52% of the homes listed for sale last spring still have not sold. For sellers, “the situation calls for a clear strategy: cut prices.”

Over half the 12,000-plus homes that were listed for sale in New York City on StreetEasy during the peak listing months of March, April, and May 2018 still have not sold as of early February, according to StreetEasy’s review of public records. This “historic wave of homes,” as StreetEasy calls it, arrived last spring “as price growth began to sputter and owners looked to cash out.” But buyers were not in the mood at those prices. And so 52% of the homes have still not sold.

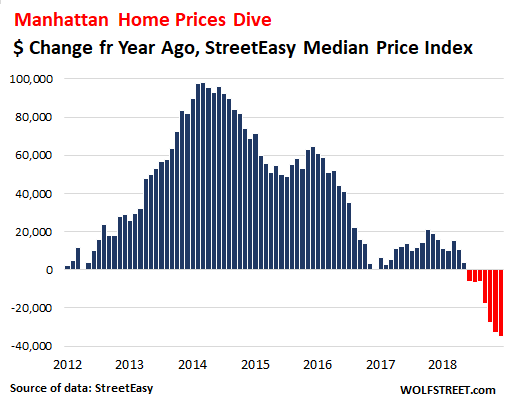

In Manhattan, 56% of the homes listed in March, April, and May 2018 have not yet sold. What makes buyers reluctant are the price declines. The StreetEasy median price index for Manhattan, at $1.132 million in December, is back where it had been in September 2015. For the past six months in a row, the median price index for Manhattan has fallen below the same month a year earlier. These are the first such year-over-year declines since Housing Bust 1. Given the dollars involved in a Manhattan home, those price declines can add up:

In New York City overall, thanks to price gains in other boroughs, StreetEasy’s median price index was still up 1.7% in December compared to a year earlier.

Across New York City, of the 48% of the homes that did sell since being listed last spring, 70% “sold significantly below their asking price,” StreetEasy said in its study. This is up from 62% over the same time period in 2017 and from 61% in 2016. This time around, the median price cut between initial listing price and recorded closing price (as shown in public records) was 5.5%.

In Manhattan, of the homes that did sell, 77% sold below their initial asking price. And “even in the comparably strong market in Queens, just 54% of homes found buyers.”

But aggressive pricing works

Of the homes that sold across New York City, only 19% sold above asking price. They “tended to be among the cheapest in their respective neighborhoods for their bedroom count,” StreetEasy explains in the study. They were put on the market with aggressive asking prices that then created buyer activity. StreetEasy:

- Homes that sold above asking price “were initially listed for a median of 8.8% below the respective 2018 median price for their neighborhood and bedroom count.”

- Homes that sold below asking price “were listed for a median of 1.2% above the respective median for their neighborhood and bedroom count.”

- Homes that failed to sell “were initially listed for a median of 6.4% above their respective benchmark median.”

The homes that were aggressively priced and then sold above asking price (about 1,000 homes in total) spend four weeks on the market.

But homes that were put on the market with a relatively higher price, but then were sold below asking price spent an average of nine weeks on the market.

The higher the price, the harder it gets:

- Homes listed at less than $1 million: 45% failed to sell.

- Homes listed at $1 million or more: 61% failed to sell.

- Homes listed at $5 million or more (656 units): 79% failed to sell.

What did unsuccessful sellers do? Pull the unit off the market.

The report explains: “Most sellers who were unable to find buyers at suitable prices have simply pulled their listings from the market. Of all listings created in spring 2018, 40% are either paused, delisted, or otherwise no longer available on StreetEasy. Only 7.5% of all the listings from the peak months, or 14% of the total unsold units, are still actively seeking buyers.”

A flood of listings for the spring home-shopping season.

With these unsold units lurking in the shadows, and “with inventory levels still near historic highs,” StreetEasy says, “we will likely continue to see heightened inventory heading into the spring home-shopping season, as these sellers try again to find a buyer.”

StreetEasy expects “another large wave of inventory to hit the market again in 2019 – one that will likely include many of the units listed but unsold in 2018.”

And the study has some suggestions:

“For sellers still seeking buyers, then, the situation calls for a clear strategy: cut prices.”

“Sellers may be tempted to hold out in the hope that some buyer will pay far above what others are offering. But with falling prices in many areas of the city, and inventory lingering on the market, such an outcome is highly unlikely. Many are willing to buy, but almost no one will be willing to pay more than what the broader market demands.”

“Buyers, on the other hand, should note the importance of doing their research. Pay special attention to how listing prices compare to neighborhood benchmarks…. Be picky, be patient, and be prepared to negotiate.”

Liquidity dries up when prices fall.

And this is what sellers in New York City are re-learning: Liquidity in a housing market exists only when the market is hot and prices rise. When bidding wars break out, anything sells, at just about any price, which causes prices to surge further.

But when the mood changes, and prices begin to fall, liquidity just evaporates. And homes sit on the market and simply fail to sell – as in New York City, with 52% of the homes listed last spring still not having sold.

But there is always liquidity somewhere, just at lower prices. To find that liquidity, sellers have to lower their aspirations and cut their asking prices. Liquidity is where the willing and able buyers are. Cut the price enough – and that’s valid for most assets – and you will find liquidity. And as buyers see those lower transaction prices in their neighborhood, they pull back further, being, as StreetEasy suggests, picky, patient, and prepared to negotiate.

Years of price gains in new houses are unwinding as homebuilders try to make deals. Read… New House Prices Drop 12% as Supply Surges

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So is there a sellers dynamic in which new sellers enter the market, anticipating that the top is in, in order to capture most of the gains, and take advantage of what may be the best chance to sell for the next few years?

Look at mortgage rates today. This economy smells. Something is really rotten here.

The high tax rate in New York and the new tax law aren’t helping either. The federal tax deduction for state tax is limited to $10,000 I think. Why would anybody want to move to one of the tax traps like New York or Chicago?

Because thats where the high paying jobs are??

Only if you are in the bloodsucking industry on Wall Street.

There are thousands of corporate headquarters in New York City. It is also a major port and the center of many other businesses than sucking blood.

“… inventory lingering on the market”

Isn’t that ‘liquidity?’

No, that’s just an asset sitting there. You need liquidity (money by buyers) to sell it.

“No, that’s just an asset sitting there. You need liquidity (money by buyers) to sell it.”

Ah, OK. I didn’t make the connection.

I’m a power trader and most of my markets are very illiquid. How this manifests itself is that you’ll have a very wide bid / ask spread, ie

$45 / $50.

Thus no one will trade because, no one wants to cross the bid/ask spread and become An instant $5 loser. That’s if they indeed judge fair value the at $45 or $50.

With a $47.25 / $47.50 market you will find a lot more players willing to lay off (or take on) risk for the cost of $.50 as opposed to $5.00 in the first example.

Until it sells it’s actually a liability… Especially if it is no longer your primary residence. In northern regions (especially of late) you gotta pay heating costs so pipes don’t freeze and rupture. Along with the general upkeep to make it appealing to potential buyers.

Much like any asset, you haven’t booked a profit until you have sold it.

As a home owner I think you should always be looking at it as a liability. Its when we stopped looking at homes in this country as places to live rather than “assets” and other bullshit that it screwed up peoples’ mentalities.

Well I would say:

-If you own your house debt free and it’s a the kind of place that suits your lifestyle needs, you are overall flat the housing market. Because you need a place to live and if the mkt goes up or down you don’t gain or lose anything relative to other houses – housing is inefficient but generally what suits you in your area will move with other such similar houses.

-If you’re renting, you are short the market.

-If you own more than one, you are long.

-And if you have a mortgage on any house you should think of it as a liability, not an asset.

@C Jones (the comment below, can’t reply directly)

Thanks! I like your comparison (flat/short/long), very nice analogy!

‘Liquidity drying up’ here seems to depend on willingness of the buyer. At least as important is the third party to most transactions: the lender.

Given enough access to easy financing, e.g. NINJA loans, buyers and sellers will push prices ever higher. But when mortgage money dries up so do prices.

That is probably the biggest factor in the change in Canada: tightened lending.

“And this is what sellers in New York City are re-learning: Liquidity in a housing market exists only when the market is hot and prices rise. When bidding wars break out, anything sells, at just about any price, which causes prices to surge further.”

Oh Sh*t. Lets hope no one overpaid in this environment!!!

Well, I think Wolf is on to something. I have been watching the local real estate data for a few months and December was the first month that we saw a decline in Y-O-Y sales here in Huntsville, Al since 2012. (Huntsville is a federally funded city of around 200,000 with around 30K fed worker/ktrs averaging $90K per annum). I have watched incredulously as, since 2015 home sales in Dec have risen from 425 to 569 in Dec 17 and then fell to 524 in Dec 18. From Dec 2015 to Dec 2018 median prices have risen from $172K to $215K and average prices from $201K to $252K.

What makes this even more interesting is that the number of houses on the market has dropped to lows not seen in well over 10 years.

So, as insulated from economic cycles as Huntsville is there was still a marked fall in sales in December. Something is clearly happening.

This is good news for anyone wanting to buy a place to live in there. I wonder how much prices will go down?

arcadian,

I have wondered that too. A lot of homes (and I mean a lot of homes) were purchased during the boom prior to 2009 and the prices then were pretty high. So I think only now are a lot of people above water on what they owe. At the same time Huntsville has a very high number of retirees. It has become very popular for both civilian and military government retirees. Home taxes in Huntsville are around $600 per $100k of home value, less than that in the developments out in the county. In addition Alabama doesn’t tax Social Security, Federal Retirements or defined benefit pension plans. So I understand why demand has increased.

But even with all the retirees I still don’t understand why the number of homes on the market has fallen so low.

“Buying a place to live” LOL how charming and quaint you are.

Don’t forget that under the auspices of the ideology that has removed from society its wealth-producing assets and thus bankrupted us – neoliberalism – we are all expected to be ‘devil take the hindmost’ speculators.

Hence we we don’t ‘buy a place to live in’ – we ‘invest in a financial asset’.

DO please move with the times!

Manhattan has always been cyclical. There have been times when you haven’t been able to sell at any price.

When I sold my Manhattan apartment in 2016, the market was hot. I was glad to take the cash and get out of town, because I knew it wouldn’t be like that forever. I had three cash offers at my listed price, which was very aggressive.

You caught the peak. It was a feeding frenzy then. Not anymore.

I just bought one. Rare bird penthouse. Waited 5 years for the right time.

Don’t know if it’s the right time. Asking price was the 2010 price.

Still got 7% below that.

Could go down certainly, but we intend to live in it.

We made the move because this type of product is very rare so it was the opportunity.

My intuition is that this is unique to the Manhattan luxury market, and frankly they are barely giving back gains from the past 18 months. Gains over the past three + years along the coasts have been so meteoric, a decline in sales and prices in Manhattan really isn’t that significant.

Watching prices like this is like watching molasses drip. I went to an open house in the SF marina yesterday. One of only two two-bedroom condos listed in the Marina, both around the average two-bedroom price in SF which is $1.5 – 1.6 million. During the fifteen minutes or so I was there, I saw four or five other couples come through to look at the place. Given that the Fed totally capitulated regarding rates and QT, we should expect to see the bubble start heading higher at some point in SF this year. I can also tell you that the people buying at these prices have enough in reserve and make enough in their careers that they will not wait around for a 20% – 30% price drop. They can withstand the pain if it comes (at least until the Fed turns on the printing presses again with full QE and interest rate suppression) – they are buying because they are at that point in their lives. It would take a job loss crisis worse than the GFC to really take out these owners.

We cannot tolerate even a 10 – 20% blip in asset prices without total and complete capitulation by the Fed encouraging further risk taking. I was in the crowd saying we expected the Fed to go in this direction and I do not see anything changing, especially with long term interest rates doing the exact opposite of what everyone expected them to do. Governments have always decided to destroy their currencies instead of devaluing assets, and it’s clear the same is happening here. The old saying seems to be true: if you plan to stay in your home at least five years then buy a home. You will make money.

It won’t take a lot to tank the market. The prices would go down because of few sellers selling low know as “Comps”.

This has happened many times before.

Not really in San Francisco. First you have to find comps that are actually lower and that does not happen much in SF proper. I search real estate apps pretty regularly to see the sale prices over the past few months. I was expecting to meaningful declines when I checked yesterday but the comps for SF are still in the stratosphere. Also I find that the majority of SF sellers are well to do and if the comps/prices are not what they want, they will just pull their property off the market and wait until prices adjust. Real Estate has been on death watch on this blog for years now, and even in spite of recent softness prices continue to march forward with the Federal Reserve clearly flagging it will never permit meaningful declines if it can do anything about it.

TrojanMan,

Here are the median prices, monthly, for condos in San Francisco.OK, median prices are volatile, but this doesn’t look very supportive of your thesis:

@Wolf – that dip coincides perfectly with the rise in interest rates and the market convulsions. Let’s see what happens now that rates are back on the floor and the Fed has clarified that is actually has very little interest in popping the everything bubble.

Please look around for an individual two bedroom/two bathroom condo in a decent part of town that isn’t a dump below $1.5 million and get back to me.

TrojanMan,

It seems you’re not looking. I just checked on Zillow. In my zip code (94109) alone, there are 17 in the price category $850K to 1.5 million, including this one, a nice one, just below 1.5 million:

https://www.zillow.com/homes/for_sale/San-Francisco-CA-94109/2088990299_zpid/97564_rid/pricea_sort/37.826565,-122.382374,37.767831,-122.461596_rect/13_zm/2_p/

If you’re willing to spend between $1 million and $1.5 million for a 2br 2ba condo, you have all kinds of choices all around SF.

Wolf, Love your website.

Hoping your interpretation of the recent Fed intention is correct. (their switch from long term MBS to shorter/medium term debt) thought that doesn’t explain why the 10y treasury is down as well.

http://tinyurl.com/yyk6kqny This is a week old 8 unit $2 million price tag complex in Long Beach. Just called the realtor. They already have 6 offers, some cash and well above asking price, she didn’t bother entertaining a potential new offer.

I hope the re market heads down but starting to have my doubts if it will be allowed.

Cheers, and thanks.

If a good unit is priced aggressively from the beginning, it will sell, and likely above asking. Everything else will sit. That’s exactly what the article said. It seems you picked one of those :-]

@Wolf – We are practically neighbors my man! Same zip code. If you ever want to grab a drink, you have my email. It’s on me…least I can do for all the mileage I’ve gotten out of your website.

With that out of the way, you found a nice unit that is slightly below $1.5 million. $1.479 million. Basically $1.5 million at $1400 a square foot. For a two bedroom/two bath 1000 sq ft condo. That’s basically my point. Sure, it’s a decent place but at $1.5 million? If you can find me a comparable place like this for $1 million, then I will concede. But you won’t find it. I’ve been keeping a close eye on SF market and I can tell you with certainty that you need to be prepared to drop $1.5 million give or take a few on a place like this.

Market is still insane.

TrojanMan,

The SF market can come down 30% and it will still be “insane.”

TrojanMan,

I’m thinking about organizing a meetup at some SF bar for all Bay Area WOLF STREET readers who are interested. I’ll post something on this soon. That would be fun.

Let’s examine your conclusion

In 2018 the median house in San Francisco was $1,374,800

Let’s assume a 1,000,000 mortgage with almost $375,000 down.

Using an interest rate of %3.92,this results in a monthly payment for 30 years of 4,728 or an annual amount=56,636

Property taxes are ~ %1.1 or ~$15,000/ year

Maintenance and repairs will run ~$5,000/year

TOTAL housing costs ( without utility costs) ~$76,636/ year

The median family income in San Francisco was 120,470 in 2017

After taxes this equals $82,884

For families making %50 more than the median This equals to an after tax income of ~121,000

For families making twice the median household income this yields an after tax income of ~154,000

Obviously any family making the median income or even % 50 more than the median income could not come close to affording the median priced house even after putting down almos %30.

A family making twice the median income could afford this house, but it would eat up almost %50 of their after tax income .

So any new housing demand for the median priced house is dependent on four groups.

1. Those few families who make much more than the median income

2. Those families with enough

assets to put up more cash . An example would be those few who sell stock in an IPO

3. Foreign buyers( think Chinese) who buy houses for all cash . Some of this group do not care about the price and just want to get money out of the China.

San Francisco housing prices are an accident waiting to happen

A tech recession will reduce the demand from buyers in the first or second category, while a trade war will ( and probably already has) eliminate buyers from China.

This reads as if it’s written by someone who is not familiar with the SF market. There are many people above that median who are competing for a limited number of homes and condos. As long as interest rates are low, they will absorb the higher prices. You speak of a tech recession as though it were 1999. The Fed just proved that we cannot absorb even a 10% decline to equities and slowing real estate appreciation before they fully scrap their laughable four interest rates for 2019 and signal a “possible” earlier end to QT and that QE could be back on the table as a reusable tool. And you think they will allow tech stocks to really come off their highs in any meaningful way? Not to mention big tech companies are flush with cash and VCs and PE have raised record capital.

Go look at the comps for SF over the past few months and tell me I’m wrong. At a certain point paying $4K a month on rent adds up. Do it for 10 years an you’ll wish you dumped it into a house even if the overall value slips. We now live in a centrally planned economy with a trapped Fed. Act accordingly.

This reads like the FED is God we will have to OBEY! They other day when I read SF FED is debating whether negative rate should have done better for the economy. My immediate response is to go find them and take a piss or a dump at their office, just to show how pissed off I am. Next time you see FED “manage” the economy and market, you remember my piss at their office. Enough piss will lead to yellow vest piss, enough yellow vest piss will scare the piss out of them, and you will see the entire SF Fed covered in piss! Now let’s talk about their God power to manage economy and we will have to act accordingly.

TrojanMan:

I’m in the same spot you are right now; growing family, have a rent controlled apt, running out of room but am waiting to see over the next 9-12 months which way it goes. My takeaway is that prices are in a bit of a tug of war; they aren’t increasing; a few price decreases here and there in SF proper, but mainly properties that used to get swooped up in a week are sitting out there for months. Sellers aren’t dropping prices meaningfully yet- I see little nibbles but not the tangible price cuts I personally am waiting for. Out in the East Bay you’re seeing some meatier price cuts.

It’s frustrating, but I have come to the conclusion that either we will get some meaningful price regression sometime soon, or I am just going to live elsewhere. If Slack, Uber Lyft, et al all IPO and create another crop of millionaires to keep buying up the housing stock, then life is too short and we’ll leave the area. I can’t look at that chart Wolf posted and jump in with two feet right now, it just doesn’t add up. I may be wrong; if so, I’ll be wrong but I’ll be able to sleep at night, probably somewhere with a lower cost of living.

IMO, tech valuations aside, the wild card here isn’t the Fed -it’s the China money that flowed in heavy from 2011-2017; the faucet has been turned off, which is good, but now you need a capitulation and a reason for them to unload the properties a la the Japanese did in the 80s/early 90s. If/when that happens, you’ll get some fast action.

If not, we will wake up and realize we just sold a good chunk of the state to absentee landlords who we also consider an enemy. So we got that going for us…..which is nice.

GSW, ere is my algo, I sick it up until I IPO or I suck it up until the bubble bust. I have been doing a lot of sucking and I am sucking it all up during the past 10 years. I did pick up my shack in 2010, so I do NOT have to leave. I do NOT work for startup so IPO option is gone. If I do NOT follow my algo and I give up before the bust, I will have to look up to the FED for rescue. I despise FED, so I will not allow myself to be in the position to be helped by THEM.

The simple math is that only the top % 20 of incomes can currently afford the median priced house in SF

The ratio of housing prices / incomes is over 11/1 in San Francisco. In my previous town of Short Hills NJ, which is rated as among the top 25 most affluent towns on the country, the ratio was nearer 5/1.

As the ratio in SF goes higher that means that even fewer can afford the median priced house.Eventually you get to the absurd situation where the ONLY buyers who

can afford the average house are those who already own a house or those who pay all cash.

The San Francisco and LA housing markets are teetering on the edge of disaster. The overall cost of living in SF is the highest in the country. Real estate taxes on new housing are the highest ( in terms of dollars) in the country. State income taxes are the highest in the country. The city has transformed itself from the most beautiful city in the country to one in which there are city workers who power wash the feces from the sidewalks and who collect needles from the parks and playgrounds.It is a city in which a car owner is almost guaranteed a broken window if he leaves anything of value in sight in a locked car.

My viewpoint is one who has just moved to the Bay Area. The traffic is unbelievable during rush hour. But the climate is much better than in NJ and the natural wonders of the area are breathtaking .

I am also worried about the Central banks monetizing in the future.

But gold is a much better gamble than the silly overpriced real estate market in CA.

@JZ – as far as the dollar is concerned, the FED is GOD and can giveth and taketh away. If the Fed decides to print more dollars to buy US treasuries or agency MBS, then the Fed can do that to its heart’s desire. They have already indicated they will do whatever it takes – nothing has really changed since Greenspan and Bernake. Powell tried to pump his chest but at the end of the day they are trapped in the same debt cycle. While they may not have omnipotent control over the economy, they can certainly make this a managed economy and kick the can down the road as far as possible, e.g. see Japan. I am not waiting three decades to buy a home.

@GSW – I agree, it is very frustrating. I love the Bay Area and grew up in California so there is no leaving for me, especially being entrenched in the financial ecosystem in SF. We may see modest price cuts in SF if the Fed allows interest rates to rise, but I would not hold my breath. It’s pretty clear they will not allow a meaningful increase in interest rates. SF is one of the center of the universe cities in the World and I have a better view than most into the amount of money flowing through this economy. The people buying the homes at current price points are for the most part flush with cash or supported by families who have their backs. It would take a GFC level event to really dent real estate prices here and even then I would not put it past people to successfully hunker down.

@Rcohn – nobody really wants to live in NJ. I hear about transplants like you out here all the time. Not so much in reverse. SF is the new financial and business center of the country, especially with its proximity to Asia.

They are not building new real estate in SF, or if they are it’s extremely high end in SOMA or public housing in the neighborhoods that couldn’t manage to keep the public housing away. The bottom 90% was never buying homes in SF to begin with and the population here has been increasing steadily.

Sure maybe there is some moderation, but without a real increase in rates or a job loss recession, I do not believe we will not see another crash in SF.

Cut rate, QE for the people. Government always have the “cure”. As long as enough people believe government has the cure, the only logical answer is to take on debt and front run other home buyers, there is NO bag holders, just gutless suckers who always complain! You dare to take out 1 million loan? I am going to take out 1.2million and bid you out! Then next one takes on 1.4 million and leave it for the government to fix! If government doesn’t find it? We will vote! Amen!

The Chinese home buyers inside China also pay cash most of the time. It is a tradition, not a desire to get money out of the country. Here people save for 30 years and buy a house instead of moving in and paying a mortgage for 30 years.

It is customary for a family to buy the son a home when he gets married, which is about age 30. This is often done decades in advance. Most new homes are sold as concrete shells, and they are left that way until the young couple wants to finish and decorate it. They do not deteriorate, being made of concrete. There is no property tax, so holding costs are nil.

Rcohn –

If you are earning double the median income and are spending 50% on housing, you are still left with $7K in a city where you don’t need to own a car. Can you live comfortably on $5K a month in disposable income in a home that has historically been appreciating at 5% per year? Of course! As long as you get 3-5% price appreciation you are still adding over $100K to your net worth each year.

I sold my condo last year to lock in gains so I could sleep at night. But emotions aside, it’s hard to imagine buying a median priced house in a prime location is ever a bad long term decision especially when you are already rich.

Sigh…. I feel you. We are all walking towards old age and retirement. Governent says, if you want to save money and buy a house in cash, you are dreaming! Because house will always gets more expensive, the more you save, the more you stay on the “treadmill”. Borrow money, get on this mortgage train, you will retire faster because you “lock in” the price today and it is only going to go UP, you will retire faster! You stay unconvinced, you wait till your friends jumped in, 5 years later, you see them way ahead while you are still on the treadmill. Government says “take a mortgage, get on aboard! or you will be left behind for ever while everybody else is getting ahead!”. So you take a mortgage, get on board, 2 years later, train wreck, half of passenger dead, you better hope you are NOT one of them.

The trick of this game? Get in after the wreck and get out before the wreck.

You say” NO,” our trick is that we will survive wreck when it happens and government will rescue and get the train back on track. Here is the thing, the disease is the same, but the cure is NOT enough this time. When you see FED is “preparing” for the wreck, you be careful.

Of course the Fed is preparing for the wreck and of course they will print more money and buy more bonds to sustain the housing market. Has Japan blown up? They have kicked the can for almost three decades. They will kick it as far as they can and so will the Fed because the alternative is the collapse of the banking system and probably capitalism and before you know it AOC is telling everyone that home ownership is evil and we should all be living in the same government assigned living quarters according to our needs.

Believe me, I am careful. When I buy, I will have a reserve and if it is not enough well then I guess my wife and I care complete losers for not planning it well enough.

I understand you. My point is this. If you believe FED is omnipotent God, then you are mistaken. They did NOT solved the business cycle, they did NOT removed the risk in market and economy. They “shifted” the risk to political risk, the kind of risk that is much more nasty than market and asset risk. Japan is a country that is dying like a zombie for 30 years. If you bought a house in Tokyo before the crash in 1990, I am NOT sure where you are now.

I watch the FED and Japan, and I act accordingly, I am scared, NOT because I will miss out on some profit or a big house to live in, but because the FED will eat this country’s value and principles from within and turn all the citizens into isolated debt slaves who look at FED for their rescue, NOT their neighbors and communities.

You could make the case that capitalism is already on its death bed, if not already dead and buried. What kind of “capitalism” is it when the Land of the Free harbors the world’s most powerful central planner? When the price of credit, the life blood of the financial system, is set by a central committee?

It’s dead in Japan, where the central bank uses its power to create money at no cost to buy stocks, and thus acquire ownership of the means of production. We once called that “communism”. In Europe, where it buys debt of private companies. Even in the US, where it not only bought Treasury debt but encroached into the territory once reserved for democratically elected representatives by buying mortgage debt, setting a precedent for buying almost anything.

When we as investors must now compete with a buyer with infinitely deep pockets in the asset markets, what hope is there left for our capital?

Bill, if what you described is true, the strategy is simple. Just front run the FED. The moment they announce they will buy something regardless price, for some scheduled amount every month like QE, you all in and front run them.

The difficulty with this is that people start to front run each other based on what everybody’s guess of what FED “will” do.Here, the only people who have an edge is FED’s friends. Sorry, we are NOT in the club. All we could do is front run FED and let FED’s friend front run us.But whenever I hear people saying “ I am going to buy house or stocks because FED WILL save us”, my response is always “you are NOT FED’s friends… “

@JZ – I agree with your comment 100%. I do not believe the FED is an omnipotent GOD. But I know they will have something to say about whether we have a deflationary or inflationary crash. I believe they will continue to reduce the value of the dollar rather than make asset holders take a haircut. They will buy whatever number of bonds it takes to keep values where they want them. Kick the debt down the road and watch the balance sheet grow. They will get cover from the fact that all other central banks must follow suit.

My preference would be they let asset holders take a haircut and keep interest rates at a reasonable level and leave them there. But that will never happen.

@Bill – I agree with your comment.

@JZ – you are right we are not the FED’s friends, but their friends are massive institutional asset holders and if running a little bit behind them but ahead of the contrarians who want to fight the fed and hold onto their cash in a QE/ZIRP/NIRP environment, until the next helicopter cash acronym is invented for the further devaluation of fiat, I am fine with that. Neither party has the political will to force any other outcome. Democrats want everything to be free on an increasing basis – how it all gets paid for is the FED’s problem – and Republicans want to continue the party so they can claim a strong economy. Any way you slice it there is one solution and that is printing more fiat.

@Trojanman, I think this very thought in everybody’s mind to dump or short dollars to buy assets to front run each other IS what FED fears the most and this IS the reason FED has to tighten. If you think you have figured out to front run FED, you are 10 years late. What wise man does in the beginning, fools do at the end, — Warren Buffet. As Wolf said, if you have money and can afford a house, buy it. All I am saying is please do NOT justify this decision based on you KNOW what the FED will do or what Trump will do or what AOC will do. You are NOT their friends, and you don’t know them. To me, I think we are in the most dangerous time. It is NOT a time to get rich, it is time to try avoid getting hurt. The contrarian view is NOT to fight the FED. The contrarian view is to long dollar when everybody else is shorting dollar and long houses, it is to long platinum and uranium when they are selling below cost of production. Nobody can fight the FED but you can use FED’s weakness to jujitsu the FED. Again, there are reasons to buy houses, but to say you do this because you KNOW what FED will do no matter how we slice it is finding an excuse to do something for other reasons.

S’what happens when your ‘prosperity’ built on debt-fueled, get-rich-quick speculation rather than production and export.

You paint yourself into a corner, and sacrifice a stable societal future for short-term sugar rush. Those who have gambled and one disappear with their winnings, with no intention of ‘giving back’.

Human beings it seems are incorrigible when it comes to this type of behavior.

‘Won’ not ‘one’.

I was once listening to a popular real estate radio show here in NYC. A caller from NJ was ranting about how amazing her house was and how evil and stupid people were for not buying it. The host said, “If the price was one dollar, do you think someone would buy it? My point is that there is always a price at which it will sell.” And the caller said indignantly, “I’m not giving it away!” Aspirational pricing is the issue. I have a neighbor who can’t sell because he wants more than twice what he paid for it several years ago.

Hey Wolf.

How about calling out the industry hacks who continue to utilize YOY figures. While this has some pertinence in highly seasonal markets, it is currently being used to buffer the truth that the trajectory of this market is downhill.

Industry types still say news is good because values are increasing slightly. This is deliberate misleading if we have had several straight months of declining conditions.

Imagine if this was used for stocks. ” XYZ has declined in price for 28 straight weeks but fortunately value is increasing since it is still 1 per cent higher than a year ago”

It is an absurd metric that will backfire horribly once we get about a year past peak prices. It will then appear to reveal huge downward trend. Of course they will then start quoting monthly numbers so it does not look as bad

Thanks

jdog,

Just look at the chart in the article — it’s a YOY chart of Manhattan home prices — and tell me if it is, as you say, “currently being used to buffer the truth that the trajectory of this market is downhill.”

YOY charts show the downhill slide in brutal frankness. YOY comparison is one of the crucial metrics.

I was actually speaking in general terms nationwide. I see the YOY being used in many assorted articles to suggest that properties are still increasing in value when, in reality, they have been reducing for several consecutive month.

I do real property valuation and analysis. Fannie and Freddie have devised an addendum for appraisals used to assess actual market trends. It is called a Market Conditions addendum identified by the number 1004mc.

It breaks down listings and sales to thier median DOMs, list prices, sales prices, and other criteria into 3 time periods. These are 0 to 3 months, 3 to 6 months, and 6 to 12 months. It is much more revealing and more precise than YOY. It is used in loan underwriting to identify current trends, but I have never seen it referenced in MSM articles. Yun is often quoted as an unbiased data source, but any trade organization exist for the promotion of its members and the NAR is no different. Many RE articles reference the YOY data and conclude that prices are still rising without proper analysis of monthly, 3 month, or 6 month median price trends. To me the fallacy of their approach is obvious. Places like NY, Vancouver, Sydney, Seattle and others are well documented and can no longer hide. However, nationwide and in numerous local markets, The YOY cover strategy is still obviously being implemented, and these folks should be called out.

Thanks for your great work.

Hello Wolf,

I am a fan of your website especially the articles on real estate trends.

1. Given the article about the lack of liquidity in NYC housing, I wonder if NYC will show up as one of the most “Splendid Housing Bubbles.”

2. Typically, how does liquidity get restored—how far do prices drop and how long does it take them to get there?

3. A significant part of the NYC housing market is coops which don’t lend themselves to speculation. How does this effect the overall NYC housing market?

Thank you for considering these questions.

Native NYer,

1. The NYC housing market itself is not available in the Case-Shiller data. They use the metropolitan area which includes parts of the surrounding states, and it’s only for single-family houses, which are not that common in a place like Manhattan. This is a HUGE and diverse market. So what I include is the New York metro “condo” index from Case-Shiller. This is somewhat more focused on the urban core of the New York City metro, rather than suburban housing areas in New Jersey, etc. This NYC condo index has been in the lineup of the “most splendid housing bubbles” from day one — and deservedly so :-]

2. Yes, asking prices need to go where the buyers are. And then there is plenty of liquidity.

3. Coops get dragged along by the condo market — the difference between the is not huge. And yes, there seems to be less speculation.

Like a slowly rising tide of economic despair, our debts will consume us.

In your previous article the median home price went from $260,000 in 2006-2007 to $340,000 in 2017-2018, which is a significant increase!

Debt cannot ultimately exceed the ability to service it. When it collectively does so, it’s value craters.

Just look at student loan debt, without the federal backstop, the entire education economy would crater.

Soooo, when it happens, LoL.

i think this chart is valuable for overall trends but in nyc it is very hard to rely on published numbers. each borough is really a seperate market wth some overlap between brooklyn and queens. in manhattan only rich people buy apts and most of those are coops which i don’t think are included in the surveys. staten island and to a lesser extent queens have tons of single family homes. the new tax laws and the new transparency requirements for buying thru an llc alao put downward pressure on prices.

“Over half the 12,000-plus homes that were listed for sale in New York City on StreetEasy during the peak listing months of March, April, and May 2018 still have not sold as of early February, according to StreetEasy’s review of public records.”

Wolf, you’re posting info from a no-name website that did not post either its data or methodology. Looks really sketchy.

Perhaps people are selling their homes because they realized they’d bought real estate in an unlivable- crap hole called NYC.

The city itself is now rapidly falling to pieces, as the trains barely run and people are fleeing the state. The city just came up with a 40 billion dollar figure for ‘fixing the trains’ and I thought -‘Didn’t anyone ever think about the fact the existing trains would stop working one day?’. Nope, it was just live one day at a time.

The Anti-New York headlines are so loud today that I think it’s driving away buyers. I wouldn’t point to it as the basis for a national trend.

Brooklyn,

“No name website?” Are you kidding? StreetEasy is focused entirely on New York City, and in New York City is one of the top, if not the top place, to go. Granted it doesn’t cover other markets, but in New York City, it’s huge.

You can check the methodology by looking at the report that I linked in the article. It’s right there. To summarize in a few words: the data for listings comes listings on its own site (the 12,000 listings); and the data for sales comes from public records, as I pointed out in the article. The pricing data for the chart was downloaded via its data page, which you can also check out.

@Brooklyn i don’t know where in brooklyn you live but it must be part of an alternative universe. the subways. need repairs largely because of damage from superstorm sandy and because ridership is at an all time high. the city certianly has many serious problems but people fleeing isn’t one of them. the population is growing by approximately 60,000 per year.

I read a comment here talking about the Fed”Cavalry “! Coming to the rescue with their magnificent QE and omitting a real possibility that we’re approaching the ( critical mass panic) that will basically be a tsunami that the Fed won’t be able to do anything about.

All you need in this market now is the First ( FEAR) crocodile to emerge from the water

You’ll be watching how the Wildebeest start trampling each other for the other side of the river!

Fight the FED and hold your cash then until you are blue in the face. Btw, where do you think all the money will come from to pay medicare and pension expenses? It will be printed via QE while controlling interest rates. You think they are actually going to make benefit/security holders take a haircut? Lol.

Here is a total disaster home in Eastside Costa Mesa ( Orange County ) … 336 Flower Street. Price $1,350.000 … which is an absolute bargain relative to what this would sell for in Coastal LA County, and people are lined up to do a walk through.

https://www.redfin.com/CA/Costa-Mesa/336-Flower-St-92627/home/3557302

I know of a few more just like this in LA county with much higher prices than this. Bidding wars on the junkers.

I bought a home ten years ago for $1M, and sold it recently for $1M, so I have not lost any money!

Devaluation of the dollar needs to be factored in. Prices on real estate in NYC may not decline as much as one would think, but in inflation adjusted dollars, it will.

There is a persistent desire for outmigration of NY baby boomers heading to tax friendly states, but in order to do this, they need to sell their existing home, and they don’t want to have to lower the price. When this logjam breaks, prices on high end properties will be “adjusted”.

I live in the Albany NY area.. totally different housing price structure from NYC and other hot area. It’s been fascinating to watch the onslaught of new housing construction in the area… 2700 SQF 4 bedrooms in the high 400K to 600K range. Just to put things in perspective, I have an 1880 Victorian, 5 BR’s and roughly 2900 SQF. I’d be lucky to get 340-350K… but I’m not complaining. New construction isn’t worth close to double the price I don’t think.

I just don’t see the jobs in the area to support that kind of pricing. I’ve had a handful of friends over the past 6-8 years take the McMansion plunge and buy $500K+ homes here. Several had to sell as they were transferred and had to move. To a person, they all lost $’s on the sale.

Problem is, it may still make sense to buy, even if you’re forecasting home prices to decline.

Say you bought the $500k new house versus rented at $30k per year. After 3 years, you would have spent $90k on rent. The house could decline by 20%+ and you would still break even after the sale. In both situations, housing costs $30k per year.

In the end, it’s a quality of life decision more than a financial decision. Renting could make sense if you think the end of the world is coming, most likely, you just won’t profit owning a house. But you need to live somewhere.

Mark,

I agree with what you said about it being a quality of life decision. But in terms of the numbers…

You said: “Say you bought the $500k new house versus rented at $30k per year. After 3 years, you would have spent $90k on rent. The house could decline by 20%+ and you would still break even after the sale. In both situations, housing costs $30k per year.”

Interest expense, property taxes, and maintenance and repairs are expenses that will never come back — unlike principal payments. So if your total mortgage payments are $30K per year, nearly all of it is interest the first year. Plus property taxes, plus maintenance and repairs… those expenses are money down the drain, just like rent (though there may be some tax advantages).

So if your 500K house declines by 20% over 3 years, you’re in the hole by 20% of $500K ($100k) plus 3 years of interest (maybe $60K), plus 3 years of property taxes (maybe $18K), plus maintenance and repairs (let’s assume it’s zero). In total, you’re in the hole by $178K. That’s what it cost you live there for three years = 60K a year!

And if you try to sell the house, you will likely have to fork over some money to pay off your mortgage because you’re likely upside down, which makes selling the house unappetizing.

There’s a couple of factors hitting the NYC market:

– US government has expanded crackdown on money laundering in real estate

– federal tax bill capped state taxes that can be deducted

– Chinese capital outflow restrictions

I read an article a couple of months ago that said the share of foreign buyers of NYC apartments has fallen by 40%.

Interesting fact: Hong Kong just passed a vacancy tax on residential units.

@Stephan Foley completely in agreement by what i’ve seen and heard in my neighborhood in lower manhattan.

I was baffled after looking at several apartment (condo) listings on streeteasy.com that their areal size where not listed. Is this typical of NY? You don’t get to know the size of what you are buying.

Here is a summary search page I just got for Manhattan apartments, 2 br, price range $1.25-$2 million. And it shows square footage right up front:

https://streeteasy.com/for-sale/manhattan/price:1250000-2000000%7Cbeds:2

fyi, sq footage is usually inflated by 10-15% to account for “common areas.”

We lived in 94109 for 10 years… definitely the most “diverse” zip code in San Francisco, stretching from the Bay to deep Tenderloin.

Hi Wolf,

Is it correct to assume that bottoms for real estate market are all different, but may have some common features?

If so how does one recognize that a real estate market is bottoming?

Thanks

NativeNYer,

Eternally great questions: “If so how does one recognize that a real estate market is bottoming?”

The answer is: bottom picking is hard and requires luck. Many people have failed trying. But others have succeeded, some of them by sheer luck of timing. Only hindsight gives clarity.