 3rd party (or shell) companies to purchase these tooling, writes off the equipment through depreciation. Financial engineering at its best.

So, after a fashion, the labor market is strong, but this does not correlate to good wages or anything like that. It’s just that there is demand for positions.

I wonder what the interest rate is on a subprime auto loan. If it’s 10% or more, a 5% delinquency doesn’t seem that bad. If it’s less than that, they are probably losing money.

They already took the profit when they extended the loan (points and fees) and then securitized the loan. So that profit and that cash is history. Now they get to take the loss. That’s why these finance companies collapse.

Subprime is very lucrative. But if you’ve been too aggressive lending and underwriting these loans, the tail end can get messy.

How much skin must the financiers keep on balance sheet these days or can they sell the whole bag of shit thru the Wall Street sausage machine to worldly ‘investors’?

It was something like 5%, in terms of the first loss, post-Financial Crisis (Dodd-Frank?). I’m working off memory here. But they changed that regulation last year to where this is no longer needed.

What?

How can that be? We are in a boom:

-The lowest Unemployment in history.

-The Longest bull stock market

-The lowest inflation in years

-The most salary gains in years

I mean people are so loaded that they install granite in the garages. Lake Tahoe = packed, Hawaii=packed, Disney wolrd = packed, Vegas= packed, Superbowl tix… no problem.

SO why people are not paying their car notes?

Some of thoses loans are 72 – 84 mo long. It must be hard to pay the note monthly after getting rent increases.

It would be nice to know the loan statistics for EV!

Could sudden battery failure be having any impact on loan default rates?

When it comes to residual values EV are a different kettle of fish!

EV boldly going where no car loans have ever gone before!

What’s different about this subprime auto loan era compared to the last one is now all subprime cars can be fitted with GPS tracking. Instead of recovery companies with tow trucks playing cat and mouse, searching for the asset at home or business addresses, for days on end, a single employee can Uber to each repo auto, and simply drive them back to the used car lot for resale to the next subprime victim, ahem, lucky buyer. Recovery costs are practically nil, and by the time the car is sold, and resold, and resold again, the profits add up. In this business model, you are hoping the buyer defaults within 6 months so you can get the car back on the lot for the next rube, ahem, valued customer.

Off topic, but Wolf did you see this? Does it mean you will be changing your views on the Fed soon? :

https://finance.yahoo.com/news/fed-finalize-plans-end-balance-sheet-runoff-coming-233201691–business.html

I read the entire speech. What she said was this: We are working on a plan, and we will announce the plan over the next few months, to let people know what we will do and let people know when it will end.

You guys need to READ this stuff — and not just the headlines.

There was NOTHING in her speech about when the Fed will actually end the QE unwind — but that they will ANNOUNCE THE PLAN in a few months.

Other than that, she repeated what I already said many times: that the QE unwind will never take the balance back to $900 billion. No one in his right mind ever thought that anyway.

What seems to be new is Daly’s statement that leads us to believe the FED will do QE before rates bottom at zero. That that not new?

“On Friday, San Francisco Fed President Mary Daly said policymakers were considering whether they to use bond purchases not just as a last resort in a financial crisis but perhaps even before the Fed has done as much as it can with rate cuts alone.”

Yeah, the Bank of Japan, which invented ZIRP and modern QE, has been using its balance sheet since 2016 for monetary policy. “Yield curve targeting” it calls this. It uses its balance sheet to manipulate the entire yield curve, particularly the long-dates yields. And why?

For the specific and announced purpose of steepening the yield curve and RAISING the 10-year yield above 0%. The BOJ was afraid of a negative 10-year yield and what this would do to the banks. This works, mostly, except until this year, when the 10-year yield dipped into the negative as long-term yields around the world have fallen. So the concept has been proven to work in raising long-term rates, more or less.

I wish the Fed would use its balance sheet to steepen the yield curve and raise long-term rates, like the bank of Japan does. All it would have to do is sell some long-dated securities. Maybe that’s what Daly was referring to, no?

I know the Fed would like a steeper yield curve, and the banks would like a steeper yield curve. So it would be logical for the Fed to use its balance sheet to try to target long-term yields in order to raise them, no?

What works in Japan won’t work in the US or in Europe.

Permanent easy central bank policy, even with “operation twist” type adjustments to the yield curve, results in massive wealth disparity which leads to unstable governments and populism.

Japan’s ultra tight immigration policy, combined with it’s unique culture, allow it to mute some of that populism.

However, when the powers that be tell a population that they can’t afford to pay them enough to raise kids so they’re going to have to ramp up immigration to replace them, they’ll get angry.

Also note that Japan has had plenty of recessions with a positive yield curve.

“You guys need to READ this stuff — and not just the headlines.”

For me, it’s to rely on Wolf to read this stuff and analyze it for me. Then it is, indeed, up to me to read the whole of his articles before commenting. (After that, my comments are profound.)

I do not understand why some people even discuss the possibility that the Fed balance sheet will go back to 2008 levels. That’s ridiculous.

Now unless Powell orders Simon Potter of the NY Fed’s SOMA ops to stop or ammend QT, it will go ahead with implementing the Normalization Policy that has been planned years ago. No mention of any order has hit the press!

On Feb 15, 43.523 Billion of Treasuries are maturing at the Fed.

On Feb 28, another 12.528 is maturing.

20.229 Billion of that has already been reinvested leaving about 5.823 still to be reinvested for Feb.

All we have to do is wait till after the 15th to see what the Fed actually did. That will tell it all. No rumors, just facts.

Typically people pay the rent and the car loan first (after food & phone). If you can’t cover your basic transportation, what does that say about ‘income’ security.

Wolf,

This data does not tell half the story. While the credit unions book appears ok now, it is a powder keg waiting for a spark. Credit unions have been paying dealers up to 2% origination fees for alt a paper. Problem is they were doing this for rock bottom rates. Pair non-earning loans with 400 to 500% of their balance sheets secured by autos with 100% plus ltv’s, and 60 month plus terms, and what do you get? The next banking industry crisis, when DQ’s spike and values plummet. Just like Community Banks took it on the chin in 08, The Credit Unions will be the ones holding the bag in the next crisis.

A loan with a low interest rate is much less likely to default than a loan with a 10% rate of 15% rate. Subprime customers are precisely the people who can least afford high interest rates. So the best way to keep your losses down is to extend these loans at rock-bottom rates. Maybe that’s why credit union default rates are so low :-]

Everyone pays dealers origination fees or spreads. F&I is the most profitable end of a dealership in part because of the spreads.

If credit unions hold loans to maturity then they don’t have to mark their books to market.

Credit rates can spike, but the computed asset values of the credit union remain the same, and they won’t have trouble borrowing & lending.

Remember that modern banking is heavily model driven even in a crisis – this is just how large banks function.

As a former banker, I could never figure out why any lender in their right mind would allow the negative balance owing on a trade in to be rolled into the new purchase. A person will no real down payment doesn’t deserve to get financing period. All purchases should require min 20% down so at least they are covering the initial depreciation. Lenders who roll negative balances into the new loan deserve to lose their ass and they will eventually or the investors who buy this “C” rated paper.

“A person (with) no real down payment doesn’t deserve to get financing period.”

That’s a bit too all-inclusive, IMO.

For example, borrowers with excellent credit ratings have taken advantage of auto manufacturers “Zero interest, No money down” offers precisely because their credit records predict reliable repayment.

“For loans to borrowers with credit scores (Above 119 the delinquency) rates were minuscule.” – Wolf

From what I can see the lenders get rewarded with incentives to push any and all loans. What I don’t see to counter the bad practices is a penalty for putting a person in these positions. I know a few people that have fallen for this “roll over” scam, the feeling of getting a new vehicle they didn’t think they could afford blinds them as buyers. That feeling fades when they see how long they are in debt for, then the payments stop when they find a cash option to replace the debt option.

Lenders make the loan based on the dealers point of sale agreement which never states that the old car is being paid off and financed in the new loan, only that its purchased as a trade in. The dealer can trade it in for whatever works for him. This is Auto Finance 101 since way back.

One reason NADA values are so high, gives everybody room to work it.

its done now, they are having harder times rolling it over….

the sales cycle is over, its the fixed ops cycle time to shine now

50% of category ‘auto finance’ is subprime? I assume these are the manufacturer’s financing deals? It sounds awfully high.

I just bought a Prius Prime. Last year’s model, and there seem to be a good number of those still standing in dealership lots in the Northeast. The incentives are extremely strong, especially when paying cash. My guess is that this is not the only brand with sales problems and car manufactures are in the process of lowering lending standards keep their lots from overflowing. That strategy will only works so long.

“50% of category ‘auto finance’ is subprime? I assume these are the manufacturer’s financing deals?”

No. Please read the article for details and context. You just looked at the chart and misunderstood the abbreviated label. “Auto finance” is the abbreviated term in the chart for a sector of non-bank lenders that specialize in auto loans, and 50% of their loan book is subprime — by far the highest among the sectors.

At the end of the day it’s all about keeping the residual values inflated.

Just goes to show that the metrics that economists/politicians use to define a ‘strong economy’ (ie lots of low-paid, insecure low-skill jobs and a mountainous pile of debt, plus a stockmarket predicated on rampant speculation – gambling, effectively, often done automatically by machine algorithm) doesn’t tally with the reality of the situation a society faces in any way, manner or form.

The difference between the financial economy, and the economy which actually affects peoples’ lives.

Not the same thing at all.

=>“A development that is surprising during a strong economy and labor market”

You know you’re in trouble when you can tell the Fed is lying to you.

In fedspeak, as in newspeak, or doublethink, or gaslighting, or propaganda, words do not have their conventional meanings.

When they say the labor market is ‘strong’, do they mean it is secure and well-paid? Of course not. That would be absurd. What they mean is that it is profitable.

When they say the economy is ‘strong’, do they mean it is sustainably and fairly delivering prosperity to all? Of course not. That would be absurd. What they mean is that it is profitable.

Profitability is the only goal. There are no other considerations. The Fed’s one and only purpose is to manage the messes created by its member banks so as to maximize profitability, and when that happens conditions are ‘strong’, which is to say, profitable.

The corrected Fed statement is:

Also absurd, since it should come as no surprise to anyone, much less the Fed, that the economy and labor market would be profitable, insofar as their member banks have every sector loaded up with optimally profitable, unsustainable debt.

And it should come as no surprise to anyone, much less the Fed, that this lofty mountain of debt is becoming unserviceable. Hence the increasing defaults, soon to become a torrent, in every sector. Not that they’re going to tell you that. Their job is to manage the messes, and this is one way they do it.

Happy gaslighting, everybody. Try not to be a sucker for every obvious lie they throw at you.

Why is your chart showing auto loan delinquency very different than Calculated Risks’ data from the New York Fed?

https://2.bp.blogspot.com/-4C6L4SPxcZQ/XGMDwp4yPoI/AAAAAAAAxNo/YWtbPiOS3JMJdgvJWmcjzJ3OyYJOoc5CACLcBGAs/s1600/NYFedQ4Delinquency2019.PNG

Ataraxia,

Because the chart you linked shows something entirely different, namely TOTAL household delinquencies, including mortgages, HELOCs, credit cards, auto loans, etc. by delinquency status. This is the summary chart from the NY Fed’s website. You should have seen this because the title of the chart says, “TOTAL BALANCE BY DELINQUENCY STATUS”

It’s on page 11 of the NY Fed’s report.

https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/hhdc_2018q4.pdf

Thanks for the clarification. I thought the CR chart was auto’s only (but total). I suspected I was missing something.

It’s hard to have sympathy for subprime borrowers when the average new car price is $40k. Many of these people likely aren’t stressed economically, but are impulsive and short-sighted.

Of course, there may be some valid defaults within the group due to true economic hardship.

OTOH, if Americans ever started living within their means, the US economy would collapse. For now it is all debt and misleading statistics, debt is still increasing faster than GDP, and the Financial Industrial Complex is sucking wealth out of the real economy like there’s no tomorrow.

There is a reason these people are subprime, their credit history shows a lack of responsibility when it comes to their personal finances. They tend to live beyond their means and to not pay their bills.

If the people writing the loans had to service them, there would be much less of a subprime problem. Instead much of this subprime debt is sold off and ends up ruining people’s pensions and retirements.

we call them credit criminals…..

once was witness to a secondary lender buying a double BK player because loan volume from the dealer client was so high…..

I got fired for TDing the customer and dealer down…..Foothill Nissan, kinkier than kink dealer

\\\

Usually the government and financial institutions don’t care about crises. This time they do, and they are trying to delay the crash, which makes me worried. Bottom line…they are the winners. But why and what are they afraid of this time?

\\\

=>But why and what are they afraid of this time?

They’re concerned that the federal deficit is hitting record highs, along with record highs in consumer and business debt, even though the economy is supposed to be doing well, so that when the economy turns down in the near future those debts will skyrocket and become unmanageable, resulting in a severe depression instead of the long-expected recession, with attendant nationwide social unrest.

Bankers and billionaires will be just fine. That’s the important thing.

Is the “Uber” effect “Lyfting” the deliquency rate as drivers realize they can’t make a decent living as an unregulated cabbie? Would be interesting to find out.

yes, the Uber program to sell cars to new uber drivers blew up as they lost 6.2K per unit….I told them in interview that it was going to blow, weekly leasing made the payments seem good but in reality it was worse than a monthly lease…..they had setup dealer office sites to push the agenda of drive for free and earn money….

fail…..

as an ABS buyer in the past….this is the only formula that works

LTV + Credit quality + Down Payment = Yield….

the problem was risk was mis-priced and yield couldn’t compensate for the credit quality

“I’ll tell you kids, I’d rather walk”!

Liam Gallagher

I am in the market for a new SUV. I prefer buying used but the car manufacturer aka Kia in this case is giving me $4k off MSRP and $4K off again by dealer which is basically almost 20% off msrp.

I gentle used car would sell for the same amount and with less warranty and 2 year old.

At this price, I’d rather buy brand new than a gentle used car although I prefer buying used…

be careful, their engines are blowing up everywhere..

I know a dealer who rented a lot to store units needing engine replacement that is taking 14-28 days to get. The surrounding dealers were turning customers away, he rented the lot, provided rental cars and is getting up to 22K for the repair and rental charges from OEM….printing money he is…

Easy credit always causes irresponsibility. We see it in the auto market with people who are upside down on their loans being able to roll their debt into the loan on new car, which simply magnifies their problem.

We see it in financed corporate stock repurchases in which debt is incurred but no new revenue is really created.

As I see it, the bond market has become a series of dominoes ready to topple. Auto loan delinquency is approaching 2009 levels, Student loan delinquency is over 10%, and rating agencies are saying that junk bonds are in danger territory.

Business Insider is reporting higher default rates, but more importantly – the loans are at least 50% higher in gross dollars than the last recession. And as WR mentioned…if this is with our “strong labor market”, things look to be going the wrong direction. Time to dust off that old saying we used to hear in the Great Recession – we are pushing on a string. Diminishing returns. Few understand how interesting things really are.

A bit of a minimalist, don’t mean to rub it in but, I still drive the 1987 Toyota pickup, bought used in 1990. 323,000 miles now, the maintenance or repair in any given year have never been more than a single monthly payment on a new car. I don’t however seem as cool as someone driving a leased beemer. I did do the math and figured I’m about $130,000 ahead of where I’d be making payments for the last 29 years (much more if invested). It’s interesting to read about choices the “normies” are making.