Consumers are doing their job only in a lackadaisical manner. But the student-loan scheme is hot.

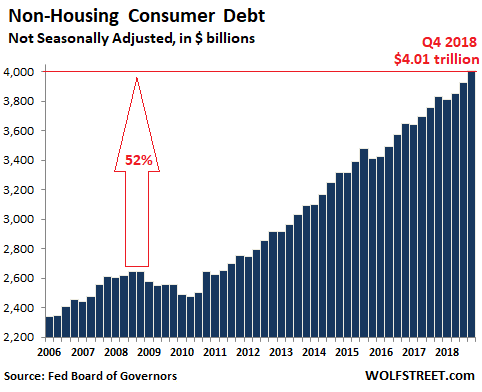

It’s a tough job, but someone’s got to do it: Propping up the massive US economy. And consumers are doing it, but in a somewhat lackadaisical manner when it comes to spending money they don’t have. Consumer debt – more enticingly, “consumer credit” similar to “extra credit” – rose 4.7% in the fourth quarter 2018 compared to the fourth quarter last year. In the year 2018, Americans added $179 billion to their balances on their credit cards, auto loans, and student loans. Every dime was spent and added to GDP. It amounted to nearly 1% of GDP. If GDP grew 3.1% in 2018, just under one third of the growth was generated by that additional consumer debt.

Without this additional consumer borrowing, if consumers had just maintained their debt levels, GDP growth might only have been 2.2% in 2018, instead of 3.1%. So, a huge round of applause is due our debt slaves that now owe over $4 trillion for the first time ever, according to the Federal Reserve Thursday afternoon:

Consumer debt includes auto loans, student loans, credit-card debt, and personal loans, but it excludes housing related debt, such as mortgages and HELOCs.

The $4.01 trillion in consumer debt is up 52% from the peak early in the Financial Crisis in Q3 2008. This is not adjusted for inflation. Over the same period, the Consumer Price Index rose 16% and nominal GDP rose 39%. Thus, Americans are sticking to their time-honored plan of out-borrowing both inflation (by a big margin) and economic growth.

Over the past 12 months, consumer debt rose by 4.7% while nominal GDP likely rose just over 5% (due to the government shutdown, Q4 GDP data has not been released yet, so I’m guessing). But nominal GDP outgrowing consumer credit growth is a rare phenomenon. The last time it occurred, and the only time since the Great Recession, was from Q1 through Q3 2015.

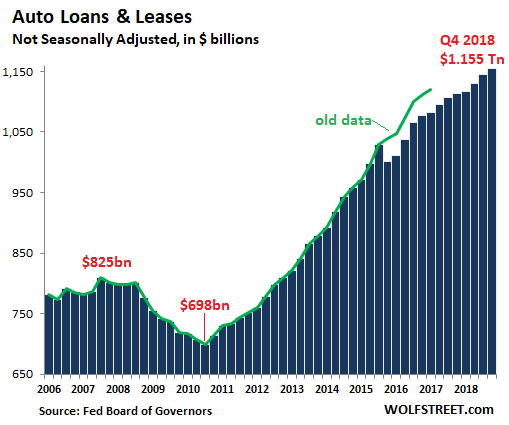

Auto loans and leases

Total auto loans and leases outstanding for new and used vehicles in Q4 jumped by $41 billion from a year ago, or by 3.7%, to a record of $1.155 trillion, despite stagnant vehicle sales. The increase was due to rising prices of vehicles, the rising average loan-to-value ratio, and the lengthening average duration of loans:

On a technical note, the green line in the chart above represents the old data before the large adjustment to consumer credit in September 2017. Every five years, consumer credit data is adjusted, based on new Census survey data. This time, it hit auto loans hard. I included the green line to show that in Q3 2015 it wasn’t a collapse of the car business that caused the precipitous drop in auto loans.

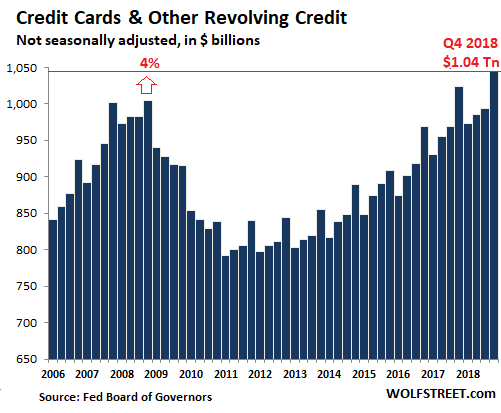

Revolving credit

Credit card debt and other revolving credit, such as personal lines of credit, in Q4 rose 2.0% year-over-year to $1.045 trillion (not seasonally adjusted). Given that nominal GDP rose around 5% over the same period, consumers clearly fell short of the job they’re expected to do. Their job is to charge up their credit cards to the max. But they’re stubbornly refusing to do it. Credit card balances in Q4 2018 were only 4% higher than Q4 2008! What are these consumers thinking?!

Baffled economists are scratching their heads, and banks are desperate. Credit card debt is the most profitable activity for banks, with usurious spreads between the rates charged on credit card balances that can go well beyond 20%, and the banks’ cost of funds, which in December was on average 1.06%, according to the San Francisco Fed’s Cost of Funds Index.

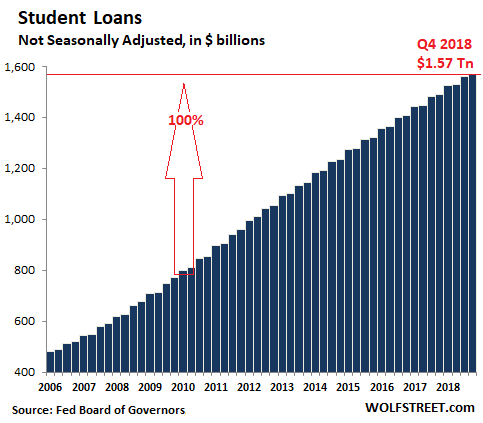

The student-loan economy

Student loans jumped by 5.3% year-over-year in Q4, or by $80 billion, to a new record of $1.57 trillion (not seasonally adjusted), having doubled since the beginning of 2010, even as higher-education enrollment declined 7% from 2010 through 2016, according to the latest data from the National Center for Education Statistics. Fewer students, but they each borrow more, to fatten entire industries from Apple and concert-ticket sellers to investors in the hot category of commercial real estate called student housing. They’re all feeding at the big trough of government-guaranteed student debt:

What is systemically wrong with the student loan scheme is that it’s a three-party deal — universities, government, and students – but without any kind of discipline imposed on them by the market or the government. It just ratchets higher quarter after quarter at a ludicrous rate, even as enrollment is declining.

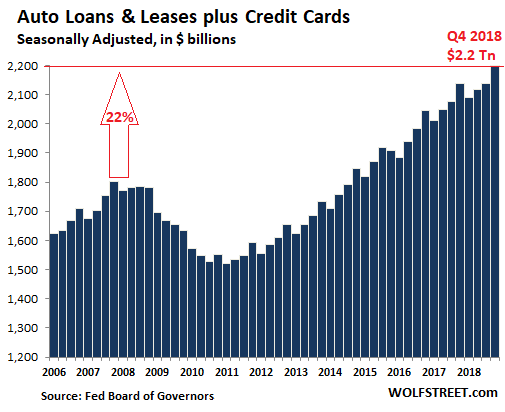

Just to see what consumer debt would look like without the student-loan scheme, here are auto loans and credit card loans combined – and it shows how lackadaisical consumers are in doing their job by borrowing money they don’t have, with the total having increased by 2.9% year-over-year. Since the peak in 2008, the total has risen 22%, while the Consumer Price Index has risen 16% and the US population 7%:

Averages hide where the difficulties are – and they’re always at the margin where people are struggling to make ends meet. Many of these folks have sub-prime rated credit, but there are also plenty of folks with high incomes and excellent credit scores, but who spend too much and borrow too much, and they’re living from paycheck to paycheck. Any shift in the labor market that would cause them to lose their jobs could push them into default in no time. And the averages don’t show the risks buried at the margins.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

From “In God We Trust” to “In Debt We Love”

I think that the current supreme court will declare any wealth tax unconstitutional. However, I do believe that an imputed income tax (a variation of the wealth tax recommended by some Democratic politicians, which would impute some income to wealth, to avoid tax-avoidance schemes, like share purchases and no dividend issuance) would be very beneficial and eliminate the enormous unfairness of our current system.

Our working class is being squeezed between low-interest rate savings accounts and low return pension plans on one hand and high-interest credit cards and hidden inflation on the other. Their incomes have decreased in real terms. The rich, on the other hand, do not have to pay taxes if they chose not to do so: too many schemes exist for them to avoid paying taxes to enumerate here.

An imputed income tax is the only way that the U.S. government may meet at least a percentage of its enormous liabilities: over $100 trillion per Forbes. It may forestall a violent revolution once the effects of the massive corruption of our government since 1992 become widely known.

I have been wondering about the “wealth tax”, and “billionaire’s tax” proposals; and mike’s comment above, that this would be an “imputed income tax”, makes sense. Makes sense in legislative terms, that is. A true “wealth tax” would really require regular walkthrough of the affluents’ holdings, which goes against constitutional guarantees of the right to be “secure in property”. (Oh, but wait, did we not already blow off that right, in order to empower the War on Drugs ?)

The desire to see the ultra-wealthy pay their righteous share is widely held. Somehow many of those who preach it are among the wealthiest (looking at you, Mr. Buffett), which makes me wonder.

Any kind of real “wealth tax”, IMHO, must require absolute inventories of all taxpayers’ wealth. And yes, at some point, you and I, Blakeslee, are paying “imputed income tax” on our backyard garden plots. That’s right, I’m saying that they will come for me, after they have come for the millionaires (they started by saying, “billionaires”, but now I hear “millionaires” in the sound bites).

I am currently middle class, and yes, I am sure that we are in their long-term plan for the payment of “imputed income tax”.

Povery and income inequality are problems. Let’s fix them. I strongly believe that longterm we do this best by using policies that maintain the basic rights guaranteed by the U.S. constitution.

Would love to see some good new ideas…..Wolf ? …anyone ?

What can the average middle class person do to help turn the tide ?

All those Yellen bucks had to go somewhere…

Before they die.

As a debt slave, I get that I should rush out and borrow money to buy a “rock” that I don’t need nor want. That part is pretty straight forward.

However, maybe you can help me here, I am confused as to whether I should throw this borrowed “rock” that I really don’t own through; 1) a bank window, 2) a car window, or 3) a university window, to achieve the maximum GNP impact?

The biggest most expensive gold-rimmed diamond-encrusted window you can find.

Sounds like we need more riots.

Sounds like you need to live within your means.

That may be coming…

rx

Someone (don’t remember who) said you can always tell those industries who are in bubbles. They build palaces.

Car window, then Uni Admin window (bigplateglass), then the Bankster’s Taj Mahal-of-mirrors .. all lined up, one behind the other in a straight line, then, hefting your homemade atlatl, propel that shiny sparkle pony through all three, with the least amount of effort !

…. rhetorically speaking, of course .. ‘;]

Throw it through a politicians window and he will dine out indefinitely.

Best comment I’ve read on here.

How to rebuild a country stone by stone.

By WES.

Debt slave edition is now available in hardback due to popular demand.

I’m tempted to borrow x amount of fiat and then converting it into gold. Wait a while and then buy many rocks to throw.

McLuhan said we should pay students to go to school. I wonder if giving them huge loans they will never pay back is the same thing?

Ambrose: Obama, AOC, and Bernie all seem to think so!

After all the federal government never pays back it’s loans!

Wolf,

You don’t actually believe the GDP or CPI numbers, do you?

“Credit card balances in Q4 2018 were only 4% higher than Q4 2008! What are these consumers thinking?! Baffled (dumbshit) economists are scratching their heads……”

Some very obvious reasons. More people are dealing in cash. More people have less money than 2008 to spend (credit cards or otherwise). More people have realized what a losing proposition credit cards are; only being used in emergencies.

“You don’t actually believe the GDP or CPI numbers, do you?”

Believe is something you do in church.

Wolf,

Great reply. You are a man after my old engineer’s heart! As a millennial would say: LMAO.

Demand for Credit Card Loans

From the WSJ “The Daily Shot”. February 05, 2019

Net percentage of domestic banks reporting stronger demand for credit card loans, has fallen to a multi year low of negative -18%.

Consumers are either tapped out, or are fearful of future economic conditions, or both!

Both, and maybe a little smarter? We can hope.

Speaking of which, the Daily Shot is frequently posting graphics from Wolf Street these days.

I’ve noticed since the middle of last year that I’ve gotten a lot less offers for 0% interest for 15 month type credit cards.

It was crazy for awhile in 2017 and early 2018 all the mailer with offers for crazy intro rates. Now it’s almost none.

I get such offers from Discover at least once every couple months. Capital One a couple times a year. My credit is good but not perfect (only in scoring terms: few accounts in history, no debt, no missed payments, no collections, etc). The thing about credit that really pisses me off is you have to continually drink from the proverbial trough in order to be able to get a drink at some point in the future. Sigh.

I put a block on my credit and think that helped a lot as I basically only get the airline cards now. One thing I don’t like is when the CC company raises your limit without asking you. If I wanted more credit, I’d ask for it. Takes a phone call to have them fix it.

to Outlookingin,

…or people are getting tired of big corporations insinuating themselves into their lives and causing trouble.

The Fly Away LAX bus station in Van Nuys will not accept cash. After a cross country flight and almost home, you are *commanded* to insert a credit card. No cash allowed. Someone loses a job. A Big Bank sucks another 3% from our community.

When buying phones for my family, I am surprised to learn my citi credit card has been locked. No reason given. I hand over $400 cash to get the phones.

I receive a letter from Citi saying “my” account has had suspicious activity” and I should call this number. It is in the Philippines and the representative is demanding I give him my personal information (which seems ironic), does not speak understandable english, refuses to let me speak to a more knowledgeable person or manager. He will not tell me why my card is locked until I “comply with his demands”. A few questions to verify identity I would understand. After all, this is not a transaction.

My wife uses her Wells Fargo credit card to pay for medical care for her dying elder brother. We get a home visit from the County “senior services” who has sent a totally uninformed person to our house to gather information on why she did this. Wells Fargo has reported her for possible elder abuse.

Do we really want the banks to control our lives in this way? Pay cash when practical. Stop sending 3% of your purchase to these bloodsucking vampires.

Another tidbit :

Median weekly US earnings grew from $728 in Q4 2008 to $900 in Q4 2018 as per BLS.

So the above C.A.G.R over 10 years is 2.14%, and in line with the 2.2% 2018 GDP growth (Excluding consumer debt) you cited above.

2% to 3% average nominal growth may be close to the actual US GDP growth trend over the last decade.

I remember Jeremy Grantham forecasting slower longer term US GDP growth as far back as 2009 and 2010.

However, he was way off the mark in a lot of his 7 year asset class forecasts.

I wonder who has credibility when it comes to forecasting. Nobody ?

It is supposed to snow here in Seattle in a couple of hours.

The American consumer is not so dumb after all. It’s wise to borrow as much as you can when the currency has a much higher value today then it will have in the future.

Borrow wealth today and pay back less wealth in the future through the magic of currency debasement. The Fed is serving free lunches and you are invited to sit at the table.

Is carrying $50,000 in debt really a bad thing if the Fed debases the currency such that minimum wage eventually exceeds $500,000/year. I don’t have a crystal ball but I can 100% guarantee that minimum wage will exceed $500,000/year in the future, so what’s the big deal with $4 trillion spread out among so many – it will amount to nothing after official policy of debasement works it’s magic. A trillion is just a number after all – just an arbitrary number – the number system goes to infinity so don’t obsess over 4 trillion.

The Fed have stated, as official policy, they will relentlessly debase the currency. I would take them at their word, if the Fed has proven skilled at anything it would be the destruction of currency value. They say they are going to do it – they will do it.

Borrow and spend as much as you can, pay back later in confetti currency. Consumers and the government are wise to continue to borrow immense sums of currency.

The debt game you play has logic.

The only unknown is timing.

And because we are not members of the connected ruling class…we will be hounded to oblivion for the debt we owe if our timing is off by just a hair.

So better not to play that game.

Minimum wage in excess of $500,000?

Okay.

This would mean that the currency is worthless.

So, a loaf of bread would possibly be as high as $25,000

How far would your half mil go? Not far.

Be careful what you wish for. It could very well come to pass.

VanDownByTheRiver, those who played like you described will end up getting what they “deserve”, NOT what they “want”.

Those who think they can “transfer” wealth from other people will most likely get their wealth/feeedom transferred out. Why? The no.1 rule for wealth transfer game is that only one guy leave the table winning while everybody else get wiped out. Many thinks they can be THE ONE, but they will get what they deserve.

I know quite a few millionaires from SoCal beach homes that were mortgaged to the hilt on purchase. When you talk to the owners, they will share their biggest financial mistake:

They should have borrowed more and bought a more expensive beach house when they were younger. They always talk about the house they could have bought with more debt then kick themselves.

Of course, their are always the few who get unlucky and max out on the mortgage debt just before an economic their job. They are the road kill. Just good old survival of the fittest.

So, all the folks who lost their homes in 2009 are road kills and your SoCal millionaires are the ones that survived. Wealth transfer is done. Kudo to the millionaires! Amen! But you know what, here in silicon valley, anybody who have a W2 job is a millionair, double income working for Google gets you 500K household income buying 3 million $ homes. Let’s forget about these millionaires, let’s talk billionaires! The 0.00001%, who receives way more FED printed money that millionaires or W2 workers. Kudos to them! Wealth transfer done right! Here is the thing, remember occupy wall street? Remember the yellow vest? The mass school shootings. The hatred that is going on within this country.

Rent seeking makes people rich and rent seeking is the common dynamic of civilizations before it fails from within or without.

Yes, road kills hates the survivors, and survivors better pay attention to them because road kills ain’t dead yet and they will do things. Then let’s talk about survival of the fittest.

The formula for success on SoCal beach homes was this: Pick a time when RE wasn’t at a huge peak. It didn’t have to be a trough, but it’s better if you pick a time it’s not crazy high. Buy your house, mortgaged to the hilt, of course. As much house as you can buy.

Now, and this is extremely important: Furnish that fucker with milk crates, furniture found in alleys, etc. Did it come with ugly 1970s avocado shag? All the better – learn to love that shag and the dog smells it came with.

Do not spend a penny on the place you don’t have to until you’ve got that mortgage paid ‘way down or all paid off. Then furnish it, upgrade it, etc with money out of your pocket or a very small refi.

The name of the game is to hang in there and keep that mortgage paid, even if you have to moonlight working at a gas station, anything. It’s a matter of just hanging in there for X amount of time.

There are many strategy to play this game, but the point is this. If the “game” is what VanDownByTiver calls it, person A taking on debt, FED showers money, person B takes bigger debt to pay person A, then the outcome of this game is widening wealth inequality. Losers hate winners. Majority will be losers as in all wealth transfer games as the widening inequality testifies. If the game is a wealth creation game, the losers respect the winners, and they will try to compete better and wealth inequality shrinks, more people are happy. I do NOT hate the players regardless of their strategy, I hate this game that FED creates and it brings out the worst of all players. NOT the best.

van_down_by_river,

The burden of variable-rate debt, such as credit card debt, cannot be lightened by currency debasement because interest rates on this debt are variable, and rise when inflation goes higher.

A fixed-rate 30-year mortgage, however, is a good hedge against inflation. But mortgage-related debts are not part of this type of consumer debt.

A fixed-rate car loan can also be a good deal, if you get a low subsidized rate.

What is your contingency plan if instead of inflation you see a deflationary collapse, where currency becomes scarce and your debt is impossible to service? But go ahead and trust the Fed; they would never mislead us. I sleep well at night knowing I don’t owe anyone a dime.

The bankers know this game…their solution is simple: Re-monitization. All your cash & bank account balances will be replaced with “new money” at something like a 1000-1 ratio, but those debts will carry over unchanged.

The only way to win the debt game is not to play.

The bankers represent the wealthy. The wealthy do not want their money devalued away by monitization. Deflation will and is slowly gaining momentum. The debt slaves will be punished.

Thanks for saying it, Edwin. I dont understand why people think the guys who have all their wealth inflated away. HyperInflation crushes housing and stocks. Deflation, however, makes assets cheaper and allows the wealthy and connected to accrue more wealth at deep discount prices and only the proles get harmed. What’s not to love?

Every penny spent as debt, is a penny which cannot be spent when it is actually earned in the future. This is the simple fact that eventually causes the recession that follows every debt based economic bubble.

Add to that someone’s debt is someone else’s asset.

An asset that can be used for collateral or as cash flow to run current operations

Default wipes out that asset.

And the dominos tumble.

Jdog

I guess so. I’ve never thought of it in such simple terms.

The student loan debt debacle is just another reason to question whether the U.S. truly has a capitalist economy. As you point out “Fewer students, but they each borrow more, to fatten entire industries…” many of which aren’t really related to getting an education. I wonder if a more helpful approach for the students would be for the student loan payments to go directly to the colleges/universities for tuition and a dorm room. Then let the students come up with the cost of books, meals, and incidentals. It wouldn’t hurt them to “have a little skin in the game”. Wouldn’t solve the problem of the rapacious educational institutions but it might help.

Unlikely to happen since it is those extraneous industries you mention “… Apple and concert-ticket sellers to investors in the hot category of commercial real estate called student housing.” that pay kickbacks to the legislators that approve the programs.

Make student loan debt dischargable in bankruptcy and get the federal government out of the business of “guaranteeing” these loans.

Skin in the game from the University.

2banana,

That is a good suggestion. As with the medical insurance fiasco there is no way to control costs. The suppliers just keep raising them and consumers don’t care since “someone else” is paying.

“consumers don’t care since “someone else” is paying.”

I’m sorry, but that is just not true. $6,000-$12,000 ANNUAL deductibles are most certainly skin in the game.

Ironically the only player without any skin in the student loan game is the is the one that benefits the most.

Feature, not Bug.

Why would the “powers that be” want to do that? Debt is the instrument by which the masters keep control of the debt slaves.

It is as Orwell said, the boot stomping on the face of humanity.

When you owe $1000 the bank is in charge when you owe a million your in charge.

No

I think you need to be owing at least £50 million to get in control.

Wolf, I get a different number for CPI over the 10 years: 19%, not 16%.

Using Nov. 2018 CPI-U figures:

(252.038-212.425)/212.425 = 19%

Looks like ex-student loans there has been little real growth in consumer debt.

In the past decade it’s been all about student, corporate and govt. debt.

Max Power,

The difference is because we’re looking at two slightly different data (seasonally adjusted v. not seasonally adjusted), and at two slightly different time periods: you start in Nov, I start in Oct. This is important because CPI dropped during the early parts of the Financial Crisis, starting in Aug 2008, which lowers the starting point.

The time period in the article starts from the peak in consumer credit in Q3 2008. So if you start counting in Nov (middle of Q4 not Q3), your starting point is lower, due to deflation at the time. But the prior peak in consumer credit was Q2 and Q3 2008. So I chose October as my starting point for CPI counting.

Monthly not-seasonally adjusted CPI was 216.5 in Oct 2008 (stand-in for Q3 2008 as the peak of consumer credit); In Dec 2018 it was 251.2 = 15.97% increase.

If I had used Sep 2008 CPI (218.8) as stand-in for Q3, the increase would have been 14.8% because CPI dropped for several quarters after that (deflation).

The other difference is that you seem to use seasonally adjusted CPI and I used “not seasonally adjusted” CPI. All data in the article is “not seasonally adjusted.” I like NSA better in long-term discussions because seasonality is apparent in the charts, and you can see it, and also because once you adjust data for seasonality, you change the data (however, I make some exceptions to this preference, such as retail sales which are so brutally seasonal that it creates so much noise it’s hard to see anything else).

I’m OK either way. CPI data isn’t that accurate anyway :-]

I’m guessing the top 10% of income earners doesn’t have consumer debt worth mentioning, so the $4T consumer debt likely relates to the middle and lower classes. If a recession hits and layoffs occur, I think you can kiss the repayment plans Goodbye.

Maybe that’s why the Fed isn’t hiking interest rates. Lots of bad things can happen if the economy goes into recession or slows down considerably. Loans won’t be repaid. Mortgages might not be repaid. Layoffs may occur. Hirings will freeze. Spending plummets. People get angry.

With debt levels this high, ordinary recessions become huge deals.

Bobber: In a credit/debt system, it is system critical that the total debt keep on growing!

It shouldn’t really be called a “system” if its unsustainable. The word “Ponzi” is a better description. If you are a buyer of stocks and bonds, you are a player.

Over the past 10 years, the debt has been growing, and the interest rate has been dropping, so the debt problem has been expanding in more ways than one.

At this point, it’s hard to take on more debt, and it’s hard to reduce the interest rate. No good choices left. The only plausible outcomes are 1) recession, default & deflation 2) massive wealth redistribution through tax policy, or 3) hyperinflationary bust followed by 1 & 2.

Welcome to the House of Pain.

Bobber: Actually there is a fourth alternative!

Lower interest rates!

Better yet NIRP! Where people are paid to borrow! Happened in Europe!

Bobber,

Remember a lot of the credit card debt will never be repaid. People will make payments till they die leaving the balance. As Wolf points out the difference in the cost of the money to the banks and that charged is incredibly high. So high they can write off the uncollected. After all the game is all about cash flow.

But I agree with you about interest rates. I’ve upset Wolf for over a year by repeating like a parrot that the FED would not raise rates by a “meaningful” amount. As you note, the results of significant interest rate increases would threaten the system. I don’t know what happens next, but as an engineer I know nothing grows exponentially for long without dire consequences.

WES: Better yet NIRP! Where people are paid to borrow!

That has been available in rolls at supermarkets for a long time. Fortunately digitalisation means that the world’s forests don’t need to be cut down for that soft experience, which also helps escape associated resource limits. Unfortunately digital currency as a form of virtual hygiene is not good enough in real world use.

Think twice before ever handling someone else’s smartphone, Bobber knows exactly the kind of house he is talking about.

Typo alert:

Baffled economists are scratching their heads, and banks a desperate

Should this be “are”

“Are” you “crazy”.

Such a trivial typo, not even worth mentioning.

I’m assuming you never had a mean nun as a teacher and it shows.

Thanks!

Wolf: I wonder if its possible to break out Student Debt and the Universities that play the biggest roles in saddling their students with it. At a certain point (probably when the MBS reduction is complete) the FED will be tasked with putting some(?) of this Student Loan debt on the balance sheet. Scary thought right?

Before that happens, who are the prime offenders that will claim they’re too big to fail? Whose sprawl into the urban infrastructure is so complete that bankruptcy would be tantamount to allowing the municipality to fail?

I think HELOCS should be included with debt numbers as a great deal of them are used to buy toys as opposed to renos, or even using them to pay down other debts.

I still stand by my past statements about debt. It can be a good thing if it is used in a wise way, like a reasonable house purchase, growing a business, whatever. But as one ages debt is not good. In Canada, (anyway), because CPP is about 1/2 of what the average SS recipient collects in the US, if you don’t have your place of residence fully paid for by retirement, you can’t retire. It’s straight forward grade 4 math.

Paulo,

HELOCs are secured by the home and thus count as housing-related debt. They’re not “consumer debt,” which is unsecured.

Also HELOCs are huge in Canada, but have faded away in the US. Americans took such a beating on them, and lost their homes because of them during the housing bust, that HELOCs have completely fallen out of favor, though banks are marketing them with all their might.

I wrote about this comparison on Sep 20, 2018…

https://wolfstreet.com/2018/09/20/heloc-balances-u-s-canada-house-price-bubble-risks-housing-bust/

By the time I wrote the article, HELOC balances in the US had fallen from $609 billion at the peak in June 2009, to $357 billion. And in the 4.5 months since I wrote the article, HELOC balances in the US have fallen another $9 billion to $348 billion.

Paulo….. The average Canadian household net worth is DOUBLE that of American networth (its a little scewed at the moment due to currency fluctuations). Canadians are not loaded with medical debt… plus we canuck have better funded schools and benefits (fully paid maternity leave ect…). Canada is a sane county that invests in its citizens.

Nicko, I find your statement interesting as I split my time between both countries. I can live for half the price in the US as long as I stay relatively healthy (US insurance is only 10 grand for the two of us as the kids are grown). So when you say Canucks are worth twice as much it doesn’t mean anything when it comes to cost of living. I prefer the US side of the border myself. It is humourous to listen to the brainwashed CBCians talk about people dying in the streets and people shooting it out with six guns down in the US.

Well, I don’t live in Canada (or the US), my millenial sister lives in Alberta. Her daughter is just starting kinder garden (free for half the day, state of the art government school), plus half a day paid daycare (~$900 a month). Ofcourse, my sister received a full year paid maternity leave (she has a well paying government job). Husband is an executive. Suffice to say, quality of life factors are very good. As oil prices rebound the economy will continue to improve. No brainwashing, Canadians get a lot of perks, quality healthcare and education, low crime… plus a more equitable society.

Yerfej,

Your response exemplifies a problem that exists in the United States. There is huge *variability* among people’s individual experiences. So, for example, in your case, the following is likely:

1. Since your kids are grown, you could be old enough to receive Medicare, which is an affordable system. (Or if you’re partly living in Canada, you may get affordable services there.)

2. The phrase “as long as I stay relatively healthy” suggests that you can completely control this. Yes, you can mitigate health problems with healthy living, but you can also get unlucky (e.g. genetic factors, car accidents, etc.) If you make it through intact, you’ll think you were right. If you get unlucky, you’ll likely have big regrets.

3. Since your kids are grown, you don’t have to face astronomical education costs. Your kids may have been educated at a time when states were subsidizing education.

4. You possibly purchased a house when they were much more affordable. You probably did the right thing and have it paid off, so your overall costs are a pittance.

It’s been said that in America, the “luxuries are cheap, and the essentials are expensive”.

A young family starting off is probably better off in Canada than the United States. Maybe the upside is not as great in Canada, but there is more assurance of getting into and remaining in the middle class.

For Rose N and other commentors re: US/Canada, (I’ll be brief and no propaganda).

Here’s the personal scoop about CDN medical. In our house we don’t go to the doctor unless we absolutely have to because both of us dislike going. However, we have never once even thought that it might cost something if we had to go. Bus fare to the clinic would be more, or in our case the gas to drive to town.

Yes there is violence and crime in Canada. We have gangs; bikers, native gangs, asian gangs, money laundering, fentanyl nightmares, etc…just like the US. But except for shootings of bangers on bangers, for the most part we never have to worry much about violence. We don’t lock our doors. I don’t ever think about a road rager with a handgun or automatic weapon. I don’t worry about being stopped by RCMP, either.

from Global: “You’re more likely to be shot to death in the United States than you are to die in a car accident in Canada”….and: “Overall, Americans are almost 70 per cent more likely to die at the end of a gun — shot by someone else, by themselves, by accident — than Canadians are to die in a car accident.

Thirty-five per cent more likely to be shot to death than Canadians are to die of a fall.”

In summary, here are the main differences:

*medical coverage, costs and availability + better outcomes for 2/3 cost per GDP (no cost to user)

*gun violence and violent death rates

*educational opportunities are leveled due to Provincial funding systems. (There aren’t rich curriculums vrs poor school (counties) curriculums)

* religion…I have no clue what religion any of our politicians practice, if any. We follow politics closely and religion is never an issue in politics or law (except hijabs in Quebec).

*Pot is legal..which I am against, but…..

* Hockey is a big deal for many. :-)

* Elections publicly funded and donations by Unions, Corporations, and Individuals limited. Public subsidy of election costs per vote and by tax credits. (No Citizen United nonsense or super PACs)

There are benefits to living on either side of the border, but as someone born in the US I can truthfully say I would never return and may not even visit ever again. We used to go to the Oregon beaches every spring, but I’m not sure if that is even an option these days. One thing is for sure, if we do return we always have and always will purchase suppemental medical coverage through BCAA…just in case. :-)

I have always found US citizens to be friendly, outgoing, hospitable, and generous to a fault. Always. However, it is painful to watch the divisiveness unfold on a daily basis because the wealth generating/distribution system pits people against people making winners and losers out of everyday living.

regards

I am baffled that with the FED no longer adding liquidity but actually removing it with their unwinding that interest rates haven’t gone up much and the stock market hasn’t really gone down. Wolf did predict a slow unwind and I was skeptical.. I am no longer.

Many people who post seem to think that the down turn has already started. At least that is my perception of reading.

It may have but I have thought many times over the last 6 or 8 years that we couldn’t go higher. And yet not only did the debts increase but so has stocks.

To me, the numbers appear phony. As in employment. How can we have had an increase in government employment while there were 800,000 on furlough plus all those contractors that did not get a pay check at all.

Yet the mortgage rates are not climbing percipitously and the stock market is only slightly down from all time highs.. Yes in some areas house prices are no longer rising and some have actually come down but not back to earth.

And during a winter that has for many been much more difficult than normal.

How long before we actually see damage? How long before a recession is apparent? Before we see defaults and bankruptcies?

Some day but not yet!

American economy and its equities market are the shining star right now in the world presently. I Still think the money flow is into the US. PE still not crazy bubble rich for snp.. plenty of innovation dependent on what innovation wave your investing in.

the auto loans bubble chart is off the charts, think were heading into a fixed ops market cycle not a sales cycle, 110 million new cars in last 6 years

I thought cars were going extinct?

I’m 47 and I’m proud to say I’ve never gone into debt. Bought my first brand new truck a year ago with cash. The only debt I’m interested in is a mortgage, but California is too damn expensive for that.

For me Art’s comment was terrific and gave me a lot to hope for.

My indebted best friend has only been saved by a relationship with someone who has saved and will also inherit. When he crunches his retirement numbers it’s always the ‘best case’ scenario. (IF this happens and I do this then…..)

Having no debts equals freedom, pure and simple. Wolf’s article was aptly named. ….Debt Slaves.

I invest in REIT, that works for me.

Credit card accounts assessed interest is up to almost to 17% in Q4. Close to 2% up in one year. Even the debt slaves are choking on that one.

I have watched in wonder over the years at the huge sums of money borrowed by students in the USA, but never really gave it much thought.

Until my son married a lady from Los Angles who had been educated in various institutions, and who did not arrive with a dowry, but with a millstone of student debt around her neck. Putting aside the obvious questions that a Father might ask, it appeared that having taken “deferments” and payment holidays etc etc the debts were rapidly rising.

Discrete enquiries brought forth the fact that these loan agreements had been co-signed by her mother, who had no means to pay , and of course the student loans could not be extinguished in bankruptcy.

At this point the Chief Executive of the Grumpy Buggers Bank (namely Myself!) was asked to assist, and out of love (sic) for my son, I did. I suggested that “we” made an offer to do a lump sum settlement for the two non-Federal loan agreements and to my surprise (and delight) the two companies settled for 27% of the outstanding balance. I had to grit my teeth and pay 90% to clear the Federal loan.

I was left wondering that the Student Loan business must be highly profitable in the USA if the companies could afford to accept 27% to settle .

“if the companies could afford to accept 27% to settle”

How much did she borrow compared to what she was expected to pay back? It just might well be 10% of the amount “owing”. In other words, even with the 27% take the creditors are still doing well.

I was slammed on here previously for saying that when this “interest on interest” is written off nobody loses anything, it’s made up BS, a bluff.

Yet here we go, in reality they are glad to take just a small part of it, which is plenty already.

I estimated that if you deducted the additional fees/interest which had been added then we paid 50% of the core debt and no fees/interest.

Sidebar to Covey-a paraphrase of H.L. Mencken that I wish I had been taught as a young man (but would I have listened?): “…never marry someone with more problems than you have…”. May we all have a better day.

In the Good Old Days a fellow might make discrete enquiries about a lady’s cooking and social skills (apologies to the more sensitive females of the species) and casual observation might indicate if ones intended fell in to the High Maintenance category, but in this mean and miserable world we seem to live in, it would seem we must now add a financial health check!!

Here in the UK our politicians decided that sending everyone off to university for 3 years was easier than trying to stimulate youth employment and as a result of introducing Tuition Fees and the Student Loans to pay for the fees generations now leaving Uni have large student debts hanging around their neck.

This debt has distorted the housing market because student debt affects the ability to borrow on a mortgage and graduates are tending to live at home longer. Even worse, the kids regard returning home to live as a viable option.

New Rule for Life!!: As soon as your kids leave home, DOWNSIZE so they cannot return!

Many really don’t have the choice when choosing a life partner. It comes down to be alone or take what you can get. Duality. Being a father is my greatest achievement, at the same time the financial strain has been an almost insurmountable burden. I would have been better off economically waiting two more decades to establish a family, but could not have kept up with a rambunctious six year old in my fifties. Everything is choices, compromise and trade offs.

In the end the only thing that matter is can you afford to live. Historically the standard slave worked for room and board and was beaten if they didn’t produce. In today’s world the average person works to pay taxes and hopes to have enough left over to pay room and board, and of course make a vehicle payment to get to work to produce the room and board payment after taxes. The problem with living in a country like Canada is that there is very little discretionary income left over. So the question needs to be answered, is it enough to just exist to fund the government machine? Most people can’t see past their immediate needs but for some it just doesn’t cut it. I can’t just exist to fund some government bureaucrats fantasy.

What you are describing is a transitional process, from the first to the second (or worse) world state condition. Just look at the trends.

Can a person in, say, Venezuela ask himself “I can’t just exist to fund some government bureaucrats fantasy” ?

He doesn’t even have this option.

American workers will be free again when we make the feds stop taxing jobs, i.e., wages, salaries, and tips.

Solution in concept is simple – delete line 7 from the IRS 1040 form.

Both the federal Income Tax and the Federal Reserve Bank were implemented to pay for WWI, and we have been at war since.

Applying the federal income tax to jobs was enacted as a war tax for WWII, ironically designed by Mr. Free Market himself, Milton Friedman. His wife never forgave him and neither do I.

We need the rallying cry of DELETE LINE 7 to reverberate throughout the land. Reclaim your freedom and your hard-earned wealth.

I don’t disagree with the idea to stop taxing wages and salaries, but neither the Federal Reserve nor the federal income tax were enacted to fight WW1.

Both of them were enacted in 1913, one year before WW1 broke out and 4 years before the US entered the war.

How convenient pff

The type of people you are describing don’t pay any taxes, only receive in distribution from the government.

You need a certain amount of income to pay taxes, then the more you earn the more you pay, but comparing the majority of workers with slaves completely misses the point. By that standards, the poor workers of today live better than kings of the slave period.

Then, Canada always struck me as a very socialist country , with most services run by the government which in my book means the more government gives the more it takes.

I think that might be the other way round – the more government takes, the more it purports to give. You might assume the difference is the same, but then you would be accepting government power as a fait accompli which is disinterested in own existence, something clearly far from the case. In fact you could extend that reality to more capitalistic systems such as the US and underline that government involvement in the financial economy , where it exists, might at times be equally unhelpful . The tenet in that circumstance is after all a socialist one, from inflation management, government guarantees, through to defense, they are deemed a need of society.

There are a multitude of formats and combinations possible in style of governance. You might for example tell us whether the pyramids were built by the slaves or the pharos, but I think the answer is undiscernable. That is to say that although the lot of all may have improved, a slave is still a slave. A slave is one who is offered less choice than the one who will profit from his work, it does not mean being physically shackled. In certain societies there are slaves who remain so due to denial by society, they are known as slaves, and yet they appear as normal people to outsiders. In fact the slavs, from which the word slave derives, had their own word (orbu if I remember) for a slave. Its root is “orphaned”, probably meant in the sense of one whose allegiance is changed.

Is any allegiance to government voluntary, taught, or forced ? I don’t think many would know how to analyse their relationship with government fully, and fortunately most people are blessed with a sense of moral to help guide them through life in real terms.

I guess it’s been accepted by the Fed, legislators, and Wall Street that we are headed toward a debt supernova that should not be prevented.

How else can you explain the existence of national debt equal to 100% of GDP and growing at $2T per year, while Republicans push through unwarranted tax cuts for political gain and Democrats seek “pie in the sky” spending programs. This is all being done with little to no serious mention of debt levels in political discourse or the media.

The national debt does not include unfunded liabilities for programs such as Social Security and Medicare. Even by the Federal government’s squirrely accounting methods, the trust are expected to run out of money in a few years. We haven’t learned much from the Germans’ experiences of the 1920’s with irresponsible fiscal policy.

An insightful story, from another really old engineer. My dad was also an engineer (a genetic defect, a kink in the DNA). He consulted for a mine owner to reduce the operating cost of a mine by replacing laborers with mules to haul the ore. Dad failed and was upbraided by the owner for over looking a major operating cost factor. The owner hired prisoners to work underground and told the engineer that if a prisoner died, you just hired a replacement, but if a mule died, you had to pay cash for a new one.

The financial moral is this. If the entire profit from a worker’s productivity goes to another, the worker is a slave. And his replacement cost is his value. Thus math shows that if you manage your finances such that 100% of your income goes to others, you made yourself a slave.

The US national debt is roughly $63,000 per person, every baby, ancient one and wage earner. The unfunded liabilities double this value, an imprecise number due to the future time related cost of money, population and more debt pile on by our betters in Congress. Each sovereign state adds more. (Mr. Richter could sharpen these numbers.)

A recent quote from OMB – WHCoS Mick Mulvaney, on the nation’s exploding deficit, yearly debt, is “nobody cares”. The Green New Deal is founded on this concept.

We live in a existential Ponzi scheme, a debt bubble, which must pop. Historically, people starve to death when this occurs. Venezuela is experiencing this today.

My question: On what day will the good times stop?

I can’t tell you the day, but I would recommend that you read the first few chapters of William Shirer’s “The Rise and Fall of the Third Reich”. Too many people and special interests want free stuff from the government and want someone else to pay for it. Just because we have a constitution that has last over 230 years, doesn’t mean that it can’t be tossed on the scrap heap of history by a future dictatorship. The Weimar constitution in Germany lasted less than 14 years.

So who are responsible for this except the people who took the loans?

My youngest son dropped out of his “prestigious” college when he realized it was a scam. I tend to agree with him.

There is a program called income based repayment for high earning people with student debt (doctors, dentists, etc). 10% of income to pay down the student debt and in 20 years the balance is “forgiven”. The only hitch is that the former debtor will have to take the written off amount as income and pay a huge tax that year. I am convinced that this program is playing a role, maybe a big role, in the student debt story. It is discussed with every student borrower at professional schools as part of their repayment plan.

According to my modeling the economy slid in to rescission around July on the micro-economic level. What I look for are indicators of subtle changes in micro-economic activity (where the money is going). If anyone is interested I’ll give some more detail. The analysis in this post indicate we’re looking at some very significant changes in the micro-economic money patterns. It takes sometime before the changes show up in the macro-economy. Of note, in this post it shows that the micro-economy is starting to hit the credit saturation point. This is where additional debt doesn’t add anything to the economy and the servicing of the existing debt is reducing micro-economic activity. Things are going to get interesting.

Here is an off the wall idea, every person about to default on their credit card or other type of non recourse debt should borrow an extra thousand bucks, or more and instead of spending it, burn it, do the figures on that.

Recently managed to downsize.No debt first time ever

and a few bucks in the bank.Went out and bought a Dyson

and some fancy (for me) kitchen stuff.Tempted to buy

the Jag. but I think I’ll stop here . Used a credit card to

get points .Felt good.

I got out of debt when I scrimped and paid off a house thirteen years ago. It was and is good to be debt free. Doing without beats paying on a loan, hands down. If you’ve got cash to pay for that Jag, then I say ok, you’ve earned it.

Part of the student loan racket has to be getting people addicted to debt right from square one, without ever knowing what it’s like to be debt free.

It is also deeply immoral: academics, and the horde of administrators, are living off the debt incurred by the clueless young – however much they might rail against Capitalism. ……

“The U.S. Bureau of Labor Statistics reports that the average salary of a University Professor was $75,430 annually as of May 2016. The lowest-paid 10 percent of all University Professors earn less than $38,290, while the highest-paid 10 percent are paid more than $168,270 per year.”

“Star” professors do well, some making half a mill, and skew the average upward. The vast majority of professors struggle to cling to the middle class, trying to pay off PHDs on around 60K a year. Adjuncts (the highest growth area for academics, earning about 20-25K)) would be better off working at fast food places, because they would at least have the possibility of benefits like medical someday. Most of the money goes to facilities- gym complexes, computer labs, elaborate food options, nice campuses- all things designed to impress parents to enroll their kids. Decades ago, even top universities had dorm rooms that were Spartan; now, they are all comfortable self-serve hotel rooms. Administrators do well- usually better than the teachers.

The lions do not concern themselves with the opinions of the sheep.

A sheep’s idea of bravery is to become the lion’s pet.

And call it liberty. You see how easily the slaves have learned to love their chains. There will be no escaping them now.

Aaww, they’re not all that bad, lion says all pets learn this way but we can take them off when we want. I knew a sheep who regularly put his head into lion’s mouth to show us how good lions really were , bravest of all he was, he had that lion trained . He hasn’t been seen lately though and they say he has was made member of the inner den , but there are a whole load of volunteers waiting to take his place if you’re interested.

It is well worth watching “Dynasties”, narrated by David Attenborough. A recent episode on lions was just followed by an episode on the painted wolf. The lions will let the painted wolves do the work of taking down prey, and after the painted wolves have taken a few mouthfuls, the lions come in for the feast. Adding injury to insult, the lions took down one of the puppies in the same episode.

The lions are comfortable in their role as kings, and they will tell you that life is rough on them as well (see Lions episode).

Not to worry, though. Alexandra Ocasio-Cortez, Elizabeth Warren, and other politicians jumping on the bandwagon, assure us that printing more money, and legislating a “billionaire’s tax” , will set things to rights.

Kind of like, Warren is saying that she will keep the lions on the reservation, and limit their activities, for the good of all; AOC proposes creating a whole new reservation with unlimited provisions for all, and that so far seems to include the lions, because creating enough money is THE answer.

So far Attenborough continues to talk scarcity and competition for sustenance; almost like he’s not buying into magical answers for the world we live in….

Thx, Wolf.

I’d also suggest that debt contributes to other problems in society when an indebted person/family worries about or experiences an income interruption. Values tend to become a lot more flexible and judgement impaired when we feel vulnerable.

Wolf – Escaping debt slave status is simply an instantaneous prisoner transfer to “wage slave” status. And escaping wage slave status is like escaping solitary confinement for the majority of Americans, compared to the ankle monitor every citizen wears while in debt slavery.

Perhaps people should learn how to work a calculator(!!!) and actually plan things out long term instead of what is minimum payment today. I see too many bad decisions from both old and young and I can not feel sorry for them anymore.

The underlying reason for the debt slave society, is the religion of materialism. Materialism is the faith based religion that the material item you do not have will make you happy. This is in spite of the fact that all the other material items you do have. do not. This faith is so strong, people are willing to ignore mathematics, logic, and even common sense in order to practice it.

Most actually believe other debt slaves care or are impressed by their most recent debt based purchases. and that their purchases will somehow make them appear successful. This religion is supported by the various media inputs the average debt slave voluntarily subjects themselves to on a nearly continual basis. Mankind seems to have always needed to worship some sort of entity, today that has taken the form of material goods.

SO depressing on SO MANY levels. of note the new high in student loan debt. these frankensteins monsters of retardedness are the stupidest thing EVER to come out of washington.

i am NOT against loans for college in theory but the structure as at present is the dog dumbest that could ever be conceived. a simple fix is to force those borrowing to have the family co-sign or, barring that, THE COLLEGE TAKING THE CASH BORROWED AS TUITIONS should guarantee the principle balance borrowed! if those that know the student borrower best (the family) won’t get in bed with them WHY WOULD THE AMERICAN TAXPAYER?! further, the easy access to cash for degrees of ALL description has been DIRECTLY RESPONSIBLE for the skyrocketing of tuitions at a rate FAR outpacing inflation no matter how calculated…if colleges want to crank up tuitions then let them have their ass in the air on the loans that the are scraping out of the kids banks due to the easy money the dope kids are borrowing. let’s see how many gender studies and cultural diversity studies degrees they backstop once they are on the hook for the loans behind those useless degrees. same with post grad degrees for folks that never ever enter the job market after their undergrad. i’d like to see how many of the heaviest loan loads are for folks with two (or more) degrees in useless majors. i am NOT saying that we should do away with liberal arts..we should NOT. we SHOULD force some financial discipline on the students, the schools and the families. right now we are letting the least sophisticated of the citizenry borrow many tens of thousands of dollars, and often WAY more than that, AND guaranteeing THE LENDER that they cannot be stiffed.

the GUARANTEED in Guaranteed Student Loan is for THE LENDER, not the borrower

YOU CAN’T MAKE THIS SHIT UP

Want to hear something that will make you all sick? I work for a government agency and my colleague, an attorney, entered the Public Loan Forgiveness Plan. His wife is a doctor and also entered the PLFP. He told me he graduated law school with $265,000 in debt (which means a large portion was refund checks and programs abroad). I should also mention he is from an upper middle class family.

PFLP determines your monthly payments based on adjusted gross income (AGI). So, he and his wife figured out a way to defer close to 75% of their income by maxing on ever available retirement plan, deferred college savings, healthcare, city pension, etc…and he managed to lower his monthly payment from around $3,500 per month (for just himself) down to $45 per month! He pays $45 per month for 10 years then gets the $265,000 plus interest forgiven! The part that makes you sick; he also gets to keep 100% of all the deferred income! So, the community pays off his loans and essentially subsidizes a million dollar retirement account for him. And oh yea…he also makes over $100k!

I’ve tried to alert Navient to this scheme every time I happen to speak to them but never get anywhere. I just wonder how many others are gaming the system.

Not many. I’m sure this story is anecdotal, as 99% of all applicants to this program are rejected.

It is like everything else, those who can afford to pay for representation can work the system. The poor to middle class can never recieve this kind of relief.

And that is exactly what happened. Basically the parents of this married couple decided it’s more financial sense to float the for 10 years while they deferred almost all of their income, because then the community all chips in to pay off (forgive) the educational debt of their adult children, while allowing them to build a million dollar retirement account in the process. My biggest issue with this is that the deferred income doesn’t get calculated for payment purposes during the 10 years of PLFP. It’s still TBD if Congress catches wind of this scheme in time to make sure that borrowers that deferred most of their income to lose their AGI, end up having to pay it back in year 10 when they request forgiveness for complying with the program.

The politicians will tell you it’s all teachers and fireman in this program, but in reality it’s doctors, lawyers, and well laid administrators that are not in roles where they are providing socmia

Services. The doctors all need residencies anyway, so they really make out because they get the experience at public hospital, then get their $300k in loans forgiven in year 10 and start or making $300k with no debt following year 10.

Just saying. I am an administrator, and I can’t remember when I was last well laid…

“What is systemically wrong with the student loan scheme is that it’s a three-party deal — universities, government, and students – but without any kind of discipline imposed on them by the market or the government.”

Student loans are unproductive credit. Fail. Bad for the economy.

this dosent tell the real debt slave story

which is the long term deliberate policy by the creditor class of putting the whole country into so much debt thru federal spending

that not even the interest can be serviced thru taxes–at that point more borrpwing becomes necessary to just pay the interest and every ‘normal’ citizen is then a slave

a captive congress takes its orders to create more and more spending–probably not even knowing the real reason

credit card, student and auto loans etc all help but are not the central lever.

institutions that can print unlimited money/credit

and then force [federal overspending] people to borrow it from them at interest

going on for millenia–read richard hoskins ‘war cycles. peace cycles’—-mafias shylocking in industries they control etc etc–first 30 minutes of ‘on the waterfront’ etc

its brilliant, beautiful , deadly and it is working