Home-equity-loan balances in Canada per capita are now 3.3 times what they were in the US during HELOC peak before it all collapsed.

Home Equity Lines of Credit – the infamous HELOCs Americans used as endless ATMs to draw equity out of their homes before home prices collapsed – played a role in the US mortgage crisis. And Americans have learned a lesson since, despite mega-efforts by the industry to revive HELOCs.

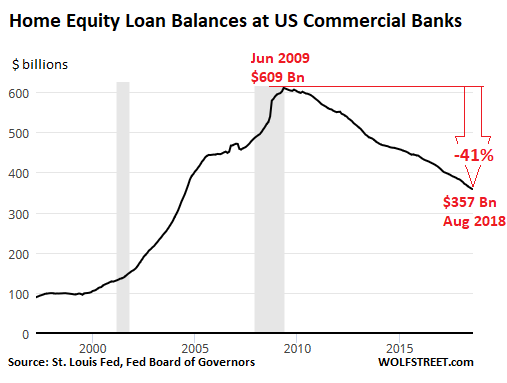

Balances of revolving home equity loans at US commercial banks soared by about 300% in seven years, from $154 billion at the beginning of 2002 right into the crisis, peaking in June 2009 at $609 billion. As the housing-and-mortgage crisis blew those dreams of the endless ATM apart, Americans learned their lessons, either defaulting on, or paying down, their HELOCs. At the end of August, HELOC balances had fallen 41% from the peak, to $357 billion – back where they’d been in 2004 on the way up – even as aggregate home values now exceed the peak of Housing Bubble 1:

This near-decade-long decline triggered lamentations by William Dudley last year, when he was still president of the New York Fed, that Americans weren’t borrowing enough against their homes, and that they therefore were too lackadaisical in their job of boosting consumer spending with borrowed money.

“The previous behavior of using housing debt to finance other kinds of consumption seems to have completely disappeared,” he said. “Instead, people are apparently leaving the wealth generated by rising home prices ‘locked up’ in their homes.”

In Canada there is no such reluctance. That makes sense because Canadians had skipped the housing bust that Americans had gone through. Instead, the Canadian home-price surge, after a brief dip during the Financial Crisis, continued until 2017 and in the process became one of the wildest and scariest housing bubbles in the world. And Canadians are loving their endless home-equity ATMs.

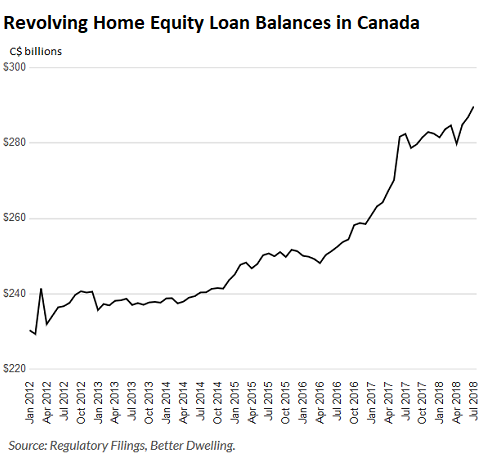

Canadians owe C$290 billion (US$225 billion) in revolving home equity debt, such as HELOCs, at the end of July, according to Better Dwelling, a Canadian real-estate site, citing data from the Office of the Superintendent Financial of Institutions (OSFI). This is up 2.6% from a year ago, and a new record:

In US dollar terms, to make it apples and apples, Canadians owe $225 billion in home equity loans. Americans owe $357 billion. But here is the thing: the US population (326 million) is about nine times larger than the Canadian population (36 million). On a per-capita basis, American owe $1,095. During the peak, they owed $1,868. Canadians on a per-capita basis now owe $6,250 — or 3.3 times as much as Americans did during the peak.

If Americans owed as much per capita as Canadians, they’d owe collectively a mind-blowing $2 trillion! Compared to the $609 billion they owed during the home equity line of credit peak in June 2009, which collapsed with such great fanfare.

Canadians have a right to be worried about this, if they spend a moment looking south across the border and studying what happened there during Housing Bust 1. It was ugly. But we already know, because it has been endlessly drummed into us: Whatever happened in the US cannot happen in Canada.

Better Dwelling points out that these home equity lines of credit fall into two categories: Loans used for personal consumption (90% of the total), and loans used by business owners to fund their small businesses (10% of the total). The first boosts consumption, the second boosts investment and hopefully production. Home equity loans used for:

- Personal consumption jumped 5.8% year-over-year to C$261 billion.

- Business purposes plunged nearly 20% year-over-year to $29 billion

Better Dwelling adds:

The balance of debt grew as home prices made the largest jump in Canadian history. In the event of a price correction, borrowers may find themselves with less equity than expected. Over a quarter of HELOC borrowers have been seniors, which is a tough age to find yourself short on cash.

Dudley, in his lamentations about the decline of HELOCs in the US since the Financial Crisis, tried to explain why the Americans have been shying away from HELOCs. Among the reasons (note the term “scarred”):

[H]ouseholds may have been scarred by the experience of seeing their neighbors who borrowed heavily during the boom lose their homes and have their credit ratings badly damaged. Observing these consequences may dissuade current homeowners from making themselves vulnerable to foreclosure by borrowing against rising home values.This would lead to an increase in a household’s precautionary demand for savings in the form of higher housing equity. This increased equity cushion would guard against the risk that the household could find itself in a negative equity position in the event of a future decline in home prices. With an equity cushion, even if the household were to experience a job loss during a future housing downturn, they would be able to sell their home, pay off the mortgage and avoid any damage to their credit.

It appears Canadians still have this “scarring” experience – and the bitter lessons it provides – in front of them.

The Bank of Canada faces a self-inflicted quandary. After keeping rates too low for too many years, it is now confronted with asset bubbles, including one of the world’s biggest and riskiest housing bubbles that has begun to deflate in some corners. Read… Toxic Mix in Canada: Spiking Inflation, Variable-Rate Mortgages, and a Housing Bubble

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Love ya WOLF!

Wrong. Sorry.

Banks in Canada lend to 100% loan to value with limited underwriting.

U.S – good luck trying to get a second mortgage. Most lenders cap at 80%, some go to 90% lev, few above that. Then they stress test the payment (use high repayment amount) AND they limit debt to income around 40%, 720 fico minimum.

Americans would LOVE to owe $2T on second mortgages. Also – everybody in Canada has adjustable rate mortgage on 1st and 2nd mortgages; U.S is all FIXED rate, so most, given the opportunity, want to roll the second into the first and get a fixed rate – Canada doesn’t have that option. . AND if you want cashout in U.S, it makes more sense to increase the amount of the first mortgage because it is fixed. Americans hate adjustable rate mortgages, and HELOCS are adjustable.

U.S Mortgage Game: Buy house at 45% debt to income. Nobody can live at this debt level, so for 2 years subsidize income using credit cards. Then, after house has appreciated 10% to 15%, cash out the equity to pay off the credit cards. Rinse repeat until the Fed ends the game.

After 2008, Fannie/Freddie needed to cap DTI’s at historical, livable level which is around 25%, 30% max. the only way you can survive a 50% dti level is if housing prices go up and you can consolidate down the road. With Fed raising, this may be over soon.

Steve,

Well, no…

About one-third of American households own their home free and clear. Another third bought their home years ago, made regular payments, and didn’t do any cash-out refies. And they have lots of equity in their homes. Both of those groups have plenty of room for HELOCs. That’s two-thirds of the homeowners — and that’s what Dudley was talking about. But they don’t want HELOCs.

Another third has little or no equity in their homes because they bought fairly recently, or because they did a cash-out refi, or because home prices haven’t gone up in their market, or for whatever reason. It’s only a portion of that third group that might have some trouble getting a HELOC if they want one. That said, lenders (particularly non-banks) are getting aggressive with HELOCs these days.

Presumably, even those who own their homes, would loose it if they couldn’t pay back the HELOC, wouldn’t they? Some people seems to be smarter than take the bait.

And there won’t be a severe downturn or pension blowup in our lifetime, or Dudley would know.

Banks are aggressively pushing HELOCs too and the minimum credit standards industry-wide (including HELOCs) are being loosened in light of the downturn that is finally seeping through.

Rates are up, volume is down, the over-inflated housing prices have finally started to see their decline – more houses are – visibly – on the market and the way the industry is maneuvering to prepare for this fight is to loosen credit standards.

The Qualified Mortgage rule created out of the Dodd Frank Act was put in place to force lenders to be more conservative in their credit qualifying of a borrower including limiting debt ratios, capping points and fees and essentially doing away with balloon loans, interest only and negative amortization.

If you abide by these rules you are a ‘qualified mortgage (QM)’. If you don’t abide by these rules you are a NON QM.

Over the past few years the market for NON QM loans has inched its way back into a comfort zone. First they were held in portfolios of the lenders who originated them – slowly though – the market has been openly looking for NON QM loans including through securitizations.

Naturally, as the market looks for these products – the industry finds ways to deliver those products. The ways to deliver those products is to – reduce credit qualifying standards including – increased LTVs and lower credit scores.

In my compliance banking senior leader who specializes in residential mortgages – Americans have ‘not’ learned their lessons.

…and they absolutely will be happy to hit up the ATM known as their house equity. And – Banks – will be there to continue to do what we they do – find ways to make money off loaning money.

This is pretty true, however, do not compare today’s non QM with last decades sub prime; they are still world’s apart.

Furthermore, most HELOC lenders are still pretty conservative. Good credit (680+) and ltvs of 80% Max. Don’t forget you still need to qualify via DTI. HELOCs today are not like they were last decade and many don’t qualify.

Thank you Wolf for the great article and feedback.

As a homeowner in the middle third (we bought long ago but still have a mortgage), we are bombarded with at least 10 calls (and snail mail) a week to refi. All of the calls offer six figures of “free” money we could access at a rate now of about 5%.

The temptation is real. 5% is still historically low compared to my first house at 12% and much better than credit cards at 28%.

So far, no emergency need for cash but it is far better to refi or take a HELOC than to run up the credit cards at near Pay Day loan rates.

If I was a “You Only Live Once” kind of guy, I’d now be buried up to my eyeballs in home debt.

Steve, go home you’re drunk. As a Canuck I know how full of crap you are. Tick tock. Watch as a flame touches all of our paper millionaires at once;gonna get hot.

“U.S Mortgage Game: Buy house at 45% debt to income. Nobody can live at this debt level, so for 2 years subsidize income using credit cards. Then, after house has appreciated 10% to 15%, cash out the equity to pay off the credit cards. Rinse repeat until the Fed ends the game.”

I don’t think he was drinking, there.

Except there’s a twist: Finance or re-finance 45% loan to income, when the economy hiccups declare bankruptcy (you can keep your house if you can keep up the payments) and tell the credit cards etc to go fish, wait 7 years, game on again.

“U.S Mortgage Game: Buy house at 45% debt to income. Nobody can live at this debt level, so for 2 years subsidize income using credit cards. Then, after house has appreciated 10% to 15%, cash out the equity to pay off the credit cards. Rinse repeat until the Fed ends the game.”

This is both kind brilliant and one of the stupidest most financially dangerous ideas I have ever heard :)

Although I am pretty sure flippers in the last bubble were crazier than this…

Funny. I am a Canuck (Oakville) living in U.S.

Canada has been extremely loose with HELOCs – there is even a great commercial you can watch on Youtube “building a 4 story waterslide, no problem, if you own home you qualify”.

The U.S has horrible HELOC products. Fannie/Freddie/FHA lending is the way to go when possible. Yes, we all get 10 offers per day for HELOCS, most of those sales calls end up trying to convince the borrower that a cash out first mortgage is the way to go. (thats where the origination money really is).

BUT, the U.S is adding some non-QM lending programs that will allow self employed borrowers back into the market. As one person commented – these are NOT anything like the old subprime (100%ltv,stated income) since most of them require 20% down payment. IN any other Country in the world, 20% down will get you the keys the next day! Unfortunately, here in the U.S, the underwriting only begins.

Home borrowing is broken in the U.S. Getting rid of Dodd-Frank, however unlikely, is the only way to fix it.

Canadians are stupid most took 5 year fixed rate mortgages only to see mortgage rates fall. If fact they always seem to take 5 year fixed rate mortgages which generally are the worse possible mortgage to take.

“The previous behavior of using housing debt to finance other kinds of consumption seems to have completely disappeared,” he said. “Instead, people are apparently leaving the wealth generated by rising home prices ‘locked up’ in their homes.”

Scumbags like this are in charge of our monetary policy? No wonder we’re so screwed.

And after the next downturn, Dudley will blame foreclosures on people who “irresponsibly” took out HELOCS for consumer spending. Not that he’d ever accept any blame for his bad advice.

+10

Typo: (not the term ‘scarred’….) Note?

“scarred” as in “scar” = wound that has badly healed.

Dudley used it – that’s why it’s in quotes.

What nick meant is that you probably meant to say “note”, not “not”.

Ah-ha! Thanks :-]

Americans and Canadians are now on the same footing when it comes to interest deductibility of HELOCs for tax purposes. It was never allowed for personal reasons in Canada, and the TCJA removed it from 2018 onward. Overall, a move that was long overdue.

I was surprised, but shouldn’t have been, when I heard Diane Olick on the PBS Nightly Business Report earlier this week talking up the “$6 trillion of home equity Americans now have, but many analysts are wondering why it’s not being tapped”. If this isn’t proof that the talking heads at CNBC, who produce the NBR, don’t know what they’re talking about, I don’t know what is.

I agree, Wolf, that many Americans learned a bitter lesson from their careless use of HELOCs a decade ago, but apparently the Mainstream Media Morons haven’t.

I think one simple reason is that not all Americans are as stupid as the media or our policy maker are hoping for. I personally have a HELOC, and it’s going to simply sit there and do nothing unless there is a real emergency. I am certainly not going to use it to take a vacation or buy a car.

Enough people got stung the last time they aren’t likely to forget the lesson. It will take a few years and a whole new generation of suckers to see how horrible a HELOC might be when used on frivolous things in a rising interest rate environment.

You call it Housing Bust 1, implying that there will be a Housing Bust 2?

:-]

Get lost with that innocent smile Wolf, pandemonium could break lose WW3, ok probably not.

Sorry

Housing bubble 2.0 is already baked in!

When median house price is way above the median salary, it is just matter of time.

Either one has to higher or the other will come down!

There are few jobs with living wages + benefits compared to a lot of Mac jobs in the gig Economy.

Student loans of nearly 1.4 T will be a drag on the future household formation!

Non-QM is coming around to try to prevent Housing Bust 2.0.

Or should I say, the elite who had access to capital when nobody else did, want to dump the millions of homes they bought at the newly inflated prices. I think the non-QM stuff will pull some marginal buyers off the sidelines, but not enough to move the needle as the elite have stopped buying and those with 3.5% rates are also standing still.

(Washington needs to get rid of Fannie/Freddie, or at least update the note. Mortgages should be portable like they are in other Countries. You lift the lien off of house A, place on house B, NOT rocket science. The NAR should have done this BEFORE mortgage rates started going up…we had 10 years to fix this!! This change would have helped to maintain housing liquidity in a rising rate environment.)

There absolutely will be a housing bust 2 and 3 and 4…. every ten years or so the market cycles.

However, the last housing bust caused a cardiac arrest in the banking system. That wont happen again because ABS and derivatives products (CDS) are not nearly as widespread and banks are not bearly as levered as before (at least not in these instruments).

Now there is more record debt of ALL and any kind and more Trillions of derivatives (>250T+)than in 2008

Mortgage debt below that of 2008. But all other household debt, auto loans, CC and student loans are at record levels. Not to mention 1+ trillion annual deficit and DEBT of 21+T

NO one learned from 2008!

So, why are HELOCs the outlier? (Auto, student, card, corporate debt, gov’t debt, etc.).

So, there was a debt orgy going on, but homeowners decided not to be responsible and buy cars and run up credit card debt??

Mortgages ABOVE 80% loan to value (and HELOCs) are hard to get nowadays. I don’t know why people are having a hard time understanding this. You can buy a BMW with a signature, no money down, with a 600 credit score. Now, try and get a HELOC with a 600 credit score….just won’t happen.

ALL of the mortgage lending since 2008 has been Fannie, Freddie, FHA – loans that you can “sell” to somebody and get them off your books. HELOCS don’t work this way – the bank that lends it, owns it. AND HELOCS got crushed in the last crash….billions upon billions written off by foreclosure and short sales. Banks are extra (some would say rightfully) cautious this time around.

HELOCs are hard to get in the U.S, MOST of the marketing pieces are sent out hoping to convert the borrower to a cash out Fannie Mae loan -fund it, sell it, not your problem anymore.

The modern day housing bubbles were caused by the Chinese. It has affected the American housing market but not to the degree it has in Australia, New Zealand and Canada. The Chinese were in the midst of destroying the entire U.S. housing market like they destroyed the Australian, New Zealand and Canadian housing market but Trump stepped in and slapped tariffs on China. Now the Chinese have backed off of buying homes worldwide and we see all the housing bubbles they created deflating.

Dead on. Vancouver is the Chinese money laundering capital of the world…also, Fentanyl from China is sold, real estate purchased.

Incomes $60k, average home (sorry, condo) price $1.2M

China is in the middle of a LBO of Canada

What is meant by the term “personal consumption”? Vacations? Stuff? More housing purchases? Bills to pay?

It could be a real big comeuppance. It would be well deserved says this Canadian. What did Forest Gump always say? “Stupid is as stupid does”.

https://www.youtube.com/watch?v=tldGgGFe194

Paolo, in IOUSA it meant gargantuan SUVs and trucks, boats, kitchen upgrades and also trips. None of which many borrowers could afford with or without a HELOC. And now, they’ve lost the ability to claim the interest paid on the HELOC against their taxable income.

All the more reason they’re a bad idea. But the Mainstreet Media Morons keep pushing them like crack.

A kitchen upgrade, at least, is a capital expenditure that may increase the value of the house…..maybe.

Non-investment spending – vacations, BMW convertibles, Harleys, paying down maxed-out credit cards, boats, pools, etc.

It could also mean unforeseen medical expenses.

The largest cause of personal bankruptcy in the US.

All developed economies are struggling with medical costs, but the US is in a league of its own. Drugs are 12 %b of TOTAL wholesale.

Medical is devouring the US economy.

Harvard has studied the prob and noted that every thing costs more in the US than anywhere else: comparable or identical.

Admin runs about 3% everywhere else. In the US it’s 8%.

Note this does not include the most expensive time: MD s arguing with insurance cos, according to docs their big headache.

At some point you have to look at results. The rest of the world has gone single payer.

I just had to have a medical procedure. Not one person in the chain of the MIC (Medical Industrial Complex) could tell me what this procedure would cost prior to having it done. My health insurance costs around $22k per year and will pay basically nothing for what I had done

Have you been to an emergency room, lately?

It’s insane

@Begbie,

Or system sucks hard. But it is expected that the hospital has no idea what their services cost. Why? Because everything is billed piecemeal from every departments billing center. And rates are always changing. And as far as I can tell hospitals have no customer facing entity to provide a complex estimate for a procedure.

The only way to get price estimates for major medical intervention is to hire a 3rd party resource that does have data on current average billing for major procedures. If you have insurance through a big company, they often pay for you to have access to such a service so you can estimate cost and coverage ahead of time for a certain hospital.

Most good insurance, for immediate life saving intervention, will allow you to use out of network hospitals for ER situations. And they state they will charge you in network fees. It is probably best to discuss that scenario with your insurance company in advance to make sure you understand the limits of this policy. Because in a real emergency you have time to consult your insurance or pick the best hospital.

Even then yes, the ER will likely kill your annual deductible because even a short visit costs at least a couple thousand… every time I have gone we have regretted the cost, even though we really had no choice. Now with an HSA it is more palatable, but still not ideal or fair.

As an example, if Canada went to actual single payer (i.e. personal responsibility) instead of financing health care costs by taxation and debt the cost would be 500 a month per person. Family of four: 24,000 dollars a year.

This is what ‘free’ healthcare costs in Canada, though it’s hidden.

I know the ‘single payer’ designation means the payer is the government, but taxpayers fund this even if they are oblivious to it. If consumers directly became the single payer, the reality would quickly cause outrage. Not many people avail themselves of 500 dollars a month in healthcare.

It’s not just pensions (most of which seem to be solvent-deficient, exempt by IOUs that can never be paid, especially government pensions, and even at the top of the markets) that will cause the effective bankruptcy of the government.

Wow….very well put!

The U.S cannot compete in the world with 20% of GDP spent on Health Care. It is the most inefficient system the world has ever seen.

(I recently had to pick up a prescription, it was $12. When CVS found out I had insurance, it jumped to $25 (my co-pay). You can’t make this stuff up!! They wouldn’t honor it, so now I go to Walgreens and don’t tell them about my insurance.)

HIV drugs that cost $75 per dose in Africa or India (many Africans get their generic medications from India) cost $3000 in the U.S.

This applies to medications across the board. Also, the U.S. is probably the only country where one has to get treatment without knowing in advance how much things will cost.

“This mind-blowing $2.04 trillion in home-equity loans would be 235% larger than the amount Americans owed during the peak in June 2009, which collapsed with such great fanfare.”

I see a peak of $609 B on the graph, and $2.04T is 335% of that.

It would be 3.3 TIMES larger. But it would be 235% more.

I buy a share of XYZ for $100 and sell for $300: The sales price is 200% larger than cost. OR the sales price is 3 times larger than the cost.

Oops. 3.35 times AS large … or 2.35 times larger (or, more).

But normally expressed as 235% larger (or, more). Wolf originally correct.

And yes, it is also 335% of the original amount.

Robt,

You are wrong on your healthcare comment. The total cost(s) of the single payer system is noted as follows:

The United States spends much more money on healthcare than Canada, on both a per-capita basis and as a percentage of GDP. In 2006, per-capita spending for health care in Canada was US$3,678; in the U.S., US$6,714. The U.S. spent 15.3% of GDP on healthcare in that year; Canada spent 10.0%.

I read all these doom and gloom stories about housing prices and massive debt and how it’s all going to blow up. Instead of blowing up the stock market hit a new high today. It’s blue skies and sunshine as far as you can see.

The housing market has already turned the corner. The stock market’s day will come too. Probably in 6 months or so so.

The next M 8.0 along the San Andreas hasn’t hit LA or the Bay Area yet, either, but that doesn’t mean it isn’t coming, and probably sooner than later.

Same thing the guy said halfway down from the top of the tower!

You are absolutely right: the moneylenders will never be expelled from the Temple.

I completely gave a while back: these people have won.

No sarcasm people, it’s the truth.

It hit a new high in mid 1929, the last time stocks were this expensive.

The market has to climb way out a limb to crash.

It would be fun to be a fly on the wall as Fed members talk privately.

My guess is they think the market has lost its mind.

So borrow money, leverage to the max, and bet it all on the DOW, or on Canadian real estate, or whatever you fancy. Because when the sun shines, it shines forever.

OR….

DON’T FIGHT THE FED. FOLLOW THE MONEY.

(I have a friend in San Fran that quit D&B in 2001 to become entrepreneur (unemployed). BUT, he owned a duplex that he bought in 1990 for $600k, rented one unit out. He made $6k/month rent on unit, then sold the unit for $3m, the other a few years later for $4M. He also bought a house with new wife for $2M (2013), just sold for $7.5M. Right time, right place. Hyperinflation hit San Fran and he was there to enjoy it.)

The U.S. stock market is 100 percent manipulated by the central bankers. If the stock market was honestly run the DOW would probably be around the 5,000 level or less today. From what I see we’re still in a long term bear market dating all the way back to the dot-com crash. When Trump is out of office the March 2009 lows will be taken out.

I hear about so many idiotic economic decisions these days that my mind is numb. I think I’ll buy some short-term bonds, then go off grid for two years.

It’s like watching a bad shootout on TV. The guys keep shooting at each other from 40 feet but they never hit anyone.

I still see Canadian mortgage brokers recommending lines of credit to borrow a down payment for a home purchase. Don’t earn and save, just keep borrowing.

With this Tom Foolery going on I just can’t see how debt levels could get so high, I think it’s the Chinese. Ya, the foreigners caused us to buy over priced homes without funding in the bank to begin with. Not our local brokers to blame, with their advice based on profit incentives instead of sound financial advice.

Sound advice would only matter if the broker paid a fine for every mortgage that went under. Imagine that world, where there are consequences for creating a debt slave instead of rewarding the vultures creating the slaves.

That’s called, “….skin in the game”…something no financial house/broker/etc. wants if they can avoid. With every mortgage sold each “seller” should be forced to retain a percentage of the original risk…..problem solved. But, “God forbid!”…that would be “government interference with the ‘free’ market!” We live in a “criminal enterprise system”. Period.

Hard to find comparable data sets for Canada and US, and won’t post various links. Overall it looks like 35-44 yr US citizens got wiped out at median net worth level compared to Canada. The Canadian overall mean net worth is much closer to the mean also, in US the separation in wealth is much more obvious. Same for income. Canadian net worth has followed a steady path, the US dropped after the bubble, to pick up again. Those figures from 2016. I won’t draw any particular conclusion, the Canadian whole seems more level but equally there must be a point where property valuations will stall, and I suppose it is then we would see how able the Canadians are in managing the effect of that on the rest of the economy.

“The Canadian overall mean net worth is much closer to the mean also”…should read… the Canadian overall median net worth is much closer to the mean also.

From what I hear on the internet, Edmonton in Canada is in dire straits having lost 10K jobs and with an expanding homeless population. On top of that, they say 50K other jobs have been lost in Canada overall. You should read up on the increase in crime in Toronto, an indicator of troubled times. There is fear that if they don’t come to some agreement with the US on trade, they may lose so many jobs that the housing market will collapse.

I was looking just now on how the market itself stood. Prices overall seem to be teetering, and I wonder if Helocs are not just a last dash for a segment of the population that are finding that they cannot keep up on expenses ? There are regions that are known to be tipping, such as Vancouver, where locals still openly admit to being priced out and forced to move…that is a very specific higher end market though, with a lot of foreign investment I think… I just wonder what state the rest off the country is in as per what you mention…doesn’t sound like a good combination – slowing foreign investment via realty , economy outside of housing on edge, very high levels of debt…add the possibility of the US economy slowing “sometime”, Europe in a (seemingly endless) difficult phase also with Brexit adding to that. Not very encouraging really viewed from outside, would be good to hear where some in the know Canadians think it is all going. Canada has been on the radar for a while, yet so far somehow it still seems to just about hang in there.

Edmonton has been doing quite well lately, propped up by government spending. Ditto for Ottawa. Calgary was hit much harder by the oil crash in 2014-15. But household debt levels everywhere in Canada are through the roof. Household debt is currently 101% of GDP. It is $1.72 for every dollar in disposable income. We have not had a severe recession in Canada since the early 1990s. An entire generation has never seen a real recession (2009 being a mere blip up here), while the older generations seem to have forgotten what a recession looks like.

Interestingly, Australia, Canada, the Netherlands, South Korea and the Scandanavian countries are the only developed countries that have not endured major recessions for the past 25 years, and also the developed countries with the highest personal debt levels. The correlation is almost perfect. It seems the longer you go without a recession, the more people believe that recessions don’t happen, or they are things that happen to other countries. And the borrowing rates reflects that.

Nassim Taleb argues that the longer the period of stability, the more cataclysmic the end of that stability is. Pressures build and build without release. When something finally blows, it really blows. Prolonged periods of stability tend to hide systemic risks and allow them to grow, completely hidden from view. Ask Bernanke how his “Great Moderation” turned out.

Hi Alistair, you’re absolutely correct ref the longer a country doesn’t have a recession the worse their debt levels are. Australia is already starting to show signs of a massive hit in property price reduction. Sad you have to have a recession to put a bit of financial sense into peoples heads.

The one radio station I listen to while driving in and around the Greater Toronto Area is a sports station (FAN 590) and of the commercials that cycle during my drive at least several of them are for shadow banking institutions offering HELOCs (e.g. Northwood Mortgage, Alpine Credit). I must hear them several times during any drive, every time I am in the car. On top of that, are an increasing number of on-demand loan firms offering $5000-$10,000; my favourite being Magical Credit that offers loans to students with no income, and anyone with bad credit. Canada has gone absolutely crazy–to say little about the housing bubble that appears to have popped.

No worries: I’m sure Justin has a program to bail them out, just as he did Kinder Morgan.

Steve,

This credit insanity goes way back, though. In 1993 I went back to upgrade at BCIT. (BC Institute of Technology). I was 38, owned my own home, and had money in the bank. I walked into the student union cafeteria for a coffee and looksee, and there were tables set up in the foyer hawking visa and mastercards. All these ‘kids’ were offered an immediate credit card with a $1500 limit….just sign on the dotted line. Fast forward to my last day. I always brought a thermos and bag lunch, but that day I was eating breakfast out with a buddy. He tried 3 credit cards in a bank machine before one could cough up $10 for the IHOP experience. I was stunned. He was 30 years old.

It was pretty shocking and has only got worse since then. The loan adds are non stop and there are even tv shows about credit card interventions. Something has to break.

Ah yes, credit cards hawked on campus in the early 1990s. Been there. Done that. Paid the price. Learned the lesson. The hard way.

Paulo,

I got my first credit card when Visa cards were known as Chargex in Canada (and BankAmericard in the US) and I was a college student. I never abused the card and paid my balance in full each month. Now, some 50 years later, my credit cards all carry no annual fees and all of them have rebate programs of one sort or another. The balances all get paid in full by their due dates. The issuers don’t make much money off of me. There is no law that says you are required to screw up your finances, but there is no law preventing you from doing so either.

In Canada, the Bank of Canada sets the interest rates, but the Office of the Superintendent of Financial Institutions (OSFI) regulates the banks and banking products. Who can see a problem there? Of course, they are both independent, and would not be influenced by each others policies.

Anybody can find the relationship between the three organizations within two minutes of google-searching:

It all runs through the Finance Department. OSFI is a organization under the umbrella of the Department of Finance, and yes, although the Bank of Canada is an independent Crown Corp, it’s also true the Deputy Minister of Finance is a non-voting member of the BoC’s board.

So they are independent, But they consult each other. Canada is a small country, and all the players know each other. The overlaps I’ve described are not secret, and as a Canadian, I’d be worried that they didn’t talk to each other.

The jobs they do are related, and coordination is simply prudence:

Finance – sets fiscal policy

BoC – sets monetary policy

OFSI – sets and enforces Banking regulation

And even if they weren’t related, all of their offices are, at maximum, about 2 to 7 blocks away from each other in Ottawa.

Is this a problem? Or a tempest in a teapot?

That’s the proper way. The BoC has in the past refused to take on a more supervisory role, even when the Minister of Finance asked them to consider it. The BoC has always insisted that bank regulation and monetary policy are two very different things. I believe they are correct. I prefer central banks to have a narrow focus on monetary policy, leaving the finer points of regulation to another authority. It’s not like the two offices never consult. In fact, they do regularly.

I do not dispute your points in theory, but as I hinted, then ultra low interest rates (correct) should have been balanced by tighter regulation of banking activities. And I include CHMC in it. That did not happen, otherwise; we would not have a housing bubble and record HELOCs, as this and other articles here pointed out.

Agreed in full. It happened eventually (first tighter CMHC rules, higher premiums and shorter amorts, then OSFI’s B20 for non-insured mortgages) but not soon enough.

Are all these numbers in US dollars or Canadian?

C$ = Canadian; $ = US

It’s been a few years since I left Oz, but HELOC was very big there too. Now, with the 120% mortgages that I’m sure are still around, the cratering property prices and the HELOC dangle over homeowners, does anyone who still lives in Oz have any opinions on what’s going on there vs Canada? Or am I waaaaaay out-of-date?

The banking commission in Australia did a study of the housing market and it is my understanding that people there have 2nd, 3rd, and even 4th mortgage loans on property. I didn’t know that was even possible. The money was mainly going to buying more investment properties. Now the banks have clamped down on lending and they even look at what you spend on groceries.

P.S.

There are some videos on Utube of 60 Minutes in Australia that discuss some of this, they are very recent too.

PPS. On YouTube there’s a guy called Martin North DFA who does daily brilliant articles on the Australian housing situation. I don’t live in Oz but the articles are still fascinating.

Canada now has the fast growing population of high-net worth individuals in the world. Energy superpower, soon legal weed, healthy immigration rates, fully embracing the post-global world. I’m not worried about Canada. —- Indeed, my property in Calgary keeps increasing in value. Winning baby!

Nicko2: Winning Baby !! in Calgary. Yeah I suppose you are with 8.2% unemployment in the city the last time I checked.

PS: My home is in Calgary…just sayin….

Calgary house prices have been flat or declining for 4 years. We aren’t an energy superpower; we can’t even get a pipeline built to get our product to market. Winning what baby?

Energy super power and winning housing in Alberta. Dude the pot isn’t legal yet, put that away and open your eyes. The government bought a pipeline that they legally blocked before even writing the cheque.

Actually, I think two pipelines if we count the long overdue one to the east coast.

Down 26 % today. I’ve never been so tempted to short as on Wednesday’s 80 dollar pop.

It’s WR’s fault for scaring me off shorting. Lol.

The business owners with leases in the new mall in Calgary probably don’t agree with you.

https://www.cbc.ca/news/canada/calgary/new-horizon-mall-calgary-retail-business-1.4831026

My guess is that those hundreds of billions in paid down HELOC debt was just refied back into a higher and longer mortgage

Are they partying like drunk idiots up there in the North Country???

Ya, winter’s coming.

Speculators haven’t accepted that there was never a real influx of foreign money buying homes across Canada and now they have to finance the flips and condos they bought that were supposed to be sold by now to rich foreigners (maybe one day we’ll find out what really happened in Vancouver, but what happened there is not happening in the rest of Canada).

The spike in debt should get worse over the next 5 years, peak pre-sale purchase of new condos and houses didn’t end until late 2017, once the homes are completed these speculators will have no where to turn but the HELOC to finance the purchases. However, there is a limited amount of space for condos and houses on the HELOC, especially when interest rates are rising and home values are decreasing. At some point their bank/private lender will say no or raise HELOC rates drastically on the borrower until they get the message.

https://pbs.twimg.com/media/DmqN73yVAAEOKGT.jpg

Slowing population growth in developed countries has been ‘offset’ or ‘countered’ by central banks with declining interest rates. Capitalism requires growth (new money) to function. That new money comes from people borrowing. As a side note most people think the fed or the goobermint create money and then send it to the banks who then lend it. This is not true. Where does money and growth actually come from? Every time you buy shit with your credit card you are creating money. Guess where that money comes from, no where. You are creating it magically out of thin air.

So ultimately economic growth must converge with population growth. Productivity and trade are also factors in but generally speaking economic growth reflects population growth in the long run.

So what can the goobermint do when population growth slows? They fake it. The economy can be juiced with continually declining interest rates to make up for the lack of population growth. But now we have a problem. Nominal rates can’t go below zero (if they do it’s not really capitalism anymore). So the fed (banking cartel) is desperately trying to avoid the Japan situation and is always looking for ways to create new ‘growth’ to make up for domestic population slowness. Helocs, asset inflation, student loans, sub prime auto. Problem is just like drinking too much at a party, its all good today but the hangover will be there tomorrow.

Clearly Canada hasn’t learned this lesson yet.

Is that quote from Dudley really from the Onion?

Very good article. This only works until the average price of real estate starts to decline. Oops, starting to happen here in Canada. We are long over due for a correction in real estate prices and consequences will likely be severe. I read in another article that only 40% of consumers with HELOC’s don’t pay down the principal every month, wow, some don’t pay anything and let the balance build. Rates are going up and real estate prices are coming down, should be interesting.

Low interest rates have got people sleep walking to a new crisis here in Canada. In Alberta where I live, all this credit is keeping the economy going, without it, well it would be a mess. But all things come to an end. Unfortunately, you have a whole generation who have grown up on cheap credit. I had 4 young people who worked for me, and all drove better cars than I did….all leased while mine was paid for in cash. “Save”, what’s that? Is there a special card or alternate PIN number?.”…but maybe this time is different….revolving credit lines… “to infinity and beyond”

I’m in Canmore, AB. Prices for real estate are unbelievably high for a town of 13,000 people. A playground for the rich as the moment, hoping a downtown will bring prices down a little. Unless, as you say, this time is different :-)

Canmore IS a playground for the rich.

“Somebody” will come up with an “App” to solve the problem…just download and poof! Everything ok. (Heavy sarc)

Hi, I’m European. Can you explain me why canadian houses are so expensive considering the material they are made of? I’m not talkig about the last bubble but generally.

Most of canadian houses are made of dry wall. It’s the cheapest material to build.

In Europe most of houses are made of brick. Not only the front walls but even the walls between the rooms in the building. Houses that are built with drywall are called cottages and are considered as recreational houses only for summer. They are very cheap just because of that drywall.

Now, if you pay hundreds of thousands $ for something that is sooooo cheap to build you must be very naive. Sorry, but nobody in Germany, Austria or Holland would pay that money for such cheap construction.

So, my question is: why is it sooo expensive in Canada?

P.S. Imagine if all Canadians would like to buy solid brick houses in Canada. How many of them could afford it?

“In Europe most of houses are made of brick.”

Let me just say this: brick is the single worst material to build a house with in any kind of earthquake zone. It’s even worse than natural stones. Brick should never be used in structural parts of a building because it “liquefies” during an earthquake and causes the building to collapse.

Drywall is just one of the layers on top of the structural materials (wood or steel). There are other layers, such as insulating materials, a moisture barrier, etc. that go into a modern building.

And brick is still used in Europe because it’s cheap.

“Brick should never be used in structural parts of a building because it liquefies” during an earthquake and causes the building to collapse.”

LOL. If this is an argument not to use brick, I can only laugh. Europe is not Asia or South America where earthquakes are common. In Germany, Austria, France, Holland, Poland, Sweden – should I name more? – people only hear about earthquakes in other parts of the world. I have lived all my life till now in Europe and never, ever experienced any earthquake. Only on TV. :)

Besides my question was not “why they build using a brick” but “why drywall houses in Canada are so horribly expensive. So your answer is not correct for my question.

Yes, brick is very cheap in Europe. But drywall is even cheaper, much cheaper. In Canada drywall is more expensive than brick in Europe. Not mention that Canada has so much wood, so the houses should be damm cheap. Instead they are crazy expensive. I am sorry for Canadians that construction companies and home agents take so much advantage of them. That’s why Canadians are most debted nation in the world.

Google … earth quakes in the Netherlands … for an enlightening experience.

And Google … earth quakes in Germany … for an even more enlightening experience.

And Italy, for crying out loud,… and… and… and…

What you need to understand, but fail to, is that drywall is only one layer in several that make up a modern wall. It’s not structural. It’s just a final layer on the inside of the building. The next layer on the inside is paint. In a brick building, you have the same principle: stucco on top of a brick wall. Or you can put drywall over your brick wall if you wish.

Then look at how modern mid-rises and high-rises are built, even in Europe, and see if you discover any structural elements of the building that are made out of brick. Decoration sure, like a thin brick layer on the outside to look pretty, but nothing structural.

Robert,

the building material is not that important.

How it is done makes all the difference.

After growing up in Germany and living for some ten years in Canada I can tell you that the drywall does not change the quality of a building substantially.

Attatching something heavy to a wall made of studs and drywall can be a nightmare but there are solutions for those problems.

Much more important is thermal insulation.

With Brick the only option is to add insulation on the outside what gets very expensive. Styrofoam on the outside of a building blocks humidity from getting out and may increase the fire risk massively. Other solutions are very expensive. The North American hollow drywall/stud construction can be filled with insulation fairly cheap and reduce heatig bills while increasing comfort substantially.

The biggest reason for using brick walls in Germany is still World War 2.

To reduce damage from bombs reinforced concrete floors help a lot.

Someone forgot to check the scenarios for danger a long time ago and so brick and concrete are still the materials of choice.

As far as I know in Spain almost all forests were cut down under Franco, so there is not a lot of construction wood available, so brick and concrete are used.

Low IQ

1. “Google … earth quakes in the Netherlands … for an enlightening experience.

And Google … earth quakes in Germany … for an even more enlightening experience.

And Italy, for crying out loud,… and… and… and”. Even if there is an earthquake in Europe from time to time, there are not thousands of victims like in Asia or South America. Even in drywall houses there are dead quite often. So, earthquakes are not a good argument.

2. You still don’t understand my question. It is: why houses in Canada, made of cheapest material are much more expensive than in Europe? The quality of canadian houses is very low. I lived in a canadian house. The walls were like made of paper. I mean the sound. When you knock at the wall it sounds like knocking a paper box. You hear everything behind the wall. That’s why many Europeans call canadian and american houses “paper houses”. :) And those cheapest material houses are much more expensive than houses in Europe which are of much better quality.

So, my question is: why are they sooooooooooo expensive? What is the reason?

Now you nailed it, as we say, and you get full and extra credit for your question (once you leave the brick nonsense out): why are houses “sooooooooooo expensive” in Vancouver and Toronto?

This is an excellent question. Now ask the same question: Why are houses in Munich or Paris soooooooo expensive? Or in London, Sydney, Melbourne, San Francisco, Los Angeles, Boston, Auckland, Hong Kong….

Yes, it’s stunning. I know. Asset price inflation has caused huge distortions in many cities around the world, and they’re now embroiled in magnificent housing bubbles — which is often called a “housing crisis” locally, because the middle class can no longer afford to buy even a dump.

Dear Wolf, to finish this topic I just say some more words.

Firstly, I am talking not the biggest canadian cities nor bubble. I mean middle size cities or towns like Ottawa, London, Kitchener.

Prices in those places are also very high.

1. Munich, Paris, London etc. are big cities and very rich. Munich for example is expenive simply because this city is also the richest in Germany. It has many car factories of most expensive cars. It is very advanced technologically. London is the financial centre, a place where many houses are being bought by millionaires from all over the world. In those cities MOST OF houses are bought for CASH.

Paris is the mecca for tourists, artists and has most famous museums and art architecture.

On the contrary most of canadian cities are not places where you have tip top advanced technology, worlds class architecture etc. Take infrastructure, highways, high speed trains in Europe and comapre them with those in Canada.

2. The more populated country the more expensive houses. Take Tokyo, London, Paris. So, it is understandable the prices are high there because the density of the cities is big.

Now, Canada has so much land and so few people. In Germany, France, Holland there are 300-400 people per square kilometer.

In Canada you have much much less.

To summarize Canada has few people, a lot of land and wood, so the houses should cost maximum $150.000.00, not more. Everything over it is pure rip off.

Robert :)